Embed Size (px)

Citation preview

October 19, 2004

Document of the World BankR

eport N

o. 3

1345-U

ZU

zbekistan

Co

un

try Finan

cial Acco

un

tability A

ssessmen

t

Report No. 31345-UZ

UzbekistanCountry Financial Accountability Assessment

Operations Policy and ServicesEurope and Central Asia Region

TABLE OF CONTENTS

PREFACE ............................................................................................................................................................... i

EXECUTIVE SUMMARY .................................................................................................................................. iv

I . COUNTRY 'BACKGROUND .......................................................................................................................... 1

GOVERNING STRUCTURES ....................................................................................... ......................... 1 ECONOMIC BACKGROUND AND PROSPECTS ...................... .......... ...... 1 RELATIONSHIP OF THE CFAA. LESDING PROGRAM AND P LOGUE IES 2

I1 . PUBLIC SECTOR BUDGET MANAGEMENT ..................................................... 4

INTRODUCTION .................................................................................................................................................... 4 PRINCIPLES AND RISKS ........................................................................................................................................ 4 THE SCOPE OF THE BUDGET ................................................................................................................................. 5 THE BUDGET PREPARATION PROCESS ................................................................................................................... 6 TRANSPARENCY AND ACCOUNTABILITY ASPECTS OF THE BUDGET PROCESS ......................................................... 6 BUDGET EXECUTIOS AND CASH MANAGEMENT ISSUES . RECENT AND PROPOSE MAIN RECOMMENDAT

Short term (within ......................................................................................................................... 9

I11 . EXTRA BUDGETARY FUNDS ....................................................................................... 11 Medium term (one to three years) ............................................................................................................... 10

INTRODUCTION . ..................................

Budget and cash management issues Governance issues

MAE RECOMMENDAT Short term (within Medium term (one ............................................................................................................... 14

I V . PUBLIC SECTOR ACCOUNTING AND FISCAL REPORTING ....... 16

INTRODUCTION .................................................................................................................................................. 16 Budget Reporting ........................................................................................................................................ 18

MAIN R E C O M ~ E N D A T I O ~ S ................................................................................................................................ 19 Short term (within one year) ....................................................................................................................... 19 Medium term (one to three years) . 19 Long term (over three years) 19

V . SELECTED REVENUE ADMINISTRATION ISSUES .................................. 21

INTRODUCTION .................................................................................................................................................. 21 ORGANIZATIONAL STRUCTURE OF TAX ADMrrl'lSTRATION ................................................................................. 22 ACCOUNTING, REPORTING AND CONTROL OF REVENUES ................................................................................... 23 MAIN RECOMMENDATIONS ................................................................................................................................ 24

Short term (within one year) ....................................................................................................................... 24 Medium term (one to three years) .............................................................................................................. 24

V I . INTERNAL CONTROLS AND INTERNAL AUDIT ..................................... 25

INTRODUCTION ... ...... 25 CURRENT SYSTEMS OF INTERh'AL CONTROL IN UZBEKISTAN 26 TOWARDS AN IMPROVED REGIME OF INT ................................... 26 b K K l V T I O N A L ARRANGEMENTS FOR FIN OF THE CONTROL AND 27

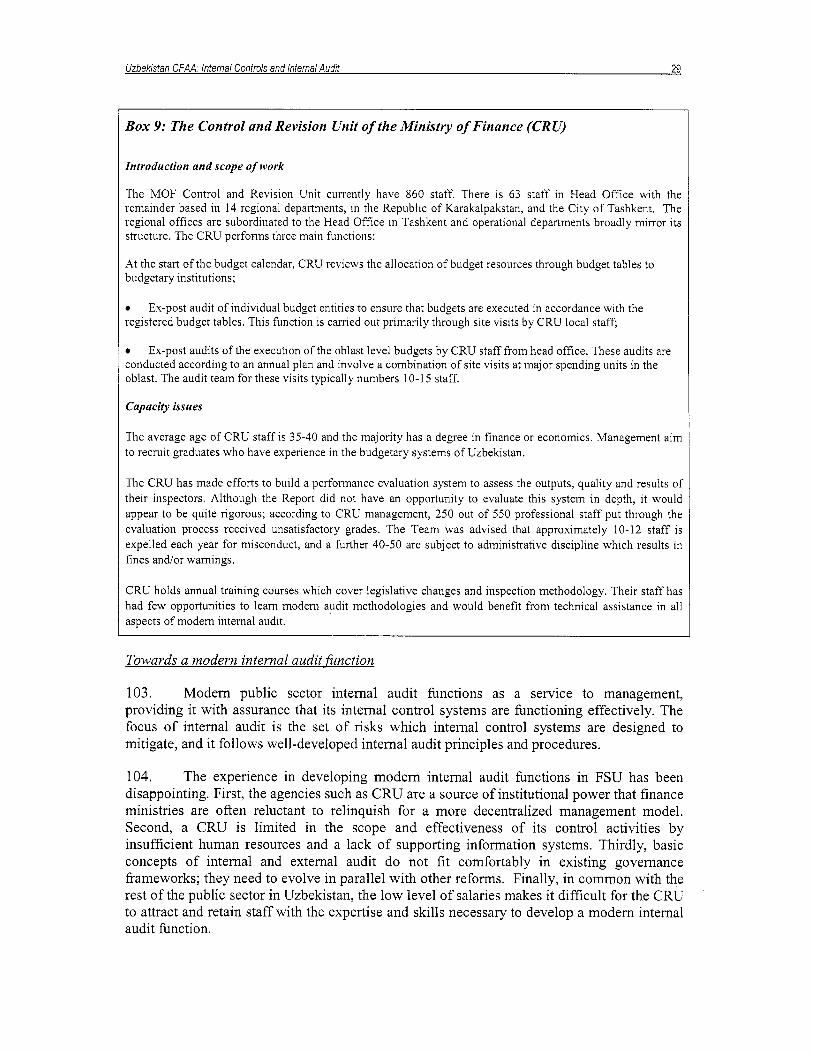

Introduction ................................................................................................................................................. 27 The Control and Revision Unit of the M in i s t y ofFinance (CRU) .............................................................. 28 Towards a modern internal audit function .................................................................................................. 29

M A I N RECOMMENDATIONS ............................................................................................................................... 30 Short term (within one year) ....................................................................................................................... 30 Medium(one to three years) ........................................................... ....... ................................ 30

Long term (over three years) ....................................................................................................................... 31

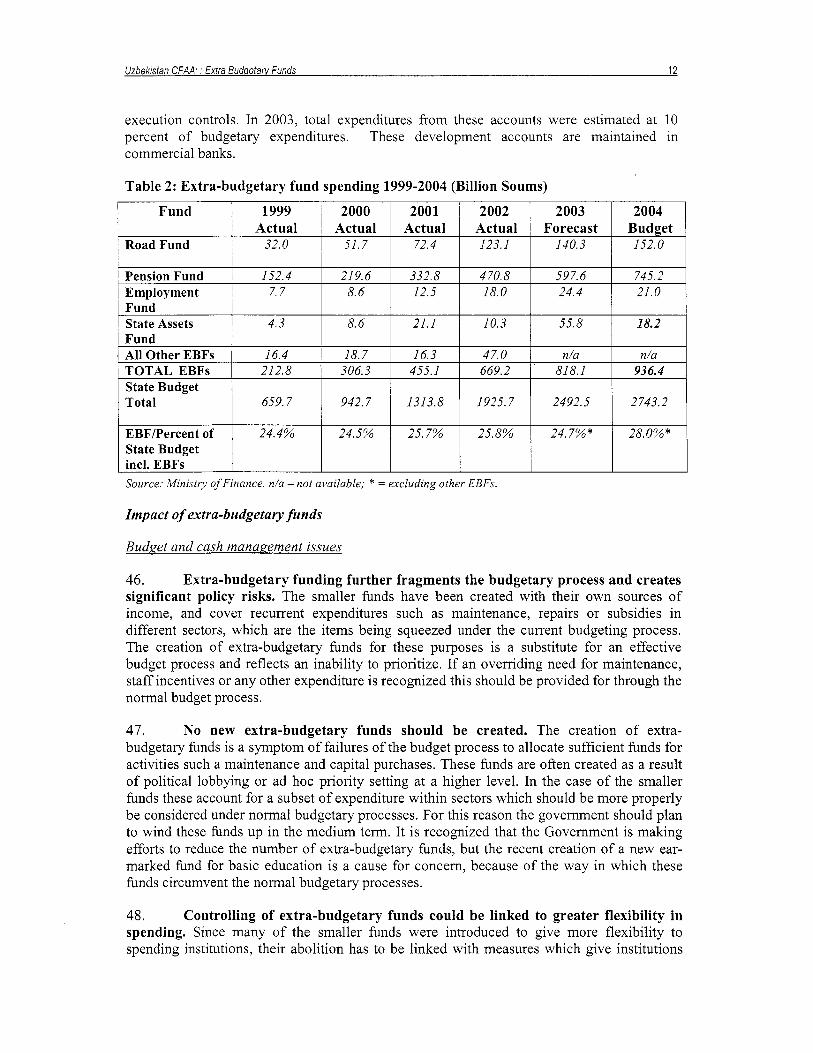

VI1 . EXTERNAL AUDIT ............................................................................................................... 32

INTRODUCTIOS PROGRESS ON T MAIN RECOMM ...................... ............................................................................................ 33

Medium term (one to three years) ............................................................................................................... 34 Long term (over three years) ....................................................................................................................... 34

VI11 . PUBLIC ENTERPRISES .................................................................................................. 35

INTRODUCTION

GOVERNANCE OF PUBLIC ENTERPRISES MAIN RECOMMENDATIONS .................. .......................................

Long term (over three years) ....................................................................................................................... 38 I X . FINANCIAL MANAGEMENT ARRANGEMENTS IN BANK- FUNDED PROJECTS ........................................................................................................................ 40

I~TRODUCTION .................................................................................................................................................. 40 FINANCIAL MANAGEMENT ARRANGEMENTS ..................................................................................................... 40

Institutional arrangements 40 Financial Management 41

TOWARDS MAPSTREAMIN INANCIAL MANAGEMENT 42 ANNEX I: Development Action Matr ix ............................................................................................................ 43

ANNEX I1 - International Standards and Codes .............................................................................................. 50

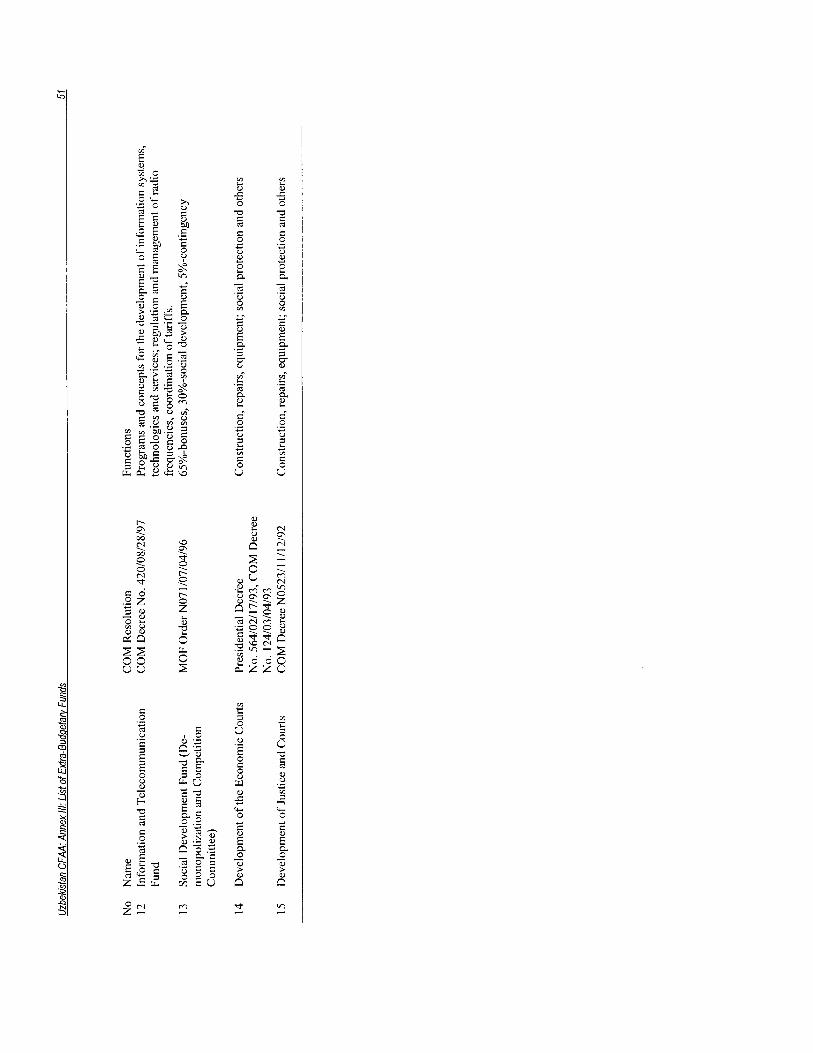

ANNEX 111: L i s t o f Extra-Budgetary Funds .................................................................................................. 51

ANNEX IV : Overview Of Governance Arrangements - Major Extra Budgetary Funds ............................ 53

TABLES

Table 1: World Bank Lending to Uzbekistan ($ Millions) ............................................................................... 2 Table 2: Extra-budgetary fund spending 1999-2004 (Billion Soums) ............................................................ 12 Table 3: Revenues o f the State Budget o f Uzbekistan (Mil l ion soums) .......................................................... 22 Table 4: Standards and Codes Promoting Financial Accountability ............................................................. 50

BOXES

Box 1: Budget Management . Institutional Issues . Key Messages from the World Bank Public

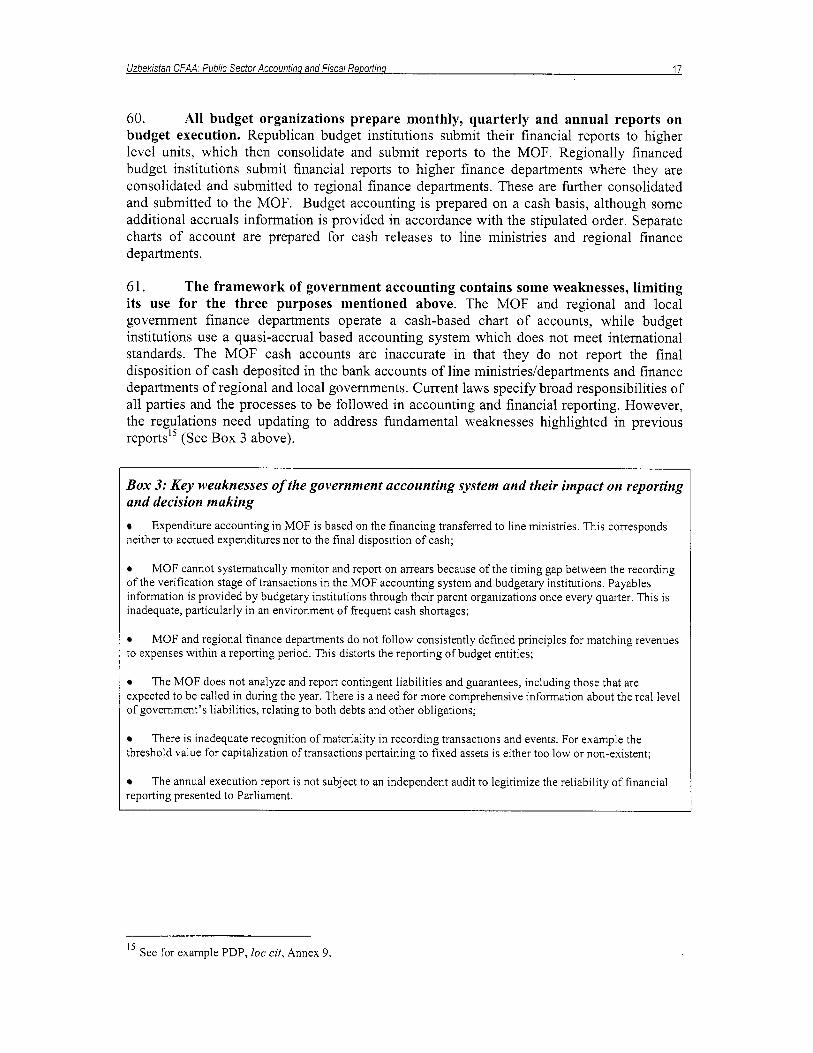

Box 2: Improving Financial management of Extra-budgetary funds ............................................................. 14 Box 3: Key weaknesses o f the government accounting system and their impact on reporting and decision making 17 Box 4: Proposed development o f government accounting standards ..................................................... 18 Box 5: Institutional Arrangements fo r Tax Policy and Administration in Uzbekistan ................................. 23 Box 6: The Control and Revision Unit (CRU) of STC ..................................................................................... 24 Box 7 : Three main features of a modern internal control systems ................................................................. 25 Box 8: Important reforms to improve public sector internal controls ............................................................ 27 Box 9: The Control and Revision Unit of the Ministry of Finance (CRU) ..................................................... 29

Expenditure Review, 2004 (PER) ......................................................................................................................... 5

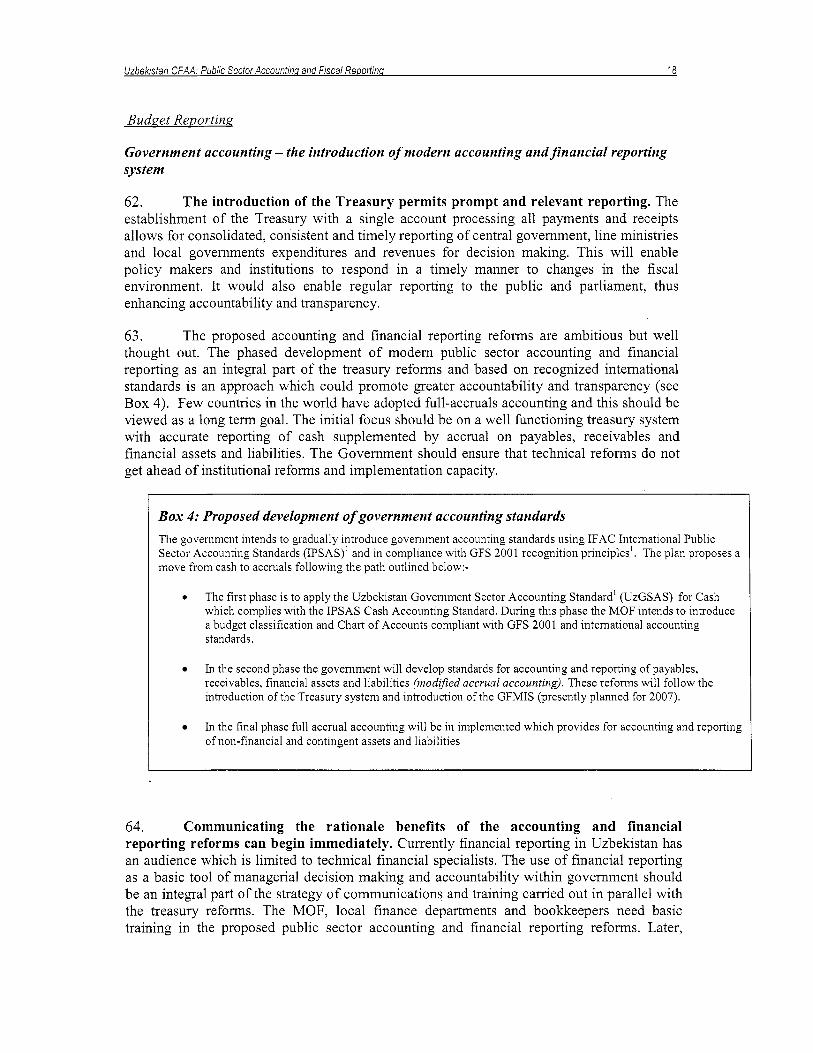

PREFACE

This report was prepared after missions to Uzbekistan in 2003 and 2004 by a Task Team comprising Andrew Mackie (Task Team Leader, ECSPS), John Ogallo (Senior Financial Management Specialist, ECSPS), Andy Macdonald (Public Sector Consultant) and Nurmukhammad Yusupov (Consultant).

This report i s based on the results o f interviews and discussions with various public sector institutions as well as an analysis o f data gathered during the mission including copies o f relevant legislation, instructions and reports. Many Government counterparts lent their support to the CFAA Mission and engaged in the dialogue. The Bank i s grateful for this cooperation.

Objectives of the CFAA

The overall objectives o f the Uzbekistan CFAA are to (i) help the government strengthen i t s public sector financial accountability arrangements; (ii) identify and document the most significant fiduciary r i sks ' in the Government public financial management systems (PFM); (iii) document the existing program o f reforms and capacity building to improve transparency and accountability aspects o f the PFM, making additional recommendations for capacity building, if necessary.

This i s the f i rst CFAA prepared by the Bank in Uzbekistan. I t s timing i s particularly relevant in the context o f a period drastic fiscal adjustment and an increased focus on the efficiency and effectiveness o f public spending. Changes to the constitution and budgetary reforms are being undertaken by the Government, with support from the donor community. The public financial management framework in Uzbekistan i s s t i l l evolving, and improvements are required in many o f i t s components. The CFAA provides an analysis o f current issues, focusing on practical, realistic and sequenced improvements in the country's P F M systems, taking into account the considerable capacity constraints in Uzbekistan. In this sense the C F A A i s primarily a forward looking assessment rather than a diagnostic o f existing problems, which have already been extensively documented in previous reports.

Since borrower countries often look for benchmarks against which their systems can be measured, this report contains clear references to those internationally accepted standards and codes which inform the most essential financial management tasks, such as budgeting, accounting, internal control, internal audit and extemal audit. In l o w capacity countries such as Uzbekistan many o f these standards should be seen as longer te rm goals which have be used to frame legislative reform and capacity building initiatives, rather than benchmarks for the assessment o f current P F M systems. A preliminary l i s t o f international standards and codes i s contained in Annex I1 to this Report as a reference document.

Experience from other countries has shown that, to be successful, reforms to the institutions and mechanisms o f financial accountability should not been seen as an end in themselves but rather as part o f broader economic, political, and fiscal reforms within government. Therefore, one o f the other objectives o f the Uzbekistan C F A A has been to explain the rationale for reform in a way which encourages broad dissemination beyond technical

' The fiduciary risk i s the r i s k o f funds not being spent for the purposes for which they have been appropriated.

.. Uzbekisfan: Counfw Financial AccountabUity Assessment 11

financial specialists within the Government. The CFAA complements two other pieces o f Bank diagnostic work; the Country Procurement Assessment Report (CPAR) wh ich was completed in 2003 and a Public Expenditure Review (PER) wh ich i s being prepared in parallel with the CFAA.

Approach

The core content o f the CFAA i s l isted below. Where possible the CFAA documents rather than duplicates analytical work camed out by the Bank and the rest o f the donor community. Where a particular i t em i s being addressed by another initiative, that donor i s identified.

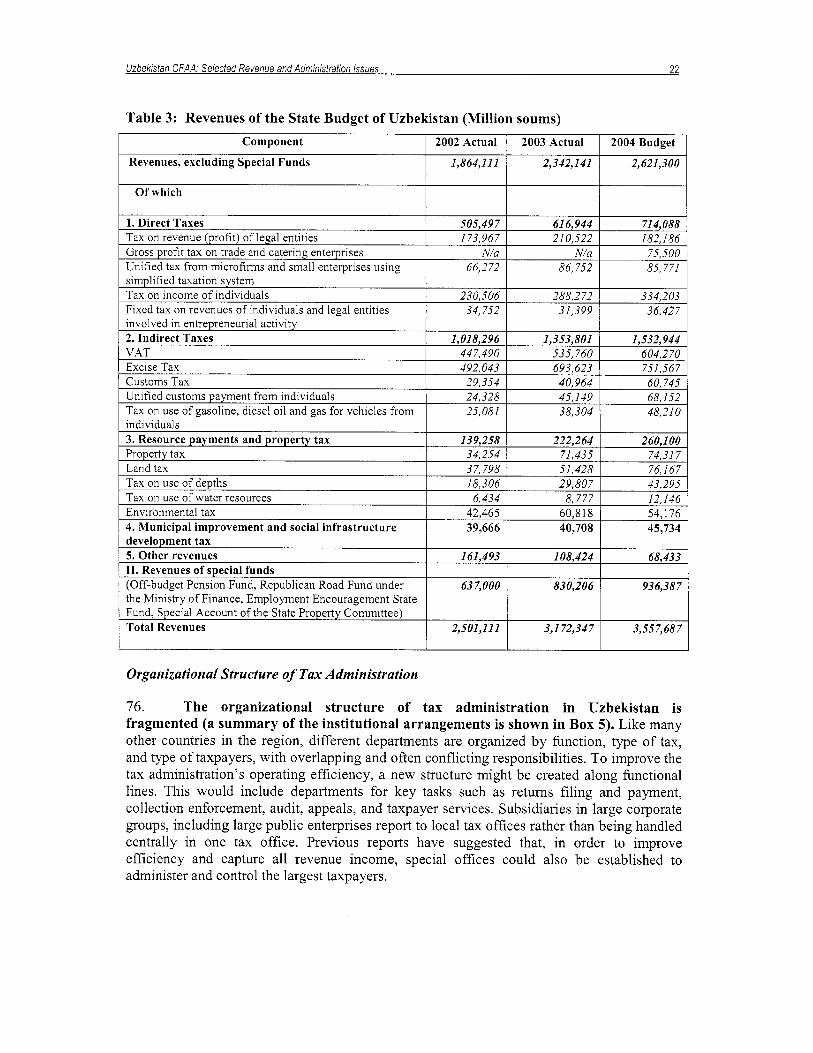

Public sector budgeting [IMF, WB, USAID, U S Treasury, EU TACIS ] - - -

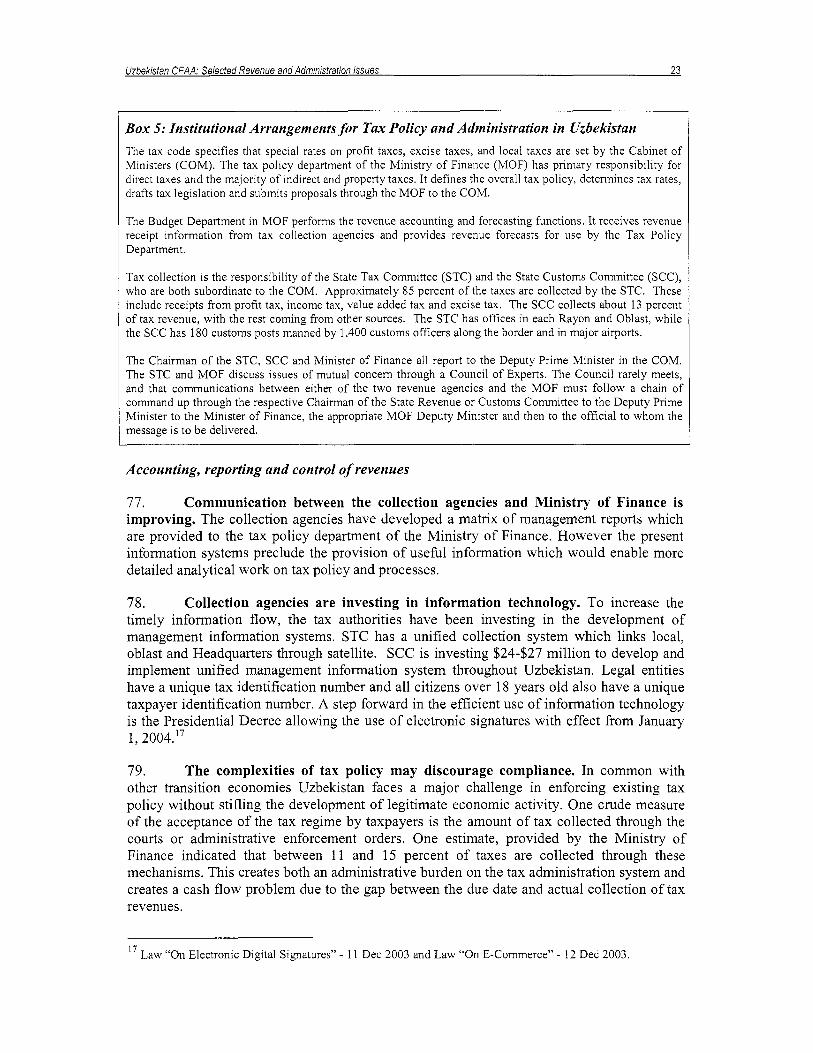

scope o f the budget (including the treatment o f extra-budgetary funds); transparency and accountability aspects o f the budget process; budget execution and cash management.

Selected revenue issues [CFAA]

Public enterprises [AsDB]

Public sector accounting and reporting [IMF, WB PFMP, CFAA]

Internal controls and internal audit [CFAA]

External audit and parliamentary oversight [CFAA]

- monitor ing and oversight - governance, f inancial reporting and audit

Arrangements for managing the proceeds o f Bank lending [CFAA]

During the scoping mission it was recognized that the CFAA Team w o u l d b e able to conduct a desk review o f m u c h o f the budget function and place reliance o n previous diagnostic w o r k and work ing closely with W o r l d Bank staf f conducting the Public Expenditure Review (PER) and the Public Financial Management Reform Project (PFMR). Beyond the consolidated state budget the government o f Uzbekistan carries out significant amounts o f resource redistribution through extra-budgetary accounts and funds, lending policies and publ ic guarantees. Given the orientation o f the CFAA and the overall materiality o f the amounts involved, the Team focused considerable attention o n the scope o f the budget entity, accountability and transparency aspects o f extra-budgetary funds and publ ic enterprises.

Accounting, internal controls/internal audit and external audit are specific areas wh ich have not received much attention in previous diagnostic reviews and have therefore been analyzed in support o f the Government’s treasury and constitutional reforms.

Public procurement has been covered extensively in the March 2003 Country Procurement Assessment Report (CPAR). In summary, the report noted that the legislative framework, institutions and enforcement regime fo r publ ic procurement are under developed. Overall the C P A R gave the procurement environment a high-risk rating. The k e y findings o f direct relevance to the CFAA are (i) that bo th internal and external controls over procurement are inadequate; (ii) procurement-related corruption i s a threat to publ ic expenditure and; (iii) the private sector has l i t t le fa i th in the fairness o f publ ic tenders. The CPAR also recommended that internal and external audit controls over procurement should b e strengthened.

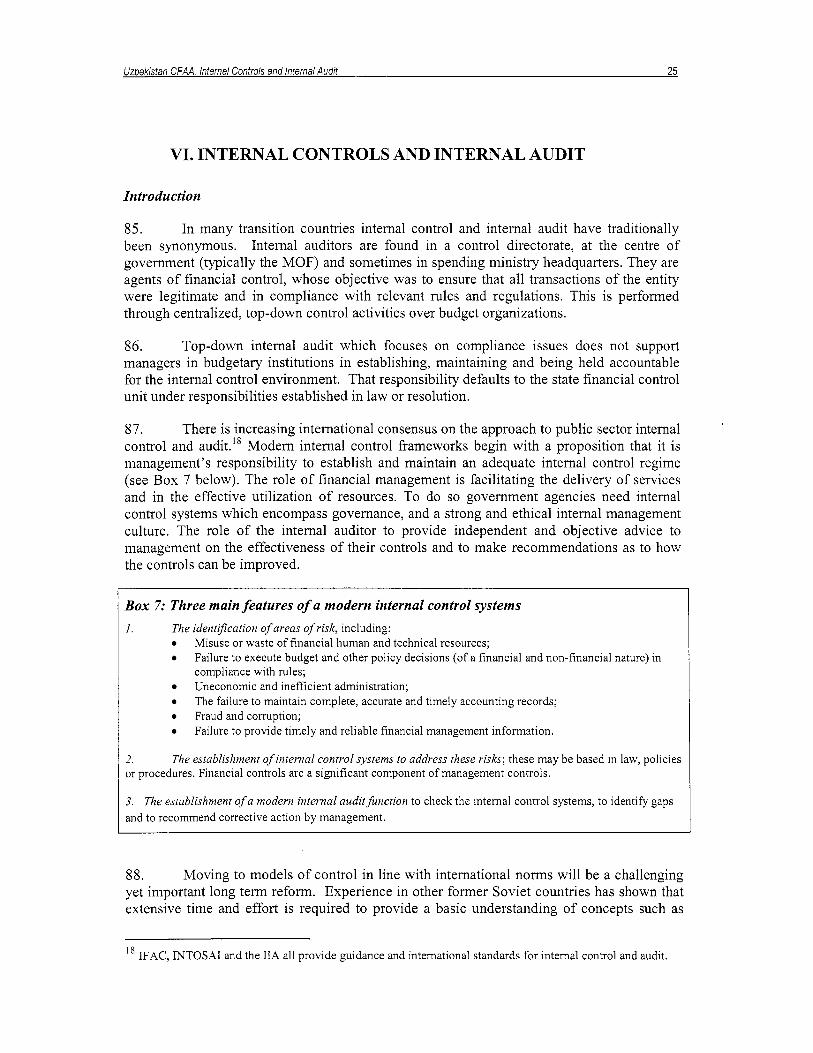

... Uzbekistan: Country Financial Accountabilifv Assessmenf 111

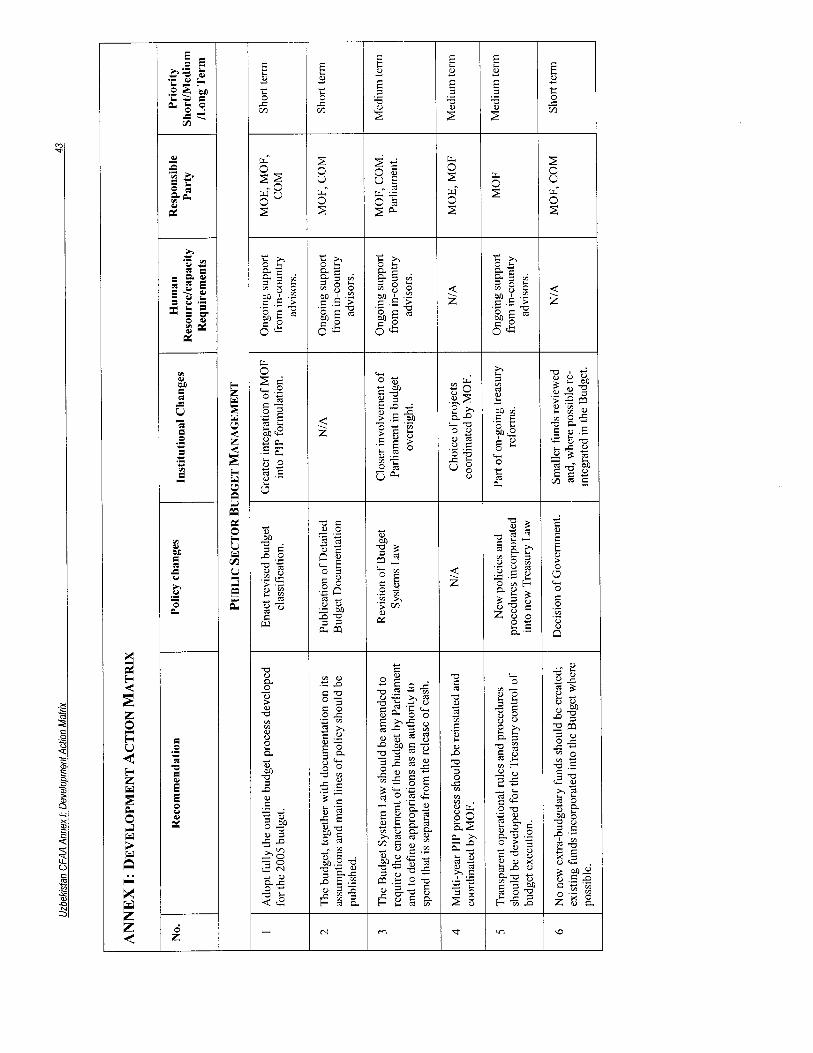

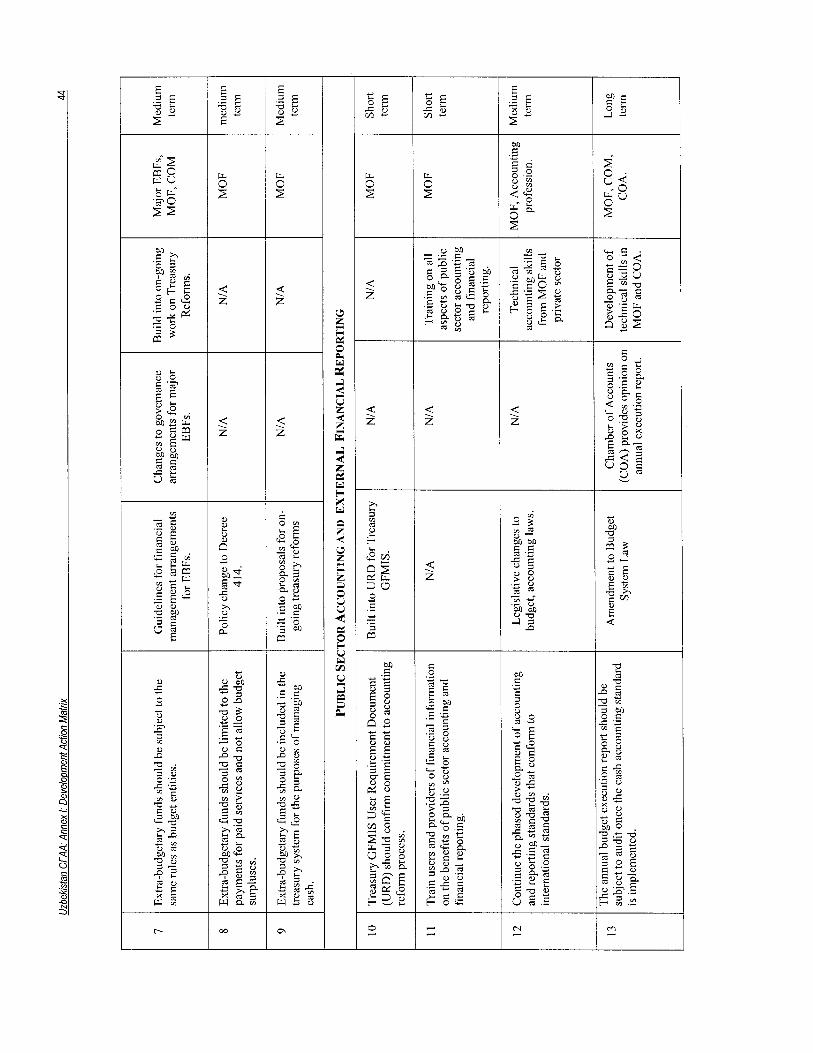

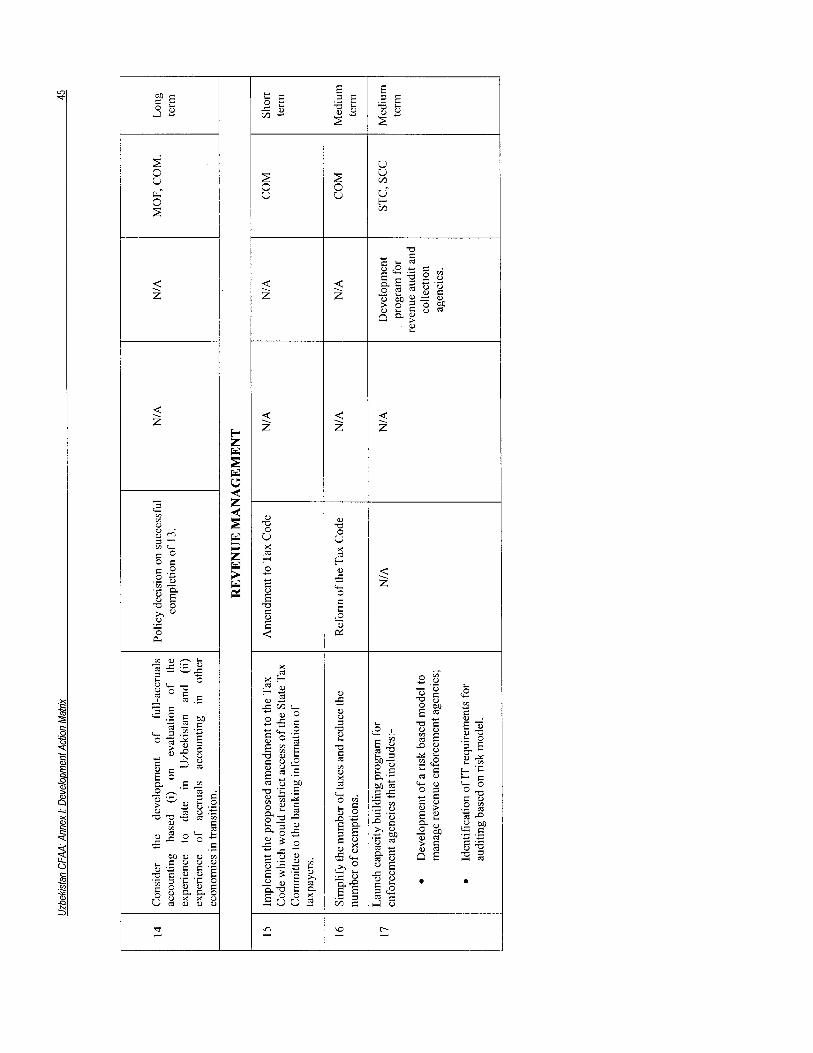

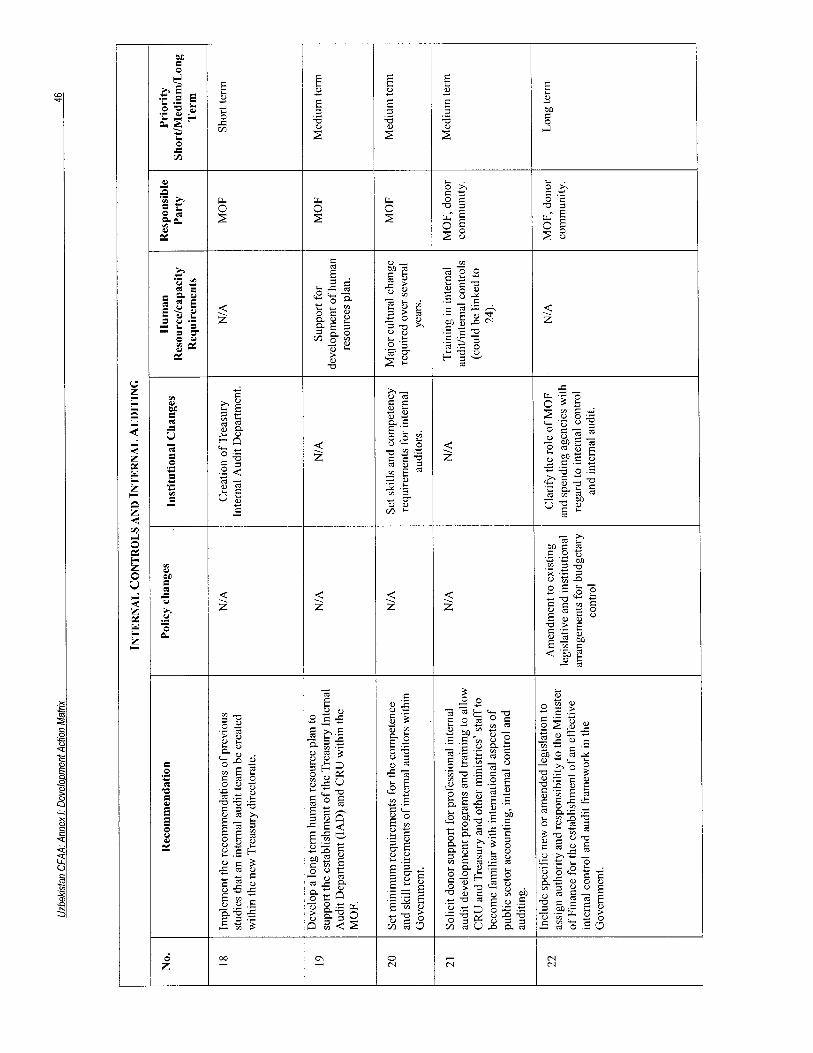

The assistance provided by donors supports Government’s efforts to establish modern financial institutions and develop staff s k i l l s and capabilities to enable it to manage i t s own affairs. The CFAA identifies those init iatives already underway, assesses the Government’s progress in each area and comments o n their fu ture plans. Where additional actions are recommended these are presented in a Development Act ion M a t r i x (see Annex I), which ident i fy a series o f proposals highlight (i) legislative reforms, (ii) institutional arrangements, (iii) human resource and capacity building and (iv) suggested timing (short, medium or long term) o f implementation o f the proposed action.

Acknowledgements

The C F A A team wishes to acknowledge the extensive and grateful cooperation and assistance received f rom staff in the various institutions who contributed to the CFAA, including officials and staff o f the Government, state agencies and enterprises, and bi-lateral and multi lateral organizations. Grateful thanks also go to the Bank’s Public Expenditure Review and Public Financial Reform Project task team, particularly Ritu Anand and Roland Clarke. In addition Mar t i n Raiser (Uzbekistan Country Manager) and Bakht ior Abdullaev (Uzbekistan Country Officer) provided invaluable in-country assistance and information. John Hegarty (Manager, Financial Management, ECA), Pascale de K e r v y n Lettenhove (ECSPS) and peer reviewers, D im i ta r Radev (IMF), Roland Clarke (ECSPE) and Hisham Ahmed W a l y (MCACS) offered m u c h appreciated comments and inputs.

Uzbekistan: CFAA Executive Summaw iv

EXECUTIVE SUMMARY

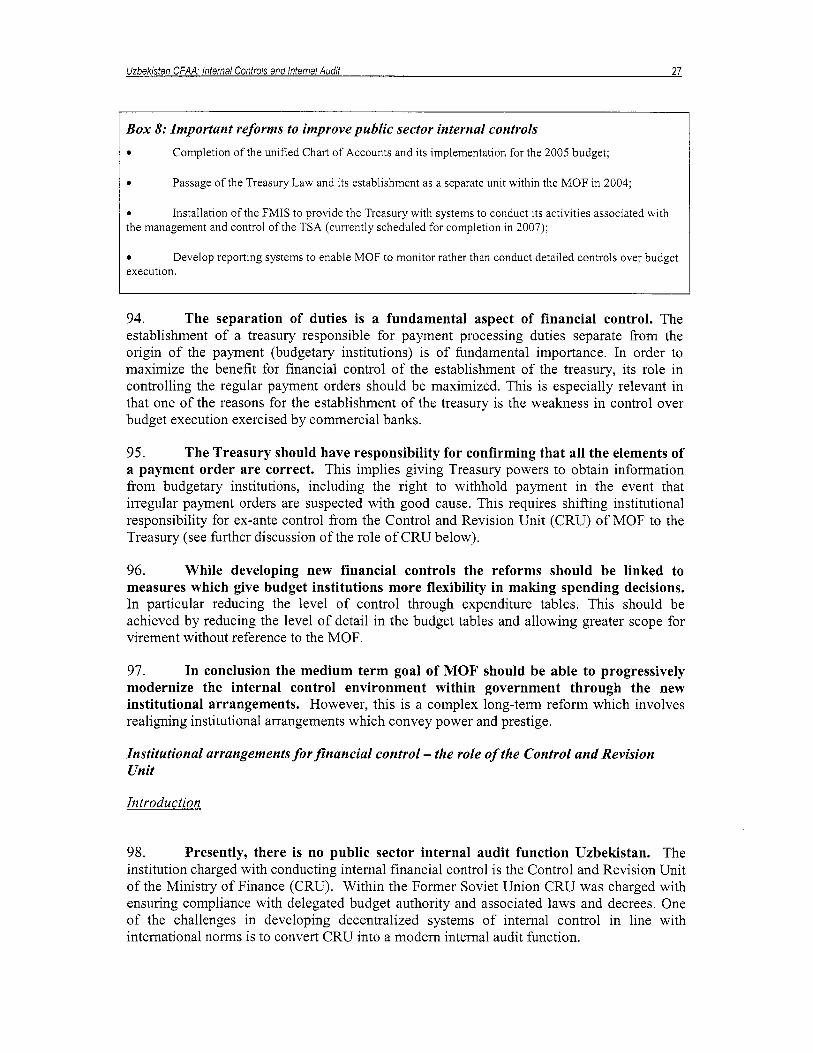

Introduction

Since declaring i t s independence in August 1991 Uzbekistan has taken a markedly different course f rom most Commonwealth o f Independent States (CIS) countries by fol lowing a gradual transition to a market economy and adopting a development strategy aimed at accelerated industrialization. Wh i le taking in i t ia l steps to the transition to a market-based economy, the State has retained the levers o f control over the reform process and an extensive ro le in the economy.

In the past f ive years Uzbekistan has faced a drastic fiscal adjustment fo l lowing a decline in budget revenues. The aggregate level o f government spending has come down, extra- budgetary funds have been reduced and streamlined somewhat, and redistribution through quasi-fiscal operations has decreased. General government expenditures, including those financed by government guaranteed borrowing, have come d o w n by over 11 percentage points o f GDP since 1998.

The out look i s for publ ic resources to become scarcer as the reforms progress further. It i s v i ta l that the Government focus o n the effectiveness o f publ ic spending and min imize and inefficiencies. There are a number o f elements o n which the Government could build improvements to the framework o f publ ic accountability. A new Constitution has been passed and a bi-cameral parliamentary system began operations in January 2005. M a j o r reforms to the health and education sector have begun. Elements o f the budget process are already being addressed through the development o f revised budget preparation procedures and the introduction o f a treasury system.

These reforms require fundamental changes to the institutions o f government and to the attitudes o f public servants. Pol icy mak ing functions o f spending ministries need to be developed and accountability f o r po l i cy and spending decisions needs to b e clarified. Management in budgetary institutions needs new tools and institutions to establish, maintain and be held accountable for the internal control environment.

This Report has been prepared with the overriding goal o f helping the government in their efforts towards strengthening control and accountability and supporting greater efficiency o f publ ic spending. The Report examines a l l areas o f publ ic sector accountability, including accountability and transparency aspects o f the budget, accounting and external financial reporting, revenue management, the internal control environment, internal and external audit and governance o f publ ic enterprises. The goal has been to present a fonvard-looking analysis o f current issues, focusing o n practical, realistic and sequenced improvements in the Country’s publ ic financial management systems. The recommendations have taken into account the considerable capacity constraints in Uzbekistan and the l imi ted history o f re form in an environment marked by severe deficiencies in transparency and accountability.

Ultimately, technical improvements in financial management will on l y be successful if they are supported by overarching institutional, economic and pol i t ical reforms. Good financial management practices underlie government’s accountability to i t s citizens through a transparent, efficient and effective use o f publ ic funds:

Uzbekistan CFAA: Executive Summary V

The k e y analysis and recommendations for establishing a sound financial accountability framework are described in the fo l lowing paragraphs:

Public sector budget management

Budget management processes in Uzbekistan create considerable r i s k s to the Government. The f i rst r i s k i s a po l i cy risk; it i s the risk that policies passed by Parliament are not implemented through the budget. The second risk, a budget and financial management risk, i s the possibil i ty that funds are no t spent according to their intended use. This risk i s compounded by a large share (about 25 percent) o f off-budget resources not subject to budget scrutiny.

I n Uzbekistan, the policy risk is signiJicant owing to process and institutional breakdowns between policies and budgeting. The greatest challenge in the re fo rm o f Uzbekistan’s publ ic finances i s to make the transition f rom institutions inherited f rom the centrally planned economy, to ones in wh ich po l i cy mak ing i s l inked to budgeting. M u c h o f the reform process requires fundamental changes, largely outside and beyond the Ministry o f Finance. First, the Government should clarify the l ong term role o f the publ ic sector in the economy, with a v iew to accelerating the transition towards a market-based economy supported by transparent and accountable publ ic institutions. Whi le economic and sector policies are developed, institutions should b e established at the center o f government to coordinate strategic po l i cy choices. Spending ministries should be reorganized along functional lines and include under them many o f the state institutions which deal directly with the MOF. N e w budgeting processes and the establishment o f the Treasury, will o f course require w o r k within the MOF. However, until n o w budget reform has largely been centered around technical developments within the MOF. One o f the m a i n tasks for the MOF i s to make the case to the Government and publ ic institutions for the need for reforms and the l ong term benefits that will ensue.

There is also a high risk that funds may not be used for their intended purposes, as the budget lacks comprehensiveness and limited budget information prohibits meaninaful budget scrutiny. The present budget i s no t comprehensive, and the budget process i s fragmented. Extra-budgetary funds account fo r one quarter of state budget expenditure and are not subject t o the same scrutiny as the budget. In addition, the formulat ion o f investment budget i s a separate process; there i s n o mechanism for consideration o f the impact o f future recurrent costs in evaluating new investments, nor i s there a mechanism for debt recording o f externally financed investments.

The C F A A recommends that n o n e w extra-budgetary funds b e created and that existing funds should be subject to the same rules for budget preparation, rev iew and audit as the budget. In addition, the process fo r recurrent and investment budget preparation should be merged with due consideration o f recurrent costs and debt impact in later years.

The transparency o f budget documentation also needs to b e significantly improved. The present budget classification i s rudimentary and insufficient to analyze the development o f po l i cy or serve as a basis to h o l d spending units accountable through budget execution. Transparency and accountabil ity w o u l d be enhanced by the publ icat ion o f budget documentation wh ich includes the budget, macroeconomic forecasts and an explanation o f the ma in budgetary measures.

In Uzbekistan, the present budget execution arrangements are inef f ic ient and non-transparent; exposing the government to the risk (a) that payments are n o t made in accordance with the

Uzbekisfan CFAA: Executive Summary vi

budget, (b) that payments are not made on a timely basis and distort the implementation o f government activities and (c) that finance officials have insufficient information to make the most effective and efficient use o f cash. Disbursement takes place through numerous government bank accounts held in commercial banks. This makes budget implementation difficult to monitor and liquidity impossible to manage. Numerous extra-budgetary accounts fbrther weaken liquidity management, budget execution monitoring and control. These problems are recognized by M O F who has begun work on the introduction o f a treasury system wi th the support o f the IMF and Wor ld Bank. The establishment o f the Treasury requires a major institutional reorganization o f MOF and considerable capacity building in the finance function across al l areas o f government.

Public sector accounting

Uzbekistan’s public sector accounting traditions were inherited from the Soviet Union; where budget reporting was merely a financial reflection o f detailed production plans. Developing a modem accounting system and financial reporting system will protect and manage public money and discharge accountability. The government has a large number o f bookkeepers who are familiar wi th double entry, accrual based accounting but who are reliant on manual systems and will need training on modem financial accounting and reporting. As part o f the treasury reforms the Government has developed a well thought-out development plan for the phased introduction o f accounting reforms based on International Public Sector Accounting Standards (IPSAS). The Report recommends that training on public sector accounting begins immediately and cautions against ambitions running ahead o f available capacity. Specifically, accruals accounting should remain a long term goal once the government has successfully implemented and reported in compliance with the cash basis o f accounting.

Revenue administration issues

As regards the revenue collection agencies the Report notes the Government’s investment in management information systems and efforts to improve the quality o f reporting between collection agencies and MOF. However, the Government s t i l l faces a major challenge o f enforcing tax pol icy without stifling the development o f legitimate economic activity. The complexities o f the current tax policy may discourage compliance. The CFAA also echoes previous reports in recommending that the commercial banking sector stops acting as a de- facto tax enforcement agency. The Report also recommends that the Government pass a proposed amendment to the Tax Code restricting access to taxpayers’ banking information.

Internal control and internal audit

In common wi th other transition economies in the region concepts o f internal control and internal audit are not well understood. The present fragmented execution system (discussed above) results in a loss o f budgetary control which can be addressed, in part through the reform o f treasury systems. Long t e r m reforms to institutions which monitor and control the budgetary process are also required. The present approach o f the Control and Revision Unit o f MOF (CRU) focuses on top-down controls over compliance which do nothing to support managers in budgetary institutions establish, maintain and be held accountable for the internal control environment. The Report proposes a phased approach to reform which builds capacity in tandem with the on-going treasury reforms and prepares C R U for a long te rm role as a modem internal audit department within Government.

Uzbekistan CFAA: Executive Summary vii

External audit

Effective external audit provides an independent assessment that the overall objectives set by Parliament and government have been reflected in the budget, scrutinizes the overall quality o f public expenditure, and management o f public assets and liabilities. To date l imited progress has been made on the development o f an independent public sector external audit function in Uzbekistan. The constitutional and budgetary reforms present an opportunity to develop such an institution. A small Chamber o f Accounts (COA) has been created within the President’s Office and could be developed into an external audit function. The Report proposes a four point development plan: (1) establishing a legislative base for the audit function; (2) increasing the transparency and disclosure o f i t s work; (3) providing additional resources to the COA; and (4) enlisting the support o f the international community to assist in i t s development. A long term goal for the C O A should be to provide a professional opinion on the government annual budget report based on international accounting standards.

Public enterprises

Uzbekistan s t i l l has a large number o f public enterprises. Due to ill-defined l ines o f authority there i s l i t t le external and internal discipline on corporate performance, and litt le separation between government and business. The Report recommends reforms to the regulatory framework; separating pol icy and regulatory activities where conflicts o f interest arise and privatizing commercial operations so they do not have access to state powers. The transparency o f financial information should be improved by a phased introduction o f publicly available financial reports prepared and audited in accordance with international standards o f accounting and auditing.

Capacity building

The capacity o f the Government to absorb and implement an ambitious series o f public sector financial management reforms wil l be a challenging long te rm exercise. Financial management training i s needed in a l l public sector institutions but the needs are particularly acute in the regions and in budgetary institutions. Many finance officers have had no formal training since the 1980’s and there i s a lack o f computers and basic guidelines to assist staff. Many o f the international developments in budgeting, accounting and auditing are completely new to technical finance specialists. They need broad exposure to the latest techniques which should also be introduced into academic programs. A high level o f literacy and numeracy, an adaptable population, and well-developed educational institutions offer obvious opportunities for improvement.

Development Action Matrix

The assistance provided by donors supports the Government’s efforts to establish modem financial institutions and to develop staff sk i l l s and capabilities to enable it to manage i t s own affairs. The CFAA identifies those initiatives already underway, assesses the Government’s progress in each area and comments on their future plans. Where additional actions are recommended these are presented in a Development Action Matr ix (see Annex I), which identifies a series o f proposals highlighting, if applicable (i) legislative reforms, (ii) institutional arrangements, (iii) human resource and capacity building and (iv) suggested timing (short, medium or long term) o f implementation o f the proposed reform.

Uzbekisfan CFAA: Execufive Summaw viii

*Underpinning a genuine reform process i s the improvement in transparency o f Government’s management o f publ ic resources. At this juncture, the Government could demonstrate i t s commitment to greater transparency with the fo l lowing measures (included in the Matr ix) which do not requir ing external assistance.

1. Budget preparation should b e made more transparent with the publication o f the budget, together with documentation o n i t s assumptions and ma in lines o f po l icy

2. In the area o f extra-budgetary fund management, at a minimum n o new extra- budgetary fund should be created; and existing funds should be incorporated into the Budget where possible. In addition, the Government should amend Decree 414 to limit extra-budgetary funds to the payments o f pa id services and not a l low budget surpluses.

3. Revenue management needs to be made more transparent: the Government should implement the proposed amendment to the Tax Code to restrict access o f the tax authorities to the banking informat ion o f taxpayers.

4. The Government should enhance transparency in publ ic enterprise management by selecting two publ ic enterprises for p i lo t audits o f their 2004 financial statements according to international standards. The results o f these audits should be published.

At the same time the Government should also start exploring possible external support for medium-term reforms particularly in the areas o f internal and external audit.

* Reforms in financial management and accountability do no t happen in a vacuum. Such reforms are unl ikely to succeed unless overall pol i t ical conditions and commitment i s fueling them. In addition to pol i t ical commitment, the management o f the transition has to be thought through. Finally, linkages between publ ic financial management and overall public sector reforms have to be understood and addressed.

Uzbekistan: CFAA Countrv Backaround 7

I. COUNTRY BACKGROUND

Governing Structures

1. An independent Uzbekistan was created in 1991. O f the 15 countries which emerged f rom the breakup o f the Soviet Union, i t i s the third largest in terms o f population (25.2 mil l ion) and the fourth largest in terms o f land mass (447,000 square kilometers). Islam Karimov has been the country’s President since independence.

2. Following a referendum, the Constitution has been amended to permit the creation o f a bicameral parliamentary system that began operations in January 2005, replacing the present unicameral system. This wil l consist o f an elected upper house (Senate) and an elected lower house (Legislative Chamber). A number o f powers previously exercised by the President have been transferred to the Senate, including the appointment o f the Prime Minister. The President has stated that the full time representatives o f the lower house will focus principally on legislative issues while the Senate wil l provide for territorial representation. Under the revised Constitution the President’s term o f office was also extended from 5 to 7 years.

Economic background and prospects

3. W h i l e taking init ial steps to the transition to a market-based economy, the State has retained an extensive role in the economy. The state continues to be involved in a wide range o f off-budget economic activities managing whole sectors o f the economy such as cotton production. Instances such as when the authorities require enterprises to perform work without payment, for example by providing employees for cotton picking or paying for urban beautification projects, point to a much larger influence o f the state than i s indicated by the quantifiable fiscal and quasifiscal operations. If control over the economy through parastatal industrial associations and state-owned commercial banks, centralized planning o f production and distribution, and heavy regulatory burden are added, the reach o f the state i s greater s t i l l . Progress in privatizing large f i rms in the banking, mining and utility sectors such as telecommunications, energy, and transport has been slow. T h e slow transition o f the Uzbek economy resulted in high levels o f Government revenues and expenditures for public and publicly guaranteed investment and extra-budgetary funds, which reached 60 percent o f GDP in the mid-1990s. In the past five years there has been a drastic fiscal adjustment following a decline in budget revenues. Between 1998 and 2003 consolidated budget expenditures, including extra-budgetary funds and net lending were slashed by 10 percentage points o f GDP. The aggregate level o f government spending also saw similar dramatic declines during the period.

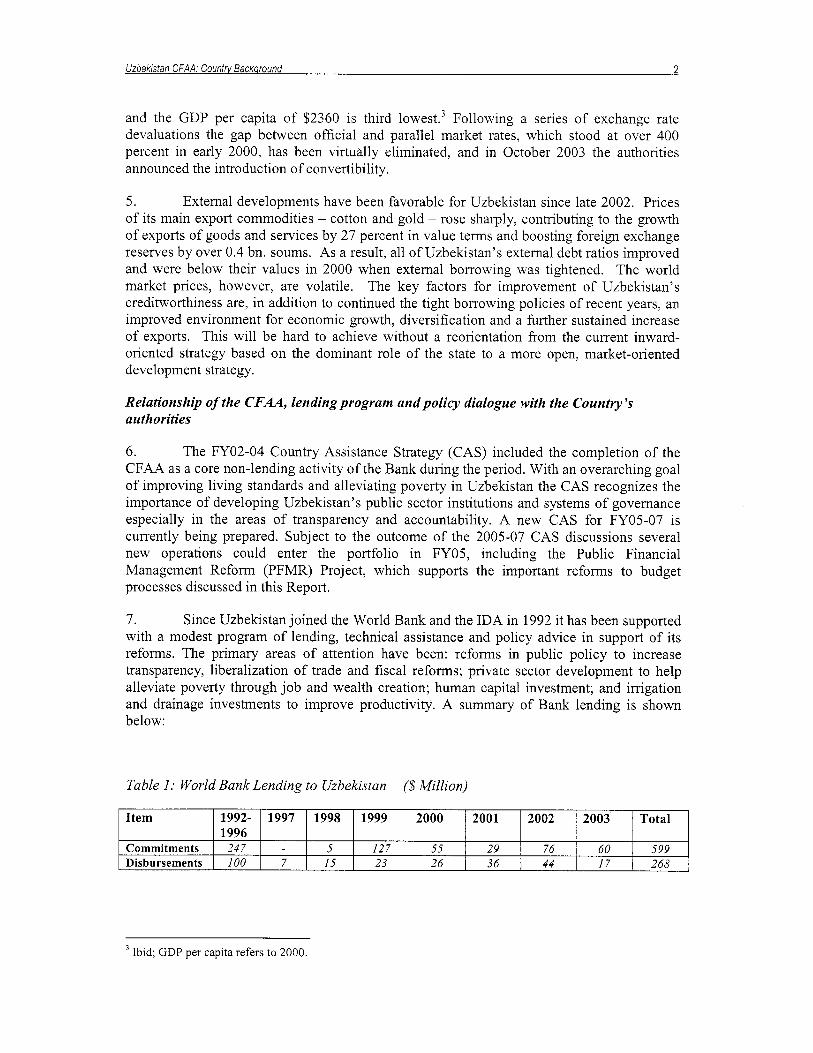

4. Throughout the late 1990’s the Government imposed strict currency controls and Government continued to set prices and quantities in major sectors (agnculture, mining and energy) o f the Uzbek economy. This enabled the Government to avoid the output slump experienced in other transition economies but it also resulted in below average growth in the post-transition period. As a result merchandize exports fel l 32 percent between 1997 and 2001, and another 14 percent in 2002 alone.2 Per capita net FDI i s now the lowest in the CIS,

’ World Bank, Uzbekistan Country Brief, 2003 p. 1.

and the GDP per capita o f $2360 i s third lowes t3 Fol lowing a series o f exchange rate devaluations the gap between of f ic ia l and parallel market rates, which stood at over 400 percent in early 2000, has been vir tual ly eliminated, and in October 2003 the authorities announced the introduction o f convertibil i ty.

Item

Commitments Disbursements

5. External developments have been favorable for Uzbekistan since late 2002. Prices o f i t s ma in export commodities - cotton and gold - rose sharply, contributing to the growth o f exports o f goods and services by 27 percent in value terms and boosting foreign exchange reserves by over 0.4 bn. soums. As a result, a l l o f Uzbekistan’s external debt ratios improved and were below their values in 2000 when external borrowing was tightened. The w o r l d market prices, however, are volatile. The k e y factors for improvement o f Uzbekistan’s creditworthiness are, in addition to continued the tight borrowing policies o f recent years, an improved environment fo r economic growth, diversif ication and a further sustained increase o f exports. This will b e hard to achieve without a reorientation f rom the current inward- oriented strategy based o n the dominant role o f the state to a more open, market-oriented development strategy.

1992- 1997 1998 1999 2000 2001 2002 2003 Total 1996

247 5 127 55 29 76 60 599 100 7 15 23 26 36 44 17 268

Relationship of the CFAA, lending program and policy dialogue with the Country’s authorities

6. The FY02-04 Country Assistance Strategy (CAS) included the completion o f the CFAA as a core non-lending activity o f the Bank during the period. With an overarching goal o f improving living standards and alleviating poverty in Uzbekistan the C A S recognizes the importance o f developing Uzbekistan’s publ ic sector institutions and systems o f governance especially in the areas o f transparency and accountability. A new C A S for FY05-07 i s currently being prepared. Subject t o the outcome o f the 2005-07 C A S discussions several new operations could enter the port fo l io in FY05, including the Public Financial Management Reform (PFMR) Project, which supports the important reforms to budget processes discussed in this Report.

7. Since Uzbekistan jo ined the W o r l d Bank and the IDA in 1992 it has been supported with a modest program o f lending, technical assistance and pol icy advice in support o f i t s reforms. The pr imary areas o f attention have been: reforms in public po l i cy to increase transparency, l iberalization o f trade and fiscal reforms; private sector development to he lp alleviate poverty through j o b and wealth creation; human capital investment; and i r r igat ion and drainage investments to improve productivity. A summary o f Bank lending i s shown below:

Ibid; GDP per capita refers to 2000.

Uzbekistan CFAA: Countw Backqround 3

8. The l imi ted lending program has been complemented by non-lending activities centered around selected fiduciary economic and sector studies. The Bank completed the Country Procurement Assessment Report (CPAR) in 2003 and a Public Expenditure Review (PER) has been prepared in parallel with the C F A A .

9. The Bank’s lending act iv i ty has been focused o n investment projects. Fiduciary safeguards and financial management in the Uzbekistan port fo l io are arranged outside the national institutions o f accountability using stand-alone project implementation units. Budget support operations are not envisaged in the next C A S cycle.

Uzbekistan CFAA: Public Sector Budget Manaqemeni 4

11. PUBLIC SECTOR BUDGET MANAGEMENT

Introduction

10. The focus o f CFAA i s o n budgetary issues wh ich impact o n public sector financial accountability. The Report analyzes both the comprehensiveness and transparency o f the budget process. Later sections o f the report analyze accountability and transparency issues arising f rom extra-budgetary funds and public enterprises.

11. This Report does not provide a detailed examination o f institutional reforms required to reform the budgetary process; nor does it review the allocation o f resources against government priorities. These issues are the domain o f the Public Expenditure Review (the k e y institutional issues arising f rom the PER analysis are summarized in B o x 1 below). The problems inherent within the present system o f budget management have been documented in previous report^.^ The ma in focus o f this chapter i s t o explain the rationale for the development o f a treasury system and provide a deeper understanding o f the challenges posed by this far-reaching init iative.

Principles and Risks

12. Public sector budgeting poses two types o f risk to sound financial management. Firstly there i s the pol icy risk related to the government fail ing to implement the budget passed by the Parliament. As discussed above, these issues are pr imar i ly dealt with in the context o f the PER. Second, there i s the financial management risk that budgetary fimds are not spent for the purposes set out in the budget. This risk i s compounded when significant government activities operating outside the budget are not subject t o normal budget scrutiny and procedures. These issues are discussed below.

13. The budget execution arrangements have an important impact on the management o f the government’s liquidity position and cash requirements. A failure to manage liquidity ef f ic ient ly creates r i sks (1) that payments are n o t made in accordance with the budget, (2) that payments are no t made o n a t imely basis and distort the implementation o f government activities and (3) that finance officials have insufficient information to make the most effective and efficient use o f cash.

14. budgeting should be reviewed:

T o understand the scope o f these risks, the fo l lowing dimension and principles o f

The scope of the budget: i s the budget comprehensive enough to a l low effective pol icy and resources linkages, review and trade-offs? Similarly, are the resources outside the budget subject t o the same policy, review, financial reporting and accountability requirements?

The budget preparation process: I s data o n budget preparation and implementation available, timely, reliable and presented in a w a y that allows the Government to assess implementation o f publ ic policies? I s the budget preparation process conducive to fiscal sustainability and responsibility, and does i t link policies and resources?

See for example the Uzbekistan: Government Financial Management, A Diagnostic Report, World Bank, ECSPE, June 2000 and Uzbekistan: Budget and Treasury Reforms, IMF Fiscal Affairs Dept, March 2003.

0 Budget presentation: I s the budget presentation transparent and clear enough to assess whether i t reflects the Government po l icy priorities, and i s the use o f the funds clearly spelled out?

Availability and quality of budget information: i s the budget available outside the Executive to a l low for open rev iew o f the Government’s proposed use o f funds?

The scope of the budget

15. In Uzbekistan, the budget excludes a significant portion of public funds. As a result, it does not a l low effective po l i cy and resources linkages, rev iew and trade-offs and does not present a comprehensive v iew o f the government sector.

16. Extra-budgetary funds (EBFs) are a large part of total State expenditure. EBFs account for approximately one quarter o f total State budget expenditures; and include four major fimds’ and additional smaller EBFs (accounting for less than 10 percent o f total EBF expenditure). M a n y o f the smaller EBFs are designed to provide incentives to budget entities engaged in revenue production. The state budget does n o t cover a l l government agencies and previous studies have recommended that the government bring a l l controlled entities in to a consolidated reporting entity. In doing so EBFs wou ld b e consolidated in to the budget and more accurately reflects central budget activities. Because o f their overall materiality the issue o f extra-budgetary accounts i s discussed in greater depth in the next section o f the CFAA.

Box 1: Budget Management - Institutional Issues - Key Messages from the World Bank Public Expenditure Review, 2004 (PER) Uzbekistan has begun major reforms to the health and education sector. Budget preparation and execution weaknesses are being addressed through the development o f revised budget preparation procedures and the introduction o f a Treasury system. These changes are part o f a l ong term process requiring a fundamental change in institutions across govemment. Pol icy mak ing functions o f spending ministries need to b e developed; accountability for po l i cy and spending decisions need t o be clarified.

In the l ong term much o f the reform o f public finances wi l l require changes outside the Min is t ry o f Finance. Institutions should be established at the center o f govemment to coordinate strategic po l i cy choices. Spending ministries should be reorganized along functional l ines and include many o f the state institutions wh ich currently deal directly with M O F . Until n o w budget re fo rm has largely been centered around technical developments w i th in the MOF. One o f the main tasks for the MOF i s to make the case to the Govemment and public institutions for the need for reforms and the long term benefits that will ensue.

Amongst the key short term recommendations o f the PER are proposals which wou ld make the presentation o f the budget more transparent and enable the Oliy Maj l i s to evaluate the effectiveness o f the allocation o f resources. In the medium to long term the PER proposes structural changes t o MOF; creating a modem organization equipped to perform the development o f macro-economic po l i cy and sustainable expenditure. The PER also recommends the creation o f high level committee o f the Cabinet o f Ministers (COM) responsible for overseeing the budget process and presenting strategic choices to the COM.

Source- Public Expenditure Review, 2004

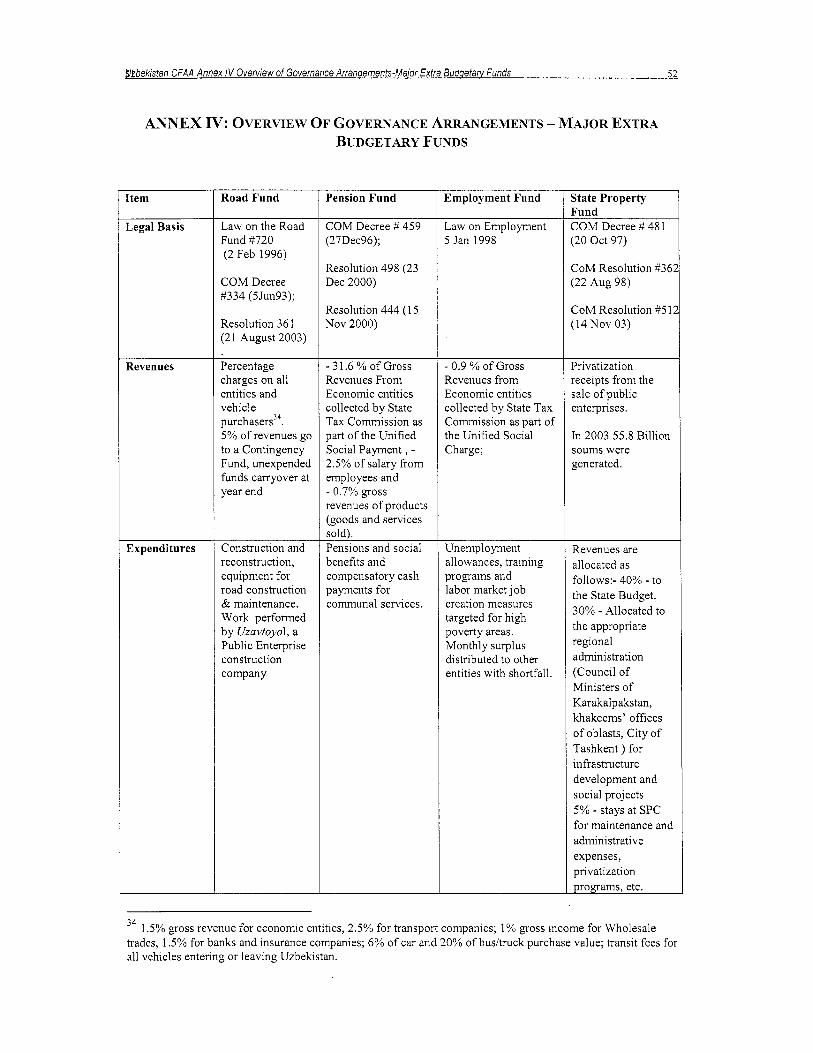

’ Road Fund, Pension Fund, Employment Fund and State Property Fund.

Uzbekistan CFAA: Public Sector Budqet Management 6

The budget preparation process

17. Pol icy development takes place centrally in the apparatus o f the Cabinet o f Ministers and the Presidential Administration. Strategic decisions take place outside the budgetary process, wh ich means that funding for new initiatives m a y be lacking or the budget will b e allocated in an ad hoc manner by MOF. Until recently there was n o in i t ia l resource envelope specified in cal l ing for budget requests. For the f i rst t ime in the 2005 budget process expenditure ceilings were set for sectors. This i s an important step forward in the budget process. However the process o f setting ceilings will require further development and formalization. In particular i t i s important that C O M approves budget ceilings for institutions and not just functions, and the process o f setting ceilings should be codi f ied in the Budget Systems L a w (BSL) o r in regulations issued by the MOF based o n the BSL . Budget requests are based upon standard cost norms and historic allocations. Notwithstanding the improvements, the present budget preparation process i s not conducive to fiscal sustainability, nor does it link policies to resources.

18. There i s no integrated evaluation o f investment and current spending in each sector. The lead agency fo r the investment budget i s no t the MOF but by the MOE wh ich i s responsible for the PIP.6Although MOF officials are involved in this process and a l l projects are formal ly subject t o a process o f appraisal, they are no t evaluated together with other publ ic resources being assigned to a particular sector, within a budgetary envelope for the sector. In addition a number o f basic decisions in the PIP are taken outside the formal budget process (for example, a p r i o r i decisions o n the numbers o f schools and hospitals to be constructed). There i s also n o mechanism for the consideration o f the impact o f recurrent cost implications (beyond the next budget year) o f new investments.

19. Separation of PIP and external financing promotes the view that such resources are additional o r free. Since a significant proportion o f the PIP i s financed f rom external borrowing, the existence o f the PIP in i t s present f o rm promotes the v iew that foreign financing i s in some sense “free” money apart f rom the budget. Al though the appraisal o f PIP projects does include an assessment o f the abi l i ty t o repay the loans these are no t taken into account as part o f the budgetary envelope available for spending by institutions.

Transparency and accountability aspects of the budget process

20. Budget documentation i s not transparent and clear enough to assess whether it reflects the Government policy priorities, and the use o f the funds i s not clearly spelled out. In addition, the budget process does no t lend i tse l f open review o f the Government’s proposed use o f funds.

21. Budget presentation suffers f r o m the fragmented budget (discussed above) and a classification which does not meet international standards. The overview tables o n spending are insufficient to analyze the development o f pol icy. Greater transparency could be achieved through presenting the budget by organizational and economic classification, with comparative data for the previous year and forecasts for the next two years.

The PIP covers both General Government investment (centralized investments) as w e l l as that carried out by publ ic enterprises financed f rom their o w n resources and direct foreign investment (decentralized investments).

Uzbekistan CFAA: Public Sector Budget Manaqement 7

22. The budget classification used for structuring the information does not allow clear accountability for the use o f resources. The functional classification i s a m i x of functional elements and economic categories, and the economic classification i s limited to four categories, as noted above. Recently considerable work has been carried out in the MOF, with the assistance o f the IMF and U S Treasury to develop functional, economic, organizational and program classifications, consistent with the standard GFS 200 1 classifications o f the IMF. This classification identifies the structural unit, the budget beneficiary and the main activity for which budget funding wil l be used. If this classification i s used for the presentation and execution o f the budget, i t would allow for clear accountability in the use o f resources by institutions, and provide the Oliy Majl is and C O M with a means to evaluate the budget in a coherent manner. I t i s expected that the GFS 2001 classification will be implemented for the 2006 budget and, in addition a programmatic budget classification will be implemented in 2007.

23. The Oliy Majlis approve a budget based on broad functional classification. Parliamentarians are provided with an aggregated overview o f proposed government budgetary expenditures and revenues and the tax and fee levels that will be required to meet the revenue budget targets. W h i l e additional information i s available on request, the format and the highly aggregated level o f the information makes i t dif f icult for an individual parliamentarian to formulate an informed opinion. The broad budget parameters are also disclosed, for the f i rs t time this year, on the M O F website. What are missing are the detailed disclosures o f the individual budgets o f the f i r s t l ine budget entities and their sub-entities that compose the main budget variables.

24. The detailed budget i s prepared aper approval by the Oliy Majlis. Once the budget i s approved in parliament a second budget process begins. Since the budget approved by the legislature does not assign resources to institutions and economic categories, i t i s only following the approval o f the budgets that the negotiations and allocation o f budgets o f institutions at the central leve l takes place by the MOF. A similar process also then takes place at the Oblast level for local institutions. On the revenue side the revenue forecasts are broken down by type o f tax and locality to reflect revenue raising plans which become obligatory for the local governments.

25. Transparency and accountability would be enhanced by the publication of Budget documentation. Publication i s standard international practice in virtually al l countries in the world. The decision o f the Government to begin publishing the details o f budget execution for 2003 i s very welcome and institutionalization o f this practice would be an important step forward in transparency. In particular this would include the budget, the macroeconomic forecasts underlying i t and an explanation o f the main budgetary measures.

Budget execution and cash management issues

26. Fragmented organizational arrangements for the budget make implementation difficult to monitor. Budget execution takes place through the Central Bank o f Uzbekistan (CBU) and commercial banks on the basis o f a monthly cash release system. There i s no distinction between the authority to spend and the release o f funds. Cash i s . disbursed into thousands o f individual bank accounts o f budget institutions. The C B U estimates that there are 120,000 Government bank accounts.

Uzbekisfan CFAA: Public Sector Budqef Manaqement a

27. The present budget execution arrangements expose the Government to important risks (1) that payments are not made in accordance with the budget, (2) that payments are not made o n a t imely basis and distort the implementation o f government activities and (3) that finance officials have insufficient information to make the most effective and efficient use o f cash. These r isks are recognized by the Government and are being addressed through the development o f the treasury system.

28. There i s uncertainty in the availability and timing of funds. In principle, budget funds are released to spending agencies o n the basis o f month ly expenditure plans. Al though funds released over the whole year are in accordance with the approved budget, to keep cash under control these releases are not automatic and are pr ior i t ized by the MOF or the Oblast Finance Department. The timing o f availabil ity o f funds i s determined in part by the availabil ity o f revenue (dependent o n seasonal o r local fluctuations) at the relevant level o f decision-making (MOF, oblast o r rayon). The need for priorit ization7 in release o f cash makes control o f execution a source o f pol i t ical and economic power, and subject to lobby ing and rent-seeking'. The resulting uncertainty as to the timing o f the release o f funds generates incentives to cash hoarding and the accumulation o f id le balances by budget organizations. Cash management i s further complicated by the rat ioning o f cash by the CBU to the banking system. Even when funds are made available through the banking system to the bank accounts o f BIs, these are unable to make payments in cash to f inal recipients. As a result arrears o f several months have occurred in wage and pension payments in some areas.

29. Extra budgetary accounts in the banking system further weaken liquidity management and fiscal control. Spending agencies use extra-budgetary accounts (established under decree 414) to manage their o w n resources. Wh i le such arrangements facilitate cost recovery, the high number o f extra-budgetary bank accounts maintained by budget institutions creates further loopholes in the fiscal control system.

Recent and proposed reforms

30. Many o f the weaknesses highlighted above are being addressed through the introduction o f a treasury system and work on the budget preparation process. The MOF has begun w o r k o n a m o d e m treasury system with the support o f the IMF and the Bank's Public Finance Reform project. A U S Treasury Advisor i s assisting the Ministry o f Finance with improv ing i t s budget preparation procedures including revising the budget classifications (introducing an organizational classification), strengthening the legal framework o f the budgetary process and improv ing the format and the content o f budget submissions prepared by l ine ministries.

31. A modern treasury system offers a number of potential benefits which can address the limitations of the current system and will assist in the implementation of budget plans and the management of public resources. Firstly, the creation o f a single treasury account and dai ly cash reports will enable the government to manage cash, f inancial assets and short term investments efficiently. The result wil l b e a reduction in the cost o f i d le

Pr ior i ty i s given to wages, pensions and utility payments. ' The problem i s exacerbated by unclear lines o f accountabil ity o f the local finance departments wh ich report t o bo th the MOF and the Oblast authorities.

Uzbekistan CFAA: Public Sector Buduet Manauement 9

balances and an increase in cash predictabil ity which can be made available to spending units. Second improved reporting through a modern Government Financial Management Informat ion System (GFMIS) provides better analytical information to moni tor the budget execution process at a l l levels o f government. Reporting o f expenditures provide reliable and timely assurance that publ ic resources have been used in conformity with the legal authorizations and mandatory requi remenkg Off ic ia ls can monitor the proport ion o f appropriations not committed and expenses committed but unpaid. Finally, systems and procedures improve the management o f domestic and foreign debt through regular recording and reporting o f loans including their associated disbursement and repayment schedules.

32. The establishment of the Treasury entails a major institutional reorganization for MOF. Under the draft proposals the Treasury will be established as a unit o f the MOF, headed by a Deputy Minister, and i t wil l comprise a Central Treasury (CT) located in the head office o f the MOF and a network o f local treasury branches (LTBs) throughout Uzbekistan. Under the new arrangements the LTBs wou ld be directly subordinate to the CT and not to local Govemments.

33. The treasury reforms will require considerable capacity building. The capacity o f the Government to absorb and implement an ambitious series o f publ ic sector financial management reforms will be a challenging and on-going exercise. Finance training i s needed in a l l publ ic sector institutions but i s particularly acute in the regions and in budgetary institutions. M a n y finance officers have had n o formal training since the 1980’s and there i s a lack o f computers and basic guidelines to assist staff.

34. MOF have identif ied 21,000 new and existing staff sub-divided in to (i) treasury staff, (ii) finance officers in MOF, oblast and rayon level finance offices and (iii) finance and accounting officers in budgetary units (predominantly in the health and education sectors). MOF propose to set up a training faci l i ty in the Treasury building to accommodate classrooms. The MOF will develop in i t ia l trainers for trainers program and develop training materials and modules based o n the skill and competences required o f finance officers.

Main Recommendations

35. conclusions drawn in the PER and are repeated in CFAA for continuity o f reporting.

The recommendations included in this section are consistent with the analysis and

Short term (within one vear)

36. Adopt fully the outline budget process developed for the 2005 budget.

i) selection o f projects. ii) classification i s presented to the COM and Oliy M a j l i s in that form.

PIP should be prepared in close collaboration with the Ministry o f Finance in the

The budget i s formulated around the organizational and programmatic

37. policy, should be published.

The budget, together with documentation on its assumptions and main lines of

Discussed in greater detail in Section I V

Medium term (one to three vears)

38. required are:

The Budget System Law should be amended. The principal amendments

i> i i) cash. This i s essential for the introduction o f the Treasury.

To require the enactment o f the budget by the Oliy Maj l is . To define appropriations as an authority to spend separate f rom the release o f

39. Multi-year PIP process should be reinstated and coordinated by MOF. The choice o f projects within the general government sphere should b e coordinated by the MOF as part o f an annual and med ium term budget process. The MOE should b e responsible for developing methodology for project appraisal and quality control o f proposed projects. The MOF should maintain a database o f ongoing projects showing their impact o n future recurrent costs, wh ich should b e integrated into a wider med ium term budget perspective.

40. Transparent operational rules and procedures should be developed for the Treasury control of budget execution. The rules should a l l ow the Treasury to ver i fy the legality o f payments, but give i t n o authority to priorit ize payments except by rules that are published by the MOF. The rules for managing budget execution should al low different levels o f control o f expenditure, and be consistent with sectoral reforms.

Uzbekistan CFAA: Extra Budsetaw Funds 11

111. EXTRA BUDGETARY FUNDS

Introduction

41. Extra-budgetary funds pose three types o f risk to sound financial management. Firstly there i s the policy risk that through poor government oversight and operational management extra-budgetary funds fai l to meet overall policy objectives. Second, there i s the performance risk, where use o f the funds for their intended purposes cannot be ascertained due to poor oversight and management. Finally, there i s the financial risk. I t has two sub-components:

e Fiscal risk: the fund may overspend i ts general budget allocation through weak

Cash management risk: by holding separate extra-budgetary funds the Government

commitment controls or unauthorized borrowing;

may have to either borrow funds when idle balances remain in the fund bank accounts or reduce cash allocations to other programs to accommodate the increased demands o f the extra-budgetary fund.

0

42. The second and third r isks (performance and financial r isks) are the most relevant to the C F A A diagnostic. These r i s k s occur because extra-budgetary accounts are off-budget and often operate outside the general budget formulation, execution, and reporting system. Simply including the fund balance sheet in the annual Government budget documentation would not be sufficient as they would s t i l l not be subject to normal budget scrutiny and procedures.

Extra-Budgetary Funds in Uzbekistan

43. The overall amounts o f spending o f extra-budgetary funds in Uzbekistan are highly material, accounting for approximately one quarter o f total State budget expenditures. Table 1 provides details o f the spending on the four major funds and over 20 smaller funds (accounting for less than 10 percent o f total extra-budgetary expenditure and presented in aggregated form).

44. The smaller funds" have been established principally to provide incentives to budget entities engaged in revenue production. These revenues can then be spent on staff bonuses, benefits, and other spending related to the entity. Revenues include the tax and customs commissions (20 percent o f penalties collected), State Property Commission (1 percent o f privatization revenues, MOF (10 percent o f C R U recoveries to the state budget)".

45. In addition spending agencies use extra-budgetary accounts (established under decree 414) to manage to provide greater flexibility in the budget execution process. I t creates provisions which allow budget entities to transfer unused budgetary funds into an extra-budgetary account, known as a development fund. The number o f these funds i s roughly equal to the number o f budget entities, approximately 13,000. These development accounts are off-budget and non-lapsing at year-end, and are not subject to normal budget

lo A l is t o f a l l extra- budgetary funds i s included in Annex IV.

Resolution in 2003. The Resolution also provides fo r estimates o f extra-budgetary funds t o b e registered with the Ministry o f Finance and i s taken into account in the budget formulation process.

The allocation o f fees and penalties to extra-budgetary funds o f the ministries were reduced by COM

execution controls. In 2003, total expenditures f rom these accounts were estimated at 10 percent o f budgetary expenditures. These development accounts are maintained in commercial banks.

Road Fund

Table 2: Extra-budgetary fund spending 1999-2004 (Billion Soums)

Actual Actual Actual Actual Forecast Budget 32.0 51.7 72.4 123.1 140.3 152.0

I Fund I 1999 1 2000 I 2001 I 2002 1 2003 I 2004 I

EBFFercent o f State Budget incl. EBFs

24.4% 24.5% 25.7% 25.8% 24.7%* 28.0%*

Source: Ministry of Finance. n/a - not available; * = excluding other EBFs.

Impact of extra-budgetary funds

Budget and cash management issues

46. Extra-budgetary funding further fragments the budgetary process and creates significant policy risks. The smaller funds have been created with their o w n sources o f income, and cover recurrent expenditures such as maintenance, repairs o r subsidies in different sectors, wh ich are the items being squeezed under the current budgeting process. The creation o f extra-budgetary funds for these purposes i s a substitute fo r an effective budget process and reflects an inabi l i ty to priorit ize. If an overriding need for maintenance, staff incentives or any other expenditure i s recognized this should be provided for through the normal budget process.

47. N o new extra-budgetary funds should be created. The creation o f extra- budgetary funds i s a symptom o f failures o f the budget process to allocate sufficient funds fo r activities such a maintenance and capital purchases. These funds are often created as a result o f pol i t ical lobbying o r ad hoc pr ior i ty setting at a higher level. In the case o f the smaller funds these account for a subset o f expenditure within sectors wh ich should b e more proper ly be considered under normal budgetary processes. F o r this reason the government should p lan to wind these funds up in the medium term. I t i s recognized that the Government i s mak ing efforts to reduce the number o f extra-budgetary funds, but the recent creation o f a new ear- marked fund for basic education i s a cause for concern, because o f the w a y in wh ich these funds circumvent the normal budgetary processes.

48. Controlling of extra-budgetary funds could be linked to greater flexibility in spending. Since many o f the smaller funds were introduced to give more f lex ib i l i ty t o spending institutions, their abol i t ion has to b e l i nked with measures which give institutions

Uzbekistan CFAA: : Extra Budqetary Funds 13

more f lex ib i l i ty in spending. This could be achieved by reducing the level o f detail in the expenditure tables and al lowing greater scope for virement wi thout reference to the Ministry o f Finance.

49. Extra-budgetary funds in the banking system weaken fiscal control and expose government to fiscal risks. Whi le development accounts facilitate cost recovery, the high number o f extra-budgetary bank accounts maintained by Budget Institutions creates loopholes in the fiscal control system. The existence o f separate bank accounts also increases financing costs and fiscal r i sks i f funds are able to borrow.

Governance issues

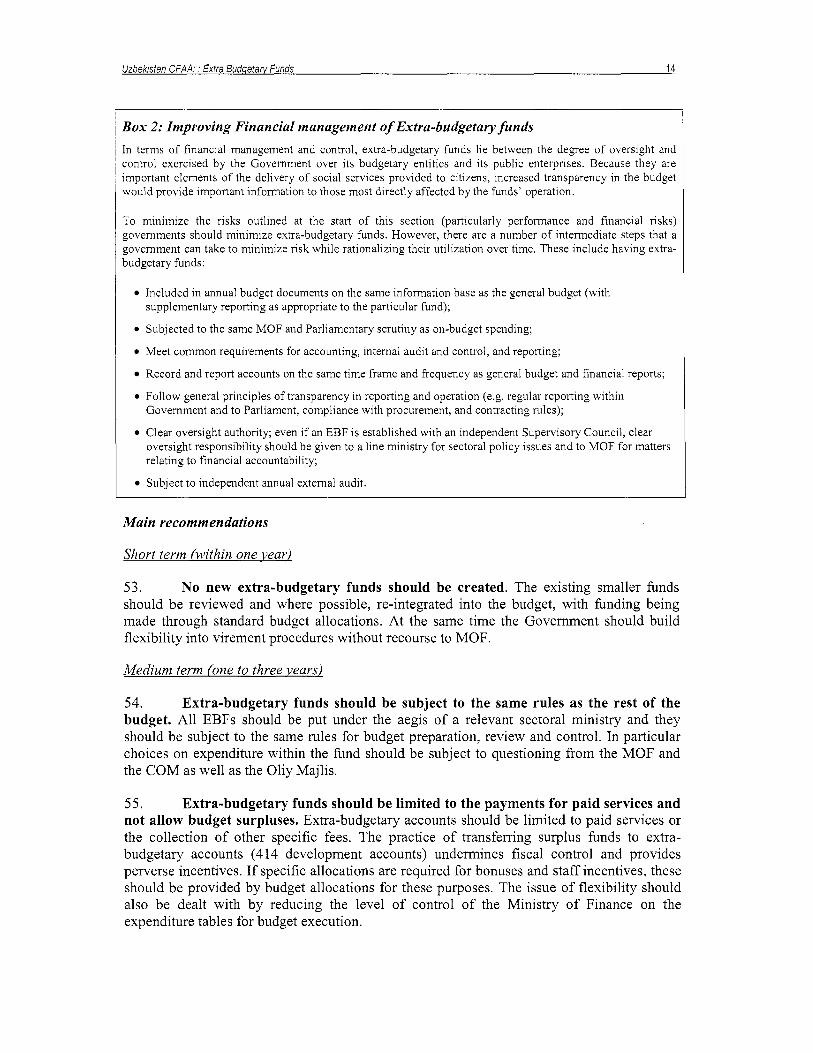

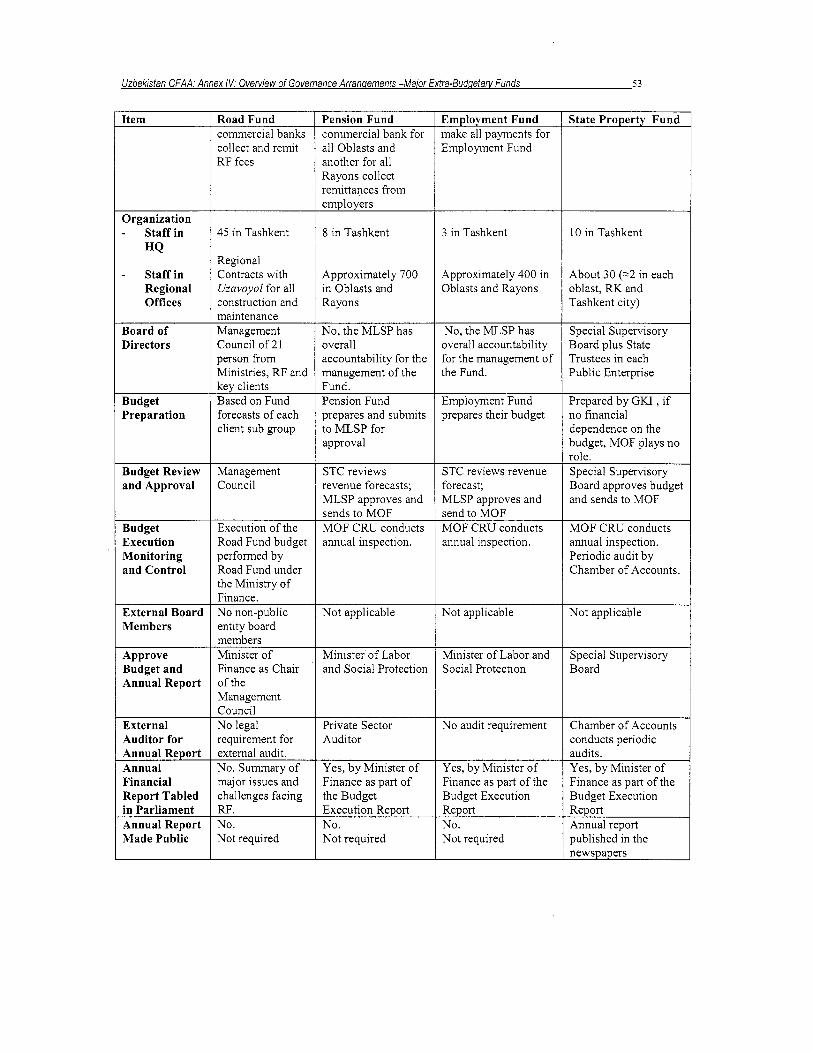

50. The CFAA conducted a review o f the four major funds financial management processes and controls (see Annex 111). F r o m this analysis i t appears that extra-budgetary funds are not as stringently monitored and controlled as other budget entities. For example wh i l e budgets are tabled in Parliament with the state budget there i s n o legal requirement fo r extra-budgetary funds’ annual reports to b e made public. The present procedures lack transparency and create an uncertain and inconsistent control and accountability environment.

51. The Government should establish common budgetary, audit, control and reporting procedures which can be scrutinized, questioned and approved by the MOF, COM and Oliy Maj l is (see Box 2). To mitigate the performance risk, extra-budgetary funds should b e consolidated in the state budget and operate the same processes o f preparation, execution, report ing and control as the rest o f the budget.

52. The governance arrangements for the Road Fund should be reviewed in the light of recent institutional changes. The m a i n supplier t o the Road Fund i s Uzavtoyol, the state construction company f i o m wh ich the Fund was recently separated. Uzavtoyal i s represented o n the Management Counci l o f the Road Fund and as such has a significant role in determining the Fund expenditures priorities, a clear conf l ic t o f interest. The Government could strengthen the contract-like relationship between the Road Fund and suppliers through an independent Management Counci l wh ich specifies the resources provided and the performance expectations o f the Fund. Governance could b e improved st i l l further if budget formulation and the determination o f the priorit ies in the Road Fund were to become the responsibility o f the appropriate sector ministry (Ministry o f Transport and Communications).

Uzbekistan CFAA: : Extra Budqetarv Funds 14

Box 2: Improving Financial management of Extra-budgetary funds In terms o f financial management and control, extra-budgetary funds l i e between the degree o f oversight and control exercised by the Govemment over i t s budgetary entities and i t s public enterprises. Because they are important elements o f the delivery o f social services provided to citizens, increased transparency in the budget would provide important information t o those most directly affected by the funds’ operation.

To minimize the risks outlined at the start o f this section (particularly performance and financial r isks) governments should minimize extra-budgetary funds. However, there are a number o f intermediate steps that a govemment can take to minimize risk whi le rationalizing their uti l ization over time. These include having extra- budgetary funds:

Included in annual budget documents on the same information base as the general budget (with

Subjected to the same M O F and Parliamentary scrutiny as on-budget spending;

Meet common requirements for accounting, intemal audit and control, and reporting;

Record and report accounts on the same time frame and frequency as general budget and financial reports;

Follow general principles o f transparency in reporting and operation (e.g. regular reporting within

Clear oversight authority; even if an EBF is established with an independent Supervisory Council, clear

supplementary reporting as appropriate to the particular fund);

Government and to Parliament, compliance w i th procurement, and contracting rules);

oversight responsibility should b e given to a l ine ministry for sectoral po l i cy issues and to MOF for matters relating to financial accountability;

Subject to independent annual extemal audit.

M a i n recommendations

Short term (within one year)

53. N o new extra-budgetary funds should be created. The existing smaller funds should be reviewed and where possible, re-integrated into the budget, with funding being made through standard budget allocations. At the same time the Government should build flexibility into virement procedures without recourse to MOF.

Medium term (one to three vears)

54. Extra-budgetary funds should be subject to the same rules as the rest of the budget. All EBFs should be put under the aegis o f a relevant sectoral ministry and they should be subject to the same r u l e s for budget preparation, review and control. In particular choices on expenditure within the fund should be subject to questioning from the MOF and the C O M as well as the Oliy Majlis.

55. Extra-budgetary funds should be limited to the payments for paid services and not allow budget surpluses. Extra-budgetary accounts should be limited to paid services or the collection o f other specific fees. The practice o f transferring surplus funds to extra- budgetary accounts (414 development accounts) undermines fiscal control and provides perverse incentives. If specific allocations are required for bonuses and staff incentives, these should be provided by budget allocations for these purposes. The issue o f f lexibil i ty should also be dealt with by reducing the level o f control o f the Ministry o f Finance on the expenditure tables for budget execution.

Uzbekistan CFAA: : Extra Budqetarv Funds 15

I n the medium term extra-budgetary funds should be included in the treasury system for the purposes of managing cash. However this objective will be achieved only to the extent that the Treasury performs the budget execution h n c t i o n and extra-budgetary accounts are fully ring fenced within the Treasury. In such a control environment hnds wou ld be released once the authorizations have been made in accordance with clearly defined procedures. Handled correctly this reform wou ld improve financial management without inappropriate l imitations being placed o n operational managementI2.

The Government envisages that w i th in the framework o f the Public Finance Management Reform Project the I 2

Treasury wi l l perform the budget execution o f extra-budgetary funds and the development accounts o f budget agencies.

IV. PUBLIC SECTOR ACCOUNTING AND FISCAL REPORTING

Introduction

56. Under the Soviet central planning system accounting was an exercise in booking- keeping; budget reporting was merely a financial reflection o f detailed production plans. M o d e m government accounting and financial reporting protect and manage publ ic money and discharge accountability. Therefore good accounting practices support transparency in the use o f funds and help c lar i fy responsibilities in funds management. When governments engage in economic act iv i ty - be it buying or selling services or borrowing and lending money they are subject to economic accountability. When they l evy and are in receipt o f revenues they are subject to pol i t ical accountability.

57. Accounting reforms should no t been seen as an end in themselves but should be seen as tools for supporting the implementation o f broader economic, political, and fiscal reforms within government. Hav ing a broad v iew o f stakeholder requirements in the context o f a countries socio-economic development i s helpful in identifying priorit ies based o n the priorit ies in the national economy. For example, changes to accounting and budgetary systems in the Uni ted K i n g d o m wou ld have been more l imi ted without pressure to restructure health and social welfare systems and reduce overall levels o f t a ~ a t i o n . ' ~

58. Government accounting has three broad purposes w h i c h can be used to illustrate priorit ies in order to build full capacity into a government accounting system.14 The basic purpose o f government accounting i s t o safeguard publ ic money and prevent corruption. The intermediate purpose i s to facilitate budgeting and planning o f revenues, expenditures and debt management. At this stage officials go beyond score-keeping and use management and cost data to conduct government operations in a more economical, effective and efficient manner. Final ly the advanced purpose o f government accounting i s t o help government discharge i t s publ ic accountability. At this stage the emphasis o f accounting shif ts f rom bureaucratic control t o accountabil ity reporting to the public. I t i s no t enough for government officials to keep accurate books and records - they are open to the publ ic through transparent and comprehensible financial statements.

Current accounting arrangements

59. Government accounting in Uzbekistan i s based on the Soviet accounting system which uses many concepts o f modern accounting including accrual measurements and double entry bookkeeping. In addition Uzbekistan has a large number o f bookkeepers w h o are trained in these concepts and are prof ic ient in their application. However, there are significant capacity constraints wh ich hinder the development o f a modem system of accounting and financial reporting. The accounting systems used at a central and local government level are predominantly manual. There i s n o central management information system; significant reliance i s p laced o n banking records and computer spreadsheet packages.