Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Cost Segregation Studies: Best PracticesReclassifying Business Personal Property to Achieve Income and Property Tax Benefits

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, APRIL 5, 2012

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Daniel McGrath, Director, Grant Thornton, Chicago, , , g

Gian Pazzia, Principal, KBKG Inc., Pasadena, Calif.

Julio Gonzalez, Founder and CEO, Engineered Tax Services, West Palm Beach, Fla.

Dennis Duffy, President, Duffy + Duffy Cost Segregation Services Inc., Westlake, Ohio

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Tax Alert: IRS takes a stand on Cost Segregation for Apartment Buildings

Author: Gian Pazzia, CCSP Principal 877.525.4462 x150 [email protected]

Summary In the recently released AmeriSouth XXXII., Tax Court Memo 2012-67, the IRS makes its first meaningful strike in its attempt to marginalize the benefits of cost segregation studies for residential rental property. For many taxpayers and CPAs, this is a complete surprise. However, KBKG clients have been warned for over a year that this was likely to happen. The IRS seems to have made a coordinated national effort on this position that can be traced back a few years as audits for cost segregation studies of apartments began popping up. While many of these audits were not being resolved in favor of taxpayers, the IRS had yet to establish formal case law directly on point with its position on apartments. Further, the IRS warned cost segregation professionals of this position at an ASCSP National Conference and indicated they were going to release a Cost Segregation Industry Directive specific to the residential rental industry. This Directive has yet to be published. KBKG believes that, much like early case law from the Investment Tax Credit era, just because this specific ruling was unfavorable, it does not mean future tax court rulings on the same issues will be consistent. KBKG provides its opinions below on several items disputed in this case. Further, this case emphasizes the benefits of using a seasoned cost segregation professional that has experience dealing with IRS audits. Facts: AmeriSouth XXXII, Ltd. acquired an apartment complex in 2003 for $10.25 million. The property was originally built in 1970. As soon as AmeriSouth bought the property, it began a $2 million renovation of the apartments that included replacing cabinets and countertops, dishwashers, garbage disposals, vent hoods, and kitchen sinks. The cost segregation study results were reported on the originally filed tax return for 2003. Roughly 33% of the property was reclassified into categories with 5 or 15 year tax lives. The components at issue include: • Site preparation and earthwork • Water-distribution system • Sanitary-sewer system • Gas line • Site electric • Special HVAC

• Special plumbing • Special electric • Finish carpentry • Millwork • Interior windows and mirrors • Special painting

AmeriSouth sold the property about the time the case was tried, and stopped responding to communications from the Court, the Commissioner, and even its own counsel. Because of AmeriSouth’s lack of responsiveness, their lawyers withdrew from the case and left the taxpayer representing itself.

The case could have been dismissed entirely, but because AmeriSouth didn't file a post trial brief, the Court deemed any factual matters not otherwise contested to be conceded. KBKG Commentary: KBKG believes that a number of positions taken in this cost segregation study are considered aggressive by most experts. Further, it also appears there was poor reference material available to substantiate the asset classifications used. However, a critical factor in this case was that the taxpayer had no interest in defending themselves, effectively giving the IRS a free pass to present their position on many issues without being challenged. We believe one of the most significant issues contested and considered by the Court relates to the appropriate comparison benchmark for an apartment. Should the Court look to see if the items in question relate to the operation and maintenance of a typical apartment building, or to the operation and maintenance of a generic shell building? The Court rationalized that the type of building does matter. KBKG does not agree with the Court in this critical decision. We note if this principal is applied to 15 year restaurant property, it would directly conflict with existing case law that supports personal property classification in restaurants. Nonetheless, if this argument holds up in future cases, it could have widespread consequences. Below are KBKG’s comments specific to items held to be real property by the Court. Site Utilities – Denied as 15 year property. Site utilities are outlined in several previously issued IRS Directives as 1250 Real Property when they relate to a typical building, and we agree. While KBKG understands methodical allocations of site utilities may be appropriate in some cases, it is hard to argue an apartment building’s gas, water, sewer, and electric service does not relate to the overall operation and maintenance of a building as described in the definition of a structural component found in §1.48-1(e)(2). Special HVAC – Denied as 5 year property. The venting connected to the stove hoods was not allowed because the Court was not convinced that they serve only the stoves. They rationalized that the stove hoods can also serve to remove odors and heat from beyond the stovetop. KBKG disagrees and believes that if proper case law was referenced, the Court would have allowed these items as 5 year property. Serving as ventilation for the building is merely incidental to its primary function of servicing the stove. Special Plumbing - Denied as 5 year property. Interestingly, the tax Court considered that AmeriSouth did not intend to periodically replace or plan to replace sinks after the 2003 renovation. While the intent to replace an item is relevant for purposes of determining Repair vs. Capitalization, it generally is not considered when determining the appropriate tax life of an asset. KBKG also notes that the Court cited the accessory test early in this case but failed to apply such test to any of the items in question. One can argue that kitchen sinks and plumbing are necessary to the business of renting apartments. Ceiling fans and Lights – Denied as 5 year property. KBKG believes this would have been ruled 5 year tangible personal property if AmeriSouth argued that the lighting provided by these combination light-fans serves to provide ambiance and only incidentally serves as general lighting. The fans were primarily decorative. Wiring – Denied as 5 year property. KBKG believes this also would have been ruled 5 year tangible personal property if AmeriSouth showed that the wiring supplied power for the appliances. The Court stated there was no evidence showing such.

Electric Panels – Denied as 5 year property. Quite simply, if a proper electrical load calculation was conducted and documented between specific equipment and the overall requirements of the building, KBKG believes this item would have been ruled 5 year tangible personal property. This has been proven in the Scott Paper case. Millwork and Finish Carpentry - Denied as 5 year property. The Court stated that the proper classification of the cabinetry is strictly an issue of their permanence and implied the same for the finish carpentry. KBKG has obtained information from unpublished resources that the general contractor who testified was not prepared to explain the steps required to remove these items and not prepared to address the six Whiteco Factors. KBKG believes the Court would have a different opinion if the permanence of these items was explained by the taxpayer in the context of the Whiteco Case. Mirrors – Denied as 5 year property. KBKG believes if proper case law was referenced, the Court would have allowed these items as tangible personal property. The Court did not dispute that the mirrors are removable. However, when AmeriSouth's former attorney called for testimony that the mirrors were decorative, their own witness stated the dining-room mirrors had “no function,” which actually supports the IRS position. I wonder if the judge scratched his head at this point in confusion and wondered which side this witness was arguing for. Closing: The story of this case is that poor preparation and documentation allowed the IRS to get their positions on the record with circumstances that favored them before the case even started. Unfortunately, according to our resources this case will not be appealed as the taxpayer has no interest in the property anymore. We know of at least two more tax court cases currently being litigated on these same issues (not public information yet). The outcome of those cases will be much more relevant to the issues at hand and we can ascertain those taxpayers have better representation. Further, this case emphasizes the risks of not using an established cost segregation firm with significant experience. Before choosing one provider over another, make sure to get multiple references of clients that actually went through IRS examination.

» Meet our expertsOur Services ■ R&D Tax Credits ■ Green Building Tax Incentives ■ Employment Tax Credits ■ Cost Segregation ■ Repair & Maintenance Review ■ Fixed Asset Depreciation Review ■ Property Tax Review ■ Sales & Use Tax ■ Expense Recovery

About KBKGEstablished in 1999 with offices across the US, KBKG provides turn-key tax solutions to CPAs and businesses. By focusing exclusively on value-added tax services that complement your traditional tax and accounting practice, we always deliver quantifiable benefits to clients. Our firm gives you access to our knowledge base and experienced industry leaders. We will help you determine which tax programs benefit your clients and we are committed to handling each client relationship with care and diligence. Our ability to work seamlessly with your team is the reason so many CPAs across the nation trust KBKG with their clients.

On March 7, 2012, the Internal Revenue Service (IRS) released two Revenue Procedures 2012-19 and 2012-20 as guidance for taxpayers to make changes to accounting methods in regards to the temporary regulations, "Repair Regulations," which were released on December 23 of 2011. These two revenue procedures are effective for taxable years beginning on or after January 1, 2012 and can be used to retroactively claim any missed deductions before January 1, 2012. » Read More on Temp Regs 263(a)

IRS PROCEDURE 2012-19 This procedure provides instruction for taxpayers to comply with the temporary regulations. For owners of real estate, the changes of interest include:

Deducting repair and maintenance costs•Deducting certain costs for investigating the acquisition of real estate (includes overhead and salaries)

•

Capitalizing acquisition or production costs•Capitalizing improvements to tangible property •

Rev Proc 2012-19 modifies Rev Proc 2011-14 by adding new automatic method changes as provided in the Repair Regulations. » Full Version - IRS Revenue Procedures 2012-19 (pdf)

IRS PROCEDURE 2012-20 For real estate owners, the changes of interest in this revenue procedure apply to taxpayers who want to adjust a method to comply with the new rules concerning:

Dispositions of MACRS property •Depreciation of Leasehold Improvements (you cannot amortize over the life of the lease)

•

General asset accounts•Changes in tax life for property depreciated under MACRS •

Rev Proc 2012-20 also modifies adds new automatic changes to Rev Proc 2011-14. » Full Version - IRS Revenue Procedures 2012-20 (pdf)

KBKG OBSERVATIONS: Taxpayers that have conducted "repair studies" by relying on the 2008 proposed regulations will likely have to give back the benefit received from that study if the items in question do not comply with the new Repair Regulations issued on December 23, 2011. The only good news for those taxpayers is that the IRS is offering audit protection to anyone that voluntarily makes the appropriate changes.

Rev. Proc. 2012-20 now clarifies that you can go back as far as you want to claim deductions for retired structural components. This might be the area that provides the most significant opportunity to claim missed deductions. In the past, when a taxpayer renovated an existing building, the IRS' position was that you could not write off the remaining basis of the structural components. This might include things like an old roof, HVAC units that were replaced, old lighting and so forth. For example, anyone that replaced a roof during a renovation is likely depreciating the new roof and the old roof. CPAs and taxpayers should review their depreciation schedules for this kind of opportunity. » Read KBKG's case study on the retirement of structural components

These new Revenue Procedures also simplify the process by allowing for two or more concurrent changes of accounting to be filed on one single Form 3115. Additionally, both Rev. Proc's allow for the use of Statistical Sampling for certain changes as long as the Sampling plan follows the guidelines provided in Rev. Proc. 2011-42. » Find out if you can qualify for a Repair/Asset Retirement Study

KBKG is committed to serving the CPA community with our deep understanding in several key areas of the tax code. Many tax professionals use our KBKG Tax Planning Matrix (recently updated for the Repair Regs) to help quickly identify and qualify which clients can benefit from several of our value added services. Additionally, please find our most current Leasehold Improvement Tax Chart (updated as of 1-12-2012) which is a must have for anyone that deals with real estate. We are pleased that so many of our CPA clients have found this to be a very useful reference during tax season.

» KBKG Tax Planning Matrix » Leasehold Improvement Tax Chart

If you have any questions regarding any of our areas of expertise, please don't hesitate to contact us. Our team is your resource and we are here to help.

Page 1 of 2KBKG

3/29/2012file://C:\Documents and Settings\gian\Local Settings\Temporary Internet Files\Content.Outlook\2...

The KBKG Team Tax Credits ▪ Incentives ▪ Cost Recovery NATIONWIDE SERVICE 877.525.4462 [email protected]

Page 2 of 2KBKG

3/29/2012file://C:\Documents and Settings\gian\Local Settings\Temporary Internet Files\Content.Outlook\2...

Tax Bulletin - February 24, 2012 Author: Gian P. Pazzia, CCSP and Luis (Lou) Guerrero, MBT

How the recent decision in Peco Foods, Inc. v. Commissioner may affect your ability to perform a cost segregation study. While the law regarding the binding nature of an asset allocation agreement under IRC Section 1060 is well established, KBKG notes the specific facts and circumstances of the Peco Foods case in making our recommendations below. Regarding the terms of a purchase agreement that includes real estate, taxpayers and their advisors should ensure that any applicable purchase agreement clearly lays out the intent of the parties and does not use all-encompassing language that indicates the allocation will be used "for all purposes (including financial and tax purposes)." In any event, the case suggests that discussions with an experienced tax depreciation expert should be strongly considered before any comparable transaction is completed.

Gian P. Pazzia, CCSP Principal » Bio

Luis (Lou) Guerrero, MBT Principal » Bio

» Meet the experts Our Services ■ R&D Tax Credits ■ Green Building Tax Incentives ■ Employment Tax Credits ■ Cost Segregation ■ Repair & Maintenance Review ■ Fixed Asset Depreciation Review ■ Property Tax Review ■ Sales & Use Tax ■ Expense Recovery

Facts: Peco Foods purchased two poultry processing plants (including all equipment) in the 1990s. Since this type of asset purchase requires an asset breakdown according to Section 1060, Peco and the seller included schedules showing how the purchase price would be allocated and then filed Form 8594 to finalize their purchase price allocations. The allocation included values for "Processing Plant Building," "Real Property Improvements," "Machinery and Equipment," and "Furniture, Fixtures and Equipment" among other items. It’s also important to note that their agreement stated that these values would be used "for all purposes including financial accounting and tax purposes."

Several years after the purchase, Peco performed a cost segregation study to further allocate the purchase price of the components within the Processing Plant Building and Real Property Improvement categories. Peco argued that they did not intend to include the values of the 1245 building property components in the allocation of personal property from their purchase agreement. The court, however, disallowed the cost segregation study and asserted that the values in the purchase agreement assigned to personal property were inclusive of all 1245 tangible personal property thus making the asset allocation agreement binding.

KBKG Observations: The details of this case leave us with some questions on the applicability of this ruling on other transactions involving an asset allocation agreement. The Tax Court’s opinion was that the contract was clear and unambiguous.

The purchase agreement in this case defined the terms "Real Property" and "Equipment" without regard to the Federal Income Tax Regulations definition of Real Property under 1.245-3(c) and Tangible Personal Property under 1.48-1(c). When reviewing the Peco agreement definitions, the courts considered the definitions from the Tax Regulations. Because the courts could not discern whether the Peco definitions were intended to characterize Real Property as anything other than what is described in the Tax Regulations, the tax courts rejected Peco’s contention that the term Processing Plant Building is ambiguous. Further, the Tax Court found that the inclusion of the word "building" was significant in its conclusion.

The Tax Court also relied on definitions found in the Merriam Webster’s Dictionary for "building" and "plant." The definition in Webster’s for "plant" includes "the land, buildings, machinery, apparatus, and fixtures employed in carrying on a trade or an industrial business," and "the buildings and other physical equipment of an institution." Webster’s describes a building as "a roofed and walled structure built for permanent use." In light of these definitions, the Tax Court believed that the buyer and seller would have simply referred to "Processing Plant" rather than "Processing Plant Building" had they intended to include special mechanical systems and other 1245 components typically identified in a cost segregation study.

Although the Tax Court Memo did not emphasize the relevance of Peco’s definition of equipment, KBKG observes that this too may have influenced their decision. The Peco agreement defined "equipment" as specifically including "tangible personal property."

Page 1 of 2KBKG

2/24/2012file://J:\Marketing\KBKG eBlast\02-24-12 Tax Bulletin - Peco cost seg\Tax Bulletin - Peco cost seg.html

Anyone familiar with cost segregation and depreciation case law knows that this can only weaken Peco’s position since most items found in a cost segregation study are considered tangible personal property in the Federal tax regulations.

Another noteworthy opinion of the Tax Court was that Peco’s decision to allocate almost twice as much of the purchase price to machinery and equipment as compared to the building, demonstrated Peco’s "intent that the original schedule allocated the purchase price among the specific assets conclusively." Without knowing exactly what machinery and equipment was included in the transaction, it’s difficult to know if the allocation was aggressive or reasonable. It would be interesting to know how much this may have influenced the final decision.

Finally we note that each transaction occurred before the IRS had formally acquiesced to the concept of cost segregation (Chief Counsel Advice was issued on May 28, 1999). Had this been considered by the Court, it may have raised doubts about the extent of certainty and awareness by both parties about all the issues related to the depreciation of a building and all of its contents.

Conclusion & Areas of Opportunity: As such, careful consideration must be paid to the descriptions and definitions that clients use when drafting their purchase documents. In situations where the purchase involves more than just real estate, such as a trade or business, it may be in the buyer’s best interest to perform a cost segregation study prior to finalizing an asset allocation agreement between the buyer and seller. By doing so, the correct allocations can be worked into the contract so both parties are in mutual agreement.

If cost segregation cannot be performed before the transaction, KBKG recommends avoiding the use of the term "building" in the agreement and substituting the term "plant" if possible. The use of the word "Improvement" by itself could also be problematic. Furthermore, we recommend that the agreement should carefully define "Machinery and Equipment" or "Furniture, Fixtures, and Equipment" by not describing these as "tangible personal property." As a precaution, we strongly recommend having a tax depreciation expert who is familiar with the applicable tax regulations and historical case law, assist in drafting your agreement for an applicable asset acquisition. KBKG can ensure that the contract is written so it will not prevent a cost segregation study from being valid.

For more information regarding cost segregation, feel free to contact your local KBKG representative. » Contact Us » Click and find out if you can benefit from cost segregation

The KBKG Team Solutions for Tax Professionals and Businesses Tax Credits ▪ Incentives ▪ Cost Recovery NATIONWIDE SERVICE 877.525.4462 [email protected]

About KBKG Established in 1999 with offices across the US, KBKG provides turn-key tax solutions to CPAs and businesses. By focusing exclusively on value-added tax services that complement your traditional tax and accounting practice, we always deliver quantifiable benefits to clients. Our firm gives you access to our knowledge base and experienced industry leaders. We will help you determine which tax programs benefit your clients and we are committed to handling each client relationship with care and diligence. Our ability to work seamlessly with your team is the reason so many CPAs across the nation trust KBKG with their clients.

Page 2 of 2KBKG

2/24/2012file://J:\Marketing\KBKG eBlast\02-24-12 Tax Bulletin - Peco cost seg\Tax Bulletin - Peco cost seg.html

American Society of Cost Segregation Professionals www.ascsp.org

1101 Pennsylvania Avenue NW, 6th Floor, Washington, DC 20004 office: 202.756.1959 fax: 312.240.2203

February 24, 2012

To: Internal Revenue Service

Re: Comments on the recently issued “Guidance Regarding Deduction and Capitalization of Expenditures

Related to Tangible Property” (Repair vs. Capitalization Temp. Regs.)

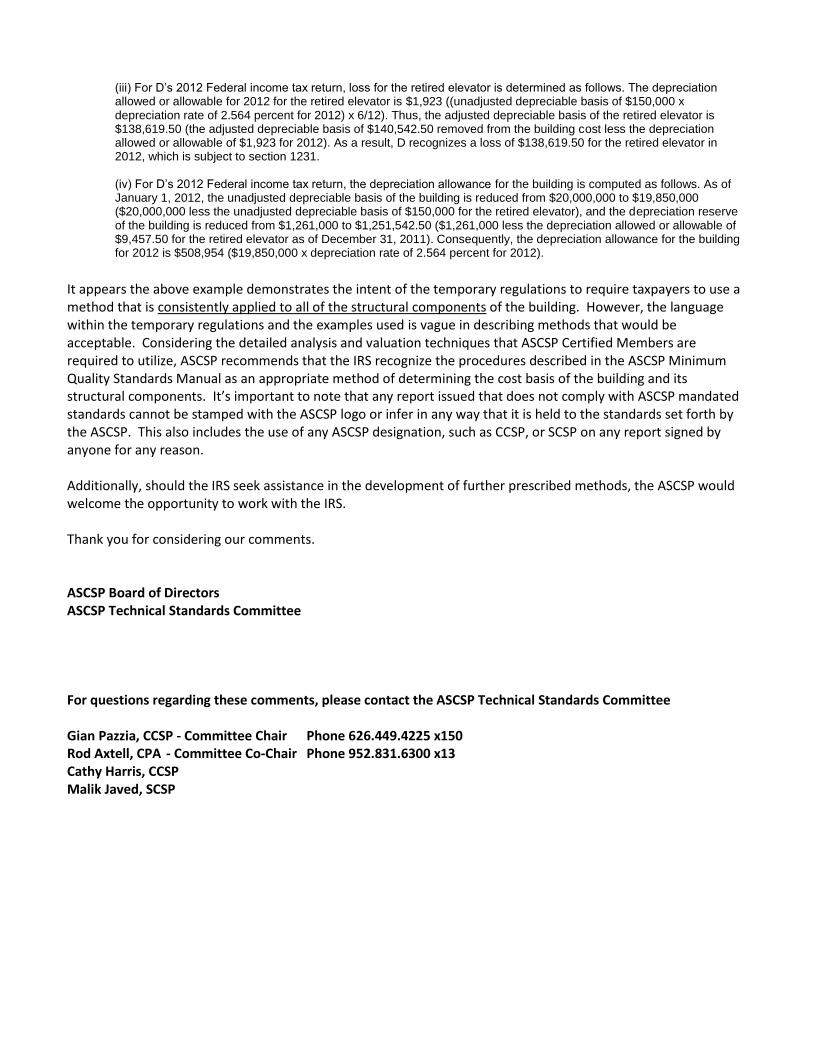

The American Society of Cost Segregation Professionals (ASCSP) represents the largest group of cost segregation professionals in the United States. The issuance of the Temporary Regulations has a direct correlation to the type of analysis that is conducted during a cost segregation study. ASCSP has a unique perspective that comes from a practical understanding of how building related expenditures may affect the use, condition, and life of property being repaired or improved as well as construction estimating and valuation techniques with respect to acquired properties. COMMENT: Disposition of Structural Components – ASCSP commends the IRS for recognizing that taxpayers who improve or replace certain structural components of a building should be allowed a retirement deduction for the replaced assets. We agree that the determination of the original or adjusted tax basis of components removed may be difficult for taxpayers. Without further guidance, we are concerned that inappropriate methodologies used will significantly misrepresent the basis of the building component being removed. As experts in this area, we emphasize that this should not be done without proper consideration of several factors that existed at the time the building or building component was placed in service. These factors include the condition of the component, age, replacement cost of the component removed and most importantly, the methodology utilized to calculate the relative fair market value of the acquired components. We believe it is important for the temporary regulations to be specific in its language to ensure this methodology is applied consistently to all of the structural components of the building along with the eight systems identified within these temporary regulations. It appears that the IRS is referencing this methodology in the following example:

Example 5. (i) On July 1, 2009, D, a calendar-year taxpayer, purchased and placed in service a multi-story office building that costs $20,000,000. The cost of each structural component of the building was not separately stated. D accounts for the building in its records as a single asset with a cost of $20,000,000. D depreciates the building as nonresidential real property and uses the optional depreciation table that corresponds with the general depreciation system, the straight-line method, a 39-year recovery period, and the mid-month convention. As of January 1, 2012, the depreciation reserve for the building is $1,261,000. (ii) On June 30, 2012, D replaces one of the building’s elevators. Because D cannot identify the cost of the structural components of the office building from its records, D uses a reasonable method that is consistently applied to all of the structural components of the office building to determine the cost of the elevator. Using this reasonable

method, D allocates $150,000 of the $20,000,000 purchase price for the building to the retired elevator. Using the optional depreciation table that corresponds with the general depreciation system, the straight-line method, a 39-year recovery period, and the mid-month convention, the depreciation allowed or allowable for the retired elevator as of December 31, 2011, is $9,457.50.

(iii) For D’s 2012 Federal income tax return, loss for the retired elevator is determined as follows. The depreciation allowed or allowable for 2012 for the retired elevator is $1,923 ((unadjusted depreciable basis of $150,000 x depreciation rate of 2.564 percent for 2012) x 6/12). Thus, the adjusted depreciable basis of the retired elevator is $138,619.50 (the adjusted depreciable basis of $140,542.50 removed from the building cost less the depreciation allowed or allowable of $1,923 for 2012). As a result, D recognizes a loss of $138,619.50 for the retired elevator in 2012, which is subject to section 1231. (iv) For D’s 2012 Federal income tax return, the depreciation allowance for the building is computed as follows. As of January 1, 2012, the unadjusted depreciable basis of the building is reduced from $20,000,000 to $19,850,000 ($20,000,000 less the unadjusted depreciable basis of $150,000 for the retired elevator), and the depreciation reserve of the building is reduced from $1,261,000 to $1,251,542.50 ($1,261,000 less the depreciation allowed or allowable of $9,457.50 for the retired elevator as of December 31, 2011). Consequently, the depreciation allowance for the building for 2012 is $508,954 ($19,850,000 x depreciation rate of 2.564 percent for 2012).

It appears the above example demonstrates the intent of the temporary regulations to require taxpayers to use a method that is consistently applied to all of the structural components of the building. However, the language within the temporary regulations and the examples used is vague in describing methods that would be acceptable. Considering the detailed analysis and valuation techniques that ASCSP Certified Members are required to utilize, ASCSP recommends that the IRS recognize the procedures described in the ASCSP Minimum Quality Standards Manual as an appropriate method of determining the cost basis of the building and its structural components. It’s important to note that any report issued that does not comply with ASCSP mandated standards cannot be stamped with the ASCSP logo or infer in any way that it is held to the standards set forth by the ASCSP. This also includes the use of any ASCSP designation, such as CCSP, or SCSP on any report signed by anyone for any reason. Additionally, should the IRS seek assistance in the development of further prescribed methods, the ASCSP would welcome the opportunity to work with the IRS. Thank you for considering our comments. ASCSP Board of Directors ASCSP Technical Standards Committee For questions regarding these comments, please contact the ASCSP Technical Standards Committee Gian Pazzia, CCSP - Committee Chair Phone 626.449.4225 x150 Rod Axtell, CPA - Committee Co-Chair Phone 952.831.6300 x13 Cathy Harris, CCSP Malik Javed, SCSP

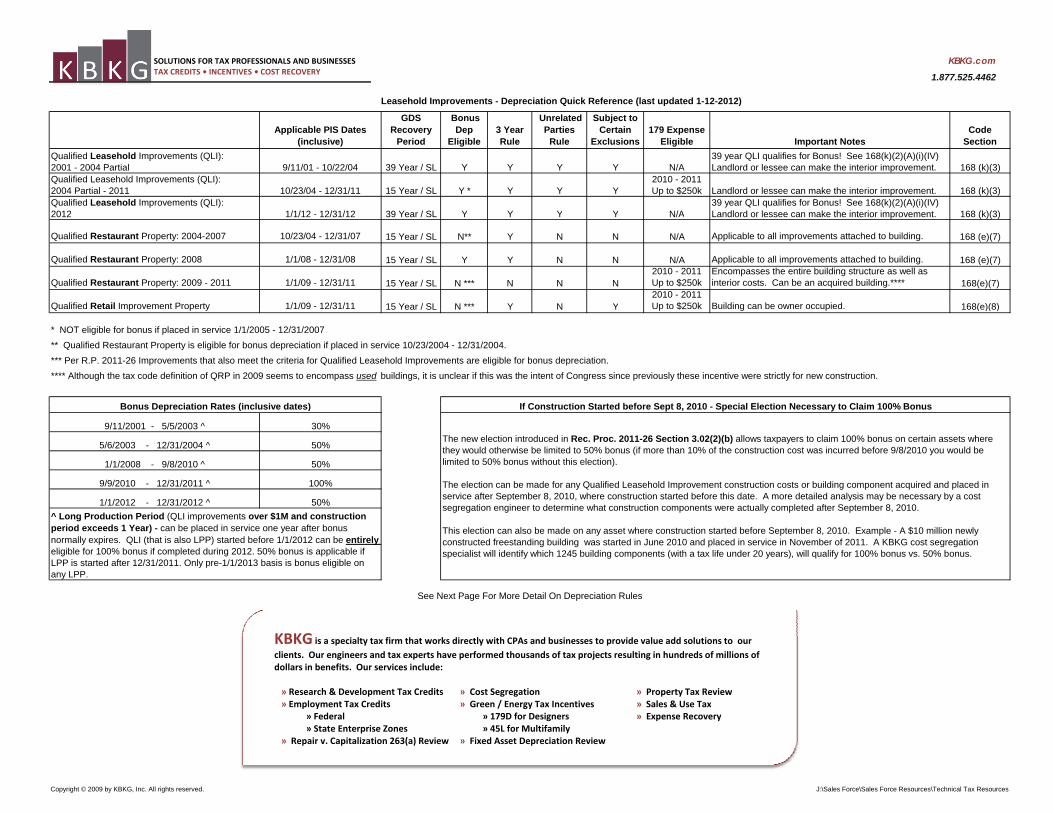

Leasehold Improvements - Depreciation Quick Reference (last updated 1-12-2012)

GDS Bonus Unrelated Subject to

SOLUTIONS FOR TAX PROFESSIONALS AND BUSINESSESTAX CREDITS • INCENTIVES • COST RECOVERY

KBKG.com1.877.525.4462

Applicable PIS Dates (inclusive)

GDS Recovery

Period

Bonus Dep

Eligible3 Year Rule

Unrelated Parties

Rule

Subject to Certain

Exclusions179 Expense

Eligible Important NotesCode

SectionQualified Leasehold Improvements (QLI): 2001 - 2004 Partial 9/11/01 - 10/22/04 39 Year / SL Y Y Y Y N/A

39 year QLI qualifies for Bonus! See 168(k)(2)(A)(i)(IV) Landlord or lessee can make the interior improvement. 168 (k)(3)

Qualified Leasehold Improvements (QLI): 2004 Partial - 2011 10/23/04 - 12/31/11 15 Year / SL Y * Y Y Y

2010 - 2011 Up to $250k Landlord or lessee can make the interior improvement. 168 (k)(3)

Qualified Leasehold Improvements (QLI): 2012 1/1/12 12/31/12 39 Year / SL Y Y Y Y N/A

39 year QLI qualifies for Bonus! See 168(k)(2)(A)(i)(IV) Landlord or lessee can make the interior improvement 168 (k)(3)2012 1/1/12 - 12/31/12 39 Year / SL Y Y Y Y N/A Landlord or lessee can make the interior improvement. 168 (k)(3)

Qualified Restaurant Property: 2004-2007 10/23/04 - 12/31/07 15 Year / SL N** Y N N N/A Applicable to all improvements attached to building. 168 (e)(7)

Qualified Restaurant Property: 2008 1/1/08 - 12/31/08 15 Year / SL Y Y N N N/A Applicable to all improvements attached to building. 168 (e)(7)

Qualified Restaurant Property: 2009 - 2011 1/1/09 - 12/31/11 15 Year / SL N *** N N N2010 - 2011 Up to $250k

Encompasses the entire building structure as well as interior costs. Can be an acquired building.**** 168(e)(7)

Qualified Retail Improvement Property 1/1/09 - 12/31/11 15 Year / SL N *** Y N Y2010 - 2011 Up to $250k Building can be owner occupied. 168(e)(8)Qua ed eta p o e e ope y / /09 /3 / 15 Year / SL N Y N Y Up o $ 50 u d g ca be o e occup ed 168(e)(8)

* NOT eligible for bonus if placed in service 1/1/2005 - 12/31/2007** Qualified Restaurant Property is eligible for bonus depreciation if placed in service 10/23/2004 - 12/31/2004.*** Per R.P. 2011-26 Improvements that also meet the criteria for Qualified Leasehold Improvements are eligible for bonus depreciation.**** Although the tax code definition of QRP in 2009 seems to encompass used buildings, it is unclear if this was the intent of Congress since previously these incentive were strictly for new construction.

B D i ti R t (i l i d t ) If C t ti St t d b f S t 8 2010 S i l El ti N t Cl i 100% B

9/11/2001 - 5/5/2003 ^ 30%

5/6/2003 - 12/31/2004 ^ 50%

1/1/2008 - 9/8/2010 ^ 50%

9/9/2010 - 12/31/2011 ^ 100%

1/1/2012 12/31/2012 ^ 50%

The new election introduced in Rec. Proc. 2011-26 Section 3.02(2)(b) allows taxpayers to claim 100% bonus on certain assets where they would otherwise be limited to 50% bonus (if more than 10% of the construction cost was incurred before 9/8/2010 you would be limited to 50% bonus without this election). The election can be made for any Qualified Leasehold Improvement construction costs or building component acquired and placed in service after September 8, 2010, where construction started before this date. A more detailed analysis may be necessary by a cost

Bonus Depreciation Rates (inclusive dates) If Construction Started before Sept 8, 2010 - Special Election Necessary to Claim 100% Bonus

1/1/2012 - 12/31/2012 ^ 50%^ Long Production Period (QLI improvements over $1M and construction period exceeds 1 Year) - can be placed in service one year after bonus normally expires. QLI (that is also LPP) started before 1/1/2012 can be entirely eligible for 100% bonus if completed during 2012. 50% bonus is applicable if LPP is started after 12/31/2011. Only pre-1/1/2013 basis is bonus eligible on any LPP.

service after September 8, 2010, where construction started before this date. A more detailed analysis may be necessary by a cost segregation engineer to determine what construction components were actually completed after September 8, 2010.

This election can also be made on any asset where construction started before September 8, 2010. Example - A $10 million newly constructed freestanding building was started in June 2010 and placed in service in November of 2011. A KBKG cost segregation specialist will identify which 1245 building components (with a tax life under 20 years), will qualify for 100% bonus vs. 50% bonus.

See Next Page For More Detail On Depreciation RulesSee Next Page For More Detail On Depreciation Rules

KBKG is a specialty tax firm that works directly with CPAs and businesses to provide value add solutions to our clients. Our engineers and tax experts have performed thousands of tax projects resulting in hundreds of millions of dollars in benefits. Our services include:

R h & D l t T C dit C t S ti P t T R i» Research & Development Tax Credits » Cost Segregation » Property Tax Review» Employment Tax Credits » Green / Energy Tax Incentives » Sales & Use Tax

» Federal » 179D for Designers » Expense Recovery» State Enterprise Zones » 45L for Multifamily

» Repair v. Capitalization 263(a) Review » Fixed Asset Depreciation Review

Copyright © 2009 by KBKG, Inc. All rights reserved. J:\Sales Force\Sales Force Resources\Technical Tax Resources

Definitions:

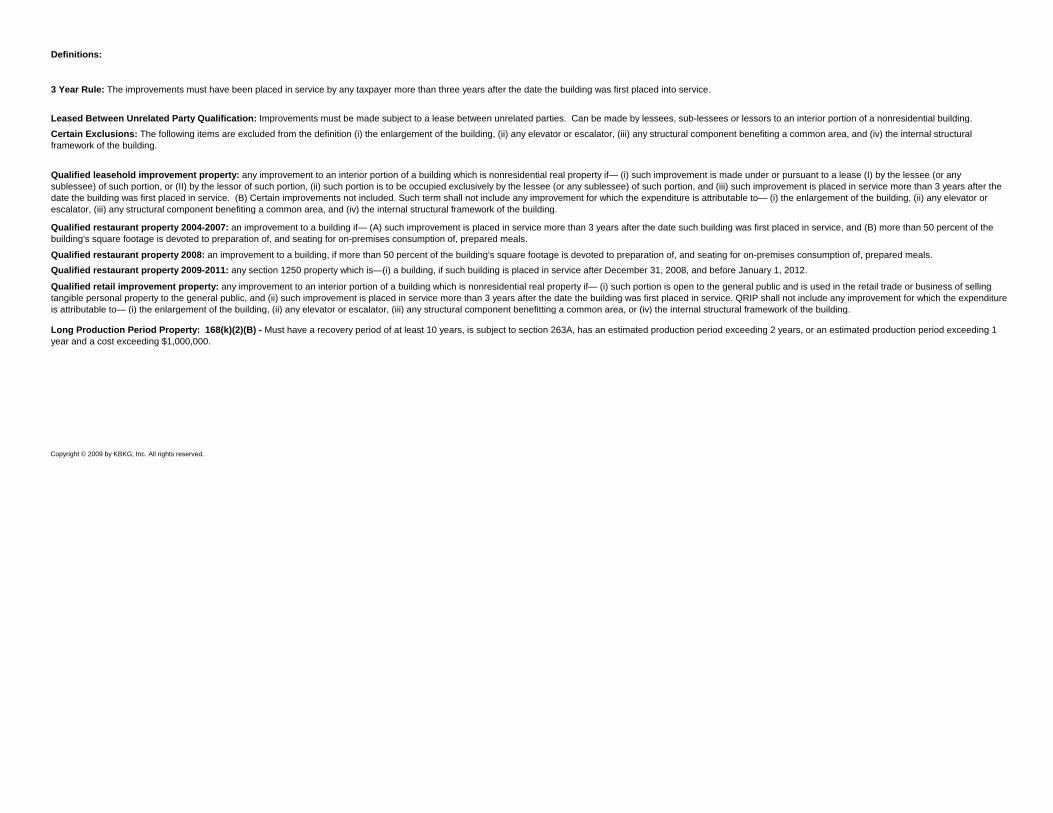

3 Year Rule: The improvements must have been placed in service by any taxpayer more than three years after the date the building was first placed into service.

Leased Between Unrelated Party Qualification: Improvements must be made subject to a lease between unrelated parties Can be made by lessees sub-lessees or lessors to an interior portion of a nonresidential building

Qualified leasehold improvement property: any improvement to an interior portion of a building which is nonresidential real property if— (i) such improvement is made under or pursuant to a lease (I) by the lessee (or any sublessee) of such portion, or (II) by the lessor of such portion, (ii) such portion is to be occupied exclusively by the lessee (or any sublessee) of such portion, and (iii) such improvement is placed in service more than 3 years after the date the building was first placed in service. (B) Certain improvements not included. Such term shall not include any improvement for which the expenditure is attributable to— (i) the enlargement of the building, (ii) any elevator or escalator, (iii) any structural component benefiting a common area, and (iv) the internal structural framework of the building.

Certain Exclusions: The following items are excluded from the definition (i) the enlargement of the building, (ii) any elevator or escalator, (iii) any structural component benefiting a common area, and (iv) the internal structural framework of the building.

Leased Between Unrelated Party Qualification: Improvements must be made subject to a lease between unrelated parties. Can be made by lessees, sub-lessees or lessors to an interior portion of a nonresidential building.

( ) y p g ( ) g

Qualified restaurant property 2009-2011: any section 1250 property which is—(i) a building, if such building is placed in service after December 31, 2008, and before January 1, 2012.

Qualified retail improvement property: any improvement to an interior portion of a building which is nonresidential real property if— (i) such portion is open to the general public and is used in the retail trade or business of selling tangible personal property to the general public, and (ii) such improvement is placed in service more than 3 years after the date the building was first placed in service. QRIP shall not include any improvement for which the expenditure is attributable to (i) the enlargement of the building (ii) any elevator or escalator (iii) any structural component benefitting a common area or (iv) the internal structural framework of the building

Qualified restaurant property 2008: an improvement to a building, if more than 50 percent of the building's square footage is devoted to preparation of, and seating for on-premises consumption of, prepared meals.

Qualified restaurant property 2004-2007: an improvement to a building if— (A) such improvement is placed in service more than 3 years after the date such building was first placed in service, and (B) more than 50 percent of the building's square footage is devoted to preparation of, and seating for on-premises consumption of, prepared meals.

Long Production Period Property: 168(k)(2)(B) - Must have a recovery period of at least 10 years, is subject to section 263A, has an estimated production period exceeding 2 years, or an estimated production period exceeding 1 year and a cost exceeding $1,000,000.

is attributable to— (i) the enlargement of the building, (ii) any elevator or escalator, (iii) any structural component benefitting a common area, or (iv) the internal structural framework of the building.

Copyright © 2009 by KBKG, Inc. All rights reserved.

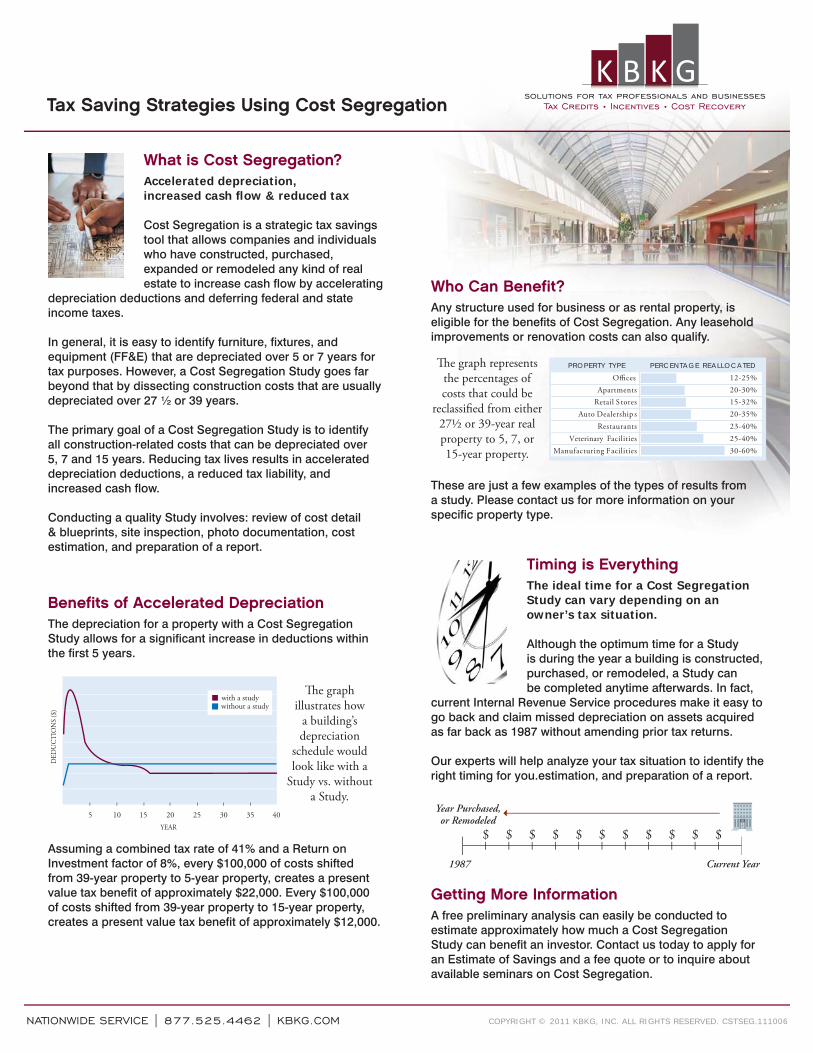

What is Cost Segregation? Accelerated depreciation, increased cash fl ow & reduced tax

Cost Segregation is a strategic tax savings tool that allows companies and individuals who have constructed, purchased, expanded or remodeled any kind of real estate to increase cash flow by accelerating depreciation deductions and deferring federal and state income taxes.

In general, it is easy to identify furniture, fixtures, and equipment (FF&E) that are depreciated over 5 or 7 years for tax purposes. However, a Cost Segregation Study goes far beyond that by dissecting construction costs that are usually depreciated over 27 ½ or 39 years.

The primary goal of a Cost Segregation Study is to identify all construction-related costs that can be depreciated over 5, 7 and 15 years. Reducing tax lives results in accelerated depreciation deductions, a reduced tax liability, and increased cash flow.

Conducting a quality Study involves: review of cost detail & blueprints, site inspection, photo documentation, cost estimation, and preparation of a report.

Benefits of Accelerated DepreciationThe depreciation for a property with a Cost Segregation Study allows for a significant increase in deductions within the first 5 years.

405 10 15 20 25 30 35YEAR

)$( SN

OITCU

DED

with a studywithout a study

Th e graph illustrates how

a building’s depreciation

schedule would look like with a

Study vs. without a Study.

Assuming a combined tax rate of 41% and a Return on Investment factor of 8%, every $100,000 of costs shifted from 39-year property to 5-year property, creates a present value tax benefit of approximately $22,000. Every $100,000 of costs shifted from 39-year property to 15-year property, creates a present value tax benefit of approximately $12,000.

Who Can Benefit?Any structure used for business or as rental property, is eligible for the benefits of Cost Segregation. Any leasehold improvements or renovation costs can also qualify.

O sApartments

Retail S toresAuto Dealership s

RestaurantsVeterinary Facilities

Manufacturing Facilities

PROPERTY TYPE PERCENTAGE REALLOCATED

12-25%20-30%15-32%20-35%23-40%25-40%30-60%

Th e graph represents the percentages of costs that could be

reclassifi ed from either 27½ or 39-year real property to 5, 7, or 15-year property.

These are just a few examples of the types of results from a study. Please contact us for more information on your specific property type.

Timing is Everything The ideal time for a Cost Segregation Study can vary depending on an owner’s tax situation.

Although the optimum time for a Study is during the year a building is constructed, purchased, or remodeled, a Study can be completed anytime afterwards. In fact, current Internal Revenue Service procedures make it easy to go back and claim missed depreciation on assets acquired as far back as 1987 without amending prior tax returns.

Our experts will help analyze your tax situation to identify the right timing for you.estimation, and preparation of a report.

1987 Current Year

Year Purchased,or Remodeled

$ $ $ $ $ $ $ $ $ $ $

Getting More InformationA free preliminary analysis can easily be conducted to estimate approximately how much a Cost Segregation Study can benefit an investor. Contact us today to apply for an Estimate of Savings and a fee quote or to inquire about available seminars on Cost Segregation.

COPYRIGHT © 2011 KBKG, INC. ALL RIGHTS RESERVED. CSTSEG.111006

Tax Saving Strategies Using Cost Segregationsolutions for tax professionals and businesses

Tax Credits • Incentives • Cost Recovery

NATIONWIDE SERVICE | 877.525.4462 | KBKG.COM