Embed Size (px)

Citation preview

Dairy Globalization Refresh: 2011 Update

Summary Findings

Commissioned by Dairy Management Inc. & U.S. Dairy Export Council

Conducted by Bain & Company

Study conducted by Bain and Co. in collaboration with industry participants

Funded by USDEC using check-off funds on behalf of Dairy Management Inc. and the Innovation Center

Globalization programs managed by checkoff staff with leadership from producers and processors

Background

2

Initial study examined implications of globalization

But since then, industry has endured rollercoaster of economic cycles

So do basic conclusions of original study still hold true?

� Have supply/demand changed to shrink demand gap identified in earlier study?

� Has the U.S. window of opportunity shortened through the entrance of new suppliers?

� Is program still viable to assist U.S. industry to become a globally consistent supplier?

Study background, purpose

3

In 2009, we identified several trends impacting the outlook for global dairy…

Dairy demand will continue to grow rapidly in developing markets

Dairy supply will be challenged to keep pace

United States is positioned to become a much larger player, but must address weaknesses

A latent demand gap is developing, creating a sizeable, though finite, window of opportunity for the United States

4

Reform U.S. pricing and risk management policies

1. Reform regulated milk pricing and price support mechanisms (IDFA, NMPF)

2. Better mechanisms for risk management, volatility reduction

Increase access to international markets

3. Trade treaties that provide net export benefits (USDEC, IDFA, NMPF)

Improve responsiveness to global demand

4. Pre-competitive sales and marketing investments and capabilities

5. Food safety assurances and traceability

6. Customer product specification requirements, globally

7. Product and technology innovation

…and recommended 7 industry and company-specific initiatives

5

The chosen outcome was for U.S. dairy to pursue actions that would make us a more Consistent Supplier

“Fortress USA”

Status Quo

� Commitment to global opportunities

� Improve commercial focus, product portfolio

� Reform FMMO, price support

� Improve forward contracts, futures markets

� Strong domestic market as basis for global trade

� Build insight/capability

Consistent Supplier

Recommended

by IC Board

6

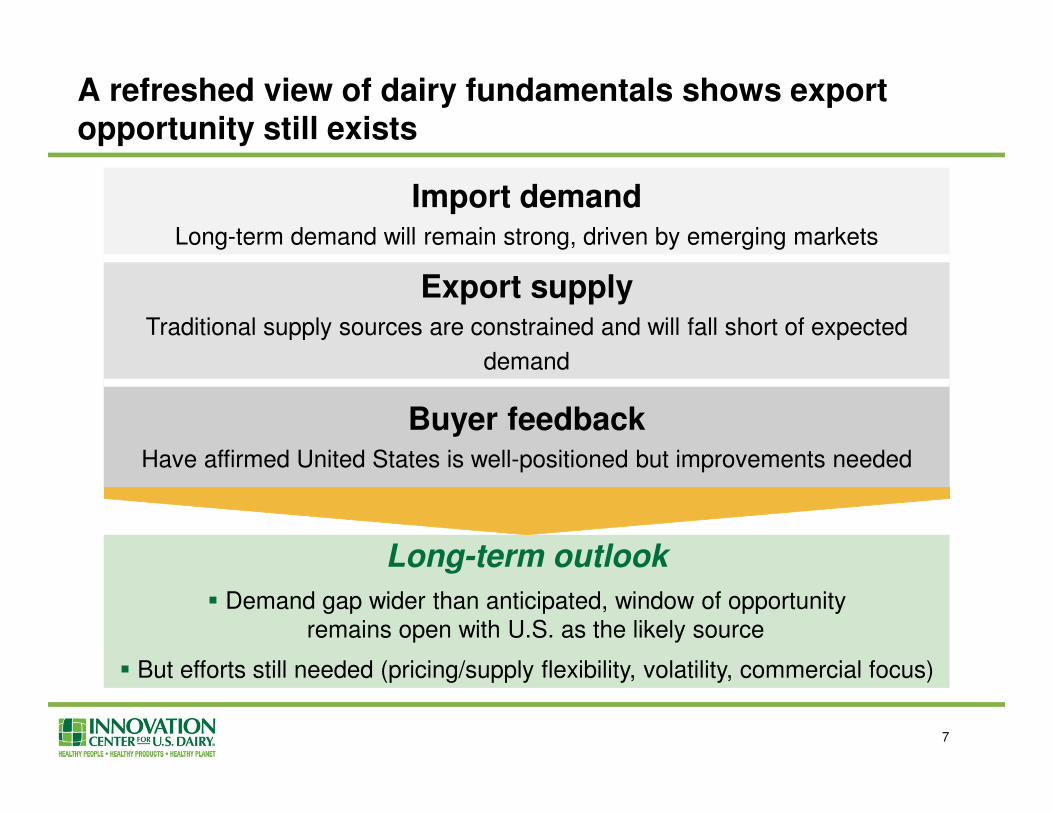

A refreshed view of dairy fundamentals shows export opportunity still exists

Import demandLong-term demand will remain strong, driven by emerging markets

Export supplyTraditional supply sources are constrained and will fall short of expected

demand

Buyer feedbackHave affirmed United States is well-positioned but improvements needed

Long-term outlook

� Demand gap wider than anticipated, window of opportunity remains open with U.S. as the likely source

� But efforts still needed (pricing/supply flexibility, volatility, commercial focus)

7

8

Forecasted growth remains strong in emerging markets

Source: Projected growth for India, Mena and SE Asia from FAPRI (2011); projected growth for China based on Bain analysis derived from OECD (2010) and GDP/consumption regression analysis

Dairy consumption is expected to grow quickly in key emerging markets…from which ~75% of new dairy consumption will come

PROJECTED GROWTH IN WORLD NON-FLUID DAIRY CONSUMPTION (’2010-15)

China: Despite foreign investments, domestic dairy farms unlikely to overcome demand gap

At most, Fonterra farms will add a fraction of total production

Additionally, they are likely to price at a premium

FONTERRA EXPECTED PRICING SCHEME VS. AVERAGE MARKET PRICE ($/cwt)

FONTERRA SHARE OF CHINA DAIRY HERD / RAW MILK PRODUCTION

Source: “Fonterra benefits from Chinese dairy market”, stuff.co.nz (4/14/2011); “Fonterra to invest in two more farms”. Fonterra media release (2/2/2010); Bain analysis; Expert interviews

9

China: Even with production growth, likely to rely on imports to meet growing demand

10

Source: “Fonterra benefits from Chinese dairy market”, stuff.co.nz (4/14/2011); “Fonterra to invest in two more farms”. Fonterra media release (2/2/2010); Bain analysis; expert interviews

CHINESE NON-FLUID DAIRY CONSUMPTIONCHINESE NON-FLUID DAIRY CONSUMPTION (FORECASTED)

5%

7%

Average 6%

CAGR

2010-19

Import markets

What has changed since 2009Est. impact, 2013 demand gap

ChinaNet imports: 486K MT, 11% of global

• Dairy consumption growth has increased and promises sustained growth over the longer term as economic development moves inland and 200M more Chinese join the middle class

• Production took a big hit from melamine crisis in ‘08-’09, widening China’s demand gap. Current industry structure makes large production increases unlikely without major investments in large, industrial farms

• Ongoing quality issues and lack of trust in domestically produced products create near-term opportunities to boost imports

• China will continue to be a net importer over the long term, but government tightening of import documentation requirements may create difficulty for U.S. imports

SE AsiaNet imports: 777K MT, 17% of global

� Although milk production increased faster than expected, local production still covers <10% of consumption

� SE Asia remains a sizeable importer of dairy products with strong potential for consumption growth

RussiaNet imports: 658K MT, 14% of global

� Production dipped during 07-10 due to droughts, high temperature and high-feed prices, widening demand gap

� Future production unclear due to recent instability in milk production and shifting government policies

� Consumption growth slow due to a declining population

� Russia expected to remain major dairy importer despite government efforts to encourage domestic production and stricter documentation requirements (effectively blocking Ukrainian and U.S. imports)

Legend Impact on demand gap: Bigger gap Small change Smaller gap

More on demand and other import markets (1)

11

Note: Net import figures as of 2010

12

Import markets

What has changed since 2009Est. impact, 2013 demand gap

MexicoNet imports: 299K MT, 7% of global

� Consumption still growing and expected to continue with stable economic growth. However, rising concerns over obesity may shift consumption toward lower-fat products

� Despite faster production growth, Mexico projected to remain a significant importer through 2015 and beyond

� Mexico extended retaliatory duties to U.S. cheese in late 2010 but recent progress on trucking dispute may restore trade levels

MENANet imports: 519K MT, 11% of global

� As a group, Algeria, Egypt and Saudi Arabia are significant dairy import markets, collectively importing more than China in 2010

� Production growing slowly, but not sufficient to cover domestic needs, and water/ forage limitations will constrain future growth

� Unrest across the region threatens near-term economic growth, though political reforms may also lead to significant long-term upside for economic (and therefore, dairy) growth

IndiaNet imports: 20K MT, 0.4% of global

� Supply has failed to keep up with domestic demand due to bad weather hampering production and continued growth in consumption

� Near-term consumption expected to outpace production despite government’s encouragement of self-sufficiency

� Imports have increased by small amount to fill demand-supply gap, with similar opportunities expected in near term

� Production has large potential to improve and should grow with government’s National Dairy Plan

� Although currently inaccessible to U.S. exporters, India’s growing imports will create opportunities for the US elsewhere in the world

Legend Impact on demand gap: Bigger gap Small change Smaller gap

12

Note: Net import figures as of 2010

More on demand and other import markets (2)

New Zealand: Constrained by several factors, dairy land growth should reach peak by 2020

Source: LIC Dec 2010, Dairy NZ, USDA GAIN Nov 2010; Lit. search, Bain analysis

0.8% CAGR1.2%

CAGR2.1% CAGR

� Most dairy land growth/conversion on South Island, where good land in demand

� Environmental regsexpected, limited land/herd growth

� Irrigation of marginal land on South Island also limited due to regs and water supplies

Dairy land likely to grow slowly beyond 2015 and peak around 2020

Several factors are expected to constrain further land growth beyond 2020

13

it

it

it

DAIRY LAND (M Hectares)

PROJECTED GROWTH (2010-20)

Bar width proportional to country’s share of EU production

Some European Union countries will expand production, while others will be flat to down

14

Source: European Commission, “Economic Impact of the Abolition of the Milk Quota Regime” (2/2009); Eurostat (for 2010 country-level production)

Countries most frequently mentioned by experts as likely to experience strong growth

Elimination of quota will lead to modest expansion of ~5%

% of total EU cow milk production

15

Export

marketsWhat has changed since 2009

Est. impact,

2013 demand gap

New ZealandNet exports: 1997K MT, 41% of global

• Production grew faster than expected during 2007-10 due to cow population growth. Consumption slumped in 2006-08 due to soaring prices, adding to export growth

• Future production growth expected to slow; could reach peak level of 23M MT by 2020

• Despite higher production, will not produce enough milk to close latent demand gap

AustraliaNet exports: 390K MT, 8% of global

� Production took a hit due to droughts, floods. Water table has improved, should spur limited production growth

� Consumption growth will remain flat, will remain a large exporter, albeit with slow production growth and limited ability to expand

EUNet exports: 1419K MT, 29% of global

• Consumption slumped in 2006-10 as high prices were followed by recession and added to export growth; consumption growth expected to remain low

• Quotas increasing 1% annually 2009-15; aggregate EU-27 production could increase by 5-8% from 2010 to 2020

• Production growth most likely result of a step change in output at 2015 by some countries as they expand production to use the full potential capacity of existing farms

• After 2015, further growth will be constrained by environmental regulations and the steep incremental investments required to expand the industry

UkraineNet exports: 64K MT, 1% of global

� Production lower in 2007-10 than previously projected due to financial, policy and quality issues; future export growth dependent on addressing these issues

� Consumption growth also slowed due to high prices and a weak economy

� Growth still possible, though unlikely to be a major exporter in the near term

Legend Impact on demand gap: Bigger gap Small change Smaller gap

More on supply and other export markets (1)

15

Note: Net export figures as of 2010

1616

Export markets

What has changed since 2009Est. impact, 2013 demand gap

BrazilNet imports: 48K MT, 1% of global

� Brazil became a net importer as production fell mainly due to poor profitability and bad weather

� Consumption continued to increase, spurred by income and population growth

� Should return to small net exporter by 2015. Still has strong exporter potential in the long term

ArgentinaNet exports: 247K MT, 5% of global

� Downturn saw production and consumption growth, but exports continued to grow off a small base. Still a relatively small exporter with decent growth potential, despite protectionist policies

� Improved dairy-grain price ratio should encourage use of feed and improve cow yields

BelarusNet exports: 312K MT, 6% of global

� Industry dependent on demand from Russia, but exports have grown at a very strong pace

� Poor economic situation will limit consumption growth and limit government ability to invest in production, though production has shown strong potential

� Exports are starting to diversify to markets other than Russia

U.S.Net exports: 322K MT, 7% of global

� Global recession, slow reaction of U.S. trade policy and period of high-feed prices could lead to a less competitive U.S. dairy industry

� Production and consumption trends remain steady with slow growth expected through 2015

Legend Impact on demand gap: Bigger gap Small change Smaller gap

16

Note: Net export figures as of 2010

More on supply and other export markets (2)

Feed prices have risen quickly over the past decade

17

Source: Bloomberg (2011)

HISTORICAL COMMODITY PRICES (indexed at 1983)

ProductChange

83-99

Change

00-10

Wheat -27% 126%

Soy Bean -33% 111%

Corn -34% 104%

Dairy producers will almost certainly face high feed costs (relative to the previous 20 year average)

Producers and processors should reassess their cost structures

to ensure competitiveness over the longer term

Source: EIU (2011), Bloomberg (2011); Bain analysis

Sustained high commodity prices also likely

AVERAGE COMMODITY PRICES (cents/bu)

18

New Zealand marginal costs include cost of shifting to 100% feed after peak production is reached under grazing model

Range of potential marginal commercial costs

Netherlands China New ZealandU.S.

High feed prices not likely to shift U.S. cost position; major expansion will be costly for most competitors

19

Source: IFCN 2010; USDA 2009; China Dairy 2010; Teagasc Ireland Dairy 2010; “The Wealth Report” (2011); Eurostat (2011); expert interviews

Despite higher feed prices, the U.S. should maintain its cost position. And, even for traditionally lower-cost producers, major commercial growth will be costly.

RAW MILK ESTIMATED MARGINAL PRODUCTION COSTS ($/MT)

Costs based on IFCN large-sized farms

Currency was also considered as a wildcard, but it is unlikely to have a near-term impact on U.S. dairy

Source: EIU (2011), Bloomberg (2011); Bain analysis

PROJECTED USD APPRECIATION/DEPRECIATION VS. KEY IMPORT CURRENCIES (10-13F)

20

� Currency trends may influence long-term cost position of suppliers while also boosting purchasing power for importers

� However, currency fluctuations unlikely to drive purchases in the short-term because buyers more likely to manage through hedging

� Even with strong U.S. dollar, latent demand gap will still exist, making export pricing levels more attractive

In summary, the window of opportunity remains open and appears to be expanding

IMPORTERS

China

Russia

Southeast Asia, Mexico, MENA, India

EXPORTERS

Brazil

Ukraine

New Zealand

European Union

Australia, Argentina, Belarus

� China shows continued growth in demand

� Russia production dipped

� Potential low-cost producers such as Brazil, Ukraine recently stumbled

� New Zealand and EU, despite modest increases, unable to fill demand gap

� Other sources—Argentina and Belarus—have good potential, but still relatively small

Net 2013 demand gap widened during the global economic downturn

Latent demand gap of 6.5-7B lbs. still exists, may be larger than estimated

21

And buyers have clearly affirmed that the U.S. is well-positioned to play a greater role

“The United States has one

very big strength. They have a

lot of milk with no

seasonality.”

“We desire to open our portfolio

and expand our supplier

base beyond Fonterra. I

would like to have the United

States as a supplier and they

are a natural choice.”

Source: Innovation Center for U.S. Dairy “Global Dairy Buyer Survey,” conducted in September 2010

“Supply is uncertain – they

want to play when price works

but we can’t be sure they will be

there. It works for spot buys, but

not for consistent, twice-monthly

deliveries. We need suppliers who are committed.”

“We are afraid to contract with

the United States because we

can’t ensure that they will

meet the commitment. That

means I have to bear the risk.”

Buyers view the United States as an important source of future supply…

…but want the United States to commit to the global market

22

Though the window of opportunity will remain open, the U.S. must take action in near-term

23

TIME HORIZON

High

Low

U.S

. D

AIR

Y

CO

MP

ET

ITIV

EN

ES

S

NEAR-TERM

� Dairy trade continuously attractive

� Buyers seek to rely more upon United States as an alternative supplier

MID-TERM

� Growth markets continue to import

� New Zealand approaches peak production levels, inducing a need for alternative suppliers

� Low-cost suppliers emerge

LONG-TERM

� Today’s emerging markets see slower growth rates

� Low-cost exporters expand capacity

POTENTIAL LONG-TERM U.S. TRAJECTORY

However, there are reminders that the window of opportunity won’t remain open indefinitely

Import demand

1. Major importers have renewed investments in domestic production

2. Recent willingness to protect local producers may give domestic producers time to increase their competitiveness

Export supply

3. Oceania and EU aggressively pursuing FTAs with developing countries

4. Long-term growth likely for some EU producers such as Ireland and Netherlands

5. Brazil, Argentina, Ukraine and Belarus hold potential

Policy reforms 6. The United States has yet to make key reforms

24

Policy reform should seek to accelerate achieving critical outcomes

U.S. dairy is uniquely positioned to seize on long-term export growth

Updated dairy policies are needed before the U.S. can fully benefit

� Global dairy demand continues to outstrip supply due to growth in developing markets

� Export markets are the strongest source for future U.S. growth

� The U.S. can become a sustainably larger player provided it can address capability gaps

� Global buyers want a more diverse supply base

� Yet, emerging suppliers make this a finite window

� Flexible pricing to let milk flow to the best/ most profitable use

� Achieve greater predictability of price thereby decreasing the cost of volatility

� Reform milk pricing systems to improve the forward/ futures market to manage price volatility

� Reform price support to remove the government as a “last resort” buyer and remove disincentives for product innovation

� Develop better mechanisms for risk management to mitigate the impact of volatility

� Modify standards of identity closer to global norms if needed to meet customer needs

The reforms, whatever their details, must enable key outcomes

� Let market incentives better align product portfolios with customer needs

� Achieve value growth for producers and processors by investment in innovation, safety and quality

25

Failure to achieve needed policy change will weaken the U.S. industry and limit its higher value realization

The U.S. will miss out on sustainable volume and value growth

� Limited opportunities for U.S. to grow milk supply and raise on-farm margins without global trade

� Greater value and profits will be available as emerging markets expand consumption – capturing this value is a priority for every expanding industry

� Stagnant industry will undermine competitiveness, investment and profit for entire sector

Unmet demand will accelerate the expansion of other producers

� Failure to fulfill rising demand will incent investment in alternate areas of supply, accelerating their emergence as global competitors

� Without the U.S., investors and buyers must turn to higher-cost sources such as the EU – and lead to a closing window of opportunity

The U.S. industry will see lower competitiveness and less ability to meet market needs

� Lack of higher growth outlets will dampen capital investment in the U.S. supply chain, leading to declining competitiveness

� The impact of volatility will increase, further damaging the industry, encouraging substitution by non-dairy alternatives

� Without a policy and economic environment that facilitates the growth and advancement of the U.S. dairy farmer, filling the latent demand gap could be out of reach

26

The 2011 “refresh” confirmed the findings of the 2009 report—we’re on the right track

Opportunity is still there, but we have a limited ability to control the “size of the prize”

What we can control is time – how quickly we move into this space

� Window of opportunity won’t stay open indefinitely

� The U.S. has yet to make key reforms needed to fully capitalize on the opportunity

� If the U.S. doesn’t make key reforms, we will miss out on sustainable volume and value growth; unmet demand will accelerate the expansion of other producers; and the U.S. industry competitiveness will erode

Concluding thoughts and implications

27

The same industry and company efforts will combine to make the U.S. a globally consistent supplier

Company specific Collective industry

Cross-border partnerships

Milk pricing reform

Risk Management,

Volatility

Quality-

(Safety)

Quality-

Traceability

(Safety)

Net benefit

trade treaties

High

Low

Sales /

capabilities

Sales /

marketing

capabilities

Specifications

Customer Product

Specifications

Product &

Innovation

Product &

Technology

Innovation

High value

standards

High-value

products meeting

international

standards

Export

Board

Export

Marketing

Board

Pri

ori

ty

28

usdairy.com/globalization

Executive summary

Factbase

White Paper

Online access to the study

29

Dairy Globalization Refresh: 2011 Update

Summary Findings

Commissioned by Dairy Management Inc. & U.S. Dairy Export Council

Conducted by Bain & Company