Embed Size (px)

Citation preview

Cost-of-Living Clauses in Union Contracts: Determinants and EffectsAuthor(s): Wallace E. Hendricks and Lawrence M. KahnSource: Industrial and Labor Relations Review, Vol. 36, No. 3 (Apr., 1983), pp. 447-460Published by: Cornell University, School of Industrial & Labor RelationsStable URL: http://www.jstor.org/stable/2523022 .

Accessed: 24/06/2014 20:08

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Cornell University, School of Industrial & Labor Relations is collaborating with JSTOR to digitize, preserveand extend access to Industrial and Labor Relations Review.

http://www.jstor.org

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES IN UNION CONTRACTS: DETERMINANTS AND EFFECTS

WALLACE E. HENDRICKS and LAWRENCE M. KAHN*

This study investigates, for the period 1969- 81, the determinants of the in- cidence and strength of cost-of-living adjustment (COLA) clauses in U.S. manufacturing and the effect of those clauses on wage inflation. The sample includes approximately 5,570 union contracts in over 2,600 bargaining relationships. The authors find that both union bargaining power and infla- tion uncertainty positively affected the probability that a COLA clause was adopted as well as the strength of the clause adopted. Negatively influencing the incidence and strength of COLA clauses during the period studied were unanticipated changes in an industry's prices. The authors also find evidence that wage inflation was greater under contracts with uncapped COLAs than under all other contracts, a result that also was positively influenced by the amount of unanticipated inflation. From these results, the authors suggest a number of possible trends in the use and effects of COLA clauses.

MANY observers believe that the increase in coverage by cost-of-living-adjust-

ment (COLA) clauses during the 1970s has made it more difficult to reduce the rate of inflation through government policies. Some authors have suggested, for example, that shocks in prices, such as OPEC's in- creases in oil prices, are transmitted through COLAs to the wage structure, causing a further transmittal of the original price

*The authors are, respectively, Professor and Associate Professor of Economics and Labor and In- dustrial Relations at the University of Illinois at Urbana-Champaign. This research was funded in part by the University's Graduate College Research Board and the Institute of Labor and Industrial Relations, University of Illinois at Urbana-Champaign and by a U.S. Department of Labor contract. The authors are in- debted to Henry S. Farber and Peter Feuille for helpful comments.

inflation.' Indeed, the Carter administra- tion, in designing voluntary wage guide- lines, attempted to restrain this transmittal effect of COLAs. Specifically, due to the acceleration of inflation in 1979, the ad- ministration ruled in October of that year that workers without COLAs could be in compliance with the guidelines and receive 8 percent increases in compensation rather than the 7 percent (exclusive of COLA) in- creases allowed those with COLAs.2 This

'See H. M. Douty, "Study of the Relationships Between Cost of Living Escalation Clauses and Infla- tion," working paper prepared for the Council on Wage and Price Stability (Washington, D.C.: COWPS, 1975) and D. Quinn Mills, Labor-Management Rela- tions (New York: McGraw-Hill, 1978), p. 227.

2See George Ruben, "Industrial Relations in 1979: Inflation Still Holds the Spotlight," Monthly Labor Review, Vol. 103, No. 2 (February 1980), pp. 11- 18.

Industrial and Labor Relations Review, Vol. 36, No. 3 (April 1983). ? 1983 by Cornell University. 0019-7939/83/3603 $01.00

447

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

448 INDISTRIAL AND LABOR RELATIONS REVIEW

negative view of the impact of COLA clauses concentrates on only one side of the picture, of course, since COLAs can pre- sumably reinforce an unexpected decelera- tion of price inflation through the same mechanism.

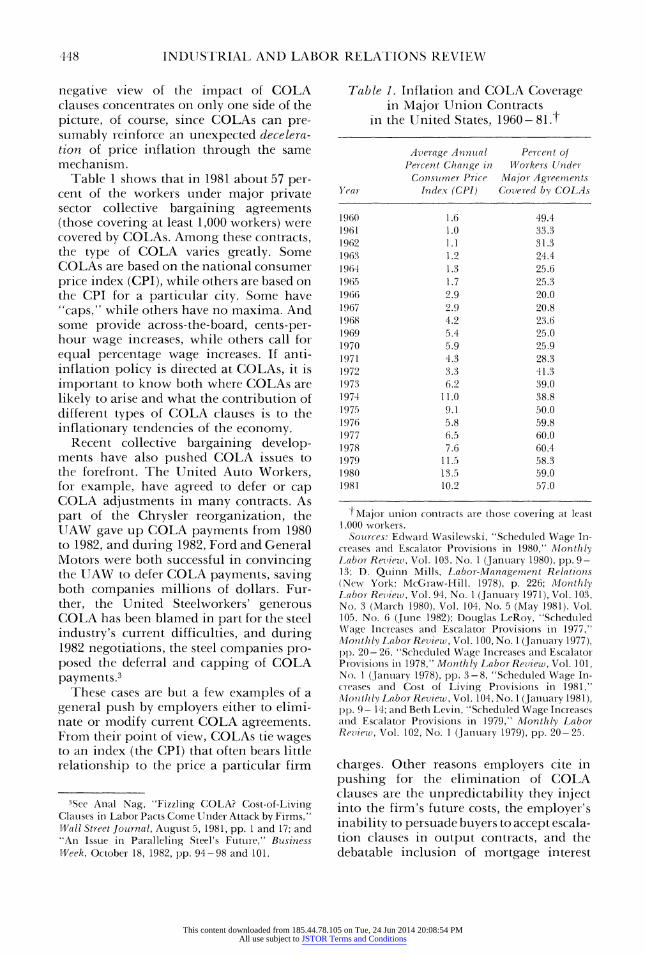

Table 1 shows that in 1981 about 57 per- cent of the workers under major private sector collective bargaining agreements (those covering at least 1,000 workers) were covered by COLAs. Among these contracts, the type of COLA varies greatly. Some COLAs are based on the national consumer price index (CPI), while others are based on the CPI for a particular city. Some have "caps," while others have no maxima. And some provide across-the-board, cents-per- hour wage increases, while others call for equal percentage wage increases. If anti- inflation policy is directed at COLAs, it is important to know both where COLAs are likely to arise and what the contribution of different types of COLA clauses is to the inflationary tendencies of the economy.

Recent collective bargaining develop- ments have also pushed COLA issues to the forefront. The United Auto Workers, for example, have agreed to defer or cap COLA adjustments in many contracts. As part of the Chrysler reorganization, the UAW gave up COLA payments from 1980 to 1982, and during 1982, Ford and General Motors were both successful in convincing the UAW to defer COLA payments, saving both companies millions of dollars. Fur- ther, the United Steelworkers' generous COLA has been blamed in part for the steel industry's current difficulties, and during 1982 negotiations, the steel companies pro- posed the deferral and capping of COLA payments.3

These cases are but a few examples of a general push by employers either to elirmi- nate or modify current COLA agreements. From their point of view, COLAs tie wages to an index (the CPI) that often bears little relationship to the price a particular firm

'See Anal Nag, "Fizzling COLA? Cost-of-Living Clauses in Labor Pacts Come Under Attack by Firms," W4all Street Journal, August 5, 1981, pp. 1 and 17; and "An Issue in Paralleling Steel's Future," Business Week, October 18, 1982, pp 94-98 and 101.

Table 1. Inflation and COLA Coverage in Major Union Contracts

in the United States, 1960-81.t

Average Amnm ila Perce t of Percent Chlange in. Workers Under Consn nmer Price Mlajor Agreements

Year Index (CPI) Covered bit COLAs

1960 1.6 49.4 1961 1.0 33.3 1962 1.1 31.3 1963 1.2 24.4 1964 1.3 25.6 1965 1.7 25.3 1966 2.9 20.0 1967 9.9 20.8 1968 4.2 23.6 1969 5.4 25.0 1970 5.9 25.9 1971 4.3 28.3 1972 3.3 41.3 1973 6.2 39.0 1974 11.0 38.8 1975 9.1 50.0 1976 5.8 59.8 1977 6.5 60.0 1978 7.6 60.4 1979 11.5 58.3 1980 13.5 59.0 1981 10.2 57.0

tMajor union contracts are those covering at least 1,000 workers.

Sources: Edward Wasilewski, "Scheduled Wage In- creases and Escalator Provisions in 1980," Monthly Labor Review, Vol. 103, No. 1 (January 1980), pp. 9- 13; D. Quinn Mills, Labor-Management Relations (New York: McGraw-Hill, 1978), p. 226; Monthlly Labor Review), Vol. 94, No. 1 (January 1971), Vol. 103, No. 3 (March 1980), Vol. 104, No. 5 (May 1981), Vol. 105, No. 6 (June 1982); Douglas LeRoy, "Scheduled Wage Increases and Escalator Provisions in 1977," Mlontly Labor Review, Vol. 100, No. 1 (January 1977), pp 209- 26, "Scheduled Wage Increases and Escalator Provisions in 1978," Monthlly Labor Review, Vol. 101, No. 1 (January 1978), pp. 3-8, "Scheduled Wage In- creases and Cost of Living Provisions in 1981," AlIontltly Labor Review, Vol. 104, No. 1 (January 1981), pmP 9- 14; and Beth Levin, "Scheduled Wage Increases and Escalator Provisions in 1979," Monthlty Labor Review, Vol. 102, No. 1 (January 1979), pp. 20-25.

charges. Other reasons employers cite in pushing for the elimination of COLA clauses are the unpredictability they inject into the firm's future costs, the employer's inability to persuade buyers to accept escala- tion clauses in output contracts, and the debatable inclusion of mortgage interest

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 449

in the CPI. From the worker's point of view, however, COLAs that index wages to the CPI serve to insulate real wages from un- anticipated price changes, without the con- tinuous renegotiation of contracts. For example, Edward Ayoub, the chief econo- mist for the steelworkers, recently said of the steel companies' request for concessions on COLA, "I don't know what alternatives the companies have in mind, but as far as we're concerned, COLA is a fundamental protection against inflation."4

A study of the determinants of COLA coverage can show which workers have the greatest desire for insulation of their real wages from price shocks, which workers have the greatest bargaining power to realize these desires, and which employers have the least to lose (or most to gain through re- duced fluctuations in real wages) by index- ing their workers' wages. Surprisingly, very little empirical evidence is available to ex- plain the behavior of unions and firms that leads to the establishment of COLA clauses. This paper is an attempt to fill that gap, by using 1969- 81 data on collective bargain- ing agreements in manufacturing industries to estimate the determinants and effects of COLA coverage.

Theoretical Considerations Several theoretical models have recently

been constructed to predict the determinants of wage indexation. These models identify the following factors as affecting the in- cidence and strength of COLAs.5 First, risk- averse workers will prefer to have their money wage levels indexed to price levels to avoid wide swings in their real wages. Sec- ond, increased uncertainty about future price changes tends to magnify this prefer-

'Nag, "Fizzling COLA?" p. 17. 5See, for example, Jo Anna Gray, "On Indexation

and Contract Length," Journal of Political Economy, Vol. 86, No. 1 (February 1978), pp. 1- 18; Costas Azariadis. "Escalation Clauses and the Allocation of Cyclical Risks," Journal of Economic Theory, Vol. 18, No. 1 (June 1978), pp. 119- 55; Ronald G. Ehrenberg, Leif Danziger, and Gee San, "Cost of Living Ad'just- merit Clauses in Union Contracts," unpublished mimeo (Ithaca, N.Y.: Cornell University, August 1982); Leif Danziger, "Uncertain Inflation and Wage Indexation,'' unpublished mimeo (Tel Aviv, Israel: Tel Aviv University, November 1981).

ence of workers for indexation. Third, firms' resistance to wage indexation will be in- fluenced by the degree to which product price changes and changes in other input prices are related to changes in the CPI. Fourth, higher negotiation costs or lower costs of administration of the CPI-based wage indexation will raise the likelihood and strength of indexation.6 Examples of higher negotiation costs include the time and resources necessary to reach agreement. Other negotiation costs might include the loss in product demand that may occur as buyers anticipate the possibility of a strike.

In the context of these models, the trade- off between negotiation costs and indexa- tion costs suggests a positive relationship between contract duration and indexation; that is, the gains from indexation (reduced variance of real wages) are greater the less frequently wages are contractually adjusted. This prediction is borne out by data for the United States: the proportions of one-, two-, and three-year major agreements having COLA clauses in 1978 were, respectively, 3 percent, 17 percent, and 71 percent. 7

Theoretical models that are based on models of efficient bargaining and that posit a constant level of risk aversion for workers also imply that union bargaining power is positively associated with both the inci- dence and magnitude of indexation.8 Even if the efficient-bargaining model is denied, greater union strength means a greater ability to impose costs on the employer if disagreement on an issue occurs. A strong union, for example, imposes high negotia- tion costs in the form of a more credible

6Ehrenberg, Danziger, and San in "Cost-of-Living Adjustment Clauses" imply that some of these pre- dictions become ambiguous if the optimal degree of indexation is greater than one, that is, if a one percent increase in prices raises wages by more than one per- cent. In the American context, however, such an out- come seems to be the exception (see below).

7See Victor Sheifer, "Cost of Living Adjustment: Keeping Up With Inflation?" Monthly Labor Review., Vol. 102, No. 6 (June 1979), pp. 14- 17.

8Ehrenberg, Danziger, and San in "Cost of Living Adjustment Clauses" include a measure of bargaining power, but they do not consider its implications. It is clear, however, that the derivative of both COLA incidence and strength with respect to bargaining power is positive.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

450 INDUSTRIAL AND LABOR RELATIONS REVIEW

strike threat. This phenomenon implies that stronger unions will have contracts that are of longer duration and more likely to contain a COLA clause than the contracts of weaker unions. Indeed, in the United States, wage indexation is almost exclu- sively a union phenomenon, and among one-year union contracts, as shown above, there are virtually no COLAs.

Some observers believe, however, that relative risk aversion is not constant but declines with income or assets.9 It seems unlikely that the demand for indexation declines with income, for that would mean that real wage insurance is an inferior good. More likely, the proportion of total com- pensation that is indexed might fall as com- pensation increases. Union power would thus have an unambiguous positive impact on the incidence of indexation, but the im- pact on the magnitude of indexation would be ambiguous, if relative risk aversion is not constant.

Of these opposing effects of union bar- gaining power on indexation, we believe, on empirical grounds, that a prediction of a positive effect is warranted in today's econ- omy. Originally, unions were opposed to wage indexation, in part because decreases in prices could lead to cuts in wage levels. In fact, indexation under the original UAW- GM contract did lead to wage reductions in 1949 and 1950. Since that time, almost all indexation formulas have precluded wage cuts. The asymmetry tends to bias indexa- tion in labor's favor.

In addition, wage indexation is a phe- nomenon almost exclusively associated with unions and occurs only rarely in short- term contracts. This suggests that the costs of wage setting are low enough to obviate any need for COLAs in the nonunion sector and in short-term union contracts. Strong unions impose a credible strike threat and thus raise the firm's desire for long-term contracts- to guarantee labor peace. Wage indexation may be the price that must be paid for these long-term contracts.

9Costas Azariadis, "Implicit Contracts and Under- employment Equilibria," Journal of Political Econ- omy, Vol. 83, No. 6 (December 1975), pp. 1183-202.

Data and Estimating Equations

The determinants of COLA coverage and of the degree of indexation were esti- mated for this analysis using the U.S. Bu- reau of Labor Statistics (BLS) tape on the characteristics of collective bargaining agreements in manufacturing during the year 1975. The sample is restricted to manu- facturing because most of the industry vari- ables used in this study are unavailable for nonmanufacturing industries. Neverthe- less, our sample does include contracts cov- ering fewer than 1,000 workers (as well as major agreements), allowing substantial variation in bargaining-unit size.

The BLS tape data were augmented in two ways. First, since the BLS tape pro- vides four-digit industry data, a variety of industry and demographic characteristics associated with each four-digit (in some cases, three-digit) industry were assigned to each contract.'0 Second, although the BLS data do not include information on wages or the size of COLA adjustments, the con- tracts themselves are on file at the U.S. De- partment of Labor. Wage-level data for janitors and laborers (a relatively homo- geneous set of occupations in terms of skills) as well as data on the size of COLA adjust- ments were collected directly from the con- tracts.11 In addition, wage changes and COLA information were gathered from various issues of the Daily Labor Report. These data were matched to the BLS tape using the BLS contract number for each agreement. These supplementary data per- mit the construction of the dependent vari- ables of this study, allowing for a total sam- ple of 5,570 contracts in 2,639 collective bargaining relationships.

The basic determinants of COLA cover- age and the degree of indexation given a COLA are accounted for in the following

"0See the appendix for data sources. The reader should be cautioned that an error-in-variables problem exists to the extent that the BLS has incorrectly classi- fied the industries.

"The authors are grateful to Debashish Bhatta- cherjee, Andrew Bruns, Cynthia Gramm, Steve Mer- kin, Christopher Pawlowicz, Ronald Seeber, and Roger Wolters for assistance in collecting and as- sembling the data.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 451

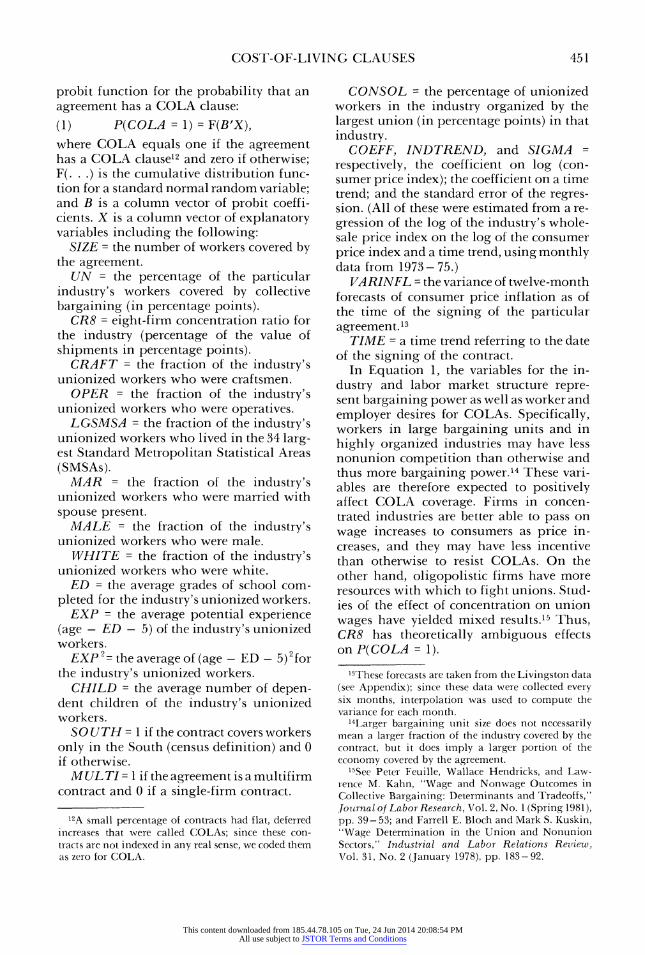

probit function for the probability that an agreement has a COLA clause: (1) P(COLA = 1) = F(B'X), where COLA equals one if the agreement has a COLA clausel2 and zero if otherwise; F(. . .) is the cumulative distribution func- tion for a standard normal random variable; and B is a column vector of probit coeffi- cients. X is a column vector of explanatory variables including the following:

SIZE = the number of workers covered by the agreement.

UN = the percentage of the particular industry's workers covered by collective bargaining (in percentage points).

CR8 = eight-firm concentration ratio for the industry (percentage of the value of shipments in percentage points).

CRAFT = the fraction of the industry's unionized workers who were craftsmen.

OPER = the fraction of the industry's unionized workers who were operatives.

LGSMSA = the fraction of the industry's unionized workers who lived in the 34 larg- est Standard Metropolitan Statistical Areas (SMSAs).

MAR = the fraction of the industry's unionized workers who were married with spouse present.

MALE = the fraction of the industry's unionized workers who were male.

WHITE = the fraction of the industry's unionized workers who were white.

ED = the average grades of school com- pleted for the industry's unionized workers.

EXP = the average potential experience (age - ED - 5) of the industry's unionized workers.

EXP2= the average of (age - ED - 5) 2 for the industry's unionized workers.

CHILD = the average number of depen- dent children of the industry's unionized workers.

SOUTH = 1 if the contract covers workers only in the South (census definition) and 0 if otherwise.

MULTI = 1 if the agreement is a multifirm contract and 0 if a single-firm contract.

l2A small percentage of contracts had flat, deferred increases that were called COLAs; since these con- tracts are not indexed in any real sense, we coded them as zero for COLA.

CONSOL = the percentage of unionized workers in the industry organized by the largest union (in percentage points) in that industry.

COEFF, INDTREND, and SIGMA = respectively, the coefficient on log (con- sumer price index); the coefficient on a time trend; and the standard error of the regres- sion. (All of these were estimated from a re- gression of the log of the industry's whole- sale price index on the log of the consumer price index and a time trend, using monthly data from 1973- 75.)

VARINFL = the variance of twelve-month forecasts of consumer price inflation as of the time of the signing of the particular agreement. 13

TIME = a time trend referring to the date of the signing of the contract.

In Equation 1, the variables for the in- dustry and labor market structure repre- sent bargaining power as well as worker and employer desires for COLAs. Specifically, workers in large bargaining units and in highly organized industries may have less nonunion competition than otherwise and thus more bargaining power.'4 These vari- ables are therefore expected to positively affect COLA coverage. Firms in concen- trated industries are better able to pass on wage increases to consumers as price in- creases, and they may have less incentive than otherwise to resist COLAs. On the other hand, oligopolistic firms have more resources with which to fight unions. Stud- ies of the effect of concentration on union wages have yielded mixed results.'5 Thus, CR8 has theoretically ambiguous effects on P(COLA = 1).

"3These forecasts are taken from the Livingston data (see Appendix); since these data were collected every six months, interpolation was used to compute the variance for each month.

"4Larger bargaining unit size does not necessarily mean a larger fraction of the industry covered by the contract, but it does imply a larger portion of the economy covered by the agreement.

"5See Peter Feuille, Wallace Hendricks, and Law- rence M. Kahn, "Wage and Nonwage Outcomes in Collective Bargaining: Determinants and Tradeoffs," journal of Labor Research, Vol. 2, No. 1 (Spring 1981), pp. 39-53; and Farrell E. Bloch and Mark S. Kuskin, "Wage Determination in the Union and Nonunion Sectors," Industrial and Labor Relations Review, Vol. 31, No. 2 (January 1978), pp. 183-92.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

459 INDUSTRIAL AND LABOR RELATIONS REVIEW

Finally, of the variables for labor market structure, CONSOL and MULTI are mea- sures of employer desires for COLAs. In- dexing introduces rigidities into the wage- setting process. Firms dealing with just one union (CONSOL) and companies with single-firm agreements (MULTI) will be better able than other companies to tolerate these rigidities.'6

The demographic variables (CRAFT, OPER, MAR, MALE, WHITE, ED, EXP, EXP", and CHILD) represent the effects of individual productivity characteristics and discrimination. These variables might therefore be expected to have the same effect on P(COLA = 1) as they have on wages. The variables MAR and CHILD may also be positively associated with workers' risk aversion and thus with their demand for indexation. Furthermore, more educated workers may be less risk averse than less educated workers. Location variables (SO UTH and LGSMSA ) are associated with union power, since unions are generally stronger in areas other than the South and in large cities.'7 Moreover, the CPI has less relevance outside large SMSAs, further suggesting a positive effect for LGSMSA.

"6It should be noted that MULTI and CONSOL may also be related to bargaining power, although these relationships are theoretically ambiguous. First, mul.tifirm contracts may take wages out of competi- tion and reduce the effective elasticity of demand for labor (compared to that under single-firm agree- ments), thus raising union power. On the other hand, multifirm contracts reduce unions' ability to wThipsaw employers. The evidence on the effect of mulltifirm contracts on wages is mixed. See Wallace Hendricks, "Labor Market Structure and Union Wage Levels," Economic Inquiry, Vol. 13, No. 3 (September 1975), pp. 401 - 16; Feuille, Hendricks, and Kahn, "Wage and Nonwage Outcomes," and Wallace Hen- ciricks and Lawrence M. Kahn, "The Demand for Labor Market Structure: An Economic Approach," unpublished mimeo (Champaign: University of Illinois, October 1982).

Second, CONSOL may be positively related to union power, since a higher value for CONSOL im- plies a greater union ability to present a united front to the employer. On the other hand, union rivalry may force union leaders to bargain more aggressively to impress their constituencies. Feuille, Hendricks, and Kahn in "Wage and Nonwage Outcomes" found an insignificant wage effect for this variable.

"7See Lloyd Reynolds, Labor Economics and Labor Relations, 8th ed. (Englewood Cliffs, N.J.: Prentice- Hall, 1982), pp. 319-41.

The variables COEFF, INDTREND, and SIGMA all refer to the behavior of the in- clustry's prices. COEFF is a measure of the responsiveness of the industry's price to the CPI; a higher value for this variable should reduce employer resistance to CO- LAs. INDTREND is a measure of the trend behavior of industry prices; industries with more rapidly rising prices, other things equal, should be less resistant to COLAs. Finally, SIGMA is a proxy for the unan- ticipated volatility of the industry's price and should, as discussed earlier, reduce the incidence of COLA clauses."8

VARINFL is intended to capture infla- tion uncertainty and is expected to increase the incidence of COLA clauses. The final variable is the time trend, TIME, which may pick up secular changes in the inci- dence of COLAs, as well as changes in the accuracy of BLS sampling of nonmajor agreements. Because of the possible biases induced by inaccurate sampling of the small agreements, we reestimated Equation 1 by restricting the sample to major contracts. The results for this reestimation did not differ from the earlier results, suggesting that this sampling bias is small.

The analysis includes no control for con- tract duration because its focus is the ulti- mate determinants of COLA coverage; and the theory of COLA clauses suggests that indexation and contract length are vari- ables chosen jointly.'9 Equation 1 is a re- duced form of this choice. The inclusion of contract duration in the equation produced a significant positive coefficient for this

"8David Estenson. in "Relative Price Variability and Indexed Labor Agreements," Industrial Rela- tioui.s, Vol. 20, No. 1 (Winter 1982), pp. 71-84, used 140 miajor rmanufactutring contracts to estimate the plrobability of a COLA clause. He used as explanatory variables the equivalent of COEFF and SIGMA in 48 two-digit industry price regressions, omitting a time trend. In constructing these two variables, we bave performed 193 four-digit industry price regres- slonis.

19See Gray, "On Indexation and Contract Length." The readler should be cautioned that many agreements appeat more than once in our sample (for example, the 1972, 1975, 1978, and 1981 contracts for a single relationship), suggesting the possibility of serial cor- relation and other problems related to the pooling of tin-e-serles and cross-section data.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 453

variable but did not affect the otherresults. Equation 1 distinguishes between con-

tracts with COLAs and those without CO- LAs. As the BLS contract data show, how- ever, there is considerable variety in the degree of indexation among contracts with COLAs. Our measure of the degree of index- ation is the share of cost-of-living payments in total wage increases (including COLA) over the life of the contract. A large value for this measure would therefore indicate a high degree of indexation. This measure is slightly different from another measure of indexation, the elasticity of wages with respect to prices.20

Because, in negotiations, trade-offs are made among indexing and other benefits, we have attempted to standardize the COLA by the size of the total wage increase. This procedure allows a closer focus on the nego- tiation-cost and risk factors that influence indexation, by examining the fraction of the total wage increase attributable to the COLA, rather than simply the level of the COLA. The following equation analyzes this issue:

(2) COLI(COL + 54C) = an + a'X + dPa + e,

where, for each contract with a COLA, COL equals the cost-of-living adjustment over the life of the contract; SWC equals the in- creases in straight-time pay other than COLA over the life of the contract; X is as defined above; Pa is the percent change in the CPI over the life of the agreement (not annualized); and e is an error term.

Similar explanatory variables (X) appear in Equations 1 and 2. Since the phenome- non being examined in the second equation is quite similar to that in the first, quali- tatively similar results are expected. More specifically, similar forces are likely to in- fluence both the incidence and the strength of COLA clauses.

We have added actual inflation over the life of the agreement as an explanatory vari- able, however, because although we are attempting to measure the parties' intended degree of indexation, our proxy consists in part of the realized COLA payments. The latter can be affected by the parties' inten-

20See Azariadis, "Escalator Clauses."

tions (such as capping the COLA) as well as by actual inflation.2' By controlling for actual inflation, we can focus on the parties' intentions: each of the other explanatory variables is viewed in Equation 9 as affect- ing the degree of indexation controlling for a given realized inflation rate. Two COLAs can give different yields at the same realized inflation rate only if the COLA clauses themselves differ.22

Empirical Results The percentage of contracts in our sample

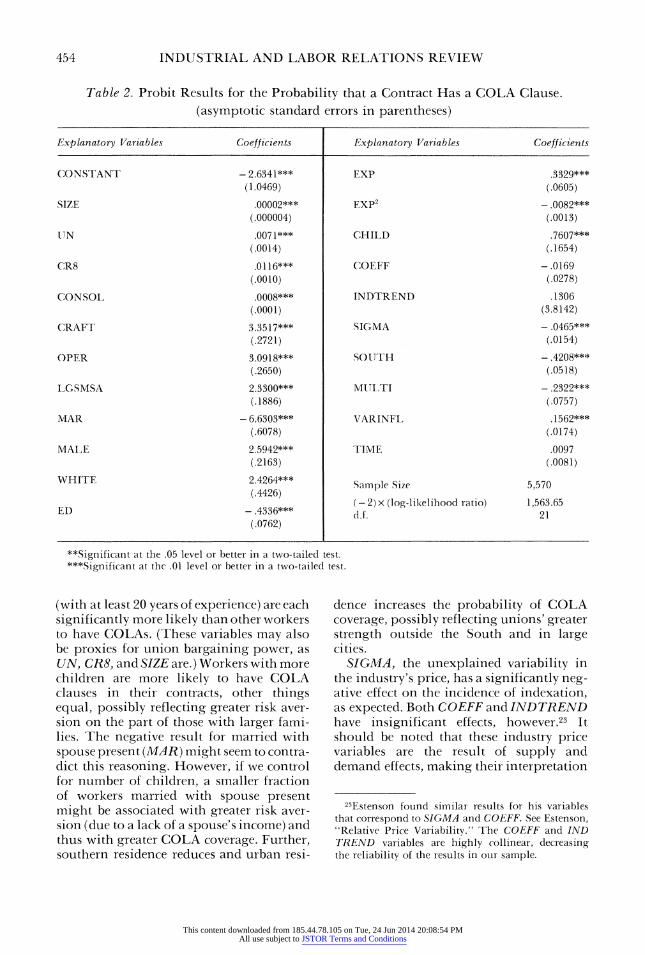

with COLAs is 45.6 percent, a figure some- what smaller than that shown in Table 1, which refers only to major agreements. This difference probably reflects the higher incidence of COLAs in large bargaining units (see below). The probit results for the probability that an agreement had a COLA are reported in Table 2.

Each of the bargaining-power proxy vari- ables (SIZE, UN, and CR8) has a significant, positive effect on COLA coverage. The SIZE result is consistent with the compari- son of COLA coverage among major agree- mnents (Table 1) and among our random sample of all contracts. In addition, single- firm bargaining and union concentration (CONSOL) both significantly raise the probability of COLA coverage (MULTI has a negative coefficient), as predicted. These results may reflect the difficulties that employer associations and groups of unions have in agreeing on a COLA pack- age acceptable to all.

The occupation and personal-charac- teristics coefficients generally have the ex- pected signs, with the exception of educa- tion, which is negative and significant, possibly reflecting a negative effect of educa- tion on risk aversion. Craftsmen, operatives, males, whites, and experienced workers

2IFor an attempt to proxy the parties' intentions in negotiating COLAs, see David Card, "Cost-of-Living Escalators in Major Union Contracts," forthcoming in Indtistrial atd Labor Relations Reviezw.

22The reader should again be cautioned about our1 pooling of time-series and cross-section data (see footnote 19). In addition, there may be a selectivity bias since the sample for Equation 2 is restricted to contracts wvith COLAs.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

454 INDUSTRIAL AND LABOR RELATIONS REVIEW

Table 2. Probit Results for the Probability that a Contract Has a COLA Clause. (asymptotic standard errors in parentheses)

Explanatory Variables Coefficients Explanatory Variables Coefficients

CONSTANT -2.6341*** EXP .3329*** (1.0469) (.0605)

SIZE .00002*** EXP2 -.0082*** (.000004) (.0013)

tTN .0071*** CHILD .7607*** (.0014) (.1654)

CR8 .0116*** COEFF -.0169 (.0010) (.0278)

CONSOL .0008*** INDTREND .1306 (.0001) (3.8142)

CRAFT 3.3517*** SIGMA -.0465*** (.2721) (.0154)

OPER 3.0918*** SOUTTH -.4208*** (.2650) (.0518)

LGSMSA 2.3300*** MULTI -.2322*** (.1886) (.0757)

MAR - 6.6303*** VARINFL .1562*** (.6078) (.0174)

MALE 2.5942*** TIME .0097 (.2163) (.0081)

WHITE 2.4264*** Sample Size 5,570 (.4426)

ED -.4426*** (- 2) x (log-likelihood ratio) 1,563.65 ED - .4336*** d.f. 21

(.0762)

**Significant at the .05 level or better in a two-tailed test. ***Significant at the .01 level or better in a two-tailed test.

(with at least 20 years of experience) are each significantly more likely than other workers to have COLAs. (These variables may also be proxies for union bargaining power, as UN, CR8, and SIZE are.) Workers with more children are more likely to have COLA clauses in their contracts, other things equal, possibly reflecting greater risk aver- sion on the part of those with larger fami- lies. The negative result for married with spouse present (MAR) might seem to contra- dict this reasoning. However, if we control for number of children, a smaller fraction of workers married with spouse present might be associated with greater risk aver- sion (due to a lack of a spouse's income) and thus with greater COLA coverage. Further, southern residence reduces and urban resi-

dence increases the probability of COLA coverage, possibly reflecting unions' greater strength outside the South and in large cities.

SIGMA, the unexplained variability in the industry's price, has a significantly neg- ative effect on the incidence of indexation, as expected. Both COEFF and INDTREND have insignificant effects, however.23 It should be noted that these industry price variables are the result of supply and demand effects, making their interpretation

23Estenson found similar results for his variables that correspond to SIGMA and COEFF. See Estenson, "Relative Price Variability." The COEFF and IND TREND variables are highly collinear, decreasing the reliability of the results in our sample.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 455

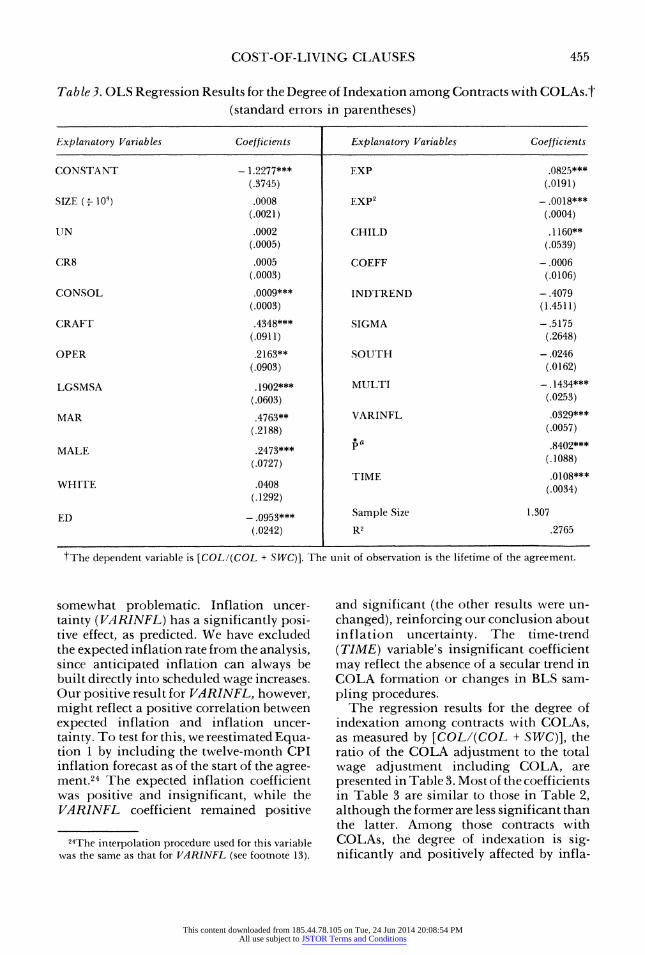

Table 3. OLS Regression Results for the Degree of Indexation among Contracts with COLAs.t (standard errors in parentheses)

Explanatory Variables Coefficients Explanatory Variables Coefficients

CONSTANT -1.2277*** EXP .0825*** (.3745) (.0191)

SIZE (- 104) .0008 EXp2 _.0018*** (.0021) (.0004)

UN .0002 CHILD .1160** (.0005) (.0539)

CR8 .0005 COEFF -.0006 (.0003) (.0106)

CONSOL .0009*** INDTREND -.4079 (.0003) (1.4511)

CRAFT .4348*** SIGMA -.5175 (.0911) (.2648)

OPER .2163** SOUTH -.0246 (.0903) (.0162)

LGSMSA .1902*** MULTI -. 1434*** (.0603) (.0253)

MAR .4763** VARINFL .0329*** (.2188) (.0057)

MALE .2473*** a .8402*** (.0727) (.1088)

TIME .0108*** WHITE .0408 (.0034)

(.1292)

ED -.0953*** Sample Size 1,307 (.0242) R2 .2765

tThe dependent variable is [COL/(COL + SWC)]. The unit of observation is the lifetime of the agreement.

somewhat problematic. Inflation uncer- tainty (VARINFL) has a significantly posi- tive effect, as predicted. We have excluded the expected inflation rate from the analysis, since anticipated inflation can always be built directly into scheduled wage increases. Our positive result for VARINFL, however, might reflect a positive correlation between expected inflation and inflation uncer- tainty. To test for this, we reestimated Equa- tion 1 by including the twelve-month CPI inflation forecast as of the start of the agree- ment.24 The expected inflation coefficient was positive and insignificant, while the VARINFL coefficient remained positive

24The interpolation procedure used for this variable was the same as that for VARINFL (see footnote 13).

and significant (the other results were un- changed), reinforcing our conclusion about inflation uncertainty. The time-trend (TIME) variable's insignificant coefficient may reflect the absence of a secular trend in COLA formation or changes in BLS sam- pling procedures.

The regression results for the degree of indexation among contracts with COLAs, as measured by [COL/(COL + SWC)], the ratio of the COLA adjustment to the total wage adjustment including COLA, are presented in Table 3. Most of the coefficients in Table 3 are similar to those in Table 2, although the former are less significant than the latter. Among those contracts with COLAs, the degree of indexation is sig- nificantly and positively affected by infla-

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

456 INDUSTRIAL AND LABOR RELATIONS REVIEW

tion uncertainty, the presence of a single- firm agreement, and union concentration, and significantly and negatively affected by industry price uncertainty. These effects are similar to those found in estimating the probability of a COLA. The result for marital status, however, conflicts with its estimated impact on COLA incidence. An overall conclusion about its effect on COLAs is thus difficult to make. Actual inflation has a strong, significantly positive effect on the degree of indexation, as would be true almost by definition.

Wage Effects of COLA Coverage Our focus up to now has been on esti-

mating the determinants of union and man- agement behavior with regard to COLAs. As discussed above, the effect of various types of COLAs on wage inflation is another issue of considerable policy importance. In par- ticular, special attention has been paid to uncapped COLAs (see above). In our sam- ple, about 35 percent of the contracts have uncapped COLAs, 10 percent have COLAs with a cap, and about 55 percent are unin- dexed. To investigate the determinants of wage inflation in our sample, we estimated the following regression for each year from 1972 to 1981:25

(3) In ( WAGEt )f o + f'Z + f ICAPt WA GEt -I + fJFREECOLAt + f3LENGTHt

+ f 4 MONTHSt + el, where

WA GEt = the hourly wage rate (including COLA and other deferred increases) for janitors or laborers at year t;

Z = a vector of explanatory variables in- cluding SIZE, UN, CR8, CRAFT, OPER, LGSMSA, MAR, MALE, WHITE, ED, EXP, EXP2 , CHILD, SOUTH, MULTI, CONSOL, and TIME;

LENGTHt = the duration of the current contract (number of months from start to finish);

MONTHSt = the number of months as of

25The availability of appropriate wage data con- strains the time periods for which wage inflation is estimated.

year t that the current contract has been in force;

CAPt 1 if in year t a given contract had a COLA clause with a formula linked to the CPI and with a maximum allowable in- crease, and 0 if otherwise;

FREECOLAt 1 if in year t a given con- tract had a COLA clause with a formula linked to the CPI and with no maximum increase, and 0 if otherwise; and

et is an error term. (For CAPt and FREECOLAt, the refer-

ence category is no COLA provision.) Equation 3 contains all of the explana-

tory variables in the first two equations, with the exception of SIGMA, COEFF, and INDTREND, whose effects are assumed to take place primarily through CAP and FREECOLA; inflation is also excluded from Equation 3, since we run a separate regression for each year. Furthermore, con- tract length is included in this equation. Although the earlier discussion suggested that CAP, FREECOLA, and LENGTH are endogenous, the identification problem in estimating Equation 3 using simultane- ous-equation methods is likely to be severe. Because of possible simultaneity bias, the following results should be interpreted cautiously. Finally, MONTHSt is included to capture the phenomenon of front-load- ing.

Table 4 displays least squares annual results for wage inflation. Contracts with uncapped COLAs yield significantly higher wage growth than unindexed agreements in every year except 1975 - 76. Agreements with capped COLAs have smaller and less significant effects than those found for FREECOLA contracts. Indeed, Table 4 shows that when Equation 3 is reestimated using pooled data with dummy variables for year, the pooled estimates yield highly sig- nificant coefficients for both variables, but only the FREECOLA effect of slightly over two percentage points is sizable relative to the overall average annual wage inflation in our sample of roughly 9 percent. The CAP and FREECOLA results are similar to those of Vroman, who did not, however, control for contract characteristics or demo- graphic and industry variables (except prof-

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 457

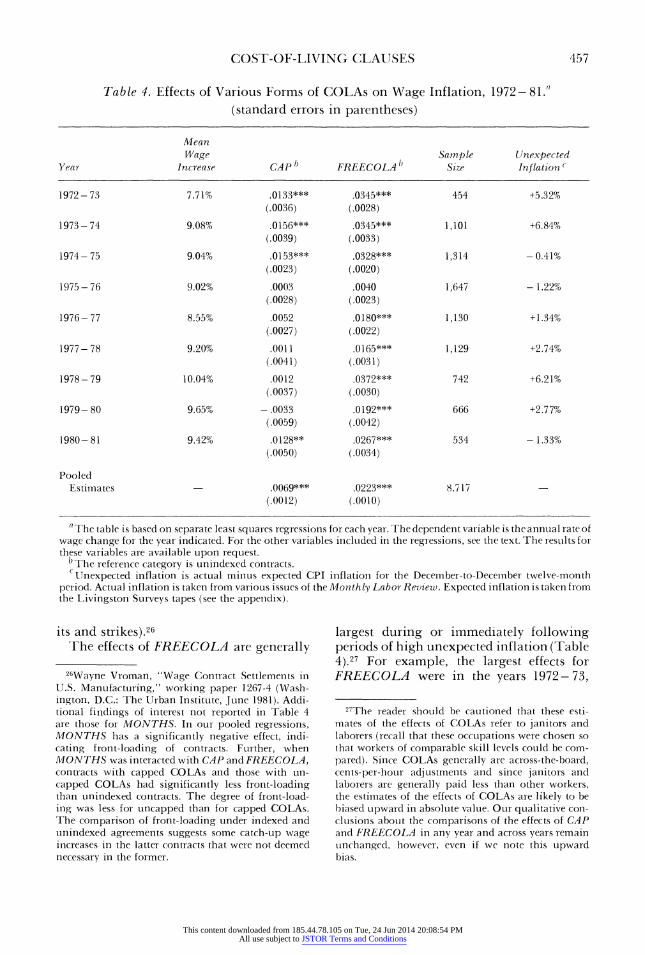

Table 4. Effects of Various Forms of COLAs on Wage Inflation, 1972- 81." (standard errors in parentheses)

Mean Wage Sample lUnexpected

Year Increase CAP FREECOLA1{ Size Inflation C

1972- 73 7.71% .0133*** .0345*** 454 +5.32% (.0036) (.0028)

1973- 74 9.08% .0156*** .0345*** 1,101 +6.84% (.0039) (.0033)

1974- 75 9.04% .0153*** .0328*** 1,314 - 0.41% (.0023) (.0020)

1975- 76 9.02% .0003 .0040 1,647 - 1.22% (.0028) (.0023)

1976- 77 8.55% .0052 .0180*** 1,130 +1.34% (.0027) (.0022)

1977- 78 9.20% .0011 .0165*** 1,129 +2.74% (.0041) (.0031)

1978- 79 10.04% .0012 .0372*** 742 +6.21% (.0037) (.0030)

1979- 80 9.65% - .0033 .0192*** 666 +2.77% (.0059) (.0042)

1980- 81 9.42% .0128** .0267*** 534 - 1.33% (.0050) (.0034)

Pooled Estimates - .0069*** .0223*** 8,717 -

(.0012) (.0010)

0The table is based on separate least squares regressions for each year. The dependent variable is the annual rate of wage change for the year indicated. For the other variables inclUded in the regressions, see the text. The results for these variables are available upon request.

')The reference category is unindexed contracts. CtUnexpected inflation is actual minus expected CPI inflation for the December-to-Decemnber twelve-month

period. Actual inflation is taken from various issues of the Monthly Labor Review. Expected inflation is taken from the Livingston Surveys tapes (see the appendix).

its and strikes).26 The effects of FREECOLA are generally

26Wayne Vroman, "Wage Contract Settlements in U.S. Manufacturing," working paper 1267-4 (Wash- ington, D.C.: The Urban Institute, June 1981). Addi- tional findings of interest not reported in Table 4 are those for MONTHS. In our pooled regressions, MONTHS has a significantly negative effect, indi- cating front-loading of contracts. Further, when MONTHS was interacted with CAP and FREECOLA, contracts with capped COLAs and those with un- capped COLAs had significantly less front-loading than unindexed contracts. The degree of front-load- ing was less for uncapped than for capped COLAs. The comparison of front-loading under indexed and unindexed agreements suggests some catch-up wage increases in the latter contracts that were not deemed necessary in the former.

largest during or immediately following periods of high unexpected inflation (Table 4).27 For example, the largest effects for FREECOLA were in the years 1972 - 73,

27The reader should be cautioned that these esti- mates of the effects of COLAs refer to janitors and laborers (recall that these occupations were chosen so that workers of comparable skill levels could be com- pared). Since COLAs generally are across-the-board, cents-per-hour adjustments and since janitors and laborers are generally paid less than other workers, the estimates of the effects of COLAs are likely to be biased upward in absolute valhe. Our qualitative con- clUsions about the comparisons of the effects of CAP and FREECOLA in any year and across years remain unchanged, however, even if we note this upward bias.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

458 INDUSTRIAL AND LABOR RELATIONS REVIEW

1973-74, and 1978-79, the three periods with the largest unexpected inflation; the smallest effect for uncapped COLAs was in 1975 - 76, when actual inflation had been less than expected inflation for two years. The effects for CAP are smaller than for FREECOLA, and from 1977 on, there does not seem to be much relation between the effects of CAP and unanticipated inflation (this issue is explored below).

In principle, one might have expected COLAs to actually reduce wage inflation during 1975- 76 to the extent that contracts without COLAs call for wage increases com- mensurate with expected inflation. It may be that during the middle to late 1970s, a period of an increasing squeeze on real wages caused by rising oil prices and falling productivity growth, COLAs were em- ployed as a mechanism to protect real wage levels from falling, in addition to smooth- ing out fluctuations in real wages.28 Alter- natively, FREECOLA may be a proxy for bargaining power.

The response of COLAs to unanticipated inflation was further investigated by build- ing this concept directly into the wage re- gression. Table 5 shows the results of this ef- fort. In this case, the dependent variable is the annualized rate of wage increase (includ- ing COLA payments plus other wage in- creases) over the life of each agreement. The explanatory variables include all those from Equation 3 except MONTHS, since the en- tire contract rather than a given year is now the unit of observation. In addition, we added expected inflation as of the beginning of the agreement ( P1 ) and interacted CAP and FREECOLA with unexpected inflation (pa - pe) over the life of the agreement. We thus assume that wages in unindexed agreements are set according to expected inflation, and we also allow inflation ex- pectations to affect indexed contracts.

Table 5 indicates that unindexed con- tracts raise wages by only about 79 percent of the expected inflation rate; however, a 95

28For evidence on the slowdown in productivity growth, see "Annual Indices Productivity, Hourly Compensation, Unit Costs, and Prices: Selected Years, 1956-80," Monthly Labor Review, Vol. 104, No. 5 (May 1981), Table 31, pp. 103-4.

Table 5. Selected Least Squares Results for Wage Inflation.t

(stndlarcd errors in parentheses)

x xp lni ntorValr/ b/es Coef icien ts

CAP -.0018 (.0028)

FREECO LA .0147*** (.0022)

(CIA X (if - P'') .0700 (.0928)

FREECOLA x (pQ _ pa) .5046*** (.065 1)

Pe .7890*** (.0889)

R2 .2218

Sample Size 2,530

tl Fl c(lepcelucclrt varialclU is the arintual late of wage changc ovcr the lifc of the contmract. For a deIscription of the other variables includcd, see the text. ResUlts for the

1thr' VMMial)lCS MeT avlilble)C U1011 IpCoreueSt.

P' is the expected annual rate of consumer price in- flatioi( as of the signing of the agreement (taken from thi Livingstoii SuIvesV, see appendix). Pa is the actual annu1al rate of cOnlSun(TI price inflation over the life of tdic agi-ecf'lel .

percent confidence interval for this effect ranges as high as about 96 percent of the expected inflation rate. Table 5 also indi- cates that during a perfectly anticipated inflation (pa = Pe), CAP has an insignificant wage effect, whereas contracts with un- capped COLAs would give significantly higher wage growth than unindexed con- tracts. This latter result may reflect a cor- relation between FREECOLA and union bargaining power not accounted for by the other variables in the model. Finally, the FREECOLA effect is significantly greater the larger is unanticipated inflation, a re- sult consistent with the annual regressions reported in Table 4. The finding that un- capped COLAs raise wages by about 50 per- cent of unanticipated inflation is consistent with other estimates of the effect of CO- LAs.29 On the other hand, the CAP unan- ticipated-inflation interaction term is small

25See Douty, "Study of the Relationships," and Vroman, "Wage Contract Settlements."

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

COST-OF-LIVING CLAUSES 459

and insignificant, suggesting the restrain- ing power of caps in COLAs.

Conclusions This paper has used data from individual

collective bargaining contracts supple- mented by industry data to estimate the determinants and effects of COLA cover- age. It is the first attempt to estimate the ef- fects of a variety of industry, demographic, and bargaining-unit characteristics on COLA coverage. It is also the first multi- variate study of the strength of COLA clauses.

Among the major findings were the fol- lowing, all assuming other things equal. First, union bargaining power and inflation uncertainty both had positive effects on the probability that a COLA clause would be adopted and on the strength of any such clause adopted. Second, unanticipated changes in an industry's prices reduced the incidence and strength of COLAs. Finally, during 1972- 81, wage inflation was greater under contracts with uncapped COLAs than under all other contracts-both those with capped COLAs and those without any COLA clauses. This last effect was posi- tively influenced by the amount of unan- ticipated inflation.

Our results have the following implica- tions for future developments in collective bargaining. First, both the growing number of union mergers and our results for CON- SOL might imply a growing incidence of COLAs in the future, as well as a rising de- gree of indexation among contracts already containing COLA clauses.30 Second, to the extent that bargaining units continue to grow in size, our findings for SIZE also sug- gest increasing COLA coverage.3' Third, our wage-inflation results suggest that COLAs do transmit price inflation to wages, especially during periods of unexpected in-

30See Gary N. Chaison, "A Note on Union Merger 'Trends, 1900- 1978," Industrial and Labor Relations Review, Vol. 34, No. 1 (October 1980), pp. 114-20.

31See Arnold Weber, "Stability and Change in the Structure of Collective Bargaining," in Lloyd Ulman, ed., Challenge to Collective Bargaining (Englewood Cliffs, N.J.: Prentice-Hall, 1967), pp. 13-36.

flation. In addition, the fact that uncapped COLAs did not have a negative effect on wage inflation during 1975- 76, a year when actual inflation was less than ex- pected, suggests that COLAs are a mechan- ism for preventing the secular decline in real wages that might otherwise occur dur- ing such periods. Perhaps the employer resistance implied by this fact helps to ex- plain why the percentage of major agree- ments (Table 1) with COLAs leveled off after 1978.

Recent developments in several indus- tries suggest that a reevaluation of COLA clauses may be at the top of the agenda of current and future negotiations. As noted earlier, in 1982, employers in the auto and steel industries demanded changes in the COLA clauses in their contracts. The major target of management is the uncapped COLA. Since these COLA clauses have been a significant source of wage increases in recent years, union opposition to this movement is obviously high. Difficult eco- nomic times in a number of basic indus- tries, however, have led several union lead- ers at least to consider a compromise in these clauses. Former UAW president Doug- las Fraser, for example, has said, "The pro- cess of collective bargaining the way we practice it is illogical. You make a settle- ment based on what you think the economy is going to be like in the next three years and you don't even know what it's going to be like in the next three months.' '32

Our evidence from the 1970s suggests that an appropriate compromise for all concerned may be the capped COLA com- bined with contracts with a duration of one or two years instead of three years. If man- agement can provide something in return, such as a profit-sharing program, a system of capped COLAs may help reduce unem- ployment and inflation in the long run. As Kenneth Moffett has noted, "Labor and Management are being forced into some kind of embrace that will help the econ- omy. "33

32"Redrawing Union Contracts," Newsweek, Feb- ruary 9, 1981, pp. 71-72.

33Ibid.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions

460 INDUSTRIAL AND LABOR RELATIONS REVIEW

Appendix Data Sources

SIZE and MULTI wvere taken directed from the BLS contracts tape. MULTI is an aggregation of the two BLS categories, "association" agreement and "induLstry/ area" agreement, both of which describe mTl1tifirlml con tracts. CONSOL was calculated directly from the BLS tape. This variable is only an estimate since there are missing contracts in each industry.

COLA, WAGE., MONTHS, and LENGTH were computed from contract information. In annual wage regressions, WAGE and MONTHS refer to December of a given year t. In addition, some wage data were taken fromn various issues of the Daily Labor Report.

Concentration was taken from the UT.S. Department of Commerce, 1972 Census of Mannufactures. Unioniza- tion was taken fronm Richard B. Freem-nan and James L. Medoff, "New Estimates of Private Sector Union- ism in the United States," Industrial and Labor Rela- tions Review, Vol. 32, No. 1 (January 1979). pp. 143- 74, and from the BLS estimates made in conjunction with its Indulstry Wage Series.

OccUpation, demographic, and regional variables (CRAFT, OPER, MALE, MAR, WHITE, ED, EXP, EXP2, CHILD, SOUTH, and LGSMISA) were pro- vided by James L. Medoff from the 1973- 75 Curre7it Population Surzvey tapes.

Wholesale- and consumer-price data were taken- from the BLS Wholesale Prices and Price Indices (1973, 1974, 1975) and the Month 1) Labor Review', variouLs issuLes. A total of 193 four-digit induLstry-plice regressions were run11.

Data on price expectations (Pe and LVARINFL) were taken fr-om the Livingston Surveys on Price Expecta- tions tapes, provided by the Federal Reserve Bank of Philadelphia. In these suLrveys (originated in 1947 by Joseph Livingstonl of the Philadelphia Inquirer), a panel of economists are asked every six imonths for their expectations regarding fUtUre wholesale- and conlsuLmer-price inflation. For further description of the Livingston data, see John A. Carlson, 'A StUdy of Price Forecasts," Artoals of Econontic and Social iMleazsulreosent, Vol. 6, No. 1 (Winiter-1977), pp.27-56.

This content downloaded from 185.44.78.105 on Tue, 24 Jun 2014 20:08:54 PMAll use subject to JSTOR Terms and Conditions