Embed Size (px)

Citation preview

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

Aidan MurphyAidan MurphyShell International - LondonShell International - London

Investing in a carbon constrained future. Investing in a carbon constrained future.

WEC Gold Medal Colloquium

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

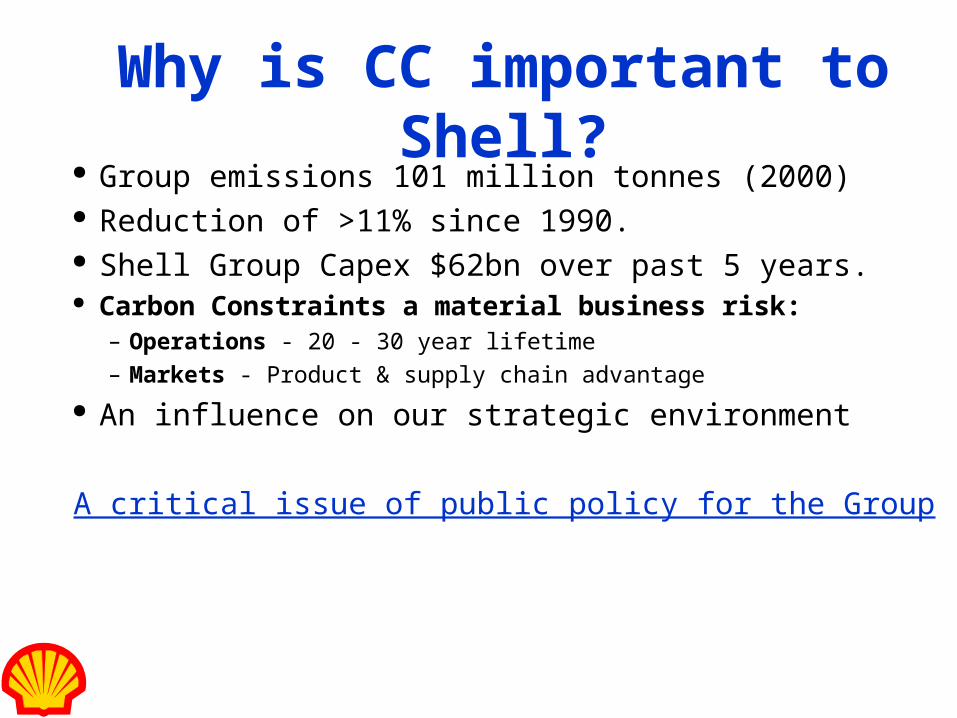

Why is CC important to Shell?

Group emissions 101 million tonnes (2000) Reduction of >11% since 1990. Shell Group Capex $62bn over past 5 years. Carbon Constraints a material business risk:

– Operations - 20 - 30 year lifetime– Markets - Product & supply chain advantage

An influence on our strategic environment

A critical issue of public policy for the Group

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

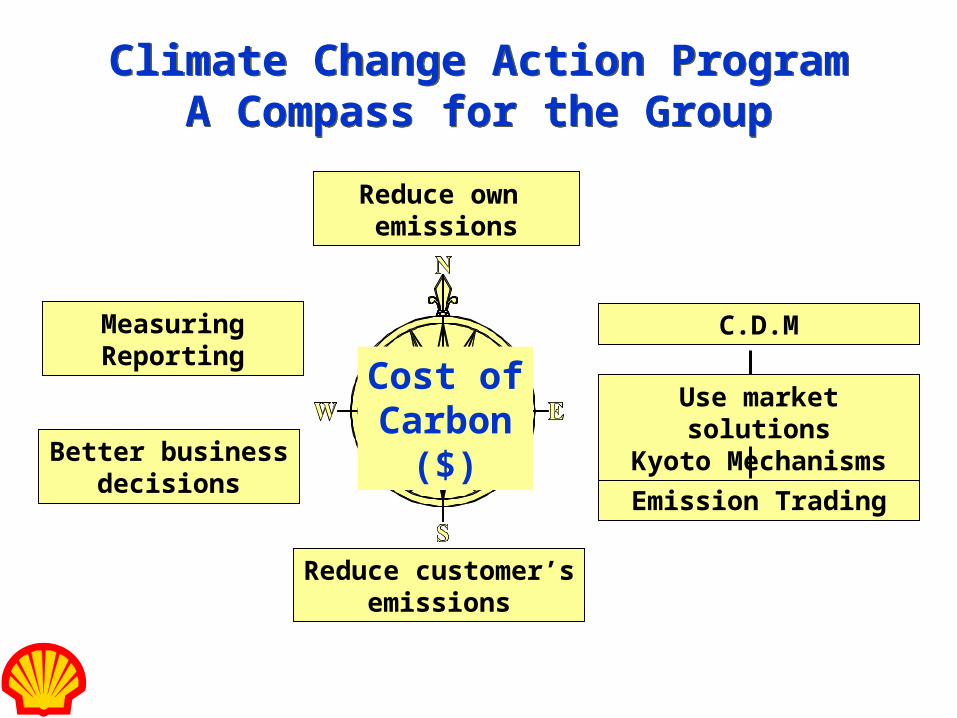

Climate Change Action ProgramA Compass for the Group

Climate Change Action ProgramA Compass for the Group

Cost ofCarbon

($)

Reduce own emissions

Reduce customer’semissions

Emission Trading

Better businessdecisions

MeasuringReporting

Use market solutions

Kyoto Mechanisms

C.D.M

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

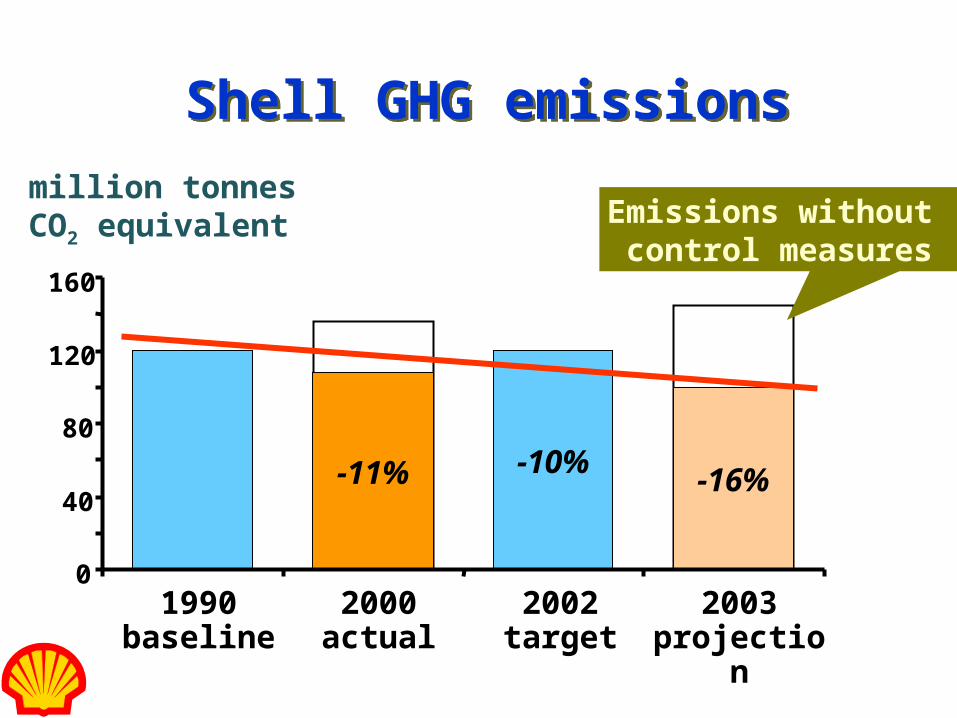

Shell GHG emissionsShell GHG emissions

-11% -10%-16%

0

40

80

120

160

1990 baseline

2000 actual

2002 target

2003 projection

million tonnesCO2 equivalent Emissions without

control measures

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

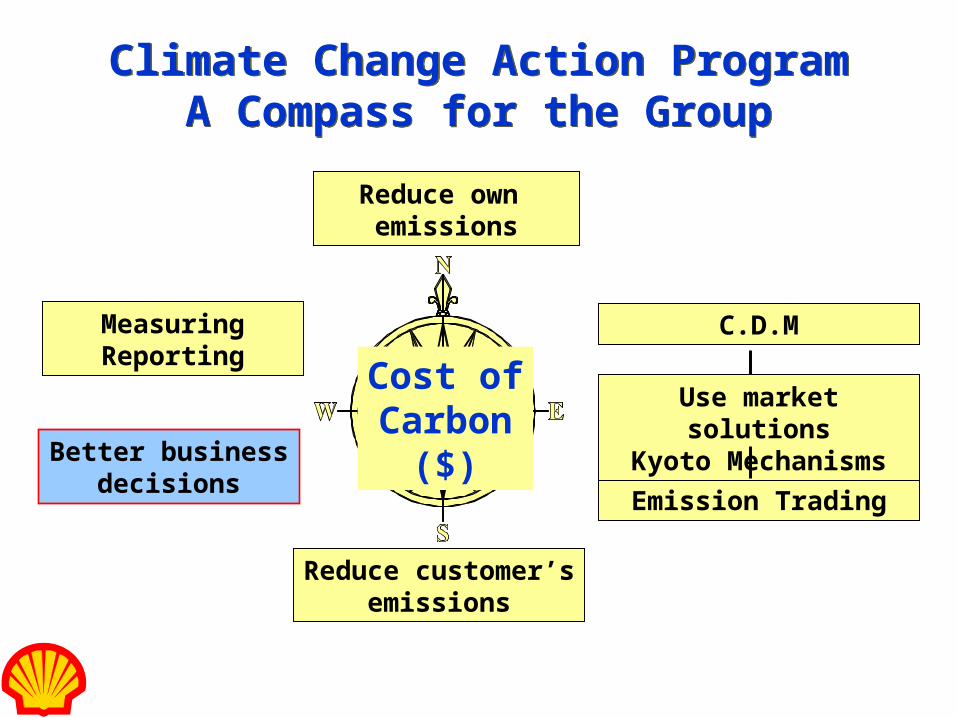

Climate Change Action ProgramA Compass for the Group

Climate Change Action ProgramA Compass for the Group

Cost ofCarbon

($)

Reduce own emissions

Reduce customer’semissions

Emission Trading

Better businessdecisions

MeasuringReporting

Use market solutions

Kyoto Mechanisms

C.D.M

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

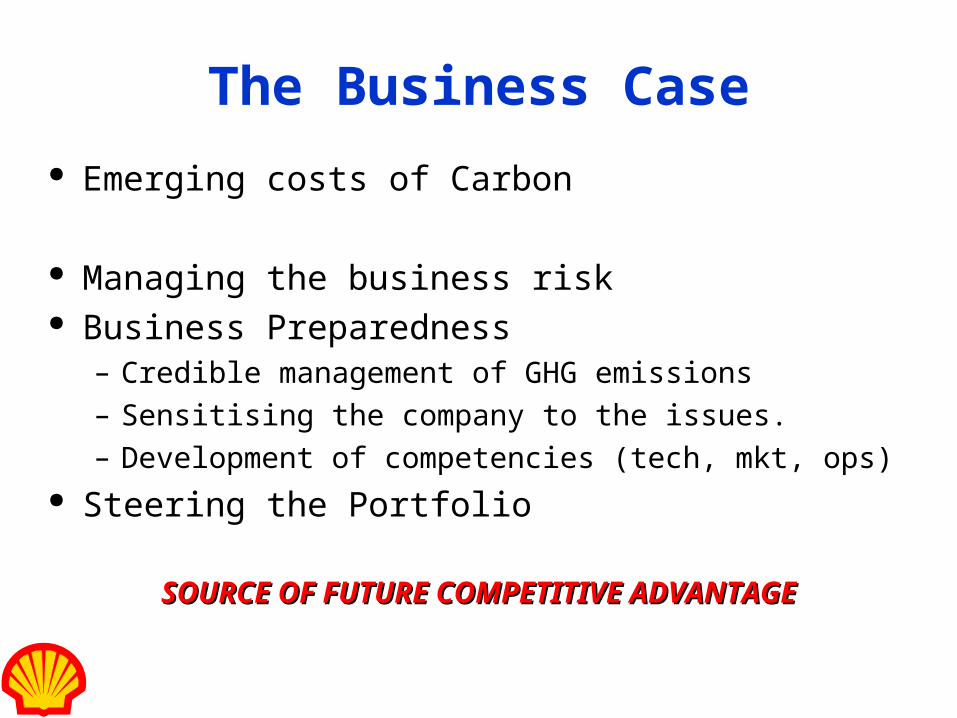

The Business Case

Emerging costs of Carbon

Managing the business risk Business Preparedness

– Credible management of GHG emissions– Sensitising the company to the issues.– Development of competencies (tech, mkt, ops)

Steering the Portfolio

SOURCE OF FUTURE COMPETITIVE ADVANTAGESOURCE OF FUTURE COMPETITIVE ADVANTAGE

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

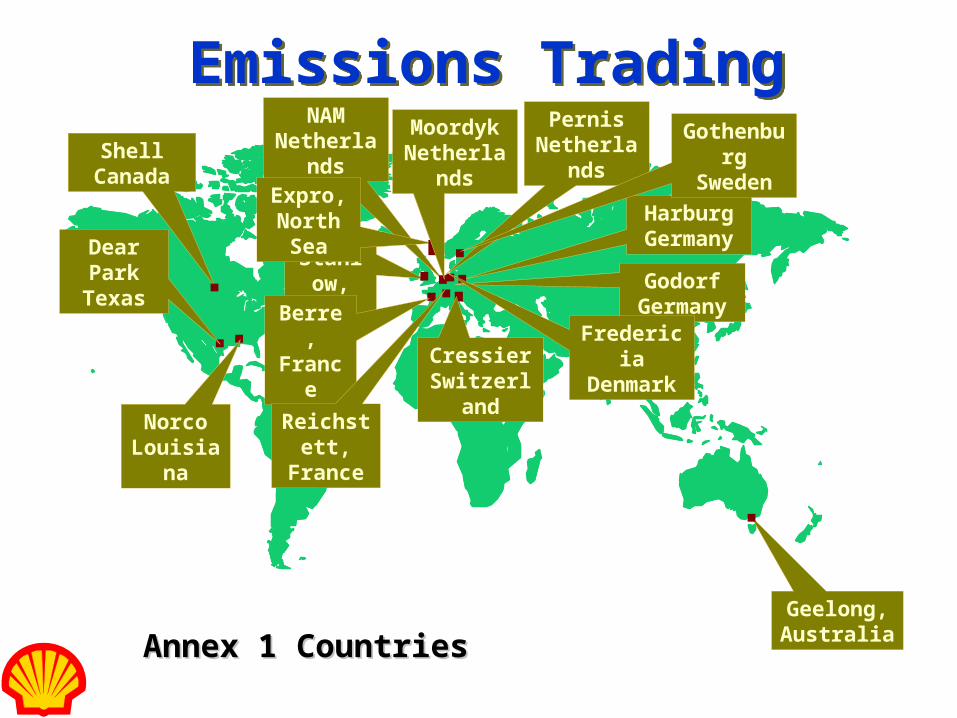

Emissions TradingEmissions Trading

Geelong,Australia

NAMNetherlands

Stanlow,UK

Dear ParkTexas

Expro,North Sea

MoordykNetherlands

Berre,France

NorcoLouisiana

CressierSwitzerland

Annex 1 CountriesAnnex 1 Countries

Shell Canada

PernisNetherlands

GodorfGermany

HarburgGermany

GothenburgSweden

Reichstett,France

FredericiaDenmark

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

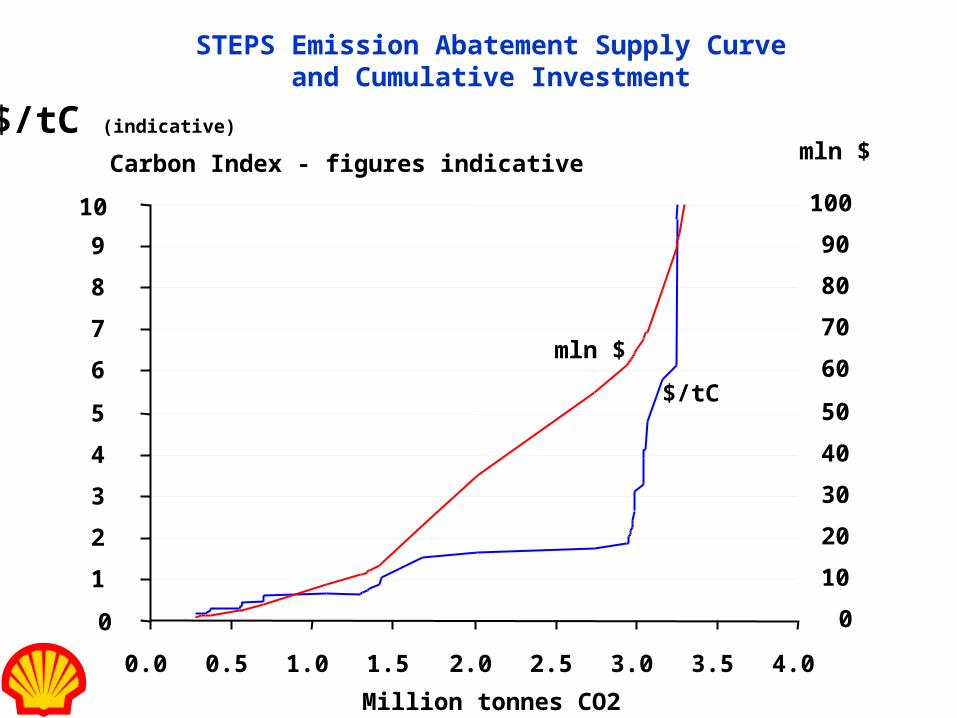

STEPS Emission Abatement Supply Curveand Cumulative Investment

Million tonnes CO2

$/tC (indicative)

mln $

$/tC

mln $

0

1

2

3

4

5

6

7

8

9

10

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

0

10

20

30

40

50

60

70

80

90

100

Carbon Index - figures indicative

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

Current Range of Carbon Cost Estimates

+ NPV

0

100

200+

US$/tonne Carbon

10

20

30

40

50

New build CCGT, ind. cogen.

Selected En.Efficiency

NAM in 2008, NAM in 2008,

Recent Trades*Recent Trades*

0

1

2

3

4

5

6

10

2025

Shell Shell Annex 1 Annex 1 (1st (1st est.)est.)

UK Carbon UK Carbon LevyLevy

NAM todayNAM today

Add’l US$/ boe

Coal to Gas Coal to Gas fuel switching fuel switching (existing capacity)(existing capacity) Micro Micro

Economic Economic StudiesStudies

IPCC, World IPCC, World BankBank

Coal to wind Coal to wind

UK Car LevyUK Car Levy

Current Current Quality Quality OffsetsOffsets

Macro Economic Macro Economic StudiesStudies

OECD, APIOECD, API

Danish LevyDanish Levy

Norway onshoreNorway onshore

Sweden & Sweden & Norway offshoreNorway offshore

Examples

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

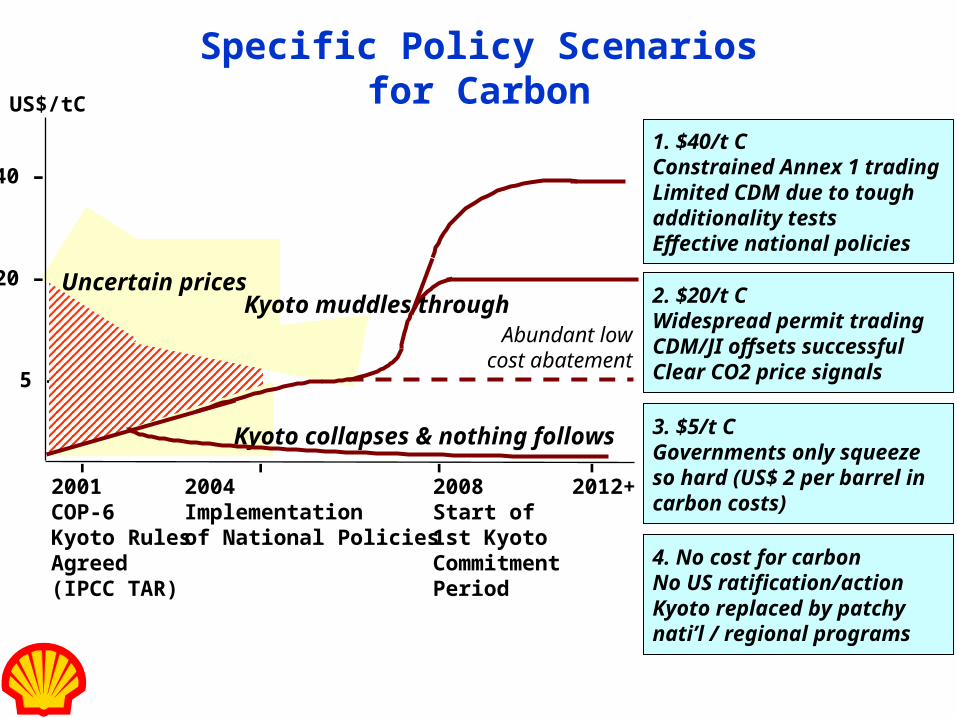

Specific Policy Scenariosfor Carbon

1. $40/t CConstrained Annex 1 tradingLimited CDM due to toughadditionality testsEffective national policies

2. $20/t CWidespread permit tradingCDM/JI offsets successfulClear CO2 price signals

3. $5/t CGovernments only squeezeso hard (US$ 2 per barrel incarbon costs)

4. No cost for carbonNo US ratification/actionKyoto replaced by patchynati’l / regional programs

US$/tC

40 –

20 –

5 –

2001COP-6Kyoto RulesAgreed(IPCC TAR)

2004Implementationof National Policies

2008Start of1st KyotoCommitmentPeriod

2012+

––––

Uncertain pricesKyoto muddles through

Kyoto collapses & nothing follows

Abundant lowcost abatement

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

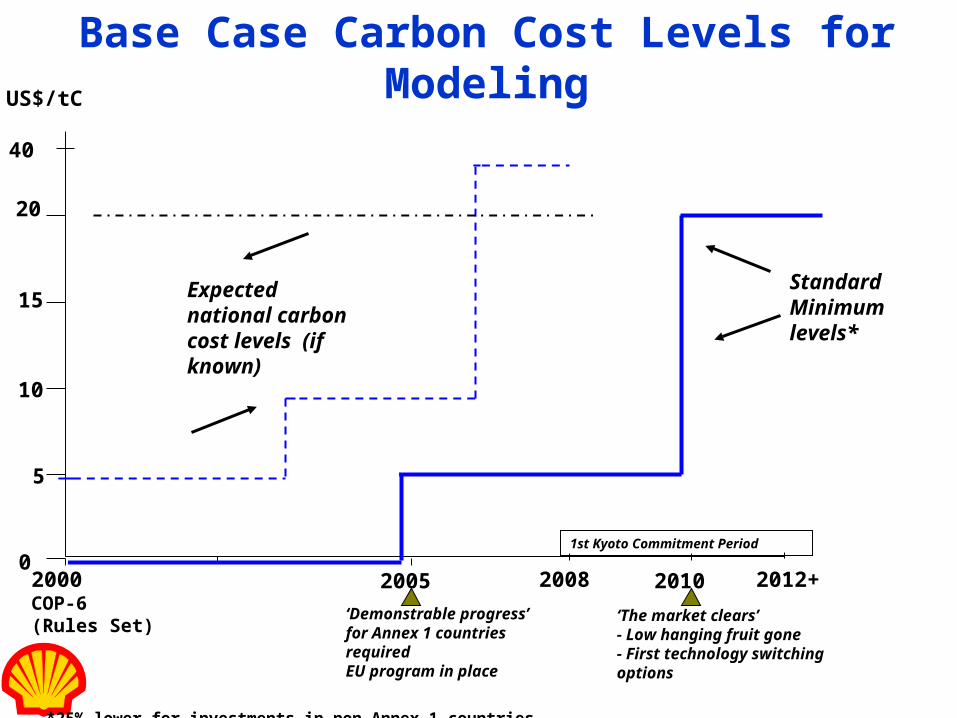

Base Case Carbon Cost Levels for Modeling

*25% lower for investments in non-Annex 1 countries.

2000COP-6(Rules Set)

2008 2010

20

5

US$/tC

2012+

1st Kyoto Commitment Period

2005

‘Demonstrable progress’ for Annex 1 countries requiredEU program in place

0

10

15Standard Minimum levels*

Expected national carbon cost levels (if known)

‘The market clears’- Low hanging fruit gone - First technology switching options

40

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

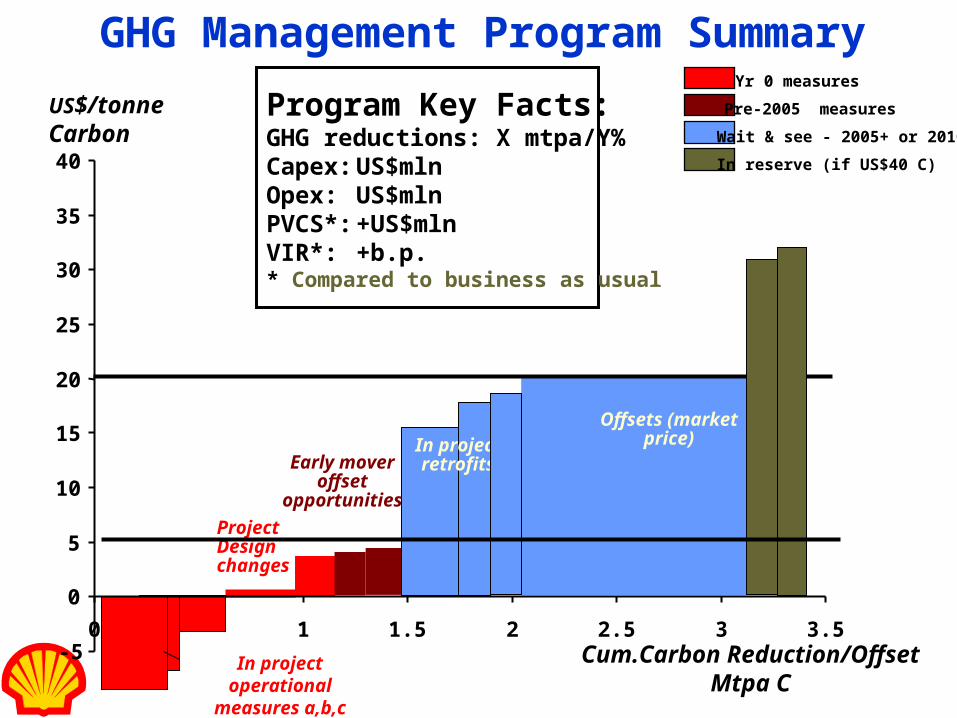

GHG Management Program Summary

-5

0

5

10

15

20

25

30

35

40

0 1 1.5 2 2.5 3 3.5Cum.Carbon Reduction/Offset

Mtpa C

Project Design changes

US$/tonne Carbon

Early mover offset

opportunities

In project operational

measures a,b,c

eg. Alternative

Energy

Offsets (market price)

Program Key Facts:GHG reductions: X mtpa/Y%Capex: US$mln Opex: US$mlnPVCS*: +US$mlnVIR*: +b.p.* Compared to business as usual

Yr 0 measures

Pre-2005 measures

Wait & see - 2005+ or 2010+

In reserve (if US$40 C)

In project retrofits

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

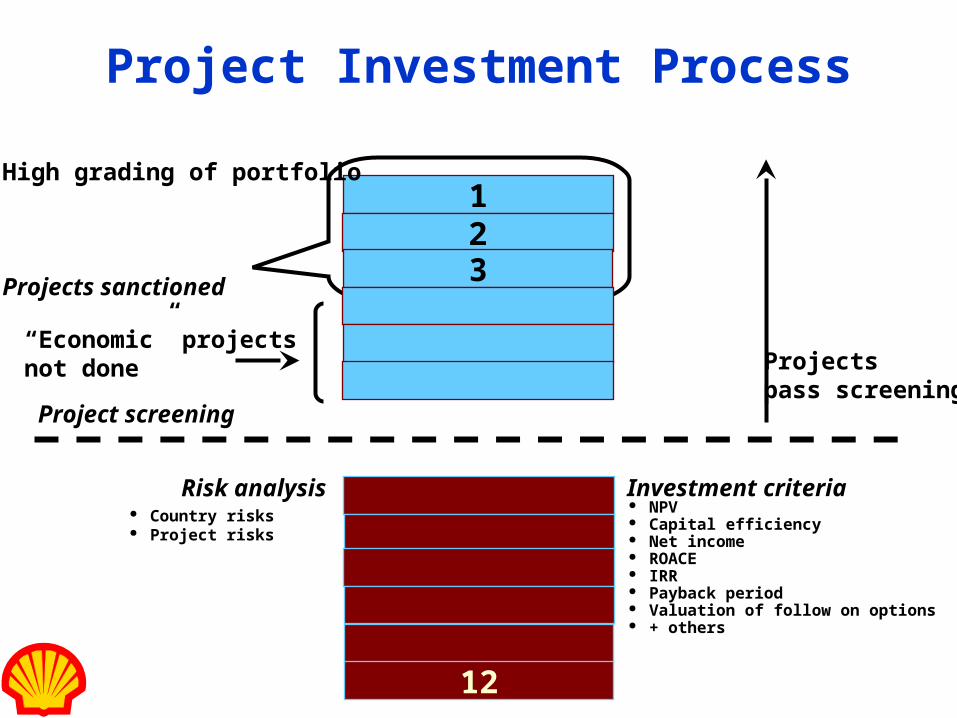

Country risks Project risks

Project Investment Process

Investment criteria NPV Capital efficiency Net income ROACE IRR Payback period Valuation of follow on options + others

Project screening

123

12

High grading of portfolio

Projects sanctioned

“Economic” projectsnot done

Risk analysis

Projectspass screening

Project investment options

cost of carbon 0699PPT A. MURPHY– CLIMATE CHANGE

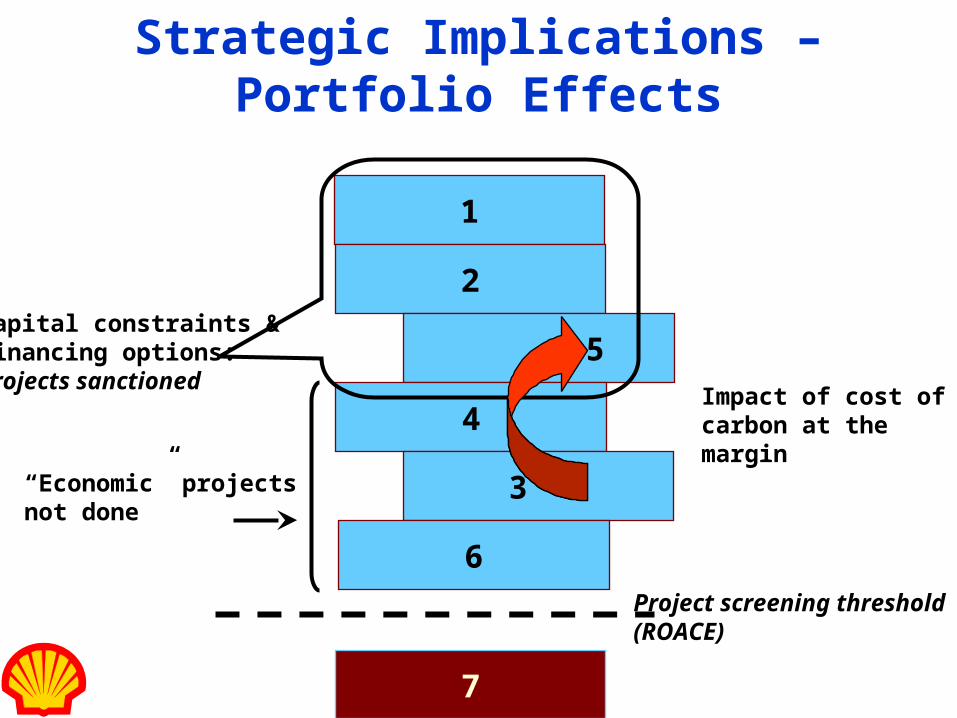

Strategic Implications – Portfolio Effects

1

2

5

4

3

6

7

Capital constraints &financing options:projects sanctioned

“Economic” projectsnot done

Impact of cost ofcarbon at themargin

Project screening threshold(ROACE)

![Wec Pwc Report[1]](https://img.pdfslide.net/doc/110x75/577d21341a28ab4e1e94b091/wec-pwc-report1.jpg)