Embed Size (px)

Citation preview

Danish Video AssociationThe Future for Home Video

May 2010

Presented by: Alison Casey, Head of Global Content

© 2010 Futuresource Consulting Ltd

Agenda

DVD Update

Blu-ray performance and major driversHardware uptakeTV trends

Opportunities for 3D

Future prospects for Digital Distribution

2

© 2010 Futuresource Consulting Ltd

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014

Packaged Film & Video

Broadband Services

Mobile Content

Online Content

Packaged Music

Box Office

Subscription TV

(Basic & Pay,

Inc VoD & PPV)

Packaged Games

Global Entertainment Media Consumer Expenditure

3

$Bn

Digital Revenues $40.2BPackaged Revenues $72.8B

497.6

376.7

413.3 420.3

450.9473.7

487.7

Total Consumer Spend* 3.6% CAGR2010-2014

432.6

© 2010 Futuresource Consulting Ltd

Packaged Media Will Continue to Dominate Video Revenues: Western Europe

4

DVD-Video

Blu-ray

Mobile Video

Online Video

Retail Value (€ Euro Billions)

TV VoD

© 2010 Futuresource Consulting Ltd

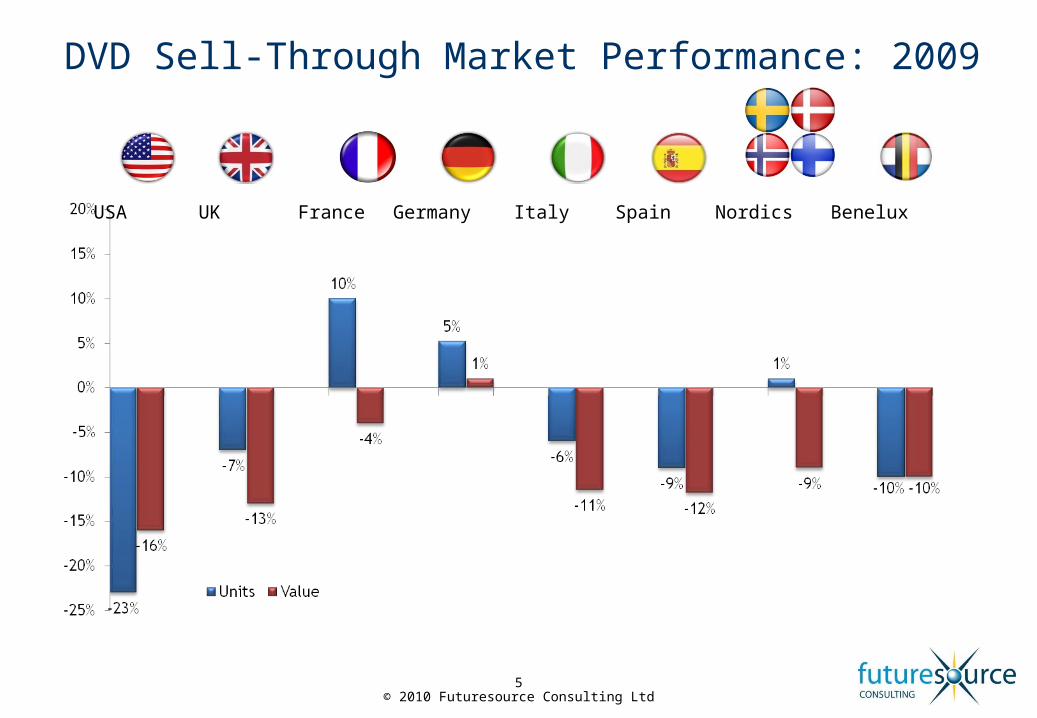

DVD Sell-Through Market Performance: 2009

5

USA UK France Germany Italy Spain Nordics Benelux

© 2010 Futuresource Consulting Ltd

DVD Sell-Through Market Performance: 2010

6

USA UK France Germany Italy Spain Nordics Benelux

© 2010 Futuresource Consulting Ltd

DVD Sell-Through Market Performance: 2009

7

© 2010 Futuresource Consulting Ltd

DVD Sell-Through Market Performance: 2010

8

© 2010 Futuresource Consulting Ltd

DVD Rental Retail Value 2009 & 2010 Forecast

9

2%

-15%

-12%

-7%

-15%-17%

-12%

-9%

0%

-17%

-14%

-9%

-17%-19%

-15%

-3%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%USA UK France Germany Italy Spain Benelux Nordics

2009 vs 2008

2010 vs 2009

2009

2010

Value: 2009 vs. 2008 & 2010 vs. 2009

© 2010 Futuresource Consulting Ltd

Retail Sales Market Development (M Units)

10

0

50

100

150

200

250

300

0

20

40

60

80

100

120

0

50

100

150

0

20

40

60

80

100

UK France

Germany Nordics

243 235 222 213 206

257

195

DVD BD

113 119 124 128 125104

119

95 95 96 96 9483

88

74 74 73 73 707265

2008 2009 2010 2011 2012 2013 2014Total Retail Value (€ Bn)

3.36 2.64 2.42 2.21 2.09 2.00 1.87

Growth Rate %

-13% -22% -8% -9% -6% -4% -7%

2008 2009 2010 2011 2012 2013 2014

Total Retail Value (€ Bn)

1.55 1.64 1.68 1.70 1.69 1.60 1.47

Growth Rate %

-3% 5% 3% 1% 0% -6% -8%

2008 2009 2010 2011 2012 2013 2014Total Retail Value (€ Bn)

1.52 1.51 1.47 1.43 1.41 1.36 1.24

Growth Rate %

-8% -1% -3% -3% -1% -4% -8%

2008 2009 2010 2011 2012 2013 2014

Total Retail Value (€ Bn)

1.00 0.94 0.95 0.93 0.91 0.87 0.79

Growth Rate %

-2% -6% 2% -3% -2% -5% -9%

BD Market Performance

© 2010 Futuresource Consulting Ltd

High Definition TV Market Development:Western Europe

12

% Homes with at least 1 HDTV

Hi Def ‘Content Gap’

‘HD Ready’ Screens

Homes receiving HD Broadcasts

172m Sets in use

97m homes

© 2010 Futuresource Consulting Ltd

High Definition TV Market Development:Nordics

13

% Homes with at least 1 HDTV

Hi Def ‘Content Gap’

‘HD Ready’ Screens

Homes receiving HD Broadcasts

10m Sets in use

8m homes

2009 – HDTV HHs

Norway

85%Denmark

79%Sweden

65%Finland

54%

© 2010 Futuresource Consulting Ltd

24.0

3.7 1.7 1.7 0.3 0.3 0.6 0.6

45.0

8.44.5 6.2

0.8 0.8 1.4 1.8

95.0

17.0

9.514.0

1.6 1.6 2.9 4.0

0

20

40

60

80

100

120

USA UK France Germany Italy Spain Benelux Nordics

2008 2009 2010

Blu-ray Retail Sales Performance: 2008 - 2010

14

Retail Sales (Million Units)

NB: 2009 refers to a 53 week calendar year

© 2010 Futuresource Consulting Ltd

Blu-ray Retail Sales Performance: 2008 - 2010

15

Retail Sales (Million Units)

© 2010 Futuresource Consulting Ltd

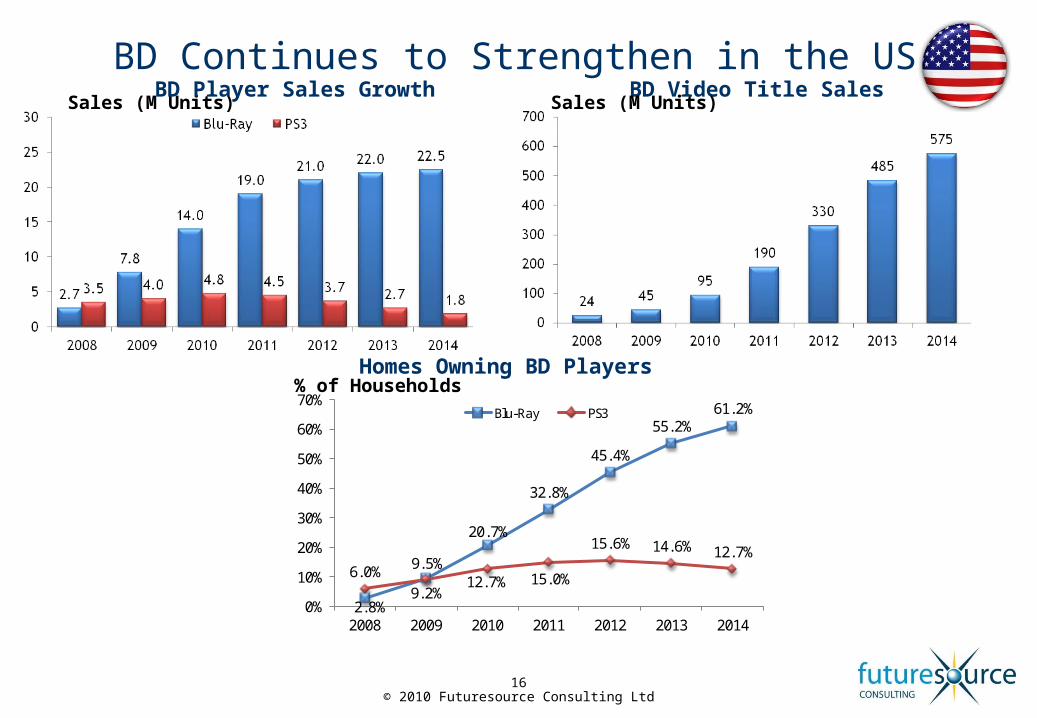

Sales (M Units)

16

BD Video Title SalesBD Player Sales GrowthBD Continues to Strengthen in the USA

2.8%

9.5%

20.7%

32.8%

45.4%

55.2%61.2%

6.0%9.2%

12.7% 15.0%

15.6% 14.6% 12.7%

0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011 2012 2013 2014

Blu-Ray PS3

% of HouseholdsHomes Owning BD Players

Sales (M Units)

© 2010 Futuresource Consulting Ltd

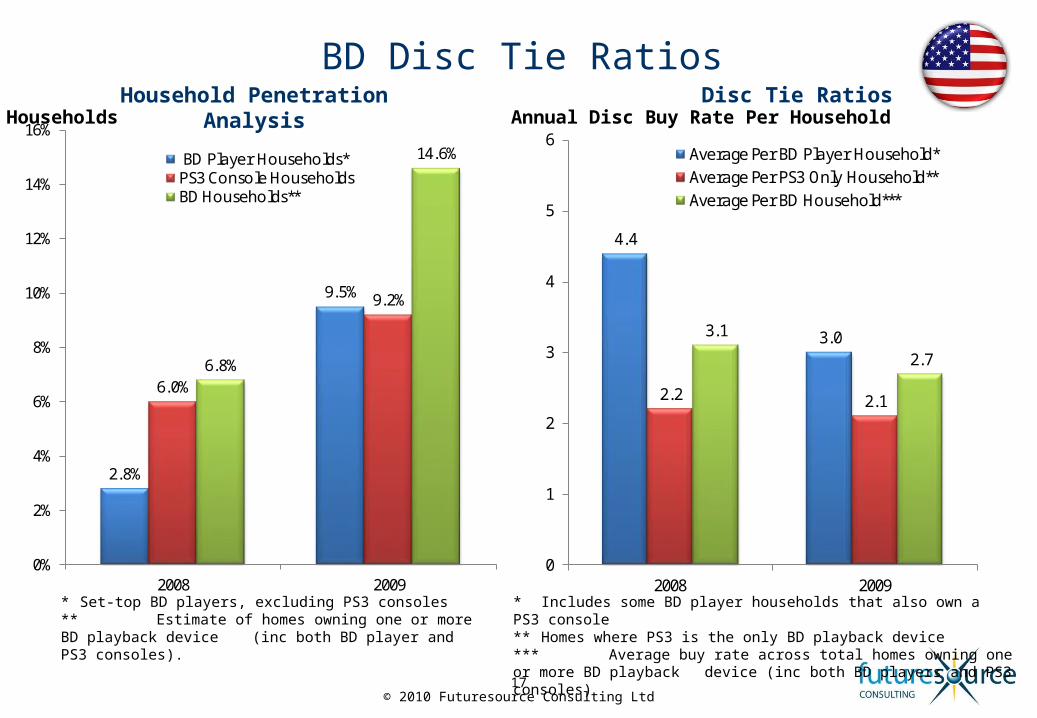

2.8%

9.5%

6.0%

9.2%

6.8%

14.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2008 2009

BD Player Households*PS3 Console HouseholdsBD Households**

17

% Households

* Set-top BD players, excluding PS3 consoles** Estimate of homes owning one or more BD playback device (inc both BD player and PS3 consoles).

4.4

3.0

2.2 2.1

3.1

2.7

0

1

2

3

4

5

6

2008 2009

Average Per BD Player Household*Average Per PS3 Only Household**Average Per BD Household***

Annual Disc Buy Rate Per Household

* Includes some BD player households that also own a PS3 console** Homes where PS3 is the only BD playback device*** Average buy rate across total homes owning one or more BD playback device (inc both BD players and PS3 consoles)

Disc Tie RatiosHousehold Penetration Analysis

BD Disc Tie Ratios

The Market Impact of 3D

© 2010 Futuresource Consulting Ltd

Global Digital Cinema Installed Base Forecast

19

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015

3D Based D-Cinema Non 3 Based D-Cinema

16.2

25.6

38.1

54.2

65.4

84.1

Thousands

Installed Base of Digital Cinema Screens (Includes IMAX)*

Total WW Screens 2010 150,000 (approx) Americas 50,000 (USA 39,000) EMEA 40,000 (EU 27 29,000) Asia Pac 60,000 (China 37k, India 14k)

75.5

8.7 63%71%

76%

78%

79%

81%

47%

© 2010 Futuresource Consulting Ltd

Consumer Awareness and Interest in 3D

20

“Have you ever watched a 3D Movie at the movie theater/cinema?”

Do Consumers Want 3D at Home?

“Soon you will able to watch a new type of 3D in the home. You will need glasses, but not the red/green ones used of the past. The quality will be much better than in the past. How interested are you in watching 3D at home?”

Source: Living With Digital Internet survey – Futuresource February 2010 (2,470 Adults)

* Aggregate of UK, Germany and France.** Reasonably, very or extremely interested

Will Consumers Be Willing To Get a New TV For 3D?“How likely is it that you would be willing to

buy a new TV to watch 3D (assuming the TV is slightly more expensive than a regular High Definition TV)?”

Yes No

USA 61% 39%

Europe* 48% 52%

Interested** Not interested

USA 71% 29%

Europe* 70% 30%

Interested** Not interested

USA 38% 62%

Europe* 45% 55%

Who Has Seen 3D on TV at Home?

“Have you ever watched anything in 3D on TV at Home?

Yes No

USA 26% 74%

Europe* 15% 85%

Who Has Seen 3D at the Cinema?

© 2010 Futuresource Consulting Ltd

Hollywood 3D Boom

16 major Hollywood 3D features in 2009, will release 20 in 2010Avatar ran for 16 weeks, 70% of US Box Office from 3D screens

Animation currently 70% of titles: new and re-releasesAll major new animations have a 3D version

Live action Science Fiction, Horror, Musicals, Action all good in 3DClassic re-releases possible e.g. The Matrix, Star Wars, Jurassic Park

21

© 2010 Futuresource Consulting Ltd

Pay-TV Sees A New Opportunity in 3D

Pay-TV will use 3D to differentiate and add subscription value3D movie VoD services: PPV and subscription Premium sports: football, tennis, title fights, World Cup, OlympicsConcerts, wildlife docs, other specials also importantCommercial market (bars, pubs) + home as 3D-Ready sets become availableUses existing infrastructure, STBs, compatible with new 3D TVs

22

Cable NetworksOperators/Content Providers

© 2010 Futuresource Consulting Ltd

3D-Ready TV Display Forecast: W Europe

23

0%

10%

20%

30%

40%

50%

2008 2009 2010 2011 2012 2013 2014 2015

Annual W European TV Display Shipments 3D-Ready TV Penetration of W European Homes**

40.5

47.051.9

54.357.6 58.7 59.5 59.6

2D only

3D-Ready*

*Glasses and transmitter may be optional extras

30m in use

** Excluding non-Full HD 3D sets sold prior to 2010

60m in use

Millions %

© 2010 Futuresource Consulting Ltd

0

10

20

30

40

50

60

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

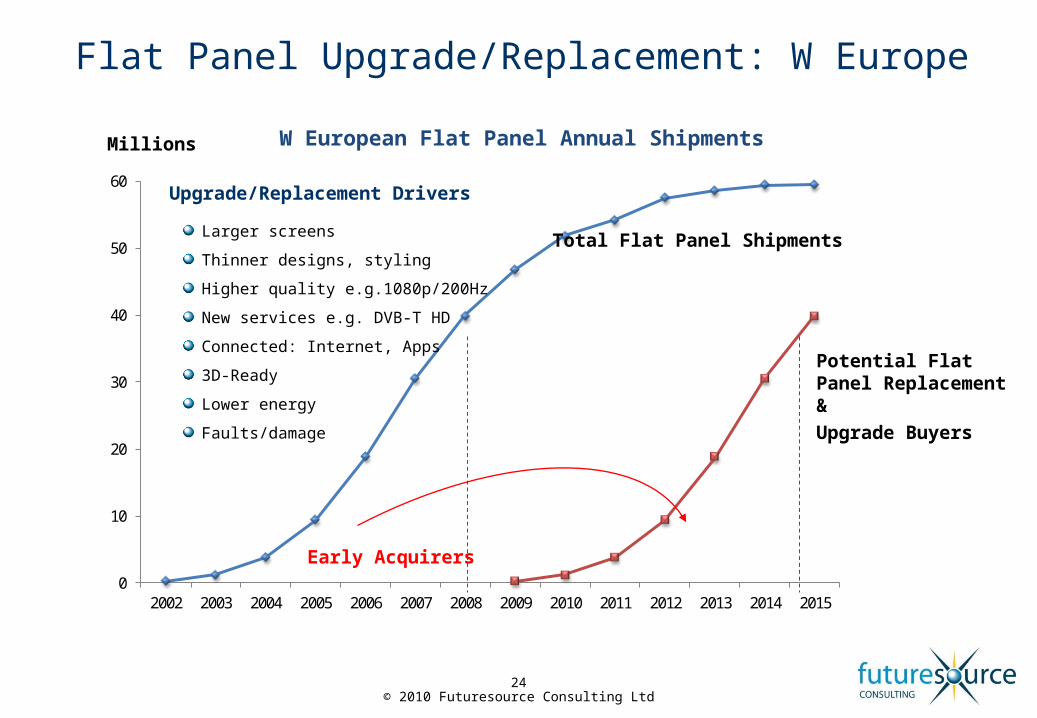

Flat Panel Upgrade/Replacement: W Europe

W European Flat Panel Annual ShipmentsMillions

Total Flat Panel Shipments

Potential Flat Panel Replacement &Upgrade Buyers

Early Acquirers

Larger screens

Thinner designs, styling

Higher quality e.g.1080p/200Hz

New services e.g. DVB-T HD

Connected: Internet, Apps

3D-Ready

Lower energy

Faults/damage

Upgrade/Replacement Drivers

24

© 2010 Futuresource Consulting Ltd

3D Blu-Ray Player Forecast: Western Europe

25

2D only

3D-Ready (embedded or firmware upgradeable)*

* Players, HTiB and Recorders

0.5 3

9

19

2630

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013 2014 20150%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 2015

Annual European Blu-ray Hardware* Shipments 3D-Ready BDP Penetration of Homes

0.82.2

5.2

10.2

17.3

24.6

28.330

31m 3D in use3D* BDPs

2D BDPs

57m 3D in use

Millions %

© 2010 Futuresource Consulting Ltd

3D Blu-ray Media Forecast: W Europe

26

2552

93143

190215

240

1

3

10

20

40

60

0

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014 2015

Millions

Annual BD Sell-Through Shipments

25

53

96

153

210

255

300

0.81.5

2.33.2

3.9 4.1 4.1

0

0.1

0.3

0.50.9

1.3

0

1

2

3

4

5

6

2009 2010 2011 2012 2013 2014 2015

$bn

Annual BD Sell-Through Retail Value

0.8

1.5

2.4

3.5

4.4

5.05.4

3D Blu-ray discs

2D Blu-ray discs

20%24%

The Digital and Online Challenge

© 2010 Futuresource Consulting Ltd

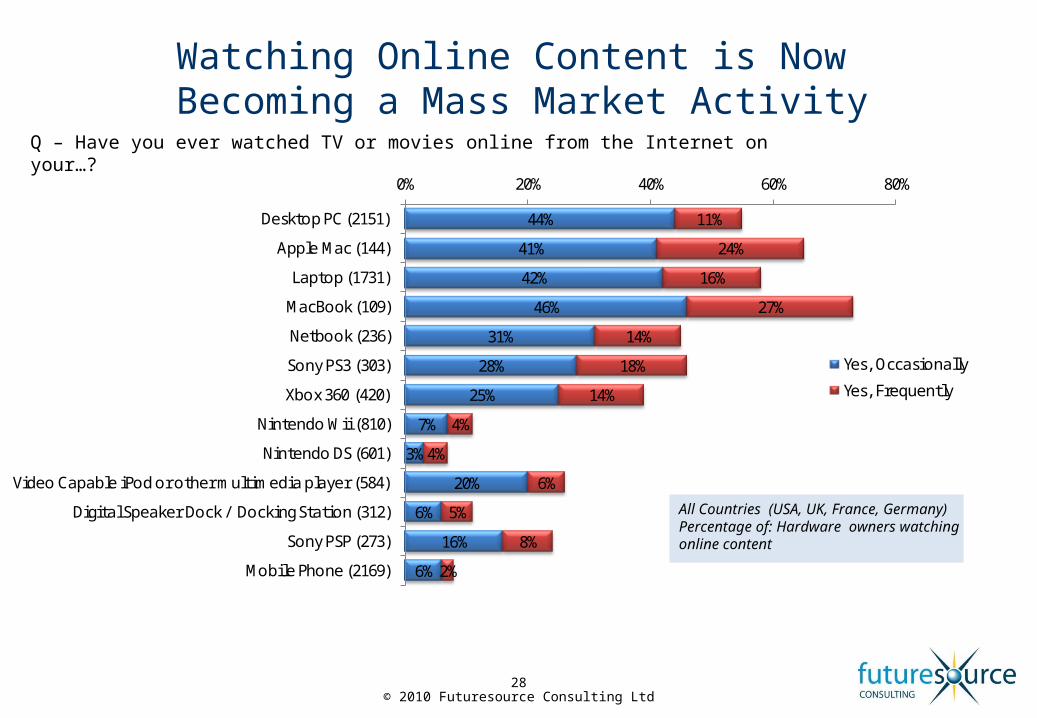

Watching Online Content is Now Becoming a Mass Market Activity

28

44%

41%

42%

46%

31%

28%

25%

7%

3%

20%

6%

16%

6%

11%

24%

16%

27%

14%

18%

14%

4%

4%

6%

5%

8%

2%

0% 20% 40% 60% 80%

Desktop PC (2151)

Apple Mac (144)

Laptop (1731)

MacBook (109)

Netbook (236)

Sony PS3 (303)

Xbox 360 (420)

Nintendo Wii (810)

Nintendo DS (601)

Video Capable iPod or other multimedia player (584)

Digital Speaker Dock / Docking Station (312)

Sony PSP (273)

Mobile Phone (2169)

Yes, Occasionally

Yes, Frequently

All Countries (USA, UK, France, Germany)Percentage of: Hardware owners watchingonline content

Q – Have you ever watched TV or movies online from the Internet on your…?

© 2010 Futuresource Consulting Ltd

Online Video Viewings Significant,But Majority is Free

29

Other Short Form & Professional Online Video 44% (29bn)

Paid-for Content 0.01% (9m)

54% (35bn)

Online TV 2% (1bn)

2009: ~65 Billion Video Views

© 2010 Futuresource Consulting Ltd

Broadband Speeds Increasing, Downloading & Streaming Video Now Possible For All

30

35 35

169 8.5 10 7 4.5 4.5

48 45

28

21 19 18 2015 15

0

10

20

30

40

50

60

70

80

90

J apan South Korea Sweden France Norway Finland Denmark UK USA

Ach

ieve

d A

ve. Bro

adban

d S

peed (m

bps)

2013 Speed 2009 Speed

Broadband

Household Penetratio

n

2009: 66% 85% 72% 74% 81% 73% 83% 70% 69%

2013: 72% 86% 77% 78% 84% 76% 85% 74% 74%

© 2010 Futuresource Consulting Ltd

Packaged Media Will Continue to Dominate Video Revenues: Western Europe

0

2

4

6

8

10

12

14

2007 2008 2009 2010 2011 2012 2013 2014

31

DVD-Video

Blu-ray

Mobile Video

Online Video

Retail Value (€ Euro Billions)

TV VoD

© 2010 Futuresource Consulting Ltd

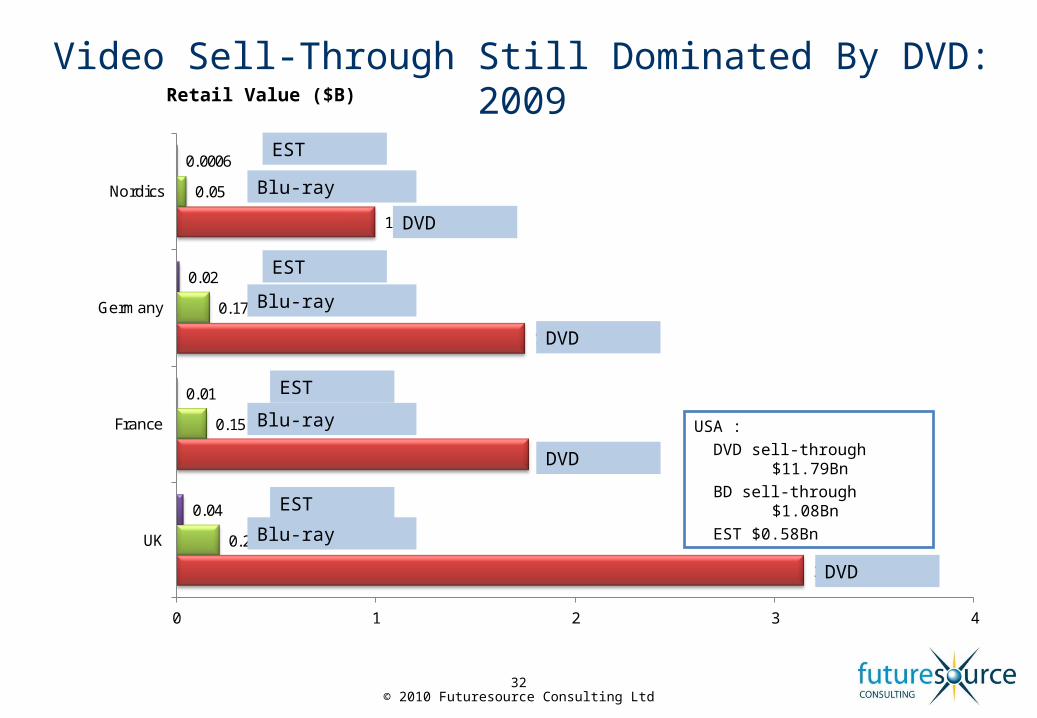

Video Sell-Through Still Dominated By DVD: 2009

32

3.15

1.77

1.75

1.00

0.22

0.15

0.17

0.05

0.04

0.01

0.02

0.0006

0 1 2 3 4

UK

France

Germany

Nordics

USA :DVD sell-through

$11.79BnBD sell-through $1.08BnEST $0.58Bn

Retail Value ($B)

EST

Blu-ray

DVD

EST

Blu-ray

DVD

EST

Blu-ray

DVD

DVD

EST

Blu-ray

© 2010 Futuresource Consulting Ltd

Importance of Video Rental/VOD: 2009

33

289.9

176.9

335.7

249.0

9.4

5.6

20.9

5.6

12.0

3.1

4.5

3.1

231.3

225.0

51.4

115.0

0 50 100 150 200 250 300 350 400

UK

France

Germany

Nordics

Retail Value ($M)

USA :DVD rental $6BnBD rental

$0.43BnOnline VoD

$0.12BnTV VoD $1.3Bn

TV VoD

Online VoDBlu-

Ray DV

DTV VoD

Online VoDBlu-

Ray DV

D

DVD

Online VoDBlu-

Ray

TV VoD

TV VoD

Online VoDBlu-

Ray DV

D

© 2010 Futuresource Consulting Ltd

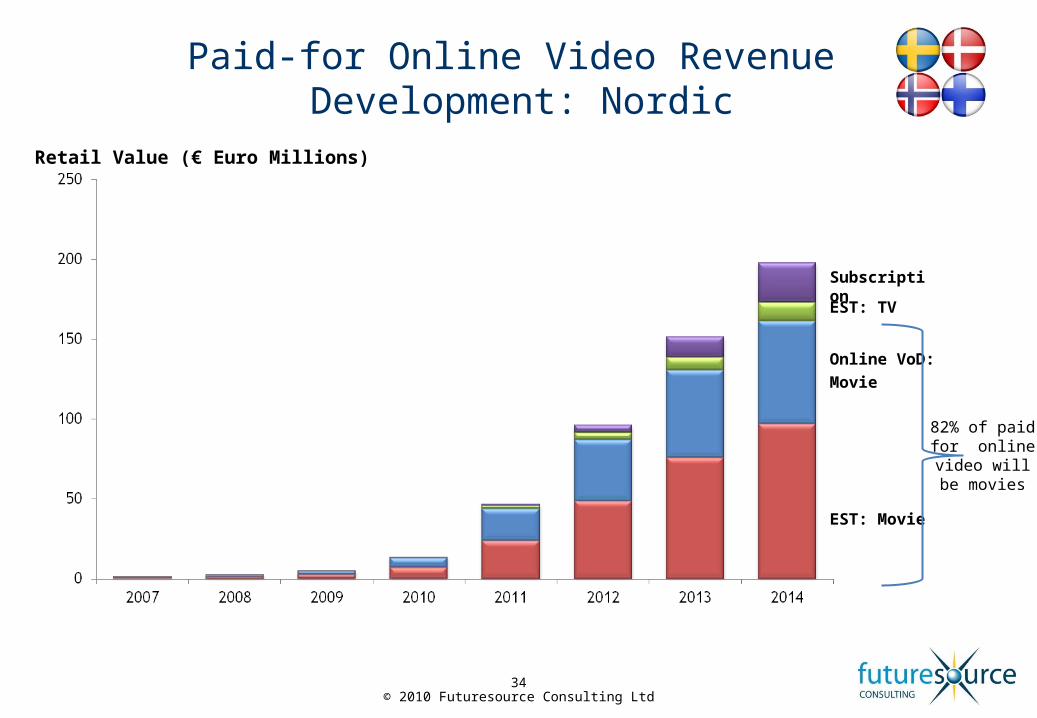

Paid-for Online Video Revenue Development: Nordic

34

EST: Movie

SubscriptionEST: TV

Online VoD: Movie

82% of paid for online

video will be movies

Retail Value (€ Euro Millions)

© 2010 Futuresource Consulting Ltd

UK

ITALY

GERMANY

NORDICS

SPAIN

FRANCE

NB: Some services will offer a mix of paid-for, free and ad-supported online video content

35

Online Video Services Struggling to Generate Revenues: Western Europe

© 2010 Futuresource Consulting Ltd

Contracting Movie Release Windows Boost Online VOD: Western Europe

36

Theatrical*

DVD Sell-Through & Rental & Electronic Sell-Through

TVoD & Online VoD

NVoD/PPV

1st Pay-TV

Typical Release Window (Months)

TVoD & Online VoD Library

Free to Air & Subscription VoD

Window

2nd Pay-TV / Holdback

period

Blackout

4 6 9 12 24Launch

*Theatrical windows on Disney’s Alice in Wonderland 10 weeks

Warner 100% D&D. Sony most titles, other majors experimenting on title by title basis

Rental service subscribers must wait 2-3 years to see titles online on a subscription basis

© 2010 Futuresource Consulting Ltd

Devices Are All Becoming IP Enabled, Significantly Increasing Online Content Opportunities:

Western Europe

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010 2011 2012 2013

Hou

seho

ld P

enet

rati

on (%

)

Games Consoles Pay-TV STB/ PVR*Digital Media Adaptors TV DisplaysBlu-ray Live Players

2013 Household Penetration

2013 Household Penetration

Digital Media Adaptors

Digital Media Adaptors

Pay-TV STB/DVRPay-TV

STB/DVR

Blu-Ray PlayersBlu-Ray Players

*Pay-TV STB/PVR includes all boxes with Ethernet input across IPTV/Cable/Satellite.

Game Consoles

Game Consoles

TV DisplaysTV Displays

37

45%

43%

36%

25%

7%

© 2010 Futuresource Consulting Ltd

Leading Connected TV Services & Online Video Partners

38

TV Brand Service Name Key Online Video Partners USA Launch

Europe Launch

USA H1 ‘09 Share

W Europe H1 ‘09 Share

Bravia Internet Video (Currently Applicast in

Europe, to be renamed in Q1 2010)

YouTube, DailyMotion, Channel 5 (UK), Mediaset (Italy). Amazon,

Yahoo! (Both USA)

Feb 2009 Feb 2009 (Applicast)

12% 11%

Viera Cast YouTube, Amazon (USA), Eurosport, ZDF (Ger), RTVE (Spain),

Bild (Ger)

May 2008

May 2009 9% 8%

Internet@TV YouTube, Yahoo!, BBC iPlayer expected in UK, Blockbuster,

Amazon (both USA)

May 2009

May 2009 21% 22%

NetCast YouTube, Netflix, Yahoo! , Vudu, Maxdome (Ger)

May 2009

Set for early 2010

10% 14%

Net TV (Europe Only) YouTube, Dailymotion, NRJ - April 2009 3% 15%

Market Share based on total TV Shipments, including both connected TVs and standard TVs

© 2010 Futuresource Consulting Ltd

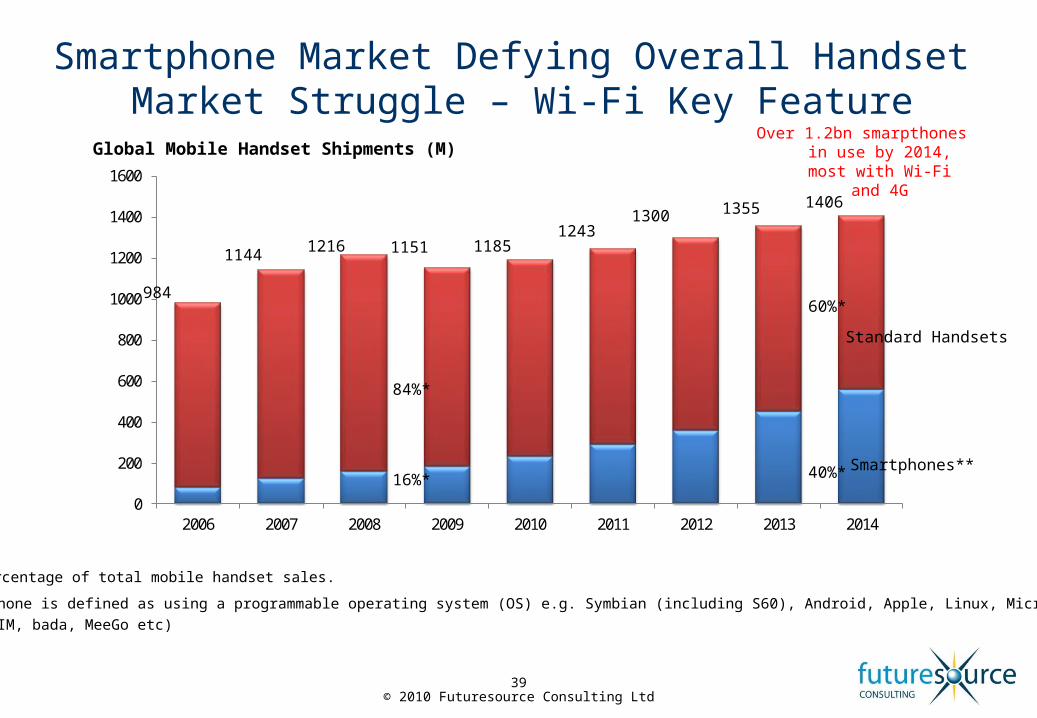

0

200

400

600

800

1000

1200

1400

1600

2006 2007 2008 2009 2010 2011 2012 2013 2014

984

1144 1216 1151 11851243

1300 1355

84%*

16%*

60%*

40%*

1406

Smartphone Market Defying Overall Handset Market Struggle – Wi-Fi Key Feature

Global Mobile Handset Shipments (M)

Smartphones**

Standard Handsets

**A smartphone is defined as using a programmable operating system (OS) e.g. Symbian (including S60), Android, Apple, Linux, Microsoft, Palm, RIM, bada, MeeGo etc)

*Percentage of total mobile handset sales.

Over 1.2bn smarpthones in use by 2014, most

with Wi-Fi and 4G

39

© 2010 Futuresource Consulting Ltd

Apple’s Market Share Grew From 9 to 14% in 200950 Million iPhones In Use Globally

40

Nokia 38% (38%)

Blackberry 19% (15%)

Others 18% (26%)

Samsung 3% (3%)

Total Smartphone Shipments 2009: 180 m

HTC 6% (7%)

Palm 2% (2%)

Apple 14% (9%)

2008 figures in brackets

Apple hardware owners significantly more likely to pay for content online.

© 2010 Futuresource Consulting Ltd

Leading Application Stores Overview

41

Apple App Store

Android Market BB App World

Nokia Ovi Store

Palm App Catalogue

Windows Marketplace

Launch Date

July 2008 October 2008 April 2009 May 2009 June 2009 October 2009

Number of Apps Available to Date

>185,000 >50,000 >6,500 >9,500 >2000 >1500

Total Downloaded Apps to Date

>4 billion >500 million Undisclosed >100 million >35 million Undisclosed

Supported Platforms

iPhone OS X Android OSBlackBerry

OS

Flash Lite, Java, Symbian

OSPalm webOS

Windows Mobile OS

Revenue Split

Developers receive 70%

Developers receive 70%

Developers receive 80%

Developers receive 70%

Developers receive 70%

Developers receive 70%

Updated April 2010

© 2010 Futuresource Consulting Ltd

2007 2008 2009 2010 2011 2012 2013

Other Paid-For Apps 0.0 0.0 1.0 2.4 4.4 7.3 9.9Mobile Apps Games 1.3 2.6 4.3 6.0 7.4Mobile Games* 3.6 4.2 4.3 4.5 4.7 4.9 5.0Mobile Video 2.7 3.4 3.9 4.6 5.5 6.8 8.0Mobile Music and Ringtones 5.8 6.1 6.1 6.1 6.5 7.0 7.6

0

5

10

15

20

25

30

35

40

12.113.7

16.6

20.3

25.3

32.0

37.9

Mobile Content Market Re-Invigorated by Apps

42

Global Consumer Spend ($ Billions)

© 2010 Futuresource Consulting Ltd

In Conclusion…

DVD now in single digit decline in most marketsUptake of Blu-ray slower than anticipated

Relationship with hardware different to DVDMarketing initiatives key to driving disc uptake

Massive consumer interest in 3D3D TVs, 3D BD players and PS3 consoles will drive 3D in the home2011 and beyond 3D will boost Blu-ray disc sales

Watching video online is now a mass market activity but mostly no one is paying

Major challenge is to develop models for digital that generate revenue

Next 5 years a major transition period from physical to digitalBroadcasters will be key in online deliveryPackaged media will remain strong if pricing and retail distribution strategies are carefully managed

43

© 2010 Futuresource Consulting Ltd44

Thank you!

Futuresource Consulting+44 (0)1582 500 [email protected]

While every effort is made by Futuresource Consulting Ltd to provide accurately researched information and carefully supported conclusions and recommendations to its client, in no event will the company or its professionals be liable for information, analysis, advice or recommendations provided to the client at any stage of the project, or be liable for actions and decisions taken as a result of this report.