Embed Size (px)

Citation preview

Corporate Tax Act

INTRODUCTION

Details of Enactment and Amendment

● Enactment: The Corporate Tax Act is a statute that provides the regulatory details of corporate taxes which are assessed on the earnings and liquidation incomes of a corporation for each fiscal year. This Act was enacted on November 7, 1949 as Act No. 62.

● Amendment: This Act has been amended almost every year, almost as an annual event, including being wholly amended in the year 1961, 1967 and 1998.

Main Contents

● The details of amendment after 1998 was such that the transparency of enterprise management shall be elevated, the corporate restructuring such as a merger or division, etc. shall be smoothly executed, and the procedure for return or payment shall be simplified.

● It is intended that the support shall be rendered to the smooth incorporation and operation of a holding company, by taking such measures as all of dividends shall not be included in operating income in case where a holding company receives the dividends from its subsidiary wherein it has made the 100% investment, as a part of dividends shall not be included in operating income pursuant to its investment ratio, even for the dividends received by the holding company from any other subsidiaries and for those received by any domestic corporations, other than the holding company, from other domestic corporations, and thus as ensuring that no double taxation shall be imposed to the dividend incomes.

● Requirements for various expenditures that are allowed as a deduction for expenditures shall be clarified pursuant to the international standards, and in case where a corporation has purchased any goods or services, such expense vouchers shall be those verifiable by the other party, such as credit card sales slips, and tax invoices, etc. but with respect to the expenditures which fail to meet the requirements of such vouchers, the amount equivalent to 2/100 of such amounts shall be imposed as an additional tax.

● The entertainment expenses in excess of a specified amount shall be recognized as expenditures only if they are paid by using credit cards or tax invoices, etc. and the limit on secret service expenses that can be recognizable as expenditures even without any evidence of expenditure shall be reduced from 20 percent to 10 percent of the maximum entertainment expenses recognizable as expenditures, and from the year 2000, the system of secret service expenses is altogether abolished.

● Corporate reorganization, for example by a merger or division, is allowed to proceed with less difficulties by allowing a merged corporation to succeed to the carry-over deficits of the extinguished corporation for a tax deduction and allowing a corporation that is divided to postpone payment of the corporate tax.

● Where a special purpose company, securities investment company, corporate restructuring investment company, or corporate restructuring real estate investment company pays a dividend of 90 percent or more of divisible profits, such amount is allowed to be deducted from the earnings in each fiscal year, and the tax withholding rates when paying the interest incomes or the dividends of profits from the securities investment trust to a domestic corporation, are reduced from 22 percent to 15 percent.

● In order to induce honesty in reporting, the rate of additional tax for failure to report or for filing under-reporting, which has been assessed uniformly 10 through 20 percent, is now differentially applied at 10 through 30 percent depending on the relative importance of dishonesty, and in case where securities are transferred at the price falling short of a normal price between the foreign corporations, which are mutually connected in special relations and have no domestic places of business, it is intended that any tax evasion shall be prevented by imposing taxes under an adjustment of such price to the normal level.

● In case where any foreign corporation transfers the stocks or subscription certificates of a domestic corporation, only the acquisition price has been previously allowed to be deducted from the transferred price in calculating gains on transfer, however, it is now ensured that an equity between the foreign corporations and domestic corporations is secured by providing that both the acquisition price and transfer expenses are to be deducted, etc.

● In case where any foreign corporation renders the services falling short of 6 months in Korea, if it carries on such services continually and repeatedly for not less than 2 years, its service places are deemed to be the domestic business places, so that any unfair tax evasion in the international transactions is prevented.

● In view of such points as having no effectiveness as a tax system in the case of special surtax to be imposed in addition to the general corporate tax on the capital gains from the transfer of real estates by the corporation, it shall be abolished, however, with respect to any capital gains from the transfer of the land and building located in the area in which the price of real estates is rapidly elevated, such system is newly set forth as adding to the corporate tax the tax amount computed by applying a 10-percent tax rate, in preparation for any recurrence of real estate speculations hereafter.

● While a 15-percent tax rate has been previously applied to the relevant excessive reserves in case where any unlisted large corporation has retained in the firm in excess of an adequate level without making any dividend from its earned surplus, it is abolished since there exists an aspect of hampering the expansion of equity capital through internal retaining of the enterprise's profits.

Wholly Amended by Dec. 28, 1998 Act No. 5581

Amended by Dec. 28, 1999 Act No. 6047

Feb. 3, 2000 Act No. 6259

Dec. 29, 2000 Act No. 6293

Dec. 31, 2001 Act No. 6558

TOP↑

CHAPTER I GENERAL PROVISIONS

■■■■ Article 1 (Definitions)

The definitions of terms used in this Act shall be as follows:

1. The term "domestic corporation" shall mean a corporation whose headquarters or main office is located in the Republic of Korea;

2. The term "non-profit domestic corporation" shall mean a domestic corporation which falls under any of the following:

(a) Corporation established under Article 32 of the Civil Act;

(b) Corporation established under the Private School Act or other special Acts whose purpose is similar to that as prescribed in Article 32 of the Civil Act (excluding any corporation other than a partnership corporation as prescribed by the Presidential Decree, which is capable of paying dividends to stockholders, employees or investors); and

(c) Unincorporated organization which is treated as a corporation under Article 13 (4) of the Framework Act on National Taxes (hereinafter, an "organization treated as a corporation");

3. The term "foreign corporation" shall mean a corporation whose headquarters or main office is located in any foreign country;

4. The term "non-profit foreign corporation" shall mean the Government or any other local government of a foreign country, or a foreign corporation (including an organization treated as a corporation) whose business purpose is not to pursue profits; and

5. The term "fiscal year" shall mean one accounting period for which the income of a corporation is calculated.

■■■■ Article 2 (Tax Liability)

(1) Corporations as prescribed in any of the following subparagraphs shall be liable to pay corporate tax on their income under this Act:

1. Domestic corporations; and

2. Foreign corporations that generate income in the Republic of Korea.

(2) Where domestic corporations and foreign corporations have any income from the transfer of land, etc. under Articles 55-2 and 95-2, they shall be liable to pay corporate tax thereon under this Act.

(3) Corporate tax shall not be imposed on the State and local governments (including local government associations; hereinafter the same shall apply) from among domestic corporations.

(4) Domestic corporations, foreign corporations, and residents and non-residents under the Income Tax Act shall be liable to pay corporate tax withheld under this Act.

■■■■ Article 3 (Scope of Taxable Income)

(1) Corporate tax shall be imposed on such income as prescribed in any of the following subparagraphs, provided that with respect to non-profit domestic corporations and foreign corporations, corporate tax shall be imposed only on such income as prescribed in subparagraph 1:

1. Income for each fiscal year; and

2. Liquidation income.

(2) Income of non-profit domestic corporations for each fiscal year shall be income obtained through business or revenue falling under any of the following subparagraphs (hereinafter, "profit-making business"):

1. Business which generates earnings and which is prescribed by the Presidential Decree, such as manufacturing, construction, wholesale or retail sale, consumer product repair, real estate, rent, and business service;

2. Interest, discounts and profits under any subparagraph of Article 16 (1) of the Income Tax Act;

3. Dividends or funds distributed under any subparagraph of Article 17 (1) of the Income Tax Act;

4. Revenue accruing from the transfer of stocks, pre-emptive subscription rights or investment equities;

5. Revenue accruing from the disposal of fixed assets (excluding fixed assets which are directly used for any business with the proper purpose and which are prescribed by the Presidential Decree); and

6. Revenue accruing from continuing acts other than that under subparagraphs 1 through 5, as prescribed by the Presidential Decree.

(3) Income of foreign corporations for each fiscal year shall be income generated in the Republic of Korea under Article 93 (hereinafter, "income generated in Korea"), provided that in case of non-profit foreign corporations, this shall be limited to income generated in Korea through profit-making businesses.

■■■■ Article 4 (Substantial Taxation)

(1) Where the corporation to which all or part of the revenue from assets or business is legally attributable and the corporation to which it is substantially attributable are different, this Act shall apply to the corporation to which the revenue is substantially attributable.

(2) The provisions concerning the calculation of the amount of taxable income subject to corporate tax shall apply to the substantial income and earnings, notwithstanding their designation or form.

■■■■ Article 5 (Trust Income)

(1) With regard to income accruing to a trust estate, the beneficiary of the trust (where no beneficiary is specified or no beneficiary exists, the trustee of the trust or his successor) shall be deemed the owner of the trust estate in the application of this Act.

(2) With regard to revenues and expenditures accruing to trust estates of corporations regulated by the Trust Business Act and the Securities Investment Trust Business Act, the revenue and expenditures shall be deemed not to accrue to the corporation.

■■■■ Article 6 (Fiscal Year)

(1) The fiscal year shall be the one accounting period prescribed by Acts and subordinate statutes or the corporation's articles of incorporation, provided that this period shall not exceed one year.

(2) Domestic corporations with no provisions concerning the fiscal year in relevant Acts and subordinate statutes or their articles of incorporation shall separately determine their fiscal year and report it together with the report on incorporation under Article 109 (1) or the registration of business under Article 111 to the chief of the regional tax office having jurisdiction over the place of tax payment (the head of the tax office under Article 12; hereinafter, the same shall apply).

(3) Foreign corporations with a place of business in the Republic of Korea under Article 94 (hereinafter "domestic place of business") that have no provisions concerning the fiscal year in relevant Acts and subordinate statutes or their articles of incorporation shall separately determine their fiscal year and report it together with the report on the establishment of a domestic place of business under Article 109 (2) or the registration of business under Article 111 to the chief of the regional tax office having jurisdiction over the place of tax payment.

(4) Foreign corporations with no domestic place of business that earn income under subparagraph 3, 7 or 8 of Article 93 shall separately determine their fiscal year and report it to the chief of the regional tax office having jurisdiction over the place of tax payment within one month of the date on which such income was first generated.

(5) Where a corporation that must report under paragraphs (2) through (4) fails to report, the corporation's fiscal year shall be from January 1st to December 31st each year.

(6) Matters relevant to the determination of the beginning date of a corporation's first fiscal year in the application of the provisions of paragraphs (1) through (5) shall be prescribed by the Presidential Decree.

■■■■ Article 7 (Change of Fiscal Year)

(1) A corporation that intends to change its fiscal year shall make report to the chief of the regional tax office having jurisdiction over the place of tax payment within three months of the date of the last day of the immediately preceding fiscal year as prescribed by the Presidential Decree.

(2) Where a corporation does not make report within any such period as prescribed in paragraph (1), its fiscal year shall be deemed to be not changed, provided that where a corporation's fiscal year which is prescribed by Acts and subordinate statutes is changed by amendment thereto, the fiscal year shall be deemed to be changed according to such amendment even if a report as prescribed in paragraph (1) is not made.

(3) Where the fiscal year is changed under paragraph (1) and the proviso of paragraph (2), the period from the beginning date of the previous fiscal year to the day before that of the changed fiscal year shall be deemed to be one fiscal year, provided that where such period is less than one month, it shall be included in the changed fiscal year.

■■■■ Article 8 (Legal Fiction of Fiscal Year)

(1) Where a domestic corporation is dissolved during a fiscal year (excluding any case in which it is dissolved due to merger, division, or merger after division), the period from the beginning date of the fiscal year to the date of registration of such dissolution (referring to the date of registration of bankruptcy in case of dissolution due to bankruptcy, and the date of dissolution in case of an organization treated as a corporation; hereinafter the same shall apply), and the period from the day after the date of such registration to the last day of said fiscal year shall each be deemed to be one fiscal year; and where the value of residual assets of a domestic corporation in the course of liquidation is settled during the fiscal year, the period from the beginning date of said fiscal year to the date of such settlement shall be deemed to be one fiscal year.

(2) Where a domestic corporation is dissolved during a fiscal year due to a merger or division (including division and merger; hereinafter, the same shall apply), the period

from the first day of the fiscal year until the date of registration of the merger or division shall be deemed to be one fiscal year of the dissolved corporation.

(3) Where a domestic corporation in the process of liquidation under Article 229, 285, 519, or 610 of the Commercial Act continues to conduct business, the period from the first day of the fiscal year until the date of registration of continuation (where registration of continuation is not made, the date of actual continuation of business; hereinafter, the same shall apply) and the period from the day after the date of registration of continuation until the last day of the fiscal year shall each be deemed to be one fiscal year.

(4) Where a foreign corporation with a domestic place of business loses that domestic place of business during the fiscal year, the period from the first day of the fiscal year until the date on which it loses that place of business shall be deemed to be one fiscal year of the corporation, provided that this shall not apply where it has another place of business in Korea.

(5) Where a foreign corporation with no domestic place of business reports to the chief of the regional tax office having jurisdiction over the place of tax payment that it is no longer generating income under subparagraph 3, 7, or 8 of Article 93, the period from the first day of the fiscal year until such report is made shall be deemed to be one fiscal year.

■■■■ Article 9 (Place of Tax Payment)

(1) The place of payment of corporate tax of domestic corporations shall be the location of the registered headquarters or main offices of each corporation, provided that for organizations to be treated as corporations, it shall be the place prescribed by the Presidential Decree.

(2) The place of payment of corporate tax of foreign corporations shall be the location of that corporation's domestic place of business, provided that for a foreign corporation with no domestic place of business earning income under subparagraph 3, 7, or 8 of Article 93, it shall be the location of each corporation's assets.

(3) Where a foreign corporation under paragraph (2) has two or more domestic places of business, the location of the place of business as prescribed by the Presidential Decree shall be the place of tax payment, and where the corporation has assets in two or more locations, the place prescribed by the Presidential Decree shall be the place of tax payment.

(4) The place of payment of corporate tax withheld under Articles 73, 98 and 98-3 shall be the location of the person liable for collecting such withholding tax as prescribed by the Presidential Decree, provided that where the person liable for collecting withholding tax under Articles 98 and 98-3 does not have the location in the Republic of Korea, the place of payment shall be the place as prescribed by the Presidential Decree.

■■■■ Article 10 (Designation of Place of Tax Payment)

(1) Where the director of a regional tax office (the director of the regional tax office under Article 12; hereinafter, the same shall apply) or the Commissioner of the National Tax Administration deems that a corporation's place of tax payment under Article 9 is inappropriate, he may, notwithstanding the provisions of Article 9, designate a place of tax payment under conditions as determined by the Presidential Decree.

(2) Where the director of the regional tax office or the Commissioner of the National Tax Administration designates a place of tax payment under paragraph (1), he shall notify the concerned corporation as prescribed by the Presidential Decree.

■■■■ Article 11 (Change of Place of Tax Payment)

(1) Where a corporation's place of tax payment changes, it shall report the change to the chief of the regional tax office having jurisdiction over the new place of tax payment within 15 days of date of the change as prescribed by the Presidential Decree. In this case, where the corporation whose place of tax payment has changed reports the change under Article 5 of the Value-Added Tax Act, it shall be deemed to have also reported the change of the place of tax payment.

(2) Where no report is made under paragraph (1), the previous place of tax payment shall be the corporation's place of tax payment.

(3) Where foreign corporation comes to have no domestic place of tax payment falling under Article 9 (2), it shall report to the chief of the regional tax office having jurisdiction over the former place of tax payment.

■■■■ Article 12 (Jurisdiction of Taxation)

Corporate tax shall be levied by the head of the tax office or director of the regional tax office with jurisdiction over the place of tax payment under Articles 9 through 11.

TOP↑

CHAPTER II CORPORATE TAX ON INCOME OF DOMESTIC CORPORATIONS FOR EACH FISCAL YEAR

SECTION 1 Tax Base and its Calculation

Subsection 1 Common Provisions

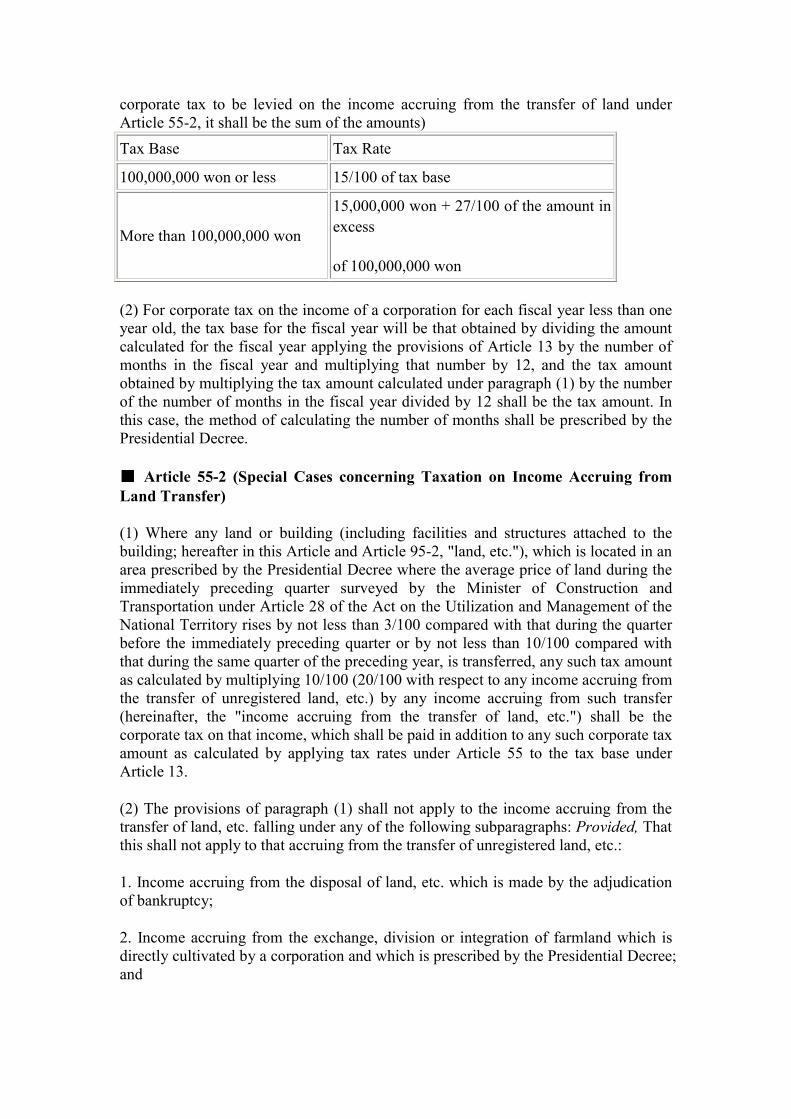

■■■■ Article 13 (Tax Base)

The tax base for corporate tax on the income of domestic corporations for each fiscal year shall be, with regards to the income for each fiscal year, the remaining sum after the amount under any of the following subparagraphs is deducted sequentially from the income amount:

1. Net operating losses incurred during each fiscal year within the five years prior to the first day of the current fiscal year that were not previously deducted in the calculation of the basis for assessment of taxes;

2. Non-taxable income under this Act and other Acts; and

3. Amount of income deduction under this Act and other Acts.

■■■■ Article 14 (Income during Each Fiscal Year)

(1) The income of a domestic corporation during each fiscal year shall be any such amount as given by deducting the deductible expenses during the fiscal year from the gross income during said fiscal year.

(2) Net operating losses of a domestic corporation during each fiscal year shall, if the deductible expenses during the fiscal year exceeds the gross income during said fiscal year, be such excesses.

Subsection 2 Calculation of Gross Income

■■■■ Article 15 (Scope of Gross Income)

(1) Gross income shall mean all the revenue accruing from transactions that create any increase in the net assets of the corporation concerned, excluding paid-up capital or equities, and others as prescribed in this Act.

(2) The amount as prescribed in any of the following subparagraphs shall be deemed to be gross income:

1. Amount of the difference between the market price and the purchase price, where securities are purchased from an individual with any special relationship as prescribed in Article 52 (1) at a price below said market price under Article 52 (2); and

2. Amount of foreign corporation tax under Article 57 (4) (limited to any case in which it is deducted).

(3) Necessary matters concerning the scope and classification of revenue under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 16 (Legal Fiction as Dividends or Distributions)

(1) The amount falling under any of the following subparagraphs shall be deemed to be dividends or surplus funds distributed by a corporation, and this Act shall apply accordingly:

1. Excess of the total value of funds and other assets acquired by a stockholder, employee or investor (hereinafter "stockholder") through the retirement of stocks, the reduction of capital or investment, or employee's resignation or withdrawal over the

amount necessary for the stockholder to acquire said stocks or investment equities (hereinafter "stocks");

2. Par value of stocks acquired through the transfer of all or part of a corporation's surplus funds into capital or investment, provided that this shall not apply where funds falling under any of the following items are transferred into capital:

(a) Capital reserve funds under Article 459 (1) 1 through 3 and 3-2 of the Commercial Act (excluding profits from the evaluation of a merger or division as prescribed by the Presidential Decree, and limited to the transfer to capital after the passage of two years from the date of retirement of any corporation's own stocks or investment equities where there are profits from such retirement and the market price under Article 52 (2) of this Act does not exceed the acquisition value at the time of the retirement); and

(b) Revaluation reserve funds under the Assets Revaluation Act (excluding the amount of any difference in the revaluation of land under Article 13 (1) 1 of the same Act);

3. Par value of stocks equivalent to the ratio of increased equities, where the ratio of equities of stockholders except for a corporation is so increased by its transfer to capital under any item of subparagraph 2 while holding its own stocks or investment equities;

4. Amount of funds and the value of other assets acquired by stockholders of a dissolved corporation (including members of an organization to be treated as a corporation) through the distribution of the residual assets of the corporation in excess of the amount necessarily spent for the acquisition of the concerned stocks;

5. Sum of the value of stocks, funds, and other assets which stockholders of a corporation that is extinguished through a merger (hereinafter "extinguished corporation") receive from a corporation that is established or maintained through the merger (hereinafter "merged corporation") due to the merger (hereinafter "cost of merger") in excess of the amount necessary for the acquisition of the stocks of the extinguished corporation; and

6. Where a corporation is divided, the sum of the value of stocks, funds, and other assets that stockholders of the divided corporation (hereinafter "divided corporation") or counterpart corporation to a corporation extinguished through division and merger receive from the corporation established through the division (hereinafter "corporation established by division") or the counterpart corporation to the division and merger due to the division (hereinafter "cost of division"), in excess of the amount necessary the acquisition of the stocks of the divided corporation or counterpart corporation to the corporation extinguished through division and merger (where the divided corporation continues to exist, limited to stocks reduced by retirement).

(2) In the application of the provisions of paragraph (1), matters relevant to the period of the distribution of profit dividends or surplus funds and the evaluation of the value of stocks shall be prescribed by the Presidential Decree.

■■■■ Article 17 (Exclusion of Proceeds from Capital Transactions from Gross Income)

In calculating the amount of income of a domestic corporation for each fiscal year, proceeds falling under any of the following subparagraphs shall not be included in gross income:

1. Surplus amount of par value of stocks issued;

2. Gains from retirement of stocks;

3. Profits from a merger, provided that profits from the evaluation of merger (hereinafter, "merger evaluation profits") as prescribed by the Presidential Decree shall be excluded; and

4. Profits from a division, provided that profits from the evaluation of division (hereinafter, "division evaluation profits") as prescribed by the Presidential Decree shall be excluded.

■■■■ Article 18 (Exclusion of Evaluation Profits from Gross Income)

In calculating the amount of income of a domestic corporation for each fiscal year, proceeds falling under any of the following subparagraphs shall not be included in gross income:

1. Profits from the evaluation of assets, provided that profits accruing from the evaluation under any subparagraph of Article 42 (1) shall be excluded;

2. Gross income carried forward;

3. The amount appropriated for taxes other than corporate tax but not included in the calculation of deductible expenses under subparagraph 1 of Article 21 or the income- proportional resident tax refunded or to be refunded;

4. Interest on refunded national or local taxes paid in error;

5. Output tax amount of value-added tax;

6. The value of 90/100 of the dividend income an institutional investor, as prescribed by the Presidential Decree, receives from stock-listed corporations (hereinafter, "stock-listed corporations") and association-registered corporations (hereinafter, "association-registered corporations") under the Securities and Exchange Act, other than those prescribed by the Presidential Decree;

7. Deleted; and

8. The amount appropriated for the prevention of net operating losses carried forward, as prescribed by the Presidential Decree, from among the value of assets received without compensation, and the amount of the reduction of debt due to the exemption from or extinction of financial obligations.

■■■■ Article 18-2 (Exclusion of Dividend Amount Received by Holding Company from Gross Income)

(1) Where the sum calculated under subparagraphs 1 and 2 exceeds that calculated under subparagraphs 3 and 4, out of profit dividends or surplus distributions which a holding company as prescribed by the Presidential Decree (including a financial holding company established under the Financial Holding Company Act; hereafter in this Article, a "holding company"), from among domestic corporations that are designated as holding companies under the Monopoly Regulation and Fair Trade Act, receives from its subsidiary (referring to any domestic corporation that is invested in by the said holding company and that meets such requirements as prescribed by the Presidential Decree in consideration of the holding company's investment ratio in the subsidiary; hereafter the same shall apply in this Article) and fictitious dividends or distributions under Article 16 (hereafter in this Article and Article 18-3, "received dividend amount"), such an excess shall not be included in gross income in calculating the amount of income for each fiscal year:

1. Any such amount as given by multiplying the received dividend amount from a subsidiary by 90/100, where an investment is made in excess of 80/100 of the total number of stocks issued by the said subsidiary or the total investment amount (40/100, in case of a stock-listed corporation or association-registered corporation), provided that it shall mean the total received dividend amount from a subsidiary, where a holding company invests in all of the total number of stocks issued by the said subsidiary or the total investment amount;

2. Any such amount as given by multiplying the received dividend amount from a subsidiary by 60/100, where the ratio of investment in the said subsidiary is below that as prescribed in subparagraph 1;

3. Any such amount as calculated under the Presidential Decree in consideration of the ratio of exclusion from gross income under subparagraphs 1 and 2, out of the interest on borrowings related to investments in a subsidiary, where there is that interest which is paid by a holding company in each fiscal year; and

4. Any such amount as given by multiplying the received dividend amount from a subsidiary by the ratio prescribed by the Presidential Decree, taking into account the subsidiary's investments in any other corporation, where the said subsidiary makes such investments in any other affiliate under the Monopoly Regulation and Fair Trade Act (hereafter in this subparagraph, "affiliate") or does so in any domestic corporation other than the affiliate in excess of 1/100 of the total number of stocks issued or total investment amount (excluding any case in which a subsidiary as prescribed in Article 2 (1) 2 of the Financial Holding Company Act makes an investment in a sub-subsidiary as prescribed in subparagraph 3 of said paragraph and a subsidiary as prescribed in said subparagraph is an institutional investor as prescribed in subparagraph 6 of Article 18 of this Act).

(2) The provisions of paragraph (1) shall not apply to the received dividend amount accruing from stocks of a subsidiary which a holding company acquires and holds within three months prior to the dividend standard date of the subsidiary.

(3) In applying the provisions of paragraphs (1) and (2), necessary matters concerning the method of calculating the ratio of investment of a holding company in a subsidiary, the calculation of amount excluded from gross income, and the submission of a detailed statement of received dividend amount, etc. shall be prescribed by the Presidential Decree.

■■■■ Article 18-3 (Exclusion of Received Dividend Amount from Gross Income)

(1) Where the sum calculated under subparagraphs 1 and 2 exceeds that calculated under subparagraph 3, out of the dividend amount which any domestic corporation receives from other domestic corporations in which it makes an investment, such an excess shall not be included in gross income in calculating the amount of income for each fiscal year:

1. Any such amount as given by multiplying by 50/100 the dividend amount which any domestic corporation receives from other domestic corporations in which it makes an investment in excess of 50/100 (30/100, in case of a stock-listed or association-registered corporation) of the total issued stocks or the total investment amount;

2. Any such amount as given by multiplying by 30/100 the dividend amount which any domestic corporation receives from other domestic corporations in which it makes an investment below the ratio as prescribed in subparagraph 1; and

3. Any such amount as calculated under the Presidential Decree in consideration of the ratio of exclusion from gross income under subparagraphs 1 and 2, out of the interest on borrowings related to investments in any other domestic corporation, where there is that interest which is paid by a domestic corporation in each fiscal year; and

(2) The provisions of paragraph (1) shall not apply to the received dividend amount as prescribed in any of the following subparagraphs:

1. Deleted;

2. Received dividend amount accruing from the holding of stocks acquired within three months prior to the dividend standard date;

3. Received dividend amount subject to the application of subparagraph 6 of Article 18 and Article 18-2; and

4. Received dividend amount from a corporation falling under any subparagraph of Article 51-2 (1).

(3) In applying the provisions of paragraphs (1) and (2), necessary matters concerning the method for calculating the ratio of investment, the calculation of amount excluded from gross income and the submission of a detailed statement of received dividend amount, etc. shall be prescribed by the Presidential Decree.

Subsection 3 Calculation of Deductible Expenses

■■■■ Article 19 (Scope of Deductible Expenses)

(1) Deductible expenses shall mean expenses incurred from transactions that cause any decrease in the net assets of a corporation, excluding the return of capital or equities, the disposal of surplus funds, and other transactions as prescribed in this Act.

(2) Except as otherwise prescribed by this Act and any other Acts, expenses under paragraph (1) shall be those losses or expenses which are incurred in connection with the business of a corporation and which are generally accepted as normal or directly related to profit-making activities.

(3) Necessary matters concerning the scope and classification of expenses under paragraphs (1) and (2) shall be prescribed by the Presidential Decree.

■■■■ Article 20 (Exclusion of Expenses due to Capital Transactions from Deductible Expenses)

In calculating the amount of income of a domestic corporation for each fiscal year, expenses falling under any of the following subparagraphs shall not be included in deductible expenses:

1. Amount appropriated as expenses in the disposal of surplus funds, provided that this shall not apply to piece rates as prescribed by the Presidential Decree;

2. Dividends on interest during construction; and

3. Margins from the discount issue of stocks.

■■■■ Article 21 (Exclusion of Various Taxes or Public Imposts from Deductible Expenses)

In calculating the amount of income of a domestic corporation for each fiscal year, taxes or public imposts falling under any of the following subparagraphs shall not be included in deductible expenses:

1. Corporate tax (including the amount of foreign corporate tax under Article 57) or income-proportional resident tax paid or to be paid in each fiscal year, the tax amount (including additional tax) paid or to be paid due to non-performance of duties as prescribed by respective tax Acts, and the purchase tax amount of value-added tax (excluding any such case as exempted from value-added tax or as otherwise prescribed by the Presidential Decree);

2. Any unpaid value of special consumption tax, liquor tax, or transport tax on unsold manufactured goods, provided that this shall not apply where the price of manufactured goods includes a reasonable tax amount;

3. Deleted;

4. Fines and penalties (including appropriate amounts for fines or penalties under noticed dispositions), fines for negligence (including penalties), additional charges for default, and fees for delinquency in payment;

5. Public imposts which are not subject to the compulsory payment under relevant Acts and subordinate statutes; and

6. Public imposts which are imposed as sanctions against the non-performance of such duties as prescribed in relevant Acts and subordinate statutes or the violation of prohibition and restriction thereunder.

■■■■ Article 22 (Exclusion of Losses from Evaluation of Assets from Deductible Expenses)

In calculating the amount of income of a domestic corporation for each fiscal year, the losses from the evaluation of assets in its possession shall not be included in deductible expenses, provided that this shall not apply to losses incurred by the evaluation of assets under Article 42 (2) and (3).

■■■■ Article 23 (Exclusion of Depreciation Costs from Deductible Expenses)

(1) In calculating the amount of income of a domestic corporation for each fiscal year, depreciation costs of fixed assets shall, only where it appropriates them for deductible expenses in the relevant fiscal year (referring to where they are appropriated for expenses in the confirmation of the settlement of accounts; hereinafter, the same shall apply), be included in deductible expenses to the extent of any such amount as calculated under the Presidential Decree (hereafter in this Article, "scope of depreciation amount"), but the portion of the appropriated amount which exceeds the scope of depreciation amount shall not be included therein.

(2) Fixed assets under paragraph (1) shall mean those assets which are prescribed by the Presidential Decree, such as buildings, machines, equipments and patent rights, other than land.

(3) Domestic corporations that appropriate depreciation costs for deductible expenses under paragraph (1) shall submit a detailed statement on depreciation costs as prescribed by the Presidential Decree to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) In applying the provisions of paragraph (1), necessary matters concerning the method of appropriation of depreciation costs for deductible expenses and the settlement of the amount exceeding the scope of the depreciation amount shall be prescribed by the Presidential Decree.

■■■■ Article 24 (Exclusion of Donations from Deductible Expenses)

(1) Of donations made during each fiscal year by a domestic corporation to support social welfare, culture, arts, education, religion, charity, or learning, as prescribed by the Presidential Decree (hereinafter, "designated donations"), any amount in excess of 5/100 of the figure obtained by subtracting the amount under subparagraph 2 from the

amount under subparagraph 1 (hereafter in this Article, "limit amount of inclusion in deductible expenses"), and donations other than designated donations shall not be included in deductible expenses in calculating the amount of income for the relevant fiscal year:

1. The income amount for the relevant fiscal year (the value prior to the inclusion of donations under paragraph (2) and designated donations in the calculation of deductible expenses; hereinafter, in this Article the same shall apply); and

2. Donations included in the calculation of deductible expenses under paragraph (2) and the total amount of net operating losses under subparagraph 1 of Article 13.

(2) The provisions of paragraph (1) and Article 29 shall not apply to donations under any of the following subparagraphs, provided that where the total amount of the donations under any of the following subparagraphs is in excess of the amount obtained by subtracting the net operating losses under subparagraph 1 of Article 13 from the income amount of the concerned fiscal year, the amount in excess shall not be included when calculating deductible expenses in the calculation of income amount for the concerned fiscal year:

1. Money and other valuables contributed to the national or a local government municipality without compensation, provided that for contributed items under application of the Act on the Regulation of Donations Collection, this shall be limited to items requisitioned under Article 5 (2) of the same Act;

2. The value of contributions for national defense, and money and other valuables contributed for the consolation and comfort of soldiers of the national armed forces; and

3. The value of money and other valuables contributed for victims of natural disasters.

(3) The value of designated donations in excess of the limit for inclusion in deductible expenses that is not included in the calculation of deductible expenses under paragraph (1) may be carried forward and included in the calculation of deductible expenses for each fiscal year that completed within three years of the first day of the fiscal year following the concerned fiscal year, as prescribed by the Presidential Decree.

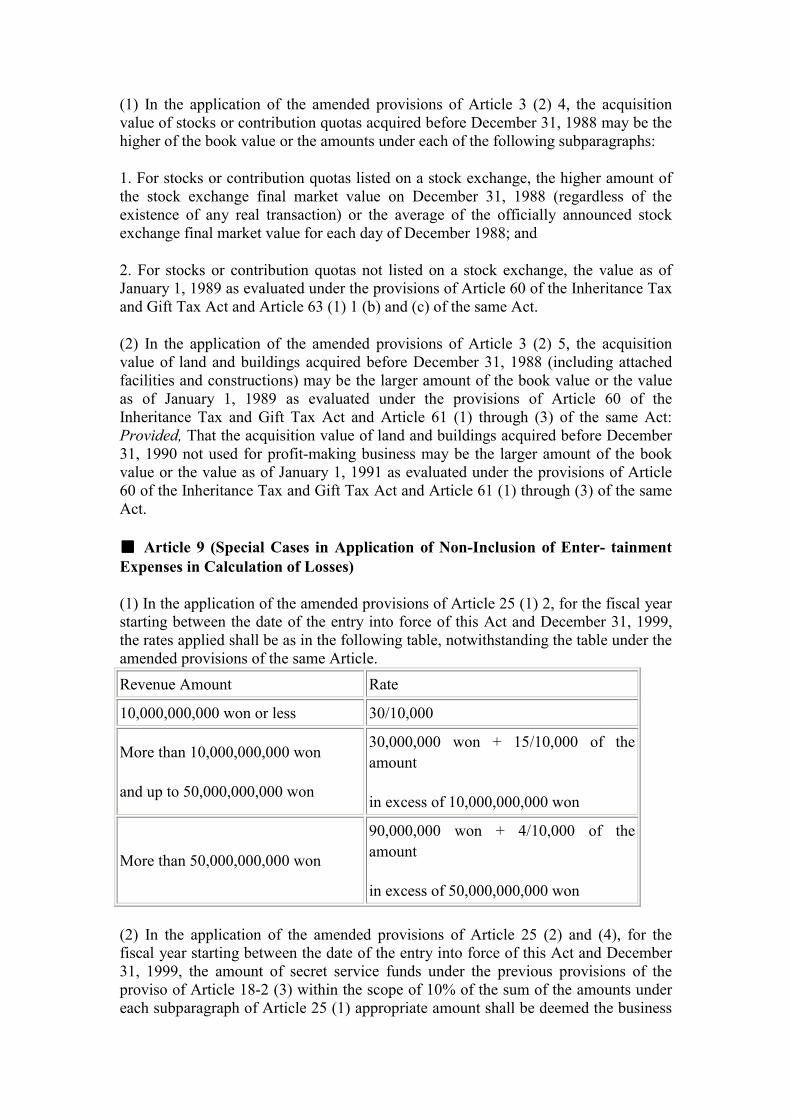

■■■■ Article 25 (Exclusion of Entertainment Expenses from Deductible Expenses)

(1) Of entertainment expenses paid by a domestic corporation in each fiscal year (excluding the amount falling under paragraph (2)), the amount exceeding the sum of that which is prescribed in any of the following subparagraphs shall not be included in deductible expenses in calculating the amount of income for the relevant fiscal year:

1. The amount obtained by multiplying the monthly income for the relevant fiscal year by 12,000,000 won (18,000,000 won for small-and medium-sized enterprises as prescribed by the Presidential Decree) and dividing by 12; and

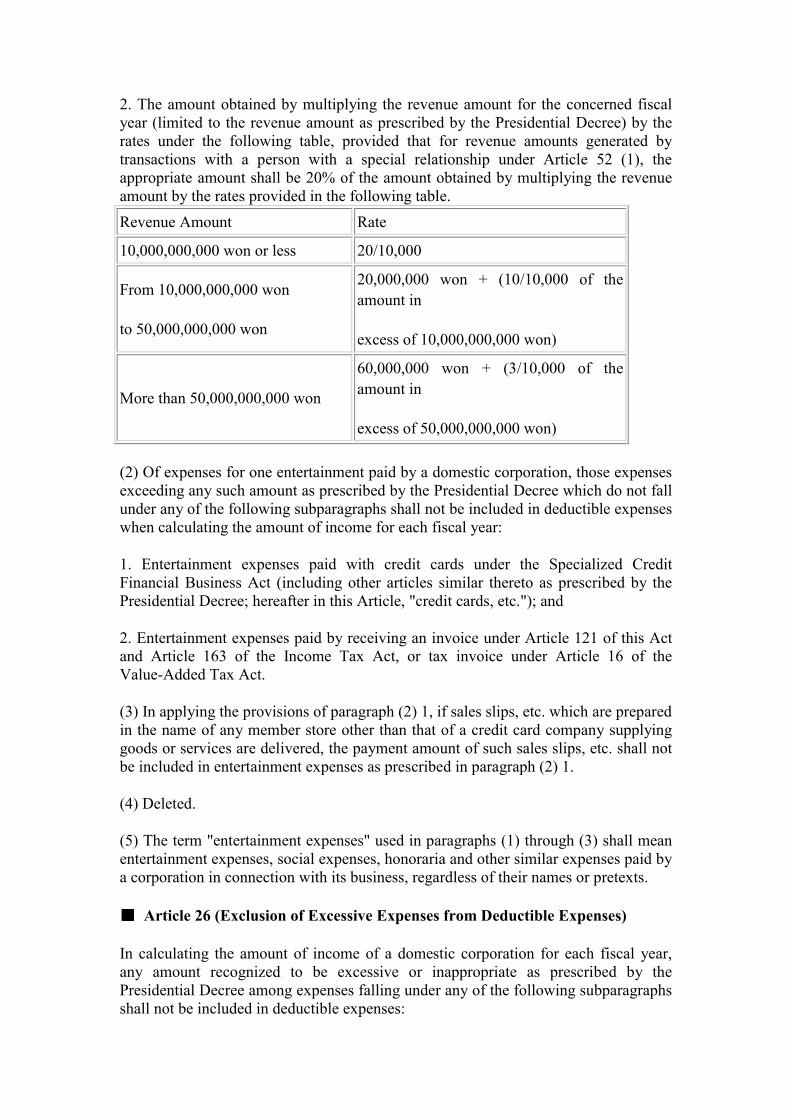

2. The amount obtained by multiplying the revenue amount for the concerned fiscal year (limited to the revenue amount as prescribed by the Presidential Decree) by the rates under the following table, provided that for revenue amounts generated by transactions with a person with a special relationship under Article 52 (1), the appropriate amount shall be 20% of the amount obtained by multiplying the revenue amount by the rates provided in the following table. Revenue Amount Rate

10,000,000,000 won or less 20/10,000

From 10,000,000,000 won

to 50,000,000,000 won

20,000,000 won + (10/10,000 of the amount in

excess of 10,000,000,000 won)

More than 50,000,000,000 won

60,000,000 won + (3/10,000 of the amount in

excess of 50,000,000,000 won)

(2) Of expenses for one entertainment paid by a domestic corporation, those expenses exceeding any such amount as prescribed by the Presidential Decree which do not fall under any of the following subparagraphs shall not be included in deductible expenses when calculating the amount of income for each fiscal year:

1. Entertainment expenses paid with credit cards under the Specialized Credit Financial Business Act (including other articles similar thereto as prescribed by the Presidential Decree; hereafter in this Article, "credit cards, etc."); and

2. Entertainment expenses paid by receiving an invoice under Article 121 of this Act and Article 163 of the Income Tax Act, or tax invoice under Article 16 of the Value-Added Tax Act.

(3) In applying the provisions of paragraph (2) 1, if sales slips, etc. which are prepared in the name of any member store other than that of a credit card company supplying goods or services are delivered, the payment amount of such sales slips, etc. shall not be included in entertainment expenses as prescribed in paragraph (2) 1.

(4) Deleted.

(5) The term "entertainment expenses" used in paragraphs (1) through (3) shall mean entertainment expenses, social expenses, honoraria and other similar expenses paid by a corporation in connection with its business, regardless of their names or pretexts.

■■■■ Article 26 (Exclusion of Excessive Expenses from Deductible Expenses)

In calculating the amount of income of a domestic corporation for each fiscal year, any amount recognized to be excessive or inappropriate as prescribed by the Presidential Decree among expenses falling under any of the following subparagraphs shall not be included in deductible expenses:

1. Personnel/labor expenses;

2. Welfare expenses;

3. Travel, education, and training expenses;

4. Business expenses of a corporation conducting an insurance business (including any mutual aid business under the Agricultural Cooperatives Act and the Fisheries Cooperatives Act; hereinafter, the same shall apply);

5. Expenses generated or paid by a corporation as a result of the joint operation or management of an identical organization or business with a person other than that corporation; and

6. Expenses other than those recognized under subparagraphs 1 through 5 as having little direct connection to the business of a corporation, as prescribed by the Presidential Decree.

■■■■ Article 27 (Exclusion of Non-Business Expenses from Deductible Expenses)

Among expenditures of a domestic corporation for each fiscal year, such expenses as prescribed in any of the following subparagraphs shall not be included in deductible expenses in calculating the amount of income for the relevant fiscal year:

1. Expenses which are incurred by acquiring and managing such assets deemed to have no direct connection to the business of the corporation concerned as prescribed by the Presidential Decree and which are prescribed by the Presidential Decree; and

2. Expenses which are deemed to have no direct connection to the business of the corporation concerned other than those as prescribed in subparagraph 1 and which are prescribed by the Presidential Decree.

■■■■ Article 28 (Exclusion of Interest Expenses from Deductible Expenses)

(1) In calculating the amount of income of a domestic corporation for each fiscal year, interest on loans falling under any of the following subparagraphs shall not be included in deductible expenses:

1. Interest on debentures for which the creditor is unknown;

2. With regards to the interest, discount amount, or profits on bonds and securities under Article 16 (1) 1, 2, 6, and 9 of the Income Tax Act, the interest, discount amount, or profits on bonds and securities as prescribed by the Presidential Decree for which the person who received payment is not known;

3. Interest on loans appropriated for construction capital as prescribed by the Presidential Decree; and

4. With regard to interest on loans paid during each fiscal year by a domestic corporation that acquires or possesses assets falling under one of the following

categories, the amount calculated as prescribed by the Presidential Decree (limited to interest on loans of an appropriate amount for the value of the concerned assets):

(a) Assets falling under subparagraph 1 of Article 27; and

(b) Provisional payments to a person with a special relationship under Article 52 (1) with no connection to the business of the concerned corporation, as prescribed by the Presidential Decree.

(2) In calculating the amount of income of a domestic corporation falling under any of the following subparagraphs which has loans (hereafter in this Article, "loans exceeding the standards") exceeding four times its equity capital as prescribed by the Presidential Decree (hereafter in this Article, "equity capital") for each fiscal year, any such amount as calculated under the Presidential Decree among the interest on loans paid by the said domestic corporation in the relevant fiscal year shall not be included in deductible expenses:

1. Stock-listed or association-registered corporation as of the last day of each fiscal year: Provided, That any such small and medium enterprise as prescribed by the Presidential Decree shall be excluded; and

2. Corporation as prescribed by the Presidential Decree in consideration of the size of its assets or capital, etc.

(3) In applying the provisions of paragraph (2), the multiple of the loan to equity capital for credit specialist financial companies under the Specialized Credit Financial Business Act and corporations, as prescribed by the Presidential Decree, may be determined in accordance with the Presidential Decree.

(4) The provisions of paragraph (2) shall not apply to cases listed in any one of the following subparagraphs:

1. Where the loan interest paid in the relevant fiscal year is 3/100 or less of the revenue amount, as prescribed relevant by the Presidential Decree;

2. Where the loan interest paid in the fiscal year is 40/100 or less of the income amount for that fiscal year (referring to the amount before the concerned loan interest is included in the calculation of deductible expenses); and

3. Where a loan in excess of the standard of the relevant fiscal year has been reduced by 20/100 or more compared to the loan in excess of the standard of the immediately prior fiscal year.

(5) Where the provisions of paragraphs (1) and (2) and the provisions of the Restriction of Special Taxation Act on the exclusion of interest on payment from deductible expenses apply simultaneously, they shall apply in the order prescribed by the Presidential Decree.

(6) Necessary matters concerning the scope and calculation of loans and interest on payment under paragraphs (1) and (2) shall be prescribed by the Presidential Decree.

Subsection 4 Inclusion of Reserve Funds and

Appropriation Funds in Deductible Expenses

■■■■ Article 29 (Inclusion of Reserve Funds for Proper Purpose Business in Deductible Expenses)

(1) Where a non-profit domestic corporation (limited to an organization as prescribed by the Presidential Decree in case of that which is deemed to be a corporation) appropriates reserve funds for proper purpose business for deductible expenses in order to pay for its proper purpose business or designated donations (hereafter in this Article, "proper purpose business") in each fiscal year, those reserve funds shall, to the extent of the sum of the amount falling under any of the following subparagraphs, be included in deductible expenses in calculating the amount of income for the relevant fiscal year:

1. Interest income amount under Article 16 (1) 1 through 11 of the Income Tax Act;

2. Distributed funds of securities investment trust proceeds under Article 17 (1) 5 of the Income Tax Act;

3. Interest amount generated by loans to members or associates of welfare projects of a non-profit domestic corporation established under special Acts; and

4. Amount obtained by multiplying the income from profit-making businesses other than that under subparagraphs 1 through 3 by the percentage as prescribed by the Presidential Decree.

(2) Where a non-profit domestic corporation spends reserve funds for proper purpose business which are appropriated for deductible expenses under paragraph (1) on proper purpose business, it shall set off the amount of those reserve funds according to the sequence of the fiscal years in which the reserve funds are appropriated. In this case, where there is a positive balance in the reserve funds for proper purpose business as of the last day of the immediately prior fiscal year and the amount spent for proper purpose business in the relevant fiscal year, the excess amount shall be deemed as having been spent from the reserve funds for proper purpose business to be set off for the relevant fiscal year, and the provisions of paragraph (1) shall apply accordingly.

(3) Where a non-profit domestic corporation with a positive balance in reserve funds for proper purpose business included in deductible expenses under paragraph (1) comes to fall under any of the following subparagraphs, the balance shall be included in gross income in calculating the amount of income for the fiscal year including the date on which the cause for that change occurs:

1. Where it is dissolved;

2. Where the proper purpose business of the corporation are all discontinued;

3. Where the approval for an organization to be treated as a corporation is revoked or is changed to a resident, under Article 13 (3) of the Framework Act on National Taxes; and

4. Where reserve funds for proper purpose business appropriated for deductible expenses are not used for proper purpose business within 5 years from the last day of the fiscal year in which they are appropriated (limited to the balance not used within 5 years).

(4) Where the balance of reserve funds for proper purpose business is included in gross income under paragraph (3) 4, an appropriate amount of interest calculated under the Presidential Decree shall be paid in addition to corporate tax for the relevant fiscal year.

(5) A non-profit domestic corporation which intends to be subject to the application of paragraph (1) shall submit a detailed statement on the concerned reserve fund, as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(6) Necessary matters concerning the scope of proper purpose business and the calculation of income generated by profit-making businesses under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 30 (Inclusion of Liability Reserve Fund in Deductible Expenses)

(1) Where a domestic corporation operating an insurance business under the Insurance Business Act, other Acts, and subordinate statutes has appropriated the liability reserve fund and contingency reserve fund as deductible expenses for each fiscal year, any amount within the scope prescribed by the Presidential Decree shall be included in deductible expenses in calculating the amount of income for the relevant fiscal year.

(2) Any liability reserve fund included in deductible expenses under paragraph (1) shall be included in gross income in calculating the amount of income for the following fiscal year.

(3) A domestic corporation which intends to be subject to the application of paragraph (1) shall submit a detailed statement on the relevant reserve fund, as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) Necessary matters concerning the disposition of the contingency reserve fund included in deductible expenses under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 31 (Inclusion of Policyholder Dividend Reserve Fund in Deductible Expenses)

(1) Where a domestic corporation operating an insurance business appropriates a policy holder dividends reserve fund in order to pay dividends to insurance policy

holders as deductible expenses for each fiscal year, an amount within the scope as prescribed by the Presidential Decree shall be included in deductible expenses when calculating the amount of income for the relevant fiscal year.

(2) Where a domestic corporation that has included the policy holder dividends reserve fund in deductible expenses under paragraph (1) pays dividends to an insurance policy holder, it shall set them off in order, beginning with the policyholder dividend reserve funds appropriated for that fiscal year.

(3) The policyholder dividend reserve funds included in deductible expenses under paragraph (1) shall be set off under paragraph (2) until the date on which three years have passed from the last day of the relevant fiscal year, and the balance remaining shall be included in gross income when calculating the amount of income for the original fiscal year.

(4) Where the balance of policyholder dividend reserve funds is included in gross income under paragraph (3), the amount equivalent to any such interest as calculated under the Presidential Decree shall be paid in addition to corporate tax for the relevant fiscal year.

(5) Where a domestic corporation with the balance of policy holder dividends reserve funds included in deductible expenses under paragraph (1) comes to fall under any of the following subparagraphs, that balance shall be included in gross income when calculating the amount of income for the fiscal year in which the cause for the corporation's change in position occurs:

1. Where it is dissolved, provided that where it is dissolved due to merger, and the merged corporation operating an insurance business succeeds to the balance, this shall not apply; and

2. Where permission for an insurance business is revoked.

(6) In applying the provisions of paragraphs (2) through (5), the amount succeeded to by a merged corporation under the proviso of paragraph (5) 1 shall be deemed to be included in deductible expenses by the merged corporation in the fiscal year when the extinguished corporation includes that amount in deductible expenses.

(7) A domestic corporation which intends to be subject to the application of paragraph (1), it shall submit a detailed statement on the relevant reserve fund, as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

■■■■ Article 32 Deleted.

■■■■ Article 33 (Inclusion of Retirement Benefits Payment Fund in Deductible Expenses)

(1) Where a domestic corporation appropriates a retirement benefits payment fund as deductible expenses for each fiscal year in order to pay retirement benefits to officers or employees, an amount within the scope calculated as prescribed by the Presidential

Decree shall be included in deductible expenses when calculating the amount of income for the relevant fiscal year.

(2) Where a domestic corporation that includes the retirement benefits payment fund in deductible expenses under paragraph (1) pays retirement benefits to an officer or employee, it shall pay those benefits first from the concerned retirement benefits payment fund.

(3) Where a domestic corporation that includes the retirement benefits payment fund in deductible expenses under paragraph (1) is merged or divided, the amount of the retirement benefits payment fund as of the date of the registration of such merger or division that is transferred to the merged corporation, the corporation established by division, or a counterpart corporation to the division and merger (hereinafter, a "merged corporation") shall be deemed to be the retirement benefits payment fund of the merged corporation on the date of the registration of the merger or division.

(4) Where a project manager comprehensively transfers the project to a domestic corporation, the provisions of paragraph (3) shall apply mutatis mutandis.

(5) A domestic corporation that wishes to be subject to the provisions of paragraph (1) must submit a detailed statement on the retirement benefits payment fund, as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(6) Matters relevant to the disposition of the retirement benefits payment fund under paragraphs (1) through (4) shall be prescribed by the Presidential Decree.

■■■■ Article 34 (Inclusion of Bad Debts Fund in Deductible Expenses)

(1) Where a domestic corporation appropriates a bad debts fund in order to cover bad debts from credit accounts, loans, and other related debentures as deductible expenses for each fiscal year, an amount up to the amount prescribed by the Presidential Decree shall be included in deductible expenses when calculating in the amount of income for the relevant fiscal year.

(2) The value of bonds that a domestic corporation possesses for which the obligor is bankrupt or the debenture cannot be collected due to causes prescribed by the Presidential Decree (hereafter in this Article, "bad debts") shall be included in deductible expenses when calculating the amount of income for the relevant fiscal year.

(3) The provisions of paragraphs (1) and (2) shall not apply to debentures falling under any of the following subparagraphs:

1. Claims for compensation arising from guarantees of obligations (not including guarantees of obligations as prescribed by the Presidential Decree); and

2. Payments listed under Article 28 (1) 4 (b).

(4) Where any domestic corporation that appropriates a bad debts fund for deductible expenses under paragraph (1) has bad debts under paragraph (2), such bad debts shall be first offset by the bad debts fund and then the remaining amount of the bad debts fund after such offset shall be included in gross income in calculating the amount of income for the next fiscal year.

(5) Bad debts included in deductible expenses under paragraph (2) that are later collected shall be included in gross income in calculating the amount of income for the fiscal year including the date of the collection.

(6) Where a domestic corporation that includes a bad debts fund in deductible expenses under paragraph (1) is merged or divided, the value of the bad debts fund of said corporation as of the date of the registration of such merger or division that is transferred to the merged corporation, etc. shall be deemed to be the bad debts fund of the merged corporation, etc. on that date.

(7) A domestic corporation that wishes to subject itself to the provisions of paragraphs (1) and (2) shall submit a detailed statement regarding bad debts funds and bad debts as prescribed by the Presidential Decree to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(8) Necessary matters concerning credit accounts, loans, and other related debentures, the scope of bad debts, and the disposition of bad debts funds and bad debts under paragraphs (1) and (2) shall be prescribed by the Presidential Decree.

■■■■ Article 35 (Inclusion of Allocation for Payment of Claims for Compensation in Deductible Expenses)

(1) Where domestic corporations as prescribed by the Presidential Decree among those conducting a credit-guarantee business under Acts appropriate an allocation for payment of claims for compensation for deductible expenses in each fiscal year, the allocation for payment of claims for compensation shall, to the extent of any such amount as calculated under the Presidential Decree, be included in deductible expenses in calculating the amount of income for the relevant fiscal year.

(2) The allocation for payment of claims for compensation included in deductible expenses under paragraph (1) shall be included in gross income in calculating the amount of income for the following fiscal year.

(3) A domestic corporation that wishes to subject itself to the provisions of paragraph (1) shall submit a detailed statement on the allocation for, payment of claims for compensation, as prescribed by the Presidential Decree to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) Necessary matters concerning the disposition of the allocation for payment of claims for compensation under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 36 (Inclusion of Value of Assets for Business Acquired through Treasury Subsidies in Deductible Expenses)

(1) Where a domestic corporation is paid assets, including subsidies, under the Act on the Budgeting and Management of Subsidies, the Local Finance Act, and other Acts as prescribed by the Presidential Decree (hereafter, in this Article, referred to as the "treasury subsidies, etc.") and uses them to acquire or improve assets used for business as prescribed by the Presidential Decree (hereafter, in this Article, referred to as the "assets used for business") by the last day of the fiscal year including the date of such payment, the amount equivalent to the value of the treasury subsidies, etc. used for the acquisition or improvement of the assets used for business may be included in deductible expenses in calculating the amount of income for the relevant fiscal year as prescribed by the Presidential Decree.

(2) Where a domestic corporation that does not use the treasury subsidies, etc. for the acquisition or improvement of assets used for business by the last day of the fiscal year including the date of payment intends to do so within one year of the first day of the following fiscal year, the provisions of paragraph (1) shall apply mutatis mutandis, and the subsidies may be included in deductible expenses. In this case, "uses" shall be deemed to mean "intends to use."

(3) Where a domestic corporation that includes the amount equivalent to the treasury subsidies, etc. in deductible expenses under paragraph (2) fails to use the amount included in deductible expenses for the acquisition or improvement of assets used for business within the time limit, or discontinues business or goes bankrupt before using that amount, the unused amount shall be included in gross income in calculating the amount of income for the fiscal year including the date of the occurrence of the cause for the corporation's failure to use the amount: Provided, That this shall not apply where the domestic corporation is merged or divided and the merged corporation succeeds to the amount. In this case, the amount shall be deemed to be included in deductible expenses of the said merged corporation under paragraph (2).

(4) In applying paragraph (1), where a domestic corporation is paid treasury subsidies, etc. in the form of assets other than money and uses them for its business operation, such treasury subsidies shall be deemed to be used for the acquisition or improvement of assets used for business.

(5) A domestic corporation that wishes to subject itself to the provisions of paragraphs (1) and (2) shall submit a detailed statement on the treasury subsidies, etc. the assets used for business acquired though the treasury subsidies, etc. (a plan for use of the treasury subsidies, etc. in any case stated in paragraph (2)), as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(6) In applying paragraphs (1) through (3), necessary matters concerning the calculation of the amount included in deductible expenses and gross income and the method of such inclusion shall be prescribed by the Presidential Decree.

■■■■ Article 37 (Inclusion of Value of Fixed Assets Acquired through Construction Charges in Deductible Expenses)

(1) Where a domestic corporation conducting a business falling under any of the following subparagraphs is provided with fixed assets making up facilities necessary

for the business, such as land, by a person who uses electricity, gas and heating, etc. or who receives convenience and benefit from those facilities in order to establish them, or where it is provided with money (hereafter in this Article, "construction charges") and uses the money for the acquisition of fixed assets composing the facilities by the last day of the fiscal year including the date of such provision, the value of said fixed assets (the amount equivalent to construction charges used for the acquisition of the fixed assets, where acquired through the construction charges) may be included in deductible expenses in calculating the amount of income for the relevant fiscal year as prescribed by the Presidential Decree:

1. Electricity-service business under the Electricity Business Act;

2. Urban gas business under the Urban Gas Business Act;

3. Liquefied petroleum gas-replenishing business, collective liquefied petroleum gas providing business, and liquefied petroleum gas sales business, under the Safety Control and Business Regulation of Liquefied Petroleum Gas Act;

4. Collective energy-providing business under subparagraph 2 of Article 2 of the Integrated Energy Supply Act; and

5. Businesses similar to the businesses under subparagraphs 1 through 4 as prescribed by the Presidential Decree.

(2) The provisions of Article 36 (2) and (3) shall apply mutatis mutandis to the inclusion in deductible expenses where fixed assets are acquired through construction charges.

(3) A domestic corporation that wishes to subject itself to the provisions of paragraphs (1) and (2) shall submit a detailed statement on fixed assets and construction charges received and the fixed assets acquired through construction charges (in cases arising under paragraph (2), a plan for the use of construction charges), as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) In applying paragraphs (1) and (2), necessary matters concerning the calculation of the amount included in deductible expenses and gross income and the method of such inclusion shall be prescribed by the Presidential Decree.

■■■■ Article 38 (Inclusion of Value of Fixed Assets Acquired through Insurance Profits in Deductible Expenses)

(1) Where a domestic corporation receives payment of insurance money due to the destruction or damage of fixed assets and uses the money for the acquisition of the fixed assets of the same type to replace the destroyed fixed assets or for the improvement of the damaged fixed assets (including the improvement of acquired fixed assets) by the last day of the fiscal year including the date of the payment, an appropriate amount for the insurance profits used for the acquisition or improvement of fixed assets may be included in deductible expenses in calculating the amount of income for the relevant fiscal year as prescribed by the Presidential Decree.

(2) The provisions of Article 36 (2) and (3) shall apply mutatis mutandis with regard to cases of acquisition or improvement of fixed assets through insurance profits in the calculation of deductible expenses. In this case, "one year" in Article 36 (2) shall be deemed "two years".

(3) A domestic corporation that wishes to subject itself to the provisions of paragraphs (1) and (2) shall submit a detailed statement on the insurance money received and fixed assets acquired or improved through insurance profits (in cases under paragraph (2), a plan for use of insurance profits), as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) In applying paragraphs (1) and (2), necessary matters concerning the calculation of the amount included in deductible expenses and gross income and the method of such inclusion shall be prescribed by the Presidential Decree.

■■■■ Article 39 Deleted.

Subsection 5 Period of Accrual of Profits and Losses

■■■■ Article 40 (Fiscal Year for Accrual of Profits and Losses)

(1) The fiscal year for accrual of gross income and deductible expenses of a domestic corporation shall be the fiscal year including the date on which the relevant gross income and deductible expenses are settled.

(2) Matters relevant to the scope of the fiscal year of accrual of gross income and deductible expenses under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 41 (Acquisition Value of Assets)

(1) The acquisition value of assets acquired by a domestic corporation through purchase, production, exchange, and donation shall be the amounts as calculated in any of the following subparagraphs:

1. For assets purchased from another person, the value of the total of the purchase price and any incidental costs;

2. For assets acquired through the corporation's own manufacture, production, construction, or other corresponding method, the value of the total of the cost of production and any incidental costs; and

3. For assets acquired other than under subparagraphs 1 and 2, the amount as prescribed by the Presidential Decree.

(2) Matters relevant to the calculation of the scope of purchase price and incidental costs and other acquisition values of assets under paragraph (1) shall be prescribed by the Presidential Decree.

■■■■ Article 42 (Evaluation of Assets and Liabilities)

(1) Where the book value of assets and liabilities possessed by a domestic corporation increases or decreases, (not including depreciation, hereinafter, in this Article, "evaluation"), the book value of those assets and liabilities in the calculation of the income amount for the fiscal year including the date of the evaluation and each subsequent fiscal year shall be the value before the evaluation, provided that this shall not apply to cases falling into any one of the following categories:

1. Deleted;

2. Evaluation of fixed assets under the Insurance Business Act and other Acts and subordinate statutes (limited to the amount of increase); and

3. Evaluation of stored assets and other assets and liabilities as prescribed by the Presidential Decree.

(2) Assets and liabilities under paragraph (1) 3 must be evaluated separately as assets or liabilities by the method prescribed by the Presidential Decree.

(3) For assets falling under any of the following categories, the book value may be reduced under paragraphs (1) and (2), notwithstanding methods prescribed by the Presidential Decree:

1. Stored assets that cannot be sold at the normal price due to damage, spoilage, or other causes;

2. Fixed assets that are damaged or broken due to natural disaster, fire, or other cause as prescribed by the Presidential Decree;

3. Stocks, as prescribed by the Presidential Decree, that the issuing corporation refuses to honor; and

4. Stocks, where a corporation that has issued them goes bankrupt.

(4) A domestic corporation that evaluates assets and liabilities under paragraphs (2) and (3) must submit a detailed statement on the evaluation of the concerned assets and liabilities, as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(5) Matters relevant to the disposition of evaluation profits and evaluation losses arising from the evaluation of assets and liabilities under paragraphs (2) and (3) shall be prescribed by the Presidential Decree.

■■■■ Article 43 (Application of Corporate Accounting Standards and Practices)

In calculating the income amount for any domestic corporation's fiscal year, where the concerned corporation applies corporate accounting standards that are generally acknowledges as fair and proper in the acquisition and evaluation of gross income and deductible expenses accrued in a fiscal year and assets and liabilities, and

continuously applies such practices, those corporate accounting standards or practices shall be followed except as otherwise provided in this Act and in the Restriction of Special Taxation Act.

Subsection 6 Special Cases Concerning Mergers and Divisions

■■■■ Article 44 (Inclusion of Reasonable Amount of Merger Evaluation Profits in Deductible Expenses)

(1) For mergers that meet the conditions listed in any of the following subparagraphs, where a merged corporation evaluates and succeeds to the assets of the extinguished corporation, an appropriate value for merger evaluation profits for those assets from the value of the assets acquired by succession (limited to assets as prescribed by the Presidential Decree) may be included in deductible expenses in calculating the amount of income for the fiscal year including the date of the registration of the merger, as prescribed by the Presidential Decree:

1. Where a merger occurs between domestic corporations that have continued to operate for one year or more after the date of registration of the merger;

2. Where the total value of the cost of merger received by stockholders of an extinguished corporation from the merged corporation in return for such merger is 95/100 or more of the value of the stocks; and

3. Where the merged corporation continues to operate a business it received by succession from the extinguished corporation until the last day of the fiscal year including the date of the registration of the merger.

(2) Where a merged corporation that includes an appropriate value for merger evaluation profits in deductible expenses under paragraph (1) discontinues a business it acquired through succession from the extinguished corporation within three years from the first day of the fiscal year following the fiscal year including the date of the registration of the merger, the amount included in the calculation of deductible expenses shall be included as gross income in the calculation of income for the fiscal year including the date the business was discontinued.

(3) A merged corporation that wishes to subject itself to the application of the provisions of paragraph (1) must submit a detailed statement on merger evaluation profits as prescribed by the Presidential Decree, to the chief of the regional tax office having jurisdiction over that corporation's place of tax payment.

(4) In applying the provisions of paragraphs (1) and (2), matters relevant to criteria for judgements regarding the continuance or discontinuance of businesses acquired by succession, calculation of deductible expenses and gross income, and the method for inclusion of deductible expenses and gross income in the calculation of income shall be prescribed by the Presidential Decree.

■■■■ Article 45 (Succession to Net Operating Losses Carried Forward at Time of Merger)

(1) For mergers that meet the conditions listed under any of the following subparagraphs, where the merged corporation succeeds to the assets of the extinguished corporation at book value, as of the date of the registration of the merger net operating losses of the extinguished corporation under subparagraph 1 of Article 13 shall be deemed net operating losses of the merged corporation, and shall be deducted from the standard of tax assessment for each fiscal year of the merged corporation as prescribed by the Presidential Decree up to the amount of income generated by the business acquired by succession:

1. Where mergers fall under any subparagraph of Article 44 (1);

2. Where the stocks received from a merged corporation by stockholders of an extinguished corporation are 10/100 or more of the total stocks issued by the merged corporation or total investment as of the day of registration of the merger; and

3. Where a merged corporation maintains separate accounting under Article 113 (3).