Embed Size (px)

Citation preview

CRC Energy Efficiency Scheme

Eight Days To GoAre You Ready?

Workshop presented 22 March 2010 by

Michael Webb, Client Services Manager

John Treble, Managing Director

The Green Consultancy Ltd

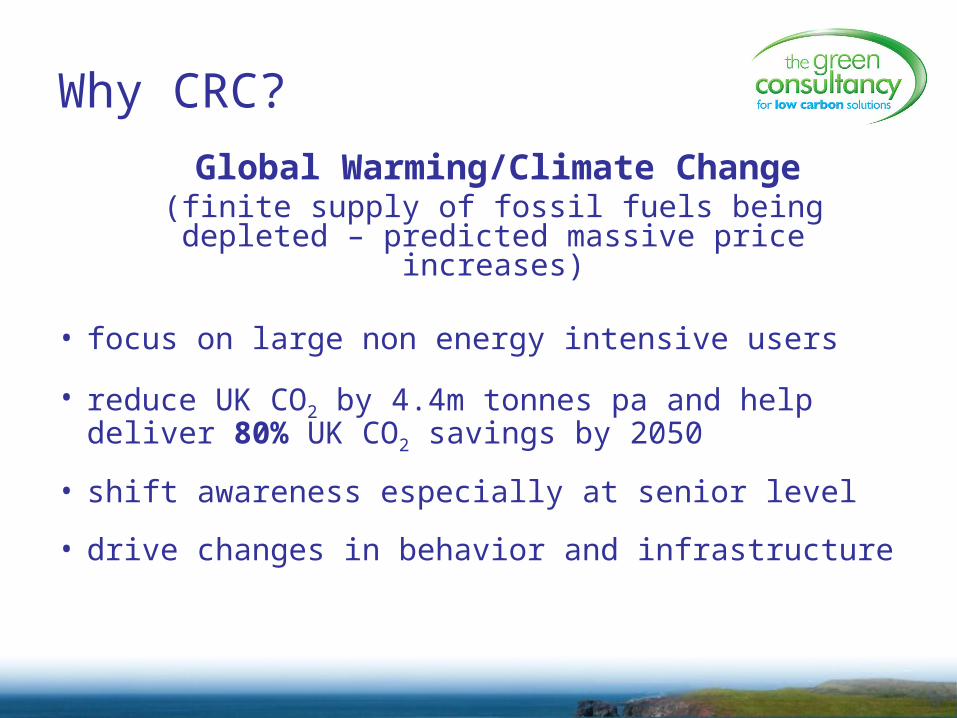

Why CRC?

Global Warming/Climate Change(finite supply of fossil fuels being depleted –

predicted massive price increases)

• focus on large non energy intensive users

• reduce UK CO2 by 4.4m tonnes pa and help deliver 80% UK CO2 savings by 2050

• shift awareness especially at senior level

• drive changes in behavior and infrastructure

How CRC Works

• 6,000 MWh HHM electricity in 2008; 5,000 participants

• highest parent organisation and all subsidiaries

• buy allowances to cover forecast annual emissions

• record and report actual emissions and surrender allowances

• receive recycling payment based on number of allowances, performance against base year and relative to other participants

• performance table published

• Phase 1 (2010-13) allowances £12 a tonne

• auctioned In Phase 2 (2013 onwards) - £50 a tonne?

How CRC Works

• compulsory; financial incentive to reduce emissions; places a price on carbon emissions

• overall emissions reduction target achieved by a ‘cap’ on total allowances set by Government (Phase 2)

• participants determine most cost-effective means to act – buy allowances or invest in energy reduction

• annual performance league table of participants - reputational driver

• not a tax (all revenue recycled back to participants)

• scheme administrator Environment Agency• scheme regulator – EA (Eng + Wales), Dept of the

Environment for N.I. , Scottish Env. Protection Agency

How CRC Works

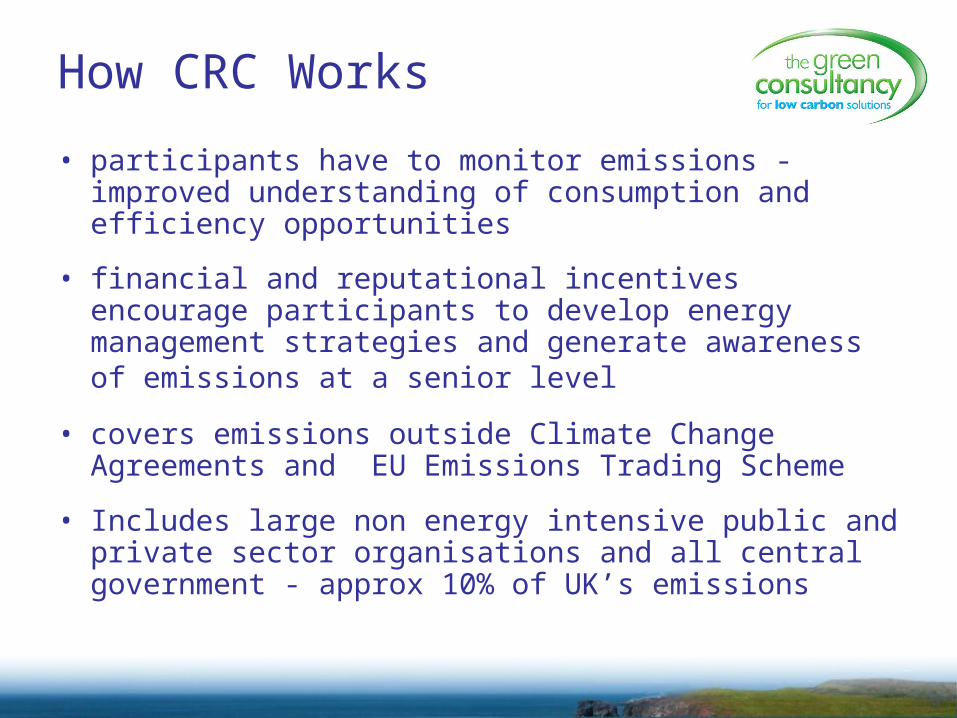

• participants have to monitor emissions - improved understanding of consumption and efficiency opportunities

• financial and reputational incentives encourage participants to develop energy management strategies and generate awareness of emissions at a senior level

• covers emissions outside Climate Change Agreements and EU Emissions Trading Scheme

• Includes large non energy intensive public and private sector organisations and all central government - approx 10% of UK’s emissions

TIMELINE

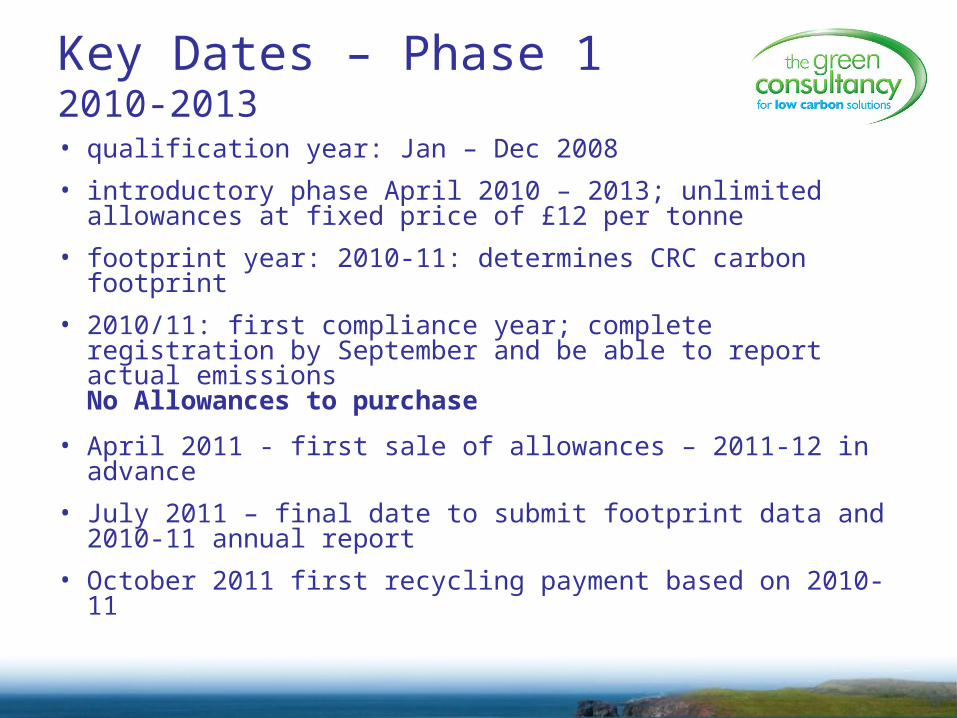

Key Dates – Phase 12010-2013• qualification year: Jan – Dec 2008

• introductory phase April 2010 – 2013; unlimited allowances at fixed price of £12 per tonne

• footprint year: 2010-11: determines CRC carbon footprint

• 2010/11: first compliance year; complete registration by September and be able to report actual emissionsNo Allowances to purchase

• April 2011 - first sale of allowances – 2011-12 in advance

• July 2011 – final date to submit footprint data and 2010-11 annual report

• October 2011 first recycling payment based on 2010-11

Key Dates – Phase 2

• April 2010: start of qualification period for year two

• 2011-2012: footprint year and first reporting year registration starts

• July 2012: first annual report + footprint report

• April 2013: first capped auction

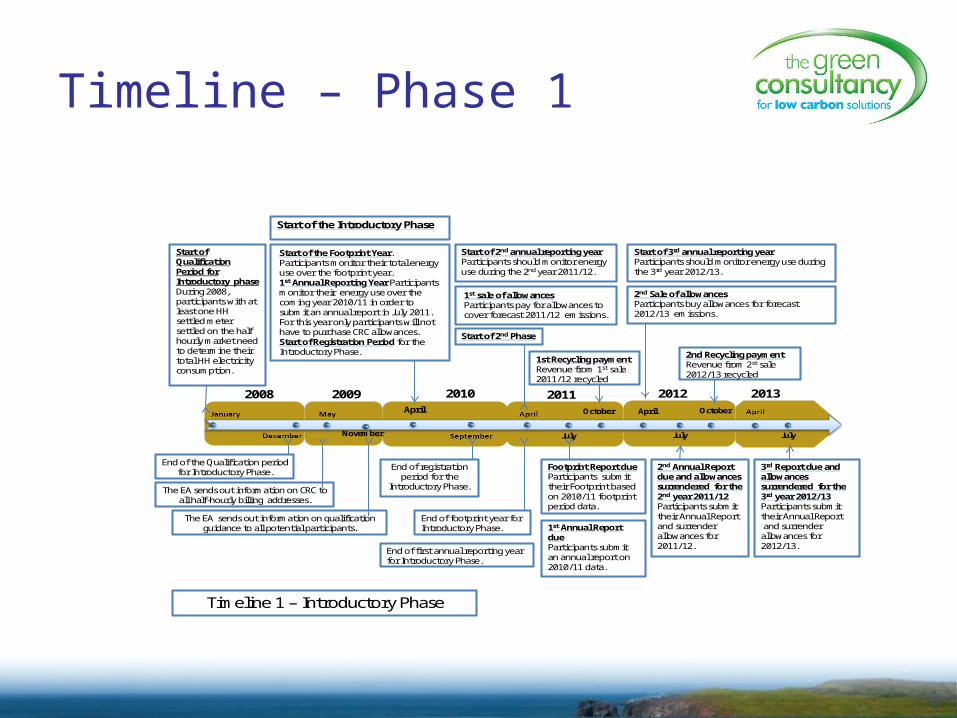

Timeline – Phase 1

November

Start of Qualification Period for Introductory phase During 2008, participants with at least one HH settled meter settled on the half hourly market need to determine their total HH electricity consumption.

The EA sends out information on qualification guidance to all potential participants.

2008 2009 2010 2011 2012April

July

October April

July

October

July

The EA sends out information on CRC to all half-hourly billing addresses.

Footprint Report due Participants submit their Footprint based on 2010/11 footprint period data.

Start of 2nd annual reporting yearParticipants should monitor energy use during the 2nd year 2011/12.

Start of 3rd annual reporting yearParticipants should monitor energy use during the 3rd year 2012/13.

3rd Report due and allowances surrendered for the 3rd year 2012/13 Participants submit their Annual Reportand surrender

allowances for 2012/13.

Timeline 1 – Introductory Phase

End of the Qualification period for Introductory Phase.

End of registration period for the

Introductory Phase.

1st Annual Report due Participants submit an annual report on 2010/11 data.

2nd Annual Report due and allowances surrendered for the 2nd year 2011/12Participants submit their Annual Reportand surrender allowances for 2011/12.

Start of the Footprint Year. Participants monitor their total energy use over the footprint year.1st Annual Reporting Year Participants monitor their energy use over the coming year 2010/11 in order to submit an annual report in July 2011. For this year only participants will not have to purchase CRC allowances. Start of Registration Period for the Introductory Phase.

1st sale of allowancesParticipants pay for allowances to cover forecast 2011/12 emissions.

End of first annual reporting year for Introductory Phase.

End of footprint year for Introductory Phase.

Start of the Introductory Phase

2013

1st Recycling payment Revenue from 1st sale 2011/12 recycled

Start of 2nd Phase

2nd Recycling paymentRevenue from 2st sale 2012/13 recycled

2nd Sale of allowancesParticipants buy allowances for forecast 2012/13 emissions.

Timeline – Phase 2

2010 2011 2012 2013 2014

Start of Footprint Year for Second PhaseParticipants will need to monitor their total energy use over the footprint year

Start of Registration for the Second Phase

Footprint Report due Participants submit their Footprint Report based on 2011/12 footprint period data

Start of the Second Phase

1st Annual Report dueParticipants submit their annual report for 2012/13

1st Annual Reporting Year for the Second Phase Participants must monitor their energy use over the coming year in order to submit an annual report in July 2013. Participants will not have to purchase CRC allowances for the first annual reporting year of the second phase.

2nd Annual Report due and allowances surrenderedParticipants submit an annual report and surrender allowances for 2013/14

1st Recycling paymentRevenue from April 2013 sale recycled.

Start of 2nd Annual Reporting YearParticipants must monitor energy use during the 2nd year 2013/14.

Timeline 2 – Second Phase

Start of Qualification Period for Second PhaseParticipants with at least one HH settled meter need to monitor their total HH electricity consumption.

Registration for the Second phase ends

Qualification period for the Second phase ends

1st Auction of allowancesParticipants bid for allowances for 2013/14 forecast emissions.

Start of 3rd Annual Reporting YearParticipants must monitor energy use during the 3rd year 2014/15.

2nd Auction of allowancesParticipants bid for allowances for 2014/15 forecast emissions.

2nd Recycling paymentRevenue from April 2014 sale recycled.

INFORMATION DISCLOSURE

QUALIFICATION

& REGISTRATION

Information Disclosure

• all organisations with a HHM settled on half hourly market at any point during calendar year 2008 but total HHM electricity less than 6000 MWh (approx 15,000)

• disclosure made via online registry– List HHMs settled on half hour market including meter point

admin number– Identify kWh via all HHMS and if below 3,000 provide contact

details, above 3,000 details of amount

• between April-September 2010

• £500 fine per HHM if failure to comply

Qualification

• 6000 MWh of electricity through any HHM settled on half hourly market Jan – Dec 2008

• estimated 5,000 organisations qualify

• participants legally required to comply; substantial fines for non compliance

• registration packs sent to all half hour billing addresses Sept 2009

• register online April – September 2010

Organisation Definition

• highest parent company responsible – as defined by companies act

• includes all UK based subsidiaries

• includes franchises

• includes companies with 50%+ ownership

• special rules for tenant/landlord

• all central government will participate

Qualification (Jan – Dec 2008)

• responsibility of “highest parent” to report

• structure at Dec 2008

• to include: information on subsidiaries; responsible person (Director); list of all HHMs; total HHM used in qualifying period

• failure to register - £5000 and £500 per additional day

• registration fee: £950, annual fee £1,290

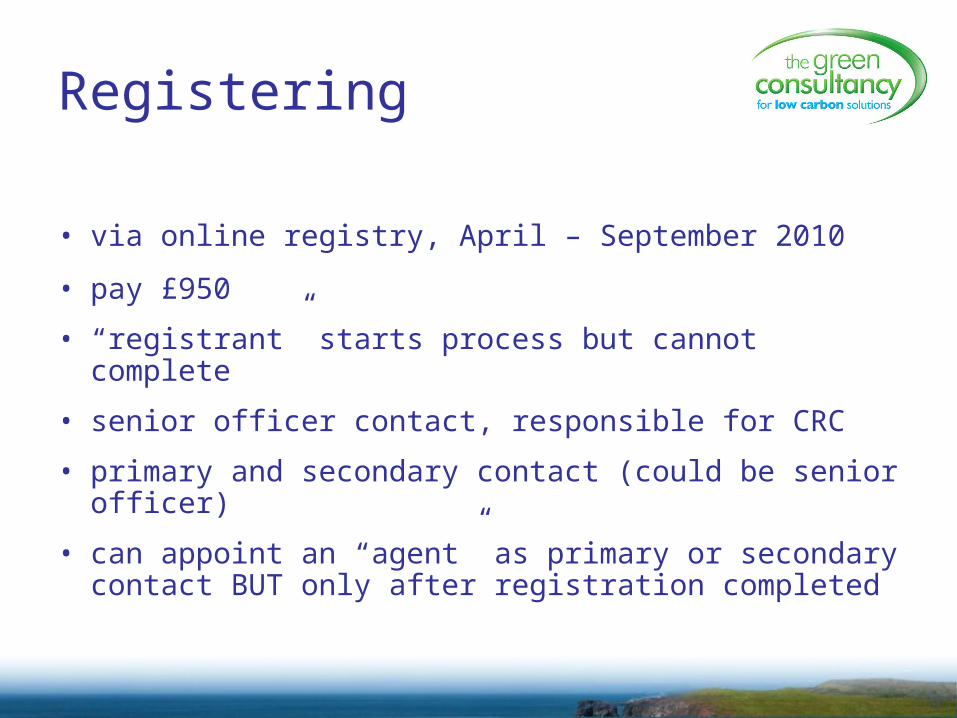

Registering

• via online registry, April – September 2010

• pay £950

• “registrant” starts process but cannot complete

• senior officer contact, responsible for CRC

• primary and secondary contact (could be senior officer)

• can appoint an “agent” as primary or secondary contact BUT only after registration completed

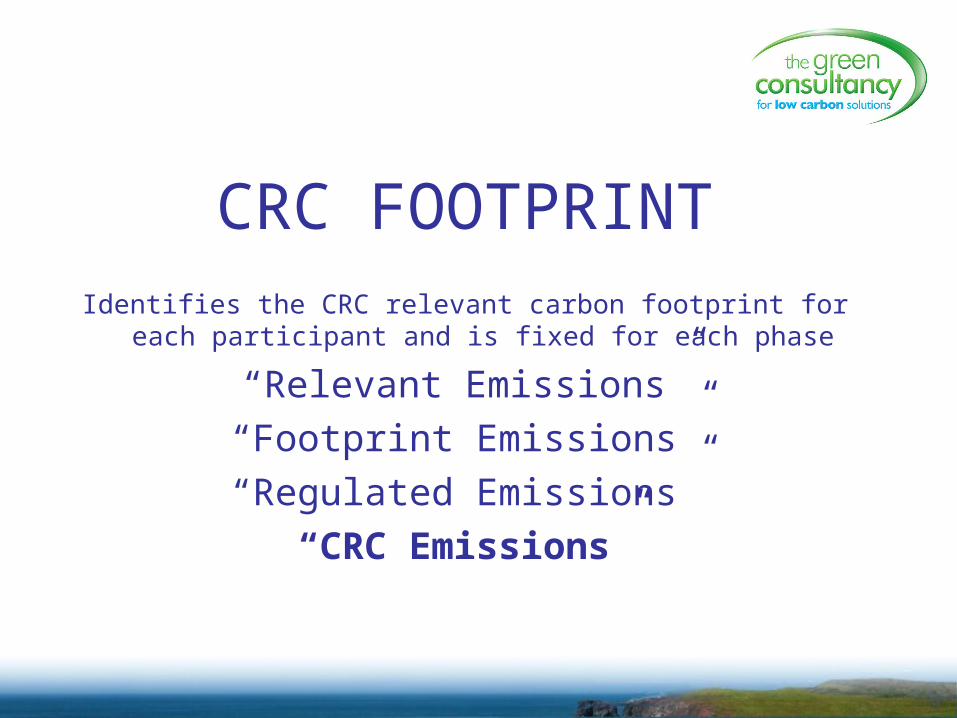

CRC FOOTPRINTIdentifies the CRC relevant carbon footprint for each participant and is

fixed for each phase

“Relevant Emissions”

“Footprint Emissions”

“Regulated Emissions”

“CRC Emissions”

Footprint Year

• participants identify and report CRC defined carbon footprint (CRC emissions)

– phase 1: April 2010 - March 2011; submit by July 2011

– phase 2: April 2011 - March 2012; submit by July 2012

“Relevant Emissions” • all energy used in period – electricity, gas, oil, etc

• based on bills – estimates increased by 10%

• suppliers legally obliged to provide information BUT customer must formally request by no later than end Feb 2011 (for 2010-11) – provided by mid May

• convert to CO2 using standard CRC factors

• deduct any transport and onward supply

RESULT = “relevant emissions”

• “relevant emissions” remain fixed for first phase

“Footprint Emissions”

• Climate Change Agreement (CCA) excluded from CRC: deduct from “relevant emissions” to give CRC “footprint emissions”

– If single entity and 25% of total emissions covered by CCA whole organisation exempt

– If 25% of a subsidiary’s organisation, that subsidiary is exempt

– If remaining HHM is under 1000 MWh then total exemption

– Proof required, if CCA lost re-enter from next compliance year

“relevant emissions” – CCA = “footprint emissions”

“Footprint Emissions”• must Include all “core” sources:

all HHMs and AMRs, profile class 5-8 meters; daily read gas; gas AMR; non daily gas if 73,200 kWh a year (unless covered by CCA or EUETS)

• if core sources + CCA or EUETS are less than 90% of total footprint emissions add non core “residual sources” to reach at least 90%

• residual sources can be included if wished

• %age covered is minimum to cover in subsequent phases

“footprint emissions” – allowable “residual sources” = “regulated emissions”

CRC Emissions

Finally…

If any emissions covered by CCAs or by EU ETS remain in the “regulated emissions” deduct to arrive at “CRC emissions”

This is the basis for reporting annual emissions and forms the basis for determining each participants “share” of total CRC footprint emissions – a key determinant of the recycling payment.

Footprint Report

• end of footprint year 2010-11, report via online registry:– “footprint emissions “– “CRC emissions”– exemptions through CCAs

• submit by end July 2011

• failure?

£5,000 fine + £500 a working day up to 40 days, then doubled

Annual Report• via online registry report annual CRC emissions by

energy source

• automatically converted into tonnes CO2

• submit by end of July following end of compliance year –first one July 2011

• surrender equivalent number of allowances

• backed up by auditable “evidence pack”

• failure: £5,000 fine plus £500 a day, doubled after 40 days; EA determines emissions and will double; allowances for doubled amount to be surrendered

• failure to surrender allowances: £40 tonne, withheld recycling payment and published

CRC Evidence Pack

Records to support information provided to EA must be kept in an evidence pack.

• records and evidence for all data used in footprint report

• all energy sources making up “relevant emissions”

• energy use and emissions for each compliance year

• evidence pack disclosed to the regulator when audited

• director required to be responsible for evidence pack

• failure to keep complete evidence pack viewable on request: £40 per CRC tonne of CO2 and published

Self Generated Electricity/Renewables

• if covered by EUETS – not in CRC

• if ROCs or FITs claimed – no CRC benefit

• no ROCS or FITs claimed – can claim CRC electricity generating credits, used to offset allowances needed

• calculated at grid average emissions factor

• use of renewables noted on league table – reputational benefit

BUYING AND SURRENDERING

ALLOWANCES

Buying AllowancesPhase 1

• April of each compliance year, one per tonne of forecast emissions

• no allowances purchased for 2010-11

• first sale of allowances in April 2011 for 2011/12

• no limit on total available in April BUT no more issued after April; fixed price of £12 per allowance from EA

• must hold and surrender sufficient allowances to cover actual emissions at year end

• can buy extra allowances after April from other participants, traders or through EU ETS “safety net”

Buying AllowancesPhase 2

• total allowances available “capped” based on data from phase one and UK carbon targets

• participants work out allowances needed at a range of price points and “bid” for different amounts

• government decides how many allowances to issue and price set by bids made by all participants

• participants failing to secure sufficient allowances have to buy from anyone holding surplus allowances at a “market” price

(marginal cost of carbon abatement)

Surrendering AllowancesPhase 1

• annual report submitted no later than 4 months after year end – July – and allowances surrenderedNo allowances to surrender for 2010-11

• cannot use allowances bought for current year to meet obligations for previous year

• can roll over unused allowances into next year BUT not from Phase 1 to Phase 2

• similar process in each year of Phase 1 after first year

PERFORMANCE

LEAGUE TABLE&

REVENUE RECYCLING

Performance League Table

• measures relative performance of all participants – approximately 5000

• performance measured against 3 “metrics” – early action, absolute, growth

• carbon reduction target, performance against target, responsible director and employee engagement, use of renewables also shown on league table

• published

• league table position determines +/- % “bonus” or “penalty”.

• bonus/penalty: year one +/- 10% rising to +/- 50% in year five

The “Metrics”

• Criteria for league table position

• All “metrics” scored and then proportionally weighted

• Absolute: %age change in emissions measured as a rolling average from “footprint” year figures

• Early Action: voluntary half hour metering + Carbon Trust Standard Accreditation

• Growth: change in emissions intensity

• Only required to report Absolute Metric BUT will be scored zero if early action and growth not reported

Absolute Metric

• compares current year emissions with average of previous five years emissions (or however many years are known starting with the footprint year – 2010-11)

• weighting– 0% in year one– 45% in year two– 60% in year three– 75% subsequently

• compulsory reporting

Early Action Metric• %age of non half hour metered CRC emissions covered

by voluntary installed automatic metering (AMR) as of March 31st 2011

• and %age of CRC emissions covered by CT Standard (or equivalent) at 31st March each year

• 50/50 split between meters and carbon standard

• weighting– 100% in year 1 – 40% in year 2– 20% in year 3– 0% subsequently

• voluntary reporting

Growth Metric

• %age change in emissions per unit of turnover or revenue compared with average for preceding 5 years

• weighting– 0% in year one – 15% in year two– 20% in year three – 25% subsequently

• voluntary reporting

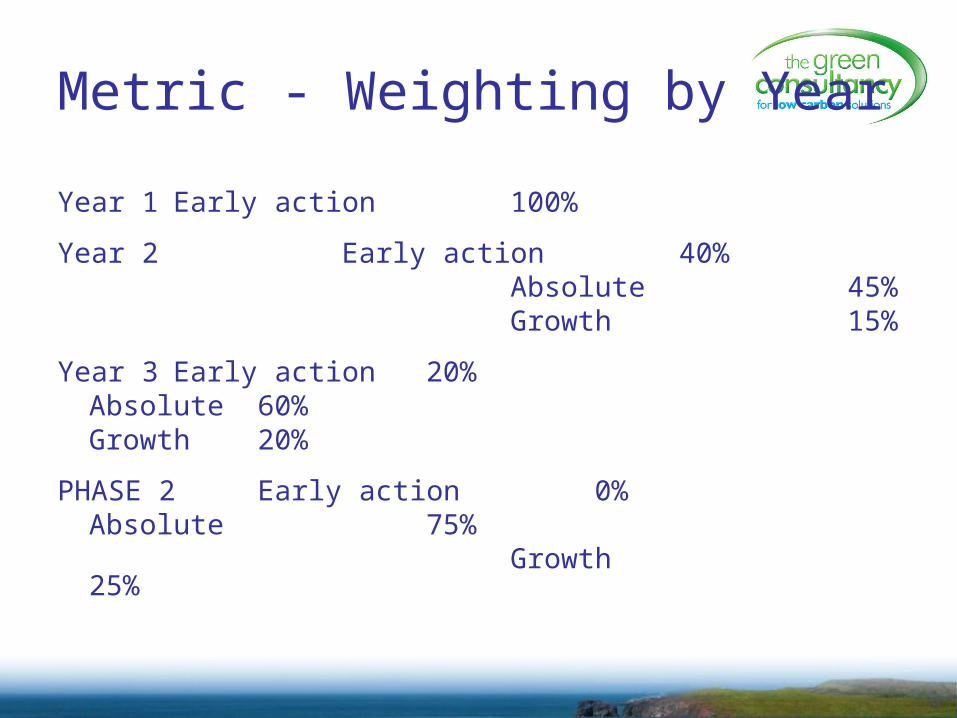

Metric - Weighting by Year

Year 1 Early action 100%

Year 2 Early action 40% Absolute 45% Growth 15%

Year 3 Early action 20%Absolute 60%Growth 20%

PHASE 2 Early action 0%Absolute 75%

Growth 25%

League Table

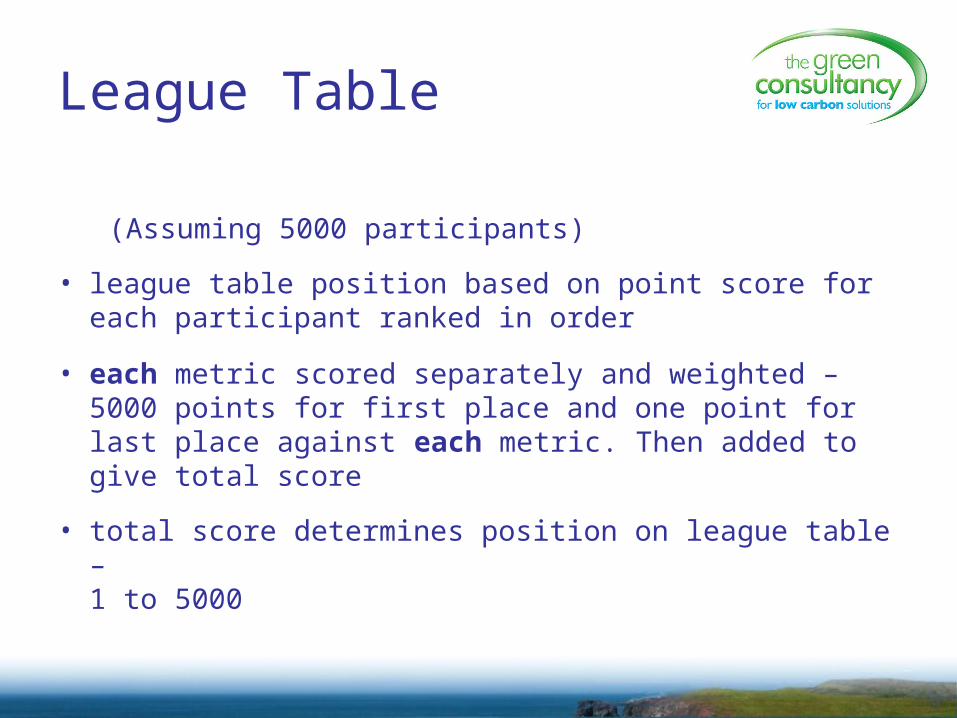

(Assuming 5000 participants)

• league table position based on point score for each participant ranked in order

• each metric scored separately and weighted – 5000 points for first place and one point for last place against each metric. Then added to give total score

• total score determines position on league table – 1 to 5000

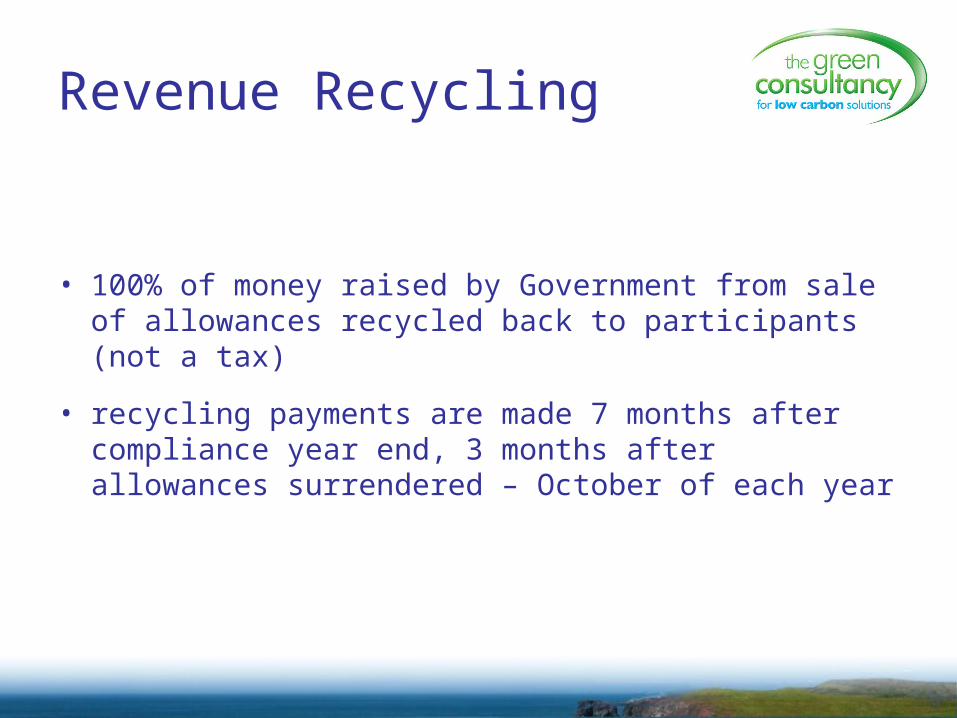

Revenue Recycling

• 100% of money raised by Government from sale of allowances recycled back to participants (not a tax)

• recycling payments are made 7 months after compliance year end, 3 months after allowances surrendered – October of each year

Recycling PaymentCalculation – it’s complicated!

Key Criteria

• League table position

• +/- bonus/penalty for year (+/-10% in year one rising to +/- 50% in year 5

• Individual base year emissions as %age of total base year emissions

• £ revenue available for recycling

• Bonus or penalty to be applied to each participant

Recycling PaymentCalculating…

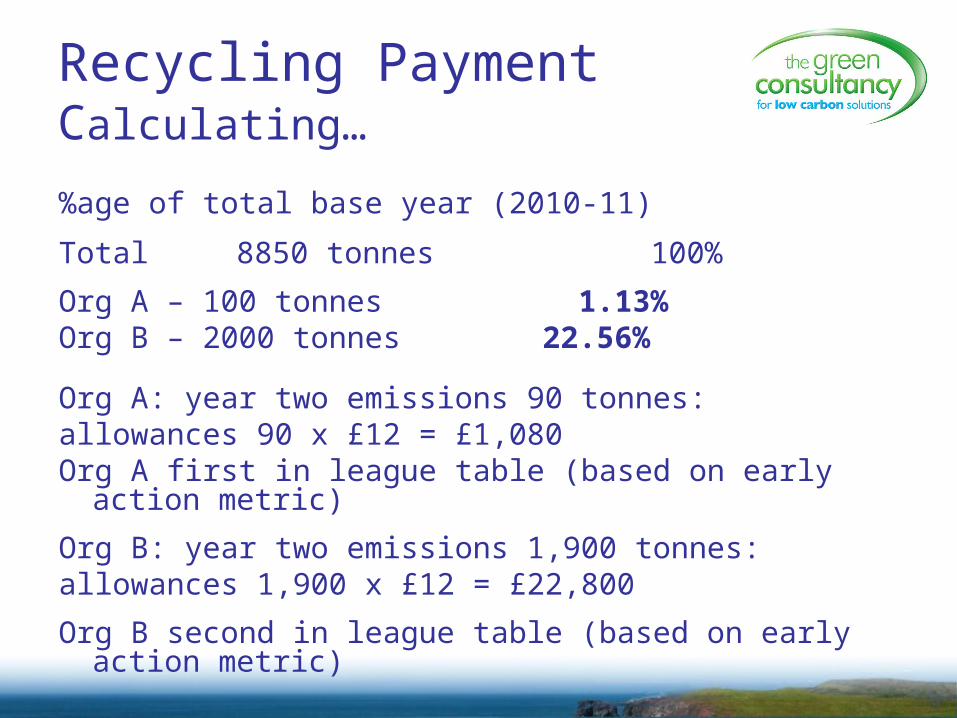

%age of total base year (2010-11)

Total 8850 tonnes 100%

Org A – 100 tonnes 1.13% Org B – 2000 tonnes 22.56%

Org A: year two emissions 90 tonnes:allowances 90 x £12 = £1,080Org A first in league table (based on early action metric)

Org B: year two emissions 1,900 tonnes:allowances 1,900 x £12 = £22,800

Org B second in league table (based on early action metric)

Recycling PaymentCalculating…

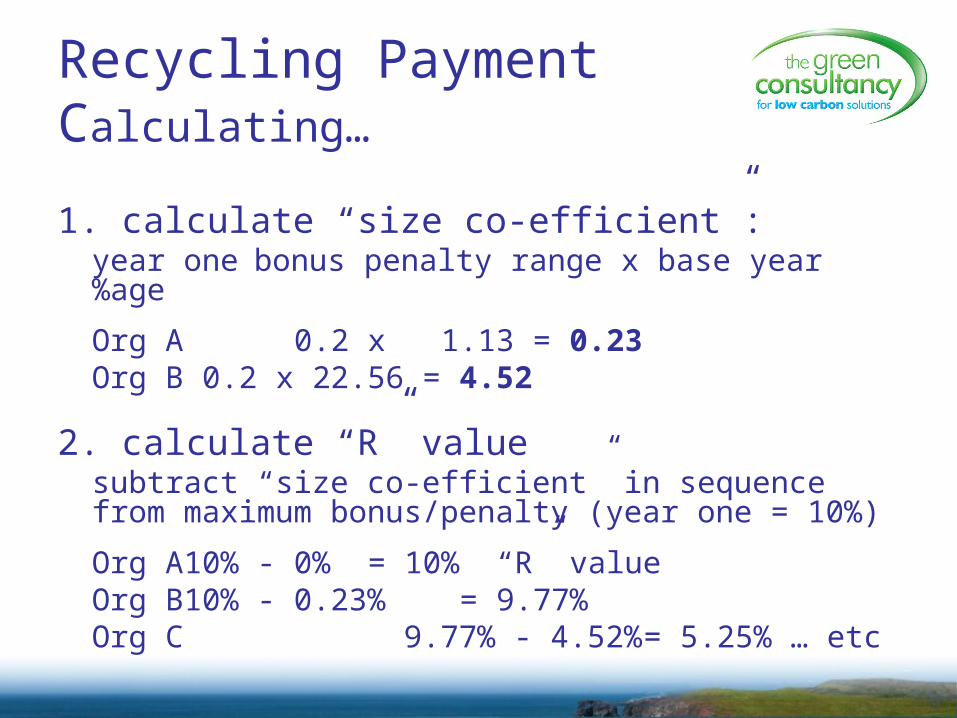

1. calculate “size co-efficient”: year one bonus penalty range x base year %age

Org A 0.2 x 1.13 = 0.23Org B 0.2 x 22.56 = 4.52

2. calculate “R” valuesubtract “size co-efficient” in sequence from maximum bonus/penalty (year one = 10%)

Org A 10% - 0% = 10% “R” valueOrg B 10% - 0.23% = 9.77% Org C 9.77% - 4.52% = 5.25% … etc

Recycling PaymentCalculating…

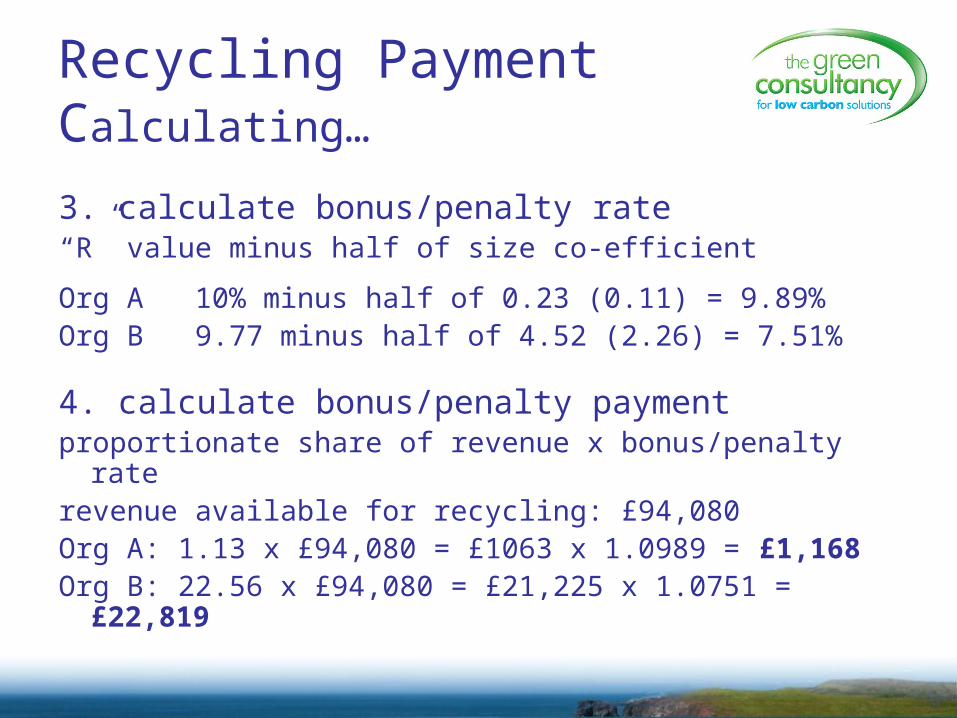

3. calculate bonus/penalty rate“R” value minus half of size co-efficient

Org A 10% minus half of 0.23 (0.11) = 9.89%Org B 9.77 minus half of 4.52 (2.26) = 7.51%

4. calculate bonus/penalty paymentproportionate share of revenue x bonus/penalty raterevenue available for recycling: £94,080Org A: 1.13 x £94,080 = £1063 x 1.0989 = £1,168Org B: 22.56 x £94,080 = £21,225 x 1.0751 = £22,819

Auditing and Regulation

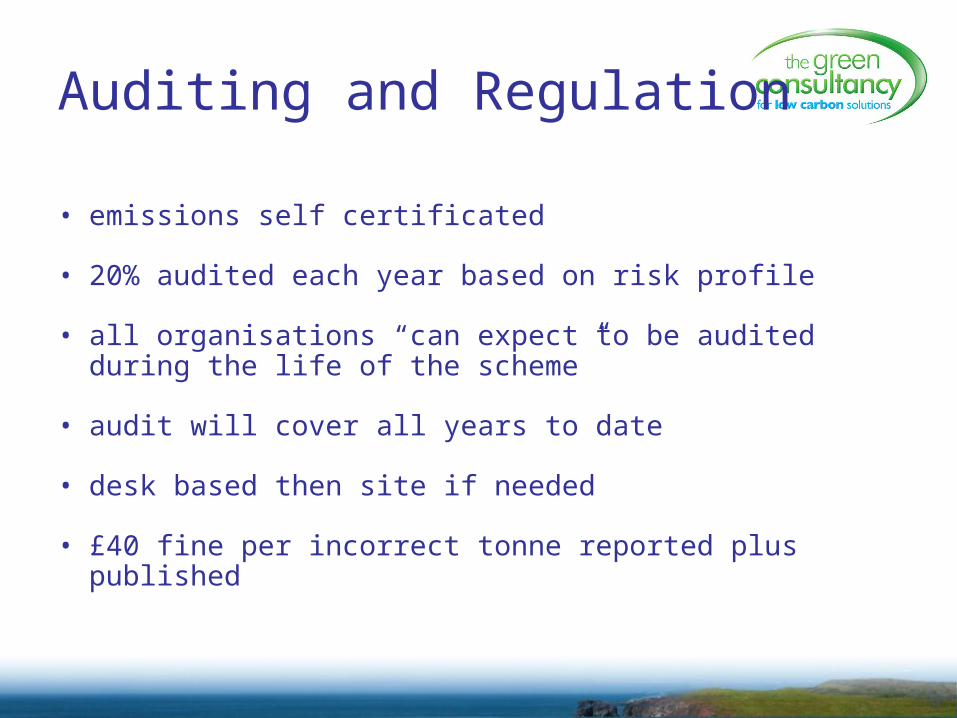

• emissions self certificated

• 20% audited each year based on risk profile

• all organisations “can expect to be audited during the life of the scheme”

• audit will cover all years to date

• desk based then site if needed

• £40 fine per incorrect tonne reported plus published

Phase 2 – Capped

• 2013-14 onwards

• process starts again, re-assess against qualification criteria, re-do footprint (2011-12)

• some organisations in phase one will drop out and others join (qualification criteria?)

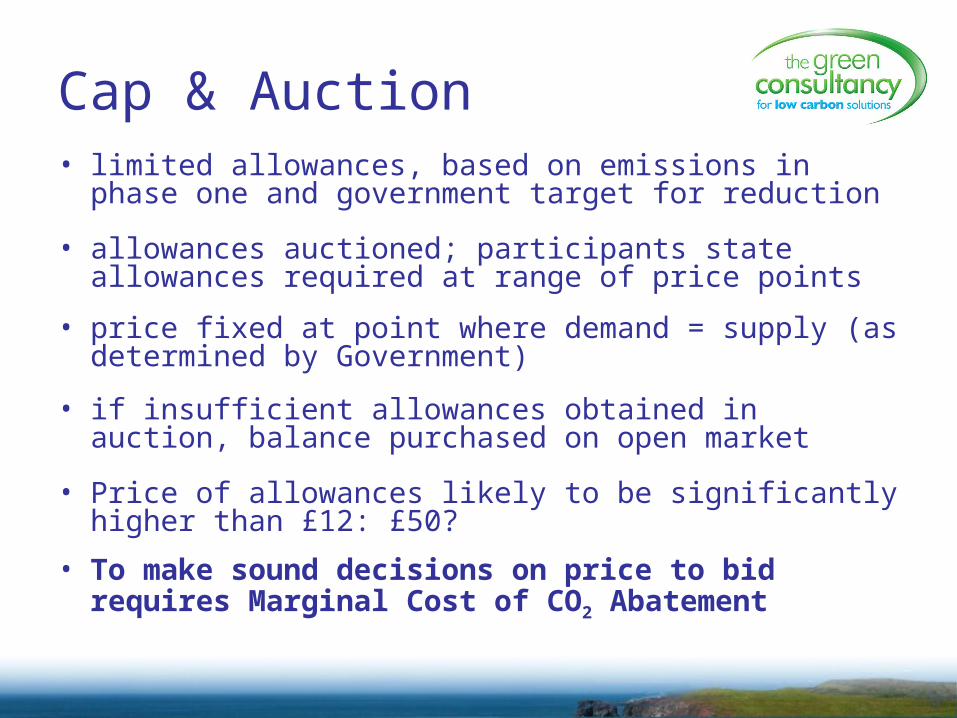

Cap & Auction• limited allowances, based on emissions in phase one

and government target for reduction

• allowances auctioned; participants state allowances required at range of price points

• price fixed at point where demand = supply (as determined by Government)

• if insufficient allowances obtained in auction, balance purchased on open market

• Price of allowances likely to be significantly higher than £12: £50?

• To make sound decisions on price to bid requires Marginal Cost of CO2 Abatement

Implications?

Costs• registration and administration fee

• administration – internal and/or external resource

• improved monitoring

• potential fines

• capital tied up in allowances – seven months a year

• loss or gain from recycling payment

Implications?

• reputation (league table published)

• requires senior management engagement

• increases importance of energy management

• Phase 2 cost of allowances unknown – could be 5-10 times more than £12 a tonne

Implications?

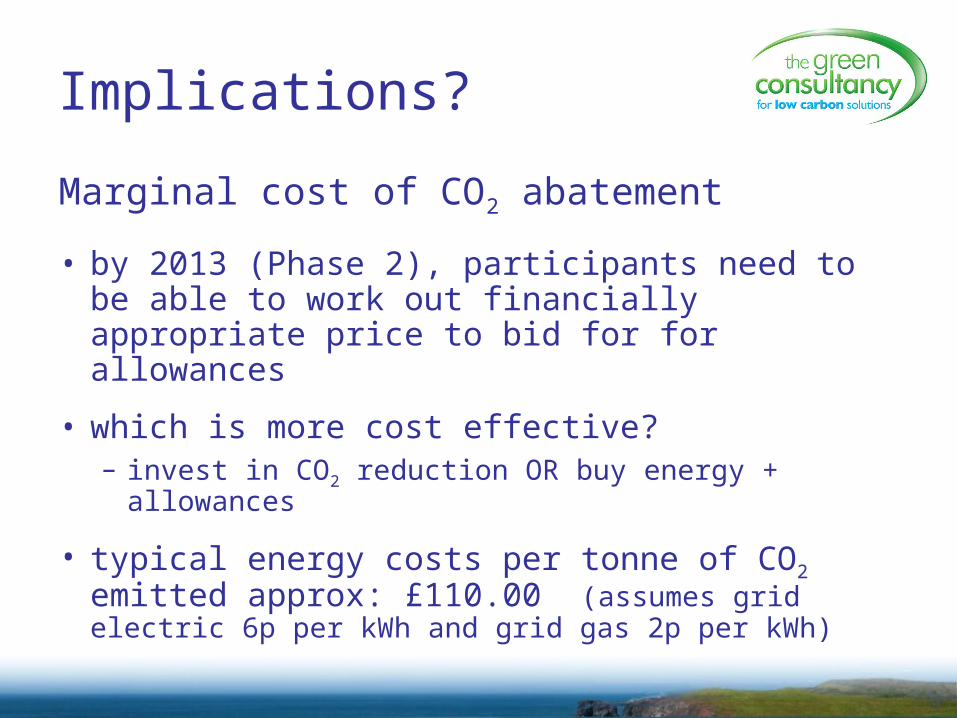

Marginal cost of CO2 abatement

• by 2013 (Phase 2), participants need to be able to work out financially appropriate price to bid for for allowances

• which is more cost effective?– invest in CO2 reduction OR buy energy + allowances

• typical energy costs per tonne of CO2 emitted approx: £110.00 (assumes grid electric 6p per kWh and grid gas 2p per kWh)

Cost Mitigation

reduced CO2 emissions =

lower allowance cost +improved recycling payment +lower energy bills

Act Now

• agree responsible senior officer and primary + secondary contacts

• set up planning and delivery group

• develop CRC strategy

• register online

• identify CRC footprint

• agree any “early action”

• adapt or develop recording and reporting system

• integrate with other energy/carbon action

• organisation wide culture change and awareness

The Wider Picture

CRCEES places greater emphasis on energy saving and carbon reduction amongst participants

In short term significant compliance requirements and incentives to reduce consumption/emissions

Incentives escalate substantially in Phase 2 when allowances are capped

HE and FE participants to think longer term about maximising energy efficiency in a cost effective manner and how to integrate CRC with other initiatives and requirements – Carbon Management Plans

HE and FE below registration threshold to consider now if likely to have to register for Phase 2

CRC, HEFCE & CMPs

• CRC and HEFCE are twin drivers demanding that most universities produce comprehensive robust Carbon Management Plans (CMPs)

• For assistance with CRC or CMPs please contact Michael Webb

• [email protected] 176300

A Challenge?

If your electricity consumption is currently 6000 – 8000 MWh for 2009-10 can you get below 6000 MWh by 2011-12?