Embed Size (px)

Citation preview

DECLARATION

I, Arpan Bhowmick, a PGDM student at IMIS, Bhubaneswar bearing roll no. 13DM068,

hereby declare that this report on Summer Internship Project titled Credit Appraisal at

Bank of India is solely my work and is prepared by me only.

I also declare that I have not revealed any sort of critical information of the bank as

per the secrecy bond I have signed with BOI before undertaking this project in their esteemed

organization.

I also declare that all the information collected from various secondary sources has

been duly acknowledged in this project report.

Place:

Date: (Arpan Bhowmick)

ACKNOWLEDGEMENT

I would like to extend my heartfelt gratitude towards the Management of Bank of

India for providing me an opportunity to undergo my Summer Internship Project in their

esteemed organization. I am extremely grateful to my external guide Mr. xxxxxxxxx

(Manager-Credit), CIC Branch, Bhubaneswar for his guidance and cooperative nature that

helped me in completing this project report. I have learned many new things about the bank

credit system while working at BOI.

I would also like to thank Mr. xxxxxxxxxxx, Senior Manager who permitted me to

work on my project in his branch and for his timely support and advice that helped me in

preparation of this report.

I express my sincere gratitude towards my internal guide xxxxxxxxxxxxx at IMIS,

Bhubaneswar for his time to time guidance and encouragement to take up this interesting

topic.

Last but not the least I would like to thank the Training & Placement Cell at IMIS

for placing me at a prestigious organization like Bank of India for my Summer Internship

Project.

(Arpan Bhowmick)

ABSTRACT

The project is on credit appraisal process of Bank of India. Credit appraisal is an

important activity carried out by the credit department of the bank to determine whether to

accept or reject the proposal for finance. In the beginning the report talks about Bank of

India’s history, its overall financial status and its decision making process.

After that this report talks about bank lending. It starts with principles of lending then

through role of RBI and then types of lending i.e. Fund based lending and Non-fund based

lending along with brief explanations and examples as well.

In the following chapter Credit appraisal is briefly overviewed before talking about

the credit appraisal process in general and then the process undertaken by BOI. It also covers

the various types of appraisals done such as commercial appraisal, technical appraisal and

financial appraisal.

Credit report and credit rating is discussed thereafter. The need of corporate credit

rating is explained in detail followed by the rating scales used by BOI.

The last but one chapter gives a screenshot of a few cases that I could fully cover

during my tenure at the CIC Branch of BOI at Rasulgarh. This includes the appraisal

procedure the bank took for a personal loan case, an automobile loan case, an education loan

and an SME loan.

In the end, I speak about my findings, conclusion and recommendations.

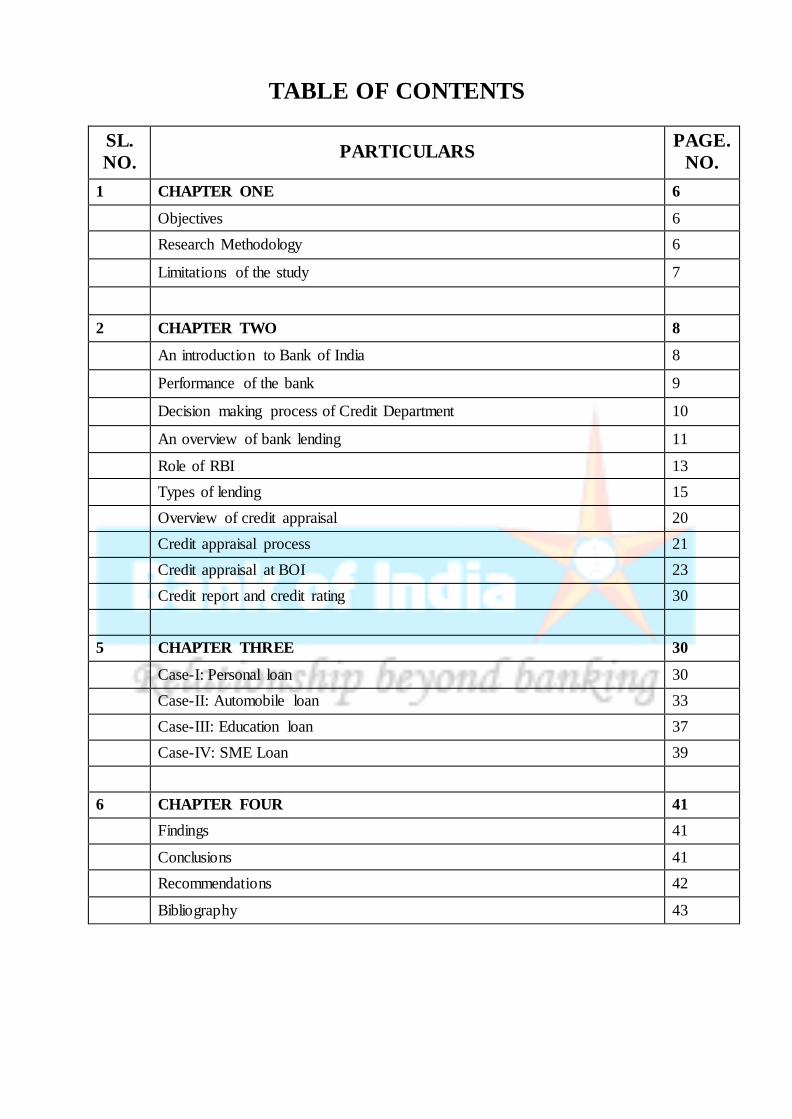

TABLE OF CONTENTS

SL.

NO. PARTICULARS

PAGE.

NO.

1 CHAPTER ONE 6

Objectives 6

Research Methodology 6

Limitations of the study 7

2 CHAPTER TWO 8

An introduction to Bank of India 8

Performance of the bank 9

Decision making process of Credit Department 10

An overview of bank lending 11

Role of RBI 13

Types of lending 15

Overview of credit appraisal 20

Credit appraisal process 21

Credit appraisal at BOI 23

Credit report and credit rating 30

5 CHAPTER THREE 30

Case-I: Personal loan 30

Case-II: Automobile loan 33

Case-III: Education loan 37

Case-IV: SME Loan 39

6 CHAPTER FOUR 41

Findings 41

Conclusions 41

Recommendations 42

Bibliography 43

CHAPTER ONE

OBJECTIVES:

- To study the credit appraisal methods.

- To understand the internal steps taken by the bank for scrutinizing the customer’s

details and credentials.

- To understand the commercial, financial & technical viability of the proposal

proposed and it’s finding pattern.

RESEARCH METHODOLOGY:

Introduction:

Credit appraisal means investigation/assessment done by the bank before providing

any loans and advances/project finance and also checks the commercial, financial

&industrial viability of the project proposed its funding pattern and further checks the

primary & collateral security cover available for recovery of such funds.

Problem statement:

To study the credit appraisal system in Bank of India

Data collection:

i. Primary data:

Informal interview with manager at Bank of India

ii. Secondary data:

- Books

- Websites

- Customer files at BOI

- Circulars of BOI

Beneficiaries:

- Researchers: This report will help researchers improving knowledge about the

credit appraisal system and to have practical exposure of the credit appraisal

system at Bank of India.

- Management students: The project will help the management student to know

the patterns of credit appraisal in Bank of India.

LIMITATIONS OF THE STUDY:

- As the credit appraisal is one of the most crucial areas for any bank, some of the

technicalities are not revealed.

- Credit appraisal system includes various types of detail studies for different areas

of analysis, but due to time constraint, our analysis was of limited areas only.

- The study was only on desk jobs related to credit. I was not exposed to the field

survey and valuation part.

- As per the bank’s terms and conditions related to internship, approaching

customers was not allowed.

- Actual balance sheets, ratios, financial statements of the customers were not

shared with me for my records and thus my study lacks certain details.

CHAPTER TWO

AN INTRODUCTION TO BANK OF INDIA

Bank of India was founded on 7th September, 1906 by a group of eminent businessmen from

Mumbai. The Bank was under private ownership and control till July 1969 when it was

nationalized along with 13 other banks.

Beginning with one office in Mumbai, with a paid-up capital of Rs.50 lakh and 50

employees, the Bank has made a rapid growth over the years and blossomed into a mighty

institution with a strong national presence and sizable international operations. In business

volume, the Bank occupies a premier position among the nationalized banks.

The Bank has 4545 branches in India spread over all states/ union territories including

specialized branches. These branches are controlled through 50 Zonal Offices. There are 54

branches/ offices and 5 Subsidiaries and 1 joint venture abroad.

The Bank came out with its maiden public issue in 1997 and follow on Qualified Institutions

Placement in February 2008.

While firmly adhering to a policy of prudence and caution, the Bank has been in the forefront

of introducing various innovative services and systems. Business has been conducted with the

successful blend of traditional values and ethics and the most modern infrastructure. The

Bank has been the first among the nationalized banks to establish a fully computerized branch

and ATM facility at the Mahalaxmi Branch at Mumbai way back in 1989. The Bank is also a

Founder Member of SWIFT in India. It pioneered the introduction of the Health Code System

in 1982, for evaluating/ rating its credit portfolio.

Presently Bank has overseas presence in 20 foreign countries spread over 5 continents – with

53 offices including 4 Subsidiaries, 4 Representative Offices and 1 Joint Venture, at key

banking and financial centres viz., Tokyo, Singapore, Hong Kong, London, Jersey, Paris and

New York.

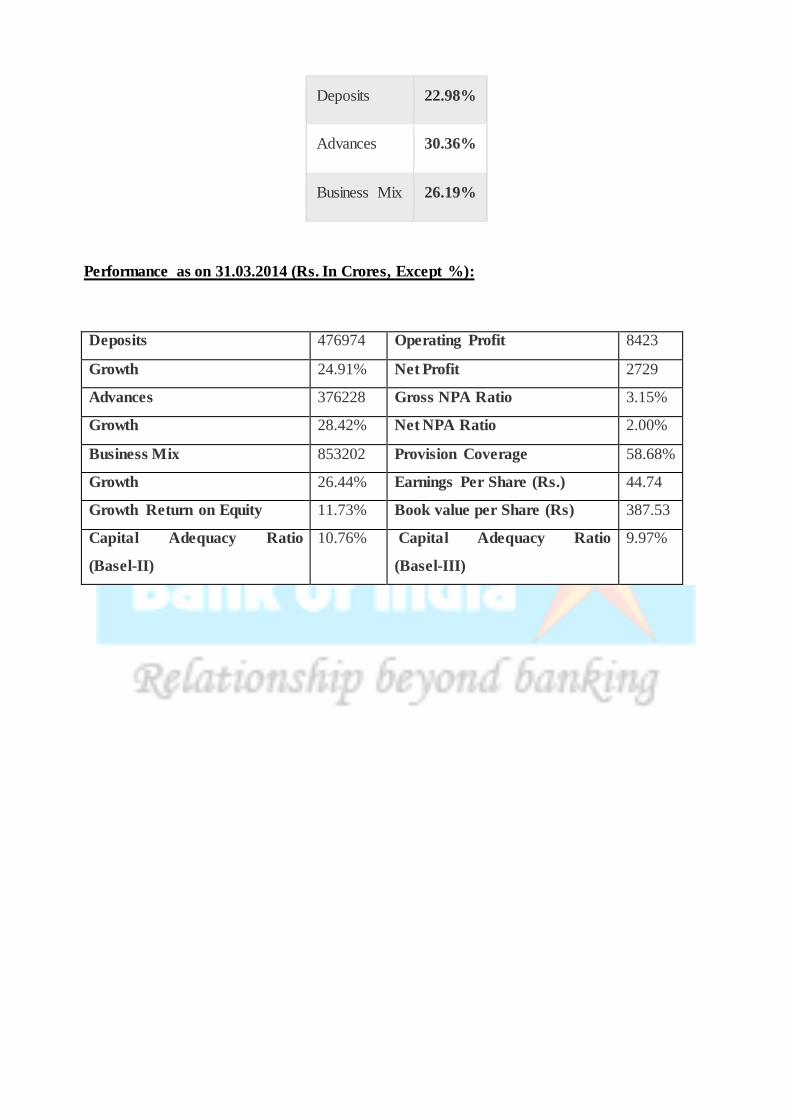

Contribution of foreign branches in the global business of the Bank as at 31.03.2014 is as

under:

Deposits 22.98%

Advances 30.36%

Business Mix 26.19%

Performance as on 31.03.2014 (Rs. In Crores, Except %):

Deposits 476974 Operating Profit 8423

Growth 24.91% Net Profit 2729

Advances 376228 Gross NPA Ratio 3.15%

Growth 28.42% Net NPA Ratio 2.00%

Business Mix 853202 Provision Coverage 58.68%

Growth 26.44% Earnings Per Share (Rs.) 44.74

Growth Return on Equity 11.73% Book value per Share (Rs) 387.53

Capital Adequacy Ratio

(Basel-II)

10.76% Capital Adequacy Ratio

(Basel-III)

9.97%

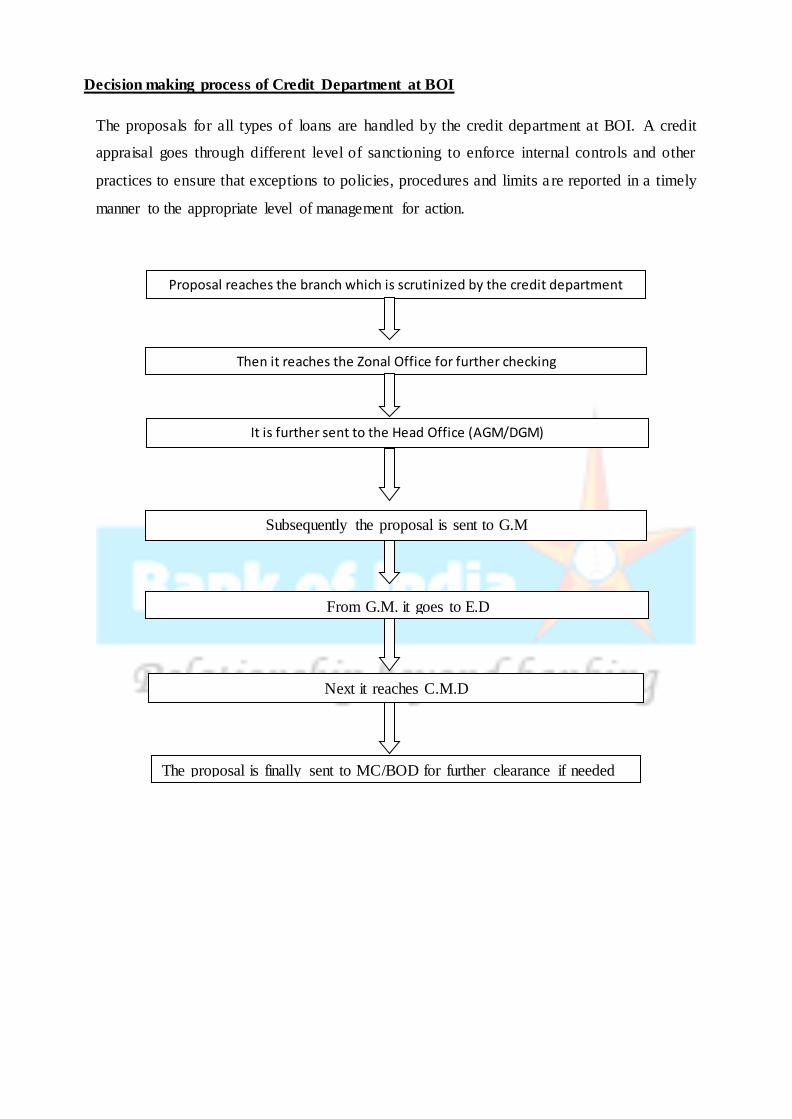

Decision making process of Credit Department at BOI

The proposals for all types of loans are handled by the credit department at BOI. A credit

appraisal goes through different level of sanctioning to enforce internal controls and other

practices to ensure that exceptions to policies, procedures and limits a re reported in a timely

manner to the appropriate level of management for action.

Proposal reaches the branch which is scrutinized by the credit department

Then it reaches the Zonal Office for further checking

It is further sent to the Head Office (AGM/DGM)

Subsequently the proposal is sent to G.M

From G.M. it goes to E.D

Next it reaches C.M.D

The proposal is finally sent to MC/BOD for further clearance if needed

AN OVERVIEW OF BANK LENDINGS

A developed country like U.S.A. sees its’ major lending activities done by Capital & Money

market, where banks provide services for merger & acquisition and other merchant banking

activities. In India lending is predominantly done by Banks. Capital Market & Money Market

are not as strong and dependable entities as yet as banks in a developing country as India and

Indian Economy. Banks have different ways of extending credit to different types of

borrowers for a wide variety of purposes.

Principles of Lending and Loan Policy:

Principles of Lending

Banks lend from the funds mobilized as deposits from public. A bank acts in the

capacity of a custodian of these funds and is responsible for its safety, security but

at the same time is also required to deliver justified and assured returns over these

borrowings. A bank looks into following aspects before lending:

Safety: the first rule of lending is to ascertain the safety of the advances made.

This means assessment of the repaying capacity of the borrower and purpose of

borrowing. It also includes assessment of contingencies and a fallback plan for the

same. This is ensured by taking adequate security (readily marketable and free of

encumbrances) by way of guarantee, collateral, charges on property, etc.

Liquidity: The second rule of lending is to ascertain how and when the repayment

of the advances made would happen and that the repayment is timely. This is to

ascertain availability of funds in future and make sure that the funds are not

locked up for a long period. This helps in maintaining balance between deposits

and advances and to meet depositor‘s obligation.

Profitability: The third rule of lending is to lend at higher rate of interest than

borrowing rate. This is called as interest spread / margin. One has to strike a

balance between profitability and safety of funds. Interest rates must be charged

competitively but at the same time spread should be adequate.

Risk diversion: An old saying says ― “never put all your eggs in one basket”. A

lender must lend to a diversified customer base. Diversification must be made in

terms of geographical locations, borrowers, industry, sector etc. It is done so as to

mitigate adverse financial effects of a business cycle, catastrophe, chain effect etc.

Loan Policy: Banks are basically a lending institution. Its major chunk of revenue

is earned from interest on advances. Each bank has its own credit policy, based on

the principles of lending, which outlines lending guidelines and establishes

operating procedures in all aspects of credit management. The po licy is drafted by

the Credit Policy Committee and is approved by the bank‘s board of directors.

The credit policy sets standards for presentation of credit proposals, financial

covenants, rating standards and benchmarks, delegation of credit approving

powers, prudential limits on large credit exposures, asset concentrations, portfolio

management, loan review mechanism, risk monitoring and evaluation, pricing of

loans, provisioning for bad debts, regulatory/ legal compliance etc. The lending

guidelines reflect the specific bank's lending strategy (both at the macro level and

individual borrower level) and have to be in conformity with RBI guidelines. The

loan policy typically lays down lending guidelines in the following areas:

Credit-deposit ratio: Banks are under an obligation to maintain certain statutory

reserves like cash reserve ratio (CRR – to be kept as cash or cash equivalents),

statutory liquidity ratio (SLR – to be kept in cash or cash equivalents and

prescribed securities), etc. These reserves are maintained for asset – liability

management (ALM) and are calculated on the basis of demand and time liabilities

(DTL). Banks may further invest in non – prescribed securities for the matter of

risk diversion. Funds left after providing for these reserves are available for

lending. The CPC decides upon the quantum of credit that can be granted by the

bank as a percentage of deposits.

Targeted portfolio mix: CPC has to strike balance between risk and return. It sets

the guiding principles in choosing preferred areas of lending and sectors to avoid.

It also takes into account government policies of lending to preferred / avoidable

sectors. The bank assesses sectors for future growth and profitability and

accordingly decides its exposure limits.

Loan pricing: Risk-return trade-off is a fundamental aspect of risk management.

Borrowers with weak financial position and, hence, placed in higher risk category

are provided credit facilities at a higher price (that is, at higher interest). The

higher the credit risk of a borrower the higher would be his cost of borrowing. To

price credit risks, bank devises appropriate systems, which usually allow

flexibility for revising the price (risk premium) due to changes in rating. In other

words, if the risk rating of a borrower deteriorates, his cost of borrowing should

rise and vice versa.

At the macro level, loan pricing for a bank is dependent upon a number of its cost

factors such as cost of raising resources, cost of administration and overheads,

cost of reserve assets like CRR and SLR, cost of maintaining capital, percentage

of bad debt, etc. Loan pricing is also dependent upon competition

Collateral security: As part of a prudent lending policy, bank usually advances

loans against some security. The loan policy provides guidelines for this. In the

case of term loans and working capital assets, bank takes as 'primary security' the

property or goods against which loans are granted. In addition to this, banks often

ask for additional security or 'collateral security' in the form of both physical and

financial assets to further bind the borrower. This reduces the risk for the bank.

Sometimes, loans are extended as 'clean loans' for which only personal guarantee

of the borrower is taken

Role of RBI:

The credit policy of a bank should be conformant with RBI guidelines; some of the important

guidelines of the RBI relating to bank credit are discussed below.

- Directed credit stipulations: The RBI lays down guidelines regarding minimum

advances to be made for priority sector advances, export credit finance, etc. These

guidelines need to be kept in mind while formulating credit policies for the Bank.

- Capital adequacy: If a bank creates assets- loans or investment-they are required

to be backed up by bank capital; the amount of capital they have to be backed up

by depends on the risk of individual assets that the bank acquires. The riskier the

asset, the larger would be the capital it has to be backed up by. This is so, because

bank capital provides a cushion against unexpected losses of banks and riskier

assets would require larger amounts of capital to act as cushion.

- Credit Exposure Limits: As a prudential measure aimed at better risk

management and avoidance of concentration of credit risks, the Reserve Ba nk has

fixed limits on bank exposure to the capital market as well as to individual and

group borrowers with reference to a bank's capital. Limits on inter-bank exposures

have also been placed. Banks are further encouraged to place internal caps on their

sector exposures, their exposure to commercial real estate and to unsecured

exposures.

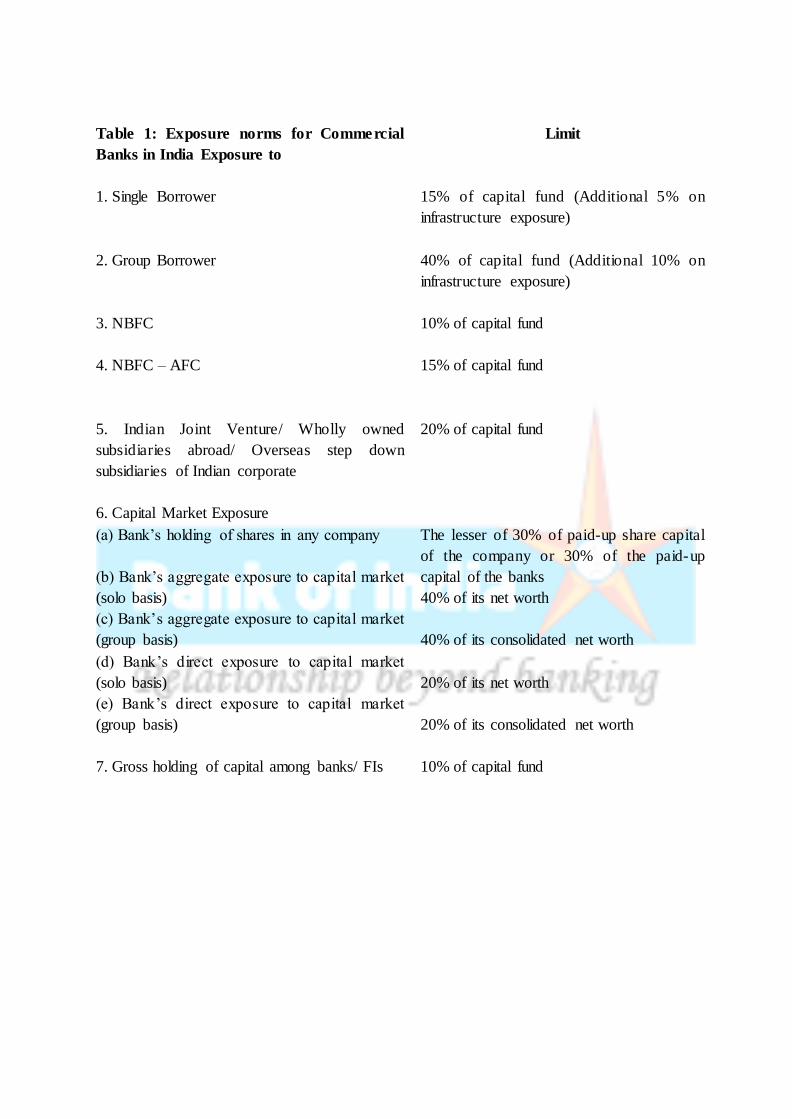

Table 1: Exposure norms for Commercial

Banks in India Exposure to

Limit

1. Single Borrower

15% of capital fund (Additional 5% on

infrastructure exposure)

2. Group Borrower

40% of capital fund (Additional 10% on

infrastructure exposure)

3. NBFC

10% of capital fund

4. NBFC – AFC

15% of capital fund

5. Indian Joint Venture/ Wholly owned

subsidiaries abroad/ Overseas step down

subsidiaries of Indian corporate

20% of capital fund

6. Capital Market Exposure

(a) Bank’s holding of shares in any company

(b) Bank’s aggregate exposure to capital market

(solo basis)

(c) Bank’s aggregate exposure to capital market

(group basis)

(d) Bank’s direct exposure to capital market

(solo basis)

(e) Bank’s direct exposure to capital market

(group basis)

The lesser of 30% of paid-up share capital

of the company or 30% of the paid-up

capital of the banks

40% of its net worth

40% of its consolidated net worth

20% of its net worth

20% of its consolidated net worth

7. Gross holding of capital among banks/ FIs 10% of capital fund

TYPES OF LENDING

Lending can be for long term tenure or short term tenure. Lending is broadly classified into

two broad categories: fund based lending and non-fund based lending.

Fund Based Lending:

This is a direct form of lending in which a loan with an actual cash outflow is given to the

borrower by the Bank. In most cases, such a loan is backed by primary and/or collateral

security. The loan can be to provide for financing capital goods and/or working capital

requirements.

Loan: -In this case, the entire amount of assistance is disbursed at one time only,

either in cash or by transfer to the company’s account. It is a single advance. The

loan may be repaid in installments, the interests will be charged on outstanding

balance.

Overdraft: - In this case, the company is allowed to withdraw in excess of the

balance standing in its Bank account. However, a fixed limit is stipulated by the

Bank beyond which the company will not be able to overdraw the account. Legally,

overdraft is a demand assistance given by the bank i.e. bank can ask for the

repayment at any point of time. However in practice, it is in the form of continuous

types of assistance due to annual renewal of the limit. Interest is payable on the

actual amount drawn and is calculated on daily product basis.

Cash Credit: - In practice, the operations in cash credit facility are similar to those

of overdraft facility except the fact that the company need not have a formal current

account. Here also a fixed limit is stipulated beyond which the company is not able

to withdraw the amount. Legally, cash credit is a demand facility, but in practice, it is

Lending Tenure

Short TermWorking Capital

Fund Based

Cash Credit

Overdraft

Non-Fund Based

Letter of Credit

Bank Guarantee

Long Term Term Loan

on continuous basis. The interests is payable on actual amount drawn and is

calculated on daily product basis. Concept of margin also plays a vital role unlike

overdraft.

Working Capital Term Loans : - To meet the working capital needs of the

company, banks may grant the working capital term loans for a period of 3 to 7

years, payable in yearly or half yearly installments.

Packing Credit: - This type of assistance may be considered by the bank to take care

of specific needs of the company when it receives some export order. Packing credit

is a facility given by the bank to enable the company to buy the goods to be exported.

If the company holds a confirmed export order placed by the overseas buyer or a

letter of credit in its favor, it can approach the bank for packing credit facility.

Non-fund Based Lending:

In this type of facility, the Bank makes no funds outlay. However, such arrangements may be

converted to fund-based advances if the client fails to fulfill the terms of his contract with the

counterparty. Such facilities are known as contingent liabilities of the bank. Facilities such as

'letters of credit' and 'guarantees' fall under the category of non-fund based credit.

The non-fund based lending in the form of letter of credit is very regularly found in the

international trade. In case the exporter and the importer are unknown to each other. Under

these circumstances, exporter is worried about getting the payment from the importer and

importer is worried as to whether he will get the goods or not. In this case, the importer

applies to his bank in his country to open a letter of credit in favor of the exporter whereby

the importer’s bank undertakes to pay the exporter or accept the bills or drafts drawn by the

exporter on the exporter fulfilling the terms and conditions specified in the letter of credit.

Letter of Credit: Letter of credit (LC) is a method of settlement of payment of a trade

transaction and is widely used to finance purchase of raw material, machinery etc. It

contains a written undertaking by the bank on behalf of the purchaser to the selle r to

make payment of a stated amount on presentation of stipulated documents and

fulfillment of all the terms and conditions incorporated therein. Letters of credit thus

offers both parties to a trade transaction a degree of security. The seller can look

forward to the issuing bank for payment instead of relying on the ability and

willingness of the buyer to pay.

Parties to a Letter of Credit:

1. Applicant/Opener: It is generally the buyer of the goods who gets the letter of credit

issued by his banker in favor of the seller. The person on whose behalf and under

whose instructions the letter of credit is issued is known as applicant/ opener of the

credit.

2. Opening bank/issuing bank: The bank issuing the letter of credit.

3. Beneficiary: The seller of goods in whose favor the letter of credit is issued.

4. Advising Bank: Notification regarding issuing of letter of credit may be directly

sent to the beneficiary by the opening bank. It is, however, customary to advise the

letter of credit through sane other bank operating at the place/country of seller. The

bank which advises the letter of credit to the beneficiary is known as advising bank.

5. Confirming Bank: A letter of credit substitutes the credit worthiness of the buyer

with that of the issuing bank. It may sometimes happen especially in import trade that

the issuing bank itself is not widely known in the exporter's country and exporter is

not prepared to rely on the L/C opened by that bank. In such cases the opening bank

may request other bank usually in the country of exporter to add its confirmation

which amounts to an additional undertaking being given by that bank to the

beneficiary. The bank adding its confirmation is known as confirming bank. The

confirming bank has the same liabilities towards the beneficiary as that of opening

bank.

6. Negotiating Bank: The bank that negotiates the documents drawn under letter of

credit and makes payment to beneficiary. The function of advising bank, confirming

bank and negotiating bank may be undertaken by a single bank only.

Letter of Credit Mechanism

Any business/industrial venture will involve purchase transactions relating to

machine/other capital goods and raw material etc., and also sale transactions relating

to its products. The customer may be an applicant for a letter of credit for his

purchases while be the beneficiary under other letter of credit for his sale transaction.

The complete mechanism of a letter of credit may be divided in three parts as under:

1. Issuing of Credit: Letter of credit is always issued by the buyer's bank (issuing

bank) at the request and on behalf and in accordance with the instructions of the

applicant. The letter of credit may either be advised directly or through some other

bank. The advising bank is responsible for transmission of credit and verifying the

authenticity of signature of issuing bank and is under no commitment to pay the

seller. The advising bank may also be required to add confirmation and in that case

will assume all the liabilities of issuing bank in relation to the beneficiary as stated

already.

2. Negotiation of Documents by beneficiary: On receipt of letter of credit, the

beneficiary shall arrange to supply the goods as per the terms of L/C and draw

necessary documents as required under L/C. The documents will then be presented to

the negotiating bank for payment/acceptance as the case may be. The negotiating

bank will make the payment to the beneficiary and obtain reimbursement from the

opening bank in terms of credit.

3. Settlement of Bills Drawn under Letter of Credit by the opener: The last step

involved in letter of credit mechanism is retirement of documents received under L/C

by the opener. On receipt of documents drawn under L/C, the opening bank is

required to closely examine the documents to ensure compliance of the terms and

conditions of credit and present the same to the opener for his scrutiny. The opener

should then make payment to the opening bank and take delivery of documents so that

delivery of goods can be obtained by him.

Types of Letter of Credit

Letter of credit may be divided in two broad categories as under:

(i) Revocable letter of credit: This may be amended or cancelled without prior

warning or notification to the beneficiary. Such letter of credit will not offer

any protection and should not be accepted as beneficiary of credit.

(ii) Irrevocable letter of credit: This cannot be amended or cancelled without the

agreement of all parties thereto. This type of letter of credit is mainly in use

and offers complete protection to the seller against subsequent development

against his interest.

Bank Guarantee: A contract of guarantee can be defined as a contract to perform the

promise, or discharge the liability of a third person in case of his default. The contract

of guarantee has three principal parties as under:

- Principal debtor: The person who has to perform or discharge the liability and for

whose default the guarantee is given.

- Principal creditor: The person to whom the guarantee for due fulfillment of contract

by principal debtor. Principal creditor is also sometimes referred to as beneficiary.

- Guarantor or Surety: The person who gives the guarantee.

Bank provides guarantee facilities to its customers who may require these facilities for

various purposes. The guarantees may broadly be divided in two categories as under:

- Financial guarantees: Guarantees to discharge financial obligations to the customers.

- Performance guarantees: Guarantees for due performance of a contract by

customers.

Let us explain with an example how guarantees work. A company takes a term loan

from Bank A and obtains a guarantee from Bank B for its loan from Bank A, for

which he pays a fee. By issuing a bank guarantee, the guarantor bank (Bank B)

undertakes to repay Bank A, if the company fails to meet its primary responsibility of

repaying Bank A.

Banks carry out a detailed analysis of borrowers' working capital requirements. Credit

limits are established in accordance with the process approved by the board of

directors. The limits on working capital facilities are primarily secured by inventories

and receivables (chargeable current assets).

OVERVIEW OF CREDIT APPRAISAL

Credit Appraisal is a process to ascertain the risks associated with the extension of the credit

facility. It is generally carried by the financial institutions, which are involved in providing

financial funding to its customers. Credit risk is a risk related to non-repayment of the credit

obtained by the customer of a bank. Thus it is necessary to appraise the credibility of the

customer in order to mitigate the credit risk. Proper evaluation of the customer is performed

this measures the financial condition and the ability of the customer to repay back the Loan in

future. Generally the credits facilities are extended against the security know as collateral.

But even though the Loans are backed by the collateral, banks are normally interested in the

actual Loan amount to be repaid along with the interest. Thus, the customer's cash flows are

ascertained to ensure the timely payment of principal and the interest.

It is the process of appraising the credit worthiness of a Loan applicant. Factors like age,

income, number of dependents, nature of employment, continuity of employment, repayment

capacity, previous Loans, credit cards, etc. are taken into account while appraising the credit

worthiness of a person. Every bank or lending institution has its own panel of officials for

this purpose.

However the 3 ‘C’ of credit are crucial & relevant to all borrowers/ lending, which must be

kept in mind, at all times.

- Character

- Capacity

- Collateral

If any one of these is missing in the equation then the lending officer must question the

viability of credit. There is no guarantee to ensure a Loan does not run into problems;

however if proper credit evaluation techniques and monitoring are implemented then

naturally the Loan loss probability / problems will be minimized, which should be the

objective of every lending Officer.

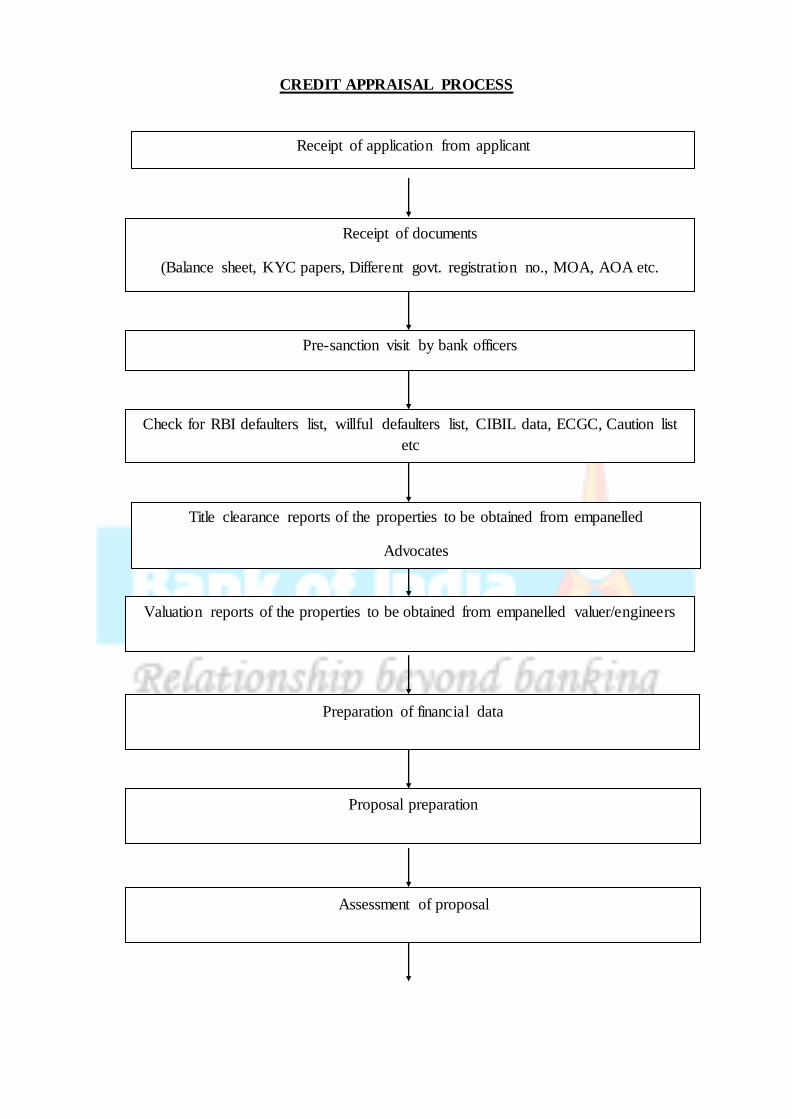

CREDIT APPRAISAL PROCESS

Receipt of application from applicant

Title clearance reports of the properties to be obtained from empanelled

Advocates

Assessment of proposal

Proposal preparation

Receipt of documents

(Balance sheet, KYC papers, Different govt. registration no., MOA, AOA etc.

Pre-sanction visit by bank officers

Preparation of financial data

Valuation reports of the properties to be obtained from empanelled valuer/engineers

Check for RBI defaulters list, willful defaulters list, CIBIL data, ECGC, Caution list

etc

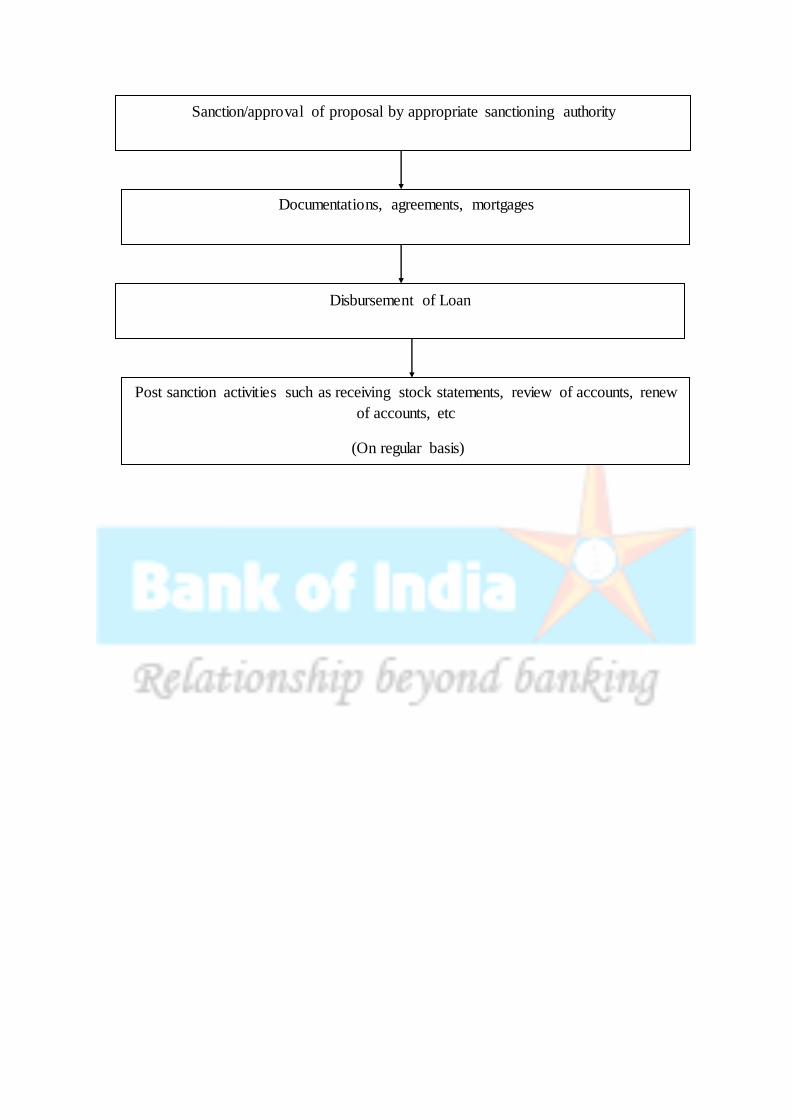

Sanction/approval of proposal by appropriate sanctioning authority

Documentations, agreements, mortgages

Disbursement of Loan

Post sanction activities such as receiving stock statements, review of accounts, renew

of accounts, etc

(On regular basis)

CREDIT APPRAISAL AT BOI

Credit Appraisal – Initial due diligence & financial analysis

The process of credit appraisal would begin with the selection of the borrower. The process

would broadly cover:

(i) Appraising the borrower/business

(ii) Appraising/assessing the credit requirement and structuring the credit delivery,

security, covenants etc. Appraisal of the borrower would include background

check and assessment of managerial, commercial, technical and financial

capability/strength, project execution/management ability, success in joint venture

for technology/ market, retention of professional talent at various levels,

management control, promoters’ shareholding etc.

Both the above aspects need to be appraised/ examined at the time of the initial entry of a

customer to the Bank as also at the time of subsequent periodic reviews. Naturally, the

appraisal would be different in respect of:

- Retail segment like personal loans for consumer durables, house etc

- Small business like loans to business enterprises

- Farming sector/agriculturists

- MSME sector

- Corporates in manufacturing, infrastructure, services, wholesale trade and other

sectors.

Background of the borrower/management

Background of the borrower needs to be done through scrutiny of antecedents, experience in

the line of business, managerial, marketing, technical competence, organizational strength,

integrity etc. Track record with us, status report from the other banks, reports in the sector

from our borrowers in similar business, RBI/CIBIL reports on defaulters/willful

defaulters/SAL of ECGC, Corporate action taken by SEBI/NSE/BSE, reports from their

vendors/dealers who may be our customers, reasonability of CMA projections, actual

performance vs estimates, frequent overdrawing, history of restructuring/OTS etc.

In case of adverse report in any of the above areas, there could be justifications/mitigations

which should be looked into. If need be the appraising officer may personally visit the other

bank for personal discussions. The gist of such oral discussion may be recorded in the file of

the borrower and brought out in the proposal. KYC guidelines as framed by RBI and adopted

by Bank are to be followed by the branches.

Commercial appraisal

The nature of the product, demand for the same, the existing and perceived competition in the

segment, ability of the proponents to withstand the same, government policies governing the

industry, etc. need to be taken into consideration. The trade practices in respect of the product

should be thoroughly understood. Branches should use the reports from ICRA/CRISIL &

Capitaline available on Stardesk.

Technical appraisal

Technical appraisal of the project needs to be carried out for industrial activity1 proposals

beyond the cut-off limits prescribed from time to time. Such appraisal may be carried out in-

house by Technical Officers working in Technical Appraisal Department/ Technical

Appraisal Cells or officers having technical expertise for the same or by an outside agency as

determined by the appropriate authority. Where technical appraisal is carried out by All India

Financial Institutions, PSU Banks/other leading banks having expertise in the area, their

report may be accepted for appraisal purposes.

Financial appraisal

Analysis of financial parameters/ratios should be done. Aspects like

i. Balance sheet strength

ii. Growth in TNW, sales, PAT etc

iii. Borrower’s ability to service the principal and interest, meet the cash flow

requirement in respect of payments under LC opened, absorb additional burden

due to escalation of raw material cost etc

iv. Position of receivables/inventory etc should be looked into.

The following parameters ratios should be computed:

i. TNW with reconciliation of change in TNW

ii. Current Ratio

iii. Total outside liabilities/equity (DER)

iv. Profit before interest, depreciation, taxes, appropriation (PBIDTA/EBIDTA)

v. Profit After Tax/Net sales

vi. Inventory + receivables/Sales ratio

vii. DSCR if the borrower enjoys any term loan with any bank/FI even if no TL is

being considered by our bank.

viii. Capital Employed

ix. PAT/Capital employed

x. Investments

xi. Segmental Revenue if applicable

CHECK POINTS FOR DUE DILIGENCE/ASSESSMENT IN CREDIT PROPOSAL

1. Articles of Incorporation - A corporate registration is the cornerstone and basis for

legitimacy, as it requires the business to rely upon its corporate name, image and

reputation.

2. Status Reports - This is useful to show that the company continues to exist and

operate as a legal entity, and has not been dissolved and/or reincorporated under

another name. Most companies that actively engage in business with serious clients

will have one that is relatively recent. Whenever new proposals are put up for

approval, status reports of the company / group needs to be obtained from their

existing bankers. Obtaining status reports is an essential step in due diligence process,

in all advance accounts.

3. Market enquiries - This serves as an important tool. Verification of the antecedents

of the borrower through discrete market enquiries could amply reveal inherent

deficiencies. Cross verification with our existing customers in the line and other

players in the line, would serve as first hand information.

4. Licenses / Certifications - Ask for a copy of licenses, permits, registrations or

certifications if they are directly related to and required for the specific work the

company must perform. If copies are not available, request the number and issuing

authority of each document.

5. Web Site Addresses - All Companies have their websites. Companies that say they

do not have a website or do not need one have to be treated with caution. Good

companies always make efforts to allow clients or partners to keep in touch with

them, receive notice of changes of office address, e-mail addresses or phone numbers,

reminders of services offered or updates on new services.

6. Resume of Managers or Key Employees - Ask for resume (also called "professional

bio") of managers / key employees of the company. This will give you some

additional leads and information to verify the company's ability to perform the work

promised and general capabilities.

7. Corporate Brochure or Company Overview - Every company should have a

professional and well-developed presentation of their business concept or services.

This evidences the level of preparation of the company, and demonstrates whether

they have sufficiently developed their capabilities. Project Reports / Information

Memoranda, are not to be taken for face value. They need to be critically examined

vis-à-vis other sources like similar businesses.

8. It should be ensured that too much dependence on consultant driven business, is

avoided by the Company. Even when consultants refer business, discussions should

be held with the promoters/CFOs.

9. ROC search – ROC search, as applicable, at the time of considering fresh advances,

needs to be done, to assess existing charge/s on company’s assets.

10. Each proposal should bear reference related to RBI/CIBIL/ECGC/ List of Defaulters /

willful Defaulter List, etc. As per existing guidelines, Branch / Zonal Office must

bring out this aspect in the proposal.

11. Pre-Sanction Inspection – Branches should note to conduct pre-sanction inspections

before submitting new proposals. Inspection reports should be prepared strictly as per

the format. Findings of the inspection should be brought out in the proposal. It should

invariably include the place of work of the entity in addition to visiting the corporate

office, meeting promoters & employees etc.

12. Critical information as envisaged in Credit policies / Circulars, are to be obtained and

scrutinized.

13. Scrutiny of statements of accounts with previous / existing bankers, to be done, to

ascertain their conduct. This is more so necessary while takeover of the facilities is

involved.

14. Risk Mitigation - Proper coverage of risk and mitigation in the proposal reflects good

understanding of the business. As per existing guidelines, Branch / Zonal Office must

bring out these aspects in the proposal.

15. Status of Litigation If the company is involved in any litigation/disputes/ arbitration,

Zone / Branch should give details in the proposal.

16. Assessment of Limits Financial parameters like DER, Current Ratio for W/C &

DSCR, DER, FACR, BEP, IRR, sensitivity analysis for Term Loan are to be properly

captured in the proposals. Proposals should not be considered without these

parameters being adequately brought out.

17. Assessment about promoter/s ability to bring in the funds envisaged, to be properly

done.

18. Risk Rating - Risk Rating Exercise for Credit Rating & Pricing has to be done as per

different Risk Scoring Modules.

19. The security which is obtained by the Bank (either as principal or as collateral) shall

be verified as to its title clearance as well as value by independent Panel Advocates/

Valuers and periodical Encumbrance Certificate shall be obtained. In this regard,

extant guidelines, is enumerated in Branch Circular from time to time are to be

meticulously observed.

Check points for Pre and Post Monitoring Norms:

PRE DISBURSEMENT:

i. Suitable monitoring of various acts by the customer/Branch officials/out-side agencies

should be done at the pre-disbursement stage. Depending upon the terms of sanction in each

case, the following actions/steps, wherever applicable, may be taken prior to disbursement:-

ii. Obtention of satisfactory credit reports from existing lenders and other service providers

such as D&B, CIBIL etc. if stipulated. Branch staff, which is processing the applications for

credit requests of new customers, should personally call on the Bank/FI with whom the

incumbent is presently enjoying facilities and discreetly enquire about the conduct and

general aspects of the account. This is in addition to obtaining status reports. The personal

visit to the operating staff of that Bank/FI may reveal more about the proposed borrower

which may not have been incorporated in the report. Wherever it is not desirable to obtain

Status Report for the fear of putting our competitor on guard, decision may be taken on the

basis of scrutiny of proponent’s statement of account for the last one year with the existing

Banker and the fact that the Sanctioning Authority has satisfied itself about the credit

worthiness of the proponents on the strength of statement of account for the last one year and

that status report is not being obtained for the fear of putting the existing banker on guard

should be recorded in the proposal.

However, in case Branch desires not to obtain ‘Status Report’ from other Bankers/Service

providers prior to disbursement then specific ‘approval’ of the higher authority viz GM

NBG and/or GM Head Office should be obtained

In such cases the Branch should obtain status report subsequently and the staff should visit

the Bank/FI immediately after disbursement to discreetly enquire about the conduct and

general aspects of the account.

iii. Adhering to Head Office guidelines for Credit Rating exercise pertaining to entry level for

new accounts.

iv. Post-sanction inspection of the unit prior to disbursement. Needless to add, pre-sanction

inspection report cannot substitute the need of pre-disbursement inspection

vi. Issuance of sanction letter and acceptance of terms, conditions and stipulations of

sanctions by the borrowers.

vii. Execution of all relevant documents, including creation of collateral security / mortgage

etc. as per terms of sanction

ix. Furnishing of Letters of guarantee by guarantors.

x. Disbursement of amounts by other participating financial agencies / Banks / Financial

Institutions etc.

Clarity in regard to draw down of amounts such as first date of disbursal and last date of

disbursal, the stages in which the monies are required to be drawn, its acceptance and

evaluation at Branch level (If these are already included in the credit proposal, the same must

be adhered to).

xii. Vetting of documents

xiii. Credit Process Audit compliance

xiv. Post Sanction Pre Disbursement approval wherever branch level sanction

xv. Keeping the duly completed/signed check list on record along with other security

documents

DURING DISBURSEMENT:

Credit delivery in loan accounts is distinct from running accounts such as Cash Credit. All

disbursements whether in loan account or in running accounts, will be related to actual /

acceptable performance of the business unit and should never lose sight of basic objective of

safety of Bank's exposure in the credit assets. The disbursements should commensurate with

the progress of the project / business activity, also taking into account the extent of margin

brought in by the promoters up to the given point of time.

The sanction of the limit is not a commitment in isolation to extend funds to the borrower

under all circumstances. It is only a financial contract to make available funds for due

performance of various business objectives and goals set out in his proposal. Bank's

disbursements depend upon due performance /compliance of/with borrower's own

commitments. Therefore, the credit delivery has to be used as an effective monitoring tool to

ensure that there are only normal and acceptable credit risks.

The following aspects wherever applicable, may be considered for monitoring:

(a) LOAN ACCOUNTS :

i. Actual Implementation vis-a-vis Project schedule.

ii. Possibility of time or cost overrun.

iii. Adequacy of arrangements to meet cost overruns.

iv. Impact of time overrun on timely cash generations of the project.

v. Verification of end-use of funds with reference to verifiable records such as invoices,

account books, registers, records, inspection of the unit etc.

vi. Certificate from Company’s Statutory Auditors on the extent of cost incurred on the

project at any given point of time, implementation progress certificate from approved

architect/contractor etc., wherever applicable.

vii. Disbursements to be made, to the extent possible, directly to the suppliers / service

providers and the element of cash withdrawals to be kept minimum.

Status report on the suppliers of machinery as per the guidelines which ensures genuineness

of supplier/transaction must be obtained.

Even while making direct payments, whenever doubt arises about the genuine nature of the

transaction, due care is to be exercised.

(b) CASH CREDIT ACCOUNTS:

i. Compliance of sanction terms / stipulations (any exception requires approval of appropriate

authority)

ii. Verification of completion of the implementation of the project/business activity and

readiness to commence commercial production.

iii. Disbursements to be made, to the extent possible, directly to the suppliers/service

providers and the element of cash withdrawals to be kept minimum.

iv. Even while making direct payments, whenever doubt arises about the genuine nature of

the transaction, due care is to be exercised.

v. Stock inspection data regarding regular movement of goods, actual sales keeping pace with

projections, not having unacceptable quality rejections in sales, not accumulating slow/

obsolete inventory, elongation of debtors beyond acceptable levels, change in credit periods

from suppliers etc.

vi. Meaningful on site/off site verification of Stock/Book Debt statements to ensure adequacy

of Drawing Power/Drawing Limit

POST DISBURSEMENT:

i. Monitoring of the actual performance of the borrowers on monthly basis by

calling for MSOD statements and comparing the same with the projected

performance figures appearing in the customer’s own CMA data submitted to

Bank, sanctioned proposal / QIS returns etc. Any substantial deviation will have to

be probed into, not waiting for submission of audited financials.

ii. Obtention of Stock/Book debts statements as per stipulation and scrutiny thereof

iii. Periodical inspections by our staff (comprehensive guidelines issued vide BC

98/16 dated 19.04.2004 and 102/96 dated 09.08.2008)

iv. Stock Audit by approved C.As as per extant policy. (Comprehensive guidelines

issued vide BC 98/61 dated 05.07.2004)

v. Timely obtention and analysis of Audited statements of Accounts.

vi. Timely review of account

vii. Conducting periodical consortium meet/ JLA meet and sharing the information

with member of consortium /JLA.

viii. Obtaining LIE report periodically and verifying the progress, wherever applicable.

Following it up & complying post disbursement conditions.

ix. Timely identification of accounts showing symptoms of strain and, wherever

considered fit, resort to prompt restructuring of the account, so that the

rehabilitation process is meaningful.

Monitoring of an account is not confined to any single office (Branches including Large

Corporate/Mid Corporate branches/Zonal Office /NBG office/Divisional Office/Head Office)

and concerted efforts will have to be made at all levels with whatever information available at

each level, to prevent any deterioration in asset quality. Under- lending or delay in lending can

be equally painful to the wellbeing/viability of the borrower’s unit and this itself can lead to

asset becoming non-performing.

CREDIT REPORT AND CREDIT RATING

The credit report is an important determinant of an individual's financial credibility. They are

used by lenders to judge a person's creditworthiness. They also help the person concerned to

narrow down on the financial problem areas.

Credit report is a document, which comprises detailed information about the credit payment

history of an applicant. It is mostly used by the lenders to determine the credit worthiness of

an applicant. The business credit reports provide information on the background of a

company. This assists one to take crucial business related decisions. People can also assess

the amount of business risk associated with a company and then decide whether they would

be comfortable in providing them with credit facilities. The degree of interest that would be

shown by investors in their company can also be gauged from the business credit reports as

they can get an idea of the conception of their customers regarding themselves. Since these

records are updated at regular intervals of time they enable people to identify the risk levels

associated with a business as well as its future. These reports also allow businesses to get

detailed information about the financial status of business partners and suppliers.

What Is A Corporate Credit Rating?

Ratings can be assigned to short-term and long-term debt obligations as well as securities,

loans, preferred stock and insurance companies. Long-term credit ratings tend to be more

indicative of a country's investment surroundings and/or a company's ability to honor its debt

responsibilities. . The ratings therefore assess an entity's ability to pay debts.

There are various organizations that perform credit rating for various business organizations.

Bank of India follows a finely defined Credit Rating Model for assessing the creditworthiness

of the applicant. The credit rating model of BOI assesses various aspects of the projects and

assigns scores against them thereby determining the risk level involved with the project.

It is divided in five sections:

1. Rating of the borrower

- Financial risk

- Management risk

2. Market condition/ Demand situation

3. Rating of the facility

4. Business consideration

5. Cash flow related parameters

1) Rating of the borrower: This part of credit rating model deals with assessing the financial

and managerial ability of the borrower. The financial ability of the firm is derived by

calculating ratios that determine the short term and long term financial position of the firm

Short term ratios include Current Ratio, determines the liquidity position of the company

over a period of one year. The current ratio is an indication of a firm's market liquidity and

ability to meet creditor's demands. It is excess of current assets over current liability. If

current liabilities exceed current assets (the current ratio is below 1), then the company may

have problems meeting its short-term obligations. If the current ratio is too high, then the

company may not be efficiently using its current assets.

According to the guidelines given to BOI the ideal level is at 1.33:1 however the acceptable

level is at 1.17:1.

However at times current ratio may not be a true indicator, the current ratio for road projects

is very high but this does not indicate that the company is not using its assets well but the

ratio is high because the activity involves more in dealing with current assets. Hence it is

important for the evaluator to understand the nature of the industry.

Long term ratio include Debt Equity Ratio is a financial ratio indicating the relative

proportion of equity and debt used to finance a company's assets. This ratio is also known as

Risk, Gearing or Leverage. A high debt equity ratio is not preferable by an investor as the

company already has acquired high amount of funds from market thereby reducing the

investor share over the securities available, increasing the risk.

It is also important for the lender bank to assess the firm’s debt paying capacity over a period.

Such capacity is derived by calculating ratio like Debt Service Coverage Ratio minimum

acceptable level is 1.50.

It is also necessary for the lender to determine the ability of the firm to achieve the projected

growth by evaluating the projected sales with actual. However such parameter remains non

applicable if the business is new.

Financial risk evaluation is only one of the parameter and not the only parameter for

determining the risk level. It is important to evaluate the Management Risk also while

evaluating the risk relating to borrower.

It is the management of the company that acts as guiding force for the firm. The key

managerial personnel should bear the capacity to bail out the company from crisis situation.

In order to remain competitive it is essential to take initiatives. Such skills are developed over

years of experience, thus for better performance it is required to have a team of well qualified

and experienced personnel.

2) Market potential / Demand Situation

A Company does not operate in isolation there are various market forces that acts in either

favorable or unfavorable manner towards its performance. Thus the rating would not give

true picture if does take market or demand situation in consideration.

The demand supply situation / market Potential plays an important role in determining the

growth level of the company like

1. Level of competition: Monopoly, Favorable, Unfavorable

2. Seasonality in demand: affected by short term seasonality, long term seasonality or

may not be affected by seasonality in demand.

3. Raw material availability

4. Location issues like proximity to market, inputs, infrastructure: Favorable, neutral,

unfavorable

5. Technology i.e. proven technology: Not to be changed in immediate future,

technology undergoes change, outdated technology.

6. Capacity utilization

3) Rating of the Facility:

The company can start functioning only after completing statutory obligations laid down by

the governing authority. Such statutory obligation involves obtaining licenses, permits for

ensuring smooth operations. Preparation and Submission of Financial Statements, Stock

statements in the standard format within the given time schedule.

4) Business Consideration:

The length of relationship with the bank enables the lender to assess the previous

performance of the account holder. A good track record acts in the favor of the applicant,

however an under-performance make the lender more vigilant.

The income value to the bank is also given due consideration.

Thus Credit Rating of the Business takes into consideration various aspects that have direct or

indirect effect on the performance of the business.

After evaluating the risk level involved the lender bank decides on lending interest rate.

In BOI they are categorized in 9 segments:

1. Lowest Risk CR-1

2. Low Risk CR-2

3. Medium Risk CR- 3

4. Moderate/ Satisfactory Risk CR- 4

5. Fair Risk CR- 5

6. High Risk CR- 6

7. Higher Risk CR- 7

8. Highest risk CR- 8

9. NPA CR- 9

In BOI, a business receiving Credit Rating above level 6 are not considered good from point

of investment and thus are avoided.

CHAPTER THREE

CASE STUDIES

(Note: The name and details of the persons in the cases herein are changed to comply with

the bank’s rules and regulations for non-disclosure of internal information.)

CASE – I

The case is about personal loan product from BOI. Ajit Sahoo needed a loan of Rs.75, 000 for

his father’s emergency surgery and thus he approached the BOI’s CIC branch in Rasulgarh.

ABOUT THE PRODUCT:

Product: BOI Star Suvidha (Personal Loan Scheme)

Eligibility: Salaried employees, professionals, individuals with high net worth

Type of advance: Demand/Term loan/Overdraft

Name of the applicant: Mr. Ajit Sahoo

Occupation: Maintenance Engineer

Salary: Rs. 1, 20, 000 per annum

Loan applied: Rs. 75, 000

Purpose: Father’s surgery

Tenure: 24 months

Rate of interest: 15.20%

PRE-SANCTION ACTIVITIES:

1. Meeting the client and discuss his/her requirements

2. Collect application form and KYC documents

3. Meeting the guarantor and collect details about income proof and net value assessment

4. Initial De-dupe check is done to check the credit reporting of the client whether he holds

any over-dues etc. The bank also checks the client in RBI defaulter list.

5. Internal verification is done by the bank which enables it to make sure that the client is

not forging with the financials of the company.

ASSESSMENTS FOR SANCTION:

ASSESSMENT I:

Net monthly income: Rs. 10,000

10 times of Net monthly income: Rs 1, 00, 000

Eligible amount under (I): Rs. 1, 00, 000 [A]

ASSESSMENT II:

Cost of project: Rs. 75, 000

Less margin: Nil

Eligible amount (II): Rs. 75, 000 [B]

ASSESSMENT III:

Gross monthly income: Rs. 10, 000

Statutory deductions: Rs. 1, 200

Net monthly income: Rs. 8, 800

Proposed loan amount: Rs. 75, 000

EMI: 3, 643.63

% of Net take home to GMI: 58.59% (satisfies bank regulations)

Loan amount requested: Rs. 75, 000 [C]

ASSESSMENT IV:

Maximum loan amount permissible under the scheme : Rs. 1, 00, 000 [D]

After all the assessments, the least amount among A, B, C and D is recommended by the

appraisal committee for sanctioning.

In this case Rs. 75, 000 is the least among all the assessments. Thus, Mr. Sahoo’s request for

a loan of Rs. 75, 000 was sanctioned.

POST-SANCTION ACTIVITIES:

1. Bank acquired documentary proof and declaration by the customer to ensure genuine

utilization of the funds.

2. In case of clean advances, documentary proof might not be required but purpose-wise

break-up of the fund utilization must be collected.

3. To ensure timely repayment of the EMI post-dated cheques or ECS mandate should

be acquired from the customer.

DOCUMENTS PROVIDED BY THE APPLICANT:

1. KYC related documents

2. Residential proof documents such as Ration card, telephone bill, electricity bill, rent

receipt, certificate from employer with signature verification

3. Passport size photographs of both applicant and guarantor to be collected and verified

by bank officials

4. Customer identification can be done through PAN card, Driving license, Photo

identity proof issued by employer

5. Identity needs to be verified by visiting the applicants residence and workplace

CASE II

The following case is about BOI’s automobile loan. My guide handed me the file of a fresh

case of the same. Mrs. Kavita Sharma (name changed), who owns a petrol pump in

Bhubaneswar applied for a loan of Rs. 4, 60, 000 for purchasing a new car.

ABOUT THE PRODUCT

Product: Star Vehicle Loan

Eligibility: Salaried employees, Professionals & self employed businessmen, HNI, NRI with

Indian joint borrowers, Senior citizens, Pensioners, Farmers, Companies, Partnership firms

and other corporate bodies

Age: Not to exceed 65 years at the time of availing the loan

Type: Demand loan/Term loan

Quantum of advance: For individuals : Rs. 25 lakhs for Indian make vehicles

Rs. 75 lakhs for imported vehicles

For NRI: Rs. 25 lakhs for any make

For companies/corporate entities: Rs. 100 lakhs

Name of the applicant: Mrs. Kavita Sharma

Occupation: Business

Nature of business: Petrol pump

Gross income: Rs. 14, 00, 000 per annum

Loan applied: Rs. 4, 60, 000

Tenure: 3 years

Rate of interest: 12% per annum

PRE-SANCTION ACTIVITIES:

1. Meeting the client and discuss his/her requirements

2. Collect application form and KYC documents

3. Collect installment letter.

4. Income tax returns/salary particulars/balance sheets to be collected

5. Initial De-dupe check is done to check the credit reporting of the client whether he holds

any over-dues etc. The bank also checks the client in RBI defaulter list.

6. Internal verification is done by the bank which enables it to make sure that the client is

not forging with the financials of the company.

7. Deviation check: The bank after checking the financial soundness of the company goes

for the verification of the deviation check of policy compliance, if any in case of major

deviations the case is presented in front of the zonal credit committee, their decision

stands the final verdict on the approval f the case.

8. The bank undertakes a complete check of financials as mentioned in the requirements,

these audited financials are put in ‘Finacle’ software of the bank and then projections

are made on the basis of financials and then various profitability ratios are analyzed and

the financial soundness of the company is analyzed. The financial viability of the

company is checked on various parameters as mentioned.

9. Hypothecation of assets purchased with bank finance & charge to be registered with the

RTO and registered as personal vehicles.

10. Comprehensive insurance of the vehicle with Bank clause.

ASSESSMENTS FOR SANCTION:

ASSESSMENT I:

Gross average annual income: Rs. 14, 00, 000

2 times of gross average annual income: Rs. 28, 00, 000

Eligible amount under (I): Rs. 28, 00, 000 [A]

ASSESSMENT II:

Cost of the vehicle: Rs. 5, 32, 630

Less margin (10%): Rs. 53, 263

Eligible amount: Rs. 4, 79, 367 [B]

ASSESSMENT III:

Gross monthly income: Rs. 1, 16, 667

Statutory deductions: Rs. 12, 890

Net monthly income: Rs.1, 03, 777

% of Net take home to Gross income : 89.4% (satisfied)

Loan amount requested: Rs. 4, 60, 000 [C]

ASSESSMENT IV:

Maximum loan amount under the scheme : Rs. 25, 00, 000 [D]

Least amount among A, B, C and D is then recommended by the CAC.

In this case, Mrs. Sharma was sanctioned a loan of Rs. 4, 60, 000 after all assessments.

POST-SANCTION ACTIVITIES:

1. Check the actual purchase of the automobile

2. Collection of hypothecation documents from the customer along with insurance

papers

3. In case of clean advances, documentary proof might not be required but purpose-wise

break-up of the fund utilization must be collected.

4. To ensure timely repayment of the EMI post-dated cheques or ECS mandate should

be acquired from the customer.

5. To prevent frauds, disbursement to the funds should be done to the vendor/auto dealer

through NEFT/RTGS to ensure that the account genuinely belongs to the dealer.

6. Annual review of accounts to be done by the bank

DOCUMENTATION:

1. Application-cum-proposal

2. Composite hypothecation agreement for charge on the asset

3. DP note and installment letter

4. Declaration and composite agreement

5. Statement of assets and liabilities of the borrower

6. Bank’s charge to be registered with RTO and a copy of the RC Book with Bank’s

charge noted thereon to be kept with documents

7. Creation of charge on collateral security if proposed/stipulated

8. IT returns/salary particulars/Balance sheets etc

9. Sanction letter – duly acknowledged

CASE-III

The following case is an education loan case of Mr. Subhasis Mohanty S/O Mr. Sukanta

Mohanty who wishes to avail a loan of Rs. 3, 00, 000 from the bank for admission into an

Engineering course.

ABOUT THE PRODUCT:

Product: BOI Star Education Loan Scheme

Eligibility: Graduation courses by recognized universities; PG courses approved by AICTE

or affiliated by UGC; Courses by national institutes like IIT, IIM, NIFT etc.

Parties: Joint borrower should normally be parents/guardian; Husband in case of married

Name of the applicants: Mr. Subhasis Mohanty/Mr. Sukanta Mohanty

Occupation of joint borrower: Auto rickshaw driver

Loan applied: Rs. 3, 00, 000

PRE-SANCTION ACTIVITIES:

1. KYC formalities should be completed

2. Checking of student’s academic documents

3. Verification of RBI defaulter’s list (joint borrower)

4. Verification of PAN

5. Admission letter from the institute

6. Evaluation of future income prospect of the student along with parent’s repayment

capacity.

ASSESSMENT:

1. Total course fee quoted by the institute : Rs. 4, 60, 000

2. Loan applied: Rs. 3, 00, 000

3. Balance amount to be borne by the joint borrower.

4. Joint borrower’s income: Rs. 1, 80, 000 per annum

5. Net worth: Rs. 8, 00, 000 (Jewelry & Land)

6. As the loan applied is below Rs. 4, 00, 000 thus no margin requirement is needed

POST-SANCTION ACTIVITIES:

1. Communication with the institute regarding the applicant’s selection and course fee

structure

2. Communicate with the institute and request for any kind of information related to

cancellation of admission.

3. No application for educational loan should be rejected without concurrence of the

next higher authority.

4. Loan must be disbursed in stages as per the requirement/demand directly to the

institution to the extent possible.

CASE-IV

Mr. Jagdish Chandra Barik is a customer of the bank who holds a current account with the

branch. He owns a cement store nearby and approached the bank for a loan of Rs. 4, 00, 000

as he wanted to expand his business.

PRE-SANCTION ACTIVITIES:

1. KYC formalities

2. Scrutiny of bank accounts

3. Family background, social reputation, duration in the business

4. Checking RBI’s willful defaulters’ list, Special Approval List (SAL) of ECGC,

CIBIL report.

5. The acceptability of the product, its market demand/supply position, market

competition, market arrangement etc. has to be checked

6. Techno-economic appraisal of the unit to be carried out as per the guidelines by

Technical Appraisal Department (TAD) of BOI.

7. Visit to the store and residence of the applicant

8. Checking store rent agreement, residence proof etc.

9. Checking of documents

ASSESSMENTS:

1. Working capital assessment:

As this unit’s WC requirement is below Rs.5 crores, the bank adopts Turnover

method for assessment as per Nayak Committee Recommendations. Under this

method the WC is arrived @ 20% of the projected turnover based on the

assumption of a three month operating cycle.

2. Financial ratios:

- Debt equity ratio: Mr. Barik’s business’ D/E ratio stood at 1.7:1 which was

considered as a very strong one by the bank.

- Current ratio: His current ration was 1.5:1 as he does business on a credit basis

more often and received the money once in a month from the customer.

- Debt Service Coverage Ratio: He had a fair DSCR ratio of 1.65:1 which implied

that he generated enough Net operating income to pay off his debts.

As all factors were satisfactory, Mr. Barik’s application was passed.

POST-SANCTION ACTIVITIES:

1. Monitoring the accounts on a regular basis

2. Visit to the store for checking of stock

3. Acquire monthly stock statement as well as receivables account

4. Balance sheet evaluation

5. Collection of repayment should be maintained

6. Prevent account form being sub-standard

7. Ensure utilization of funds for genuine purpose

CHAPTER FOUR

FINDINGS

- Credit appraisal is done to check the commercial, financial & technical viability of the

project proposed and its funding pattern & further checks the primary or collateral

security cover available for the recovery of such funds.

- Credit is core activity of the banks and important source of their earnings which go to

pay interest to depositors, salaries to employees and dividend to shareholders.

- Credit and risk go hand in hand.

- In the business world risk arises out of:-

Deficiencies /lapses on the part of the management

Uncertainties in the business environment

Uncertainties in the industrial environment

Weakness in the financial position

- The loan policy of BOI contains various norms for sanction of different types of

loans.

- For each type of loan, there are different norms as per the guidelines of RBI.

- The assessment of financial risk involves appraisal of the financial strength of the

borrower based on performance & financial indicators

- After studying a few cases, I found that in some cases, loan is sanctioned due to

strong financial parameters

CONCLUSIONS:

- The requirement of credit is ever increasing.

- In most of the cases, hypothecation and/or mortgage are used to create securities for

the banks.

- Every bank has its own internal credit rating procedure to rate the clients (Borrowers).

- After doing the assessment of the financial indicators it is up to the judgment of the

top management of the bank to sanction such loan. The very decision could be against

the assessment result.

- If the company is with bank from inception stage then they are given preference, as

credible and loyal party over their financial indicators.

RECOMMENDATIONS:

- Closely monitoring and inspecting the activities and stocks of the borrowers from

time to time can avoid the misuse of advances.

- The bank must further secure itself by holding a second charge on all the fixed assets

of the borrower.

- The time period taken by the banks to sanction the limits should be significantly

reduced to allow the borrowers to make use of the credit when the need is most felt.

- There should be a standard rating process to remove the subjectivity and different

perceptions of the rater (person who does credit rating process for a borrower

company). It will remove the human biasness in the process.

- Personal guarantee does not give any physical asset to the bank. It is for the moral

binding on the part of the borrower. Hence, bank should prefer to use this type of

guarantee as this will reduce the default rate on the part of borrower.

- Faster dispersion of credit is of paramount importance. A proposal has to pass through

different channels which lead to delay in the dispersal of credit. There is a need of

drastic reduction in these channels for faster decision making. This will curtail

avoidable delays, improved efficiency besides reducing appraisal time as well as cost.

BIBLIOGRAPHY:

Websites:

www.rbi.org.in

www.wikipedia.com

www.investopedia.com

www.bankofindia.co.in

www.indianbankassociation.com

Books referred:

- I.M. Pandey - Financial Management - Vikas Publishing House Pvt. Ltd.

- M.Y. Khan and P.K. Jain - Financial Management - Vikas Publishing house ltd.

- Credit and Banking - K. C. Nanda (e-Book)

Bank of India journals:

- BOI Credit Policy-2014 (Revised) e-book

- BOI individual loan policy documents

- Customer loan files from bank’s records