Embed Size (px)

DESCRIPTION

A really informative presentation by Dr Bhasker Chatterji on CSR Activities for corporates.

Citation preview

Dr. Bhaskar ChatterjeeDG&CEO

Indian Institute of Corporate Affairs

SECTION 135» Every company having a net worth of rupees five

hundred crore or more (100 million $ or more),or a turnover of rupees one thousand crore or more (200 million $ or more) , or a net profit of rupees five crore or more (1 million $ or more) during any financial year shall constitute a Corporate Social Responsibility Committee of the Board consisting of three or more directors, out of which at least one director shall be an independent director;

» The Board's report shall disclose the composition of the Corporate Social Responsibility Committee.

2

3) The Corporate Social Responsibility Committee shall,

a. formulate and recommend to the Board, a Corporate Social Responsibility Policy which shall indicate the activities to be undertaken by the company as specified in Schedule VII;

b. recommend the amount of expenditure to be incurred on the activities referred to in clause (a); and

c. monitor the Corporate Social Responsibility Policy of the company from time to time.

3

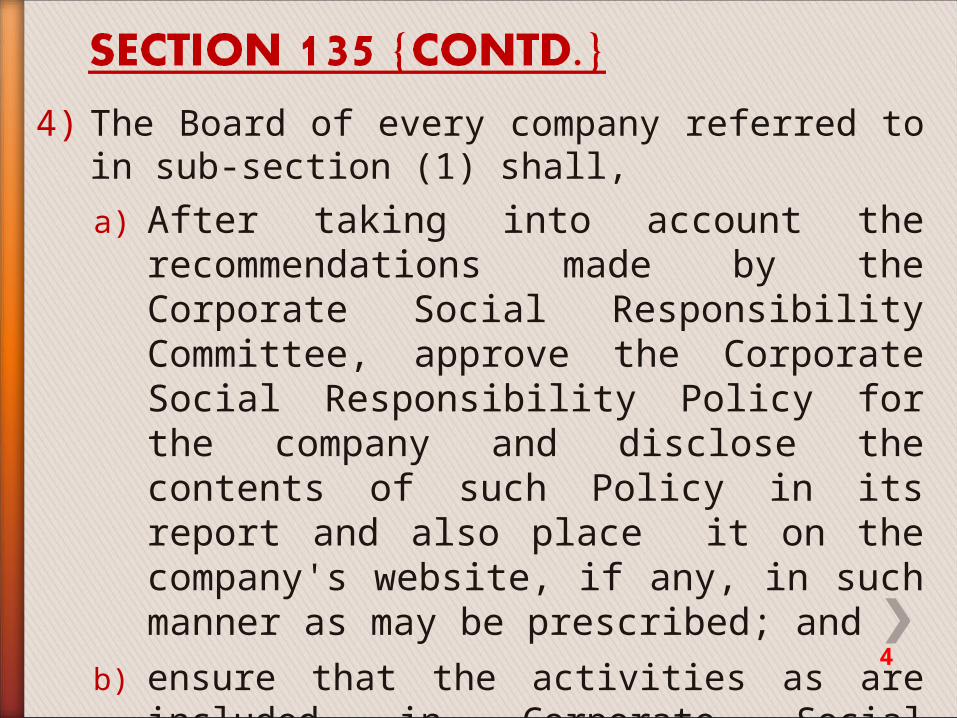

4) The Board of every company referred to in sub-section (1) shall,

a) After taking into account the recommendations made by the Corporate Social Responsibility Committee, approve the Corporate Social Responsibility Policy for the company and disclose the contents of such Policy in its report and also place it on the company's website, if any, in such manner as may be prescribed; and

b) ensure that the activities as are included in Corporate Social Responsibility Policy of the company are undertaken by the company.

.4

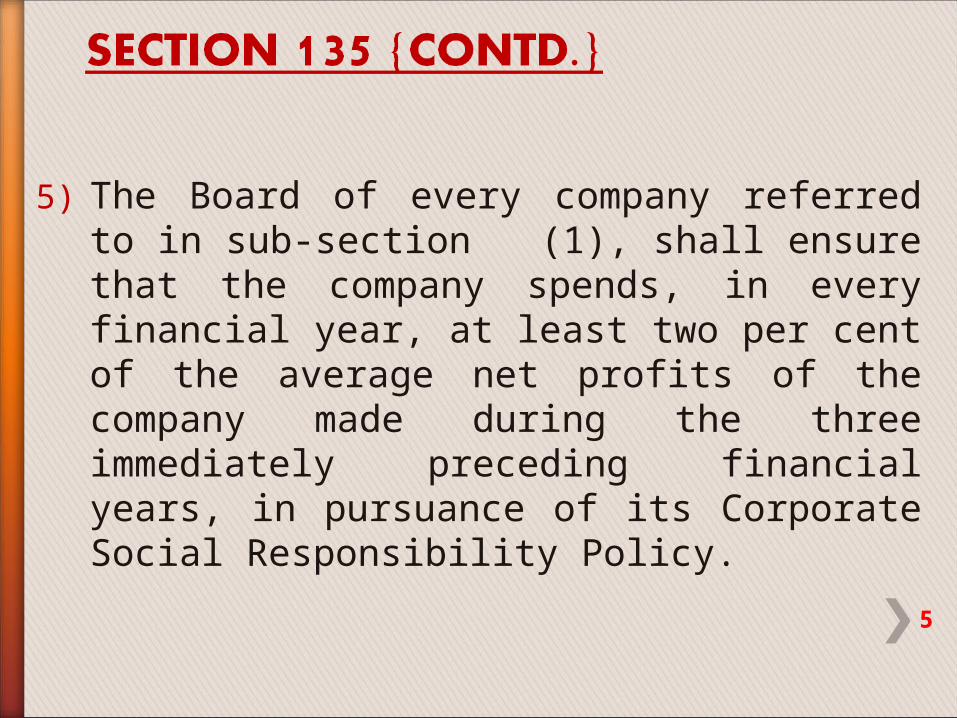

5) The Board of every company referred to in sub-section (1), shall ensure that the company spends, in every financial year, at least two per cent of the average net profits of the company made during the three immediately preceding financial years, in pursuance of its Corporate Social Responsibility Policy.

5

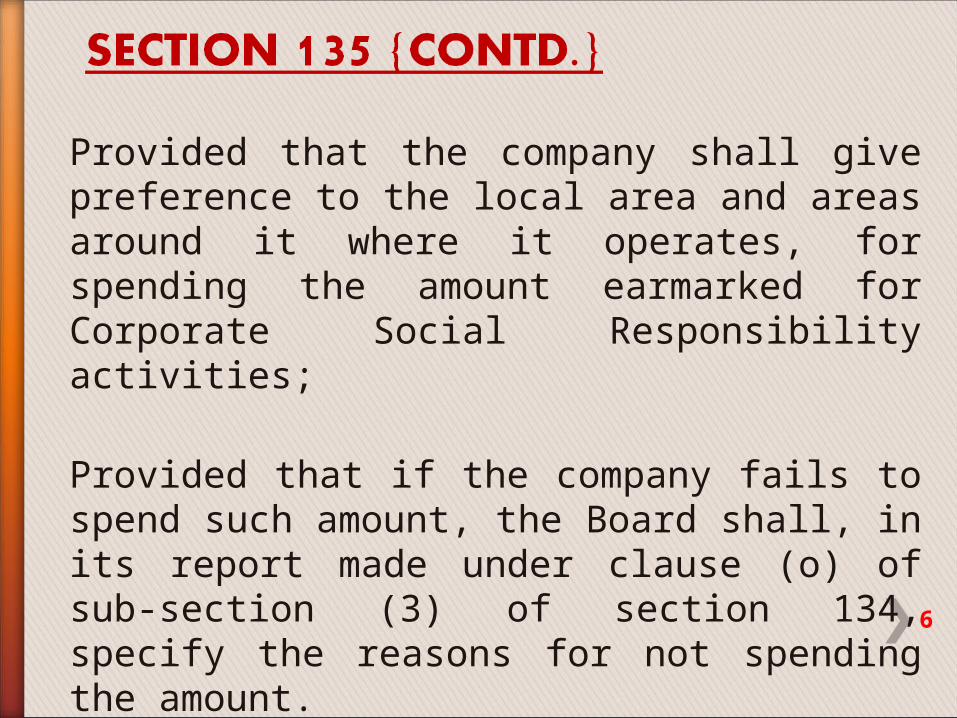

Provided that the company shall give preference to the local area and areas around it where it operates, for spending the amount earmarked for Corporate Social Responsibility activities;

Provided that if the company fails to spend such amount, the Board shall, in its report made under clause (o) of sub-section (3) of section 134, specify the reasons for not spending the amount.

6

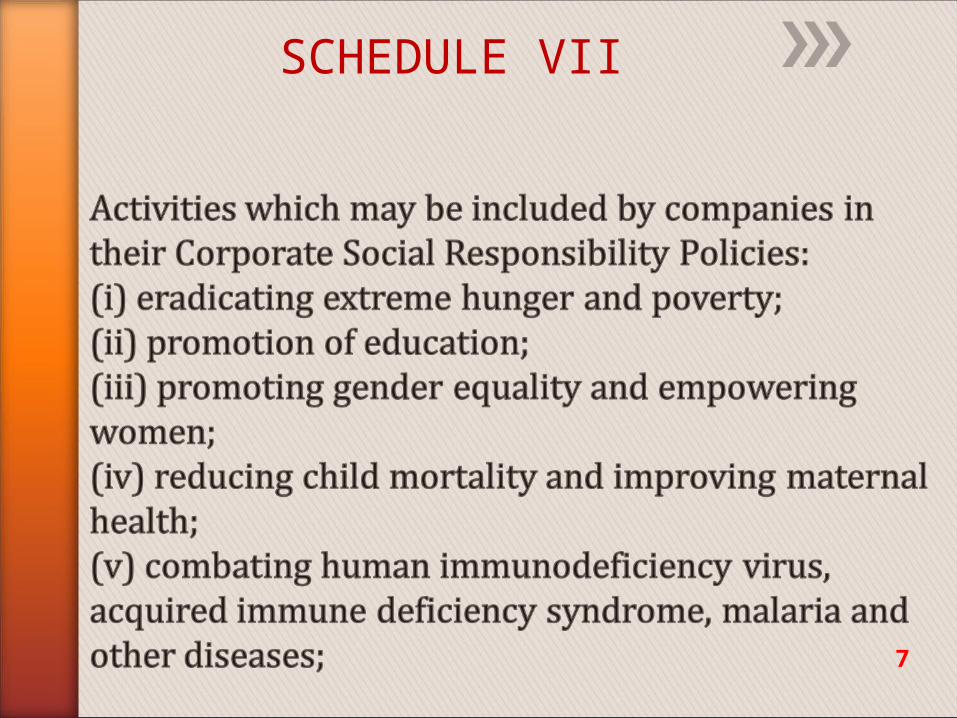

SCHEDULE VII

7

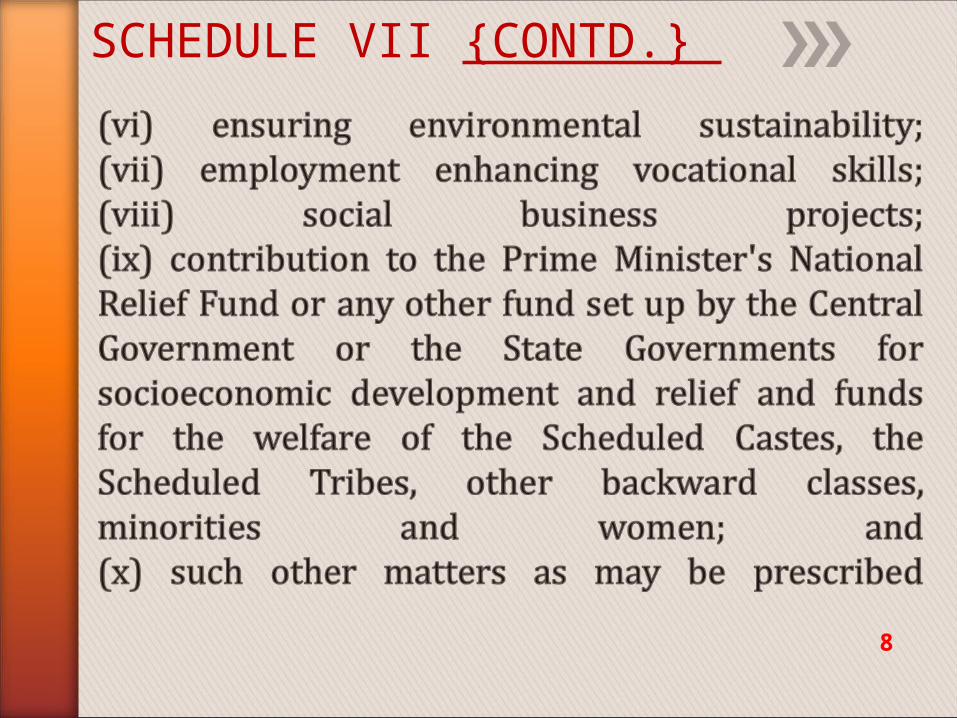

SCHEDULE VII {CONTD.}

8

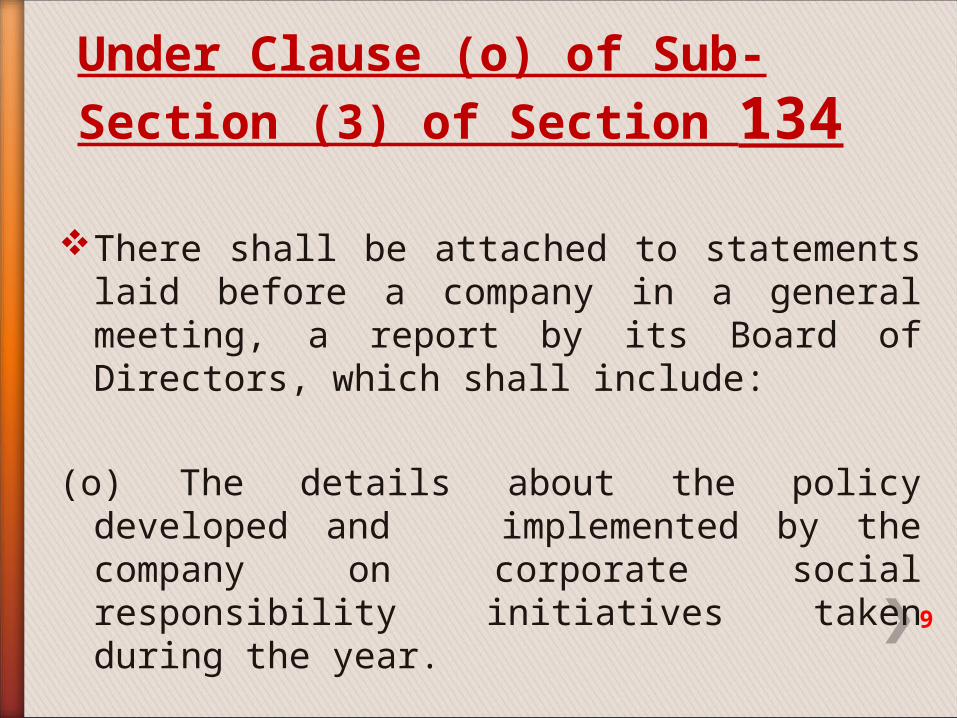

Under Clause (o) of Sub-Section (3) of Section 134

There shall be attached to statements laid before a company in a general meeting, a report by its Board of Directors, which shall include:

(o) The details about the policy developed and implemented by the company on corporate social responsibility initiatives taken during the year.

9

If a company contravenes the provisions of this section, the company shall be punishable with fine which shall not be less than fifty thousand rupees but which may extend to twenty-five lakh rupees and every officer of the company who is in default shall be punishable with imprisonment for a term which may extend to three years or with fine which shall not be less than fifty thousand rupees but which may extend to five lakh rupees, or with both.

Sub Section (8) of Section 134

10

If a company or any officer of a company or any other person contravenes any of the provisions of this Act or the rules made thereunder, or any condition, limitation or restrictions subject to which any approval, sanction, consent, confirmation, recognition, direction or exemption in relation to any matter has been accorded, given or granted, and for which no penalty or punishment is provided elsewhere in this Act, the company and every officer of the company who is in default or such other person shall be punishable with fine which may extend to ten thousand rupees, and where the contravention is continuing one, with a further fine which may extend to one thousand rupees for every day after the first during which the contravention continues.

Section 450

11

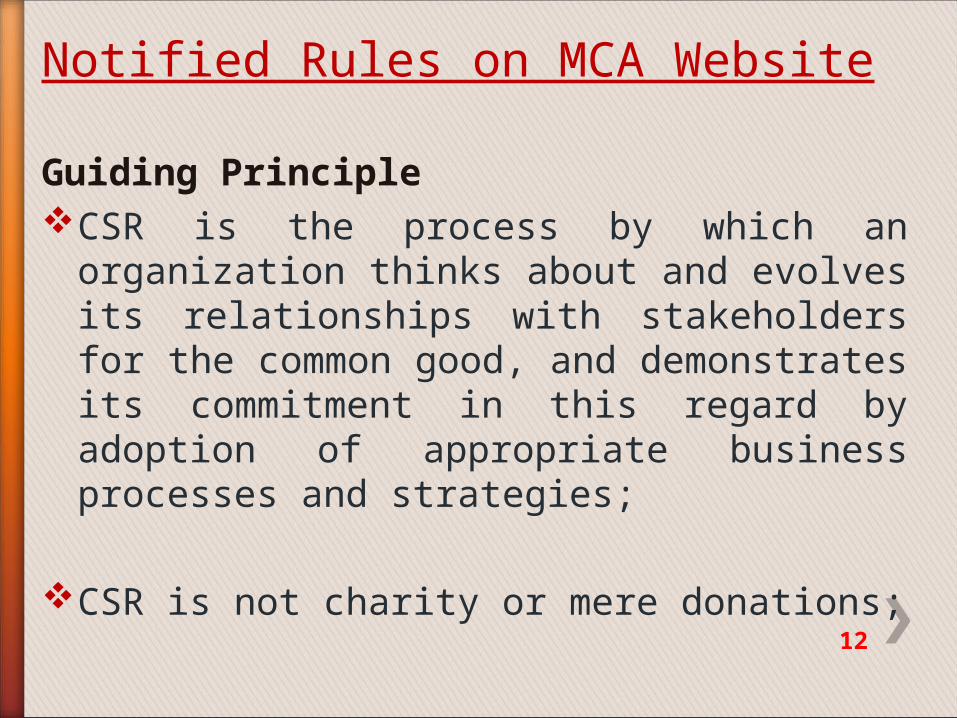

Guiding PrincipleCSR is the process by which an organization thinks

about and evolves its relationships with stakeholders for the common good, and demonstrates its commitment in this regard by adoption of appropriate business processes and strategies;

CSR is not charity or mere donations;

Notified Rules on MCA Website

12

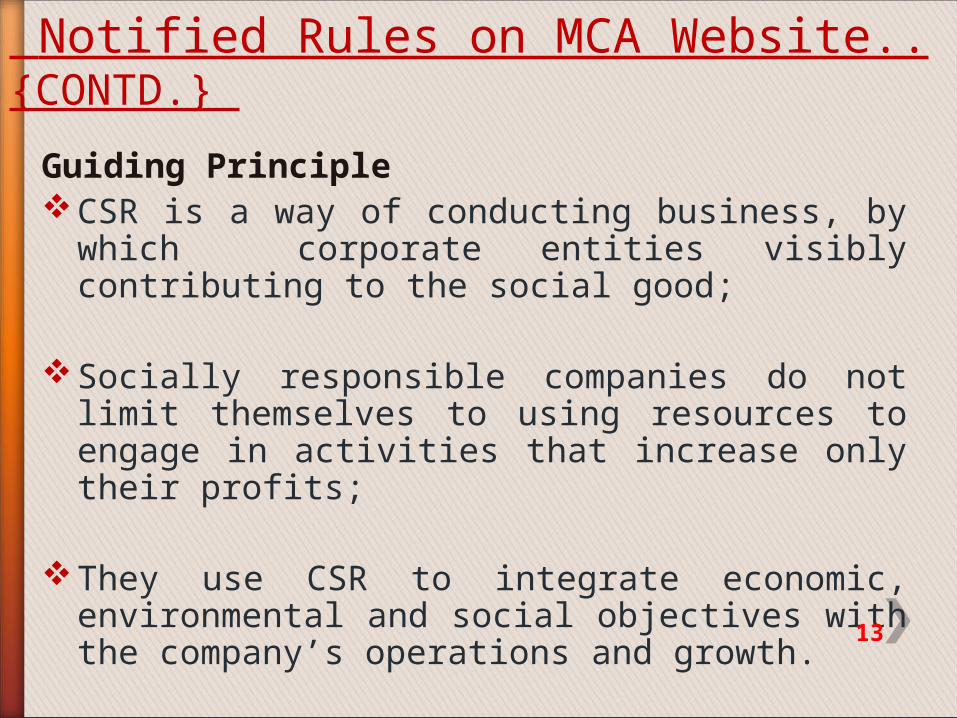

Guiding PrincipleCSR is a way of conducting business, by which

corporate entities visibly contributing to the social good;

Socially responsible companies do not limit themselves to using resources to engage in activities that increase only their profits;

They use CSR to integrate economic, environmental and social objectives with the company’s operations and growth.

Notified Rules on MCA Website..{CONTD.}

13

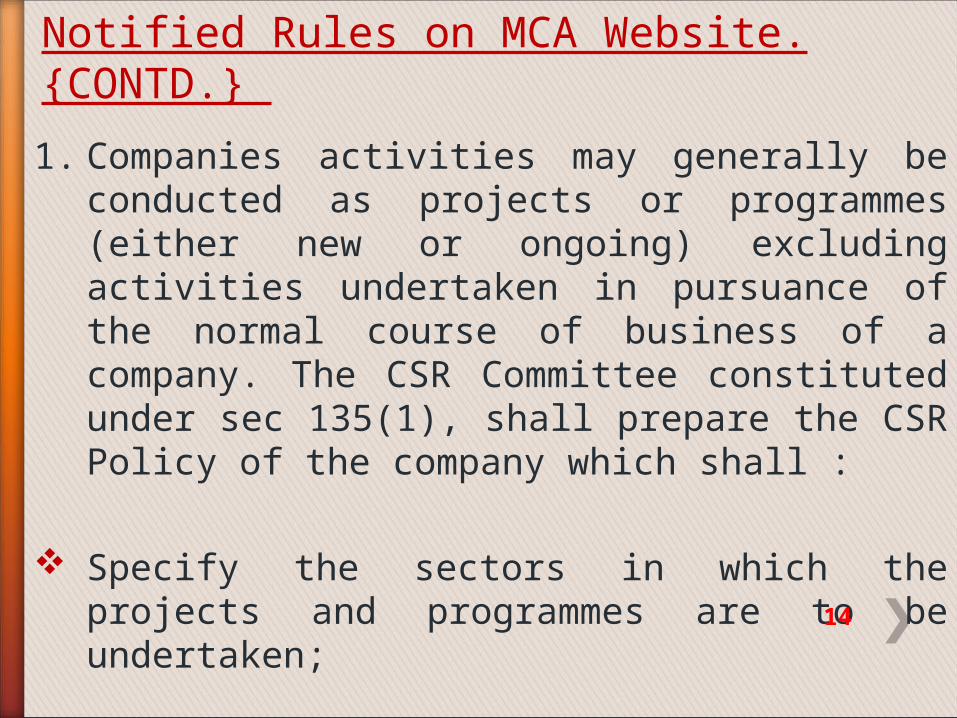

1. Companies activities may generally be conducted as projects or programmes (either new or ongoing) excluding activities undertaken in pursuance of the normal course of business of a company. The CSR Committee constituted under sec 135(1), shall prepare the CSR Policy of the company which shall :

Specify the sectors in which the projects and programmes are to be undertaken;

Notified Rules on MCA Website.{CONTD.}

14

Prepare a list of CSR projects/programmes which a company plans to undertake during the implementation year, specifying modalities of execution in the areas/sectors chosen and implementation schedules for the same;

Focus on integrating business models with social and environmental priorities and processes in order to create shared value;

Provide that surpluses arising out of CSR activities will not be part of the business profits of a company.

Notified Rules on MCA Website..{CONTD.}

15

2. The CSR Committee shall prepare a transparent monitoring mechanism for ensuring implementation of the projects / programmes / activities proposed to be undertaken by the company.

Notified Rules on MCA Website..{CONTD.}

16

3. Where a company has set up an organization which is registered as a Trust or Section 8 Company, or Society or any other form of entity incorporated in India to facilitate implementation of its CSR activities in accordance with its stated CSR Policy,

a) The contributing company should specify the activities to be undertaken by such an organization utilizing funds provided by it;

b) The contributing company shall establish a monitoring mechanism to ensure that the allocation is spent for the intended purpose only.

Notified Rules on MCA Website..{CONTD.}

17

4. A company may also conduct/implement its CSR programmes through Trusts, Societies or Section 8 companies incorporated in India, which are not set up by the company itself;

5. Such spends may be included as part of its prescribed CSR spend only if such organizations have an established track record of at least three years in carrying on activities in related areas.

Notified Rules on MCA Website...{CONTD.}

18

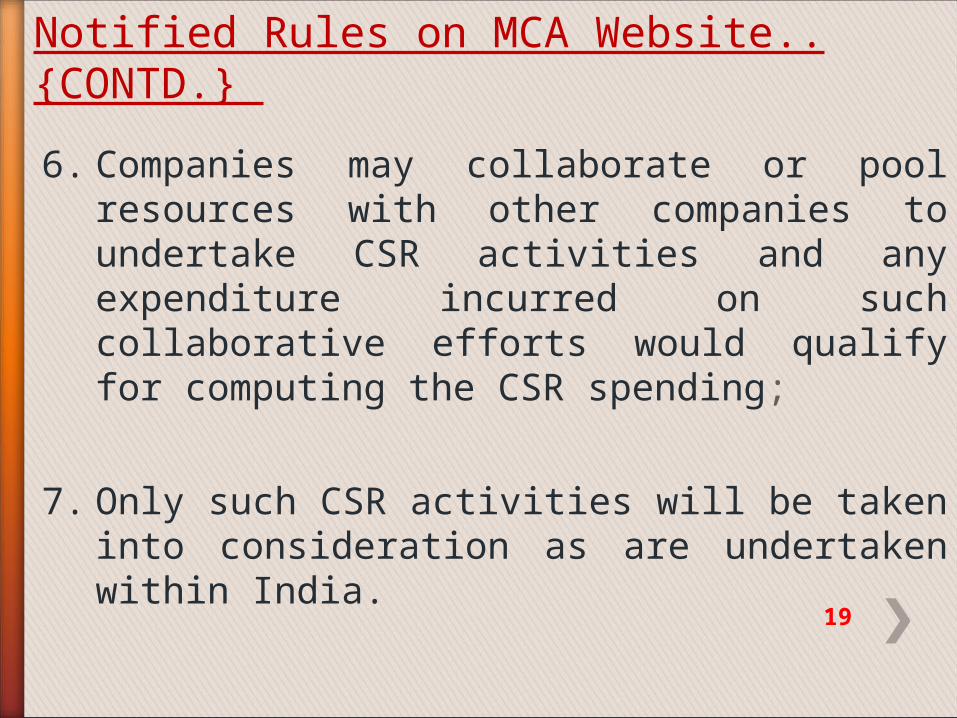

6. Companies may collaborate or pool resources with other companies to undertake CSR activities and any expenditure incurred on such collaborative efforts would qualify for computing the CSR spending;

7. Only such CSR activities will be taken into consideration as are undertaken within India.

Notified Rules on MCA Website..{CONTD.}

19

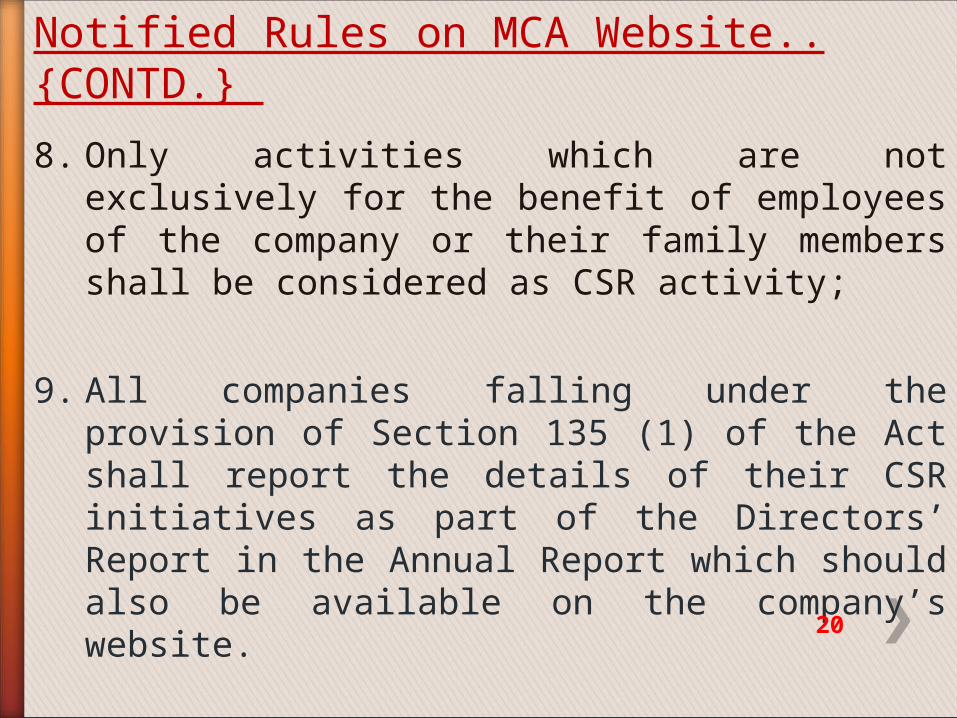

8. Only activities which are not exclusively for the benefit of employees of the company or their family members shall be considered as CSR activity;

9. All companies falling under the provision of Section 135 (1) of the Act shall report the details of their CSR initiatives as part of the Directors’ Report in the Annual Report which should also be available on the company’s website.

Notified Rules on MCA Website..{CONTD.}

20

What is CSR and what is not?

21

What is CSR? What is not CSR?

It should be rupee measurable;

That which is not rupee measurable is not a CSR activity;

It must bring direct benefits to marginalized , disadvantaged, poor or deprived sections of the community;

If it does not benefit the poor & backward sections of the community it is not a CSR activity;

It should not pre-dominantly benefit employees of the company;

Employee benefits will not count as CSR;

What is CSR and what is not?

22

What is CSR? What is not CSR?

It can be related to the core business or the business model. It can thus deliver shared value;

It must not be part of the core business of the company;

Where a shared value project is to be shown as CSR, the company should quantify the direct rupee benefit accruing to the identified beneficiaries;

The total value of the project itself cannot be shown as CSR;

It must be a sustained activity over a period of time;

One-off or intermittent activities will not count as CSR;

23

What is CSR? What is not CSR?CSR activities must be in the form of projects/programmes. Thus CSR activities should be projectivized ;Components of a project are as follows: •Need Based Assessment/Baseline Survey/Study•Clearly identified time frame•Specific annual financial allocation•Clearly identified milestones•Clearly identified & measurable objectives /goals•Robust & periodic review & monitoring•Evaluation & Assessment (Where possible, by third party)

Pure philanthropy or mere donations will not count as CSR

What is CSR and what is not?

24

What is CSR What is not CSR?

Corporates are expected to fund projects from their own accounts through implementing agencies;

Government programmes/initiatives can be complemented/supplemented

Programmes/projects must be within India;

Funds/moneys deposited in Central or Government accounts will not count as CSR;

Government programmes/initiatives should not be duplicated.

Programmes/projects undertaken outside India will not count as CSR;

What is CSR and what is not?

25

What is CSR What is not CSR?

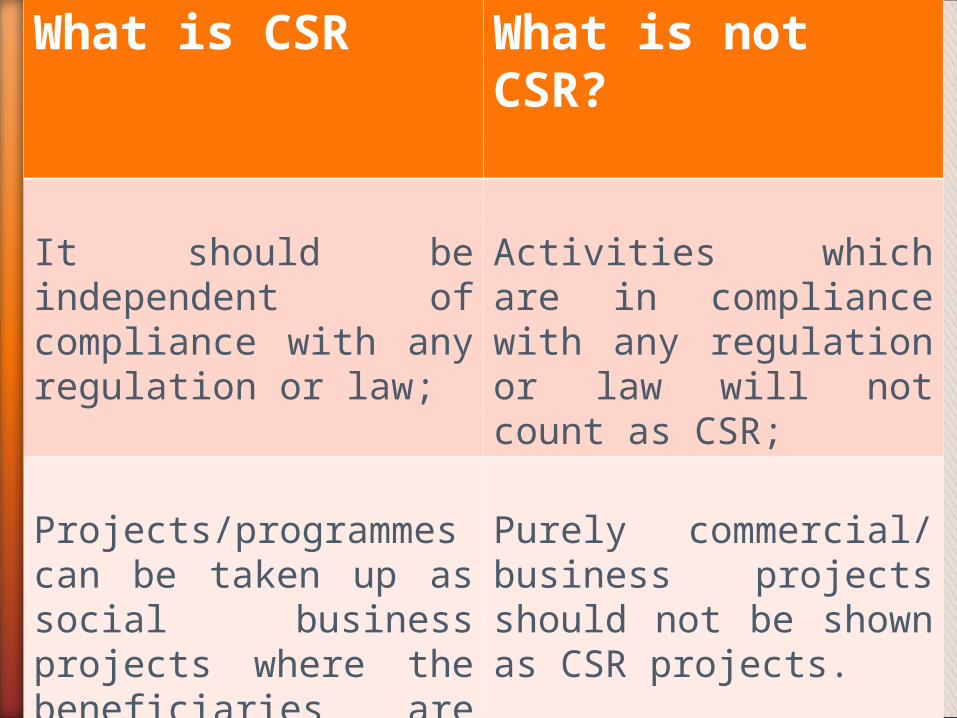

It should be independent of compliance with any regulation or law;

Activities which are in compliance with any regulation or law will not count as CSR;

Projects/programmes can be taken up as social business projects where the beneficiaries are the poor and marginalised.

Purely commercial/ business projects should not be shown as CSR projects.

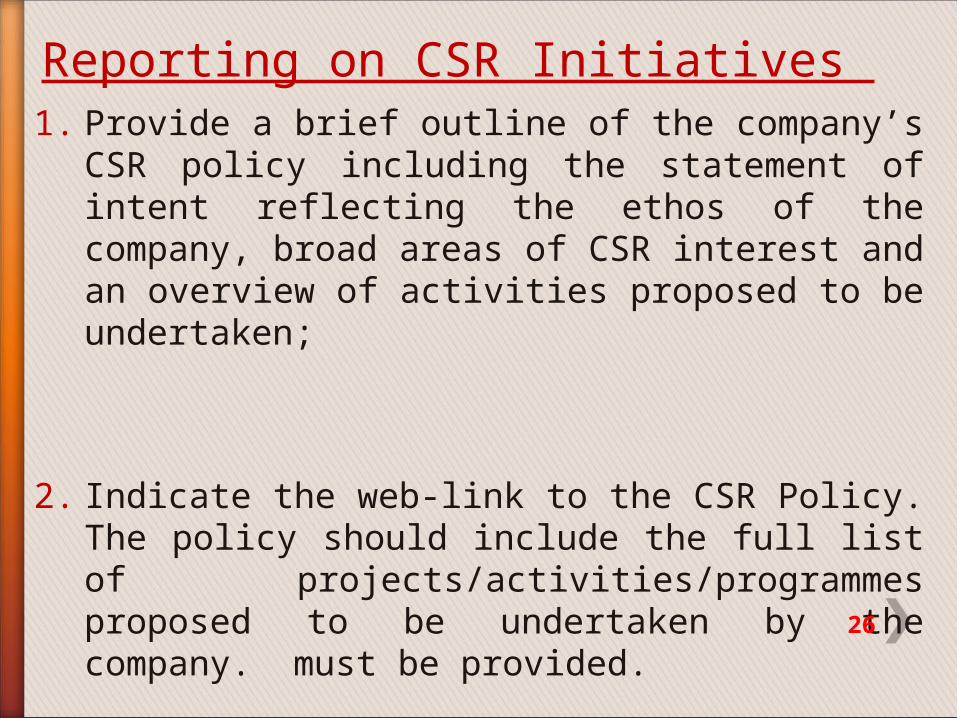

1. Provide a brief outline of the company’s CSR policy including the statement of intent reflecting the ethos of the company, broad areas of CSR interest and an overview of activities proposed to be undertaken;

2. Indicate the web-link to the CSR Policy. The policy should include the full list of projects/activities/programmes proposed to be undertaken by the company. must be provided.

Reporting on CSR Initiatives

26

3. The composition of CSR Committee

4. Average Net Profit of the company for last 3 financial years

5. Threshold limit (2% of this amount as in 4 above)

Reporting on CSR Initiatives…{CONTD.}

27

6. Details of CSR activities/projects undertaken during the year in the following table :

total amount to be spent for the year;

amount carried forward from earlier years;

Amount spent during the year as below;

Amount carried forward for the year.

y

Reporting on CSR Initiatives…{CONTD.}

28

7. In case the company has failed to spend the 2% of Average Net Profit (INR) of last 3 financial years, please provide the reasons for not spending the amount;

8. A responsibility statement of the CSR Committee, that the CSR Policy implementation and monitoring thereof is, in letter and spirit, in compliance with CSR Objectives.

Reporting on CSR Initiatives…{CONTD.}

29

6. Details of CSR activities/projects undertaken during the year in the following table : (cont’d)

* Give details of Implementing Agency

30

Reporting on CSR Initiatives…{CONTD.} 1

.

S

r

N

o

.

2.

CSR

project/activit

y identified

3.

Sector in

which the

project is

covered

4.

Projects/

Programmes

1.Local

areas/others

2.Specify the

state/district

5.

Amount

outlay

(budget)

project/pro

gramme

wise

6.

Amount

spent on

the

programm

e/project

Subheads

1.Direct

expenditur

e on

projects

2.Over

heads

7.

Cumulative

spend upto

the

reporting

period

8.

Amount

spent

Direct

through

impleme

nting

agency

Total

30

Signed

………………………………………….. (CEO/Managing Director/Director)

…………………………………… (Chairman CSR Committee)

Reporting on CSR Initiatives…{CONTD.}

31

THE SIZE OF THE CSR SPACE

Around 16,245 companies fall within the purview of Section 135;

Around 20,000 crores in total, will be spent by Corporates each year on CSR;

Around 30,000 Directors of Boards will be directly involved.

32

WHAT THE CSR ROLL OUT ENTAILS» Need for a large number of CSR professionals

(around 30,000 – 16,000 companiesx2);

» Need to create an NGO Hub which will, inter alia, empanel credible implementing agencies;

» Need to create a shelf of projects from which companies and Implementing Agencies may choose;

33

CSR ROLL OUT ENTAILS Contd… Currently there are approx. 3.3 million (33 lakh) regd. NGO’s in India;

Probably around ten lakh fully functional - ready to face implementation challenges;

Average absorptive capacity of NGOs – around 20 lakhs annually;

Hence around 1,00,000 NGOs required at the very least to carry forward CSR agenda.

34

IICA TO TAKE CSR FORWARDBeginning June 2014, will start world’s

first Professional Course on CSR;

Duration – 9 months; Methodology: On-line

First year: 200 candidates – 100 open, 100 sponsored;

Will start empanelment of NGO’s – 3 tier process: Registration, Document Verification; Field level test checks;

35

IICA TO TAKE FORWARD CSR Contd…Will create a Shelf of Projects;

For this will invite proposals on an open forum;

Anyone or any institution/body can submit;

Proposals will be evaluated by IICA;

Those considered doable, replicable, scalable, will be shortlisted,

36

IICA TO TAKE CSR FORWARD…Those whose projects have been shortlisted, will be asked to make

presentation;

Selected projects will be suitable rewarded;

Selected projects will be placed on IICA web site for Companies to select from and fund;

More than one Company can pool their resources to fund a

project;

IICA would be happy to coordinate this and finalise project funding;

IICA would also assist in locating mutually acceptable implementing agency;

37

IICA TO TAKE FORWARD CSR Contd…

Will create a comprehensive Data Base of Projects undertaken and executed;

Will compile all returns filed by companies and prepare data analytics;

Will assist all initiatives in the training and capacity development of Company and NGO personnel.

38

39