Embed Size (px)

Citation preview

Banks’ Endogenous Systemic Risk Taking

David Martinez-Miera

Universidad Carlos III

Javier Suarez

CEMFI

Banking and Regulation: The Next Frontier

A RTF-CEPR-JFI Workshop, Basel, 22-23 January 2015

1

Introduction

• The recent crisis has evidenced the need to better understand banks’contribution to systemic risk

• One of the dimensions of this multifaceted phenomenon is the ex-posure to common shocks

• In this paper, we analyze:

— The dynamic trade-offs behind banks’ voluntary exposure toan infrequent & large common shock(attractive to them due to standard risk-shifting incentives)

— The extent to which capital requirements (CRs) contribute toreduce the resulting systemic risk & increase social welfare

— Issues such as the optimal level of CRs, their gradual introduction& cyclical adjustment

2

• Simple dynamic equilibrium model in which bank capital dy-namics is formalized like in other papers in recent literature

(limited wealth of bankers who retain earnings and/or suffer lossesfrom prior investments)

— But the role of bank capital is different

∗Meh-Moran’10: Monitoring incentives a laHolmström-Tirole’97∗ Gertler-Kiyotaki’10: Preventing fund diversion a laHart-Moore’94

— Here, it reduces systemic gambling incentives through twochannels:

∗ Leverage reduction effect (standard)[Van den Heuvel’08 & many micro-banking models]

∗ Last bank standing effect (novel — as for CRs)[akin to Perotti-Suarez’02]

3

Related literature

Papers beyond those already mentioned:

• Ranciere-Tornell-Westermann’08: myopic firms adopt “risky growthstrategies” due to lenders’ expectation of a systemic bailout when acrisis occurs

• Brunnermeier-Sannikov’14, He-Krishnamurthy’14: similar capital dy-namics but no time-varying systemic risk-taking & no discussion onCRs

• Risk taking in banking:— under deposit insurance: Kareken-Wallace’78 & many more

— effect of CRs: Hellmman-Murdock-Stiglitz’00, Repullo’04

— equilibrium/dynamic considerations: Acharya-Yorulmazer’07-08,Farhi-Tirole’12

4

Our modeling of systemic risk taking

1. Firms’ production technology is subject to failure risk & can bemanaged in two modes:

• non-systemic (xi=0): its failure is purely i.i.d.• systemic (xi=1): if a rare shock occurs, all fail at once

2. Firms need bank loans to pay inputs in advance: li=ki+wni

3. Lending to systemic firms is socially inefficient, but...

• Highly levered banks may find it privately profitable• Systemic lending is not ex-ante detectable→ Regulation sets a common capital requirement: ei ≥ γli

4. Bankers competitively allocate their wealth e as capital across banks

5

Key variables

• Capital requirements are satisfied with inside equity

→ Single state variable is bankers’ aggregate wealth e

∗ grows quickly if bank profits are high∗ gets lost if invested systemically and shock realizes

• Two important endogenous variables

v(e) : value of one unit of bankers’ wealth

x(e) : fraction of bankers’ wealth invested in systemic banks

[Banks specialize as systemic or non-systemic]

6

Key insights

1. Systemic risk taking is maximal after several calm periods[bankers’ reaction to the lower shadow value of their wealth]

2. Higher capital requirements...

• reinforce the last bank standing effect [GOOD]

•make bank capital effectively scarcer at all times⇒ less credit⇒ lower economic activity [BAD]

3. The socially optimal capital requirements

• are quite high• should be gradually introduced• should not be lowered after a crisis

7

Key equations*

• Banks fix the terms of their supply of loans to firms taking bankers’required value-weighted return as given

• Bankers allocate their wealth et across banks taking the returnsoffered to them by banks as given

vt = ψ + (1− ψ)βmax{Et(vt+1R0t+1), Et(vt+1R1t+1)}

Rjt+1: gross return on equity under xi = j

vt+1: marginal value of bankers’ wealth at end of t

⇒ Indifference requires Et(vt+1R0t+1) = Et(vt+1R1t+1) (1)

⇒ we look at a representative bank of each class

• Law of motion of total bank capital etet+1 = φ(1 + r)wt + (1− ψ)[(1− xt)R0t+1 + xtR1t+1]et

8

Definition of equilibrium*

• Stationary law of motion for et ∈ [e, e]

• Tuple (v(e), x(e); k(e), w(e), R0(e), R01(e)) describingendogenous variables for each e ∈ [e, e]such that {et} and {vt, xt; kt, wt, R0t+1, R

01t+1} are

compatible with:

1. Individual optimization

2. Market clearing

––––––––––––––––––Indifference condition for xt ∈ (0, 1):

[(1− ε)v(e0t+1) + εv(e1t+1)]R0t+1 = (1− ε)v(e0t+1)R01t+1

⇒ ∃ self-equilibrating mechanism for xt9

Rest of the talk

1. Baseline parameterization

2. Graphical presentation of key results

3. Quantitative results

4. Applications

5. Conclusions

10

Baseline parameterization (1 period = 1 year)

T1. Baseline parameter valuesPatient agents’ discount rate ρ 0.02Impatient agents’ discount factor β 0.96Total factor productivity A 2Physical capital elasticity α 0.3Depreciation rate in successful firms δ 0.05Depreciation rate in failed firms λ 0.35Idiosyncratic default rate of non-systemic firms π0 0.03Idiosyncratic default rate of systemic firms π1 0.018Probability of a systemic shock ε 0.03Bankers’ exit rate ψ 0.20Fraction of wage income earned by bankers φ 0.05

[Parsimonious model: 11 parameters only]

11

•Why these values?

— Low real interest rates such as prior to the recent crisis

—A = 2 is inconsequential (levels in 0 to 100 range)

— α = 0.30 produces labor share ' 70%

— δ and λ match K/Y ' 3-4 & LGD' 45%

— π0, π1, and ε ⇒ sufficient room of risk shifting

[expected default rates 3%—4.7%; systemic shocks every 33y]

— Bank capital dynamics (highly tentative):

ψ: bankers’ expected active life = 5y

φ: capital brought in by active bankers = 5%of agg. labor income

12

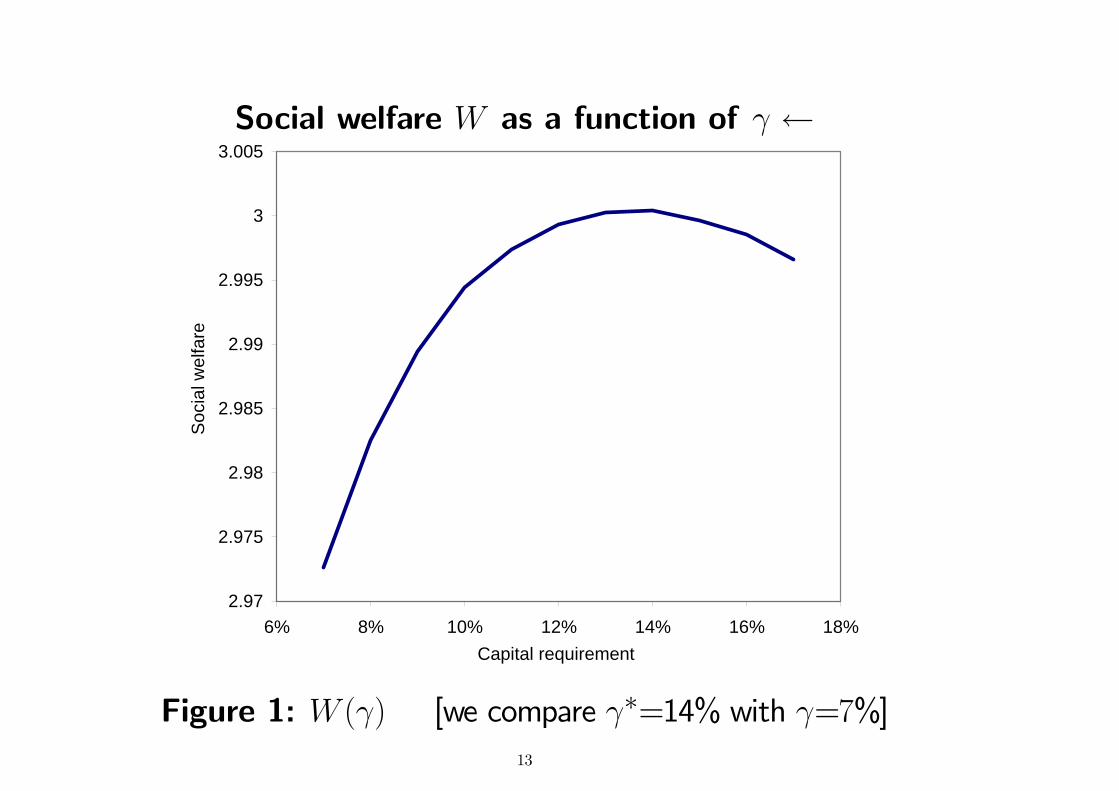

Social welfare W as a function of γ ←

2.97

2.975

2.98

2.985

2.99

2.995

3

3.005

6% 8% 10% 12% 14% 16% 18%Capital requirement

Soc

ial w

elfa

re

Figure 1: W (γ) [we compare γ∗=14% with γ=7%]13

v(e) and x(e) under low and optimal γ ←

0

1

2

3

4

5

6

7

8

9

10

0 0.5 1 1.5 2 2.5Aggregate amount of bank capital (e)

Mar

gina

l val

ue o

f ban

k ca

pita

l (v)

optimal capital requirement (14%)

low capital requirement (7%)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0 0.5 1 1.5 2 2.5Aggregate amount of bank capital (e)

Sys

tem

ic ri

sk ta

king

(x)

optimal capital requirement (14%)

low capital requirement (7%)

Figure 2a: v(e) Figure 2b: x(e)

14

Equilibrium dynamics with low and optimal γ ←

Equilibrium dynamics (CR=7%)

0

0.5

1

1.5

2

2.5

3

0 0.5 1 1.5 2 2.5Aggregate bank capital at t

Agg

rega

te b

ank

capi

tal a

t t+1

Dynamics if no shock realizes

Dynamics if shock realizes

45-degree line

Equilibrium dynamics (CR=14%)

0

0.5

1

1.5

2

2.5

3

0 0.5 1 1.5 2 2.5Aggregate bank capital at t

Agg

rega

te b

ank

capi

tal a

t t+1

Dynamics if no shock realizes

Dynamics if shock realizes

45-degree line

Figure 3a (γ =7%) Figure 3b (γ =14%)

15

Equilibrium dynamics with low and optimal γ ←

Ergodic distribution (CR=7%)

00.20.40.60.8

1

0 0.5 1 1.5 2 2.5Aggregate bank capital

Freq

uenc

y

Ergodic distribution (CR=14%)

00.20.40.60.8

1

0 0.5 1 1.5 2 2.5Aggregate bank capital

Freq

uenc

y

Figure 3c (γ =7%) Figure 3d (γ =14%)

16

Quantitative results

• Optimal capital requirements: positive and large (14%)

• Comparison CR=7%→ CR=14% (unconditional means)

— Lower fraction of systemic loans: 71%→ 25%

— Higher loan rates: 4.1%→ 5.6%

— Lower macro aggregates: bank credit (—21%), GDP (—8.5%)

— Higher social welfare: ' +0.9% permanent consumption

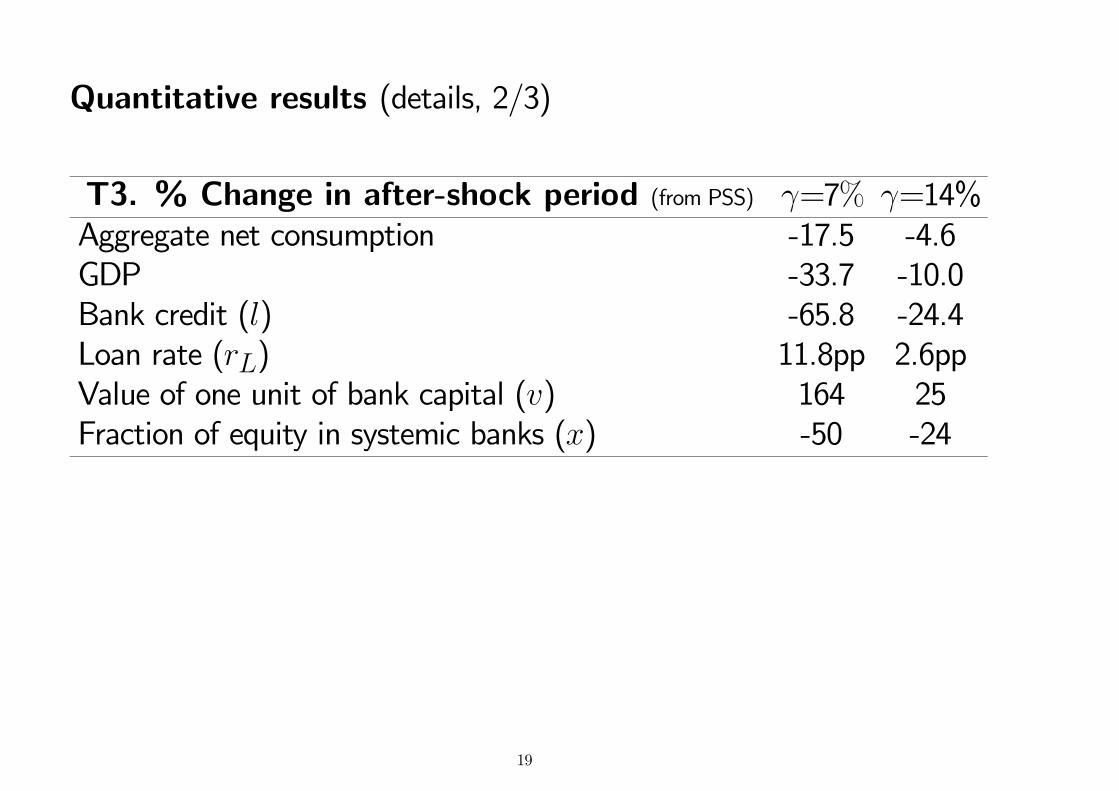

• Variation in year-after-shock aggregates:

— CR=7%: loan rate (+11.8pp), bank credit (-66%), GDP (-34%)

— CR=14%: loan rate (+2.6pp), bank credit (-24%), GDP (-10%)

17

Quantitative results (details, 1/3)

T2. Main unconditional means γ = 7% γ = 14% ∆%Welfare (equivalent consumption flow) 2.97 3.00 0.9GDP 4.54 4.15 -8.5Bank credit (l) 19.30 15.28 -20.8Bank equity (e) 1.35 2.14 58.3Loan rate (rL) (in %) 4.1 5.6 1.5ppDeposit insurance costs 0.16 0.04 -76.2Value of one unit of bank capital (v) 1.37 1.90 38.1Fraction of equity in systemic banks (x) 0.71 0.25 -64.9

18

Quantitative results (details, 2/3)

T3. % Change in after-shock period (from PSS) γ=7% γ=14%Aggregate net consumption -17.5 -4.6GDP -33.7 -10.0Bank credit (l) -65.8 -24.4Loan rate (rL) 11.8pp 2.6ppValue of one unit of bank capital (v) 164 25Fraction of equity in systemic banks (x) -50 -24

19

Quantitative results (details, 3/3)

T4. Other macro & financial ratios γ = 7% γ = 14%Labor income/GDP 0.67 0.68Physical capital/GDP 3.58 3.03Bank credit/GDP* 4.25 3.71Deposit insurance costs/GDP (%) 3.5 0.9ROE at non-systemic banks (%) 10.2 17.0ROE at systemic banks if no shock realizes (%) 18.7 21.2

[*: suggests exuberance due to lax regulation]

20

Applications

• Transitional dynamics from moving γ and impact on welfare:

There is value (and limits to the value) ofapplying gradualism in rising γ

[Best: moving from 7% to 13% in 9 years]

• Assessment of countercyclical capital requirements

— They have a bad effect on incentives—Overall, there is no net gain from making them countercyclical— But sticking to flat requirements may not be time-consistent

21

2.973

2.978

2.983

2.988

2.993

2.998

0 5 10 15 20 25 30Years of transition (T)

Soc

ial w

elfa

re

8%

9%

10%

11%12%

13%14%

15%

22

Conclusions

• Dynamic equilibrium model of banks’ endogenous systemic risk-taking

• Allows us to assess the macroprudential role of capital requirementsusing an internally consistent welfare metrics:

They reduce credit and output in calm times but also systemic risktaking⇒ interior socially optimal level

• The identified last bank standing effect implies that systemic risktaking increases as the economy expands...

Yet, systemic risk taking increases if the CRs are cyclically adjusted

23