Embed Size (px)

Citation preview

1

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND

ADMINISTRATORS

International Qualifying Scheme Examination

CORPORATE SECRETARYSHIP JUNE 2011

Suggested Answers

The suggested answers are published for the purpose of assisting students in their

understanding of the possible principles, analysis or arguments that may be identified

in each question

2

SECTION A

Q1.

Andy, Ben, Joyce and Kenneth were classmates when they studied fashion

design at university nearly ten years ago. During their studies, they dreamed

that one day they would have their own business selling fashion of their own

design. Their dream has now come true now. They have recently incorporated a

private company limited by shares to sell their fashion in the company name of

ABJ & K Fashion Limited. The date of incorporation is 11 February 2011. As well

as investing their own funds in the company themselves, they have invited

Andy’s aunt, Mrs. Chiu, to invest in the company.

Both the authorised and issued capital is 3,000,000 ordinary shares of $1 each.

Andy, Ben, Joyce, Kenneth and Mrs. Chiu are the founders of the company and

the shareholdings are the ratio 2:2:2:3:1 respectively. All of them except Mrs.

Chiu are the first directors of the company. Kenneth and Joyce are the chairman

of the board and the first secretary of the company respectively. Messrs. Tong &

Cheung & Co. will be appointed as the auditors and tax representative of the

company. The financial year end will be fixed at 30 June. The registered office is

situated at 3/F, 22 Tai Yau Road, Hong Kong. The quorum of directors’ meetings

is two as fixed in the articles of association of the company.

The board of directors appointed their friend, Jenny, as an additional director of

the company on 25 February 2011. Jenny has experience in the fashion

industry. According to the company’s articles of association, a share

qualification of 100,000 shares is required for every director of the company.

Jenny acquired her required shares on 23 May 2011. Jenny signed an

agreement on behalf of the company on 10 May 2011 to rent premises as one of

the company’s retail outlets.

On 27 May 2011, the company received bad news from Andy: His aunt, Mrs.

Chiu, passed away suddenly two weeks ago. Andy notified the company that

Mrs. Chiu’s son wished to have Mrs. Chiu’s shares registered in his name.

In addition, Joyce’s husband has just been informed by his employer that he

needs to move to Shanghai to set up a new business there. Joyce informed ABJ

& K Fashion Limited that she would go with her husband to Shanghai and would

primarily live in Shanghai in the near future. She plans to remain in her positions

as both the secretary and a director of the company. However, she intends to

3

appoint her sister to be her representative to attend board meetings and to act

on her behalf as a director if she is not in Hong Kong.

REQUIRED:

Q1 (a) Draft the minutes of the first board meeting for AB J & K Fashion Limited. (Note: The appointment of Jenny as an additional di rector is NOT included in the minutes of the first board meeting)

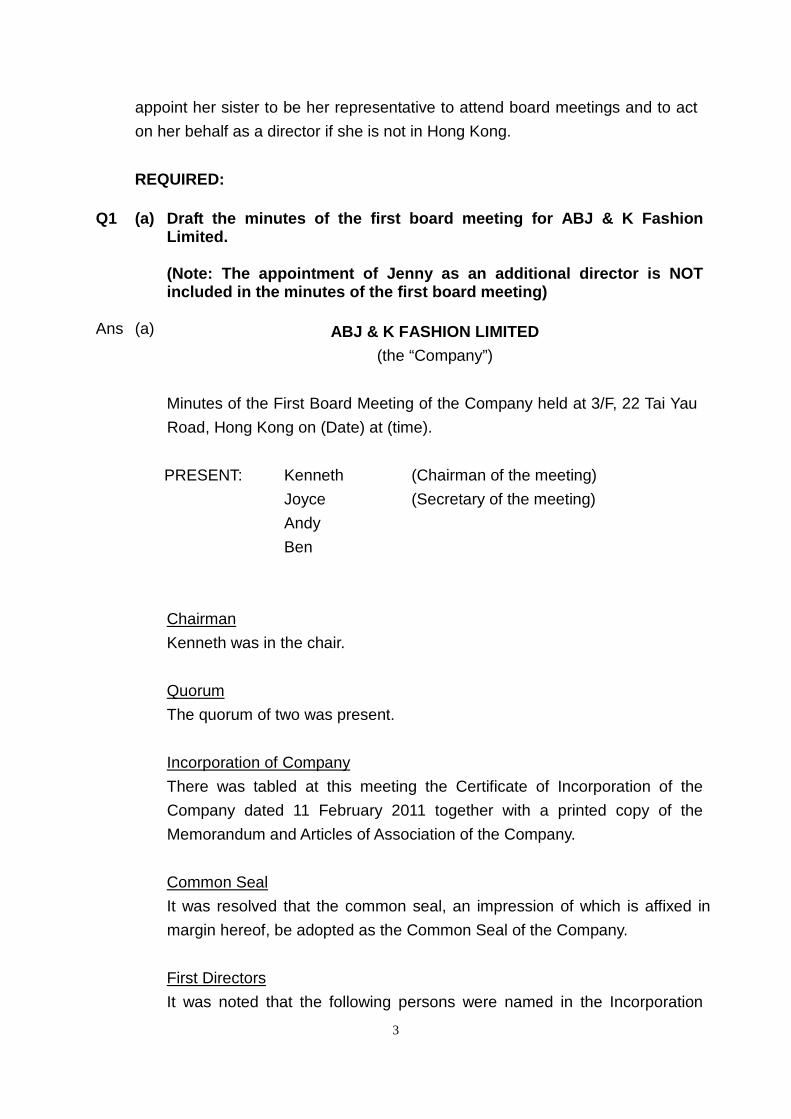

Ans (a) ABJ & K FASHION LIMITED

(the “Company”)

Minutes of the First Board Meeting of the Company held at 3/F, 22 Tai Yau

Road, Hong Kong on (Date) at (time).

PRESENT: Kenneth (Chairman of the meeting)

Joyce (Secretary of the meeting)

Andy

Ben

Chairman

Kenneth was in the chair.

Quorum

The quorum of two was present.

Incorporation of Company

There was tabled at this meeting the Certificate of Incorporation of the

Company dated 11 February 2011 together with a printed copy of the

Memorandum and Articles of Association of the Company.

Common Seal

It was resolved that the common seal, an impression of which is affixed in

margin hereof, be adopted as the Common Seal of the Company.

First Directors

It was noted that the following persons were named in the Incorporation

4

Form (NC1) as the first directors of the Company.

Kenneth

Andy

Ben

Joyce

Registered Office

It was resolved that the registered office of the Company be situated at 3/F,

22 Tai Yau Road, Hong Kong. Secretary

It was noted that Joyce was named as the first secretary in the Incorporation

Form (NC1).

Financial Year End

It was resolved that the financial year end of the Company be fixed at 30

June and the first accounts of the Company be made up to 30 June 2012.

Auditors

It was resolved that Messrs. Tong & Cheung & Co., Certified Public

Accountants, be appointed as the first auditors of the Company at a fee to

be agreed with the directors.

Tax Representative

It was resolved that Messrs. Tong & Cheung & Co., Certified Public

Accountants, be appointed as the tax representative of the Company.

Founder Members’ Shares

It was noted that the authorised and issued capital of the Company be

$3,000,000 divided into 3,000,000 ordinary shares of $1 each. The founder

members to the Memorandum of Association had taken up shares as

follows:

Andy 600,000 shares

Ben 600,000 shares

Joyce 600,000 shares

Kenneth 900,000 shares

5

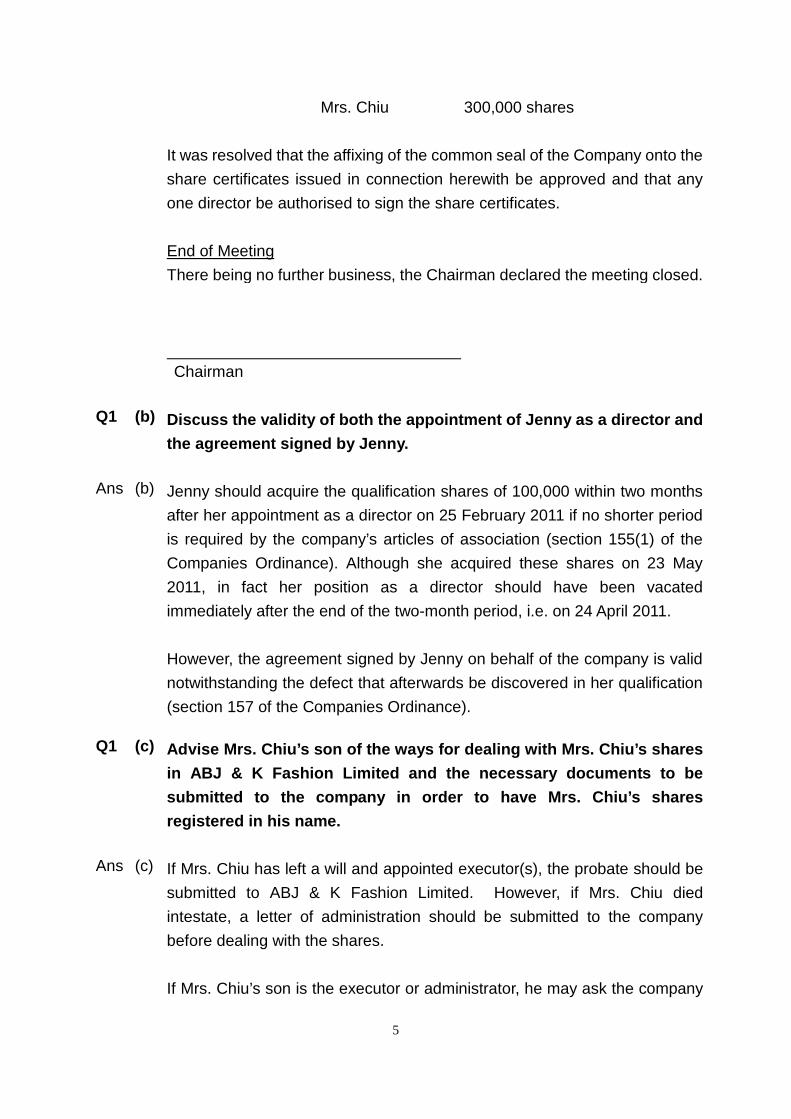

Mrs. Chiu 300,000 shares

It was resolved that the affixing of the common seal of the Company onto the

share certificates issued in connection herewith be approved and that any

one director be authorised to sign the share certificates.

End of Meeting

There being no further business, the Chairman declared the meeting closed.

Chairman

Q1 (b) Discuss the validity of both the appointment of Jen ny as a director and

the agreement signed by Jenny.

Ans (b) Jenny should acquire the qualification shares of 100,000 within two months

after her appointment as a director on 25 February 2011 if no shorter period

is required by the company’s articles of association (section 155(1) of the

Companies Ordinance). Although she acquired these shares on 23 May

2011, in fact her position as a director should have been vacated

immediately after the end of the two-month period, i.e. on 24 April 2011.

However, the agreement signed by Jenny on behalf of the company is valid

notwithstanding the defect that afterwards be discovered in her qualification

(section 157 of the Companies Ordinance).

Q1 (c) Advise Mrs. Chiu’s son of the ways for dealing with Mrs. Chiu’s shares

in ABJ & K Fashion Limited and the necessary docume nts to be

submitted to the company in order to have Mrs. Chiu ’s shares

registered in his name.

Ans (c) If Mrs. Chiu has left a will and appointed executor(s), the probate should be

submitted to ABJ & K Fashion Limited. However, if Mrs. Chiu died

intestate, a letter of administration should be submitted to the company

before dealing with the shares.

If Mrs. Chiu’s son is the executor or administrator, he may ask the company

6

to enter his name in the register of members by submitting to the company a

letter of request if the company’s articles of association permit. Alternatively,

he can present to the company for registration a stamped instrument of

transfer transferring the shares to his name.

Q1 (d) Advise the board of directors of ABJ & K Fashion Li mited on Joyce’s

intention to:

i. remaining in her position as the secretary and a director after

leaving Hong Kong; and ii. delegating her authority as a director to her s ister, and relevant

requirement(s) and procedures to be followed.

Ans (d) If Joyce primarily lives in Shanghai, she cannot remain in place as the

company secretary. The secretary of a company should ordinarily reside in

Hong Kong (section 154 of the Companies Ordinance). However, she can

remain in place as a director as there is no such requirement for a director.

As there is no specific qualification requirement for being the secretary of a

private company, the board of directors may consider appointing any one of

them or any other person who ordinarily resides in Hong Kong as the

secretary. The company can also appoint a body corporate with a registered

office or place of business in Hong Kong to be the secretary.

Joyce can appoint her sister as her alternate director.

However, Joyce has no power to delegate her authority to an alternate

director unless this is authorized by the articles of association of ABJ & K

Limited or the power to do so is included in the terms of her appointment.

If Joyce has the power to appoint an alternate director:

� the appointment is usually required to be in writing

� a board resolution should be passed to approve the appointment

� a Form D2A must be filed with the Companies Registry within 14 days

� the Register of Directors should be updated

7

SECTION B (Answer THREE questions from this section)

Q2. ABC Great Trading Limited is a private company limited by shares incorporated

on 4 August 2002. Its business is manufacturing and retailing garments. The

company has a number of chain stores in which it sells its garments. Annie,

Beatrice and Catherine are the only directors and shareholders of the company.

The major supplier of the company is Beatrice Trading Limited, a Hong Kong

company in which Beatrice is the sole director and shareholder.

The shareholders of ABC Great Trading Limited find that maintaining the

business is not easy as the competition in the garment industry is severe. The

company has a cashflow problem and always delays payment to Beatrice

Trading Limited. The shareholders are now considering whether to terminate

the company.

The assets of the company including machinery and finished products which, if

realised, will be sufficient to settle the amount due to Beatrice Trading Limited,

the only creditor of the company. REQUIRED:

Q2 (a) Critically analyse different modes available for te rminating ABC

Great Trading Limited and advise the most appropria te method.

Ans (a) The different modes for terminating ABC Great Trading Limited include:

Members’ voluntary winding up

If ABC Great Trading Limited’s assets (including machinery and finished

products) can be realised and are sufficient to settle the company’s

liabilities in full within a period not exceeding 12 months from the

commencement of the winding up, a members’ voluntary winding up can

be adopted to terminate the company. As ABC Great Trading Limited has

more than two directors, a majority of the directors of the company must

execute a certificate of solvency and state in the certificate that they have

made full enquiry into the affairs of the company and have formed the

opinion that the company will be able to pay its debts in full within a period

not exceeding 12 months from the commencement of the winding up.

8

Creditors’ voluntary winding up

Creditors’ voluntary winding up under section 228A or section 241 of the

Companies Ordinance may be adopted for liquidating the company if the

board of directors of ABC Great Trading Limited considers that the

company is insolvent. Compared with the members’ voluntary winding

up, this kind of winding up is not so time- and cost-efficient as the

procedures are more complicated. The procedures include holding

creditors’ meetings and appointing a committee of inspection if creditors

think fit.

Deregistration

Under section 291AA of the Companies Ordinance, an application to

deregister a private company (including a dormant company under section

344A) can be made if:

� All the members of the company agree to the deregistration

� The company has ceased to carry on business or ceased operation for

more than three months immediately before the application

� The company has no outstanding liabilities

Since ABC Great Trading Limited is a private company, if the company has

ceased operation for more than three months and all the shareholders

agree to the deregistration, an application can be made to deregister the

company. However, this procedure is also subject to a waiver of debt

executed by Beatrice Trading Limited for the amount owed by the

company.

Although a members’ voluntary winding up is more time- and cost-efficient

than a creditors’ voluntary winding up, deregistration is the most

appropriate way to dissolve ABC Great Trading Limited as the company

does not need to go through the costly and timely winding up processes

(e.g. appointment of liquidator) and does not need to publish relevant

information in the gazette at the company’s own cost (e.g. notice to

creditors and notice of final meeting).

9

Q2 (b) Assume that the shareholders of ABC Great Trading Limited finally decide

to cease the company’s operations. However, they still want to maintain

the company’s existence as they have put a great deal of effort into the

company and they are not sure whether they will start business up again in

the near future.

Propose and explain to the shareholders the most ap propriate

method to fulfil their requirements and advise them of the formalities

they will need to follow.

Ans (b) Under section 344A of the Companies Ordinance, a private company is

allowed to declare itself a dormant company if it has not entered into a

“relevant accounting transaction” or it specifies a date after which it will not

enter into a relevant accounting transaction. A dormant company is

exempt from the statutory requirements of holding annual general

meetings, filing annual returns, appointing auditors and preparing audited

accounts; however the company still needs to pay a business registration

fee every year.

Declaring ABC Great Trading Limited dormant is therefore an efficient way

of maintaining the company if no relevant accounting transaction occurs.

The company will then be exempt from the above-mentioned statutory

requirements and paying the relevant fees, e.g. audit fee, to maintain its

existence. If the shareholders recommence the company’s business in

the future, they would not need to go through the incorporation procedures

again in order to re-activate the company.

In order for the company to become dormant, the following formalities

should be followed:

� Convene and hold a board meeting to authorize the convening of a

general meeting and the issue of a notice

� Despatch a notice to those members who are entitled to attend the

meeting

� Pass a special resolution at the general meeting to:

� Declare that the company will become dormant either as from the

date of delivery of the special resolution to the Companies

Registry or as from a specified date

10

� Authorize directors to file the special resolution to the Companies

Registry

� Declare that prior to the company ceasing to be dormant, the

directors shall deliver to the Companies Registry a further special

resolution declaring that the company intends to enter into a

relevant accounting transaction

� Thereafter, the special resolution must be filed with the Companies

Registry within 15 days.

11

Q3. Silver & Bronze Limited is a private company limited by shares with 10,000

issued and fully paid-up voting shares. Anderson, Benny, Charlie, Dickson and

Eddie are the shareholders of the company. The equity ratio is 3:3:1:1:2.

Charlie and Dickson are the only directors of the company.

On 1 February 2011, Anderson and Benny asked the directors of the company

to convene an extraordinary general meeting to consider altering the company’s

articles of association.

At the beginning of March 2011, Anderson and Benny found that the directors

had still not yet started the process to convene a general meeting. They

convened a general meeting themselves on 6 March 2011, arranging for the

meeting to be held on 3 April 2011.

Eddie, who intended to vote for the resolution, found that he would not be able

to attend the meeting. He appointed his wife, Janet, to attend the meeting on

his behalf.

All the shareholders attended the meeting personally on 3 April 2011 except for

Eddie, who had appointed Janet as his proxy to attend and vote on his behalf.

Even though Anderson, Benny and Janet agreed to the resolution for the

alteration of the company’s articles of association at the extraordinary general

meeting, Charlie and Dickson argued that the resolution could not be passed as

Janet was not a shareholder of the company and therefore she could not vote.

They also argued that the general meeting was not properly convened.

REQUIRED:

Comment on the validity of the above issues with re gard to the laws of

meeting.

Ans

Section 113 of the Companies Ordinance provides that members holding not

less than one-twentieth of the paid-up capital and carrying the right of voting at

a general meeting of a company can ask the directors to convene a general

meeting. If the directors do not within 21 days from the date of the deposit of the

requisition proceed duly to convene a meeting for a day not more than 28 days

12

after the date on which the notice convening the meeting is given, the

requisitionists, or any of them representing more than one-half of the total

voting rights of all of them, may themselves convene a meeting, but any

meeting so convened shall not be held after the expiration of three months from

the date of the deposit of the requisition.

As the directors of Silver & Bronze Limited did not proceed to convene a

general meeting to consider altering the company’s articles of association within

21 days after the deposit of the requisition for convening a general meeting on 1

February, Anderson and Benny (holding not less than one-twentieth of the

paid-up capital with voting rights) could convene a general meeting themselves

on 6 March for the meeting to be held on 3 April (within three months from the

date of the deposit of the requisition). The requisition should state the objects of

the meeting and should be signed by Anderson and Benny, the requisitionists,

and deposited at the registered office of the company (section 113 of the

Companies Ordinance).

A company may by special resolution alter its articles of association (section

13(1) of the Companies Ordinance) and not less than 21 days' notice,

specifying the intention to propose the resolution as a special resolution, is

required for the relevant meeting (section 116 of the Companies Ordinance). As

Anderson and Benny had convened the general meeting on 6 March for the

meeting to be held on 3 April, not less than 21 days' notice had been given for

the meeting in accordance with section 116 of the Companies Ordinance.

Section 114A provides that if the articles of the company do not make other

provision, two members personally present shall be a quorum. Article 55 of

Table A mentions that two members present in person or by proxy shall be a

quorum. As all the five shareholders of Silver & Bronze Limited attended the

general meeting personally or by proxy, a quorum had been formed if the

company adopted Table A.

Section 114C of the Companies Ordinance also provides that, except for

companies not having a share capital, any member of a company entitled to

attend and vote at a meeting of the company shall be entitled to appoint another

person (whether a member or not) as his proxy to attend and vote at the

meeting instead of him. Unless the articles otherwise provide, a proxy shall not

be entitled to vote except on a poll. So even though Janet is not a member, she

13

could still act as a proxy for Eddie to attend the meeting subject to lodging a

duly completed and signed proxy form with the company’s office within the

prescribed time limit as stated in the company’s articles of association.

A resolution put to the vote of the general meeting shall be decided on a show

of hands unless a poll is demanded (article 60 of Table A) and on a show of

hands every member present in person shall have one vote, and on a poll every

member shall have one vote for each share of which he is the holder (article 64

of Table A). On a poll votes may be given either personally or by proxy (article

69 of Table A). So if Table A is adopted by Silver & Bronze Limited, Janet could

not vote on a show of hands (section 114C of the Companies Ordinance).

Besides, the resolution for the alteration of the company’s articles of association

could not be passed on a show of hands if only Anderson and Benny voted for

the resolution.

However, Janet could demand or join in demand for a poll (section 114D of the

Companies Ordinance). So, Janet, Anderson and Benny could demand or join

in demand a poll (article 60 of Table A) if the resolution could not be passed by

a show of hands. On a poll, if Anderson, Benny and Janet voted for the

resolution (8,000 out of 10,000 votes, i.e. not less than three-fourths of the

votes cast), the special resolution for the alteration of the company’s articles of

association could be successfully passed (section 116 of the Companies

Ordinance).

14

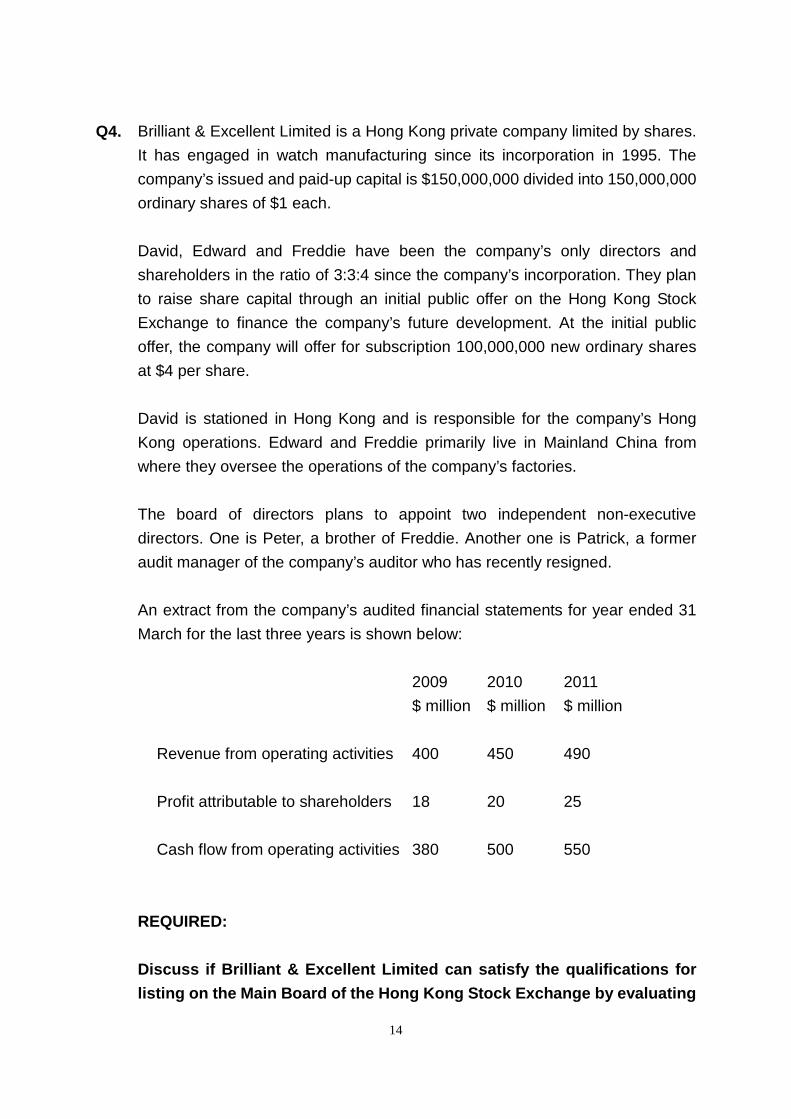

Q4. Brilliant & Excellent Limited is a Hong Kong private company limited by shares.

It has engaged in watch manufacturing since its incorporation in 1995. The

company’s issued and paid-up capital is $150,000,000 divided into 150,000,000

ordinary shares of $1 each.

David, Edward and Freddie have been the company’s only directors and

shareholders in the ratio of 3:3:4 since the company’s incorporation. They plan

to raise share capital through an initial public offer on the Hong Kong Stock

Exchange to finance the company’s future development. At the initial public

offer, the company will offer for subscription 100,000,000 new ordinary shares

at $4 per share.

David is stationed in Hong Kong and is responsible for the company’s Hong

Kong operations. Edward and Freddie primarily live in Mainland China from

where they oversee the operations of the company’s factories.

The board of directors plans to appoint two independent non-executive

directors. One is Peter, a brother of Freddie. Another one is Patrick, a former

audit manager of the company’s auditor who has recently resigned.

An extract from the company’s audited financial statements for year ended 31

March for the last three years is shown below:

2009 2010 2011

$ million $ million $ million

Revenue from operating activities 400 450 490

Profit attributable to shareholders 18 20 25

Cash flow from operating activities 380 500 550

REQUIRED:

Discuss if Brilliant & Excellent Limited can satisf y the qualifications for

listing on the Main Board of the Hong Kong Stock Ex change by evaluating

15

the different criteria it needs to meet the basic l isting requirements.

Ans The following should be considered when determining if Brilliant & Excellent

Limited satisfies the listing qualifications:

� The company must meet the profit test [Rule 8.05(1) of Listing Rules],

market capitalization/revenue/cashflow test [Rule 8.05(2)] or market

capitalization/revenue test [Rules 8.05(3)].

� Brilliant & Excellent Limited is able to meet the profit test since:

1) the profits attributable to shareholders of the company for 2009, 2010

and 2011 are $18 million, $20 million and $25 million respectively which

satisfy the requirement of at least $50 million in the last three financial

years with at least $20 million in the most recent year, and aggregate

profits of at least $30 million in the two preceding years)

2) management continuity for at least the three preceding financial years

3) ownership continuity and control for at least the most recent audited

financial year

� However, Brilliant & Excellent Limited is unable to satisfy the market

capitalization/revenue/cashflow test as the revenue of the company for 2011

is $490 million which is below the requirement of at least $500 million for the

most recent audited financial year and the market capitalization is only

$1,000 million [(150+100) million x $4] which is below the requirement of $2

billion at the time of listing; this is despite the fact that the company is able

to meet the requirement of positive cashflow from operating activities of at

least $100 million in aggregate for the three preceding financial years.

� Brilliant & Excellent Limited is also unable to satisfy the market

capitalization/revenue test as the company’s revenue for 2011 is below the

requirement of at least $500 million for the most recent audited financial

year and the market capitalization is below the requirement of $4 billion at

the time of listing.

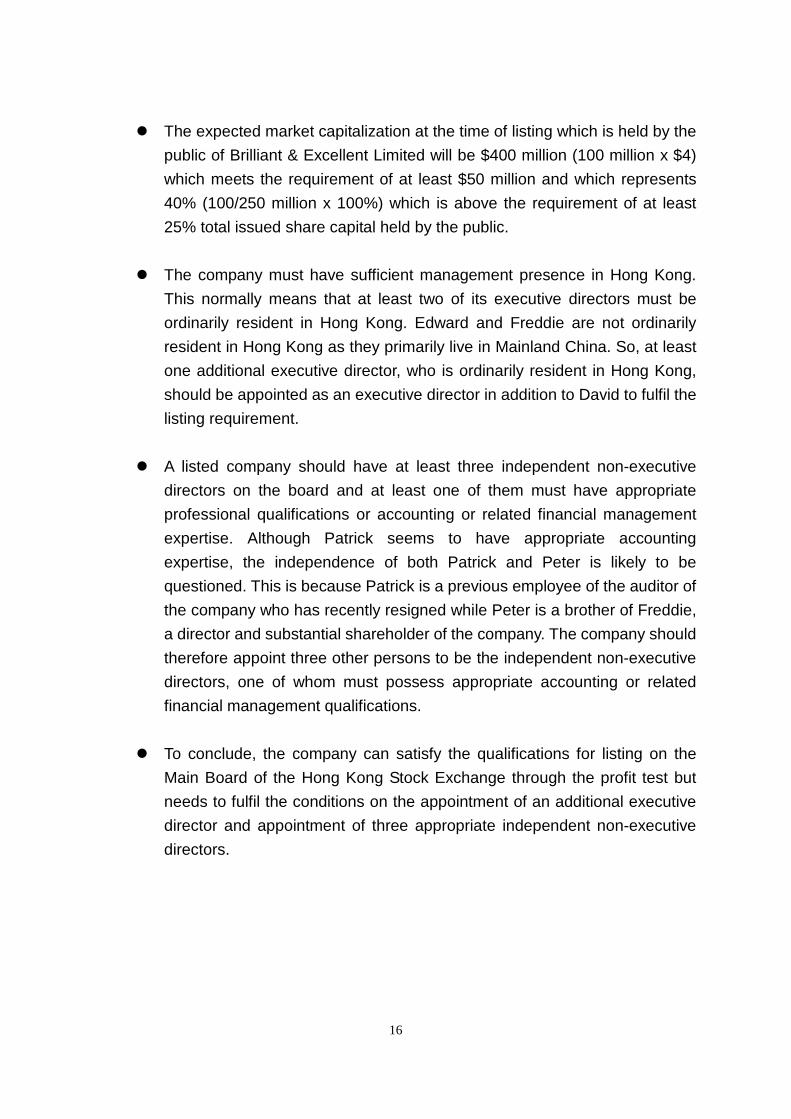

� The expected market capitalization of Brilliant & Excellent Limited is $1,000

million which satisfies the requirement of the expected market capitalization

of at least $200 million at the time of listing.

16

� The expected market capitalization at the time of listing which is held by the

public of Brilliant & Excellent Limited will be $400 million (100 million x $4)

which meets the requirement of at least $50 million and which represents

40% (100/250 million x 100%) which is above the requirement of at least

25% total issued share capital held by the public.

� The company must have sufficient management presence in Hong Kong.

This normally means that at least two of its executive directors must be

ordinarily resident in Hong Kong. Edward and Freddie are not ordinarily

resident in Hong Kong as they primarily live in Mainland China. So, at least

one additional executive director, who is ordinarily resident in Hong Kong,

should be appointed as an executive director in addition to David to fulfil the

listing requirement.

� A listed company should have at least three independent non-executive

directors on the board and at least one of them must have appropriate

professional qualifications or accounting or related financial management

expertise. Although Patrick seems to have appropriate accounting

expertise, the independence of both Patrick and Peter is likely to be

questioned. This is because Patrick is a previous employee of the auditor of

the company who has recently resigned while Peter is a brother of Freddie,

a director and substantial shareholder of the company. The company should

therefore appoint three other persons to be the independent non-executive

directors, one of whom must possess appropriate accounting or related

financial management qualifications.

� To conclude, the company can satisfy the qualifications for listing on the

Main Board of the Hong Kong Stock Exchange through the profit test but

needs to fulfil the conditions on the appointment of an additional executive

director and appointment of three appropriate independent non-executive

directors.

17

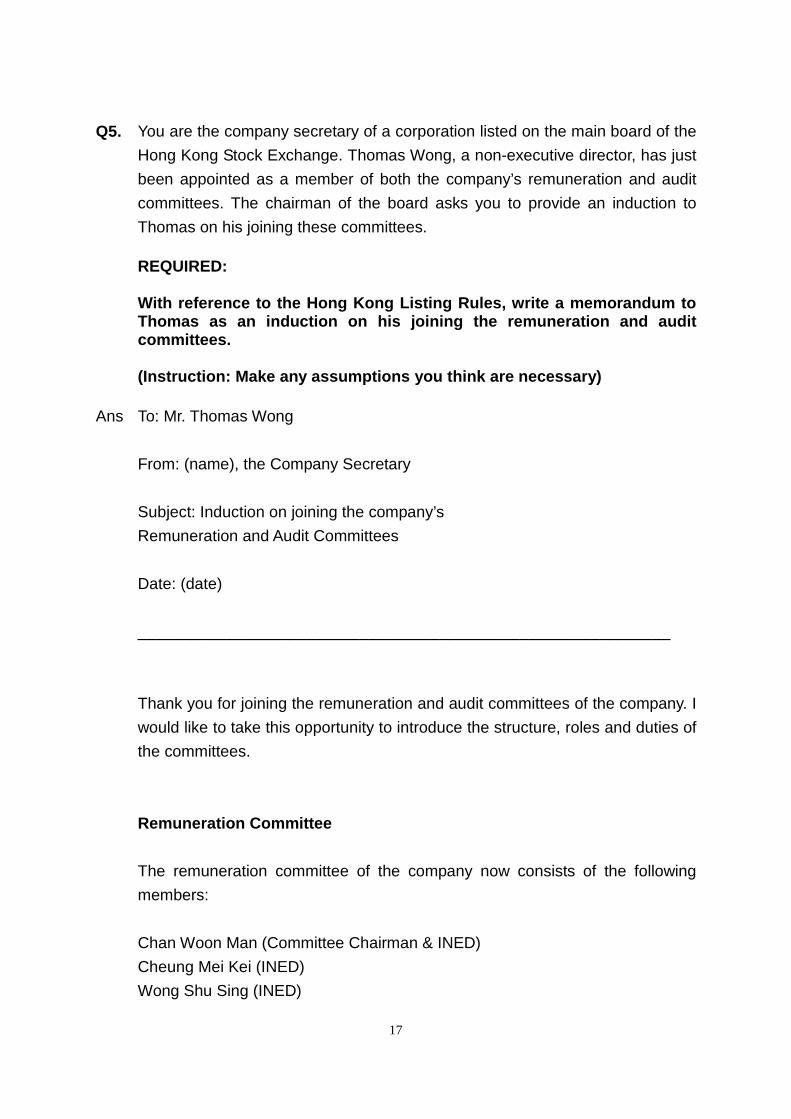

Q5. You are the company secretary of a corporation listed on the main board of the

Hong Kong Stock Exchange. Thomas Wong, a non-executive director, has just

been appointed as a member of both the company’s remuneration and audit

committees. The chairman of the board asks you to provide an induction to

Thomas on his joining these committees. REQUIRED: With reference to the Hong Kong Listing Rules, writ e a memorandum to Thomas as an induction on his joining the remunerat ion and audit committees. (Instruction: Make any assumptions you think are ne cessary)

Ans To: Mr. Thomas Wong

From: (name), the Company Secretary

Subject: Induction on joining the company’s

Remuneration and Audit Committees

Date: (date)

____________________________________________________________

Thank you for joining the remuneration and audit committees of the company. I

would like to take this opportunity to introduce the structure, roles and duties of

the committees.

Remuneration Committee

The remuneration committee of the company now consists of the following

members:

Chan Woon Man (Committee Chairman & INED)

Cheung Mei Kei (INED)

Wong Shu Sing (INED)

18

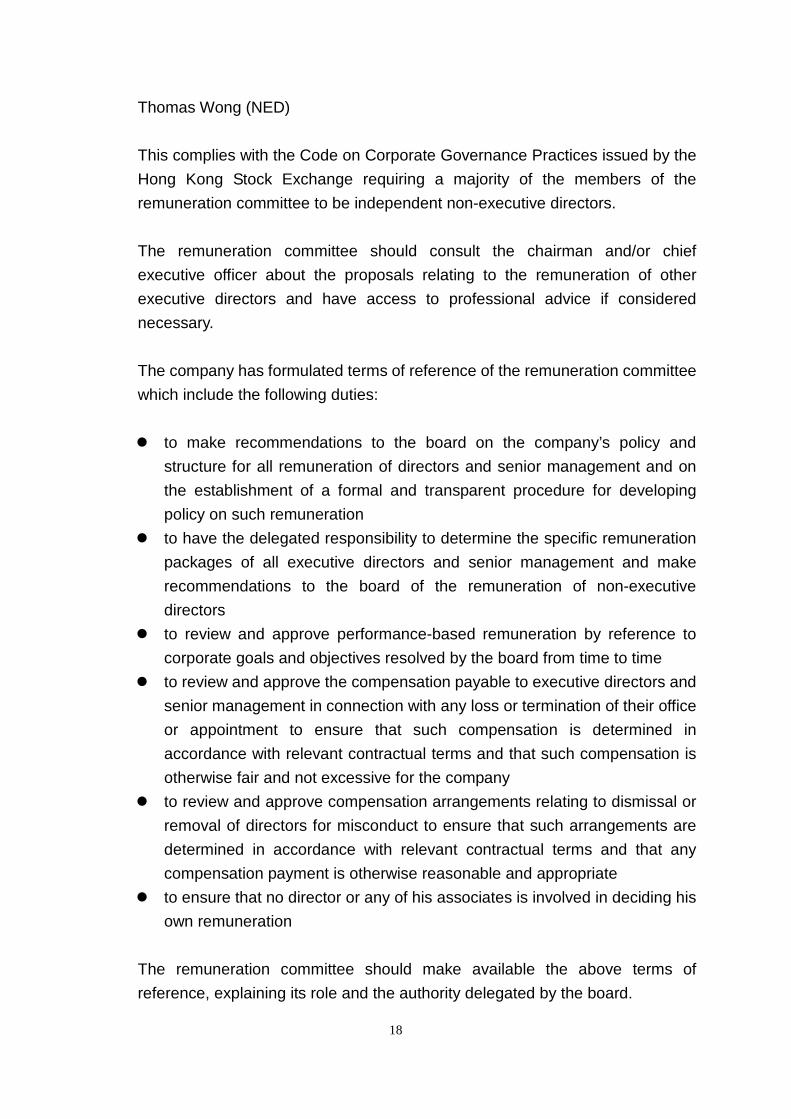

Thomas Wong (NED)

This complies with the Code on Corporate Governance Practices issued by the

Hong Kong Stock Exchange requiring a majority of the members of the

remuneration committee to be independent non-executive directors.

The remuneration committee should consult the chairman and/or chief

executive officer about the proposals relating to the remuneration of other

executive directors and have access to professional advice if considered

necessary.

The company has formulated terms of reference of the remuneration committee

which include the following duties:

� to make recommendations to the board on the company’s policy and

structure for all remuneration of directors and senior management and on

the establishment of a formal and transparent procedure for developing

policy on such remuneration

� to have the delegated responsibility to determine the specific remuneration

packages of all executive directors and senior management and make

recommendations to the board of the remuneration of non-executive

directors

� to review and approve performance-based remuneration by reference to

corporate goals and objectives resolved by the board from time to time

� to review and approve the compensation payable to executive directors and

senior management in connection with any loss or termination of their office

or appointment to ensure that such compensation is determined in

accordance with relevant contractual terms and that such compensation is

otherwise fair and not excessive for the company

� to review and approve compensation arrangements relating to dismissal or

removal of directors for misconduct to ensure that such arrangements are

determined in accordance with relevant contractual terms and that any

compensation payment is otherwise reasonable and appropriate

� to ensure that no director or any of his associates is involved in deciding his

own remuneration

The remuneration committee should make available the above terms of

reference, explaining its role and the authority delegated by the board.

19

Audit Committee

The audit committee of the company now consists of the following members

which complies with rule 3.21 of the Listing Rules:

Chan Woon Man, FCCA (Committee Chairman & INED)

Wong Shu Sing (INED)

Wong Chi Fai (INED)

Thomas Wong (NED)

The committee comprises non-executive directors only, with a minimum of three

members and at least one is an independent non-executive director with an

appropriate professional qualification. The chairman of the committee is an

independent non-executive director.

I am the secretary of the audit committee and responsible for ensuring that full

minutes of the committee meetings have been kept. Draft and final versions of

minutes of the audit committee meetings are sent to all members of the

committee for comment and records respectively, in both cases within a

reasonable time after the meeting.

The terms of reference of the audit committee include the following duties:

� to be primarily responsible for making recommendations to the board on the

appointment, reappointment and removal of the external auditor, and to

approve the remuneration and terms of engagement of the external auditor,

and any questions of resignation or dismissal of that auditor

� to review and monitor the external auditor’s independence and objectivity

and the effectiveness of the audit process in accordance with applicable

standards

� to develop and implement policy on the engagement of an external auditor

to supply non-audit services

� to monitor the integrity of the company’s financial statements and the

company’s annual report and accounts, half-year report and, if prepared for

publication, quarterly reports, and to review significant financial reporting

judgments contained in them

� members of the committee must liaise with the company’s board of

20

directors, senior management and the qualified accountant and must meet,

at least once a year, with the company’s auditors

� the committee should consider any significant or unusual items that are, or

may need to be, reflected in such reports and accounts and must give due

consideration to any matters that have been raised by the company’s

qualified accountant, compliance officer or auditors

� to review the company’s financial controls, internal control and risk

management systems

� to discuss with the management the system of internal control and ensure

that management has discharged its duty to have an effective internal

control system

� to consider any findings of major investigations of internal control matters as

delegated by the board or on its own initiative and management’s response

� where an internal audit function exists, to ensure co-ordination between the

internal and external auditors, and to ensure that the internal audit function

is adequately resourced and has appropriate standing within the company,

and to review and monitor the effectiveness of the internal audit function

� to review the group’s financial and accounting policies and practices

� to review the external auditor’s management letter, any material queries

raised by the auditor to management in respect of the accounting records,

financial accounts or systems of control and management’s response

� to ensure that the board will provide a timely response to the issues raised

in the external auditor’s management letter

� to report to the board on the matters set out in this code provision

� to consider other topics, as defined by the board

The audit committee should make available the above terms of reference,

explaining its role and the authority delegated by the board.

This induction brief aims to give you an introduction to the committees you are

joining. I also attach the minutes of the two committees’ meetings over the past

12 months for your reference. I will be pleased to provide any appropriate

information regarding the committees which you require.

21

Q6. You are the company secretary of Prosperous Future Development Limited, a

private company incorporated in Hong Kong. Betty Fong, a shareholder holding

5,000 ordinary shares in the company, has just informed the board of directors

that she has recently lost her share certificate No. 20. She therefore requests

that the company issue a new share certificate as a replacement.

Betty also tells the board that she is considering liquidating her investment in

the company in order to finance her son’s further studies. She therefore asks

the board whether the company can buy back her shares for a consideration of

$500,000. The company’s distributable profits are $300,000.

REQUIRED:

Q6 (a) Write a reply letter to Betty explaining the formal ities regarding the

company’s issue of a new share certificate in place of the lost one.

(Instruction: A full letter is not required. You ar e only required to

write the content of the letter)

Ans (a) Re: Replacement of lost share certificate

With reference to your reporting the loss of your share certificate No. 20

and requesting a replacement, we would like to advise you of the

formalities regarding the replacement of the lost share certificate as

follows:

1) Please submit an application for the issue of a new certificate, a letter

of indemnity or a bank guarantee with a fee of (amount of fee, if any)

covering the issue of a new certificate.

2) If all the documents under above item 1 are in order, we will arrange to

pass a board resolution to approve the cancellation of the lost

certificate and the issue of a new certificate.

3) We will also record the cancellation and issue of the certificate in the

register of members.

22

4) Finally, we will issue a new share certificate and notify you to collect

the new certificate when it is available.

If you have any further queries, please do not hesitate to contact us.

Q6 (b) Prosperous Future Development Limited asks Betty to sign a letter

indemnifying the company in respect of the lost share certificate.

Draft the indemnity letter to be signed by Betty.

Ans (b) INDEMNITY FOR LOST SHARE CERTIFICATE

To: Prosperous Future Development Limited

(company address)

I, Betty Fong of (registered address), do hereby request Prosperous

Future Development Limited to issue a duplicate certificate to me for 5,000

shares of the Company registered in the name of Betty Fong, for the

following original certificate being lost:

Certificate No. No. of Shares Type of Shares

20 5,000 Ordinary

In consideration of the Company agreeing to issue the duplicate certificate

requested by me, I do hereby agree to keep indemnified the Company and

hold the Company harmless from and against all claims, liabilities, losses,

charges, damages, costs and expenses which may be made against or

suffered or incurred by the Company by reason or in consequence of the

issue of such duplicate certificate or otherwise howsoever in relation

thereto.

Date this 3 day of June 2011

SIGNED by Betty Fong )

in the presence of : )_______________________

) Betty Fong

23

Q6 (c) Advise the board if it is feasible for the company to purchase Betty’s

shares.

Ans (c) Fully paid shares may be purchased out of the company’s distributable

profits or out of the proceeds of a fresh issue of shares made for the

purpose of a repurchase. Private companies may also make repurchases

out of capital.

If the consideration for the repurchase of Betty’s shares is $500,000, then

it exceeds the distributable profits, $300,000, by $200,000. The

repurchase would then be partly out of capital. This can be done only if

the is company is able to pay its debts for a year after the repurchase

(section 49K of the Companies Ordinance). The repurchase of shares out

of capital should also be authorised by the company’s articles of

association and approved by a special resolution in a general meeting.

The company may also repurchase Betty’s shares partly out of the

proceeds of a fresh issue of shares. This should also be authorised by the

company’s articles of association and approved by a special resolution in

a general meeting. In order to do this, there should be sufficient unissued

authorised capital to cover the intended issue of new shares. Otherwise,

an increase in authorised capital should be made.

So Prosperous Future Development Limited can repurchase Betty’s

shares partly out of distributable profits, proceeds of a fresh of shares

and/or out of capital subject to the fulfilment of the above conditions.

END

![The Company Secretaries Act, 1980 · The Company Secretaries Act, 1980 No. 56 of 1980 [10th December, 1980] ... of the Indian Partnership Act, 1932, and includes,- (i) the limited](https://img.pdfslide.net/doc/110x75/5e8bc048b77fae4d1c5c335e/the-company-secretaries-act-1980-the-company-secretaries-act-1980-no-56-of-1980.jpg)

![Segmentação semântica Segmentação de elipses e retângulos ... · cv2.imwrite(argv[3],QP) else: qp=255.0*((qp/2.0)+0.5) # Entre 0 e 255 qp=np.clip(qp,0,255) QP=np.uint8(qp) cv2.imwrite(argv[3],QP)](https://img.pdfslide.net/doc/110x75/5fdd6f6848d04c49b8566bce/segmentao-semntica-segmentao-de-elipses-e-retngulos-cv2imwriteargv3qp.jpg)