Embed Size (px)

Citation preview

PROPERTY INSURANCE FUNDAMENTALS

by

CPMI Professional Development, Inc.

Copyright January 2020 First printed 1999

CPMI Professional Development, Inc., 691 W. Spring Creek Pl. #150 Springville, UT 84663e-mail: [email protected] Phone: 815-271-8200 Website: www.cpmipro.com

This textbook and the material herein are intended for the exclusive use of participants in the training programsof CPMI Professional Development, Inc. and are to be used in preparation for state insurance producer exams

and continuing education courses. Reproduction of this material for or distribution to individuals in a way not inkeeping with the sales and rental agreements of CPMI Professional Development, Inc. is strictly prohibited.

The proper use of the video and textbook program should be sufficient in aiding the student to pass the producerexam. Final results on the exam, however, will depend on the background and effort that each individual brings

to it, and therefore no guarantees can be given based on the content of this course alone.

This material is designed for educational purposes only and is not intended as financial or legal advice. If legalor other professional advice is required, the services of a competent professional should be sought.

Any reproduction of this textbook or any portion of it without the written permission of CPMI ProfessionalDevelopment, Inc. is strictly prohibited and will be prosecuted to the full extent of the law.

CPMI Professional Development, Inc. 2

TABLE OF CONTENTSStudying for the State Insurance Producer Licensing Exam....................................................9Tips for Taking the Insurance Licensing Exam....9

Learning the Material Using the Text, Video, and Audio Resources......................9Answering the Review Questions and Taking the Practice Exams.......................10

Before Taking the Insurance Licensing Exam....11Section I – General Insurance Concepts..................12

Risk Management Key Terms.......................12Insurance..................................................12Indemnity.................................................12Loss..........................................................12Insurable Interest......................................12Risk..........................................................12Negligence................................................13Self-Insurance...........................................13Applicant..................................................13Insurer......................................................13Insured......................................................13Agent/Producer.........................................13Policy Owner............................................13Binder.......................................................13Certificate of Insurance.............................13Endorsement.............................................13Waiver and Estoppel.................................13Accident...................................................14Occurrence...............................................14Exposure...................................................14Hazard......................................................14Peril..........................................................14Maslow's Hierarchy of Needs...................14National Association of Insurance Commissioners (NAIC)............................14Tort...........................................................15Co-Insurance............................................15Deposit Premium......................................15Burglary....................................................15Robbery....................................................15Larceny.....................................................15Theft.........................................................15Mysterious Disappearance........................15Liability....................................................15Actual Cash Value....................................15

Personal Lines vs. Commercial Lines............15Methods of Handling Risk.............................15

Avoidance.................................................15Retention..................................................16Sharing.....................................................16Reduction.................................................16Transfer....................................................16

Elements of Insurable Risks..........................16Adverse Selection..........................................16Reinsurance...................................................16Indemnity/Pay on Behalf Of..........................17Limits of Liability..........................................17Deductible.....................................................17

Insurers...............................................................17Types of Insurers...........................................17

Multi-Line Insurance Companies.............17Stock Companies......................................17Mutual Companies....................................17Reciprocal Companies..............................17Risk Retention Groups..............................17Purchasing Groups....................................17Risk Retention Groups (RRG) vs. Purchasing Groups (PG)...........................18Fraternal Benefit Societies........................18Syndicate Insurers (Lloyd's Associations) 18Surplus/Excess Lines Insurers..................18Private vs. Government Insurers...............18

Admitted vs. Non-Admitted Insurers.............19Admitted Insurer/Authorized Insurer........19Non-Admitted Insurer/Non-Authorized Insurer......................................................19

Domestic, Foreign, and Alien Insurers..........19Domestic Insurer......................................19Foreign Insurer.........................................19Alien Insurer.............................................19

Financial Solvency Status (Independent Rating Services)........................................................19Marketing (Distribution Systems)..................19

Types of Agents/Marketing Systems........19Producers and General Rules of Agency.............20

Insurer as Principal........................................20Producer/Insurer Relationship.......................20

Agency Agreement/Contract....................20Insurance Agent vs. Broker......................20Professionalism and Ethical Conduct.......20Fiduciary...................................................20Captive Insurance Companies..................21

Authority and Powers of Producers...............21Law of Agency.........................................21Express Directive......................................21Implied Directive......................................21Apparent Directive...................................21

Responsibilities to the Applicant and Insured21Common Situations for Errors and Omissions.................................................21

Contracts.............................................................22Elements of a Legal Contract.........................22

1. Offer and Acceptance...........................22

CPMI Professional Development, Inc. 3

2. Consideration........................................223. Competent Parties.................................224. Legal purpose.......................................22Mutual Agreement....................................22

Characteristics of an Insurance Contract........22Two Party Contracts.................................22Third Party Contracts................................23Contract of Adhesion................................23Aleatory Contract.....................................23Personal Contract......................................23Unilateral Contract...................................23Conditional Contract.................................23Contract of Indemnity...............................23

Legal Interpretations Affecting Contracts......23Ambiguities in a Contract of Adhesion.....23Reasonable Expectations..........................23Utmost Good Faith...................................23Representations/Misrepresentations..........23Warranties................................................23Concealment.............................................24Fraud........................................................24

Unfair Marketing Practices............................24Misrepresentation.....................................24Unfair Policy Replacement.......................24Discrimination..........................................24Rebating...................................................24Redlining..................................................25Boycotting................................................25Intimidation..............................................25Monopoly in the Insurance Business........25Misappropriation of Funds.......................25False Financial Statements.......................25

Section I – General Insurance Concepts Review Questions............................................................26

Section II – Property Insurance Concepts................29Principles and Concepts......................................29

Insurable Interest...........................................29Underwriting.................................................29

Function....................................................29Sources of Underwriting Information:......29Rating Types.............................................29Loss Ratio.................................................29

Rates..............................................................29Types of Rates..........................................29Loss Costs................................................30Components/Premium Determination.......30

Hazards..........................................................30Physical....................................................30Moral........................................................30Morale......................................................30Legal.........................................................30

Causes of Loss (Perils)..................................30

Named Perils vs. Open-Perils........................30Named Peril Policies................................30Open-Peril Policies...................................30

Direct and Indirect Losses.............................30Direct Loss...............................................30Consequential or Indirect Losses..............30

Liability.........................................................31Absolute/Strict Liability...........................31Vicarious Liability....................................31

Proximate Cause............................................31Blanket vs. Specific Insurance.......................31Basic Types of Construction..........................31

Basic Types of Construction.....................31Classifications of Construction.................31

Loss Valuation...............................................32Sentimental Value....................................32Resale Value.............................................32Actual Cash Value (ACV)........................32Replacement Cost.....................................32Functional Replacement Cost...................32Guaranteed Replacement Cost..................32Market Value............................................32Agreed Value............................................32Stated Amount..........................................32Valued Policy...........................................32Limit of Liability......................................32Fire Legal Liability...................................32

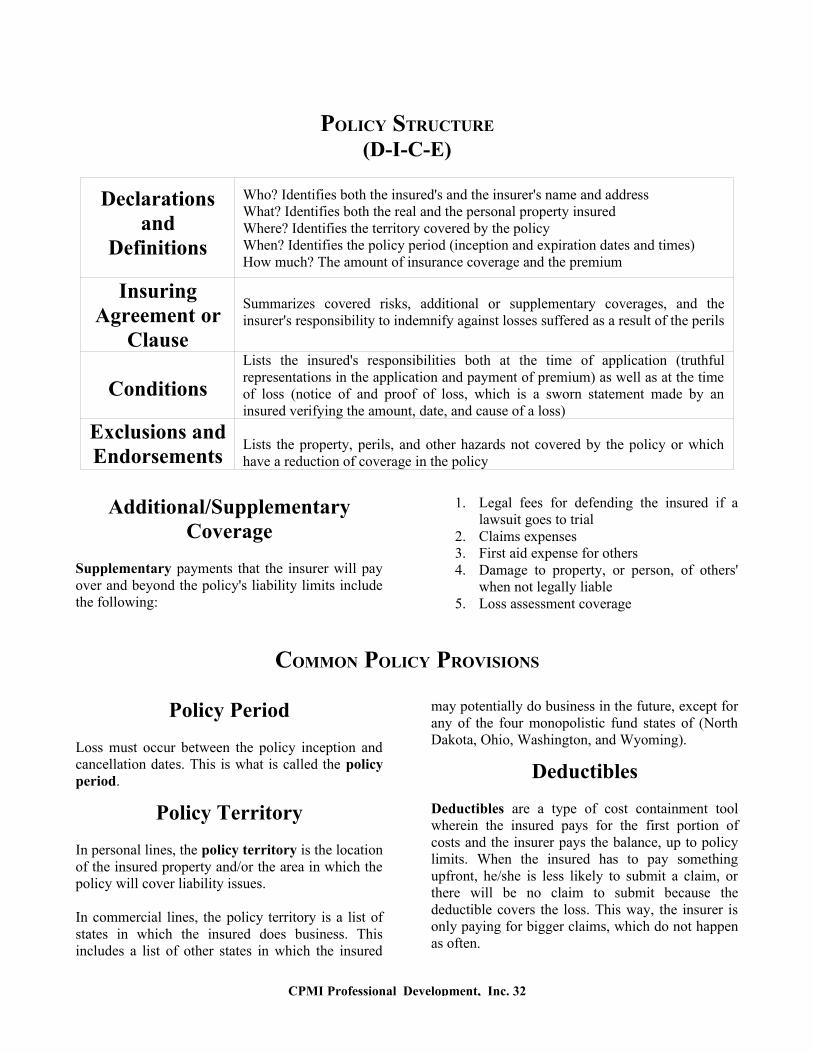

Policy Structure..................................................33(D-I-C-E).......................................................33Declarations and Definitions.........................33Insuring Agreement or Clause.......................33Conditions.....................................................33Exclusions and Endorsements........................33Additional/Supplementary Coverage.............33

Common Policy Provisions................................33Policy Period.................................................33Policy Territory.............................................33Deductibles....................................................33Other Insurance.............................................34

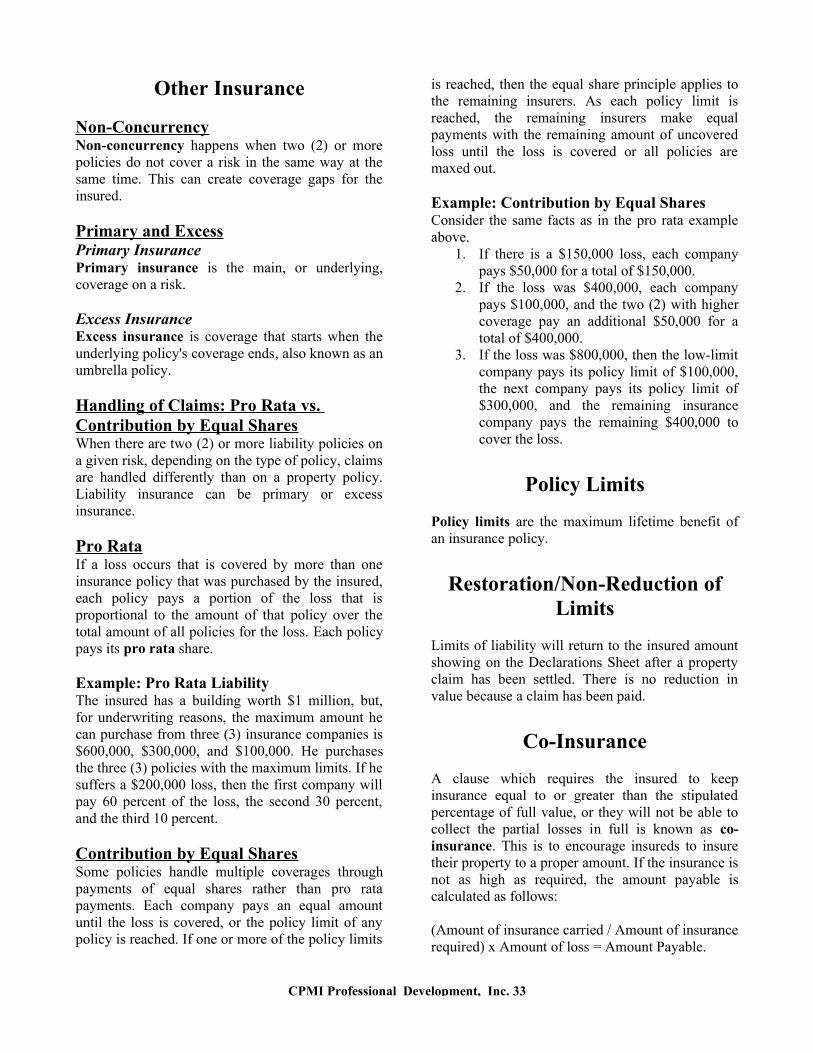

Non-Concurrency.....................................34Primary and Excess..................................34Handling of Claims: Pro Rata vs. Contribution by Equal Shares...................34Pro Rata....................................................34Contribution by Equal Shares...................34

Policy Limits.................................................34Restoration/Non-Reduction of Limits............34Co-Insurance.................................................34Vacancy or Unoccupancy..............................35Named Insured Provisions.............................35

Insured's Duties After Loss (Claims Handling):.................................................35

CPMI Professional Development, Inc. 4

Appraisal and Arbitration.........................35Assignment...............................................35Abandonment...........................................35

Insurer Provisions..........................................35Duty to Defend.........................................35Liberalization Clause................................35Subrogation..............................................35Salvage.....................................................36Claim Settlement Options.........................36

Third Party Provisions...................................36Standard Mortgagee Clause......................36Loss Payable Clause.................................36No Benefit to the Bailee...........................36

Personal Property Lines......................................36State and Federal Laws, Regulations and RequiredProvisions...........................................................36

State Property and Casualty Insurance Guaranty Association....................................36Standard Fire Policy......................................37Cancellation and Non-Renewal.....................37

Private Residence.....................................37Commercial..............................................37Basic Property Insurance-Death of Named Insured......................................................37

Negligence.....................................................37Elements of a Negligent Act.....................37Four (4) Basic Categories of Individuals that Cannot Be Held Negligent.................38Defenses Against Negligence...................38Common Law Defenses............................38

Binders..........................................................38Insurance Consultation Services Exemption..39

Fair Credit Reporting Act...................................39Use of Credit Information..............................39

How Long Can Negative Information Stay on a Credit Report?...................................39

Fraud and False Statements................................40Those with Felony Records......................40Those Permitting/Complicit in These Actions.....................................................40Penalties...................................................40

Privacy Protection...............................................40Terrorism Risk Insurance Act (TRIA)................40

Purpose.....................................................40Definitions................................................40Requirement for Terrorism Risk Coverage to be Offered.............................................41Effect on Workers Compensation.............41

Extension Act of 2005...................................41Re-Authorization Act of 2007.......................42The Terrorism Risk Insurance Program Re-Authorization Act (TRIPRA) of 2015............42

Minimum Threshold and Certification.....42Program Trigger.......................................42

Section III – Dwelling Policy (DP)..........................44Characteristics and Purpose................................44

Eligibility..................................................44Coverage Forms: Perils Insured Against and Property Covered................................................44

Definitions................................................44Standard Fire Policy Perils............................44Extended Coverage Perils..............................44Basic Form (DP-1).........................................45Broad Form (DP-2)........................................45Special Form (DP-3)......................................45

General Exclusions.............................................46Conditions..........................................................46Selected Endorsements.......................................47

Special Provisions for States..........................47Automatic Increase in Insurance....................47Broad Theft Coverage....................................47Dwelling Under Construction........................47

Personal Liability Supplement............................47Ordinance or Law...............................................47Section III – Dwelling Policy (DP) Review Questions............................................................48

Section IV – Homeowners’ Policy...........................49Purpose...............................................................49Coverage Forms..................................................49

HO-1..............................................................49HO-2 – HO-8.................................................49

Broad Form/HO-2 (Named Peril).............49Special Form/HO-3 (Special Peril)/Open-Peril).........................................................49Homeowners Contents/Tenant/Renter’s Coverage/HO-4.........................................50Comprehensive Form/HO-5 (Special Peril/Open-Peril)...............................................50Condominium Unit Owner Form/HO-6....50

Market Value/ Modified Coverage Form HO-8.......................................................................50

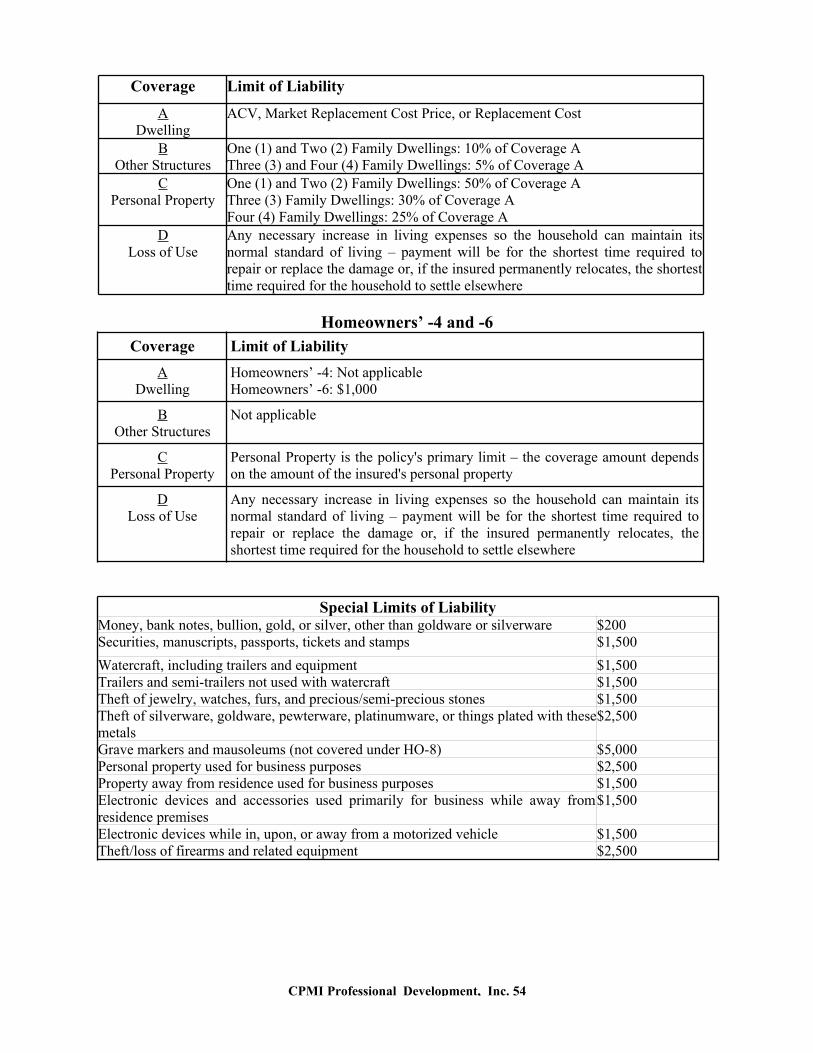

Property and Liability Coverages.......................51Coverage A-Dwelling....................................51Coverage B-Other Structures.........................51Coverage C-Personal Property.......................51Coverage D-Loss of Use................................51Coverage E-Personal Liability.......................51Coverage F-Medical Payments to Others......51Additional Coverages....................................51

Perils Insured Against.........................................52Broad Form/HO-2, Named Perils.............52Special Form/HO-3, Special Perils/Open-Peril..........................................................52Homeowners Contents/Tenant/Renter's

CPMI Professional Development, Inc. 5

Coverage/HO-4.........................................53Comprehensive Form/HO-5 (Special Peril/Open-Peril)...............................................53Condominium Unit Owner Form/HO-6....53

Additional Homeowners’ Notes..........................53Pair and Sets Clause.................................53Additional/Supplemental Coverages.........53

Exclusions..........................................................53Conditions..........................................................54

Personal Property Replacement Cost.............54Homeowners’ -2, -3, -5, and -8 Policies. . .54

Selected Endorsements.......................................56Special Provisions for States..........................56Limited Fungi, Wet or Dry Rot, or Bacteria Coverage........................................................56Permitted Incidental Occupancies/Business Pursuits..........................................................56Earthquake.....................................................56Scheduled Personal Property/Personal Article Floater............................................................56Home Day Care.............................................56

Windstorm or Hail....................................57Special Additional Amount of Insurance forCoverage A...............................................57Identity Fraud Expense Coverage.............57Functional Replacement Cost...................57Property Remediation for Escaped Fuel and Limited Lead and Escaped Liquid Fuel Liability....................................................57

Mobile Home Policies........................................57Restrictions on Mobile Home Policy Coverage...................................................57

Section IV – Homeowners’ Policy Review Questions............................................................58

Section V – Commercial Package Policy.................60Introduction........................................................60

Insurance Services Office (ISO)...............60Components of a Commercial Policy.................60

Common Policy Declarations........................61Interline Endorsements..................................61One or More Coverage Parts.........................61

Commercial Property..........................................61Commercial Property Conditions Form.........61Commercial Coverage Forms........................61

Building and Personal Property................61Condominium Association.......................62Condominium Commercial Unit-Owners. 62Builders Risk............................................62Business Income.......................................62Legal Liability..........................................62Extra Expense...........................................62

Causes of Loss Forms: Basic, Broad, and

Special...........................................................63Selected Commercial Property Endorsements.......................................................................63

Ordinance or Law.....................................63Spoilage....................................................63Peak Season Limit of Insurance................63Value Reporting Form..............................63Earthquake................................................64

Commercial Inland Marine.................................64Nationwide Marine Definition.......................64Commercial Inland Marine Conditions Form 64Inland Marine Coverage Forms.....................64

Accounts Receivable................................64Bailee's Customer.....................................64Commercial Articles.................................64Commercial Contractor's Equipment Floater..................................................................64Electronic Data Processing (EDP)............64Equipment Dealers...................................64Installation Floater....................................65Jeweler's Block.........................................65Signs.........................................................65Camera and Musical Instrument Dealers Form.........................................................65Valuable Papers and Records...................65

Transportation Coverages..............................65Common Carrier Cargo Liability..............65Motor Truck Cargo Forms........................66Transit Coverage Forms...........................66Released Bills of Lading...........................66

Equipment Breakdown Coverage.......................66Parts of an Equipment Breakdown Policy 66Coverages.................................................66

Covered Property...........................................66Conditions.....................................................67

Periodic Inspection and the Suspension Provision...................................................67

Equipment Breakdown Protection Coverage Form..............................................................67Selected Endorsements..................................67

Business Income – Report of Values........67Actual Cash Value....................................67

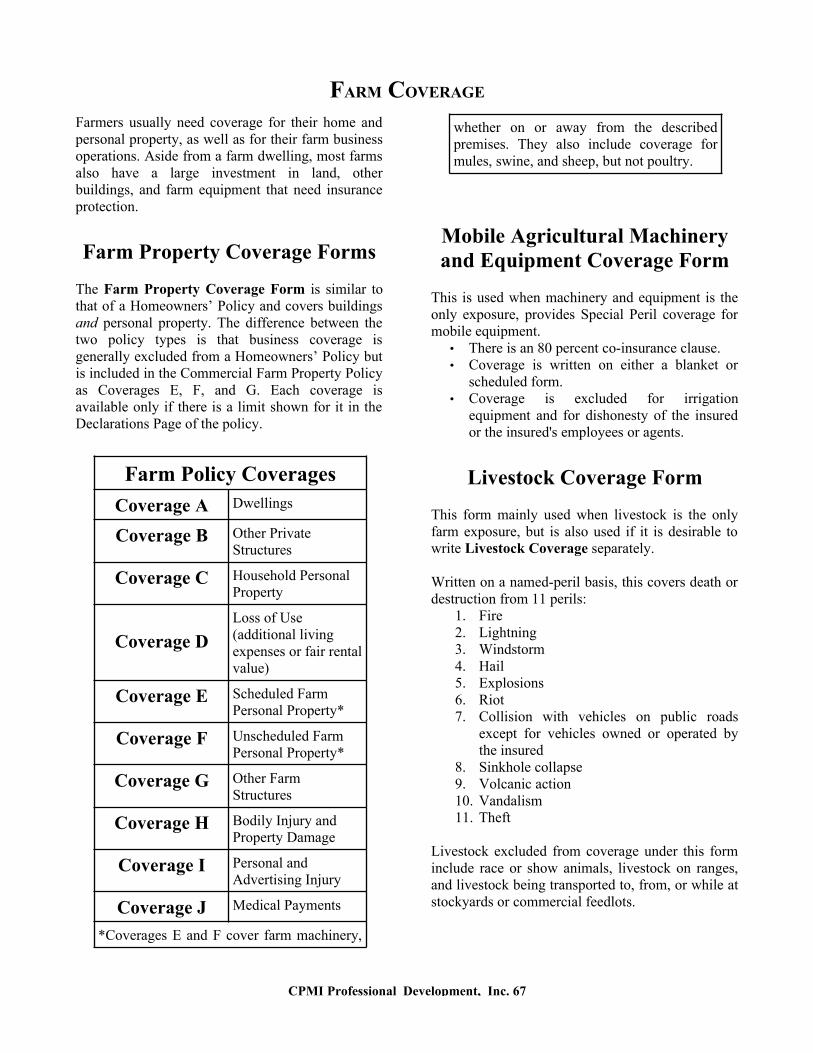

Farm Coverage...................................................68Farm Property Coverage Forms.....................68Coverage A....................................................68Coverage B....................................................68Coverage C....................................................68Coverage D....................................................68Coverage E....................................................68Coverage F....................................................68Coverage G....................................................68Coverage H....................................................68

CPMI Professional Development, Inc. 6

Coverage I.....................................................68Coverage J.....................................................68Mobile Agricultural Machinery and EquipmentCoverage Form..............................................68Livestock Coverage Form..............................68Definitions.....................................................69Causes of Loss (Basic, Broad and Special)....69Conditions.....................................................69

Loss Conditions........................................69Exclusions.....................................................70Limits............................................................72Additional Coverages....................................72

Farm Umbrella Coverage.........................72Section V – Commercial Package Policy Review Questions............................................................73

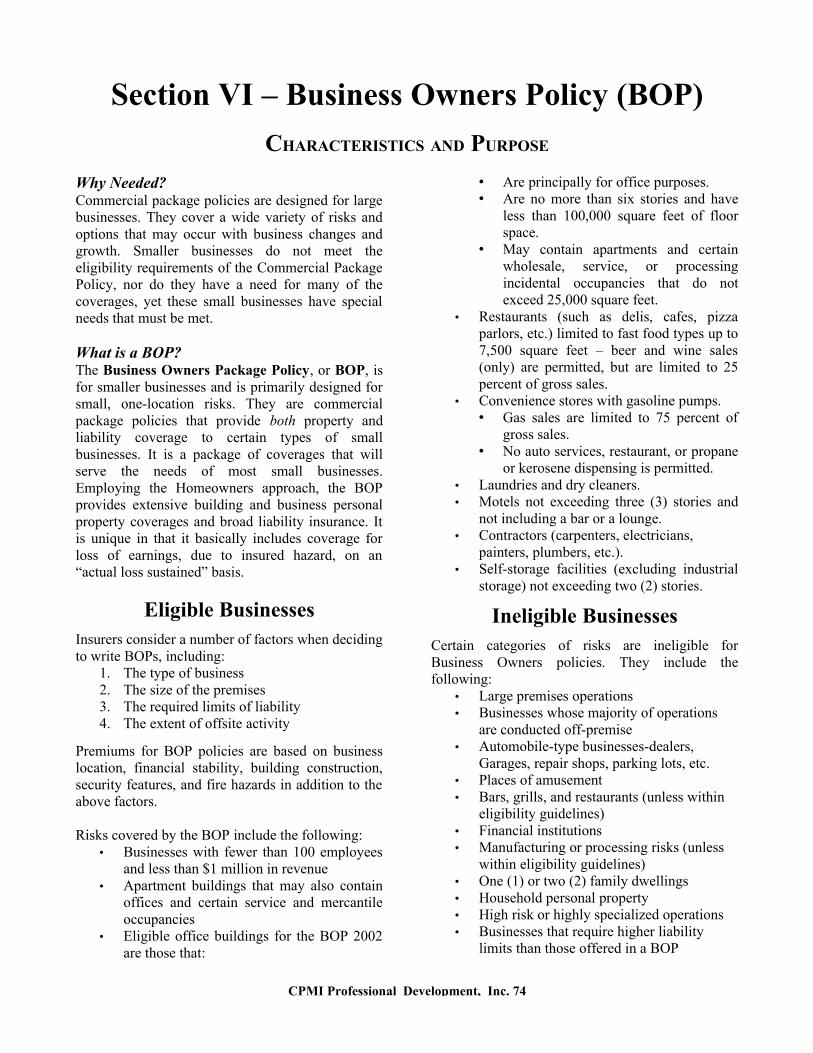

Section VI – Business Owners Policy (BOP)..........75Characteristics and Purpose................................75

Eligible Businesses........................................75Ineligible Businesses.....................................75

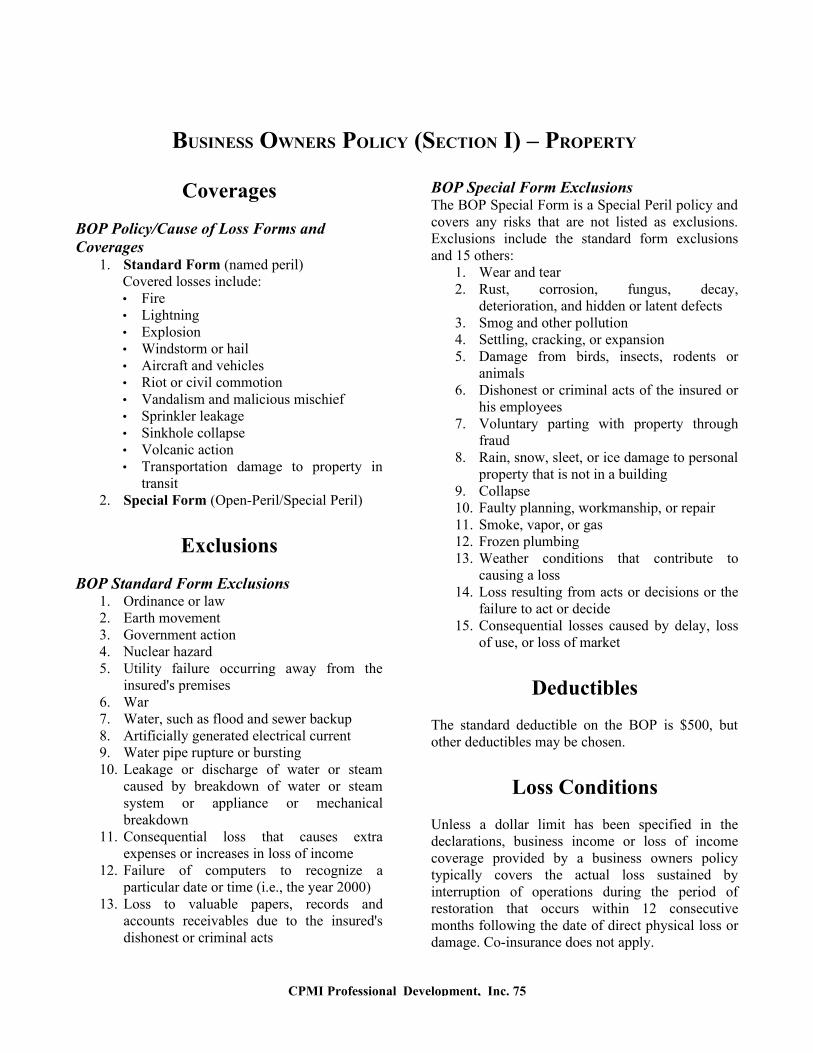

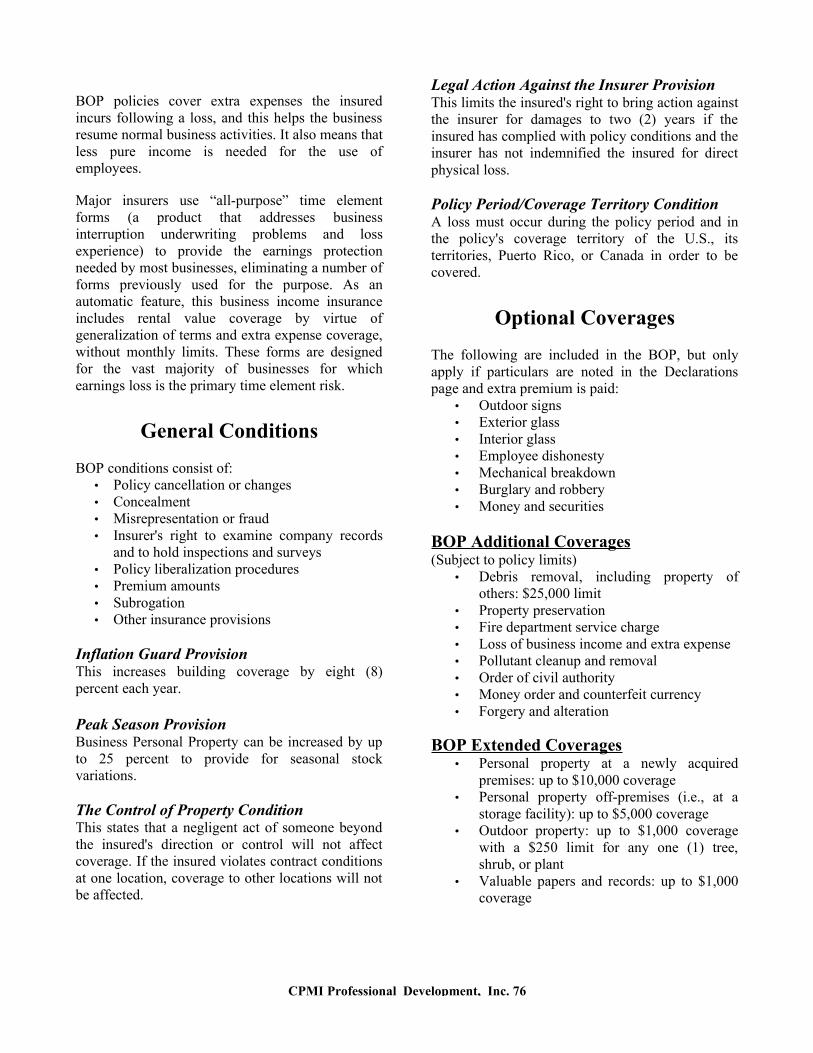

Business Owners Policy (Section I) – Property. .76Coverages......................................................76Exclusions.....................................................76Deductibles....................................................76Loss Conditions.............................................76General Conditions........................................77Optional Coverages.......................................77

BOP Additional Coverages.......................77BOP Extended Coverages.........................77

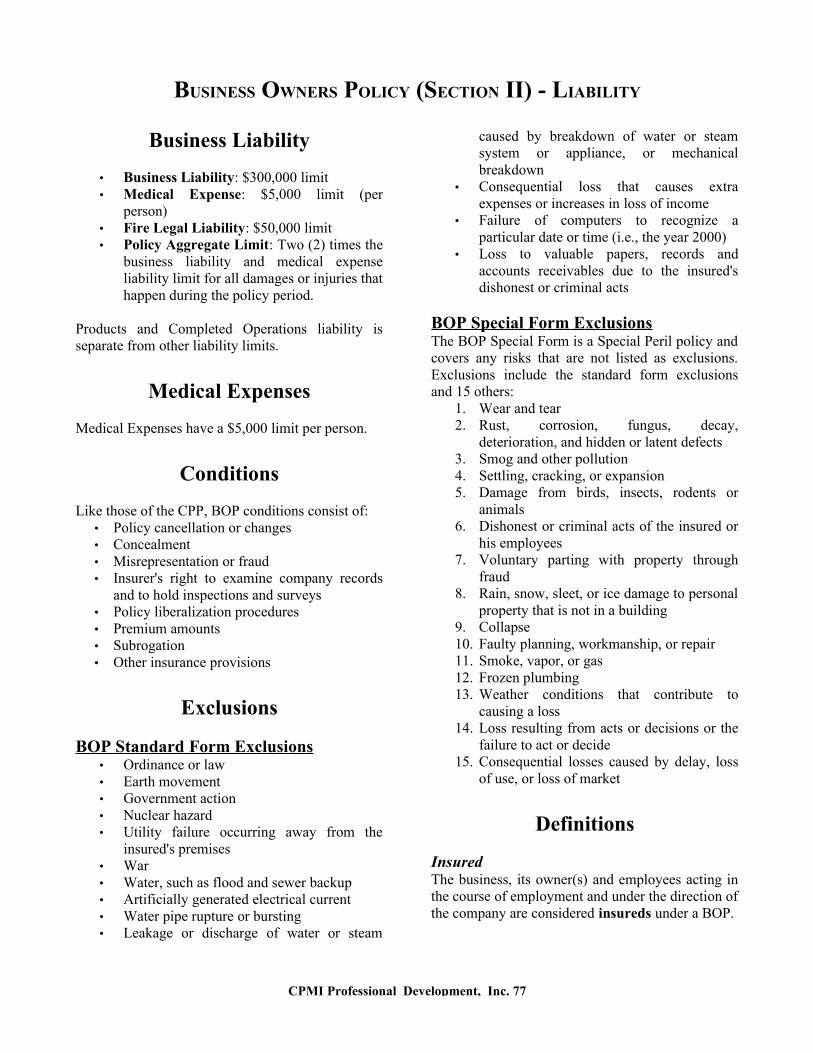

Business Owners Policy (Section II) - Liability..78Business Liability..........................................78Medical Expenses..........................................78Conditions.....................................................78Exclusions.....................................................78

BOP Standard Form Exclusions...............78BOP Special Form Exclusions..................78

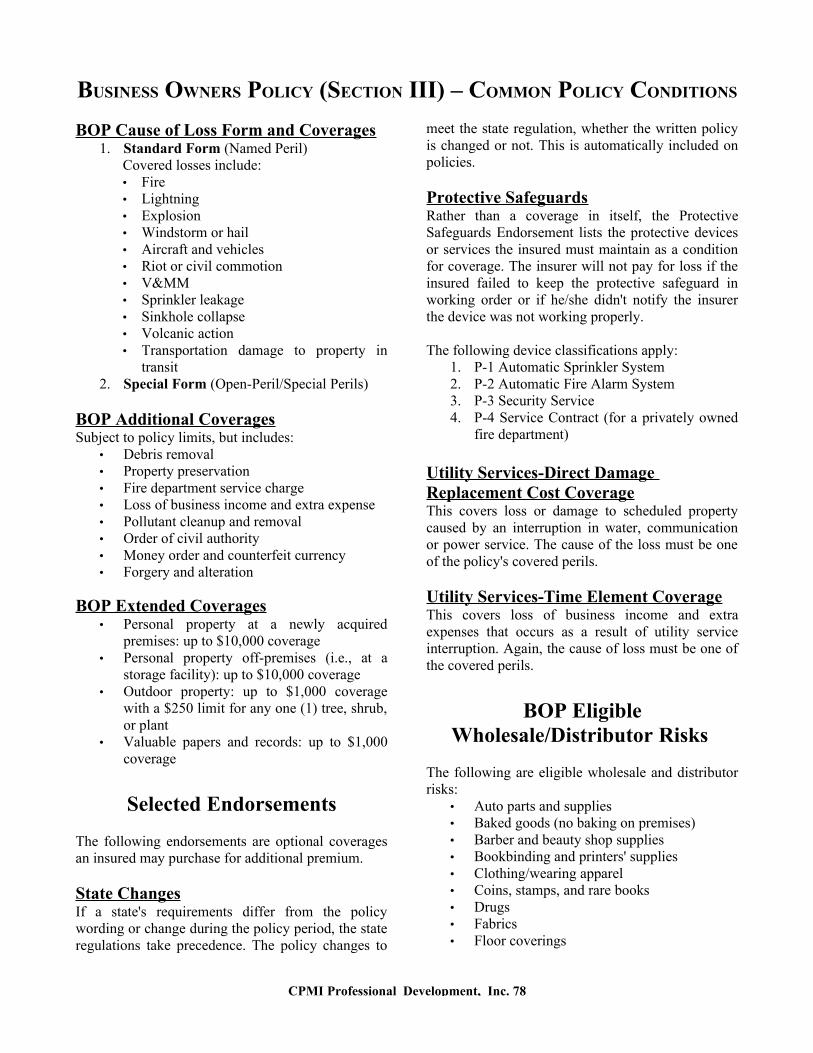

Definitions.....................................................78Business Owners Policy (Section III) – Common Policy Conditions...............................................79

BOP Cause of Loss Form and Coverages. 79BOP Additional Coverages.......................79BOP Extended Coverages.........................79

Selected Endorsements..................................79State Changes...........................................79Protective Safeguards...............................79Utility Services-Direct Damage Replacement Cost Coverage.....................79Utility Services-Time Element Coverage. 79

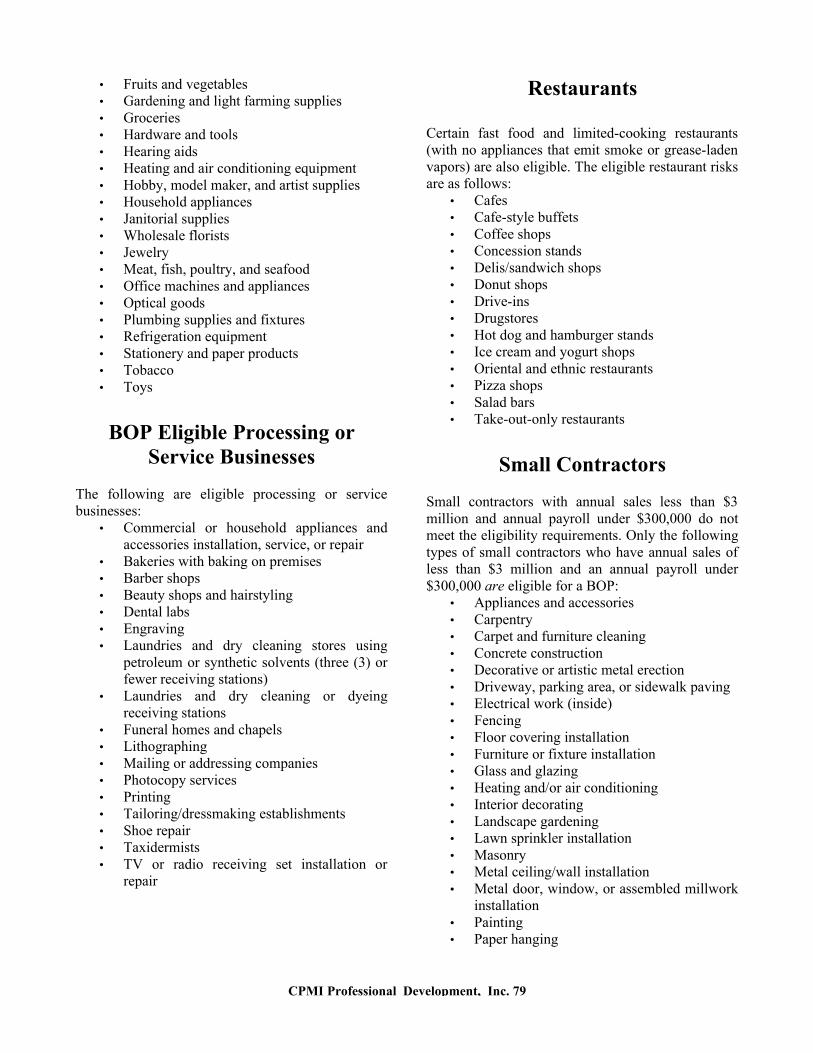

BOP Eligible Wholesale/Distributor Risks....79

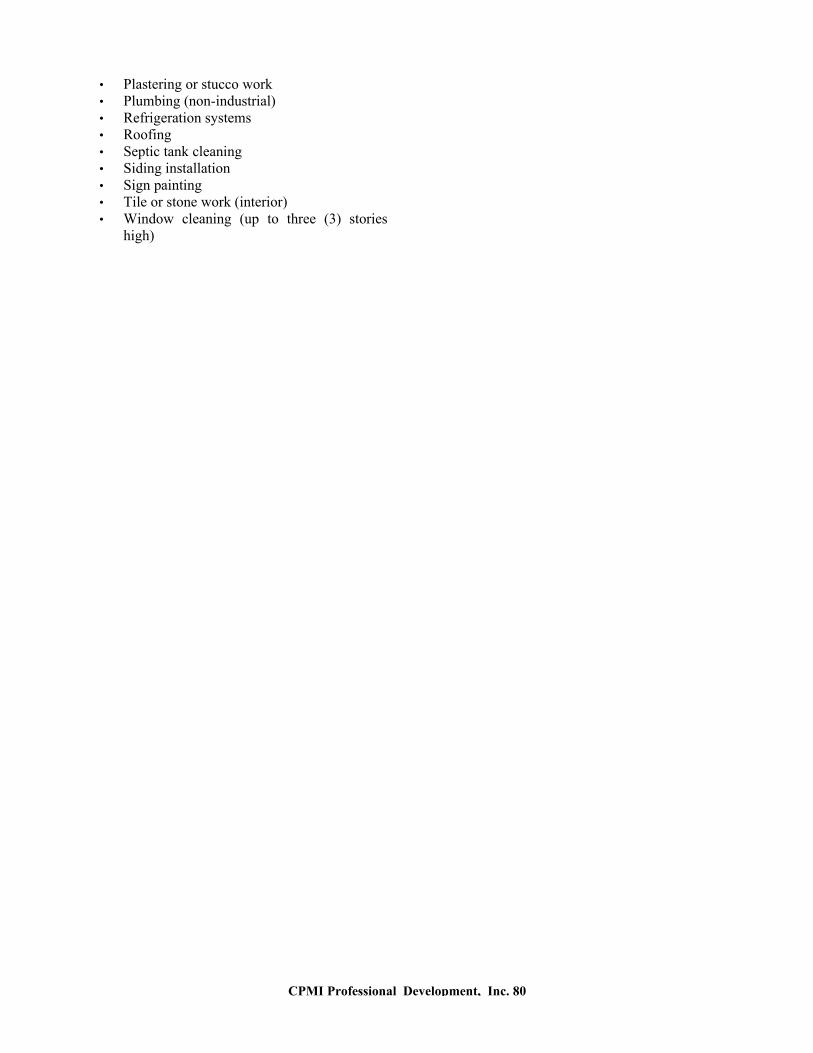

BOP Eligible Processing or Service Businesses.......................................................................80Restaurants....................................................80Small Contractors..........................................80

Section VI – Business Owners Policy (BOP) Review Questions...............................................82

Section VII – Other Coverages and Options............83Aviation Insurance..............................................83

Aircraft Hull..................................................83Aircraft Liability............................................83

Ocean Marine Insurance.....................................83Major Coverages...........................................83

Hull Insurance..........................................83Cargo Insurance........................................83Freight Insurance......................................83

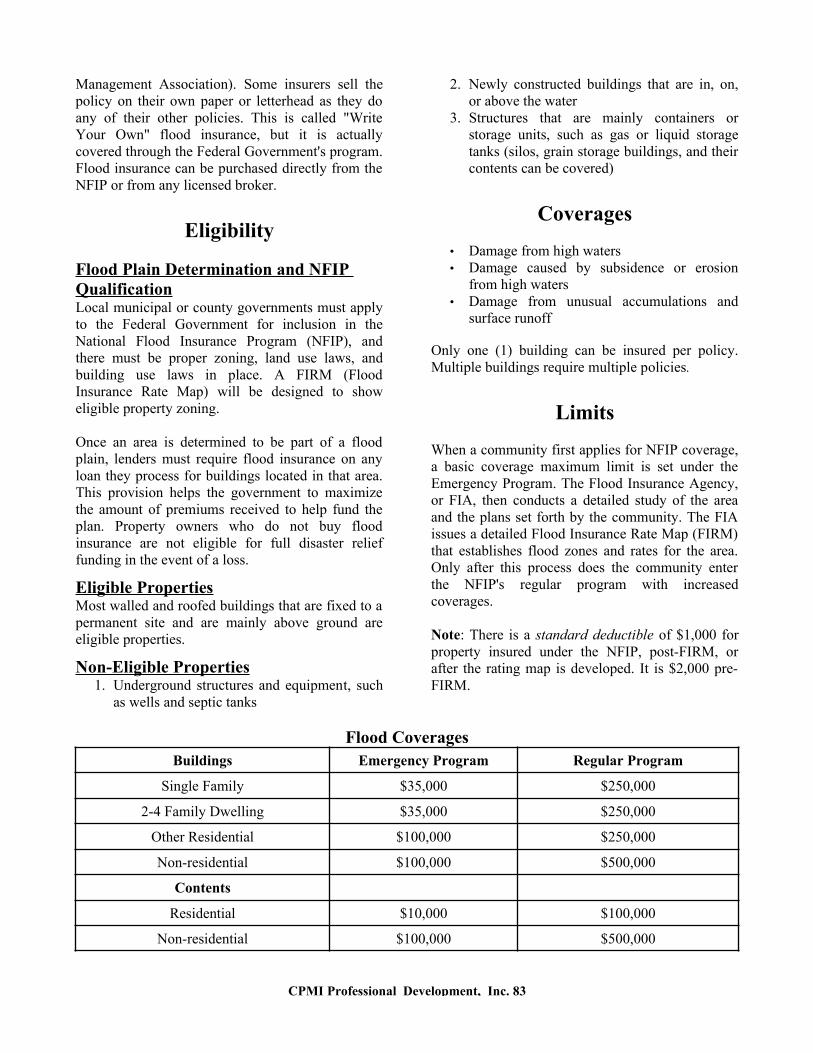

National Flood Insurance Program.....................83“Write Your Own” vs. Government Flood Insurance Policies..........................................83Eligibility.......................................................84

Flood Plain Determination and NFIP Qualification.............................................84Eligible Properties....................................84Non-Eligible Properties............................84

Coverages......................................................84Limits............................................................84

Other Policies.....................................................85Boatowners....................................................85Difference in Conditions................................85

Residual Markets (Including FAIR Plans)..........85Joint Underwriting/Joint Reinsurance Pool....85

Mine Subsidence Insurance................................86Federal Crop Insurance and the Risk Management Agency (RMA)...................................................86

Risk Management Agency (RMA)................86Section VII – Other Coverages and Options Review Questions...............................................87Practice Exam.....................................................88Answers to Review Questions............................94

Section I – General Insurance Concepts........94Section II – Property Insurance Concepts......95Section III – Dwelling Policy (DP)................95Section IV – Homeowners’ Policy.................96Section V – Commercial Package Policy.......96Section VI – Business Owners Policy (BOP) 97Section VII – Other Coverages and Options. .97

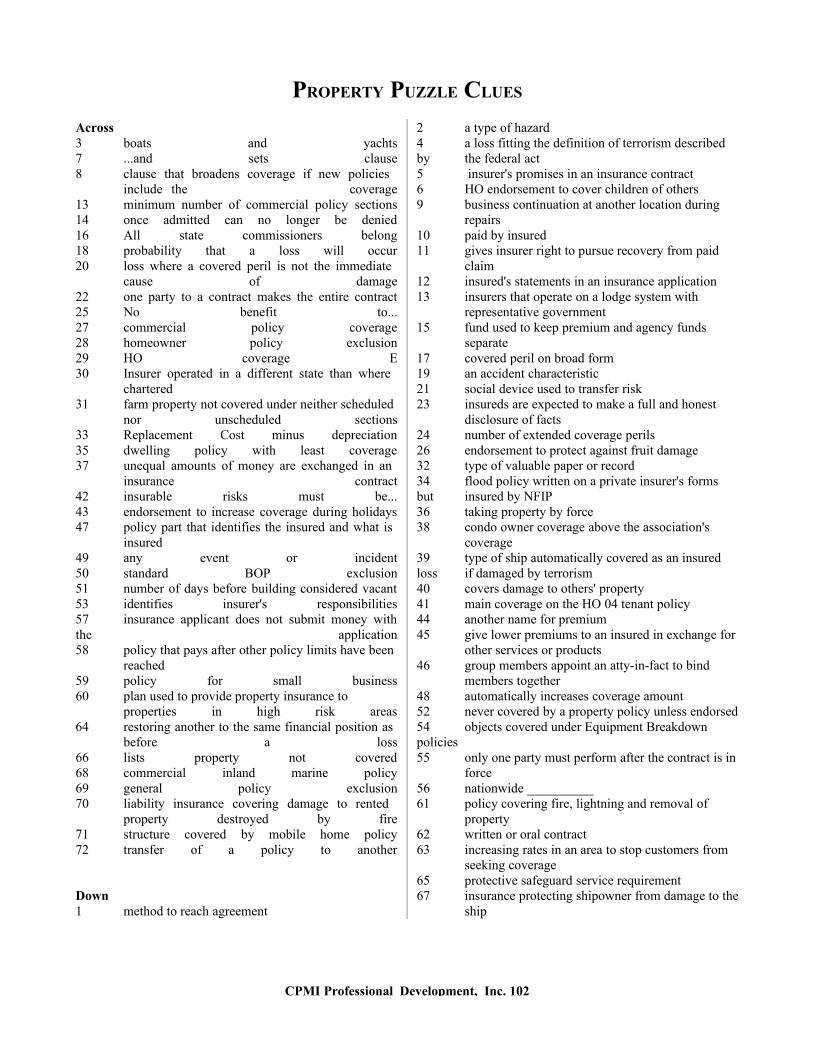

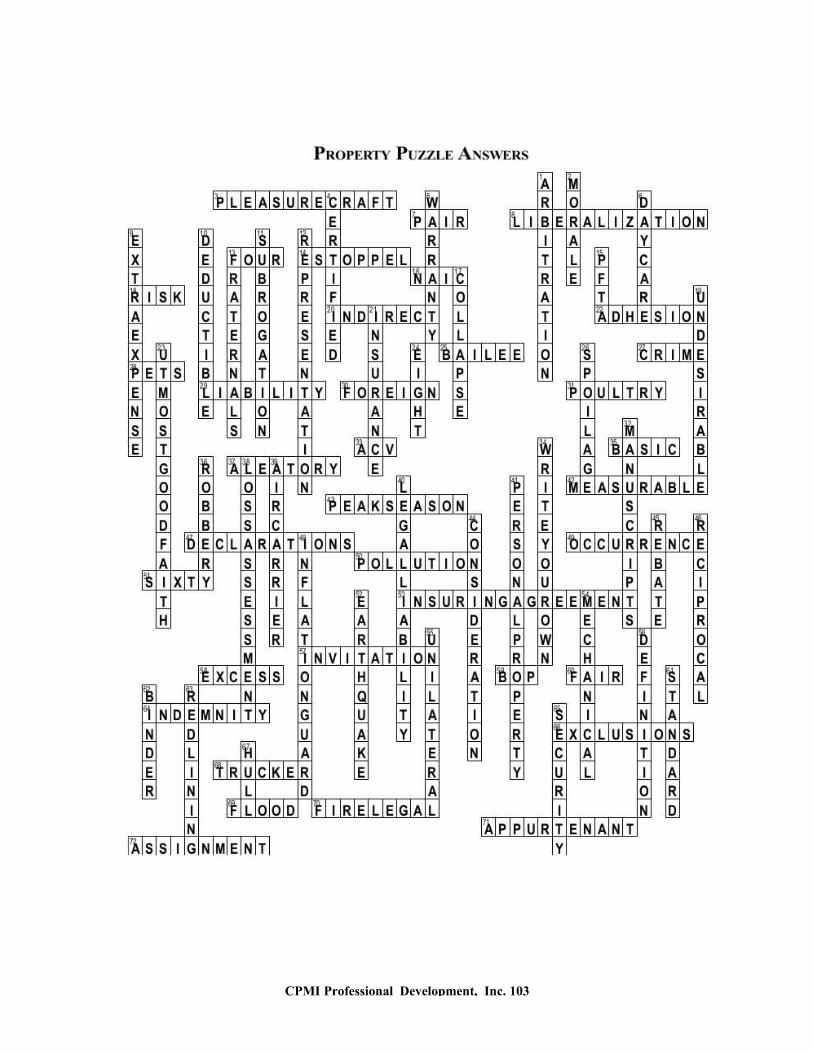

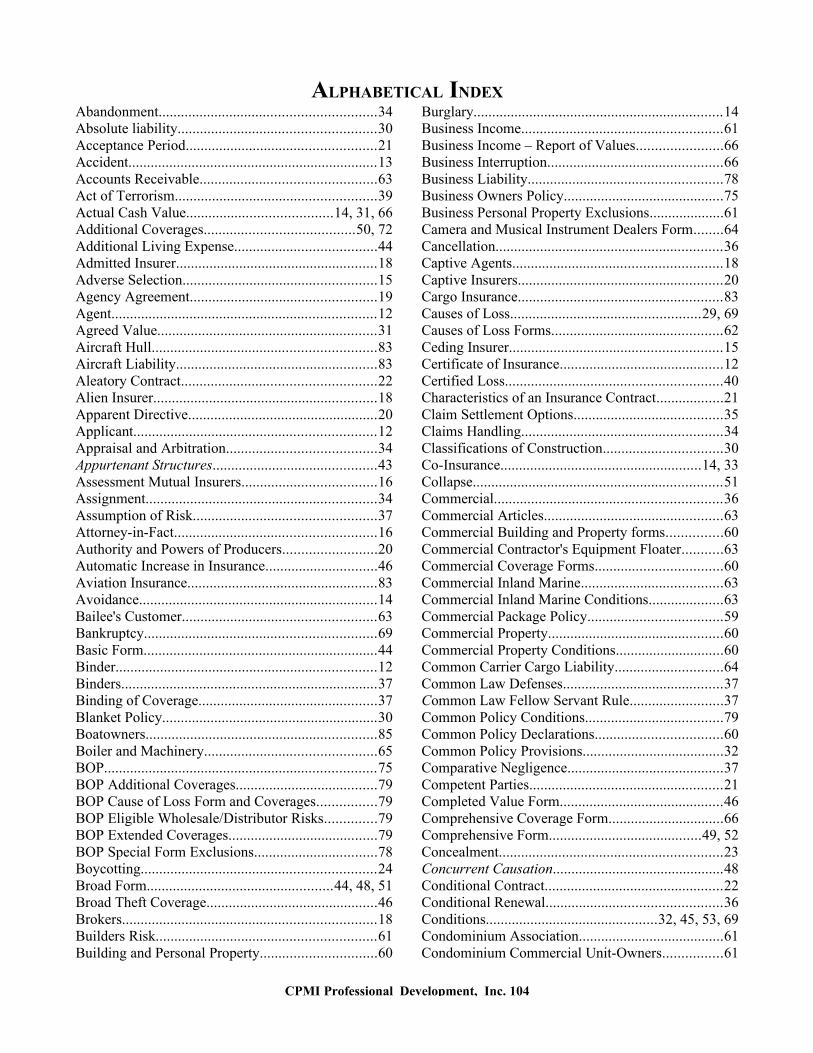

Answers to Practice Exam..................................98Property Puzzle Clues.......................................103Alphabetical Index............................................106

CPMI Professional Development, Inc. 7

STUDYING FOR THE STATE INSURANCE PRODUCER LICENSING EXAMThe material needed to study for the insuranceproducer exam is divided into two sections: (1)Insurance Fundamentals and (2) State Law. Theinsurance fundamentals information is covered inthis textbook. The video and audio seminars (ifavailable) reinforce the insurance fundamentalsinformation. The state law information is in theseparate state law textbook. Regardless of yourstate, the state licensing exam requires that youthoroughly learn the material in these textbooks.There is no substitute for study.

It is recommended that you study at least 20 hoursper line of insurance you plan to get licensed in. Forexample, if you are studying for both Life andHealth, you would likely want to study for at least40 hours. Your individual needs may be more orless than what is recommended. We have found thatthe best way for you to learn this material is tofollow the steps listed below:

1. Study the material in this text, as well as thematerial in your State Law textDILIGENTLY. You must know the

material.2. Take the section review quizzes, practice

exam, and several tests in the ExamAdvantage online questions. If you scorepoorly, review and study the material in thetext again.

3. Take the certified Course Completion Examin the online Exam Advantage section (ifrequired in your state).

CPMI Professional Development, Inc. appreciatesthat you chose our course to aid in your study ofProperty Insurance Fundamentals. We also offerfundamental courses for the following:

1. Life Insurance2. Accident and Health Insurance3. Casualty Insurance

CPMI offers continuing education courses that youwill want to use as you progress in your career.Visit our website for a complete list of other coursesat: www.cpmipro.com

TIPS FOR TAKING THE INSURANCE LICENSING EXAM

Congratulations on choosing CPMI ProfessionalDevelopment, Inc. to help you pass the statelicensing exam! The insurance fundamentals andstate-specific textbooks contain the information youwill need to pass the licensing exam. Our video andaudio seminars are also available to enhance yourlearning experience, and the Exam Advantageonline testing helps review the material and lets youknow if you are ready to take the state exam.

This study program is not designed to be acomprehensive course in insurance. It is designed togive you the basic information you need to pass thestate licensing exam. The exam is not easy, but notethat you can, and should, pass the exam the firsttime you take it if you study and have a good graspon the material. The information in this course iscondensed and addresses the information you willneed to know for the exam without a lot of extramaterial, but you must know it well. What followsare tips to help prepare you for your state exam.

Learning the Material Using the Text, Video, and Audio Resources

1. Decide that you will pass the exam the firsttime you take it.

2. If you have the video, take notes whilewatching the seminar. Watch the programstraight through the first time so that youcan follow the flow of the information.

3. If you have the audio CDs, listen to themmultiple times to help the memorizationprocess.

4. Read and reread the text multiple times,section by section, to make sure youunderstand the material.

5. Repetition is important. Studies show thatadults generally learn best when they dividetheir study time into manageable chunks.Take a 10 minute break after reading eachsection of the material. Study diligentlyover the course of several days.

CPMI Professional Development, Inc. 8

Answering the Review Questions and Taking the Practice Exams

1. Answer the review questions after the endof each section. If you get any of the reviewquestions wrong, review that section of thetext.

2. When you take the practice exam at the endof the text, try to answer questions withoutlooking at the text. If you don't know theanswer, turn to the text. When you gothrough the exam additional times, try notto turn to the text.

3. Go with your first instinct. Often times, thefirst answer you choose for a question is thecorrect one – if you are taking an educatedguess. Statistically, you are more likely tochange a correct answer to an incorrect oneif you go back and change your initialanswers.

4. Try not to spend too much time onquestions that you absolutely don't knowthe answer to. Choose your best guess.Eliminate whatever might be obviouslywrong, and move on to those questions youdo know. Remember, you are allowedabout 45 wrong answers on the state exam.

5. Read the questions carefully. It can help toreword the questions to make sure youunderstand what is being asked.

About half of the questions on the exam arerelatively straight forward facts. For example:

The concept of restoring someone to the samefinancial position in which they were before a lossis called:

A. InsuranceB. Indemnity *C. RiskD. Hazard

About a quarter of the questions require somedeductive reasoning. For example:

J and R insure their building for $140,000 under aBuilding and Personal Property Coverage Form.AB Bank holds a $70,000 mortgage on the building.When the building is destroyed by a propane gasexplosion, the insurance company discovers that thebuilding was used to store hot air balloons andtanks, when J and R had told them at time of theapplication that the building would be used to storeoffice furniture and files. How much will the insurerpay?

A. $70,000 to J and R and $70,000 to the bankB. $70,000 to J and R, nothing to the bankC. Nothing to J and R, $70,000 to the bank *D. Nothing. Premiums will be refunded to J

and R.

Other questions are asked in the negative. Watch forthis type of question:

Which of the following statements about thesubrogation clause is NOT correct?

A. It exists in many insurance contracts.B. It prevents double collection for a loss by

an insured.C. It allows larger claim payments than are

possible without it. *D. It places the ultimate burden of loss on an

at-fault third party.

There is temptation to mark the first answerperceived as correct, which is A. What the questionis asking, though, is for the answer which is notcorrect about the subrogation clause. Be sure to readeach question carefully and understand what thequestion is really asking. Make sure you answer thequestion that is asked. For example:

Which of the following is not an unfair claimspractice?

A. Attempting to settle a claim on the basis ofan altered application

B. Rebating *C. Failure to affirm or deny coverage within a

reasonable period of timeD. Requiring the submission of a preliminary

claim report

(Rebating is an Unfair Trade Practice, not an UnfairClaims Practice.)

CPMI Professional Development, Inc. 9

Which one of the following is not covered by BodilyInjury and Property Damage in the CommercialGeneral Liability policy?

A. Premises and OperationsB. Contingent LiabilityC. Manufactures and ContractorsD. A customer falls down some stairs on the

company's premises and breaks a leg. *

(This is covered by Medical Expense Coverage, notby Bodily Injury and Property Damage.)

BEFORE TAKING THE INSURANCE LICENSING EXAM

The day before the exam, make sure you have yourprelicense course completion certificate (if requiredby your state) in an easily accessible place to takewith you to the exam. Also, be sure to bring twoforms of ID with you to the test center, with at leastone being a picture ID. Familiarize yourself withhow to get to the exam site so you will not bescrambling before you need to leave for the exam.

Get a good night's rest the night before the exam.Studies also show that a meal with protein helpspeople stay more alert. Avoid candy or a meal highin sugar or fat before the exam, as they tend to makeyour mind less alert.

Eat a light meal before going to the test. Do not eatmany carbohydrates, as they tend to make you tired.

Arrive at the exam site 15-30 minutes before yourexam is scheduled to begin so you will be restedand at ease. Arriving late can make you nervous, orit may cause you to miss your exam completely.

You may not take certain items into the test. Youwill need to put coats, purses, cell phones, books,any calculators, and some types of watches into alocker before entering the test center. Anything thatmight have answers in it or cover answers thatmight be written on your person should not be takento the exam site.

When you get to the cubicle to take your test, therewill be a computer and material for notes. Take afew minutes to clear your mind, and write downsome information with which you have somedifficulty. This will help to recall information whileyou are taking the test. You will need to turn any

material on which you wrote notes into the examproctor upon finishing the test and leaving thefacility. Do not take any notes with you from thetesting center.

When you start the test program, you will have theopportunity to take a review program that will showyou how to operate the testing program. You canmark questions for review at the end of your test,review all questions, or close the exam. Once youclose the exam, whether to finish or move on toanother test, you will not be able to return to theclosed test. If taking more than one exam, you willbe given the opportunity to pause the program andtake a restroom break. You may not look at anymaterials to review test information, and you maynot take any information into the restroom with you.

There will be monitors who walk around thefacility. Don’t let this make you nervous; themonitors are verifying everyone is taking the examwithout assistance. There may also be mirrorsaround the facility, so the monitors can better viewtest takers’ work spaces. Don’t let this make younervous either.

As you leave the test center, you will be given yourtest results. If you did not pass the test, or any partof it, ascertain what your score was and schedule asecond attempt within a few days. This will allowyou to review the study material without forgettingwhat you had already learned prior to your firstattempt at the state exam.

When you pass the test, CONGRATULATIONS!You will now be able to apply for your insuranceproducer license per your state's requirements.

CPMI Professional Development, Inc. 10

Section I – General Insurance Concepts

Risk Management Key Terms

InsuranceInsurance is a contract that binds the insurer toindemnify (compensate) the insured againstspecified types of loss in return for money(premiums). Insurance is designed to protect thefinancial well-being of an individual, company, orother entity against the financial risks associatedwith unexpected loss. In exchange for the premiumpayments from the insured, the insurer agrees to paythe policyholder upon the occurrence of specificevents. In most instances, the insured pays for aportion of each loss in the form of a policydeductible, and the insurer pays for the balance ofthe loss up to the policy limit of insurance.

Law of Large NumbersThe Law of Large Numbers is a theory that statesthat it is more likely to predict a particular outcomeas the number of units in a group increases. Thebigger the observed sample, the more accurate thepredicted results will be. It is the scientificallycalculated pooling, growth, and distribution ofmoney to satisfy two (2) different objectives:

1. The paying of benefits to survivors ofsomeone who dies while covered

2. The providing of distribution of benefits bylump sum or with guaranteed lifetimepayments

Insurance ratings are based on the Law of LargeNumbers. For example, an insurer is more likely topredict the number and types of auto insuranceclaims as the number of auto insurancepolicyholders increases.

IndemnityIndemnity is the underlying principle of insurance,which is restoring an insured to the same financialposition that existed before a loss occurred.

LossLoss is the source of a claim for damages under aninsurance policy. Losses cause a financial loss to theinsured due to loss of property, a liability fromsomething the insured did to someone else, or theloss due to the loss of a loved one, or losses due to

medical problems. Loss arises from the occurrenceof an event that is insured by a policy.

Direct Physical LossA direct physical loss is a loss in which damageoccurs as the result of an occurrence without anintervening cause, such as hail damage to the roofof a house.

Intervening CauseAn intervening cause is an event that interrupts thechain of causation by providing an independentcause of the final result.

Indirect or Consequential LossAn indirect or consequential loss is a loss in whichdamage occurs as the result of a direct loss, such asthe insured's increase in expenses when required tostay in a hotel because a hail-damaged home cannotbe lived in.

Insurable InterestInsurable interest is the concept that insurance canonly be purchased when the applicant has a potentialfor financial loss – if the insured person died, or ifthe insured items were destroyed or not in theirpossession. In Property and Casualty insurance,insurable interest must be present at the time of loss,as well as at the time of application. In Lifeinsurance, insurable interest is only required at thetime of application.

RiskRisk has two (2) meanings: (1) The property orparty that is insured, and (2) The uncertainty of loss.

Pure RiskA pure risk is a situation that only involves thechance for loss, or no loss, such as propertyownership.

Speculative RisksSpeculative risks are situations that involves thechance for either a loss or a gain, such as gambling.

Relationship Between Risk and PremiumThere is a direct correlation between risk andpremium. The greater the risk, either in value or inpotential for a loss or claim, the greater thepremium will be.

CPMI Professional Development, Inc. 11

NegligenceNegligence is conduct that is culpable because itmisses the standard required by law of a reasonableperson in protecting others or the interests of othersagainst risky or harmful acts of other people. It is:

1. The failure to do something that areasonable person would do OR

2. Doing something that a reasonable personwould not do

Self-InsuranceSelf-Insurance refers to making financialpreparations to meet risks by setting aside sufficientfunds in advance to meet estimated losses, ratherthan purchasing an insurance policy.

ApplicantThe individual who applies for insurance is theapplicant.

InsurerInsurer is another name for an insurance company.

InsuredAn insured person is:

1. Any member of the insured household whois a relative or is under 21 years of age.

2. A child or parent living with the insured,regardless of their age.

3. Any other member of the insured householdwho is under the age of 21.

There are three (3) types of insureds:1. Named Insured: This is the person(s)

listed as an insured in the Declarationspage.

2. First Named Insured: This is the firstinsured listed and the person to whom theinsurer sends correspondence such asrenewal notices or policy changes.

3. Additional Insured: This is the individualor entity who, other than the named insured,qualifies as an insured under the policy.This is especially the case if there is aspecific interest involved, such as amortgage or a business arrangement.

Note: The definition of Insured has been expandedunder the Homeowners’ policy to include “otherpersons under the age of 21 and in your care or thecare of a resident of your household who is yourrelative.”

Agent / Producer An individual who is state-licensed to solicit andsell insurance for one or more insurance companiesis either an agent or a producer. He/she must beauthorized by an insurer (known as the principal) toact on its behalf.

Policy OwnerThe policy owner is the person who:

1. Applies for a policy.2. Takes responsibility for premium payment.3. Has the right to cash values, dividends, and

policy proceeds.4. Has the ability to change beneficiaries and

other policy particulars.

BinderA binder is a written or oral contract made by anagent that puts a policy immediately but temporarilyinto effect for a specified period of time, from thetime initially bound until accepted or canceled bythe insurance company, that includes all the termsof and endorsements to the policy. The minimumthat an agent needs in order to put a binder intoeffect is the insured's promise to pay the premiumwithin a certain time frame. All policy terms andconditions are in force until a policy is issued orcoverage is declined by the insurer on whom thebinder was written. Agents must be careful not toexceed their binding authority, as the company isliable for the entire risk until reviewed and acceptedor canceled by the insurer.

Certificate of InsuranceA document issued by an insurance company/brokerthat is used to verify the existence of insurancecoverage under specific conditions granted to listedindividuals is known as a certificate of insurance.

EndorsementAn attachment to a document that amends or adds toit is known as an endorsement. Typically, it is anadded provision to an insurance policy. Also referredto as a "rider."

Waiver and Estoppel WaiverThe voluntary abandonment of a known or legalright or advantage is a waiver.

CPMI Professional Development, Inc. 12

Waiver of RightsA waiver of rights is the intentional relinquishmentof a known right. The insured would need to sign aform if they are relinquishing their rights in a policyor claim settlement.

EstoppelThe idea that once a fact has been admitted to betrue by a previous action it can no longer be deniedto be true is known as estoppel.

AccidentAn accident is an unforeseen and unintended eventthat is identifiable as to time and place.

OccurrenceAn event, including continuous and repeatedexposure to conditions, which results in bodilyinjury or property damage neither expected norintended from the standpoint of the insured isknown as occurrence.

ExposureExposure is the condition of being at risk forfinancial loss due to hazards or unforeseen events.

HazardA hazard is a condition that increases the chancefor loss or the severity of loss. There are four (4)types:

1. Physical – Physical hazards are created bythe use, condition, or occupancy of property,such as damaged steps or worn auto tires.

2. Moral – Moral hazards are created by theinsured's habits, such as dishonesty orcriminal activity. It is a situation in whichone party gets involved in a risky eventknowing that it is protected against the riskand the other party will incur the cost.

3. Morale – Morale hazards are created bythe attitudes of the insured, such asindifference because the insured knowshe/she is insured. An example would be notmaking sure doors and windows are lockedbefore leaving home. If anything is stolen,the insured doesn’t worry because it’sinsured. While a Moral hazard describes aconscious change in behavior to try tobenefit from an event that occurs, a Moralehazard describes an unconscious change ina person's behavior when he/she is insured.

4. Legal – Legal hazards are created whenlegal authority in a certain situation isunclear or unsettled. These can arise fromchanges in the law or from court rulings. Anexample would be a change in the buildingcode requiring new construction to usedifferent materials.

PerilPeril is the cause of a loss or the event insuredagainst. Examples: fire, lightning, theft, etc.

1. A Named Peril Policy is a policy that onlyprovides insurance for perils that arespecifically listed or named in the policy.

2. An Open-Perils Policy is a policy thatprovides insurance for all perils exceptthose specifically excluded in the policy.

Maslow's Hierarchy of NeedsThe five (5) primary needs that every individualstrives to satisfy (in ascending order) are:

1. Physiological Needs2. Security3. Affiliation4. Esteem5. Self-Actualization

This hierarchy of needs is important for theinsurance producer to know because customers needto have one level of need met before worrying aboutthe next. For instance, customers usually need tohave the physiological need for food and shelter metbefore you would approach them about buying lifeinsurance for charitable causes.

National Association of Insurance Commissioners (NAIC)All state insurance directors or commissioners aremembers of the National Association of InsuranceCommissioners, also known as the NAIC. Thegroup has no official legislative powers.

The NAIC tries to standardize insurance lawsthroughout the country by recommending modellegislation in each commissioner’s home state.

Individually the commissioners or directors do notmake any laws, they enforce insurance laws in theirown states. They do this by determining the types ofpolicies that can be sold in their state, bydetermining the amounts of surplus that insurers

CPMI Professional Development, Inc. 13

must maintain, by investigating complaints ofagents and insurance companies, and by examiningagents and insurers.

TortIn common law jurisdictions, a tort is a civil wrongthat unfairly causes someone else to suffer loss orharm resulting in legal liability for the person whocommits the tortious act. Although crimes may betorts, the cause of legal action is not necessarily acrime, as the harm may be due to negligence whichdoes not amount to criminal negligence. Thevictims of the harm can recover their loss asdamages in a lawsuit. In order to prevail, theplaintiff in the lawsuit must show that the actions,or lack thereof, was the legally recognizable causeof the harm. A person may be found not guilty in acriminal case, but can still be found guilty or legallyliable in a lawsuit.

Co-InsuranceCo-insurance is another cost containment feature ina Property (usually commercial) insurance policy.The co-insurance clause requires a specified amountof insurance based on the value of the insuredproperty. If the insured insures the property for lessthan this amount, he or she must share in apercentage of a loss to the same percent that theproperty is underinsured at the time of the loss. Itencourages insuring of property to the properamount.

Deposit PremiumA deposit premium is an initial or provisionalpremium required by an insurer that is based onestimated information and is subject to an audit todetermine the actual risk amount and a premiumadjustment after the end of the policy period. Afteradjustment, the premium becomes the final premium.This is most often used in Workers Compensationand Liability insurance.

BurglaryBurglary is breaking and entering (into a building,safe, etc.) with felonious intent and with visiblesigns of forced entry – for example: a brokenwindow, jimmied door, or blown safe. (Study tip:Burglary. Building. Both start with B.)

RobberyRobbery is the taking of personal property ofanother by force or fear of force.

LarcenyLarceny is the taking or removal of another'spersonal property with the intent to permanentlydeprive them of it. This could be burglary orrobbery, but if property is taken without force, fearof force, or breaking and entering, it is still larceny.Walking into someone's house through an unlockeddoor and picking up jewelry is an example oflarceny.

TheftTheft is the unlawful taking of the property ofanother, including burglary, robbery and larceny.

Mysterious DisappearanceMysterious disappearance means that personalproperty is missing, but there is no provable causefor its disappearance; the property might have beenlost or stolen.

LiabilityLiability is a legally enforceable debt or obligation.

Actual Cash ValueThe replacement cost at the time of loss, minusdeprecation, is known as actual cash value.

Personal Lines vs. CommercialLines

Property insurance and Casualty insurance can befurther divided into Personal and Commercial lines.Personal lines includes Homeowners’, Personal Autoinsurance, and other related things owned byindividuals. Commercial lines includes BusinessProperty and Liabilities (a loss caused by thebusiness to others), Commercial Auto (Trucking,Business Auto) owned by businesses, and alsoincludes Commercial Crime coverages.

Methods of Handling RiskWhen managing risk, an insured may choose toavoid, retain, transfer, share, or reduce risk.

AvoidanceAvoidance is refraining from engaging in activitythat might give rise to risk, such as not owning ordriving a car to avoid the risk of car accidents.

CPMI Professional Development, Inc. 14

RetentionRetention is assuming responsibility for loss. Inthis case, the individual will be totally responsiblefor paying losses. Retention is the most commonmethod of handling risk, typically in the form ofdeductibles or choosing not to purchase insurance.

SharingSharing is spreading risk among several entities ora large number of people, such as by insurancecompanies or physicians.

ReductionReduction decreases the chance for loss byremoving or reducing hazards that might cause anaccident to happen, such as wearing safety gogglesor installing safety railings around a dangerous area.

TransferTransfer means shifting the risk for loss from oneparty (the insured) to another (the insurer), eitherthrough the purchase of an insurance policy orissuance of another contractual agreement (e.g., holdharmless agreement).

Elements of Insurable Risks

To be considered insurable, a risk must:1. Be accidental and due to chance.2. Be measurable with respect to value.3. Be predictable.4. Be one unit in a large enough pool of units

that the law of large numbers allows for theaccurate prediction of loss.

5. Not be catastrophic in nature.6. Generate a rate that is reasonable and

affordable.

Pure risks are insurable; speculative risks are notinsurable.

Adverse Selection

Adverse selection is the tendency of persons whopresent a greater-than-average degree of risk for lossto apply for, or continue, insurance to a greater

extent than persons with average or less-than-average degree of risk for loss. Normal risks mayseek insurance elsewhere, possibly at a lower cost.If a person becomes sick, he/she may be unable toget insurance elsewhere and are, therefore, morelikely to maintain the current coverage.

Reinsurance

Reinsurance is insurance sold and purchasedbetween two (2) insurance companies for the purposeof transferring and sharing risk, usually catastrophicrisk or losses in excess of a specific amount (e.g.,$500,000 or $10,000,000).

ReinsurerA reinsurer is the insurer selling reinsurance toceding insurers.

Ceding InsurerA ceding insurer is the insurer buying reinsurancefrom a reinsurer. The ceding insurer issues primarypolicies of insurance to individuals and/orbusinesses.

Reinsurance Contract or TreatyTwo (2) types of reinsurance contracts are sold:

1. Facultative Reinsurance: The cedinginsurer offers individual risks to thereinsurer, and the reinsurer may choose toaccept or reject each individual risk.

2. Treaty Reinsurance: The reinsurer writescoverage for one or more lines of insuranceissued by the ceding insurer based on termsstated in the reinsurance contract. Treatyreinsurance continues in force unlesscanceled by one of the parties of the treaty,and the reinsurer cannot reject individualrisks.

The following types of reinsurance apply primarilyto Property and Casualty insurance, but are thesubject of all licensing exams:

1. Excess of Loss Reinsurance: The reinsureronly pays for losses that exceed a certaindollar amount (e.g., $500,000).

2. Proportional Reinsurance: the reinsureronly pays a share of every reinsured loss(e.g., 90%).

CPMI Professional Development, Inc. 15

Indemnity/Pay on Behalf OfIndemnity can be thought of as pure and simpleprotection from a loss by being reimbursed or paid asum to make you whole after you incurred a cost orexperienced a loss.

On Behalf Of refers to someone else beside theperson experiencing the loss paying for that lost orcost in your stead. It is paid for you instead of youpaying for it directly.

An example might be where your insurancecompany makes a payment to the an entity that youwere financially responsible to. This indemnifiesthem on your behalf rather than you paying themdirectly for it yourself.

Limits of Liability

Limits of Liability means the maximum amount theinsurer will pay for loss or damage covered by aninsurance policy.

Deductible

A deductible is the monetary amount an insuredmust pay before the insurer will begin making losspayment. A deductible is a form of risk-sharing andcost containment. Most forms of insurance containstandard deductible amounts (e.g., $500) and theinsured may choose higher or lower deductibles. Asa deductible increases (e.g., the insured pays formore of the loss), the policy premium decreases.

INSURERS

Types of Insurers

Multi-Line Insurance Companies Multi-line insurance companies are insurers thatwrite more than one (1) line of insurance.

Stock CompaniesInsurers organized under the laws of the state inwhich they are incorporated that are owned byshareholders who elect officers and directors andshare in profits through stock growth and dividendsare called stock companies.

Mutual CompaniesCompanies of this type have no capital stock andare owned by policyholders who share profitsthrough dividends and who can attend and vote atcompany meetings. Mutual insurers are furtherdivided into the following:

1. Assessment Mutual Insurers share lossesamong group members. In a pureassessment group, no premium is paid inadvance, but losses are assessed to eachmember as they occur. In an advancepremium assessment group, premiums arepaid at the beginning of each assessmentperiod and any claims are paid from thesepremiums. If there are more claims than

premiums paid in, then additionalassessments are levied against eachmember. If money is left at the end of theperiod, then the money is returned to thegroup members.

2. Non-Assessable Mutual Insurers charge afixed premium and the policyholders cannotbe assessed further. Reserves and surplusare maintained to provide payment of allclaims.

Reciprocal CompaniesGroups that exchange insurance on each other arereciprocal companies.

1. Members appoint and empower anattorney-in-fact that legally bindsmembers to insure each other.

2. Members share in any profits through lowerpremiums, or in any losses by assessments.

3. Insured members are called subscribers.

Risk Retention GroupsA mutual insurance company that insures people inthe same profession or business is known as a riskretention group.

Purchasing GroupsA purchasing group is not an insurance company.Rather, a purchasing group can be any group of

CPMI Professional Development, Inc. 16

persons with similar or related liability risks whoform an organization whose purpose is to purchasecommercial liability insurance on a group basis. Nospecific requirements are imposed regarding thelegal structure of a purchasing group. In the case ofa trade association, a simple resolution of the boardauthorizing the organization's officers to makearrangements to purchase commercial liabilityinsurance on a group basis would be sufficient toestablish the purchasing group. Members of apurchasing group must be in similar or relatedbusinesses which exposes them to similar or relatedliability risks.

Risk Retention Groups (RRG) vs. Purchasing Groups (PG)Both risk retention groups (RRGs) andpurchasing groups (PGs), require members to behomogeneous, (i.e., engaged in similar businessesor activities that expose them to similar liabilities).

The primary difference between RRGs and PGs isthat RRGs retain risk while PGs do not. PGspurchase insurance from an insurer, who issues thepolicies and serves as the risk bearer. RRGs, asinsurers, issue policies to their members and bearrisk. Another key difference between the two (2)entities is that RRGs typically require members tocapitalize the company whereas PGs require nocapital.

Fraternal Benefit SocietiesMembership is based on religious, ethnic, ornational lines, and noted primarily for social andcharitable functions. Fraternal Benefit Societies,also called Fraternals, are societies, orders, orsupreme lodges, with no capital stock that may ormay not be incorporated. Fraternal BenefitSocieties:

1. Are conducted solely for the benefit ofmembers and their beneficiaries, and are notfor profit.

2. Operate on a lodge system with ritualisticform of work.

3. Have a representative form of government.4. Provide benefits in accordance with their

charter.5. Started offering Life insurance for the

benefit of their poorer members on anassessment basis, but have expanded tooperate the same as other insurers today,though they still offer insurance only tomembers or their families.

Syndicate Insurers ( Lloyd's Associations ) Syndicate insurers are not true insurancecompanies.

1. They provide a place for members to meetand transact the business of insuranceindividually or as groups through asyndicate manager.

2. They provide assistance in gatheringunderwriting information and handlingclaims and disputes among syndicatemembers.

3. Members are individually and wholly liablefor all risks they accept, with no limitationson liability. This lack of liability limits isActual Cash Value

4. Replacement cost at time of loss minusdepreciation is the primary reasonsyndicates are not widespread today.

5. An example of this is Lloyd's of London.

Surplus/ Excess Lines Insurers These types of insurers provide insurance notoffered through admitted insurers.

1. The full amount or type of insurance mustnot be available through admitted insurers.

2. Financial consideration cannot be adeciding factor.

3. While a surplus/excess lines insurer isselling insurance in a state, if the coverageis offered by an admitted insurer, the non-admitted insurer must stop selling insurancein the state, or apply to become an admittedinsurer.

Private vs. Government Insurers While private insurers offer coverage for morecommon risks, there are some situations that areunacceptable to them. If there is the potential forspecial, great, or catastrophic risks, thosepossibilities are usually indemnified by State andFederal Government insurers.

The State or Federal Government sometimes covercertain types of insurance that private insurerscannot or will not insure. Insurers in each state arerequired to participate in shared or involuntarymarkets. These markets provide coverage for high-risk insurance applicants that do not meet normalunderwriting standards.

Some states require that these high-risk applicants

CPMI Professional Development, Inc. 17

be assigned to individual insurers on apredetermined basis while others require that lossesfrom these individuals be shared.

1. Property insurance FAIR plans provideinsurance to property owners in inner-cityand high-risk areas who are unable to obtaininsurance through normal market channelsbecause of property location or othersituations over which they have no control.If turned down in the normal market, theproperty owner may apply for insurancethrough the state's FAIR plan that followsits own guidelines to insure the property.

2. Examples of Federal Government insuranceinclude Social Security, Medicare, Floodinsurance, and Federal Crop andcCrimeinsurance. State governments sometimesoffer competitive funds that compete withprivate insurers, or monopolistic funds thatwill not allow insurers to compete in certainareas. One such example of this is that somestates (North Dakota, Ohio, Washington,and Wyoming) provide WorkersCompensation insurance benefits.

Admitted vs. Non-AdmittedInsurers

Admitted Insurer /Authorized Insurer An insurer authorized by a state's insurancedepartment to transact business in that state isknown as an admitted insurer or an authorizedinsurer.

Non-Admitted Insurer /Non- A uthorized InsurerInsurance companies not authorized to transactbusiness in a state because they either didn't seekadmission to the state or failed to comply with staterequirements are known as non-admitted insurersor non-authorized insurers.

Domestic, Foreign, and AlienInsurers

Domestic InsurerDomestic insurers are insurers that transactbusiness in the state where they are chartered.

Foreign InsurerA foreign insurer is an insurer transacting businessin a state but that is chartered under the laws of adifferent state or one of the U.S. territories.

Alien InsurerAn alien insurer is an insurer organized under thelaws of a jurisdiction outside of the United States orits territories.

Financial Solvency Status(Independent Rating Services)

Independent evaluation services provideinformation on companies such as financialstrength, management caliber, and efficiency ofoperation.

1. They publish guides which analyze almostall Property and Liability business insurers.

2. They review underwriting results,management, adequacy of reserves forliabilities that are not discharged, adequacyof policyholder reserves to absorb shocklosses, and soundness of investments.

If properly used, these rating services help avoiddelinquent insurance companies. Ratings should bechecked over a period of years to verify trends forthe companies. A.M. Best and Weiss Research aretwo (2) companies that have guides availablethrough most public libraries.

Marketing (Distribution Systems)

Types of Agents/ Marketing Systems Exclusive/Captive Agents or ProducersAgents appointed by an insurer to represent thecompany by selling and servicing policies on itsbehalf, representing only one company, are knownas exclusive/captive agents or producers.

Independent Agents or BrokersIndependent agents or brokers are agents thatrepresent several insurers and can, therefore, offervarious premiums to the customer.

Nonresident AgentAn agent authorized to write business in a stateother than the one in which he or she lives is anonresident agent.

CPMI Professional Development, Inc. 18

Direct WriterA direct writer is an insurer that deals directly withthe insured through a salaried representative orcaptive/exclusive agent rather than throughindependent brokers.

Direct Mail/Direct ResponseDirect mail and direct response policies aremarketed from the company's home office ratherthan through agents. Marketing is done throughdirect mail, internet, newspapers, magazines, radio,or TV.

PRODUCERS AND GENERAL RULES OF AGENCY

Insurer as PrincipalInsurance companies are principals of theinsurance agent, which means that the insurerempowers the agent to act as a representative of theprincipal (the company). Legally, the acts of theagent are considered to be the acts of the principal,so the agents' acts extend the insurance company'sliability.

Producer/Insurer RelationshipAgency Agreement/ContractThe relationship between the insurer and theproducer is defined in the agency agreement. Thiscontract details the responsibilities of both parties.In return for commission or salary paid by thecompany, and the authority to represent the insurerin conducting business on the company's behalf, theproducer:

1. Is first and foremost the representative ofthe insurance company and has an ethicalobligation to follow the rules of the insurer,to submit applications only for those risksthat the insurer deems appropriate, and toservice the policies of company customers.He or she is paid commission or salary bythe company and is given authority torepresent the company in conductingbusiness on the company's behalf.

2. Acts as the representative go-between forthe company and the insured, with primaryresponsibility to the company as theprincipal, while treating the customer in afair and ethical manner.

3. Provides correct information to thecustomer about policy coverages.

4. Processes any requests for or cancellationsof coverage in a timely fashion.

5. Has no authority beyond that which theinsurer gives him or her.

Insurance Agent vs. BrokerSuperficially, an insurance agent and a brokerlook identical as both of them are selling insurancepolicies. The main difference between the two (2)entities lies in the relation these persons have withthe insurer and the insured. An insurance agent isdesignated by the insurance company to sell itsproducts by convincing people to buy thecompany's policies, whereas a broker worksindependently and matches the needs of a clientwith the products available with any of theinsurance companies. Both need a license to carryout their business in a state and both getcommission from the company.

Professionalism and Ethical ConductWhen acting as representatives of their companies,agents are expected to have and exhibit professionalcompetence that can be shown through:

1. A broad education and background.2. Strong insurance-specific knowledge and

continued education in the insurance field.3. Membership in professional societies and

associations.4. Ethical behavior, including honesty,

integrity, acting in good faith, and theknowledge of and obedience to insuranceindustry regulations and codes.

5. Concern over customers’ welfare over one’sown.

FiduciaryAn individual who holds a position of public trustand confidence is a fiduciary. Insurance agents arefiduciaries to both the companies they represent andtheir clients. As fiduciaries, agents are expected tobe professional and to act ethically.

Financial Responsibilities1. Money received in return for an insurance

policy or binding of insurance coverage is

CPMI Professional Development, Inc. 19

held in a fiduciary capacity and may not beused by the agent for any other purpose.

2. Many states require producers to maintain aPremium Fund Trust Account (PFTA) ifthey hold premium money for any length oftime before giving it to the insurer. ThePFTA must be separate from personal orother business accounts.

Captive Insurance Companies A captive insurer is a company whose business isprimarily supplied and controlled by the one interestor group of related interests that set the company upto insure their assets and operations. In this type ofsituation, coverage can usually be provided at alower cost than that which is available in the generalinsurance market.

A captive insurance company may be a non-admitted, non-resident, or foreign insurer, and thereare mainly two (2) types:

1. Pure captive companies, which are whollycontrolled by one parent

2. Group captive companies, which areinsurers owned by a number of otherwiseunaffiliated firms that are in the same typeof business.

Authority and Powers ofProducers

Law of AgencyAccording to the Law of Agency, an agent's actionsare regarded the same as if the company itselfperformed the action. The agent is a representativeof the insurer and acts for the insurer. As such, theinsurer becomes partially liable for the actions ofthe agent. It is the insurer's responsibility to monitorthe compliance of its agents in order to verify thatthey follow all required laws. An agent representsthe company through several directives.

Express DirectiveExpress directive is when authority is expresslygiven to the producer, either orally or in writing inhis/her contract. Examples of this include: thecountersigning and delivering of policies. Expressdirective clauses are such things as scale ofcommissions, ownership of contracts sold, andcontract cancellation procedures.

Implied Directive The doctrine of “ostensible authority,” or implieddirective, gives agents unwritten authority toperform incidental acts that the public assumes theagent to have. Example: Exclusive Property andCasualty agents can bind insurance coverage. If theagent binds a particular risk, the company is boundto that risk and must pay for any losses until itcancels the contract.

Apparent DirectiveApparent directive is neither expressly given norimplied, but exists because the agent has used it inthe past without the insurer stopping him or herfrom doing so, or it is authority that a reasonableperson would assume an agent to have. If the agenthas paid minor claims in the past and beenreimbursed by the insurer, it is apparent he or shehas the authority to do so.

Responsibilities to the Applicantand Insured

For risks covered by the policy, the insurer mustpay all sums up to the policy limits that the insuredbecomes legally liable to pay; in other words, theinsurer pays the lower of the claim (loss) or thepolicy limits. Deductibles will be applied to anyproperty claims, but there is no deductible formedical or liability claims. The producer hasresponsibilities that are owed to applicants and/orinsureds. He or she will:

1. Act only in the best interests of his or herclients.

2. Only provide accurate and up-to-dateinformation and advice to customers aboutpolicies and coverages.

3. Aid with the accurate completion ofapplications and any other accompanyingdocumentation.

4. Service policies as necessary and accordingto the desires of the insured.

5. Process any coverage changes orcancellations.

6. Act only within the scope of authority thathas been given them by the insurer.

Common Situations for Errors and Omissions

1. Failure to adequately explain policycoverages or claim procedures

CPMI Professional Development, Inc. 20

2. Unfairly/inadequately comparing policycoverages when replacing an existing policy

3. Failure to get the policyholder's signatureupon delivery

4. Failure to explain changes made to thepolicy during underwriting

Note: Obtain all necessary signatures and copies ofdocumentation, summaries, and examples. Allconversations should be documented.

CONTRACTS

Elements of a Legal Contract

Insurance ContractA contract is a binding agreement between two (2)or more parties, legally enforceable to do certainthings. In an insurance contract, the insured agreesto pay a monetary premium and abide by certainagreements in exchange for the insurer agreeing toindemnify the insured in case of loss.

There are four (4) principle elements that must be inevery legal contract.

1. Offer and Acceptance An insurance policy is the written statement of theterms of the contract. There must be both an offerand an acceptance.

During the offer period the applicant submits anapplication along with the correct premium. Duringthe acceptance period the insurer issues the policy.

If the applicant does not submit money with theapplication, it is not an offer, but it is an invitationto the insurer to make an offer, and the agent cannotbind coverage.

2. Consideration The applicant's consideration is the premium, andthe insurer's consideration is the promise toindemnify the insured in the event of a loss.3. Competent Parties A party to a contract is one who holds theobligations and receives the benefits of a legallybinding agreement. When two (2) parties enter intoan agreement, there are two (2) distinct roles eachplay: the promisor and the promisee.

When a contract benefits others who are not party tothe agreement, these third-party beneficiariesreceive benefits of a contract, while not owing anyobligation.

All parties concerned must have legal capacity toenter into a contract. This is best shown by definingthose who do not have legal capacity to enter into acontract. This includes:

1. Minors2. Those legally declared incompetent3. People under the influence of drugs or

alcohol

In the case of minors, the insurer may be required touphold the terms of the contract while minors maynot be.

4. Legal purpose The insurance policy owner must have an insurableinterest in the property or person being insured.Insurable interest is defined as having a financialinterest wherein the insured could lose financialposition if the property were damaged or destroyed,or if the person was injured or died.Mutual AgreementAny changes the insurer makes must be agreed to inwriting by the insured, or the policy will not beissued.

Characteristics of an InsuranceContract