Embed Size (px)

Citation preview

Credit-Linked Notes

Nick Johal

Thursday 4th June 2015

Agenda

Investing in Credit for DFMs – issues and challenges

What are the benefits of taking a synthetic credit exposure?

What are the risks?

Questions & Appendix

2

Investing in Credit – Issues DFMs face

Prospectus Directive

Duration

Liquidity

Supply

Retail Bonds

Absolute Return/Strategic Bond Funds

3

Tailwinds for Credit

Demographics

Annuities changes and NISA

Benign inflation environment

Japanification of Europe

Technicals

4

What are the benefits of taking a synthetic credit

exposure?

5

Credit Linked Note (CLN)

6

A credit linked note (CLN) is a form of funded credit derivative. It is structured as a security with an embedded

credit default swap allowing the issuer to transfer a specific credit risk to credit investors.

Synthetically, the risk profile is similar to being ‘long’ the reference entity.

On the Issue date, the investor buys the CLN at par value. As a note holder, he is entitled to receive the coupons

linked to the credit risk of the underlying.

At maturity;

If no Credit Event has occurred since inception, the Notes are redeemed at par value on the maturity date.

If a Credit Event has occurred since inception, the Notes are redeemed by paying the Recovery Value to the

note holder. The investor bears a loss of {(1-R)*N]. In a worst case scenario, investors could lose their entire

investment.

Various iterations are possible e.g.

Single name CLN – The note is issued with protection sold on one reference entity

Basket CLN – The note is issued with protection sold on a basket of defined reference entities.

First-To-Default baskets

Credit Linked Note (CLN) – simple cashflows

7

Investor Bank CDS Market

Treasury desk

100

CLN

CDS

Spread

100 Funding

Ref Entity

Ref Entity

Transparent and easy to price

8

CLN coupon = CDS spread + Swap rate + funding - cost

*priced 18/11/2014

SKYLN 8y CLN Coll

8y £ Swap rate (IRSB) 2.00

CDS Spread (CDX/CDSW) 1.00

Funding 0.05

Cost -0.10

CLN coupon (%) 2.95

Liquid, Flexible, Access

9

Credit

Duration

Denomination

Coupon Type

Currency

Priced at Par

Positive Basis

Costs vs Funds

Curves

CDS Liquidity

QCB

Economic BenefitFlexibilityAccess

Supply no longer an issue

10

Format Debt Instrument

Currency GBP

Issuer SG Issuer (Secured)

Settlement / Recovery American Cash settlement / Market Recovery**

Collateral Any mixture of Gilts, Investment Grade Bonds or FTSE 100 Stocks*

Payment Frequency Semi-Annual (30/360)

Maturity 10/04/2022 Capital Protection Full capital at risk

*If stocks posted an extra 10% haircut applied **As determined by the ISDA process

Reference Entity Coupon pa S&P Moody's Fitch Reference Entity Coupon pa S&P Moody's Fitch

Pfizer Inc 2.02% AA A1 A+ BHP Billiton Ltd 2.45% A+ A1 A+

Anheuser-Busch InBev NV 2.08% A A2 A Telefonica SA 2.45% BBB Baa2 BBB+

AstraZeneca PLC 2.10% AA- A2 A+ UPM-Kymmene OYJ 2.51% BB+ Ba1 nr

Munich Re 2.10% nr Aa3 AA- SSE PLC 2.52% A- A3 A-

Dixons Retail PLC 2.16% nr nr nr UniCredit SpA 2.60% BBB- Baa2 BBB+

British American Tobacco PLC 2.17% A- A3 A- Severn Trent PLC 2.61% BBB- Baa1 nr

BT Group PLC 2.20% BBB nr BBB Tate & Lyle PLC 2.61% BBB Baa2 nr

Next PLC 2.22% BBB Baa2 nr Rio Tinto PLC 2.62% A- A3 A-

Lloyds Banking Group PLC 2.24% BBB A2 A ITV PLC 2.73% BBB- Baa3 nr

National Grid PLC 2.24% A- Baa1 BBB Marks & Spencer Group PLC 2.77% BBB- nr BBB-

Barclays PLC 2.25% BBB A3 A Firstgroup PLC 2.82% BBB- nr BBB-

HSBC Holdings PLC 2.25% A Aa3 AA- United Utilities Group PLC 2.82% nr nr nr

Rentokil Initial PLC 2.34% BBB nr nr Jaguar Land Rover Automotive 2.88% BB Ba2 BB-

Royal Bank of Scotland Group P 2.34% BBB- Baa2 A British Airways PLC 2.93% BB Ba3 nr

Sky PLC 2.35% BBB Baa2 BBB- Nokia OYJ 2.93% BB Ba2 BB

Imperial Tobacco Group PLC 2.35% BBB Baa3 BBB Safeway Inc 2.95% B B2 nr

Legal & General Group PLC 2.36% A A3 A J Sainsbury PLC 3.04% nr nr nr

BP PLC 2.37% A A2 A Peugeot SA 3.20% B+ Ba3 B+

Prudential PLC 2.40% A+ A2 A+ Fiat SpA 3.30% nr nr BB-

Standard Chartered PLC 2.41% A- A2 AA- Tesco PLC 3.34% BB+ Ba1 BBB-

Vodafone Group PLC 2.41% A- Baa1 BBB+ Glencore PLC 3.38% BBB nr nr

Lafarge SA 2.42% BB+ Ba1 BB+ Anglo American PLC 3.47% BBB Baa2 BBB

Enel SpA 2.43% BBB Baa2 BBB+ Rallye SA 4.09% nr nr nr

Royal & Sun Alliance Insurance 2.43% A A2 A- Ladbrokes PLC 4.13% BB Ba2 BB

Renault SA 2.44% BB+ Ba1 BBB- ArcelorMittal 4.25% BB Ba1 BB+

(CL01) 10y MKS fixed-floating CLN

11

Issuer SG Issuer

Currency GBP

Maturity 10y

Issue Price 100%

Coupon s/a

Recovery Market

Settlement American

3.8% pa years 1 & 2

6m£L + 125bps thereafter,

paid UTD

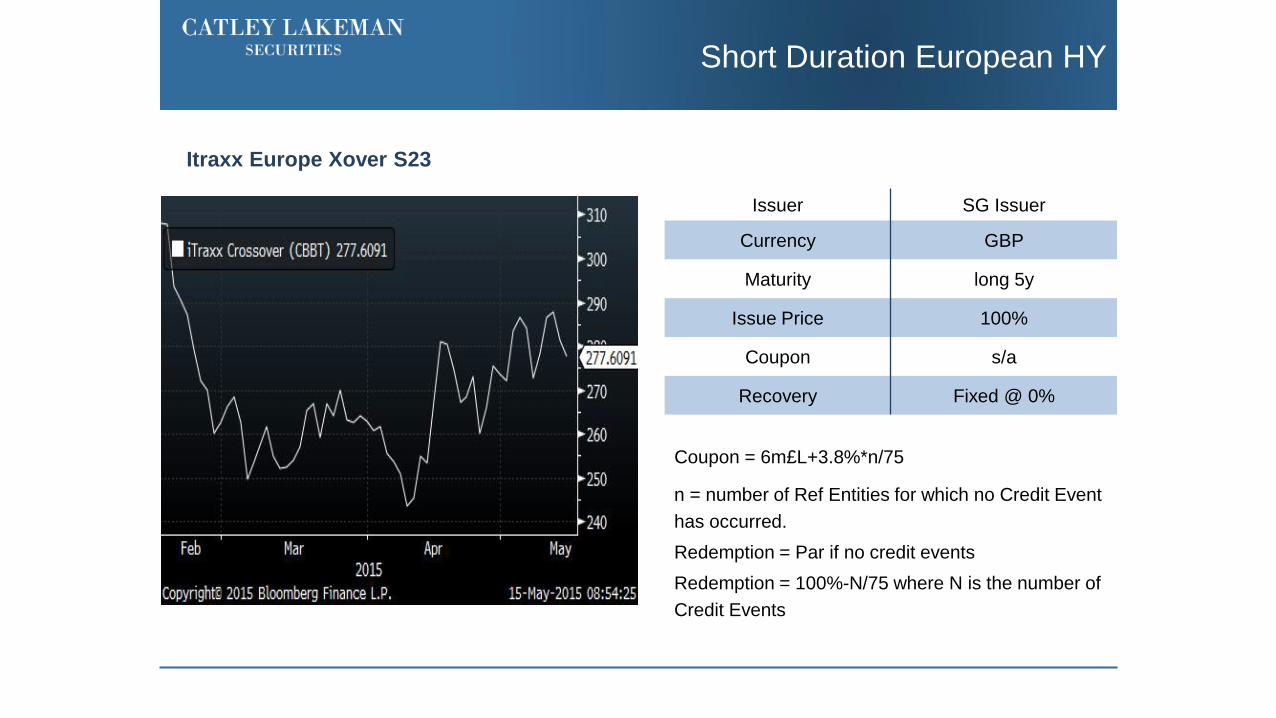

Short Duration European HY

12

Itraxx Europe Xover S23

Issuer SG Issuer

Currency GBP

Maturity long 5y

Issue Price 100%

Coupon s/a

Recovery Fixed @ 0%

Coupon = 6m£L+3.8%*n/75

n = number of Ref Entities for which no Credit Event

has occurred.

Redemption = Par if no credit events

Redemption = 100%-N/75 where N is the number of

Credit Events

What are the risks?

13

Risks & Mitigants

14

MTM/Basis risk

Issuer risk

Liquidity

Transparency

Quanto

Collateral (for secured issues)

Questions & Appendix

15

Credit Derivatives - CDS basics

16

Can be Cash or physically settled. If physically settled, additional complexity of CTD bond.

CDS – Credit Event

17

The Credit Risk of a Reference Entity (corporate or government) can be thought of as the risk that it

will experience a Credit Event over a predefined time horizon.

Definition of a Credit Event

1. Bankruptcy

2. Failure to pay

3. Restructuring (not applicable to US entities)

4. Repudiation & Moratorium (only for Sovereign entities)

The definition of a Credit Event is standardised across all counterparties in the credit market as per

the terms defined by International Swaps and Derivatives Association (ISDA)

Credit Indices

18

Offer Liquidity, Tradability and Transparency

Index components are selected by the Index sponsor based on specific criteria: liquidity, trading

volumes, rating, etc. The rolls occur every six months for standardised contracts.

iTraxx Main Europe 125 European IG corporates

iTraxx Xover (Europe) 75 most liquid sub IG European names

CDX North America 125 North American IG corporates

This is a marketing communication and has not been prepared in accordance with legal requirements designed to promote

independence of investment research and is not subject to any prohibition of dealing ahead of the dissemination of investment

research.

The information in this document is derived from sources believed to be reliable but which have not been independently verified. Any

prices included within this communication are for indicative purposes only. Catley Lakeman Securities makes no guarantee of its

accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor is it liable for damages

arising out of any person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary

data. The opinions in this document constitute the present judgment of Catley Lakeman Securities, which is subject to change

without notice.

This document is neither an offer to sell, purchase or subscribe for any investment nor a solicitation of such an offer. This document

is intended for the use of institutional and professional customers and is not intended for the use of private customers. This document

is not intended for distribution in the United States of America or to US persons. This document is intended to be distributed in its

entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any

recipient.

Catley Lakeman Securities is regulated by the Financial Conduct Authority. Firm FSA Reference No. 484826. Catley Lakeman

Securities is the trading name of Catley Lakeman LLP. Registered Office: One Eleven Edmund Street, Birmingham. B3 2HJ.

Registration Number: OC336585

DISCLAIMER

19

![D1.1 NEMESIS social innovation learning framework]€¦ · (HealthApp), Kostapanos Miliaresis, (Ethelon), Melina Taprantzi, (Wise Greece), Esther García Garaluz (ENESO), Angela Catley,](https://img.pdfslide.net/doc/110x75/606603227e5d70019917e6a9/d11-nemesis-social-innovation-learning-framework-healthapp-kostapanos-miliaresis.jpg)