Embed Size (px)

Citation preview

De Nederlandsche Bank Eurosysteem

Single Euro Payments Area and the Payment Services Directive Michael van Doeveren

2nd Conference of the Macedonian Financial sector on Payments and Securities settlement Systems Ohrid 29 June 2009

De Nederlandsche Bank

De Nederlandsche Bank Eurosysteem

Agenda

What, why and how about SEPA? SEPA-products Payment Services Directive Impact of SEPA Migration Closing remarks

De Nederlandsche Bank Eurosysteem

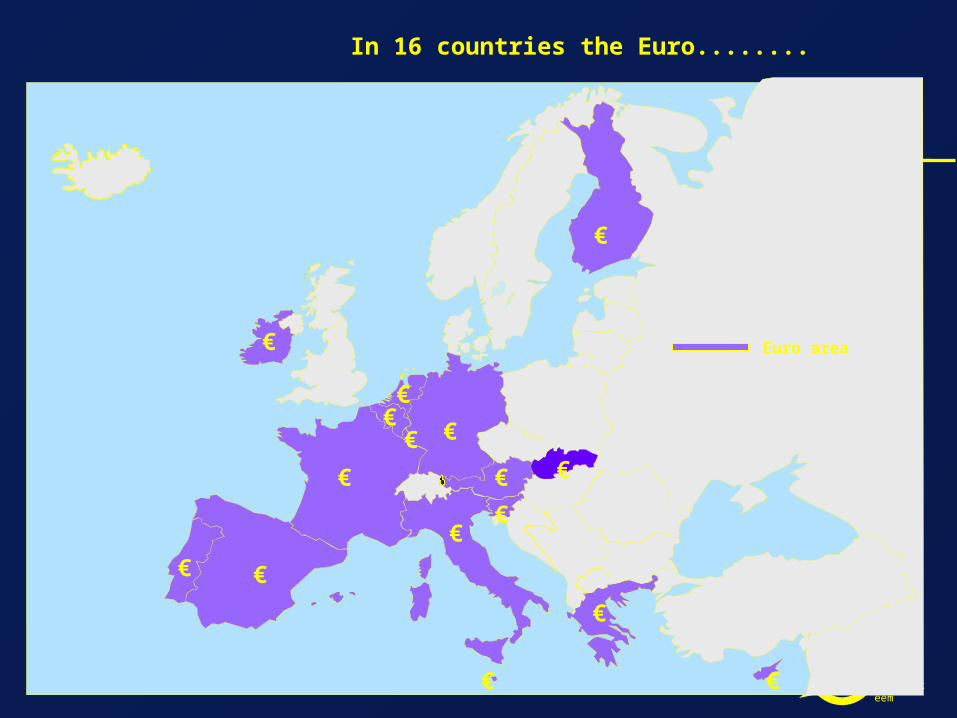

In 16 countries the Euro........

Euro area

€

€

€

€

€

€

€

€

€

€ €

€ €

€

€ €

De Nederlandsche Bank Eurosysteem

.....but completely different standards, products and rules for retail payments…

€

€

€

€

€

€

€

€

€

€ €

€ €

€

€ €

De Nederlandsche Bank Eurosysteem

and the goal of the European Union is to achieve an integrated European payments market

EU

€

€

€

€

€

€

€

€

€

€ €

€

€

€

€

De Nederlandsche Bank Eurosysteem

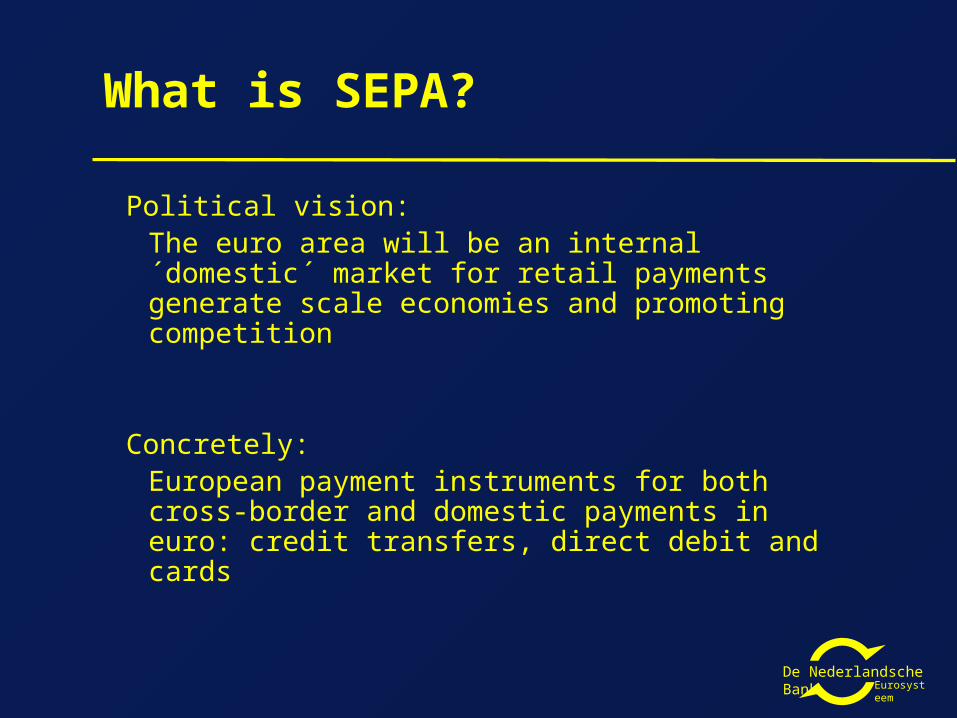

What is SEPA?

Political vision:The euro area will be an internal ´domestic´ market for retail payments generate scale economies and promoting competition

Concretely:European payment instruments for both cross-border and domestic payments in euro: credit transfers, direct debit and cards

De Nederlandsche Bank Eurosysteem

Why SEPA?

European PoliticsImprovement European economy: Lisbon agenda

EconomicsInternal market: volume and competition

Banks To prevent ‘further regulation’ after Regulation 2560/2001

Especially Cross-border banks can profit from new market circumstances

De Nederlandsche Bank Eurosysteem

How to realise SEPA?

Self-regulation: European Payment Council of banks develops standards and products

Payment Services Directive: legal harmonisation

De Nederlandsche Bank Eurosysteem

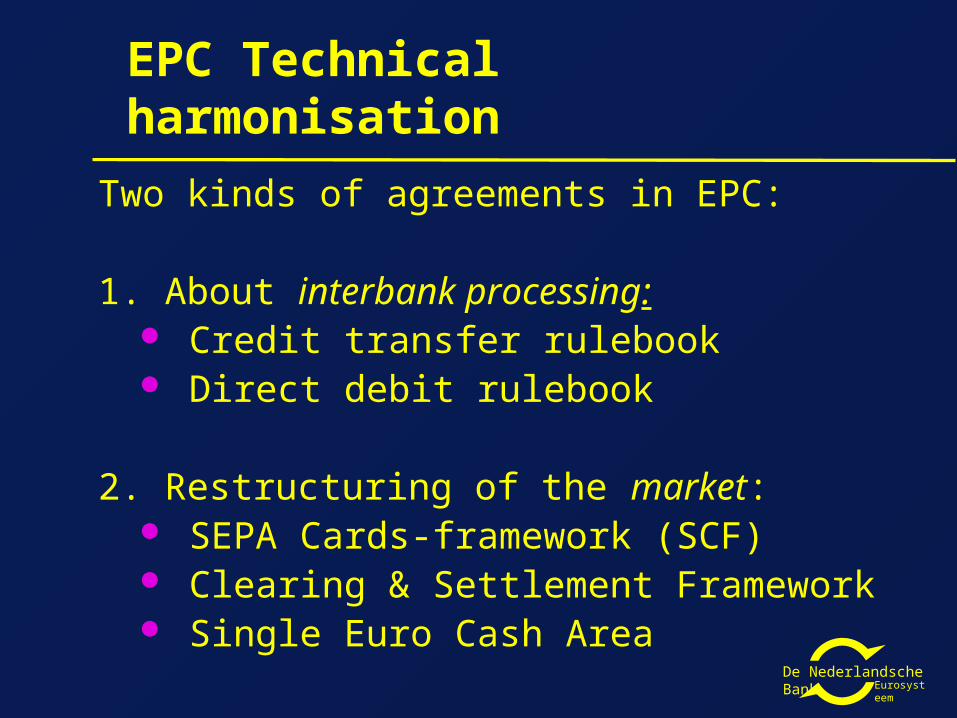

EPC Technical harmonisation

Two kinds of agreements in EPC:

1. About interbank processing: Credit transfer rulebook Direct debit rulebook

2. Restructuring of the market: SEPA Cards-framework (SCF) Clearing & Settlement Framework Single Euro Cash Area

De Nederlandsche Bank Eurosysteem

buyer seller

good/service

debit paymentinstruction

bank bank

paymentinstruction

debit credit

creditpaymentinformation

paymentinformation

Payment chain

clearing

De Nederlandsche Bank Eurosysteem

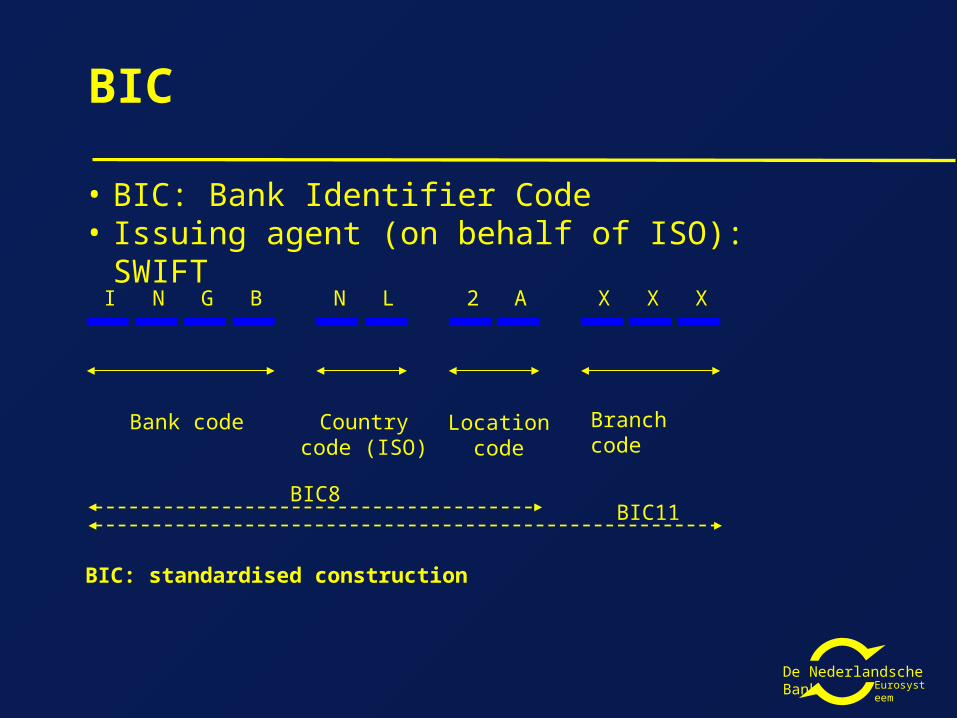

BIC

• BIC: Bank Identifier Code• Issuing agent (on behalf of ISO): SWIFT

Bank code Countrycode (ISO)

Locationcode

Branch code

BIC: standardised construction

BIC8BIC11

I N XG B N L 2 A X X

De Nederlandsche Bank Eurosysteem

IBAN

• IBAN : International Bank Account Number• Administrator of Register of national IBANs (on behalf of ISO): SWIFT

Countrycode (ISO)

Bank identifierCheck digit

Domestic accountNumber

• Remarks:

- The Bank Identifier in an IBAN is country specific

- The length of the bank identifier varies from country to country

- Each country has its own Basic Bank Account Number system

• Summary:

- Country code and check-digits : uniform

- Bankidentifier and BBAN : country specific

De Nederlandsche Bank Eurosysteem

IBAN examples

IBAN Examples

Finland FI21 1234 5600 0007 85France FR14 2004 1010 0505 0001 3M02 606 lengte

27Germany DE89 3704 0044 0532 0130 00Ireland IE29 AIBK 9311 5212 3456 78Luxembourg LU28 0019 4006 4475 0000Netherlands NL91 ABNA 0417 1643 00 lengte

18Norway NO93 8601 1117 947Poland PL61 1090 1014 0000 0712 1981 2874 lengte

28United Kingdom GB29 NWBK 6016 1331 9268 19(composition: country code check digits Bankidentifier branchindentifier BBAN)Source: www.swift.com 20080811 IBAN Registry• Remarks:

• IBAN and BIC contain both bank identifiers, but they could differ

• IBAN and BIC contains both a country code, but they could differ

De Nederlandsche Bank Eurosysteem

SEPA Credit Transfer (in use since 28 January 2008)

SEPA Credit Transfer: Standard for bank to bank credit transfers in euro (mass payments)

Payments are made for the full original amountIBAN and BIC are obligedISO 20022 UNIFI standards (XML-language)140 characters of remittance information are

delivered to the beneficiary Unstructured or restructured remittance

information as agreed between partners

De Nederlandsche Bank Eurosysteem

SEPA Direct Debit(coming from 1 November 2009 on)

SEPA Direct Debit: Standard for bank to bank Direct Debits in euro

Payments are made for the full original amountIBAN and BIC are obligedISO 20022 UNIFI standards (XML-language)One-off or recurrentA mandate is signed by the debtor (e-mandate)Pre-notification (mostly 14 calender days in advance)Refunds (PSD: 8 weeks) and returns

De Nederlandsche Bank Eurosysteem

Competition on cards in SEPA

De Nederlandsche Bank Eurosysteem

Point-of-sale card payment system

De Nederlandsche Bank Eurosysteem

SEPA Cards FrameworkPolicy scope (1)

Seperation of scheme governance from underlying processing

Open non-discriminatory scheme membershipSingle, pan-European licenseOpen and transparant pricing policiesEMV-implementation: Chip and PIN

implementation shift for all cards by end 2010

De Nederlandsche Bank Eurosysteem

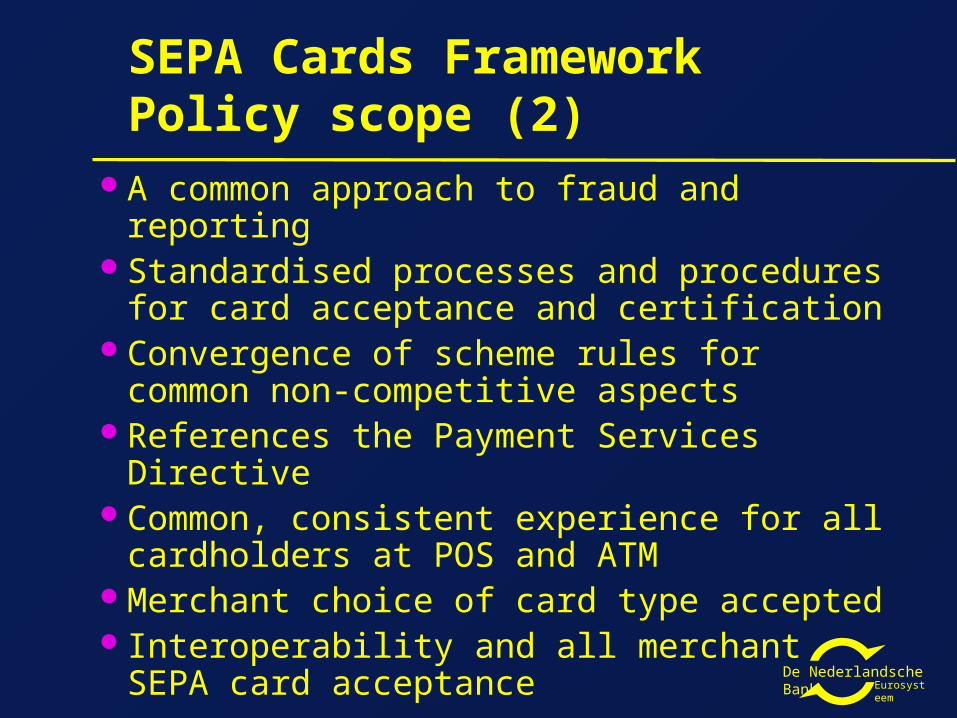

SEPA Cards FrameworkPolicy scope (2)

A common approach to fraud and reportingStandardised processes and procedures for

card acceptance and certificationConvergence of scheme rules for common

non-competitive aspectsReferences the Payment Services DirectiveCommon, consistent experience for all

cardholders at POS and ATMMerchant choice of card type acceptedInteroperability and all merchant SEPA card

acceptance

De Nederlandsche Bank Eurosysteem

SEPA for cardsVision of the Eurosystem (1) The Consumer can choose between different

debit card brands The Merchant can choose which debit cards

brands he or she accept The cards market is competitive, reliable and

efficient, as well as for card holders, merchants as for processing

More aspiration is needed in the SEPA for cards: need for an additional European debit card scheme

Further card standardisation is vital

De Nederlandsche Bank Eurosysteem

SEPA for cardsVision of the Eurosystem (2)

All technical and legal barriers are eliminated Interchange fees should not be misused to

generate excess revenues for the banking system, at the costs of merchants and cardholders

Preference for no MIF-model: see for example the MasterCard and VISA cases

Ideal situation: ‘Any card at any terminal’

De Nederlandsche Bank Eurosysteem

Need for Standardisation!

De Nederlandsche Bank Eurosysteem

Standardisation SEPA for Cards

Card to terminal (EMV)

Terminal-to-acquirer (EPAS, ERIDANE)

Acquirer-to-issuer (ISO 8583 and ISO 20022)

Certification of cards and payment terminals

De Nederlandsche Bank Eurosysteem

Options for SEPA Compliancy

• Select one (or more) of the international schemes to replace the current national schemes

• Make national schemes SCF-compliant

• Co-branding of national systems with international systems

De Nederlandsche Bank Eurosysteem

Initiatives for additional European Card schemes

PayFair:merchant initiativeEAPS: cooperation of national schemesMonnet: French and German banksTransforming a three party payment scheme?Other?

De Nederlandsche Bank Eurosysteem

Impact of SEPA for cards

ConsumersUse of cards in the whole SEPA area: any card at any terminal

RetailersMore choise: terminal, acceptance of brands, acquiring

Banks and payment schemesChange of markets, new products, new systems

De Nederlandsche Bank Eurosysteem

Milestones

Credit transfer and Direct debitEuropean Rulebooks are the basis for products of the banks

Framework for clearing and settlementCredit transfers from 28 January 2008 onDirect debit from end 2009 on

CardsSEPA Cards FrameworkAfter 2010 only SEPA-cards

De Nederlandsche Bank Eurosysteem

Role public sector

SEPA is a project banks: self-regulation via EPC

However… European Commission

Payment Services Directives Public users are the early adopters

Eurosystem: catalyst role 6th Progress report November 2008

De Nederlandsche Bank Eurosysteem

Legal harmonization: Payment Services Directive

Content: Proportional supervisory regime for non-bank payment service providers

Transparency requirementsRules about the relationship of the payment service provider and user

De Nederlandsche Bank Eurosysteem

Payment Institution

What is a payment institution?Non bank provider of payment services, and:End usersTransferable balances: no cashOwns customer funds temporarilyPure intermediaryPayments are a main activity

De Nederlandsche Bank Eurosysteem

Payment institutions

Proportional prudential supervisionLicense Capital requirementsInternal processes

De Nederlandsche Bank Eurosysteem

Rights and obligations

Information requirements - single payment transactions

Information to the payer

prior after receipt

Information needed Execution time

ChargesReference exchange

rate

Transaction Identifier, payeeAmount of the payment

Charges payableexchange rate usedDate of receipt order

Reference, payerAmountCharges

Exchange rateCredit value date

Information to the payee

De Nederlandsche Bank Eurosysteem

Rights and obligations

Information requirements - Payments via framework contract

prior after receipt

Information for payee

Payment service providerSupervisor

Product featuresCharges

Safeguard requirements

Transaction identifier, payeeAmount Charges

Exchange rate usedDebit value date

Transaction identifier, payerAmountCharges

Exchange rate usedCredit value date

De Nederlandsche Bank Eurosysteem

Rights and obligations

Other obligations for the providerd + 1No sending of unsolicited payment

instrumentsUser provides incorrect unique identifier:

reasonable efforts to recover fundsAnd more..

De Nederlandsche Bank Eurosysteem

Rights and obligations

Obligations for the userAct according to the contractReasonable safety measuresDirect notification of loss/theftAnd more..

De Nederlandsche Bank Eurosysteem

PSD wrap up

PSD provides harmonisation of: Market access: besides credit institutions and

electronic money institutions also payment institutions

Rights and obligationsImplementation in national legislation

ultimately 1november 2009

De Nederlandsche Bank Eurosysteem

Non SEPA Compliant instruments

9%

SEPA Credit Transfers29%

SEPA Cards36%

SEPA Direct Debits26%

Potential for SEPA compliancy NL

De Nederlandsche Bank Eurosysteem

Impact of SEPA

ConsumersUse IBAN and BIC Use of cards in the whole SEPA area

Firms (private and public)Easier cash-management and administrationStandard formats (ISO 20022 XML)Use of IBAN and BICCentralisation of accounts and direct debits

RetailersMore choise: terminal, acceptance of brands, acquiring

BanksChange of markets, new products, new systems

De Nederlandsche Bank Eurosysteem

Benefits of SEPA

Efficiency, level playing field and transparency lead to cost benefits for society in the long run

Reduction costs for average user of payment services in Europe

Comfort/User-friendliness

Innovation

De Nederlandsche Bank Eurosysteem

Migration

Aim: a smooth migration to SEPATo organise nationallyMarket drivenSpeed can differ between countriesStakeholder involvement and communication are

important tools for successNeed for an end date

De Nederlandsche Bank Eurosysteem

Migration Plan of the Netherlands

Objective: an orderly and efficiently change over from domestic payments to SEPA

Scope: all existing payment instruments for which there is a SEPA-alternative

Consequences and choices for different stakeholders

Market driven migration Identifying barriers, changes and solutions Mid 2009 evaluation: an end date can foster

migration

De Nederlandsche Bank Eurosysteem

Points of concern SEPA National Forum on the Payment System

Price developments Range of options open to consumers and retailers,

caterers and other regarding debit card brands User-friendliness of migration to IBAN and BIC Safety of SEPA direct debit Prolongation of direct debit contracts and mandates Standardisation in the Bank-client domain Interbank Swich support service Dispute handling Accessibility of the noncash payment system Consultation process

De Nederlandsche Bank Eurosysteem

Closing remarks

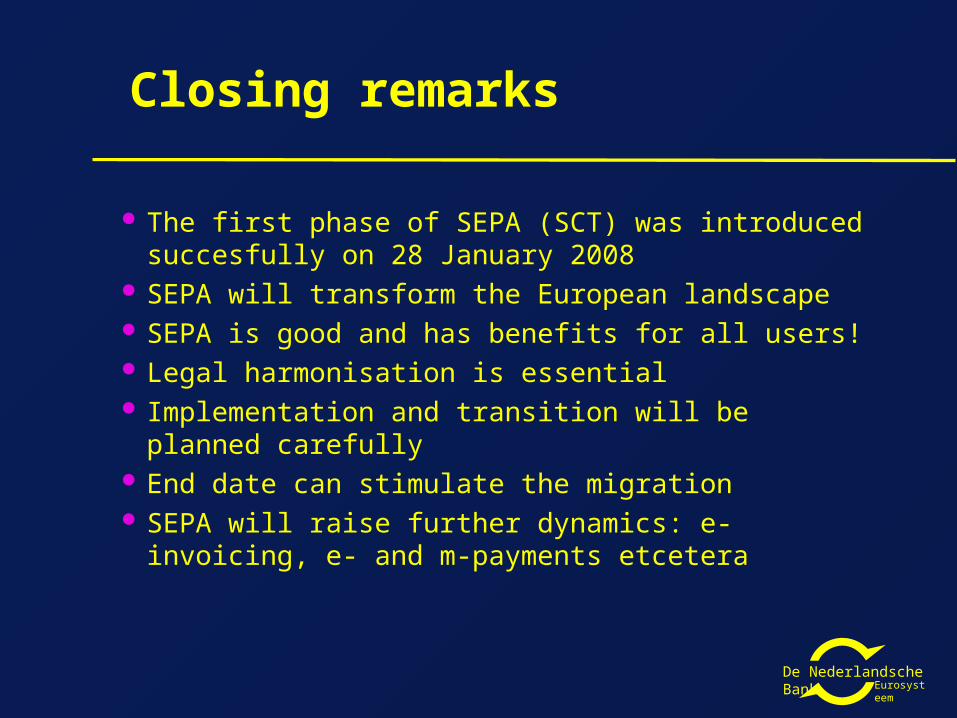

The first phase of SEPA (SCT) was introduced succesfully on 28 January 2008

SEPA will transform the European landscape SEPA is good and has benefits for all users! Legal harmonisation is essential Implementation and transition will be planned

carefully End date can stimulate the migration SEPA will raise further dynamics: e-invoicing, e- and

m-payments etcetera