Embed Size (px)

Citation preview

1

CSR ratings: Does more information add more value?

Magali DelmasUCLA

PRI Academic Network Conference2014 Montreal

2

CSR Ratings• $3.74 trillion in assets managed according to

socially responsible criteria/strategies 2010 (SIFF 2012)

• More than 50 different sustainability ratings

3

4

Are green companies managed differently?

The tip of the iceberg?

5

6

Competitive Advantage

H1 H2

Absorptive Capacity

KnowledgeAcquisition

Comparative CostAdvantage

Reputation Advantage

Innovation/ Differentiation

Advantage

Environmental Proactivity

Regulatory Proactivity

Operational Improvement

EnvironmentalPartnerships

Environmental Reporting

KnowledgeAssimilation

KnowledgeTransformation

KnowledgeExploitation

Delmas, M., Hoffmann, V. H., & Kuss, M. (2011).

Corporate Social Responsibility

ISO 14001 standard

Organic Labeling

Fair Trade

Other CSRstandards

EmployeeTraining

Labor Productivity

Interpersonal contacts

Employee positive social identification

with firm

Employee retention

Employee health and Safety

Firm attractivenessto prospective

employees

The adoption of environmental and social practices is associated with greater labor productivity.

EmployeeEngagement

7Delmas, M. A., & Pekovic, S. (2013).

8

Research questions

• What do SRI ratings actually measure?• What aspect of SRI does the market respond to?• When do SRI investments pay?

– Delmas, M., Etzion, D., & Nairn-Birch, N. (2013). Triangulating Environmental Performance: What Do Corporate Social Responsibility Ratings Really Capture?. The Academy of Management Perspectives, amp-2012.

– Delmas, M., Etzion, D., & Nairn-Birch, N. (2014). Temporal Dynamics of Environmental and Financial Performance: The Case of Greenhouse Gas Emissions. Draft

What do EP ratings actually measure?

• Data on 475 companies produced by three widely used ratings agencies from 2004-2007

9

Ratings Variable Name Description

Trucost Total Damage Cost Total environmental damage cost (mUSD)

KLD AnalyticsConcerns Total Total Environmental Concerns

Strengths Total Total Environmental Strengths

Sustainable Asset Management (SAM)

Eco-efficiency Environmental Performance (Eco-Efficiency)

Reporting Environmental Reporting

10

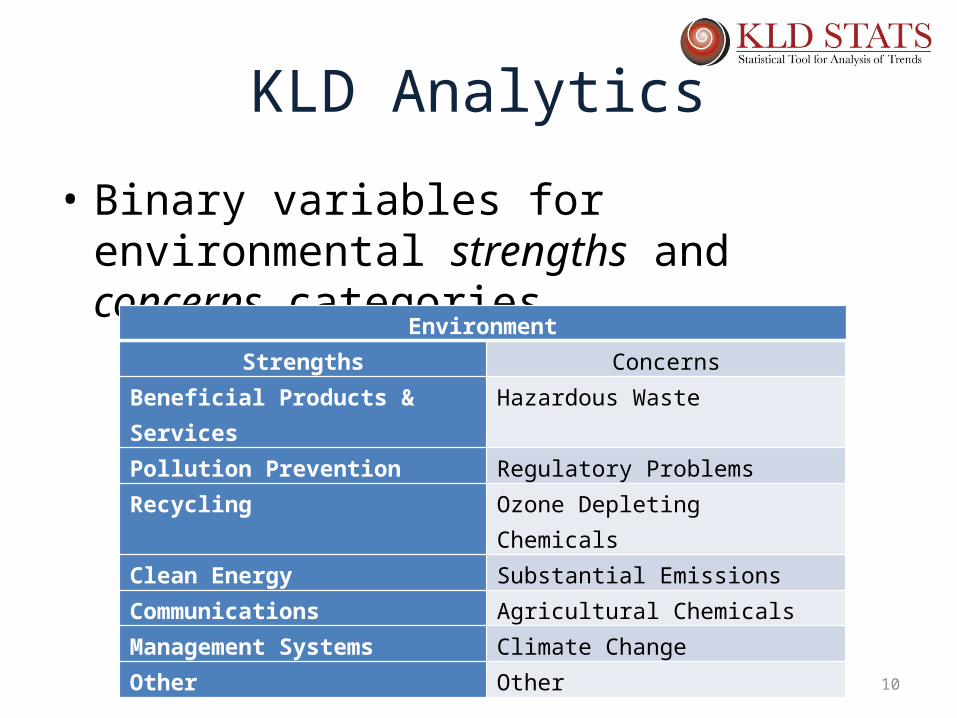

KLD Analytics

• Binary variables for environmental strengths and concerns categories

EnvironmentStrengths Concerns

Beneficial Products & Services Hazardous WastePollution Prevention Regulatory ProblemsRecycling Ozone Depleting ChemicalsClean Energy Substantial EmissionsCommunications Agricultural ChemicalsManagement Systems Climate ChangeOther Other

11

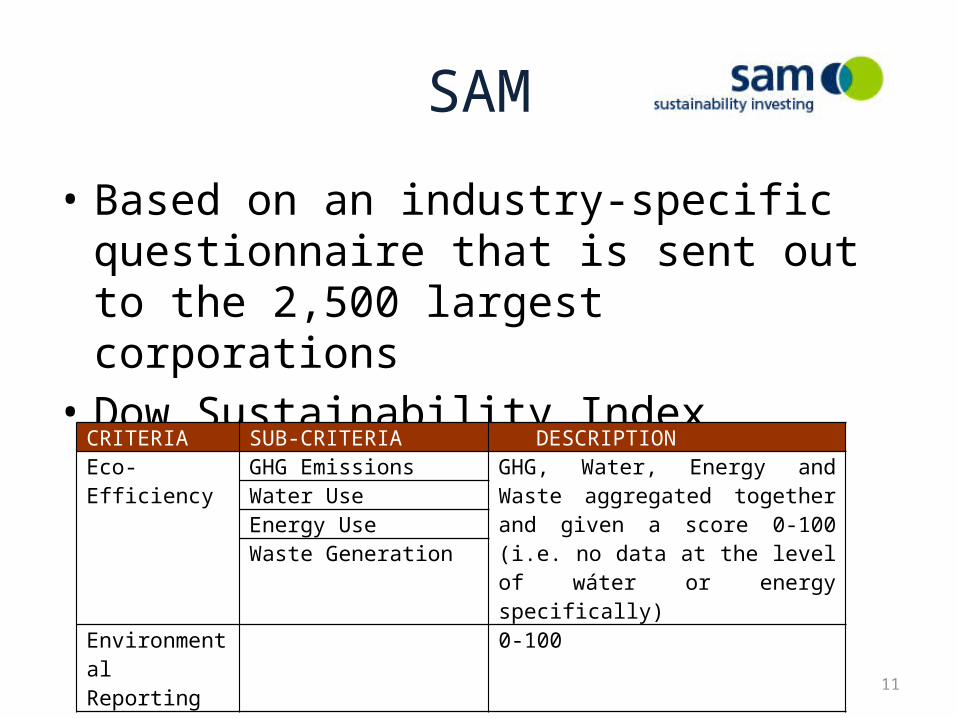

SAM

• Based on an industry-specific questionnaire that is sent out to the 2,500 largest corporations

• Dow Sustainability Index

CRITERIA SUB-CRITERIA DESCRIPTIONEco-Efficiency GHG Emissions GHG, Water, Energy and Waste

aggregated together and given a score 0-100 (i.e. no data at the level of wáter or energy specifically)

Water UseEnergy UseWaste Generation

Environmental Reporting

0-100

12

Natural capital metrics carbon and other Greenhouse Gas (GHG) emissions, water use, resource dependency, air/land/water pollutants, waste.Financial: externality valuation ($), impact ratio (proxy for potential contingent resource liability), profit at risk.

13

CorrelationsData Source

Variable Trucost

KLD SAM SAM KLD

Trucost 1 Total Damage 1.00

KLD 2 Total Concerns 0.61 1.00

SAM 3 Eco-efficiency 0.35 0.46 1.00

SAM 4 Reporting 0.32 0.44 0.76 1.00

KLD 5 Total Strengths 0.23 0.38 0.66 0.58 1.00

14

Principal Component Analysis

• Reduce the dimensionality of a data set• Convert a set of observations of possibly correlated variables

into a set of values of linearly uncorrelated variables called principal components

Data Source Environmental Performance Variable

Component (rotated)

1 2

SAM Eco-efficiency 0.87 0.26SAM Reporting 0.85 0.24KLD Strengths Total 0.85 0.11KLD Concerns Total 0.11 0.92Trucost Total Damage 0.32 0.83

Eigenvalue 2.32 1.66Variation Explained 46.34% 33.17%Cumulative Variation Explained

46.34% 79.50%

15

Two components?

Processes

Outcomes

Envi

ronm

enta

l Rati

ngs

Principal Components80% of original data

Energy and Water UsageGHG emissions

SAM Eco-efficiency

Environmental Reporting SAM Reporting

Beneficial Products & Services, Pollution Prevention, Recycling, Clean Energy, Communication, Mgt Systems

KLD Strengths

Hazardous Waste, Regulatory Problems, Substantial Emissions, Climate Change

KLD Concerns

Total damage to the environment associated with firm activity

Trucost Total Damage

16

What does the market respond to?Variables Tobin’s q

1 2PC environmental processes

0.116

(0.005)**PC environmental outcomes

0.030

(0.568)Trucost Total Damage 0.000 (0.408) KLD Total Concerns -0.051 (0.273) SAM Eco-efficiency 0.004 (0.018)* SAM Reporting 0.002 (0.240) KLD Total Strengths -0.030 (0.518) Leverage -0.042 -0.042 (0.000)** (0.000)**Growth 0.036 0.041 (0.230) (0.162)Capital Intensity 0.090 0.088 (0.043)* (0.050)*Firm Size -0.174 -0.168 (0.000)** (0.000)**Observations 741 741Number of groups 385 385

Market values better environmental processes, but is not concerned with outcomes

Only one of original ratings variables affects financial performance…too much information?

17

Implications

• Process measures may be more easily communicated and assessed – Preferred to outcome performance measures that are

harder to attain, evaluate and rank. – Consistent with Rennekamp (2012): More readable

disclosures lead to stronger reactions from small investors• Performance or output measures might be outdated

– Ex Toxic Releases (2012 releases just out)• If process measures are more abundant and can be

easily fed into ratings methodologies, they will influence market valuation

18

Issue with Disclosure

• Companies may excel at reporting, governance and the utilization of environmental performance systems, yet they may still emit substantial amounts of pollution.

19

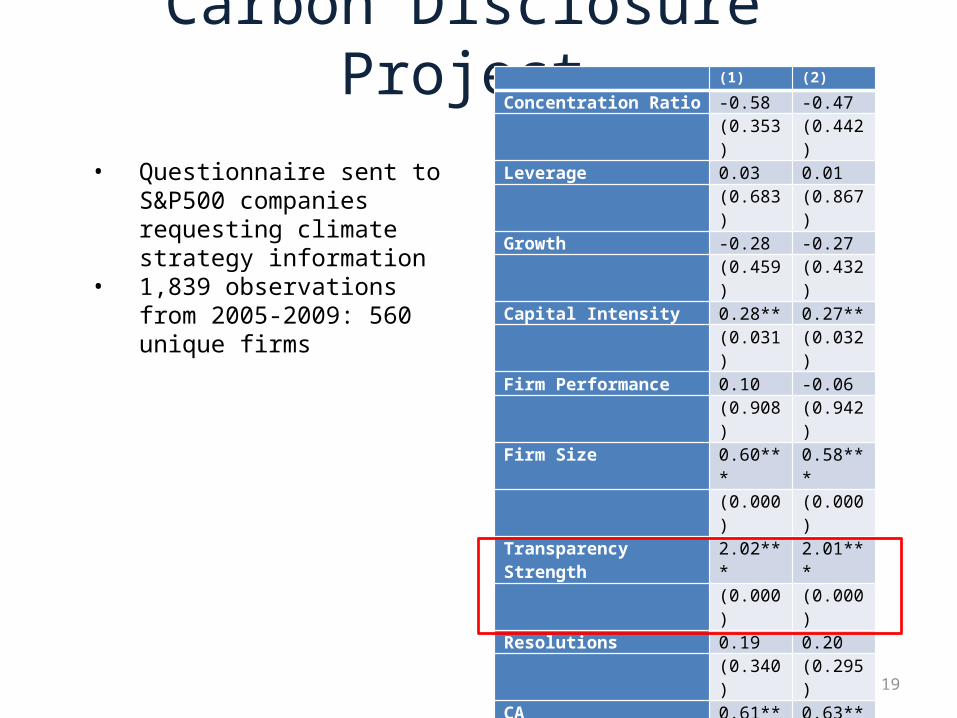

Carbon Disclosure Project (1) (2)

Concentration Ratio -0.58 -0.47 (0.353) (0.442)Leverage 0.03 0.01 (0.683) (0.867)Growth -0.28 -0.27 (0.459) (0.432)Capital Intensity 0.28** 0.27** (0.031) (0.032)Firm Performance 0.10 -0.06 (0.908) (0.942)Firm Size 0.60*** 0.58*** (0.000) (0.000)Transparency Strength 2.02*** 2.01*** (0.000) (0.000)Resolutions 0.19 0.20 (0.340) (0.295)CA 0.61** 0.63** (0.049) (0.043)RGGI -0.01 0.00 (0.962) (0.996)RPS 0.01 -0.03 (0.958) (0.891)GHG Emissions -0.01 0.07 (0.863) (0.304)GHG Emissions2 0.03**

(0.029)

Observations 1839 1839

Firms 549 549McFadden’s R=squared 0.2367 0.2334

Log-likelihood -974.4 -978.6

• Questionnaire sent to S&P500 companies requesting climate strategy information

• 1,839 observations from 2005-2009: 560 unique firms

20

Disclosure vs. GHG Emission

4 6 8 10 12 14 16 18

-0.5

0.0

0.5

1.0

1.5

GHG Emissions (log)

Od

ds

Ra

tio (

log

)

Likelihood of disclosing increases as a firm approaches either end of the environmental performance spectrum.

21

Correlation between KLD Strenghts and KLD concerns:0.413**

22

Investor decision making process

• We need a better understanding of what information is used by investors– For example, would investors favor more accessible,

standardized information on CSR? • Surveys

– Berry and Junkus (2012) 5,000 Individual investors, demographics of investors

– Cohen et al., (2011) 750 retail investors,• Lower use of CSR variables as compared to economic and

governance information• Venue most preferred for investors: third parties and financial

professionals and advisors

23

SRI & Behavior

• Further research should study in more details investors’ responses to different types of CSR data: format, framing and salience– How is the information provided?– What is the source of the information?– How often is it updated?

• Experiments & simulations?– Elliott et al (2014)

24

SRI and Time• Trade-off between social benefits of a healthy environment and private

cost to business: devoting resources to environmental management detracts from profit maximization (Friedman, 1970)

• Firms can generate competitive advantage through proactive environmental strategies (Porter and Van der Linde, 1995; Reinhardt, 1999)– Ability to innovate, market opportunities– Unexploited inefficiencies– Risk mitigation

• The financial effects of firm environmental behavior may be time dependent, thus resolving the conundrum of whether it does or does not pay to be green.

Short-term Long-term

Financial Performance

(ROA) (Tobin’s q)

Reduction of GHG

- +

No cost on carbon emissionsNo hidden efficiency gains

Market anticipates regulationsHigh performing firms are better positioned to minimize future regulatory scrutiny and compliance costs

Data 900 firms -2004-2008

• Environmental performance- Trucost• Total GHG Emissions, Direct GHG Emissions, Supply Chain

GHG Emissions, Water Abstraction, General Waste, Heavy Metals, Natural Resources

• Environmental practices – KLD• Environmental strengths, environmental concerns

• Financials- Compustat• ROA, Tobin’s Q, Log of annual change in sales ratio, Log of total

debt divided by total assets, Log of capital expenditures divided by total sales, Log of total assets

• Tobin’s q– Firm’s market value/ replacement cost of assets (Chung

and Pruitt (1994)).

27

ROA(t+1) Tobin’s q (t+1)

Total GHG Emissions 0.019(0.009)*

-0.750 (0.107)**

Water Abstraction -0.001

(0.001)-0.007 (0.011)

General Waste 0.001 (0.002)

-0.007 (0.041)

VOCs 0.001 (0.001)

0.017 (0.017)

Heavy Metals -0.001 (0.002)

-0.019 (0.033)

Natural Resources 0.001 (0.001)

0.026 (0.016)

KLD Concerns 0.002 (0.003)

0.091 (0.055)

KLD Strengths 0.001 (0.003)

-0.098 (0.049)*

Disclosure 0.001 (0.005)

-0.060 (0.082)

Growth 0.007 (0.002)**

0.045 (0.022)*

Leverage -0.001 (0.001)

-0.010 (0.009)

Capital Intensity 0.000 (0.002)

-0.089 (0.059)

Firm Size -0.047 (0.005)**

-0.568 (0.086)**

n 3316 2678Number of firms 1095 880

28

Implications

• Relationship between environmental and financial performance varies between short- and long-term horizons

• We show the importance of contrasting different measures of performance

• Our results suggest that managers adopting a short-term perspective will eschew proactive strategies in favor of less risky and more immediately profitable investments.

• On the other hand a forward-looking manager who anticipates a shift toward conditions more amenable to proactive environmental behavior will gain competitive advantage over a longer time horizon by developing the necessary resource base and capabilities.

29

Towards a behavioral research approach

• It is important to examine the different ways in which managers as well as investors conceptualize economic value and thereby, indirectly, sustainability and corporate social responsibility.

• Field experiments and simulations to better understand investors’ behavior

• Response to non financial information:– Format, framing and salience– System of investors’ evaluation: rewards and promotion– Demographics (education background, gender etc…)

30

Thank you