Embed Size (px)

Citation preview

Advanced banking Guidance for conversation on banking services

Trainers Notes for advanced banking with clients

2 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

This session pack has been produced as part of Citizens Advice Financial Skills for Life.

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Citizens Advice is an operating name of the National Association of Citizens Advice Bureaux, Charity registration number 279057, VAT number 726020276, Company Limited by Guarantee, Registered number 1436945 England. Registered office: Citizens Advice, 3rd Floor North, 200 Aldersgate Street, London, EC1A 4HD

Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, Citizens Advice assumes no responsibility. The user of the information agrees that the information is subject to change without notice. To the extent permitted by law, Citizens Advice excludes all liability for any claim, loss, demands or damages of any kind whatsoever (whether such claims, loss, demands or damages were foreseeable, known or otherwise) arising out of or in connection with the drafting, accuracy and/or its interpretation, including without limitation, indirect or consequential loss or damage and whether arising in tort (including negligence), contract or otherwise.

3 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Advanced banking The aim of this session is to help advisers to provide a session to clients that goes into detail about bank accounts and associated products. This session is specifically aimed at those clients who already have bank accounts and are aware of most banking products, but would benefit from learning more about their various features in detail. Objectives are that by the end of this session clients will be able to:

• List different payment methods

• Distinguish between Direct Debits and Standing Orders

• Use a chequebook with confidence

• Understand detailed use of a bank statement

General Guidance Notes on delivering a group financial capability session are available elsewhere on the Citizens Advice website. These notes are for the trainers use only. A separate handout pack should be used with every client in the group, which will include signposts for further information and guidance.

Trainers are encouraged to feedback to the Financial Skills for Life team with any feedback about training materials or resources. If you have any comments, please contact: [email protected]

4 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Contents

Session Specific Guidance 5

Lesson Plan 7

1. Ways to Pay 8

2. Different types of account 9

3. Direct debits vs Standing orders 11

4. Direct debit and standing order Factsheet 12

5. Cheques explained 13

4. Filling in cheques 14

5. Reading a bank statement 15

6. Managing cashflow 16

7. What now and Where next? 19

Evaluation Guidance 20

Trainers notes 22

5 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Session specific guidance

Subject information Trainers do not need to have specialist money advice knowledge or experience but must have a basic understanding of the different types of bank accounts, bank account features and be able to signpost learners to sources of further advice and information. The pack contains all the key information for the topics covered. Any additional information that is given should be taken from an up to date and accurate source such as:

• the money management section of www.adviceguide.org.uk

• the Money Advice Service free leaflets at www.moneyadviceservice.org.uk including ‘borrowing money’, ‘credit cards’ and ‘credit unions’.

This session aims to help learners understand the financial products available to them. For this learners should be referred to their local Citizens Advice or other advice agency. Materials

• Blank flip chart paper • Marker pens • Note paper and pens for learners • Blu tack • Calculators • Prepared cut-outs for word-matching activity

Manage expectations – Make it clear to clients that the session is a brief overview of banking products, and the most essential elements of financial capability that relate to it. As a one-off session, there will not be the time to explore any single element in any great detail. Signpost and empower – Ensure that clients are aware that after the session they will have a clear idea where to go to answer outstanding queries and to get further assistance. Pacing – Due to the length of the session, it is recommended to allow at least one break for the clients. Be aware of this when planning total timings for sessions.

6 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Top tips

7 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

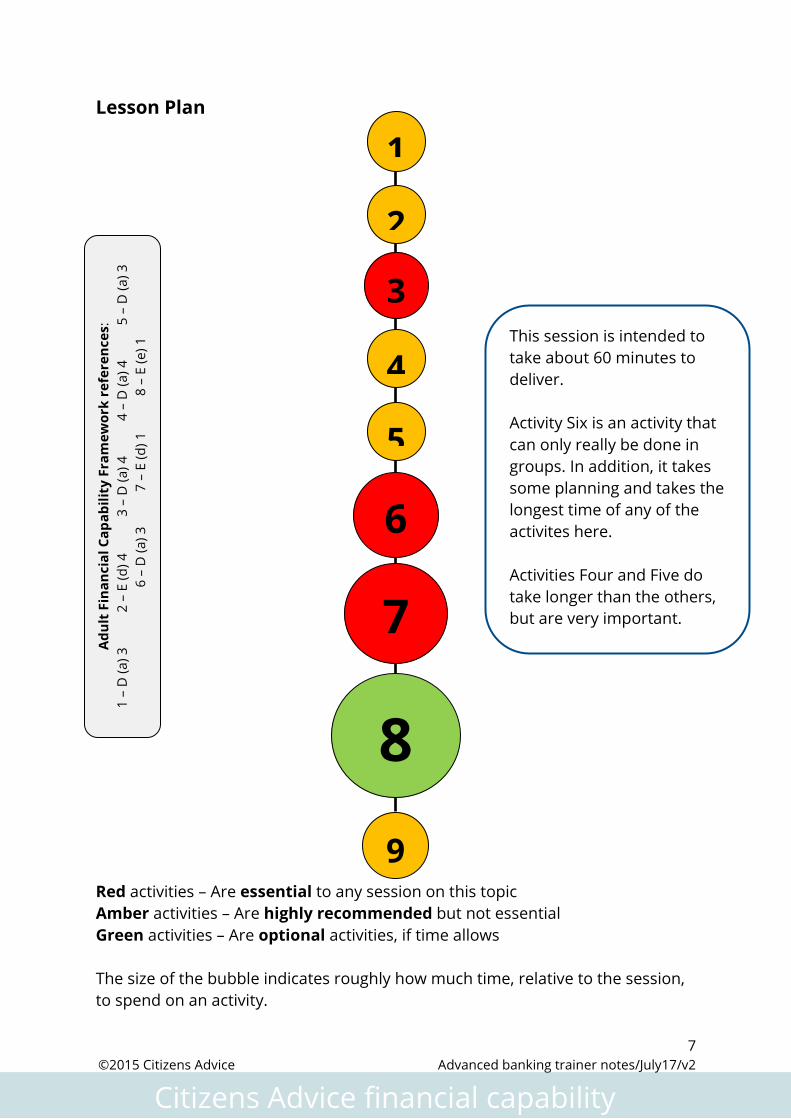

Lesson Plan Red activities – Are essential to any session on this topic Amber activities – Are highly recommended but not essential Green activities – Are optional activities, if time allows The size of the bubble indicates roughly how much time, relative to the session, to spend on an activity.

1

2

3 This session is intended to take about 60 minutes to deliver. Activity Six is an activity that can only really be done in groups. In addition, it takes some planning and takes the longest time of any of the activites here. Activities Four and Five do take longer than the others, but are very important.

6

7

9

8

Adu

lt F

inan

cial

Cap

abili

ty F

ram

ewor

k re

fere

nces

: 1

– D

(a) 3

2

– E

(d) 4

3

– D

(a) 4

4

– D

(a) 4

5

– D

(a) 3

6

– D

(a) 3

7

– E

(d) 1

8

– E

(e) 1

4

5

8 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Ways to pay

There is no specific intended way to use this activity, although it is a good one to bring up different payment methods with clients. The cards on handout D1 are useful for the clients to keep for their own reference but they can also be used in any of the following ways:

• Put learners into pairs and give each pair a set of ‘Ways to pay’ cards. Ask them to spend a few minutes looking through them and then to choose one each that explains a way to pay they don’t often use or they aren’t very familiar with. Ask them to read the card and to think of an example of how someone might use this type of payment.

• Learners can pick out the cards for ways to pay that need a bank account and then discuss how they came to that decision. These are: standing order, direct debit, debit card, credit card, cheque, store card.

• In the whole group ask them to call out names of ways to pay that they

know. As they do so, discuss each card and then hand them out for the clients reference.

• Learners can decide which method of payment is best suited for a one-off payment such as a couch or TV.

If this was useful, why not try…

Banking – Direct Debits vs Standing Orders Banking – Ways to pay for the weekly shop

AIC 20 - A

9 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Different types of accounts

There are several different options open to advisers when discussing different types of bank accounts with a client, or group of clients. The D2 handouts are deliberately open-ended to allow advisers to use them as they see fit. Before the session choose the types of bank account for this activity that are most relevant to the group. For example, only use credit unions if there is one locally. Several recommended activity types follow, but advisers are welcome to develop their own.

• Discuss the bank accounts with the client.

• Ask the client to list the features that mean most to them, then try to match these up to the features on the quick reference table to identify the best bank account for them.

• The client can state what the differences between types of account are

and the adviser can in turn discuss whether these are true or false using the factsheets provided.

• In groups, clients can each be allocated one type of account and then list

its strengths and weaknesses. This can then be fed back to the class.

• Advisers can provide local banking leaflets or information from the local credit union, to give context to the discussion.

• Clients can come up with pros and cons of each account, before rating

them out of 10 for usefulness.

AIC 20 - A

10 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Points that are useful to cover if groups don’t, or to clarify if needed: Basic bank accounts – banks often give them names e.g. ‘first steps’.

Basic bank accounts – may have a small ‘buffer zone’ so if balance is down to £8, £10 can be withdrawn at £10 only cash point machines.

Current accounts – if overdrawn, and benefits or wages are paid in, a client can write a letter asking the bank to ‘earmark’ amounts for specific payments, such as a direct debit for gas.

Current accounts – may also have names, like ‘premier’, but this may mean that there is a monthly fee for extra features such as travel insurance.

All accounts – because of money laundering law (anti-terrorism) proof of identity and address has tightened up. If clients have difficulty with getting the documents the banks are asking for the banks may accept others, such as a letter from a doctor or social worker.

If this was useful, why not try…

Banking – Which account? Banking – Ways to pay

11 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Direct Debits vs Standing Orders

Use the questions on handout D3 as a platform to launch discussion with the clients. Answers

1. Direct Debit

2. Standing Order

3. Direct Debit

4. Direct Debit

5. Standing Order

6. Standing Order Ensure that clients appreciate that both standing orders and direct debits can be preferable to ad-hoc payment methods. Also stress that Direct Debits allow variance in payments, whilst also offering a guaranteed protection scheme.

If this was useful, why not try…

Banking – What is a debit card? Banking – Filling in a cheque

AIC 20 - A

12 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Factsheet: Direct debits and standing orders

Factsheet BAD4 can be simply provided to a client, but it is recommended that the adviser goes through it with them step by step. Each tip would benefit from basic anecdotes and conversational context that makes the tip relevant to the clients own circumstances.

AIC 20 – A

If this was of use, why not try…

Credit – Explaining Jargon – A story

13 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Cheques explained

Using handout BAD5, discuss the basic features of a standard cheque with the clients. Top tips Cheques were due to be phased out in the UK in 2018: that is no longer the case and they are here to stay. However, they are much less common than they used to be. Unfortunately, this means that when a client does have to write a cheque then they are often unsure how to do this. Ensure clients understand the importance of writing a cheque properly, and that failing to do so can mean missed payments or can make it easier for someone to commit fraud with their money. Cheques are still often used the in the ‘grey economy’ where cash in hand is often used as payment. Examples of the ‘grey economy’ include:

o Takeaways o Beauty parlours o Tattoo studios o Plumbers and other handymen o Car mechanics

Note: people often think that post-dating a cheque (writing in a date in the future) means it cannot be cashed till then. This is not true: a bank will cash it no matter what the date is. Any general anecdotes and tips are welcome here.

If this was useful, why not try…

Banking – What is a debit card? Banking – Types of bank card

AIC 20 – A

14 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Filling in cheques

Requires the handout BAD6. Ask the clients to identify the errors with each cheque, here are the answers:

1. No name on the cheque. Explain how this could then be paid to anyone.

2. No amount on the cheque book.

Explain that any amount could then be filled in. At this point, also stress that the number should be written clearly and be impossible to amend or change.

3. Amounts do not match.

In this instance, the bank would – understandably – return the cheque as they would not know how much it relates to. This counts as a bounced cheque, and advisors may wish to use this to discuss what charges apply to bounced cheques.

4. No signature.

When writing their own cheque, stress to the clients, the importance of following the guidance. For example, depending on how £70 is written, it is easy to amend both the number and the words to reflect different amounts:

• £70 can be amended to £700 therefore, writing £70— is more secure. • The word ‘seventy’ can be amended to ‘seven’ easily.

If this was useful, why not try…

Banking – What is a debit card? Banking – Reading a bank statement

AIC 20 - A

15 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Reading a bank statement

Using handout BAD7, ask the clients to read the bank statement and answer the following questions

1 How much money is coming in? £950.54 2 How much money is going out? £1178.79

3 What is the closing balance? £228.25

4 How much money in a month is spent on Starbucks? £13.05

5 How much money is withdrawn from cash machines? £200.00

6 If Mr Griffin is consistently overdrawn by the same amount each

month, how much will his debt be in 12 months’ time? £2739

7 Where can you stop spending? TK Maxx, M&S, Next, Wetherspoon pub, can Mr Griffin walk or cycle to work?

8 Why is it important to check your bank account? To make sure there

are no mistakes, to check how much money you have left, to check that money is not missing, e.g. fraud

The critical point to stress is that the bank statement has led to debt being incurred. The clients spending pattern has revealed a budget which is not balanced. Most importantly, this overspend occurred when rent was paid at the end of the month. Advisors may stress to clients that they should ensure that fixed expenditure always comes out on a fixed date set for soon after they are paid.

If this was useful, why not try…

Banking – Direct Debits vs Standing Orders Banking – What is a debit card Banking – Financial acronyms

AIC 20 – A B D

16 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Managing cash flow

This activity is only of use in groups. Allocate the following roles to participants with the corresponding label, available from the handout:

• Main character • Bank • Landlord • Club • Taxi driver • Electricity supplier • Mobile phone Company • Corner shop • Council

If you have fewer than 9 participants some will need to take more than one role. The adviser will need to prepare something to represent money and debt, ideally, these would be 100 black tokens and 100 red tokens. Different local offices will have different resources regarding this. In the absence of tokens, clients could simply write the figures down on two different colours of paper, or even just use pens with two different colours of ink. Give the bank all the red tokens and the client all the black tokens. Then read out the following scenario, getting the participants to play their parts as you go along. Recommended points to cover:

• Make sure that essential bills are paid first, perhaps by direct debit, but need to be sure the timing is right to ensure the money is in the account to avoid bank charges.

• Plan expenditure on non-essentials when there is money in the account.

AIC 20 – A B C D

T

17 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Our main character has just been paid £100 in wages (or benefits) and the money has gone into their bank account. Hand the £100 worth of black tokens to the ban). Our main character decides to treat themself and buys a new mobile phone for £30 plus a £10 top up. Client takes £40 worth of their black tokens from the bank and gives them to the mobile phone company. The landlord calls round for the rent which is due. Client takes £60 worth of black tokens from the bank and gives them to the landlord. Main character’s friends call round to go clubbing. The main character has to take £15 out of a cash point machine. They uses the one in the local shop which charges £3 for withdrawals. Client takes £18 in red tokens from the bank. Main character has a great night out. They spend £5 to get into the club and a further £8 on drinks. Client gives £13 in red tokens to the club. Followed by £5 on the taxi home. Client gives £5 to the cab driver. Main character’s electricity runs out and they top up their key by £10. Client takes £10 in red tokens from the bank and gives these to the electricity supplier. Main character needs to top up their phone. This costs them £10. Client takes £10 in red tokens from the bank and gives them to the phone company. Main character’s £20 council tax bill comes through. They know they can be in serious trouble if they don’t pay this so they do. Client takes £20 in red tokens from the bank and gives them to Council. Main character has run out of food so goes to the corner shop and spends £12 on some bread, baked beans and biscuits. Client takes £12 in red tokens from the bank and gives them to the corner shop. Ask the group to add up all the red tokens spent (£70). This is the amount the client has had to go overdrawn on their account. The bank charges them £10 for this. Bank gives client another £10 worth of red tokens bring the total the client owes the bank to £80.

18 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Landlord

Mobile Phone

Electricity Company

Club

Corner Shop

Council

Bank

Client

Taxi

19 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Activity: Where Now, and What Next?

Use handout BAD9 to ask the client to pick four things that they will start to use from the end of the session. It is important that they do not feel that any of these changes are insurmountable. Highlight the basic signposts on the bottom of this handout, and encourage clients to explore them.

Help the client to decide what action they can take to start saving money - do not be over-optimistic about what can be achieved. One small achievable step will help to improve client confidence and enable them to see that they can start taking control of their spending.

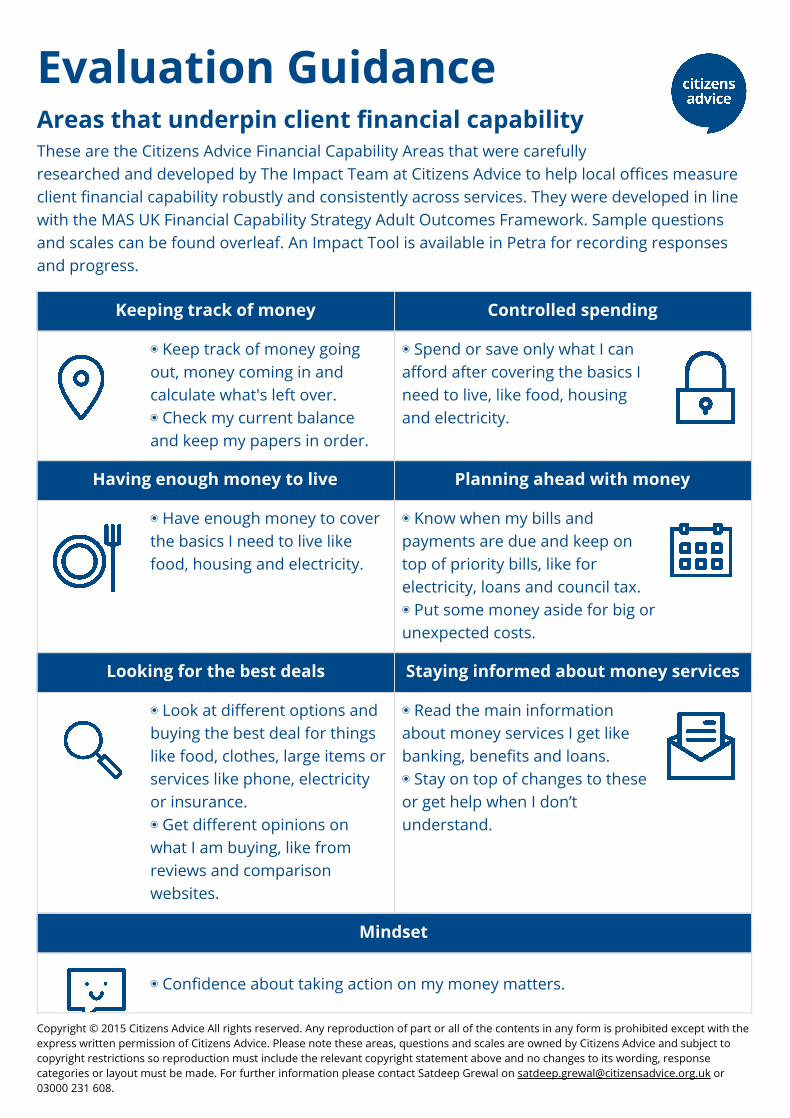

Evaluation Guidance Areas that underpin client financial capability These are the Citizens Advice Financial Capability Areas that were carefully researched and developed by The Impact Team at Citizens Advice to help local offices measure client financial capability robustly and consistently across services. They were developed in line with the MAS UK Financial Capability Strategy Adult Outcomes Framework. Sample questions and scales can be found overleaf. An Impact Tool is available in Petra for recording responses and progress.

Keeping track of money Controlled spending

◉ Keep track of money going out, money coming in and calculate what's left over. ◉ Check my current balance and keep my papers in order.

◉ Spend or save only what I can afford after covering the basics I need to live, like food, housing and electricity.

Having enough money to live Planning ahead with money

◉ Have enough money to cover the basics I need to live like food, housing and electricity.

◉ Know when my bills and payments are due and keep on top of priority bills, like for electricity, loans and council tax. ◉ Put some money aside for big or unexpected costs.

Looking for the best deals Staying informed about money services

◉ Look at different options and buying the best deal for things like food, clothes, large items or services like phone, electricity or insurance. ◉ Get different opinions on what I am buying, like from reviews and comparison websites.

◉ Read the main information about money services I get like banking, benefits and loans. ◉ Stay on top of changes to these or get help when I don’t understand.

Mindset

◉ Confidence about taking action on my money matters.

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Please note these areas, questions and scales are owned by Citizens Advice and subject to copyright restrictions so reproduction must include the relevant copyright statement above and no changes to its wording, response categories or layout must be made. For further information please contact Satdeep Grewal on [email protected] or 03000 231 608.

Sample questions and scales for measuring client financial capability These questions can be used to ascertain how good someone’s financial capability is and so, what their level of need is. They also allow you to track progress by being used to follow-up with how someone is getting on after you have helped them.

Score 1 to 3 Score 4 Score 5 to 7

Low financial capability Average financial capability Advanced financial capability

High need Medium need Low need

Keeping track of money ◉ Calculate money going out, money coming in and what's left over. ◉ Check my current balance and keep my papers in order. Rate your knowledge about the above

No knowledge

No to some knowledge

Some knowledge

Some to good

knowledge

Good knowledge

Good to excellent knowledge

Excellent knowledge

Don’t know

1 2 3 4 5 6 7 ▢

How often do you do the above?

Never Never to sometimes

Sometimes

Sometimes to often

Often

Often to very often

Very often

Don’t know

1 2 3 4 5 6 7 ▢

Staying informed about money services ◉ Read the main information about money services I get like banking, benefits and loans. ◉ Stay on top of changes to these or get help when I don’t understand. Rate your knowledge about the above:

No knowledge

No to some knowledge

Some knowledge

Some to good

knowledge

Good knowledge

Good to excellent knowledge

Excellent knowledge

Don’t know

1 2 3 4 5 6 7 ▢

How often do you do the above?

Never Never to sometimes

Sometimes

Sometimes to often

Often

Often to very often

Very often

Don’t know

1 2 3 4 5 6 7 ▢

Mindset How much confidence do you have about taking action on your money matters?

No confidence

No to some confidence

Some confidence

Some to good confidence

Good confidence

Good to high confidence

High confidence

Don’t know

1 2 3 4 5 6 7 ▢

Copyright © 2015 Citizens Advice All rights reserved. Any reproduction of part or all of the contents in any form is prohibited except with the express written permission of Citizens Advice. Please note these areas, questions and scales are owned by Citizens Advice and subject to copyright restrictions so reproduction must include the relevant copyright statement above and no changes to its wording, response categories or layout must be made. For further information please contact Satdeep Grewal on [email protected] or 03000 231 608.

22 ©2015 Citizens Advice Advanced banking trainer notes/July17/v2

Citizens Advice financial capability

Trainers notes