Embed Size (px)

Citation preview

Current Situation and Prospect of

China Cement Industry

Xuemin Zeng

November 17th, 2008

1. Current Situation of China Cement Industry

1.1 Cement output

The cement output in 2007 reached up to 1.36 billion tons, an increase of 10.12% over the

same period last year, and the output of cement clinker was 0.962 billion tons, an increase of

10.2% over the same period last year, among which the output of decomposition kiln cement

clinker was 0.491 billion tons, an increase of 22.1% over the same period last year.

Proportion of new dry process cement was 51%, an increase of 5% over the same period last

year.

全国

-

50,000

100,000

150,000

200,000

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

0

5

10

15

20

产量(万吨) 增速(%)China Output

(10,000t)Growth Rate (%)

Cement Output in China

Year Output(10,000t) Growth Rate(%)

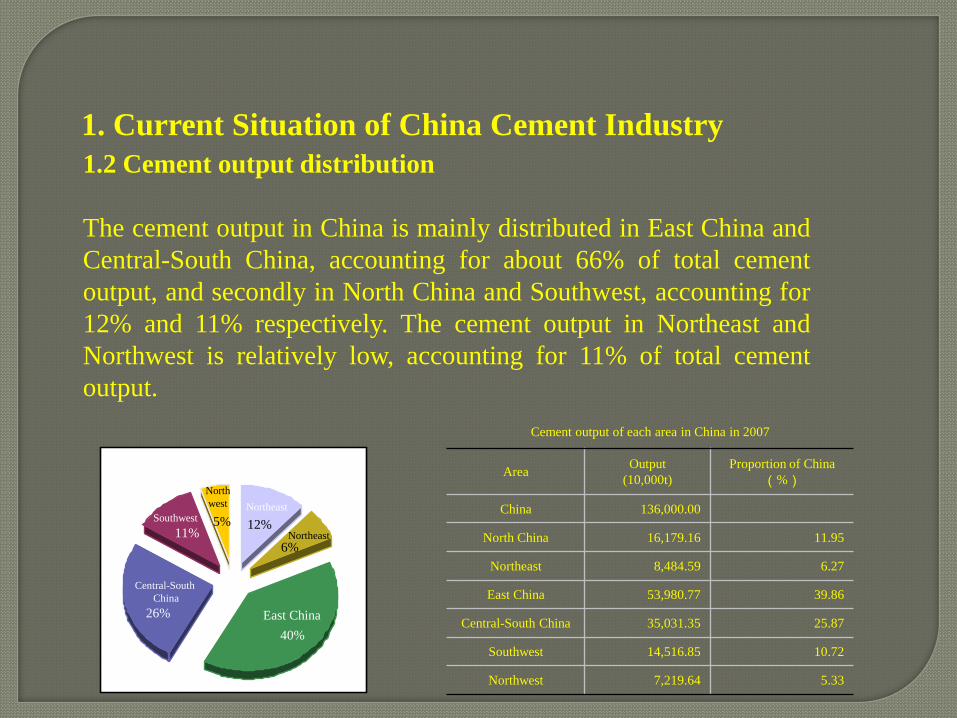

1.2 Cement output distribution

The cement output in China is mainly distributed in East China and

Central-South China, accounting for about 66% of total cement

output, and secondly in North China and Southwest, accounting for

12% and 11% respectively. The cement output in Northeast and

Northwest is relatively low, accounting for 11% of total cement

output.

1. Current Situation of China Cement Industry

Cement output of each area in China in 2007

AreaOutput

(10,000t)

Proportion of China

(%)

China 136,000.00

North China 16,179.16 11.95

Northeast 8,484.59 6.27

East China 53,980.77 39.86

Central-South China 35,031.35 25.87

Southwest 14,516.85 10.72

Northwest 7,219.64 5.33

Output proportion of each area in China(%)

Central-South

China

26% East China

40%

North

west

5%

Northeast

12%Southwest

11% Northeast

6%

1.3 Production line of new dry process cement clinker

By the end of 2007, the statistics from China Cement Association

showed that there were 798 production lines of new dry process

clinker and 607.04 million tons of annual total clinker production

capacity (based on running rate of 86%). Among them, production

lines under 2000t/d were 320, accounting for 17.83% of total

clinker production capacity; production lines between 2000t/d and

5000t/d were 340, accounting for 45.73% of total clinker production

capacity; and production lines at 5000t/d and above were 137,

accounting for 36.8% of total clinker production capacity.

1. Current Situation of Cement Industry in China

1.4 Fast growth of enterprise group

In 2007, up to 12 enterprise groups, with designed clinker

production capacity exceeding 10 million tons, had 213 production

lines of new dry process and 239.54 million tons of designed clinker

production capacity, which took up 26.7% and 39.5% in China

respectively. Average size of production capacity per line of

enterprise group was 1.5 times more than average size of single

line in the whole industry, which showed the charm of

reorganization and alliance.

1. Current Situation of China Cement Industry

1. Current Situation of China Cement Industry

1.4 Fast growth of enterprise groupProduction capacity of new dry process clinker of large

enterprise group by the end of 2007

Group

Conch Group

Vanda Group

Shanshui Group

Huaxin Group

Jidong Cmment

Sinoma Group

Tianrui Group

Lafarge Shui On

Huarun Cement

Beijing JinYu

Hongshi Cement

Zhejiang Three Lions

Total

Number of

production line

Clinker production

capacity in 310 days

(10,000t)

Clinker production

capacity in 320 days

(10,000t)

47 7,223.00 7,456.00

24 2,563.70 2,646.40

20 2,011.90 2,076.80

15 1,869.30 1,929.60

15 1,674.00 1,728.00

18 1,314.40 1,356.80

9 1,255.50 1,296.00

19 1,243.10 1,283.20

8 1,100.50 1,136.00

15 1,091.20 1,126.40

9 1,085.00 1,120.00

10 1,023.00 1,056.00

209 23,454.60 24,211.20

1.5 Cement export situation

In 2007, the export quantity of cement and clinker was 33.01 million tons,

decreasing by 8.6% over last year, and the export value was 1.15 billion US dollars,

decreasing by 2.6% over last year. Among them, the export quantity of cement was

15.19 million tons, decreasing by 21.7%, and the export quantity of clinker was

17.81 million tons, increasing by 6.5%.

On July 1st, 2007, the government issued a policy on abolishing the cement

drawback, and continuous RMB appreciation restrained the fast growth of cement

export, which results in the increase of the export price.

1. Current Situation of China Cement Industry

-

1,000

2,000

3,000

4,000

96 97 98 99 00 01 02 03 04 05 06 07

-50

-

50

100

150

200

250出口水泥(万吨)

增速(%)

Cement Export (10,000t)

Growth Rate (%)

1.6 Improvement on cement technology and equipment level

In China, serialized and large-scaled cement industrial technology equipment have been

developed, and are striding towards ecologization. Cement industrial technology is

advancing rapidly with the fast development of new dry process cement. Technology and

equipment of 1,000t/d to 10,000t/d series production line have been developed for new

dry process, among which technology and equipment of 6000t/d production line and

below have been fully localized and technology and equipment of 1000t/d production

line have been basically localized, so as to greatly increase the technical and economic

index. All these mark that main technical index of new dry process cement complete

technology and equipment in China has reached the world class, which allows

enterprises to compete in the global market of cement equipment. By the end of June

2008, export projects of cement equipment in China reached up to 150, with annual

clinker production capacity of 0.11 billion tons, cement equipment export of 0.7 million

tons and project contact amount of 8.3 billion US dollars. Export regions cover 49

countries, including Europe, United States, etc., and the cement industry is one of the

industrial trades in China that utilize self-owned intellectual property to drive the export

of complete technology and equipment.

1. Current Situation of China Cement Industry

1. Current Situation of China Cement Industry

1.6 Cement technology and equipment

Market Share

(Production capacity) Market Share (Amount)

Figure 1-3: China cement technology and equipment from 2003 to 2007

International market share (%)

2007(forecast)0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2003 2004 2005 2006

1.7 Energy consumption of unit product

In 2007, the total amount of energy consumption of building materials industry

was 193 million tons of standard coal, accounting for 8.5% of total amount of

energy consumption in China. The total amount of energy consumption of

cement industry was 143 million tons of standard coal, accounting for 73.59%

of total amount of energy consumption in building materials industry.

Therefore, energy saving in cement industry is the most important part of

energy saving in building materials industry.

Energy consumption of unit product has been further reduced. The primary

statistics of Information Center of China Building Materials Federation showed

that in 2007, the comprehensive energy consumption per ton cement clinker

was 138kg of standard coal, a decrease of 2.0% over the same period last year,

and the comprehensive energy consumption per ton cement was 115kg of

standard coal, a decrease of 4.0% over the same period last year. The year 2007

witnessed the closure of 520 enterprises having backward production lines, and

the elimination of 57 million tons of cement clinker output, equaling to around

80 million tons of cement output.

1. Current Situation of China Cement Industry

Total

outputGrowth

rateTotal

Comprehensive energy consumption

Utilization

amount

Growth

rate

(10,000t) (%)(%)

(tce)(%)

Growth

rate

Growth

rate(%)

(kgce) (%) (kgce) (%)

2005 106885 9.85 11730 7.22 14.07 -2.71 148 -1.33 127 -9.29 22905 3.15

2006 123611 15.65 13102 11.7 12.77 -9.25 142 -4.01 120 -5.54 28359 23.81

40800(forecast)

-2 115 -4.2 43.989.14 11.76 -7.91 1382007 136100 10.1 14300

Solid Waste

Per ton clinker Per ton cementYear

Cement Output Energy Consumption

1.7 Energy consumption of unit product

1. Current Situation of China Cement Industry

Table 1-3 Energy consumption situation of cement industry in recent years

Energy consumption

Growth

rate

Growth

rate

Product comprehensive energy

consumption Per 10,000 yuan value added

(10,000t) (10,000t)

Energy consumption

1.8 Cement waste heat power-generation and CDM project

By the end of 2007, there had been 122 new dry process production lines that

have been installed with waste heat power-generation equipment, with

generator sets of 92, installed capacity of 740MW and power-generation

capacity of 4.96 billion kWh, which equaled to save 1.82 million tons of

standard coal and reduce 4.73 million tons of CO2 emission. In 2007, 86 waste

heat power-generation production lines had been put into production, with

installed generator set of 59, installed capacity of 571MW, power-generation

capacity of 3.83 billion kWh, which equals to save 1.4 million tons of standard

coal and reduce 3.62 million tons of CO2 emission.

By May 13th, 2008, the State Development and Reform Commission approved

1,295 CDM projects. Among them, CDM projects of cement industry were 86,

account for 6.6% of total amount, where annual CO2 emission reduction was

estimated to be over 8.1 million tons and waster heat power-generation and

calcium carbide slag of cement manufacture was involved.

1. Current Situation of China Cement Industry

2.1 Cement output from January to September 2008

From July to September 2008, cement enterprises in Beijing and its

surrounding areas reduced the output of 10 million tons due to the Olympic

event. In early this year, the cement output was reduced by 11 million tons due

to snow and ice disasters in South China. Also cement enterprises affected in

Wenchuan Earthquake, lost and reduced the cement output by 7 million tons.

These three major factors resulted in reducing the output by 28 million tons

and decreasing the growth rate of cement output by 2% in the whole year.

From January to September, the cement output was 1012.16 million tons, a

comparable increase of 6.88% (deducting the output of eliminated enterprises

last year), and an increase of 2.48% over the same period last year (984.16

million tons). The clinker output was 664.03 million tons, a comparable

increase of 5.59% and an increase of 4.63% over the same period last year

(636.47 million tons). These meant that 41.64 million tons of cement or 9.56

million tons of clinker were eliminated. In either comparable increase or

increase over the same period last year, the growth rate of cement and clinker

output had been greatly decreased.

2. Prospect of China Cement

2.2 Cement market analysis and forecast

Cement, as a complete marketized product, is mainly restricted by the speed of national

economic development, investment in fixed assets, real estate development, so that the

cement output relies on market demand. Three reasons enable the cement to attract

domestic and international investors. The first reason is mature technology and equipment

of cement new dry process production line, large scale of single line, short construction

period, moderate investment amount, and low threshold of investors’ access. Secondly,

cement product and production technology is slow are renewed slowly. Thirdly, market

demand does not reach the peak. Cement market demand shows periodic change, some

investment risk exists and overall yield rate is not high, but general income is comparably

stable, so it is suitable for long-term investment.

Just because of the characteristics mentioned above, driven by market demand (profit),

investors can make quick response. The investor who is the first to take the opportunity is

the first to gain the money. Meanwhile, it has also brought the consequence of rushing

headlong into mass action and caused the market and price fluctuation, which results in

gaining profit and losing money. After the next peak of market comes, cement enterprises

can retrieve the money lost, so as to maintain the cement industry to advance wave upon

wave.

2. Prospect of China Cement

2.2 Cement market analysis and forecast

After the implementation of “The Eleventh Five-Year Plan”, the growth rate of

cement output will face the trend of overall decline according to the law of

wave upon wave advance in cement industry and current international and

domestic microeconomic situation. Although the government came on with

new policies to keep economic growth, it will take a certain time to recover

economic growth rate due to backward inertia. Meanwhile, time difference of

lag response exists in cement industry, so that the growth rate of cement output

will inevitably decrease during the last three years of “The Eleventh Five-Year

Plan”.

The growth rate of cement output in 2006 and 2007 was 15.65% and 10.10%

respectively, and the growth rate of cement output from 2008 to 2010 is

forecasted to be 5%, 3% and 5% respectively. Then during “The Eleventh Five-

Year Plan”, the average growth rate of cement output is 7.84%, and the basic

law is obviously reflected on the line chart.

2. Prospect of China Cement

2.2 Cement market analysis and forecast

2. Prospect of China Cement

12.93

7.71

17.85

4.66

12.31

0

5

10

15

20

六五 七五 八五 九五 十五 十一五

7.84

预计

(%)

Average growth rate of cement output (%) from “The

Sixth Five-Year Plan” to “The Eleventh Five-Year Plan”

Forecast

2. Prospect of China Cement

2.3 Major development trend of cement industry in future

1. Growth rate of cement output decreases. The growth rate of gross national product and

investment in fixed assets decrease, which causes the growth rate of cement market demand

to decrease. With constant improvement in technical content of investment in fixed assets,

the cement demand for investment in fixed assets per RMB10,000 decreases from 4.5 tons

in 2000 to current 0.5 tons. Also the growth rate of investment in real estate shows a

downward trend. All these factors will certainly drive the growth rate of cement output to

decrease.

2. Growth rate of investment in fixed cement assets decreases. Tight monetary policy

results in the increased difficulty of obtaining bank loans. In addition, the government

increases the access threshold of environmental protection, resource collection and

industrial land. Provisional Regulations of the People’s Republic of China on Cultivated

Land Occupation Tax issued on January 1st 2008, increases original tax standard by 400%

with the highest standard up to RMB50 per square meter. Fourthly, the construction cost

increases, with great increase of steel, land, resources, labor and other expenses, and the

trend towards profit of investment will also drive the growth rate of investment to decrease.

2. Prospect of China Cement

2.3 Major development trend cement industry in future

3. Export quantity of cement decreases. In 2007, the reduction of cement export quantity

did not fully result from abolishing export drawback. The reduction mainly involved the

decrease in the cement exported to United States. Due to the weak economy of US and the

rapid development of cement industry and constantly increasing quantity in cement export

in Mexico, Brazil and Southeast Asia, the cement quantity exported to US will continue to

decrease in China. Countries in Middle East successively put newly built cement production

lines into production to reduce the import quantity of cement, and transportation cost has

been greatly increased due to strong rise of oil price, which are main factors to limit the

export quantity. From January to September this year, the export quantity of cement and

clinker is 21.04 million tons, decreasing by 21.5% over the same period last year.

4. Sale price of cement rises. The production cost of cement has been greatly increased

because the price of all raw materials and fuel, and cost of transportation and labor goes up.

The rise in cost will certainly be passed to the sale price of cement in order to counteract the

price hike factors. Whether the price hike factors are properly passed will directly

determine the economic efficiency of enterprise and industry. From January to August of

this year, the profit of cement industry is RMB18.214 billion.

2. Prospect of China Cement

2.3 Major development trend for cement industry in future

5. Development of large enterprise groups speeds up. Rapid expansion of enterprise size,

through reorganization, alliance, merger and extension, has become an approach for large

enterprise groups to develop in recent years. At present, the whole environment where the

cement industry is located, is very beneficial for large enterprise groups to grow up. A large

number of enterprises have realized that they are too weak to compete with large enterprise

groups, which leads “disarming” to large enterprise groups has become the trend. Large

enterprise groups have many financing approaches, including bank loan, obtaining funds

from secondary market, internal financial capital, industrial capital, fund etc. Also large

enterprise groups have made a deep research on the market, thus carrying out rational

investment, together with great support from local government, resulting in relatively low

construction cost and high technical level. All these have become the key factors for the

development of large enterprise groups.

6.Enterprises with backward productivity quit market quickly. With the implementation of

policy on eliminating backward enterprises and strengthening supervision by local

governments, it is wise for enterprises that cannot conform to national industrial policies or

reach the standard of environmental protection, to quit the market, after obtaining policy

support. Following the year of 2007, 2008 and 2009 may have the highest number of

enterprises with backward productivity that quit the market.

2. Prospect of China Cement

2.3 Major development trend of cement industry in future

7. Waste heat power generation projects increases rapidly. At present, the amount of waste

heat power generation projects under construction and in the proposed stage has exceeded

the sum of the 2007. With the rise of electricity price and implementation of CDM project,

waste heat power generation project will be the 1stchoice for enterprises with good

conditions.

8. Energy saving and emission reduction technology transformation project develops fast,

and management level is constantly improved. The only way for most enterprises to survive

and develop is to implement technology transformation for the purpose of energy saving,

emission reduction, environmental protection and comprehensive utilization of resources.

Besides waste heat power-generation, many measures become popular, such as installing

frequency control device, implementing separate grinding technology, revamping of mill,

installing clinker finishing crusher and kiln outlet high-temperature gas analyzer, revamping

of grate cooler, using of grinding aid, increasing of mixed material parameters, etc. Taking

energy efficiency benchmarking as good opportunity, enterprises can implement the project

of energy saving and emission reduction technology transformation in order to improve

enterprise management level, which can get best effect at least cost and achieve the

purposes.

2. Prospect of China Cement

2.3 Major development trend of cement industry in future

9. For the purpose of energy saving, consumption reduction, environmental

protection and comprehensive utilization of resources, the development of

technology and equipment speeds up. “The Eleventh Five-Year Plan” Special

Planning of Major technology and equipment Research and Major Industrial

Technology Development in China put forward “It is important to develop: energy

saving technology and new process of high energy consumption industry, new

technology of high efficient combustion energy saving of industrial furnace,

industrial wastewater treatment, SO2 emission control technology, safe disposal

technology of municipal solid waste and hazardous waste, disposal technology of

the municipal solid waste of ecological restoration, clean production technology,

comprehensive utilization technology of industrial waste.” Based on the good

opportunity, the research, design and manufacture enterprises in cement industry

will have new breakthrough in research and development of technology and

equipment of above aspects, and accelerate the establishment of policies and

regulations, and standard specification.