Embed Size (px)

Citation preview

Credit Suisse Technology Conference

November 2007

Credit Suisse Technology Conference

November 2007

Oleg Khaykin EVP & COOKen Joyce Chief Administrative OfficerJim Fusaro Corporate VP, Wire Bond Products

2

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 2 Nov-07, OKHAY

Forward Looking Statement DisclaimerAll information and other statements contained in this presentation, other than statements of historical fact, constitute forward looking statements within the meaning of federal securities laws. These forward-looking statements involve a number of risks, uncertainties, assumptions and other factors that could affect our future results and cause actual results and events to differ materially from our historical and expected results and those expressed or implied in these forward looking statements. Our historical financial information, and the risks and other important factors that could affect the outcome of the events set forth in these statements and that could affect our operating results and financial condition, are contained in our filings with the Securities and Exchange Commission, including our Form 10-Q for the quarter ended September 30, 2007. We undertake no obligation to review or update any forward-looking statements to reflect events or circumstances occurring after this presentation.

Guidance PolicyOur financial guidance for the quarter is contained in our earnings release and is effective only on the date given. In accordance with our policy, we will not update, reaffirm or otherwise comment on any prior financial guidance in connection with this presentation.

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 3 Nov-07, OKHAY

Amkor’s Role in the Semiconductor Value Chain

Enabling semiconductor advancements . . .

. . . To deliver physical world benefits

Outsourced Semiconductor Assembly and Test (OSAT)Outsourced Semiconductor Assembly and Test (OSAT)

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 4 Nov-07, OKHAY

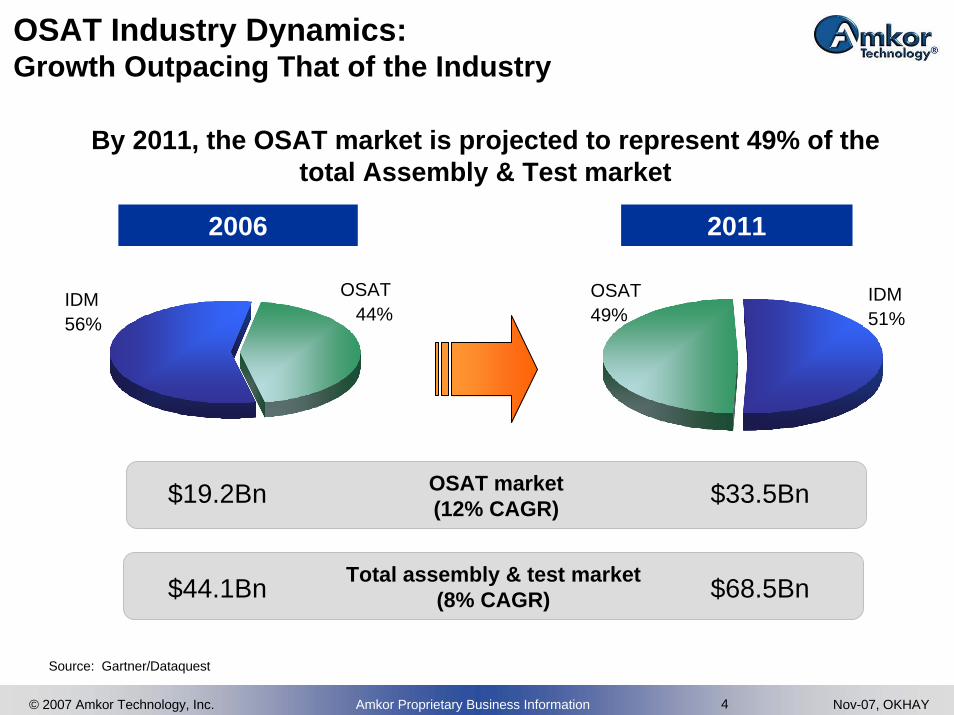

OSAT market (12% CAGR)$19.2Bn

By 2011, the OSAT market is projected to represent 49% of the total Assembly & Test market

2006 2011

Source: Gartner/Dataquest

$33.5Bn

Total assembly & test market(8% CAGR)$44.1Bn $68.5Bn

OSAT Industry Dynamics:Growth Outpacing That of the Industry

IDM56%

IDM51%

OSAT49%

OSAT44%

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 5 Nov-07, OKHAY

OSAT Industry Dynamics:Consumer Spending Primary Driver of Industry Growth

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 6 Nov-07, OKHAY

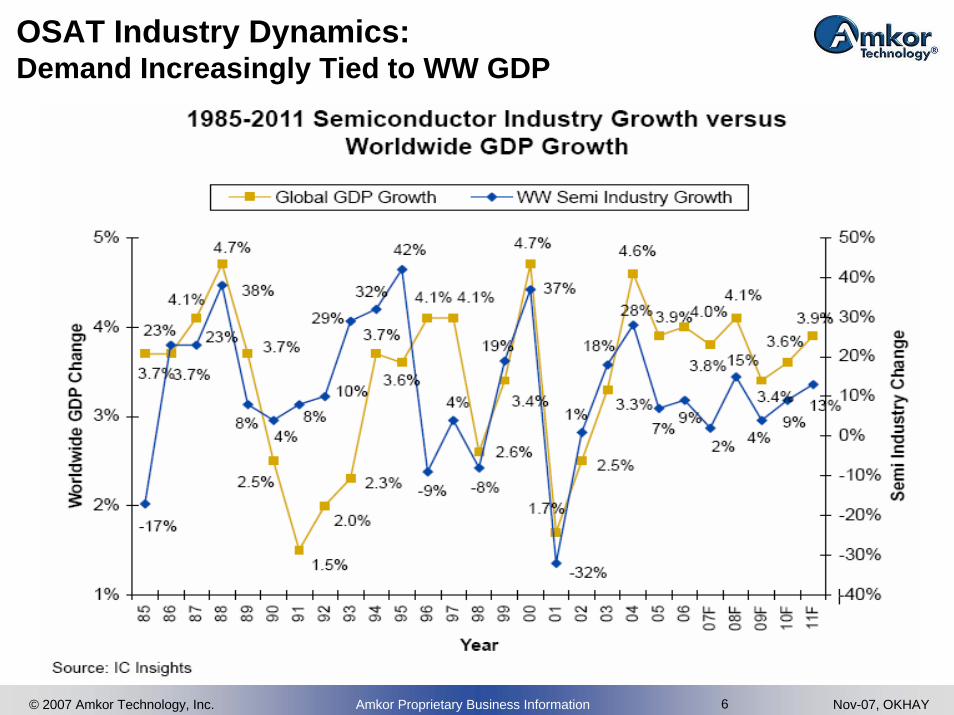

OSAT Industry Dynamics:Demand Increasingly Tied to WW GDP

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 7 Nov-07, OKHAY

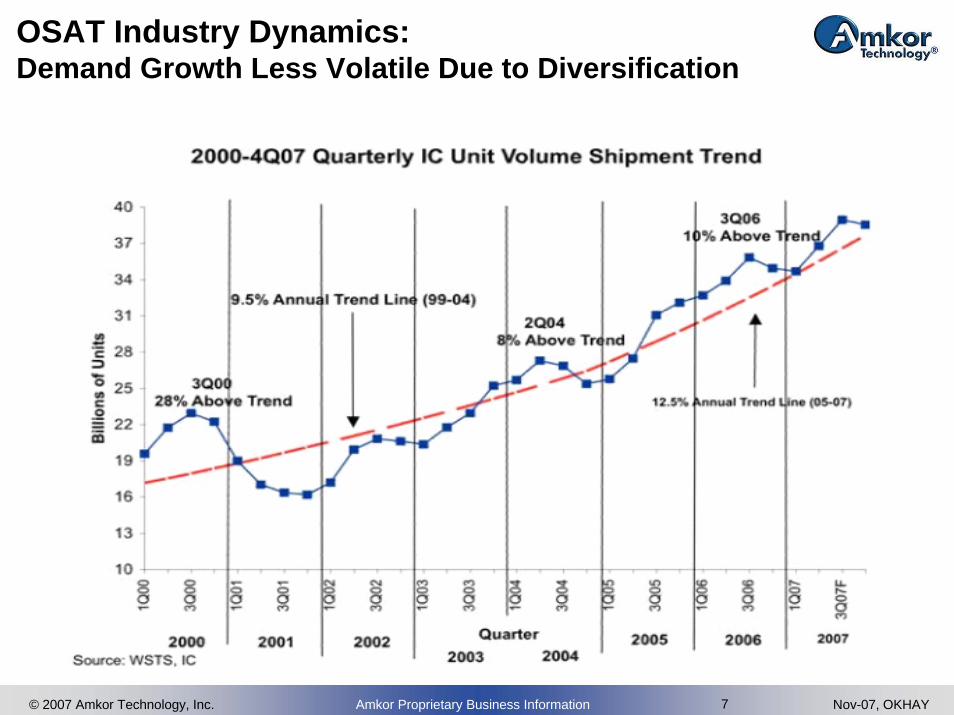

OSAT Industry Dynamics:Demand Growth Less Volatile Due to Diversification

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 8 Nov-07, OKHAY

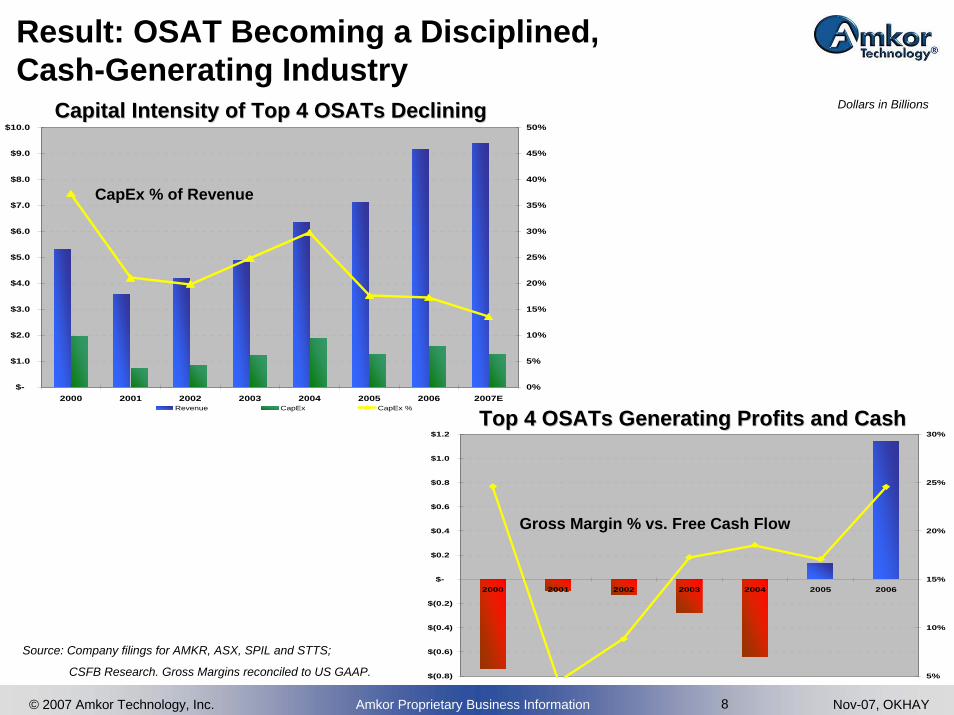

Result: OSAT Becoming a Disciplined, Cash-Generating Industry

Dollars in Billions

Source: Company filings for AMKR, ASX, SPIL and STTS;

CSFB Research. Gross Margins reconciled to US GAAP.

$-

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

2000 2001 2002 2003 2004 2005 2006 2007E0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Revenue CapEx CapEx %

$(0.8)

$(0.6)

$(0.4)

$(0.2)

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

2000 2001 2002 2003 2004 2005 2006

5%

10%

15%

20%

25%

30%Top 4 Top 4 OSATsOSATs Generating Profits and CashGenerating Profits and Cash

Gross Margin % vs. Free Cash Flow

Capital Intensity of Top 4 Capital Intensity of Top 4 OSATsOSATs DecliningDeclining

CapEx % of Revenue

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 9 Nov-07, OKHAY

Amkor Strategy and Competitive Positioning

• Technology leadership

– Driving technology and product development to meet challenging end market demands

• Industry’s leading innovator over the past seven years: MLF® (QFN), POP, and FusionQuad™

– Strategic alliances with Tier 1 IC companies and OEMs

• World class manufacturing infrastructure

– Strategic geographical footprint

– Operational scale and scope

– Competitive cost structure

OSAT Partner of Choice

Operating Model Focused on Sustainable Growth

• Profitability and cash flow through industry cycles

• Capital deployment decisions based on ROIC

• Generating cash to fund growth, reinvestment and R&D and to service debt

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 10 Nov-07, OKHAY

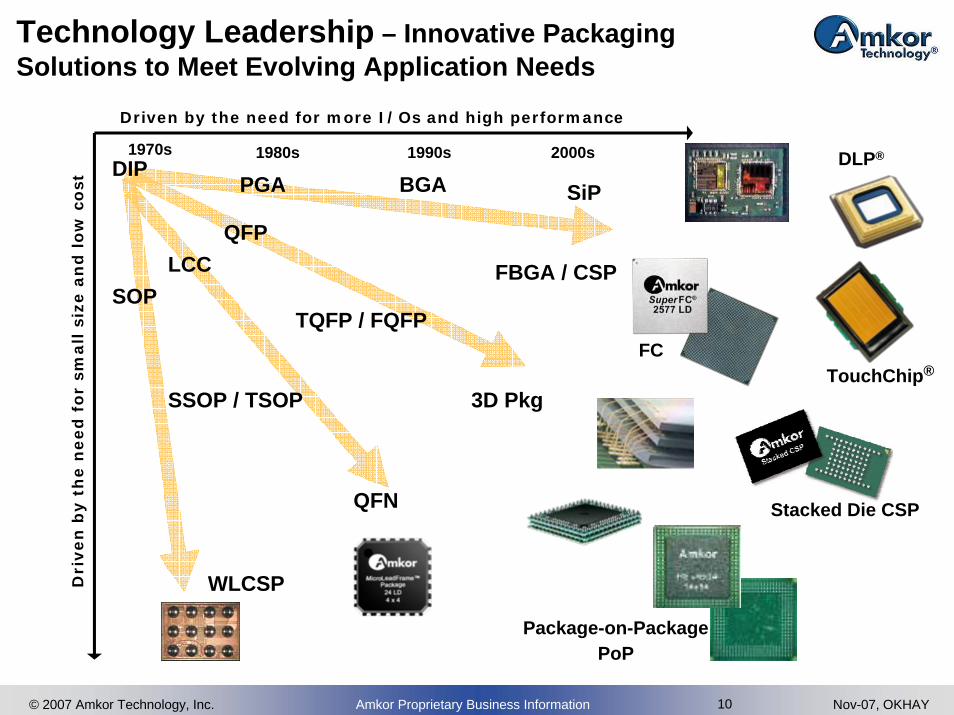

Driven by the need for more I/Os and high performance

Dri

ven

by t

he n

eed

fo

r sm

all s

ize a

nd

lo

w c

ost

1970s 1980s 1990s 2000sDIP

SOPLCC

QFP

PGA

TQFP / FQFP

SSOP / TSOP

BGA SiP

FBGA / CSP

3D Pkg

QFN

WLCSP

Package-on-PackagePoP

Stacked Die CSP

TouchChip®FC

DLP®

Technology Leadership – Innovative Packaging Solutions to Meet Evolving Application Needs

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 11 Nov-07, OKHAY

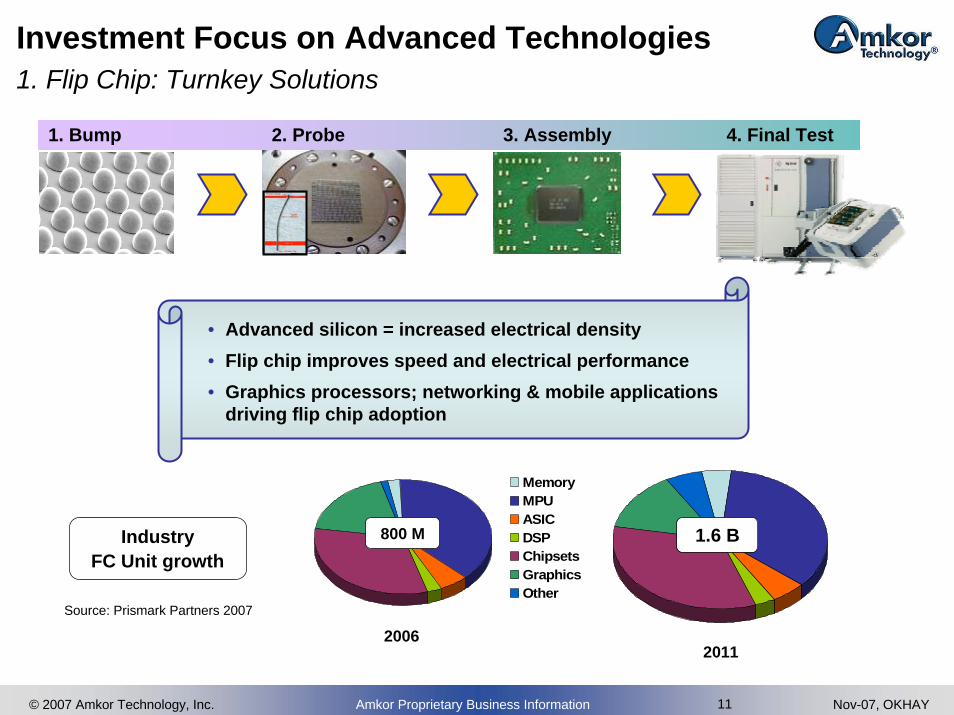

2. Probe1. Bump 3. Assembly 4. Final Test

MemoryMPUASICDSPChipsetsGraphicsOther

1.6 B 800 M

Source: Prismark Partners 2007

2006 2011

IndustryFC Unit growth

• Advanced silicon = increased electrical density• Flip chip improves speed and electrical performance• Graphics processors; networking & mobile applications

driving flip chip adoption

Investment Focus on Advanced Technologies1. Flip Chip: Turnkey Solutions

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 12 Nov-07, OKHAY

Investment Focus on Advanced Technologies2. Wafer Level Packaging

FunctionalityExpands silicon functionality in wireless applications

Miniaturization Broad range of technologies and processes (e.g., Fan-out, TSV, etc.) to enable multi-die and SiP solutions

PerformanceImproves heat dissipation for wireless applications

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 13 Nov-07, OKHAY

Investment Focus on Advanced Technologies3. 3-D Package Solutions

• Vertically stacking 2 or more die to increase functionality & reduce package footprint

• PoP package provides OEMs with a platform to cost effectively integrate logic + memory devices

• Turnkey capability for bottom and top package applications

• Broad portfolio of 3D package solutions

Package-on-Package (PoP)

4SS-SCSPStacked-SiP

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 14 Nov-07, OKHAY

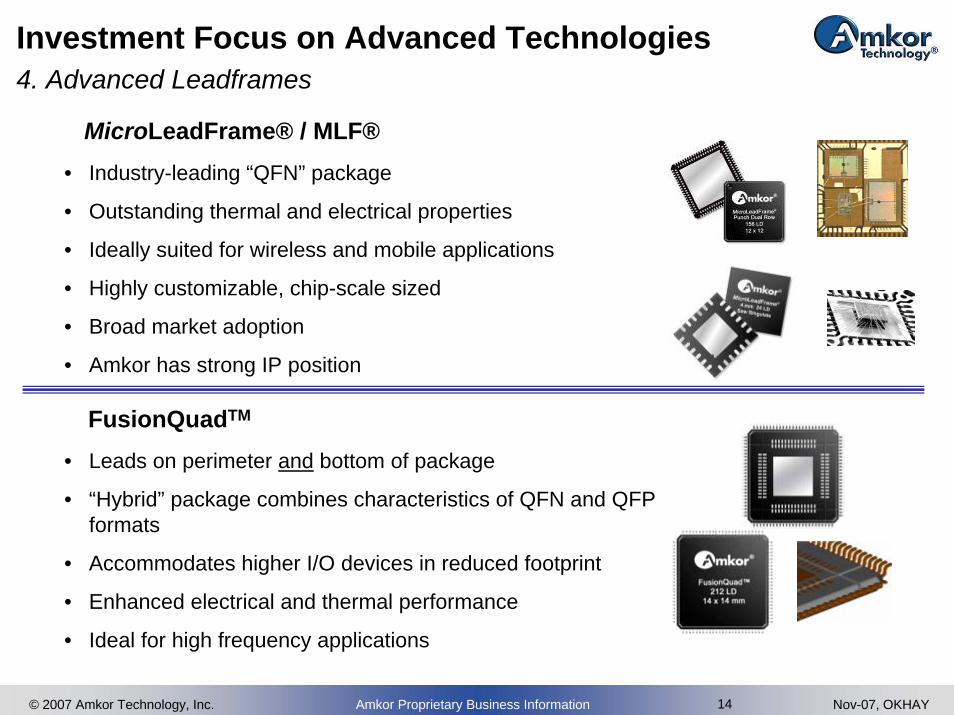

• Leads on perimeter and bottom of package

• “Hybrid” package combines characteristics of QFN and QFP formats

• Accommodates higher I/O devices in reduced footprint

• Enhanced electrical and thermal performance

• Ideal for high frequency applications

• Industry-leading “QFN” package

• Outstanding thermal and electrical properties

• Ideally suited for wireless and mobile applications

• Highly customizable, chip-scale sized

• Broad market adoption

• Amkor has strong IP position

Investment Focus on Advanced Technologies4. Advanced Leadframes

FusionQuadTM

MicroLeadFrame® / MLF®

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 15 Nov-07, OKHAY

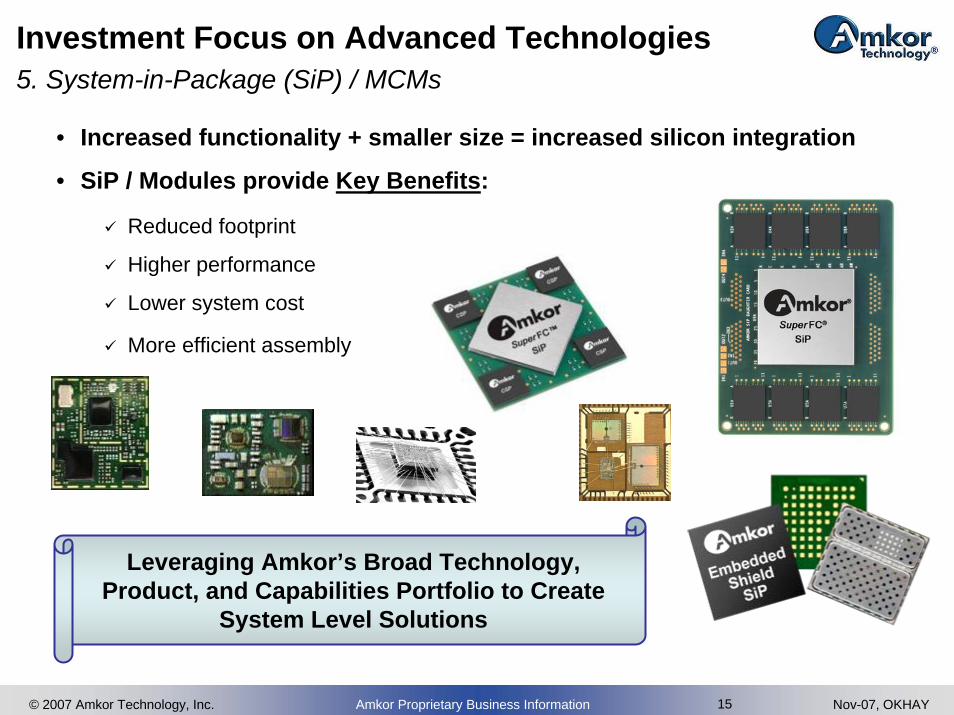

Investment Focus on Advanced Technologies5. System-in-Package (SiP) / MCMs

• Increased functionality + smaller size = increased silicon integration

• SiP / Modules provide Key Benefits:

Reduced footprint

Higher performance

Lower system cost

More efficient assembly

Leveraging Amkor’s Broad Technology, Product, and Capabilities Portfolio to Create

System Level Solutions

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 16 Nov-07, OKHAY

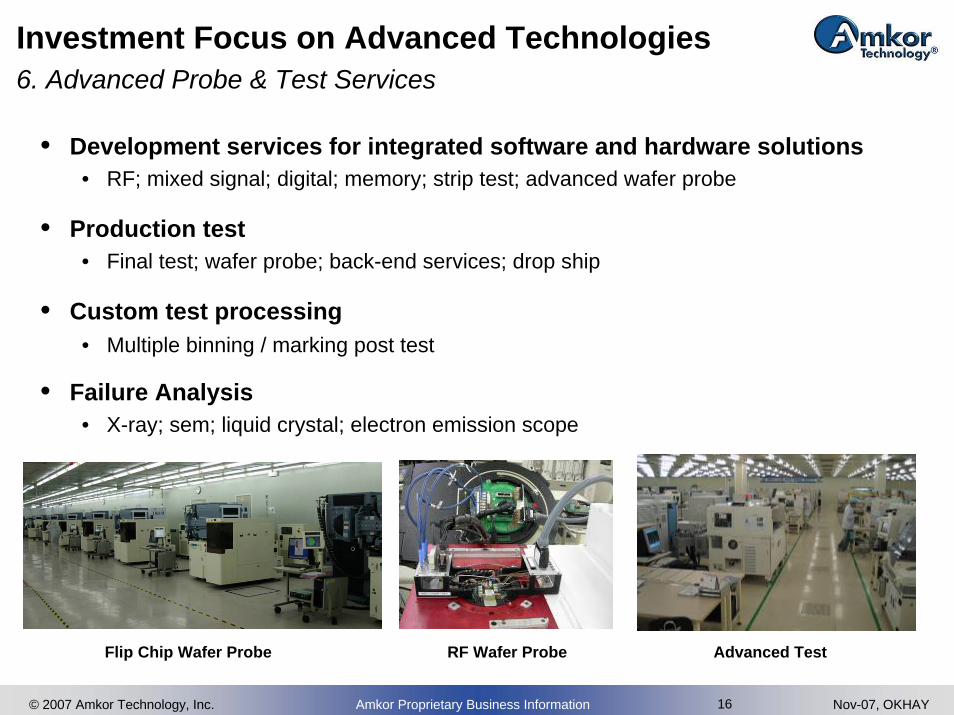

Flip Chip Wafer Probe RF Wafer Probe Advanced Test

Investment Focus on Advanced Technologies6. Advanced Probe & Test Services

• Development services for integrated software and hardware solutions• RF; mixed signal; digital; memory; strip test; advanced wafer probe

• Production test• Final test; wafer probe; back-end services; drop ship

• Custom test processing• Multiple binning / marking post test

• Failure Analysis• X-ray; sem; liquid crystal; electron emission scope

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 17 Nov-07, OKHAY

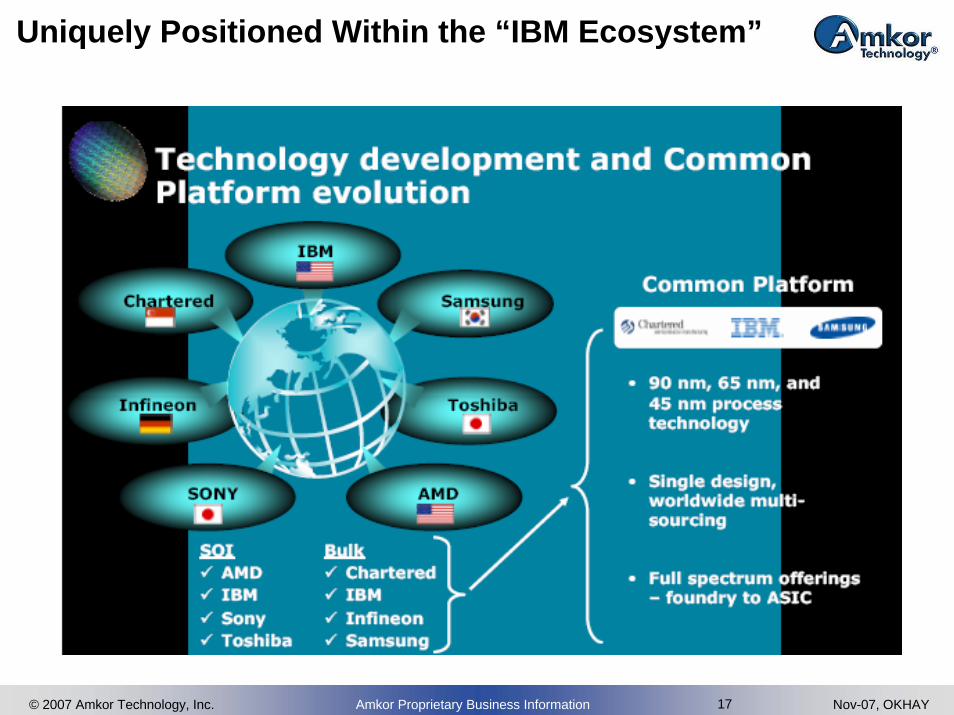

Uniquely Positioned Within the “IBM Ecosystem”

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 18 Nov-07, OKHAY

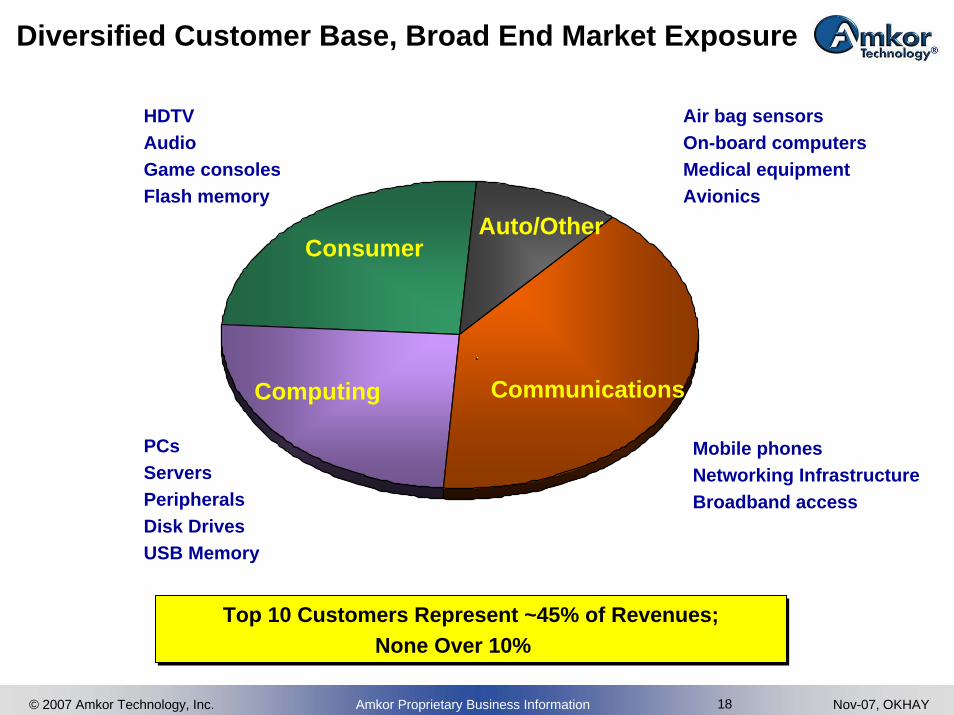

Diversified Customer Base, Broad End Market Exposure

Mobile phonesNetworking InfrastructureBroadband access

PCsServersPeripheralsDisk DrivesUSB Memory

HDTVAudioGame consolesFlash memory

Air bag sensorsOn-board computersMedical equipmentAvionics

Top 10 Customers Represent ~45% of Revenues;None Over 10%

Top 10 Customers Represent ~45% of Revenues;None Over 10%

Consumer

Computing

Auto/Other

Communications

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 19 Nov-07, OKHAY

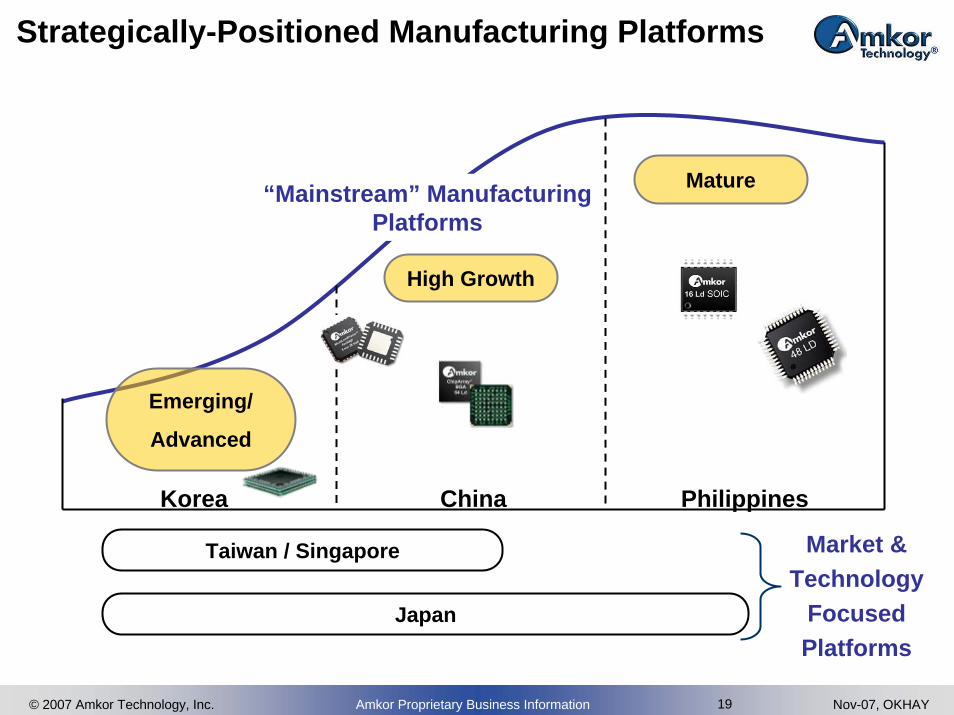

Strategically-Positioned Manufacturing Platforms

Korea China Philippines

Japan

Taiwan / Singapore

Mature

High Growth

Emerging/

Advanced

Market & Technology

FocusedPlatforms

“Mainstream” ManufacturingPlatforms

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 20 Nov-07, OKHAY

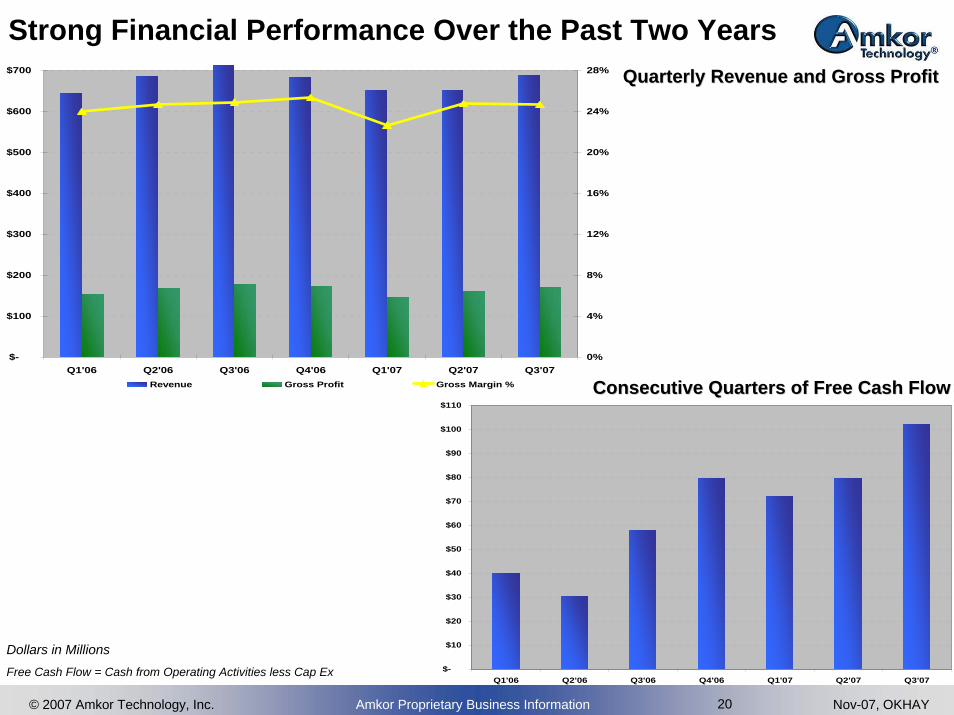

Strong Financial Performance Over the Past Two Years

$-

$100

$200

$300

$400

$500

$600

$700

Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'070%

4%

8%

12%

16%

20%

24%

28%

Revenue Gross Profit Gross Margin % Consecutive Quarters of Free Cash FlowConsecutive Quarters of Free Cash Flow

Quarterly Revenue and Gross ProfitQuarterly Revenue and Gross Profit

Dollars in MillionsFree Cash Flow = Cash from Operating Activities less Cap Ex $-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'07

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 21 Nov-07, OKHAY

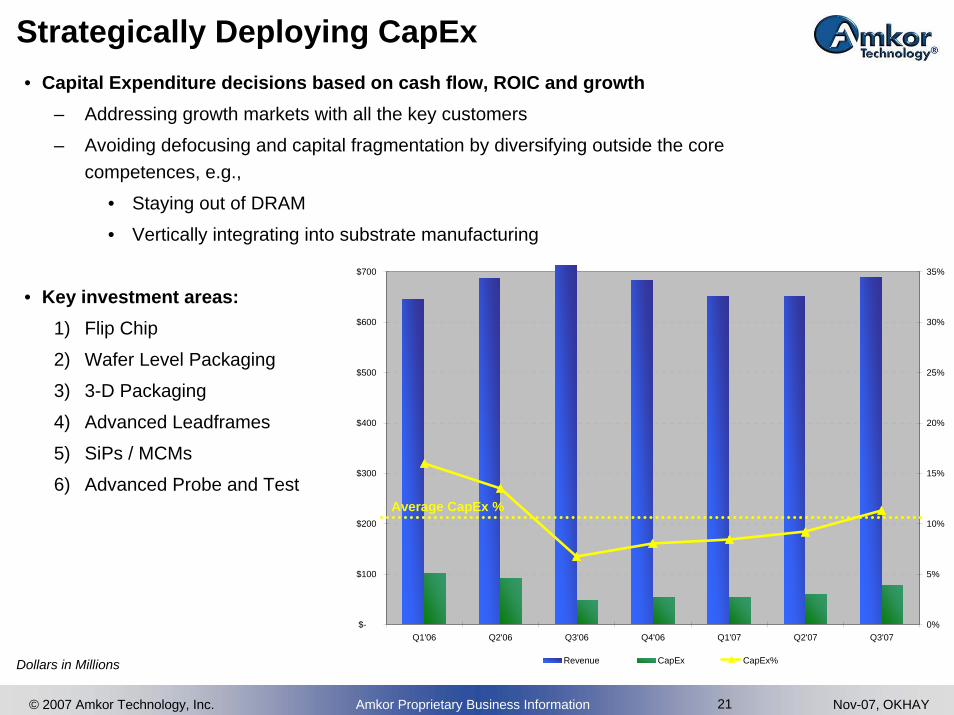

Strategically Deploying CapEx• Capital Expenditure decisions based on cash flow, ROIC and growth

– Addressing growth markets with all the key customers

– Avoiding defocusing and capital fragmentation by diversifying outside the core competences, e.g.,

• Staying out of DRAM

• Vertically integrating into substrate manufacturing

• Key investment areas:1) Flip Chip

2) Wafer Level Packaging

3) 3-D Packaging

4) Advanced Leadframes

5) SiPs / MCMs

6) Advanced Probe and Test

$-

$100

$200

$300

$400

$500

$600

$700

Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'070%

5%

10%

15%

20%

25%

30%

35%

Revenue CapEx CapEx%

Average CapEx %

Dollars in Millions

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 22 Nov-07, OKHAY

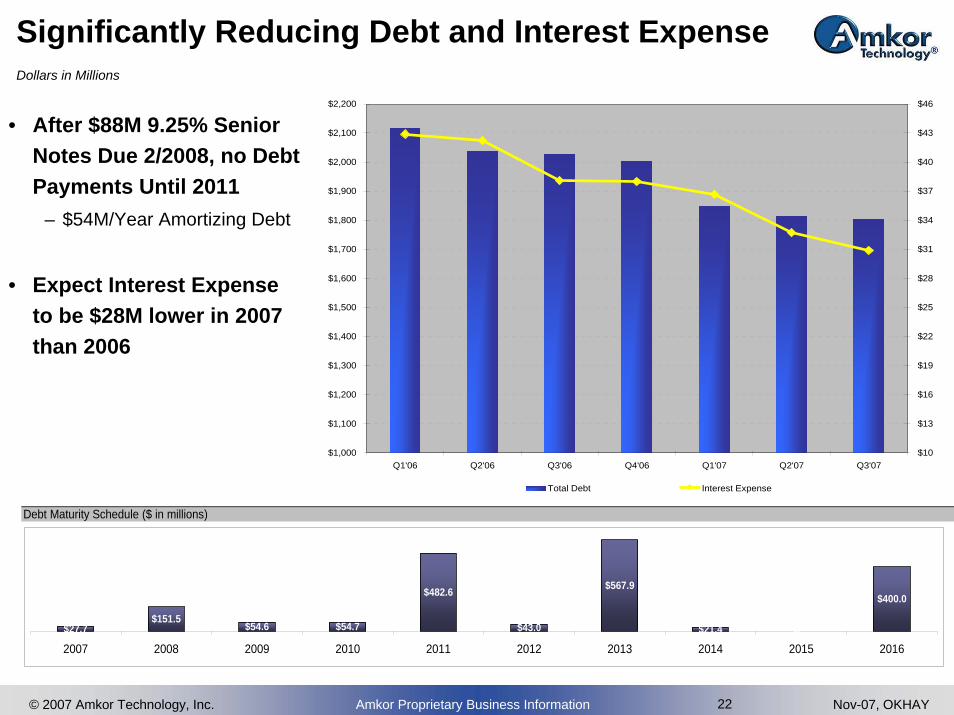

Significantly Reducing Debt and Interest Expense

Debt Maturity Schedule ($ in millions)

$27.7$151.5

$54.6 $54.7

$482.6

$43.0

$567.9

$21.4 $-

$400.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

• After $88M 9.25% Senior Notes Due 2/2008, no Debt Payments Until 2011

– $54M/Year Amortizing Debt

• Expect Interest Expense to be $28M lower in 2007 than 2006

Dollars in Millions

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

$2,000

$2,100

$2,200

Q1'06 Q2'06 Q3'06 Q4'06 Q1'07 Q2'07 Q3'07$10

$13

$16

$19

$22

$25

$28

$31

$34

$37

$40

$43

$46

Total Debt Interest Expense

© 2007 Amkor Technology, Inc. Amkor Proprietary Business Information 23 Nov-07, OKHAY

Summary: Amkor Investment Thesis

• Increasing attractiveness of the OSAT industry

– Decreased volatility of end market demand

• Reduced capital intensity and improved profitability of the sector

– Greater IP intensity increasing value-add of assembly and test

– Growth rate exceeding overall industry, continued outsourcing trend by IDMs

• Amkor is well-positioned for success in OSAT

– Industry’s innovator and technology leader

– Deep ties to tier-1 IC companies, foundries and OEMs

– Targeting attractive growth markets that generate returns and cash flow

– Strategically positioned manufacturing platforms

– Building a strong financial track record

• Free cash flow and healthy margins

• Capital investment discipline

• Improved capital structure

• Profitable through industry’s down cycle

Q & A