Embed Size (px)

Citation preview

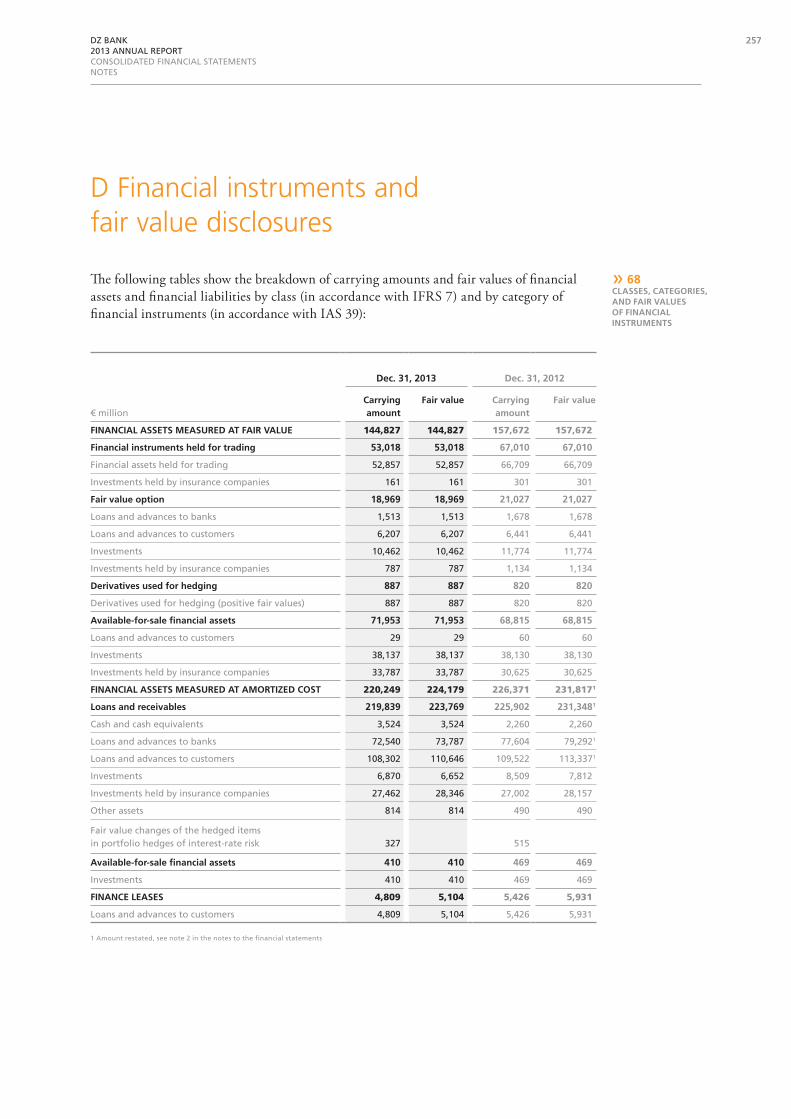

d financial instruments and fair value disclosures

» 68ClassEs, CatEgOriEs, and fair valuEs Of finanCial instrumEnts

The following tables show the breakdown of carrying amounts and fair values of financial assets and financial liabilities by class (in accordance with IFRS 7) and by category of financial instruments (in accordance with IAS 39):

dec. 31, 2013 dec. 31, 2012

€ millionCarrying amount

fair value Carrying amount

fair value

finanCial assEts mEasurEd at fair valuE 144,827 144,827 157,672 157,672

financial instruments held for trading 53,018 53,018 67,010 67,010

Financial assets held for trading 52,857 52,857 66,709 66,709

Investments held by insurance companies 161 161 301 301

fair value option 18,969 18,969 21,027 21,027

Loans and advances to banks 1,513 1,513 1,678 1,678

Loans and advances to customers 6,207 6,207 6,441 6,441

Investments 10,462 10,462 11,774 11,774

Investments held by insurance companies 787 787 1,134 1,134

derivatives used for hedging 887 887 820 820

Derivatives used for hedging (positive fair values) 887 887 820 820

available-for-sale financial assets 71,953 71,953 68,815 68,815

Loans and advances to customers 29 29 60 60

Investments 38,137 38,137 38,130 38,130

Investments held by insurance companies 33,787 33,787 30,625 30,625

finanCial assEts mEasurEd at amOrtizEd COst 220,249 224,179 226,371 231,8171

loans and receivables 219,839 223,769 225,902 231,3481

Cash and cash equivalents 3,524 3,524 2,260 2,260

Loans and advances to banks 72,540 73,787 77,604 79,2921

Loans and advances to customers 108,302 110,646 109,522 113,3371

Investments 6,870 6,652 8,509 7,812

Investments held by insurance companies 27,462 28,346 27,002 28,157

Other assets 814 814 490 490

Fair value changes of the hedged items in portfolio hedges of interest-rate risk 327 515

available-for-sale financial assets 410 410 469 469

Investments 410 410 469 469

finanCE lEasEs 4,809 5,104 5,426 5,931

Loans and advances to customers 4,809 5,104 5,426 5,931

1 Amount restated, see note 2 in the notes to the financial statements

257DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

dec. 31, 2013 dec. 31, 2012

€ millionCarrying amount

fair value Carrying amount

fair value

finanCial liabilitiEs mEasurEd at fair valuE 74,756 74,756 93,035 93,035

financial instruments held for trading 45,805 45,805 58,756 58,756

Financial liabilities held for trading 45,770 45,770 58,715 58,715

Other liabilities 35 35 41 41

fair value option 26,564 26,564 31,266 31,266

Deposits from banks 5,042 5,042 6,572 6,572

Deposits from customers 7,575 7,575 9,476 9,476

Debt certificates issued including bonds 12,612 12,612 13,816 13,816

Subordinated capital 1,335 1,335 1,402 1,402

derivatives used for hedging 2,387 2,387 3,013 3,013

Derivatives used for hedging (negative fair values) 2,387 2,387 3,013 3,013

finanCial liabilitiEs mEasurEd at amOrtizEd COst 223,245 226,538 231,057 235,6881

Deposits from banks 86,319 87,505 94,024 95,3761

Deposits from customers 90,973 92,797 82,693 85,2751

Debt certificates issued including bonds 41,341 41,984 49,474 50,359

Other liabilities 1,472 1,472 1,635 1,635

Subordinated capital 2,891 2,780 2,900 3,043

Fair value changes of the hedged items in portfolio hedges of interest-rate risk 249 331

finanCE lEasEs 30 34 31 35

Other liabilities 30 34 31 35

finanCial guarantEE COntraCts and lOan COmmitmEnts 146 146 145 145

financial guarantee contracts 99 99 87 87

Other liabilities 99 99 87 87

loan commitments 47 47 58 58

Provisions 47 47 58 58

1 Amount restated, see note 2 in the notes to the financial statements

Given the complex structure of home savings contracts and the multitude of scales of rates and charges, there is currently no suitable method for calculating the fair value of an individ-ual contract as at the balance sheet date. Consequently, the fair value cannot be determined using either comparable market prices or suitable option pricing models. The fair values of financial assets and financial liabilities resulting from building society operations are there-fore shown in simplified form at their carrying amounts. On the basis of the models used for building society management, which comprise both collective and non-collective business including deposits, the overall performance of building society operations during the report-ing year was positive.

258 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

The carrying amounts and fair values reported under investments held by insurance compa-nies relate to receivables and fixed-income securities matched as cover for long-term insurance contract obligations as part of insurance operations. Because these instruments are normally held over their entire maturity, interest-rate-related changes in fair value during the maturity of the financial assets balance each other out in full. The fair value of investments held by insurance companies is only recognized in the proportion attributable to the shareholders of the DZ BANK Group.

financial inStrumentS meaSured at coSt

Investments include shares and other variable-yield securities, investments in subsidiaries, interests in joint ventures, and investments in associates measured at cost with a total carrying amount of €410 million (December 31, 2012: €469 million). There are no active markets for these investments, nor can their fair value be reliably determined by using a valuation technique based on assumptions that do not rely on available observable market data. Furthermore, there are no other markets for these financial instruments. The purpose of these investments is largely to support the business operations of the DZ BANK Group on a permanent basis.

In the year under review, the DZ BANK Group sold a small volume of investments in non-consolidated subsidiaries and other shareholdings in entities in which the group had no significant influence, these investments being measured at cost. This resulted in only negligible losses on disposal.

In 2012, the DZ BANK Group had sold investments in non-consolidated subsidiaries and other shareholdings in companies in which the group had no significant influence with a total carrying amount of €21 million measured at cost. This resulted in gains on disposal of €1 million.

259DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

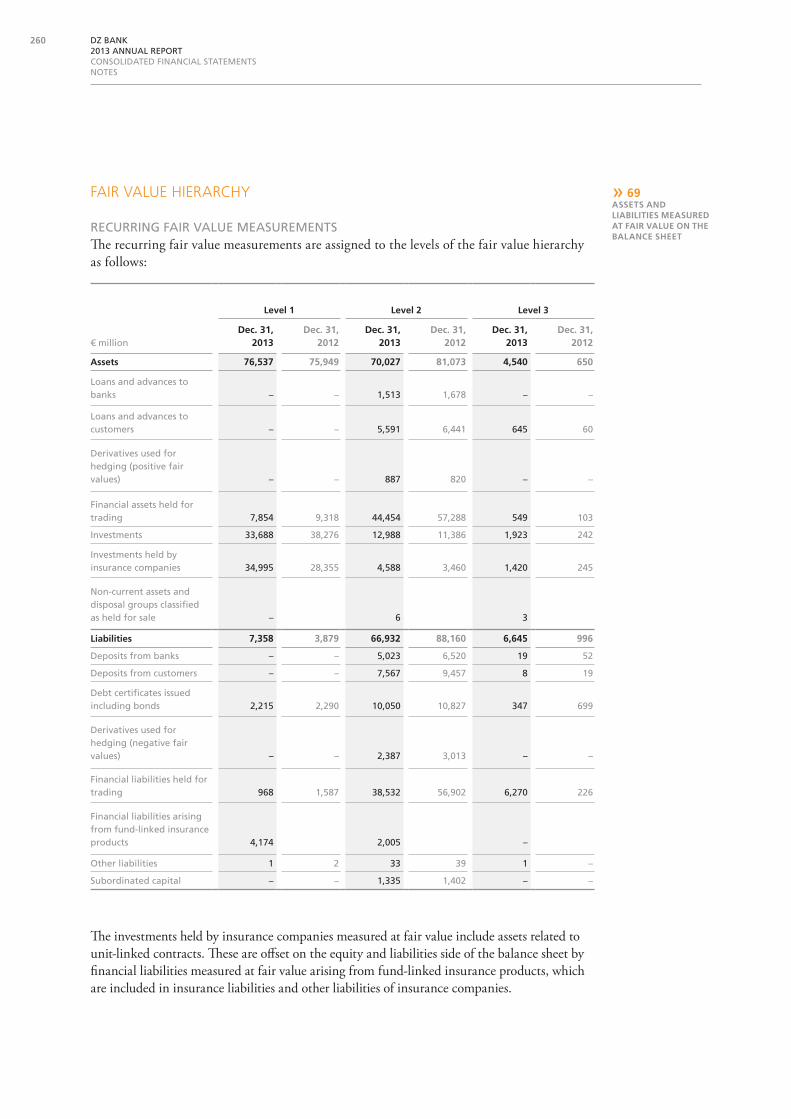

» 69assEts and liabilitiEs mEasurEd at fair valuE On thE balanCE shEEt

fair value hierarchy

RECuRRING FAIR vALuE mEASuREmENtSThe recurring fair value measurements are assigned to the levels of the fair value hierarchy as follows:

The investments held by insurance companies measured at fair value include assets related to unit-linked contracts. These are offset on the equity and liabilities side of the balance sheet by financial liabilities measured at fair value arising from fund-linked insurance products, which are included in insurance liabilities and other liabilities of insurance companies.

level 1 level 2 level 3

€ milliondec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31,

2012

assets 76,537 75,949 70,027 81,073 4,540 650

Loans and advances to banks – – 1,513 1,678 – –

Loans and advances to customers – – 5,591 6,441 645 60

Derivatives used for hedging (positive fair values) – – 887 820 – –

Financial assets held for trading 7,854 9,318 44,454 57,288 549 103

Investments 33,688 38,276 12,988 11,386 1,923 242

Investments held by insurance companies 34,995 28,355 4,588 3,460 1,420 245

Non-current assets and disposal groups classified as held for sale – 6 3

liabilities 7,358 3,879 66,932 88,160 6,645 996

Deposits from banks – – 5,023 6,520 19 52

Deposits from customers – – 7,567 9,457 8 19

Debt certificates issued including bonds 2,215 2,290 10,050 10,827 347 699

Derivatives used for hedging (negative fair values) – – 2,387 3,013 – –

Financial liabilities held for trading 968 1,587 38,532 56,902 6,270 226

Financial liabilities arising from fund-linked insurance products 4,174 2,005 –

Other liabilities 1 2 33 39 1 –

Subordinated capital – – 1,335 1,402 – –

260 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

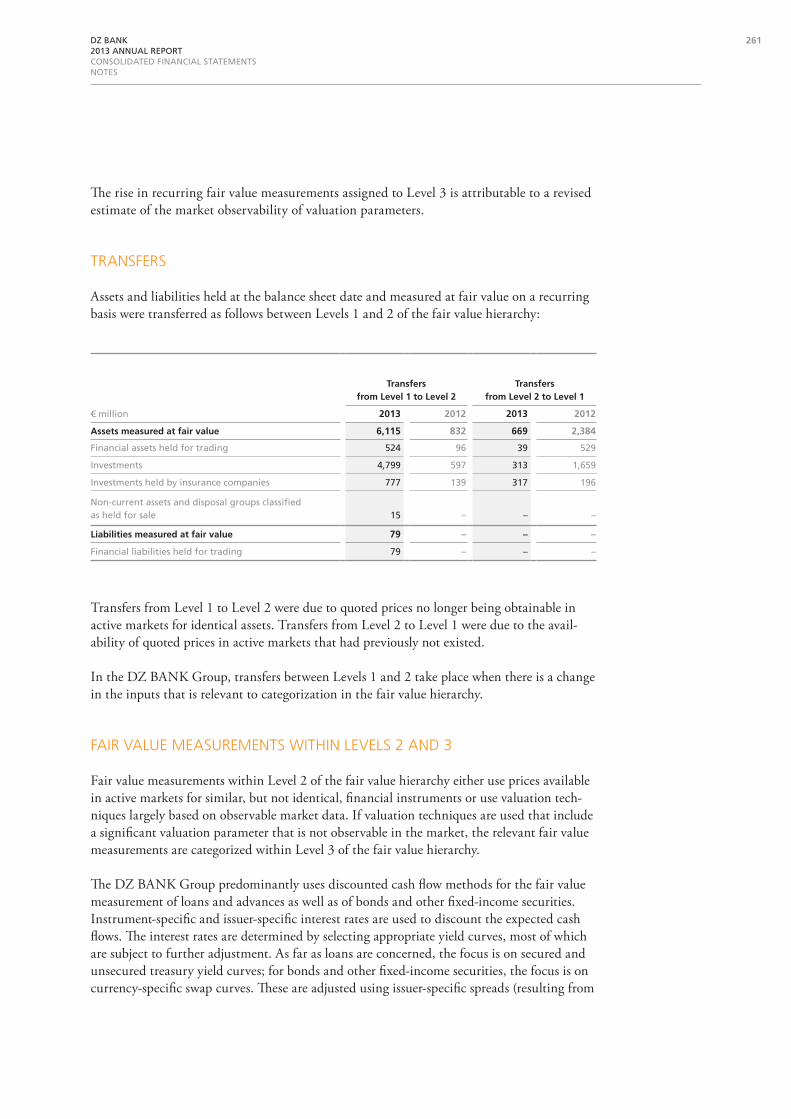

The rise in recurring fair value measurements assigned to Level 3 is attributable to a revised estimate of the market observability of valuation parameters.

tranSferS

Assets and liabilities held at the balance sheet date and measured at fair value on a recurring basis were transferred as follows between Levels 1 and 2 of the fair value hierarchy:

transfersfrom level 1 to level 2

transfersfrom level 2 to level 1

€ million 2013 2012 2013 2012

assets measured at fair value 6,115 832 669 2,384

Financial assets held for trading 524 96 39 529

Investments 4,799 597 313 1,659

Investments held by insurance companies 777 139 317 196

Non-current assets and disposal groups classified as held for sale 15 – – –

liabilities measured at fair value 79 – – –

Financial liabilities held for trading 79 – – –

Transfers from Level 1 to Level 2 were due to quoted prices no longer being obtainable in active markets for identical assets. Transfers from Level 2 to Level 1 were due to the avail-ability of quoted prices in active markets that had previously not existed.

In the DZ BANK Group, transfers between Levels 1 and 2 take place when there is a change in the inputs that is relevant to categorization in the fair value hierarchy.

fair value meaSurementS within levelS 2 and 3

Fair value measurements within Level 2 of the fair value hierarchy either use prices available in active markets for similar, but not identical, financial instruments or use valuation tech-niques largely based on observable market data. If valuation techniques are used that include a significant valuation parameter that is not observable in the market, the relevant fair value measurements are categorized within Level 3 of the fair value hierarchy.

The DZ BANK Group predominantly uses discounted cash flow methods for the fair value measurement of loans and advances as well as of bonds and other fixed-income securities. Instrument-specific and issuer-specific interest rates are used to discount the expected cash flows. The interest rates are determined by selecting appropriate yield curves, most of which are subject to further adjustment. As far as loans are concerned, the focus is on secured and unsecured treasury yield curves; for bonds and other fixed-income securities, the focus is on currency-specific swap curves. These are adjusted using issuer-specific spreads (resulting from

261DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

the issuer’s internal and external credit rating, sector, and risk category), basis swap spreads, unobservable liquidity spreads, and other spreads. In exceptional cases, the notional amount of the debt instrument in question provides the best evidence of fair value.

The fair value measurements of liabilities attributable to registered creditors, debt certificates issued including bonds, and subordinated capital are determined in the same way as for the debt instruments held by using discounted cash flow methods. The modeling of instrument-specific and issuer-specific interest rates for the discounting is based on secured and unsecured funding caps for liabilities and on the relevant subordinated spreads respectively. Basis swap spreads are also used in some cases.

The fair value measurements of shares and other variable-yield securities and of long-term equity investments accounted for in accordance with IAS 39 are determined by applying income capitalization approaches and observing transaction prices. The best indicator of fair value is deemed to be the transaction prices for recent transactions involving the relevant financial instruments, provided there have been any such transactions. Essentially, the fair value is measured using income capitalization approaches in which future income and dividends – calculated on the basis of forecasts and estimates – are discounted, taking risk parameters into account.

The fair value measurements of investment fund units are determined using the pro rata net asset value. This is adjusted for any outstanding performance-related remuneration entitlements of fund managers; risk adjustments are also taken into account. Some long-term equity invest-ments in real-estate companies are also measured at net asset value. In this case, the liabilities are subtracted from the fair values of the real estate tied up in the company and the result is multiplied by the percentage of shareholding. The prices of units in real-estate funds that are not managed by the DZ BANK Group are provided by the fund management company that manages these funds. These units are measured regularly at net asset value. Fair value measure-ments are also based on valuations, current values, and prices in recent transactions.

The fair value measurement of OTC derivatives applies the option in IFRS 13.48, which enables the total net amount to be measured. In the first step, credit risk is not taken into account. The fair values of OTC option derivatives are measured using generally accepted option pricing models such as the Black-Scholes and Black 76 models or the one-factor and two-factor Hull-White models. Share/index options are measured on the basis of the local volatility model with constant forward skew using a Monte Carlo simulation. Non-option, interest-rate-based OTC derivatives are generally measured in accordance with the multiple-curve approach. Variable cash flows are projected using tenor-specific fixing curves. When future cash flows are discounted, liquidity-related adjustments are made to the relevant yield curves – similarly to the method applied to non-derivative interest-bearing financial instru-ments. In order to determine the fair value of forward forex transactions, the differences between translation at the spot rate and the agreed forward rate are calculated. In the second step, credit risk arising from derivatives is recognized after the total net amount has been determined. Credit valuation adjustments (CVA) are recognized to account for counterparty credit risk and debt valuation adjustments (DVA) are recognized to account for the group’s own credit risk. Their measurement also takes account of collateral and uses market-implied parameters with matching maturities or internal parameters with matching maturities for the probability of default and loss given default.

262 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

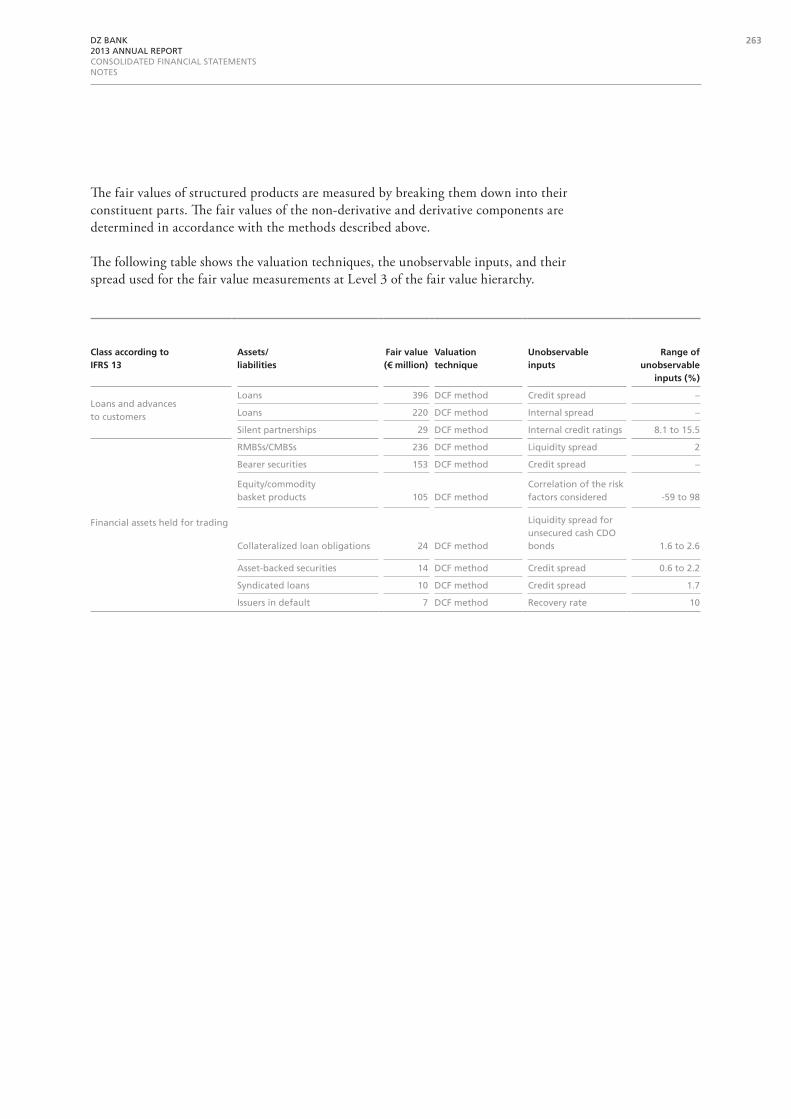

The fair values of structured products are measured by breaking them down into their constituent parts. The fair values of the non-derivative and derivative components are determined in accordance with the methods described above.

The following table shows the valuation techniques, the unobservable inputs, and their spread used for the fair value measurements at Level 3 of the fair value hierarchy.

Class according to ifrs 13

assets/liabilities

fair value (€ million)

valuation technique

unobservable inputs

range of unobservable

inputs (%)

Loans and advances to customers

Loans 396 DCF method Credit spread –

Loans 220 DCF method Internal spread –

Silent partnerships 29 DCF method Internal credit ratings 8.1 to 15.5

Financial assets held for trading

RmBSs/CmBSs 236 DCF method Liquidity spread 2

Bearer securities 153 DCF method Credit spread –

Equity/commodity basket products 105 DCF method

Correlation of the risk factors considered -59 to 98

Collateralized loan obligations 24 DCF method

Liquidity spread for unsecured cash CDO bonds 1.6 to 2.6

Asset-backed securities 14 DCF method Credit spread 0.6 to 2.2

Syndicated loans 10 DCF method Credit spread 1.7

Issuers in default 7 DCF method Recovery rate 10

263DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

Class according to ifrs 13

assets/liabilities

fair value (€ million)

valuation technique

unobservable inputs

range of unobservable

inputs (%)

Investments

Bearer securities 1,296 DCF method Internal spread -2.1 to 1.3

vR Circle 428 DCF methodmultiple-year default probabilities 0 to 100

Bearer securities 80 DCF method Credit spread –

Profit-participation certificates, long-term equity investments 50 DCF method

Assumptions for measurement of risk parameters 9.5 to 10.1

Collateralized loan obligations 14 DCF method

Liquidity spread for unsecured cash CDO bonds 1.6 to 2.6

Investment fund units

44 Net asset value – –

2 DCF method Liquidity spread 25

Investments in subsidiaries 6Income capitaliza-tion approach Future income –

ABSs 3 DCF method Credit spread 0.6 to 2.2

Investments held by insurance companies

Investments in subsidiaries and associates, variable-yield securities, other long-term equity investments, investment fund units

1,136Net asset value method Net asset value –

246Income capitaliza-tion approach Future income –

Registered profit-participation certificates 34 Notional amount – –

variable-yield securities 3Prices offered by issuers – –

Derivatives (positive fair values) 1 Indicative valuationForward exchange rates –

Non-current assets and disposal groups classified as held for sale Real estate 3

Standard valuation methods

Future rent, reference prices –

Deposits from banks and customers

Nth-to-default credit-linked notes 27 DCF method Credit correlation 55 to 80

Debt certificates issued including bonds

Nth-to-default credit-linked notes 200 DCF method Credit correlation 55 to 80

vR Circle 147 DCF methodmultiple-year default probabilities 0 to 100

Financial liabilities held for trading

Equity/commodity basket products 5,762 DCF method

Correlation of the risk factors considered -59 to 98

vR Circle 282 DCF methodmultiple-year default probabilities 0 to 100

Nth-to-default credit-linked notes 226 DCF method Credit correlation 55 to 80

Other liabilities Derivatives (negative fair values) 1

Hull-White, Black 76

Credit spread, volatilities –

264 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

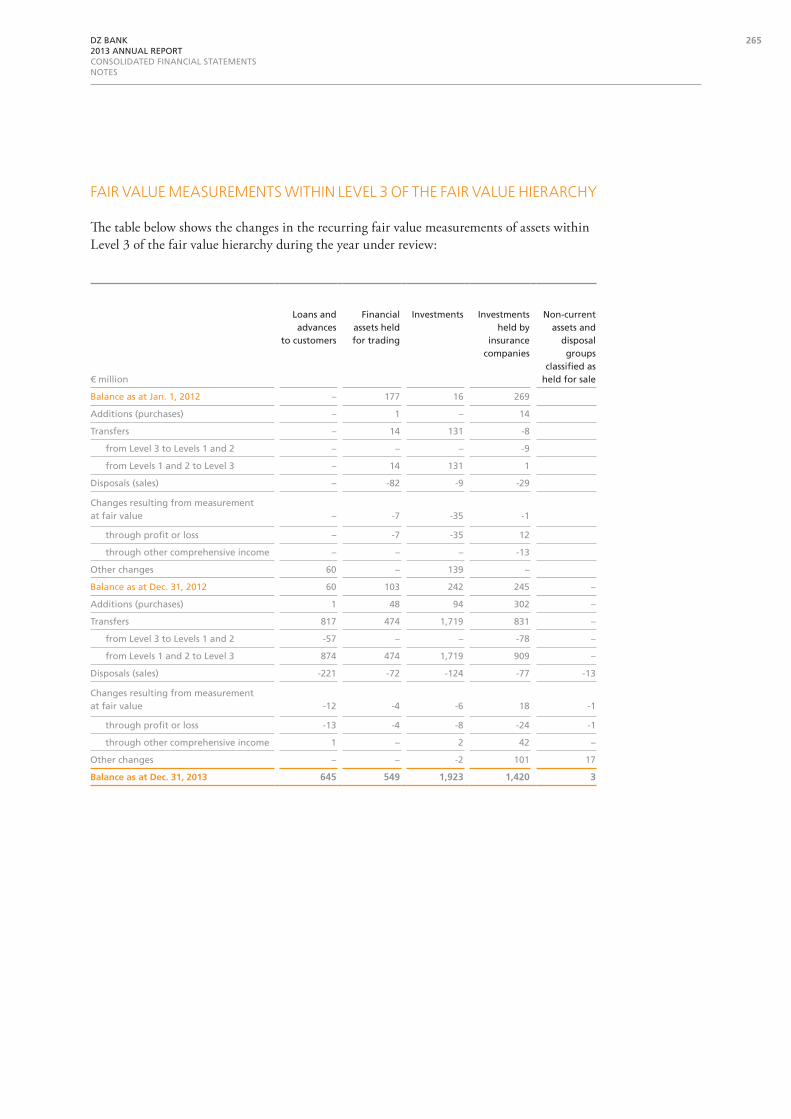

fair value meaSurementS within level 3 of the fair value hierarchy

The table below shows the changes in the recurring fair value measurements of assets within Level 3 of the fair value hierarchy during the year under review:

€ million

Loans and advances

to customers

Financial assets held for trading

Investments Investments held by

insurance companies

Non-current assets and

disposal groups

classified as held for sale

Balance as at Jan. 1, 2012 – 177 16 269

Additions (purchases) – 1 – 14

transfers – 14 131 -8

from Level 3 to Levels 1 and 2 – – – -9

from Levels 1 and 2 to Level 3 – 14 131 1

Disposals (sales) – -82 -9 -29

Changes resulting from measurement at fair value – -7 -35 -1

through profit or loss – -7 -35 12

through other comprehensive income – – – -13

Other changes 60 – 139 –

Balance as at Dec. 31, 2012 60 103 242 245 –

Additions (purchases) 1 48 94 302 –

transfers 817 474 1,719 831 –

from Level 3 to Levels 1 and 2 -57 – – -78 –

from Levels 1 and 2 to Level 3 874 474 1,719 909 –

Disposals (sales) -221 -72 -124 -77 -13

Changes resulting from measurement at fair value -12 -4 -6 18 -1

through profit or loss -13 -4 -8 -24 -1

through other comprehensive income 1 – 2 42 –

Other changes – – -2 101 17

balance as at dec. 31, 2013 645 549 1,923 1,420 3

265DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

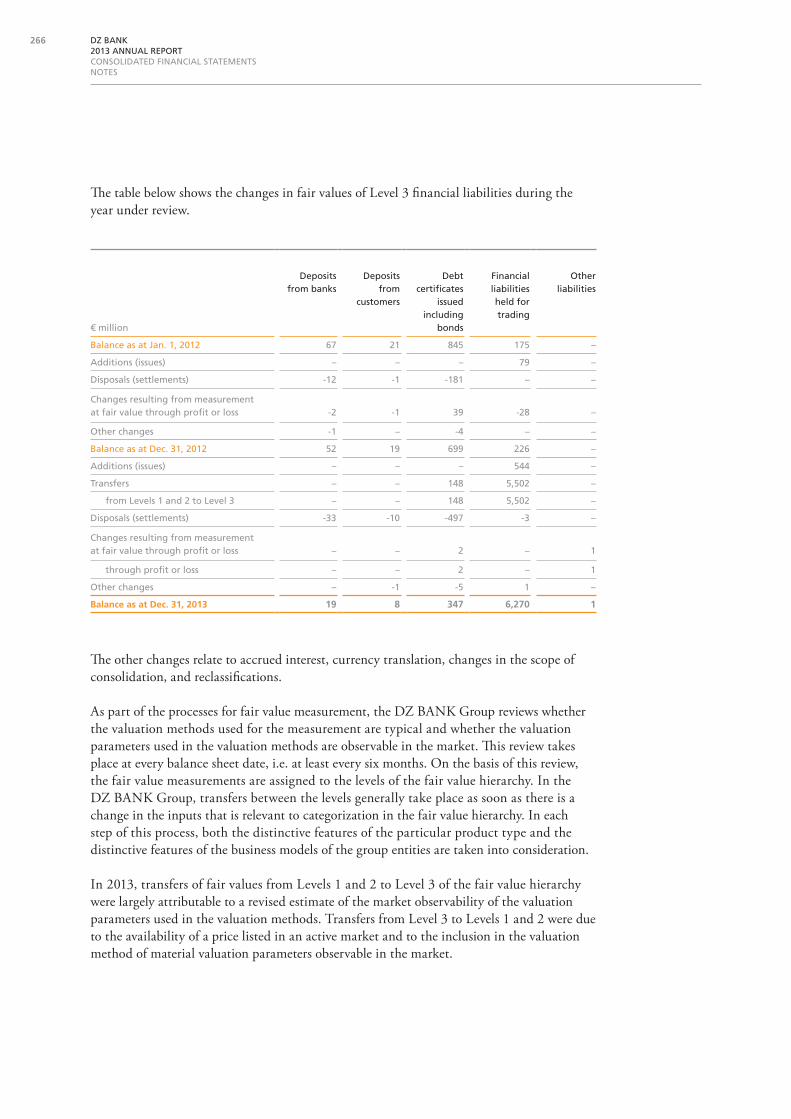

The table below shows the changes in fair values of Level 3 financial liabilities during the year under review.

The other changes relate to accrued interest, currency translation, changes in the scope of consolidation, and reclassifications.

As part of the processes for fair value measurement, the DZ BANK Group reviews whether the valuation methods used for the measurement are typical and whether the valuation parameters used in the valuation methods are observable in the market. This review takes place at every balance sheet date, i.e. at least every six months. On the basis of this review, the fair value measurements are assigned to the levels of the fair value hierarchy. In the DZ BANK Group, transfers between the levels generally take place as soon as there is a change in the inputs that is relevant to categorization in the fair value hierarchy. In each step of this process, both the distinctive features of the particular product type and the distinctive features of the business models of the group entities are taken into consideration.

In 2013, transfers of fair values from Levels 1 and 2 to Level 3 of the fair value hierarchy were largely attributable to a revised estimate of the market observability of the valuation parameters used in the valuation methods. Transfers from Level 3 to Levels 1 and 2 were due to the availability of a price listed in an active market and to the inclusion in the valuation method of material valuation parameters observable in the market.

€ million

Depositsfrom banks

Depositsfrom

customers

Debt certificates

issued including

bonds

Financial liabilities held for trading

Other liabilities

Balance as at Jan. 1, 2012 67 21 845 175 –

Additions (issues) – – – 79 –

Disposals (settlements) -12 -1 -181 – –

Changes resulting from measurement at fair value through profit or loss -2 -1 39 -28 –

Other changes -1 – -4 – –

Balance as at Dec. 31, 2012 52 19 699 226 –

Additions (issues) – – – 544 –

transfers – – 148 5,502 –

from Levels 1 and 2 to Level 3 – – 148 5,502 –

Disposals (settlements) -33 -10 -497 -3 –

Changes resulting from measurement at fair value through profit or loss – – 2 – 1

through profit or loss – – 2 – 1

Other changes – -1 -5 1 –

balance as at dec. 31, 2013 19 8 347 6,270 1

266 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

The amount recognized in profit or loss resulting from the recurring fair value measure-ments within Level 3 of assets and liabilities held at the balance sheet date constituted a loss of €48 million during the year under review (2012: loss of €1 million). The profit or loss is contained in the line items gains and losses on trading activities, gains and losses on invest-ments, other gains and losses on valuation of financial instruments, and gains and losses on investments held by insurance companies and other insurance company gains and losses.

A worsening in the credit rating of 1 percent would lead to a decrease of €16.4 million in the fair values of the loans and advances to customers reported within Level 3. In the case of investments, the same change would lead to a decrease of €0.1 million in the amount recognized in profit or loss.

Alternative assumptions about the liquidity spreads used could lead to significant changes in respect of unsecured collateralized loan obligations reported under investments and financial assets held for trading. All other things being equal, a rise of 1 percent in liquidity spread assumptions would lead to a decrease recognized in profit or loss in the fair value of these financial assets of €0.5 million and a decrease recognized in other comprehensive income in their fair value of €0.2 million. The credit spread used for a very small proportion of the ABS portfolio is derived from research reports produced by third-party banks. Alternative assumptions about the credit spreads used could lead to significant changes in respect of this portfolio. All other things being equal, a rise of 1 percent in credit spread assumptions would lead to a decrease recognized in profit or loss in the fair value of these financial assets of €0.5 million and a decrease recognized in other comprehensive income in their fair value of €0.2 million.

Alternative assumptions about the correlations used could lead to significant changes in respect of the equity/commodity basket products reported under financial liabilities held for trading. All other things being equal, a rise of 1 percent in correlation assumptions would lead to a decrease recognized in profit or loss in the fair value of these financial liabilities of €2.5 million. Alternative assumptions about the default correlations used could lead to significant changes in the fair values of nth-to-default credit-linked notes reported under financial assets held for trading, financial liabilities held for trading, deposits from banks and customers, and debt certificates issued including bonds. All other things being equal, a rise of 1 percent in correlation assumptions would lead to an increase in the fair value of these financial liabilities of €0.1 million (December 31, 2012: €0.4 million).

Sensitivity analysis is used to calculate the aforementioned changes in the fair value measure-ments. Non-performing exposures and strategically held investments in subsidiaries and other shareholdings whose fair values are calculated using an income capitalization approach are not included in the sensitivity analysis.

267DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

exerciSe of option purSuant to ifrS 13.48

The option offered by IFRS 13.48 of measuring a net risk position for financial assets and financial liabilities is used for portfolios whose components are recognized under the balance sheet items financial assets held for trading, investments, loans and advances to banks, loans and advances to customers, and financial liabilities held for trading.

fair value hierarchy

RECuRRING FAIR vALuE mEASuREmENtSRecurring fair value measurements of assets and liabilities that are not recognized at fair value on the balance sheet, but whose fair value must be disclosed, are assigned to the levels of the fair value hierarchy as follows:

fair value meaSurementS within levelS 2 and 3

The fair value measurements of assets and liabilities that are not recognized at fair value on the balance sheet largely correspond to the fair value measurements of assets and liabilities that are recognized at fair value on the balance sheet.

The following table shows the valuation techniques and the unobservable inputs used in these techniques for the fair value measurements at Level 3 of the fair value hierarchy.

» 70assEts and liabilitiEs nOt mEasurEd at fair valuE On thE balanCE shEEt

as at dECEmbEr 31, 2013

€ million level 1 level 2 level 3

assets 670 128,578 96,916

Cash and cash equivalents – 3,524 –

Loans and advances to banks – 72,148 1,639

Loans and advances to customers – 19,937 90,709

Investments 564 4,768 1,730

Investments held by insurance companies 106 27,855 2,187

Property, plant and equipment, and investment property – 183 –

Other assets – 163 651

liabilities 3,355 175,492 47,790

Deposits from banks – 86,486 1,019

Deposits from customers – 48,272 44,525

Debt certificates issued including bonds 3,327 37,458 1,199

Other liabilities 28 906 637

Subordinated capital – 2,370 410

268 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

Class according to ifrs 13

assets/liabilities

fair value € million

valuation technique

unobservable inputs

Loans and advances to banks Loans 1,638 DCF methodCredit spread, recovery rate

Building loans 1 Amortized cost –

Loans and advances to customers

Loans 62,248 DCF method

Credit spread, recovery rate, internal spread

Building loans 27,130 Amortized cost –

Secured loans 1,199 Amortized cost –

Shareholders‘ loans, profit-sharing rights, silent partnerships, other loans and advances 132 DCF method Internal credit ratings

Investments

Shares and other variable-yield securities and investments in subsidiaries, interests in joint ventures, and investments in associates 410 Cost –

RmBSs/CmBSs 426 DCF method Liquidity spread

Collateralized loan obligations 408 DCF method Liquidity spread

Bearer securities 229 DCF method Credit spread

mortgage-backed securities 199 DCF method Duration

Bonds 48 DCF method Credit spread

Profit-participation certificates 7 DCF method Estimated cash flows

ABSs 3 DCF method Liquidity spread

Investments held by insurance companies

Investment property 1,717Standard valuation methods

Future rent, reference prices in the market

Loans 198Standard valuation methods

Credit spread, volatilities

Loans and bank accounts 187 Cost –

Investment property 85 Cost –

Other assets

Credit balances with banks 588 Cost –

Other loans and advances 61 Cost –

Other loans and advances 2 Amortized cost –

Deposits from banks Home savings deposits 1,015 Amortized cost –

Nth-to-default credit-linked notes 4 DCF method Credit correlation

269DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

» 71finanCial instrumEnts dEsignatEd as at fair valuE thrOugh prOfit Or lOss

Class according to ifrs 13

assets/liabilities

fair value € million

valuation technique

unobservable inputs

Deposits from customers

Home savings deposits 44,486 Amortized cost –

Loans 23 DCF method Credit spread

Overpayments on consumer finance loans 9 Cost –

Nth-to-default credit-linked notes 7 DCF method Credit correlation

Debt certificates issued including bonds Commercial paper 1,199 Amortized cost –

Other liabilities

Loans 455 Amortized cost –

trade payables, payables from land ownership 74 Cost –

Non-controlling interests in special funds 57 Cost –

Bonds 27 Amortized cost –

Subordinated loans 17 Amortized cost –

Share capital repayable on demand 5 Amount repayable –

Other payables 2 Amortized cost –

Subordinated capital Share capital repayable on demand 410 Amount repayable –

loanS and receivableS deSignated aS at fair value through profit or loSS

The following table shows the maximum exposure to credit risk of loans and receivables designated as at fair value through profit or loss:

€ milliondec. 31,

2013dec. 31,

2012

Loans and advances to banks 1,513 1,678

Loans and advances to customers 6,249 6,492

Investments 479 506

Investments held by insurance companies 376 763

total 8,617 9,439

Financial guarantee contracts with a value of €3,759 million (December 31, 2012: €4,333 mil-lion) furnished by affiliated banks mitigate this credit risk.

270 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

» 72rEClassifiCatiOns

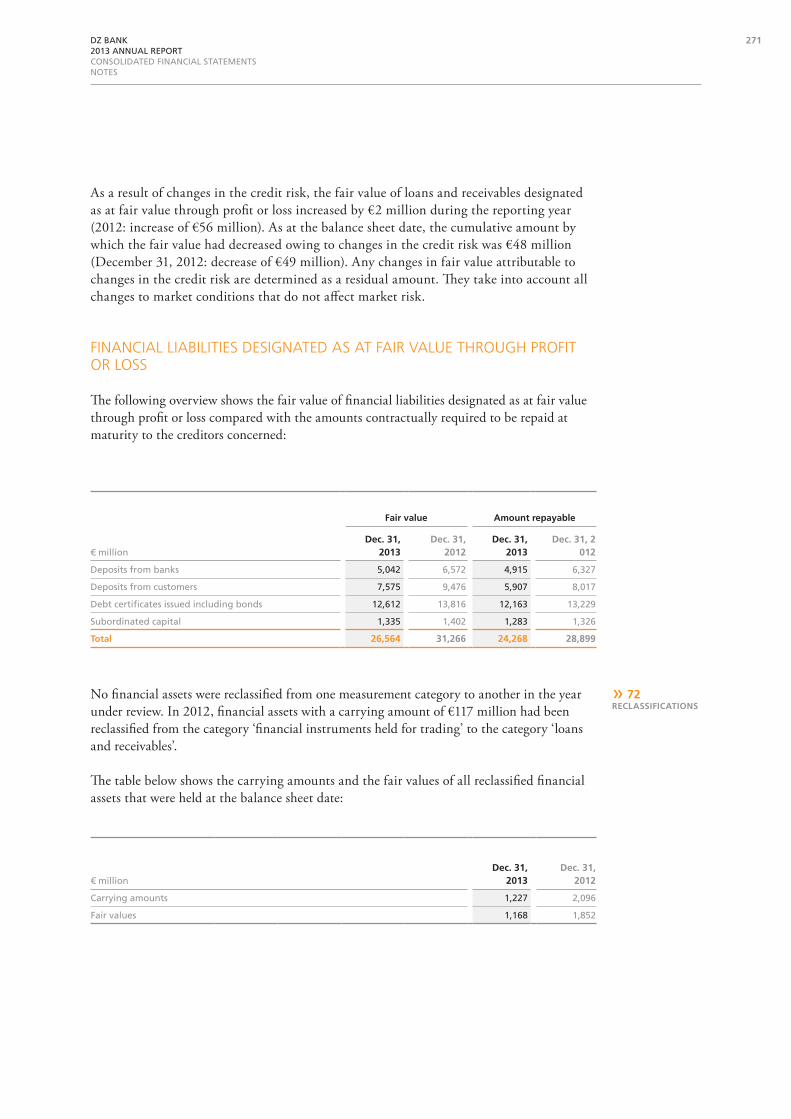

As a result of changes in the credit risk, the fair value of loans and receivables designated as at fair value through profit or loss increased by €2 million during the reporting year (2012: increase of €56 million). As at the balance sheet date, the cumulative amount by which the fair value had decreased owing to changes in the credit risk was €48 million (December 31, 2012: decrease of €49 million). Any changes in fair value attributable to changes in the credit risk are determined as a residual amount. They take into account all changes to market conditions that do not affect market risk.

financial liabilitieS deSignated aS at fair value through profit or loSS

The following overview shows the fair value of financial liabilities designated as at fair value through profit or loss compared with the amounts contractually required to be repaid at maturity to the creditors concerned:

No financial assets were reclassified from one measurement category to another in the year under review. In 2012, financial assets with a carrying amount of €117 million had been reclassified from the category ‘financial instruments held for trading’ to the category ‘loans and receivables’.

The table below shows the carrying amounts and the fair values of all reclassified financial assets that were held at the balance sheet date:

fair value amount repayable

€ milliondec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31, 2

012

Deposits from banks 5,042 6,572 4,915 6,327

Deposits from customers 7,575 9,476 5,907 8,017

Debt certificates issued including bonds 12,612 13,816 12,163 13,229

Subordinated capital 1,335 1,402 1,283 1,326

total 26,564 31,266 24,268 28,899

€ milliondec. 31,

2013dec. 31,

2012

Carrying amounts 1,227 2,096

Fair values 1,168 1,852

271DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

If all the reclassifications in previous financial years had not taken place, an additional gain of €62 million before taxes would have been recognized in the income statement in 2013 as a result of the fair value measurement (2012: gain of €114 million). In addition, gains before taxes of €18 million in respect of the fair value measurement would have been recognized in other comprehensive income in the reporting year (2012: gains before taxes of €308 million).

In 2013, profit before taxes included a loss of €1 million from gains, losses, income, and expenses in connection with all the reclassified financial assets held (2012: loss of €23 million).

The range of effective interest rates for the financial assets reclassified in 2012 was, at the time of reclassification, 2.2 percent to 5.8 percent. At the date of reclassification, cash flows amounting to €137 million were expected to be recovered for the financial assets reclassified in 2012.

Financial assets and financial liabilities reference standard master agreements, such as ISDA Master Agreements and German Master Agreements for Financial Futures. The standard master agreements contain a global netting agreement that only gives rise to a legally enforceable right to set off the amounts after a future event has occurred (in particular, insolvency).

The following tables show financial assets that were offset as at the balance sheet date, that are subject to a legally enforceable global netting agreement, or that are subject to a similar arrangement:

» 73OffsEtting Of finanCial assEts and finanCial liabilitiEs

272 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

as at dECEmbEr 31, 2013

€ million

gross amount of

financial assets before

offsetting

gross amount of

offset financial liabilities

net amount of financial

assets(carrying amount)

associated amounts not offset on the

balance sheet

net amount

Financial instru-ments

Cash collateral received

Derivatives 22,225 – 22,225 15,918 2,747 3,560

Reverse repos/securities borrowing 15,748 – 15,748 15,608 – 140

total 37,973 – 37,973 31,526 2,747 3,700

as at dECEmbEr 31, 2012

€ million

gross amount of

financial assets before

offsetting

gross amount of

offset financial liabilities

net amount of financial

assets(carrying amount)

associated amounts not offset on the

balance sheet

net amount

Financial instru-ments

Cash collateral received

Derivatives 35,404 – 35,404 27,404 2,936 5,064

Reverse repos/securities borrowing 14,543 – 14,543 14,489 – 54

Other financial instruments 76 – 76 2 10 64

total 50,023 – 50,023 41,895 2,946 5,182

273DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

as at dECEmbEr 31, 2012

€ million

gross amount of

financial liabilities

before offsetting

gross amount of

offset financial

assets

net amount of financial

liabilities(carrying amount)

associated amounts not offset on the

balance sheet

net amount

Financial instru-ments

Cash collateral received

Derivatives 37,867 – 37,867 27,236 7,659 2,972

Repos/securities lending 5,402 – 5,402 5,384 7 11

Other financial instruments 10 – 10 10 – –

total 43,279 – 43,279 32,630 7,666 2,983

» 74salE and rEpurChasE agrEEmEnts, sECuritiEs lEnding

tranSferS of financial aSSetS

In 2013, the only transfers carried out by the DZ BANK Group in which the transferred assets remained on the balance sheet in their entirety were transfers under sale and repurchase agreements (repos), in which the DZ BANK Group was the original seller, and transfers as part of securities lending transactions.

as at dECEmbEr 31, 2013

€ million

gross amount of

financial liabilities

before offsetting

gross amount of

offset financial

assets

net amount of financial

liabilities(carrying amount)

associated amounts not offset on the

balance sheet

net amount

Financial

instru-ments

Cash collateral received

Derivatives 21,535 – 21,535 15,733 4,556 1,246

Repos/securities lending 9,460 – 9,460 9,348 2 110

total 30,995 – 30,995 25,081 4,558 1,356

The following tables show financial liabilities that were offset as at the balance sheet date, that are subject to a legally enforceable global netting agreement, or that are subject to a similar arrangement:

274 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

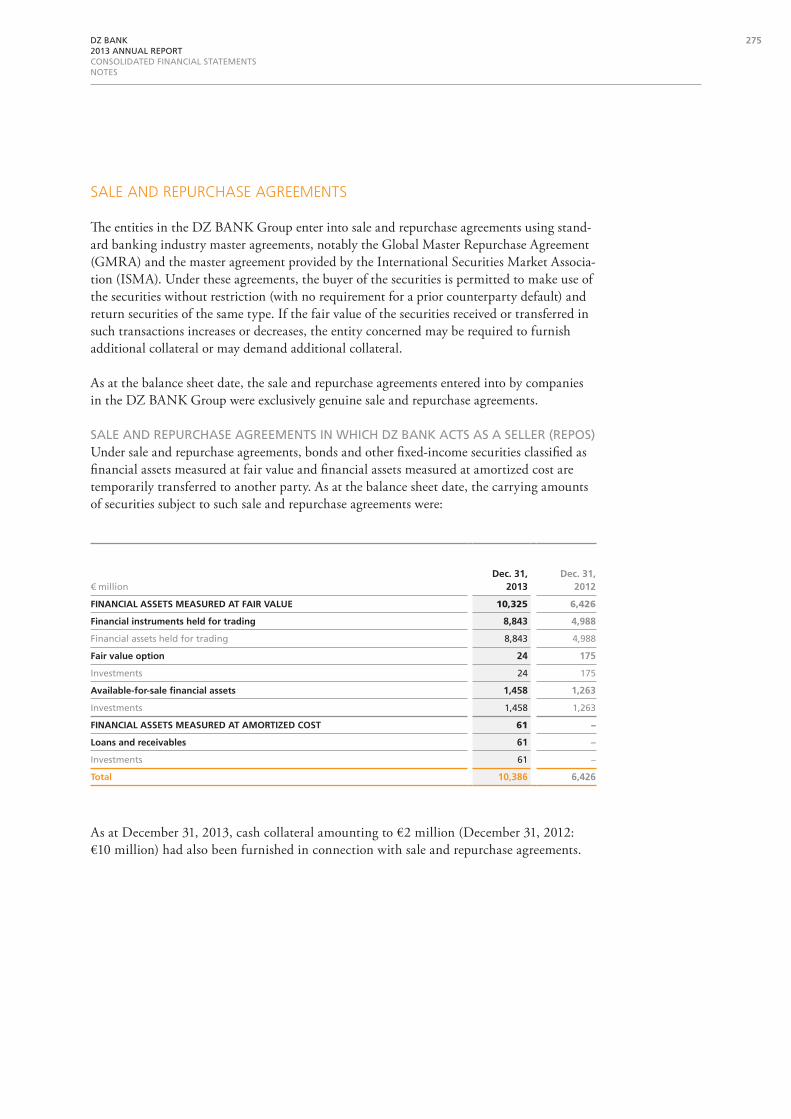

Sale and repurchaSe agreementS

The entities in the DZ BANK Group enter into sale and repurchase agreements using stand-ard banking industry master agreements, notably the Global Master Repurchase Agreement (GMRA) and the master agreement provided by the International Securities Market Associa-tion (ISMA). Under these agreements, the buyer of the securities is permitted to make use of the securities without restriction (with no requirement for a prior counterparty default) and return securities of the same type. If the fair value of the securities received or transferred in such transactions increases or decreases, the entity concerned may be required to furnish additional collateral or may demand additional collateral.

As at the balance sheet date, the sale and repurchase agreements entered into by companies in the DZ BANK Group were exclusively genuine sale and repurchase agreements.

SALE AND REPuRCHASE AGREEmENtS IN WHICH DZ BANK ACtS AS A SELLER (REPOS)Under sale and repurchase agreements, bonds and other fixed-income securities classified as financial assets measured at fair value and financial assets measured at amortized cost are temporarily transferred to another party. As at the balance sheet date, the carrying amounts of securities subject to such sale and repurchase agreements were:

€ milliondec. 31,

2013dec. 31,

2012

finanCial assEts mEasurEd at fair valuE 10,325 6,426

financial instruments held for trading 8,843 4,988

Financial assets held for trading 8,843 4,988

fair value option 24 175

Investments 24 175

available-for-sale financial assets 1,458 1,263

Investments 1,458 1,263

finanCial assEts mEasurEd at amOrtizEd COst 61 –

loans and receivables 61 –

Investments 61 –

total 10,386 6,426

As at December 31, 2013, cash collateral amounting to €2 million (December 31, 2012: €10 million) had also been furnished in connection with sale and repurchase agreements.

275DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

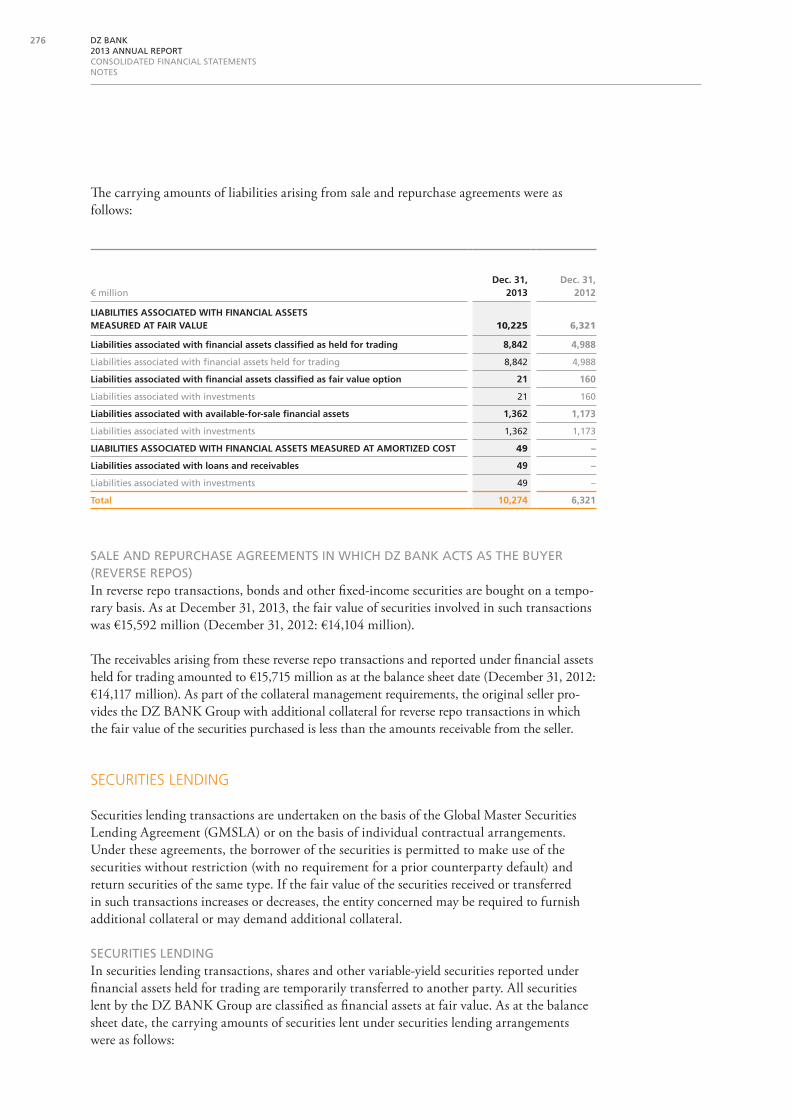

SALE AND REPuRCHASE AGREEmENtS IN WHICH DZ BANK ACtS AS tHE BuyER (REvERSE REPOS)In reverse repo transactions, bonds and other fixed-income securities are bought on a tempo-rary basis. As at December 31, 2013, the fair value of securities involved in such transactions was €15,592 million (December 31, 2012: €14,104 million).

The receivables arising from these reverse repo transactions and reported under financial assets held for trading amounted to €15,715 million as at the balance sheet date (December 31, 2012: €14,117 million). As part of the collateral management requirements, the original seller pro-vides the DZ BANK Group with additional collateral for reverse repo transactions in which the fair value of the securities purchased is less than the amounts receivable from the seller.

SecuritieS lending

Securities lending transactions are undertaken on the basis of the Global Master Securities Lending Agreement (GMSLA) or on the basis of individual contractual arrangements. Under these agreements, the borrower of the securities is permitted to make use of the securities without restriction (with no requirement for a prior counterparty default) and return securities of the same type. If the fair value of the securities received or transferred in such transactions increases or decreases, the entity concerned may be required to furnish additional collateral or may demand additional collateral.

SECuRItIES LENDINGIn securities lending transactions, shares and other variable-yield securities reported under financial assets held for trading are temporarily transferred to another party. All securities lent by the DZ BANK Group are classified as financial assets at fair value. As at the balance sheet date, the carrying amounts of securities lent under securities lending arrangements were as follows:

€ milliondec. 31,

2013dec. 31,

2012

liabilitiEs assOCiatEd with finanCial assEts mEasurEd at fair valuE 10,225 6,321

liabilities associated with financial assets classified as held for trading 8,842 4,988

Liabilities associated with financial assets held for trading 8,842 4,988

liabilities associated with financial assets classified as fair value option 21 160

Liabilities associated with investments 21 160

liabilities associated with available-for-sale financial assets 1,362 1,173

Liabilities associated with investments 1,362 1,173

liabilitiEs assOCiatEd with finanCial assEts mEasurEd at amOrtizEd COst 49 –

liabilities associated with loans and receivables 49 –

Liabilities associated with investments 49 –

total 10,274 6,321

The carrying amounts of liabilities arising from sale and repurchase agreements were as follows:

276 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

Collateral is provided or received as part of collateral management arrangements in connec-tion with financial assets held for trading that are lent under securities lending agreements. In this process, all positions with the counterparty concerned are netted to determine the collateral to be provided or received.

SECuRItIES BORROWINGThe fair value of borrowed securities as at the balance sheet date was as follows:

€ milliondec. 31,

2013dec. 31,

2012

financial instruments held for trading 16 6

Financial assets held for trading 16 6

available-for-sale financial assets – 578

Investments held by insurance companies – 578

total 16 584

€ milliondec. 31,

2013dec. 31,

2012

Bonds and other fixed-income securities 377 113

Shares and other variable-yield securities 76 211

total 453 324

€ milliondec. 31,

2013dec. 31,

2012

Financial assets held for trading 8,859 4,994

Investments 1,543 1,438

Investments held by insurance companies – 578

total 10,402 7,010

Collateral is furnished for borrowed securities as described in the collateral management arrangements above.

SecuritieS Subject to a Sale and repurchaSe or lending agree-ment that the recipient may Sell or pledge elSewhere aS collat-eral with no requirement for a prior counterparty default

All securities transferred to another party by entities in the DZ BANK Group under sale and repurchase agreements or securities lending agreements may be sold or pledged elsewhere as collateral by the recipient without restriction.

The carrying amounts of the individual balance sheet items concerned are as follows:

277DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

collateral pledged

The breakdown of the carrying amount of financial assets pledged as collateral for liabilities is as follows:

» 75COllatEral

€ milliondec. 31,

2013dec. 31,

2012

Loans and advances to banks 32,704 31,845

Loans and advances to customers 486 498

Financial assets held for trading 7,588 10,800

Investments 2 13

Investments held by insurance companies 391 382

total 41,171 43,538

Loans and advances to banks with a carrying amount of €10 million are pledged as collat-eral for contingent liabilities. No collateral was pledged for contingent liabilities in 2012.

Of the total financial assets pledged as collateral for liabilities, financial assets held for trading and investments with a carrying amount of €1,885 million (2012: €1,320 million) may be sold or pledged elsewhere as collateral by the recipient, even if the relevant entity in the DZ BANK Group is not in default.

Funds received from Germany’s KfW development bank that are to be specifically used for the purposes of development program loans are passed on to affiliated banks. The resulting loans and advances to affiliated banks are lodged with the KfW bank as collateral.

The loans and advances to customers pledged as collateral are building loans issued as part of KfW development program loans. The amounts due to the KfW development bank are secured by assigning to KfW the receivables arising from the forwarding of the development loans together with the collateral furnished by the borrowers.

Securities and money market placements recognized as financial assets held for trading are pledged as collateral for exchange-traded forward transactions, non-exchange-traded deriva-tives and for forward forex transactions. These arrangements are governed by standard industry collateral agreements.

The investments pledged as collateral comprise securities furnished as collateral to cover a facility for short-term drawdown of funding in the event of a financial squeeze.

The investments held by insurance companies are predominantly securities pledged as collateral as part of the reinsurance business; this collateral may only be sold or pledged by the recipient in the event of default by the assignor.

278 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

» 76itEms Of inCOmE, ExpEnsE, gains, and lOssEs

collateral held

Foreign mortgage rights with a fair value of €37 million (December 31, 2012: €100 million) used as collateral for loans and advances to customers may be repledged as collateral or sold, even in the absence of any payment default by the party providing the collateral. However, there is an obligation to return the collateral to the owner.

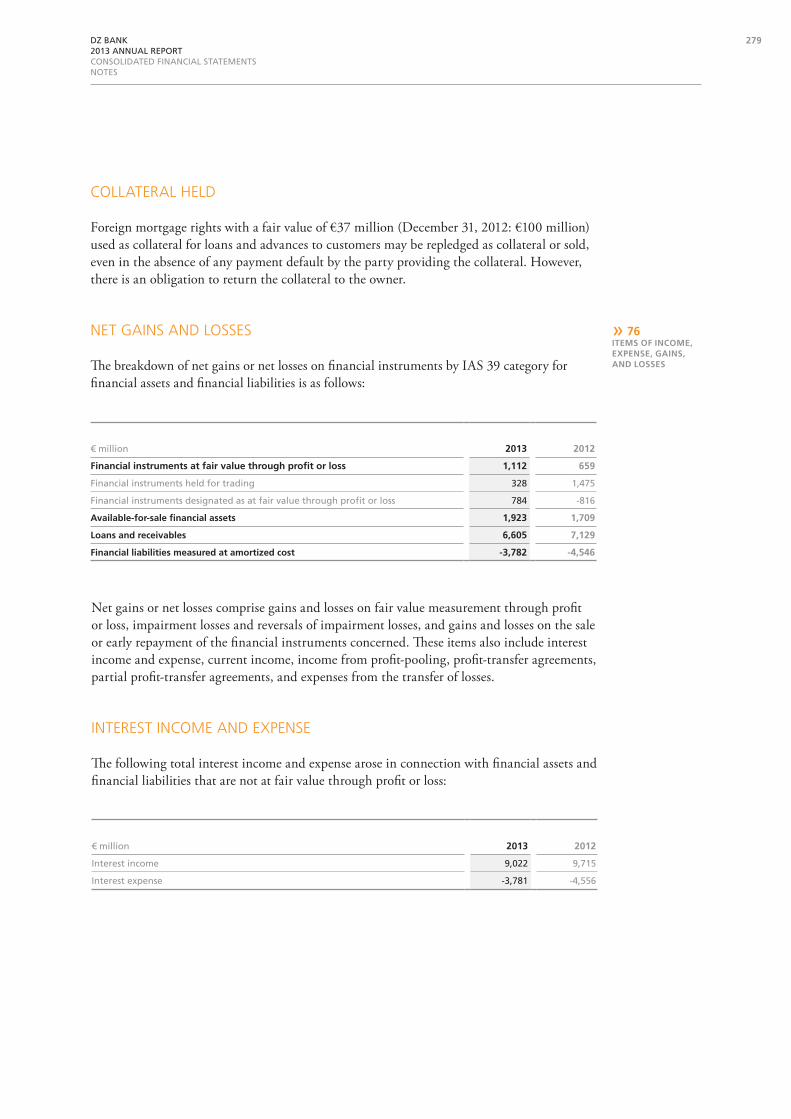

net gainS and loSSeS

The breakdown of net gains or net losses on financial instruments by IAS 39 category for financial assets and financial liabilities is as follows:

€ million 2013 2012

financial instruments at fair value through profit or loss 1,112 659

Financial instruments held for trading 328 1,475

Financial instruments designated as at fair value through profit or loss 784 -816

available-for-sale financial assets 1,923 1,709

loans and receivables 6,605 7,129

financial liabilities measured at amortized cost -3,782 -4,546

€ million 2013 2012

Interest income 9,022 9,715

Interest expense -3,781 -4,556

Net gains or net losses comprise gains and losses on fair value measurement through profit or loss, impairment losses and reversals of impairment losses, and gains and losses on the sale or early repayment of the financial instruments concerned. These items also include interest income and expense, current income, income from profit-pooling, profit-transfer agreements, partial profit-transfer agreements, and expenses from the transfer of losses.

intereSt income and expenSe

The following total interest income and expense arose in connection with financial assets and financial liabilities that are not at fair value through profit or loss:

279DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

fee and commiSSion income and expenSeS

€ million 2013 2012

finanCial assEts mEasurEd at fair valuE -100 -160

available-for-sale financial assets -100 -160

Loans and advances to customers -13 –

Investments -9 -2

Investments held by insurance companies -78 -158

finanCial assEts mEasurEd at amOrtizEd COst -1,254 -1,200

loans and receivables -1,202 -1,181

Loans and advances to banks -26 -13

Loans and advances to customers -1,141 -1,047

Investments -33 -119

Investments held by insurance companies -2 -2

available-for-sale financial assets -52 -19

Investments -52 -19

finanCE lEasEs -35 -82

Loans and advances to customers -35 -82

€ million 2013 2012

fee and commission income

from financial instruments not at fair value through profit or loss 600 593

from trust and other fiduciary activities 1,869 1,669

fee and commission expenses

for financial instruments not at fair value through profit or loss -808 -734

for trust and other fiduciary activities -665 -571

intereSt income on impaired financial aSSetS

Interest income arising from unwinding the discount on impaired loans and advances recognized at present value as specified in IAS 39.A93 amounted to €39 million (2012: €67 million).

impairment loSSeS on financial aSSetS

The table below shows impairment losses on financial assets broken down by class of financial instrument.

280 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

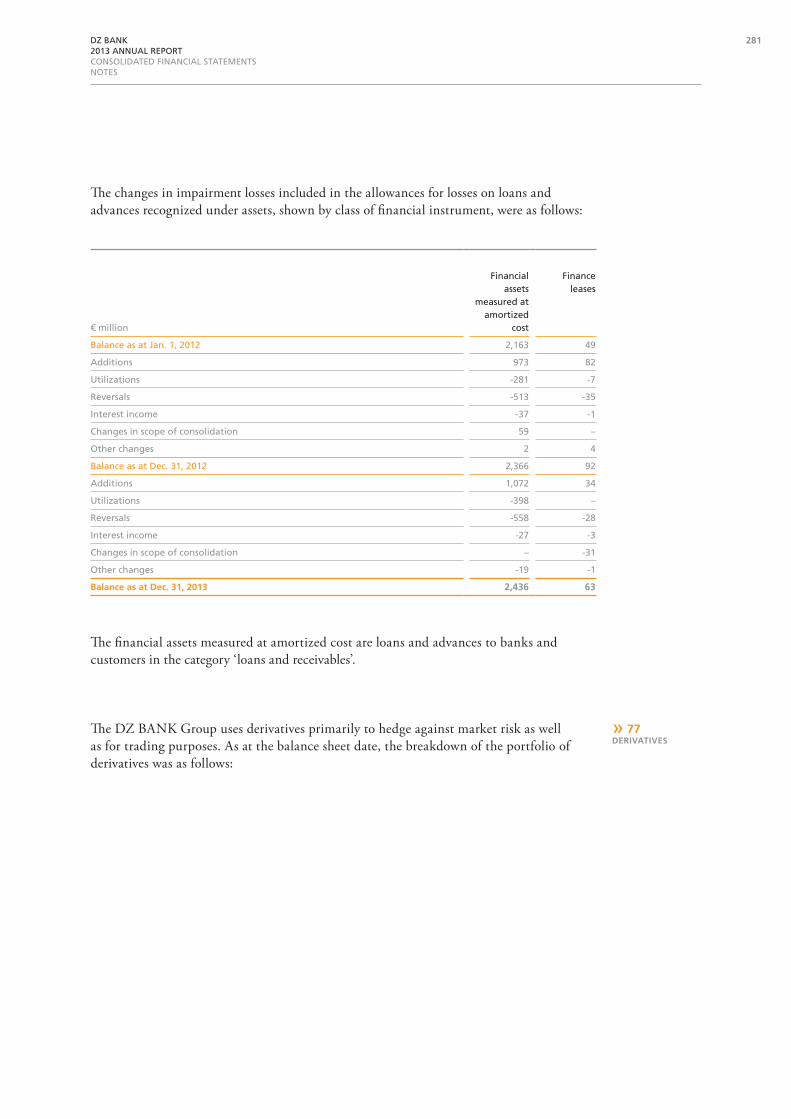

The changes in impairment losses included in the allowances for losses on loans and advances recognized under assets, shown by class of financial instrument, were as follows:

The financial assets measured at amortized cost are loans and advances to banks and customers in the category ‘loans and receivables’.

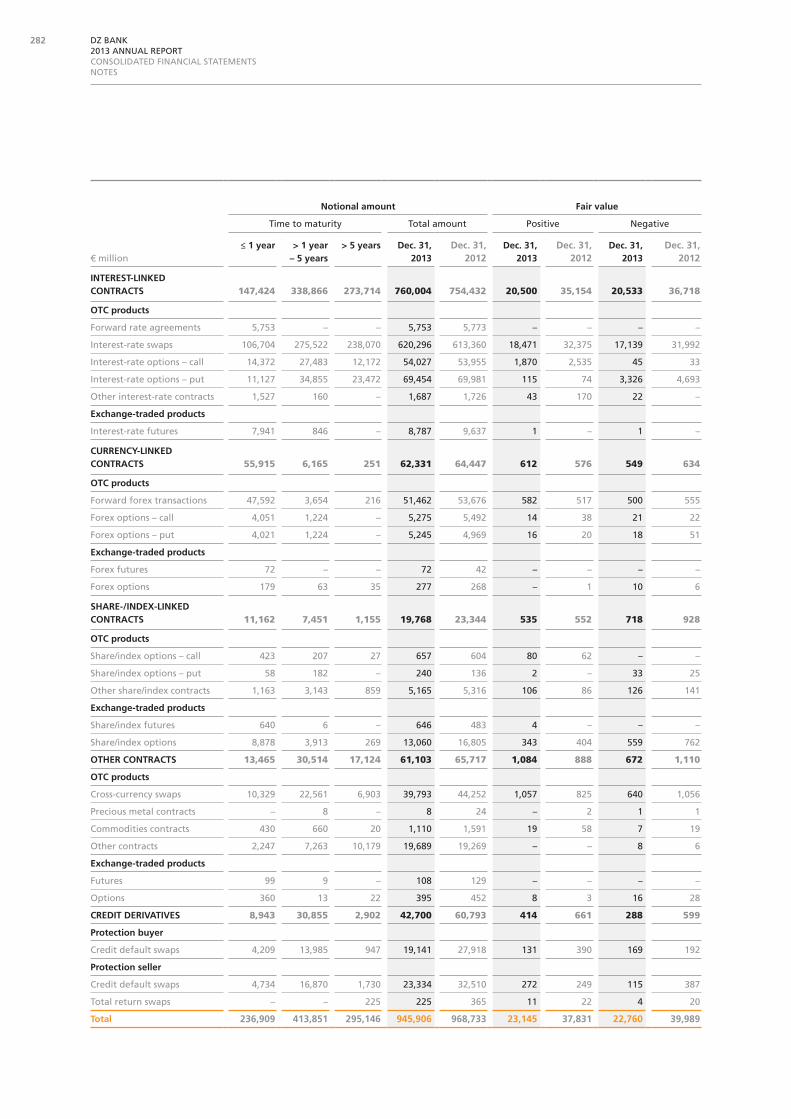

The DZ BANK Group uses derivatives primarily to hedge against market risk as well as for trading purposes. As at the balance sheet date, the breakdown of the portfolio of derivatives was as follows:

€ million

Financial assets

measured at amortized

cost

Finance leases

Balance as at Jan. 1, 2012 2,163 49

Additions 973 82

utilizations -281 -7

Reversals -513 -35

Interest income -37 -1

Changes in scope of consolidation 59 –

Other changes 2 4

Balance as at Dec. 31, 2012 2,366 92

Additions 1,072 34

utilizations -398 –

Reversals -558 -28

Interest income -27 -3

Changes in scope of consolidation – -31

Other changes -19 -1

balance as at dec. 31, 2013 2,436 63

» 77dErivativEs

281DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

notional amount fair value

time to maturity total amount Positive Negative

€ million≤ 1 year > 1 year

– 5 years> 5 years dec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31,

2012

intErEst-linkEd COntraCts 147,424 338,866 273,714 760,004 754,432 20,500 35,154 20,533 36,718

OtC products

Forward rate agreements 5,753 – – 5,753 5,773 – – – –

Interest-rate swaps 106,704 275,522 238,070 620,296 613,360 18,471 32,375 17,139 31,992

Interest-rate options – call 14,372 27,483 12,172 54,027 53,955 1,870 2,535 45 33

Interest-rate options – put 11,127 34,855 23,472 69,454 69,981 115 74 3,326 4,693

Other interest-rate contracts 1,527 160 – 1,687 1,726 43 170 22 –

Exchange-traded products

Interest-rate futures 7,941 846 – 8,787 9,637 1 – 1 –

CurrEnCy-linkEd COntraCts 55,915 6,165 251 62,331 64,447 612 576 549 634

OtC products

Forward forex transactions 47,592 3,654 216 51,462 53,676 582 517 500 555

Forex options – call 4,051 1,224 – 5,275 5,492 14 38 21 22

Forex options – put 4,021 1,224 – 5,245 4,969 16 20 18 51

Exchange-traded products

Forex futures 72 – – 72 42 – – – –

Forex options 179 63 35 277 268 – 1 10 6

sharE-/indEx-linkEd COntraCts 11,162 7,451 1,155 19,768 23,344 535 552 718 928

OtC products

Share/index options – call 423 207 27 657 604 80 62 – –

Share/index options – put 58 182 – 240 136 2 – 33 25

Other share/index contracts 1,163 3,143 859 5,165 5,316 106 86 126 141

Exchange-traded products

Share/index futures 640 6 – 646 483 4 – – –

Share/index options 8,878 3,913 269 13,060 16,805 343 404 559 762

OthEr COntraCts 13,465 30,514 17,124 61,103 65,717 1,084 888 672 1,110

OtC products

Cross-currency swaps 10,329 22,561 6,903 39,793 44,252 1,057 825 640 1,056

Precious metal contracts – 8 – 8 24 – 2 1 1

Commodities contracts 430 660 20 1,110 1,591 19 58 7 19

Other contracts 2,247 7,263 10,179 19,689 19,269 – – 8 6

Exchange-traded products

Futures 99 9 – 108 129 – – – –

Options 360 13 22 395 452 8 3 16 28

CrEdit dErivativEs 8,943 30,855 2,902 42,700 60,793 414 661 288 599

protection buyer

Credit default swaps 4,209 13,985 947 19,141 27,918 131 390 169 192

protection seller

Credit default swaps 4,734 16,870 1,730 23,334 32,510 272 249 115 387

total return swaps – – 225 225 365 11 22 4 20

total 236,909 413,851 295,146 945,906 968,733 23,145 37,831 22,760 39,989

282 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

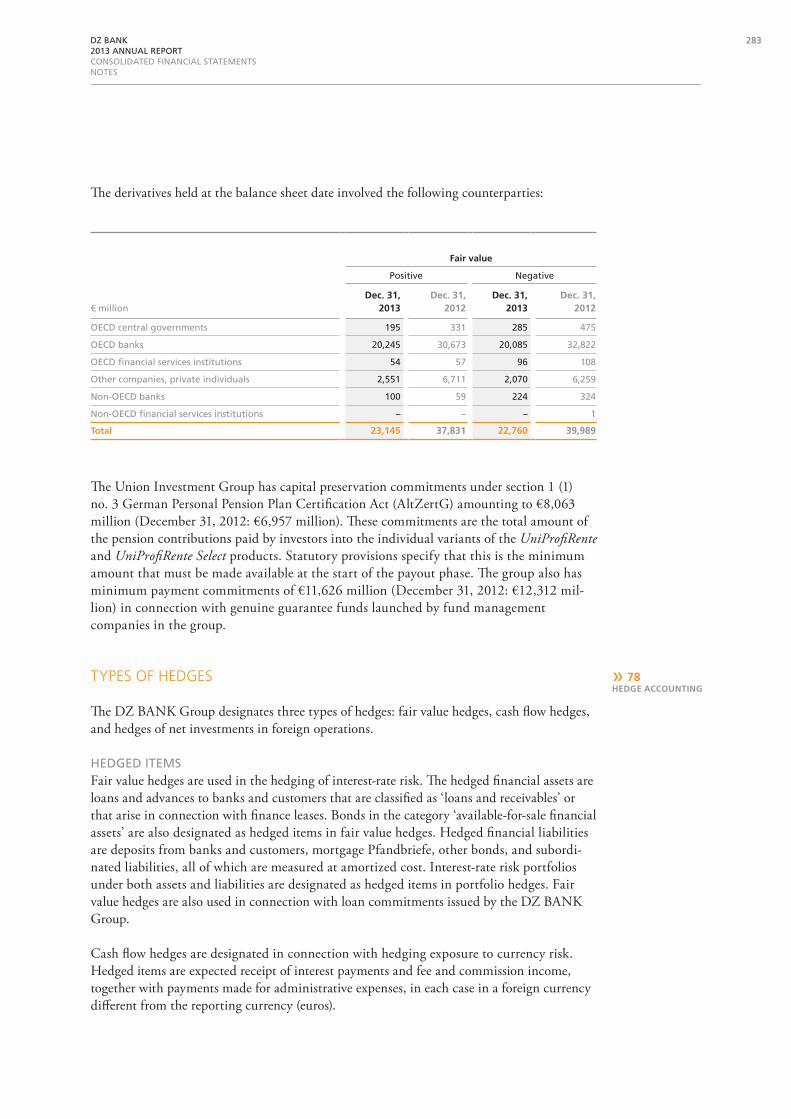

The derivatives held at the balance sheet date involved the following counterparties:

fair value

Positive Negative

€ milliondec. 31,

2013dec. 31,

2012dec. 31,

2013dec. 31,

2012

OECD central governments 195 331 285 475

OECD banks 20,245 30,673 20,085 32,822

OECD financial services institutions 54 57 96 108

Other companies, private individuals 2,551 6,711 2,070 6,259

Non-OECD banks 100 59 224 324

Non-OECD financial services institutions – – – 1

total 23,145 37,831 22,760 39,989

The Union Investment Group has capital preservation commitments under section 1 (1) no. 3 German Personal Pension Plan Certification Act (AltZertG) amounting to €8,063 million (December 31, 2012: €6,957 million). These commitments are the total amount of the pension contributions paid by investors into the individual variants of the UniProfiRente and UniProfiRente Select products. Statutory provisions specify that this is the minimum amount that must be made available at the start of the payout phase. The group also has minimum payment commitments of €11,626 million (December 31, 2012: €12,312 mil-lion) in connection with genuine guarantee funds launched by fund management companies in the group.

typeS of hedgeS

The DZ BANK Group designates three types of hedges: fair value hedges, cash flow hedges, and hedges of net investments in foreign operations.

HEDGED ItEmSFair value hedges are used in the hedging of interest-rate risk. The hedged financial assets are loans and advances to banks and customers that are classified as ‘loans and receivables’ or that arise in connection with finance leases. Bonds in the category ‘available-for-sale financial assets’ are also designated as hedged items in fair value hedges. Hedged financial liabilities are deposits from banks and customers, mortgage Pfandbriefe, other bonds, and subordi-nated liabilities, all of which are measured at amortized cost. Interest-rate risk portfolios under both assets and liabilities are designated as hedged items in portfolio hedges. Fair value hedges are also used in connection with loan commitments issued by the DZ BANK Group.

Cash flow hedges are designated in connection with hedging exposure to currency risk. Hedged items are expected receipt of interest payments and fee and commission income, together with payments made for administrative expenses, in each case in a foreign currency different from the reporting currency (euros).

» 78hEdgE aCCOunting

283DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

Hedges of net investments in foreign operations are designated in connection with hedging exposure to currency risk. The hedged items are interests in joint ventures and investments in associates accounted for using the equity method and denominated in foreign currency.

HEDGING INStRumENtSInterest-rate swaps and swaptions are designated as hedging instruments in fair value hedges of financial assets and financial liabilities.

Forward forex transactions are used as hedging instruments in cash flow hedges and hedges of net investments in foreign operations.

ASSESSmENt OF HEDGE EFFECtIvENESSThe prerequisite for recognizing a hedge under IAS 39 is that the hedge must be highly effective on both a prospective and retrospective basis. Highly effective in this case means that the changes in fair value or expected cash flows for the hedged items must be offset by the changes in fair value or expected cash flows for the hedging instruments within a range of 80 percent to 125 percent specified by IAS 39. Hedge effectiveness must be assessed and documented at every balance sheet date as a minimum. If this assessment identifies that a hedge has not achieved the required effectiveness, the hedge must be reversed retrospectively to the balance sheet date of the last assessment in which the hedge was found to be effective.

In the case of fair value hedges, prospective effectiveness is assessed by using sensitivity analyses (based on the basis point value method), the dollar offset method, a noise threshold value, and linear regression analysis. Retrospective effectiveness is assessed primarily by using the dollar offset method, a noise threshold value, and linear regression analysis. In these methods, the cumulative changes in the fair value of the hedged items attributable to the hedged risk are compared with the changes in the fair value of the hedging instruments.

When assessing the retrospective and prospective effectiveness of cash flow hedges, the changes in the present value of the expected or actual cash flows for the hedged item are compared against the change in the fair value of the hedging instrument.

The prospective effectiveness of hedges of net investments in foreign operations is assessed by means of sensitivity analyses. The dollar offset method is used for the retrospective assessment of effectiveness.

284 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

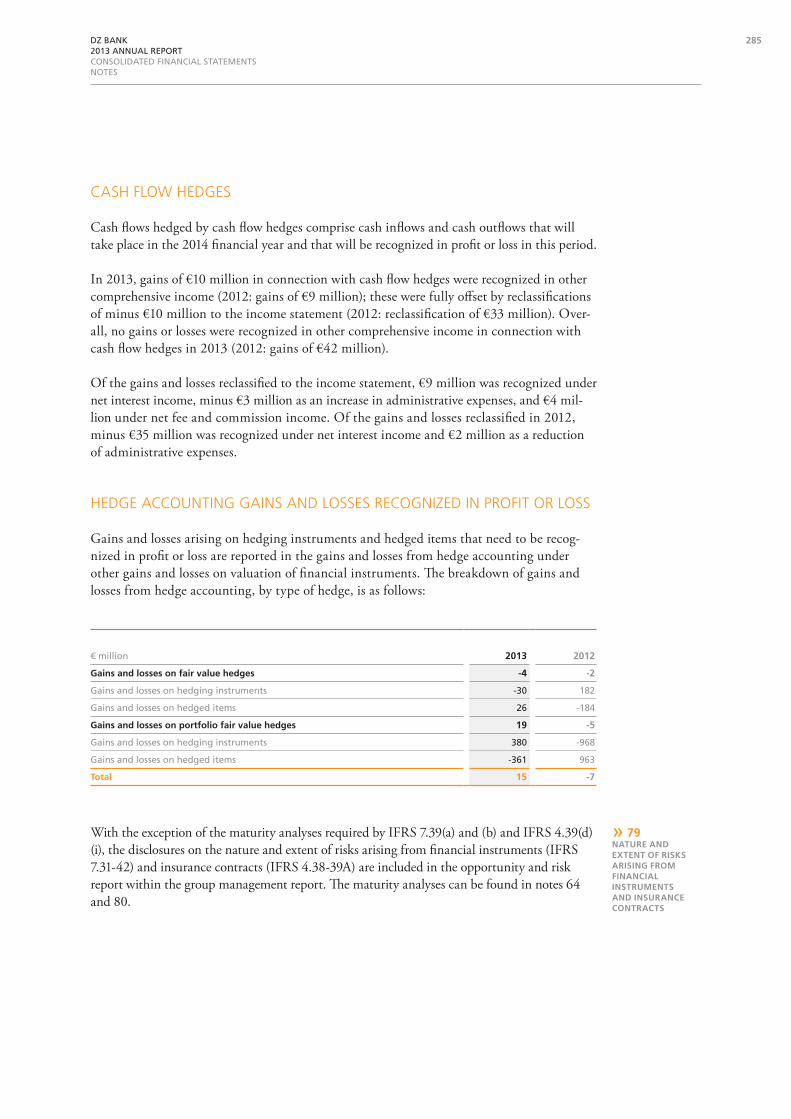

caSh flow hedgeS

Cash flows hedged by cash flow hedges comprise cash inflows and cash outflows that will take place in the 2014 financial year and that will be recognized in profit or loss in this period.

In 2013, gains of €10 million in connection with cash flow hedges were recognized in other comprehensive income (2012: gains of €9 million); these were fully offset by reclassifications of minus €10 million to the income statement (2012: reclassification of €33 million). Over-all, no gains or losses were recognized in other comprehensive income in connection with cash flow hedges in 2013 (2012: gains of €42 million).

Of the gains and losses reclassified to the income statement, €9 million was recognized under net interest income, minus €3 million as an increase in administrative expenses, and €4 mil-lion under net fee and commission income. Of the gains and losses reclassified in 2012, minus €35 million was recognized under net interest income and €2 million as a reduction of administrative expenses.

hedge accounting gainS and loSSeS recognized in profit or loSS

Gains and losses arising on hedging instruments and hedged items that need to be recog-nized in profit or loss are reported in the gains and losses from hedge accounting under other gains and losses on valuation of financial instruments. The breakdown of gains and losses from hedge accounting, by type of hedge, is as follows:

€ million 2013 2012

gains and losses on fair value hedges -4 -2

Gains and losses on hedging instruments -30 182

Gains and losses on hedged items 26 -184

gains and losses on portfolio fair value hedges 19 -5

Gains and losses on hedging instruments 380 -968

Gains and losses on hedged items -361 963

total 15 -7

With the exception of the maturity analyses required by IFRS 7.39(a) and (b) and IFRS 4.39(d)(i), the disclosures on the nature and extent of risks arising from financial instruments (IFRS 7.31-42) and insurance contracts (IFRS 4.38-39A) are included in the opportunity and risk report within the group management report. The maturity analyses can be found in notes 64 and 80.

» 79naturE and ExtEnt Of risks arising frOm finanCial instrumEnts and insuranCE COntraCts

285DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

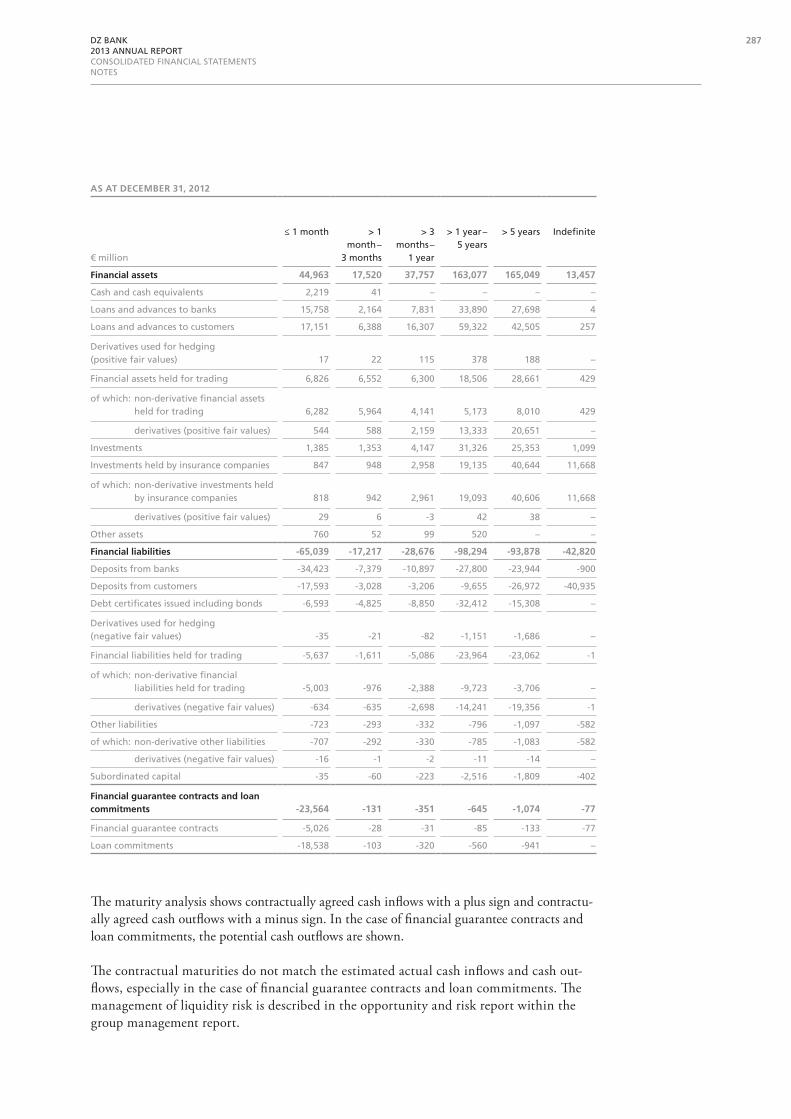

» 80maturity analysis

as at dECEmbEr 31, 2013

€ million

≤ 1 month > 1 month –

3 months

> 3 months –

1 year

> 1 year – 5 years

> 5 years Indefinite

financial assets 39,927 19,888 37,931 152,885 158,831 13,384

Cash and cash equivalents 3,520 4 – – – –

Loans and advances to banks 11,275 2,973 7,717 31,941 27,178 30

Loans and advances to customers 16,250 5,953 15,372 56,953 44,980 47

Derivatives used for hedging (positive fair values) 18 20 116 445 269 –

Financial assets held for trading 5,289 8,561 7,137 15,080 17,776 975

of which: non-derivative financial assets held for trading 4,864 8,009 5,119 4,834 6,928 975

derivatives (positive fair values) 425 552 2,018 10,246 10,848 –

Investments 1,260 1,253 4,586 27,243 25,191 1,518

Investments held by insurance companies 1,150 1,112 2,947 20,618 43,437 10,813

of which: non-derivative investments held by insurance companies 1,136 1,085 2,939 20,539 43,367 10,813

derivatives (positive fair values) 14 27 8 79 70 –

Other assets 1,165 12 56 605 – 1

financial liabilities -67,458 -15,708 -23,196 -87,652 -75,342 -47,603

Deposits from banks -28,576 -6,608 -10,125 -26,473 -22,488 -1,013

Deposits from customers -23,072 -3,167 -2,835 -9,152 -23,571 -45,010

Debt certificates issued including bonds -6,969 -3,404 -4,919 -28,660 -13,427 –

Derivatives used for hedging (negative fair values) -25 -18 -84 -1,262 -943 –

Financial liabilities held for trading -8,264 -2,143 -4,920 -18,357 -11,863 -589

of which: non-derivative financial liabilities held for trading -7,758 -1,521 -2,678 -9,661 -3,240 -586

derivatives (negative fair values) -506 -622 -2,242 -8,696 -8,623 -3

Other liabilities -535 -335 -311 -1,104 -1,152 -580

of which: non-derivative other liabilities -533 -330 -311 -1,090 -1,137 -580

derivatives (negative fair values) -2 -5 – -14 -15 –

Subordinated capital -17 -33 -2 -2,644 -1,898 -411

financial guarantee contracts and loan commitments -23,061 -109 -197 -612 -955 -61

Financial guarantee contracts -4,816 -40 -2 -147 -91 -61

Loan commitments -18,245 -69 -195 -465 -864 –

286 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

as at dECEmbEr 31, 2012

€ million

≤ 1 month > 1 month –

3 months

> 3 months –

1 year

> 1 year – 5 years

> 5 years Indefinite

financial assets 44,963 17,520 37,757 163,077 165,049 13,457

Cash and cash equivalents 2,219 41 – – – –

Loans and advances to banks 15,758 2,164 7,831 33,890 27,698 4

Loans and advances to customers 17,151 6,388 16,307 59,322 42,505 257

Derivatives used for hedging (positive fair values) 17 22 115 378 188 –

Financial assets held for trading 6,826 6,552 6,300 18,506 28,661 429

of which: non-derivative financial assets held for trading 6,282 5,964 4,141 5,173 8,010 429

derivatives (positive fair values) 544 588 2,159 13,333 20,651 –

Investments 1,385 1,353 4,147 31,326 25,353 1,099

Investments held by insurance companies 847 948 2,958 19,135 40,644 11,668

of which: non-derivative investments held by insurance companies 818 942 2,961 19,093 40,606 11,668

derivatives (positive fair values) 29 6 -3 42 38 –

Other assets 760 52 99 520 – –

financial liabilities -65,039 -17,217 -28,676 -98,294 -93,878 -42,820

Deposits from banks -34,423 -7,379 -10,897 -27,800 -23,944 -900

Deposits from customers -17,593 -3,028 -3,206 -9,655 -26,972 -40,935

Debt certificates issued including bonds -6,593 -4,825 -8,850 -32,412 -15,308 –

Derivatives used for hedging (negative fair values) -35 -21 -82 -1,151 -1,686 –

Financial liabilities held for trading -5,637 -1,611 -5,086 -23,964 -23,062 -1

of which: non-derivative financial liabilities held for trading -5,003 -976 -2,388 -9,723 -3,706 –

derivatives (negative fair values) -634 -635 -2,698 -14,241 -19,356 -1

Other liabilities -723 -293 -332 -796 -1,097 -582

of which: non-derivative other liabilities -707 -292 -330 -785 -1,083 -582

derivatives (negative fair values) -16 -1 -2 -11 -14 –

Subordinated capital -35 -60 -223 -2,516 -1,809 -402

financial guarantee contracts and loan commitments -23,564 -131 -351 -645 -1,074 -77

Financial guarantee contracts -5,026 -28 -31 -85 -133 -77

Loan commitments -18,538 -103 -320 -560 -941 –

The maturity analysis shows contractually agreed cash inflows with a plus sign and contractu-ally agreed cash outflows with a minus sign. In the case of financial guarantee contracts and loan commitments, the potential cash outflows are shown.

The contractual maturities do not match the estimated actual cash inflows and cash out-flows, especially in the case of financial guarantee contracts and loan commitments. The management of liquidity risk is described in the opportunity and risk report within the group management report.

287DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

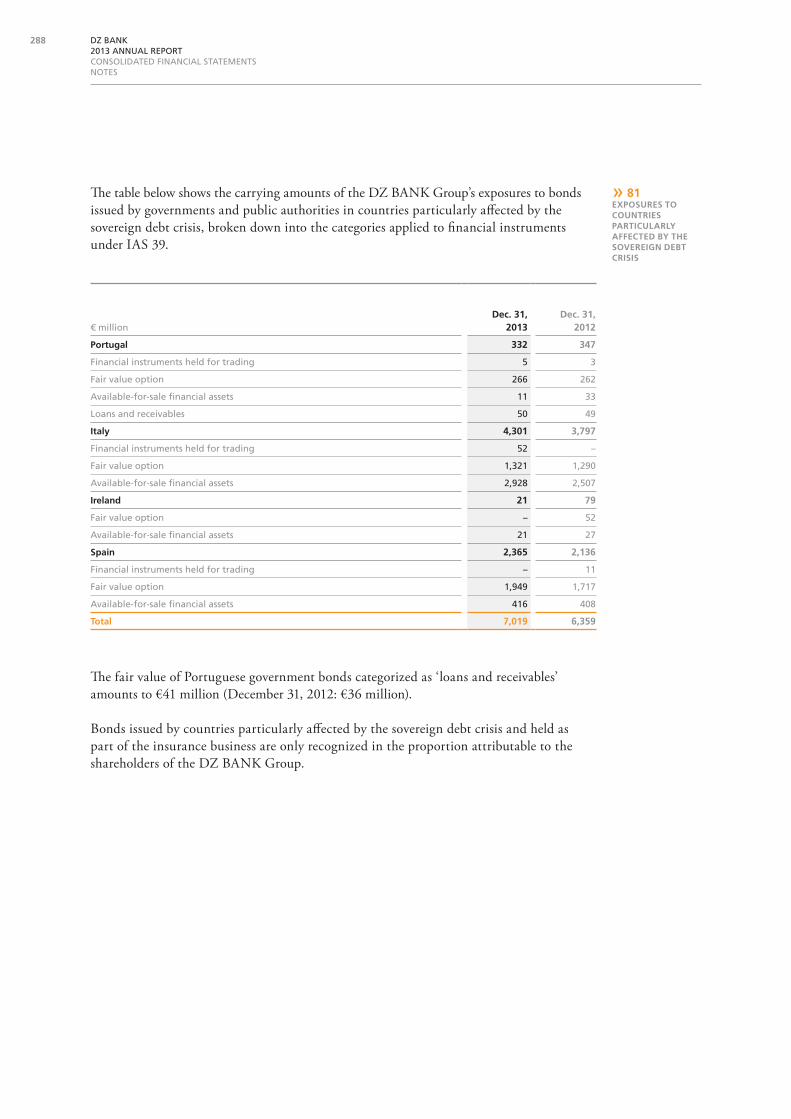

The table below shows the carrying amounts of the DZ BANK Group’s exposures to bonds issued by governments and public authorities in countries particularly affected by the sovereign debt crisis, broken down into the categories applied to financial instruments under IAS 39.

» 81ExpOsurEs tO COuntriEs partiCularly affECtEd by thE sOvErEign dEbt Crisis

The fair value of Portuguese government bonds categorized as ‘loans and receivables’ amounts to €41 million (December 31, 2012: €36 million).

Bonds issued by countries particularly affected by the sovereign debt crisis and held as part of the insurance business are only recognized in the proportion attributable to the shareholders of the DZ BANK Group.

€ milliondec. 31,

2013dec. 31,

2012

portugal 332 347

Financial instruments held for trading 5 3

Fair value option 266 262

Available-for-sale financial assets 11 33

Loans and receivables 50 49

italy 4,301 3,797

Financial instruments held for trading 52 –

Fair value option 1,321 1,290

Available-for-sale financial assets 2,928 2,507

ireland 21 79

Fair value option – 52

Available-for-sale financial assets 21 27

spain 2,365 2,136

Financial instruments held for trading – 11

Fair value option 1,949 1,717

Available-for-sale financial assets 416 408

total 7,019 6,359

288 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

Fair value hierarchy

The recurring fair value measurements as measured and recognized on the balance sheet are assigned to the levels of the fair value hierarchy as follows:

Level 1 Level 2 Level 3

€ millionDec. 31,

2013Dec. 31,

2012Dec. 31,

2013Dec. 31,

2012Dec. 31,

2013Dec. 31,

2012

Portugal 277 298 5 – – –

Financial instruments held for trading – 3 5 – – –

Fair value option 266 262 – – – –

Available-for-sale financial assets 11 33 – – – –

Italy 3,082 2,970 1,185 827 34 –

Financial instruments held for trading – – 52 – – –

Fair value option 931 897 390 393 – –

Available-for-sale financial assets 2,151 2,073 743 434 34 –

Ireland 21 79 – – – –

Fair value option – 52 – – – –

Available-for-sale financial assets 21 27 – – – –

Spain 806 731 1,520 1,405 39 –

Financial instruments held for trading – – – 11 – –

Fair value option 753 670 1,196 1,047 – –

Available-for-sale financial assets 53 61 324 347 39 –

Total 4,186 4,078 2,710 2,232 73 –

impairment

No impairment losses were recognized to cover exposures in respect of the bonds from other countries particularly affected by the sovereign debt crisis (Portugal, Italy, Ireland, and Spain) because there was insufficient objective evidence of impairment.

289DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES

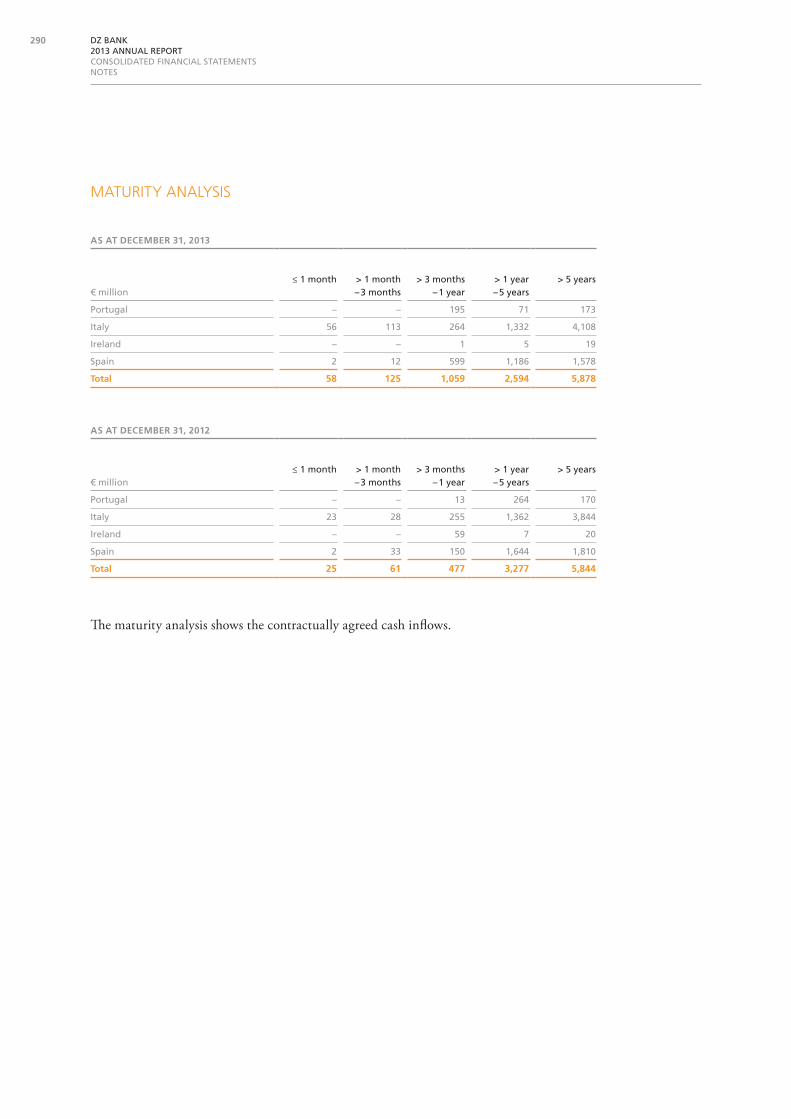

maturity analysis

AS AT December 31, 2013

€ million≤ 1 month > 1 month

– 3 months> 3 months

– 1 year> 1 year – 5 years

> 5 years

Portugal – – 195 71 173

Italy 56 113 264 1,332 4,108

Ireland – – 1 5 19

Spain 2 12 599 1,186 1,578

Total 58 125 1,059 2,594 5,878

AS AT December 31, 2012

€ million≤ 1 month > 1 month

– 3 months> 3 months

– 1 year> 1 year – 5 years

> 5 years

Portugal – – 13 264 170

Italy 23 28 255 1,362 3,844

Ireland – – 59 7 20

Spain 2 33 150 1,644 1,810

Total 25 61 477 3,277 5,844

The maturity analysis shows the contractually agreed cash inflows.

290 DZ BANK 2013 ANNUAL REPORTCONSOLIDATED FINANCIAL STATEMENTSNOTES