Embed Size (px)

Citation preview

County Tax Lien Sales in Indiana

DISCLAIMER

This presentation provides general information about Indiana tax sales and

the statutory obligations of lien buyers following a tax sale. However, legal

information is not the same as legal advice, which is the application of the

law to a specific situation. This presentation is not meant to provide

comprehensive guidelines for any particular situation. The information

herein is not guaranteed to be correct, complete, or current. You should not

act or rely on any information in this presentation without seeking the

advice of an attorney.

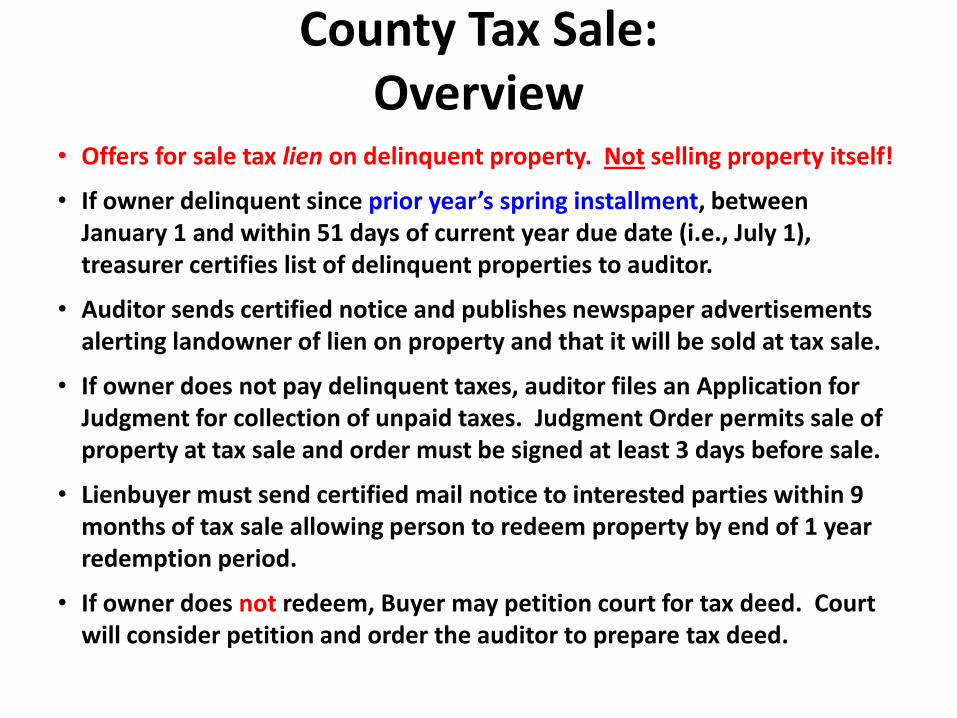

County Tax Sale:Overview

• Offers for sale tax lien on delinquent property. Not selling property itself!

• If owner delinquent since prior year’s spring installment, between January 1 and within 51 days of current year due date (i.e., July 1), treasurer certifies list of delinquent properties to auditor.

• Auditor sends certified notice and publishes newspaper advertisements alerting landowner of lien on property and that it will be sold at tax sale.

• If owner does not pay delinquent taxes, auditor files an Application for Judgment for collection of unpaid taxes. Judgment Order permits sale of property at tax sale and order must be signed at least 3 days before sale.

• Lienbuyer must send certified mail notice to interested parties within 9 months of tax sale allowing person to redeem property by end of 1 year redemption period.

• If owner does not redeem, Buyer may petition court for tax deed. Court will consider petition and order the auditor to prepare tax deed.

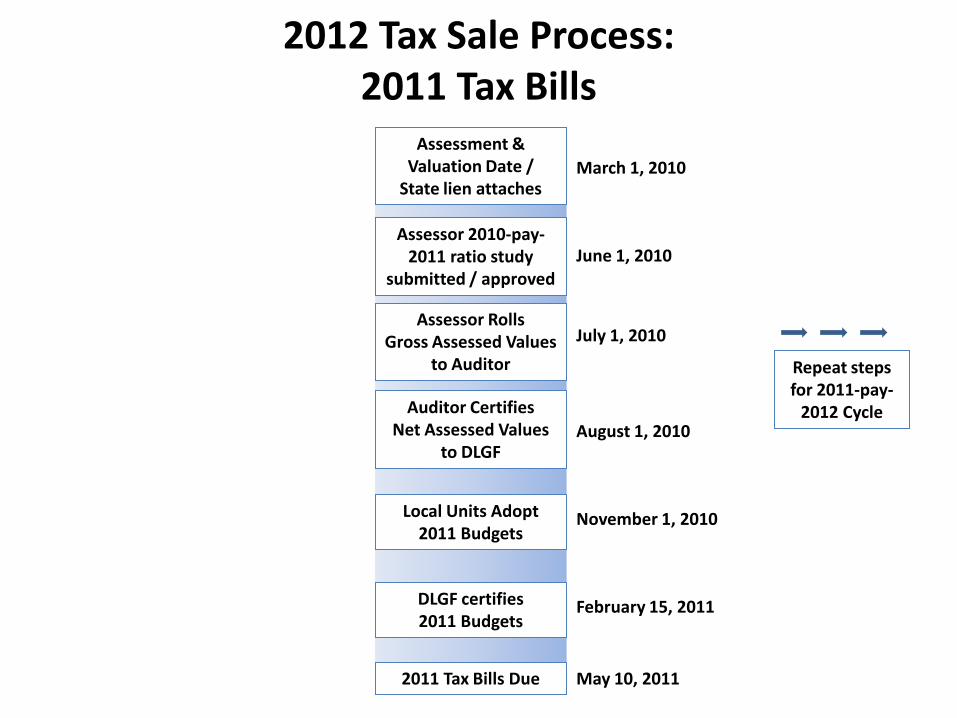

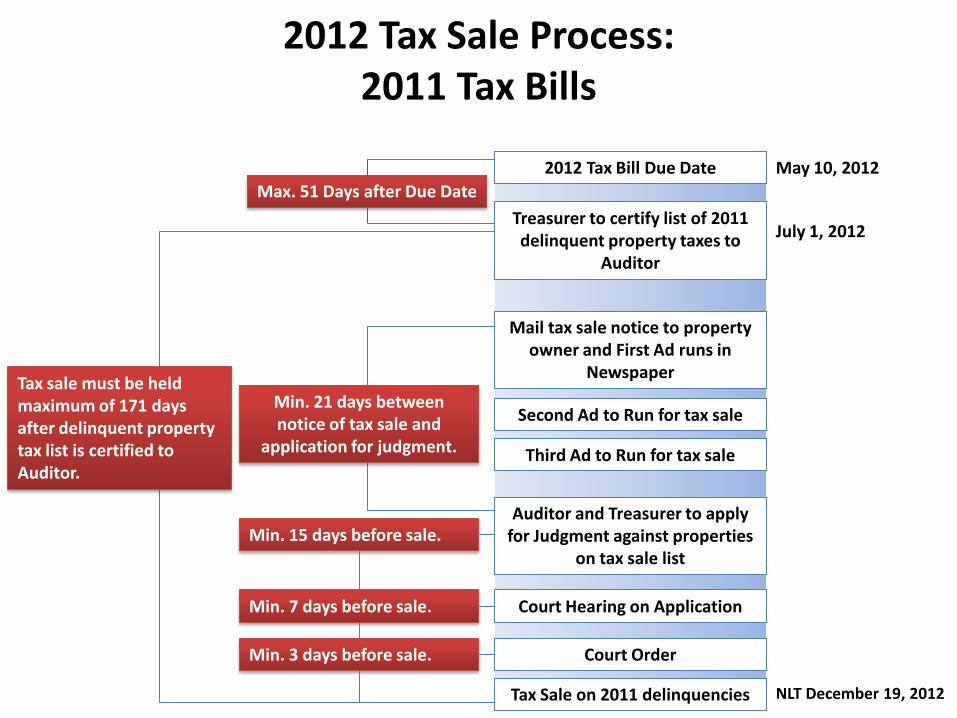

2012 Tax Sale Process: 2011 Tax Bills

June 1, 2010

July 1, 2010

August 1, 2010

February 15, 2011

Assessor 2010-pay-2011 ratio study

submitted / approved

Assessor Rolls Gross Assessed Values

to Auditor

Auditor Certifies Net Assessed Values

to DLGF

November 1, 2010Local Units Adopt 2011 Budgets

DLGF certifies 2011 Budgets

2011 Tax Bills Due May 10, 2011

Repeat steps for 2011-pay-

2012 Cycle

Assessment & Valuation Date /

State lien attaches March 1, 2010

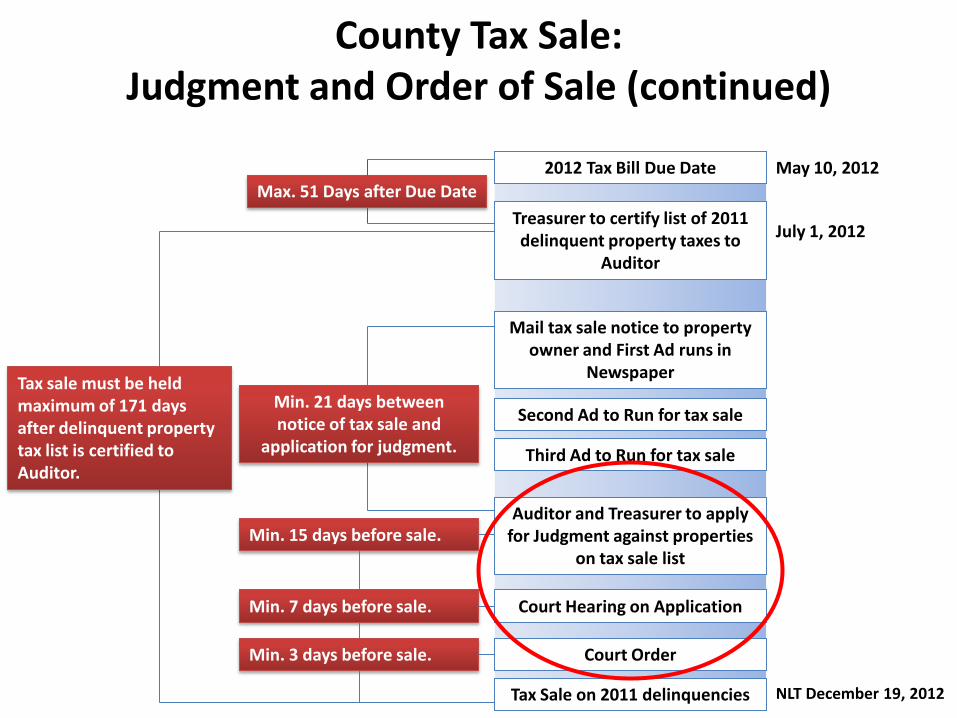

May 10, 2012

July 1, 2012

2012 Tax Bill Due Date

Treasurer to certify list of 2011 delinquent property taxes to

Auditor

Mail tax sale notice to property owner and First Ad runs in

Newspaper

Second Ad to Run for tax sale

Auditor and Treasurer to apply for Judgment against properties

on tax sale list

Max. 51 Days after Due Date

Third Ad to Run for tax sale

Min. 21 days between notice of tax sale and

application for judgment.

Court Hearing on Application

Court Order

Tax Sale on 2011 delinquencies

Min. 15 days before sale.

Min. 7 days before sale.

Min. 3 days before sale.

Tax sale must be held maximum of 171 days after delinquent property tax list is certified to Auditor.

NLT December 19, 2012

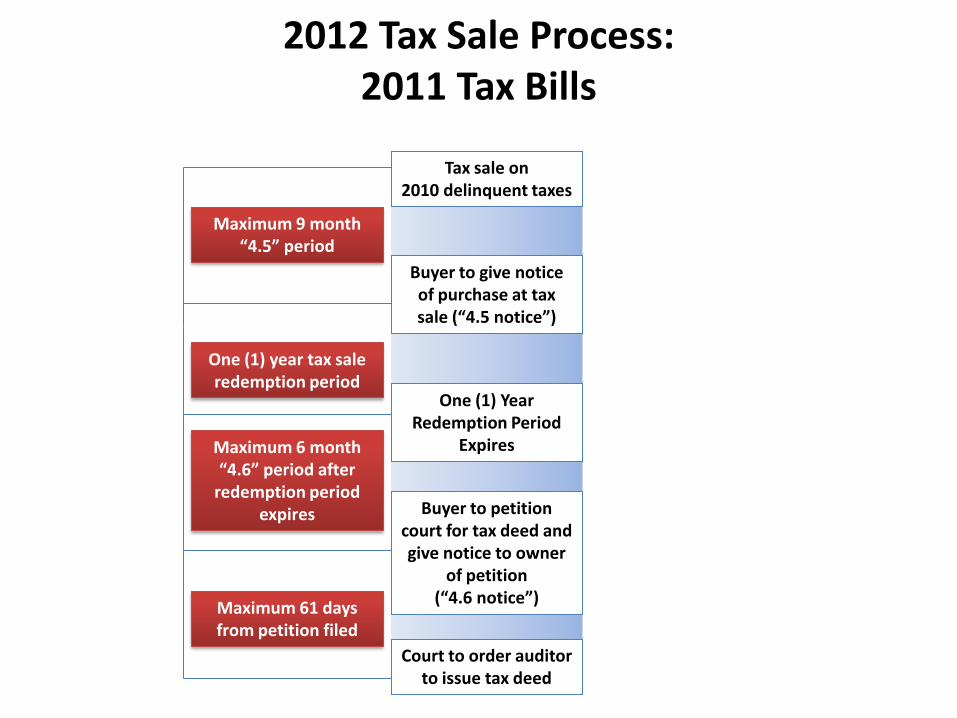

2012 Tax Sale Process: 2011 Tax Bills

Tax sale on 2010 delinquent taxes

Buyer to give notice of purchase at tax sale (“4.5 notice”)

One (1) Year Redemption Period

Expires

Maximum 9 month “4.5” period

Buyer to petition court for tax deed and give notice to owner

of petition (“4.6 notice”)

Court to order auditor to issue tax deed

One (1) year tax sale redemption period

Maximum 6 month “4.6” period after

redemption period expires

Maximum 61 days from petition filed

2012 Tax Sale Process: 2011 Tax Bills

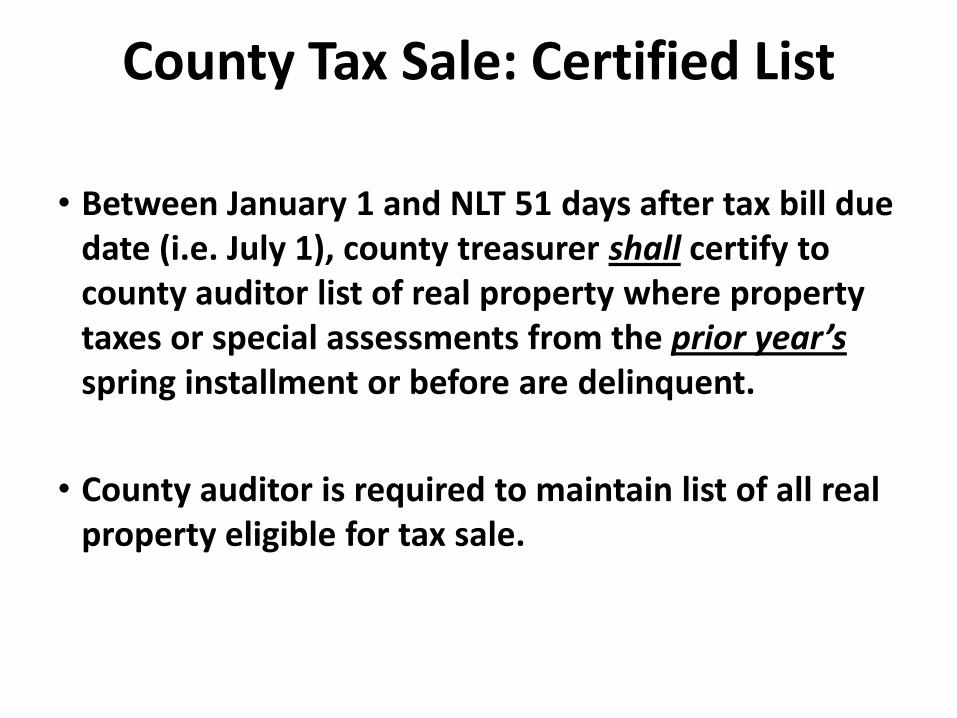

County Tax Sale: Certified List

• Between January 1 and NLT 51 days after tax bill due date (i.e. July 1), county treasurer shall certify to county auditor list of real property where property taxes or special assessments from the prior year’sspring installment or before are delinquent.

• County auditor is required to maintain list of all real property eligible for tax sale.

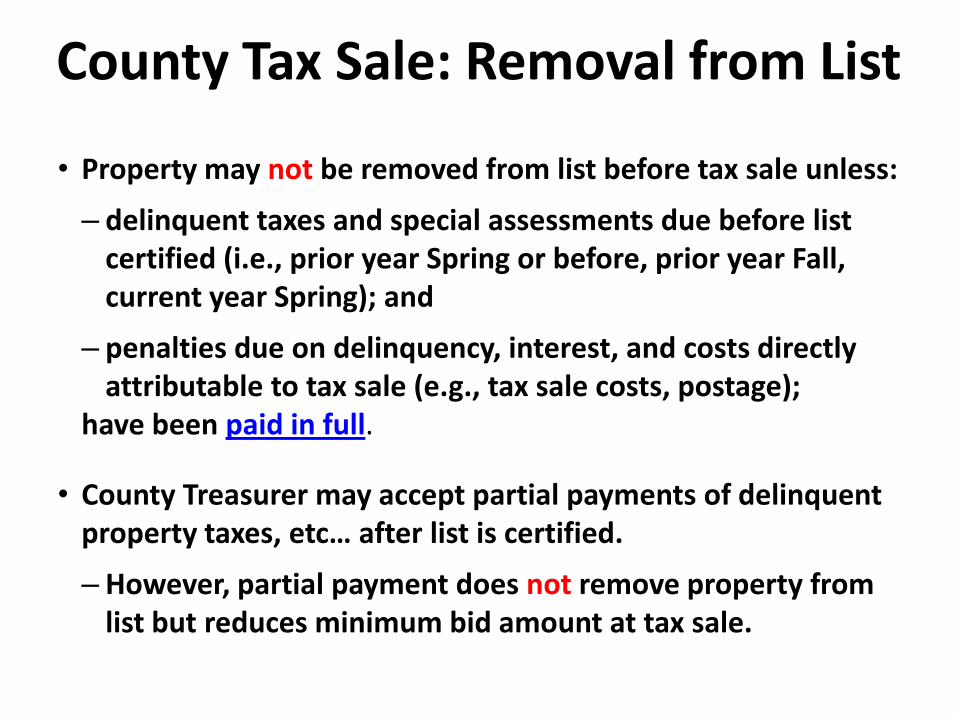

County Tax Sale: Removal from List

• Property may not be removed from list before tax sale unless:

– delinquent taxes and special assessments due before list certified (i.e., prior year Spring or before, prior year Fall, current year Spring); and

– penalties due on delinquency, interest, and costs directly attributable to tax sale (e.g., tax sale costs, postage);

have been paid in full.

• County Treasurer may accept partial payments of delinquent property taxes, etc… after list is certified.

– However, partial payment does not remove property from list but reduces minimum bid amount at tax sale.

County Tax Sale: Notice

• Tax sale process involves issuance of 3 notices to owner:

– County Auditor’s Notice of Tax Sale – (1) newspaper advertisements for three weeks; and (2) certified mail sent to last known address and, if certified mail receipt not returned, then by first class.

– Buyer’s Notice of Right to Redemption – sent to owner of property/person with substantial interest (“4.5 Notice”).

– Buyer’s Notice of Filing a Petition for Tax Deed – sent to owner of property/person with substantial interest (“4.6 Notice”).

• Title conveyed by a tax deed may be defeated if the 3 required notices were not issued in substantial compliance with legal requirements.

County Tax Sale: Auditor’s Newspaper Advertisement

• List of tracts or real property eligible for sale.

• Sold at public auction to highest bidder, subject to redemption.

• Minimum Bid: Property will not be sold for less than:– delinquent taxes and special assessments;– taxes and special assessments due in year of tax sale, whether or not

delinquent [e.g., November 10, 2012 installment];– all penalties due on delinquencies; – Greater of $25 or postage and publication costs, and any other actual

costs incurred by county; and– any unpaid costs due from prior tax sale.

• Redemption Amount (SEE LATER SLIDE)

County Tax Sale: Auditor’s Newspaper Advertisement

• Location by key number and street address, if any, or common description other than legal description.

– Township assessor, or county assessor, upon written request from county auditor, shall provide information to be in notice.

– Misstatement in key number or street address does not invalidate valid sale.

• Name of single owner; or name of at least one (1) of the owners with multiple owners.

• Procedure to be followed for Judgment and Order of Sale.

• Location, date, and time of county tax sale.

• Surplus disposition (SEE LATER SLIDE)

County Tax Sale: Auditor’s Certified Mail Notice

• Notices to be mailed NLT 21 days before earliest date of application of Judgment and Order for Sale may be filed.

• Notice of Sale sent by certified mail, return receipt to owner of record at the last known address of owner of property as indicated in records of county auditor on date tax sale list is certified (i.e., July 1).

• Send notice by first class mail to owners from whom certified mail return receipt was not signed and returned.

– If both notices are returned due to incorrect addresses, county auditor shall research their records to determine more accurate address.

– Failure to obtain more accurate address does not invalidate otherwise valid sale.

• Required Contents of Certified Mail Notice:

1. Key number and street address, if any, or other common description of property other than legal description.

2. Components of amount required to redeem from tax sale.

• County auditor must present proof of mailing to court along with application for Judgment and Order for sale.

• Failure by owner to receive or accept notice does not affect validity of Judgment and Order.

• Owner of property shall notify auditor of their correct address.

• Notice considered sufficient if mailed to address required.

County Tax Sale: Auditor’s Certified Mail Notice

County Tax Sale: Judgment and Order of Sale

• NLT 15 days before tax sale, court examines updated list of real property remaining on tax sale list.

• NLT 7 days before tax sale, court conducts hearing regarding any objections/defenses to parcels included in sale. Court required to send notice to each objecting party of time and place of hearing.

• NLT 3 days before tax sale, court enters judgment for those taxes, special assessments, etc. that appear to be due.

– Judgment is against each tract or item of real property for each kind of tax, special assessment, penalty, or cost.

– Clerk to enter order for sale of property with judgments against it.

• Court order constitutes list of real property offered for sale.

County Tax Sale: Judgment and Order of Sale (continued)

May 10, 2012

July 1, 2012

2012 Tax Bill Due Date

Treasurer to certify list of 2011 delinquent property taxes to

Auditor

Mail tax sale notice to property owner and First Ad runs in

Newspaper

Second Ad to Run for tax sale

Auditor and Treasurer to apply for Judgment against properties

on tax sale list

Max. 51 Days after Due Date

Third Ad to Run for tax sale

Min. 21 days between notice of tax sale and

application for judgment.

Court Hearing on Application

Court Order

Tax Sale on 2011 delinquencies

Min. 15 days before sale.

Min. 7 days before sale.

Min. 3 days before sale.

Tax sale must be held maximum of 171 days after delinquent property tax list is certified to Auditor.

NLT December 19, 2012

County Tax Sale: Conduct of Sale

• County tax sale must:

– be held at times and place stated in notice of sale; and

– not extend beyond 171 days after list is certified to auditor.

• Real property may not be sold to collect:

– delinquent personal property taxes; or

– taxes or special assessments which are chargeable to other real property.

• Real property may not be sold if all delinquent taxes, penalties, costs, etc… are paid before tax sale.

• Treasurer must sell real property, subject to the right of redemption, to highest bidder at public auction.

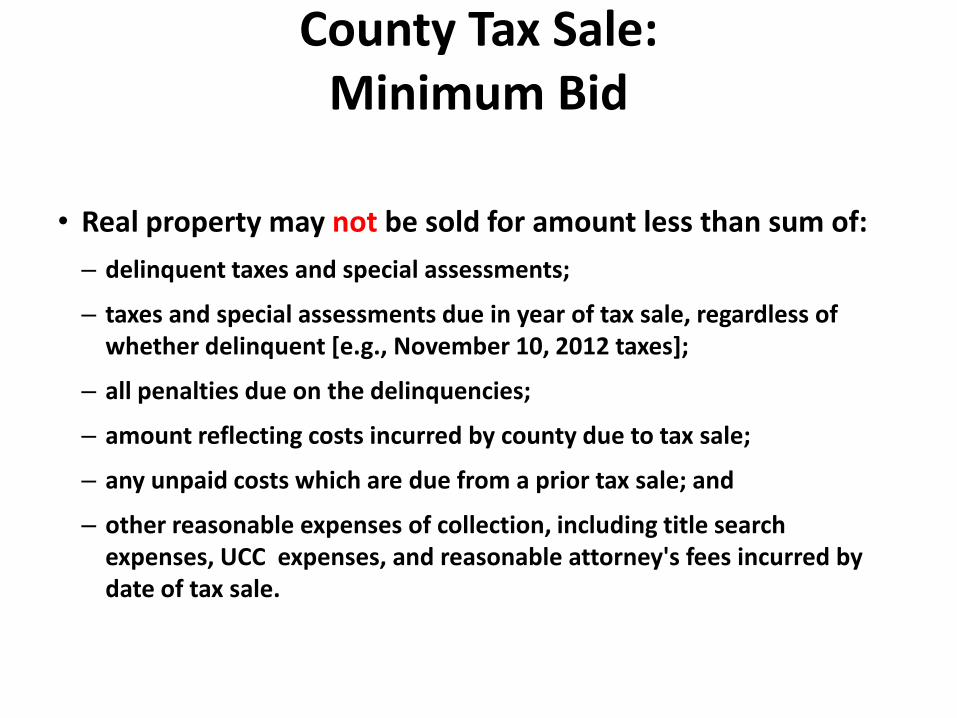

County Tax Sale:Minimum Bid

• Real property may not be sold for amount less than sum of:

– delinquent taxes and special assessments;

– taxes and special assessments due in year of tax sale, regardless of whether delinquent [e.g., November 10, 2012 taxes];

– all penalties due on the delinquencies;

– amount reflecting costs incurred by county due to tax sale;

– any unpaid costs which are due from a prior tax sale; and

– other reasonable expenses of collection, including title search expenses, UCC expenses, and reasonable attorney's fees incurred by date of tax sale.

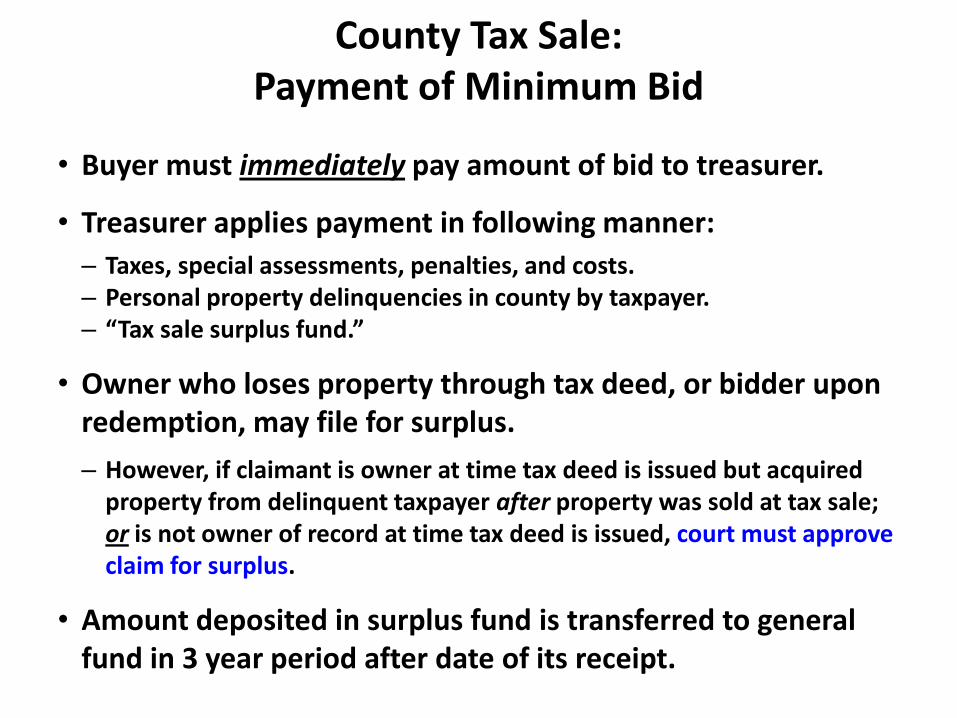

• Buyer must immediately pay amount of bid to treasurer.

• Treasurer applies payment in following manner:

– Taxes, special assessments, penalties, and costs.– Personal property delinquencies in county by taxpayer.– “Tax sale surplus fund.”

• Owner who loses property through tax deed, or bidder upon redemption, may file for surplus.

– However, if claimant is owner at time tax deed is issued but acquired property from delinquent taxpayer after property was sold at tax sale; or is not owner of record at time tax deed is issued, court must approve claim for surplus.

• Amount deposited in surplus fund is transferred to general fund in 3 year period after date of its receipt.

County Tax Sale:Payment of Minimum Bid

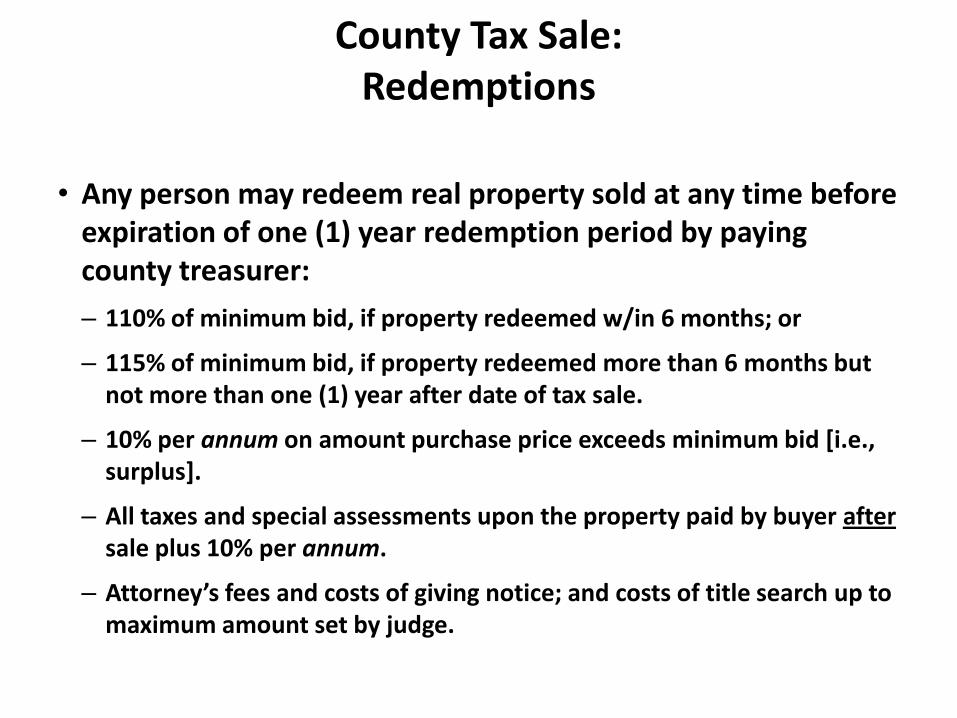

• Any person may redeem real property sold at any time before expiration of one (1) year redemption period by paying county treasurer:

– 110% of minimum bid, if property redeemed w/in 6 months; or

– 115% of minimum bid, if property redeemed more than 6 months but not more than one (1) year after date of tax sale.

– 10% per annum on amount purchase price exceeds minimum bid [i.e., surplus].

– All taxes and special assessments upon the property paid by buyer aftersale plus 10% per annum.

– Attorney’s fees and costs of giving notice; and costs of title search up to maximum amount set by judge.

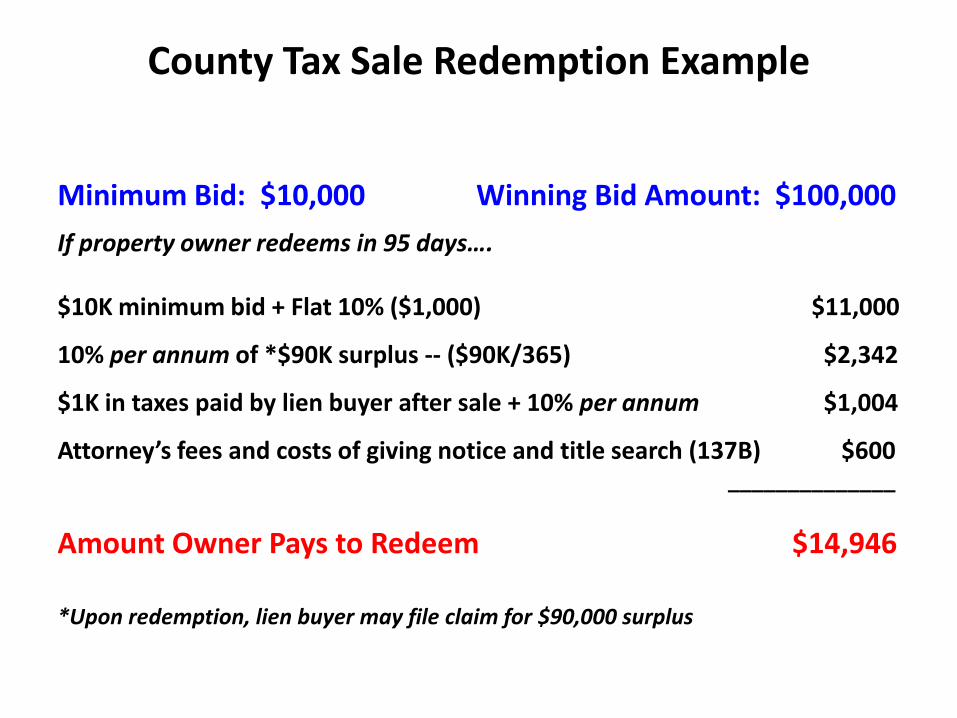

County Tax Sale:Redemptions

Minimum Bid: $10,000 Winning Bid Amount: $100,000

If property owner redeems in 95 days….

$10K minimum bid + Flat 10% ($1,000) $11,000

10% per annum of *$90K surplus -- ($90K/365) $2,342

$1K in taxes paid by lien buyer after sale + 10% per annum $1,004

Attorney’s fees and costs of giving notice and title search (137B) $600______________

Amount Owner Pays to Redeem $14,946

*Upon redemption, lien buyer may file claim for $90,000 surplus

County Tax Sale Redemption Example

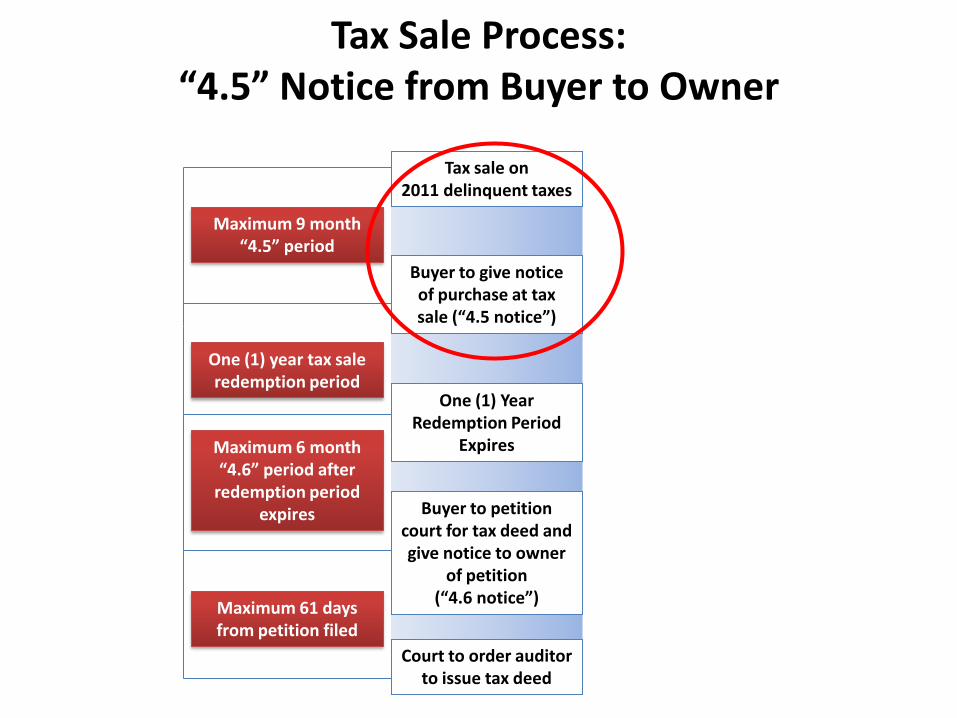

Tax Sale Process: “4.5” Notice from Buyer to Owner

Tax sale on 2011 delinquent taxes

Buyer to give notice of purchase at tax sale (“4.5 notice”)

One (1) Year Redemption Period

Expires

Maximum 9 month “4.5” period

Buyer to petition court for tax deed and give notice to owner

of petition (“4.6 notice”)

Court to order auditor to issue tax deed

One (1) year tax sale redemption period

Maximum 6 month “4.6” period after

redemption period expires

Maximum 61 days from petition filed

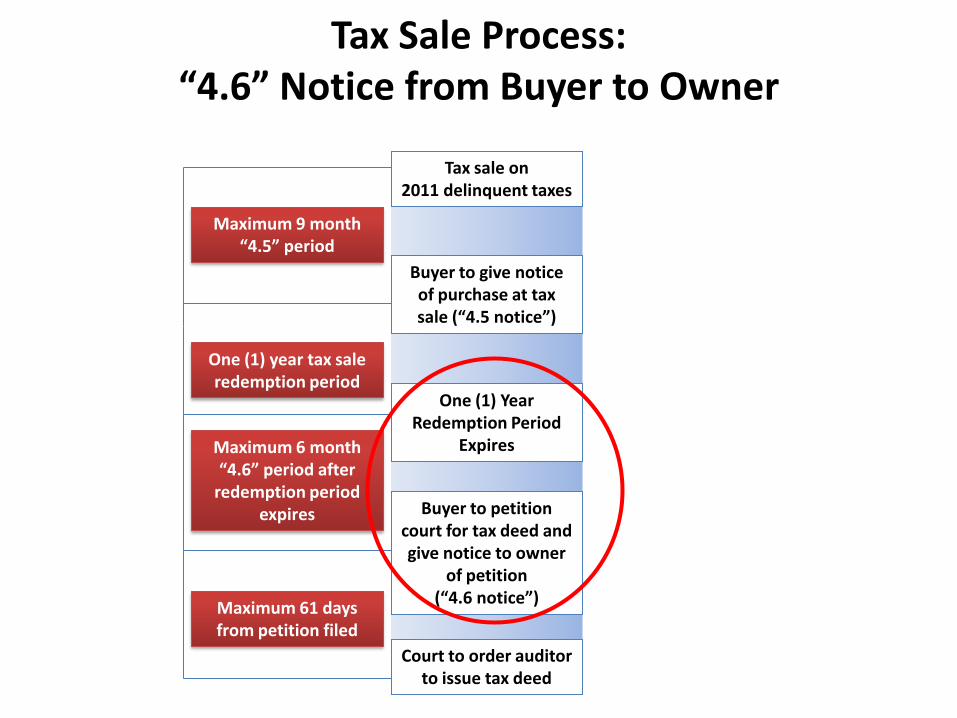

Tax Sale Process: “4.6” Notice from Buyer to Owner

Tax sale on 2011 delinquent taxes

Buyer to give notice of purchase at tax sale (“4.5 notice”)

One (1) Year Redemption Period

Expires

Maximum 9 month “4.5” period

Buyer to petition court for tax deed and give notice to owner

of petition (“4.6 notice”)

Court to order auditor to issue tax deed

One (1) year tax sale redemption period

Maximum 6 month “4.6” period after

redemption period expires

Maximum 61 days from petition filed

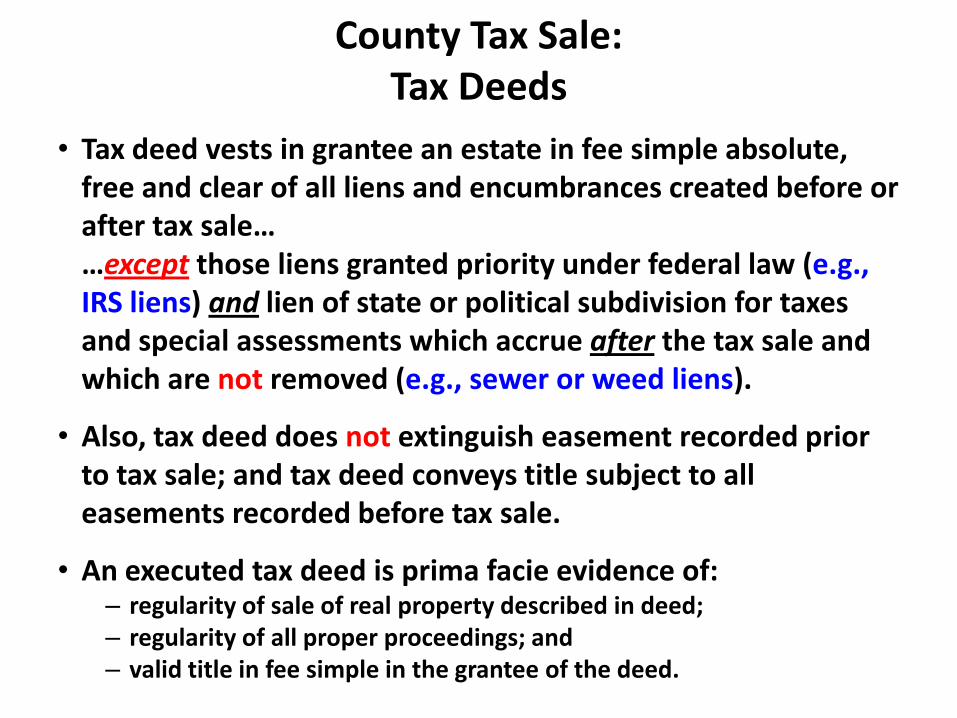

• Tax deed vests in grantee an estate in fee simple absolute, free and clear of all liens and encumbrances created before or after tax sale……except those liens granted priority under federal law (e.g., IRS liens) and lien of state or political subdivision for taxes and special assessments which accrue after the tax sale and which are not removed (e.g., sewer or weed liens).

• Also, tax deed does not extinguish easement recorded prior to tax sale; and tax deed conveys title subject to all easements recorded before tax sale.

• An executed tax deed is prima facie evidence of:– regularity of sale of real property described in deed;– regularity of all proper proceedings; and– valid title in fee simple in the grantee of the deed.

County Tax Sale:Tax Deeds

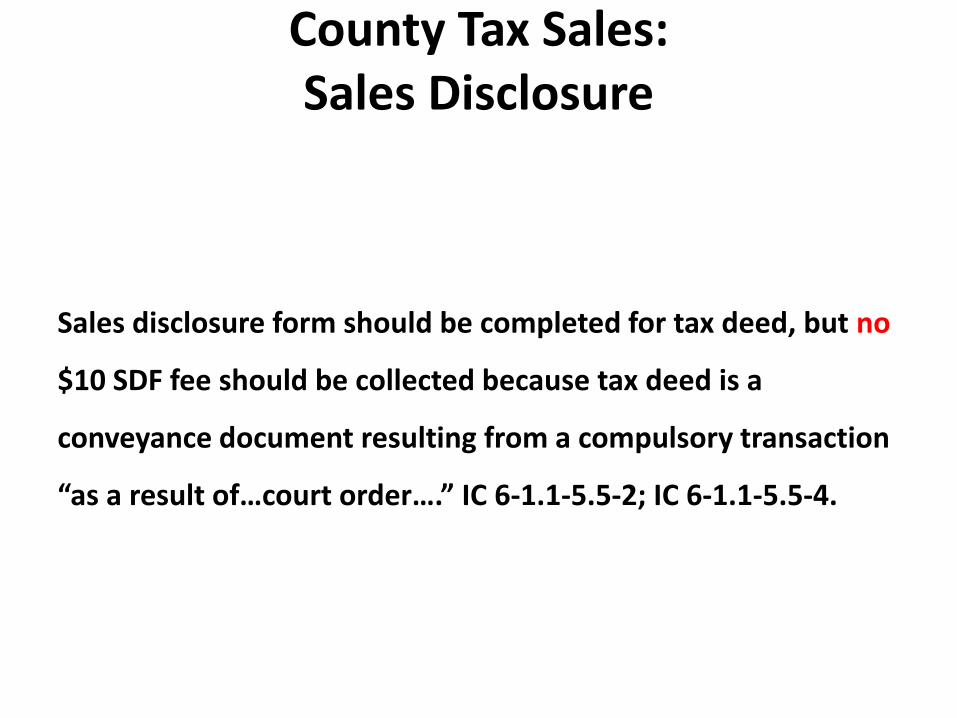

County Tax Sales: Sales Disclosure

Sales disclosure form should be completed for tax deed, but no

$10 SDF fee should be collected because tax deed is a

conveyance document resulting from a compulsory transaction

“as a result of…court order….” IC 6-1.1-5.5-2; IC 6-1.1-5.5-4.

Commissioners’ Certificate Sale

• County commissioners are issued a tax sale certificate for all properties where a lien was not sold at county tax sale.

– Awarded same rights as Buyer; however, do not pay money. – May offer for sale tax sale certificate for reduced minimum bid.– May establish selling price for certificate by resolution.

• Buyer of lien at Commissioner’s Certificate Sale will pay amount established by commissioners and are issued tax sale certificate with same requirements as property purchased at county tax sale.

• Significant difference between certificate sale and prior county tax sale is Certificate Sale redemption period is 120 days and minimum bids are reduced.

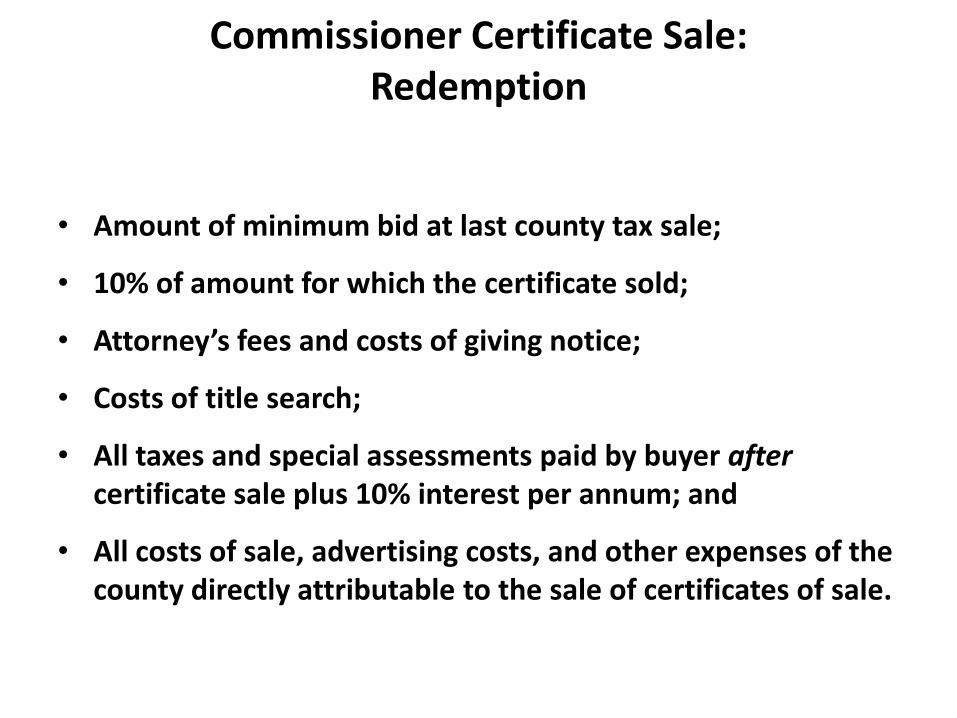

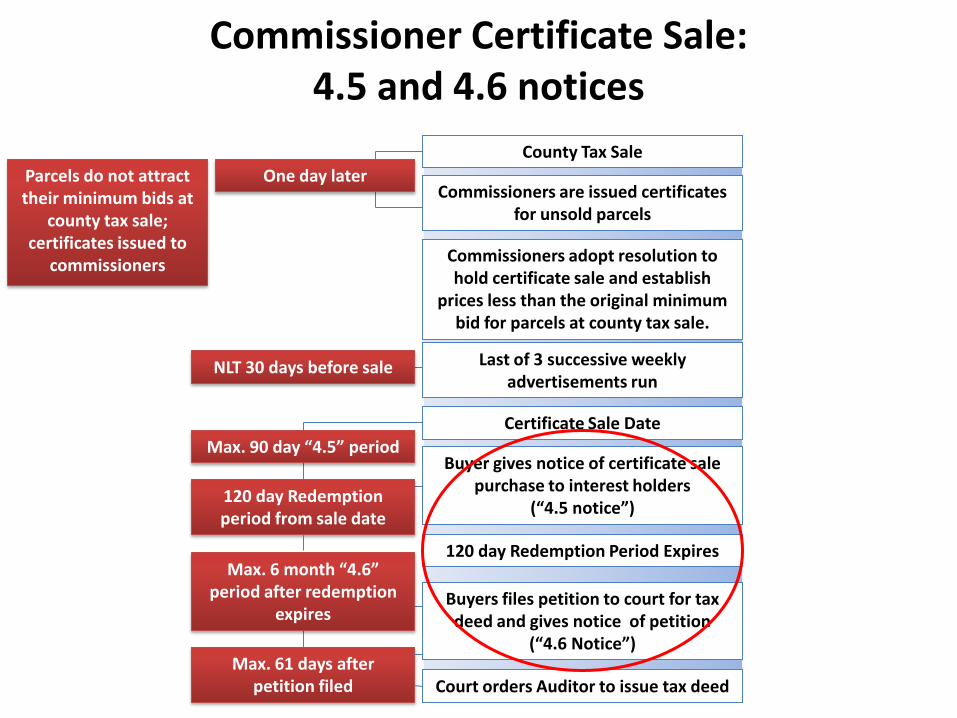

Commissioner Certificate Sale:Overview

County Tax Sale

One day laterCommissioners are issued certificates

for unsold parcels

Commissioners adopt resolution to hold certificate sale and establish

prices less than the original minimum bid for parcels at county tax sale.

Last of 3 successive weekly advertisements run

Certificate Sale Date

Buyer gives notice of certificate sale purchase to interest holders

(“4.5 notice”)

120 day Redemption Period Expires

Buyers files petition to court for tax deed and gives notice of petition

(“4.6 Notice”)

Court orders Auditor to issue tax deed

Parcels do not attract their minimum bids at

county tax sale; certificates issued to

commissioners

NLT 30 days before sale

Max. 90 day “4.5” period

120 day Redemption period from sale date

Max. 6 month “4.6” period after redemption

expires

Max. 61 days after petition filed

Commissioner Certificate Sale:Process

• Amount of minimum bid at last county tax sale;

• 10% of amount for which the certificate sold;

• Attorney’s fees and costs of giving notice;

• Costs of title search;

• All taxes and special assessments paid by buyer aftercertificate sale plus 10% interest per annum; and

• All costs of sale, advertising costs, and other expenses of the county directly attributable to the sale of certificates of sale.

Commissioner Certificate Sale:Redemption

Certificate Amount (county tax sale minimum bid): $10,000

Certificate Sale Minimum Bid: $500

Winning Bid Amount at Certificate Sale: $9,000

If property owner redeems in 45 days from commissioners’ certificate sale….

Amount of minimum bid at last county tax sale $10,000

10% of amount for which certificate sold ($9K x 10%) $900

Attorney’s fees and costs of giving notice; and title search $500

Taxes paid after sale plus 10% interest per annum $0

All costs of sale (county and vendor)-$25 county fee for advertising $25-10% of winning bid amount to vendor for Internet sale $900

____________

Redemption Amount to be Paid $12,325

Certificate Sale: Redemption Example

County Tax Sale

One day laterCommissioners are issued certificates

for unsold parcels

Commissioners adopt resolution to hold certificate sale and establish

prices less than the original minimum bid for parcels at county tax sale.

Last of 3 successive weekly advertisements run

Certificate Sale Date

Buyer gives notice of certificate sale purchase to interest holders

(“4.5 notice”)

120 day Redemption Period Expires

Buyers files petition to court for tax deed and gives notice of petition

(“4.6 Notice”)

Court orders Auditor to issue tax deed

Parcels do not attract their minimum bids at

county tax sale; certificates issued to

commissioners

NLT 30 days before sale

Max. 90 day “4.5” period

120 day Redemption period from sale date

Max. 6 month “4.6” period after redemption

expires

Max. 61 days after petition filed

Commissioner Certificate Sale:4.5 and 4.6 notices

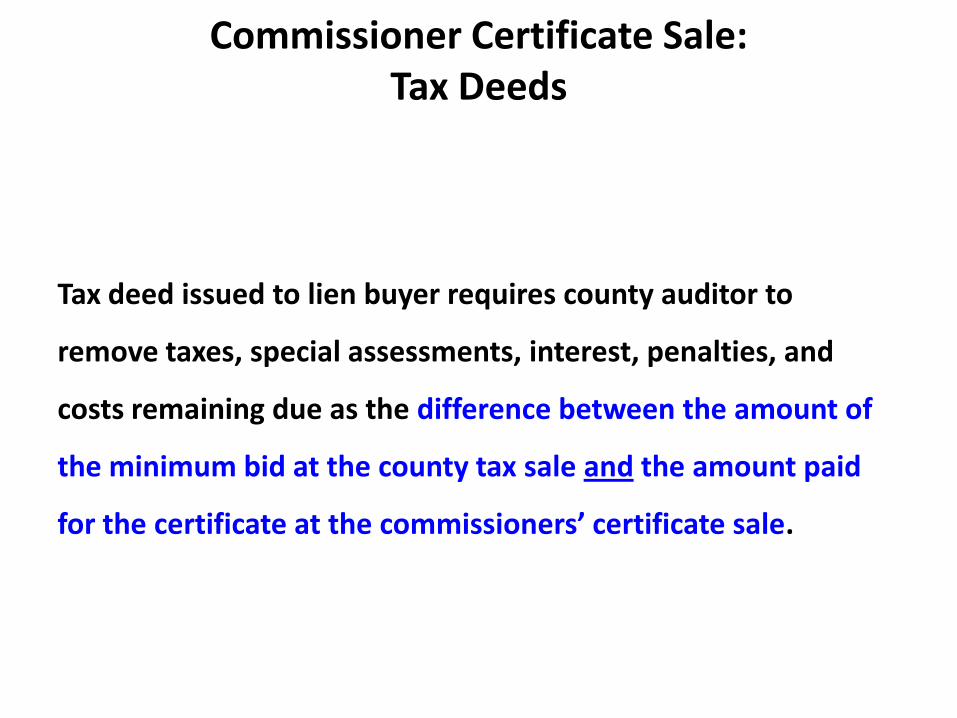

Tax deed issued to lien buyer requires county auditor to

remove taxes, special assessments, interest, penalties, and

costs remaining due as the difference between the amount of

the minimum bid at the county tax sale and the amount paid

for the certificate at the commissioners’ certificate sale.

Commissioner Certificate Sale:Tax Deeds

Questions?

SRI, Inc.

8082 Bash Street

Indianapolis, IN 46250

www.sri-taxsale.com

Office: (317) 842-5818

Toll Free: (800) 800-9588