Embed Size (px)

Citation preview

CTP NewsAs usual, there is a lot to report on in the CTP space! In this edition of CTP News, along with our usual examination of premium rate movements and cases of interest, we report on the NSW Law and Justice Review, privatisation plans in SA and the new WA lifetime care scheme.

In this edition, we:

>> Discuss claim farming, which has the potential to drive

up costs, and therefore premiums

>> Update you on premium rates and affordability – mostly

small movements, except NZ

>> Report on developments across the CTP jurisdictions.

We also highlight recent court cases of interest, including

one from the High Court.

d’finitiveKeeping you informed. AUGUST 2015

[ accident compensation ]

Please contact one of our CTP experts if you have any questions or comments about this d’finitive, or to learn more about Finity’s CTP offering. Alternatively, read more at finity.com.au.

2015 Winner - Professional Services Firm of the Year

6 times winner Australian & New Zealand Insurance Industry Award ‘Service Provider of the Year’

Australian Insurance Industry Awards – Inaugural Inductee into the Hall of Fame

finity.com.au

Sydney +61 2 8252 3300 Auckland +64 9 306 7700 Melbourne +61 3 8080 0900

2 d’finitive AUGUST 2015

Claim Farming – What is it and is it a problem for CTP?Claim farming is a practice where third party intermediaries encourage individuals to make insurance claims, and then ‘sell’ these claims on to lawyers or claims management companies.

In the UK, a rising number of unsolicited approaches from ‘claim farmers’ (including phone calls and text messages) led to 2013 legislation which, in effect, banned referral fees. Such fees (of up to £800 per referral!) were believed to be encouraging false claims and contributing to escalating insurance premiums.

In Australia, there have been recent reports of claim farming within the CTP industry. CTP regulators have issued warnings in respect of:

>> Members of the public being ‘cold called’ and asked to provide or confirm personal information about their involvement in a motor vehicle accident

>> Callers fraudulently telling motorists that they are owed money for motor accident claims and asking for bank account details

>> Callers falsely associating themselves with government agencies, legal firms and insurance companies

>> Callers encouraging motorists to lodge fraudulent claims with CTP insurers.

The obvious concern is that claim farming will add to transaction costs, encourage unmeritorious claims and ultimately increase premiums for all motorists.

Although there are no industry statistics to indicate how widespread the problem may be, we have observed an increase in claim frequency in NSW that may be at least partly related to such activities. We note that the following regulatory constraints are in place:

>> NSW’s Motor Accidents Compensation Regulation 2015, effective 1 April 2015, deals with legal costs and, in effect, bans referral fees for CTP claims.

>> Queensland’s Personal Injury Proceedings Act 2002 prohibits legal firms from touting or cold calling motorists involved in motor vehicle accidents, and from encouraging claims for CTP compensation.

It will be interesting to see whether the new NSW regulatory provisions, along with community awareness campaigns in NSW and Queensland, will reduce claim frequency.

Is claim farming driving up claim frequency?

FIGURE 1 – CTP RATES AT JULY 2015: STANDARD MOTOR CAR

AUGUST 2015 d’finitive 3

Update on Premiums

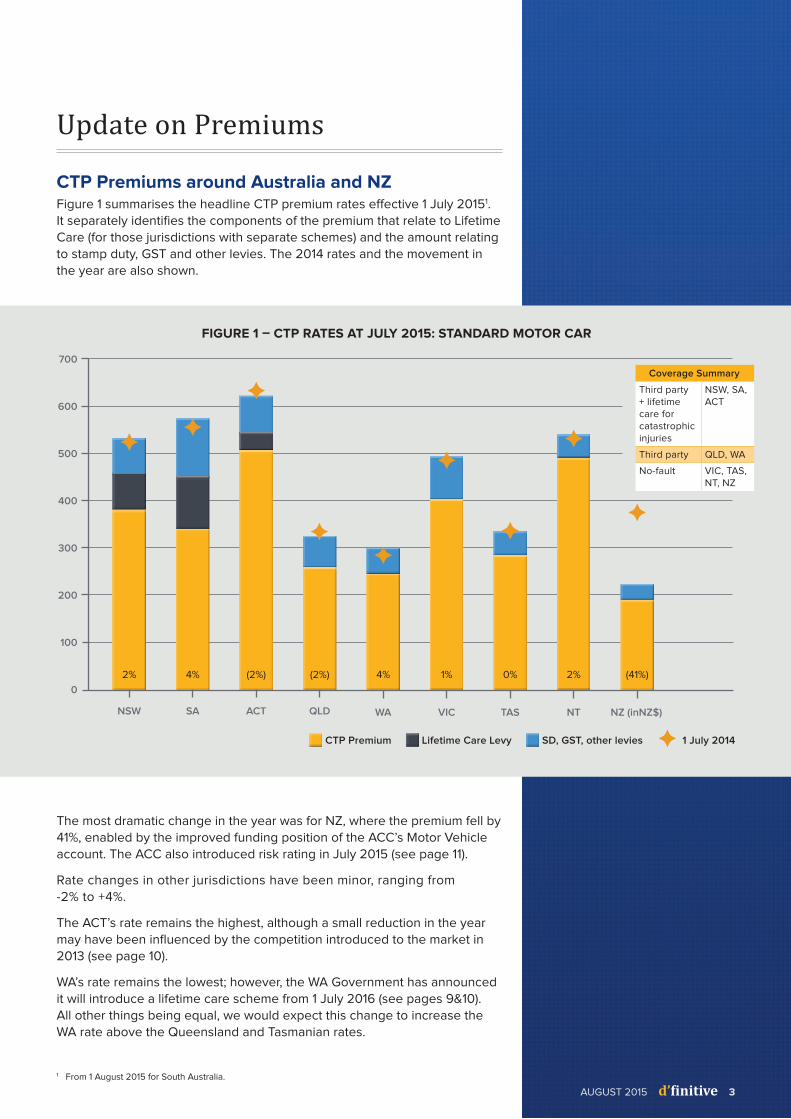

CTP Premiums around Australia and NZFigure 1 summarises the headline CTP premium rates effective 1 July 20151. It separately identifies the components of the premium that relate to Lifetime Care (for those jurisdictions with separate schemes) and the amount relating to stamp duty, GST and other levies. The 2014 rates and the movement in the year are also shown.

1 From 1 August 2015 for South Australia.

700

600

500

400

300

200

100

0

CTP Premium Lifetime Care Levy SD, GST, other levies F 1 July 2014

The most dramatic change in the year was for NZ, where the premium fell by 41%, enabled by the improved funding position of the ACC’s Motor Vehicle account. The ACC also introduced risk rating in July 2015 (see page 11).

Rate changes in other jurisdictions have been minor, ranging from -2% to +4%.

The ACT’s rate remains the highest, although a small reduction in the year may have been influenced by the competition introduced to the market in 2013 (see page 10).

WA’s rate remains the lowest; however, the WA Government has announced it will introduce a lifetime care scheme from 1 July 2016 (see pages 9&10). All other things being equal, we would expect this change to increase the WA rate above the Queensland and Tasmanian rates.

NSW SA ACT QLD WA VIC TAS NT NZ (inNZ$)

2% 4% (2%) (2%) 4% 1% 0% 2% (41%)

Coverage Summary

Third party + lifetime care for catastrophic injuries

NSW, SA, ACT

Third party QLD, WA

No-fault VIC, TAS, NT, NZ

FF

F

FF

F

F

F

F

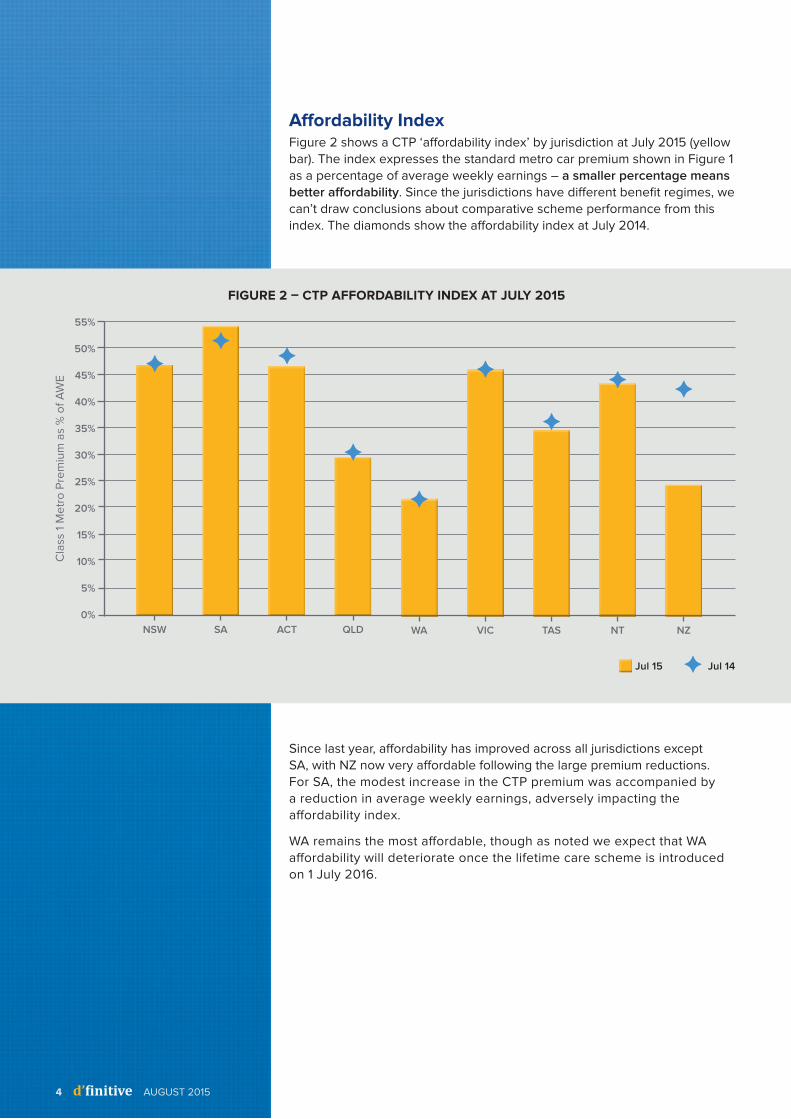

Affordability IndexFigure 2 shows a CTP ‘affordability index’ by jurisdiction at July 2015 (yellow bar). The index expresses the standard metro car premium shown in Figure 1 as a percentage of average weekly earnings – a smaller percentage means better affordability. Since the jurisdictions have different benefit regimes, we can’t draw conclusions about comparative scheme performance from this index. The diamonds show the affordability index at July 2014.

4 d’finitive AUGUST 2015

FIGURE 2 – CTP AFFORDABILITY INDEX AT JULY 2015

55%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Jul 15 F Jul 14

Since last year, affordability has improved across all jurisdictions except SA, with NZ now very affordable following the large premium reductions. For SA, the modest increase in the CTP premium was accompanied by a reduction in average weekly earnings, adversely impacting the affordability index.

WA remains the most affordable, though as noted we expect that WA affordability will deteriorate once the lifetime care scheme is introduced on 1 July 2016.

Cla

ss 1

Me

tro

Pre

miu

m a

s %

of

AW

E

NSW

F

SA

F

ACT

F

QLD

F

WA

F

VIC

F

TAS

F

NT

F

NZ

F

Jurisdiction Roundup

New South Wales

A new independent insurance regulator

In early August 2015, the NSW Government announced its plan to reform its insurance operations. Most of the changes relate to workers’ compensation, but there are two key changes that will impact on CTP:

>> There will be a new independent insurance regulator, the State Insurance Regulatory Authority (SIRA). SIRA will assume the regulatory functions of the MAA in relation to CTP, as well as regulation of workers’ compensation and home building compensation. The MAA will be abolished if the proposed Act is passed.

>> The Lifetime Care and Support Authority will come under the banner of a new agency, Insurance and Care NSW (ICNSW). ICNSW will also oversee the areas currently managed by the WorkCover Nominal Insurer, the Dust Diseases Authority, SICorp and the Sporting Injuries Compensation Authority.

Further details can be found here: insurancereforms.nsw.gov.au

Premium increases for some insurers

Figure 3 shows the premium rates for a ‘model driver’ at August 2015 compared to February 2015.

AUGUST 2015 d’finitive 5

Revised cost regulations now in-forceIn the March 2015 edition of CTP News, we discussed the then-proposed changes to the NSW cost regulations. The changes have now been passed, and the Motor Accidents Compensation Regulation 2015 commenced on 1 April 2015.

Since February, QBE, Zurich and the two Allianz brands have all increased premiums by 4% or around $20. The Suncorp and IAG prices are unchanged.

After QBE’s rate rise, the two Suncorp brands AAMI and GIO are the cheapest; Zurich remains the most expensive. The range between the highest and lowest premiums has widened from $77 to $98.

Su

nco

rp

Feb 15 Aug 15

$0 $400 $500 $600

FIGURE 3 – NSW CLASS 1 METRO PREMIUMS

Allianz

CIC-Allianz

AAMI

GIO

NRMA

QBE

Zurich

Alli

an

zIA

G

6 d’finitive AUGUST 2015

Law & Justice Review of CTP

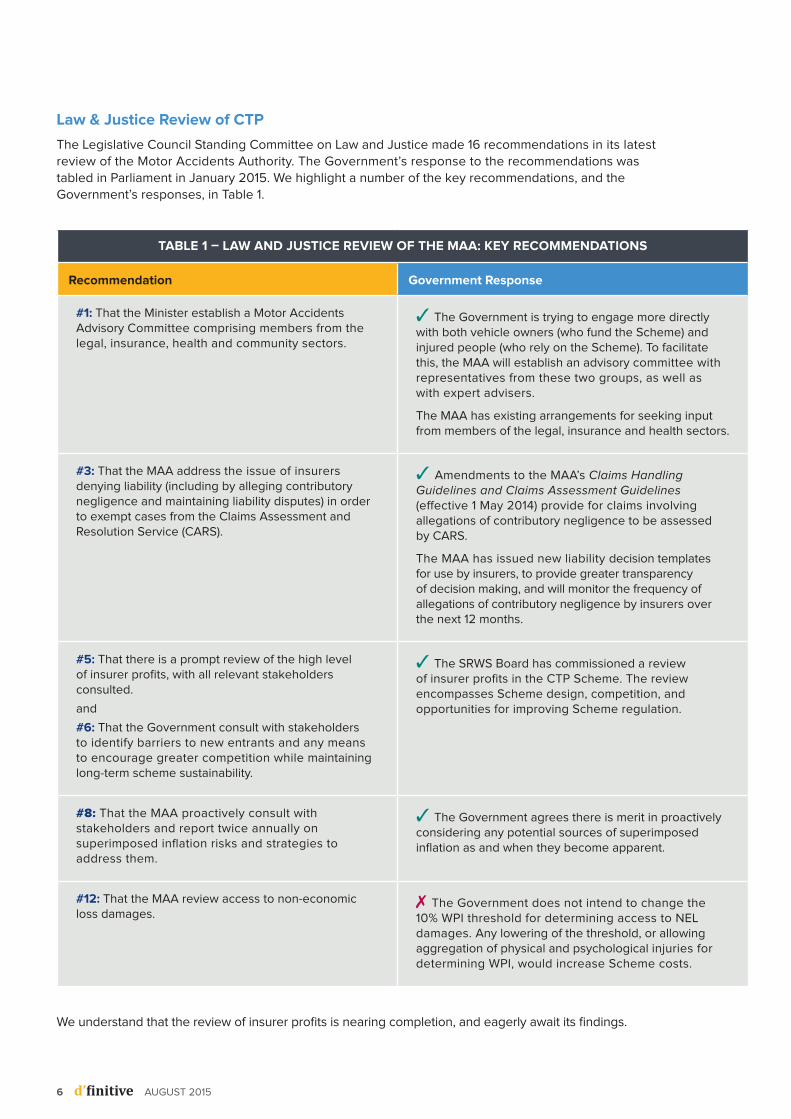

The Legislative Council Standing Committee on Law and Justice made 16 recommendations in its latest review of the Motor Accidents Authority. The Government’s response to the recommendations was tabled in Parliament in January 2015. We highlight a number of the key recommendations, and the Government’s responses, in Table 1.

TABLE 1 – LAW AND JUSTICE REVIEW OF THE MAA: KEY RECOMMENDATIONS

Recommendation Government Response

#1: That the Minister establish a Motor Accidents Advisory Committee comprising members from the legal, insurance, health and community sectors.

✓ The Government is trying to engage more directly with both vehicle owners (who fund the Scheme) and injured people (who rely on the Scheme). To facilitate this, the MAA will establish an advisory committee with representatives from these two groups, as well as with expert advisers.

The MAA has existing arrangements for seeking input from members of the legal, insurance and health sectors.

#3: That the MAA address the issue of insurers denying liability (including by alleging contributory negligence and maintaining liability disputes) in order to exempt cases from the Claims Assessment and Resolution Service (CARS).

✓ Amendments to the MAA’s Claims Handling Guidelines and Claims Assessment Guidelines (effective 1 May 2014) provide for claims involving allegations of contributory negligence to be assessed by CARS.

The MAA has issued new liability decision templates for use by insurers, to provide greater transparency of decision making, and will monitor the frequency of allegations of contributory negligence by insurers over the next 12 months.

#5: That there is a prompt review of the high level of insurer profits, with all relevant stakeholders consulted.

and

#6: That the Government consult with stakeholders to identify barriers to new entrants and any means to encourage greater competition while maintaining long-term scheme sustainability.

✓ The SRWS Board has commissioned a review of insurer profits in the CTP Scheme. The review encompasses Scheme design, competition, and opportunities for improving Scheme regulation.

#8: That the MAA proactively consult with stakeholders and report twice annually on superimposed inflation risks and strategies to address them.

✓ The Government agrees there is merit in proactively considering any potential sources of superimposed inflation as and when they become apparent.

#12: That the MAA review access to non-economic loss damages.

✗ The Government does not intend to change the 10% WPI threshold for determining access to NEL damages. Any lowering of the threshold, or allowing aggregation of physical and psychological injuries for determining WPI, would increase Scheme costs.

We understand that the review of insurer profits is nearing completion, and eagerly await its findings.

4

32

1

0

56

78

9

10

AUGUST 2015 d’finitive 7

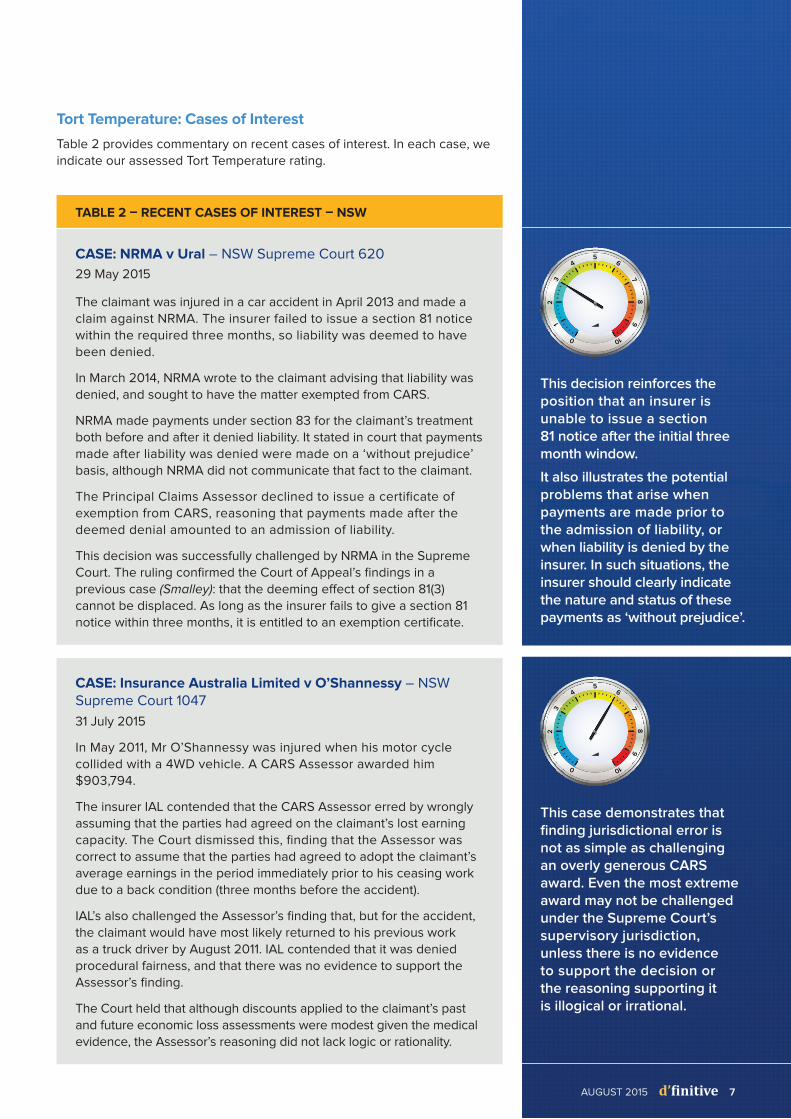

Tort Temperature: Cases of Interest

Table 2 provides commentary on recent cases of interest. In each case, we indicate our assessed Tort Temperature rating.

TABLE 2 – RECENT CASES OF INTEREST – NSW

CASE: NRMA v Ural – NSW Supreme Court 620

29 May 2015

The claimant was injured in a car accident in April 2013 and made a claim against NRMA. The insurer failed to issue a section 81 notice within the required three months, so liability was deemed to have been denied.

In March 2014, NRMA wrote to the claimant advising that liability was denied, and sought to have the matter exempted from CARS.

NRMA made payments under section 83 for the claimant’s treatment both before and after it denied liability. It stated in court that payments made after liability was denied were made on a ‘without prejudice’ basis, although NRMA did not communicate that fact to the claimant.

The Principal Claims Assessor declined to issue a certificate of exemption from CARS, reasoning that payments made after the deemed denial amounted to an admission of liability.

This decision was successfully challenged by NRMA in the Supreme Court. The ruling confirmed the Court of Appeal’s findings in a previous case (Smalley): that the deeming effect of section 81(3) cannot be displaced. As long as the insurer fails to give a section 81 notice within three months, it is entitled to an exemption certificate.

CASE: Insurance Australia Limited v O’Shannessy – NSW Supreme Court 1047

31 July 2015

In May 2011, Mr O’Shannessy was injured when his motor cycle collided with a 4WD vehicle. A CARS Assessor awarded him $903,794.

The insurer IAL contended that the CARS Assessor erred by wrongly assuming that the parties had agreed on the claimant’s lost earning capacity. The Court dismissed this, finding that the Assessor was correct to assume that the parties had agreed to adopt the claimant’s average earnings in the period immediately prior to his ceasing work due to a back condition (three months before the accident).

IAL’s also challenged the Assessor’s finding that, but for the accident, the claimant would have most likely returned to his previous work as a truck driver by August 2011. IAL contended that it was denied procedural fairness, and that there was no evidence to support the Assessor’s finding.

The Court held that although discounts applied to the claimant’s past and future economic loss assessments were modest given the medical evidence, the Assessor’s reasoning did not lack logic or rationality.

4

32

1

0

56

78

9

10

This decision reinforces the position that an insurer is unable to issue a section 81 notice after the initial three month window.

It also illustrates the potential problems that arise when payments are made prior to the admission of liability, or when liability is denied by the insurer. In such situations, the insurer should clearly indicate the nature and status of these payments as ‘without prejudice’.

This case demonstrates that finding jurisdictional error is not as simple as challenging an overly generous CARS award. Even the most extreme award may not be challenged under the Supreme Court’s supervisory jurisdiction, unless there is no evidence to support the decision or the reasoning supporting it is illogical or irrational.

8 d’finitive AUGUST 2015

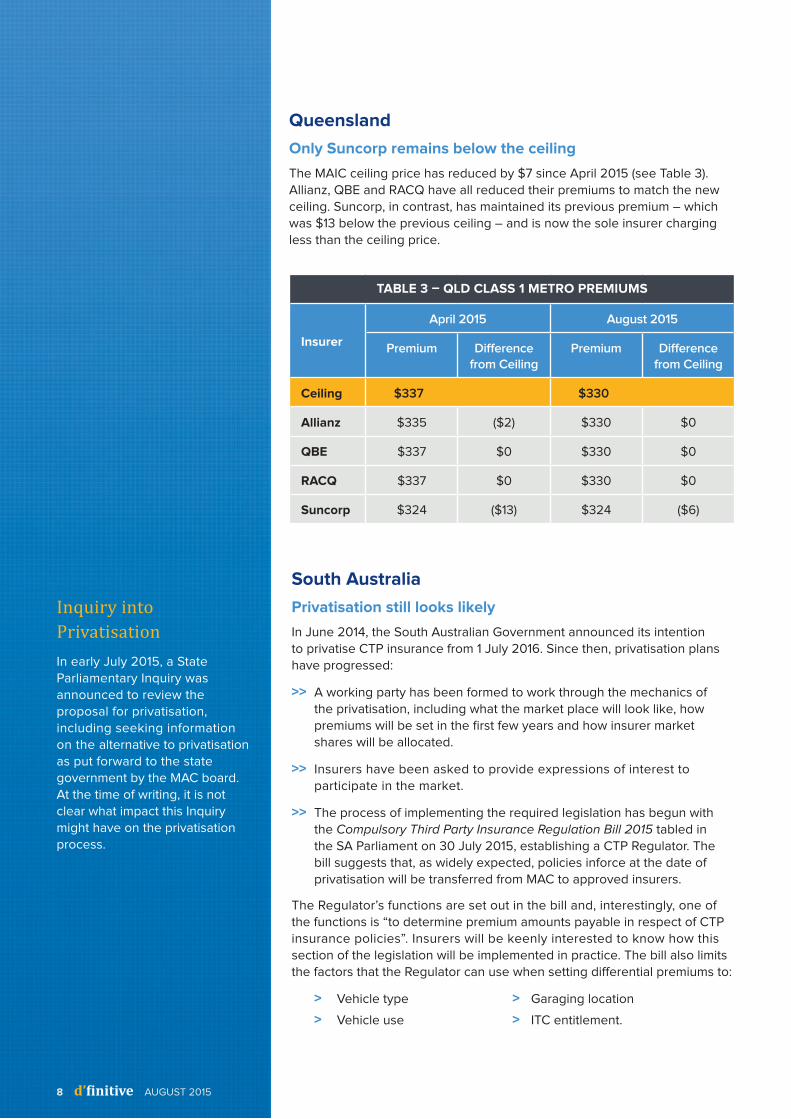

Queensland

Only Suncorp remains below the ceiling

The MAIC ceiling price has reduced by $7 since April 2015 (see Table 3). Allianz, QBE and RACQ have all reduced their premiums to match the new ceiling. Suncorp, in contrast, has maintained its previous premium – which was $13 below the previous ceiling – and is now the sole insurer charging less than the ceiling price.

South Australia

Privatisation still looks likely

In June 2014, the South Australian Government announced its intention to privatise CTP insurance from 1 July 2016. Since then, privatisation plans have progressed:

>> A working party has been formed to work through the mechanics of the privatisation, including what the market place will look like, how premiums will be set in the first few years and how insurer market shares will be allocated.

>> Insurers have been asked to provide expressions of interest to participate in the market.

>> The process of implementing the required legislation has begun with the Compulsory Third Party Insurance Regulation Bill 2015 tabled in the SA Parliament on 30 July 2015, establishing a CTP Regulator. The bill suggests that, as widely expected, policies inforce at the date of privatisation will be transferred from MAC to approved insurers.

The Regulator’s functions are set out in the bill and, interestingly, one of the functions is “to determine premium amounts payable in respect of CTP insurance policies”. Insurers will be keenly interested to know how this section of the legislation will be implemented in practice. The bill also limits the factors that the Regulator can use when setting differential premiums to:

> Vehicle type > Garaging location

> Vehicle use > ITC entitlement.

TABLE 3 – QLD CLASS 1 METRO PREMIUMS

Insurer

April 2015 August 2015

Premium Difference from Ceiling

Premium Difference from Ceiling

Ceiling $337 $330

Allianz $335 ($2) $330 $0

QBE $337 $0 $330 $0

RACQ $337 $0 $330 $0

Suncorp $324 ($13) $324 ($6)

Inquiry into PrivatisationIn early July 2015, a State

Parliamentary Inquiry was announced to review the proposal for privatisation, including seeking information on the alternative to privatisation as put forward to the state government by the MAC board. At the time of writing, it is not clear what impact this Inquiry might have on the privatisation process.

Western Australia

NIIS Scheme to start from 1 July 2016

The Western Australian Government has announced its intention to establish a National Injury Insurance Scheme (NIIS) in that state from 1 July 2016. However, the details differ a little from the NIIS/lifetime care schemes that have been established in other jurisdictions with fault based schemes.

The proposed new scheme would provide cover for people catastrophically injured in motor vehicle accidents who cannot currently claim compensation under the existing CTP scheme (at-fault persons or those involved in no-fault accidents).

Individuals who are catastrophically injured and covered by the CTP scheme will have two options once their injuries have stabilised:

>> Receive NIIS-style care and support entitlements via the existing CTP scheme.

>> Settle via a lump sum payment and self-manage their care from that point (as for other CTP claimants).

This second option of the proposed new arrangements is contrary to the agreed NIIS minimum benchmarks, which do not allow care and support entitlements to be commuted; WA was not among the seven jurisdictions that agreed to the minimum benchmarks.

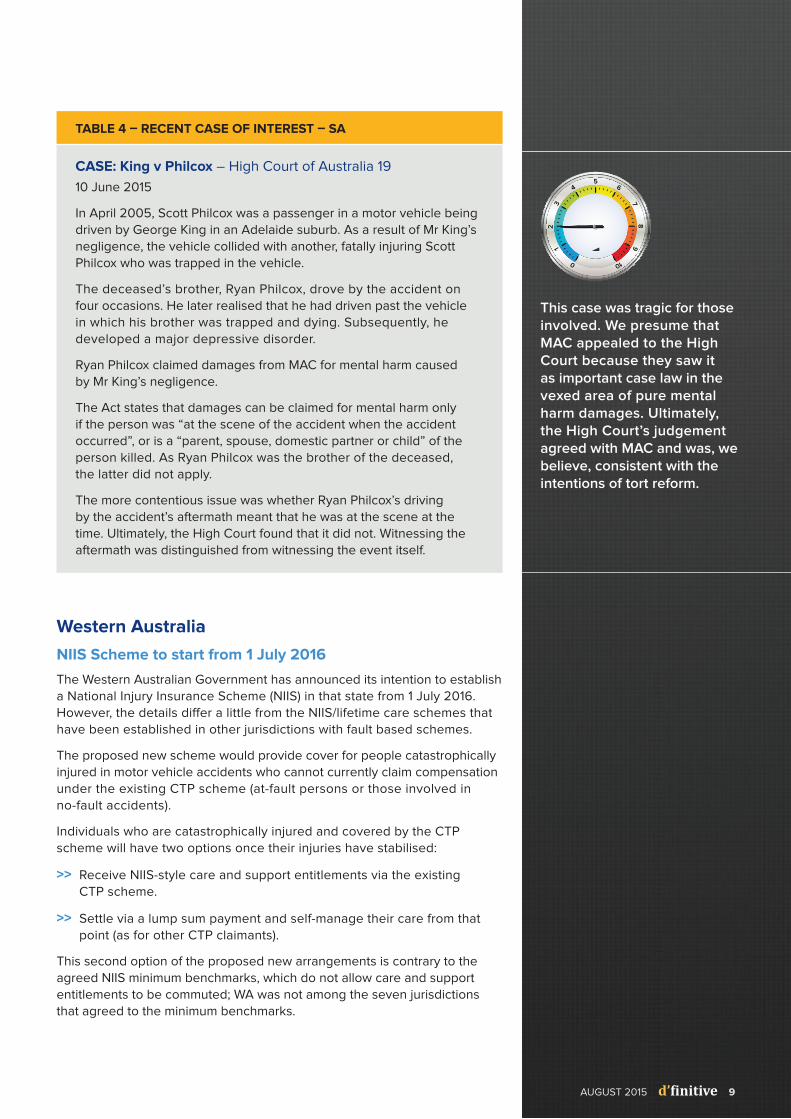

TABLE 4 – RECENT CASE OF INTEREST – SA

CASE: King v Philcox – High Court of Australia 19

10 June 2015

In April 2005, Scott Philcox was a passenger in a motor vehicle being driven by George King in an Adelaide suburb. As a result of Mr King’s negligence, the vehicle collided with another, fatally injuring Scott Philcox who was trapped in the vehicle.

The deceased’s brother, Ryan Philcox, drove by the accident on four occasions. He later realised that he had driven past the vehicle in which his brother was trapped and dying. Subsequently, he developed a major depressive disorder.

Ryan Philcox claimed damages from MAC for mental harm caused by Mr King’s negligence.

The Act states that damages can be claimed for mental harm only if the person was “at the scene of the accident when the accident occurred”, or is a “parent, spouse, domestic partner or child” of the person killed. As Ryan Philcox was the brother of the deceased, the latter did not apply.

The more contentious issue was whether Ryan Philcox’s driving by the accident’s aftermath meant that he was at the scene at the time. Ultimately, the High Court found that it did not. Witnessing the aftermath was distinguished from witnessing the event itself.

This case was tragic for those involved. We presume that MAC appealed to the High Court because they saw it as important case law in the vexed area of pure mental harm damages. Ultimately, the High Court’s judgement agreed with MAC and was, we believe, consistent with the intentions of tort reform.

4

32

1

0

56

78

9

10

AUGUST 2015 d’finitive 9

10 d’finitive AUGUST 2015

FIGURE 4 – ACT PREMIUMS: PRIVATE USE PASSENGER VEHICLE

610

600

590

580

570

560

550

540

530

Pri

vate

Pa

sse

ng

er

Ve

hic

le P

rem

ium

Jul 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15 Jun 15 Jul 15 Aug 15 Sep 15

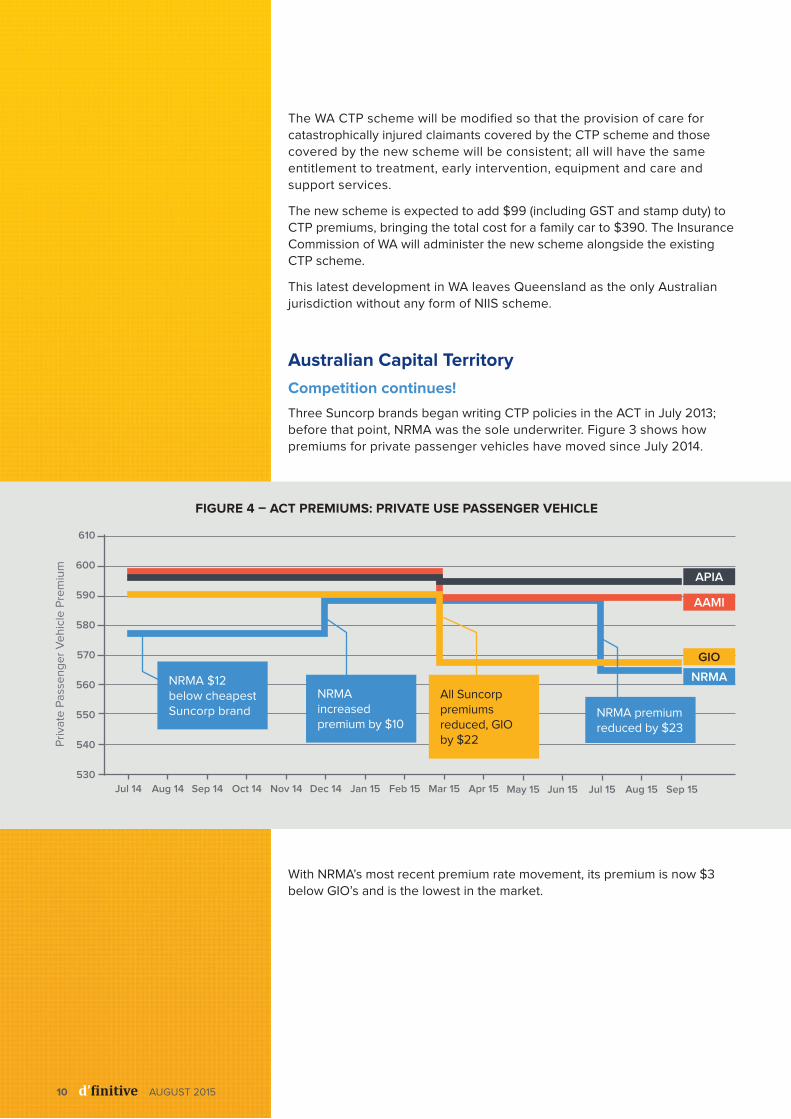

The WA CTP scheme will be modified so that the provision of care for catastrophically injured claimants covered by the CTP scheme and those covered by the new scheme will be consistent; all will have the same entitlement to treatment, early intervention, equipment and care and support services.

The new scheme is expected to add $99 (including GST and stamp duty) to CTP premiums, bringing the total cost for a family car to $390. The Insurance Commission of WA will administer the new scheme alongside the existing CTP scheme.

This latest development in WA leaves Queensland as the only Australian jurisdiction without any form of NIIS scheme.

Australian Capital Territory

Competition continues!

Three Suncorp brands began writing CTP policies in the ACT in July 2013; before that point, NRMA was the sole underwriter. Figure 3 shows how premiums for private passenger vehicles have moved since July 2014.

With NRMA’s most recent premium rate movement, its premium is now $3 below GIO’s and is the lowest in the market.

NRMA

AAMI

GIO

APIA

NRMA $12 below cheapest Suncorp brand

NRMA increased premium by $10

All Suncorp premiums reduced, GIO by $22

NRMA premium reduced by $23

AUGUST 2015 d’finitive 11

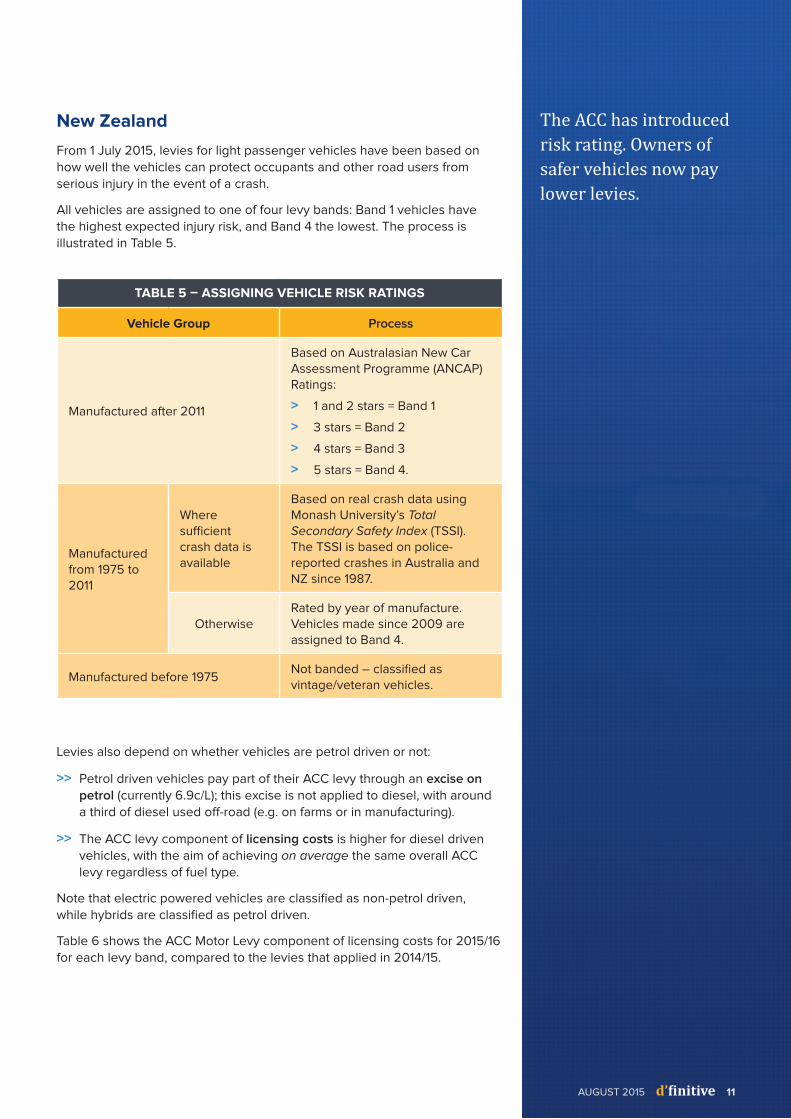

New Zealand

From 1 July 2015, levies for light passenger vehicles have been based on how well the vehicles can protect occupants and other road users from serious injury in the event of a crash.

All vehicles are assigned to one of four levy bands: Band 1 vehicles have the highest expected injury risk, and Band 4 the lowest. The process is illustrated in Table 5.

TABLE 5 – ASSIGNING VEHICLE RISK RATINGS

Vehicle Group Process

Manufactured after 2011

Based on Australasian New Car Assessment Programme (ANCAP) Ratings:

> 1 and 2 stars = Band 1

> 3 stars = Band 2

> 4 stars = Band 3

> 5 stars = Band 4.

Manufactured from 1975 to 2011

Where sufficient crash data is available

Based on real crash data using Monash University’s Total Secondary Safety Index (TSSI). The TSSI is based on police-reported crashes in Australia and NZ since 1987.

OtherwiseRated by year of manufacture. Vehicles made since 2009 are assigned to Band 4.

Manufactured before 1975Not banded – classified as vintage/veteran vehicles.

Levies also depend on whether vehicles are petrol driven or not:

>> Petrol driven vehicles pay part of their ACC levy through an excise on petrol (currently 6.9c/L); this excise is not applied to diesel, with around a third of diesel used off-road (e.g. on farms or in manufacturing).

>> The ACC levy component of licensing costs is higher for diesel driven vehicles, with the aim of achieving on average the same overall ACC levy regardless of fuel type.

Note that electric powered vehicles are classified as non-petrol driven, while hybrids are classified as petrol driven.

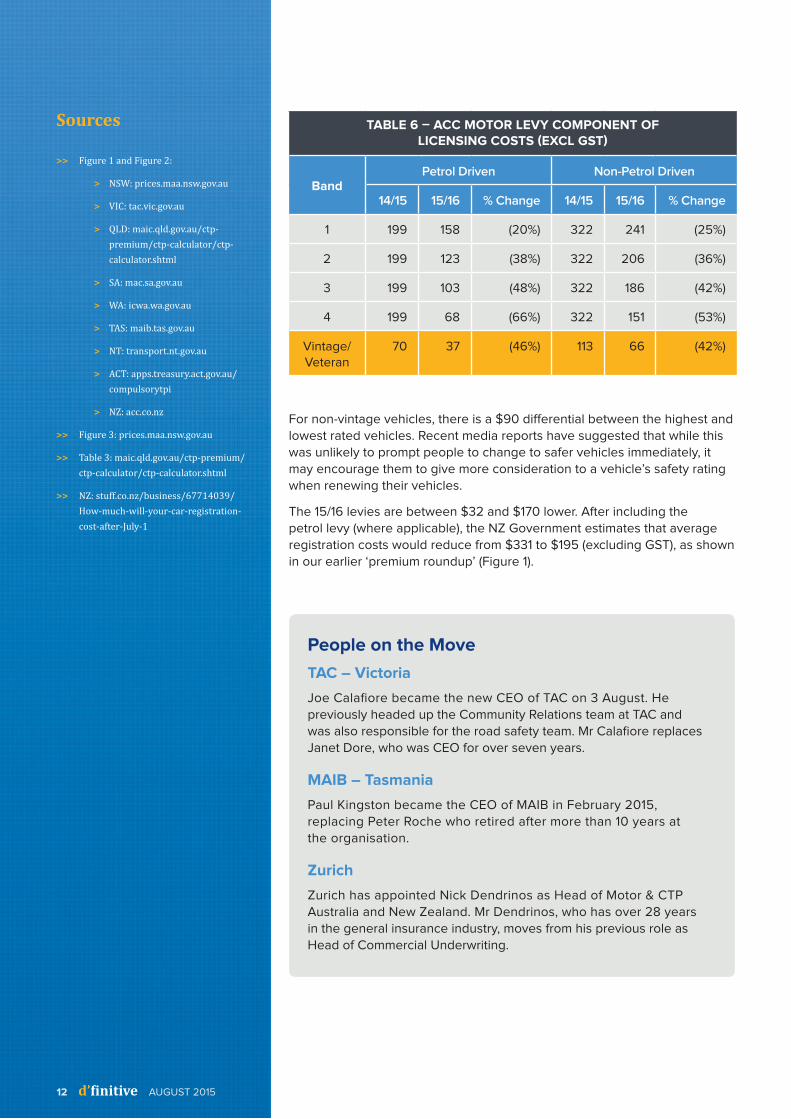

Table 6 shows the ACC Motor Levy component of licensing costs for 2015/16 for each levy band, compared to the levies that applied in 2014/15.

The ACC has introduced risk rating. Owners of safer vehicles now pay lower levies.

12 d’finitive AUGUST 2015

For non-vintage vehicles, there is a $90 differential between the highest and lowest rated vehicles. Recent media reports have suggested that while this was unlikely to prompt people to change to safer vehicles immediately, it may encourage them to give more consideration to a vehicle’s safety rating when renewing their vehicles.

The 15/16 levies are between $32 and $170 lower. After including the petrol levy (where applicable), the NZ Government estimates that average registration costs would reduce from $331 to $195 (excluding GST), as shown in our earlier ‘premium roundup’ (Figure 1).

People on the Move

TAC – Victoria

Joe Calafiore became the new CEO of TAC on 3 August. He previously headed up the Community Relations team at TAC and was also responsible for the road safety team. Mr Calafiore replaces Janet Dore, who was CEO for over seven years.

MAIB – Tasmania

Paul Kingston became the CEO of MAIB in February 2015, replacing Peter Roche who retired after more than 10 years at the organisation.

Zurich

Zurich has appointed Nick Dendrinos as Head of Motor & CTP Australia and New Zealand. Mr Dendrinos, who has over 28 years in the general insurance industry, moves from his previous role as Head of Commercial Underwriting.

TABLE 6 – ACC MOTOR LEVY COMPONENT OF LICENSING COSTS (EXCL GST)

BandPetrol Driven Non-Petrol Driven

14/15 15/16 % Change 14/15 15/16 % Change

1 199 158 (20%) 322 241 (25%)

2 199 123 (38%) 322 206 (36%)

3 199 103 (48%) 322 186 (42%)

4 199 68 (66%) 322 151 (53%)

Vintage/Veteran

70 37 (46%) 113 66 (42%)

Sources

>> Figure 1 and Figure 2:

> NSW: prices.maa.nsw.gov.au

> VIC: tac.vic.gov.au

> QLD: maic.qld.gov.au/ctp-premium/ctp-calculator/ctp-calculator.shtml

> SA: mac.sa.gov.au

> WA: icwa.wa.gov.au

> TAS: maib.tas.gov.au

> NT: transport.nt.gov.au

> ACT: apps.treasury.act.gov.au/compulsorytpi

> NZ: acc.co.nz

>> Figure 3: prices.maa.nsw.gov.au

>> Table 3: maic.qld.gov.au/ctp-premium/ctp-calculator/ctp-calculator.shtml

>> NZ: stuff.co.nz/business/67714039/How-much-will-your-car-registration-cost-after-July-1

Finity’s CTP Team

Finity’s CTP team prides itself on looking beyond the pure analytics to gain a deeper understanding of the cost drivers for schemes. This means we can respond appropriately in valuations, premium setting and scheme design.

In addition to our actuaries, Finity has a dedicated group of claims and operational insurance experts in our management consulting practice, who

can assist with claims and expense management.

Actuaries:

Aaron Cutter [email protected] +61 2 8252 3321

Estelle Pearson [email protected] +61 2 8252 3331

Gillian Harrex [email protected] +61 3 8080 0901

Management consultants:

Graeme Adams [email protected] +61 2 8252 3314

Raj Kanhai [email protected] +61 2 8252 3332

This article does not constitute either actuarial or investment advice. While Finity has taken reasonable care in compiling the information presented, Finity does not warrant that the information is correct.

Copyright © 2015 Finity Consulting Pty Limited.

If you would like to receive future

editions of CTP News, please contact

Renae Hoskins on +61 2 8252 3350 or at

d’finitive[ accident compensation ]

finity.com.au

Finity Consulting Pty Limited ABN 89 111 470 270

2015 Winner - Professional Services Firm of the Year

6 times winner Australian & New Zealand Insurance Industry Award ‘Service Provider of the Year’

Australian Insurance Industry Awards – Inaugural Inductee into the Hall of Fame

Australia

Sydney

Tel +61 2 8252 3300 Level 7, 155 George Street The Rocks, NSW 2000

New Zealand

Auckland

Tel +64 9 306 7700 Level 5, 79 Queen Street Auckland 1010

Melbourne

Tel +61 3 8080 0900 Level 3, 30 Collins Street Melbourne, VIC 3000

Karen Cutter Tel + 61 2 8252 [email protected] Office

Kane Boulton Tel + 61 2 8252 [email protected] Office

Contact the Authors