Embed Size (px)

Citation preview

19/11/2015

1

CRA and Fundraising:

Is There a Crackdown?

Presentation to the AFP Congress 2015 November 23, 2015

Mark Blumberg ([email protected]) Blumberg Segal LLP

GlobalPhilanthropy.ca 2

Blumberg Segal LLP

Blumberg Segal LLP is a law firm based in Toronto, Ontario

Mark Blumberg is a partner at Blumbergs who focuses on non-profit and charity law

Assists charities from across Canada with Canadian and international operations and foreign charities fundraising in Canada www.canadiancharitylaw.ca and www.globalphilanthropy.ca

Free Canadian Charity Law Newsletter. Sign up at: http://www.canadiancharitylaw.ca/index/php/pages/subscribe

(416) 361-1982 or 1-866-961-1982

www.twitter.com/canadiancharity

GlobalPhilanthropy.ca 3

Introduction

Legal information not legal advice

Views expressed are my own

Questions during and at end

Logistics and timing

19/11/2015

2

GlobalPhilanthropy.ca 4

Charity Law Basics

Registered charities are regulated by Charities Directorate of the Canada Revenue Agency (CRA)

Registered charities fall under both federal and provincial jurisdiction

Non-profits and charities are both tax exempt

Income Tax Act – concept of “registered charity” can issue “official donation receipt” with income tax savings for donor

Benefits and restrictions on registered charities

GlobalPhilanthropy.ca 5

Fundraising by Registered Charities

CRA’s Guidance on Fundraising (CG-013):

http://www.cra-arc.gc.ca/chrts-gvng/chrts/plcy/cgd/fndrsng-eng.html

My page on the fundraising guidance:

http://tinyurl.com/8x99n2j

PDF Version of Guidance

http://www.globalphilanthropy.ca/images/uploads/CRA_Fundraising_Guidance_April_20,_2012_-_final.pdf

GlobalPhilanthropy.ca 6

CRA Fundraising Guidance

Consultation draft in 2008

Published guidance on June 11, 2009

Revised guidance in April 2012 (“Guidance”)

19/11/2015

3

GlobalPhilanthropy.ca 7

Introduction

New guidance updates and replaces CPS-028, published on June 11, 2009.

One document, rather than 2

GlobalPhilanthropy.ca 8

Organization of Guidance

Fundraising by Registered Charities A. Introduction B. Summary C. Application and jurisdiction D. What is fundraising? E. Definitions F. When is fundraising not acceptable? G. Evaluating a charity's fundraising H. Factors that may influence the CRA’s evaluation of a charity’s

fundraising Appendix A – Examples of fundraising activities Appendix B – Allocating fundraising expenditures Appendix C – Best practices Appendix D – Questions and answers Footnotes

GlobalPhilanthropy.ca 9

Summary

Fundraising Guidance deals with fundraising issues under the Income Tax Act (Canada) and regulation of registered charities, not provincial or other regulation

Fundraising must be conducted within legal parameters

Guidance applies to all registered charities

Guidance is general advice – see facts of specific situation

19/11/2015

4

GlobalPhilanthropy.ca 10

Summary - Unacceptable Fundraising

Fundraising is acceptable provided that is not:

a purpose of the charity (a collateral, non-charitable purpose);

delivering a more than incidental private benefit (a benefit that is not necessary, reasonable, or proportionate in relation to the resulting public benefit);

illegal or contrary to public policy;

deceptive; or

an unrelated business.

GlobalPhilanthropy.ca 11

Summary – Indicators and Factors

6. When evaluating a charity’s fundraising activities, the CRA will consider a range of indicators and factors, including the following:

Resources devoted to fundraising relative to resources devoted to charitable programs;

Fundraising without an identifiable use or need for the proceeds;

The charity’s fundraising expenses to fundraising revenue ratio;

GlobalPhilanthropy.ca 12

Summary – Indicators and Factors (continued)

Inappropriate purchasing or staffing practices, including:

purchases of fundraising merchandise or services that do not increase fundraising revenue;

paying more than fair market value for fundraising merchandise or services; and

sole source or not-at-arm’s length contracts with suppliers or service providers.

Activities where most of the gross revenues go to contracted non-charitable parties;

Commission-based fundraiser remuneration or payment of fundraisers based on the amount or number of donations;

19/11/2015

5

GlobalPhilanthropy.ca 13

Summary – Indicators and Factors (continued)

Misrepresentations in fundraising solicitations or in disclosure about

fundraising costs, revenues or practices;

Fundraising initiative or arrangements that are not well documented;

The size of the charity;

Causes with limited appeal;

Donor development programs; and

Involvement in gaming activities.

GlobalPhilanthropy.ca 14

Fundraising Ratio

Ratio of costs to revenue over fiscal period – under 35%

This ratio is unlikely to generate questions or concerns by the CRA.

Ratio of costs to revenue over fiscal period – 35% and above

The CRA will examine the average ratio over recent years to determine if there is a trend of high fundraising costs. The higher the ratio, the more likely it is the CRA will be concerned the charity is engaged in fundraising that is not acceptable, requiring a more detailed assessment of expenditures.

Ratio of costs to revenue over fiscal period – above 70%

This level will raise concerns with the CRA. The charity must be able to provide an explanation and rationale for this level of expenditure to show that it is not engaged in unacceptable fundraising.

GlobalPhilanthropy.ca 15

Definition of Fundraising

As a general rule, fundraising is any activity that includes a solicitation of present or future donations of cash or gifts in kind, or the sale of goods or services to raise funds, whether explicit or implied.

19/11/2015

6

GlobalPhilanthropy.ca 16

What is Fundraising?

Fundraising activities can be carried out by the registered charity (board members, directors, members, staff or volunteers), or by anyone acting on its behalf (under a contractual agreement), and include;

Direct activities, such as:

Face to face canvassing, telemarketing, major gift work with individuals, and direct mail,

Internet or media campaigns (for example, electronic mail, online publications, web sites, television or radio);

Printed information, advertisements or publications (for example, newspapers, flyers, brochures and magazines);

GlobalPhilanthropy.ca 17

What is Fundraising? (continued)

• Events (for example, sports tournaments, runs, walks, auctions, dinners, galas, concerts and travel or trekking adventures);

• Sales of goods or services; or

• Donor stewardship, and membership or corporate sponsorship programs; and

Indirect or related activities, such as:

researching and developing fundraising strategies and plans or prospective donors;

recruiting and training development officers;

hiring fundraisers; or

donor recognition programs.

GlobalPhilanthropy.ca 18

Exclusions from Fundraising

Fundraising does not include:

1. Seeking grants, gifts, contributions, or other funding from other charities or government;

2. Recruiting volunteers to carry out the general operations of the charity; or

3. Related business activities. (See CPS-019, What is a Related Business?)

19/11/2015

7

GlobalPhilanthropy.ca 19

Misrepresentation

For example, registered charities must not misrepresent:

Which charity will receive the donation;

The geographic area in which the charity operates, and the amount or type of work it undertakes;

Whether they have hired third-party fundraisers, and how those fundraisers are compensated; or

The percentage of funds raised that will go to charitable work.

Claims that 100% of the money raised by a third party will go to the charity, or that 100% of money raised by the charity conducting its own fundraising will be used for charitable activities by the charity, must always be made with care.

Charities usually have some expenses for their fundraising activities, and may be required to pay substantial fees to any third-party fundraiser it employs. As these expenditures ultimately reduce the charity’s fundraising revenue, this type of claim could be considered to be deceptive.

GlobalPhilanthropy.ca 20

Appendices

Appendix A – Examples of fundraising activities

Appendix B – Allocating fundraising expenditures

Appendix C – Best practices

GlobalPhilanthropy.ca 21

Allocation of Expenditures

All expenditures should be allocated to one or more of:

Charitable expenditures

Fundraising

Management and administration

Political activity

Other expenditures as applicable

19/11/2015

8

GlobalPhilanthropy.ca 22

Why Allocate?

Activity can relate to many objectives

Ratios, public perception and disclosure

T3010 and disbursement quota

GlobalPhilanthropy.ca 23

Allocation on Fundraising

GlobalPhilanthropy.ca

GlobalPhilanthropy.ca 24

All Costs of Certain Activities = Fundraising

The CRA generally considers all costs associated with certain activities to be fundraising expenditures:

Any activity that involves the selection of participants or targeting of an audience based on their ability and/or likelihood to give;

Activities with content related to gaming, such as lotteries and bingos;

Dissemination of information, such as generic branding (that is, activities focusing on the general promotion or marketing of the charity's name and logo, image or past work), and activities that raise awareness about a charity's cause or work whether or not conducted in conjunction with fundraising, unless the activity can be shown to further the charitable purpose (see Characteristics of charitable, fundraising, management/administrative and political content below for more details).

19/11/2015

9

GlobalPhilanthropy.ca 25

All Costs of Certain Activities = Fundraising (continued)

Infomercials and telemarketing as defined and used for Canadian Radio-

television and Telecommunications (CRTC) purposes;

Branding or promoting the charity through cause-related or social marketing;

Activities that involve sports, including games, running, walking, cycling and mountain climbing, with participants being encouraged or expected to raise pledges; and

Golf tournament and gala dinner fundraisers.

GlobalPhilanthropy.ca 26

Understating Fundraising Expenses

Where a charity knowingly or negligently understates its fundraising expenses on line 5020 of Form T3010 or elsewhere, this is taken into account in assessing whether the charity has acted reasonably.

Inaccurate reporting is grounds for compliance action under the Income Tax Act.

2012 Budget – CRA can suspend charity’s receipting privileges for incomplete or inaccurate T3010 filing.

GlobalPhilanthropy.ca 27

Disclosure

The CRA recommends that charities provide complete disclosure of all fundraising costs, revenues, practices, and arrangements so that members of the public—and, more specifically, donors or prospective donors—are not deceived or misled about the resources from fundraising that are ultimately available to a registered charity for its programs, services, or gifts to qualified donees.

19/11/2015

10

GlobalPhilanthropy.ca 28

Disclosure

To be meaningful, disclosure must be accurate, accessible, and timely.

GlobalPhilanthropy.ca 29

Reserve Fund Policy

“A reserve fund policy may assist a charity when planning, explaining, and justifying its approach to fundraising to donors and to the CRA. It may help to ensure that a charity fundraises with an identifiable use or need, reducing the risk of failing to devote resources to charitable activities or engaging in fundraising that forms a collateral purpose. A transparent and publicly accessible policy may also help ensure that fundraising appeals are not misleading or deceptive, by misrepresenting the charity's financial position and the extent or urgency of its need for funds.”

GlobalPhilanthropy.ca 30

Reserve Fund Policy (continued)

The size of a justifiable reserve fund will depend on a charity’s

particular situation. For example, when establishing a reserve fund, the charity could show it has taken into account factors such as:

Typical annual expenditures; size; long-term plans; donor base; projected revenue; current and projected economic conditions; anticipated changes to the environment in which the charity operates; contingencies; and known risks being faced.

Review policy periodically to take into account the changing needs of the charity.

19/11/2015

11

GlobalPhilanthropy.ca 31

Questions - Third Party Events

Local organizations or individuals sometimes hold a fundraising event on their own initiative, and donate the proceeds to our charity. We are not connected to these organizations, individuals, or events in any way, and often are unaware the events have even taken place until we receive the money.

Q. Do we have to ensure that these local organizations and individuals comply with the fundraising guidance?

GlobalPhilanthropy.ca 32

Third Party Events

A. No. This guidance does not apply to fundraising activities carried on by organizations that are not registered charities, or by individuals or organizations with whom/which a registered charity does not have a fundraising arrangement.

A charity must ensure that any individual or organization that carries out fundraising activities on its behalf complies with this guidance.

GlobalPhilanthropy.ca 33

Sword and Shield

“While recognizing the necessity of fundraising, the CRA expects charities to be transparent and to not devote excessive amounts of time and/or resources to fundraising as opposed to fulfilling their charitable purposes.”

“It also confirms to the public that fundraising expenditures are appropriate and in fact necessary for the sustainability of the sector.”

19/11/2015

12

GlobalPhilanthropy.ca 34

Ontario Public Guardian and Trustee

Charitable Fundraising: Tips for Directors and Trustees

http://www.attorneygeneral.jus.gov.on.ca/english/family/pgt/charbullet/bulletin-8.asp

The courts have stated that fundraising costs must be reasonable in relation to the amount of funds raised.

GlobalPhilanthropy.ca 35

Director Liability

“The Public Guardian and Trustee can require a charity to account for donations and related expenses of a fundraising campaign and can require information about fundraising appeals. If the Public Guardian and Trustee has serious concerns about fundraising expenses the charity may be asked to pass its accounts before the court. Directors and trustees can be personally liable for fundraising costs that are found to be unreasonable.”

GlobalPhilanthropy.ca 36

PGT: Factors to Consider with Contract

Appendix A: Factors to Consider Before Signing a Fundraising Contract

Has the fundraiser provided references from other charities for which similar campaigns have been conducted? Were those charities satisfied with the results that were achieved?

Are the fees and charges reasonable? If potential donors were aware of the fees and charges associated with a donation, would they still make the donation?

Does the fundraiser subscribe to a code of ethics?

Are the terms of the contract clear and well understood?

19/11/2015

13

GlobalPhilanthropy.ca 37

PGT: Factors to Consider with Contract (continued)

Are acceptable fundraising methods specified in the contract? Are the fundraising methods consistent with the written fundraising plan?

Will the fundraising campaign generate sufficient revenue to allow the charity to engage in activities related to its charitable purpose?

Are canvassers required to provide accurate information to potential donors about the proportion of the donation that will be used for charitable purposes?

Are canvassers required to identify themselves as commercial fundraisers? Are they prohibited from representing themselves as employees or volunteers of the charity?

Will fundraisers provide donors with receipts? Is the fundraiser required to keep receipt books secure and safe? If the charity is not registered under the Income Tax Act, will canvassers make this fact clear to donors?

GlobalPhilanthropy.ca 38

PGT: Factors to Consider with Contract (continued)

Will the donor list remain the exclusive property of the charity?

Will the donation bank account remain under the sole control of the charity?

How will fees and charges be calculated? If there is a disagreement, how will it be resolved?

Will the fundraiser provide a full accounting for expenses and funds received? Will the fundraiser provide periodic accountings to enable the charity to monitor the performance of the campaign? Will receipts and vouchers be provided to document all disbursements?

When does the contract terminate? Are there any penalties for terminating the contract early if the charity is not satisfied with the services that are provided?

GlobalPhilanthropy.ca 39

Special Purpose Fundraising

Raising funds for special purpose

Only use funds for that purpose

Good idea to have alternative purpose, if original purpose cannot be carried out or surplus funds

Communicate purpose and alternative to potential donors

Otherwise may need to return funds or apply to court

Keep record of fundraising campaign and purpose

19/11/2015

14

Third Party Fundraising Events

GlobalPhilanthropy.ca 41

Third Party Events with Volunteers

Many charities have third party events with volunteers

Engages volunteers and volunteers raise funds

Importance of low cost fundraising

Risk Management for these events

GlobalPhilanthropy.ca 42

Documentation for Third Party Events

Application for event

Agreement between charity and third party fundraiser

19/11/2015

15

GlobalPhilanthropy.ca 43

Issues

Roles and Responsibilities

Financial responsibility

Budget

Insurance and Liability

Use of logos and TM of charity

Issuance of receipts

Indemnity

Use of professional fundraiser

Compliance with laws

Permits

GlobalPhilanthropy.ca 44

Issues (continued)

Marketing and Promotional Material approval

Prohibited Conduct: eg. commissions; behaviour that is counter to the mission; nuisance to the public; events which may be misleading or deceptive; partisan political activities;

Restrictions on type of solicitation – eg. direct solicitation (including but not limited to door-to-door canvassing, telemarketing or internet).

Restrictions on who may be solicited – current sponsors, national corporations etc. – prior approval?

Other restrictions from gift acceptance policy

GlobalPhilanthropy.ca 45

Issues (continued)

Remittances of funds to charity

Reporting to charity – donor list, advantages etc.

Exclusivity of event to charity (not joint event)

Right of cancellation by charity

Reporting of complaints by organizers

Right to use photos taken at event

Recognition

Non-Assignment

Term

19/11/2015

16

Abusive Schemes

Recent Charity Fundraising Revocations

GlobalPhilanthropy.ca 48

Childhope Foundation Canada

Childhope Foundation Canada was audited for the period from July 1, 2008 to June 30, 2009

The following areas of non-compliance with the Income Tax Act were identified:

Failure to devote resources to charitable purposes;

Official Donation Receipts;

Information Return (Form T3010); and

Remuneration and Benefits Reporting.

http://www.globalphilanthropy.ca/images/uploads/Childhope_Foundation_Canada_Redacted.pdf

19/11/2015

17

GlobalPhilanthropy.ca 49

Childhope Foundation Canada (continued)

Failure to devote resources to charitable purposes

CRA found that the fundraising expenses as a proportion of fund raised by door to door soliciting, telemarketing and donations boxes was 74.45% and fundraising expenses as a proportion of total revenue of 64.10%.

The issue of high cost fundraising was raised by CRA during a previous audit in 2004 and a review of the fundraising expenses for 2005 to 2007 were also high.

A compliance agreement was entered into, where it was agreed that fundraising expenses would be no more than 20%.

The use of professional fundraisers contributed to the high ratios and in 2008, when they were not used, the expenses were only 40.8% of related donations or 33.7% of the total revenue.

GlobalPhilanthropy.ca 50

Childhope Foundation Canada (continued)

CRA made the following comments regarding the fundraising practices:

“Registered charities, or third parties acting on their behalf, are not permitted to engage in conduct that is contrary to public policy … The courts have held that fundraising contracts can be harmful to the public interest if the terms of the contract are such that the charity does not retain the greater share of the amount collected and/or if they result in the misrepresentation to the public about whether donated amounts go to the charity or to pay the fundraising company collecting them.”

“Where the costs of a fundraising activity are not, on their face, in reasonable proportion to the funds raised or to the funds subsequently available to the charity to support its charitable activities, the need for disclosure in order to ensure that donors are not inadvertently misled has been emphasised by the court.

GlobalPhilanthropy.ca 51

Childhope Foundation Canada (continued)

“When [the Organization] enters into arrangements in which it devotes its

financial and human resources to for-profit entities such as third party fundraisers/contractors, events planners, etc., we would consider that it has devoted resources to non-charitable activities … such arrangements with third parties could be viewed as providing an excessive or disproportionate private benefit that makes the fundraising unacceptable.”

“By pursuing these non-charitable purposes, the Organization has failed to demonstrate that … as a charitable organization, all the resources of which are devoted to charitable activities.”

19/11/2015

18

GlobalPhilanthropy.ca 52

Cancer Survivors’ Fund of Canada

Cancer Survivors’ Fund of Canada was audited for the period from April 1, 2008 to March 31, 2011

The following areas of non-compliance with the Income Tax Act were identified:

Failure to devote resources to charitable purposes;

Providing undue private benefit;

Failure to maintain adequate books and records; and

Failure to file an information return (T3010).

http://www.globalphilanthropy.ca/images/uploads/Cancer_Survivors_Fund_of_Canada_-_CRA_letters_about_revocation.pdf

GlobalPhilanthropy.ca 53

Cancer Survivor’s Fund of Canada (continued)

Failure to devote resources to charitable purposes

CRA noted that the Organization’s intended purposes and activities were to provide scholarships for cancer survivors but that it was predominately involved in fundraising.

Fundraising costs were 98% and 92% of all total expenditures in 2009 and 2010, respectively.

The Organization hired MTC as a the sole fundraiser and was only guaranteed 10% of the gross receipts with the balance paid to MTC.

GlobalPhilanthropy.ca 54

Cancer Survivor’s Fund of Canada (continued)

CRA reviewed the following “Areas of Concern”

Sole-source fundraising contracts without proof of fair market value;

Non-arm’s length fundraising contracts without proof of fair market value;

Fundraising initiatives or arrangements that are not well-documented;

Fundraising merchandised purchases that are not at arm’s length, not at fair market value, or not purchased to increase fundraising revenue;

Activities where most of the gross revenues go to contracted non-charitable parties;

Commission-based fundraiser remuneration or payment of fundraisers based on amount or number of donations;

Total resources devoted to fundraising exceeding total resources devoted to program activities; and

Misrepresentations in fundraising solicitations or in disclosures about fundraising or financial performance.

19/11/2015

19

GlobalPhilanthropy.ca 55

Cancer Survivor’s Fund of Canada (continued)

CRA noted that the Organization did not follow any “Best Practices”

including:

Prudent planning processes;

Appropriate procurement processes;

Good staffing processes;

Ongoing management and supervision of fundraising practice;

Adequate evaluation processes;

Use made of volunteer time and volunteered services or resources; and

Disclosure of fundraising costs, revenue and practice.

GlobalPhilanthropy.ca 56

Cancer Survivor’s Fund of Canada (continued)

CRA made the following comments regarding the fundraising practices:

The Organization engaged in prohibitive fundraising practices because fundraising was the main and independent purpose of the Organization. Moreover, the fundraising arrangement could be considered contrary to public policy because it misrepresented to the public the amount available for use by the charity. Fundraisers were told that ‘fundraising costs may exceed fifty percent of the donations,’ when in fact the agreement guaranteed MTC ninety percent of gross receipts. As well the fundraising activity resulted in more than an incidental or proportionate private benefit to MTC.”

“The Organization did not employ any best practices that would have reduced the risk of unacceptable fundraising. On the contrary … the Organization was involved in fundraising practices that were areas of concern.

GlobalPhilanthropy.ca 57

The Voice of the Cerebral Palsied of Greater Vancouver

The Voice of the Cerebral Palsied of Greater Vancouver was audited for the period from April 1, 2006 to March 31, 2008

The following areas of non-compliance with the Income Tax Act were identified:

Failure to devote resources to charitable purposes;

Failure to maintain adequate books and records;

Books and records;

Registered Charity Information Return;

Disbursement quota; and

Statements of remuneration paid.

http://www.globalphilanthropy.ca/images/uploads/The_Voice_of_the_Cerebral_Palsied_of_Greater_Vancouver_-_CRA_letters_about_charity_revocation.pdf

19/11/2015

20

GlobalPhilanthropy.ca 58

The Voice of the Cerebral Palsied of Greater Vancouver (continued)

Failure to devote resources to charitable purposes

The Organization’s fundraising activities included door-to-door canvassing using 4 locally contracted fundraisers and telemarketing.

There was a fundraising contract with a professional fundraising company but no contracts for the door-to-door fundraisers.

During a previous audit, the Organization was informed that the absence of such contracts was unacceptable. The previous auditor noted that no fundraising earnings statements were presented or retained by the Charity for its fundraising contractors and there was a lack of follow up in maintaining constant weekly contact with the door-to-door fundraisers to ensure the funds collected were accounted for.

GlobalPhilanthropy.ca 59

The Voice of the Cerebral Palsied of Greater Vancouver (continued)

During the current audit period, over $140,000 was raised but only $10,500 (7.5%) was remitted to the Organization after costs and commission.

During a previous CRA audit, 60% of gross revenue was paid to the sales director.

In 2003 and 2004 89% of gross revenue raised was paid to a third party fundraiser to cover its costs.

CRA found the Organization did not commit to its undertaking of September 21, 2005, in which it stated:

“We are in the process of restructuring the way we do fundraising to reduce the costs of these fundraising activities. We have contacted all of our fundraisers with who we have contracts. We notified them about the requirement to spend 80% of receipted income for charitable purposes and we will adjust our contract with them to meet this requirement.”

Less than 15% of total income and less than 20% of receipted income was spent on charitable activities during the current audit period.

GlobalPhilanthropy.ca 60

The Voice of the Cerebral Palsied of Greater Vancouver (continued)

CRA made the following comments regarding the fundraising practices:

“The fundraising activities of the Charity include door-to-door canvassing using 4 locally contracted fundraisers and telemarketing. These facts in themselves are not contentious, but the lack of control and accountability over the fundraising activities, revenues and expenditures paid certainly are.”

“Our audit of the Charity failed to reveal the practices and procedures of the Charity maintains and acts upon when retaining the services of third party fundraisers. Our audit has revealed the Charity has no prudent planning processes, no on-going management of or supervision of the activities undertaken on the Charity’s behalf by the third party fundraisers nor does the Charity engage in regular evaluation process … The Charity was often unable to contact its fundraisers, and while it concerned some board members, there were no discussions of alternative resolutions.”

19/11/2015

21

GlobalPhilanthropy.ca 61

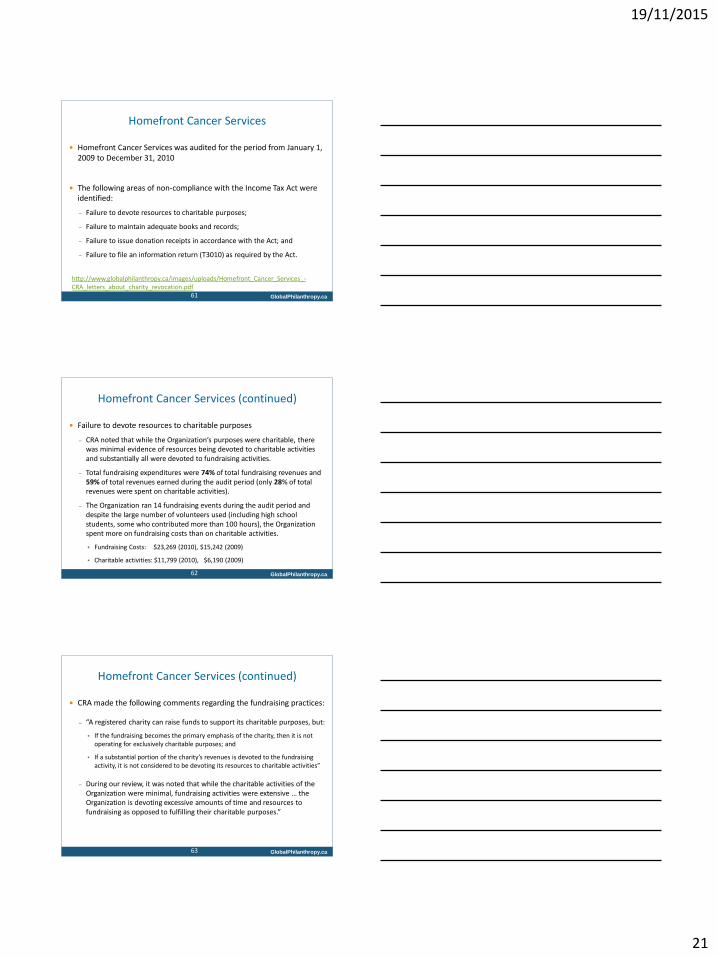

Homefront Cancer Services

Homefront Cancer Services was audited for the period from January 1, 2009 to December 31, 2010

The following areas of non-compliance with the Income Tax Act were identified:

Failure to devote resources to charitable purposes;

Failure to maintain adequate books and records;

Failure to issue donation receipts in accordance with the Act; and

Failure to file an information return (T3010) as required by the Act.

http://www.globalphilanthropy.ca/images/uploads/Homefront_Cancer_Services_-CRA_letters_about_charity_revocation.pdf

GlobalPhilanthropy.ca 62

Homefront Cancer Services (continued)

Failure to devote resources to charitable purposes

CRA noted that while the Organization’s purposes were charitable, there was minimal evidence of resources being devoted to charitable activities and substantially all were devoted to fundraising activities.

Total fundraising expenditures were 74% of total fundraising revenues and 59% of total revenues earned during the audit period (only 28% of total revenues were spent on charitable activities).

The Organization ran 14 fundraising events during the audit period and despite the large number of volunteers used (including high school students, some who contributed more than 100 hours), the Organization spent more on fundraising costs than on charitable activities.

Fundraising Costs: $23,269 (2010), $15,242 (2009)

Charitable activities: $11,799 (2010), $6,190 (2009)

GlobalPhilanthropy.ca 63

Homefront Cancer Services (continued)

CRA made the following comments regarding the fundraising practices:

“A registered charity can raise funds to support its charitable purposes, but:

If the fundraising becomes the primary emphasis of the charity, then it is not operating for exclusively charitable purposes; and

If a substantial portion of the charity’s revenues is devoted to the fundraising activity, it is not considered to be devoting its resources to charitable activities”

During our review, it was noted that while the charitable activities of the Organization were minimal, fundraising activities were extensive … the Organization is devoting excessive amounts of time and resources to fundraising as opposed to fulfilling their charitable purposes.”

19/11/2015

22

GlobalPhilanthropy.ca 64

National Wild Turkey Federation - Canada

National Wild Turkey Federation – Canada was audited for the period from September 1, 2006 to August 31, 2010

The following areas of non-compliance with the Income Tax Act were identified:

Failure to devote resources to charitable purposes;

Issuing receipts not in accordance with the Act;

Failure to maintain adequate books and records; and

Inaccurate completion of T3010 Registered Charity Information Return.

http://www.globalphilanthropy.ca/images/uploads/National_Wild_Turkey_Federation_-_Canada_-_CRA_letters_about_charity_revocation.pdf

GlobalPhilanthropy.ca 65

National Wild Turkey Federation – Canada (continued)

Failure to devote resources to charitable purposes

CRA noted that while the Organization’s purposes were charitable, there was minimal evidence of resources being devoted to charitable activities and substantially all were devoted to fundraising activities.

Total fundraising expenditures were 81% of total revenues earned during the audit period (only 11% of total revenues were spent on charitable activities).

The Organization ran 80 banquets during the audit period and despite the large number of volunteers used, the Organization spent more on fundraising costs than on charitable activities.

Fundraising Costs: $535,796 (2010), $507,918 (2009)

Charitable activities: $72,450 (2010), $75,169 (2009)

GlobalPhilanthropy.ca 66

National Wild Turkey Federation – Canada (continued)

The Organization has an operating procedures agreement with the National Wild Turkey Federation – US, which provided that all costs of the banquets and a 15% Regional administration fee were deducted from total revenues. The net proceeds from the fundraising events were allocated as follows

Provincial Super Fund – 56%, Local chapter fee – 4%, Provincial chapter fee – 1%, National projects – 24% and Administration – 15%

While the Organization’s “Super Fund” and National projects were included in CRA’s assessment of the charitable activities, CRA noted that the literature for the Organization’s “Super Fund” indicated that the fund was ‘dedicated to the conservation of wild turkey and preservation of our hunting heritage’. The preservation of wild turkey was within the Organization’s objects, however, the preservation of hunting heritage were not with in the objects and would not be considered charitable activities.

19/11/2015

23

GlobalPhilanthropy.ca 67

National Wild Turkey Federation – Canada (continued)

CRA made the following comments regarding the fundraising practices:

“It is expected that fundraising be ancillary and incidental to the charity’s charitable purposes. Fundraising should be a means to an end. In other words, it is carried on to generate funds to carry out charitable activities. The amount incurred for fundraising costs should be reasonable and proportionate to the amount of funds raised for charitable activities and programs.”

“If, on the other hand, a significant portion of the charity’s resources and funds are spent on fundraising or retained by the fundraiser, fundraising could be considered an end itself. In this case fundraising could be a separate and collateral purpose of the charity, and the charity would not be devoting all of its resources to its charitable purposed.

GlobalPhilanthropy.ca 68

More Resources

How Much Should a Canadian Charity Spend on Overhead? http://www.donorsguide.ca/pdfs/Blumberg.pdf

How to effectively donate to a Canadian charity - some suggestions from a charity lawyer

http://www.globalphilanthropy.ca/index.php/blog/comments/how_to_effectively_donate_to_a_canadian_charity_-_some_suggestions_from_a_c/

Donating to a Canadian charity in a disaster - suggestions to ensure funds gets to the most needy

http://www.canadiancharitylaw.ca/index.php/blog/comments/donating_to_a_canadian_charity_in_a_disaster_-_suggestions_to_ensure_funds_/

“Bill C-470 and the Backlash Against Fundraising” - by Malcolm Burrows http://www.globalphilanthropy.ca/index.php/blog/comments/bill_c-

470_and_the_backlash_against_fundraising_-_by_malcolm_burrows/

Giving to charity: Information for donors http://www.cra-arc.gc.ca/chrts-gvng/dnrs/menu-eng.html

GlobalPhilanthropy.ca 69

Thank you! Blumberg Segal LLP

Barristers & Solicitors

390 Bay Street, Suite 1202

Toronto, Ontario, M5H 2Y2

Tel. (416) 361-1982 ext. 237

Toll Free (866) 961-1982

Fax. (416) 363-8451

Email: [email protected]

Twitter at: http://twitter.com/canadiancharity

www.canadiancharitylaw.ca and www.globalphilanthropy.ca

![WELCOME [afptoronto.org]afptoronto.org/wp-content/uploads/2017/11/G-15-You... · non-profits on corporate governance and tax compliance • Assist in transactional proceedings](https://img.pdfslide.net/doc/110x75/5f84724fcaac7b4aee2c17b9/welcome-non-profits-on-corporate-governance-and-tax-compliance-a-assist-in.jpg)