Embed Size (px)

Citation preview

296

CHAPTER 7

DATA ANALYSIS

Index :

7.1 Introduction 297

7.2 Member Brokers Questionnaire and Analysis of the Data 297

7.3 Investor’s Questionnaire and Analysis of the Data 331

297

CHAPTER 7

DATA ANALYSIS

7.1 Introduction:

It is necessary to understand the opinions of the brokers and the

investors about the equity derivatives market it was felt necessary to collect

data through questionnaires. It was also important to gather the primary data

from the brokers and the investors in the equity derivatives markets to

formulate the opinion about the issues, concerns and other relevant changes that

could be suggested in the equity derivatives markets. For the purpose, there

were two types of structured questionnaires prepared to gather the primary data,

one for the investors and the other for the members/stock brokers. The data was

sought from the investors and the member brokers in the physical as well as the

online mode. The details of the questionnaire and the analysis of the data are

elaborated in this chapter.

7.2 Member Brokers Questionnaire and Analysis of the Data:

The primary information was also sought from the brokers in the equity

derivatives market though the interviews, meetings and online mode. Largely

the data was gathered through the circulation of questionnaire in the online

mode from the nationwide network of the brokers. The questionnaire was

designed to understand the type of broking entity and which exchanges it is

registered on, types of clients they deal with and through which mode etc. The

questionnaire further focused on seeking opinion on need of certified dealers

operating the terminals, only certified retail investors, allowing options to

clients and their profiling, preference of equity derivative product for

investment and periodicity of contracts preferred by clients, purpose of trading

and any strategies adopted for the same by clients, opinion on contract size,

risks of concern, margining system for brokers and margins levied, effective

utilization of capital deployed, risk management system, need to increase the

stocks in the equity derivatives market, need for wide basket of products, need

298

to reduce the transaction cost, need to change in the regulation style, need for

OTC derivatives market in India like global markets etc.

For the purpose of collection of primary data from the brokers, a

questionnaire was collected from stock brokers across the broking industry

spread across India. The questionnaire form was sent to all the broking

members in the industry. The help was also taken from Association of National

Exchanges Members of India (ANMI), a PAN India body comprising of the

trading members of National Stock Exchange of India Limited (NSEIL) and

Bombay Stock Exchange (BSE) spread across the country to circulate the

questionnaire form to all the brokers in the broking fraternity.

There were 903 and 1329 equity derivatives brokers registered as of

December 2011 for trading in the equity derivatives segment of BSE and NSE

respectively. Most of the brokers have obtained registration on both the

exchanges in the equity derivatives segment. As an intensive study of

derivatives market in India, for the purpose of study the questionnaire was

sought from all the brokers keeping in mind to cover at least 5% brokers, i.e. 66

brokers of NSE and 45 brokers of BSE as sample respondents, with a view to

project working of the derivatives market in India, understand trends observed

and the problems faced by them. However, since responses to the questionnaire

could be collected from 80 brokers of NSE and 65 brokers of BSE, all these

responses to the questionnaire were taken as a sample. These respondents’

practical exposure helped in understanding the problems and prospects of

derivatives market in India.

However, due to company policies, many broking outfits and officials

could not express the view of the organization and hence large number of these

responses were mentioned to be their personal view and not of the company. With

this caveat, the responses were evaluated. The revelations of the responses to the

questionnaires have been evaluated and tabulated below under various heads:

1. Break up of equity broking entities as per their membership on Indian

Exchange(s):

As mentioned earlier, there were 80 respondents who provided

responses to the questionnaire. The brokers can obtain various types of

memberships as described in the earlier chapter like Limited Trading

Membership, Trading membership clubbed with Self Clearing Membership,

299

Trading and Clearing membership and Professional Clearing membership.

Some of these broking entities are brokers on both the exchanges i.e. BSE

and NSE as well. The table given below shows that some of the broking

entities has obtained multiple memberships on the exchanges:

Table 7.1

Category-wise Break-up of respondent brokers of equity derivatives

memberships

Equity Derivatives

Membership Response Percent Response Count

BSE (Limited TM) 2.5% 2

BSE (TM) 45.0% 36

BSE (T & CM) 37.5% 30

BSE (SCM) 6.3% 5

BSE (PCM) 0.0% 0

Total BSE Respondents 65

NSE (TM) 50.0% 40

NSE (T & CM) 53.8% 43

NSE (SCM) 22.5% 18

NSE (PCM) 1.3% 1

Total NSE Respondents 80

Source: Questionnaire

There were 65 brokers of BSE and 80 brokers of NSE who

responded to the questionnaire. As can be seen from the above table, there

were large respondents who were TMs i.e. 50% in NSE and 45% in BSE

and T&CMs i.e. 53.8% in NSE and 37.5% in BSE. There were also no

brokers having PCM membership on BSE amongst the respondents. The

representation in the bar chart form is given below:

Chart 7.1

Category-wise Break-up of respondent brokers of equity derivatives

memberships

Source: Questionnaire

300

2. Category of Clients the broking entities deal with

The broking entities deal with various types of clients such as FIIs,

Sub-accounts, Financial Institutions, Non Resident Indians (NRIs), High

Net-worth Individuals (HNIs), Retail Clients etc. The researcher had asked

the equity derivatives brokers about the type of clients they deal with in

order to understand the nature of brokers responding to the questionnaire to

evaluate need to expand the sample if required to make the same broad

based. The answers received to the subsequent questions then would be

responded by the respondents based on their experiences of dealing with

these different types of clients. The following table gives the break-up of

category of clients the brokers deal with:

Table 7.2

Category of Clients the broking entities deal with in the equity

derivatives market

Responses Response

Percent Response Count

Institutional Clients (FIIs, Sub-accounts) 58.8% 47

Financial Institutions, Mutual Funds 66.3% 53

NRI clients 77.5% 62

HNI Clients 85.0% 68

Retail Clients 77.5% 62

Total Responses 80

Source: Questionnaire

As can be seen from the above table, large number of brokers who

filled up the questionnaire dealt with HNI clients (85%), followed by Retail

and NRI clients (77.5%), then with Financial Institutions, Mutual Funds

(66.3%) and lastly with Institutional Clients (FIIs, Sub-accounts) (58.8%).

Thus, the respondent base is broad based and they dealt with varied set of

clients in their equity derivatives dealing on day to basis. Hence, the

answers to the subsequent questions would be broad based and taking into

considerations the experiences of these brokers in dealing with such a

varied set of clients.

The column chart given below shows the breakup of various

categories of clients the respondents who filled up the questionnaire deal

with:

301

Chart 7.2

Category of Clients the broking entities deal with in the equity

derivatives market

Source: Questionnaire

It can be seen from the above chart that more than 50% of the

respondents have dealt with all the set of clients in the equity derivatives

market such as Institutional Clients, Financial Institutions, NRI clients, HNI

clients and retail clients. Thus, the respondent broker’s base is broad based.

3. Certification of dealers operating trading terminal in equity derivatives

segment:

At the time of allowing derivatives market in India, as

recommended in the L. C. Gupta committee report, SEBI has mandated all

the dealing terminals should be operated by only the derivatives certified

persons. This was the requirement in 2000, when many people did not have

any knowledge about the derivatives market and the products in the

derivatives market. Also, if the persons manning the dealing terminals did

not have basic knowledge about the derivatives market, the risk that can

pose to the market could be huge. Besides, this there were also chances of

mis-selling of the derivatives products to the investors. Hence, at that point

of time there was a need felt to allow only derivatives certified persons to

operate the dealing terminal. For this purpose, NSE and BSE have put in

place a facility for testing and certification by launching NSE's Certification

in Financial Markets (NCFM) and BSE's Certification on Financial Markets

(BCFM) respectively.

302

The NCFM and BCFM are an online testing and certification

programmes. These programmes test the practical knowledge and skills

required to operate in the financial markets. Tests are conducted in a

secured and unbiased manner and certificates are awarded based on merit of

the candidate to qualify the on-line test. The exchanges offer a certification

in Derivatives Market (Dealers) Module for the dealers. These certificates

are valid for a period of three years which can further be renewed for a

period of two years.

The brokers have grown in size and stature over a period of time.

Today, big brokers have thousands of terminals operated PAN India either

from their own office or from their branches or the sub-broker/Authorized

Person’s network. There is also responsibility casted on the brokers for

resolution of any grievances from the clients with regard to any act of either

their employee or by any other associated individuals/entities in any

capacity with them. Thus, it was felt necessary by the researcher to

understand from the broker’s to understand whether such a certification

should be made mandatory or this requirement over a period of time has

lost its significance and the guidelines in this regard need to be relaxed.

Hence, for this purpose the brokers were asked to respond to the

appropriateness of the requirement of only certified dealers should be

operating the terminal in today’s scenario. The outcome of the responses to

the questionnaire is as follows:

Table 7.3

Requirement of operating trading terminal in equity

derivatives segment by only certified dealers is Appropriate

Responses Response Percent Response Count

YES 81.3% 65

NO 18.8% 15

Total Participants 80

Source: Questionnaire

The representation of the responses as tabulated above is presented

in the Pie Chart form below:

303

Chart 7.3

Need of operating trading terminal in equity derivatives segment by only

certified dealers is appropriate

Source: Questionnaire

As can be seen for the above table and chart, 81.3% of the brokers

feel that the terminals should be operated by certified dealers only. It is only

18.8% of the respondents who feel otherwise. The main reason for large

number of respondents feeling the need is that any misconduct or mistake

of the dealers, the broker is responsible/ liable for their actions. They also

understand that the chances of certified dealers doing the mistake are less

than the completely naïve dealer. Thus, a large number of brokers support

the requirement of the only certified dealers operating the trading terminal.

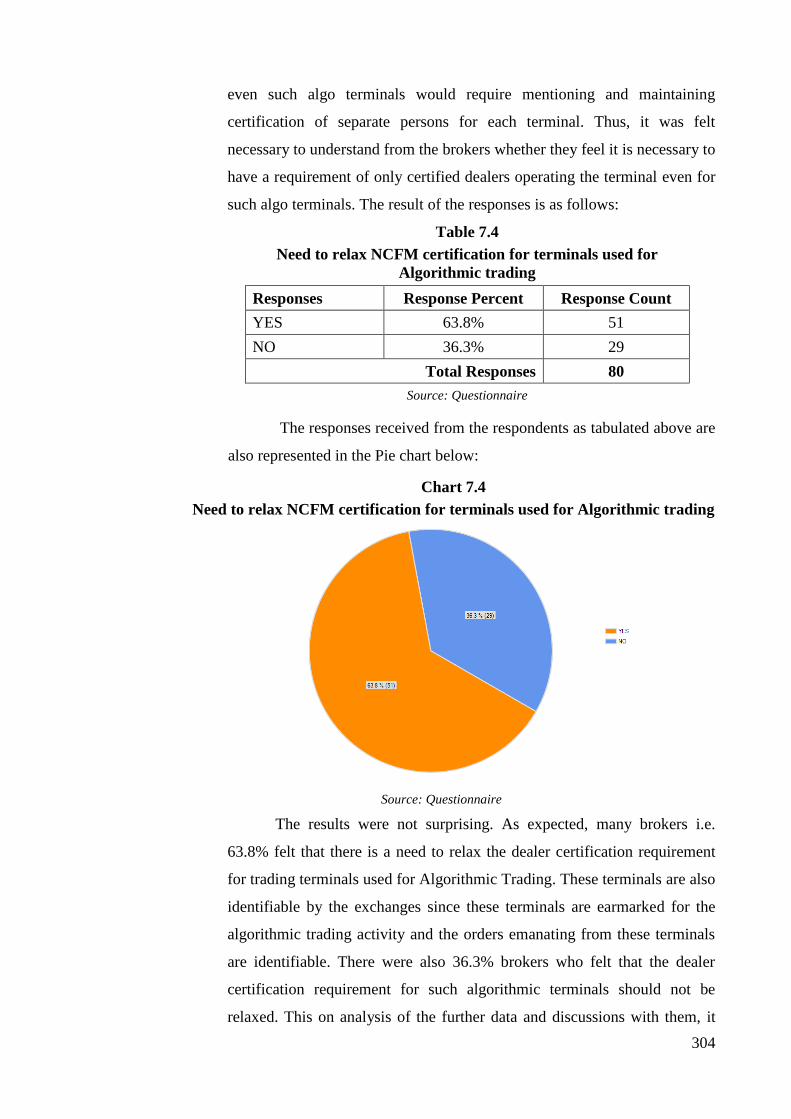

4. Certification requirement for the algorithmic terminals:

One is able to understand the comfort of the brokers drawing from

the fact that only the certified dealers are manning the terminals will reduce

the mistakes such as punching errors, not misunderstanding the premium

per lot with per share etc. However, today with the advancement of

technology and the class of High Frequency Traders, the trading activity

pattern has been shifting to automated trading activity through system build

algorithms which is also called as algorithmic trading. In the algorithmic

trading, there is no manual intervention of the dealers for placing the orders

as the orders are placed by the system itself based on the built in logic and

parameters set.

As per existing requirement, any new terminal in the equity

derivatives segment is allotted only to the person who is certified. Hence,

304

even such algo terminals would require mentioning and maintaining

certification of separate persons for each terminal. Thus, it was felt

necessary to understand from the brokers whether they feel it is necessary to

have a requirement of only certified dealers operating the terminal even for

such algo terminals. The result of the responses is as follows:

Table 7.4

Need to relax NCFM certification for terminals used for

Algorithmic trading

Responses Response Percent Response Count

YES 63.8% 51

NO 36.3% 29

Total Responses 80

Source: Questionnaire

The responses received from the respondents as tabulated above are

also represented in the Pie chart below:

Chart 7.4

Need to relax NCFM certification for terminals used for Algorithmic trading

Source: Questionnaire

The results were not surprising. As expected, many brokers i.e.

63.8% felt that there is a need to relax the dealer certification requirement

for trading terminals used for Algorithmic Trading. These terminals are also

identifiable by the exchanges since these terminals are earmarked for the

algorithmic trading activity and the orders emanating from these terminals

are identifiable. There were also 36.3% brokers who felt that the dealer

certification requirement for such algorithmic terminals should not be

relaxed. This on analysis of the further data and discussions with them, it

305

was found out that many of them who were not in favor of such relaxation

do not use any such algorithmic trading systems.

Thus, it is felt that the regulatory body may like to revisit the

requirement with regard to the dealer certification requirement for the

terminals used for algorithmic trading.

5. Opinion on Basic Test requirement for admitting clients in the Equity

Derivatives

Derivatives per se are considered to be complex products. Hence, it

is also presumed that many investors and clients do not understand this

product and the investment techniques. Many of them are also not familiar

with the terminologies used in the equity derivatives and the risks involved

in trading in the derivatives markets. It has also been seen from many

complaints filed by the investor that the investors were completely unaware

of the derivatives products but were still trading without understanding the

risks and consequences of trading in derivatives. Thus, it was felt necessary

to understand from the brokers whether it would be prudent to make it

mandatory for all derivative investors to take up the basic derivatives test

before allowing them to trade in the equity derivatives market. The results

of the questionnaire are as follows:

Table 7.5

Opinion on Basic Test requirement for admitting clients in the

Equity Derivatives

Responses Response Percent Response Count

YES 71.3% 57

NO 28.8% 23

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above are

also presented in the Pie chart below:

306

Chart 7.5

Opinion on Basic Test requirement for admitting clients in the Equity

Derivatives

Source: Questionnaire

As can be seen from the above table and the chart, 71.3%

respondents feel that there should be basic test taken up by the investors

before them being allowed to trade in the equity derivatives market for the

first time trading where as only 28.8% do not feel for such a need.

Considering the above responses, the regulators may like to evaluate such

requirement and may like to evaluate the manner in which the test can be

carried out since this requirement also should not become a stumbling block

for investors to participate in the market and keep away large number of

first time investors from the equity derivatives market. The test may cover

various aspects like products in the equity derivatives, margin requirements,

their rights and obligations, risks associated with the derivatives trading etc.

The process can be made easy by allowing the clients to take up the test

online and may be of a very short duration.

6. Need to restrict certain set of investors from trading in the Options

The options are leveraged product. Leverage is used to amplify

investment gains and losses on money invested. The buyer of the option has

to pay only the premium and can have unlimited upside. However, seller of

the option receives only the premium amount involved but in the adverse

scenarios there could be unlimited downside to the seller. Thus, the options

are risky for seller of the options and if the investors are naïve and do not

understand the product he/she may wipe out the entire funds available with

him/her and sometimes may end up into debt. Thus, it was considered to

307

understand from the respondents whether the options should be restricted to

certain set of clients, say those clients with high risk appetite, those with the

income above some threshold and such other criteria. The outcome of the

responses to the questionnaire was very surprising. The same has been

tabulated below:

Table 7.6a

Option trading be restricted to certain set of investors

Responses Response Percent Response Count

YES 50.0% 40

NO 50.0% 40

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.6a

Option trading be restricted to certain set of investors

Source: Questionnaire

As mentioned earlier, the result was really surprising. There was no

conclusion that could be drawn from the questionnaire. 50% of the

respondents felt that options should be restricted to certain set of investors

and other 50% felt that options trading should not be restricted to any

investors. This could be analysed in light of the recent trading pattern where

in FY 2011-12, 72% of the trading volume is attributed to the Index options

trading and around 3% trading has taken place in Stock Options. Thus,

options trading accounted for almost 75% of the total market volume during

the FY2011-12. This also means a generation of revenue for the brokers. In

308

the event any set of clients are restricted, it would also affect the income of

the brokers. This could be one of the reasons to explain the outcome. There

are also few brokers who service mainly institutional clients and may not

get affected by any guideline in this regard. However, keeping in mind the

risk that is involved in selling the option for the small investor or who have

got very low risk appetite, it would be prudent to introduce such a

restriction which may get extended to sell side only.

The researcher also tried to find out whether the above suggestion

given is enforceable since the brokers are required to know the risk appetite

of the clients through client profiling, if the suggestion is to be implemented.

Thus, question was asked on whether the brokers currently carry out any

profiling of their clients before allowing them to trade in the equity

derivatives. The outcome of the responses to the questionnaire is as follows:

Table 7.6b

Client profiling is carried out before allowing any clients to trade

in equity derivatives

Responses Response Percent Response Count

YES 83.8% 67

NO 16.3% 13

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.6b

Client profiling is carried out before allowing any clients to trade in equity

derivatives

Source: Questionnaire

309

As can be seen from the above table and chart, the client profiling is

carried out of the client by almost 83.8% of the respondents. It is only

16.3% of the respondents do not carry out any such client profiling, some of

these are dealing with only the institutional clients hence does not require to

carry out any client profiling for them. Hence, it can be concluded that

almost all of the brokers are already carrying out the client profiling of

clients to understand the client’s risk appetite and to understand the

suitability of the products offered to them.

7. The product preferred by the clients of the brokers:

Even though, it has been tried to find out from the investors directly,

an attempt was made to find out from the brokers the most preferred

product of their clients. It was found out that in line with the trading pattern

exhibited on the exchange platform the most preferred product by the client

is Index Options. The results of the responses to the questionnaire have

been tabulated below:

Table 7.7

The most preferred type of product used by clients in

Equity Derivatives

Answer Options Response Percent Response Count

Index Futures 22.5% 18

Index Options 63.8% 51

Stock Futures 10.0% 8

Stock Options 3.8% 3

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.7

The most preferred type of product used by clients in Equity Derivatives

Source: Questionnaire

310

As can be seen from the above table and chart, the respondents

mentioned that 63.8% of the clients prefer index options, followed by

22.5% of the clients preferring index futures, then 10% of the clients

preferring stock futures and lastly 3.8% clients preferring stock options.

Thus, respondents mentioned that the most preferred by their clients are

Index Options, followed by Index Futures, then Stock Futures and lastly the

Stock Options.

8. Type of trading activity for which equity derivatives products used by

investors:

There are various types of activities for which the product can be

used such as for speculation, hedging and arbitrage activities. The

researcher tried to understand the type of activities from the brokers for

which the derivatives products are used by the investors. The outcome of

the responses to the questionnaire is tabulated below:

Table 7.8

Type of trading activity for which equity derivatives

products used by investors

Responses Response Percent Response Count

Hedging 73.8% 59

Speculation 91.3% 73

Arbitrage 42.5% 34

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Column Chart below:

Chart 7.8

Type of trading activity for which equity derivatives products used by investors

Source: Questionnaire

311

As can be seen from the above table and chart, most of the investors

prefer all kinds of trading activity at different points of time. Outcome

shows that 91% of the investors carry out the trading activity of speculative

nature, followed by hedging activity which is also carried out by 74%

investors and then the arbitrage activity which is carried out by 42% of the

investors at some point of the time or other.

9. Various strategies used for Equity Derivatives Trading by investors:

There are many strategies that can be used in the equity derivatives

market depending upon the market scenario, risk appetite of the investor

and the outlook on the future of the market. The researcher tried to find out

from the brokers which are the strategies that are normally used by the

clients of the brokers at various points of time. The outcome of the

responses to the questionnaire is as follows:

Table 7.9

Various strategies used for equity derivatives trading by

investors

Responses Response Percent Response Count

Straddle 23.8% 19

Strangle 18.8% 15

Protective put buying 3.8% 3

Protective call buying 3.8% 3

Covered call writing 20.0% 16

Collar 1.3% 1

Covered put writing 12.5% 10

Reverse Collar 1.3% 1

Butterfly Spread 13.8% 11

Condor 5.0% 4

Strip 0.0% 0

Strap 0.0% 0

None of the strategy used 17.5% 14

Almost all the strategies

used at some point 56.3% 45

Other (please specify) 4

Total Responses 80 Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Column Chart below:

312

Chart 7.9

Various strategies used for equity derivatives trading by investors

Source: Questionnaire

As can be seen from the above, the respondents have indicated that

56.3% of the times clients use almost all these strategies at some point or

the other. There are 17.5% of the respondents who are of the opinion that

the clients do not use any strategy but merely trade in the market. This can

be for the intraday speculation in the derivatives product. As per

respondents, the other strategies used were straddle by 23.8% times by

clients, covered call writing by 20% times by clients, strangle by 18.8%

times by clients, butterfly spread by 13.8% times by clients, covered put

writing by 12.5% times by clients and remaining various other strategies by

less than 5% times by clients. This indicates that there are large number of

investors who are now familiar with of the equity derivatives market and

products and are also familiar with the various strategies that can be applied

while trading in the equity derivatives market.

10. Need for reduction in contract size for stock and index derivatives

contracts to get larger participation

The contract size since the beginning of the equity derivatives

trading in India was standardized at the value of Rs. 2 lacs. Subsequently, in

December 2007 the mini contracts only on the stock indexes with the

contract size value of reduced to Rs. 1 lac were allowed by SEBI. However,

313

these mini contracts now have been banned by SEBI since November 30,

2012. Thus, it was felt necessary to understand from the brokers whether

there is any need to revisit the contract size now after the market has been

matured for over a decade. The results of the responses received for this

question are tabulated below:

Table 7.10a

Need for reduction in contract size for stock and index

derivatives contracts

Responses Response Percent Response Count

YES 50.0% 40

NO 50.0% 40

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.10a

Need for reduction in contract size for stock and index derivatives contracts

Source: Questionnaire

It was surprising to see that the broker’s opinion on whether the

contract size value should be reduced has been equally divided in the ratio

of 50:50. Further, in order to understand the contract size value that would

be found appropriate by the brokers, the brokers were asked to indicate the

contract size value considered to be suitable by them.

These respondents who had indicated that they preferred reduction

in the contract size indicated various options below Rs. 2 lacs of values and

other indicated more than Rs. 2 lacs of value options. The results from the

respondents were as follows:

314

Table 7.10b

Contract size (in terms of contracts value) appropriate for derivatives

contracts

Responses Response Percent Response Count

Upto Rs. 10,000/- 1.3% 1

Rs. 10,001/- to Rs. 50,000/- 5.0% 4

Rs. 50,001/- to Rs. 1,00,000/- 20.0% 16

Rs. 1,00,001/- to Rs. 2,00,000/- 28.8% 23

Rs. 2,00,001/- to Rs. 4,00,000/- 40.0% 32

Above Rs. 4,00,001/- 5.0% 4

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.10b

Contract size (in terms of contracts value) appropriate for derivatives contracts

Source: Questionnaire

It is very interesting to see that 50% of total respondents felt that

there was no need to reduce the contract size value to attract more

participation in the equity derivatives trading. They felt that the contract

size of Rs. 2 lacs to Rs. 4 lacs would be appropriate. Further, those who felt

that there should be reduction in the contract size value, 57% of them felt

that the contract size should be between Rs. 1 lac to Rs. 2 lacs, 32% of them

felt that the contract size should be between Rs, 50,000/- to Rs. 1 lac.

Thus, if this outcome is seen in combination with the outcome of the

responses to the questionnaire of the investor, there is strong urge felt from

the investor to reduce the size of the contract value to increase participation

in the equity derivatives market from the retail investors.

315

11. Derivatives Exchanges to start physical delivery settlement for equity

derivatives

SEBI vide its circular dated July 15, 2010 allowed the stock

exchanges to start the physical delivery settlement in the equity derivatives

subject to certain conditions laid down by the regulator. BSE started the

physical delivery settlement in February 2011, however in the absence of

any liquidity on the exchange, this product did not click. However, NSE did

not start this product on the exchange platform. Thus, the need was felt by

the researcher to ask the brokers whether NSE starting this product on its

exchange platform could make this product successful and get further

participation from the investors. The outcome of the responses to the

questionnaire is as follows:

Table 7.11

Both the Indian Derivatives Exchanges should start the

physical delivery settlement for equity derivatives

Responses Response Percent Response Count

YES 71.3% 57

NO 28.8% 23

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.11

Both the Indian Derivatives Exchanges should start the physical delivery

settlement for equity derivatives

Source: Questionnaire

316

It can be seen from the above table and the chart that 71.3% of the

respondents feel that both the Indian Derivatives Exchanges should start the

physical delivery derivatives contacts in the Indian market whereas only

28.8% respondents feel that the status quo may be maintained and even

when the exchanges start the physical delivery derivatives contracts on both

the exchanges there may not be many participants who would participate.

12. Efficiency of Current margining system to use the capital of the

brokers

There is considered to be stringent requirement of the capital on the

exchanges. The structure for the equity derivatives market is such that the

Clearing members are required to place adequate capital with the clearing

corporation to enjoy uninterrupted trading access and activity. If the capital

with exchange is short and not made good in time, the exchange may

deactivate such clearing members from further placing/receiving fresh order

and would put the clearing members in the square off mode. Thus, in order

to avoid such situation it is not only the excess capital infusion is necessary,

but it is necessary to understand from the brokers whether the capital placed

by them with the Exchange or the Clearing Corporation is efficiently and

effectively used. The outcome of responses to the questionnaire is as

follows:

Table 7.12

Current margining system is appropriate and it efficiently

uses the capital of brokers

Responses Response Percent Response Count

YES 88.8% 71

NO 11.3% 9

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

317

Chart 7.12

Current margining system is appropriate and it efficiently uses the

capital of brokers

Source: Questionnaire

As can be seen from the above table and the chart, 88.8%

respondents feel that the current margining system effectively uses the

capital deployed by the brokers. It is only 11.3% respondents who feel that

their capital deployed is not effectively used in the current margining

system. There was also one of the suggestions which came from the

respondent that the clearing corporation may consider passing on the

interest earned on the cash deposited with them by the brokers in order to

make the best use of the capital deployed by them. Thus, exchanges may

evaluate this suggestion considering the rules, regulations and bye-laws of

the exchange and the other regulatory guidelines.

13. Adequacy/excessiveness of margins levied in Indian Equity Derivatives

Market

Today, exchanges and clearing corporations collect various types of

margins such as initial margin, premium margin, assignment margins, and

exposure margins from the brokers for the trading activity carried out in the

equity derivates market. It was thus felt necessary by the researcher to

understand from the brokers whether they feel the pinch of margins and

they feel that the margins levied by the exchanges are excessive. The

outcome of the responses to the questionnaire has been tabulated below:

Table 7.13

Margins levied today in Indian Equity Derivatives Market

are excessive

Responses Response Percent Response Count

YES 68.8% 55

NO 31.3% 25

Total Responses 80

Source: Questionnaire

318

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.13

Margins levied today in Indian Equity Derivatives Market are excessive

Source: Questionnaire

It can be seen from the above table and chart that almost 68.8%

respondents feel that the margins charged by the exchanges are excessive

whereas 31.3% of the respondents feel that the margins charged are

appropriate and not excessive. Margins are primary for the risk

management and to ensure smooth functioning of the equity derivatives

market without any default by the brokers and their clients. In light of the

feeling of the market participants, the regulatory body may evaluate

reducing the margin requirements wherever possible by further extending

the benefit of cross margining across exchanges under the same broker or

cross margining benefits for additional products. However, the regulator has

to take a balanced approach and has to also ensure that the collection of

margin is adequate to ensure that there are no defaults on the exchanges and

it does not cause any systemic risk.

14. Strength of the existing risk management system adopted by the

Exchanges

An incident happened on October 05, 2012 when the S&P Nifty, the

benchmark index of NSE, plunged by 900 points, or 16 per cent, within two

minutes at around 9.49 am. The crash wiped out almost over Rs 3 lakh

crores ($58 billion) which was caused by a mere Rs 650 crores sell order by

one of the broker Emkay Global Financial Services.

319

As understood from the news reports, it was a single order that

placed 59 trades at a significantly lower price which pulled down the index

from 5,773 to 4,888. Nifty finally closed at 5,747 on that day after the

market recovery took place when the news of freak trade spread cooling off

the market. The news article further states that the broker wanted to place a

basket sell order for Rs 65 crores for an institutional client but punched in

an order worth Rs 650 crores by error.

As per the existing index filters, the trading on the exchanges should

be halted for an hour if there is a fall of 10% in the Nifty or Sensex before

1.00 pm and for 30 minutes if the limit is breached between 1 pm and 2:30

pm. These norms are similar if indices rise or fall by 15 per cent and 20 per

cent. Thus, in the above instance even when there was fall of 16% before

1.00 pm, NSE halted trades for less than 15 minutes from 9.51 am and

resumed trading at 10:04 am. Besides this, there also should have been

market halt at 10% fall in the index which did not happen till index fell by

16%. Even though, there was no monetary distress caused to the exchange

or there were no defaults, this freak trade has raised the eyebrows on the

shallow depth of the market and the flaws in risk management system.

Thus, it was felt necessary by the researcher to ask the brokers their opinion

on the strength of the risk management system adopted by the exchange.

The outcome of responses to the questionnaire is as follows:

Table 7.14

Strength of the existing risk management system adopted by the

Exchanges

Responses Response Percent Response Count

Excellent 13.8% 11

Strong 66.3% 53

Medium Strong 18.8% 15

Weak 1.3% 1

Very Weak 0.0% 0

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

320

Chart 7.14

Strength of the existing risk management system adopted by the Exchanges

Source: Questionnaire

As can be seen from the above table and the chart, 13.8%

respondents feel that the risk management system adopted by the exchanges

is excellent, 66.3% respondents feel that the risk management system

adopted by the exchanges is strong, and 18.8% feel the same is medium

strong. Thus, largely the respondents feel that the risk management system

adopted by the exchanges is adequate. However, the recent incident pointed

out above where Nifty plunged by almost 16% within two minutes and still

the index filters did not get triggered thereby halting the market nor was

broker’s terminal who placed the orders got deactivated in time revealed

that there are still few gaps in the system and the risk management system

needs to be made robust. The regulatory body and the exchanges need to

take some concrete steps to plug all such loopholes to ensure that the

trading system and the risk management system are strong and robust to

avoid recurrence of such events in future.

15. Risk of the most concern in the equity derivative market to clients /

brokers:

As discussed earlier in the chapters, there are various risks that are

embedded while trading in the equity derivatives segment. They are mainly

Systemic risk, Market risk or Price risk or Potential Loss risk, Settlement

risk, Credit risk or Counterparty Default risk, Liquidity risk, Operational

risk and Legal risk. The researcher hence felt necessary to understand from

the brokers which are the risk that is of their prime concern while trading in

321

the equity derivatives market today. The outcome of responses to the

questionnaire has been tabulated below:

Table 7.15

Type of Risk of most concern in the equity derivative market for

brokers

Responses Response

Percent

Response

Count

Systemic risk 37.5% 30

Market Risk/Price Risk/Potential Loss Risk 41.3% 33

Settlement risk 1.3% 1

Credit Risk/Counterparty Default risk 1.3% 1

Liquidity Risk 8.8% 7

Operational Risk 10.0% 8

Legal Risk 0.0% 0

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.15

Type of Risk of most concern in the equity derivative market for brokers

Source: Questionnaire

As can be seen from the above table, the respondents today are more

concerned about Market Risk/Price Risk/Potential Loss Risk which

accounts as a concern of almost 41.3% respondents, followed by Systemic

Risk which accounts as a concern of almost 37.5% respondents and then the

Operational Risk which accounts as a concern of almost 10% respondents.

The other risks such as settlement risk, credit risk/counterparty default risk

and operational risk account for 11.4% respondents. There has not been any

concern on the Legal Risk by any respondents. This is due to the fact that

322

all the contracts are now standardized and structured as per guidelines of the

regulatory body, thereby leaving no scope for the legal risk.

16. Revisit to the criteria for inclusion of the stocks in the equity

derivatives market:

SEBI has laid down the criteria for inclusion of stocks in the equity

market derivatives and the same has been modified from time to ensure the

sanctity of the market. At the time of introduction of the equity derivatives

on the single stocks in 2001-02, there were 31 stocks included in the list.

Slowly and steadily as the regulatory body and the exchanges drew comfort

from the market functioning, the number of stocks in the equity derivatives

list went on increasing 265 in 2007-08 and has now again come down to

151 stocks. Thus, it was felt necessary to understand from the market

participants that whether the criteria adopted today for inclusion of the

stocks is appropriate to maintain the same list of stocks or the same should

be made further stringent to reduce the stocks in the list or should be

relaxed to increase the number of stocks in the list on which equity

derivatives are traded. The outcome of responses to the questionnaire was

as follows:

Table 7.16

The criteria for inclusion of the stocks in the equity derivatives

market

Responses Response

Percent

Response

Count

Be diluted to include more number of stocks 55.0% 44

Be made stricter to reduce number of stocks 22.5% 18

Remain as it is (the current universe of stocks is ok) 22.5% 18

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

323

Chart 7.16

The criteria for inclusion of the stocks in the equity derivatives market

Source: Questionnaire

As can be seen from the above table and the chart, there are 55%

respondents who feel that the criteria for selection/inclusion of the stocks in

the equity derivatives market should be relaxed and more number of stocks

should be included. Also, 22.5% of the respondents felt that the criteria

should be stringent and the number of stocks currently covered under the

equity derivatives coverage should be reduced further, whereas the same

22.5% of respondents felt that the criteria adopted today is good and it

should remain same, at the same time retaining the similar number of stock

universe being covered under the equity derivatives market. Thus, it is felt

that the SEBI and the Exchanges may revisit the criteria adopted today for

selection/inclusion of the stocks in the equity derivatives market to include

few more stocks in the list to provide additional stock contracts to trade to

the market participants.

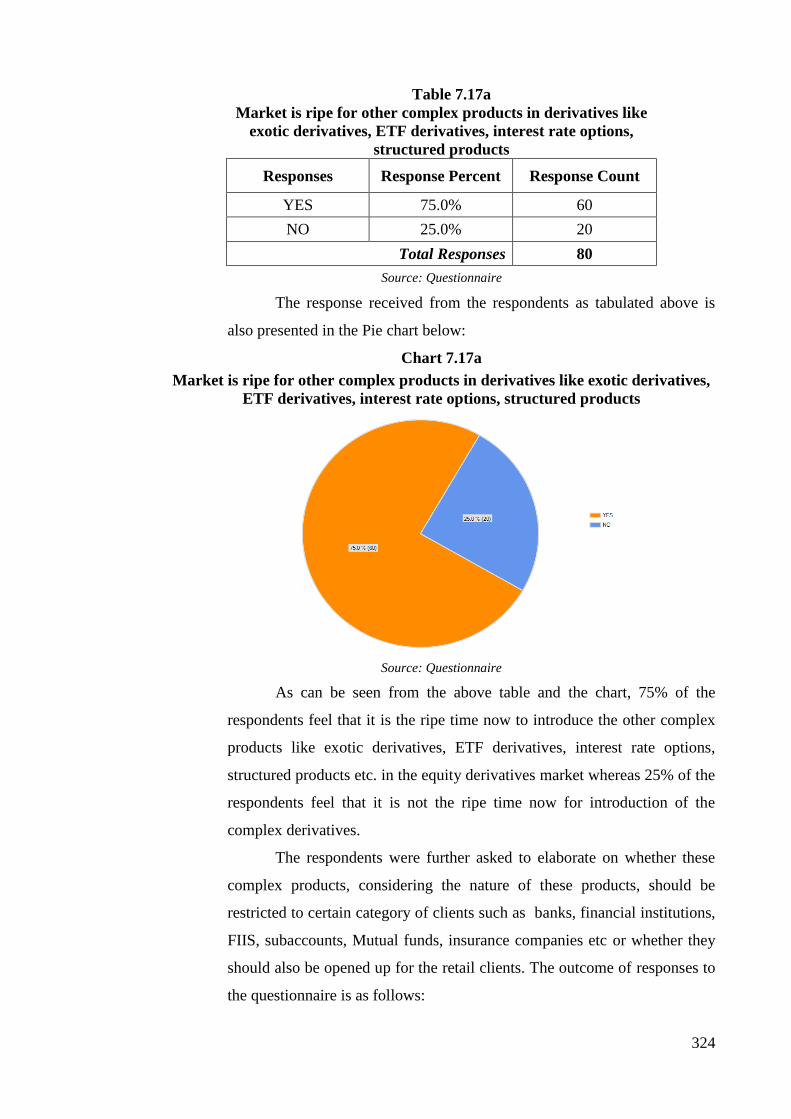

17. Readiness of market for other complex products in derivatives:

It has now been more than a decade since equity derivatives have

been launched in the Indian markets and there are still limited products on

the stock exchanges available for trading to the investors. The respondents

were also asked whether the time is ripe introduce other complex products

such as exotic derivatives, ETF derivatives, interest rate options and the

structured products etc. the outcome of responses to the questionnaire is as

follows:

324

Table 7.17a

Market is ripe for other complex products in derivatives like

exotic derivatives, ETF derivatives, interest rate options,

structured products

Responses Response Percent Response Count

YES 75.0% 60

NO 25.0% 20

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.17a

Market is ripe for other complex products in derivatives like exotic derivatives,

ETF derivatives, interest rate options, structured products

Source: Questionnaire

As can be seen from the above table and the chart, 75% of the

respondents feel that it is the ripe time now to introduce the other complex

products like exotic derivatives, ETF derivatives, interest rate options,

structured products etc. in the equity derivatives market whereas 25% of the

respondents feel that it is not the ripe time now for introduction of the

complex derivatives.

The respondents were further asked to elaborate on whether these

complex products, considering the nature of these products, should be

restricted to certain category of clients such as banks, financial institutions,

FIIS, subaccounts, Mutual funds, insurance companies etc or whether they

should also be opened up for the retail clients. The outcome of responses to

the questionnaire is as follows:

325

Table 7.17b

Complex products be opened for institutional players and not

to retail clients

Responses Response Percent Response Count

YES 85.0% 68

NO 15.0% 12

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.17b

Complex products be opened for institutional players and not to retail clients

Source: Questionnaire

It can be seen from the above table and the chart that almost 85% of

the respondents feel that these complex products should be restricted to

only banks, financial institutions, FIIs, Sub-accounts, Mutual Funds,

Insurance companies etc. It was only 15% of the respondents felt that these

products also should be extended to retail clients as well. Thus, since many

respondents feel that it is ripe time to introduce the other complex products

like exotic derivatives, ETF derivatives, interest rate options, structured

products etc. in the equity derivatives market, the Regulatory body and the

exchanges may like to consider introducing these complex products in the

market restricting them to only the category of investors like banks,

financial institutions, FIIs, Sub-accounts, Mutual Funds, Insurance

companies etc and not to the retail investors.

326

18. Opinion on Possible Export of Equity Derivatives Market to Offshore

happening:

The news items about the Open Interest in NIFTY futures on SGX

have taken over the NSE’s Nifty futures Open Interest figures which started

surfacing since January 2012. As pointed out in the earlier chapter, there

has been concern on the export of turnover happening to the offshore

exchanges mainly SGX. In light of this development, the brokers were

asked to give their views on this transition seen is across the globe. One of

the factors highlighted here was higher transaction cost as one of the big

factor in such a shift in the NIFTY Index Futures happening from NSE to

SGX. The broker’s opinion was sought to understand whether development

of such export of volumes and trading to the offshore exchanges is due to

higher transaction cost. The outcome of responses to the questionnaire is

tabulated below:

Table 7.18

Higher transaction costs in India transferring trading in

NIFTY Index Futures to SGX

Responses Response Percent Response Count

YES 93.8% 75

NO 6.3% 5

Total Responses 80

Source: Questionnaire

The response received from the respondents is also presented in the

Pie chart below:

Chart 7.18

Higher transaction costs in India transferring trading in NIFTY

Index Futures to SGX

Source: Questionnaire

327

As can be seen from responses to the questionnaire, a whopping

93.8% of the respondents feel that the export of volume and trading activity

to the offshore exchange mainly SGX can be attributed to higher transaction

costs in India compared to those in the offshore markets. Hence, the

government really needs to take the note of the concerns of the market and

work towards reducing transaction cost. The earlier analysis has revealed

that the major part of the transaction cost is the Securities Transaction Tax.

Hence, the Government really needs to work towards easing the burden to

ensure that the equity derivatives market remains onshore.

19. Acceptance of direct pledge from big clients by Clearing Corporations

The researcher while interacting with various brokers had got the

feedback that current collateral pledge and placing process with the

Clearing Corporation is only available to the Clearing Members and Self

Clearing Members at large. The Clients have to place the collaterals with

the Trading Members who in turn, if possible, place such collateral with the

Clearing Members and Clearing Members then if possible places these

collaterals with the Clearing Corporation. Some of the collaterals accepted

by the Trading Members and Clearing Members are also not possible to be

placed further with the Clearing Members and Clearing Corporations

respectively such as Bank Guarantees and Fixed Deposits obtained from the

clients and Trading Members discharged or lien marked in favour of

Trading Members and Clearing Members respectively. This kicks in the

need for capital requirement by the TMs and CMs separately to grant such

clients/TMs the exposures. Thus, it was felt by the researcher to get the

opinion of various other brokers on the thought of an idea of Custodial

Participants and Big clients bringing in collateral of more than Rs. 1 crore

should be directly allowed to place such collateral with the

Exchange/Clearing Corporation. The outcome of responses to the

questionnaire is tabulated below:

Table 7.19

Collateral be permitted to be directly pledged with the Clearing

Corporations

Responses Response Percent Response Count

YES 87.5% 70

NO 12.5% 10

Total Responses 80

Source: Questionnaire

328

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.19

Collateral be permitted to be directly pledged with the Clearing Corporations

Source: Questionnaire

As can be seen from the above table and the chart, 87.5%

respondents are of the opinion that the custodial participants and big clients

bringing in collateral of more than Rs. 1 crore should be permitted to

directly pledge the collateral with the clearing Corporation. This appears to

be giving the brokers a huge relief in utilization of their capital and their

funds which may accordingly get freed to make use for further trading

activity or any other such use. Thus, it is felt that the Exchange and the

regulators may look at this option depending upon the comfort drawn by the

Exchanges and also the feasibility of the structure that is conducive to the

market. It may decide on the amount which may be Rs. 1 crore or Rs. 5

crores or Rs. 10 crores or whatever the Exchange and the Clearing

Corporation draws comfort with for the best utilization of the collateral.

20. Need to shift to the Principle based regulation from the Rule based

regulation

It has been tendency of the market to complain about the regulators

being very strict and does not act taking into consideration the practical

aspect of implementation of the directives issued to the exchanges and the

participants.

There is a long standing debate about the relative merits of rule-

based versus principle-based regulatory systems. Rule-based regulation

prescribes in detail how to behave. For example, the limit on the Pune-

329

Mumbai Expressway is 80 Km/hour. In principle-based regulation norms

are formulated as guidelines. The exact implementation is left to the subject

of the norm. For example, in the above instance drive responsibly as high

speed driving causes accident.

One of the strongest criticisms against the SEBI is that it adopts rule

based regulations. There is plethora of rules that the intermediaries in the

system are required to adhere. This is considered to inhibit risk taking and

innovation. Principle based regulation points to the success that the

Financial Service Authority (FSA) has had in UK. It is said that FSA

intervenes only if a situation warrants such intervention, say, if certain

undesirable outcomes have resulted. Thus, it was felt necessary to

understand from the brokers whether there is a need for the regulator to

shift from rule based regulation to principle based regulation. The outcome

of responses to the questionnaire has been tabulated below:

Table 7.20

Need to shift to the principle based regulation from the rule

based regulation

Responses Response Percent Response Count

YES 70.0% 56

NO 30.0% 24

Total Responses 80

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.20

Need to shift to the principle based regulation from the rule based regulation

Source: Questionnaire

As can be seen from the above results and the pie chart, almost 70%

respondents feel that there is a need for the regulatory body to shift from the

330

rule based regulation to principle based regulations. The market has now

evolved over a period of time into a matured market where financial

products such as securities, derivatives and other such financial products are

effectively fungible. Also, the brokers, banks and other such intermediaries

operate as group companies offering most of the financial market services.

Application of too many specific rules will only allow the bad apples to

escape effective regulation. The implementation of the rules may happen

only on paper whereas the implementation may not happen in the spirit.

Thus, it is felt that understanding the need of the hour and the sentiment of

the respondents for the change required in the approach by the regulators,

the regulatory body may adopt the principle based regulatory approach than

the existing rule based regulatory approach.

21. Allowing Over The Counter (OTC) derivatives in India like global

markets:

Over-the-counter (OTC) derivatives are private contracts negotiated

between parties. The main advantage of OTC derivatives markets is that it

gives unlimited flexibility in contract design. The underlying asset can be

anything, the size of the contract can be any amount, and the delivery can

be made at any time and at any location. The only requirement of an OTC

contract is a willing buyer and seller. There are also disadvantages of OTC

markets such as willing buyers and sellers are required to spend time in identifying

each other, there is credit risk involved etc. Some of the examples of OTC

products are Exotics, Swaps, and Forward Rate Agreements etc. Thus, it was felt

necessary to understand from the markets that whether now market has

matured enough to accept that there should be OTC derivatives in the Indian

Markets. The outcome of responses to the questionnaire is as follows:

Table 7.21

Allowing Over The Counter (OTC) derivatives in the Indian

markets

Responses Response Percent Response Count

YES 51.3% 41

NO 48.8% 39

Total Responses 80

Source: Questionnaire

331

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

Chart 7.21

Allowing Over The Counter (OTC) derivatives in the Indian markets

Source: Questionnaire

It can be seen from the responses received from the respondents that

the opinion on allowing Over-The-Counter derivatives in India is divided.

Almost, 51.3% respondents feel that the OTC derivatives should be allowed in

India whereas 48.8% of the respondents feel that the same should not be

allowed in India. Since, the opinion of the respondents is divided, it is felt that

the regulators may form its view after analysis the pros and cons of allowing

OTC derivatives in India. It may also be noted that the WFE report states that

OTC market is a very big market in EAME region.

7.3 Investor’s Questionnaire and Analysis of the Data:

There are lacs of investors who trade everyday in the equity markets and

many of them also in the equity derivatives market. The actual figure of number

of client is also not possible to be arrived at since this data is not published

anywhere. Further, the clients can trade through multiple brokers and hence

they have multiple client codes at the exchange level. Hence, even with the data

of clients from the brokers, it would be difficult to identify the unique clients.

The primary information from the investors was collected through the

questionnaire which was circulated from the online mode, through the

interviews and meetings. It was circulated to the individuals at large. The

questionnaire could reach large number of investors online and they answered

to all the questions patiently. Largely the data could be gathered through online

mode by collecting the responses to the questionnaire across nation. The

332

questionnaire was designed to understand personal profile of the investor such

as age, gender, place of residence, education, experience in derivatives market,

category of investor, income range, occupation details etc. The questionnaire

further focused on seeking other equity derivatives market related information

like derivatives training undertaken, the need for the same, where does investor

invest, preference of equity derivative product for investment and periodicity of

contracts, purpose of trading and any strategies adopted for the same, opinion

on contract size, what kind of risk is of his concern, what does investor think of

growth of equity derivatives market in India, margins levied, need for wide

basket of products etc.

The questionnaire was circulated online to gather the responses from the

investors in the equity derivatives segment. The respondents were selected by

adopting random sampling technique. There were as many as 6617 responses

received to the questionnaire. The same were analyzed as below to arrive at the

result of the questionnaire. The results to the questions asked have been

analyzed below:

1. Sample investor population on the basis of the gender:

The investors were asked to disclose their gender in order to analyse

which gender has more number of investors in the equity derivatives market

and if any other conclusion could be drawn out of the same. The table

representing the division of sample population on the basis of gender of the

investors is given below:

Table 7.22

Gender of Investor Respondents

Answer Options Response Percent Response Count

Male 87.9% 5817

Female 12.1% 800

Total Responses 6617

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

333

Chart 7.22

Gender of Investor Respondents

Source: Questionnaire

As can be seen from the above table and chart, out of the total 6617

responses received for the questionnaire, 87.9% of the sample population

was Male population and 12.1% of the sample population was Female

population thereby denoting that a large number of investors are male in the

equity derivatives market. This may be due to large working and earning

population is male who also make investment decisions on their own.

2. Sample investor population on the basis of the Age:

The researcher further tried to find out the age group of the investors

in the equity derivatives market. The table representing the division of

sample population on the basis of age of the investors is given below:

Table 7.23

Age of Investor Respondents

Responses Response Percent Response Count

18 - 25 Years 15.0% 995

26 - 35 Years 64.1% 4241

36 - 45 Years 6.1% 401

46 - 55 Years 9.8% 650

55 - 65 Years 4.5% 301

Above 65 Years 0.4% 29

Total Respondents 6617

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Pie chart below:

334

Chart 7.23

Age of Investor Respondents

Source: Questionnaire

As we can see from the above table and Pie Chart, there is a large

population of respondents falling in the Age group of 26-35 accounting for

64.1%, followed by respondents falling in the Age group of 18-25

accounting for 15.0% of the total sample population, followed by

respondents falling in the Age group of 46-55 accounting for 9.8% of the

total sample population, then the respondents falling in the Age group of

36-45 accounting for 6.1% of the total sample population, then the

respondents falling in the Age group of 55-65 accounting for 4.5% of the

total sample population and respondents falling in the Age group of above

65 years accounted for merely 0.4% of the total sample population.

3. Sample investor population on the basis of the State of Residence:

The investors in the equity derivatives market in India are located in

nook and corner of the country. Thus, the data was gathered through the

questionnaire online to get the maximum diversified responses from all over

India. The responses received were then classified into various buckets of

the States. The same has been tabulated below in the table:

335

Table 7.24

Break up of Respondents based on State/Union Territory/Country of

Residence

Sr. No. State/Union Territory /

Country of Residence

No. of

Respondents %

1 Andhra Pradesh 819 12.38%

2 Assam 19 0.29%

3 Bihar 71 1.07%

4 Chandigarh 115 1.74%

5 Chhattisgarh 17 0.26%

6 Dadra Nagar Haveli 3 0.05%

7 Delhi 541 8.18%

8 Goa 9 0.14%

9 Gujarat 252 3.81%

10 Haryana 220 3.32%

11 Himachal Pradesh 32 0.48%

12 Jammu and Kashmir 6 0.09%

13 Jharkhand 52 0.79%

14 Karnataka 396 5.98%

15 Kerala 28 0.42%

16 Madhya Pradesh 250 3.78%

17 Maharashtra 1869 28.25%

18 Nagaland 4 0.06%

19 Orissa 68 1.03%

20 Pondicherry 4 0.06%

21 Punjab 173 2.61%

22 Rajasthan 350 5.29%

23 Sikkim 16 0.24%

24 Tamil Nadu 448 6.77%

25 Tripura 3 0.05%

26 Uttar Pradesh 436 6.59%

27 Uttaranchal 25 0.38%

28 West Bengal 389 5.88%

29 Outside India 2 0.03%

Total 6617 100.00%

Source: Questionnaire

The response received from the respondents as tabulated above is

also presented in the Bar chart below:

336

Chart 7.24

State/Union Territory/Country of Residence wise Break up of Respondents

Source: Questionnaire

As can be seen from the above table and bar chart from the

responses received to the questionnaire, almost 28.25% of respondents are

from Maharashtra, 12.38% of respondents are from Andhra Pradesh,

8.18% of respondents are from Delhi, 6.77% of respondents are from Tamil

Nadu, 6.59% of respondents are from Uttar Pradesh, 5.88% of respondents

are from West Bengal, 5.29% of respondents are from Rajasthan, 5.98% of

respondents are from Karnataka, 3.78% of respondents are from Madhya

Pradesh, 3.32% of respondents are from Haryana, 3.81% of respondents

are from Gujarat, 2.61% of respondents are from Punjab, 1.74% of

respondents are from Chandigarh, 1.07% of respondents are from Bihar,

1.03% of respondents are from Orissa and from other states and union

territories the respondents are less than 1%.

4. Sample investor population on the basis of Education:

Since, equity derivatives market is considered to be sophisticated,

the investors were asked their education background to understand the level

337

of education taken by the investors. The responses received to the

questionnaire have been tabulated below:

Table 7.25

Highest Education Obtained by the Respondents

Responses Response Percent Response Count

10th Std 0.1% 4

12th std 1.3% 84

Graduate 70.0% 4634

Post graduate 28.5% 1884

Doctorate 0.2% 11

Other (please specify) 141

Total Respondents 6617

Source: Questionnaire

The representation of the responses received to the questionnaire is

represented in the pie chart form as given below:

Chart 7.25

Highest Education Obtained by the Respondents

Source: Questionnaire

As we can see from the above Pie Chart, there is large population of

investors who are Graduates accounting for 70.0% of the total sample

population, followed by Post Graduates accounting for 28.5% of the total

sample population. There were also few Doctorates accounting for 0.2% of

the total sample population and there were 1.4% undergraduates. Thus, it

may be noted that a large number of respondents were well educated i.e.

almost 98.7% of the population were above graduate level.

5. Sample investor population on the basis of experience in the equity

derivatives market:

The equity derivatives market in India has now been more than a

decade old. It is necessary to know the experience of the investors

338

responding to the questionnaire. Out of the total 6617 respondents, the

investors had varied experience in the equity derivatives market. These

were bucketed accordingly in various buckets depending on the number of

years of experience i.e. upto 1 years of experience, 1-2 years of experience,

2-5 years of experience, 5-10 years of experience, and above 10 years of

experience in the equity derivatives markets. The outcome of responses to

the questionnaire has been tabulated in the table below:

Table 7.26

Experience in Equity Derivatives Market of the Respondents

Responses Response

Percent

Response

Count

Zero days to 1 Year 13.9% 917

More than 1 Year but less than 2 Years 20.7% 1373

More than 2 Years but less than 5 Years 51.9% 3434

More than 5 years but less than 10 Years 13.4% 887

More than 10 Years 0.1% 6

Total Respondents 6617

Source: Questionnaire

The pie chart representation of the division of sample population on

the basis of experience of the investors is given below:

Chart 7.26

Experience in Equity Derivatives Market of the Respondents

Source: Questionnaire

As we can see from the above Pie Chart, there is large population of

investors who are having good experience of trading in the equity

derivatives market. Almost 51.9% of the total respondents have experience

of more than 2 years but less than 5 years of trading in equity derivatives,

20.7% of the total respondents had an experience of 1-2 years, 13.9% have

339

2-5 years of experience, 13.4% of population has 5-10 years of experience

and 0.1% of population have above 10 years of experience of the total

sample population. Hence, as can be seen the population of the respondents

was fairly diversified.

6. Sample investor population on the basis of category of investor:

The investors are normally categorized into retail, High Net-worth

Individuals (HNIs), Non Residential Indians (NRIs), Corporate Bodies

(Private Limited Company, Limited Company etc), Mutual Funds, Banks

and Other Financial Institutions (MFs, Banks and Other FIs), Foreign

Institutions (Foreign Institutional Investors, Sub-accounts and Overseas

Corporate Bodies). The researcher tried to find out from the respondents the

type of investors chosen as a sample. The breakup of the same is provided

below in the table:

Table 7.27

Population on the Basis of Category of Investor

Responses Response

Percent

Response

Count

Retail 97.3% 6441

High Net-worth Individual (HNI) 2.5% 163

NRIs 0.0% 1

Indian Corporates (Pvt Ltd Co, Ltd Co etc) 0.1% 4

Foreign Institutions (FII, Sub-Account, OCBs) 0.0% 1

MFs, Banks, Insurance Companies, Other

Financial Institutions 0.1% 7

Total Respondents 6617

Source: Questionnaire

The pie chart representation of the division of sample population on

the basis of category of investors they fall in is given below:

Chart 7.27

Population on the Basis of Category of Investor

Source: Questionnaire

340

As can be seen from the above Pie Chart, there is large population

of investors who belong to retail category. Out of total respondents, almost

97.3% of population belongs to Retail category, 2.5% of population belongs

to HNI Category and 0.2% of population belongs to all other categories

such as NRI, Corporate Bodies, MFs, Banks and Other Financial

Institutions.

7. Sample investor population on the basis of income of respondents:

It is very important to know the income range of the investors since

there are questions asked with regard to value of contract they would want

in the equity derivatives, type of activities carried out by them in the equity

derivatives market etc. All the respondents were bucketed accordingly

depending on the income range they fall into i.e. income of upto Rs. 1 lac,

income of Rs. 1-5 lacs, income of Rs. 6-10 lacs, income of Rs. 10-15 lacs,

income of Rs. 15-25 lacs and income above 25 lacs. The summary of the

respondents based on the income range as disclosed by them is presented in

the following table:

Table 7.28

Income Range of the Respondent Investors

Responses Response

Percent

Response

Count

Upto Rs. 1 lac 6.5% 429

Rs. 1,00,001 - Rs. 5 lacs 78.3% 5180

Rs. 5,00,001 - Rs. 10 lacs 8.8% 580

Rs. 10,00,001 - Rs. 15 lacs 1.1% 72

Rs. 15,00,001 - Rs. 25 lacs 3.2% 211

Above Rs. 25 lacs 2.2% 145

Total Respondents 6617

Source: Questionnaire

The pie chart representation of the division of sample population on

the basis of income range of respondents is given below:

341

Chart 7.28

Income Range of the Respondent Investors

Source: Questionnaire

As can be seen from the above table and the Pie Chart, large

respondent population falls in the income range of Rs. 1 lac to Rs 5 lacs. As

we see from the above table, almost 78.3% of the respondent population fall

in the income range of Rs. 1,00,001 – Rs. 5 lacs, 8.8% of population fall in

the income range of Rs. 5,00,001 – Rs. 10 lacs, 6.5% of population fall in

the income range of upto Rs. 1 lac, 3.2% of population fall in the income

range of Rs. 15,00,001 - 25 lacs, 2.2% of population fall in the income

range of above Rs. 25 lacs and 1.1% of population fall in the income range

of Rs. 10,00,001 – Rs. 15 lacs. Thus, the large number of respondent base is

largely skewed towards the income range of Rs. 1-5 lacs. Thus, as can be

seen from the above, the respondents belonged to diverse income groups.

8. Sample investor population on the basis of occupation of respondents:

It was also necessary to understand the occupation of the respondent

population in order to know the kind of investors in the equity derivatives market

participate. The respondents were bucketed according to their occupation in

various buckets. The same are presented below in the tabular form:

Table 7.29

Population on the Basis of Occupation of the Investor

Responses Response Percent Response Count

Service 80.5% 5326

Business 9.2% 611

Professional 0.6% 39

Agriculturist 0.3% 17

Retired 2.0% 133

Housewife 3.4% 224

Student 4.0% 267

Total Respondents 6617

Source: Questionnaire

342

The pie chart representation of the division of sample population on

the basis of occupation of the respondents is given below:

Chart 7.29

Population on the Basis of Occupation of the Investor

Source: Questionnaire

As can be seen from the above table and the Pie Chart, almost

80.5% of population belongs to service class, 9.2% of population belong to

business class, 4.0% of population are Students, 3.4% of population are

Housewives, 2.0% of population are retired persons, 0.6% of population are

Professionals and 0.3% of population is Agriculturist. Thus, we see that

large number of investors appear to be the service or working class. Thus,

large number of respondents belonged to service class.

9. Analysis of Training requirements in Equity Derivatives

The respondents were advised to mention whether they had

undergone any training in derivatives from NSE, BSE or Broking firms

before starting trading in equity derivatives. This is important to know since

the respondents with good experience and with some training in derivatives

would be in a better position to answer the questions on training

requirement, strategy used, pace of growth of market etc. The respondents

were candid enough to respond to the question. There are many brokers

who offer online trading to their clients. Hence, apart from the Exchanges

and the regulatory body, the broking entities also conduct sessions for the

investors to make them understand the equity derivatives market and to

familiarize the clients with their online trading platform. The responses of

the respondents have been tabulated below in the table:

343

Table 7.30a

Respondents who have undergone some training in derivatives

Responses Response Percent Response Count

YES 33.1% 2188

NO 66.9% 4429

Total Respondents 6617

Source: Questionnaire

The pie chart representation of the division of respondents who had

undergone some training in equity derivatives before starting trading has

been given below:

Chart 7.30a

Respondents who have undergone some training in derivatives

Source: Questionnaire

As can be seen from the above table, almost 66.9% of total

respondents have not undergone any training before starting trading activity

in the equity derivatives market. Only 33.1% of the respondents had

undergone some training in derivatives from NSE, BSE or Broking Firms

before starting trading in equity derivatives. It was interesting to know that

there is a good number of investors who have undergone the training before