Embed Size (px)

Citation preview

Cost AllocationIssues

Chapter 5

Managerial Accounting

Concepts and Empirical Evidence

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

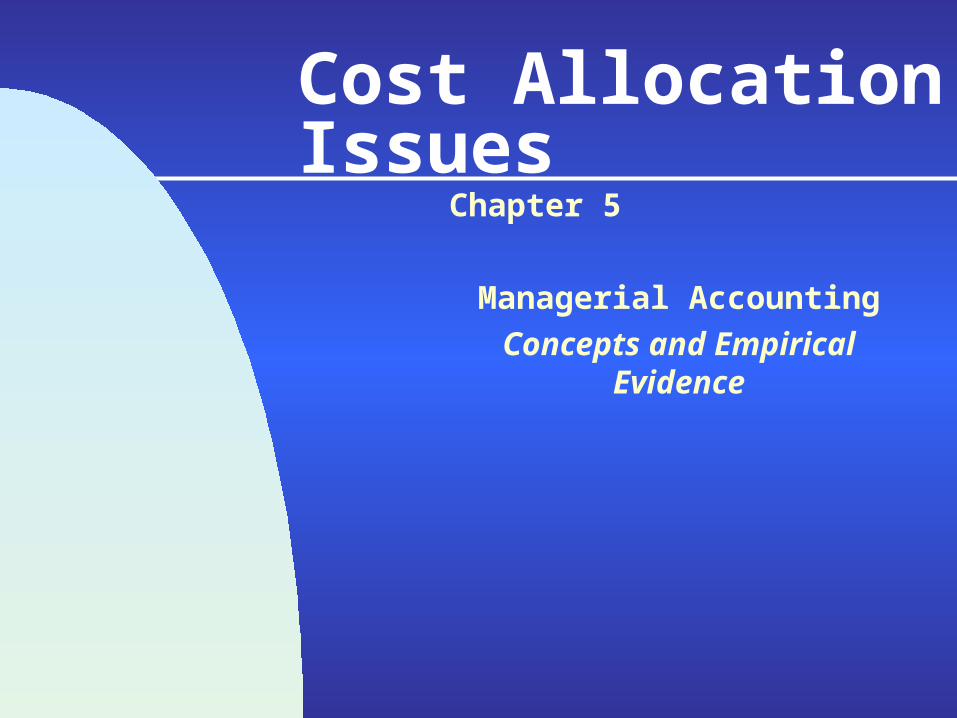

Single Base vs. Multiple Base Approach to Allocating Indirect Costs

Y = b0+b1X1+b2X2+…+bnXn , … Eq. 5.3

IC = f (X 1 , X 2 ,…... X n) , … Eq. 5.1

Y = B0+B1X1+B2X2+….+BnXn+ , … Eq. 5.2

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

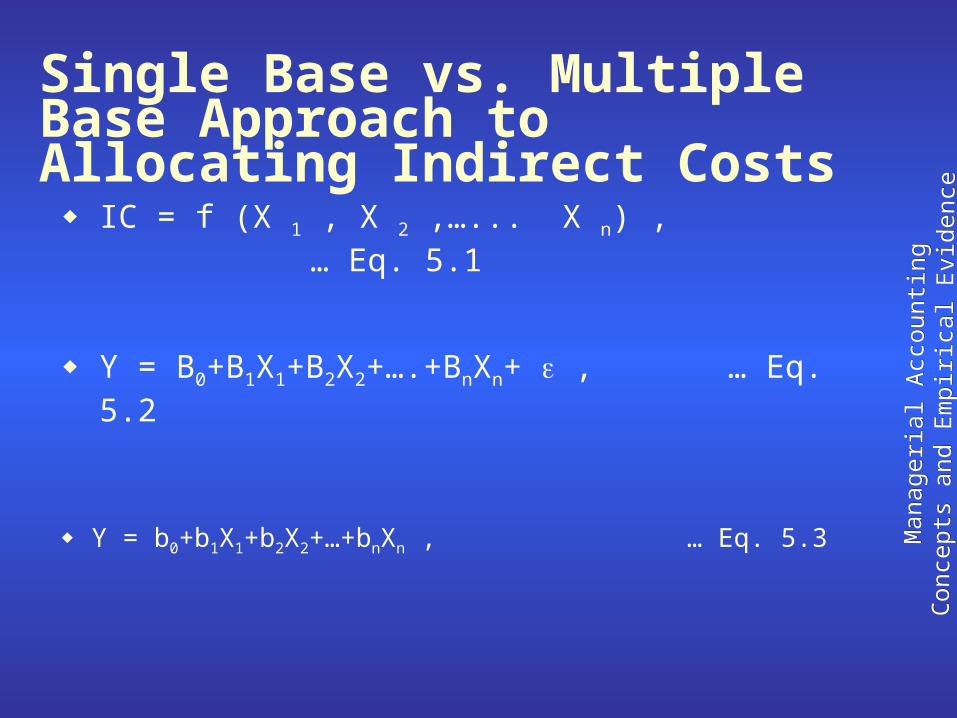

Vad CorporationRegression Analysis

MonthIndirect

Costs ($) YLabor

Hours (X1)Machine

Hours (X2)Machine

Setup (X3)1 16,764 1,287 1,000 7

2 19,440 1,530 1,010 10

3 15,018 1,104 986 7

4 18,960 1,446 1,154 9

5 20,148 1,494 1,024 11

6 16,902 1,235 950 9

7 16,286 1,167 1,077 8

8 19,492 1,388 922 12

9 13,276 885 991 7

10 14,694 1,000 892 7

11 19,752 1,415 1,110 1

12 14,446 964 986 18

13 17,664 1,257 880 11

14 20,432 1,523 981 11

15 13,638 953 1,023 7

16 15,448 113 1,103 7

17 13,148 958 1,041 5

18 17,616 1,319 1,045 9

19 13,826 1,056 955 6

20 17,284 1,260 1,053 7

Data Summary

Estimated Model:

Y = 1,446.22 + 8.38 X1 + 1.68 X2 + 398.56 X3

^

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

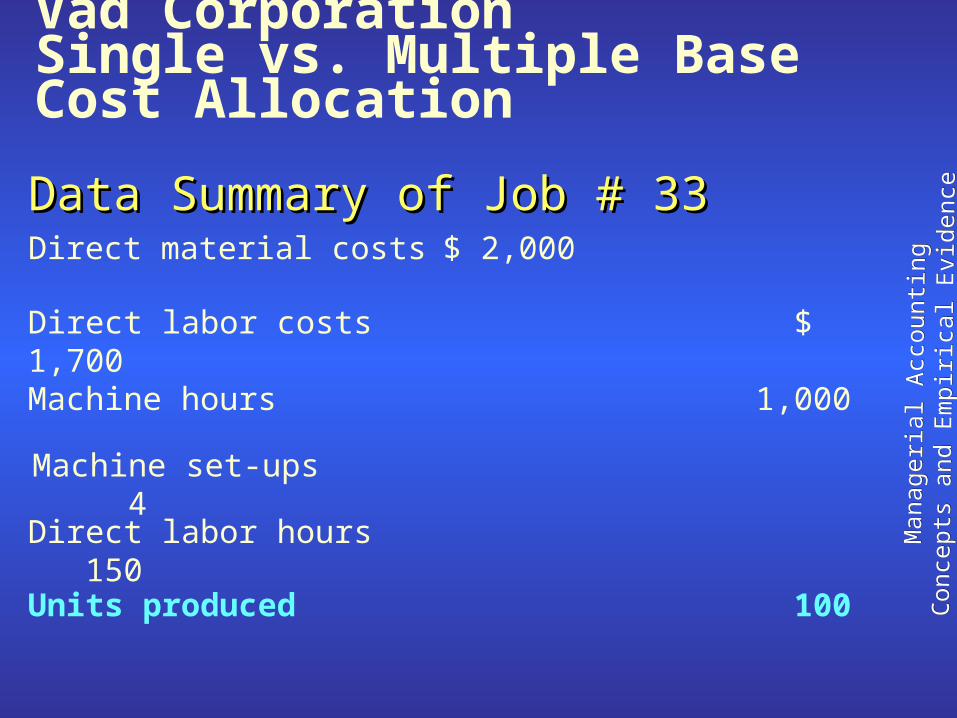

Data Summary of Job # 33Data Summary of Job # 33Direct material costs $ 2,000

Direct labor costs $ 1,700

Machine hours 1,000

Machine set-ups 4

Direct labor hours 150Units produced 100

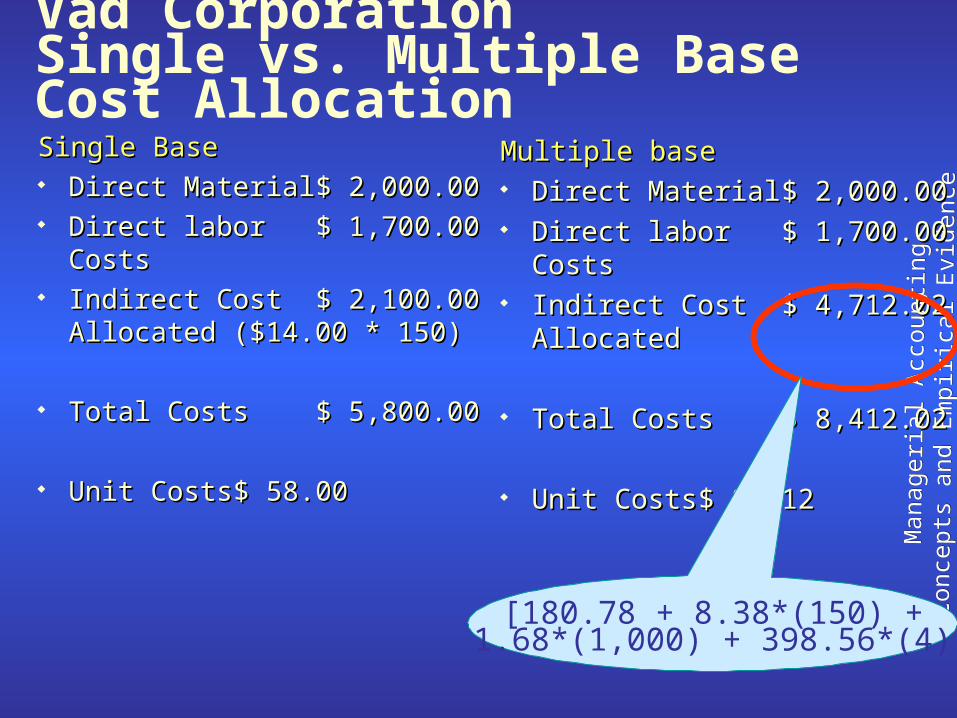

Vad CorporationSingle vs. Multiple Base Cost Allocation

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

Single BaseSingle Base Direct MaterialDirect Material $ $

2,000.002,000.00 Direct labor Direct labor $ 1,700.00$ 1,700.00

CostsCosts Indirect CostIndirect Cost $ 2,100.00$ 2,100.00

Allocated ($14.00 * 150)Allocated ($14.00 * 150)

Total CostsTotal Costs $ 5,800.00$ 5,800.00

Unit CostsUnit Costs $ 58.00$ 58.00

Vad CorporationSingle vs. Multiple Base Cost Allocation

Multiple baseMultiple base Direct MaterialDirect Material $ $

2,000.002,000.00 Direct labor Direct labor $ 1,700.00$ 1,700.00

CostsCosts Indirect CostIndirect Cost $ 4,712.02$ 4,712.02

AllocatedAllocated

Total CostsTotal Costs $ 8,412.02$ 8,412.02

Unit CostsUnit Costs $ 84.12$ 84.12[180.78 + 8.38*(150) +

1.68*(1,000) + 398.56*(4)]

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

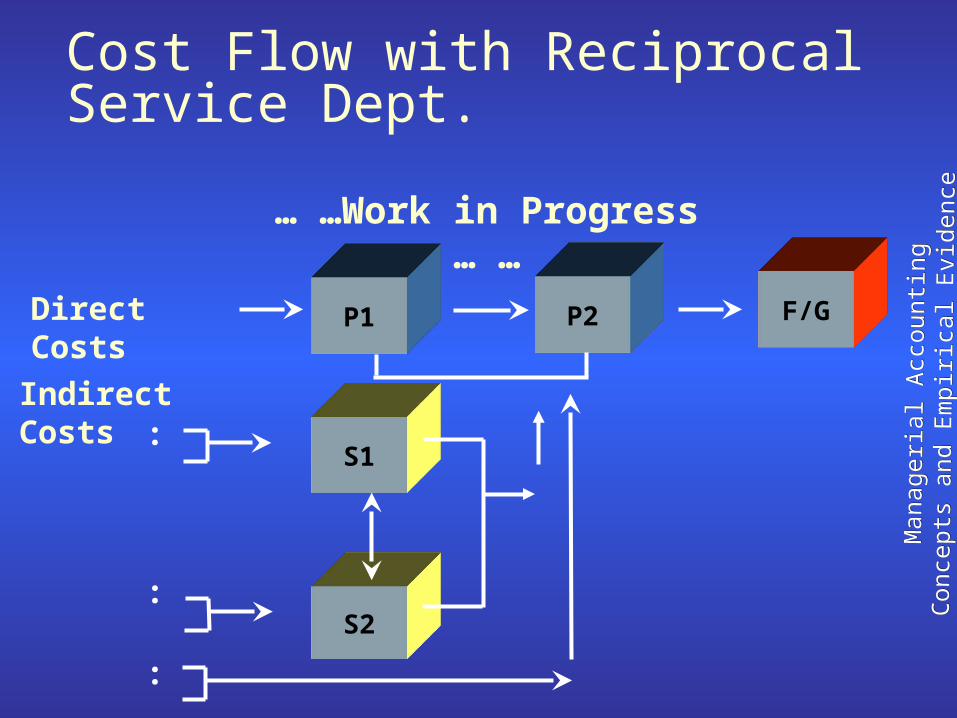

Cost Flow with Reciprocal Service Dept.

P1Direct Costs F/GP2

… …Work in Progress … …

Indirect Costs

S2

S1:

:

:

:

:

:

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

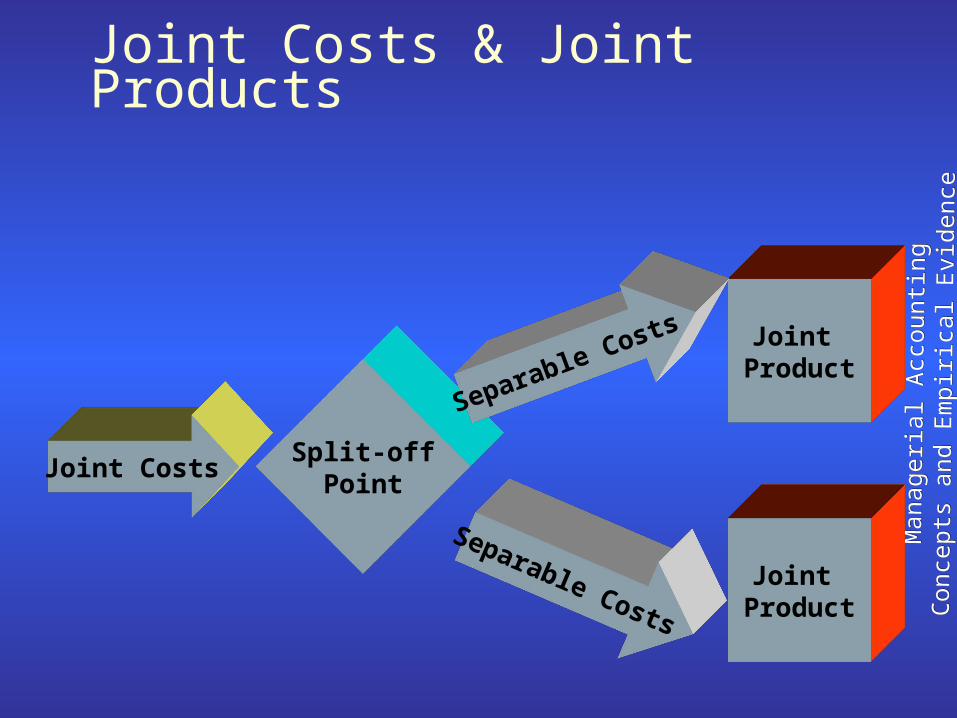

Joint Costs & Joint Products

Joint Product

Joint Product

Split-offPoint

Joint Costs

Separable Costs

Separable Costs

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

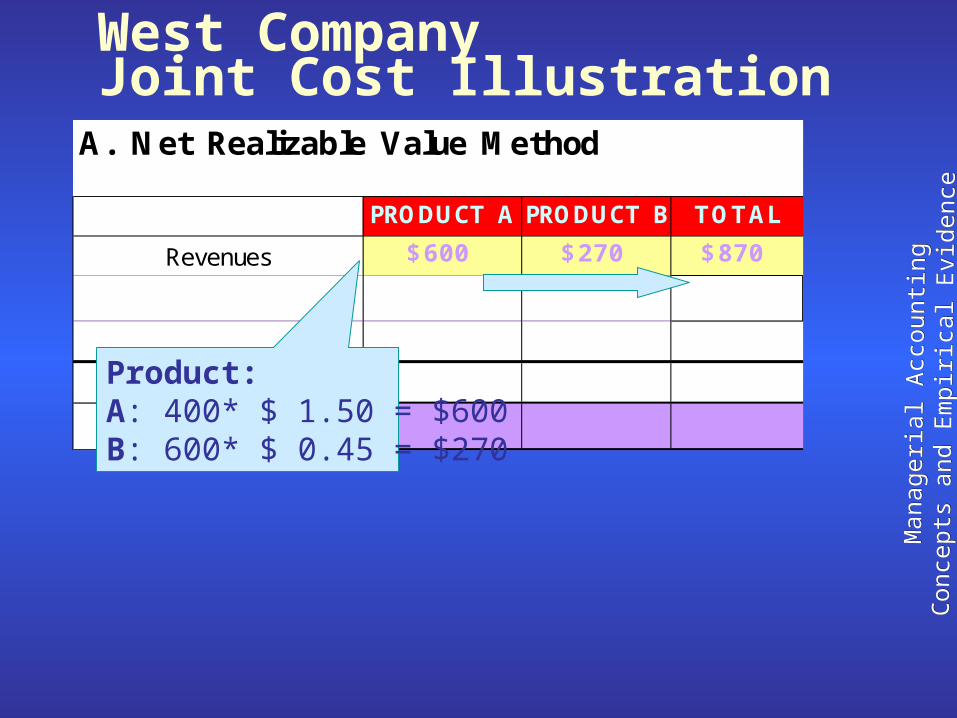

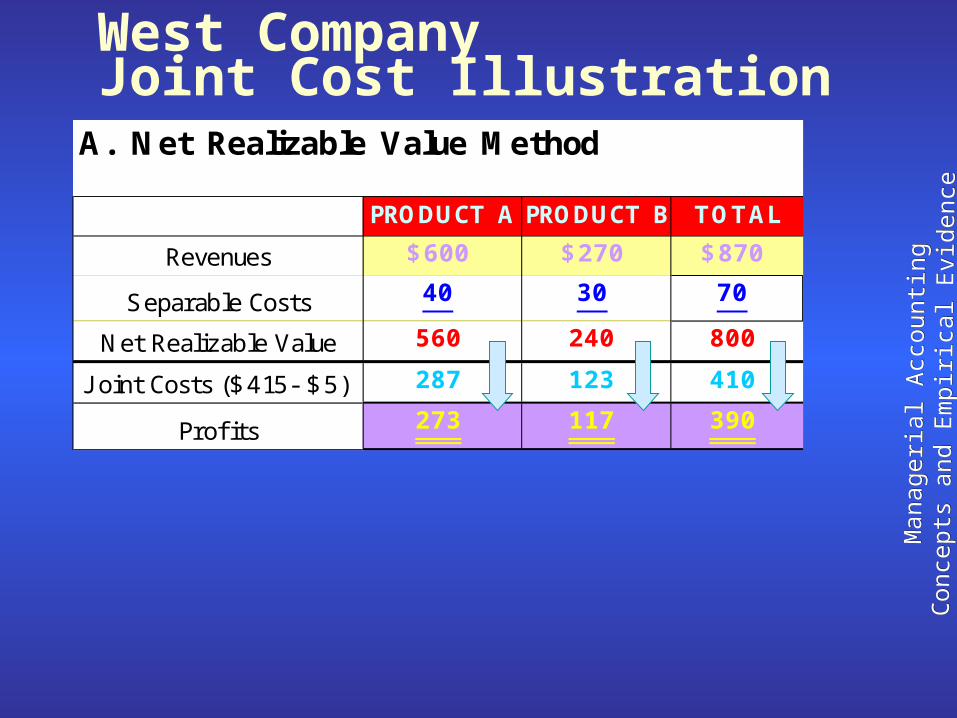

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

TOTAL

Revenues $270

PRODUCT A PRODUCT B

$870$600

Product:A: 400* $ 1.50 = $600B: 600* $ 0.45 = $270

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

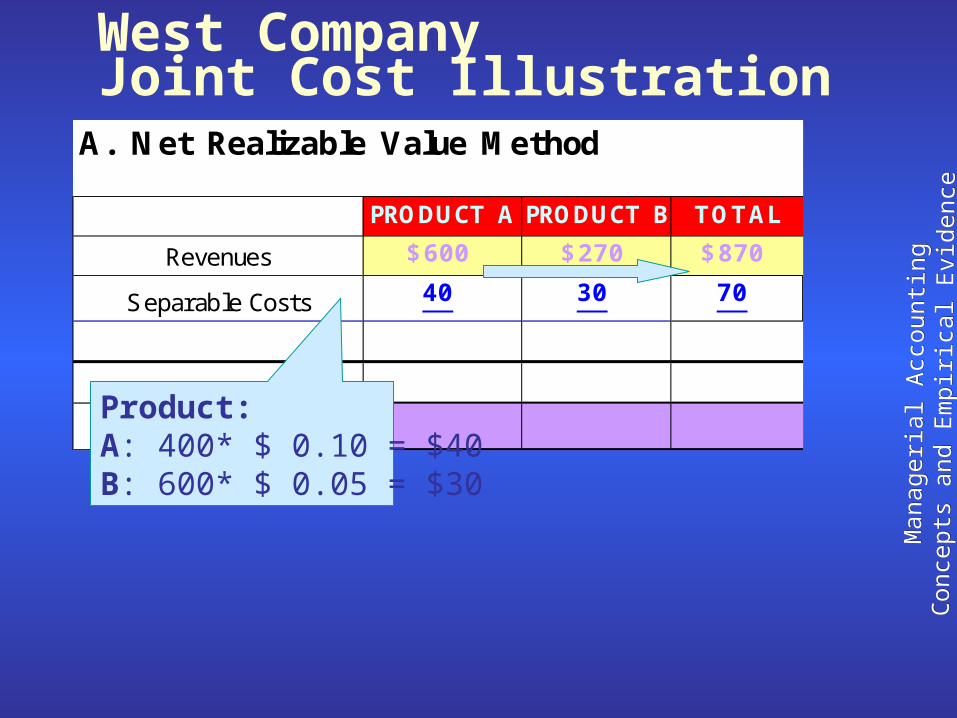

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

$600

40

Product:A: 400* $ 0.10 = $40B: 600* $ 0.05 = $30

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

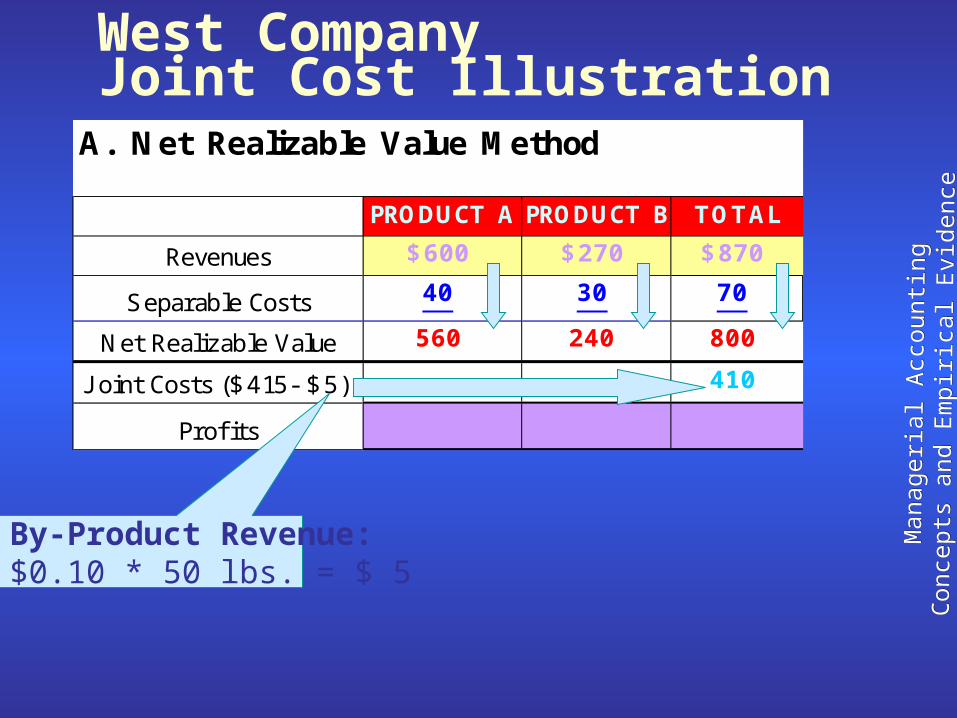

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

800240

Profi ts

J oint Costs ($415- $5) 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

Net Realizable Value

$600

40

560

By-Product Revenue:$0.10 * 50 lbs. = $ 5

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

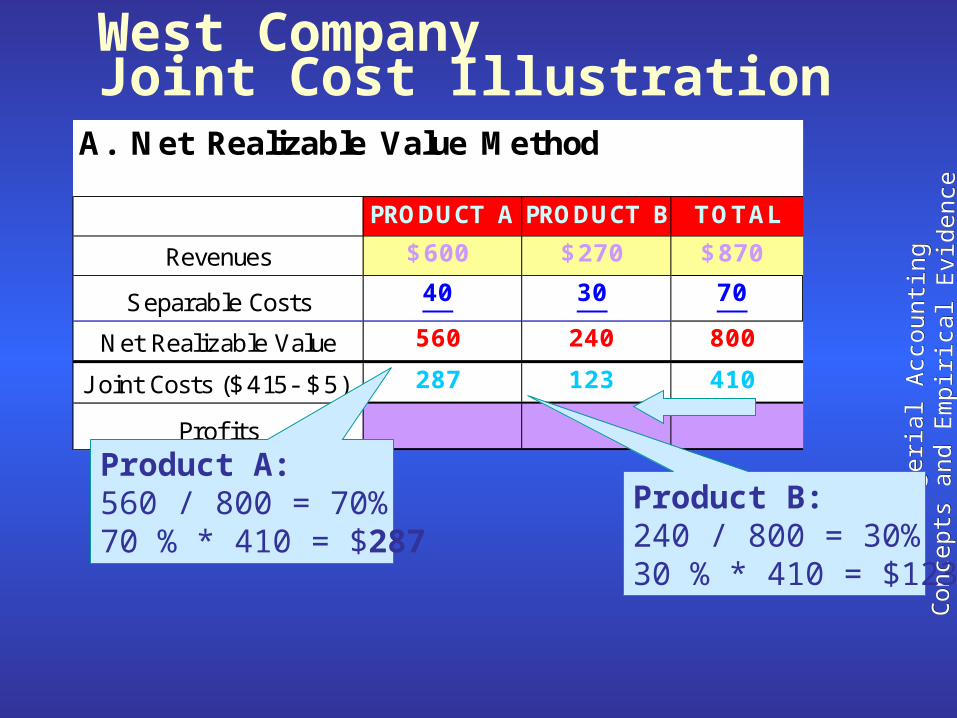

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

800240

Profi ts

J oint Costs ($415- $5) 287 123 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

Net Realizable Value

$600

40

560

Product A:560 / 800 = 70%70 % * 410 = $287

Product B:240 / 800 = 30%30 % * 410 = $123

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

Net Realizable Value

$600

40

560

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

800240

Profi ts

J oint Costs ($415- $5) 287 123 410

273 117 390

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

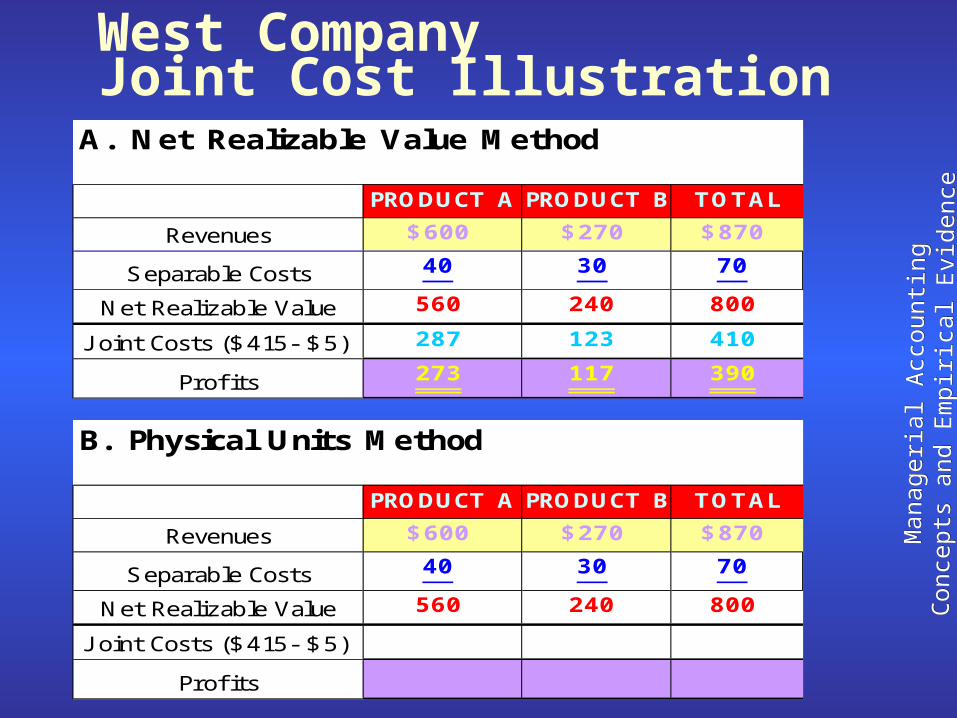

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

B. Physical Units Method

273 117 390

$600 $270 $870

PRODUCT B TOTAL

J oint Costs ($415- $5) 287 123 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

70

Net Realizable Value

$600

40

560

PRODUCT A

800240

Profi ts

Revenues

Net Realizable Value 560 240

Separable Costs 40 30

800

J oint Costs ($415- $5)

Profi ts

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

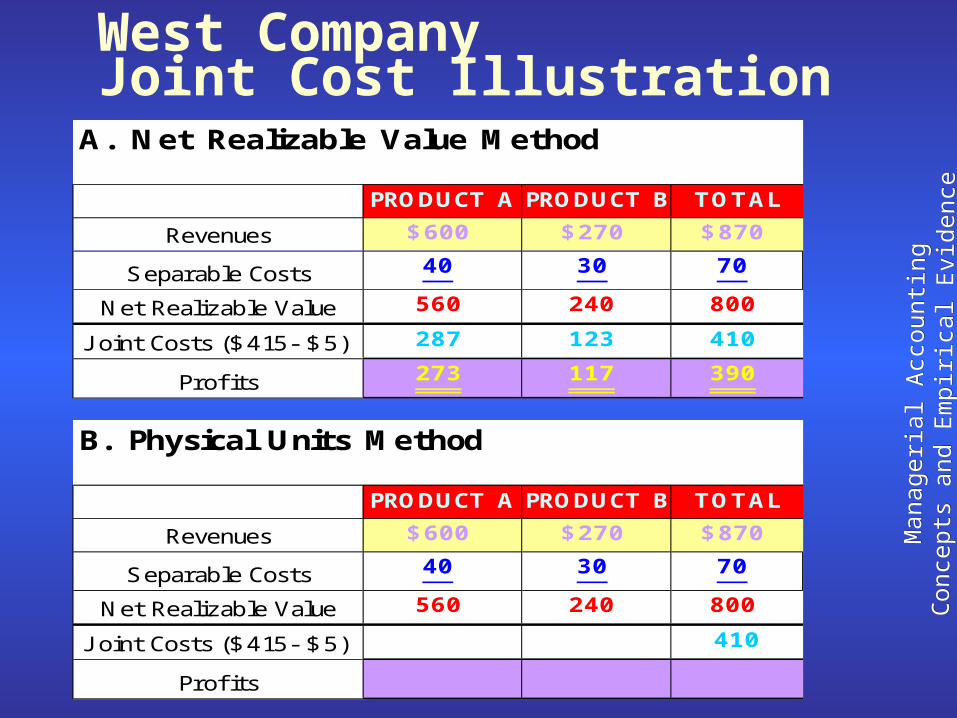

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

B. Physical Units Method

273 117 390

$600 $270 $870

PRODUCT B TOTAL

J oint Costs ($415- $5) 287 123 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

70

Net Realizable Value

$600

40

560

PRODUCT A

800240

Profi ts

Revenues

Net Realizable Value 560 240

Separable Costs 40 30

800

J oint Costs ($415- $5) 410

Profi ts

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

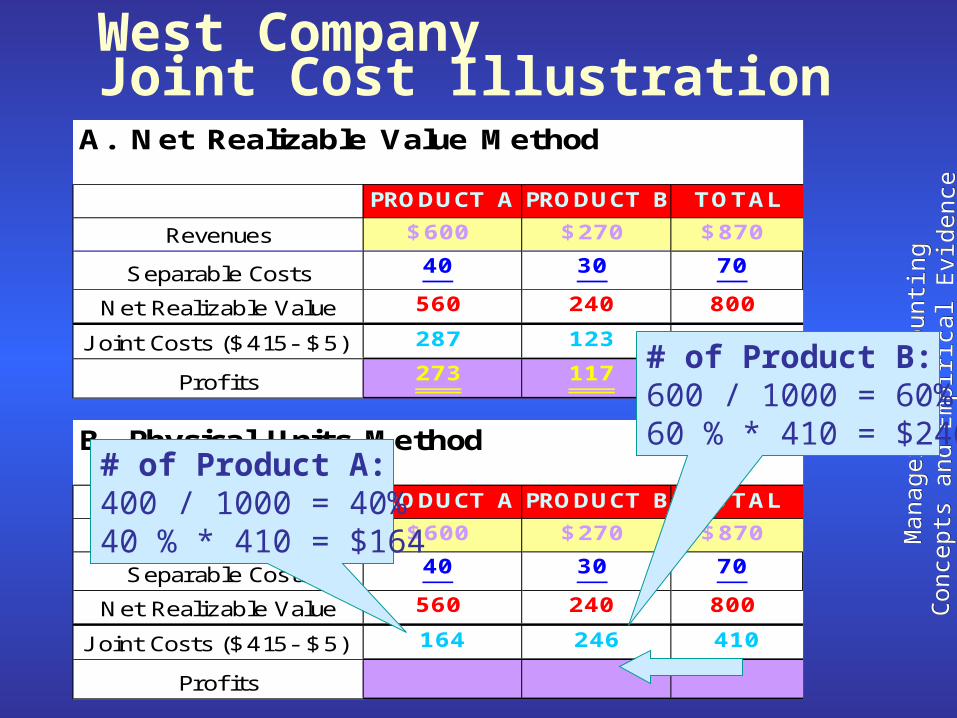

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

B. Physical Units Method

273 117 390

$600 $270 $870

PRODUCT B TOTAL

J oint Costs ($415- $5) 287 123 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

70

Net Realizable Value

$600

40

560

PRODUCT A

800240

Profi ts

Revenues

Net Realizable Value 560 240

Separable Costs 40 30

800

J oint Costs ($415- $5) 164 246 410

Profi ts

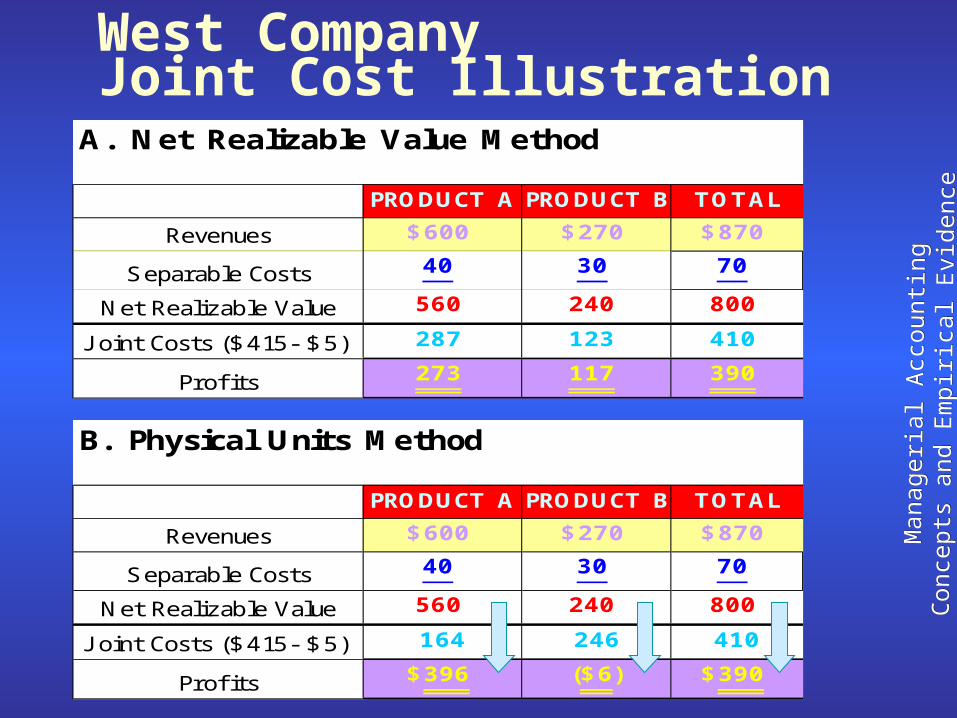

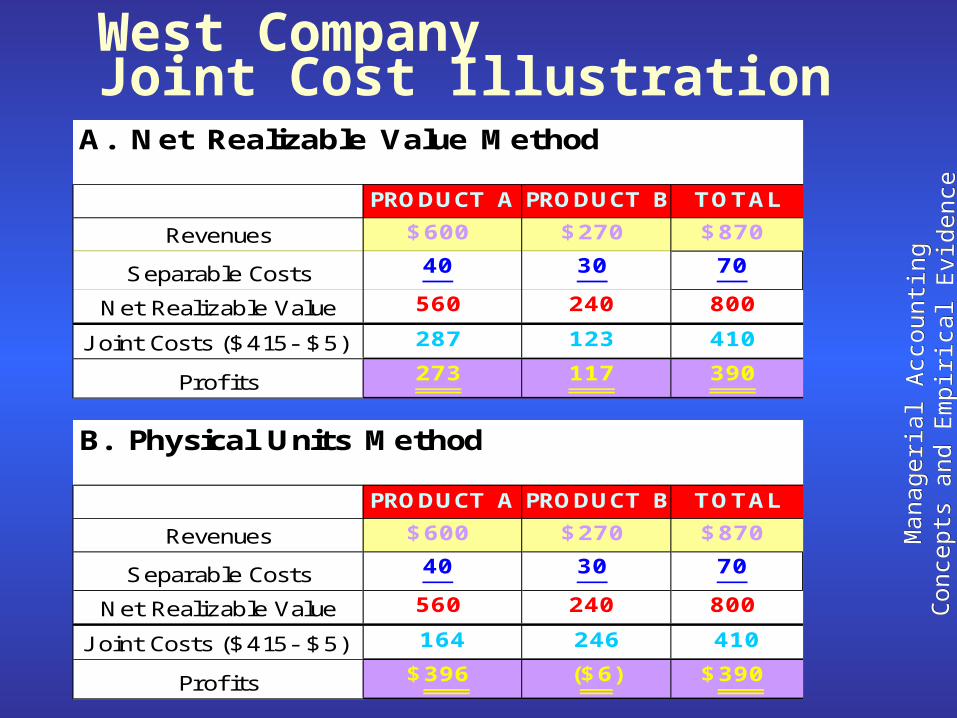

# of Product A:400 / 1000 = 40%40 % * 410 = $164

# of Product B:600 / 1000 = 60%60 % * 410 = $246

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

B. Physical Units Method

273 117 390

$600 $270 $870

PRODUCT B TOTAL

J oint Costs ($415- $5) 287 123 410

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

70

Net Realizable Value

$600

40

560

PRODUCT A

800240

Profi ts

Revenues

Net Realizable Value 560 240

Separable Costs 40 30

800

J oint Costs ($415- $5) 164 246 410

Profi ts $396 ($6) $390

Manageri

al A

ccou

nti

ng

Manageri

al A

ccou

nti

ng

Conce

pts

and E

mpir

ical Evid

ence

Conce

pts

and E

mpir

ical Evid

ence

West CompanyJoint Cost Illustration

A. Net Realizable Value Method

B. Physical Units Method

Profi ts $396 ($6) $390

800

J oint Costs ($415- $5) 164 246 410

Revenues

Net Realizable Value 560 240

Separable Costs 40 30 70

Net Realizable Value

$600

40

560

TOTAL

Revenues

Separable Costs

$270

30

PRODUCT A PRODUCT B

$870

70

PRODUCT A

800240

Profi ts

J oint Costs ($415- $5) 287 123 410

273 117 390

$600 $270 $870

PRODUCT B TOTAL