Embed Size (px)

Citation preview

CURRENCY BOARD IN THE BALKANS

THE POLITICAL ECONOMY OF CURRENCY BOARDS IN THE BALKANS

by Mervyn K Lewis* and Zeljko Sevic**

Introduction

Currency boards are often seen as a way of putting monetary policy on autopilot,divorcing monetary affairs from politics. For example, Walters and Hanke (1992):

Although the currency board system did not have all the virtues or faults which wereattributed to it, it did have some singular advantages. To some extent it depoliticisedthe monetary system and insulated the public purse from plundering politicians.There was no resort to the printing press to reward political allies or ruin one’sopponents. It gave a real credibility to the fixed exchange rate so that peoplewillingly held both currency and deposits knowing that they would maintain theirvalue. Similarly, it precluded the possibility that the exchange rate would be used toattempt to solve political and social problems. These constraints, once thought to bevices, are now widely regarded as virtues (p. 561).

In fact, currency boards are by nature highly political. Their introduction involves amarked change to the status quo, and they usually need to be enacted and put in place bymeans of a change in laws, which requires the consent of parliament or an equivalentbody or caucus. Since any institution, no matter how bound it is by a set of rules, isadministered by people, it can also be changed by people acting through the samecaucus to amend or revoke the law. For these reasons, any hankering after a ‘non-political’ mode of monetary policy is hopelessly naïve: adopting any monetary reformis a political act; so is continued adherence, in the face of alternatives, to the rules of thesystem introduced.

The Balkans have been, in recent times, partial to currency boards. A currencyboards option was proposed to transitional economies as early as 1990, with the worksof Hanke and Schuler (1991), when the former was an adviser to the Yugoslav FederalDeputy Prime Minister Zivko Pregl (representing Slovenia on the Federal ExecutiveCouncil). The former Yugoslavia did not consider this proposal, not realising that sucharrangements would come to dominate the area some ten years later. Currently,currency board-type monetary systems operate in Bosnia and Herzegovina and

MOCT-MOST 3-4: 285-310, 2000.© 2001 Kluwer Academic Publishers. Printed in The Netherlands.

* National Australia Bank Professor in the School of International Business at the University ofSouth Australia, Adelaide** Principal Lecturer in Accounting and Finance and the Head of the Accounting and FinanceSubject Group at the University of Greenwich Business School; First Vice-President and CEO ofthe Balkan Center for Public Policy and Related Studies

Bulgaria, while Montenegro (still a republic in the Federal Republic of Yugoslavia) andKosovo (a UN protectorate) introduced currency boards as a step to achieving fulleconomic independence.

This paper will demonstrate that the currency board arrangements (CBAs) differamongst themselves, and that there are many differences in perceptions of theirduration. It follows that we need to consider the political economy of why currencyboards are adopted, and also why countries leave them, for the reality is that countrieswhich opt for a currency board system invariably do exit, often with good results. Theseare matters we now consider before going on to examine the situation in particularcountries and the political and institutional arrangements necessary for the successfuloperation of a currency board in Balkan countries/territories.

1. The Currency Board Option

Currency boards are not for all, and only a few countries choose to operate them. In1960, 38 countries had a CBA. Now, there are CBAs operating in 9 countries (and 11, ifwe include Montenegro and Kosovo) with recent entrants in the 1990s, Bosnia,Bulgaria, Estonia, Lithuania and Argentina, joining Djibouti (1949), Brunei (1967),East Caribbean (1968) and Hong Kong SAR (1986). Table 1 gives details of the systemsin the nine countries.

Those economies attracted to the arrangement can be grouped into three categories:small open economies with limited expertise of central banking and possessing nascentfinancial markets; countries that wish to ally themselves with a broader trade orcurrency area; and countries seeking to enhance the credibility of disinflationarypolicies by means of external stabilisation. Although the three categories are notmutually exclusive, most of the recent adherents fall into the third grouping, whereasthe ex-colonies, which previously made up the membership, were of the other types.

Some of the recent participants have resorted to currency board arrangements whenother methods of controlling inflation have failed; others have learnt from theirexperience and gone straight to the currency board option. In all cases the results arestriking: the currency board has served to bring inflation speedily under control. InBulgaria’s case, inflation fell from 2,040 per cent per annum in the first quarter of 1997to 1.0 per cent per annum in 1998.

This success is associated with the decision to switch from internal stabilisation toexternal stabilisation. Whatever the system, every country is ultimately responsible forits own inflation performance; the issue is how this is to be done, and in particularwhether to do so by means of internal or external stabilisation. Internal stabilisationinvolves using domestic monetary policy to keep the purchasing power of a country’smoney reasonably stable in terms of goods and services on domestic markets. Such apolicy will usually require disconnecting domestic prices from external developments,equilibrating the balance of payments directly by flexible exchange rates. Freeingmonetary policy in this way from external flows makes each country’s inflation ratedepend essentially on its own national policy settings.

By contrast, external stabilisation involves fixing the value of money in terms of

286 Moct-Most, Nos. 3-4, 2000

Mervyn K

Lew

is and Zeljko Sevic T

he Political Econom

y of Currency B

oards in the Balkans

287Table 1 - FEATURES OF EXISTING CURRENCY BOARDS1

Economy Year Reserve Reserve Assets Minimum Cover Actual Cover2 Deposits in Foreign

began Currency Currency2

Argentina 1991 U.S. dollar 2/3 foreign assets and gold; 1/3 Argentina’s 100% of base money 139% of base money 53%

government bonds denominated in U.S.$ 27% of M2

Brunei- 1967 Singepore Liquid foreign assets and securities 70% of the central bank’s About 80% of the n.a.

Darussalem dollar current liabilities central bank’s demand

liabilities

Bosnia 1997 DM/euro DM assets, except for 1/2 of the central 100% of the central bank’s 100% of base money 86%

bank’s capital monetary liabilities 66% of M2

Bulgaria 1997 euro Foreign assets and gold 100% of base money plus 105% of base money 56%

some excess coverage 84% of M2

Djibouti 1949 U.S. dollar Foreign assets 100% of circulating 125% of base money n.a.

currency 22,5% OF M2

Estonia 1992 DM/euro Foreign assets and gold 100% of base money, 145% of base money 41%

excluding the central 41% of M2

bank’s certificates

Hong Kong, 1983 U.S. dollar Foreign assets 105% of currency 109% of base money 44%

China 7% of M2

Lithuania 1994 U.S. dollar Foreign assets and gold 100% of base money and 105% of base money 61%

the central bank’s 63% of M2

liquid liabilities

ECCB3 1968 U.S. dollar Foreign assets and gold 60% of base money 82-99% of base money n.a.

12-20% of deposits

Notes: 1 Excluding Bermuda (since 1915), Cayman Islands (since 1972), Falkland Islands (since 1899), Faroe Islands (since 1940), Gibraltar (since 1972).2 For 1998.3 Eastern Carribean Central Bank: comprising Antigua and Barbuda, Dominica, Grenada, St Kitts and Nevis, St. Lucia, St Vincent and the Grenadians.

Sources: Ghosh, Gulde and Wolf (1998, Kopcke (1999).

foreign money (or some other external object); there is a direct link between themacroeconomic behaviour of the domestic economy and that of the country to which itis tied which precludes the taking of independent, national policies for internalstabilisation of prices. By opting for external stabilisation, a country forgoes itsmonetary autonomy and effectively delegates to the major country the responsibility forits inflation performance. Monetary policy is in essence ‘outsourced’, in the descriptionof Dornbusch and Giavazzi (1999).

There are three ways in which external stabilisation can be achieved. One is byallowing the other currency to circulate and replace the local currency (either de jure asin Panama or de facto as occurs under ‘dollarisation’). Declaring a fixed exchange ratepeg, and following through with the policy measures needed to sustain the fixed link, isanother. A CBA constitutes the third way. All three have different implications formonetary independence and the nature of monetary policy. The first obviously removesany potential for domestic monetary policy. The second requires active use of domesticmonetary policy, but the policy actions must be directed to the overriding goal ofmaintaining the exchange rate peg. With a currency board, monetary policy is put intoautomatic mode.

A currency board1 is often defined as an arrangement which fixes the exchange rateof the currency board country to that of an anchor currency. That in fact is not quite thecase. Strictly speaking, the currency board does not peg the exchange rate but insteaddetermines and maintains the parity at which notes (and coins) issued by it exchange forthe currency of the reserve currency country. The fixed exchange rate follows from, andis a consequence of, this arrangement.

In its purest form, a currency board is an institution which issues currency fully (i.e.at least 100 per cent) backed by the reserves of foreign assets – there is no fiduciaryissue – and which stands ready to redeem the domestic currency on demand at a fixedprice in terms of the foreign currency (or currencies). Its sole purpose is to issue or buyback currency as and when the public demand it. The board’s staff thus undertake twofunctions: exchanging notes and coins for the reserve currency, and investing its assetsin high-grade securities denominated in the reserve currency.

Although in principle the currency board is required to convert on demand all offersto it of domestic or reserve currency, most of the foreign exchange business is normallycarried out by the banks which operate much as they would do in the absence of theboard. The result is that the currency board can effectively confine itself to acceptingand paying the reserve currency by cheque or electronic transfer, leaving the job ofsupplying reserve currency to the commercial banks.

However, the currency board does not back bank deposits. The guarantee ofautomatic convertibility and the 100 per cent reserve-currency backing condition doesnot extend to bank deposits or other financial assets. In order to shift wealth from localcurrency bank deposits into the foreign reserve currency, via the currency board, the

288 Moct-Most, Nos. 3-4, 2000

1 In addition to the references cited in the text of this paper, other recent studies of currencyboard systems include Bennett (1994), Humpage and McIntyre (1995), Pautola and Backé(1998), Enoch and Gulde (1998) and Gulde (1999).

individual must initially convert the bank deposit into domestic currency and thenpresent the local currency to the currency board for conversion into the foreigncurrency. In practice, most entities will simply convert their bank deposits directly intoforeign currency, relying in the first place upon banks maintaining the convertibility ofbank deposits into domestic currency and thus the reserve currency, and in the secondplace upon the competitiveness of the inter-bank currency market to ensure that theexchange rates at which bank deposits trade for foreign exchange will be broadly in linewith the rates offered by the currency board.

Nevertheless, even if it is rarely used, the existence of the roundabout conversionroute via the CBA – and confidence in its retention – puts strict limits upon marketexchange rates. Consequently, the exchange rate at which bank deposits trade forforeign exchange will deviate within relatively small arbitration points from thecurrency board’s defined parity.

1.1. Money Creation

With the domestic currency convertible at a fixed price in terms of a reserve currency,the currency-issuing authority has no control over the quantity in circulation which isconsequently determined by the demand to hold it. The board acts as a sort ofwarehouse, storing reserves in the form of foreign currency securities and issuing notesand coins in their place. It is the central bank of the reserve-currency country thatdetermines the supply of reserves. But it does so for the whole currency area, includingthe currency board country. The only way for the board to acquire new reserves is toobtain currency from the reserve-currency country, which in turn means that residentsin the country must run a balance of payments surplus.

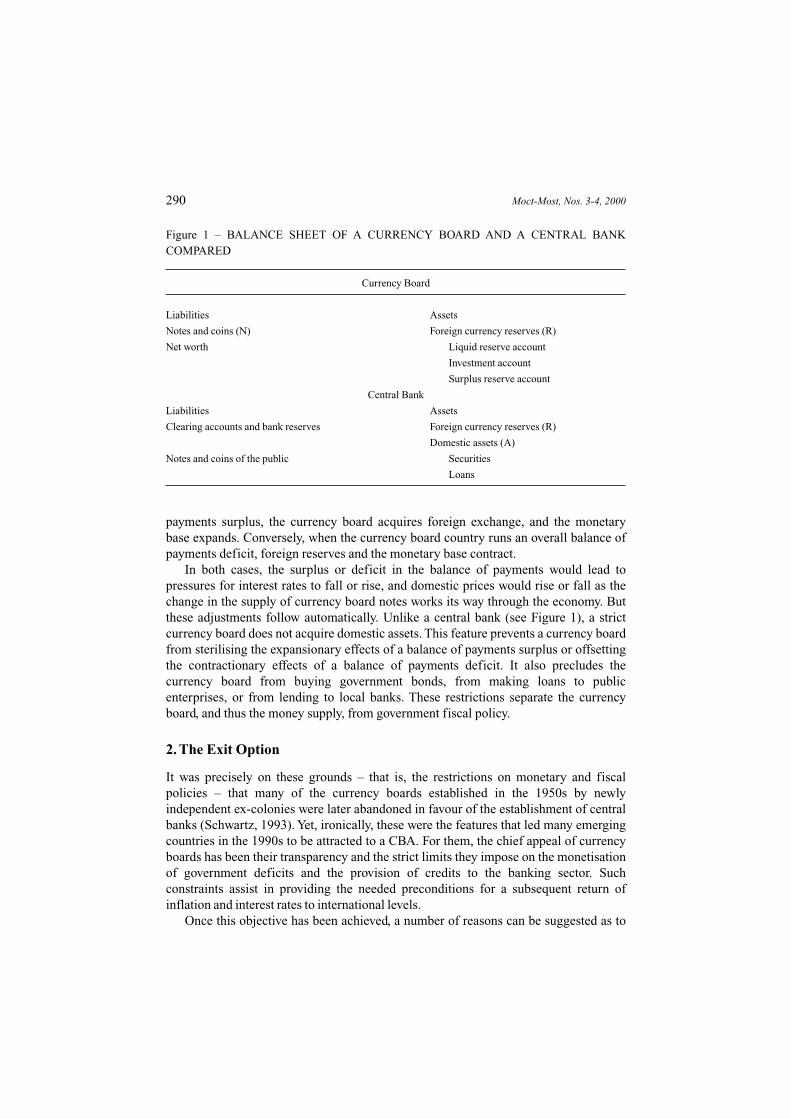

At the simplest, the only source of money creation is from international reserves, inline with the classical specie-flow theory or the monetary theory of the balance ofpayments2. From Figure 1, we can see that the monetary base is synonymous with thebalance sheet of the currency board, comprising currency board notes (N) held by thepublic and the banks, backed by foreign reserves (R). The currency board’s reserveholdings are directly related to the balance of payments via the balance of paymentsidentity

∆R = X – Z + K (1)

where (X – Z) is the current account surplus and K is the net private capital inflow, thesum of which adds to the official acquisition of foreign exchange.

Overall, the monetary base, and to that extent the money supply, moves in line withthe balance of payments position, the degree of proportionality in the latter casedepending upon the constancy of the bank reserve ratio and the public’s currency tobank deposit ratio. When the currency board country runs an overall balance of

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 289

2 For a brief account of these theories, and references to the literature, see Lewis and Mizen(2000).

payments surplus, the currency board acquires foreign exchange, and the monetarybase expands. Conversely, when the currency board country runs an overall balance ofpayments deficit, foreign reserves and the monetary base contract.

In both cases, the surplus or deficit in the balance of payments would lead topressures for interest rates to fall or rise, and domestic prices would rise or fall as thechange in the supply of currency board notes works its way through the economy. Butthese adjustments follow automatically. Unlike a central bank (see Figure 1), a strictcurrency board does not acquire domestic assets. This feature prevents a currency boardfrom sterilising the expansionary effects of a balance of payments surplus or offsettingthe contractionary effects of a balance of payments deficit. It also precludes thecurrency board from buying government bonds, from making loans to publicenterprises, or from lending to local banks. These restrictions separate the currencyboard, and thus the money supply, from government fiscal policy.

2. The Exit Option

It was precisely on these grounds – that is, the restrictions on monetary and fiscalpolicies – that many of the currency boards established in the 1950s by newlyindependent ex-colonies were later abandoned in favour of the establishment of centralbanks (Schwartz, 1993). Yet, ironically, these were the features that led many emergingcountries in the 1990s to be attracted to a CBA. For them, the chief appeal of currencyboards has been their transparency and the strict limits they impose on the monetisationof government deficits and the provision of credits to the banking sector. Suchconstraints assist in providing the needed preconditions for a subsequent return ofinflation and interest rates to international levels.

Once this objective has been achieved, a number of reasons can be suggested as to

290 Moct-Most, Nos. 3-4, 2000

Figure 1 – BALANCE SHEET OF A CURRENCY BOARD AND A CENTRAL BANKCOMPARED

Currency Board

Liabilities Assets

Notes and coins (N) Foreign currency reserves (R)

Net worth Liquid reserve account

Investment account

Surplus reserve account

Central Bank

Liabilities Assets

Clearing accounts and bank reserves Foreign currency reserves (R)

Domestic assets (A)

Notes and coins of the public Securities

Loans

why countries may come to consider that a currency board has outlived its usefulness.One is the sheer lack of flexibility, particularly the inability to deal with monetary andprice disturbances, other than by what Roubini (1998) calls ‘cheating’ i.e. departingfrom the mechanical operation of the currency board by various subterfuges. Then,again, the currency board link itself may be the source of disturbance if it erodescompetitiveness of the local currency. Or, perhaps an exit may be prompted by a beliefthat domestic policies are strong enough to maintain market credibility in their ownright. In order to examine how the balance of costs and benefits of a currency boardarrangement may alter over time, we need to consider in more detail some of thecharacteristics of currency board systems.

2.1. Reserves Cover

Holding 100 per cent backing for the domestic currency represents a resource cost.While reserves can be invested in interest bearing financial assets, some part must bemaintained in liquid form. Generally, 30 –50 per cent of asset backing for notes issuedis in the liquid reserve account, and 50 –70 per cent held in the investment account(Hanke and Schuler, 1992). In addition, many currency boards which specify aminimum of 100 per cent backing of reserve currency maintain reserve cover at morethan 100 per cent in a surplus reserve account. One reason is to allow for fluctuations inthe value of foreign assets such as bonds and marketable securities, another is toprovide confidence in case of financial crisis. The portfolio as a whole presumablyearns less than having the funds invested in capital projects or imported capitalequipment, and this represents an opportunity cost.

One solution is to lower the official reserve backing below 100 per cent, allowingfiduciary issues of domestic currency and introducing what has become known as a‘modified currency board system’ (Hanke and Schuler, 1994). Argentina, for example,allows for a minimum foreign currency reserve of 66 per cent, not 100 per cent aswould be required for an orthodox arrangement. Other countries have grafted boardsonto existing central banks, which have retained some of their old powers, but areconstrained by currency board type rules governing the exchange rate and reservebacking. Such arrangements may erode confidence in the authorities’ commitment tothe system, while removing one of the currency board’s principal features – the inabilityof the monetary authorities to finance a budget deficit by money creation.

Another way of diluting the resource cost occurs when there is the growth ofunbacked, private issues of fiduciary money in the form of bank deposits. If the bankscan function effectively with domestic or foreign currency reserves that are somefraction of their outstanding liabilities, so that the quantity of money is much larger thanthe stocks of international reserves, society gets its monetary services at a lower costwhile individuals benefit from the explicit or implicit interest (services) which bankspay on deposits.

CBAs are often described as modern day equivalents of specie systems, such asthe gold standard (Hanke and Schuler, 1992; IMF 1997; Kopcke, 1999). It was a

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 291

feature of the gold standard that an economising process like that described in theprevious paragraph occurred over time without design, undertaken by banks and otherinstitutions engaging in financial intermediation which involves maturitytransformation and able successfully to issue call liabilities considered as ‘good asgold’. However, one by-product of this expansion, with the pyramiding of anincreasing quantity of debt money on a limited quantity of gold, was the creation ofthe potential for instability in times of crises when the threat of gold conversionsloomed.

Under gold there was usually some leeway for the authorities to come to the aid ofbanks when gold conversions threatened their solvency. Under CBA this support maynot be possible. Currency boards, in their pure form, cannot extend credit to thegovernment, the banking system, or anyone else. This is because a currency board canact as lender of last resort only to the extent that it has, or can draw upon, externalreserves in excess of those needed to back the monetary base. Its capacity to support thecommercial banking system is therefore bound to a degree that a conventional centralbank is not, and this limited ability for the currency board to act as lender of last resortmeans that the banking system must be sufficiently robust so as to function without thebacking of central bank credit extensions. All of this means that the cast iron guaranteeof the convertibility of domestic currency into the reserve currency is obtained at theexpense of endangering the convertibility of commercial bank deposits into domesticnotes and coins.

A further corollary is that more of the burden of adjustment is thrown upon thebanking system and, by implication, the economy as a whole. Establishment of acurrency board may represent an unequivocal commitment by the governmentconcerned, but it is not an entirely convincing one since the law creating the board canalways be reversed. The example of Hong Kong in 1997 makes clear that even the mostimpregnable position can come under attack (Kasa, 1999). The reserves may be thereand in abundance, but will the authorities be willing to put them on the line and defendthe fixed parity at all costs? With the monetary base contracting and an expectation of adevaluation in the offing, interest rates must rise to levels which demonstrate that theauthorities remain committed to the peg. This reliance on interest rates to equilibratefinancial markets forces banks, for their part, to assume a larger share of the burden ofadjustment, either by borrowing reserves from abroad or by contracting their ownbalance sheets in line with the contraction of liquidity. That contraction then shifts theburden onto product and labour markets. Here we have the deflationary spectre whichaccompanies any gold standard type rule. For currency boards to deliver their promiseof credibility and monetary stability, they must be seen as durable commitments. Butfor the peg to be seen as durable, so must the banking system, while wages and pricesneed to be flexible enough to weather any currency market volatility.

Bank collapses have occurred in some currency board countries (Hong Kong in1986, Estonia 1992 and 1994, Argentina and Lithuania in 1995) and, although thesewere handled without abandoning or suspending the operation of the board, in somecases the “rules of the game” were honoured more in the letter than in the spirit of thelaw. In other cases where currency boards have come under speculative attack, unusual

292 Moct-Most, Nos. 3-4, 2000

forms of intervention were required (such as the open market operations by the HongKong authorities in the stock market in 1998 and 1999, and the special discount windowof the Hong Kong Monetary Authority introduced in September 1998).3

2.2. Price Inflation

A currency board can limit the rate of inflation in an economy, but cannot guarantee alow rate of inflation or the absence of significant price movements. The fixing ofexchange rates under external stabilisation is not in itself sufficient for price stability. Itmerely fixes relative price relations between the countries which are pegged and allowsfor only one monetary policy across the linked systems. That policy could beinflationary, and this would be imported by the fixed peg. Yet, marked inflation ratedifferentials can arise even when a country anchors itself to a low inflation country,because of significant differences in productivity growth rates.

The reason is that the tendency to absolute (or relative) price equality applies only totradable goods and services; competition will ensure that there cannot be large andpersistent price discrepancies, at least in the longer run, for goods and services of thesame quality which are readily transportable. When scaled in terms of a commoncurrency, prices for such internationally traded goods tend to be much the same in allcompetitive markets.

But suppose that one country has a high rate of productivity in its internationallytraded goods sector. The country concerned will be able to pay its workers larger wageincreases than elsewhere while remaining competitive on world markets. Most likely,wages growth will not be confined to the traded sector and will flow on to wages in thenon-traded industries (predominantly services). If productivity there is growing moreslowly than in other parts of the economy, prices will increase more rapidly for non-traded than for traded goods and services. This is because the wage increases aresimilar, but productivity growth is different.

In each country the inflation rate is a mixture of inflation in the traded and non-traded sectors. Inflation in traded goods will tend to equality, implying no loss incompetitiveness, but the high productivity country will have more rapid inflation in thenon-traded goods sectors and a higher inflation rate overall. The greater the gap inproductivity, the greater will be the inflation gap between the countries. Japan had ahigher inflation rate than the United States under Bretton Woods. For much the samereasons, despite Hong Kong having tied its currency to the US dollar since 1983 using acurrency board scheme, the rate of inflation in Hong Kong from 1983 to the mid-1990swas, on average, more than double that in the United States.

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 293

3 As no market supply of HK dollars exists outside Hong Kong, speculators wishing to sellHK dollars have to borrow them first, then convert them into foreign currency, forcing interestrates up. In October 1997, following Taiwan’s devaluation, short-selling pushed up rates to 280per cent pa. on settlement day (October 23). Access to the special discount window noweffectively expands HK dollar liquidity beyond the HK dollars in circulation, theoretically up tothe full amount of Hong Kong’s foreign exchange reserves, reducing the extent to which rates willbe pushed up in future crises (East Asia Analytical Unit, 1999).

2.3. Competitiveness

A currency board system imparts considerable stability to the nominal exchange rateexpressed in terms of the reserve currency. But, it does not necessarily stabilise eitherthe real exchange rate or the trade-weighted exchange rate (in nominal or real terms).The former requires sufficient flexibility of wages and prices to bring aboutconformity of inflation rates. The latter requires that the exchange rates of othercountries, which have trade and financial links with the currency board country, movein line with that of the reserve currency. Otherwise, any change in the relationshipbetween those countries’ exchange rates vis-à-vis that of the reserve-currency countrymight alter the currency-board country’s competitiveness relative to that of those othercountries.

Hong Kong after the onset of the Asian currency crisis in 1997 illustrates the point.Following the floating and large depreciation of the Thai baht in July 1997, there werelarge falls in the currencies of Korea, Malaysia, Indonesia and the Philippines.Singapore and Taiwan allowed their currencies to float down. So did the yen. But theHong Kong currency board system held firm. This ‘success’ came at a price. Over theperiod June 1997 to March 1998, the Hong Kong dollar appreciated by nearly 13 percent against the yen and by 12 per cent against its trading partners in nominal terms and14 per cent in real terms. With depreciation blocked by the currency board system,something else had to give in order for Hong Kong to restore its competitiveness. Whatensued was a classic gold standard type deflation of nominal prices across the board –retail prices, wages and asset values – which has continued into 2000.

None of the ‘modified currency board systems’ noted earlier have addresseddirectly the problem of swings in competitiveness, although the choice of the anchorcurrency has generated much soul-searching. As Kopcke (1999) notes, many of thefactors governing the choice of reserve currency are the same as those for ascertainingwhether an optimal currency area exists. One is the degree of diversification of trade.The greater is the diversification, the greater the problem in selecting any particularcurrency, given that fixing to one of the major currencies will imply substantialfluctuations relative to the others. For near European countries the obvious candidatesare the US dollar and the Euro. Foreign exchange market considerations and‘globalisation’ of trade and finance favour the US dollar, whereas actual (or potential)trade links might support a Euro link. The fact that Lithuania opted for the US dollarand Bulgaria for a DEM/Euro peg shows that there is no natural choice, and bothcountries remain exposed to variations in competitiveness resulting from cross-Atlanticexchange rate swings.

Clearly, the longer a currency board is in operation the longer it is exposed to theoccurrence of asymmetric shocks between the two countries while the absence of otheradjustment mechanisms available for ‘metropolitan’ regions such as fiscal transfers andlabour market migration will become more apparent. An inflexible commitment toparity deprives the country of one tool for mitigating the effects of exchange ratemisalignments.

There is an obvious solution to the problem of competitiveness, which borrows from

294 Moct-Most, Nos. 3-4, 2000

the gold standard and Alfred Marshall’s symmetallic standard.4 Although the existingcurrency boards have confined themselves to one currency, in principle a board coulduse two, or a basket of, currencies as a base. Many countries already peg theircurrencies to a trade-weighted basket, and the dual currency board system simplycarries this concept through in a more rigid form. It would imply that reserves wouldneed to be kept in both currencies, but many currency-board countries do so already byholding gold alongside the reserve currency. Some simplicity of operation wouldadmittedly be lost, yet a basket system-especially of two currencies – is not much morecomplex than a system based on a single foreign currency, while a good choice of thebasket would avoid much of the variation in competitiveness that can arise when thecurrency is fixed to one particular currency – witness the case of Hong Kongconsidered above.

A further merit of a dual or basket currency board system may have little to do witheconomics. Linking to a major currency such as the US dollar may simply be politicallyunacceptable to many countries because it smacks of colonial status; certainly, a yen-link would be ruled out in Asian countries once colonised by Japan, even if it makeseconomic sense. By contrast, the basket system may be seen as evidence of greatereconomic sophistication and political independence.

2.4. Other Considerations

Another factor conditioning a country’s willingness to stay with a currency boardsystem is the limited nature of the fiscal discipline under a currency board arrangement.A currency board of the traditional sort is entirely passive; all it does is convert notesand coins either into or out of the reserve currency as the public and the banks demand.It has no other money-creating capacity, and thus cannot finance government deficitsby issuing more money. But budget deficits per se are not prevented, so long as they arefinanced from borrowings and not from money creation (i.e. seigniorage). If fiscaldeficits are the problem, then a currency board goes only part way to solving theproblem. The real solution has to involve reforms to expenditure programmes andtaxation. When this is done, the currency board is to some extent redundant as a device

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 295

4 Towards the end of the nineteenth century, leading economists such as Edgeworth, Fisher,Marshall, Pierson and Walras debated the respective merits of gold and silver as anchors forcommodity-backed money. Marshall (1887) argued that the greatest stability could be achieved ifprices were tied to a basket of gold and silver rather than to fixed amounts of either metal, and thiswas the basis of his proposed alternative of symmetallism. Under symmetallism, the monetaryunit would be defined in terms of gold and silver rather than gold or silver, as under bimetallism.One can imagine, say, one ounce of gold and fifteen ounces of silver combined in one bar.Broadening the base to the two metals would lessen the impact of demand and supply variationsaffecting one metal alone, and thus lead to a less variable price level. In effect, the idea is thatshocks to the relative prices of each metal will cancel each other out to some extent in the impactupon the relative price of the basket as a whole, leading to a more stable price level than wouldresult from either one of the two metals or a bimetallic system.

for fiscal discipline, although it may have provided the initial spur to begin the reformprocess.

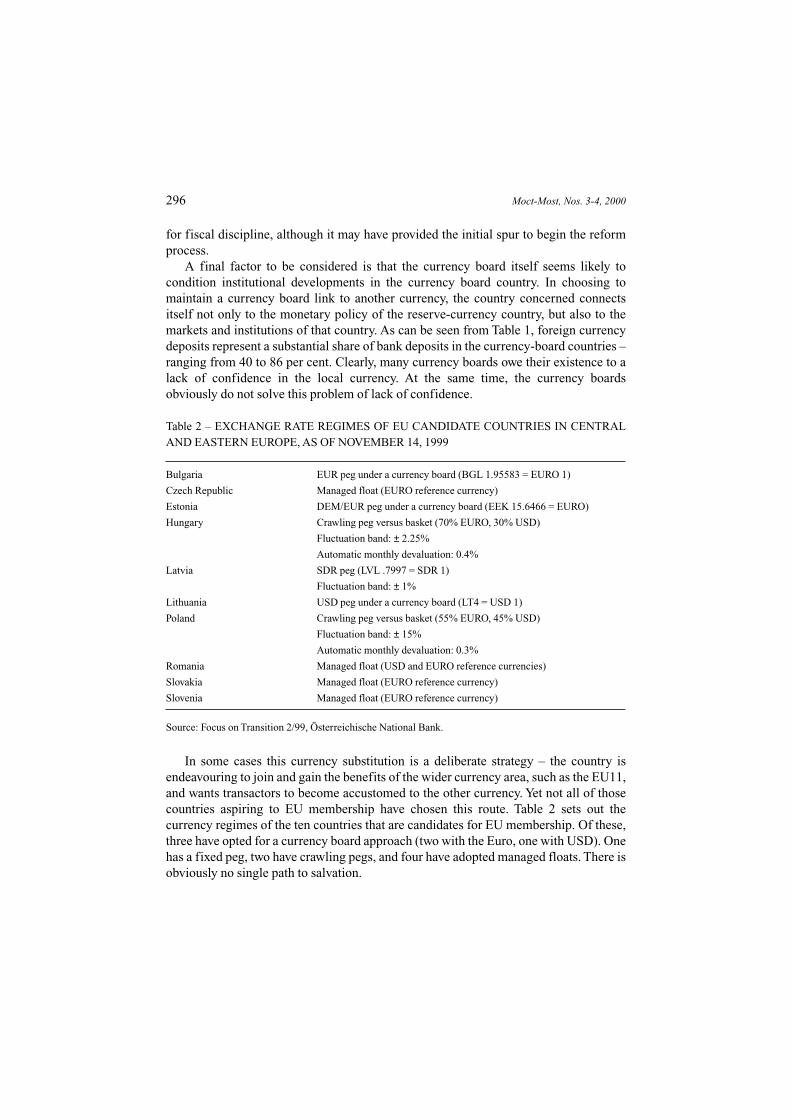

A final factor to be considered is that the currency board itself seems likely tocondition institutional developments in the currency board country. In choosing tomaintain a currency board link to another currency, the country concerned connectsitself not only to the monetary policy of the reserve-currency country, but also to themarkets and institutions of that country. As can be seen from Table 1, foreign currencydeposits represent a substantial share of bank deposits in the currency-board countries –ranging from 40 to 86 per cent. Clearly, many currency boards owe their existence to alack of confidence in the local currency. At the same time, the currency boardsobviously do not solve this problem of lack of confidence.

Table 2 – EXCHANGE RATE REGIMES OF EU CANDIDATE COUNTRIES IN CENTRALAND EASTERN EUROPE, AS OF NOVEMBER 14, 1999

Bulgaria EUR peg under a currency board (BGL 1.95583 = EURO 1)

Czech Republic Managed float (EURO reference currency)

Estonia DEM/EUR peg under a currency board (EEK 15.6466 = EURO)

Hungary Crawling peg versus basket (70% EURO, 30% USD)

Fluctuation band: ± 2.25%

Automatic monthly devaluation: 0.4%

Latvia SDR peg (LVL .7997 = SDR 1)

Fluctuation band: ± 1%

Lithuania USD peg under a currency board (LT4 = USD 1)

Poland Crawling peg versus basket (55% EURO, 45% USD)

Fluctuation band: ± 15%

Automatic monthly devaluation: 0.3%

Romania Managed float (USD and EURO reference currencies)

Slovakia Managed float (EURO reference currency)

Slovenia Managed float (EURO reference currency)

Source: Focus on Transition 2/99, Österreichische National Bank.

In some cases this currency substitution is a deliberate strategy – the country isendeavouring to join and gain the benefits of the wider currency area, such as the EU11,and wants transactors to become accustomed to the other currency. Yet not all of thosecountries aspiring to EU membership have chosen this route. Table 2 sets out thecurrency regimes of the ten countries that are candidates for EU membership. Of these,three have opted for a currency board approach (two with the Euro, one with USD). Onehas a fixed peg, two have crawling pegs, and four have adopted managed floats. There isobviously no single path to salvation.

296 Moct-Most, Nos. 3-4, 2000

3. The Balkans:A Curse of the Supremacy of Politics

3.1. The Nature of Currency Boards in the Balkans

If currency boards are both out of crisis this genesis applies to the Balkans where crisishas been the rule rather than the exception. This commonality is an obvious point ofdeparture. In all four countries and territories where currency boards have recently beenintroduced, this action followed a profound and serious financial crisis. In Bulgaria theCBA was introduced in 1997, in response to serious economic failure of the previoussocialist government. The first free general elections in Bulgaria were won by right-wing political parties, but they failed to deliver a ‘better life’, and on at the nextelections reformed communists, calling themselves socialist, took power but did littlebetter. In July 1997 the next Bulgarian (right-wing) government introduced a CBA inorder to strengthen discipline and stop the fall in GDP and economic devastation of thecountry. Bulgarians liked some features of it, such as extending the scope of hardbudget constraint, and its facilitating an opening up of the economy. However, theywere fully aware that the CBA emerged only when trust in traditional institutions failed.The Bulgarian National Bank, despite its de jure independence, was unable to deliverunder both socialist and right wing governments, because the political factor wasstronger than expected. A politically dependent central bank is prone to serve desires ofpoliticians and grant unbacked credits to the government, or finance the governmentthrough inflation (Sevic, 1997).

In this respect a CBA is not a universal monetary system, as it is used generallywhen the public has lost confidence in the central bank and its abilities to use traditionalmonetary instruments in an effective manner. Often countries themselves perceive it asa transitional arrangement, which can lead to the full restoration of central banking, or‘dollarisation’ of a country. Success of the currency board is linked directly withpolitical consensus in the country, and some authors regard CBA as a specific contractbetween the public and the government. In Bulgaria, the currency board was introducedwhen all other attempts to stabilise the currency and the economy failed, so the onlyviable solution was to go with an external stick to monetary anchor and devise aninstitutional framework to support it.

Contrastingly, the CBA in Bosnia and Herzegovina was introduced from abroad byexternal forces, following the conclusion of the Dayton Peace Agreement. The CentralBank was created as a unique federal institution, with equal representations of allnational entities and all major national groups living in Bosnia and Herzegovina.However, it was clearly stipulated that the Bank will work ‘according to the rule knownas a currency board’ (Art. 2/1 Law on the CBBiH), as a safeguard against itspoliticisation. Also, in order to ensure unbiasedness in the first years of operation, theLaw on the Central Bank of Bosnia and Herzegovina stipulated that the first governorwill be appointed by the IMF and will not be a citizen of Bosnia and Herzegovina or anyneighbouring country. The formal structure of the Central Bank is designed to supportcollective work within the bank and ensure full representation of all three ethnicpeoples.

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 297

In the case of Bosnia and Herzegovina financial crisis was not triggered byineffective stabilisation policies like in Bulgaria, but by war and destruction that tookplace from 1992 to 1995. The Currency Board in Bosnia and Herzegovina sustained thestability of the Convertible Mark (Konvertibilna marka, i.e. KM) with strong supportfrom the international community, as even up to this point full industrial production inthe country was not restored, and all non-economic services were still being fullysubsidised by the international donors.

In the case of Montenegro the situation is more complicated. Montenegro is stillpart of the new Yugoslav federation, and formally does not have full monetarysovereignty. However, in practice, the Montenegrin government has undertakenmeasures to promote monetary independence and full ‘dollarisation’ of the country.5 InNovember 1999, the Montenegrin government passed the decree which introduced theGerman mark (DEM) as legal tender in Montenegro, parallel to the Yugoslav dinar. Themonetary board was entrusted with the power to fix exchange rates, and often the boardundervalued the Yugoslav dinar explaining its actions as a normal consequence ofrational expectations and general distrust of the Montenegrin public towards federalinstitutions. Although it may be true (see Sevic and Rabrenovic, 1999), it might also beclaimed that the CBA dispossesses those who receive federal transfers in Yugoslavdinars (YUDIN), such as all federal employees (army, customs, air traffic control, etc.)and retired people who receive federal pensions.

At present, the currency board operates independently of the National Bank ofYugoslavia in Montenegro, although the most prominent members of the board weremostly senior officials of the National Bank of Yugoslavia in Belgrade. But, theMontenegrin currency board’s role is very specific, as it is not empowered to issue notesand just provides financial stability in the country. The reasons why the board exists isthat both currencies are in circulation in Montenegro and the board must decide on theofficial exchange rate between YUDIN and DEM in the territories of Montenegro.From a purely theoretical point of view, although Montenegro formally has a CBA inplace, in fact it is a semi-officially ‘dollarised’ country, and there is not much need forcurrency board arrangements, except to fix the relative exchange rate on a routine dailybasis.

A similar situation exists in Kosovo. Following the conflict between Yugoslavia andthe NATO alliance in 1999, the UN took over civil administration of the southernSerbian province of Kosovo and Metohiya, with NATO troops providing the security forthe operation. In order to re-launch life in the province, notwithstanding, the UNSecurity Council Resolution 1244(1999), the UNMIK Civil Administrator BernardKouchner has introduced the German Mark as legal tender in the territory of theprovince. While Yugoslav Dinars can be used for some transactions in the province,officially all payments must be made in German marks, and financial documentsdrafted in DEM. Although the UNMIK Economics Department monitors theperformance and monetary mass circulation in the province, a formal currency board

298 Moct-Most, Nos. 3-4, 2000

5 Although we continue to use the term ‘dollarisation’ in the Balkan context “Euroisation”would be more accurate.

does not exist, and the province is in fact fully ‘dollarised’ using the most dominantEuropean currency.

3.2. Why Have Currency Boards in a Balkan Environment?

Only Bosnia and Herzegovina and Bulgaria can be said to be in fact countries that havecurrency board arrangements in place, while Montenegro and Kosovo are in factterritories where full ‘dollarisation’ has occurred. In theory, CBAs and ‘dollarisation’are alternative routes to external stabilisation, but in the Balkan applications they havebecome intertwined. Despite this formal distinction, the main reason for the emergenceof CBAs was the presence of a financial or other social crisis. The currency board wasperceived as an instrument for achieving social stability and an institution to restorepublic confidence in monetary institutions. But, again, a currency board in its pureform cannot and does not conduct any monetary policy; it ensures that all currency incirculation is backed by the chosen hard currency, or low riskless and transaction costfree securities (but not issued by the home government of the country in case).

Can a CBA succeed without preconditions defined by the US Council of EconomicAdvisers as the ‘solid fundamentals of adequate reserves, fiscal discipline and a strongand well-managed financial system, in addition to the rule of law’(Council of EconomicAdvisers, 1999, p. 289)? None of the countries in this case could provide all or even someof these prerequisites, yet they created sustainable currency boards. How did it happen?First, Balkan countries had some foreign exchange reserves to start with, and long on-going inflation (or rather hyperinflation) assisted in devaluing monetary mass in thecountry, allowing low foreign exchange reserves to cover the volume of money incirculation. Second, the Clinton Government administration wanted to see the Bosnianand Bulgarian experiments succeed, and was ready to assist the national governments insecuring initial funding, and support the venture (Hanke, 2000).

Balkan countries are not renowned for fiscal or any other discipline. Tax evasion isrife and over 30 per cent of the economy still lies outside the official financial flows.Cash is still the preferred means of settling payments, despite a payment systeminfrastructure being built in all those countries. It is difficult to assess the extent towhich tax collection has been improved in transition years. Given extensive tax evasion,it is unlikely that the financial institutions will behave much better, and they will try tosecure extra profit on the margins of the financial regulation. Usually, the financialregulations are in place and de jure very strict, but they fall down when it comes toimplementing discipline and there is very little, if anything, that the central bank or anyother financial regulatory body can do to force financial institutions to behave in theprescribed manner. The Balkan countries do not have well-managed financial systemsand it is really very hard to tell when this will change significantly. Building institutionsis not enough, without a culture of compliance.

The rule of law (or its continental European equivalent rechtstaat) is an ideal towhich all these countries aspire, but at the moment the gap between the legal system(set of prescribed rules) and legal order (set of rules together with social behaviourbased upon those rules) is still very large, and it is difficult to say when it will be closed.

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 299

Lawyers usually believe that it may take a generation to alter the situation. Again, thesituation is very different from the one that the Council of Economic Advisers requirefor the successful launch of CBAs.

Despite the lack of usual initial institutional prerequisites, the currency boardexperiment has generally succeeded in the Balkan countries. In the first year ofoperation in Bulgaria inflation fell to around 1 per cent, and GDP turned from anegative to a positive trend, while foreign exchange reserves tripled (Cf. Yotzov, et al1998; Culp, Hanke and Miller, 1999). No currency board failed to deliver financialstability through a fully convertible stable currency (Culp, Hanke and Miller, 1999).Certainly no problems have emerged in the Balkan countries, such as a delay instructural reform and privatisation, overvaluation of national currency at a faster rate ofgrowth in labour productivity and a high volatility of government deposits, althoughthese countries still find it difficult to compete in the world market due to a lowcompetitiveness of export-oriented output.

At the same time, however, financial sector stabilisation has so far failed to produceequivalent results on the real sector of the economy. Despite positive results, the realsector of the economy is still fairly slow to grasp the advantages of a stable economicenvironment. The CBA generally ensures the application of hard budget constraintsacross different sectors, but it seems that it is very difficult to prevent the use of publicfunds to salvage important state-owned enterprises. On the other hand, stable financialconditions put pressure on firms to be efficient in real, not nominal terms. In the past,even poorly performing firms were able to meet the minimum of their tax commitmentsdue to inflationary adjustment. Now, postponing tax payments will not reduce the realvalue of the burden. Consequently, some of the activities and money flows, move toillegal channels. However, enforcement of tax laws is not within the powers of either thecurrency board or the central bank, and there is little they can do to improve thesituation. A shift from legal to illegal channels can seriously affect the ability of thebanks to assess an investment project, as published financial statements will not give atrue and fair view of a company and its operations. In Bosnia and Herzegovina, due tosignificant grant inflow, the amount of credits granted to all sectors of the economy aregrowing, but the same cannot be said of any other country/territory in the Balkanssubscribing to the currency board concept.

The fixed exchange rate in all countries concerned seems not only to ensure stabilitybut also to force companies to become more competitive, as all the countries havecomparatively low labour costs and export mainly labour intensive products. One of theproblems that may appear in the longer run is a negative trend of the Euro, and ipso factoGerman mark, against the dollar. This can be strengthened by large monetary assistanceof US government and non-governmental organisations to the countries in the region. InBulgaria there is an additional psychological factor dating from the old communist years,in terms of the general preference towards the US dollar. Monetary and credit aggregatesstagnated in aggregate terms. Also, the share of domestic assets in broad money generallyis continuously declining and often falls below one-fifth. In a pure CBA, money supply, assuch, depends on real money demand which depicts the state of the financial sector and itsliquidity, via the balance of payments identity, as shown earlier.

300 Moct-Most, Nos. 3-4, 2000

Another problem has come from the inability of the national banks to act as a lenderof last resort. This triggers strong changes in the banking sector and a number of banksgo into liquidation and receivership. In turn, this can undermine the public perceptionof the banking sector and, with falling savings, it can impact adversely upon economicgrowth in the longer term. However, it is possible to reverse these negative trends,through the installation of a deposit protection scheme operated outside the centralbank, or even a state-sponsored private insurance scheme for financial institutions.Despite the overall situation in Bosnia and Herzegovina, it seems that the situation thereis improving and it has been noted that citizens opt to save (if they can afford) indomestic KM, as this has proved to be a stable currency. In other countriesimplementing CBAs, large sums of money are still outside the banking system – acharacteristic true of many other Balkan countries, including even Croatia, whichdemonstrates the best economic results among Balkan transitional economies (Cf.Jovancevic, 2000). The inability of a CBA to grant credits also impinges on banks asthey can grant credits only from their own sources and those sources must be fullybacked by the foreign exchange at their disposal. Therefore, the percentage share of thecredit portfolio in bank assets has shrunk significantly, and its quality is still to beascertained. Obviously, the currency board does not have as part of its agendarestructuring and supporting banking reform. Banks must take care of themselves withregard to their solvency and liquidity. It is the general belief that with globalisation thestability of the countries in which currency boards operate will improve, as theinternational banks will be able to grant credits to their subsidiaries and branches in thecountries in question and they will not have to appear at the discount window andrequire assistance from the central bank. Taking advantage of interest differentials cantrigger some foreign banks to buy domestic currency on the local inter-bank market andinvest abroad, making revenue on a positive margin. But, it should not happen if thecentral bank does its job and a portion of the remaining country risk is still included inthe interest rates charged.

3.3. National Differences

Currency boards may have delivered some stability in the Balkans, but clearly they havehad some modifications as well, departing from a generally prescribed model (Cf.Williamson, 1995; Hanke, Jonung, Schuler, 1993; Hanke and Schuler, 1991; Lewis andMizen, 2000, etc.). Bosnia has gone for a pure currency board under its New Zealandchief. A classical CBA maintains full foreign exchange cover and cannot extend anycredits to the state, state agencies, regional and local governments and their bodies, etc.Usually the currency board can service credits against purchases of special drawingrights from the IMF. This latter instrument can be used as a safeguard if seriousproblems in maintaining monetary stability emerge. However, in Bulgaria the boardsupplies not only notes and coins but also deposits, and has the power to regulate banks,as a third department has been created in the Bulgarian National Bank which deals withbanking supervision. Also, in Bulgaria the currency board earns money on theconversion of DEM into Bulgarian Lev, although those revenues amount up to only 1

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 301

per cent of the total revenues. Bulgaria initially opted for restricted rather than fullcapital account convertibility, being frightened from rapid liberalisation and its adverseaffects that were demonstrated in the past in many Latin-American countries(Williamson, 1995). In contrast to the Bulgarian solution a classical concept of CBArequires full convertibility, of both current and capital accounts.

The Bulgarian National Bank (that operates as the currency board) has by lawdefined its monetary liabilities as consisting of all banknotes and coins in circulationissued by the BNB and any balances on accounts held by other parties with the BNB,with the exception of the accounts held by the IMF. In fact, BNB acts as a fiscal andbanking agent for the state, and supplies deposits which are mainly governmentdeposits and commercial bank reserves. As any currency board is prevented fromengaging in an open market operation (as it cannot conduct any active monetarypolicy), they usually keep compulsory reserves of the commercial bank as an additionalinstrument in securing monetary stability. Thus, the question remains as to how thismeasure of monetary policy of a clearly administrative nature goes hand in hand withstructural changes in the banking sector and strengthening of competition and marketforces in the national banking sector (Cf. Sevic and Sevic, 1998). It can also be claimedthat this departure from the classical CBA in Bulgaria was made as a direct result ofanother diversion, i.e. BNB jurisdiction over banking supervision. Consequently, BNBis also authorised to perform the LLR function in case of any systemic risk to thestability of the banking system. The BNB is authorised to extend credit to solvent banksexperiencing an acute need of liquidity but only against collateral of liquid assets andonly in the event of a liquidity risk affecting the stability of the whole banking system. Itis understood that the BNB will act professionally and will judge each eventual case onproper lending criteria.

In all countries considered the currency board is prevented from engaging in openmarket operations. However, it is very difficult to believe that the central banks(currency boards) would even be able to engage in those operations as the market isfairly thin and few instruments exist. In the case of Bosnia and Herzegovina the CentralBank may even be technically prepared for conducting monetary policy using openmarket operations, similar to those in use in the former Yugoslavia from the mid-1970s(Cf. Sevic , 1996). While in Bosnia open market operations are explicitly forbidden bylaw and no other government agency is authorised to engage in them, in contrast, inBulgaria the Ministry of Finance can engage in very limited activities on the openmarket, but with the assistance of BNB. Namely, BNB places government securities onboth the primary and secondary markets (which is now more common even for somedeveloped western countries). Since the BNB acts purely as an agent of the treasury,there is no effect of its actions on the banks’ credibility and stability of the nationalcurrency. Although from an economic point of view there is no problem, from a legalstandpoint it is not clear as to whether BNB is a disclosed or undisclosed agent, and thisproblem may emerge when the customer is a foreign entity (Cf. Sevic, 1994).

The CBAs in the Balkans have also one typical Balkan characteristic. Namely, theyare allowed to hold only foreign exchange and hard currency, and not securitiesregardless of their level of liquidity and the rating of an issuer. In conflict with this

302 Moct-Most, Nos. 3-4, 2000

provision is the fact that the seigniorage earned will be retained by the currency boarduntil it amounts to 10 per cent (or 5 per cent in the case of Bosnia and Herzegovina) of thecover, and thereafter will become a revenue of the government budget. The currencyboards are also expected to announce interest rates, and to explain the methodology used.In Bulgaria, for instance, the base interest rate is the average yield on three-monthgovernment treasury bills for each auction held by the Fiscal Services Department in theprimary market. In the case of Bosnia and Herzegovina the central bank law did notstipulate how the base interest rate will be formed and made known to the wider public.

In Montenegro the situation is not clear as yet as to what will happen with thecurrency board, following the fall of president Milosevic and the election of Dr VojislavKostunica as a new Yugoslav president determined to reinforce federal agreement andre-negotiate the conditions of the united country. The currency board in Montenegrowas to a large extent engineered by Professor Steve H. Hanke, and was created tosafeguard Montenegro from a highly inflationary policy of the National Bank ofYugoslavia (NBY), the federal central bank. The idea of the introduction of thecurrency board in Montenegro was first put forward in 1998 by Dr Zeljko Bogetic ofthe IMF, who is a Yugoslav national of Montenegrin origin. After his experience withthe Bulgarian currency board, where he was actively involved in the design of thecurrency board, he assumed that a similar solution could save Montenegro fromineffective federal policies. It was not advocated as a framework for the monetarysovereignty of Montenegro.

When the ‘dollarisation’ of Montenegro occurred it was designed to support thedevelopment of the Montenegrin economic structure and prevent discrimination by thefederal government. As the Montenegrin leadership began to distance themselves fromMilosevic, they were embraced by the western governments as reformers and victims ofMilosevic’s oppression. In fact, there was very little difference between the regimes inSerbia and Montenegro. Both rested on a vast police and para-military force, a highlevel of insecurity, corruption and rent-seeking by those close to the leaders and ‘rulingfamily gangs’. However, being at least formally against Milosevic gave credibility andeven more important, financial and technical support to Djukanovic’s regime.Subsequent privatisation scandals and scams support the claims that Djukanovic’sregime was endorsed by the western governments as democratic only because it wasagainst Milosevic. The change of political climate in Serbia, the election of a newfederal president, and overall democratic transition in Serbia will certainly seriouslyaffect Djukanovic’s long-term plans for independence, as now further fracturing of theBalkans could lead to further regional instability, and it is not on the agenda of either theSECI or Stability Pact initiatives.

Technically, the Montenegrin government lead by Mr Filip Vujanovic, a close friendof president Djukanovic, introduced the German mark as official legal tender inMontenegro in November 1999, and pledged itself to operate on the principles of acurrency board. However, as we have already said, this case is really ‘dollarisation’ratherthan a classical CBA. It also relied heavily on western support, especially in maintaininga balanced budget. For instance, almost one third of the budget revenues came fromsubsidies paid by the US (22.83 per cent) and EU (8.17 per cent of the budget). It is clear

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 303

that the Montenegrin government will be totally unable to meet its commitments withoutdirect support from abroad. Very little has been done on structural changes in theeconomy, except many public promises to privatisation (as it is widely believed thatprivatisation will solve all the country’s problems). Montenegro may soon be pushed toresolve its differences with Serbia and strengthen the federation. Following the electionof Dr Kostunica as a new Yugoslav Federal President, some western officials beganreferring to Serbia-Montenegro using the official, constitutional name – the FederalRepublic of Yugoslavia.

Not anticipating these changes in leadership at the federal level, the Montenegringovernment has prepared a draft of the law on a Montenegrin central bank, and it wasexpected that the draft would pass the parliamentary procedure by the end of 2000. Inthe law it is stipulated that Montenegro will introduce the EURO as its nationalcurrency, and that the central bank will provide financial stability. However, the law didnot really visualise the creation of a central bank as such, since the new institution willnot be given the power to issue its own currency. Rather, monetary policy revolvesaround the German mark as the monetary base, as the means of payment and as thecurrency of reserves until EURO cash is introduced and the German mark ceases to belegal tender used in its home country. The central bank would also be responsible for themaintenance of a sound banking sector and an efficient payment system for therepublic. Either those who prepared the law did not have a full understanding of CBAsthat the law in fact promotes, or they deliberately wrote in ambiguities. There isenvisaged the possibility that at a certain point in time the country can depart from thefixed parity and the use of EURO and establish a different currency system, withoutchanging the law. Something like this can be found in the documents establishingLuxembourg’s monetary institute, but the purpose of article 6 of the act was to legallyprepare the institute for the possibility that it will be asked to operate as a central bank,if the fixed parity rule changes. Recently the Institute transmuted into the Bank ofLuxembourg, being a part of the European System of Central Banks.

The draft of law gives the central bank the authority to license, supervise, regulateand liquidate banks and other financial institutions in Montenegro, along with dealersand brokers engaged in foreign exchange. The central bank is empowered to provideshort-term liquidity support to troubled banks, but only if they are fully licensed inMontenegro and under certain conditions. All the loans must be fully collateralised, thecollateral being securities of member states of the European Union. The maturity ofloans or their renewal is one business day and interest on these loans will be at least oneper cent higher that the existing inter-bank rate. The central bank is also expected toprovide an efficient payment system, and be empowered to regulate all the clearinghouses in the country. However, it is not completely clear what will happen to theexisting payment system administration which is, although publicly owned, a relativelyefficient clearing place. It seems that the payment system administration will berequired to compete with other clearing houses, and will initially provide privatepayment services before commercial banks are equipped and trained to performpayment services for their customers. In the current draft of law, the central bankcouncil will have seven members, with up to three being citizens of foreign countries.

304 Moct-Most, Nos. 3-4, 2000

All members will serve a term of six years. However, it is most unlikely that thisprovision will pass parliamentary scrutiny. When the idea of the Montenegrin currencyboard was first mooted, there were proposals to appoint a number of foreigners to theboard, and locate the board formally abroad (in Switzerland). But, in the end the boardwas based in Podgorica, Montenegro’s main city, and not many foreigners have beenthere long enough to influence the board and its work. It is very difficult to say what thefuture will be of the still unborn Montenegrin central bank, but certainly without a‘green light’ from abroad, primarily the US and EU, it is most unlikely that the bank willever be established, although the NBY Chief Office in Podgorica will continue tooperate as a detachment of the National Bank of Yugoslavia, as a federal institution.

The southern Serbian province Kosovo is another area which is officially‘dollarised’. Using the powers invested in him, Mr Kouchner, the SpecialRepresentative of the UN Secretary-General and head of UNMIK, has created de factoan independent economic area in Kosovo. Although de jure Kosovo is still part ofYugoslavia based on the UN Security Council Resolution 1244 (1999), in fact it is moreand more an independent territory. The German mark has been declared a legal tenderin Kosovo, although the Yugoslav dinar is still in circulation and some payments can bemade in YUDIN. However, the foreign exchange rate between the YUDIN and the DEMis very unfavourable, so in fact the YUDIN is being pushed out of circulation. Althoughit is claimed that Kosovo operates a CBA, in fact it is a fully dollarised territory. All thepayments are made in German marks, and all the people’s incomes are in Germanmarks. Only occasionally are some payments made in Yugoslav dinars and mainly in thenorthern part of Kosovo where there is still a noticeable number of Serbs. According toRegulation No. 1999/4 there is a difference between private and compulsory payments.While compulsory payments favour the German mark, in private payments contractualparties can negotiate the currency in which they want their contract executed.

It is very difficult, if not impossible, to assess the results of UNMIK and the CBA inKosovo, as the territory is still economically under-performing and relies heavily on thedirect and reciprocal support from the international community, primarily the US andEU. Bearing in mind that Kosovo was an investment black hole of the formerYugoslavia, it begins from a low base. Even in the Ottoman times tax collection inKosovo was very low, and law and order were never fully established. Kosovo seemsdestined to be an under-performing spot in Europe (after Albania), and it is mostunlikely that any benefits of a stable monetary system will be seen in the near future.Creating a responsible, accountable and interacting society remains the prime objective.

3.4. What are the Next Steps?

The history of CBAs have taught us that the currency boards have, generally been seento be temporary and transitional arrangements. Most of those in the BritishCommonwealth were replaced by central banks. Although CBAs are fashionable again,those countries with a long monetary tradition and history (like Bulgaria where thenational bank was established in 1879) will likely return eventually to their roots, while

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 305

others may choose to keep currency boards as long as the financial discipline is notpresent within the banking and financial system.

Both Bosnian and Bulgarian CBAs were set up with long-term features. Also, thereis currently no political will to change in order to avoid another spiral of hyperinflation.Experiences from other countries with a longer history of CBAs, like Hong Kong,Argentina and Estonia, have shown that the arrangement is able to survive shocks ofdifferent magnitude and nature in the context of an unchanged institutional framework,albeit at considerable short-term cost to the country concerned. Some countries, such asLithuania, have implemented apparently conflicting exit strategies, focusing to peg onthe US dollar and seek membership of the EU – a policy explicable in terms of thecitizens’ preferences for US currency over DEM, which dates back to the former USSRtimes.

If a country decides to exit from the CBA, it usually reverts back to managedexchange rate flexibility and a fully operational central bank in charge of monetarypolicy. Another viable option for CEE countries in the long run is membership in theEuropean Monetary Union. The latter idea is not so novel, as there were many scholarsin the early 1990s arguing, at the time, for the introduction of the ECU in countries ofcentral and eastern Europe. The former option is workable if the new monetary systemgains public confidence and the system can provide the full application of hard budgetconstraint across the country, and classical central banking institutions are restructuredin a way that secures their efficiency and effectiveness. However, the shortcoming ofthis arrangement is that no one knows whether a country is capable of re-creating anactive central banking arrangement until it happens.

The option of joining the EU is theoretically available to all these Balkan countries,although Bulgaria is a step closer to being an associate member of the EU. The law onBNB even stipulated that from 1st January 1999 the currency will be related to theEuro, although it is in fact related to the German mark. Obviously the experience ofoperating under a CBA can be invaluable to a country attempting to join the EU; thecurrency board-like system ensures the stability of macro-economic indicators and alsoallows the country to get used to rules similar to those under which a monetary unionoperates. Indeed, it is always open to these countries to institute full ‘dollarisation’ ofthe economy and acceptance of Euro as the currency, with or without closerinstitutional arrangements with the EU and the European Central Bank. It is mostunlikely that the EU would pass a legal act corresponding to the American InternationalMonetary Stability Act (S. 1879 and H.R. 3493) of November 1999, sponsored bySenator Connie Mack and Representative Paul Ryan, which allows sharing ofseigniorage earned on the notes in circulation in a particular country. Besides possibleloss of seigniorage (stock and flow components), such currency substitution may incursome additional costs not envisaged by the policy-makers in a country adopting aforeign currency as its own. These could include one-off initial costs of introducing theforeign currency, costs of losing the LLR function, flexibility and the loss of flexibilityin monetary policy. However, full dollarisation delivers some substantial benefits, suchas lower transaction costs, lower current and future inflation, and greater transparencyand openness (Cf. Hanke, 2000).

306 Moct-Most, Nos. 3-4, 2000

While both Bosnia and Herzegovina and Bulgaria may consider all optionsregarding the CBA exit option, or the introduction of Euro ‘dollarisation’ on the way toa full membership of the EU, both territories currently applying currency board-likemonetary systems will be required to find another solution. In Montenegro the choiceof a monetary policy option will depend on the future democratisation of Serbia and apolitical decision of western leaders as to whether they want to see Yugoslavia fullydisintegrated or not. Similarly these choices will apply to Kosovo. Kosovo can,theoretically, again be part of democratic Serbia, but the question is whether the westwill be able to control the push for complete independence by the Kosovo Albanianleaders. Otherwise, Kosovar leaders are on course to transforming themselves frombeing close allies of NATO to open enemies if full independence of Kosovo is ruled outby western politicians. Whatever the result, the solution of the Kosovo crisis willrequire huge financial and political commitments by the international community.

4. Conclusion

The introduction of a currency board is a highly sensitive political issue which requiresnational consensus to be resolved effectively. The strict implementation of currencyboard rules usually has as by-products increased social tensions, rising unemploymentin the short and medium-term, dissatisfied unions and, as all instruments of radicalreform, requires serious social costs to be borne by the society (Sevic, 1997). Historyhas taught us that financial crisis and currency boards often go hand-in-hand, since theimplementation of the CBA is usually preceded by a serious financial crisis which turnsinto a complex social crisis, with all spheres of society affected. Even a long history ofcentral banking does not guarantee the effectiveness of a central banking function, as isshown in the case of Bulgaria.

The Bulgarian National Bank is one of the oldest central banks established inEurope in the 19th century and certainly the oldest in the Balkans and the whole CEE.However, it has failed to deliver financial stability and, after many attempts to resolvethe crisis, Bulgaria (under, at the time, a new right-wing government) resorted to a CBAand limitation of BNB functions. The process did not go without conflicts and manyleft-wing parties and trade unions objected, but finally a more or less effective socialdeal was made to give the currency board a shot. The currency board certainly deliveredmore than was expected in Bulgaria, although it operated under very difficultinternational conditions (conflict in the former Yugoslavia, NATO bombing campaignand conflict in Kosovo, UN sanctions against the western neighbour Yugoslavia, etc.),but enjoyed the full support of the Clinton administration (Hanke, 2000), which wasimportant from both financial and psychological viewpoints.

In Bosnia and Herzegovina the currency board arrangement was forced upon thecountry following the Dayton Peace Agreement in 1995. Two years were needed to getthe Bosnian Central Bank in full swing, but it seems that it also has achieved noticeableresults, although there is still clearly a difference in the performance between ethnicareas. Dollarisation in both Montenegro and Kosovo, although introduced more as apolitical measure than an economic one, served the purpose and delivered stability of

Mervyn K Lewis and Zeljko Sevic The Political Economy of Currency Boards in the Balkans 307

the system, and allowed small growth in real wages, although at the expense of risingunemployment. But, it should be noted that both Kosovo and Montenegro, alongsideBosnia and Herzegovina, are fully subsidised by the international community and it isvery difficult to assess the individual influence of the CBA on their overall economicperformance. They will also remain subsidised for years to come.

Currency boards in the Balkans thus proved to be political exercises, mainlyexpensive for the international community, but they delivered the necessary level ofeconomic stability which underpinned necessary institutional building and supportedmoves towards the creation of a responsible and accountable civil society. Thesepolitical by-products of currency boards may prove to be more lasting than theeconomic. But, in the meantime they have also begun delivering economic returns.

References:Avramov, R. (1999), The Role of a Currency Board in Financial Crises: The Case of

Bulgaria, BNB DP/6/1999, Sofia: BNB.Bennett, A.G.G. (1994), Currency Boards: Issues and Experiences, Paper on Policy Analysis

and Assessment, PPAA/94/18, International Monetary Fund, Washington.Bogetic, Z . (1999), ‘Official’or ‘Full’Dollarization: Recent Issues and Experiences, mimeo,

IMF, Washington, D.C.Bogetic, Z. and S. H. Hanke (1999), The Montenegrin Marka, Podgorica: Antena M.Central Bank BiH (1997-1999), Annual Report, various issues.Central Bank BiH, Bulletin, various issues.Council of Economic Advisers (1999), The Annual Report of the Council of Economic

Advisers, USGPO, Washington, D.C.Culp, C.L., S.H. Hanke and M.H. Miller (1999), The Case for an Indonesian Currency

Board, Journal of Applied Corporate Finance, 11(4), pp. 57-65.De Grauwe, P. (1997), The Economics of Monetary Integration, 3rd edition, Oxford

University Press, Oxford.Dobrev D. (1999), The Currency Board in Bulgaria: Design, Peculiarities and Management

of Foreign Exchange Cover, BNB DP/9/1999, Sofia: BNB.Dornbusch, R. and F. Giavazzi (1999), Hard currency and sound credit: a financial agenda

for Central Europe, EIP Papers, 4(2), pp. 25-32.East Asia Analytical Unit (1999), Asia’s Financial Markets. Capitalising on Reform,

Canberra: Department of Foreign Affairs and Trade.Enoch, C. and A-M. Gulde (1998), Are Currency Boards a Cure for All Monetary Problems?

Finance and Development, 35(4), pp. 40-43.Ghosh, A. R., A. M Gulde and H. C. Wolf (1998), Currency Boards: The Ultimate Fix? IMF

Working Paper WP/98/8, Washington.Gros, D., et al. (2000), Notes on the Economy of Montenegro, CEPS, Brussels.Gulde, A-M. (1999), The Role of the Currency Board in Bulgaria’s Stablization, Finance and

Development, 36(3), pp. 36-39.Hanke, S.H. (2000), Some Reflections on Monetary Institutions and Exchange-Rate Regimes,

Testimony before the International Financial Institutions Advisory Commission of the UnitedStates Congress, mimeo, US Congress: Washington, D.C.

Hanke, S.H., L. Jonung and K. Schuler (1993), Russian Currency and Finance A CurrencyBoard Approach to Reform, Routledge, London.

Hanke, S.H. and K. Schuler (1990), Monetarna reforma i razvoj jugoslovenske privrede[Monetary Reform and Development of Yugoslav Economy], Belgrade: Ekonomski institut.

Hanke, S.H. and K. Schuler (1991), Monetary Reform and the Development of a YugoslavMarket Economy, Centre for Research into Communist Economies, London.

308 Moct-Most, Nos. 3-4, 2000

Hanke, S.H. and K. Schuler (1992), Currency Boards for Eastern Europe, Geld and WahrungWorking Papers 23, Johann Wolfgang Goethe – Universität, Frankfurt am Main.

Hanke, S.H. and K. Schuler (1994), Currency Boards for Developing Countries: AHandbook, International Centre for Economic Growth, San Francisco.