Embed Size (px)

Citation preview

Cost Variance Analysis

DefinitionsDefinitions

STANDARD COSTS – are predetermined or target unit costs of production which should be attained under efficient conditions. It is the amount and costs of direct material, direct labor, and factory overhead required to produce one unit of finished product.

STANDARD COST SYSTEM – is an accounting system which uses standard costs rather than actual costs to account for units as they flow through the manufacturing process.

Objectives of Standard Cost System1. To help a business operate

more effectively and more efficiently

2. It helps accomplish organization goals by obtaining optimum output from the inputs available.

Uses of Standard Costing1. Inventory2. Planning and controlling costs3. Measurement of performance4. Budget preparation5. Motivating employees

Types of Standards

1. Basic (Fixed) Cost Standards – are standards that are unchanged year after year.

2. Perfection (Ideal or Theoretical) Cost Standards – are absolute minimum costs attainable under operating conditions.

3. Current Attainable Cost Standards – standard that can be attained under efficient operating conditions. It is useful for employee motivation, product costing and budgeting.

Setting Direct Materials StandardsStandard Quantity - Industrial engineers develop

specification for the kinds and quantities of materials used in producing the goods budgeted.

- Operation schedules list the materials and quantities required for the expected volume of production.

Standard Price- Information from the

operation schedule and bills of material established jointly by the engineering department, the manufacturing supervisor and the accountant becomes the basis for the material price standard.

Variance Analysis

- Analysis of variances reveals that causes of deviations between standard and actual costs. This feedback aids in planning future goals, controlling costs and evaluating performance.

Variances – are the difference between standard and actual costs. A variance is considered FAVORABLE if actual costs are less than the standard costs, and UNFAVORABLE if actual costs exceed standard costs.

Standard Time- Examination of past payroll and

production records can reveal the worker-hours used on various jobs and can help determine standard performance.

- Time reports from the workers for a limited period will be a good basis for the standard.

- If possible, time and motion study should be the basis for the standard

- The time study seeks to develop time standards and price rates which the average operator can meet daily

Setting Labor Standards

Standard Labor Rate- Labor rates should be determined by considering the

current rates as well as the competitive markets.

Methods in determining the labor rate standards:1. A company may establish a standard rate for the job,

regardless of who performs the job, the rates stays the same, or

2. A company may establish a rate for an individual worker and the worker receives this rate regardless of the work performed.

If labor contracts exist, the wage is relatively fixed and canbe used as standard.

Setting Overhead Standards- Factory overhead cost standards provide

a means of allocating factory overhead to cost inventories for pricing decisions and controlling expenses

- A capacity level is selected as the volume based or denominator capacity.

- Costs are allocated on a volume related or non-volume related base.

Commonly used volume-related basis:a. Machine hoursb. Direct labor-hoursc. Direct labor costsd. Direct materials costse. Units or production

- After expressing volume based on machine hours, the number of inspection, or another basis, the factory incurred at this level is estimated.

Responsibility: the Purchasing Department is usually responsible for material price variances. However, the Production Department could be responsible for unfavorable price variance occurring (1) because of a request for rush order due to poor scheduling or (2) when they specify certain brand-name materials or materials of certain grade or quality other those initially included in the bill of materials.

The possible causes of materials quantity or usage variance are as follows:

1. Waste and loss of materials in handling and processing2. Substitution of defective or non-standard materials3. Spoilage or production of excess scrap because or inexperienced

workers or poor supervision4. Lack of proper tools or machines5. Variation yields from materials

Responsibility: Production line supervisors should be held responsible for materials under their control.

Operating Performance EvaluationAnalysis of Variances

- The variance or difference between actual costs and standard costs can be separated and analyzed into two components: Price Variance and Efficiency Variance

DIRECT MATERIALS VARIANCE ANALYSIS- Difference between actual costs and standard cost of materials

used is called a material cost variance- This variance is made up of a price variance and a usage or

quantity or efficiency variance

The possible causes of materials price variance are as follows:1. Fluctuations in market price of materials2. Purchasing from distant suppliers, which results in additional

transportation costs3. Failure to take cash discounts available4. Purchasing materials of substandard quality or in uneconomical lots5. Unfavorable purchase terms

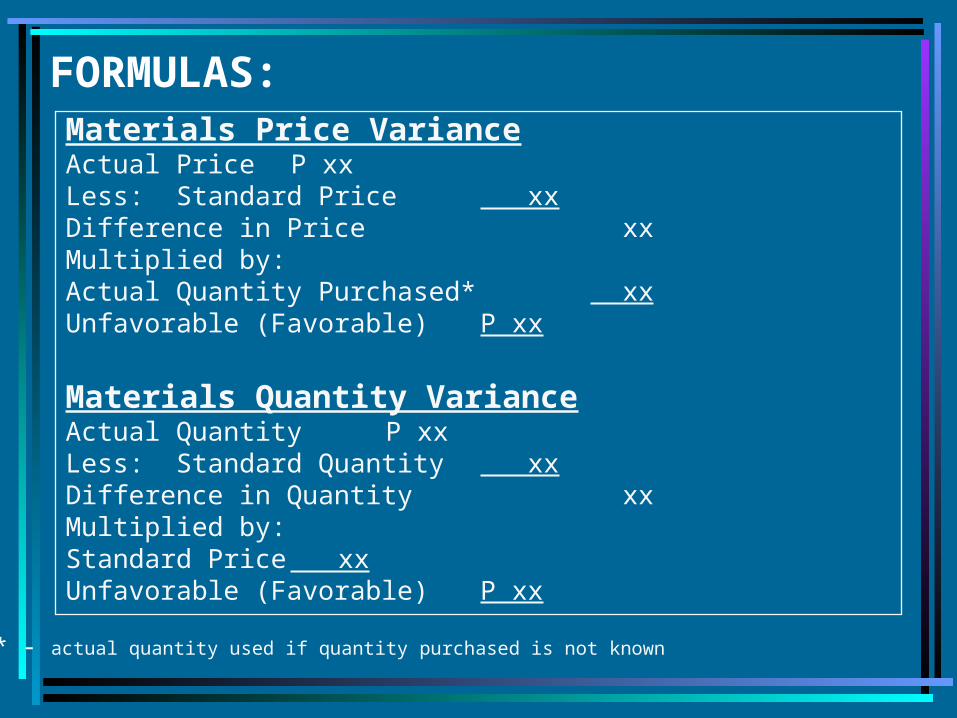

FORMULAS:Materials Price VarianceActual Price P xxLess: Standard Price xxDifference in Price xxMultiplied by: Actual Quantity Purchased* xxUnfavorable (Favorable) P xx

Materials Quantity VarianceActual Quantity P xxLess: Standard Quantity xxDifference in Quantity xxMultiplied by:Standard Price xxUnfavorable (Favorable) P xx

* - actual quantity used if quantity purchased is not known

SAMPLE PROBLEM: MATERIALS VARIANCE

ABC Company has budgeted 50,000 units of output using 50,000 units of raw materials at a total material cost of P100,000. Actual output was 50,000 units of product that require 45,000 units at a cost of P2.10 per unit. The direct material price variance and usage variance are:

Price Usagea. P 4,500 UF P10,000 Fb. P 4,500 F P10,500 Fc. P 5,000 F P10,500 UFd. P10,000 F P 4,500 UF

SOLUTION:

Materials Price Variance

Actual Price P 2.10Standard Price (P100,000 / 50,000 units) 2.00Difference in Price P 0.10x Actual Qty Used 45,000Material Price

Variance P 4,500 U

Material Quantity Variance

Actual Quantity 45,000

Standard Quantity 50,000

Difference in Qty 5,000

x Standard Price P 2

Material Usage

VarianceP10,000 F

Answer: a

DIRECT LABOR VARIANCE ANALYSIS

- Labor cost variance is the difference between actual labor cost and standard labor cost.

- This variance may be analyzed into two components namely: the labor rate variance and the labor usage or efficiency variance

The possible causes of labor rate variance are as follows:1. Inexperienced workers hired2. Change in labor rate particularly peak season that has not been

incorporated in standard rate3. Use of an employee having a wage classification other than that

assumed when the standard for a job was set4. Use of a greater number of higher-paid employees in the group than

anticipated.

Responsibility: if production line supervisors have the authority to match workers and machines to task by hiring the proper grade of labor, line supervisors should be responsible. They will also be responsible if they control the wage rate of their labor force. If they do not, the Personnel Department may be responsible.

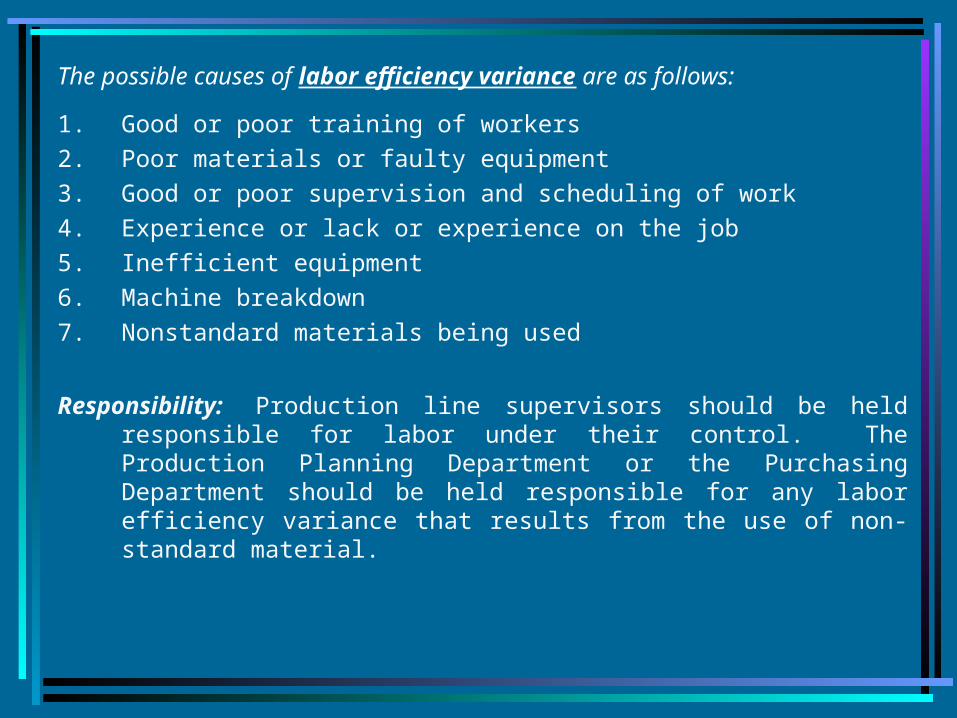

The possible causes of labor efficiency variance are as follows:

1. Good or poor training of workers2. Poor materials or faulty equipment3. Good or poor supervision and scheduling of work4. Experience or lack or experience on the job5. Inefficient equipment6. Machine breakdown7. Nonstandard materials being used

Responsibility: Production line supervisors should be held responsible for labor under their control. The Production Planning Department or the Purchasing Department should be held responsible for any labor efficiency variance that results from the use of non-standard material.

FORMULAS:

Labor Rate VarianceActual Labor Rate P xxLess: Standard Labor Rate xxDifference in Rate xxMultiplied by: Actual Hours xxUnfavorable (Favorable) P xx

Labor Efficiency or Time VarianceActual Hours xxLess: Standard Hours xxDifference in Hours xxMultiplied by:Standard Labor Rate P xxUnfavorable (Favorable) P xx

SAMPLE: DIRECT LABOR RATE VARIANCE

Information on XYZ Co.’s direct labor costs for May 2005 is as

follows:Standard direct labor hours 35,000Actual direct labor hours 34,500Total direct labor payrollP241,500Direct labor efficiency variance – favorableP 3,200

What is XYZ Co.’s direct labor rate variance?a. P17,250 F c. P21,000 Fc. P20,700 UF d. P21,000 F

SOLUTION:

Actual Hours 34,500Standard Hours 35,000Difference (500) x Standard Rate ?Direct Labor Rate Efficiency Variance P(3,200)F

Thus, P3,200 F / 500 = P 6.4 Std. Rate

Actual Rate = P241,500 / 34,500 = P7

Actual Rate P 7.00Standard Rate 6.40Difference in Rate P0.60x Actual Hours 34,500Direct Labor Rate

VarianceP20,700 U

Answer: b

SAMPLE PROBLEM: DIRECT LABOR EFFICIENCY VARIANCE

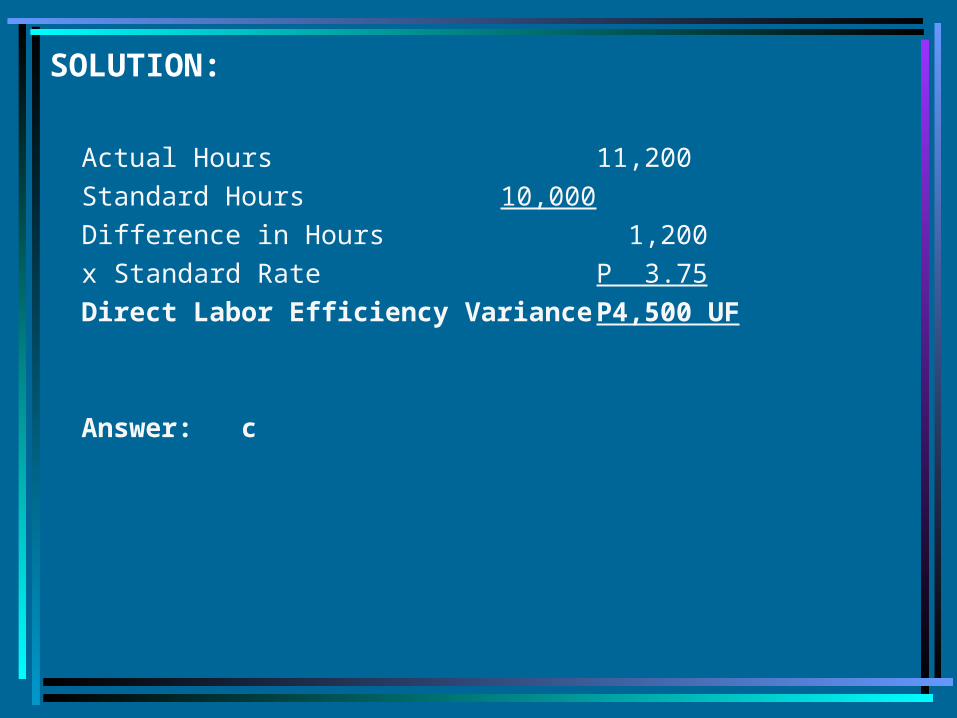

Information on Ace Company’s direct labor cost is as follows:Standard direct labor rate P 3.75Actual direct labor rate P 3.50Standard direct labor hours 10,000Actual direct labor hours 11,200

What is the direct labor efficiency variance?a. P4,200 UF c. P4,500 UFb. P4,200 F d. P4,500 F

SOLUTION:

Actual Hours 11,200Standard Hours 10,000Difference in Hours 1,200x Standard Rate P 3.75Direct Labor Efficiency Variance P4,500 UF

Answer: c

FACTORY OVERHEAD VARIANCE ANALYSISVARIABLE MANUFACTURING OVERHEAD- Total variance manufacturing overhead variance is the difference

between actual variable overhead and standard variable overhead allowed on actual output.

- This may be broken down into:a) Variable overhead spending varianceb) Variable overhead efficiency variance

The possible causes of variable overhead spending variance or price/controllable variance are as follows:

1. Actual costs, e.g. machine power, materials handling, supplies were different from those expected because of fluctuations in market prices or rates

2. Increase in energy costs3. Waste in using supplies4. Avoidable machine breakdowns5. Wrong grade of indirect material and indirect labor6. Lack of operators or tools

Responsibility: Supervisors of cost centers are responsible because they have some degree of control over these budget or expense factors.

The possible causes of variable overhead efficiency variances are as follows:

- This is attributable to efficiency in using the base on which variable overhead is applied. So that if the basis of the variable overhead application is direct labor hours, the causes of the labor efficiency variance will also be the causes of the variable overhead efficiency variance.

Responsibility: Production line supervisors are responsible for this variance. This variance shows how much of the factory’s capacity has been consumed or released by off-standard labor performance. If machine-hours are the basis for applying factory overhead, the variance measures the efficiency of machine usage.

FIXED MANUFACTURING OVERHEAD VARIANCE ANALYSIS

- In variance analysis, fixed manufacturing costs are treated differently from variable manufacturing costs.

- It is usually assumed that fixed costs are unchanged when volume changes, so the amount budgeted for fixed overhead is the same in both the master and flexible budgets.

- This is consistent with the variable costing method of product costing.

- There are no input-output-relationships for fixed overhead.- The difference between the actual fixed overhead and the

budgeted fixed overhead at normal capacity falls under the category of a price variance (also called spending or budget variance)

- The difference between the budgeted fixed overhead and applied fixed overhead represents the volume or capacity variance

The possible causes of capacity or volume variance are as follows:

1. Poor production scheduling2. Unusual machine breakdowns3. Storms or strikes4. Fluctuations over time5. Decrease in customer demand6. Excess plant capacity7. Shortage of skilled workers

COMBINED MANUFACTURING OVERHEAD (Variable and Fixed) VARIANCE ANALYSIS:

Controllable VarianceActual Factory Overhead (AFOH) PxxLess: Budget allowed based on Std. Hrs. (BASH) Fixed (at normal capacity) Pxx Variable (Std. Hrs.* x Variable Overhead Rate) xx xxUnfavorable (Favorable) Pxx

TWO-WAY VARIANCE METHOD

Capacity or Volume VarianceBudget allowed based on Standard Hours (BASH) PxxLess: Standard hours x Standard Overhead Rate (SHSR) xxUnfavorable (Favorable) Pxx

* Standard Hours = Equivalent Production or Allowed hours based on actual production x Standard hours per unit

Total Manufacturing Overhead Variance Pxx

THREE-WAY VARIANCE METHODSpending VarianceActual Factory Overhead (AFOH) P xxLess: Budget allowed on Actual hours (BAAH)

Fixed (at normal capacity) Pxx Variable (Actual Hrs. x Variable Overhead Rate) xx xx

Unfavorable (Favorable) P xx

Variable Efficiency VarianceBudget allowed on Actual Hours (BAAH) P xxLess: Budget allowed on Standard hours (BASH)

Fixed (at normal capacity) Pxx Variable (Std. Hrs. x Variable Overhead Rate) xx xx

Unfavorable (Favorable) P xx

Volume VarianceBudget allowed on Standard Hours (BASH) P xxLess: Standard hours x Standard Overhead Rate (SHSR) xxUnfavorable (Favorable) P xx

Total Overhead Variance P xx

SPENDING VARIANCE

Actual Factory Overhead (AFOH) P xx

Less: Budget Allowed based on Actual Hours (BAAH) xxUnfavorable (Favorable) P xx

FOUR-WAY VARIANCE METHOD

VARIABLE EFFICIENCY VARIANCE

Budget Allowed based on Actual Hours (BAAH) P xx

Less: Budget Allowed based on Standard Hours (BASH) xxUnfavorable (Favorable) P xx

FIXED EFFICIENCY or EFFECTIVENESS VARIANCE

Standard Hours xx

Less: Actual Hours xxUnfavorable (Favorable) xxMultiplied by: Fixed Overhead Rate xxUnfavorable (Favorable) P xx

IDLE CAPACITY VARIANCE

Normal Capacity Hours xx

Less: Actual Hours xxUnfavorable (Favorable) xxMultiplied by: Fixed Overhead Rate xxUnfavorable (Favorable) P xx

SAMPLE PROBLEM: FACTORY OVERHEAD VARIANCES

The STD Household Company has established standard costs for the cabinet department, in which one size of MX cabinet is made. The standard costs of producing one of these MX cabinets are shown below:

Standard Cost Card – MX CabinetDirect Material: Lumber 50 board feet at P4 P200Direct Labor: 8 hours at P10 80Overhead Costs: Variable – 8 hours at P5 40

Fixed – 8 hours at P3 24Total Standard Unit Cost P344

During June 2004, 500 of these cabinets were produced. The cost of operations during the month is shown below. There are no work-in-process at the beginning and end of the month.

Direct material purchased: 30,000 board feet at P4.10 P123,000Direct materials used: 24,000 board feetDirect labor: 4,200 hours at P9.50 39,900Overhead costs: Variable costs 22,000

Fixed costs 11,000

The budgeted overhead for the cabinet department based on normal monthly activity of 4,500 hours is P36,000 of which P22,50 is variable and P13,500 is fixed overhead.

REQUIRED: Compute for the Factory Overhead Variance using: (a) Two-way analysis, (b) Three-way analysis and (c) Four-way analysis

Thank you!