Embed Size (px)

Citation preview

Credit Scoring

Beyond the Numbers

MASFAA Conference 2006

Presenter

Sean Kiley Vice President of Operations for Key Education Resources

Goals of Presentation

Improve your understanding of credit scoring

Historical perspective Calculation Types Usage

Demonstrate validity of credit score utilization

Increase awareness for the need to manage your credit

Provide resources to manage your credit

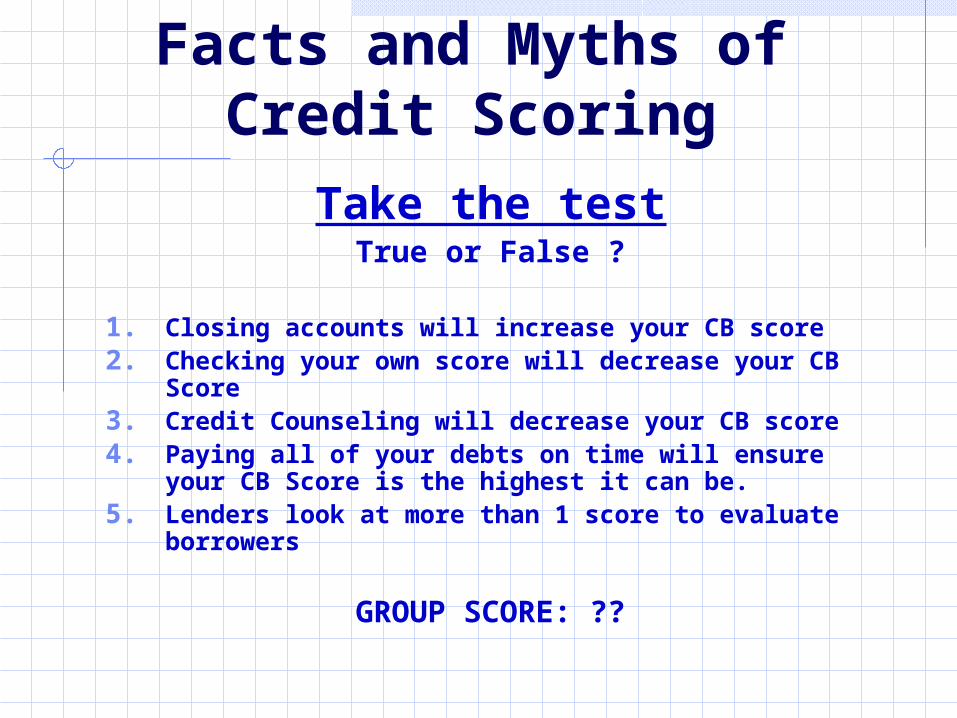

Facts and Myths of Credit Scoring

Take the testTrue or False ?

1. Closing accounts will increase your CB score2. Checking your own score will decrease your CB

Score3. Credit Counseling will decrease your CB score4. Paying all of your debts on time will ensure

your CB Score is the highest it can be. 5. Lenders look at more than 1 score to evaluate

borrowers

GROUP SCORE: ??

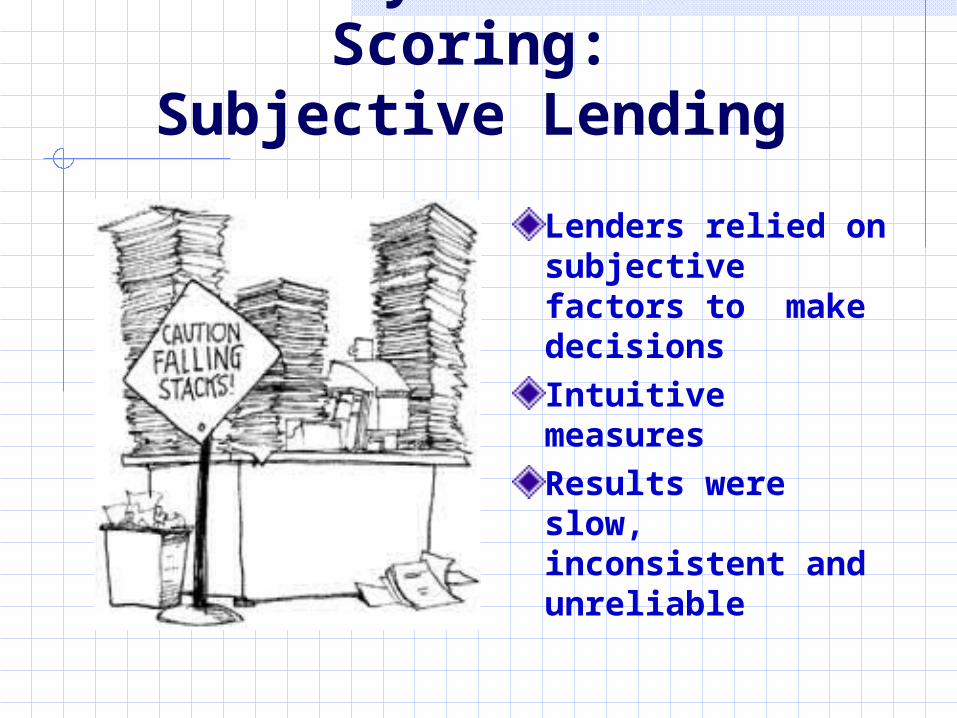

History of Credit Scoring:

Subjective Lending

Lenders relied on subjective factors to make decisionsIntuitive measuresResults were slow, inconsistent and unreliable

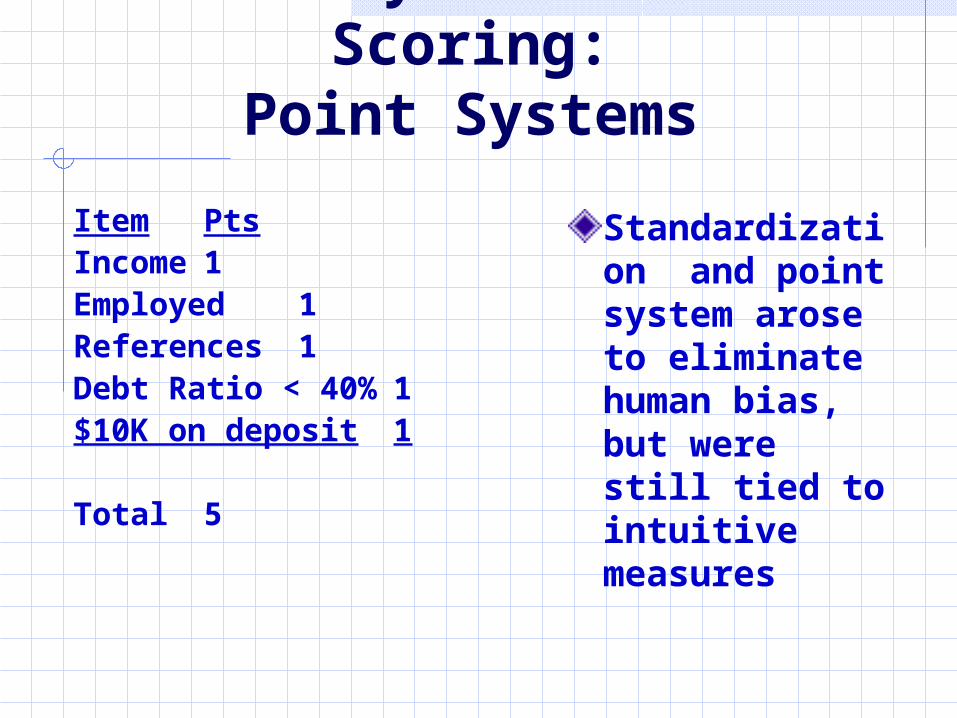

History of Credit Scoring:

Point Systems

ItemPts

Income 1Employed 1References 1Debt Ratio < 40% 1$10K on deposit 1

Total 5

Standardization and point system arose to eliminate human bias, but were still tied to intuitive measures

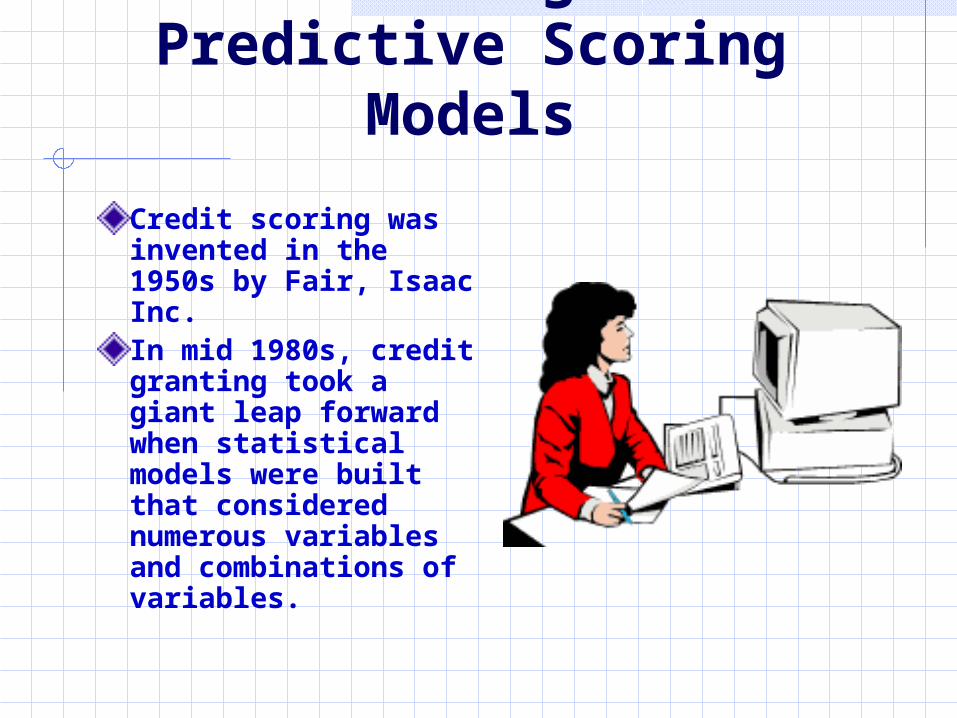

History of Credit Scoring:

Predictive Scoring Models

Credit scoring was invented in the 1950s by Fair, Isaac Inc.In mid 1980s, credit granting took a giant leap forward when statistical models were built that considered numerous variables and combinations of variables.

What Is Credit Scoring ?

Credit Scoring is a system used to facilitate decision making.Method of converting large amounts of difficult to compare data into a single point score that facilitates comparisonProcess of analyzing past performance trends to predict future performance

How Is a Credit Scoring Model Developed

Analysis of a large set of consumers (>= 1 Million)Identification of common variables that define behaviorStatistical models are then built that assign weights to each variableAdding all variables combines to make an individual score

Types of Credit Scoring

Classic FICO Equifax Bankruptcy Navigator IndexExperian: Scorex PlusNextGen FICOIndustry Specific Risk Models (auto, credit card)Custom credit scoringVantage

Alternative Credit Scoring

MarketMax (Equifax)Crossview (Experian)

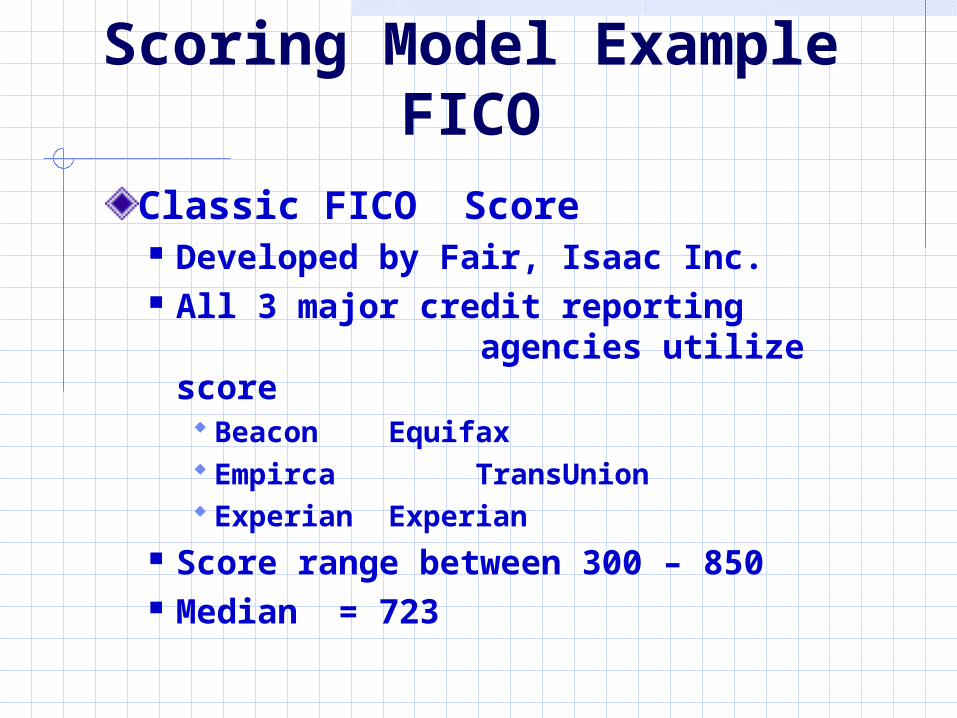

Scoring Model ExampleFICO

Classic FICO Score Developed by Fair, Isaac Inc. All 3 major credit reporting

agencies utilize score Beacon EquifaxEmpirca TransUnionExperian Experian

Score range between 300 – 850 Median = 723

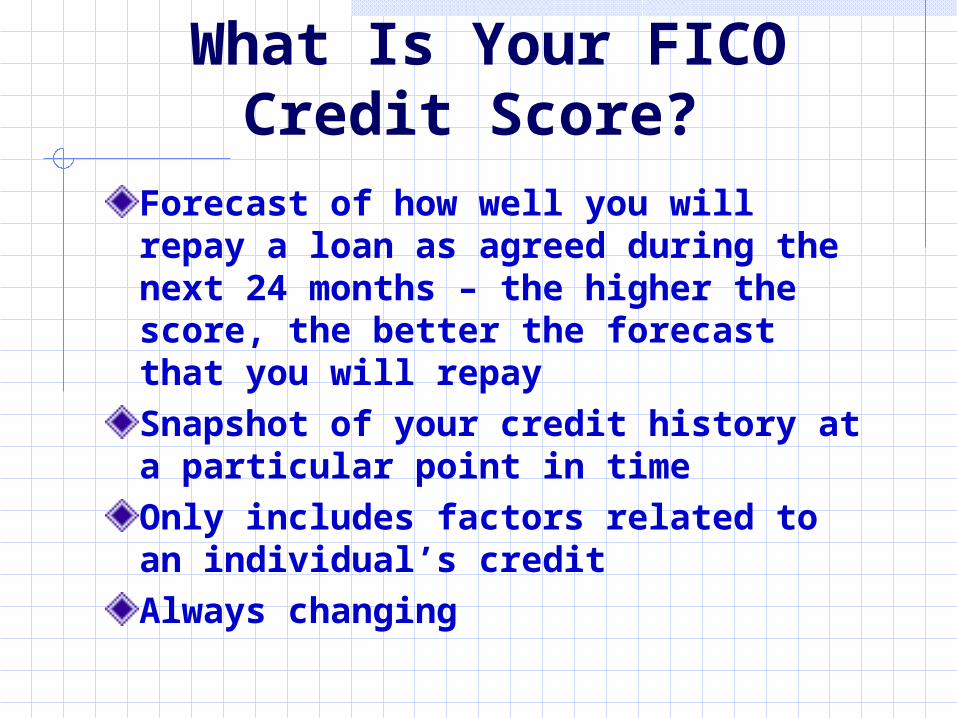

What Is Your FICO Credit Score?

Forecast of how well you will repay a loan as agreed during the next 24 months – the higher the score, the better the forecast that you will repaySnapshot of your credit history at a particular point in timeOnly includes factors related to an individual’s creditAlways changing

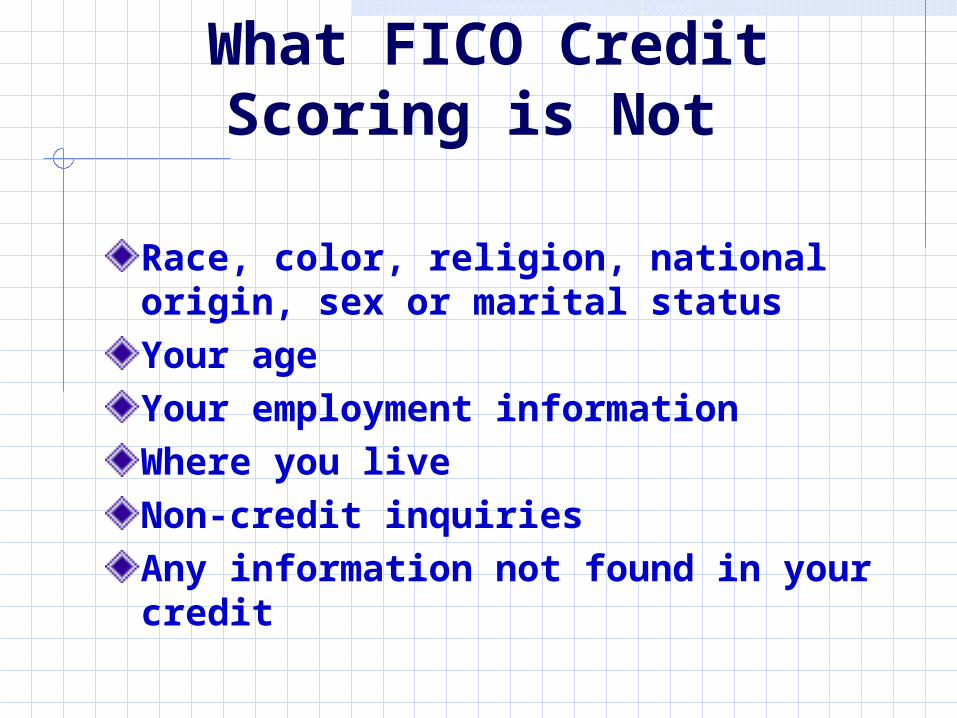

What FICO Credit Scoring is Not

Race, color, religion, national origin, sex or marital statusYour ageYour employment informationWhere you liveNon-credit inquiriesAny information not found in your credit

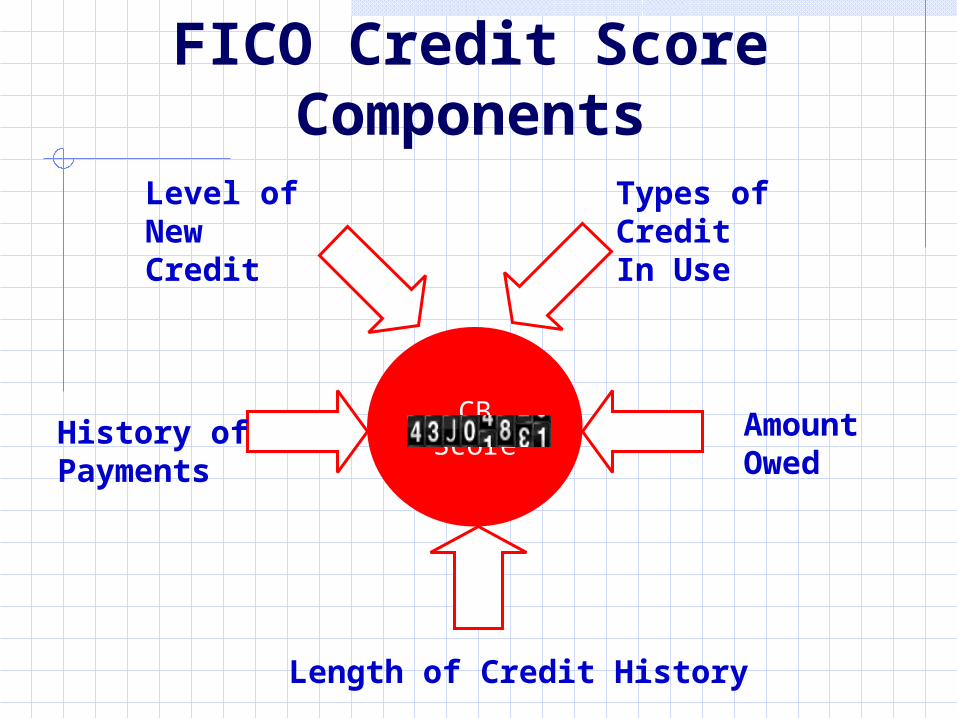

FICO Credit Score Components

CB ScoreHistory of Payments

Amount Owed

Types of CreditIn Use

Level of New Credit

Length of Credit History

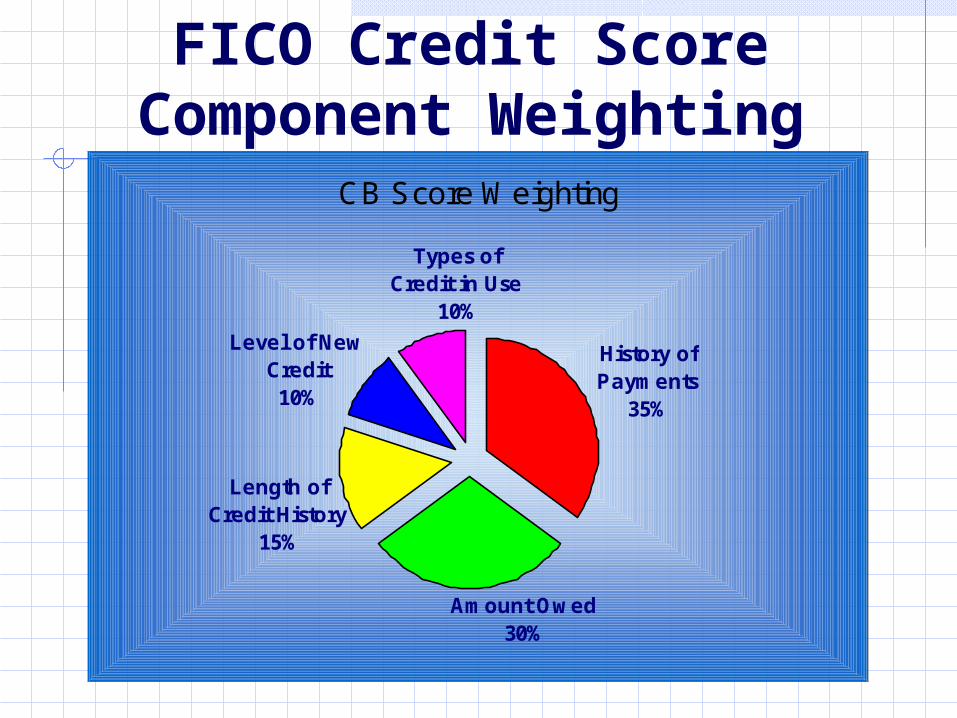

FICO Credit Score Component Weighting

CB Score Weighting

History of Payments

35%

Types of Credit in Use

10%

Level of New Credit10%

Length of Credit History

15%

Amount Owed30%

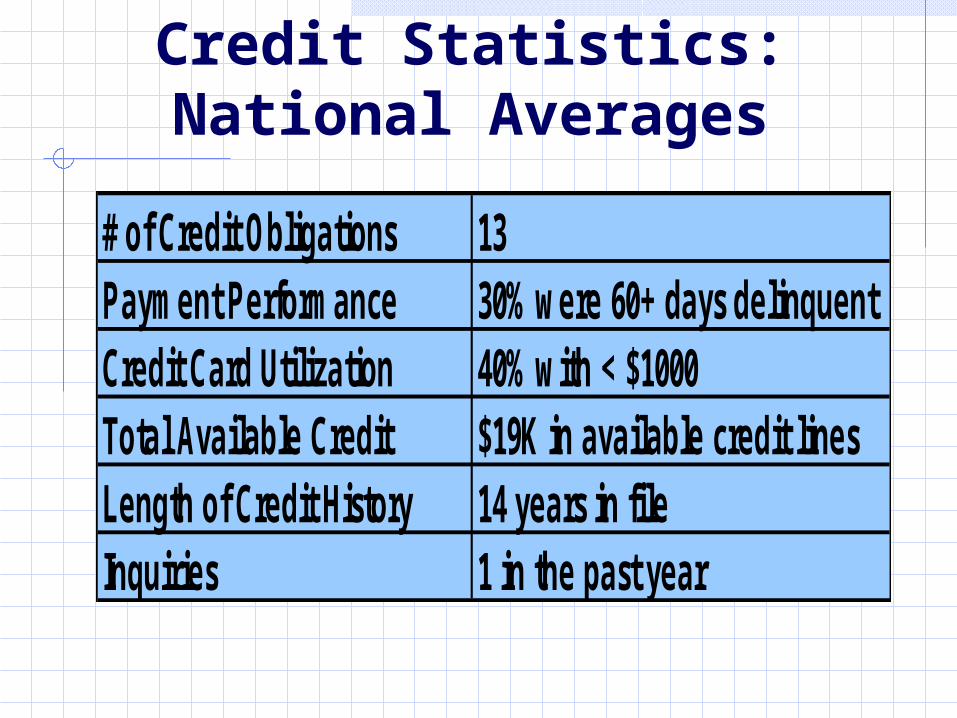

Credit Statistics:National Averages

# of Credit Obligations 13Payment Performance 30% were 60+ days delinquentCredit Card Utilization 40% with < $1000Total Available Credit $19K in available credit linesLength of Credit History 14 years in fileInquiries 1 in the past year

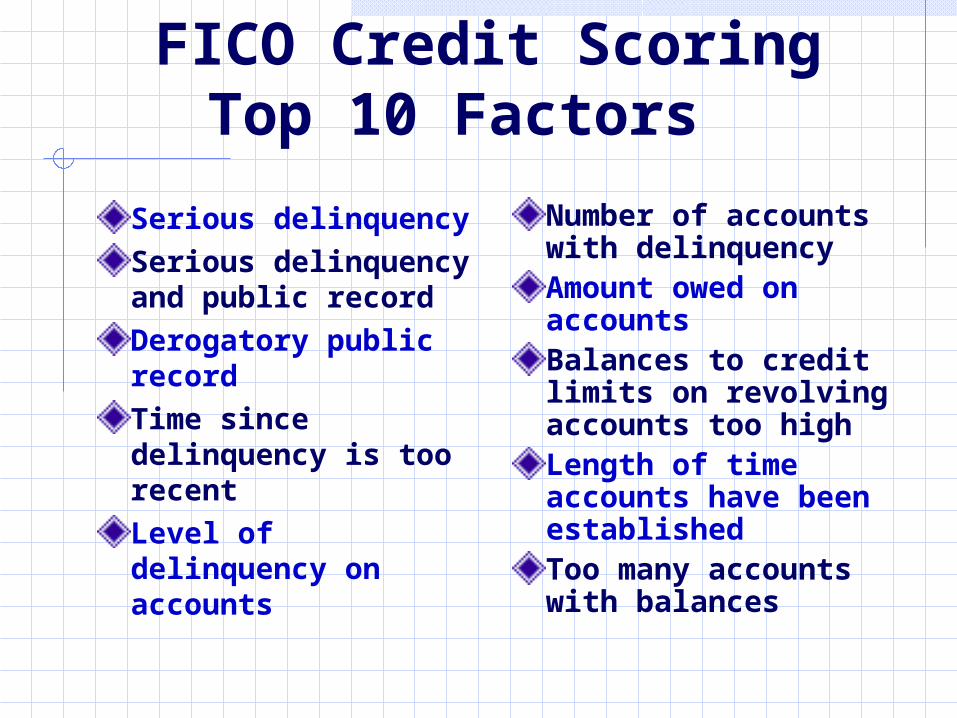

FICO Credit Scoring Top 10 Factors

Serious delinquencySerious delinquency and public recordDerogatory public recordTime since delinquency is too recentLevel of delinquency on accounts

Number of accounts with delinquencyAmount owed on accountsBalances to credit limits on revolving accounts too highLength of time accounts have been establishedToo many accounts with balances

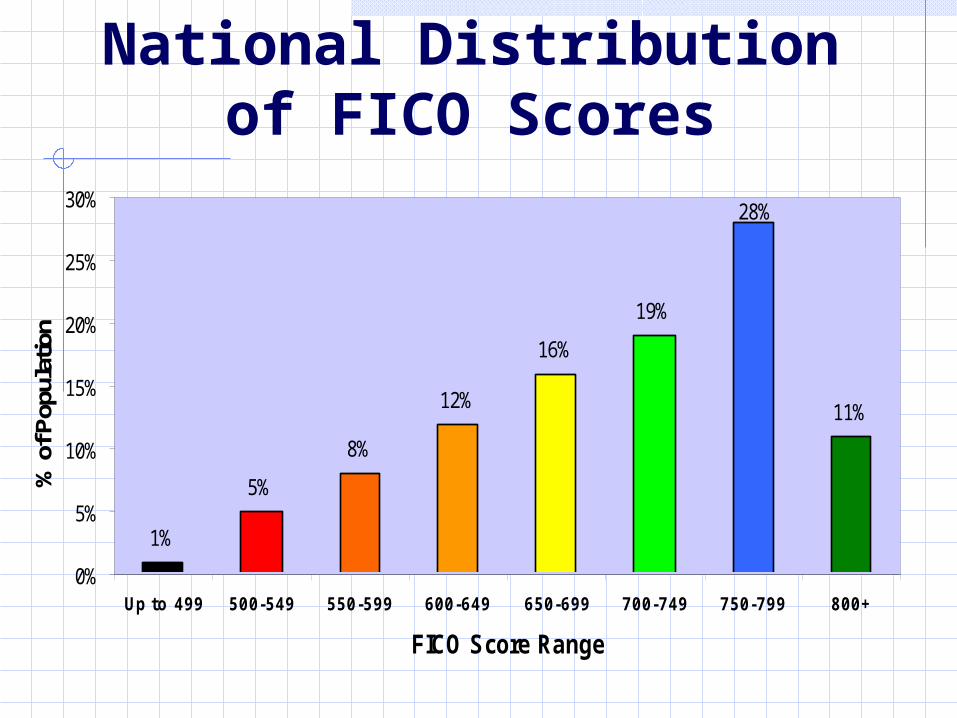

National Distribution of FICO Scores

1%

5%

8%

12%

16%

19%

11%

28%

0%

5%

10%

15%

20%

25%

30%

Up to 499 500-549 550-599 600-649 650-699 700-749 750-799 800+

FICO Score Range

% o

f Pop

ulat

ion

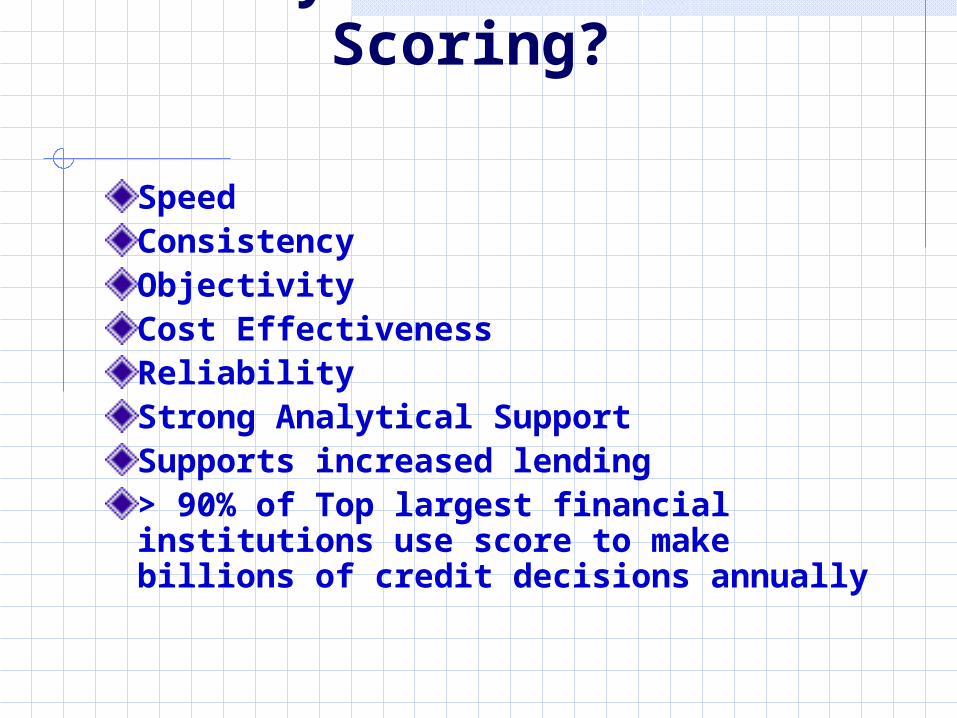

Why Use Credit Scoring?

SpeedConsistencyObjectivityCost EffectivenessReliabilityStrong Analytical SupportSupports increased lending> 90% of Top largest financial institutions use score to make billions of credit decisions annually

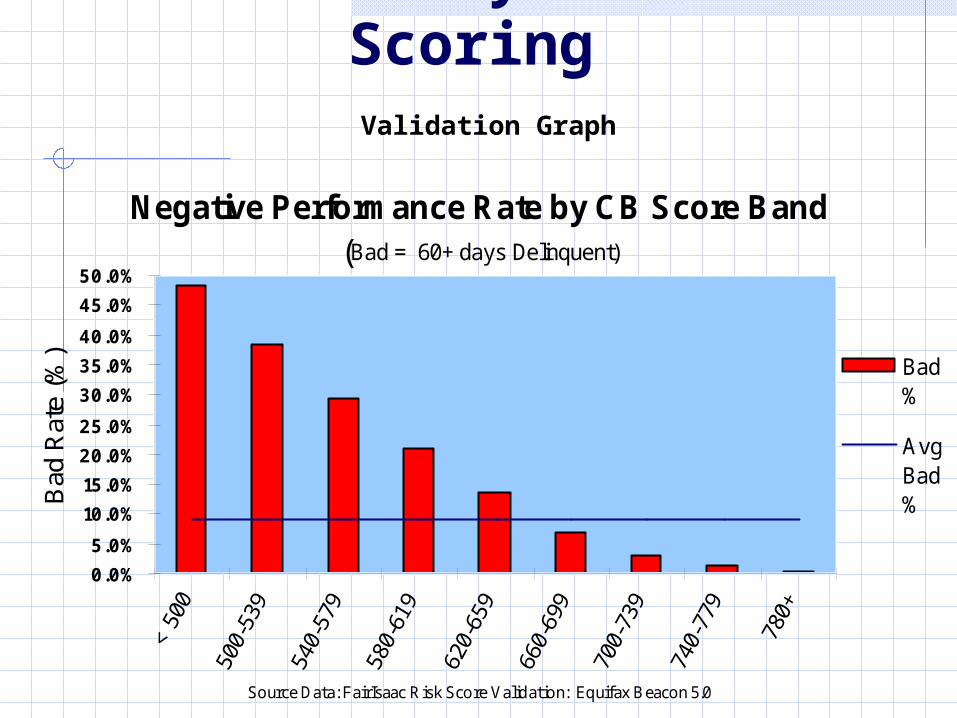

Reliability of FICO Scoring Validation Graph

Negative Performance Rate by CB Score Band(Bad = 60+ days Delinquent)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Source Data: FairIsaac Risk Score Validation: Equifax Beacon 5.0

Bad

Rat

e (%

) Bad%

AvgBad%

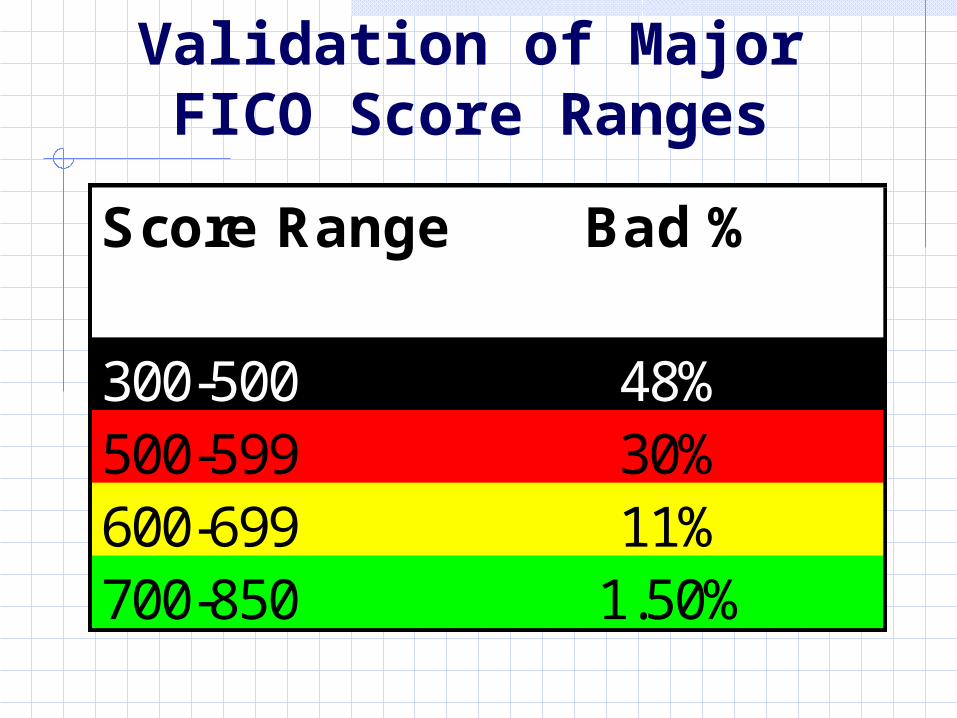

Validation of Major FICO Score Ranges

Score Range Bad %

300-500 48%500-599 30%600-699 11%700-850 1.50%

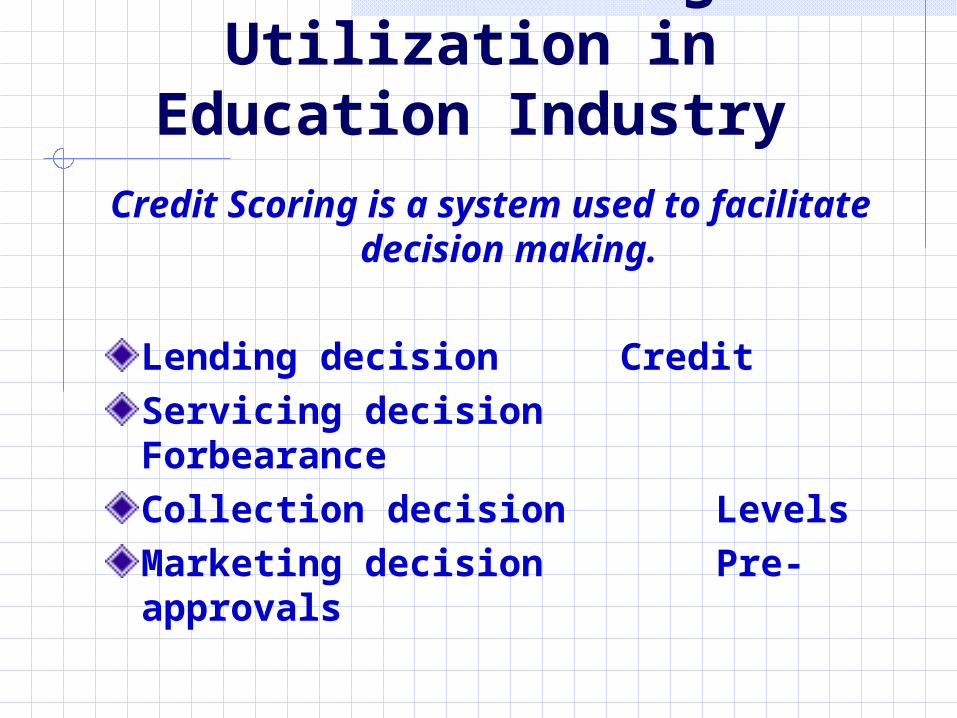

Credit Scoring Utilization in Education

IndustryCredit Scoring is a system used to

facilitate decision making.

Lending decision CreditServicing decisionForbearanceCollection decision LevelsMarketing decision Pre-approvals

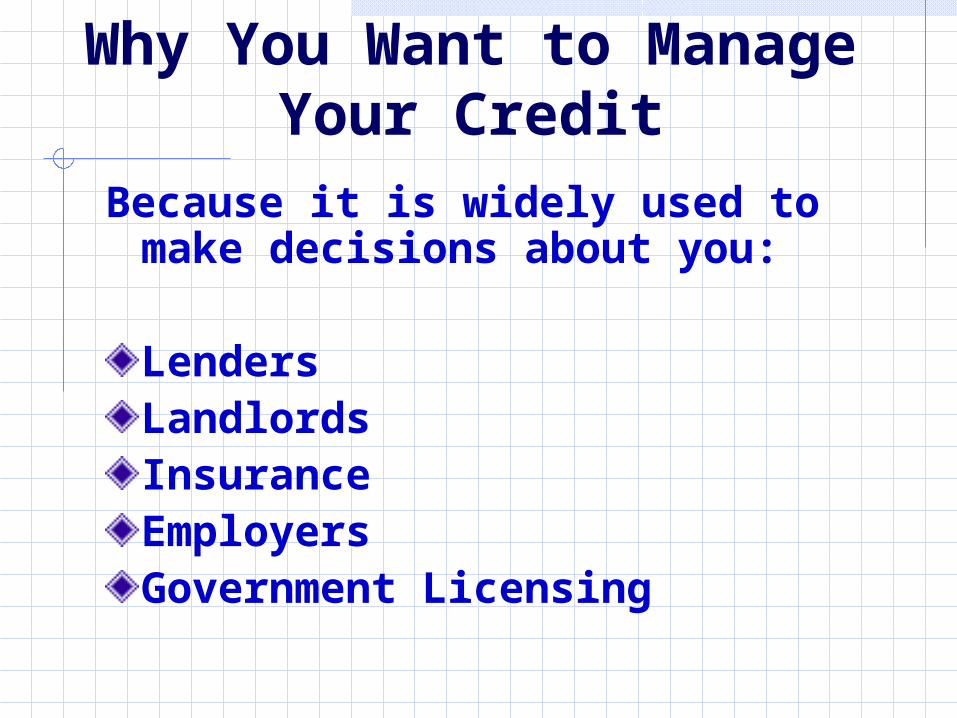

Why You Want to Manage Your Credit

Because it is widely used to make decisions about you:

LendersLandlordsInsuranceEmployersGovernment Licensing

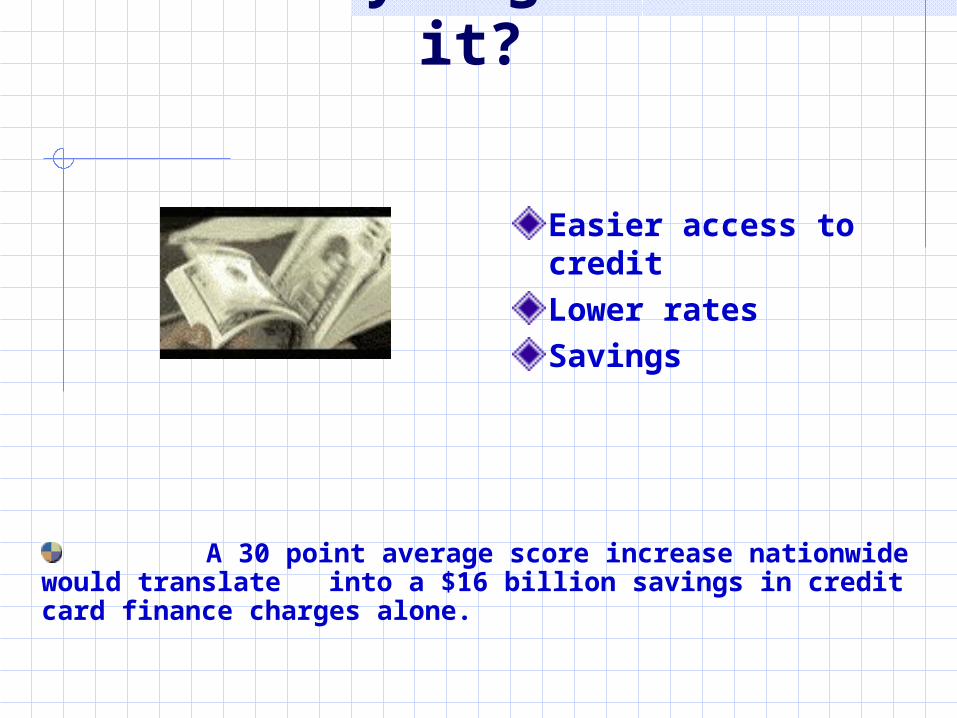

What do you get out of it?

Easier access to creditLower ratesSavings

A 30 point average score increase nationwide would translate into a $16 billion savings in credit card finance charges alone.

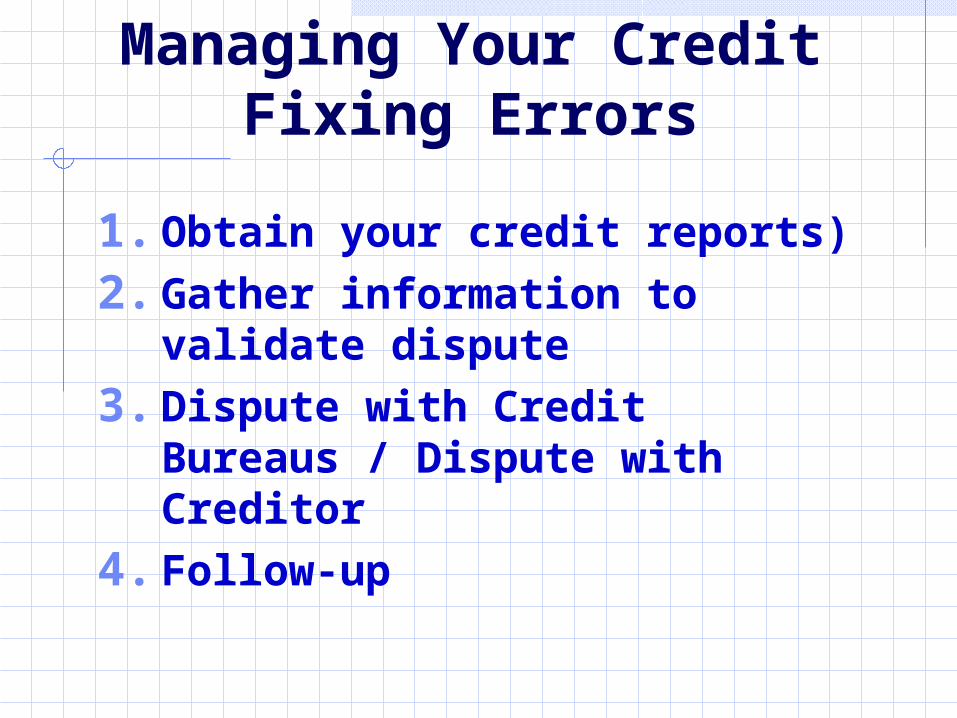

Managing Your CreditFixing Errors

1. Obtain your credit reports)2. Gather information to

validate dispute3. Dispute with Credit Bureaus /

Dispute with Creditor4. Follow-up

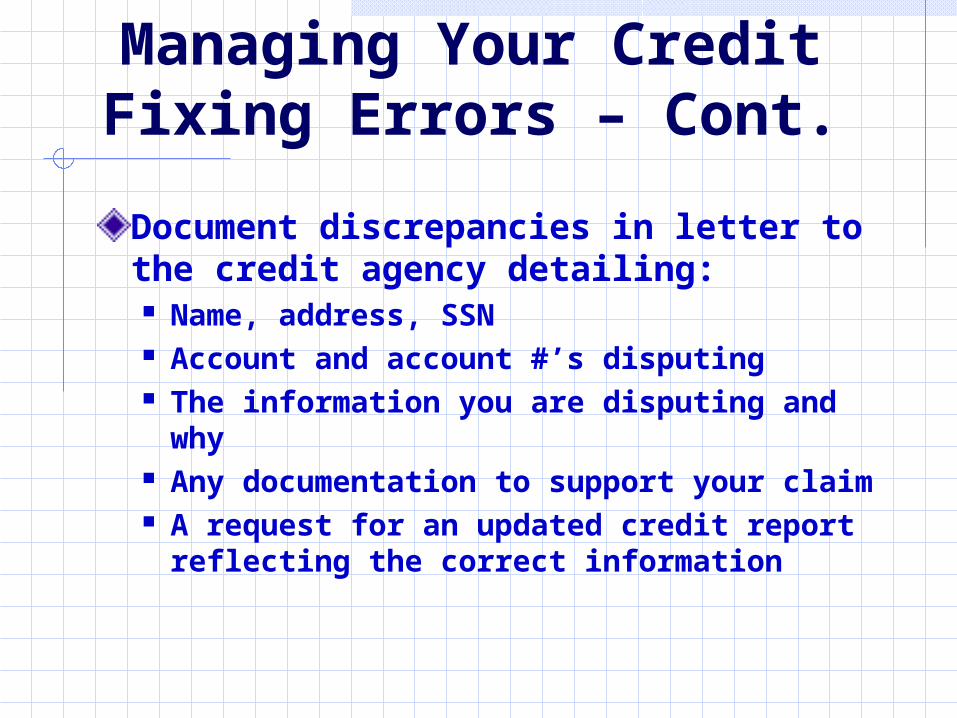

Managing Your CreditFixing Errors – Cont.

Document discrepancies in letter to the credit agency detailing: Name, address, SSN Account and account #’s disputing The information you are disputing and

why Any documentation to support your

claim A request for an updated credit report

reflecting the correct information

Getting Your Credit Report

2003 Fair and Accurate Credit Transactions Act (FACT ACT)Annual Credit Report.COM(877) FACTACTMust provide free if denied credit within 60 daysReview for accuracy annuallyDispute incorrect information

Resources for Credit Bureaus and FICO

ScoresExperian1(888)397-3742www.experian.com

CBI/Equifax1(800)685-1111www.equifax.com

MYFICO.COM

TransUnion Corp1(800)888-4213www.transunion.com

ANNUALCREDITREPORT.COM

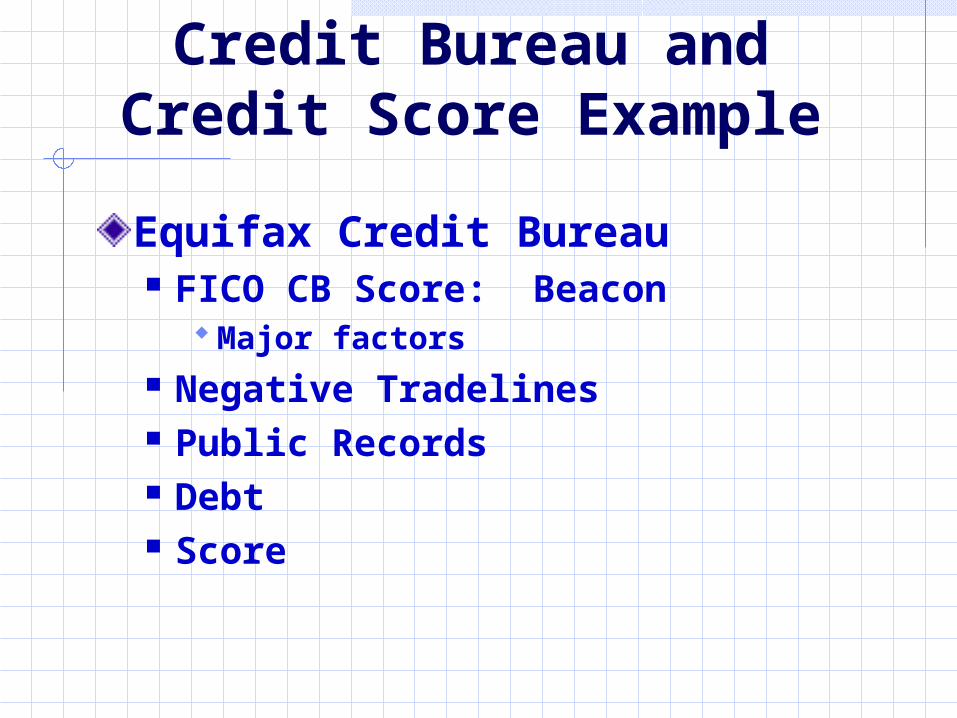

Credit Bureau and Credit Score Example

Equifax Credit Bureau FICO CB Score: Beacon

Major factors Negative Tradelines Public Records Debt Score

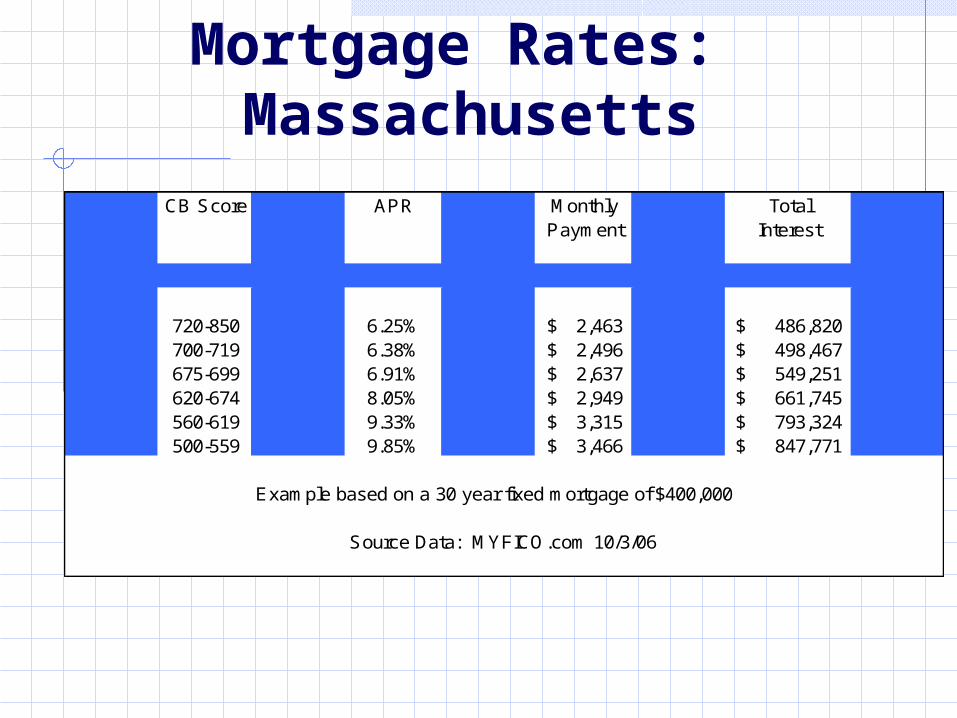

Credit Scores & Mortgage Rates: Massachusetts

CB Score APR Monthly TotalPayment Interest

720-850 6.25% 2,463$ 486,820$ 700-719 6.38% 2,496$ 498,467$ 675-699 6.91% 2,637$ 549,251$ 620-674 8.05% 2,949$ 661,745$ 560-619 9.33% 3,315$ 793,324$ 500-559 9.85% 3,466$ 847,771$

Example based on a 30 year fixed mortgage of $400,000

Source Data: MYFICO.com 10/3/06

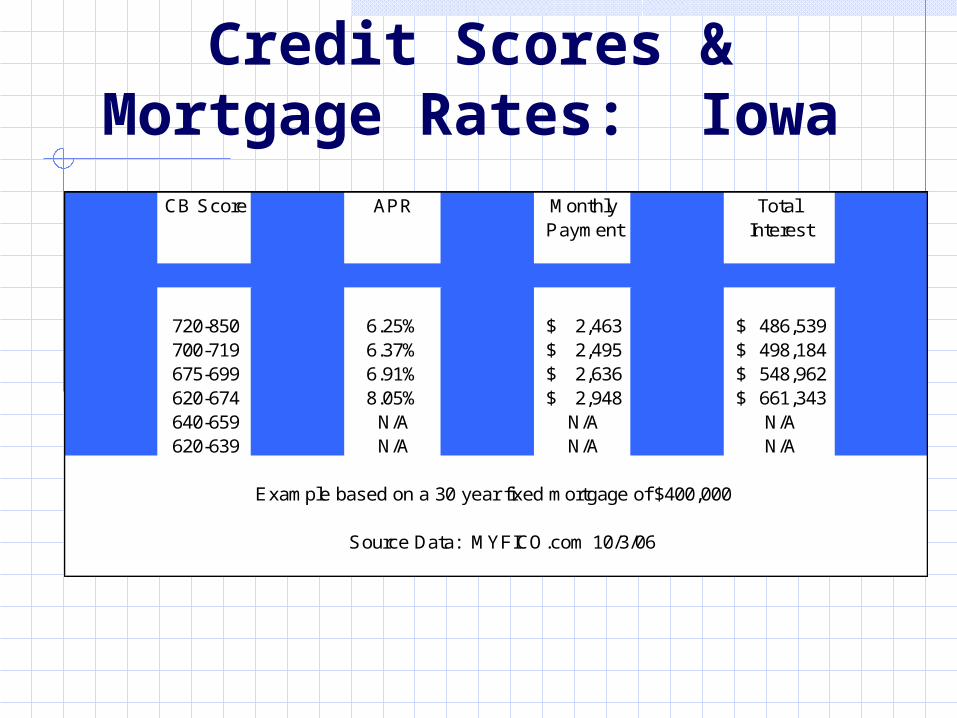

Credit Scores & Mortgage Rates: Iowa

CB Score APR Monthly Total Payment Interest

720-850 6.25% 2,463$ 486,539$ 700-719 6.37% 2,495$ 498,184$ 675-699 6.91% 2,636$ 548,962$ 620-674 8.05% 2,948$ 661,343$ 640-659 N/A N/A N/A620-639 N/A N/A N/A

Example based on a 30 year fixed mortgage of $400,000

Source Data: MYFICO.com 10/3/06

Credit Summary

Pay bills on timeManage your debt load appropriatelyReview your credit Repeat

Questions

MASFAA Conference 2006