Embed Size (px)

DESCRIPTION

Mutual fund year book

Citation preview

CRISIL Mutual Fund Year BookApril 2013

Mutual Funds - The right road to diversification

CRISIL Mutual Fund Year Book

About CRISIL Limited

About CRISIL Research

CRISIL Privacy

Disclaimer

CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leading ratings agency. We are also the foremost provider of high-end research to the world's largest banks and leading corporations.

CRISIL Research is India's largest independent and integrated research house. We provide insights, opinions, and analysis on the Indian economy, industries, capital markets and companies. We are India's most credible provider of economy and industry research. Our industry research covers 70 sectors and is known for its rich insights and perspectives. Our analysis is supported by inputs from our network of more than 4,500 primary sources, including industry experts, industry associations, and trade channels. We play a key role in India's fixed income markets. We are India's largest provider of valuations of fixed income securities, serving the mutual fund, insurance, and banking industries. We are the sole provider of debt and hybrid indices to India's mutual fund and life insurance industries. We pioneered independent equity research in India, and are today India's largest independent equity research house. Our defining trait is the ability to convert information and data into expert judgements and forecasts with complete objectivity. We leverage our deep understanding of the macro economy and our extensive sector coverage to provide unique insights on micro-macro and cross-sectoral linkages. We deliver our research through an innovative web-based research platform. Our talent pool comprises economists, sector experts, company analysts, and information management specialists.

CRISIL respects your privacy. We use your contact information, such as your name, address, and email id, to fulfill your request and service your

account and to provide you with additional information from CRISIL and other parts of The McGraw-Hill Companies, Inc. you may find of interest. For

further information, or to let us know your preferences with respect to receiving marketing materials, please visit www.crisil.com/privacy. You can view

McGraw-Hill’s Customer Privacy Policy at http://www.mcgrawhill.com/site/tools/privacy/privacy_english.

Last updated: March 7, 2013

CRISIL Research, a division of CRISIL Limited (CRISIL), has taken due care and caution in preparing this Report based on the information obtained

by CRISIL from sources which it considers reliable (Data). However, CRISIL does not guarantee the accuracy, adequacy or completeness of the Data

/ Report and is not responsible for any errors or omissions or for the results obtained from the use of Data / Report. This Report is not a

recommendation to invest / disinvest in any company covered in the Report. CRISIL especially states that it has no financial liability whatsoever to the

subscribers / users / transmitters / distributors of this Report. CRISIL Research operates independently of, and does not have access to information

obtained by CRISIL’s Ratings Division / CRISIL Risk and Infrastructure Solutions Limited (CRIS), which may, in their regular operations, obtain

information of a confidential nature. The views expressed in this Report are that of CRISIL Research and not of CRISIL’s Ratings Division / CRIS. No

part of this Report may be published / reproduced in any form without CRISIL’s prior written approval.

1

Table of contents

Foreword ................................................................................................................ 3

Overview ................................................................................................................ 5

I - Mutual fund industry reports double digit growth .................................................. 7

II - Way forward for the mutual fund industry.......................................................... 10

III - Equity market up 28% in 2012 ......................................................................... 12

IV - Gilt prices surge as RBI cuts Repo rate ........................................................... 14

Category wise mutual fund performance ........................................................... 17

I - Category wise risk / return trade-off & indicative investment horizons ................ 18

II - Equity & Hybrid Equity - Small & Midcap Funds outperform .............................. 20

III - Sector / Thematic - Banking Funds dominate 2012, Gold Funds lose lustre ..... 21

IV- Debt & Hybrid Debt - Gilt Funds outperform on softening interest rates ............ 22

Articles ................................................................................................................ 23

I - The Science of Financial Planning - Next Frontier for Investment Advisors ........ 25

II - Declining interest rate scenario - Long-term debt funds to benefit ..................... 28

III - Liquid funds - An alternative to savings bank deposits ..................................... 30

IV - Go for paper gold ............................................................................................ 32

V - Protect the downside in equities through capital protection oriented funds ........ 34

Factsheets ........................................................................................................... 37

Annexures ........................................................................................................... 63

I - Fund House Wise Ranks (December 2012) ....................................................... 65

II - AUM Trends..................................................................................................... 66

III - CRISIL Mutual Fund Ranking Methodology ..................................................... 69

IV - CRISIL Mutual Fund Ranking Category Definitions ......................................... 71

Glossary of terms used in the factsheets ............................................................... 73

List of Abbreviations used in the Year Book ........................................................... 75

2

3

Foreword

We are pleased to release the third edition of The CRISIL Mutual Fund Year Book, a one-stop insight on the mutual fund industry.

This is in line with our objective of making markets function better and improving connect with retail investors.

2012 was a turnaround year for the Indian capital markets. Equities emerged as the star performer with the benchmark CNX Nifty

gaining 28%. The debt market too performed well with long-term debt funds gaining prominence due to some easing of monetary

stance by the Reserve Bank of India (RBI) and expectations of further easing by the central bank to pump prime the economy. The

central bank announced a 25 basis points (bps) repo rate cut on January 29, 2013.

The mutual fund industry’s average assets under management (AUM) grew by 15% in 2012 to Rs 7.87 trillion in December 2012;

debt funds’ AUM rose by over 26% to Rs 5.34 trillion and equity funds’ AUM by 19% to Rs 1.92 trillion. This trend continued even in

2013 when industry AUM touched an all-time high of Rs 8.26 trillion in January 2013. Assets of gold exchange traded funds (ETFs)

climbed to Rs 11.7 billion (bn) in December 2012 as domestic gold prices increased by 12% over the year.

The focus on retail investors and improving the penetration of mutual funds continued through the year with Securities and

Exchange Board of India (SEBI) announcing various guidelines to promote investor education, reduce operational bottlenecks and

costs. The regulator directed fund houses to allocate 2 basis points of their AUM towards investor education initiatives. Meanwhile,

29 asset management companies (AMCs) conducted over ten thousand investor education programs in 200 cities covering nearly

two lakh participants during April 2012 to January 2013. Measures to improve mutual fund penetration included launch of the Rajiv

Gandhi Equity Savings Scheme (RGESS), which provides tax incentives to first-time equity investors. Further, SEBI doled out

incentives to fund houses that distribute their products beyond the top 15 cities. Single plan structures and introduction of direct

plans were other investor friendly measures introduced by the regulator.

It has always been CRISIL’s endeavour to help investors take better informed investment decisions. As part of our refreshed

content, the Year Book contains articles on select themes which were very pertinent in the year gone by and continue to hold

relevance. It also covers market and industry overview, key industry statistics, way forward and one-page factsheets on schemes

which were CRISIL Fund Rank 1 in all four quarters of 2012.

The CRISIL Mutual Fund Year Book is also available on www.crisil.com free of cost.

We hope you find the coverage informative.

Sandeep Sabharwal

Senior Director – Capital Markets

CRISIL Research

4

This page is intentionally left blank

5

Overview

6

This page is intentionally left blank

7

I - Mutual fund industry reports double digit growth

The domestic mutual fund industry’s average AUM rose by 15% Year-on-Year (y-o-y) to Rs 7.87 trillion in December 2012 while

month-end AUM rose by over 24% to Rs 7.60 trillion. In comparison, the industry had recorded a flat growth in 2011. The mutual

fund industry continued its positive AUM trend into 2013 and touched Rs 8.13 trillion in February, slightly lower than its all time high

of Rs 8.26 trillion achieved in January 2013.

Inflows into income and gilt funds led to asset growth in 2012

Inflows of Rs 613 bn into income funds (long-term debt funds, Fixed Maturity Plans (FMPs), short term and ultra-short term debt

funds) and gilt funds - on expectations of a fall in interest rates following slowing domestic growth - and easing inflation (see Figure

1) resulted in asset growth. Bond prices (Net Asset Value or NAVs) and interest rates (yields) move in opposite directions. Further,

funds with longer average portfolio maturities benefit more in a falling interest rate environment. Accordingly, long term debt

oriented funds benefit from a fall in interest rates and attract more AUM. The RBI lowered its key interest rate (Repo rate) by 0.50%

(50 bps) first in April 2012 and later by 25 bps in January 2013 to 7.75%. AUM of long term bond funds and gilt funds rose by over

317% (YoY) in 2012 to Rs 680 bn while that of short maturity debt funds (including liquid funds) rose by over 22% to Rs 2.31 trillion.

The debt category continued to corner a major share of mutual fund assets with 70% in 2012.

Figure 1: Year-wise mutual funds’ AUM and inflow/ outflows

* Month-end AUM as of December every year

Source: AMFI

Equity funds see profit booking though AUM grows with markets

AUM of equity funds rose by nearly 19% (y-o-y) to Rs 1.92 trillion as of December 2012. Equity funds rose on account of mark to

market gains - the benchmark CNX Nifty was up by 28% in 2012 mainly on reform measures announced by the Indian government

and inflows from foreign institutional investors (FIIs). Investors, however, booked profits in equity funds and the category witnessed

net outflows of Rs 156 bn during 2012 compared with inflows of Rs 77 bn in 2011. The CNX Nifty had fallen by over 24% in 2011.

Top 10 AMCs control 77% of AUM

The industry - consisting of 44 fund houses - continued to remain top heavy; as of December 2012, top five fund houses comprised

54% of AUM while the top 10 fund houses comprised 77% of AUM. The bottom 10 fund houses contributed less than 1% of the

AUM. HDFC Mutual Fund retained its top AUM position at Rs 1.02 trillion ( up Rs 130 bn y-o-y) as of December 2012 followed by

Reliance Mutual Fund at Rs 931 bn ( up Rs 87 bn y-o-y) and ICICI Prudential Mutual Fund at Rs 815 bn (up Rs 121 bn y-o-y). Birla

Sun Life Mutual Fund recorded the highest average growth in AUM, increasing by Rs 166 bn to Rs 770 bn during the year. Tata

Mutual Fund reported the highest decline in AUM in absolute terms, declining by Rs 17 bn to Rs 197 bn.

4,000

5,000

6,000

7,000

8,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

2008 2009 2010 2011 2012

(Rs in bn)(Rs in bn)

Inflows/ Outflows AUM* (RHS)

8

The industry also saw some consolidation with L&T Mutual Fund buying the assets of Fidelity Mutual Fund. AIG Mutual Fund

changed its name to PineBridge Mutual Fund. Srei Infrastructure and Parag Parikh Financial Advisory Services received SEBI’s

approval to start mutual fund business in India. Industry players who sold some of their stake to foreign / domestic players were as

follows -

■ Axis Bank inked an agreement with Schroder Singapore Holdings (wholly owned subsidiary of global AMC major Schroders) to

sell Axis Asset Management Company’s 25% share for an undisclosed amount.

■ Religare Enterprises Ltd sold 49% of its stake in Religare Asset Management Ltd to the US-based Invesco Ltd.

■ Bank of India acquired 51% stake in Bharti AXA Mutual Fund for an undisclosed amount.

■ Nippon Life Insurance bought a 26% stake in Reliance Capital Asset Management for close to Rs 14.50 bn.

Mutual funds lose around 24 lakh folios in 2012

While the industry’s assets increased, its investor base decreased over the 1-year period ended September 2012, according to the

Association of Mutual Funds in India (AMFI). The industry lost around 24 lakh folios i.e. investor accounts during the said period.

Most of the decline was seen in retail folios (especially in the equity category) as investors booked profits and exited the market

following the gains in underlying market during the calendar year. Debt mutual fund schemes however gained over 8 lakh folios

during the same period. This can be attributed to investors looking at relatively safer investment options post the volatility in the

domestic equity markets in 2011. This also indicates that retail investors are finding debt mutual funds increasingly attractive.

Corporates continued to dominate the mutual fund AUM with 46% share followed by high net-worth individuals (HNIs) with 25%

share and retail investors with 23% share as per the September 2012 folio data. Corporates had 60% share in the AUM of debt

oriented funds.

2012 - A year of regulations to improve mutual fund penetration

2012 was a watershed year for the mutual fund industry in terms of regulations / initiatives taken to improve penetration, promote

investor education, reduce complexities and provide direct access for informed investors. Following were the key regulations

announced during the year.

■ SEBI allowed AMCs to charge additional expenses, up to 30 bps, proportionate to the inflows from locations beyond the top 15

cities to improve the geographical penetration of mutual funds. However, the expenses will be reversed if the inflows are

redeemed within one year.

■ AMCs allowed fungibility across various expense heads in total expense ratio. This provides them increased flexibility to

allocate costs.

■ AMCs can annually set aside at least 2 bps of AUM for investor education initiatives.

■ To avoid differential treatment across investor classes, SEBI has directed all AMCs to follow a single expense structure across

plans from October 1, 2012 instead of plans based on the minimum investment amount (for instance institutional and super-

institutional plans). All funds now have only one plan across investor classes.

■ SEBI introduced ‘Direct Plans’ from January 1, 2013 through which investors can apply directly to the AMC instead of through

distributors. Such plans will have a lower expense ratio as these will not charge distribution expenses.

■ The government introduced the RGESS for first time equity investors with an annual income less than or equal to Rs 1 million.

They will be eligible for a 50% tax deduction under Section 80CCG (new section) on investments up to Rs 50,000 in pre-

defined stocks, close-ended mutual fund schemes (listed) and ETFs besides public offerings from select government

companies. The latest Union Budget proposed that the deduction will be allowed for three consecutive financial years while the

income limit was increased to Rs 1.2 mn.

■ SEBI allowed cash transactions in mutual fund schemes to the extent of Rs 20,000 to enhance the reach to small investors.

■ Mutual funds allowed to participate in repos in corporate debt securities with some riders.

■ SEBI stipulated a ceiling of 0.12% for cash market transactions and 0.05% for derivatives dealings with respect to brokerage

and transaction costs to investors.

9

■ Mark-to-market valuation component in debt securities applicable to those securities with a residual maturity of more than 60

days from September 30, 2012 compared to 91-days-and-beyond earlier.

■ Overseas individual investors allowed to invest up to US$1 bn in corporate bonds and debt schemes of mutual funds without

any lock-in period.

− SEBI allowed postal agents, retired officials from government, banks, retired teachers, etc. to distribute simple mutual fund

products, to spread out mutual fund distribution.

− AMFI issuing mutual fund Common Account Statement (CAS) in an electronic form, called ‘eCAS’; this will replace paper

statements.

Important Regulations Pertaining to Mutual Funds in the Union Budget

1. Securities Transaction Tax (STT) reduced for equity futures and mutual funds/ ETF redemptions. Further, only the seller of

units will need to pay STT. This will be effective from June 1, 2013.

2. Increased the rate of tax on distributed income (dividends) from 12.5% to 25% for all types of funds, other than equity oriented

funds, in all cases where distribution is made to an individual or a Hindu undivided family (HUF). This amendment will take

effect from June 1, 2013.

3. Introduction of a special taxation regime in respect of taxation of income of securitisation entities, wherein no additional income

tax shall be payable, if the income distributed by the securitisation trust is received by a person who is exempt from tax under

the Income Tax Act.

4. ETFs, debt mutual funds and asset-backed securities allowed as investments for provident and pension funds.

5. Mutual fund distributors can become members in the mutual fund segment of stock exchanges to leverage the stock

exchange’s network to improve their reach and distribution.

10

II - Way forward for the mutual fund industry

The Indian mutual fund industry has come a long way since entry loads were banned in 2009; when many stakeholders were

skeptical on the way forward. The industry has matured by introducing best practices, increasing the transparency levels and

raising the bar on investor friendliness. Exogenous factors such as regulatory changes, increased consolidation, market volatility

and varying risk appetite amongst investors have all contributed to its metamorphosis. The way ahead clearly involves steps to

making mutual funds a part of the common man’s portfolio. In this piece we have detailed a five-pronged strategy to do so.

1. Clarity in Product Positioning

Mutual funds’ AUM so far has been mainly dominated by institutional investors and HNIs. Retail investors have been largely

conspicuous by their meager presence as the share of mutual funds in household savings continues to be less than 5%. Only the

‘knowledgeable’ or ‘qualified’ investors know what to choose from. For example, corporates go for liquid and ultra short term funds.

HNIs, on the other hand, have used debt-oriented funds such as FMPs, long term income funds, gilt funds to their advantage. In

contrast, retail investors have mostly invested in equity funds, but have done so intermittently and not in a secular manner. Except

for the equity linked saving schemes (ELSS) category which is utilized for tax benefits under section 80C (includes a 3-year lock-in

period), retail investors largely exited equity funds in a bear phase (outflows) and entered in a bull phase (inflows) instead of the

other way round. The only category where retail interest has grown exponentially is in gold ETFs, mainly due to the long bull-run in

gold prices and general awareness about gold as an asset class.

AMCs thus need to sharpen and focus their product positioning for retail investors but at the same time keep it simple. Products

must be positioned clearly based on risk-reward potential. Investors, in turn, should take the help of financial planning specialists or

refer to independent rankings to select the right funds as well as periodically monitor their performance. In this direction, SEBI has

allowed allocation of 2 bps of AUM for investor education.

2. Consolidation of funds – need of the hour

The Indian mutual fund industry has about 1,250 unique funds across 44 AMCs, which further have around 8,000 options (growth,

dividend, re-investment with multiple frequencies - daily, monthly, quarterly, etc). In a country where financial literacy is low,

choosing among the vast expanse of funds is a major challenge. Investors need to choose from funds with similar or slight variation

in investment objective and funds whose names do not indicate much about their characteristic.

The need of the hour for AMCs is to consolidate funds with similar objectives as well as provide fund names that are simple to

understand and give some indication of the risk return trade-off and investment horizon. SEBI’s latest initiative on product labeling

that directs AMCs to colour code all funds based on risk and return measures besides its guidelines on single-plan structures in

October 2012 are key initiatives in this direction.

3. Innovation

Steve Jobs once said: “Innovation distinguishes between a leader and a follower.” It is true for any industry. Over the years,

different mutual fund products and services have caught investors’ attention – such as gold fund of funds / gold ETFs and

systematic investment plans (SIPs).

Mutual funds in developed markets have a higher penetration through innovative products which offer long-term wealth creation

options such as lifecycle and target maturity funds. In the US retirement industry, close to US$1 trillion or one-fifth of the total

US$4.7 trillion as of 2011 is invested in hybrid funds (a bulk of target date and lifestyle funds is counted in this category). The

nature of these products is such that the asset allocation between equity and fixed income is adjusted based on the investor’s time

horizon. Additionally, there are annuity products which provide regular income in the post-employment years.

India too needs many more innovations in the retirement space. According to the United Nations population statistics, India’s share

of people aged 65 and older is expected to increase from 5% to 14% between 2010 and 2050, while the share of the oldest age

11

group (80 years and older) is expected to triple from 1% to 3%. With only 12% of India’s current population under pension

coverage, the need for innovation in this space is very high. Many simple innovations could be looked at like fixed income ETFs,

real estate ETFs, strategy-based ETFs among others. Besides innovative products, out-of-the-box thinking is also required on the

distribution side especially to target more new investors.

4. Technology - a key driver

Investors must be aware that information on funds such as portfolio composition, return comparison with the stated benchmark and

fund management details are available on AMC sites. Transparency and easy access to funds will increase investor confidence.

With more than half the country owning mobile phones, the latter will clearly emerge as the communication medium in the years

ahead. Language barriers and financial illiteracy can be reduced with multi-lingual applications that can be accessed through

handheld devices and on social media. Technology will also help in straight-through processing of trades through the remotest

corner of the country, besides collation and analysis of customer behaviour so as to help sell mutual funds in an effective manner.

Fund houses can assist clients in tracking their portfolios through intermediary platforms and wrap services (consolidates and

manages an investor’s portfolio or financial plans through a single window). Investors can thus view their entire portfolio at a single

click, enabling them to track their current financial position on a daily basis as well as receive alerts. They can also understand their

total tax liability and maintain documentation of all purchases, sales, deposits and withdrawals in one repository.

5. Banks to play a bigger role

The first point of contact for the common man with the financial world is the local bank branch. With more than 80,000 bank

branches spread across India, mutual fund penetration can significantly improve even if 50% of these branches are trained to sell

mutual funds. With majority of AUM concentrated in the metros, the banking network can help expand the reach of mutual funds

across the length and breadth of the country. SEBI’s recent regulation which allows AMCs to charge an additional 0.30% on inflows

coming from beyond the top 15 towns is a welcome step towards ensuring larger and diverse retail participation. It is encouraging

to note that the data on commissions published by AMFI indicates that the banking sector is the largest distributor segment,

accounting for 42% of the total commissions paid in 2011-12.

The following steps can be considered to increase mutual fund penetration through banks:

■ Dedicate efforts towards training of banks’ staff.

■ Invest in financial planning tools to facilitate customers.

■ Use the ATM network to enable customers to buy and sell mutual fund units.

■ Mutual funds and banks could jointly work on investor awareness programmes along with independent industry experts.

■ Have a bank-like experience while investing in mutual funds such as updating performance of funds in a mutual fund passbook

through any bank branch.

Summing up

The future of the mutual fund industry rests in the twin-power of increasing financial literacy and showcasing the suitability of mutual

funds in an investor’s portfolio. AMCs and product distributors need to work closely to achieve the target of higher penetrat ion of

mutual funds in household savings. The launch of RGESS is a step in the right direction – to encourage the first-time investor to

look at mutual funds for tax and investment planning. Quintessentially, a more investor-friendly approach in product development,

communication and distribution would go a long way in making mutual funds a pull product.

12

III - Equity market up 28% in 2012

The Indian equity market improved significantly in 2012 with the benchmark index CNX Nifty rising around 28% to recover most

losses witnessed in the previous calendar year when the index was down by 24%. The sharp gains were led by a mix of positive

domestic and global news. A strong reform stance taken by the Indian government - the much-awaited foreign direct investment

(FDI) in retail, airlines, trading exchanges, raising FDI cap in broadcast services, restructuring state-owned power distribution

companies and fuel price hike to address the burgeoning fiscal deficit - helped market sentiments. Further, the government’s strong

resolve to curtail fiscal deficit and promote growth followed by liquidity-infusing measures and interest rate cuts announced by the

RBI along with strong quarterly earnings from index majors added to the gains. The central bank cut the cash reserve ratio (CRR)

by a total of 1.75% over the year and the repo rate by 0.5% in April 2012 and by another 0.25% in January 2013.

Near-record buying by FIIs during the year was also an important factor in propelling the markets. FIIs were net buyers of equities

aggregating Rs 1.29 trillion in 2012, the second highest on record after Rs 1.33 trillion of buying seen in 2010 and compared with

net selling of Rs 34 bn in 2011.

Figure 2: FII inflows vs CNX Nifty Movement

Source: SEBI, NSE

Strong global cues included global central banks’ liquidity easing stance as well as some signs of easing of the European debt

crisis amidst approval of bailout funds for the critically impacted countries. The US Federal Reserve proposed to enhance its bond-

buying (stimulus) program by $85 bn per month and resolved to keep interest rates at record lows until mid-2015. The European

Central Bank (ECB) too unveiled a new bond-buying programme aimed at containing the region's debt crisis.

Market gains were capped amid signs of economic weakness in the domestic and global economies. The Indian economic growth

is expected to slide to 5% in 2012-13 as per the latest Economic Survey, the lowest growth rate in almost 10 years. The global

economy too has shown deceleration with the International Monetary Fund (IMF) calculating growth at 3.2% for the calendar year

2012, down from 3.9% seen in the previous year. Worries on the fiscal cliff in the US and lack of any final resolution for the euro

zone debt crisis later in the year also capped gains for the Indian equity market.

-20

36

92

148

204

260

4,500

4,800

5,100

5,400

5,700

6,000

De

c-1

1

Ja

n-1

2

Fe

b-1

2

Mar-

12

Ap

r-1

2

Ma

y-1

2

Ju

n-1

2

Ju

l-1

2

Aug

-12

Sep

-12

Oc

t-1

2

No

v-1

2

De

c-1

2(FII Inv Rs bn)(CNX Nifty)

FII monthly net investment (Rs Bn) CNX Nifty Value

13

Table 1: Movement of Key Equity Market Indices

Index 31-Dec-12 30-Dec-11 Absolute Change % change

CNX Nifty 5905.10 4624.30 1280.80 27.70

CNX 100 5847.50 4477.35 1370.15 30.60

CNX Bank 12474.25 7968.65 4505.60 56.54

CNX Realty 281.30 184.20 97.10 52.71

CNX FMCG 15175.25 10217.15 4958.10 48.53

CNX Auto 4830.55 3390.55 1440.00 42.47

CNX Mid Cap 8505.10 6111.85 2393.25 39.16

CNX Small Cap 3710.15 2711.85 998.30 36.81

CNX Pharma 6035.00 4576.25 1458.75 31.88

CNX Infra 2585.00 2124.90 460.10 21.65

CNX Commodities 2522.40 2113.85 408.55 19.33

CNX Metal 2900.25 2464.60 435.65 17.68

CNX Energy 7927.40 6968.10 959.30 13.77

CNX IT 6024.95 6139.00 -114.05 -1.86

*Sectors sorted by highest to lowest in terms of % change

Source: NSE

All sectoral indices ended higher in 2012 barring the CNX IT Index (down 1.86%) (see Table 1). Interest rate-sensitive sectors such

as CNX Bank and CNX Realty were up 56.5% and 52.7%, respectively, on strong buying following expectations of more interest

rate cuts by the RBI. CNX FMCG soared 48.5% as investors followed defensive sectors amidst the volatility seen in the market.

The sector benefitted from strong earnings reports from index majors such as Hindustan Unilever (HUL). CNX IT was the only

laggard, as the export-oriented sector was impacted by signs of a slowdown in the global economy, especially the US. Weak

earnings report from index major Infosys also brought down the index in the year.

Table 2: Movement of Key Global Equity Market Indices

Indices 31-Dec-12 30-Dec-11 Absolute Change % Change

Dow Jones Industrial Average 13104.14 12217.56 886.58 7.26

Nasdaq Composite 3019.51 2605.15 414.36 15.91

FTSE 100 (London) 5897.81 5572.28 325.53 5.84

Nikkei 225 (Japan) 10395.18* 8455.35 1939.83 22.94

Straits Times (Singapore) 3167.08 2646.35 520.73 19.68

Hang Seng (Hong Kong) 22656.92 18434.39 4222.53 22.91

*Data as of December 28, 2012

Global equity markets too reported a positive trend; key global equity indices analysed closed positive in 2012 (see Table 2). The

positive growth for global equities was led by the US markets which rose on hopes of domestic economic recovery, especially after

the US Federal Reserve enhanced its bond-buying program in the year. Re-election of Barack Obama as the US President and

abatement of the US fiscal crisis also aided the US markets. Global equities were supported by measures taken in Europe to ease

the debt crisis in the form of easy monetary stance adopted by major central banks and approval of bailout to highly fiscal debt-

ridden countries in the region.

Japan’s Nikkei was the biggest index gainer, up around 23% as the export-oriented index was helped by weakening of yen

throughout the year. The index was also helped by stimulus measures both fiscal and monetary-induced in the country during the

year. Hong Kong’s Hang Seng came a close second, helped by the positive global cues and hopes of revival in growth in the

domestic economy. Meanwhile, Britain’s FTSE gained the least, up around 6% as gains for the index were capped by weak

domestic economic indicators and worries about the European debt crisis.

14

IV - Gilt prices surge as RBI cuts Repo rate

Inter-bank call money rates ranged mostly near the repo rate during the year amid strong demand from banks. Spike in call rates

was seen during periods of higher demand such as quarter-ends due to advance tax outflows, fiscal year end on March 31, 2012

and reporting fortnights. Widening of the liquidity deficit in the banking system due to higher withdrawals and rise in credit

disbursement during the festival season also put pressure on call rates during November. The RBI tried to cap any major spike in

call rates through its liquidity infusing measures mainly a 175 bps (1.75%) cut in the CRR over the year at regular intervals and

open market operations (OMOs) to buy back gilts. A cut in the key interest rate viz., the repo rate by 50 bps (0.50%) to 8.00% in

April 2012 also helped reduce call money rates. The RBI announced two more 25 bps repo rate cuts in its January and March

policy review in 2013.

Figure 3: Movement of MIBOR vis-à-vis Repo and LAF

Source: NSE, RBI

Gilt prices rose in the calendar year especially in the second half driven by expectations of monetary easing by the RBI following

signs of slowing gross domestic product (GDP) growth and fall in the inflation rate (wholesale price index or WPI). India’s GDP is

expected to slow down to 5% growth rate in 2012-13 as per the Central Statistical Office (CSO) compared with 6.2% seen in the

previous fiscal. CRISIL Research also expects that growth in the Indian economy is likely to fall below the 5% mark in the second

half of the current financial year. The WPI inflation rate fell to 7.18% in December 2012 compared with 7.74% in the year ago

period. This fell further to 6.84% in February 2013, however higher compared to a three year low of 6.62% in January 2013.

The repo rate cut coupled with other liquidity infusing measures by the RBI also augured well for gilts. Sentiments for gilts improved

due to strong measures by the central government to reduce fiscal deficit pressures and raising of FIIs limits in gilts by $5bn to

$15bn. The yield on the 10-year benchmark paper 8.15%, 2022 fell to 8.05% as of December 31, 2012, down 51 bps from 8.56% in

the year ago period. The yield sharply declined further to 7.87% as of February 28, 2013 on expectations of more repo rate cuts

ahead.

0.00

0.50

1.00

1.50

2.00

2.50

7%

8%

9%

10%

11%

12%

13%

31-D

ec

-11

26

-Ja

n-1

2

21-F

eb-1

2

18-M

ar-

12

13

-Apr-

12

09

-Ma

y-1

2

04

-Jun

-12

30

-Ju

n-1

2

26

-Ju

l-12

21-A

ug-1

2

16-S

ep-1

2

12

-Oct-

12

07-N

ov

-12

03-D

ec

-12

29-D

ec

-12

(Rs Trillion)(% yield)

Mibor Repo LAF (RHS)

15

Figure 4: Movement of the 10-year G-Sec yield

Source: CRISIL Fixed Income Database

Table 3: Key Debt Market Indicators / Yield

31-Dec-12 31-Dec-11 31-Dec-12 31-Dec-11

Call 9.50% 8.55% 10 year AAA 8.92% 9.41%

CBLO 8.66% 7.45% Cash Reserve Ratio (CRR) 4.25 6.00

Repo Rate 8.00% 8.50% Statutory Liquidity Ratio (SLR) 23.00 24.00

3 month CP 8.99% 9.65% Government Bonds Outstanding (Rs. Bn) 31966 26710

3 month CD 8.44% 9.37% Corporate Bonds Outstanding (Rs. Bn) 333 395

91-day T Bill 8.16% 8.58% Primary Issuances during the year (Rs.Bn) 3363 2431

365 day T Bill 8.00% 8.28% Bank Credit (Rs Bn) 50272 43656

1 year AAA 8.85% 9.69% Bank Deposits (Rs Bn) 64773 58279

1 Year CP 9.45% 10.10% Credit Deposit Ratio 77.61 74.91

1 Year CD 8.75% 9.67% FII Debt Yearly Net Investments (Rs Bn) 354 408

5-year G-Sec 8.03% 8.43% WPI Inflation 7.18% 7.74%

10-year G-Sec 8.05% 8.56% CPI Inflation 11.17% 6.49%

Source: CRISIL Fixed Income Database

8.0%

8.2%

8.4%

8.6%

8.8%

31-D

ec-1

1

31

-Jan

-12

29-F

eb

-12

31

-Ma

r-1

2

30

-Apr-

12

31-M

ay

-12

30

-Ju

n-1

2

31

-Ju

l-12

31-A

ug-1

2

30-S

ep-1

2

31

-Oct-

12

30-N

ov

-12

31-D

ec-1

2

10 Yr G-Sec Yield

16

This page is intentionally left blank

17

Category wise mutual fund performance

18

I - Category wise risk / return trade-off & indicative investment horizons

S

No

Fund

Type

Investment

Category Investment Universe

Benchmark

Index

Expected

Returns Risk

Indicative

Investment

Horizon

1 Large Cap

Equity

Equity Oriented

Funds

Funds that invest predominantly in large

cap stocks

CNX Nifty High High More than 5

years

2 Diversified

Equity

Equity Oriented

Funds

Funds that invest in stocks across

market capitalisation and sectors

CNX 500 High High More than 5

years

3 Small and

Midcap

Equity

Equity Oriented

Funds

Funds that invest predominantly in small

and mid-cap stocks

CNX Midcap Very High Very High More than 5

years

4 ELSS Equity Oriented

Funds

Diversified equity funds that have a 3

year lock - in period and provide income

tax exemption under section 80 C upto

Rs 1 lakh

CNX 500 High High More than 5

years

5 Index Equity Oriented

Funds

Funds that track an index and invest

into companies in the same proportion

as that index. These funds seek to

provide returns (pre-expenses) in line

with the index. Exchange traded index

funds can be traded on an exchange

The index

that is

tracked by

the fund.

High High 5 years

6 Arbitrage Equity Oriented

Funds

Funds that buy equity securities in the

cash market and sell them in the futures

market. These funds seek to generate

returns through the mispricing that

exists between the cash and futures

markets. In these funds all the stocks

are completely hedged

CRISIL

Liquid Funds

index

Low Low More than 1

year

7 Thematic

Equity

Equity Oriented

Sector Funds

Sector funds that invest in companies

from a specified sector. Most common

sector themes are infrastructure and

banking

Relevant

sectoral

indices

Very High Very High More than 5

years

8 Capital

Protected

Equity Oriented

Hybrid Funds

Funds that follow an investment

structure which seeks to protect the

initial investment from capital erosion

CRISIL

Monthly

Income

Plans Index

/ CRISIL

Balanced

Funds Index

Low Low 3-5 years

9 Balanced Equity Oriented

Hybrid Funds

Funds that invest at least 65% of the

corpus into equity stocks and the

remainder into debt securities

CRISIL

Balanced

Fund Index

Moderate Moderate 5 Years

10 FMPs Debt Oriented

Funds

Closed ended mutual fund schemes

with predefined maturities (30 days to 5

years) that invest predominantly in CDs,

CPs and debentures whose maturity or

tenure matches with that of the scheme.

The basic objective of FMPs is to

generate steady returns over a fixed

tenure

Usually

compared

with FD

rates

Moderate Moderate 30 days to 5

years

19

S

No

Fund

Type

Investment

Category Investment Universe

Benchmark

Index

Expected

Returns Risk

Indicative

Investment

Horizon

11 Liquid Debt Oriented

Funds

Funds that invest into short term

corporate debt papers, CDs and money

market instruments with a residual

maturity of up to 91 days

CRISIL

Liquid Funds

index

Very Low Very Low Less than

90 days

12 Ultra Short

Term

Debt Oriented

Funds

Funds that invest into short term

corporate debt papers, CDs, money

market instruments and government

securities but whose maturity profile is

upto 1 year. It lies between liquid funds

and short term income funds

CRISIL

Liquid Funds

index

Low Very Low Less than 1

year

13 Short-term

Income

Debt Oriented

Funds

Funds that invest into short term

corporate debt papers, CDs, money

market instruments and government

securities and whose maturities are

beyond that of ultra short debt funds

and upto 3 years.

CRISIL

Short Term

Bond Funds

index

Moderate Low More than 1

year

14 Long-term

Income

Debt Oriented

Funds

Funds that invest in long-term corporate

debt papers and government securities

and whose maturities range between

few months and can go even beyond 25

years depending on the prevalent

interest rate scenario

CRISIL

Composite

Bond Funds

index

Moderate Moderate 3 years

15 Gilt Debt Oriented

Funds

Funds that invest in securities issued by

the central and state governments and

whose maturities range between few

months and can go even beyond 25

years depending on the prevalent

interest rate scenario

CRISL Gilt

Index

Moderate Moderate 3 years

16 Monthly

Income

Plans

Debt Oriented

Hybrid Funds

Hybrid funds that invest a small portion

(15-30%) in equity stocks and seek to

declare monthly dividends based on

cash flows

CRISIL

Monthly

Income

Plans Index

Moderate Moderate 3 Years

17 Gold ETFs Gold Funds that invest in physical gold and

seek to track the domestic spot price of

gold. These funds are traded on an

exchange

CRISIL Gold

Index

Moderate Moderate 5 years

20

II - Equity & Hybrid Equity - Small & Midcap Funds outperform

Category Average Returns % 1 Year 2 Years 3 Years 5 Years 7 Years 10 Years

Large Cap Equity Funds 29.19 -0.23 5.48 0.09 12.34 22.83

Diversified Equity Funds 32.33 0.66 6.58 1.06 12.42 25.27

Small & Midcap Funds 41.69 3.36 9.52 0.99 12.20 28.03

ELSS 32.05 0.33 6.14 -0.83 9.11 22.82

Index Funds 27.72 -1.78 4.22 -1.29 10.18 17.37

International Equity Funds 17.64 3.15 5.20 1.73 8.08 NA

Hybrid Equity (Balanced Funds) 26.99 3.98 7.87 4.07 12.23 18.55

Benchmark Indices

CNX Nifty 27.70 -1.89 4.32 -0.77 11.03 18.35

CNX 500 31.84 -2.02 3.09 -2.39 9.83 19.88

CNX Smallcap 36.81 -4.88 2.09 -8.54 7.83 NA

CNX Midcap 39.16 -2.01 4.59 -1.56 11.24 23.82

S&P 500 International 13.41 6.48 8.54 -0.58 1.92 4.94

CRISIL Balanced Funds index 21.28 1.89 5.64 2.83 10.15 14.17

Point-to-Point returns as of December 31, 2012

Categories as per CRISIL Mutual Fund Ranking of December 2012 except International Funds

Returns are annualised for a period of more than 1-year

Highlighted cells denote the maximum returns in that time period

Analysis

All equity oriented categories ended in the positive in 2012 due to upbeat domestic equity markets. The small and midcap category

was the biggest gainer in the year, up nearly 42% mainly on the back of a rally in mid-cap stocks. The CNX Midcap index was also

up by 39% in 2012. This category also outperformed other categories in the 3 and 10 year period. Diversified equity funds were the

topmost gainers in the 7 year period. The equity oriented hybrid category, represented by balanced funds, performed strongly in the

year 2012, with returns of 27% marginally lower than those of the CNX Nifty index. These funds mainly benefitted due to their

dynamic allocation to equities, which rose during the year in a bullish market. A reduction in key interest rates also benefited the

debt component of these funds as interest rates and bond prices move in opposite directions. Thus bonds benefit when interest

rates fall. These funds also outperformed other equity categories in 2 and 5 year period.

21

III - Sector / Thematic - Banking Funds dominate 2012, Gold Funds lose lustre

Category Average Returns % 1 Year 2 Years 3 Years 5 Years 7 Years 10 Years

Sector Funds - FMCG 40.81 27.19 26.43 12.96 18.44 29.39

Sector Funds - Pharma & Healthcare 32.23 9.84 16.96 13.71 14.68 NA

Sector Funds - Banking & Finance 55.64 1.60 11.87 6.65 18.30 NA

Sector Funds - IT 6.34 -7.54 2.80 -0.50 7.36 17.23

Thematic - Infra 28.34 -7.84 -3.31 -8.43 9.69 9.51

Gold Funds* 11.09 20.39 20.86 21.96 NA NA

Benchmark Indices

CNX FMCG 48.53 26.95 28.14 19.09 19.24 21.37

CNX Pharma 31.88 8.92 17.09 13.70 15.36 19.40

CNX Bank 56.54 2.85 11.36 4.80 15.54 26.08

CNX IT -1.86 -10.30 1.17 4.59 6.38 -10.88

CNX Infrastructure 21.65 -13.52 -10.46 -15.54 3.84 NA

CRISIL Gold Index 11.95 21.62 22.05 23.28 NA NA

Point-to-Point returns as of December 31, 2012

Returns are annualised for a period of more than 1-year

Thematic Infrastructure category based on CRISIL Mutual Fund Ranking for December 2012

*includes ETFs and Fund of Funds

Highlighted cells denote the maximum returns in that time period

Analysis

In the sector and thematic funds category, Banking & Finance dominated in 2012 and were up by 56% on expectations of interest

rate cuts by the RBI thus reducing the cost of funds for the sector. The RBI cut the key repo rate by 0.50% in April 2012 and by

0.25% in January 2013. Defensive sectors like FMCG, Pharma & Healthcare were the next best performers as volatile markets

prompted investors to go for stocks of these sectors as well. IT sector funds were the worst performers in 2012 as the export

oriented sector was plagued by worries of slowdown in the global economy and weak earnings report from index majors. FMCG

sector funds dominated the performance of longer periods like 2, 3, 7 and 10 years.

Gold funds, especially Gold ETFs, which have seen huge demand in the past two years, posted lacklustre performance in 2012 due

to range bound gold prices. However, these funds have given nearly 22% annualised returns in the 5-year period of their existence.

22

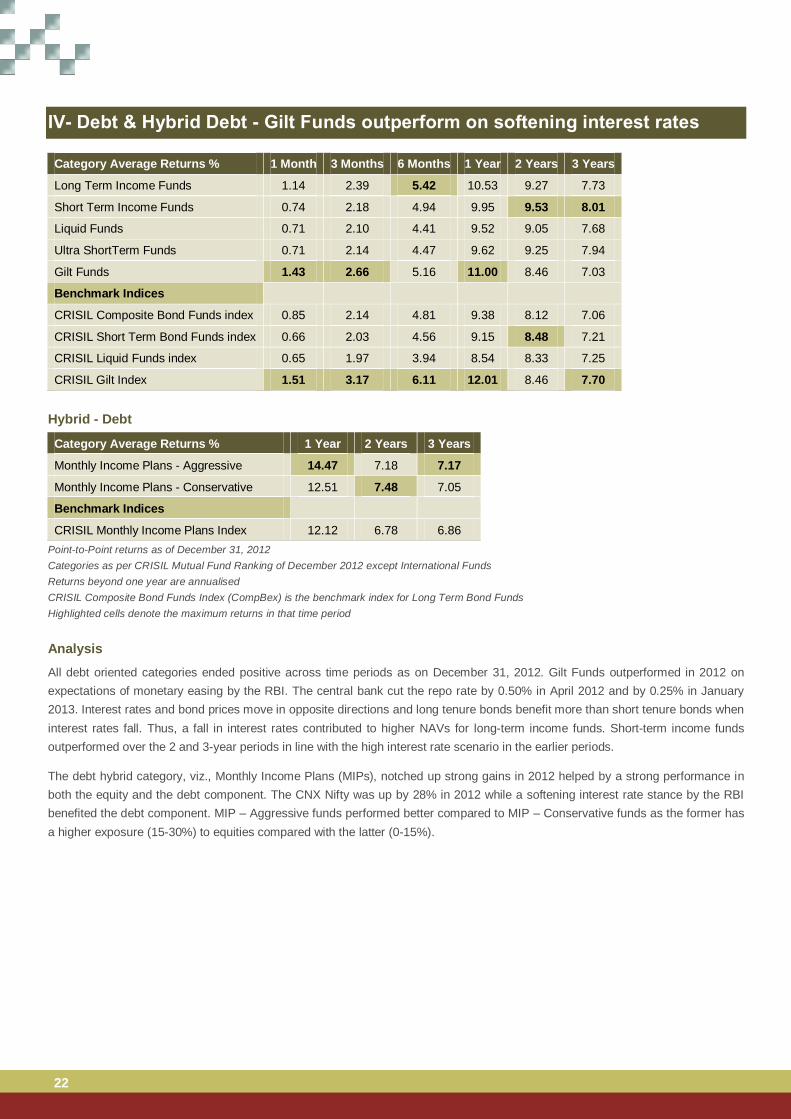

IV- Debt & Hybrid Debt - Gilt Funds outperform on softening interest rates

Category Average Returns % 1 Month 3 Months 6 Months 1 Year 2 Years 3 Years

Long Term Income Funds 1.14 2.39 5.42 10.53 9.27 7.73

Short Term Income Funds 0.74 2.18 4.94 9.95 9.53 8.01

Liquid Funds 0.71 2.10 4.41 9.52 9.05 7.68

Ultra ShortTerm Funds 0.71 2.14 4.47 9.62 9.25 7.94

Gilt Funds 1.43 2.66 5.16 11.00 8.46 7.03

Benchmark Indices

CRISIL Composite Bond Funds index 0.85 2.14 4.81 9.38 8.12 7.06

CRISIL Short Term Bond Funds index 0.66 2.03 4.56 9.15 8.48 7.21

CRISIL Liquid Funds index 0.65 1.97 3.94 8.54 8.33 7.25

CRISIL Gilt Index 1.51 3.17 6.11 12.01 8.46 7.70

Hybrid - Debt

Category Average Returns % 1 Year 2 Years 3 Years

Monthly Income Plans - Aggressive 14.47 7.18 7.17

Monthly Income Plans - Conservative 12.51 7.48 7.05

Benchmark Indices

CRISIL Monthly Income Plans Index 12.12 6.78 6.86

Point-to-Point returns as of December 31, 2012

Categories as per CRISIL Mutual Fund Ranking of December 2012 except International Funds

Returns beyond one year are annualised

CRISIL Composite Bond Funds Index (CompBex) is the benchmark index for Long Term Bond Funds

Highlighted cells denote the maximum returns in that time period

Analysis

All debt oriented categories ended positive across time periods as on December 31, 2012. Gilt Funds outperformed in 2012 on

expectations of monetary easing by the RBI. The central bank cut the repo rate by 0.50% in April 2012 and by 0.25% in January

2013. Interest rates and bond prices move in opposite directions and long tenure bonds benefit more than short tenure bonds when

interest rates fall. Thus, a fall in interest rates contributed to higher NAVs for long-term income funds. Short-term income funds

outperformed over the 2 and 3-year periods in line with the high interest rate scenario in the earlier periods.

The debt hybrid category, viz., Monthly Income Plans (MIPs), notched up strong gains in 2012 helped by a strong performance in

both the equity and the debt component. The CNX Nifty was up by 28% in 2012 while a softening interest rate stance by the RBI

benefited the debt component. MIP – Aggressive funds performed better compared to MIP – Conservative funds as the former has

a higher exposure (15-30%) to equities compared with the latter (0-15%).

23

Articles

24

This page is intentionally left blank

25

I - The Science of Financial Planning - Next Frontier for Investment Advisors

The Indian cricket team made history by winning the recent Border-Gavaskar Trophy 4-0 against Australia, the first clean sweep

four test match series for the Indian cricket team in its history of 80 years. Was Indian skipper Mahendra Singh Dhoni merely lucky

or was it hard-work, planning, perseverance and the team work that led to the win? As all of us would agree - it was clearly the

latter. The same traits matter even while planning for one’s finances. It is important to plan right from the time we receive our first

pay-cheque so that we can achieve our various financial goals – the idea is to sow now to reap later.

Most of us usually negate the need for an expert to guide us in planning investments for the future. This may have been acceptable

in the 90s when the domestic financial markets were still under developed. Today, after witnessing a 180-degree shift, we have a

plethora of financial products across asset classes to choose from. Thus, by only investing in traditional financial products like bank

fixed deposits, postal savings and money back insurance policies, we are missing out on a big opportunity to achieve our goals

faster.

Today, to know the best possible way to achieve the financial goals, one has to engage in a more detailed exercise – a.k.a.

financial plan - to ensure our goals are achieved with greater confidence. Financial planning is the process of meeting lifetime

goals through proper management of finances. Lifetime goals may include buying a house, saving for children’s education or

planning for retirement. With the advancement of technology and availability of financial tools, financial planning has evolved and

become more scientific. Table 4 denotes the difference between traditional and scientific financial planning.

Table 4: Scientific Financial Planning versus Non-Scientific (Traditional) Financial Planning

Scientific Financial Planning Non-Scientific Financial Planning

Looks at a more holistic picture of assets and liabilities,

income, expenses and goals

Uses a macro view of an individual’s finances and looks only

at surplus after expenses

Considers every goal and maps products to each goal

separately

Only looks at major financial goals

Plan prepared by specialists like certified financial planners Plan prepared by the next door financial advisor with an

objective of selling the product rather than meeting the specific

needs

These are strategic long-term plans and are only monitored for

product performance; rebalancing is done to maintain asset

allocation

Plans are not sacrosanct but change at short notice

Products recommended based on an individual’s risk profile

across asset classes like equity, debt and gold

‘One size fits all’ traditional product portfolio and includes bank

fixed deposits, postal deposits and traditional insurance

policies; largely debt focused

There is a complete audit trail of all recommendations and

changes proposed in the plan at any time

There is no audit trail of recommendations

Insurance is planned to support exigencies of an individual and

are largely term policies

Insurance is looked upon as an investment (money back

policies) and not as a support for extreme exigencies

Medical insurance is part of the financial planning process Most individuals are not covered under medical insurance

Process involves regular interactions with the financial planner Process is mostly a one-time exercise

26

Scientific financial planning - the process

Scientific financial planning is a five-step process: (i) data gathering and risk profiling through a questionnaire, (ii) analysing needs/

goals, (iii) asset allocation, (iv) product recommendation (including insurance), and (v) portfolio monitoring.

1. Data gathering and risk profiling: Involves analysing information about the person’s financial situation (details of assets,

liabilities, income, expenses and investments) and administering a questionnaire to assess one’s risk appetite. Based on the

answers (which are scored), the final score is mapped to a risk profile from low risk appetite to high risk appetite viz.,

conservative, moderate, moderately aggressive, aggressive and very aggressive.

2. Needs analysis: Involves a discussion on an individual’s financial needs such as debt repayment obligations, funds required

for children’s education/marriage, leisure and travel as well as charity if needed. A financial planner then prepares a cash flow

statement based on the current state of finances and investments to check whether all goals can be met in the desired time.

Table 5: A Typical Cash flow Statement

Calendar

year

Income

(growing by

10% p.a.)

Liabilities

like EMI

etc

Lifestyle

Expenses

(growing by

10% p.a.)

Disposable

Income that

flows into

investments (g)

Value of

Investments

(growing by

12% p.a.)

Goals Goal Status

a b c d=a-b-c g h

Year 1 500,000 125,000 250,000 125,000 - -

Year 2 550,000 125,000 275,000 150,000 140,000 -

Year 3 605,000 125,000 302,500 177,500 324,800 -

Year 4 665,500 125,000 332,750 207,750 562,576 -

Year 5 732,050 125,000 366,025 241,025 862,765 500,000 Bought a Car - Goal Met

Year 6 805,255 125,000 402,628 277,628 676,245 -

Year 7 885,781 125,000 442,890 317,890 1,068,337 500,000

Marriage Expenses-Goal

Met

Year 8 974,359 125,000 487,179 362,179 992,575 -

Year 9 1,071,794 125,000 535,897 410,897 1,517,324 -

Year 10 1,178,974 125,000 589,487 464,487 2,159,608 1,000,000

Down payment for a

second home - Goal Met

Goals are subtracted partly from disposable income and partly from investment value

Table 5 shows a typical cash flow based on annual income, expenses, liabilities like EMI, net disposable income after

subtracting income from expenses / liabilities. The investor’s three goals, i.e., car, marriage and down-payment of second

home are met through disposable income and partial withdrawal of investments. It is possible to improve these cash flows and

meet additional goals through scientific financial planning wherein investments would be optimally deployed based on risk

profile and asset allocation.

3. Asset allocation: This basically maps an investor’s risk appetite to a portfolio which contains a mix of asset classes (say

equity, debt and gold). The portfolio is allocated across these asset classes in an optimal manner based on a mathematical

model. Accordingly, an investor with a lower risk appetite (conservative) will have a higher allocation to debt while an investor

with a higher risk appetite (very aggressive) will have higher allocation to equity.

27

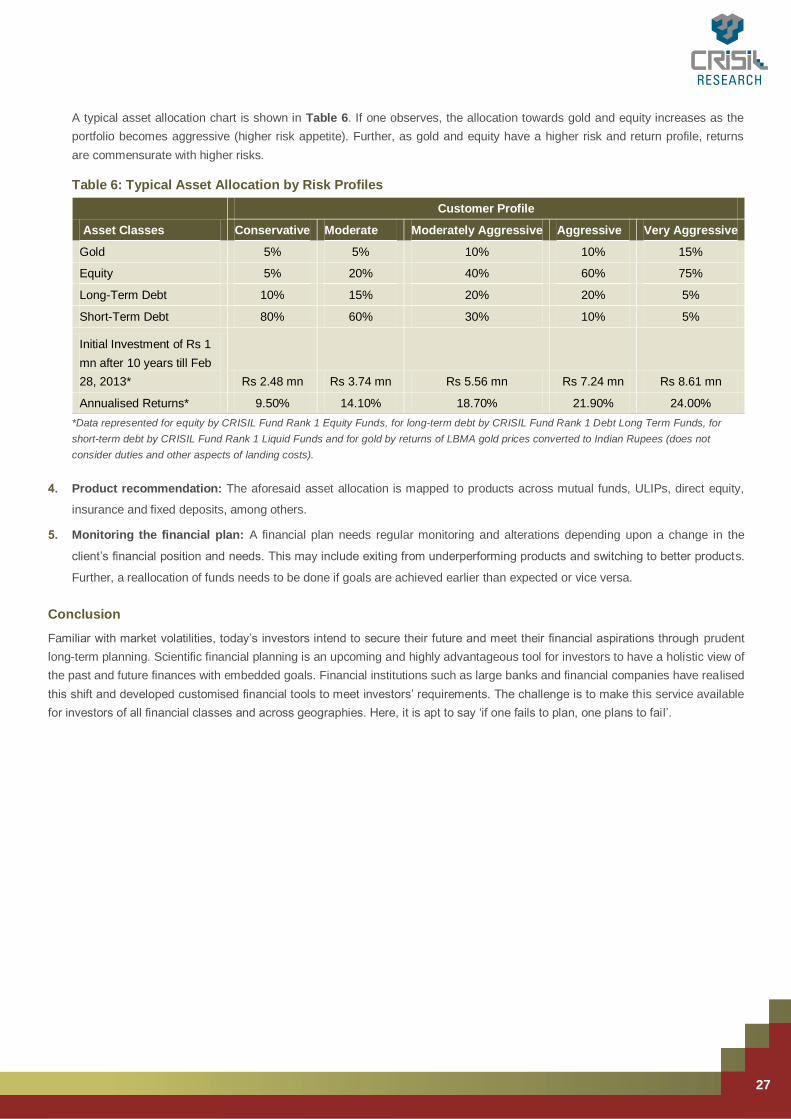

A typical asset allocation chart is shown in Table 6. If one observes, the allocation towards gold and equity increases as the

portfolio becomes aggressive (higher risk appetite). Further, as gold and equity have a higher risk and return profile, returns

are commensurate with higher risks.

Table 6: Typical Asset Allocation by Risk Profiles

Asset Classes

Customer Profile

Conservative Moderate Moderately Aggressive Aggressive Very Aggressive

Gold 5% 5% 10% 10% 15%

Equity 5% 20% 40% 60% 75%

Long-Term Debt 10% 15% 20% 20% 5%

Short-Term Debt 80% 60% 30% 10% 5%

Initial Investment of Rs 1

mn after 10 years till Feb

28, 2013* Rs 2.48 mn Rs 3.74 mn Rs 5.56 mn Rs 7.24 mn Rs 8.61 mn

Annualised Returns* 9.50% 14.10% 18.70% 21.90% 24.00%

*Data represented for equity by CRISIL Fund Rank 1 Equity Funds, for long-term debt by CRISIL Fund Rank 1 Debt Long Term Funds, for

short-term debt by CRISIL Fund Rank 1 Liquid Funds and for gold by returns of LBMA gold prices converted to Indian Rupees (does not

consider duties and other aspects of landing costs).

4. Product recommendation: The aforesaid asset allocation is mapped to products across mutual funds, ULIPs, direct equity,

insurance and fixed deposits, among others.

5. Monitoring the financial plan: A financial plan needs regular monitoring and alterations depending upon a change in the

client’s financial position and needs. This may include exiting from underperforming products and switching to better products.

Further, a reallocation of funds needs to be done if goals are achieved earlier than expected or vice versa.

Conclusion

Familiar with market volatilities, today’s investors intend to secure their future and meet their financial aspirations through prudent

long-term planning. Scientific financial planning is an upcoming and highly advantageous tool for investors to have a holistic view of

the past and future finances with embedded goals. Financial institutions such as large banks and financial companies have realised

this shift and developed customised financial tools to meet investors’ requirements. The challenge is to make this service available

for investors of all financial classes and across geographies. Here, it is apt to say ‘if one fails to plan, one plans to fail’.

28

II - Declining interest rate scenario - Long-term debt funds to benefit

After a strict interest rate regime through 2010 and 2011, the RBI eased its monetary stance in April 2012. It cut its benchmark

lending rate - the repo rate - by a total of 100 bps (1%) between April 2012 and now; 7.5% as of March 2013. In such a scenario,

long-term debt funds emerge as an appropriate tool of investment. This category typically generates superior returns in a falling

interest rate environment.

Interest rate cuts are an upshot of slowing domestic growth rate and fall in inflation. As per the Economic Survey released in

February 2013, India’s GDP is expected to grow at 5% in 2012-13 compared with 6.2% and 9.3% growth in 2011-12 and 2010-11,

respectively. Inflation measured by the Wholesale Price Index (WPI) was 6.84% in February 2013, down from 7.56% a year ago,

but higher compared to the three-year low of 6.62% in January 2013. The RBI has warned that high current account deficit (CAD)

and inflationary expectations limit the possibility of further rate cuts. CRISIL Centre for Economic Research (CCER) expects the

RBI to reduce policy rates by at most 25-50 bps during 2013-14.

Why will long-term debt funds benefit?

Long-term debt funds include income funds (which invest a majority of their corpus in long tenure debt instruments issued by

corporates) and gilt funds (which invest in bonds issued by the central or state governments). The value of the underlying debt

instruments in a fund’s portfolio fluctuates on a daily basis (known as market risk) due to factors such as interest rate movement

and the liquidity situation. The price of a debt instrument and interest rates (yields) move in opposite directions, i.e., price of the

bond rises when interest rates fall and vice versa.

The net asset value (NAV) of a debt fund scheme replicates the prices of the underlying securities. Hence, if interest rates fall, the

NAV of debt funds rises. In a declining interest rate scenario, long-term debt funds would benefit more than short-term debt funds

due to the longer maturity of the underlying securities held by the former. Short-term funds, whose portfolio contains securities with

a shorter maturity, would see a lower price change as they mature faster and the new securities purchased lock into a lower yield in

a falling interest rate scenario.

Gilt funds carry lower credit risk than income funds

Though both gilt and income funds carry a market risk owing to interest rate movements, gilt funds have a lower credit risk as they

invest only in government securities. Income funds, on the other hand, invest in both government securities and corporate bonds.

Table 7: Investing in Debt Funds

Salient Features Watch Out For

1. Professional Management - Investors get

fund managers to make and monitor

investments based on the interest rate

outlook.

2. Diversification – Invested across securities -

issuers and sectors - which lowers the risk.

3. Regular income - As dividends (subject to

investor choosing this option).

4. Liquidity – Open-ended debt funds can be

bought and sold on any business day.

5. Tax benefits - Investments for a period of

more than 12 months qualify for long-term

capital gains tax at 20% with indexation and

10% without indexation.

1. Interest rate risk – Investors should look at the underlying interest

rate cycle before investing. Long-term debt funds benefit in a falling

interest rate regime while it is vice versa for short-term funds.

2. Credit risk – Investors can gauge the credit risk of a debt fund by the

security-wise rating profile disclosed in its portfolio. Investors may also

refer to the Credit Quality Rating (CQR) of the fund. Gilt funds do not

carry a credit risk to the extent of the gilt component.

3. Concentration risk – Funds that have a diversified portfolio of debt

instruments but do not majorly concentrate on a few sectors or issuers

are ideal for investments.

4. Lock-in period – Close-ended funds or FMPs have a lock-in period.

5. Exit loads – Investors must check whether any exit load is applicable

for early withdrawal from an open ended debt fund.

29

Market cycle case study is intuitive

CRISIL has performed a market cycle case study (see Table 8) to analyse returns from income and gilt funds over the past 10

years. As seen in the following table, gilt funds followed by income funds have generated superior returns in the market cycles

where interest rates had fallen. In the three periods - 2000-04, 2008 and post April 2012 - when interest rates declined, returns from

gilt funds were the highest across debt fund categories followed by income funds. The returns were higher than the corresponding

bank fixed deposit rates available during these periods. This indicates that if RBI cuts interest rates in the coming year, gilt funds

and income funds are likely to outperform other categories of debt funds.

Table 8: Market Cycle Case Study

Market Cycles

Period

No of

Years

10 Year Government

Bond Yields (%) Annualized Returns (%)

3 Year FD

Rates (%) Start Date End Date

As on

Start Date

As on

end date

Liquid

Funds

Income

Funds

Gilt

Funds

Short Term

Debt Funds

Secular decline in

yields in 2000-04 1-Apr-00 30-Apr-04 4.08 11.1 5.19 6.97 11.89 16.15 12.17 10.50

Flat to high interest

rate period of 2004-08 30-Apr-04 31-Jul-08 4.25 5.19 9.54 6.45 3.69 3.32 5.86 5.38

Sharp correction in

yields in 2008 31-Jul-08 31-Dec-08 0.42 9.54 5.32 9.17 34.61 60.12 17.81 7.88*

Flat to high interest

rate period of 2008-11 31-Dec-08 16-Apr-12 3.29 5.32 8.45 6.49 4.74 1.93 6.54 9.88

Post RBI's repo rate

cut in April 16-Apr-12 28-Feb-13 0.87 8.45 7.87 9.06 10.91 11.99 9.48 9.04*

*One-year FD rate

Note - FD rates at the start of the period.

Annualised returns based on average of CRISIL Mutual Fund Ranking category as of December 2012

Conclusion

Historically, long-term debt funds have given superior returns in a falling interest rate scenario. Assuming interest rates are cut,

returns from long-term debt funds are expected to increase during the current falling interest rate cycle too. However, the quantum

of returns will depend on the pace and degree of rate cuts. It has been observed that those who invested early in the interest rate

cycle gained more than those who invested later as the cycle matured. Investors can refer to the quarterly CRISIL Mutual Fund

Ranking available on www.crisil.com to choose superior performing funds in these categories.

30

III - Liquid funds - An alternative to savings bank deposits

Provides higher returns with a reasonable degree of safety Liquid funds are mutual funds that, by way of their investments into debt market securities, offer higher post-tax returns vis-à-vis

savings bank accounts. Besides this, they also offer a reasonable degree of safety in terms of the principal invested and most

importantly offer high liquidity. Retail investors who park their short term surplus funds in savings bank accounts for liquidity should

be aware of the existence of this remunerative option. According to AMFI, of the Rs 2.04 trillion AUM in liquid funds as on February

2013, retail investors constituted less than a 1% share while the rest was held by high net-worth individuals, corporates, banks and

financial institutions. On the other hand, the size of savings bank deposits has continued to grow despite yielding only a nominal

rate of return. The quantum of money in savings bank accounts in scheduled commercial banks was over Rs 15 trillion as on March

31, 2012 (Source – RBI).

Liquid funds vs similar options available from banks

Liquid funds are mutual fund schemes where the primary objective is to invest in debt instruments with maturities of less than 91

days, generating optimal returns while maintaining safety and high liquidity. Liquid funds primarily invest in money market

instruments such as certificates of deposits (CDs), commercial papers (CPs) and government treasury bills. Such a portfolio helps

liquid funds provide high liquidity to investors. Accordingly, redemption requests are processed within 24 hours.

Table 9: Comparison of savings deposit, fixed deposit and liquid funds

Savings deposit Fixed deposit Liquid funds

Liquidity High Medium High

Annualised returns 4%# 6.50-8.75%* 7.11 - 10.00%**

Minimum lock-in No Yes 1 day

Principal guarantee Government-backed

guarantee of up to Rs 1 lakh

Government-backed

guarantee of up to Rs 1 lakh

No guarantee

Safety (to the principal amount) High High Medium

Penalty (on early withdrawals) No Yes1 No@@

Availability of cheque facility Yes No No

Tax 0-30%^ 0-30%^ 25%^^ in dividend option

0-30%^ in growth option

(<1 year investment)

10 or 20%@ in growth option

(>1 year investment)

* The interest rate varies with the tenor of the deposit, source: SBI

**1-year returns as on February 28, 2013 of CRISIL Mutual Fund Ranked schemes (for quarter ended December 2012)

^ depending upon tax bracket of the investor, plus 3% cess

^^ plus 10% surcharge and 3% cess

@ 10% without indexation or 20% with indexation whichever is lower plus 3% cess

#some banks offer more than 4% but with a higher minimum balance requirement

@@Most liquid funds do not charge any exit load

Liquid funds, although not backed by any principal guarantee, are relatively safe instruments as the portfolios of liquid funds mostly

comprise ‘A1+’ rated CPs and CDs (highest rating for these types of securities) with a maximum maturity of 91 days. CRISIL’s

rating of ‘A1+f’ signifies “very strong” protection against losses from credit defaults.

1 These charges vary across banks. For term deposits with SBI, the depositor would receive 0.5% less for any premature withdrawal provided the

deposit remains with the bank for more than 7 days.

31

However, the marginally higher risk in liquid funds as compared to a savings deposit is compensated by superior returns of liquid

funds especially post tax (see Table 10)

The tax advantage

There are two options of investing in a liquid fund: i) growth option and ii) dividend option. In the case of growth option, returns from

liquid funds would attract short term capital gains if redeemed within a year (as per the investor’s income tax bracket) and long term

capital gains if redeemed after a year (10% without indexation and 20% with indexation plus cess). In the case of a dividend option,

although dividends are tax-free in the hands of the investor, there is a dividend distribution tax (DDT) which is paid by the mutual

fund house before the dividend is distributed to unit holders.

Post tax, liquid funds yield better returns vis-à-vis savings deposits, where the interest earned on the latter would be taxed based

on an individual’s tax slab. Investment in a fixed deposit would also attract tax on returns as per the investor’s tax-bracket

(maximum of 30% plus cess).

Table 10: 1-year returns across investment types (as of February 28, 2013)

Investment type Investment amount

(Rs)

Indicative

yield

Pre-tax returns

(Rs)

Tax rate

(highest)

Post-tax returns

(Rs)

Post tax

yield

Savings account

500,000

4.00%# 20,000 30.900% 16,910 3.38%

Fixed deposits 6.50%* 32,500 30.900% 22,458 4.49%

Liquid fund – Dividend 9.29%^ 46,450 28.325% 36,197 7.24%

Liquid fund – Growth 9.29%^ 46,450 10.300%** 41,805 8.36%@

#some banks offer more than 4% but with a higher minimum balance requirement

*State Bank of India fixed deposit rate for 241 days to less than 1 year

^ 1-year returns of CRISIL Fund Rank 1 Liquid Funds (ranks as of December 2012)

** Tax rate without indexation, assuming an investment of 1 year and 1 day

@yields could be higher if indexation benefits are availed

Choosing a liquid fund

Choosing an appropriate liquid fund can be a challenge as there are about 60 funds offered by various fund houses. Further, most

liquid funds have very little differentiation. The variation in returns between the best performing and worst performing scheme is

almost 3% for the 1-year period ended February 28, 2013. Hence, it is important for investors to assess the various schemes

before investing. Alternatively, investors may refer to CRISIL’s quarterly Mutual Fund Ranking which uses various NAV and

portfolio attributes to rank liquid funds.

Conclusion

Liquid fund is an alternate investment avenue for individuals to park their short term surplus funds. While bank deposits (fixed and

savings) are easier to access and offer some degree of principal protection, the higher yield combined with the liquidity and taxation

benefits make liquid funds an attractive option. However, liquid funds are not completely risk-free, and an investor must carry out

basic checks before investing. Further, investors must spread their savings across fixed deposits, savings bank account and liquid

funds, thereby enjoying the benefits each of these avenues have to offer.

32

IV - Go for paper gold

Gold has been treasured as a valuable commodity for as long as one can remember. With the shifting sands of time, it has evolved

as an important asset class. From barter trade to jewellery investment and now paper gold, the sheen continues and its universal

appeal is intact. Gold has proven to be a safe-haven investment option as well as a good diversifier due to its low correlation with

other asset classes such as equity and debt. In recent times, gold has given almost similar returns (18% annualised) as provided by

equities (CNX Nifty index) over the past 10 years till February 28, 2013. It has also given positive returns for every calendar year for

over a decade. In India, where gold buying is an integral part of social and religious customs, investors now have the option of

buying gold in dematerialised or paper form. Paper gold not only offers the convenience of holding the yellow metal in an electronic

form with greater price transparency but also negates the risk of storage and theft. Further, with the launch of the CRISIL Gold

Index, investors now have a standard benchmark for gold prices in India. The index is freely available on give exact link.

Three paper gold options in India

Gold ETFs – These are passively managed mutual funds that invest money in standard gold bullion (99.5% purity). In India,

assets managed under gold ETFs have increased nearly 15-fold in the past four years from Rs 7.80 bn in February 2009 to Rs

115.60 bn in February 2013 (this also includes mark-to-market gains of 90% shown by the CRISIL Gold Index during the period).

Since they are traded on exchanges, gold ETFs provide high liquidity and transparency in prices. Investment in gold ETFs

requires opening demat account with broker registered with National Stock Exchange (NSE) or Bombay Stock Exchange (BSE).

Gold mutual funds – These are fund of funds (FoFs) that invest the corpus in either their own gold ETFs or a foreign gold fund

which is the mother fund. Gold mutual funds provide investors the facility of systematic investment plans (SIP) wherein they may

invest in gold regularly and avail benefits of rupee cost averaging, i.e. buying more units when prices are low and less units

when prices are high. Currently, Indian fund houses offer 13 gold FoFs (including two foreign FoFs), managing average assets

of Rs 50.61 bn as of December 2012 (includes average AUM of Rs 9.22 bn by foreign FoFs). It also gives retail investors an

opportunity to invest in paper gold in amounts as small as Rs 500 (via SIPs) and without having to open a demat account (unlike

gold ETFs).

E-gold – Investors can purchase gold in electronic form via E-gold – a product launched by the National Spot Exchange Limited

(NSEL). Investors in E-gold can buy and sell gold in denominations as small as 1 gram. A major advantage of E-gold is the

investor gets an option to convert paper gold into physical gold in addition to all the perks of investing in gold in the paper form.

Gold offers risk diversification

Gold as an asset class offers twin benefits: diversifies an investor’s portfolio and limits the downside risk in times of uncertainty

owing to its low to negative correlation with other asset classes. As seen in Table 11, gold has provided the highest returns in four

out of the five years in the bear phase, clearly indicating the superiority of the asset class in times of equity market turmoil.

Table 11: Performance of gold, equity and debt