Embed Size (px)

Citation preview

1

CORPORATE

SUSTAINABILITY

REPORT 2011

2

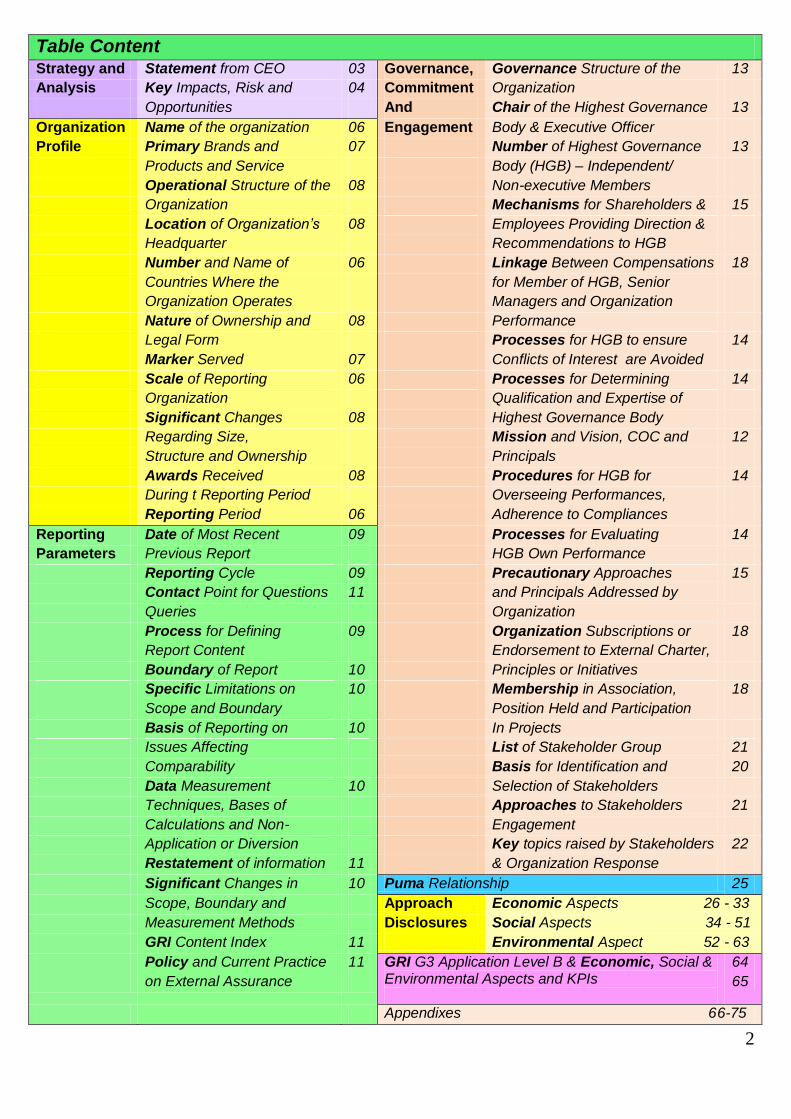

Table Content Strategy and Statement from CEO 03 Governance, Governance Structure of the 13

Analysis Key Impacts, Risk and 04 Commitment Organization

Opportunities And Chair of the Highest Governance 13

Organization Name of the organization 06 Engagement Body & Executive Officer

Profile Primary Brands and 07 Number of Highest Governance 13

Products and Service Body (HGB) – Independent/

Operational Structure of the 08 Non-executive Members

Organization Mechanisms for Shareholders & 15

Location of Organization’s 08 Employees Providing Direction &

Headquarter Recommendations to HGB

Number and Name of 06 Linkage Between Compensations 18

Countries Where the for Member of HGB, Senior

Organization Operates Managers and Organization

Nature of Ownership and 08 Performance

Legal Form Processes for HGB to ensure 14

Marker Served 07 Conflicts of Interest are Avoided

Scale of Reporting 06 Processes for Determining 14

Organization Qualification and Expertise of

Significant Changes 08 Highest Governance Body

Regarding Size, Mission and Vision, COC and 12

Structure and Ownership Principals

Awards Received 08 Procedures for HGB for 14

During t Reporting Period Overseeing Performances,

Reporting Period 06 Adherence to Compliances

Reporting Date of Most Recent 09 Processes for Evaluating 14

Parameters Previous Report HGB Own Performance

Reporting Cycle 09 Precautionary Approaches 15

Contact Point for Questions 11 and Principals Addressed by

Queries Organization

Process for Defining 09 Organization Subscriptions or 18

Report Content Endorsement to External Charter,

Boundary of Report 10 Principles or Initiatives

Specific Limitations on 10 Membership in Association, 18

Scope and Boundary Position Held and Participation

Basis of Reporting on 10 In Projects

Issues Affecting List of Stakeholder Group 21

Comparability Basis for Identification and 20

Data Measurement 10 Selection of Stakeholders

Techniques, Bases of Approaches to Stakeholders 21

Calculations and Non- Engagement

Application or Diversion Key topics raised by Stakeholders 22

Restatement of information 11 & Organization Response

Significant Changes in 10 Puma Relationship 25

Scope, Boundary and Approach Economic Aspects 26 - 33

Measurement Methods Disclosures Social Aspects 34 - 51

GRI Content Index 11 Environmental Aspect 52 - 63

Policy and Current Practice 11 GRI G3 Application Level B & Economic, Social & Environmental Aspects and KPIs

64

on External Assurance 65

Appendixes 66-75

3

Chief Executive Officer Statement

PCCS Group and its subsidiary JIT Textiles Limited has progressed

considerably in overall business performance which was matched by

positive developments in our sustainability agenda.

At PCCS Group – JIT Textiles Ltd, we take a long-term systematic

approach to sustainability objectives. In 2010/2011 period, we

developed roadmaps with specific action plans to achieve our 2010-

2011 strategic sustainability KPIs in partnership with our key

customers. We further improved our natural resource utilization, and

re-aligned several operational decisions in line with our sustainability

philosophy.

During the last two years, our progress in achieving savings in energy

and water were well documented. In addition to successful Energy

Saving programs, we also implemented fuel saving measures in

transportation and logistics system. As a result we achieved

substantial savings in diesel consumption. We were also able to

quickly share best practices in energy saving within the PCCS Group.

Our audit scores in CSR, Technical Quality, Sustainability and Safety

from annual audits conducted by key customers recorded huge

improvements and were rated among top in Asia.

We participated fully with our key customers in compliance with EU‟s

initiatives on Restricted Substances List and Kid‟s Safety Program. In

2011, we helped to develop a bio-degradable plastic bag for our

garments.

Through 2009-2012, we have intensified our localization process in

our human resources development. Through various training and

human resource development programs, increasing number of local

staff were able to make vertical progression in their careers within the

PCCS Group. As a result, we are now less dependent on expatriates

to fill in managerial and supervisory positions in the company.

JIT Textiles Limited has pioneered a workers‟ welfare program in

Cambodia. Through our unique in-house “Jouy K‟nier” (Self-Help)

Program, workers were able to enjoy welfare benefits far better than

those provided by the local Labor Law.

We firmly believe our commitment to sustainability makes us a

stronger business and will help to ensure PCCS Group and JIT

Textiles Limited will always be able to contribute to the society they

are operating in.

John Cha

Chief Executive Officer

Oct 2012

CEO : John Cha

4

Key Impacts, Risks and Opportunities

JIT Textiles Ltd (JIT) sustainability challenges (risks) and opportunities associated with the business goals and

operations are identified, prioritized and managed using our Company Risk Management Procedure:

Consider issues raised by our key stakeholders and international benchmarks for sustainability

performance

These findings are reported to our Head of Departments Committee periodically and inform of our

strategic planning and operating plan processes. There are 7 general aspects:

Aspects Challenges Opportunities Impacts 1. Global Macro

Economic

risks

Managing global macroeconomic

risks including

Natural resources

Raw material pricing

volatility

EU economy slum

Currency fluctuations

Applying management system and

governance processes effectively to ensure

Current and emerging risks are identified,

assessed and managed within our risk

appetites and

Opportunities are leveraged.

Fluctuating

sales volume

Cost Impacts

2. Environmental

Impacts of

Operations

Regulatory and stakeholder

expectations for operations with

low environmental impacts.

Reduction of environmental impacts

On manufacturing processes and products

to create new competitive advantage and

Reduce costs.

Sustainability

cost regarding

environmental

protection

3. Changing

Customer

Tastes

Changing consumer tastes

towards sustainable finishing

products

Be a leader in garment industry

Creating new areas of competitive

advantage through supply chain

partnerships and product life cycle

assessment capabilities

Maintaining sustainable value for our

customers.

Additional cost

to meet the

customers‟

tastes

4. Community

Support for our

Operations

Meeting social responsibility

requirements in return getting

community support for our

operations

To build effective partnerships and seek

constructive dialogue with the

communities in which we operate.

Social

responsibility

cost

5. Occupational

Health and

Safety

Regulatory and stakeholder

expectations for occupational

health and safety standard

To become internationally recognized for

Our safe work practices

Sharing our expertise with our suppliers

and customers

Helping customers and suppliers achieve

their own corporate social responsibility

goals.

Sustainability

cost regarding

occupational

health and

safety

6. Risk in

Emerging

Markets

Managing the political, cultural

and social risks associated with

our growth in emerging markets

Positively influence the development of

countries in the emerging markets into which

we are expanding

Delivering employment opportunities

Supporting local communities,

Contributing to the countries‟ economies

and demonstrating good governance and

supply chain integrity.

Cost of

maintaining

competitive

advantage in

orders

(Competition

from

Myanmar)

7. Climate

change

Melting of icebergs

Rising of seawater level

Widening of Ozone layer

Extreme weather conditions

worldwide.

Reducing the greenhouse gas intensity of

our processes and products to help

protect the environment.

Sustainability

cost regarding

environmental

protection

5

Besides the 7 general aspects above mentioned, there are 2 major threats faced by JIT during the year and the

impacts can be summarized as follows: -

From 1st of January, 2011, EU (European Union) further extended its GSP (Generalized

System of Preference) tax privilege to Cambodia garment manufacturers for all materials

imported from overseas which subsequently converted to finished goods and exported to

EU countries, meaning tax saving ranging 10% to 18% to EU buyers.

Lured by the exotic trade privilege, investors saw Cambodia as a new garment investment

heaven, made up their decision fast by closing down or shifting some of the factories in

other regions of the world, especially China when the labor cost was so high to make

garment industry volatile and unviable, and set up new factories in Cambodia especially in

the vicinity of Phnom Penh city. The existing factories in Cambodia took the opportunities to

enlarge their current production scale or even build new factories for their expansions.

Such influx of new investment or expansion would inevitable caused labor shortage in the

market.

Garment factories started to complete for both skillful and new labors to fill up the

employment vacancy. In order to retain existing workers and attract new comers for

business growth and expansion (Total workforce: 2010: 2,500 & 2011: 3,200), JIT resorted

increment both in salary and allowances to fulfill our business goal.

Consequently, the monthly basic wage plus allowances alone have increased from US$71

to US$87, representing 23% rise. The total wages (direct and indirect) shoot up 26% or

US$1,435,500 partly due to basic wage and allowances increment at the same time

increased the total workforce by about 700 workers and the rests by overtime claims.

Besides, JIT offered competitive remuneration by practicing the skill grading system to

workers whose monthly basic salary was higher than US$61 and enjoying incentives based

on productivity outputs.

Such sharp rise in remuneration resulted in the adverse consequence of low net profit

margin of mere 1% level in 2011, and the Company expected the government would further

increase the national minimum wage in the coming years. The estimated profit of

US$500,000 in the earlier year forecast was far outran by the wage increment of

US$1,435,500.

The lifting of EU (European Union) sanctions against Myanmar is bound to have an impact

on the Cambodian garment sector. The EU announced earlier that it was lifting sanctions

against the country. Japan and Canada have made similar announcements very recently.

The Cambodian garment industry will certainly be affected after EU sanctions against

Myanmar are abolished, but the extent of the effect was not known because the details of

the EU suspension of sanctions against Myanmar were not announced yet.

The impact on local apparel companies in Cambodia will not be felt soon and that, for the

time being at least, the local garment industry will not move to Myanmar.

What if EU, Japan, Canada and other western countries finally announce the lifting of

sanctions, we can expect a new round of investment in Myanmar by which customers may

pull away some orders from Cambodia to this country in near future. Cambodia garment

sector could be badly hit when more factories start operating in Myanmar and EU enforces

GSP system in two to three years‟ time.

L

A

B

O

R

C

O

S

T

M

Y

A

N

M

A

R

6

Organizational Profile

Highlights

Strategic Suppliers to Puma, adidas, GAP, United Colors of Benetton, Oxylane (Decathlon),

ECI and Li Ning - world class apparel companies, based on our repeated performance as a

prominent supplier in terms of quality garment supply and compliance programs.

Li Ning, a China renowned brand, placed order in JIT for producing its garments for the first

time in 2011.

Operation Expansion by opening up 10 more Sewing Lines.

Name and Principal Activity of JIT

JIT Textiles Limited (JIT) is a rapidly growing

company located in Phnom Penh city, the capital

of Kingdom of Cambodia.

Our principal activity is the manufacturing of

sportswear of which is supported by the provision

of branding services of renowned world class

apparel companies.

We manufacture knitted & woven garments

comprising T-Shirts, Polo, Jacket, Hoody, Jog

Pants and active wears fit for men, women and

children of all ages

Within a very short period of time, the Company

has earned a solid reputation globally in the

readymade garment sectors, producing over 4

million pieces in 2011

Location and Country of Operation

Address: National Road #4, Sangkat Chom

Chau, Khan Darngkor, Phnom Penh city

Location: 7 Km in the western direction of

Phnom Penh International Airport. JIT only

operates on this premise in Cambodia.

Scale of JIT as at 31-Dec-2011

Land area – 20,380 M2

Building covered areas – 19,220 M2

Building blocks – 4 major blocks (1 corporate

office and 3 production blocks)

Total workforce – 3,206 employees

Production - 4.5 million pieces (Capacity: 6

million pieces)

Facilities - Cutting, sewing, packing and In-house embellishment (heat transfer, printing & embroidery)

Reporting Period

This is our second annual Sustainability

Report, following the path that JIT incorporated

in 2007 as a Cambodia supplier of 12

renowned world class apparel companies.

2011 report will highlight the scenario of

sustainability initiatives in scope of its

economic, social and environmental

performances throughout the year i.e. 1-Jan-

2011 to 31-Dec-2011

It contains information linked to last year

sustainability concerns where applicable plus

additional KPIs with respective disclosures of

Management Approaches.

7

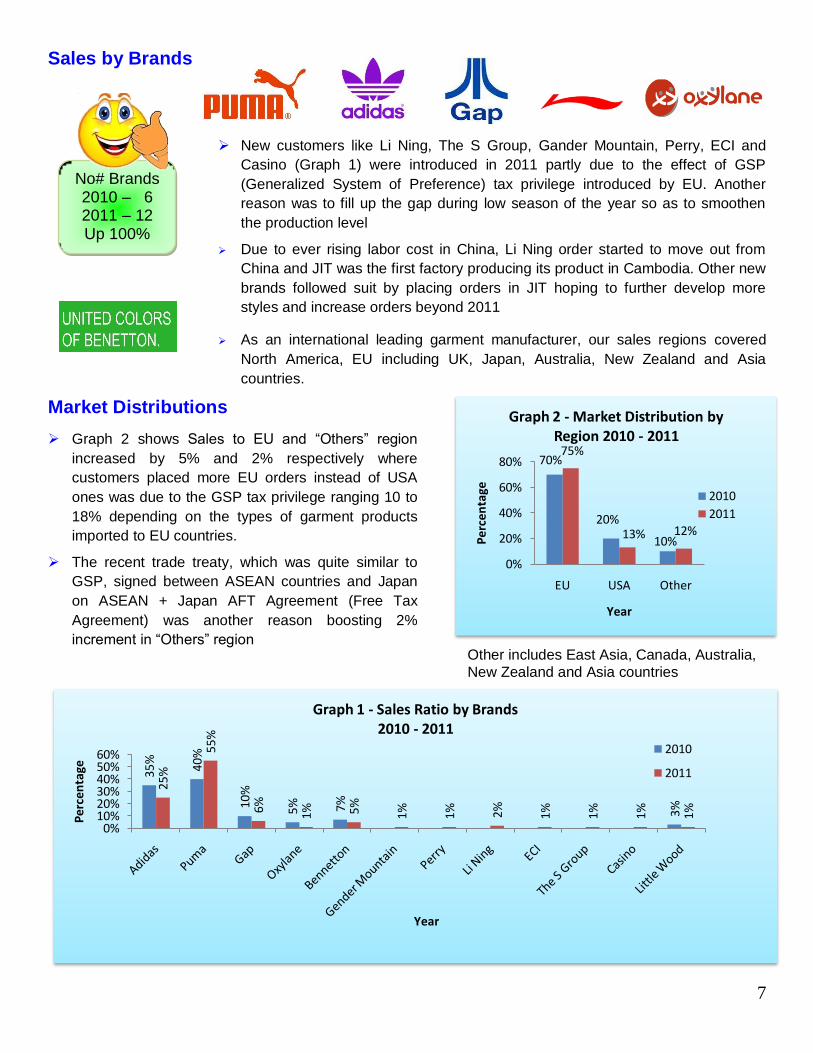

Sales by Brands

New customers like Li Ning, The S Group, Gander Mountain, Perry, ECI and

Casino (Graph 1) were introduced in 2011 partly due to the effect of GSP

(Generalized System of Preference) tax privilege introduced by EU. Another

reason was to fill up the gap during low season of the year so as to smoothen

the production level

Due to ever rising labor cost in China, Li Ning order started to move out from

China and JIT was the first factory producing its product in Cambodia. Other new

brands followed suit by placing orders in JIT hoping to further develop more

styles and increase orders beyond 2011

As an international leading garment manufacturer, our sales regions covered

North America, EU including UK, Japan, Australia, New Zealand and Asia

countries.

Market Distributions

Graph 2 shows Sales to EU and “Others” region

increased by 5% and 2% respectively where

customers placed more EU orders instead of USA

ones was due to the GSP tax privilege ranging 10 to

18% depending on the types of garment products

imported to EU countries.

The recent trade treaty, which was quite similar to

GSP, signed between ASEAN countries and Japan

on ASEAN + Japan AFT Agreement (Free Tax

Agreement) was another reason boosting 2%

increment in “Others” region

70%

20%

10%

75%

13% 12%

0%

20%

40%

60%

80%

EU USA Other

Per

cen

tage

Year

Graph 2 - Market Distribution by Region 2010 - 2011

2010

2011

35%

40%

10%

5% 7% 3%

25%

55%

6% 1% 5% 1% 1% 2% 1% 1% 1% 1%

0%10%20%30%40%50%60%

Pe

rcen

tage

Year

Graph 1 - Sales Ratio by Brands 2010 - 2011

2010

2011

No# Brands 2010 – 6 2011 – 12 Up 100%

Other includes East Asia, Canada, Australia,

New Zealand and Asia countries

8

Operational Structure of JIT

The structure of PCCS Group is shown below where JIT is 100% control of the holding company PCCS

GROUP BHD.

The Holding Company, PCCS Group Berhad (Ltd), is located and registered in Malaysia and listed in Kuala

Lumpur Stock Exchange (BURSA Malaysia) since 1995.

JIT is incorporated in Cambodia in 2007 as part of group expansion of overseas business activities. It is a

legal and separate entity registered in the country of Cambodia with Incorporation Registration No#:

1326/08E

The operations in the production floor can be grouped as follows: -

Sample Garment Development – JIT is capable of sample garment making from the beginning, based

on customer‟s technical design requirement, up to the last stage of development and

Bulk production – JIT performs CMT (Cut-Make-Trim) manufacturing process for the renowned brands

above mentioned.

PCCS Group Structure

PCCS

Group Bhd

(Holding

Company)

JIT

Textiles

Limited

Shem

Yee

Garments

Sdn. Bhd.

Jusca

Development

Sdn. Bhd

Beauty

Electronic

Embroidery

Center

Sdn. Bhd

Beauty

Apparels

(Cambodia)

Ltd

SA One

Garment

Ltd

Perusahaan

Chan

Choo Sing

Sdn.Bhd

Other

subsidiaries

Global

Apparels

Limited

Beauty Silk

Screen(M)

Sdn. Bhd.

JIT

Embroidery

Limited

Beauty Silk

Screen

Limited

Significant Changes There are no significant changes from previous reporting period regarding the structure and legal

ownership of JIT except the followings:

Size of operation – Additional of 10 new sewing lines of about 40 workers per line comprising sewing

ironing and packing operators, QC staff and line leader totaling 400 workers in sewing section

Manpower recruitment - Total workforce of 3,206 employees, an increment of 700 (including the 400

above mentioned) workers at the end of 2011 when compared to last year‟s.

Awards

JIT did not receive any award during the year of 2011

9

Reporting Parameters

Highlights

JIT is a subsidiary of PCCS Group Berhad (Ltd), a public listed company

in Kuala Lumpur Stock Exchange, and publishes its Financial Report in

accordance to International Accounting Standard and KL Stock

Exchange Regulations

Most Recent Report and Reporting Cycle

We started our first Sustainability Report in 2010 covering relevant information fro2m 1-Jan-2010 to 31-

Dec-2010 for the purpose of enhancing communication with our stakeholders and ever increasing demand

of corporate reporting transparency and decided to report on a yearly basis.

This is the second Sustainability Report of JIT, covering relevant information throughout the Year of 2011,

after taking accounts of materiality assessment that influenced it, which also included additional information

relevant to the Global Reporting Initiative (GRI) or where JIT deemed appropriate.

Process of Defining Report Content

Purpose of Report We need to emphasize the fundamental

purposes of this sustainability report as

each of them relates to:

our concern on the global climate

change,

our attention to the implementation of

sustainable development,

our emphasis towards Corporate Social

Responsibility (CSR) and

our commitment to the business transparency, social contribution and controlling pollution within the premises for conservation of the environment.

Core Aspects

JIT continues publishing this report which adheres to

the Global Reporting Initiative (GRI) guidelines (G3) as

the basic structure, which breaks down into five core

aspects:

Governance,

Economic performances,

Corporation Social Responsibility,

Environmental performances and

In-depth coverage on certain related issues.

These five aspects resonate with the disclosed

indicators on sustainability.

Consideration for Report Creation Process

Identify the business goals, objectives, target the main aspects relating to this report

Identify the connectivity parties, i.e. our reporting stakeholders to determine their

interests and influences over our business operation and management.

Selections of aspects as prioritized by stakeholders and Performance Indicators

associated with these aspects by applying materiality, inclusiveness and

completeness principals and respective disclosures of Management Approaches

(DMA) in relation to KPIs that we have selected and

Monitoring the collecting of relevant information for the selected indicators by

applying the comparability, reliability, accuracy, clarity, timeliness and balance

principals.

10

Scope and Boundary of Report

PCCS Group – Narrative on Group structure and legal formality

JIT – Covers all aspects of JIT operations which includes:

Waste Collection – Information on the recycled wastes

Customers – Information pertaining to sale and supply chain activities and

Fabric, accessories and packing suppliers which are our strategic supply chain partners

Besides these, general information pertaining to garments industry in Cambodia would be

disclosed accordingly to help readers understand better the business situation of the Company.

Limitations on Scope and Boundary

Even though steps have been taken to ensure full disclosure and

transparency, we are unable to disclose all information due to the following

limitations:

Only key stakeholders were selected meaning we were unable to disclose

certain aspects and performance indicators raised by the other

stakeholders

Certain data or information are unavailable for comparison due to its

completeness and relevancy to this GRI report

Basis of Reporting on Issues Affecting Comparability

As JIT did not have any subsidiary company and did not involve in joint venture

business, leased facilities, outsourced operation with any other company, the

basis of reporting which might significantly affects its comparability for the years

of 2010 and 2011 did not exist.

Significant Changes

There was no significant change from previous reporting period in the scope,

boundary or measurement methods applied in the report.

Measurement Techniques and Basis of Calculation

During the report creation process, we followed the disclosure requirement and

measurement techniques or methods recommended by GRI Reporting

Guidelines and simple linear calculation process was applied throughout this

report.

Where such techniques and methods were not available, we applied the

international acceptable standards of techniques and measurement. If such

standards were not available, we applied our internal standards based on our

assumptions. In both cases, disclosure would be made in the relevant sections

of this report.

11

Reporting Performance Indicators

We reported 24 Performance KPIs based on the GRI G3 (Global Reporting Initiatives) guidelines after

taking into consideration of the requests by some of our stakeholders and others which were needed

internally for better understanding and discussion.

Even though there were 13 new KPIs being reported for the first time in 2011, we managed to collect all the

data and information in each respect for comparison and providing relevant information to the readers of

this report.

External Assurance for the Report The Company decided to follow the GRI G3 guidelines with self-declared Level B.

JIT has no intention to obtain external assurance for this report. The GRI Content Index is disclosed on

Page 64 for reference.

Restatement

There was no restatement in the 2011 Sustainability Report.

Contact Window & Request for Feedback Producing a Sustainability Report not only is an arduous task but also requires countless hours of data

collection, collation and analysis. As such, we invite all readers for open discussion by providing us your

views on the quality and usefulness of this report.

While every effort has been made to ensure the accuracy of the information, anyone seeking to rely on

information in this report or seeking to draw detailed conclusions from the data should contact JIT for

verification and assistance.

Carlsbin Ng – Sustainability Committee Officer

Email: [email protected]

Tel: +85512333920 (Cambodia)

Economic KPIs

2010 – 02 2011 – 02 Sustained

Social KPIs

2010 – 03 2011 – 11 Up 267%

Environmental KPIs

2010 – 06 2011 – 11 Up 83%

Total KPIs

2010 – 11 2011 – 24 Up 118%

12

Governance Commitment and Engagement

Highlights GMAC

Member of Garment Manufacturer Association in Cambodia (GMAC) since 2007. One of JIT

A.G.M. is the Exco member of the Association.

Member of Fair Factories Cambodia (FFC) under the External Charter of ILO (Internal Labor

Organization)

The sustainability goals and objectives of JIT is in line with the following customers: -

Puma Sustainability Target 2011-2015 which launched in 2011 by Developing

Sustainability Projects and Target Plans (SPTP) from 2010 baseline year

adidas Sustainability Plan 2011-2015 which also launched in 2011 and monitored the

progress through internet EMeReT System (Environmental Metric Reporting Tool) from

2010 baseline year.

In-house Charity - “Jouy K‟nier” (“Self-Help” in Khmer) 2010: US$8,240 2011:US$4,593

Mission & Vision

• Our Mission is to provide our customers with the highest quality garment withthe lowest environmental impact

• Our Vision is to help conserve and protect our planet‟s resources through theuse of innovation and methods that maximizes operating efficiencies in allareas of our business.

Environmental Sustainability

• JIT is committed to leading the industry in minimizing the impact of its activitieson the environment. As a Company, we act in compliance with the law relatingto the environment and are committed to the integration of sound environmentalpractices in our business decisions. We recognize the direct and indirectenvironmental impacts of our operations and support the principles ofsustainable development.

Social Sustainability

• To be a responsible corporate entity, our corporate culture is built on respect forthe society in which we operate and an inclusive perspective on ourstakeholders embracing not just shareholders and staff, customers andbusiness partners but the community at large. Creation of value for society, helppeople in need and focus on the top priorities of the country – healthcare andeducation.

Economic Sustainability

• Profitable growth and long-term business success ensure our commitment tosustainable economic development. Maximizing resources utilization andminimizing costs are the driving forces towards ensuring that activities andinitiatives are economically viable. We practice long term gains which alwayshas preferences over short term yields.

Internal Code

of Conduct

• JIT developed internal code of conduct and principals which are in line with the statutory and customers‟ requirements

13

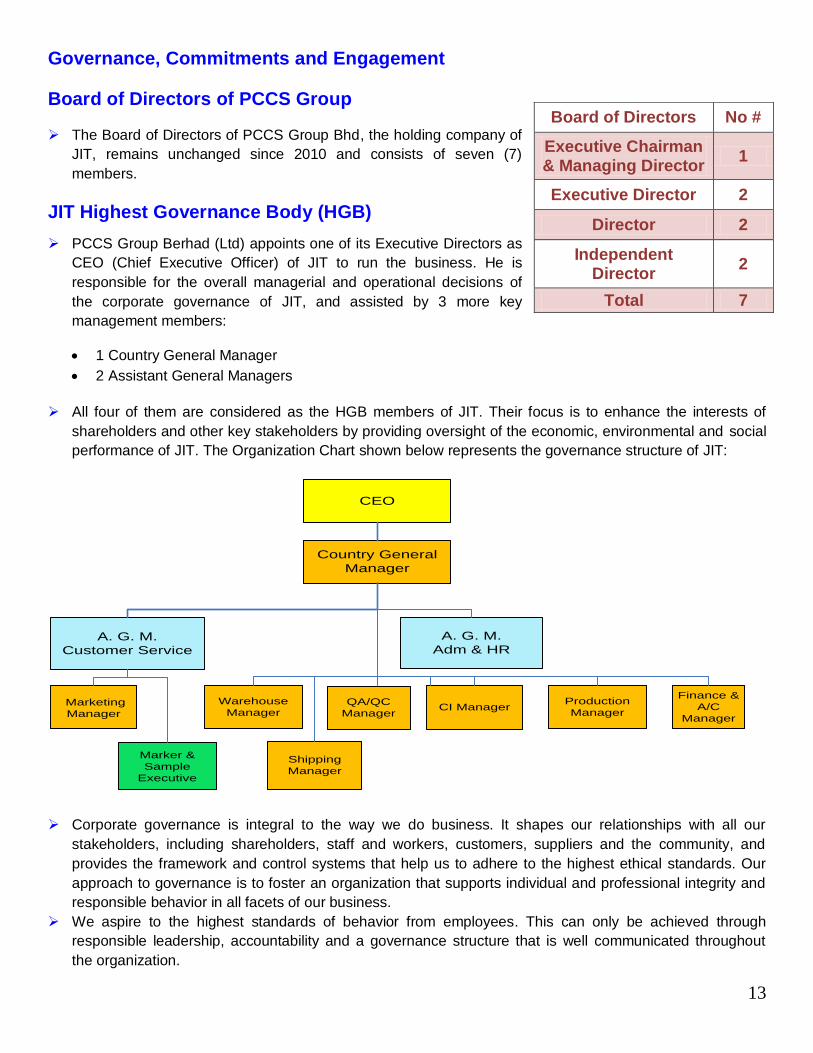

Governance, Commitments and Engagement

Board of Directors of PCCS Group

The Board of Directors of PCCS Group Bhd, the holding company of

JIT, remains unchanged since 2010 and consists of seven (7)

members.

JIT Highest Governance Body (HGB)

PCCS Group Berhad (Ltd) appoints one of its Executive Directors as

CEO (Chief Executive Officer) of JIT to run the business. He is

responsible for the overall managerial and operational decisions of

the corporate governance of JIT, and assisted by 3 more key

management members:

1 Country General Manager

2 Assistant General Managers

All four of them are considered as the HGB members of JIT. Their focus is to enhance the interests of

shareholders and other key stakeholders by providing oversight of the economic, environmental and social

performance of JIT. The Organization Chart shown below represents the governance structure of JIT:

A. G. M.

Customer Service

Country General

Manager

A. G. M.

Adm & HR

CEO

QA/QC

Manager

CI Manager

Production

Manager

Warehouse

Manager

Finance &

A/C

Manager

Shipping

Manager

Marketing

Manager

Marker &

Sample

Executive

Corporate governance is integral to the way we do business. It shapes our relationships with all our

stakeholders, including shareholders, staff and workers, customers, suppliers and the community, and

provides the framework and control systems that help us to adhere to the highest ethical standards. Our

approach to governance is to foster an organization that supports individual and professional integrity and

responsible behavior in all facets of our business.

We aspire to the highest standards of behavior from employees. This can only be achieved through

responsible leadership, accountability and a governance structure that is well communicated throughout

the organization.

Board of Directors No #

Executive Chairman & Managing Director

1

Executive Director 2

Director 2

Independent Director

2

Total 7

14

Qualification and Experiences

CEO and 3 other members of Highest Governance Body (HGB) are selected

and employed by the PCCS Group‟s Board of Directors based on their

extensive knowledge of the JIT‟s industry or experiences in financial reporting

and risk management.

CEO holds a Master Degree in MBA (Finance) and Degree in Environmental

and Social Study with more than 30 years of experiences as Lean Consultant.

Conflict of Interest

To ensure full disclosure and transparency, all members of HGB, managers and Head of Departments are required to report any potential conflicts of interest to the Company.

Already inbuilt conflict of interest into Employment Manual as an important element of the Employment Policy and Procedure, each employee should be abided by in full while providing employment service to the Company.

Identification and Management of Performances, Risks and Opportunities and

Adherence of Compliances

The HGB for overseeing the organization‟s identification and management of economic, environmental and

social performance, including relevant risks and opportunities, and adherence of compliance with

internationally agreed standards, codes of conduct and principals becomes part of its managerial functions

to keep the Company economically viable and sustainable.

Procedure is in place by setting and communicating performance standards including goals and objectives

and expectations, observing and providing feedback, and conducting appraisals enables JIT to achieve the

best results through identifying and managing these performances and adhering compliances.

Well-established executive, audit and compliance and human resources also ensure that their

responsibilities are upheld and executed to the highest level.

Should assessment is required; SWOT analysis is applied to evaluate the risks and opportunities.

Highest Governance Body (HGB) Performance Evaluation

The HGB performance evaluation process, including goal setting,

performance measurement, regular performance feedback, employee

recognition, and documentation of employee progress, is set by the Board of

Directors (BoD) of PCCS Group to ensure the successes both in JIT

business operation and members of HGB achievements on a yearly basis.

The performance appraisal is part of that process and provides an excellent

opportunity for BoD to communicate with the HGB members about past

performance, evaluate their job satisfaction, and make plans for JIT future

performance.

MBA Environmental & Social Degree

15

Precautionary Approach to Risk Management

A response to the organization‟s approach to risk management in operational

planning or the development and introduction of new products can be summarized

as follows:

Identification and prioritization of risks,

Reporting of these findings to our Head of Departments Committee periodically

and inform of our strategic planning and operating plan processes,

Execution of programs and monitoring of planned activities to mitigate the risk

level

Evaluation of the effectiveness of the plans and review for future actions

Mechanism for Shareholders and Employees Providing Direction & Recommendation

The concerns of the stakeholders, especially the shareholders and employees in providing direction and

recommendations, are well deal with by the Highest Governance Body (HGB) of JIT and other

committees as elaborated in the coming statements through direct involvement in operational activities

and the channels of communication.

Direction and recommendation from shareholders and employees can be conveyed to the parties below

mentioned by many ways such as agenda tabled for discussion in the meetings.

Outcomes of the discussion pertaining to issues raised by shareholders and employees will be

addressed by with solutions and relevant remedial actions.

Direction and Recommendation to Group Level

PCCS Group Berhad (Ltd) holds Annual General Meeting in Malaysia where all shareholders decide on

matters relating to the overall business and management of the Group companies. The intention and

expectation of the shareholders were conveyed to Board of Directors (BoD) during the meeting.

The BoD conducts regular board meeting, based on the strategy set in Annual General Meeting, to

oversee the overall operation and management of all subsidiaries within the Group and supervises the

HGB members to carry out managerial and operational decision makings in the interest of JIT.

JIT Factory-wide Level

The HGB members

They hold weekly senior management meeting to formulate policy,

objectives and goals, make decisions regarding the business strategies

and targets formally set, monitor the running of business, analyzed and

review the business outcomes.

The Head of Departments Committee (HODC)

HODC holds weekly meeting to discuss the daily business activities and

operations of the Company where its sub-committee, Sustainability

Advisory Committee (SAC) (formerly known as Sustainability

Committee) reports directly to HOD Committee on events pertaining to

sustainability.

16

By Functional Committee Level

Sustainability

Advisory

Committee

Health, Safety &

Environmental

Committee

Corporate Social Responsibility

Committee

In-house Charity

Fund

Labor Union

No# of Management (Mgmt) and Employee (Empe) Members

Sustainability Advisory Committee (SAC)

While SAC is responsible for the sustainability activities, its implementation and development programs is

further assisted by sub-committees namely HSE, HR, LEAN and CRS, each with specific functions related

to their fields of specializations. The representatives from each sit in the SAC meeting on the monthly

basis.

Reports

Health, Safety &

Environment

Committee

( HSEC)

Reports

Human Resource

(HR) Department

Board of

Directors CEO

Head of

Departments

Committee

(HODC)

Sustainability

Advisory

Committee

(SAC)

Reports

Corporate Social

Responsibility

Committee

(CSRC)

Reports Reports Reports

Reports LEAN

Department

Health, Safety and Environmental Committee (HSEC)

It is a sub-committee of the SAC, which has general oversight responsibility for compliance:

Oversee the company‟s implementation of compliance programs, policies and procedure that are

designed to be responsive to the various compliance and regulatory risks facing the company

Assist the SAC in fulfilling its oversight responsibility for the Company‟s compliance, polic ies and

procedures

Members comprise of personnel both from management and local employees with 50% and 50%

proportion respectively (2010: 50% to 50%). It holds monthly meeting to discuss the related issues.

2010: 4 – 1

2011: 4 – 1

Sustained

2010: 7 – 10

2011: 8 – 12 Mgmt Up 14%

Empe Up 20%

2010: 5 – 5

2011: 5 – 5

Sustained

2010: 0 – 3

2011: 0 – 3

Sustained

2010: 0 – 15

2011: 0 – 15

Sustained

17

Corporate Social Responsibility Committee (CSRC)

CSR policy functions as a built-in, self-regulation mechanism whereby

monitors and ensures its active compliance with the spirit of the law, ethical

standards and international norms.

The goal of CSR is to embrace responsibility for the Company‟s actions and

encourages a positive impact through its activities on the environment,

consumers and all stakeholders.

The major projects which the Committee is currently running are the In-house

Social Charity Fund and customers CSR audit sustainability. The ratio of

management to local workers is 50% to 50% (2010: 50% to 50%) and the

Committee meets on a quarterly basis and report to SAC accordingly.

In-house Social Charity Fund

It is named as “Jouy K‟nier” (“Self-Help” in Khmer) and provides charitable fund to

the employees since 2010 in the following circumstances:

Natural disasters like flood and fire suffered by families of employees,

Injury & sickness suffered by employees,

Death of immediate family members of the employees and

New born babies of employees

From the Employee Survey feedback, charitable foundation is useful for

strengthening factory reputation and relationship among employees. JIT has set a

good example by engaging in charitable project directly and determining conditions

of providing assistance to employees when needed. It strives to provide better

service in this respect so that the welfare of the employees would be further

enhanced in future.

Social Charity Fund distributed: 2010: US$8,240, 2011: US$4,593. For more detail

information, please refer Table A in the Appendixes.

The fund paid was contributed and shared equally by JIT and the Labor Union

whose cash collected are from its members. Even though the cash amount

distributed in 2011 was lower than last year, we strongly believed that all

employees were aware of such fund and the claim entitlements.

Labor Union

Labor union named United Labor Union is formed under the local

legislation. It is an independent body formed by the employees of the

Company taking charge of the welfare and rights of the Union‟s

members.

Union members take part in trainings, both conducted internally or by

external consultants, on HR and union topics so that the minimum

statutory and customers requirements are made known to them. The

union conducts meeting with management on a monthly basis.

CSRC Ratio Mgmt – Employee 2010: 50% - 50% 2011: 50% - 50%

Donations 2010: US$8,240

2011: US$4,593

Union members 2010: 2,140 (85.45%) 2011: 2,350 (87.92%) of total workforce

18

EXCO – Deputy

Chairman

Informal dialogues For informal issues-based discussions with Line Leaders and Supervisors in

all departments of JIT, HOD (Head of Department) conducts regular meetings

to listen to the needs of employees and take initiatives to make improvements.

Issues raised by the employees or complaints received from employees‟

suggestion box are brought to the meeting to openly discuss and corrective

actions taken to mitigate or settled accordingly.

Linkage between Compensations for HGB, Managers and

JIT’s Performance

As JIT is 100% owned by PCCS Group Bhd, the holding company is entitled

to any dividend which is proposed by the Board of Directors, and approved

by shareholders during the Annual General Meeting. There was no dividend

declared in 2010 and 2011

Members of HGB and managers obtained their respective remunerations and

fringe benefits based the employment contracts signed between JIT. Bonus

will be given based on the overall financial performance of JIT on the yearly

basis.

JIT did not specifically allocate certain amount of cash as compensation to

them in respect of social and environmental performances that they

achieved.

Subscription or Endorsement to External Charter

JIT is a member of Fair Factory Cambodia (FFC) under the Endorsement to

External Charter of ILO (Internal Labor Organization) since 2007.

Under this endorsement agreement, FFC conducts compliance audit twice a

year on unannounced basis. JIT participated in certain training courses

conducted by FFC so that the latest developments and update information on

labor, legislations, code of conducts, principles and standards were followed

up and closely adhered to.

GMAC Membership and Position Held

JIT is a member of Garment Manufacturer Association in Cambodia (GMAC)

since 2007 up-to-date and enjoys some of the prominent benefits:

Obtaining first hand information of government and relevant authority

via GMAC

Active in negotiation with governmental bodies via GMAC so that the

interest of members is protected.

GMAC

19

GMAC EXCO Member

One of JIT Assistant General Managers, Mr. YT Choon is the

Deputy Chairman of GMAC since 2009 until up-to-date. Being an

EXCO member in GMAC, he is actively involves in the followings:

Trade facilitations which involve Ministry of Commerce, Council

of Development of Cambodia and Custom Trade Department, a

sub-unit of Ministry of Finance.

Industrial Relations which involve ILO, National Labor Union and

Ministry of Labor,

Financial arrangements between members and the Ministry of

Finance, especially on the tax matters (corporate and employee)

Negotiation on the construction of National Garment Institute –

Donation of US$3 million from France

Promoting Cambodia as a garment sourcing center. GMAC organized a forum in Japan, 2008

Encouraging fabric mills to invest in Cambodia. GMAC organized a forum in DongGuang city, China,

2011

Training programs – GMAC is collaborating with JODC (Japan Overseas Development Corporation)

on paper pattern design course to local Khmers

Exhibitions

Act as a co-organizer for a series of trade fairs such as SASFA Global Forum Seminar in Phnom Penh &

Workshop and Cambodia Trade Fair in Siam Reap

The activities that JIT participated in 2011 were as follows: -

Garment Trade Fair in New Delhi

Cambodia Trade Fair in Phnom Penh

….

20

2011: 7 2011: 7

Sustained

Identification of Stakeholders and Selection for Engagement

Goals

Setting

Sales

Growth Energy Saving

CO2

Emission

Reduction

Waste

Reduction

Water

Saving

No# of

Stakeholders

2011

Target

2010

Based Yr.

Based on

2010 Sales

Based on Per Piece of Garment

Produced

Based on

Per Worker

The process of identification, selection and engaging of stakeholders is done by SAC and HESC

committees during report preparation stage.

They start liaising with relevant departments, meeting stakeholders and governmental bodies‟

representatives to identify business goals, aspects and related indicators that are relevant and appropriate

to the report by considering factors:

Usefulness, reliability, materiality and inclusiveness of stakeholders

Sustainability context, completeness of data/information needed to be collected and represented.

Expectations and interest of the organization and stakeholders which are equally important when

deciding the content of the report.

The process of identification of business goals, aspects and performance indicators includes:

Using various approaches such as relevancy of business goals; prioritize stakeholders, principal of

materiality, stakeholder inclusiveness, completeness and sustainability context.

The business goals and types of positive and negative impacts associated with possible actions

counter-balance the negative impacts.

Business Goals and Targets Settings

JIT‟s key business goals and targets set, taking 2010 as the baseline year,

with related stakeholders can be summarized as follows:

2011 Sales Growth – 5% (2010: 2%)

Energy Saving – 20% both for direct and indirect energy sources based on per piece of garment

produced

CO2 Reduction – 20% on the direct and indirect energy used in JIT based on the conversion rate on

quantity or volume of emissions and effluents

Waste Reduction - Encourage the recycle of by-products and wastes by 10% based on total materials

Water Saving – 15% based on consumption per employee

Full compliances on statutory and regulatory and customer‟s requirements covering economic, social

and environmental aspects and impacts. Target: Zero fine

Quality Policy – The Company is committed to understand, meet, and when possible, exceed

customer‟s requirements through the continuous improvement of our processes and dedicated to

delivering defect-free product on-time at the most competitive price possible

5%

20%

20%

10%

15%

21

Engagement Methods

The potential stakeholders were identified when we defined the business goals

and main aspects. To determine the level of engagement, we analyzed the rate

of “Influence” and “Control” to these stakeholders and vice versa.

Our stakeholders provide a diverse range of perspectives and we maintain

various formal management systems to engage with, listen to and learn from

them. We take their feedback seriously, and when appropriate and relevant to

our business, incorporate it into our thinking and planning.

To prioritize our stakeholders and their concerns, we set the engagement plan,

taking into considerations of the following aspects:

significant/strong influences and/or,

significant impacts on the economic, environmental and social issues

between us,

the relevance of the stakeholders‟ relationship both direct & indirect to our

business and

the importance of the particular issue being raised

After brainstorming process, those stakeholders with significant impacts both

positive and negative outcomes were selected by taking the factors above

mentioned into consideration, the higher the total score, the stronger is the

connection and the final list of stakeholders is shown in Table 1 which are

similar to 2010 for sustainability report creation.

1 Employees

2 Shareholders

3

Government –

Ministry of

Labor, Tax

Department &

Ministry of

Environment

4 Customers

5 Waste

Collectors

6 Suppliers

7 Local

Community

Table 1

Like 2010 where the sustainability engagement team continued contacting and communicating with the

selected stakeholders on our intention to engage them again in 2011. Feedback from above stakeholders

revealed that they were willing to be engaged again for 2011 GRI report creation.

In the events when a particular stakeholder group is in a large group such as employee and local

community, different approaches had been applied to collect information to ensure the accuracy and

reliability of them. In cases of certain limitation of approaching the issues, we interpreted the aspects into

simple and practical issues to help our stakeholders understand more easily hence providing relevant

information in return.

The members of Sustainability Advisory Committee have done the engagement activities with potential

stakeholders their concerns on our business operations as well as main aspects of the report by the

following ways:

face to face interview,

telephone enquiry,

direct dialogue,

extract of data and information and analysis, email correspondence and

questionnaires

22

Stakeholders’ Feedback – Key Concerns

Governmental Bodies 1. Tax Department - It mentioned that not only JIT (the Company)

paid the monthly employee tax amount on time by withholding

individual employee tax portion but also disclosed the income of

individual employee on the gross amount, meaning the Company is

obliged by the legislative requirements to withhold tax and set a good

example for other factories to fully comply in Cambodia.

JIT has regular face-to-face meeting or through email with Tax

Department officers pertaining to updating of tax information.

Prioritized stakeholders

Aspects chosen by

stakeholders

List of aspect to be reported

List of indicators associated

with aspects

Materiality test

List of indicators to be reported

Completeness test

Determination of Materiality and Reporting Indicators

For this Report content, we have carried out the tests of reporting principals

including Materiality, Inclusiveness, Completeness, Sustainability Context and

the steps taken can be summarized in the Engagement Process Flow on the

right

Prioritization of stakeholders together with inclusiveness, list of aspects

chosen by stakeholders and to be reported have been disclosed and

explained in the foregoing statements. The following principals are equally

important:

Materiality

After considering the potential core indicators and associated main aspects,

we applied the materiality tests by answering several relevant test questions

for each indicator. First 24 highest scored indicators were selected for GRI

Reporting creation purpose.

Those indicators with adverse effects were considered if those would affect

our performances. Subsequently, JIT would implement corrective actions to

check such drawbacks.

Completeness

We applied completeness tests to the following issues to ensure that the contents

reflect our significant aspects and allow our stakeholders to review our

performance:-

Inclusiveness of entities which our Company has control and influences over

them or to be controlled by them

Providing sufficient information concerning to stakeholders concerns or

company impacts

Reporting on significant events or impacts

Engagement

Process Flow

23

2. Ministry of Labor - It emphasized that the

Company should continue providing high quality

working condition to all employees.

Knowing that the total workforce has increased to

3,200 employees, the Company has continuously

playing greater role in providing job opportunities to

the residents surrounding the Factory as well to the

rural workers despite the fact the basic salary has

increased by about 25% since last year due to the

influx of foreign businessmen investing in

Cambodia at the beginning of 2011.

The Company has to submit certain reports to the

Ministry and meet them on a monthly basis hence

labor issues can be brought to discuss freely.

3. Ministry of Environment - It stressed the

importance of meeting the minimum legislative

and regulatory requirements of environmental

protection.

Based on the audit reports done half-yearly, JIT

passed all regulatory tests such as drinking

water content, machinery and equipment

operation standards, water treatment discharge,

noise and heat levels.

In addition, JIT achieved best practices in

Energy, Water and wastes reduction by more

than 30% in 2011 comparing to 2010

performances. During closing meeting, the

Ministry officers discussed directly with us on

the matters to be improved in each audit.

Customers 4. As part of the supply chain, customers support and encourage JIT in sustainable

compliance practices in order to maintain the world leading garments manufacturer

status concerning product and conservation of environment.

Puma has upgraded JIT CSR (Corporate Social Responsibility) status from B+ to A

grade in S.A.F.E. audit in 2011.

Suppliers 5. The feedback from existing suppliers still concentrated in strengthening the

business partnership in material supply chain.

Non ASEAN countries suppliers admitted that they have grabbed the chance by

trading big quantity of materials throughout the year due to EU (European Union)

further extends the GSP (Generalized System of Preference) trade privilege to

Cambodia manufacturing sectors.

All fabric suppliers have to come to JIT for the types, quantity and quality of fabric

for the new sample garments development in each season.

6. Community Hawkers

Local Community hawker‟s sales increased by 25% (between 100,000 to 240,000

riel or US$25 – US$60) when compared to last year.

Approximate earnings of 60,000 to 120,000 riel (US$15 to US$30). The sales

volume was higher than last year because JIT split the lunch break into two

sessions, i.e. one at 10:15am and another at 11:00 am as the total numbers of

workers has increased considerably. 90% of the hawkers admitted that they relied

heavily on the income earned from here to support their family lives.

24

Employees

7. Employees‟ Survey conducted in 2011 summarized the following key points: Employees’ Survey Summary

Areas of

discussions

Significant improvements Satisfaction

Level

A Occupational Health & Safety 2010 2011

Working

conditions –

Noise, Heat,

Ventilations

Noise reduction - Constructed concrete building to install the

generator located about 15 meters away from the nearest production

floor. In 2010, the generator is located 3 to 5 meters away from the

Electrical and Embroidery Departments. Decibel: 2010: 93 2011:65

(Acceptable level: 75 and below)

Heat reduction – Using shelters made of fabric mesh to block the

directly contact of sunshine to production floors.

Exhaust fans used in water curtain cooling system of which take

away the heat from the production floor are covered with hollow

cylinder-shape fabric to prevent sunlight.

Extending the function of water curtain cooling system by additional

2 hours per day from 8:30 am to 4:30 pm. {Normally from 9:30 am to

3:30 pm } Temperature: 2010: 32OC, 2011: 29OC

79% 87%

B High risks

areas

Shifted the Printing Ink Chemical Room out of production floor and

allow having chemical ink for single day‟s consumption only in the

Design Room. The exposure of hazardous chemical to printing

workers has greatly reduced.

75% 90%

C Day Care

Center

Double the current size of the Day Care Center plus a playground for

the children of the JIT employees to stay more comfortably.

78% 95%

D Recycled

Waste Store

Constructed a concrete store to keep recycled wastes for the

protection of the environment.

JIT management conducts monthly meetings with the Labor Union and Shop Stewards on workers welfare and

concerns.

Shareholders

8. The importance of profit to a business is that JIT knows exactly what

can be spent to make the business prospers and makes sure that we

can develop our merchandise and services to make them better to

attract more customers to the business. Other benefits derived from

profit in business includes but not limited to:-

It helps in the development of the company position in the market,

It judges the position of their management ,working involvement of

workers and healthy proper accounting and

It acts as a benchmark for future challenge of the Company and

long-term stable business development and expansion so that the

revenue generated can be further distributed to all relevant

stakeholders.

25

Obtaining Grade A in PUMA

S.A.F.E. audit rating with score

of 96.96% in 2011

Sustaining Grade A in Technical audit

conducted by Puma for two consecutive

years with same score of 96% in 2010-

2011

All these years, we are pride of ourselves in our ability in providing Puma

the branding services it required in a cost and brand-concious manner

JIT materializes the corporation vision which focuses on top quality, cost effectiveness, excellent customer service and on time delivery in our sustainable products

Total Puma garments made 2010 – 2.11 million pieces, 2011 – 2.49 million pieces

Puma Sustainability Program 2011-2015 - Monitor the progress through E-KPI Measurement System (internet Enablon System)

Vincent Ng, Cambodian boy starts drawing World Cat

26

Economic

Economic Management Approach

Profitable growth and long-term business success ensure our commitment to

sustainable development. Transparent, honest and fair business dealing helps

position JIT to realize opportunities for our continuous growth and outperform

our stakeholders‟ expectations.

By demonstrating good governance, sensible risk taking and transparency in

communication, business continuity and expansion is most effective when it is

integrated with business processes and organizational management systems.

JIT continues allocating an appropriate proportion of its fund or profit

generated into environmental protection expenditures and investments which

we believe that the short term spending brings greater long term gains to the

Company.

GRI Report published annually is one of the many ways of JIT in providing

information regarding economic performance and market presence of the

Company.

JIT offers competitive benefits to our stakeholders which are better than that

of similar industries of the country in most cases, making it an attractive

garment manufacturer in Cambodia.

By demonstrating good governance, sensible risk taking and transparency in

communication, business continuity and expansion is most effective when it is

integrated with business processes and organizational management systems.

27

Economic Highlights

2011, Cambodia continued to be granted by European Union (EU) the privilege of Generalized

System of Preference (GSP) where all materials imported from overseas, irrespective of

countries of origin, will enjoy tax relief for buyers importing garments in EU countries.

Sales increased by 57 % from 2.90 million in 2010 to 4.55 million pieces in 2011 with more

efficient materials utilization rate and natural resources usages.

Continue using PUMA-approved environmentally friendly CHT inks for all screen printing

panels.

Deployment of Lean Manufacturing System to maintain sustainability growth and expansion as

well as making it another profitable year in 2011

Doing Business in Cambodia

Doing business in Cambodia was becoming more competitive than before d ue to the shortage of labor

and ever rising labor cost. Global rising labor and material costs, especially in China, had resulted many

foreign investors to look for alternatives for production base and selected Cambodia as one of their

choices.

Cambodia has become a popular prospect for foreign investment, with regional investors, such as China,

Malaysia and South Korea, seeking to capitalize on emerging business opportunities. Since then,

garments factories competed among each other both for skillful as well as new workers to fill up their job

vacancies.

The garment and footwear industry has been the main magnet for foreign investment since 1993.

However, in recent years, other sectors of the economy have been catching up, including tourism,

construction, telecommunication, extractive industries and exploration of mineral resources. Investment

opportunities in Cambodia are plentiful and substantial for both local and foreign investors.

It is the newest investment destination in the region especially the GSP tax privilege system strengthened

by EU.

It has become even more attractive after the Royal Government devoted more attention to strengthening

political stability and the rule of law, and mobilizing all available resources for greater economic

development. All these add to the acute labor shortage in the country.

Major Steps Taken in Sustaining Business Growth

Major steps have been taken in 2011 to check the ever increasing labor cost while striving to sustain

business growth and expansion. During the year, the Company continuously practicing Lean

Manufacturing System which focused on the following aspects:

Incoming materials and production management - Close monitoring processes on procurement,

accessories & fabric consumptions, reduce defective parts to the minimum level during production,

28

Quality – emphasis on the upgrading of quality standard

Efficiency – focus on daily productivity as well as documentation process efficiencies to increase output

and practice over shipment of finished goods if allowed by customers and

Waste Reduction – Physical and process wastes are 2 major areas where all workers have to take

steps to mitigate or eliminate them aiming at shortening lead time, improving quality and saving cost.

Non-production overheads – Tightening the expenditures by removing repetitive activities of same

nature, reduced frequency and timings and spending based on approved amount.

Requested an average 10% increase in CM price but customers only approved about 5% which was

reflected in the FOB price of the finished garments.

Some of the prominent outcomes of such implementation can be summarized as follows (refer to

Financial Overview 2010-2011 below):

Cost saving of around 4% in procurement and control of materials amounting to US$715,500,

Overheads saving by 3% amounting to US$135,100,

The balance of estimated US$850,000 was from the increased FOB price

In short, Lean initiatives implementation is inevitably one of the key factors to the success in maintaining

sustainable growth and expansion as well as making it another profitable year to JIT operation.

It‟s of great challenge to the Company as well as to all staff and workers in achieving higher target set for

2012 as the expansion actions are essential to meet the requirements and expectations of our

stakeholders.

FINANCIAL OVERVIEW OF 2010-2011

Summary of 2011 financial results by referring to Graph 3 below:

Sales

Profit

Production

Volume

In general, 2011 business was good with quite constant production

volume to fill-up the monthly capacity throughout the year

Sales orders in pieces increased tremendously by 57% and it was

able to be absorbed by production floors after successful recruitment

of workers

Increase in FOB sale price by 13% was lower than the target of 20%

set previously due to competitive selling price set by the customers

Materials

Wages

Rising material costs by 13% and labor shortage have become great

challenge to operate apparel manufacturing factory profitability in

Cambodia

When labor shortage problem existed, JIT increased basic wage

which was higher than the National minimum amount and extra

allowances to maintain the labor force resulting 28% and 22% rises

for direct and indirectly wages respectively

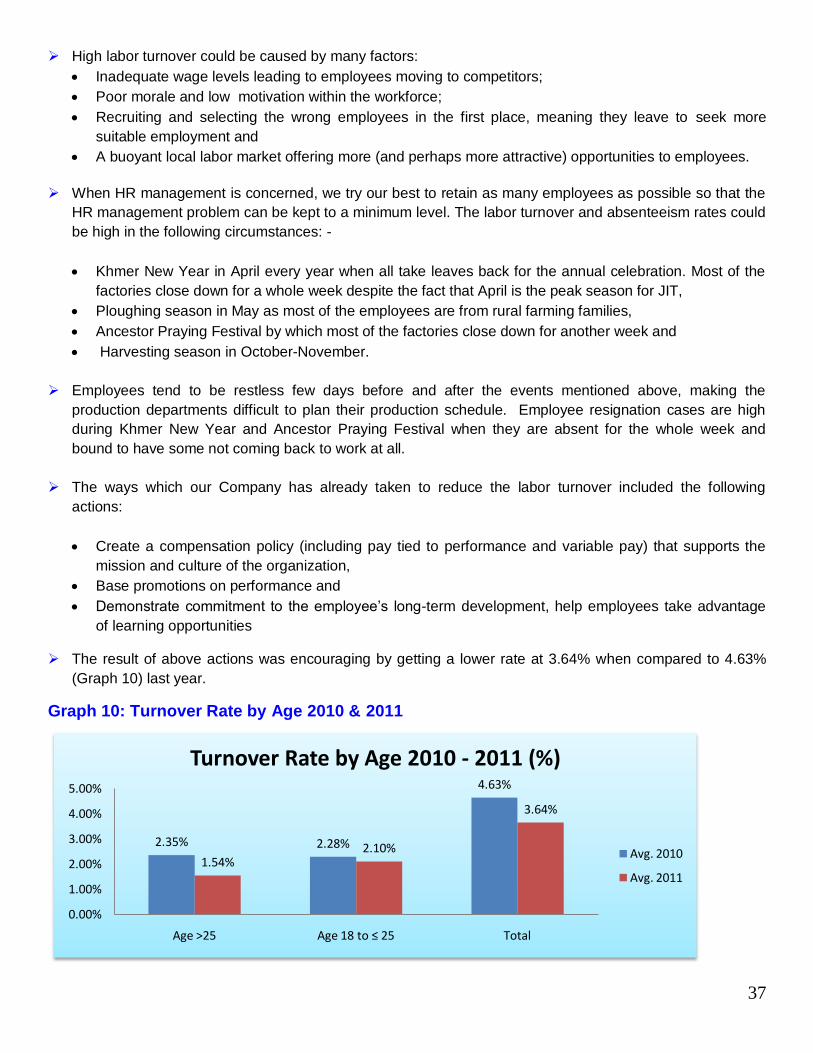

Uncertainty is perhaps the biggest challenge facing apparel industry in future. The economic situation in

Europe and US, swings in garment prices, acute labor shortage and rising operating costs, all add up to

a worrying year. There may be opportunities to increase productivity and reduce non-value added

activities to create competitive advantage for JIT to sustain growth and expansion in the coming years.

29

SalesProfit

MarginProfit

Raw Materials

Direct Wages

Indirect wages

Sales in million pieces

Total workforce

Percentage 13% 62% 82% 13% 28% 22% 57% 28%

13%

62%82%

13% 28% 22%57%

28%

0%

50%

100%

Per

cen

tage

Major Corporate & Financial Ratios2010 V.S. 2011

Graph 3: Revenue and its Distribution

Note: For more details, please refer to Table B in Appendixes.

Comparison of Business Forecast and Actual Outcomes By comparing the targets set in the first GRI Report, 2010, Graph 4 displayed the forecasted figures

against actual outcome of the financial situation:

Sales volume was 6% short of

forecasted figure due to the actual

average FOB price slightly lower than

expected. Forecast sale in 2012:

US$30 million (2010: US$28.5

million) increased by 5%

Economic value retained (profit)

slummed by 40% mainly due to rising

direct and indirect labor cost and

partially due to rising material cost.

Forecast labor cost in 2012: 25% of

Turnover (2011: 24%)

Sales in pieces shot up by 34% due

to GSP (Generalized System of

Preference by EU) effect. Forecast

manufacturing pieces in 2012: 5.5

million pieces, (2011: 4.55 pieces)

22% increase.

Due to expansion of 10 sewing lines.

More manpower was needed. JIT

expects to maintain same number of

workers in 2012 (2011: 3,200

workers)

Graph 4: 2011 Business Forecast Vs. Actual

Sales ProfitSales in pieces Workforce

Percentage -6% -40% 34% 18%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Per

cen

tage

2011 Business Forecast V.s. Actual Expenditure

30

Market Presence & Localization of Manpower The balance between the employment of right people and machinery is one of the fundamental principal if

one Company wishes to carry out its production efficiently. The Recruitment Procedure emphasizes on the

prioritization in selection of local citizens during new intake process with no racial and gender

discrimination.

We continue strengthening the collaboration between stakeholders, especially the local community where

most of our workers stay in so that they are able to work in JIT factory as near to their residences as

possible

In addition, JIT has gained confidence from the renowned buyers to be the strategy supplier in this respect

which is also in line with the government objective to prioritize local citizens in the recruitment process.

Graph 5 displays workforce diversification as at 31-Dec-2010 & 2011 in the Company

Khmer workers have increased by 1.32%, representing 716 employees whereas expatriates reduced

slightly from 96 to 84 persons. The company management was confident that the trend of hiring local

supervisors and middle management level personnel was positive and in lined with the Ministry of Labor

who represents the governmental body in ensuring fair recruitment process is being exercised and fully

support in searching of local manpower.

Despite the fierce manpower recruitment competition both from existing and new factories surrounding

JIT, statistical data showed that 78% of the total workforce remained working with us after one year of

development. Many approaches have been applied by HR Department with the assistance of Head of

Departments to upgrade the skill and competence level of employees

BY providing trainings and disseminating relevant knowledge, skill and techniques to the exiting workers,

some new faces were being promoted to the managerial level. They have shown their capabilities in their

respective fields of expertise. This reflects the eagerness of the Senior Management to localize workers

working in management positions.

2010 2011

Khmers 96.18% 97.50%

Chinese 2.46% 1.35%

Malaysians 0.96% 0.82%

Filipinos 0.32% 0.27%

Hongkies 0.08% 0.03%

Indonesian 0 0.03%

0%20%40%60%80%

100%120%

Per

cen

tage

Graph 5 -Workforce by Nationality2010 - 2011

Khmers

Chinese

Malaysians

Filipinos

Hongkies

Indonesian

31

In general, there are some improvements in localization of management posts. The Company plans to

increase at least one local manager in 2012

Graph 6 below shows a promising result, especially the supervisory and technical level locals with 78% and

334% improvements respectively. The Ministry of Labor encourages the Company continues training local

workers in order to take up the posts previously occupied by expatriates such as HOD (Head of

Department), executives, supervisors and leaders

6: Workforce by Employment Type at 31-Dec-2010 & 2011

Note: For more details, please refer to Table C in Appendixes.

Total Environmental Protection Expenditures and Investments by Type and Reinvestment

JIT has numerous environmental protection projects in hand since its incorporation in 2007. By tracking

and analyzing the expenditures and investments over a period of time, these data allows us to judge the

value of complex organizational or technological investments for improving environmental performance.

The Sustainability Advisory Committee and our Finance and Accounts Department have developed a set of

environmental management accounting system that tracks multiple categories of information including

reinvestment strategy. Both parties review the progress of the projects on a yearly basis and decide what

should be done for the following years.

This indicator focuses on waste disposal, emissions treatment, remediation costs, as well as prevention

and environmental management costs. Pictures shown on next page are some of the environmental

protection initiatives carried out in JIT and the details on the categories and benefits are disclosed in

Tables D & E in the Appendixes.

Managerial Supervisory Technical Clerical Operational Sub-total

Percentage 0% 78% 334% 33% 14% 30%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Per

cen

tage

Workforce by Employment Type Ratio31-Dec-2010 V.s. 2011

32

1. Spiral staircase 2. Cooling System - 3. Aboveground Water 4. “Totoo” car

sliding slope Water Curtain Tanks

Benefits

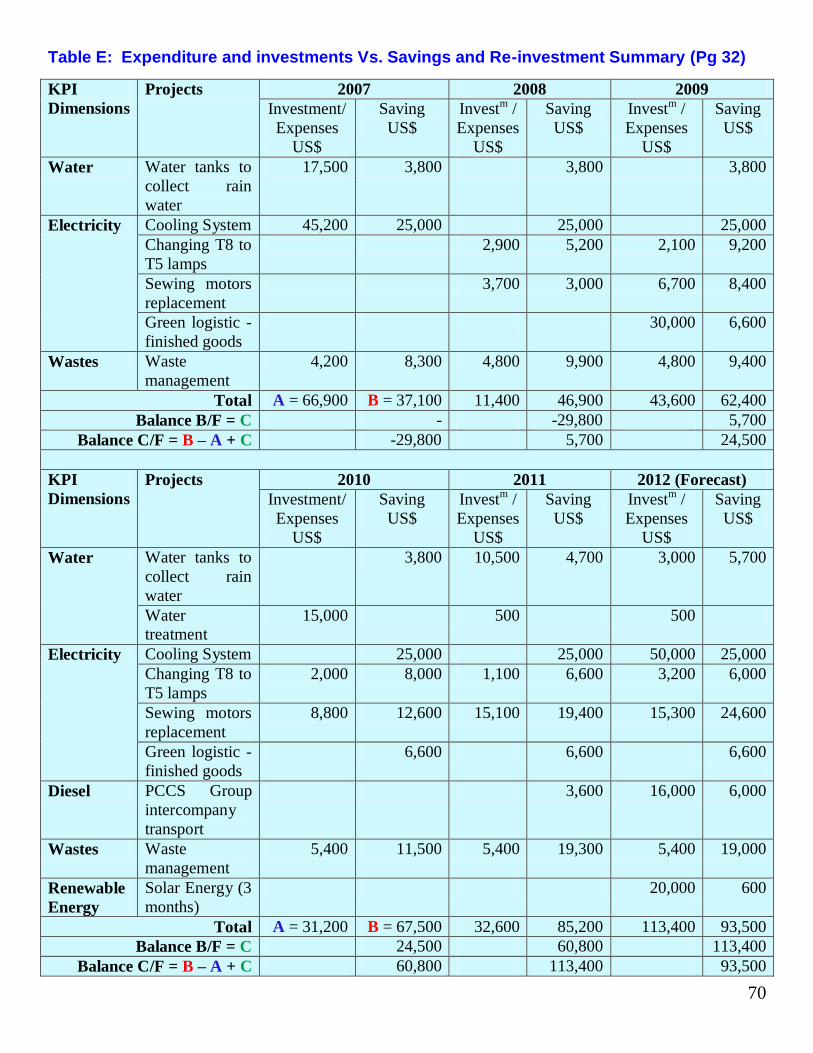

The accumulated net financial benefit from 2007 to 2011 as shown in Graph 7 below was US$113,400

(Saving US$299,100 - Investment/Expenses US$185,700) and the balance can be utilized for future

improvements especially in renewable energy investment.

While we believe that our collective commitment to environmental initiatives, we continue our investments

so that benefits to employees and JIT factory is greater from the past.

Graph 7: Expenditure and Investments Vs. Savings and Re-investment Summary

Note: For more details, please refer to Tables D & E in the Appendixes.

Expenses mentioned in Graph 7 include prevention and environmental management costs, regulatory

treatment and testing costs but excluding fines for non-compliance with environmental regulation.

2007 2008 2009 2,010 20112012 ( Foreca

st )

Balance B/F 0 -29,800 5,700 24,500 60,800 113,400

Investment/ Expenses US$ 66,900 11,400 43,600 31,200 32,600 113,400

Saving US$ 37,100 46,900 62,400 67,500 85,200 93,500

Balance C/F -29,800 5,700 24,500 60,800 113,400 93,500

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

USD

Year

Expenditure & Investment V.s. Saving and Reinvestment2007 - 2012

Balance B/F

Investment/ Expenses US$

Saving US$

Balance C/F

33

2012 Improvement Projects

JIT reinvests on environmental protection projects from the surplus

generated from the current practice. As the effort to protect the

environment is an endless process, we take the initiatives to

continuous meet or exceed all the environmental legislation that

relates to the Company:

Renewable energy- solar generated lights as street lights for

exterior space,

Re-invest in cooling system as the fixture has reached the full

5 years of depreciation,

Replacing polybags with fabric bags to store cut-panels in

Cutting Section.

Significant Fines and Non-Monetary Sanction The level of non-compliance within the organization helps to

indicate the ability of management to ensure that operations conform to certain performance parameters. From an economic perspective, ensuring compliance helps to reduce financial risks that occur either directly through fines or indirectly through impacts on reputation.

The strength of an organization‟s compliance record can also affect

its ability to expand operations or gain permits. The strength of an

organization‟s compliance record can also affect its ability to

expand operations or gain permits.

Transparency in reporting encouraged JIT to report fines and non-

monetary sanctions in terms of the focus of laws. Since its

incorporation in 2007, JIT has not identified any non-compliance

with laws or regulations therefore no monetary fines or non-

monetary sanctions being imposed by any party so far.

Significant fines for non-compliance with laws and regulations concerning the provision and use of products and services. In order to avoid fines in respect to this section, all Head of

Departments are taking charge of the relevant statutory and

regulatory compliances by closely monitoring to ensure full

compliance at all times.

Similarly, JIT has not identified any non-compliance with laws or

regulations concerning the provision and use of products and

services therefore no monetary fines being imposed by any party

so far since 2007

34

Social

Social Management Approach JIT regards itself as an active member of the society so that we are committed to

acting in the best interests of our employees and the community people who live

and work near our Factory. After all, we benefit from highly motivated and well-

qualified employees, satisfied customers and good relations with our stakeholders

that are based on mutual trust.

To be a responsible corporate entity, we create value for society and all employees

in the best practice of:

JIT is committed to providing a happy, safe and healthy working environment for

all employees. We constantly engage and develop our employees to the full

extent by providing a diverse and equal work opportunity to them in order to

attract and retain the best individuals for our continuous growth,

JIT helps employees in need through our “Jouy K‟nier” (“Self-Help” in Khmer)

donations and focus on the top priorities of the country – healthcare and

education,

JIT constantly conducts open and constructive dialogue with our communities

relating to economic, social and environmental aspects and impacts,

JIT does not discriminate on the basis of gender, ethnicity personal

characteristics or belief and

JIT is not involved in activities including child labor forced labor, discrimination