Embed Size (px)

Citation preview

Cost Behavior:Analysis and Use

Chapter

5

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

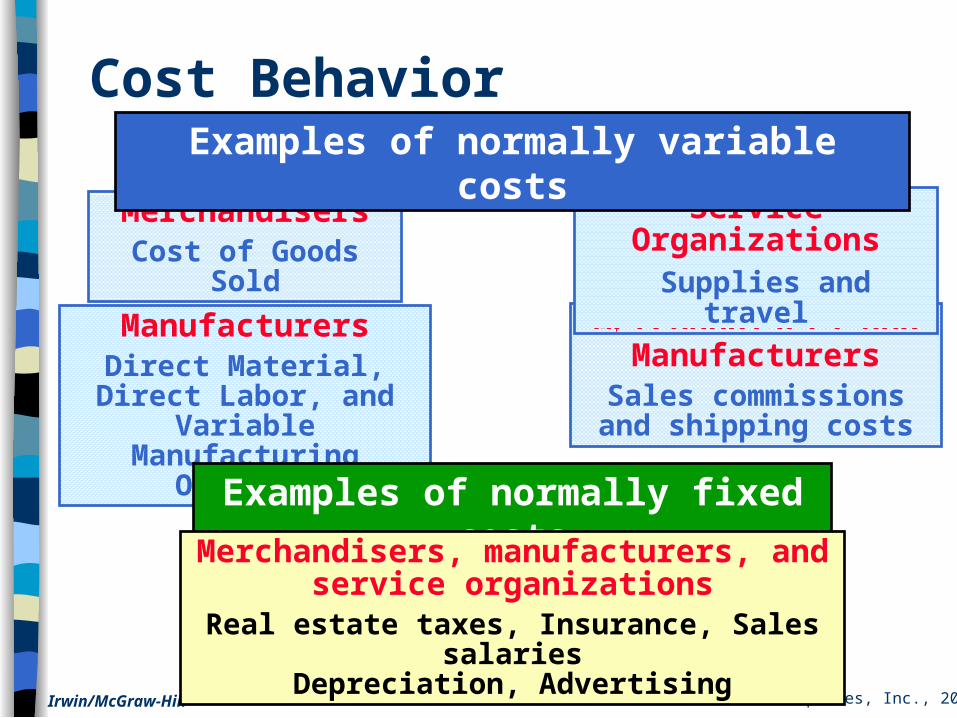

Cost Behavior

MerchandisersCost of Goods Sold

ManufacturersDirect Material, Direct Labor, and Variable

Manufacturing Overhead

Merchandisers and Manufacturers

Sales commissions and shipping costs

Service Organizations Supplies and travel

Examples of normally variable costs

Examples of normally fixed costs

Merchandisers, manufacturers, and service organizations

Real estate taxes, Insurance, Sales salariesDepreciation, Advertising

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

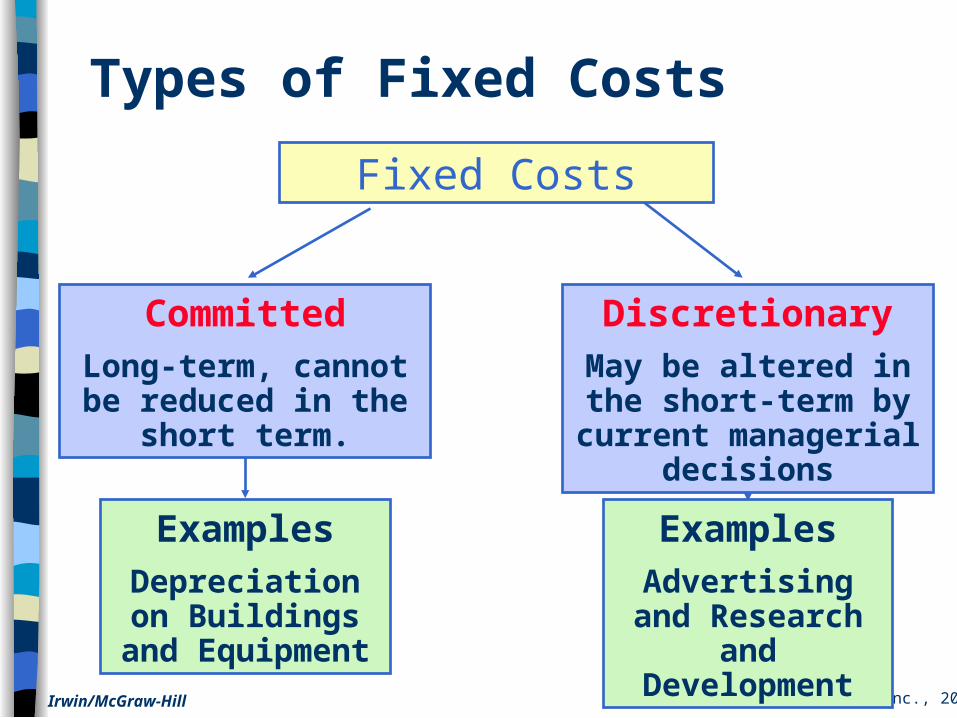

Types of Fixed Costs

Fixed Costs

DiscretionaryMay be altered in the short-term by current managerial decisions

CommittedLong-term, cannot be reduced in the short

term.

ExamplesDepreciation on Buildings and

Equipment

ExamplesAdvertising and Research and Development

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Example: Office space is available at a rental

rate of $30,000 per year in increments of 1,000 square feet. As

the business grows more space is rented,

increasing the total cost.

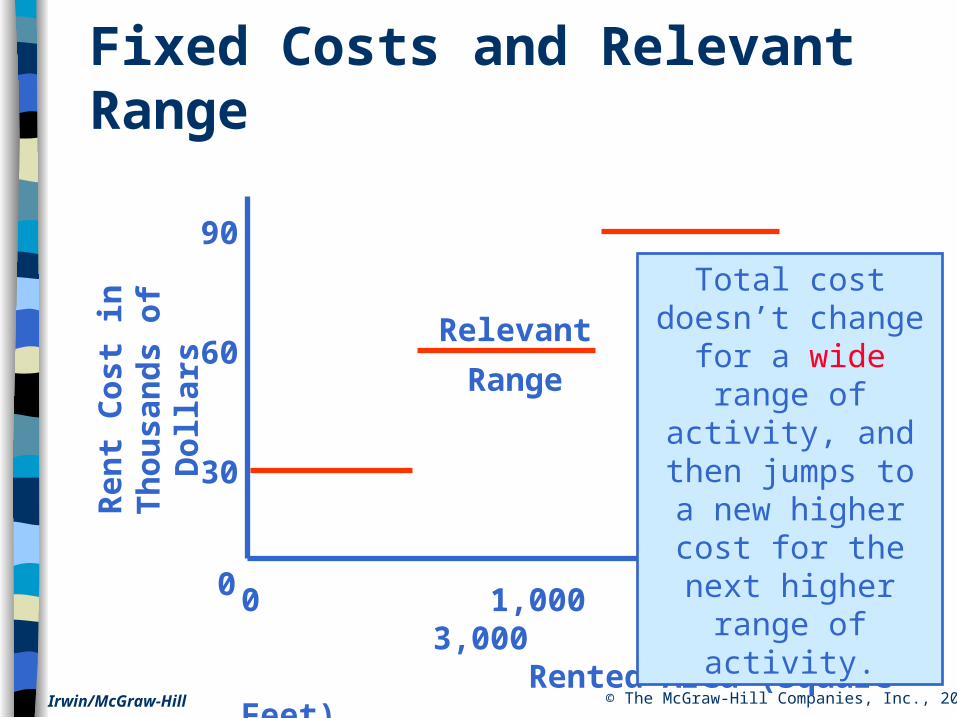

Fixed Costs and Relevant Range

Continue

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Ren

t C

ost

in

T

ho

usa

nd

s o

f D

oll

ars

0 1,000 2,000 3,000 Rented Area (Square Feet)

0

30

60

Fixed Costs and Relevant Range

90

Relevant

Range

Total cost doesn’t change for a wide range of activity,

and then jumps to a new higher cost for

the next higher range of activity.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

A mixed costhas both fixed and variablecomponents.

Mixed Costs

Consider thefollowing electric utility example.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

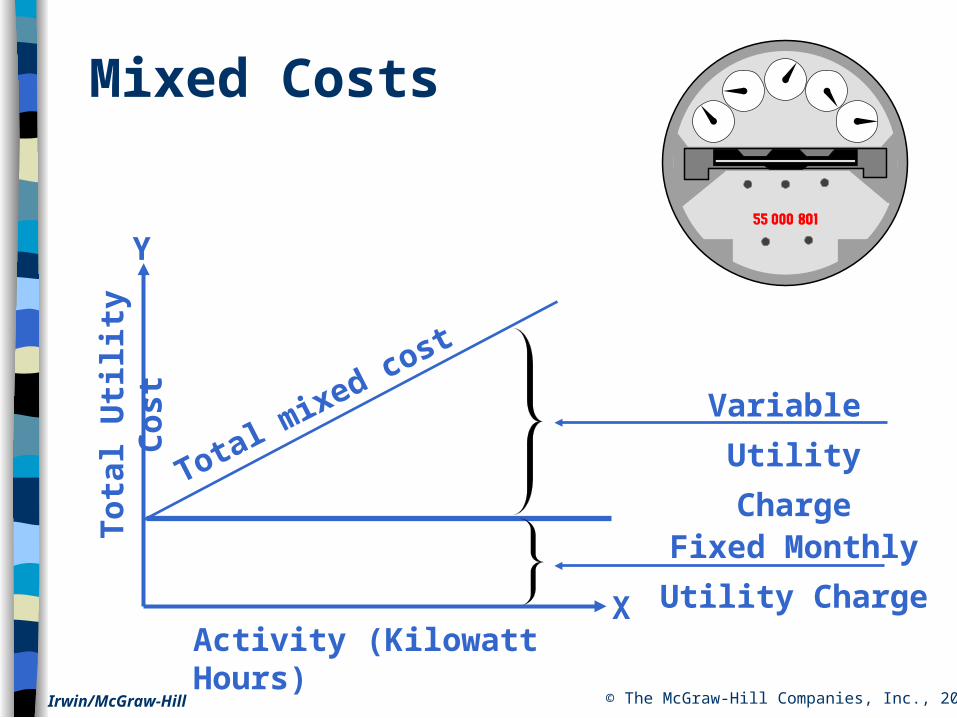

Fixed Monthly

Utility Charge

Variable

Utility Charge

Activity (Kilowatt Hours)

To

tal

Uti

lity

Co

stMixed Costs

X

Y

Total mixed cost

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

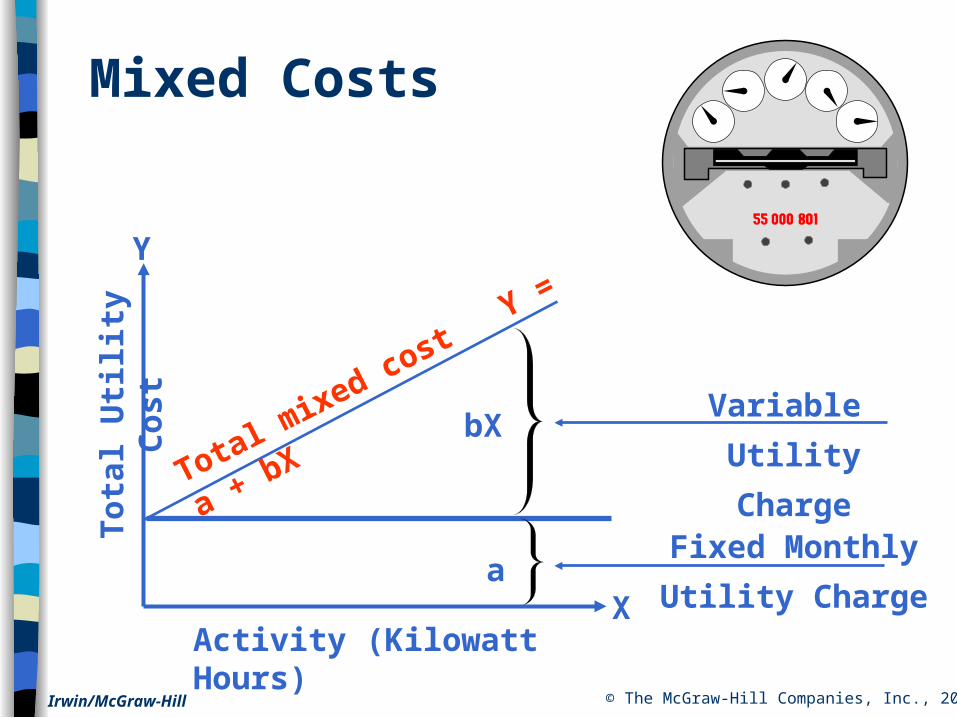

Fixed Monthly

Utility Charge

Variable

Utility Charge

Activity (Kilowatt Hours)

To

tal

Uti

lity

Co

st

Total mixed cost Y

= a + bX

Mixed Costs

bX

aX

Y

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

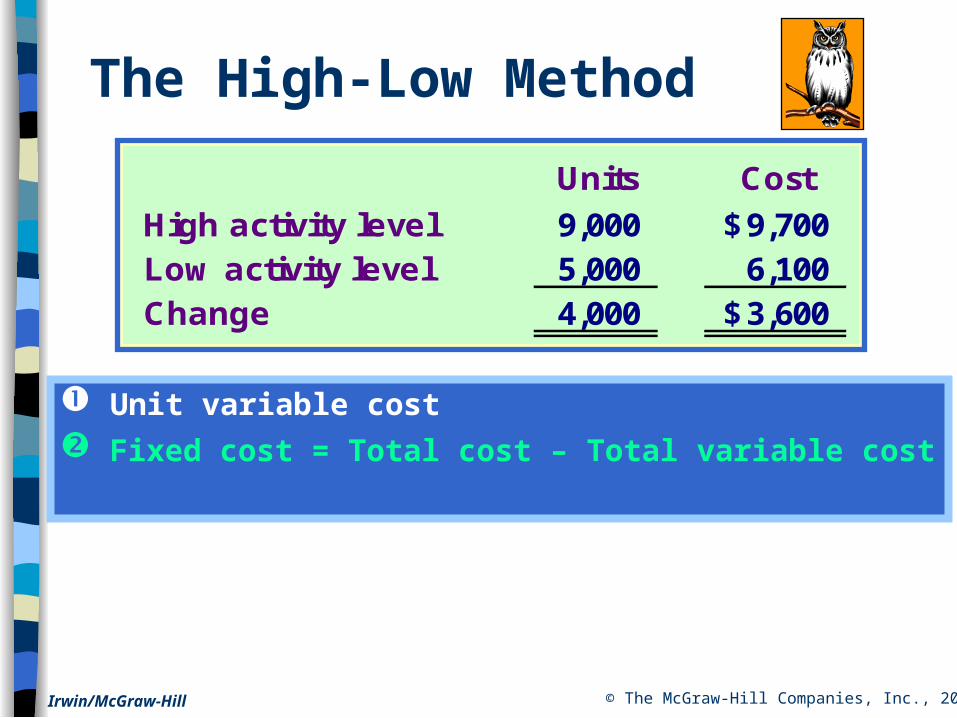

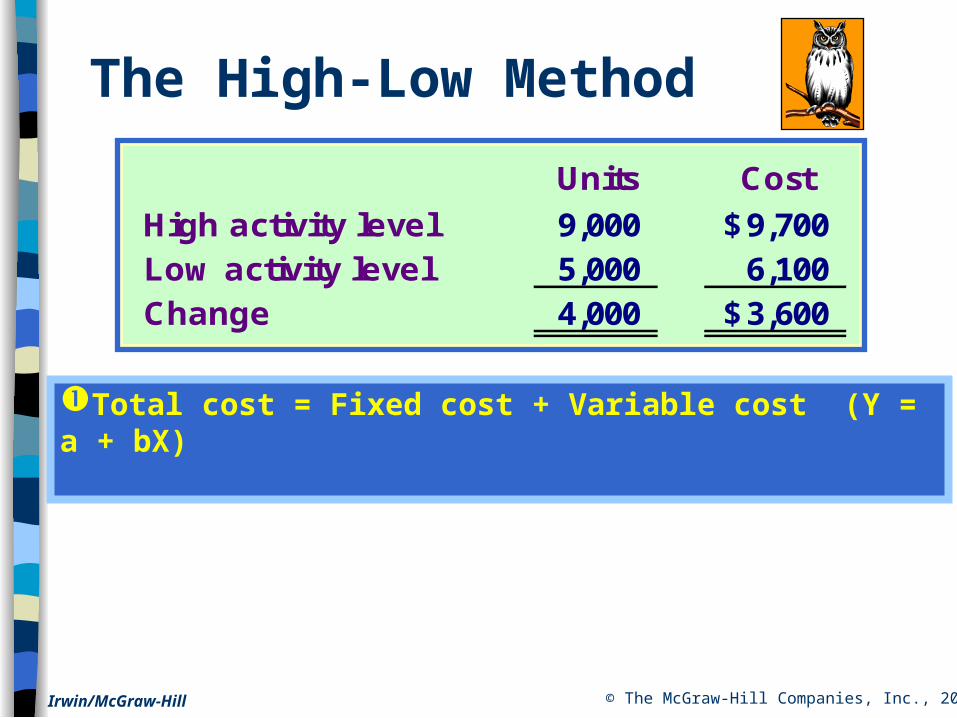

Unit variable cost =Changein costChange in units

Units Cost

High activity level 9,000 9,700$ Low activity level 5,000 6,100 Change 4,000 3,600$

The High-Low Method

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Units Cost

High activity level 9,000 9,700$ Low activity level 5,000 6,100 Change 4,000 3,600$

The High-Low Method

Unit variable cost Fixed cost = Total cost – Total variable cost

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Total cost = Fixed cost + Variable cost (Y = a + bX)

Units Cost

High activity level 9,000 9,700$ Low activity level 5,000 6,100 Change 4,000 3,600$

The High-Low Method

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

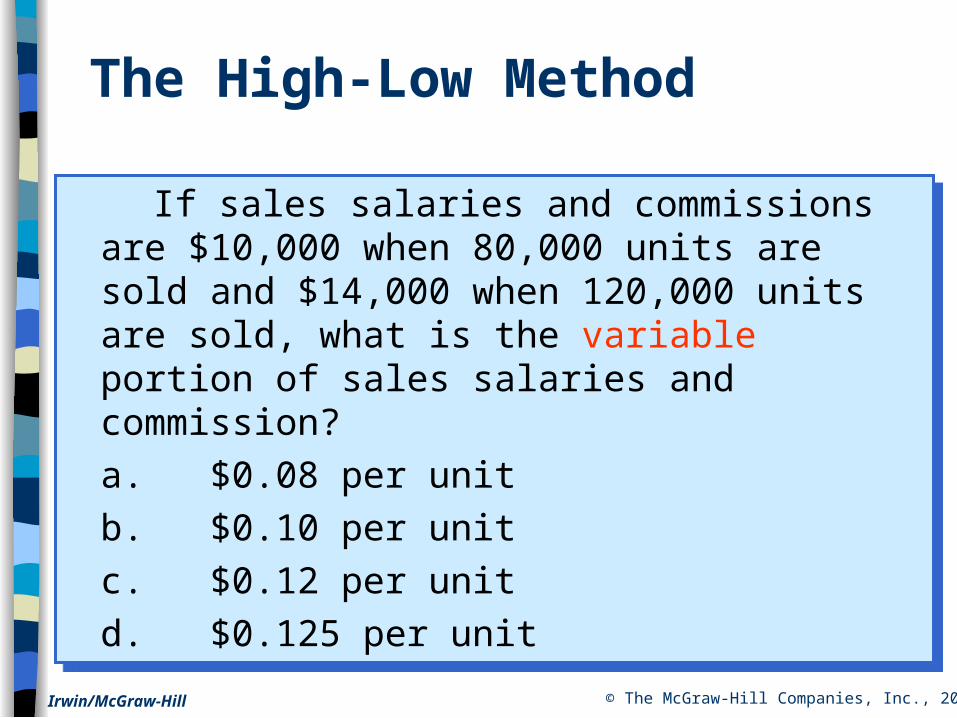

If sales salaries and commissions are $10,000 when 80,000 units are sold and $14,000 when 120,000 units are sold, what is the variable portion of sales salaries and commission?

a. $0.08 per unit

b. $0.10 per unit

c. $0.12 per unit

d. $0.125 per unit

If sales salaries and commissions are $10,000 when 80,000 units are sold and $14,000 when 120,000 units are sold, what is the variable portion of sales salaries and commission?

a. $0.08 per unit

b. $0.10 per unit

c. $0.12 per unit

d. $0.125 per unit

The High-Low Method

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

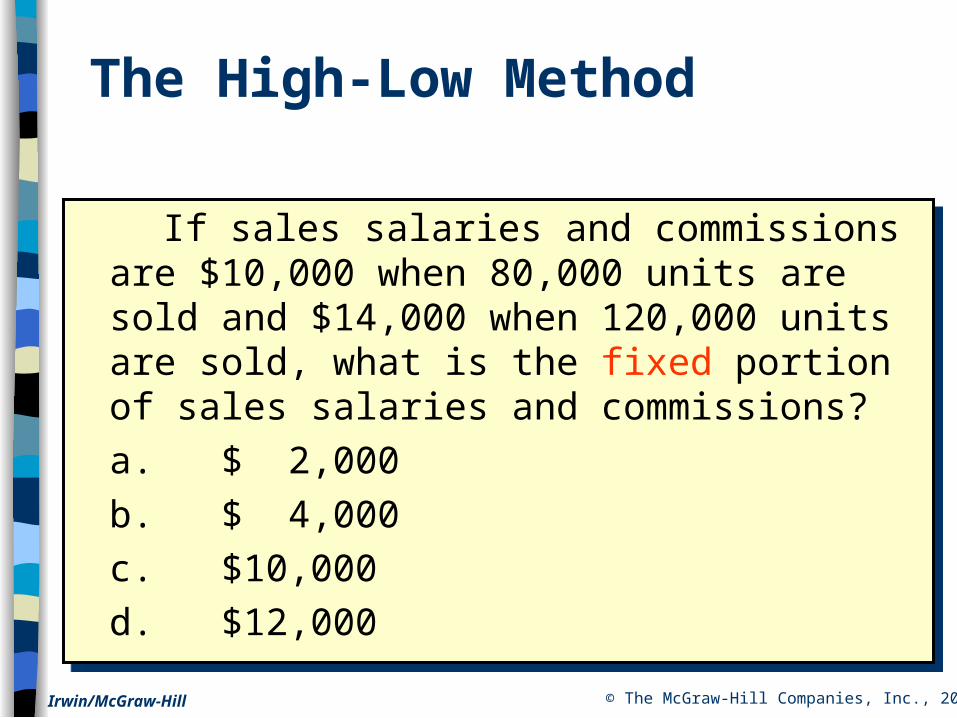

If sales salaries and commissions are $10,000 when 80,000 units are sold and $14,000 when 120,000 units are sold, what is the fixed portion of sales salaries and commissions?

a. $ 2,000

b. $ 4,000

c. $10,000

d. $12,000

If sales salaries and commissions are $10,000 when 80,000 units are sold and $14,000 when 120,000 units are sold, what is the fixed portion of sales salaries and commissions?

a. $ 2,000

b. $ 4,000

c. $10,000

d. $12,000

The High-Low Method

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

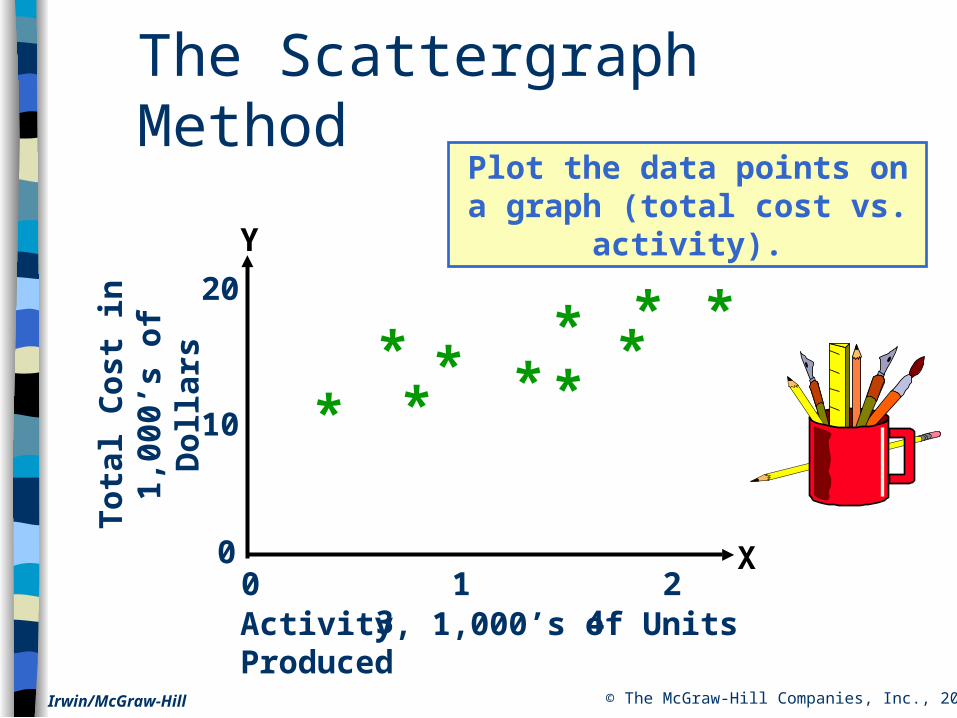

The Scattergraph MethodPlot the data points on a

graph (total cost vs. activity).

0 1 2 3 4

*

To

tal

Co

st i

n1,

000’

s o

f D

oll

ars

10

20

0

***

**

**

*

*

Activity, 1,000’s of Units Produced

X

Y

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

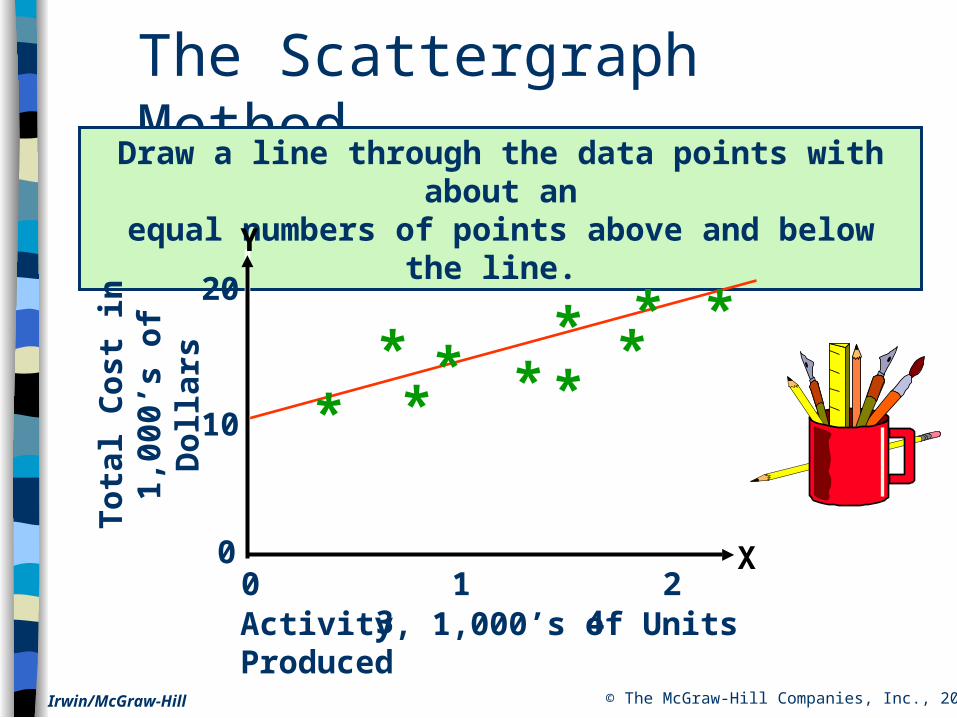

The Scattergraph MethodDraw a line through the data points with about an

equal numbers of points above and below the line.

0 1 2 3 4

*

To

tal

Co

st i

n1,

000’

s o

f D

oll

ars

10

20

0

***

**

**

*

*

Activity, 1,000’s of Units Produced

X

Y

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

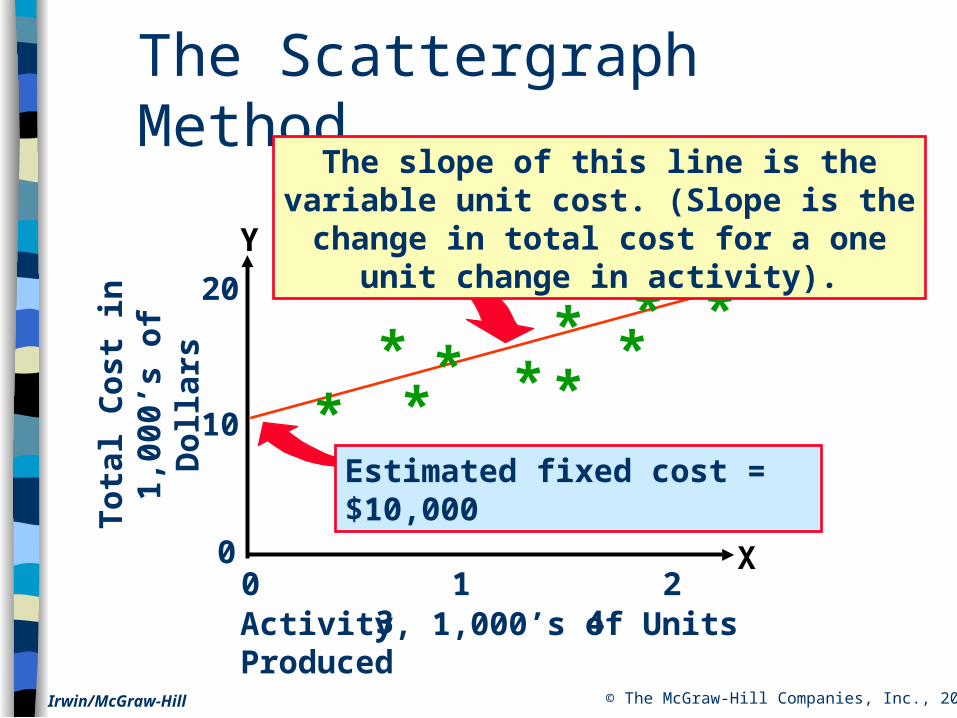

The Scattergraph Method

Estimated fixed cost = $10,000

0 1 2 3 4

*

To

tal

Co

st i

n1,

000’

s o

f D

oll

ars

10

20

0

***

**

**

*

*

Activity, 1,000’s of Units Produced

X

Y

The slope of this line is the variable unit cost. (Slope is the change in total cost

for a one unit change in activity).

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

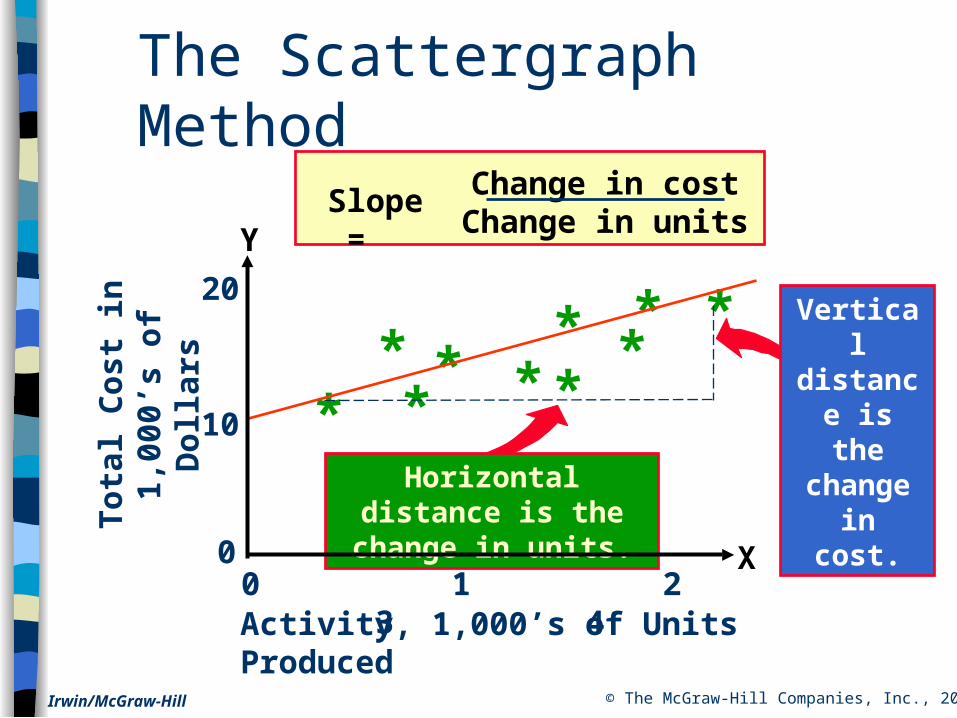

The Scattergraph Method

Slope = Change in costChange in units

Horizontal distance is the change in units.

0 1 2 3 4

*

To

tal

Co

st i

n1,

000’

s o

f D

oll

ars

10

20

0

***

**

**

*

*

Activity, 1,000’s of Units Produced

X

Y

Vertical distance

is the change in cost.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Accountants and managers may use computer software to fit a regression line through the data points.

The cost analysis objective is the same: Y = a + bx

Least-Squares Regression Method

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Least Squares Regression in Excel

Enter y-values in one columnEnter x-values in adjoining columnUse the Function button to compute the slope and intercept of the best-fitting line between the points.

For the statistical functions labeled Slope and Intercept, enter the required information in the dialogue boxes. Use the “Help” for instructions.

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

Let’s put our

knowledge of cost

behavior to work by

preparing a

contribution format

income statement.

The Contribution Format

© The McGraw-Hill Companies, Inc., 2000Irwin/McGraw-Hill

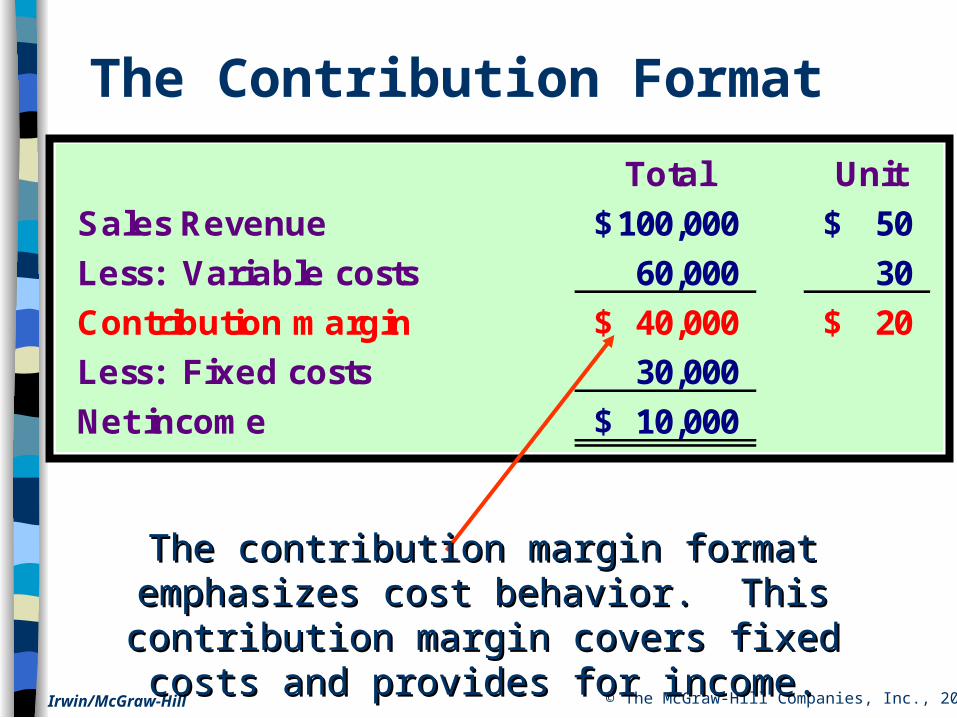

The Contribution Format

Total Unit

Sales Revenue 100,000$ 50$

Less: Variable costs 60,000 30

Contribution margin 40,000$ 20$

Less: Fixed costs 30,000

Net income 10,000$

The contribution margin format emphasizes cost The contribution margin format emphasizes cost behavior. This contribution margin covers fixed behavior. This contribution margin covers fixed

costs and provides for income.costs and provides for income.