Embed Size (px)

Citation preview

ON Tuesday 13 June 2017, 2.00 UTC+1/London

HOSTED BY

CRS and Trustees

STEP WEB EVENTS

www.stepwebevents.org

13 June 2017

STEP

The Common Reporting Standard Practice Note on CRS and Trusts

John Riches and Samantha Morgan

Aim of this session

• To go through – The Practice Note on CRS and Trusts – FATF related developments

Application of the rules

• In looking at CRS it is necessary to consider – Implementing legislation – OECD Commentary – OECD Handbook – Local guidance

• There is a lack of consistency between these and a lack of consistency as to how the Standard has been implemented in each jurisdiction

RMW Law LLP

Background to the Practice Note

• STEP met with HMRC and OECD Secretariat to discuss some of the practical issues which trustees were facing and to see if any clarity could be reached

• The meetings took place at the end of 2016 / early 2017 before guidance was issued in most offshore jurisdictions

RMW Law LLP

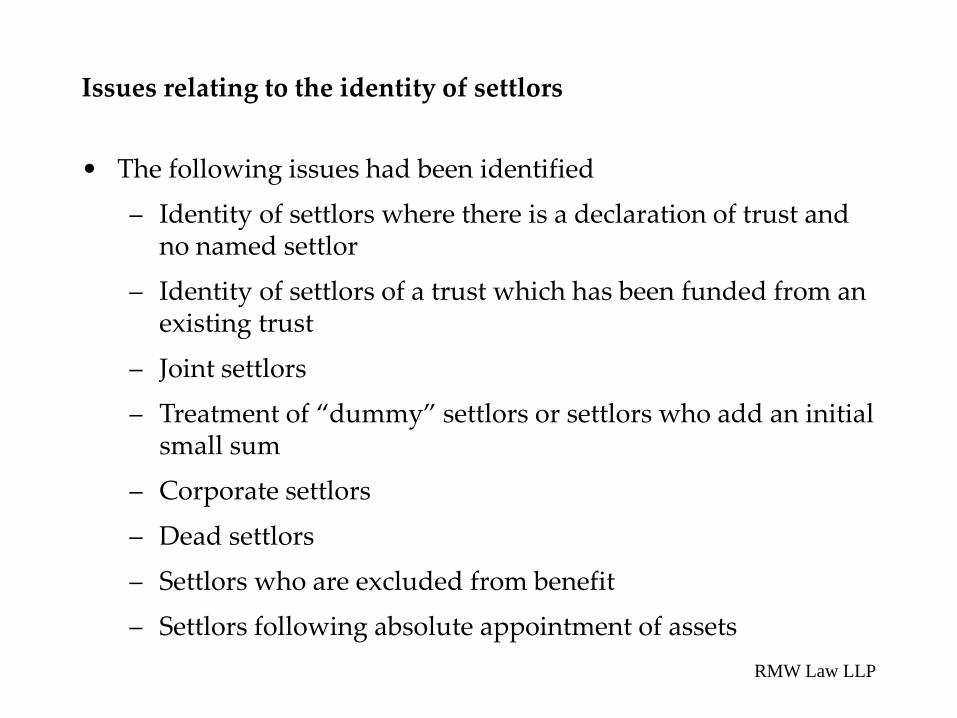

Issues relating to the identity of settlors

• The following issues had been identified

– Identity of settlors where there is a declaration of trust and no named settlor

– Identity of settlors of a trust which has been funded from an existing trust

– Joint settlors

– Treatment of “dummy” settlors or settlors who add an initial small sum

– Corporate settlors

– Dead settlors

– Settlors who are excluded from benefit

– Settlors following absolute appointment of assets

RMW Law LLP

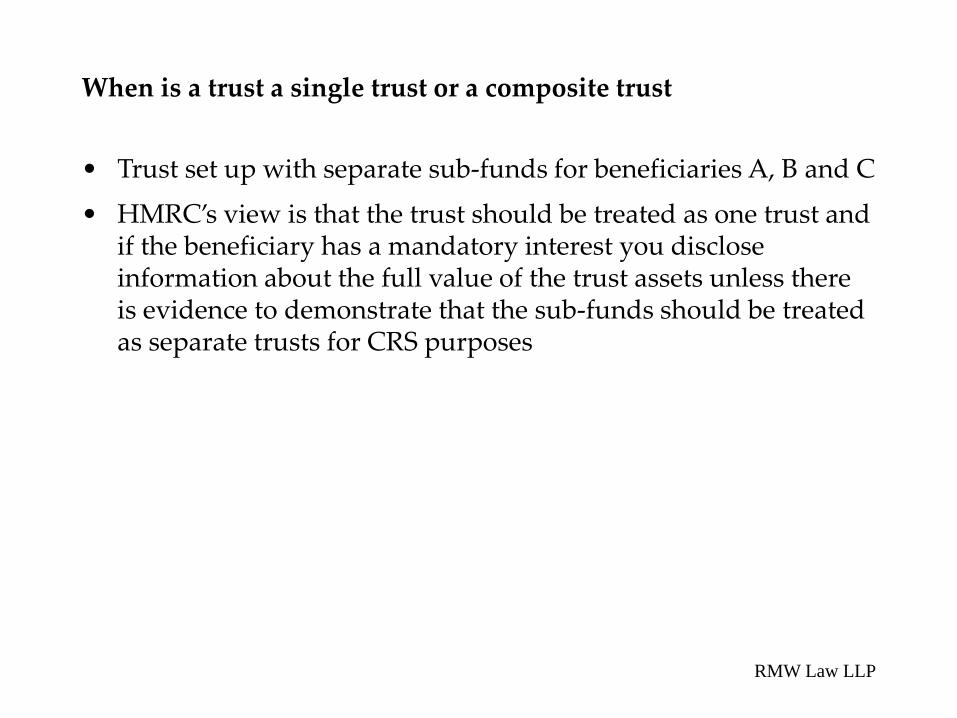

When is a trust a single trust or a composite trust

• Trust set up with separate sub-funds for beneficiaries A, B and C

• HMRC’s view is that the trust should be treated as one trust and if the beneficiary has a mandatory interest you disclose information about the full value of the trust assets unless there is evidence to demonstrate that the sub-funds should be treated as separate trusts for CRS purposes

RMW Law LLP

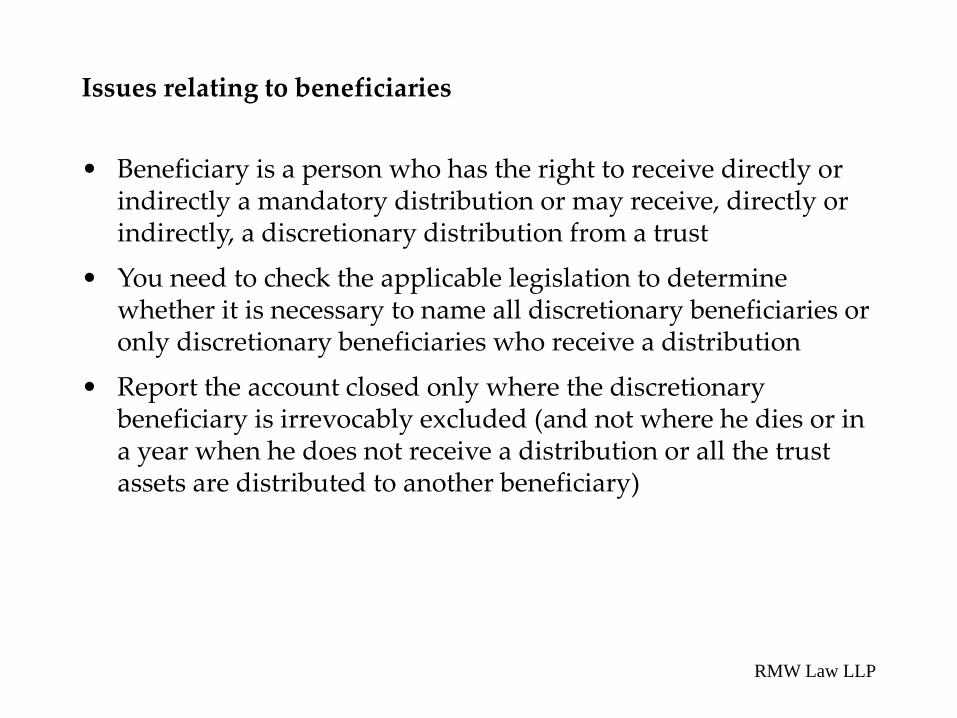

Issues relating to beneficiaries

• Beneficiary is a person who has the right to receive directly or indirectly a mandatory distribution or may receive, directly or indirectly, a discretionary distribution from a trust

• You need to check the applicable legislation to determine whether it is necessary to name all discretionary beneficiaries or only discretionary beneficiaries who receive a distribution

• Report the account closed only where the discretionary beneficiary is irrevocably excluded (and not where he dies or in a year when he does not receive a distribution or all the trust assets are distributed to another beneficiary)

RMW Law LLP

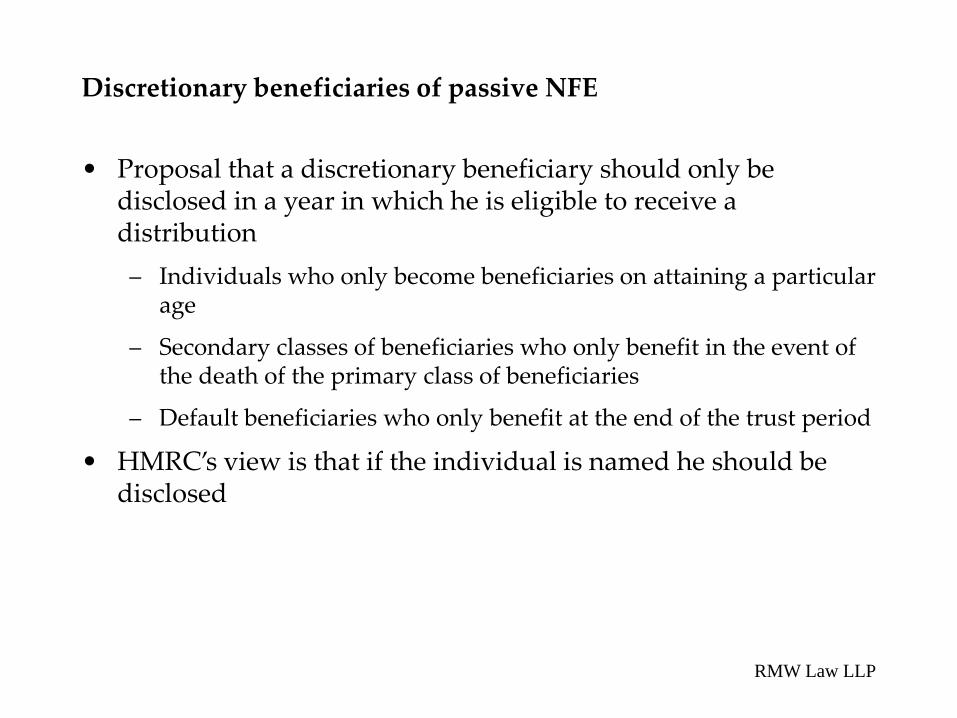

Discretionary beneficiaries of passive NFE

• Proposal that a discretionary beneficiary should only be disclosed in a year in which he is eligible to receive a distribution

– Individuals who only become beneficiaries on attaining a particular age

– Secondary classes of beneficiaries who only benefit in the event of the death of the primary class of beneficiaries

– Default beneficiaries who only benefit at the end of the trust period

• HMRC’s view is that if the individual is named he should be disclosed

RMW Law LLP

Beneficiaries receiving mandatory distributions

• Meaning of mandatory beneficiary – Beneficiary with life interest

– More than one beneficiary with life interest in sub-fund

• HMRC’s view is that disclose full value of trust fund with respect to each beneficiary unless can show that should be treated as separate trusts

– Grantor trust where income payable to or on the order or direction of the grantor – probably not a mandatory beneficiary but me be natural person exercising effective control

RMW Law LLP

Protectors

• Trust which is a Passive NFE – Protector named in definition of “Controlling Person”

– Not necessary to consider whether he has effective control

RMW Law LLP

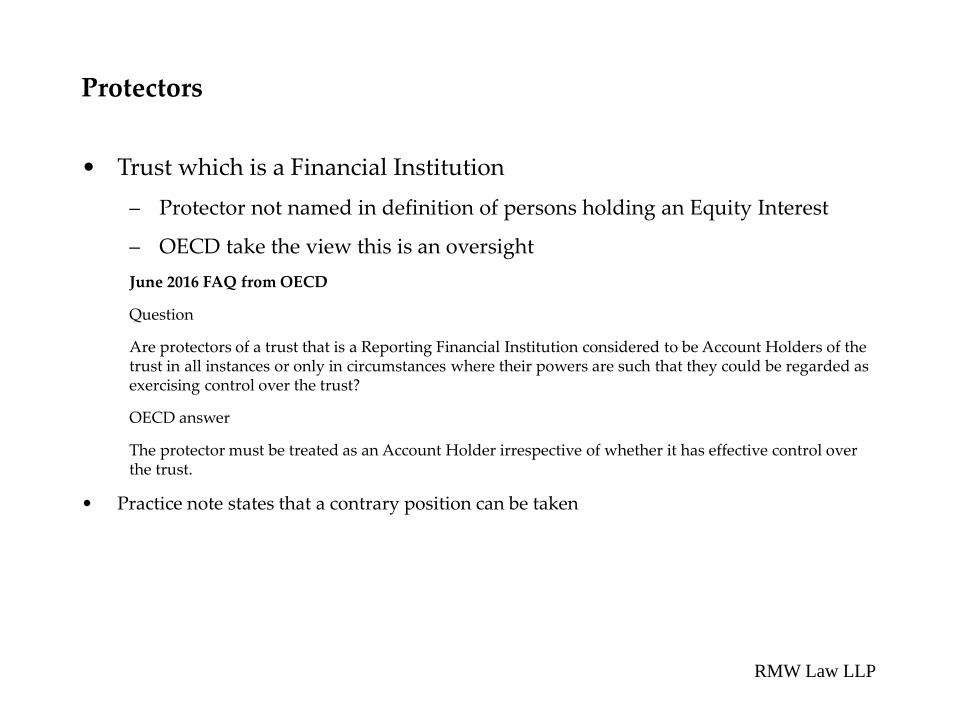

Protectors

• Trust which is a Financial Institution – Protector not named in definition of persons holding an Equity Interest

– OECD take the view this is an oversight June 2016 FAQ from OECD

Question

Are protectors of a trust that is a Reporting Financial Institution considered to be Account Holders of the trust in all instances or only in circumstances where their powers are such that they could be regarded as exercising control over the trust?

OECD answer

The protector must be treated as an Account Holder irrespective of whether it has effective control over the trust.

• Practice note states that a contrary position can be taken

RMW Law LLP

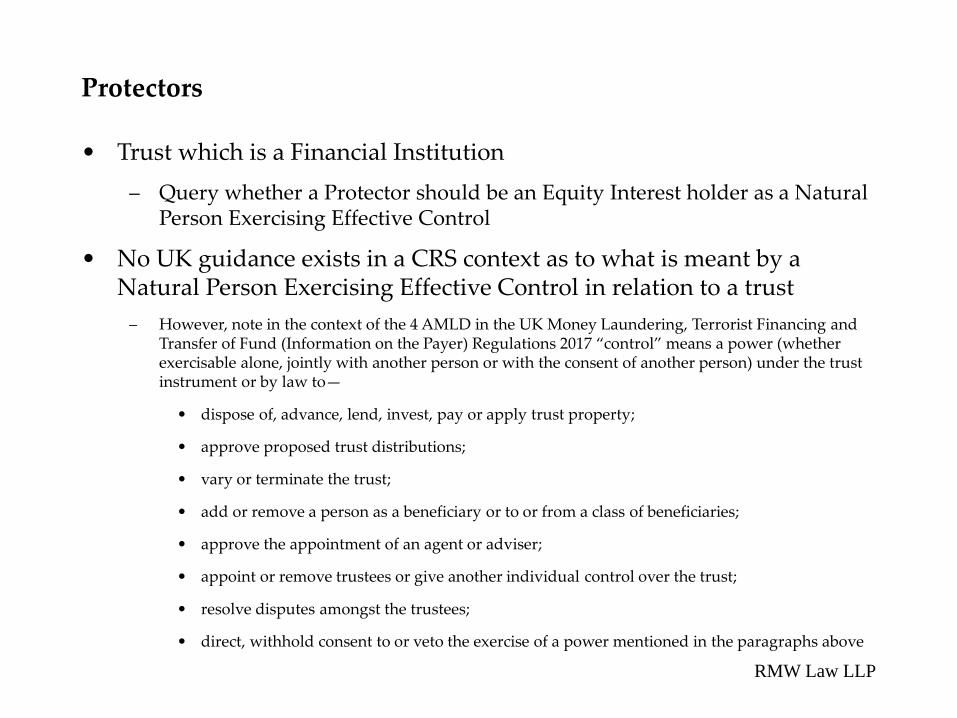

Protectors

• Trust which is a Financial Institution – Query whether a Protector should be an Equity Interest holder as a Natural

Person Exercising Effective Control

• No UK guidance exists in a CRS context as to what is meant by a Natural Person Exercising Effective Control in relation to a trust

– However, note in the context of the 4 AMLD in the UK Money Laundering, Terrorist Financing and Transfer of Fund (Information on the Payer) Regulations 2017 “control” means a power (whether exercisable alone, jointly with another person or with the consent of another person) under the trust instrument or by law to—

• dispose of, advance, lend, invest, pay or apply trust property;

• approve proposed trust distributions;

• vary or terminate the trust;

• add or remove a person as a beneficiary or to or from a class of beneficiaries;

• approve the appointment of an agent or adviser;

• appoint or remove trustees or give another individual control over the trust;

• resolve disputes amongst the trustees;

• direct, withhold consent to or veto the exercise of a power mentioned in the paragraphs above

RMW Law LLP

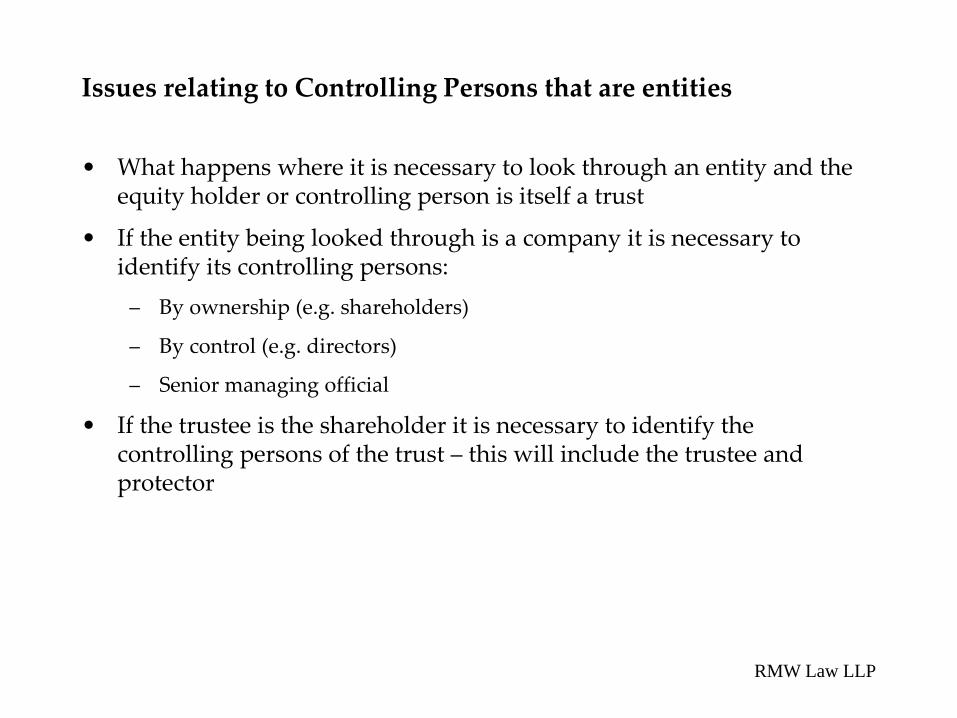

Issues relating to Controlling Persons that are entities

• What happens where it is necessary to look through an entity and the equity holder or controlling person is itself a trust

• If the entity being looked through is a company it is necessary to identify its controlling persons:

– By ownership (e.g. shareholders)

– By control (e.g. directors)

– Senior managing official

• If the trustee is the shareholder it is necessary to identify the controlling persons of the trust – this will include the trustee and protector

RMW Law LLP

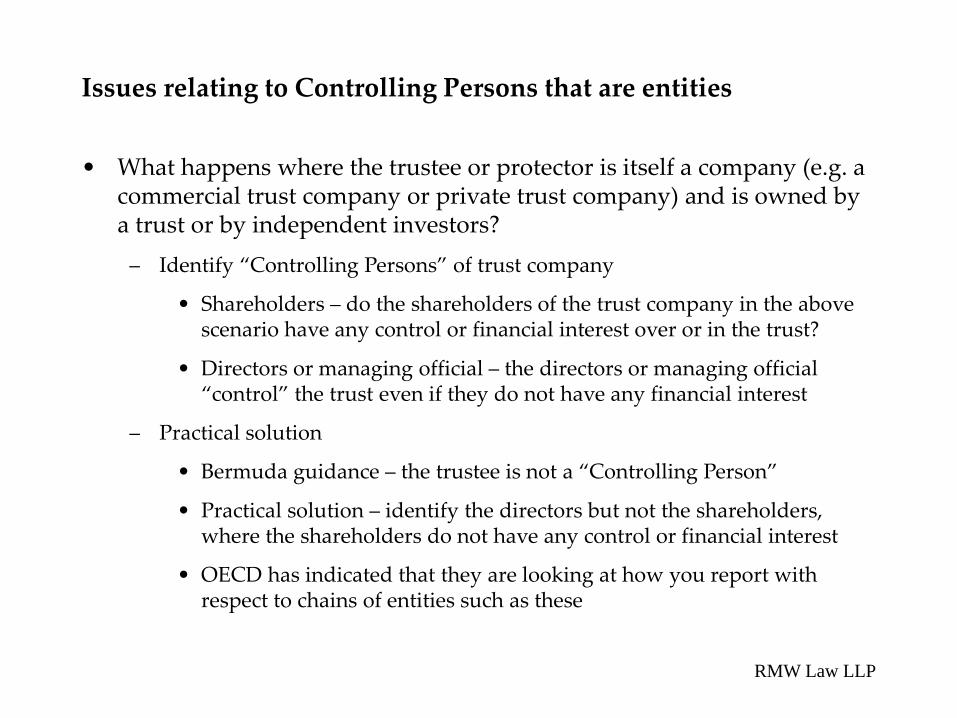

Issues relating to Controlling Persons that are entities

• What happens where the trustee or protector is itself a company (e.g. a commercial trust company or private trust company) and is owned by a trust or by independent investors?

– Identify “Controlling Persons” of trust company

• Shareholders – do the shareholders of the trust company in the above scenario have any control or financial interest over or in the trust?

• Directors or managing official – the directors or managing official “control” the trust even if they do not have any financial interest

– Practical solution

• Bermuda guidance – the trustee is not a “Controlling Person”

• Practical solution – identify the directors but not the shareholders, where the shareholders do not have any control or financial interest

• OECD has indicated that they are looking at how you report with respect to chains of entities such as these

RMW Law LLP

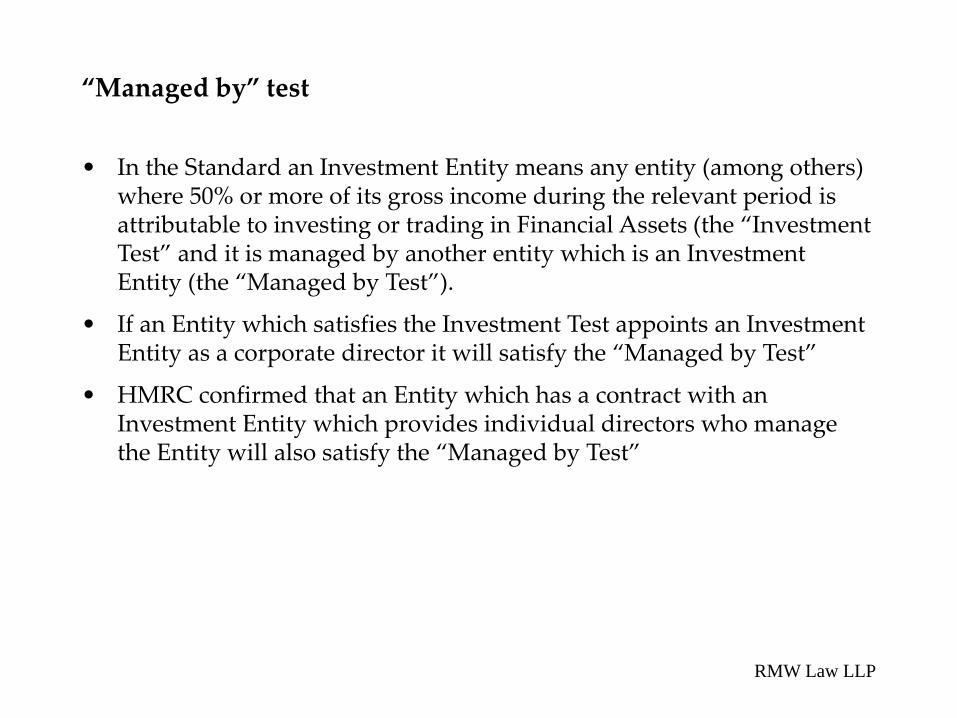

“Managed by” test

• In the Standard an Investment Entity means any entity (among others) where 50% or more of its gross income during the relevant period is attributable to investing or trading in Financial Assets (the “Investment Test” and it is managed by another entity which is an Investment Entity (the “Managed by Test”).

• If an Entity which satisfies the Investment Test appoints an Investment Entity as a corporate director it will satisfy the “Managed by Test”

• HMRC confirmed that an Entity which has a contract with an Investment Entity which provides individual directors who manage the Entity will also satisfy the “Managed by Test”

RMW Law LLP

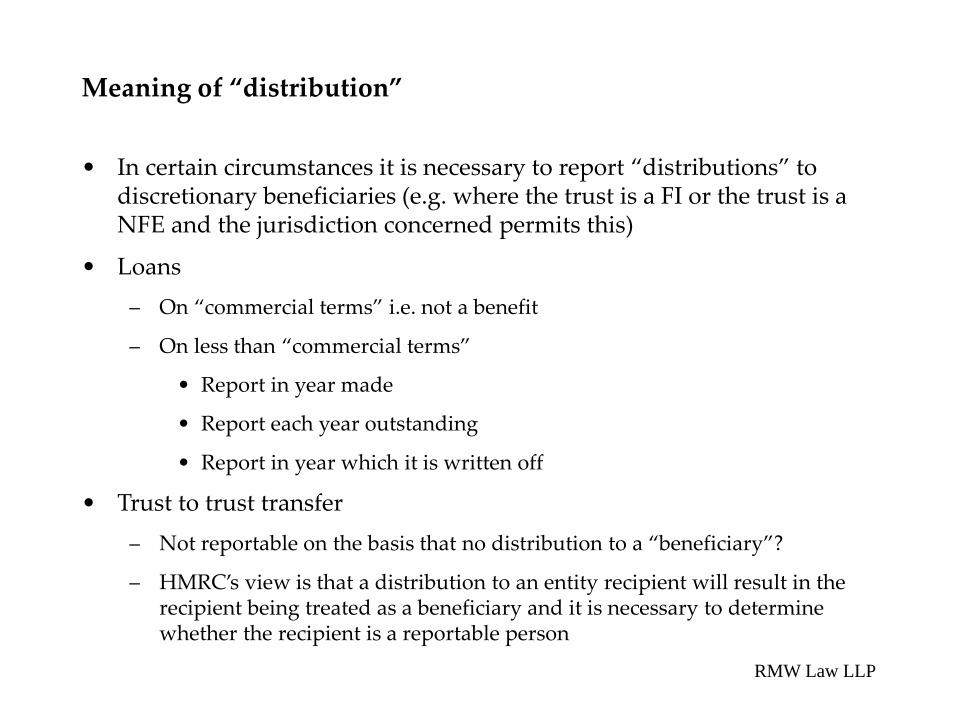

Meaning of “distribution”

• In certain circumstances it is necessary to report “distributions” to discretionary beneficiaries (e.g. where the trust is a FI or the trust is a NFE and the jurisdiction concerned permits this)

• Loans – On “commercial terms” i.e. not a benefit

– On less than “commercial terms”

• Report in year made

• Report each year outstanding

• Report in year which it is written off

• Trust to trust transfer – Not reportable on the basis that no distribution to a “beneficiary”?

– HMRC’s view is that a distribution to an entity recipient will result in the recipient being treated as a beneficiary and it is necessary to determine whether the recipient is a reportable person

RMW Law LLP

Valuation of trust assets

• Lack of clarity on how to value trust assets

• Bermuda guidance – Noting that the CRS Handbook describes the account balance of a settlor as the "total value of all

trust property", it also allows the use of the value that is used for reporting to the Account Holder on the investment results for a given period for settlors and mandatory beneficiaries. If the value has not been recalculated, then the CRS Handbook provides that the account balance for settlors and mandatory beneficiaries may be the value of the interest upon acquisition or the total value of all trust property.

RMW Law LLP

Importance of local guidance

• The earlier discussion covers HMRC’s view of CRS

• Local guidance in other jurisdictions often takes a different view

• Query as to whose guidance applies? – e.g. Luxembourg bank account held by Bermuda Passive NFE

RMW Law LLP

FATF

• Use of “beneficial ownership” concept as basis for trust registers and its implications

– UK trust register

• Future developments

RMW Law LLP

QUESTIONS? Questions may be asked over the phone or submitted over the web: •PHONE If you wish to ask a question over the telephone, please press *1 on your telephone and wait for your name to be announced by the operator. If you wish to cancel your request, please press the # key. •WEB If you wish to submit a question via the web you can do so by typing your question into the Q&A panel on the right hand side of your screen on the web platform, and then selecting ‘send to all panellists’.

CONTACT: Email: [email protected] Website: www.stepwebevents.org

Tomorrow: 14 June

Join the webinar at https://global.gotomeeting.com/join/143497445

**No prior registration required** See also: www.step.org/webevents

STEP Web Events