Embed Size (px)

Citation preview

Current Outlook on AIFMD for Luxembourg Real Estate Structures

www.pwc.lu/real-estate

Including latest update of ESMA final advice of 16 November 2011

January 2012

The Alternative Investment Fund Managers Directive (‘the AIFMD’ or ‘the Directive’) entered into force on 21 July 2011. Its aim is to provide a harmonised and comprehensive regulatory and supervisory framework within the EU as well as a single EU market for managers of Alternative Investment Funds (AIFs). The ultimate deadline for EU Member States to transpose the Directive into their national law is just 18 months away (22 July 2013). Alternative Investment Fund Managers (AIFMs) existing in July 2013, will have until July 2014 to obtain authorisation from their relevant competent authority. On 16 November 2011, the European Securities and Markets Authority (ESMA) issued final technical advice to the EU Commission on

possible implementing measures (ESMA Final Advice, thereafter) of the AIFMD. Final implementation measures from the EU Commission are expected to be issued by July 2012. With 499 pages, the Final Advice is the first major foray by ESMA into the regulation, outlining its policy thinking in four key areas:

1. General provisions and operating conditions impacting managers;2. General provisions impacting funds;3. Transparency and;4. Depositary requirements.

We have used the Directive and ESMA Final Advice as the basis for summarising the major points of the Directive.

In the following sections, we will highlight the key issues covered by the Directive and ESMA Final Advice with a special focus on the real estate sector. In addition, we will provide a Luxembourg perspective focusing on the practical steps that real estate fund managers will need to take, in order to be ready when the full regulatory framework comes into force.

Luxembourg is the domicile for a number of regulated and unregulated real estate vehicles. The step towards compliance with the AIFMD is less significant than for regulated structures. Unregulated structures have not been subject to any regulatory framework to date and will therefore be significantly impacted by the Directive. The most difficult question is to determine who the AIFM is for these, often complex, structures. The answer to this question first depends on which entity(ies) within the overall structure would meet the definition of an AIF. The Luxembourg unregulated real estate structures are usually

intermediate vehicles established for tax optimisation purposes. There is no specific exemption for Special Purpose Vehicles considered in the Directive. If the structure meets the definition of a holding company, the Directive does not apply. However, many such structures may not strictly meet this definition and, depending on the facts and circumstances, may meet the definition of an AIF (for instance when the structure has more than one investor/shareholder and when it invests in accordance with an investment policy). This potentially means that, in addition to the top level fund/structure, the SPV will also be considered as an AIF. While this situation intuitively does not make sense, neither the Directive nor ESMA’s Final Advice give a clear answer.

In the following analysis, we will focus on the areas impacting regulated real estate vehicles highlighting the gaps that will need to be filled post AIFMD implementation.

2 • PwC

Major areas covered by the AIFMD

Current status of the Directive

Requirements impacting managers cover scope and authorisation, capital requirements, delegation, conduct of business, conflicts of interest, remuneration and risk management. We further discuss a number of these areas which we believe to be most relevant to real estate managers.

Scope and authorisationAll EU fund managers will be affected by the AIFMD – most will be required to fully comply with the Directive by July 2013. Only managers with aggregate Assets under Management (AuM) of less than EUR 100 million leveraged or EUR 500 million unleveraged, under specific conditions, will be subject to a lighter registration and reporting regime.

Luxembourg perspective – Medium impact for regulated structures

The question is who will be the AIFM for the Luxembourg real estate structures considered AIF under the Directive. In Luxembourg, UCI Part II, SIFs and SICARs will be considered to be AIFs. These structures may already have an external manager in the form of Chapter 15 or Chapter 16 Management Company or may be self-managed. When self-managed, the structure itself will be the AIFM. When the management is under the responsibility of a Chapter 15 or 16 Management Company, the AIFM will be that Management Company.

Capital requirementsMany real estate structures will face increased capital requirements under the AIFMD, which establishes a minimum capital requirement of EUR 125,000. In addition, when AuM exceed EUR 250 million, additional capital equal to 0.02% of the amount exceeding EUR 250 million will be required, with the amount capped at EUR 10 million. Structures, which are internally managed, will have a minimum capital requirement of EUR 300,000. Finally, in order to cover potential professional liability risks, the AIFM (external or self managed) will need to have additional own funds or hold a professional indemnity insurance or a combination thereof. Based on ESMA Final Advice, additional funds required will amount to a minimum of 0.01% of AuM (with the possibility to lower the amount

to 0.008% under certain circumstances.)

Luxembourg perspective – Low impact for self-managed regulated structures and Medium to High impact for others

Capital requirements of the Directive are expected to have a limited impact for internally managed Luxembourg real estate AIFs, (self managed Part II UCIs, SIFs and SICARs), as the minimum capital to be reached after 6 to 12 months, for these vehicles, is far above EUR 300,000.For Chapter 15 management companies, additional capital may only be required to cover professional liability risks if a separate insurance is not subscribed.Chapter 16 management companies (with an initial capital of EUR 125,000) will need to increase their capital and establish specific monitoring procedures. To illustrate, a Chapter 16 management company managing AuM of €580 million, would need to double its initial capital from EUR 125,000 to EUR 249,000 (including additional own funds calculated based on 0.01% of AuM to cover professional liability risks).

DelegationUnder the Directive, managers will be able to delegate their functions to third parties under certain conditions. When delegating portfolio management and/or risk management, the delegate will need to be an authorised and supervised asset manager. As per ESMA Final Advice, where such delegate is domiciled outside the EU, the non-EU delegate must be authorised or registered for the purpose of asset management based on local criteria and must be effectively supervised by an independent competent authority. In addition, regulatory cooperation agreements must be in place between the home state of the AIFM and the supervisory authorities of the delegate. One key aspect highlighted in the ESMA Final Advice is the fact that, regardless of the level of delegation, the AIFM cannot become a letter box entity and must retain the necessary expertise and resources to supervise the delegated tasks effectively and manage the risks associated with the delegation as well as retain the power to make decisions in key areas which fall under the responsibility of the senior management.

Current outlook on AIFMD for Luxembourg Real Estate Structures • 3

General provisions and operating conditions impacting managers

4 • PwC

Luxembourg perspective – Limited impact for Part II UCIs /Medium impact for other regulated funds

Current delegation requirements in Luxembourg applicable to management companies of Part II UCIs are to some extent in line with the delegation requirements of the Directive. The draft of the new SIF law introduces delegation requirements also similar to those of the Directive. No such requirement exists for managers of SICARs. The Luxembourg Law for regulated funds will need to be changed. As from 2013, AIFMs will need to make sure that their current delegation schemes are ‘AIFMD compliant’ and that when delegation of significant functions occurs, the necessary level of substance and monitoring is in place. This will most likely require the attribution of additional resources to the operations of the AIFM.

Conflicts of interestThe AIFM will need to implement and maintain effective procedures and controls to identify, prevent, manage and monitor conflicts of interest entailing a material risk of damage to the interests of the AIFs or investors. In addition, conflicts of interest which cannot be prevented will need to be disclosed to investors.

Luxembourg perspective – Medium to High impact for regulated structures

The Directive’s requirements are in line with those of the Law of 17 December 2010 relating to UCIs. In addition, the draft law for SIFs also introduces the need for organisational measures to reduce the risk of conflict of interests. To date, the law for SICARs is silent on this matter. It can also be noted that INREV guidelines already address such measures.

Risk managementThe AIFM will need to establish, implement and maintain an adequate and documented risk management policy adapted to the risk profile of the AIFs managed. The risk management function is to be permanent, functionally and hierarchically separate from operating units including portfolio management. If, based on the principle of proportionality, the function is not functionally and hierarchically separate, additional safeguards (subject to regular review by the governing body) will need to be put in place. As part of the risk management framework, the AIFM will be required to establish and implement quantitative and/or qualitative risk limits for each AIF, taking into account all relevant risks. Moreover, the effectiveness of the function will need to be assessed, monitored and tested (via use of stress tests and back-testing) on a regular basis.

Luxembourg perspective – Medium to High impact for regulated structures

The risk management function as described in the Directive and ESMA Final Advice is aligned to a large

extent to the requirements under the UCITS framework. To date, the non UCITS world has not been subject to such requirements. While, the SIFs draft law introduces the requirement for an appropriate risk management policy, a number of additional changes will need to occur. Specific focus will need to be placed on the requirement for an independent risk management function. This will most likely be challenging for the real estate industry as the risk management and the portfolio management functions have historically worked hand and hand.

Fund structure and marketingAll EU AIFMs will have to be fully compliant with the Directive in 2013 at which point they will have an entrance route into Europe by means of the onshore passport for the distribution to professional investors (as defined in MIFID). For non-EU AIFMs and non-EU funds, from 2013 until at least 2018, existing country private placement regimes will remain available for marketing of fund interests across the EU. The only requirements applicable will be 1) the need for regulatory cooperation agreements between the non-EU jurisdiction involved (AIFM and/or AIF) and the home state of the AIFM (if EU) or each of the member states where the non-EU AIF is distributed and 2) compliance with all transparency provisions. In addition, as from 2015, if confirmed by ESMA, non-EU AIFMs will be able to take advantage of the EU passport regime, provided that they fully comply with the Directive and that regulatory cooperation and tax agreements are in place. Finally, as from 2018, national private placement regimes will most likely be terminated based on advice from the ESMA, at which point non-EU AIFMs will be required to be fully compliant with the Directive.It is important to highlight that distribution to retail investors will remain subject to local rules and marketing requirements.

Luxembourg perspective – Medium impact for EU AIFMs

As noted above, all EU AIFMs will be fully impacted by the Directive. Non-EU AIFs managed by EU AIFMs, however, will not have access to the passport until at the earliest 2015. EU AIFMs may consider re-domiciling their offshore funds to the EU (and in particular to Luxembourg) to benefit from the passport as from 2013. Moreover, while the use of private placement regimes will be available for non-EU AIFs until 2018, in the coming years, certain continental European countries may very well make entry into their jurisdiction more difficult under these regimes. The Directive will force real estate players to analyse alternative business models and assess their strategy including the re-domiciliation of funds and potentially of service providers. It is difficult to predict today what the optimal model will be going forward. Most changes will be driven by investors’ appetite for the EU passport and the evolution of national private placement regimes.

Current outlook on AIFMD for Luxembourg Real Estate Structures • 5

Requirements impacting the funds which are most relevant to the real estate industry are: leverage, liquidity and valuation.

Limitations on leverage

One of the key changes introduced by the Directive is the requirement for the AIFM to set the leverage limits for each of the AIFs it manages and to demonstrate that those limits are reasonable and are being complied with at all times. For AIFs employing significant leverage, the AIFM will need to report information about the overall leverage employed to the competent authorities and to investors on a periodical basis. The reporting to competent authorities will be used for the purpose of identifying the extent to which leverage is contributing to the build up of systemic risk. Competent authorities may impose limits as a means to ensure the stability and integrity of the financial system. In its Final Advice, ESMA requires that leverage be calculated under two separate methods: the Gross Method and the Commitment Method. In calculating leverage, temporary borrowings fully covered by investors’ capital commitments are excluded; as is leverage at the level of the portfolio companies. However, the AIFM will need to look through corporate structures and include leverage to the extent these structures have recourse to the AIF through cross collateralisation or guarantees.

Luxembourg perspective – Low impact for regulated structures

There is concern from the industry with respect to the competent authorities’ ability to impose limits and in particular that such limits would be left at the discretion of each national authority without proper harmonisation across Europe.

Levels of leverage have already been an area of focus for regulators and institutional investors. As such we do not expect this provision to be of a significant impact for the real estate industry.

Valuation

The Directive stipulates that independent valuations are to be carried out for each AIF. For open-ended funds, in its Final Advice, ESMA specifies that the valuation of other assets, such as real estate, has to take place at least once a year, unless there is evidence that the last determined value is no longer fair and/or proper. ESMA acknowledges that performing a valuation at the same frequency as subscriptions and redemptions for such assets would not be feasible.

For closed ended funds, the Directive specifies that the valuation of assets should be performed in case of an increase or decrease of the capital of the AIF. There is no additional guidance in ESMA’s Final Advice. The industry would argue, that in practice, it is understood that the only issue of (or subscription for) units of closed-ended AIFs takes place at the point of acceptance by the AIFM of the commitment by the proposed investor to the fund.

With respect to the independence of the valuer, the Directive provides two options: either the valuation is performed by an independent external valuer or by the AIFM itself only if the valuation function is functionally independent from the portfolio management and conflicts of interest are mitigated.

Luxembourg perspective – Low impact for regulated structures

In Luxembourg, independent valuers are already required by law for Part II UCIs but not for a SIF or SICAR. However, for these vehicles, valuation practices have been an area of focus of the CSSF in recent years. In practice, regulated funds most often involve independent valuers either because it is stipulated in their governing documents or as a best practice. The current practice to use independent valuers for annual valuations should remain adequate given the propositions by ESMA Final Advice.

Liquidity Management

The AIFM will need to implement, for each AIF it manages (except unleveraged closed-ended AIFs), an appropriate liquidity management system , adopt procedures to monitor the liquidity risk of the AIF and make sure that the liquidity profile of the investments of the AIF complies with its underlying obligations.

Luxembourg perspective – Medium impact for regulated structures

Special requirements on liquidity are currently not applicable in Luxembourg for non-UCITS. However, the need for appropriate mechanisms to manage liquidity has been an area of focus of the CSSF in recent years. Formal and documented liquidity procedures and controls will need to be implemented. In practice, mechanisms are well established in the real estate industry for managing liquidity. As such, while this requirement may necessitate some formalisation, it should not have a significant impact on current structures.

General provisions impacting funds

Transparency requirements address required disclosures in the annual report of the AIFs, disclosures to investors before they invest and on a periodical basis and reporting to competent authorities.

In terms of the annual report of the AIF, aside from the increased information expected in the fund’s report of activity, the only noteworthy requirement concerns the disclosure of the remuneration. The annual report will need to include the total remuneration of the AIFM’s staff split into fixed and variable as well as information on remuneration policies and practices for relevant categories of staff.

In terms of the disclosures to investors, the AIFM will have to make full disclosure to investors (before they invest), including a description of the investment strategy and objectives of the AIF, the types of assets which the AIF may invest in, techniques it may employ and procedures to be used to alter the investment strategy. The periodical disclosures will cover information on the use of leverage, liquidity and risk management, trading activity and, for real estate managers, information on portfolio investments.

Side letters are commonly used in real estate funds. Under the AIFMD, disclosure

requirements with respect to these arrangements go beyond current practice guidelines (such as those of INREV).

Finally, extensive qualitative and quantitative disclosures will need to be reported to the AIFM’s home state regulator on an annual, semi annual or quarterly basis depending on the level of AuM. Competent authorities may, if deemed necessary for effective monitoring of systemic risk, request more frequent disclosures as well as additional ad hoc reporting.

Luxembourg perspective – Medium impact for regulated structures

The AIFMD increases the disclosure requirements for investors and the regulator in comparison with current Luxembourg requirements. Additional procedures and processes as well as coordination with service providers will be necessary. On the positive side, ESMA recognises the current accounting standards and policies in its Final Advice. As such, there should be minimal impact on the format and content of the audited financial statements and related disclosures of the AIFs when prepared under Luxembourg GAAP or IFRS.

Transparency

6 • PwC

Current outlook on AIFMD for Luxembourg Real Estate Structures • 7

In the future, real estate fund managers will be required to appoint a single depositary that will be liable to the fund and its investors. For EU funds, the depositary has to be EU domiciled. For non-EU funds it can be a third country depositary subject to the cooperation agreements and other conditions. The AIFMD establishes rules regarding the delegation of safekeeping functions.

Although, generally funds will be required to appoint a depositary which is a credit institution or similar, Member States will be able to permit closed-end real estate funds to appoint law firms, notaries or other authorised investment firms.

The depositary’s responsibility over other assets (such as real estate) is that of safekeeping. The depositary will need to verify ownership and

maintain a record of such assets. These safekeeping duties will apply on a look through basis to underlying assets held by any structure controlled directly or indirectly by the AIF or by the AIFM on behalf of the AIF. Depositaries will need to review their current set up, develop and adapt their systems and procedures, as the requirements of the Directive differ significantly from existing ones.

Luxembourg perspective – Low impact for regulated structures

For many jurisdictions the requirement to have a depositary is new. There is less impact on Luxembourg regulated funds, as this requirement already exists. However, as the Directive significantly redefines the depositary’s roles and responsibilities, existing agreements will need to be redrafted.

Depositary requirements

8 • PwC

Understanding a new regulation and more importantly its impact can be challenging, and especially when there is a lack of detail and clarity. The Directive contains many technical requirements to be implemented by real estate managers, some of which may require significant modifications to their current structures and organisation. We have a multi-disciplinary and multi-industry team (including real estate) of professionals in business strategy, operation and structuring, regulatory compliance, tax, remuneration and assurance services ready to assist you: identify and assess the many impacts of the Directive on your organisation and develop an integrated response to the AIFMD. Our team works closely with the PwC European AIFMD working group to ensure knowledge and best practices are shared on a Pan-European basis. Our experts can:• As a first step, make a diagnosis to understand

how and where the Directive will impact your business and products;

• On completion of this diagnosis, create a map of your overall structural framework focusing on the products (including investor specific issues), on entities (who is in, who is out, and how different entities may be impacted) and

on relationships (both internal and external);• Provide an analysis of impacted areas and

gaps, make recommendations on where, from a human capital, systems and strategic perspectives, you may need to take further actions to ensure compliance moving forward while taking into account the commercial imperatives.

• Finally, if required, bring the necessary support and advice to assist you further with implementing any enhancements to your organisation as well as analysing any tax consequences that may arise.

Integral to this assistance is our deep knowledge of the real estate industry in Luxembourg and Europe and our expertise in the AIFMD. Our team of experts has remained close to each step of the development of the Directive and related implementation measures and has been engaged in on-going dialogues with key stakeholders, including asset managers, service providers, trade associations and regulators.

How we can help you

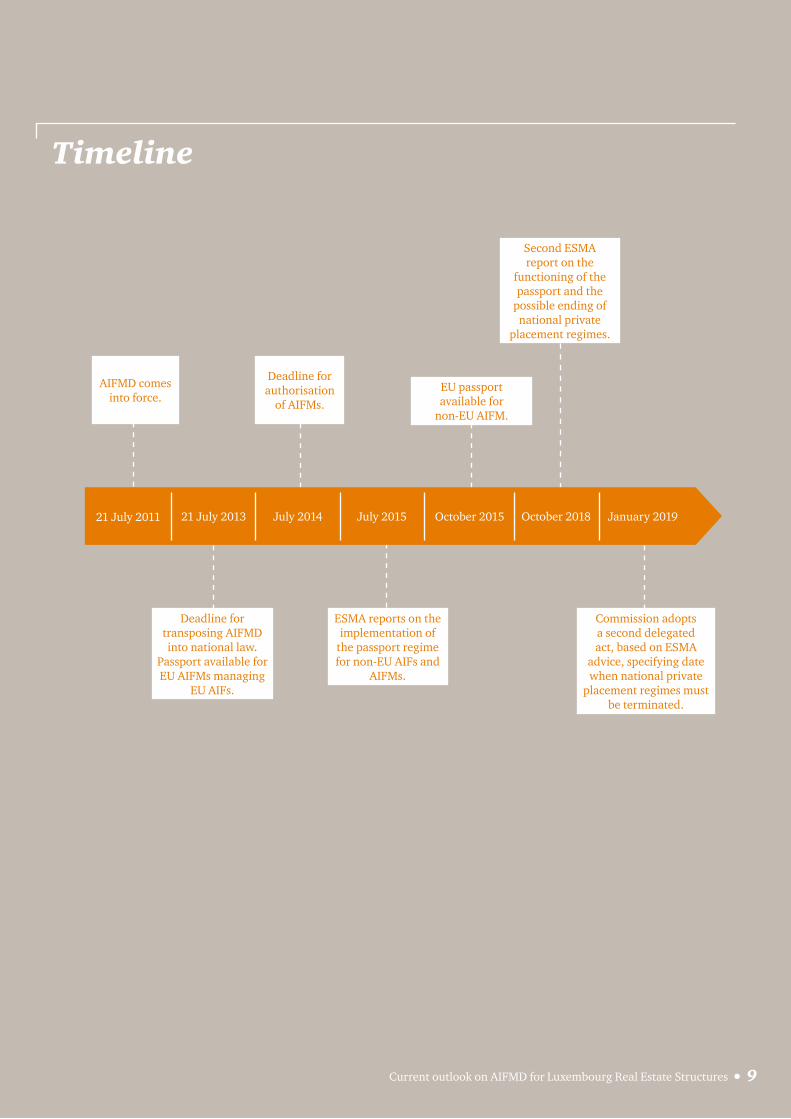

Timeline

AIFMD comes into force.

ESMA reports on the implementation of

the passport regime for non-EU AIFs and

AIFMs.

EU passport available for

non-EU AIFM.

Deadline for transposing AIFMD into national law.

Passport available for EU AIFMs managing

EU AIFs.

Deadline for authorisation

of AIFMs.

Commission adopts a second delegated act, based on ESMA

advice, specifying date when national private

placement regimes must be terminated.

Second ESMA report on the

functioning of the passport and the

possible ending of national private

placement regimes.

21 July 2011 21 July 2013 July 2014 October 2015July 2015 October 2018 January 2019

Current outlook on AIFMD for Luxembourg Real Estate Structures • 9

If you are looking for someone to talk to, give us a call.

Assurance

Kees HageGlobal Real Estate Leader

Tel: +352 49 48 48 2059 Email: [email protected]

Kees has extensive experience in the broader real estate environment. He is excellently positioned to answer your questions regarding AIFMD. In addition, he is chairman of our global IFRS Real Estate International Accounting Group as well as a member of the Global Asset Management Leadership Team. He is MRICs certified and the co-chair on the “Emerging Trends in Real Estate” publications, released in partnership with the Urban Land Institute and PwC.

Olga Huizinga Assurance Real Estate Director

Tel: +352 49 48 48 2219 Email: [email protected]

Olga is an audit director in the Real Estate and Asset Management Group in Luxembourg. She has developed strong experience in the audit of regulated and unregulated real estate structures. She specialises in AIFMD and IFRS. Olga is a member of the PwC Luxembourg AIFMD working group which focuses on the impact of the Directive on real estate structures.

Amaury Evrard Luxembourg Real Estate Leader

Tel: +352 49 48 48 2106 Email: [email protected]

Amaury has significant experience in financial accounting for Real Estate and Infrastructure as well as in advising clients during the set-up phase on structuring, regulatory and operational issues both for closed and open ended structures. He has developed a strong knowledge of the impact of AIFMD on the Luxembourg vehicles. He is also a member of the SICAR committee set up by the regulator and a member of the ALFI Real Estate Working Group and the chairman of the ALFI Infrastructure Working Group.

Catherine Rückel Assurance Real Estate Partner

Tel: +352 49 48 48 2137 Email: [email protected]

Catherine is specialised in Asset Management and Real Estate funds. She is particularly familiar with product structuring for the German market and represents PwC Luxembourg in various international working groups and industry associations.

Marie-Elisa Roussel Luxembourg AIFMD Leader

Tel: +352 49 48 48 2582 Email: [email protected]

Marie-Elisa coordinates the Luxembourg firm’s AIFMD initiatives for every line of services (audit, tax and advisory) covering all industries including real estate. In role, she also works closely with our network firms throughout the European Central Region and is involved with the ALFI AIFMD working group. She had a in depth knowledge of the Directive as well as ESMA’s advice on possible implementing measures. Marie-Elisa, along with the members of the Luxembourg AIFMD working group, has been focusing on the analysis of the impacts of the Directive for the Luxembourg structures.

Kenneth Iek Assurance Real Estate Partner

Tel: +352 49 48 48 2278 Email: [email protected]

Kenneth is a real estate partner specialising in cross border real estate structures. With real estate and asset management clients, he specialises in IFRS, AIFMD and INREV NAV. Kenneth is a member of PwC’s IFRS Asset Management and Real Estate International accounting Group and ALFI’s Real Estate Working Group on the AIFMD.

10 • PwC

Current outlook on AIFMD for Luxembourg Real Estate Structures • 11

Tax

Regulatory Impact

Remuneration and HR questions

Maarten Verjans Tax Real Estate Director

Tel: +352 49 48 48 3014 Email: [email protected]

Maarten is a Tax director in the Real Estate Group where he is in charge of international Real Estate structures.Maarten is a specialist on tax structuring and is well positioned to answer your questions about the tax impact of AIFMD on your real estate structures.

Alexandre Jaumotte Real Estate Tax Leader

Tel: +352 49 48 48 5380 Email: [email protected]

Alexandre is a Tax Partner. He is Tax Leader of the Real Estate and Infrastructure Group where is in charge of a large portfolio of international Real Estate and Infrastructure clients. Alexandre is also heading within PwC Luxembourg a desk dedicated to the Russian market.

Xavier Balthazar Regulatory Partner

Tel: +352 49 48 48 3299 Email: [email protected]

Xavier is a subject matter expert in banking, securitisation and investment funds regulations. He has a unique expertise of regulatory requirements applicable to regulated entities in Luxembourg and in particular of the impacts of the AIFMD on Luxembourg structures. He is a member of the firm’s AIFMD working group.

Christian Scharff Advisory, HRS Partner

Tel: +352 49 48 48 2051 Email: [email protected]

Christian is known for his extensive experience and expertise in Human Resource Management, not only in the industrial, financial and pharmaceutical sectors, but also in the public sector. He is an expert in the remuneration area working on the regulatory, design and linkage with performance aspects. In addition, Christian is chairman of Luxembourg’s “Institut pour le Mouvement Societal” (IMS).

© 2012 PricewaterhouseCoopers S.à.r.l. All rights reserved.

This document has been prepared for the intended recipients only. To the extent permitted by law, PricewaterhouseCoopers LLP does not accept or assume any liability, responsibility or duty of care for any use of or reliance on this document by anyone, other than (i) the intended recipient to the extent agreed in the relevant contract for the matter to which this document relates (if any), or (ii) as expressly agreed by PricewaterhouseCoopers LLP at its sole discretion in writing in advance.

Why PwC Luxembourg?

PwC Luxembourg (www.pwc.lu) is the largest professional services firm in Luxembourg with over 2100 people employed from 57 different countries. It provides audit, tax and advisory services including management consulting, transaction, financing and regulatory advice to a wide variety of clients from local and middle market entrepreneurs to large multinational companies operating from Luxembourg and the Greater Region. It helps its clients create value by giving comfort to the capital markets and providing advice through an industry focused approach.