Embed Size (px)

Citation preview

Analyst - Andrew Walker

Equity Analysis Discussion Material

March 2016

Analyst Contact InfoCell: (682) 622-6006

Email: [email protected]

DaVita HealthCare Partners Inc. consists of two divisions, Kidney Care and HealthCare Partners (HCP).

DaVita Kidney Care is a leading provider of dialysis services in the United States, treating patients with chronic kidney failure and end stage renal disease. DaVita Kidney Care strives to improve patients' quality of life by innovating clinical care, and by offering integrated treatment plans, personalized care teams and convenient health-management services. As of December 31, 2015, DaVita Kidney Care provided dialysis services to a total of approximately 180,000 patients at 2,369 outpatient dialysis centers, of which 2,251 centers are located in the United States and 118 centers are located in 10 countries outside of the United States.

HealthCare Partners division is a patient and physician focused integrated health care delivery and management company. Since 1992, HealthCare Partners has been committed to developing innovative models of healthcare delivery that improve patients' quality of life while containing healthcare costs. HealthCare Partners manages and operates medical groups and affiliated physician networks in Arizona, California, Nevada, Florida, New Mexico and Colorado. As of December 31,2015, HealthCare Partners had approximately 807,400 capitated members under its care.

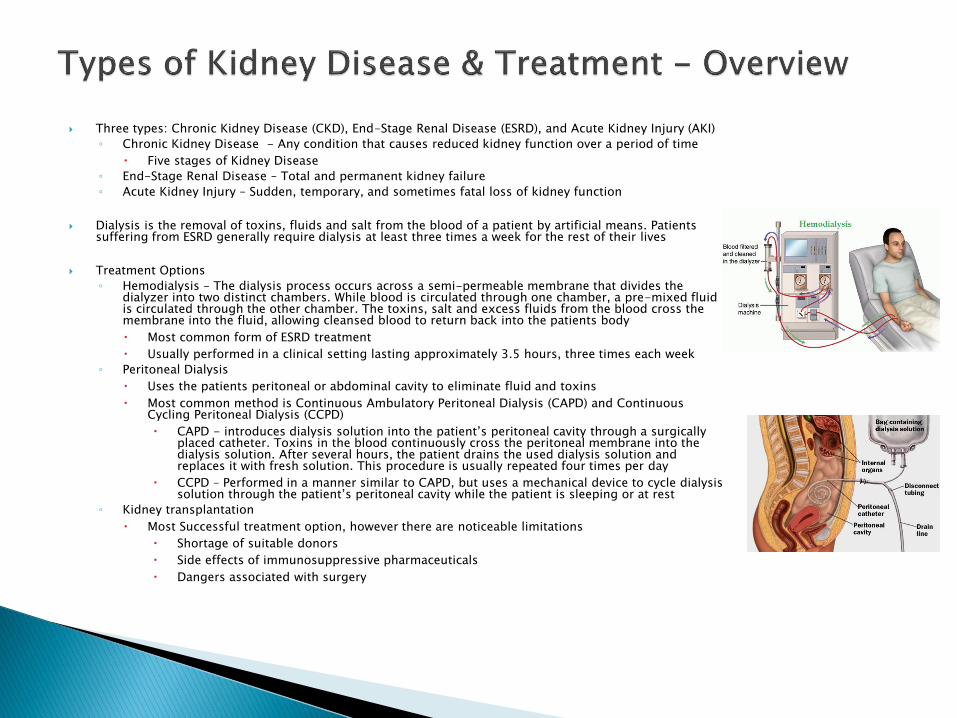

Three types: Chronic Kidney Disease (CKD), End-Stage Renal Disease (ESRD), and Acute Kidney Injury (AKI)

◦ Chronic Kidney Disease - Any condition that causes reduced kidney function over a period of time

Five stages of Kidney Disease

◦ End-Stage Renal Disease – Total and permanent kidney failure

◦ Acute Kidney Injury – Sudden, temporary, and sometimes fatal loss of kidney function

Dialysis is the removal of toxins, fluids and salt from the blood of a patient by artificial means. Patients suffering from ESRD generally require dialysis at least three times a week for the rest of their lives

Treatment Options

◦ Hemodialysis – The dialysis process occurs across a semi-permeable membrane that divides the dialyzer into two distinct chambers. While blood is circulated through one chamber, a pre-mixed fluid is circulated through the other chamber. The toxins, salt and excess fluids from the blood cross the membrane into the fluid, allowing cleansed blood to return back into the patients body

Most common form of ESRD treatment

Usually performed in a clinical setting lasting approximately 3.5 hours, three times each week

◦ Peritoneal Dialysis

Uses the patients peritoneal or abdominal cavity to eliminate fluid and toxins

Most common method is Continuous Ambulatory Peritoneal Dialysis (CAPD) and Continuous Cycling Peritoneal Dialysis (CCPD)

CAPD - introduces dialysis solution into the patient’s peritoneal cavity through a surgically placed catheter. Toxins in the blood continuously cross the peritoneal membrane into the dialysis solution. After several hours, the patient drains the used dialysis solution and replaces it with fresh solution. This procedure is usually repeated four times per day

CCPD – Performed in a manner similar to CAPD, but uses a mechanical device to cycle dialysis solution through the patient’s peritoneal cavity while the patient is sleeping or at rest

◦ Kidney transplantation

Most Successful treatment option, however there are noticeable limitations

Shortage of suitable donors

Side effects of immunosuppressive pharmaceuticals

Dangers associated with surgery

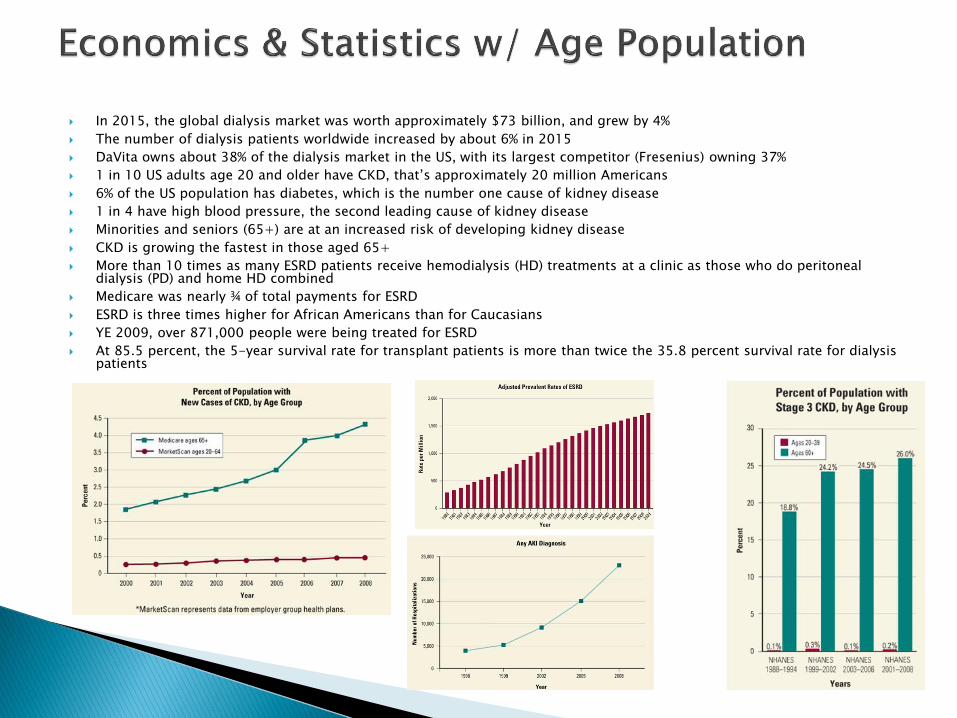

In 2015, the global dialysis market was worth approximately $73 billion, and grew by 4%

The number of dialysis patients worldwide increased by about 6% in 2015

DaVita owns about 38% of the dialysis market in the US, with its largest competitor (Fresenius) owning 37%

1 in 10 US adults age 20 and older have CKD, that’s approximately 20 million Americans

6% of the US population has diabetes, which is the number one cause of kidney disease

1 in 4 have high blood pressure, the second leading cause of kidney disease

Minorities and seniors (65+) are at an increased risk of developing kidney disease

CKD is growing the fastest in those aged 65+

More than 10 times as many ESRD patients receive hemodialysis (HD) treatments at a clinic as those who do peritoneal dialysis (PD) and home HD combined

Medicare was nearly ¾ of total payments for ESRD

ESRD is three times higher for African Americans than for Caucasians

YE 2009, over 871,000 people were being treated for ESRD

At 85.5 percent, the 5-year survival rate for transplant patients is more than twice the 35.8 percent survival rate for dialysis patients

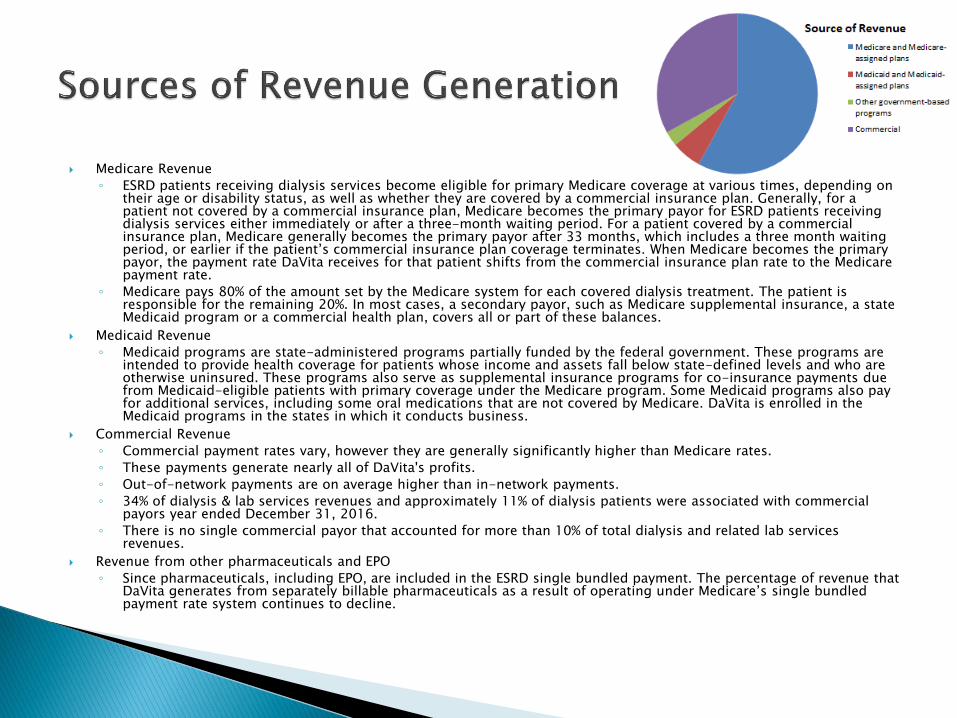

Medicare Revenue

◦ ESRD patients receiving dialysis services become eligible for primary Medicare coverage at various times, depending on their age or disability status, as well as whether they are covered by a commercial insurance plan. Generally, for a patient not covered by a commercial insurance plan, Medicare becomes the primary payor for ESRD patients receiving dialysis services either immediately or after a three-month waiting period. For a patient covered by a commercial insurance plan, Medicare generally becomes the primary payor after 33 months, which includes a three month waiting period, or earlier if the patient’s commercial insurance plan coverage terminates. When Medicare becomes the primary payor, the payment rate DaVita receives for that patient shifts from the commercial insurance plan rate to the Medicare payment rate.

◦ Medicare pays 80% of the amount set by the Medicare system for each covered dialysis treatment. The patient is responsible for the remaining 20%. In most cases, a secondary payor, such as Medicare supplemental insurance, a state Medicaid program or a commercial health plan, covers all or part of these balances.

Medicaid Revenue

◦ Medicaid programs are state-administered programs partially funded by the federal government. These programs are intended to provide health coverage for patients whose income and assets fall below state-defined levels and who are otherwise uninsured. These programs also serve as supplemental insurance programs for co-insurance payments due from Medicaid-eligible patients with primary coverage under the Medicare program. Some Medicaid programs also pay for additional services, including some oral medications that are not covered by Medicare. DaVita is enrolled in the Medicaid programs in the states in which it conducts business.

Commercial Revenue

◦ Commercial payment rates vary, however they are generally significantly higher than Medicare rates.

◦ These payments generate nearly all of DaVita's profits.

◦ Out-of-network payments are on average higher than in-network payments.

◦ 34% of dialysis & lab services revenues and approximately 11% of dialysis patients were associated with commercial payors year ended December 31, 2016.

◦ There is no single commercial payor that accounted for more than 10% of total dialysis and related lab services revenues.

Revenue from other pharmaceuticals and EPO

◦ Since pharmaceuticals, including EPO, are included in the ESRD single bundled payment. The percentage of revenue that DaVita generates from separately billable pharmaceuticals as a result of operating under Medicare’s single bundled payment rate system continues to decline.

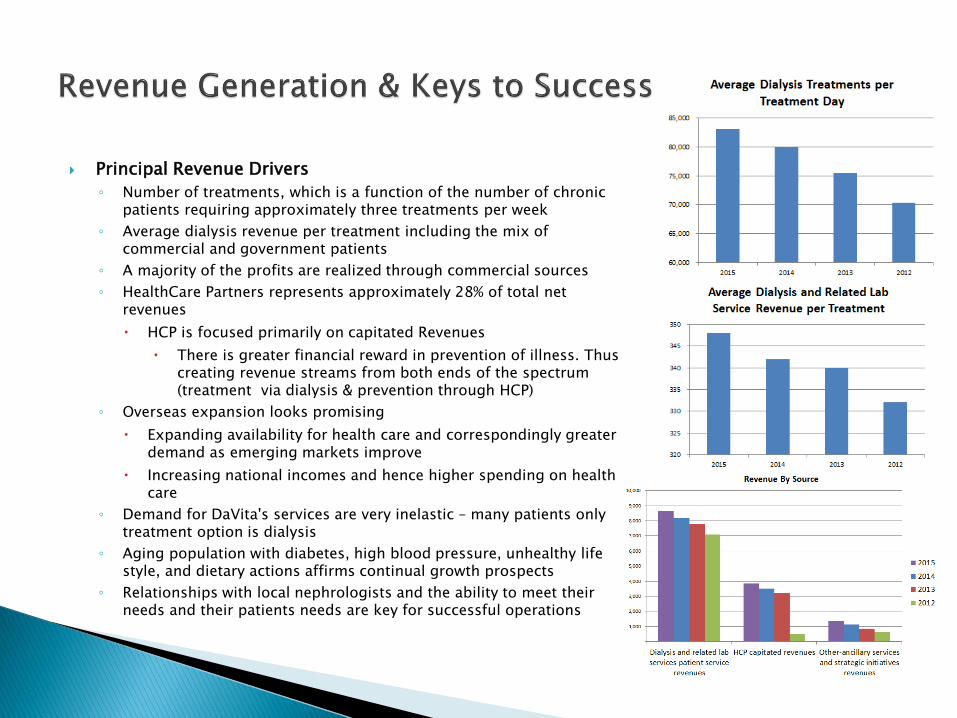

Principal Revenue Drivers

◦ Number of treatments, which is a function of the number of chronic patients requiring approximately three treatments per week

◦ Average dialysis revenue per treatment including the mix of commercial and government patients

◦ A majority of the profits are realized through commercial sources

◦ HealthCare Partners represents approximately 28% of total net revenues

HCP is focused primarily on capitated Revenues

There is greater financial reward in prevention of illness. Thus creating revenue streams from both ends of the spectrum (treatment via dialysis & prevention through HCP)

◦ Overseas expansion looks promising

Expanding availability for health care and correspondingly greater demand as emerging markets improve

Increasing national incomes and hence higher spending on health care

◦ Demand for DaVita's services are very inelastic – many patients only treatment option is dialysis

◦ Aging population with diabetes, high blood pressure, unhealthy life style, and dietary actions affirms continual growth prospects

◦ Relationships with local nephrologists and the ability to meet their needs and their patients needs are key for successful operations

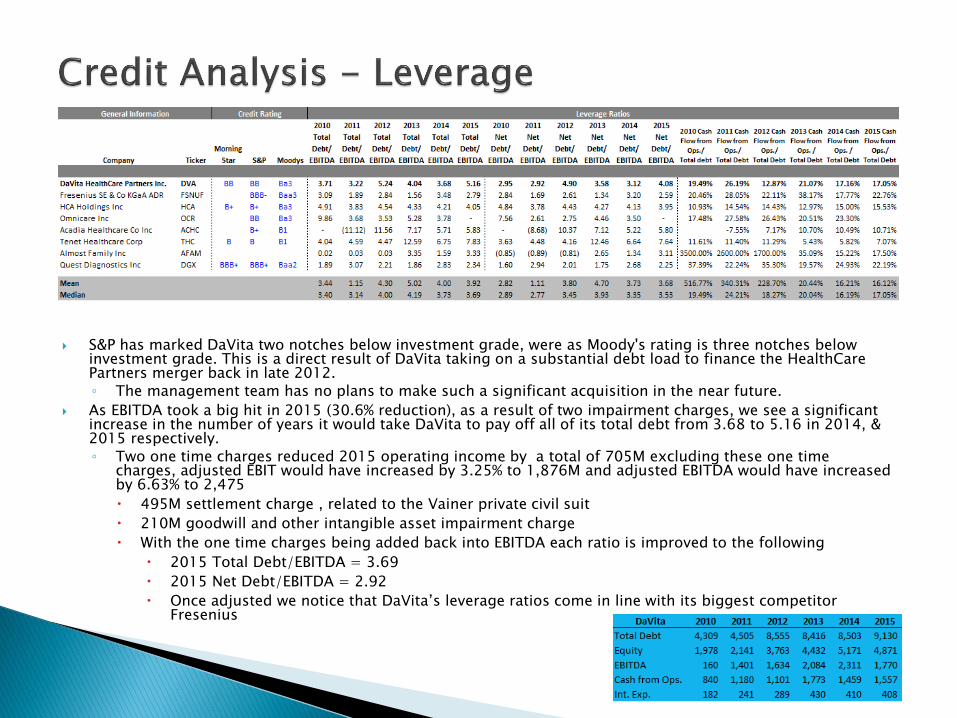

S&P has marked DaVita two notches below investment grade, were as Moody's rating is three notches below investment grade. This is a direct result of DaVita taking on a substantial debt load to finance the HealthCare Partners merger back in late 2012.◦ The management team has no plans to make such a significant acquisition in the near future.

As EBITDA took a big hit in 2015 (30.6% reduction), as a result of two impairment charges, we see a significant increase in the number of years it would take DaVita to pay off all of its total debt from 3.68 to 5.16 in 2014, & 2015 respectively. ◦ Two one time charges reduced 2015 operating income by a total of 705M excluding these one time

charges, adjusted EBIT would have increased by 3.25% to 1,876M and adjusted EBITDA would have increased by 6.63% to 2,475

495M settlement charge , related to the Vainer private civil suit

210M goodwill and other intangible asset impairment charge

With the one time charges being added back into EBITDA each ratio is improved to the following

2015 Total Debt/EBITDA = 3.69

2015 Net Debt/EBITDA = 2.92

Once adjusted we notice that DaVita’s leverage ratios come in line with its biggest competitor Fresenius

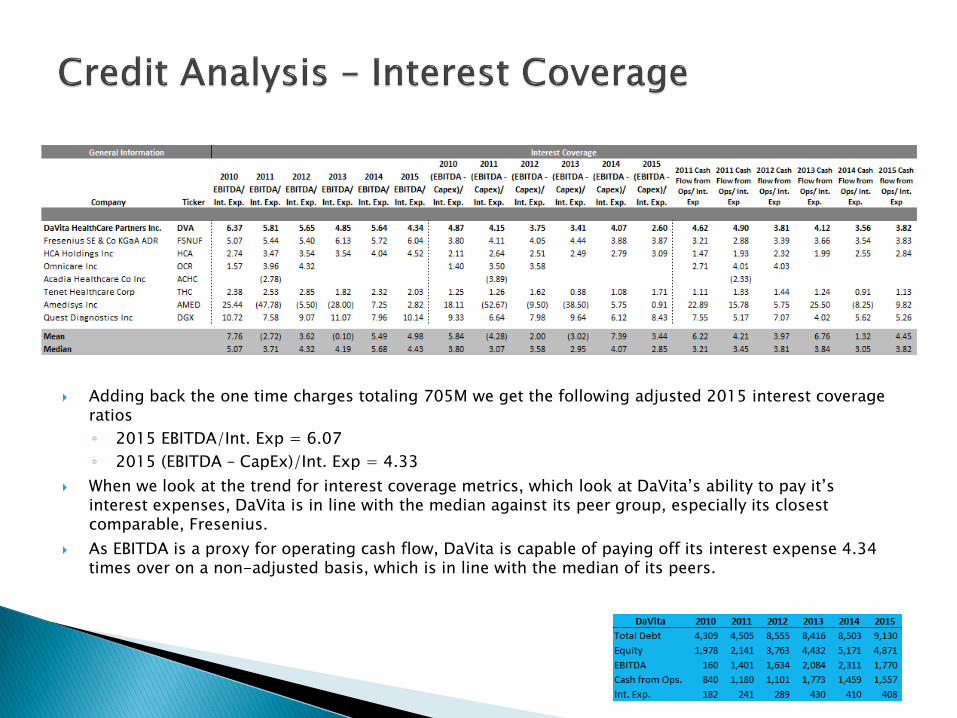

Adding back the one time charges totaling 705M we get the following adjusted 2015 interest coverage ratios

◦ 2015 EBITDA/Int. Exp = 6.07

◦ 2015 (EBITDA – CapEx)/Int. Exp = 4.33

When we look at the trend for interest coverage metrics, which look at DaVita’s ability to pay it’s interest expenses, DaVita is in line with the median against its peer group, especially its closest comparable, Fresenius.

As EBITDA is a proxy for operating cash flow, DaVita is capable of paying off its interest expense 4.34 times over on a non-adjusted basis, which is in line with the median of its peers.

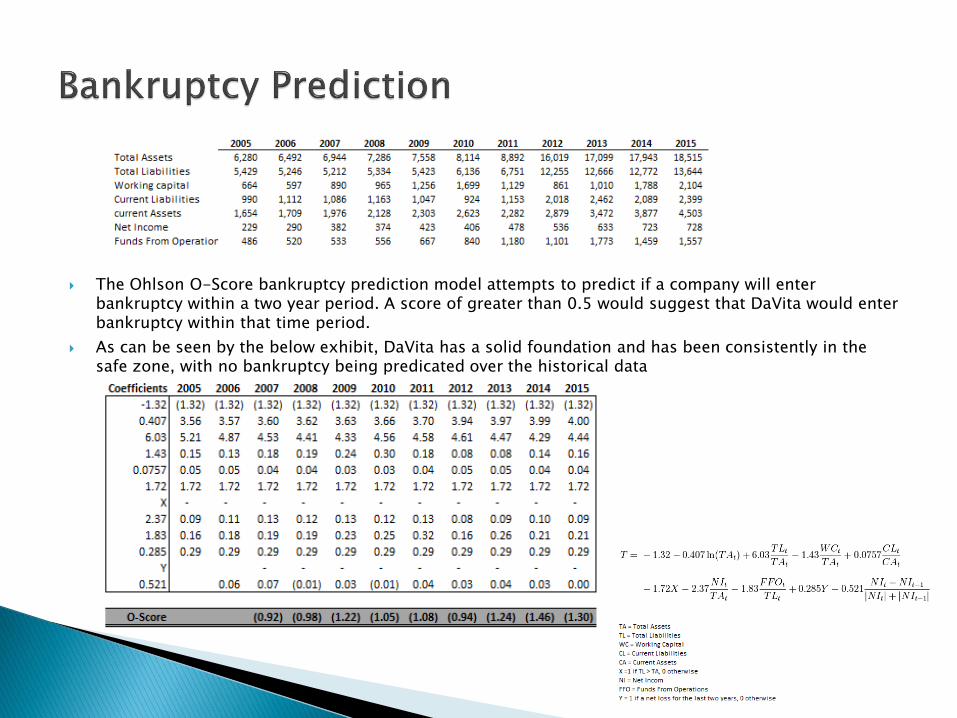

The Ohlson O-Score bankruptcy prediction model attempts to predict if a company will enter bankruptcy within a two year period. A score of greater than 0.5 would suggest that DaVita would enter bankruptcy within that time period.

As can be seen by the below exhibit, DaVita has a solid foundation and has been consistently in the safe zone, with no bankruptcy being predicated over the historical data

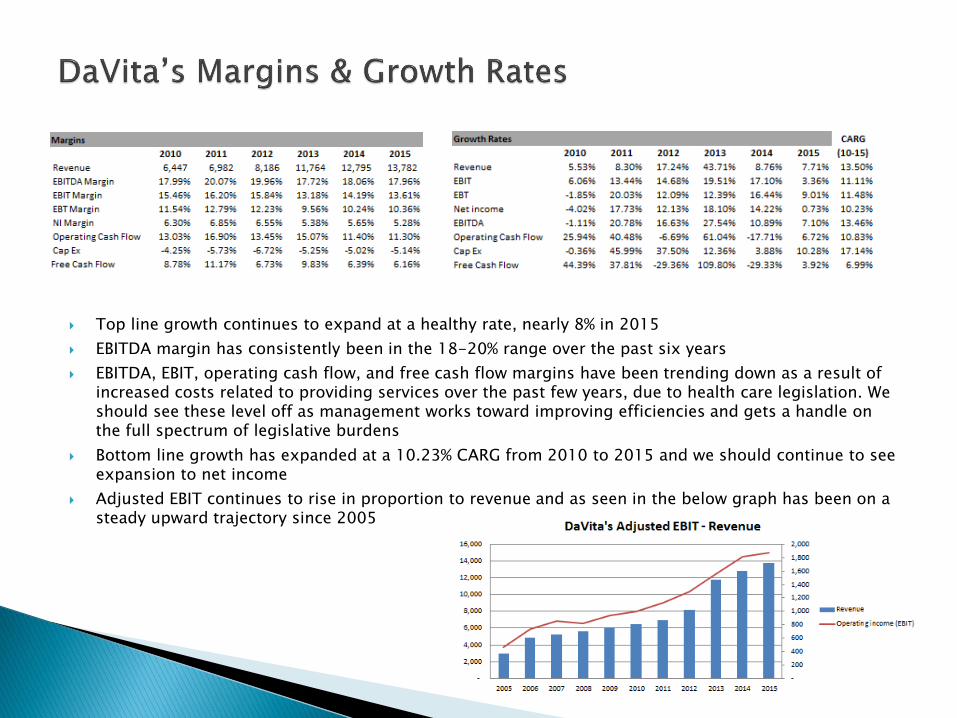

Top line growth continues to expand at a healthy rate, nearly 8% in 2015

EBITDA margin has consistently been in the 18-20% range over the past six years

EBITDA, EBIT, operating cash flow, and free cash flow margins have been trending down as a result of increased costs related to providing services over the past few years, due to health care legislation. We should see these level off as management works toward improving efficiencies and gets a handle on the full spectrum of legislative burdens

Bottom line growth has expanded at a 10.23% CARG from 2010 to 2015 and we should continue to see expansion to net income

Adjusted EBIT continues to rise in proportion to revenue and as seen in the below graph has been on a steady upward trajectory since 2005

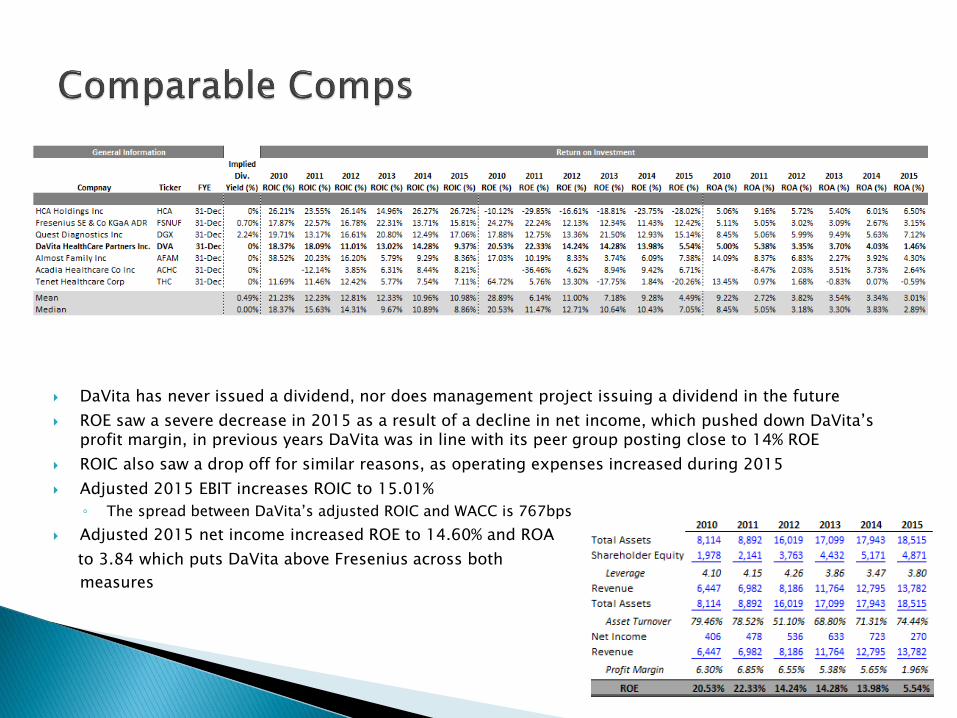

DaVita has never issued a dividend, nor does management project issuing a dividend in the future

ROE saw a severe decrease in 2015 as a result of a decline in net income, which pushed down DaVita’s profit margin, in previous years DaVita was in line with its peer group posting close to 14% ROE

ROIC also saw a drop off for similar reasons, as operating expenses increased during 2015

Adjusted 2015 EBIT increases ROIC to 15.01%

◦ The spread between DaVita’s adjusted ROIC and WACC is 767bps

Adjusted 2015 net income increased ROE to 14.60% and ROA

to 3.84 which puts DaVita above Fresenius across both

measures

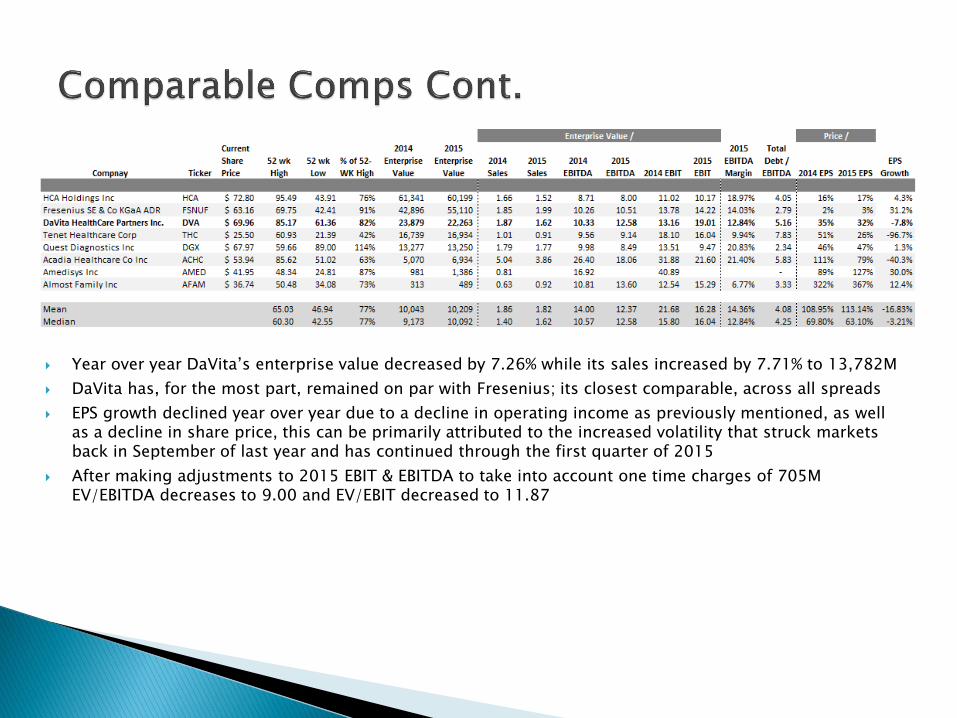

Year over year DaVita’s enterprise value decreased by 7.26% while its sales increased by 7.71% to 13,782M

DaVita has, for the most part, remained on par with Fresenius; its closest comparable, across all spreads

EPS growth declined year over year due to a decline in operating income as previously mentioned, as well as a decline in share price, this can be primarily attributed to the increased volatility that struck markets back in September of last year and has continued through the first quarter of 2015

After making adjustments to 2015 EBIT & EBITDA to take into account one time charges of 705M EV/EBITDA decreases to 9.00 and EV/EBIT decreased to 11.87

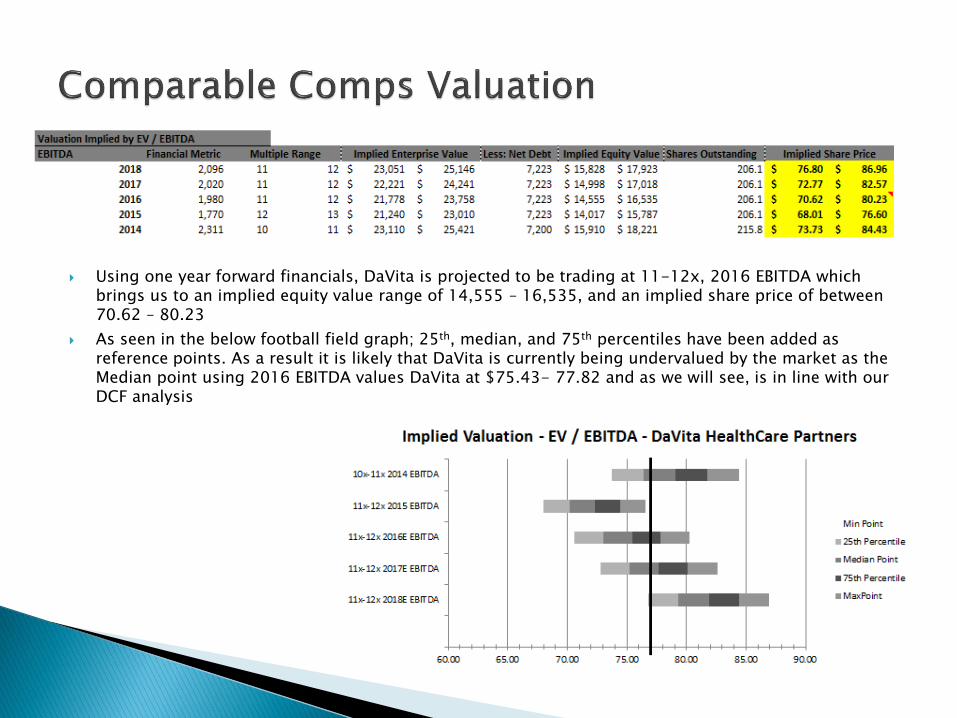

Using one year forward financials, DaVita is projected to be trading at 11-12x, 2016 EBITDA which brings us to an implied equity value range of 14,555 – 16,535, and an implied share price of between 70.62 – 80.23

As seen in the below football field graph; 25th, median, and 75th percentiles have been added as reference points. As a result it is likely that DaVita is currently being undervalued by the market as the Median point using 2016 EBITDA values DaVita at $75.43- 77.82 and as we will see, is in line with our DCF analysis

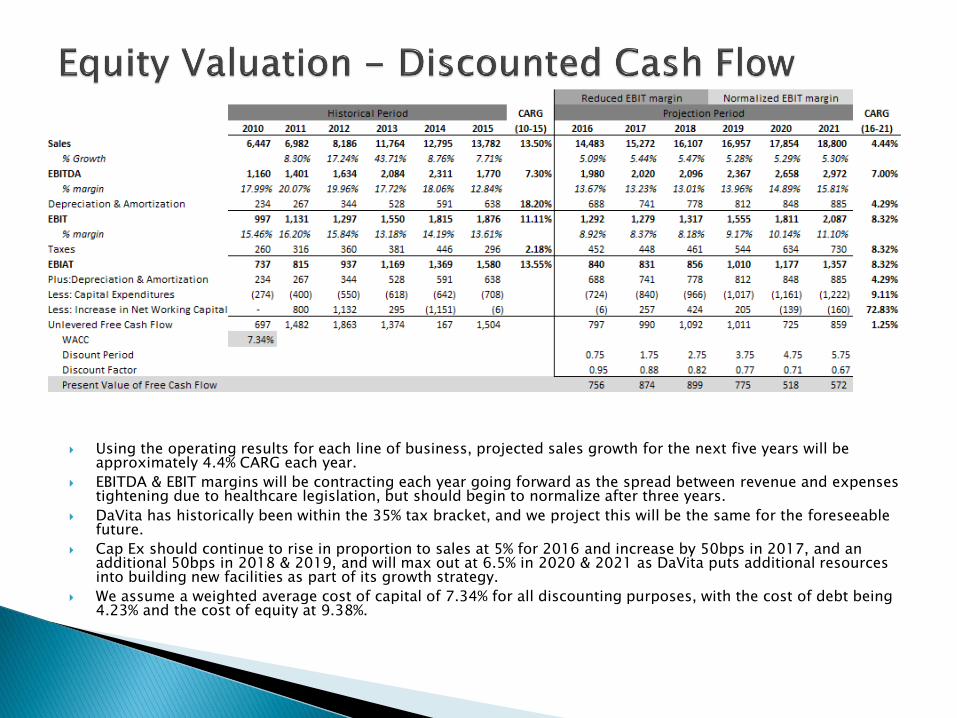

Using the operating results for each line of business, projected sales growth for the next five years will be approximately 4.4% CARG each year.

EBITDA & EBIT margins will be contracting each year going forward as the spread between revenue and expenses tightening due to healthcare legislation, but should begin to normalize after three years.

DaVita has historically been within the 35% tax bracket, and we project this will be the same for the foreseeable future.

Cap Ex should continue to rise in proportion to sales at 5% for 2016 and increase by 50bps in 2017, and an additional 50bps in 2018 & 2019, and will max out at 6.5% in 2020 & 2021 as DaVita puts additional resources into building new facilities as part of its growth strategy.

We assume a weighted average cost of capital of 7.34% for all discounting purposes, with the cost of debt being 4.23% and the cost of equity at 9.38%.

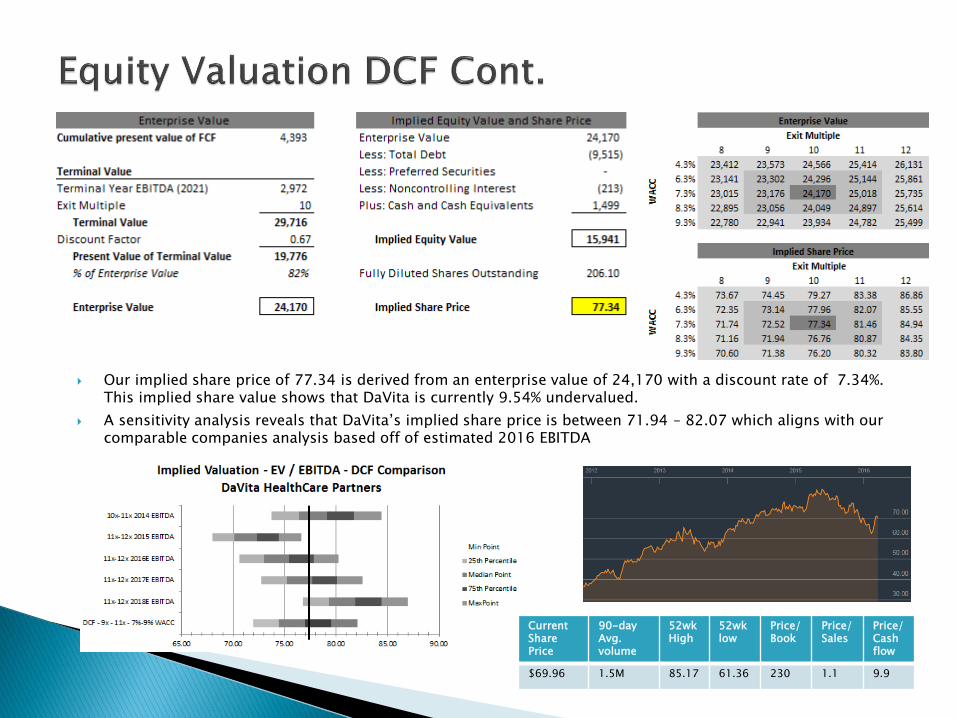

Our implied share price of 77.34 is derived from an enterprise value of 24,170 with a discount rate of 7.34%. This implied share value shows that DaVita is currently 9.54% undervalued.

A sensitivity analysis reveals that DaVita’s implied share price is between 71.94 – 82.07 which aligns with our comparable companies analysis based off of estimated 2016 EBITDA

Current Share Price

90-dayAvg.volume

52wk High

52wklow

Price/Book

Price/ Sales

Price/ Cash flow

$69.96 1.5M 85.17 61.36 230 1.1 9.9

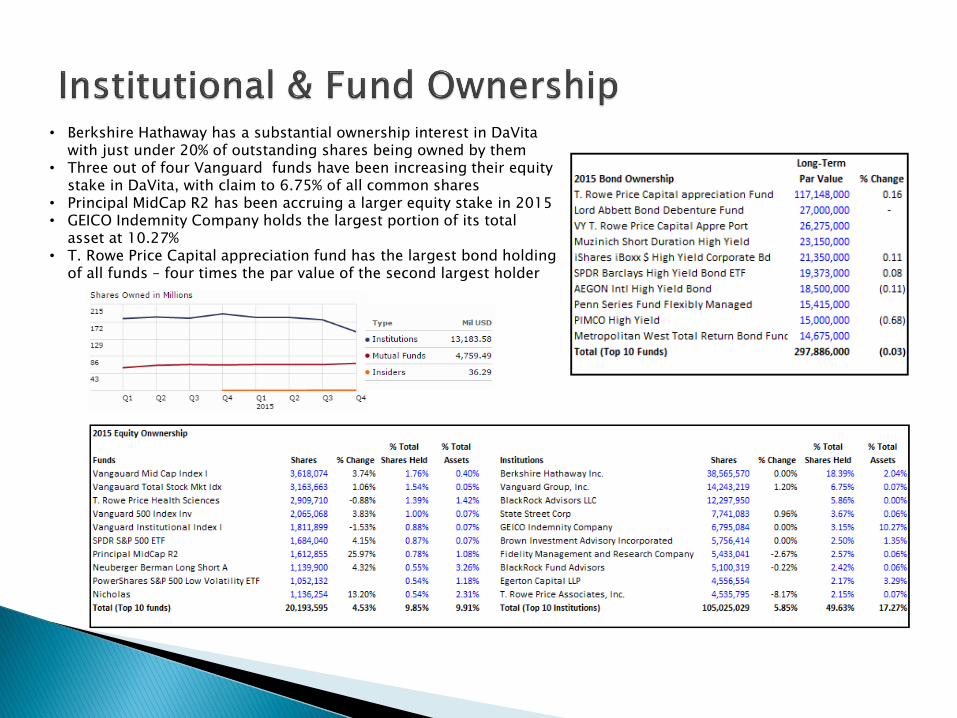

• Berkshire Hathaway has a substantial ownership interest in DaVita with just under 20% of outstanding shares being owned by them

• Three out of four Vanguard funds have been increasing their equity stake in DaVita, with claim to 6.75% of all common shares

• Principal MidCap R2 has been accruing a larger equity stake in 2015• GEICO Indemnity Company holds the largest portion of its total

asset at 10.27%• T. Rowe Price Capital appreciation fund has the largest bond holding

of all funds – four times the par value of the second largest holder

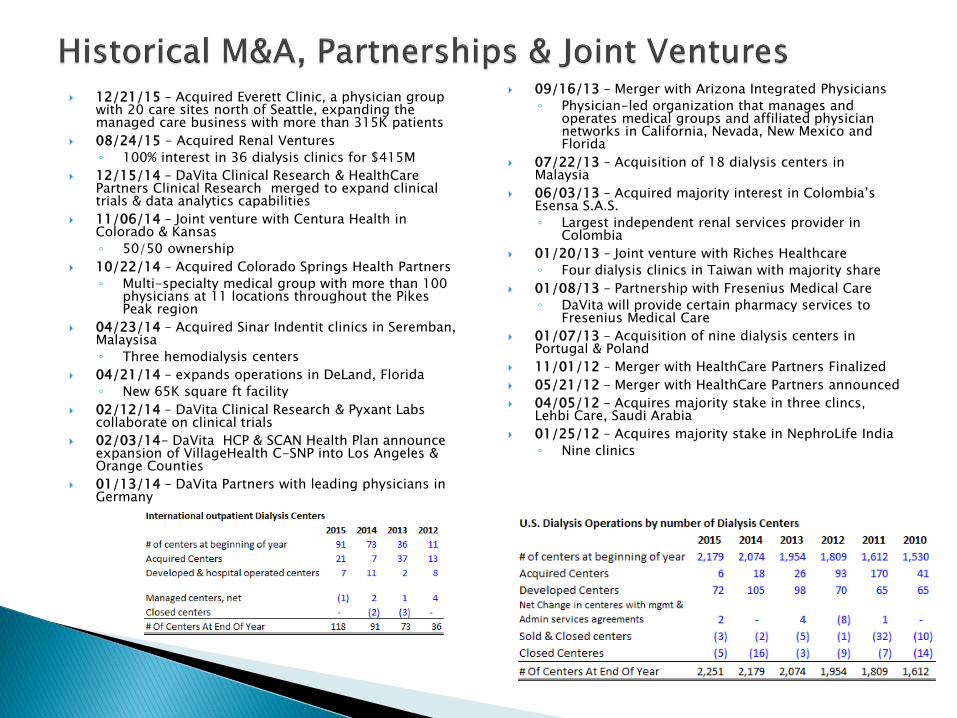

12/21/15 – Acquired Everett Clinic, a physician group with 20 care sites north of Seattle, expanding the managed care business with more than 315K patients

08/24/15 - Acquired Renal Ventures

◦ 100% interest in 36 dialysis clinics for $415M

12/15/14 – DaVita Clinical Research & HealthCare Partners Clinical Research merged to expand clinical trials & data analytics capabilities

11/06/14 – Joint venture with Centura Health in Colorado & Kansas

◦ 50/50 ownership

10/22/14 – Acquired Colorado Springs Health Partners

◦ Multi-specialty medical group with more than 100 physicians at 11 locations throughout the Pikes Peak region

04/23/14 – Acquired Sinar Indentit clinics in Seremban, Malaysisa

◦ Three hemodialysis centers

04/21/14 – expands operations in DeLand, Florida

◦ New 65K square ft facility

02/12/14 – DaVita Clinical Research & Pyxant Labs collaborate on clinical trials

02/03/14- DaVita HCP & SCAN Health Plan announce expansion of VillageHealth C-SNP into Los Angeles & Orange Counties

01/13/14 – DaVita Partners with leading physicians in Germany

09/16/13 – Merger with Arizona Integrated Physicians

◦ Physician-led organization that manages and operates medical groups and affiliated physician networks in California, Nevada, New Mexico and Florida

07/22/13 – Acquisition of 18 dialysis centers in Malaysia

06/03/13 – Acquired majority interest in Colombia’s Esensa S.A.S.

◦ Largest independent renal services provider in Colombia

01/20/13 – Joint venture with Riches Healthcare

◦ Four dialysis clinics in Taiwan with majority share

01/08/13 – Partnership with Fresenius Medical Care

◦ DaVita will provide certain pharmacy services to Fresenius Medical Care

01/07/13 – Acquisition of nine dialysis centers in Portugal & Poland

11/01/12 – Merger with HealthCare Partners Finalized

05/21/12 – Merger with HealthCare Partners announced

04/05/12 – Acquires majority stake in three clincs, Lehbi Care, Saudi Arabia

01/25/12 – Acquires majority stake in NephroLife India

◦ Nine clinics

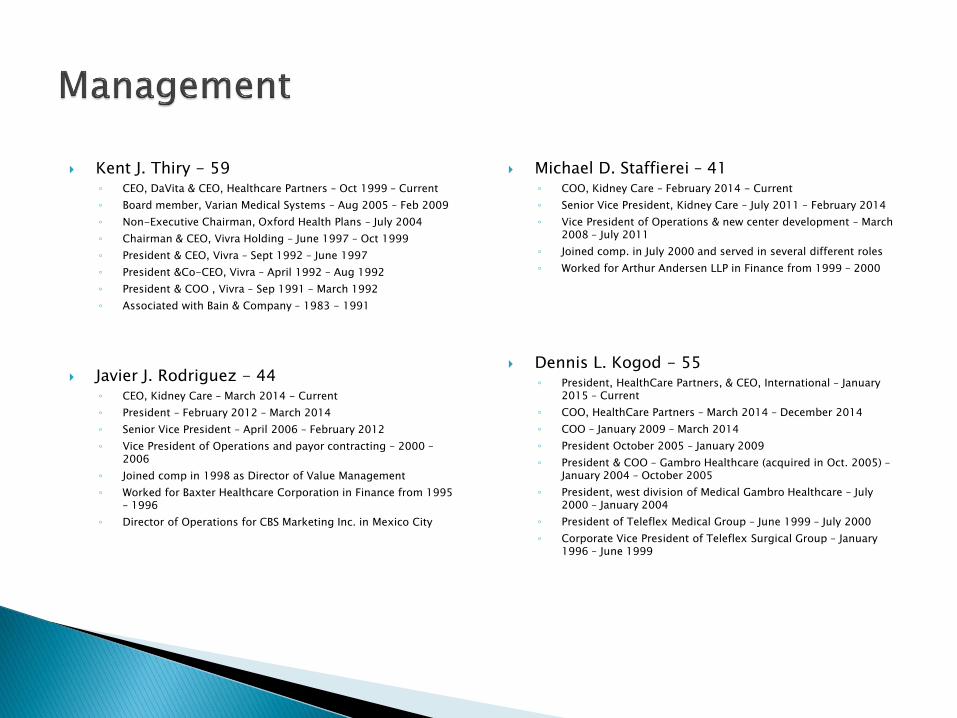

Kent J. Thiry - 59◦ CEO, DaVita & CEO, Healthcare Partners – Oct 1999 – Current

◦ Board member, Varian Medical Systems – Aug 2005 – Feb 2009

◦ Non-Executive Chairman, Oxford Health Plans – July 2004

◦ Chairman & CEO, Vivra Holding – June 1997 – Oct 1999

◦ President & CEO, Vivra – Sept 1992 – June 1997

◦ President &Co-CEO, Vivra – April 1992 – Aug 1992

◦ President & COO , Vivra – Sep 1991 – March 1992

◦ Associated with Bain & Company – 1983 - 1991

Javier J. Rodriguez - 44◦ CEO, Kidney Care – March 2014 - Current

◦ President – February 2012 – March 2014

◦ Senior Vice President – April 2006 – February 2012

◦ Vice President of Operations and payor contracting – 2000 –2006

◦ Joined comp in 1998 as Director of Value Management

◦ Worked for Baxter Healthcare Corporation in Finance from 1995 – 1996

◦ Director of Operations for CBS Marketing Inc. in Mexico City

Michael D. Staffierei – 41 ◦ COO, Kidney Care – February 2014 - Current

◦ Senior Vice President, Kidney Care – July 2011 – February 2014

◦ Vice President of Operations & new center development – March 2008 – July 2011

◦ Joined comp. in July 2000 and served in several different roles

◦ Worked for Arthur Andersen LLP in Finance from 1999 – 2000

Dennis L. Kogod - 55◦ President, HealthCare Partners, & CEO, International – January

2015 – Current

◦ COO, HealthCare Partners – March 2014 – December 2014

◦ COO – January 2009 – March 2014

◦ President October 2005 – January 2009

◦ President & COO – Gambro Healthcare (acquired in Oct. 2005) –January 2004 – October 2005

◦ President, west division of Medical Gambro Healthcare – July 2000 – January 2004

◦ President of Teleflex Medical Group – June 1999 – July 2000

◦ Corporate Vice President of Teleflex Surgical Group – January 1996 – June 1999

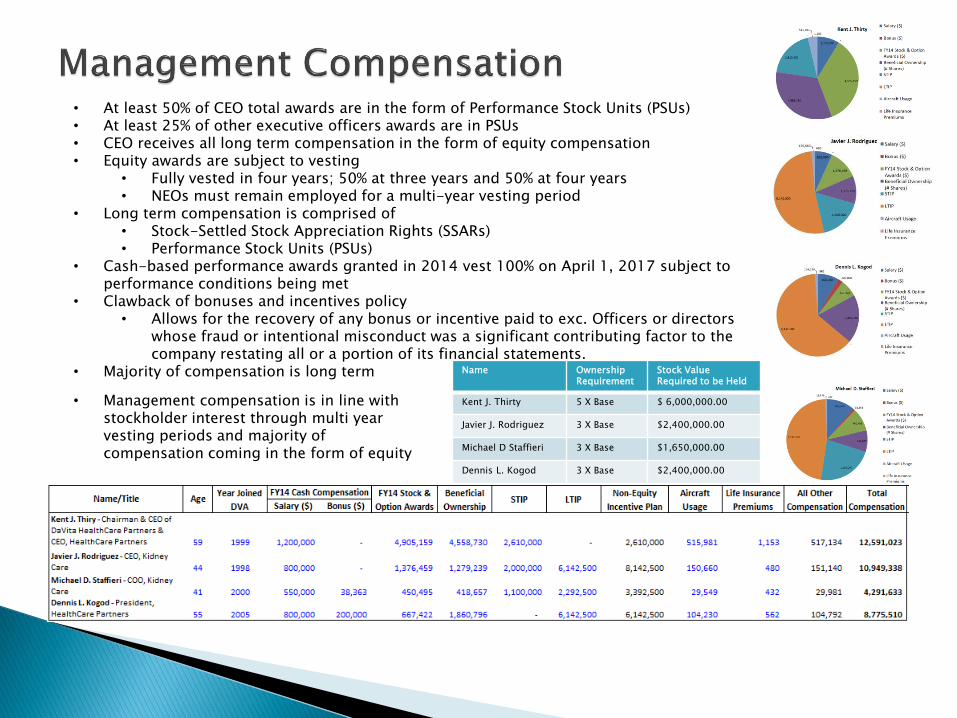

Name Ownership Requirement

Stock Value Required to be Held

Kent J. Thirty 5 X Base $ 6,000,000.00

Javier J. Rodriguez 3 X Base $2,400,000.00

Michael D Staffieri 3 X Base $1,650,000.00

Dennis L. Kogod 3 X Base $2,400,000.00

• At least 50% of CEO total awards are in the form of Performance Stock Units (PSUs)• At least 25% of other executive officers awards are in PSUs• CEO receives all long term compensation in the form of equity compensation• Equity awards are subject to vesting

• Fully vested in four years; 50% at three years and 50% at four years• NEOs must remain employed for a multi-year vesting period

• Long term compensation is comprised of• Stock-Settled Stock Appreciation Rights (SSARs)• Performance Stock Units (PSUs)

• Cash-based performance awards granted in 2014 vest 100% on April 1, 2017 subject to performance conditions being met

• Clawback of bonuses and incentives policy• Allows for the recovery of any bonus or incentive paid to exc. Officers or directors

whose fraud or intentional misconduct was a significant contributing factor to the company restating all or a portion of its financial statements.

• Majority of compensation is long term

• Management compensation is in line with stockholder interest through multi year vesting periods and majority of compensation coming in the form of equity

Kent J. Thiry - Chairman & CEO of DaVita HealthCare Partners Inc. & CEO of HealthCare Partners◦ Chairman of the board & CEO of Vivra Holdings, Inc.

◦ VP of Bain & Company

◦ fmr board member of Varian Medial Systems Inc.

◦ Non-Exc. Chairman of Oxford Health Plans, Inc.

Pamela M. Arway - Former President of American Express International, Japan, Asia-Pacific, Australia region◦ President of American Express International

◦ Board member of the Hershey Company

◦ Board member of Iron Mountain Inc.

Charles G. Berg - Former Non-Executive Chairman of WellCare Health Plans, Inc.◦ Exc Chairman of the board of WellCare Health Plans, Inc.

◦ Senior advisor to Welsh, Carson, Anderson & Stowe

◦ Exc. With Oxford Health Plans, Inc.

◦ Operating Council of Consonance Capital Partners

Carol Anthony "John" Davidson - Former Senior VP, Controller, & CAO of Tyco International, Ltd.◦ SVP, Controller & CAO of Tyco International

◦ VP, Audit, risk & compliance & corporate controller of Dell

◦ Eastman Kodak Comp.

◦ Director of Legg Mason Inc.

◦ Member of the board of Trustees o the Financial Accounting Foundation

◦ Board of Governors of FINRA

Barbara J Desoer – CEO, Citibank, N.A.◦ Fmr. CFO, Citibank from Oct 2013 – April 2014

◦ Fmr President, Bank of America Home Loans, & Global Tech & Ops Exc.,

◦ Serves on the advisory Council of the Haas School of Business at the University of California at Berkeley

◦ Fmr. Board member of various non-profit and privately held corporations

Paul J. Diaz - President & CEO of Kindred Healthcare, Inc.◦ Exc Vice Chair of Kindred Healthcare, Inc.

◦ Managing Director of Falcon Capital Partners, LLC

◦ Exc. With Mariner Health Group, Inc.

◦ Board member of Kindred

◦ Board member of Georgetown University Law Center

◦ Fmr. board member of PharMerica Corporation

Peter T. Grauer - Chairman of the Board, Treasurer, and former CEO of Bloomberg, Inc.◦ Chairman of the board of Bloomberg, Inc.

◦ Non-Exc director of glencore plc

◦ Managing Director of Credit Suisse First Boston

John M. Nehra - General Partner of New Enterprise Associates◦ New Enterprise Associates

◦ Managing general partner of Catalyst Ventures

Dr. William L. Roper - CEO of University of North Carolina Health Care System, Dean of the UNC School of Medicine, & Vice Chancellor for Medical Affairs of UNC◦ CEO, University of North Carolina Health Care System SVP, of Prudential

Health Care

◦ Director of the Centers for Disease Control & Prevention on the White House Staff

◦ Chairman of the board of National Quality Forum

◦ Boardmember of medco Health Solutions, Inc.

Roger J. Valine - Former President and CEO of Vision Service Plan◦ CEO of Vision Service Plan

◦ Fmr. Board member of American specialty Health Incorporated & SureWest Communications

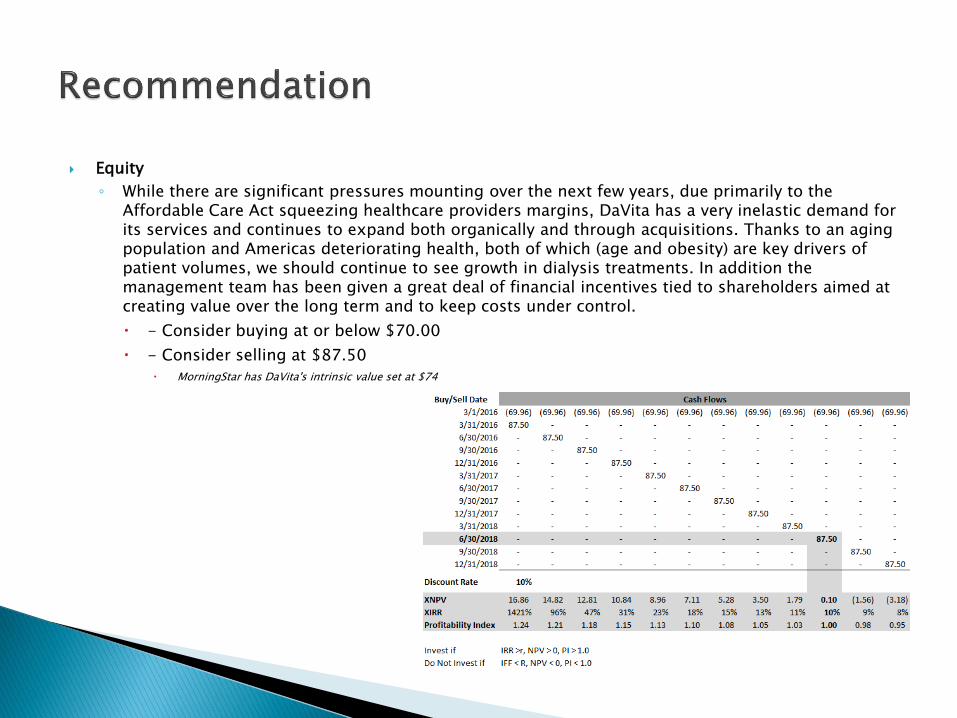

Equity

◦ While there are significant pressures mounting over the next few years, due primarily to the Affordable Care Act squeezing healthcare providers margins, DaVita has a very inelastic demand for its services and continues to expand both organically and through acquisitions. Thanks to an aging population and Americas deteriorating health, both of which (age and obesity) are key drivers of patient volumes, we should continue to see growth in dialysis treatments. In addition the management team has been given a great deal of financial incentives tied to shareholders aimed at creating value over the long term and to keep costs under control.

- Consider buying at or below $70.00

- Consider selling at $87.50

MorningStar has DaVita's intrinsic value set at $74

This material has been prepared by myself, and myself alone, employing appropriate expertise, and in the belief that it is fair and not misleading. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified, therefore, I do not guarantee its accuracy. This is not an offer or solicitation of an offer to buy or sell any security or investment. Any opinion or estimates constitute my own best judgment as of this date, and are subject to change at any time without notice.