Embed Size (px)

Citation preview

ERD TECHNICAL NOTE NO. 15

DEBT MANAGEMENT ANALYSIS

OF NEPAL’S PUBLIC DEBT

SUNGSUP RA, CHANGYONG RHEE, AND JOON-HO HAHM

December 2005

Sungsup Ra is Senior Economist in the South Asian Department, Asian Development Bank; Changyong Rhee isProfessor in the Department of Economics, Seoul National University; and Joon-Ho Hahm is Associate Professorat the Graduate School of International Studies, Yonsei University, Seoul, Republic of Korea.

Asian Development Bank6 ADB Avenue, Mandaluyong City1550 Metro Manila, Philippineswww.adb.org/economics

©2005 by Asian Development BankDecember 2005ISSN 1655-5236

The views expressed in this paperare those of the author(s) and do notnecessarily reflect the views or policiesof the Asian Development Bank.

FOREWORD

The ERD Technical Note Series deals with conceptual, analytical, ormethodological issues relating to project/program economic analysis orstatistical analysis. Papers in the Series are meant to enhance analytical rigorand quality in project/program preparation and economic evaluation, andimprove statistical data and development indicators. ERD Technical Notesare prepared mainly, but not exclusively, by staff of the Economics andResearch Department, their consultants, or resource persons primarily forinternal use, but may be made available to interested external parties.

CONTENTS

Abstract vii

I. Introduction 1

II. Outline of Methodology 3

III. Efficient Frontier and Benchmark Portfolio for Domestic Government Debt 4

A. The Data: Basic Profiles of Government Debt Portfolios in Nepal 4B. Obtaining the Efficient Portfolio Set Conditional

upon Existing Domestic Debt Structure 6C. Benchmark Portfolios and Optimal Borrowing Strategies 13

IV. Efficient Frontier and Benchmark Portfoliofor External Government Debt 13

A. The Data: Basic Profiles of External Debt Portfolios in Nepal 14B. Derivation of Efficient Portfolio Set Conditional

upon Existing External Debt Structure 14C. Benchmark Portfolios and Optimal Borrowing Strategies 17

V. Concluding Remarks 19

References 20

ABSTRACT

This paper estimates an optimal target portfolio of sovereign debt forNepal that minimizes long-term financing cost. In the analysis, a practicalframework is applied, which is built upon the traditional mean–varianceefficient frontier approach and simultaneously employs a relatively newconcept of cost-at-risk (CaR). The framework is flexible enough to incorporateother factors such as liquidity risk. Simulation results show that the Nepalieconomy needs to increase longer-term domestic borrowing instruments, andthat the maturity structure of domestic bonds should be simplified. Thesimulation also suggests an optimal currency composition of external debtsin Nepal.

11111ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

I. INTRODUCTION

High levels of sovereign debt are a common feature of modern economies. With the increasedsophistication and liberalization of financial markets, this has made the problem of debt managementone of the most important issues in economic policy. In this paper, we take up the question of whatis a desirable scheme for Nepal’s sovereign debt management.

The optimal volume and sustainability of sovereign debt are important issues with regard tosovereign debt management.1 However, sustainability of sovereign debt may be more important thanits management, particularly for an underdeveloped economy with a relatively large burden of sovereigndebt such as Nepal. It should be also noted that effective sovereign debt management increasessustainability.

The Nepali economy relies heavily on short-term domestic debt and highly concessional foreignaid loans of long maturity. More than 60% of domestic debt has maturities of one year or shorter,and less than 9% of domestic debt has maturities of 10 years or longer. The bulk of the cheap foreignloans have maturities longer than 30 years and account for more than 57% of the financing of thebudget deficits in Nepal. Concessional foreign loans have been the best source of financing, but willnot be available forever. Therefore, the problem of debt management is increasingly important forthe Nepali economy.

Beyond the problem of debt sustainability, why does sovereign debt management matter? First,sovereign debt management has important effects on the real economy.2 The financial decisions ofa sovereign borrower may have an impact on the expected returns not only on government securitiesbut also on private assets, especially if the economy is large and/or restrictions exist on capital mobility.Changes in the relative supply of debt instruments may affect risk premia and, in particular, theexpected return that private investors require to hold equities and private debt. Through the financialmarket, government debt decisions may influence the cost of funds and, thus, total real investment.Second, debt management may redistribute risks. With incomplete markets for private financialassets, the introduction of a new government security instrument would lead to a reallocation ofrisks and would possibly open up new opportunities for individuals to share risk. Finally, debtmanagement matters because it affects taxation and changes the distribution of taxes across futurecontingencies. Taxes distort the investment and labor choices of private agents. High and variabletax rates reduce people’s incentives to work and produce.

1 For sustainability issues, see Cohen (1991) and Eaton (1992), among others.2 Only under restrictive assumptions about private agents’ altruism and rationality, completeness and efficiency of financial

markets, and type of taxes, does the sovereign debt management not matter. See Missale (1999, chapter 2).

22222 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

The ultimate objective of sovereign debt management is to minimize the long-term cost of debtgiven the trade-off between expected debt service costs and risks associated with various borrowingstrategies to finance the borrowing requirements of the government. The problem of debt managementinterpreted in this way is a common issue for most economies.3 In this study, the problem is to findan optimal target debt portfolio that minimizes the long-term cost of debt given the trade-off betweenexpected debt service costs.

In the analysis, we apply a practical analytical framework studied in Hahm and Kim (2003)to Nepali data and identify the target portfolio structure for managing sovereign debt. The analyticalframework is built upon the traditional mean–variance efficient frontier approach and employsa relatively new concept of cost-at-risk (CaR) to identify a target benchmark portfolio. Whilethe efficient frontier and CaR measures are estimated from the perspective of debt servicecost risk, the benchmarking framework is flexible enough to incorporate other factors suchas liquidity risks and counter-party asset structures as additional criteria in identifying thebenchmark portfolio.

Sovereign debt generally consists of domestic and foreign debts. Thus, one has to considerdomestic and foreign debts together in analyzing issues of sovereign debt. In the case of Nepal, however,we analyze portfolios of domestic and foreign debts separately due to the limited availability of data.

In analyzing portfolios of domestic debt, we focus on the maturity structure of the debt andseek answers to the following questions: First, how can we characterize the trade-off between expecteddebt service cost and risk given the current structure of the debt and borrowing requirements inthe future? Second, what is the optimal debt maturity structure given the cost and risk trade-offidentified in the first step? Finally, what is the best policy for debt issuance to obtain the benchmarkportfolio structure?

Reviewing the basic profiles of the Nepali central government domestic debts, we see twonoticeable features: First, short-term bonds with maturities of less than 5 years constitute about87% of the whole portfolio. Longer-term debt is usually associated with lower risk (volatility) buthas a higher average cost of borrowing. A shorter-term debt is associated with a lower average costof borrowing but with higher risk. The government needs to balance the cost and risk of borrowingby choosing an appropriate portfolio of borrowing. Second, there are various durations/maturitiesof bonds and the amount of bonds in each duration is small, implying that the market is fragmented,thus liquidity problems may arise. Our simulation analysis shows that the Nepali economy needsto move to longer-term domestic borrowing and that the issue profile of domestic bonds should besimplified.

On the other hand, in analyzing portfolios of foreign debt, we focus on the currency compositionof the debt and follow the same procedure as for analyzing portfolios of domestic debt. Due to limitedavailability of data we could not consider all the currencies. Also, for many currencies the loansare in the form of a multi-currency loan, for which we do not have enough data. In this report weconsider only four currencies: Saudi riyal (SAR), Kuwaiti dinar (KWD), United States dollar (USD),and Special Drawing Rights (SDR) relative to Nepali rupee (NRS).

3 See Carracedo and Dattels (1997) and Cassard and Folkerts-Landau (1997), among others, for surveys of the objectivesand practices of sovereign debt management in various countries.

33333ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

SSSSSECTIONECTIONECTIONECTIONECTION II II II II IIOOOOOUTLINEUTLINEUTLINEUTLINEUTLINE OFOFOFOFOF M M M M METHODOLOGYETHODOLOGYETHODOLOGYETHODOLOGYETHODOLOGY

From our simulation study we obtained an optimal currency composition of 10% SAR,10% KWD, 80% USD, and 0% SDR. This result is consistent with statistical features of eachof the four currencies under study. That is, comparing the mean and variability of the borrowingcosts, we found that USD dominates in both mean and variance of the cost; SAR is betterthan KWD in the mean cost, but KWD is better than SAR in variability; and SDR is inferiorto all the other three in both mean and variance.

Our discussion proceeds as follows: In Section II, we explain the methodology of ouranalysis. Sections III and IV apply the method explained in Section II to Nepali sovereigndebt portfolios. For both domestic and external sovereign debt portfolios we identify targetdebt structures and derive optimal borrowing mixes. Section V concludes our analysis.

II. OUTLINE OF METHODOLOGY

We adopt the approach of Hahm and Kim (2003) for our analysis,4 i.e., we consider the problemof determining the sovereign debt portfolio as a portfolio optimization problem. As noted byClaessens (1992), the problem can be represented as a variant of the following stochasticdynamic programming:

Minimize E{f(s ; d)}, where d is in D (1)

where d stands for a sequence of decisions to be made, and D is the set of all acceptable decisions;E is an expectation operator and the function f is an objective function that serves as decision criteria.s provides a description of possible future environments when the consequences of the decisions dare evaluated. In a dynamic discrete time setting, where time 0 and 1 represent today and nextperiod and so on, the above problem can be restated as follows:

Find d = (d0, d1(s1), d2(s1,s2), …) (2)

such that d0 in D0,

d1(s1) in D1(s1; d0),

d2(s1,s2) in D2(s1,s2; d0,d1(s1)), ………..

which minimizes E{f(s1,s2,…; d0,d1,……)}

In the context of sovereign debt management, d may correspond to decisions on thematurity structure of the government debt portfolio or on the currency composition in thecase of external sovereign debt. The vector of random variables s may correspond to the termstructure of interest rates, exchange rates, GDP growth rates, and so forth. The choice setD represents the range of possible decisions and reflects policy constraints such as the minimumexposure to a specific currency or the maximum percentage of refinancing. The subsequentchoice set D in the future depends upon the realizations of random variables as well as previousdecisions. For instance, the debt portfolio structure to be realized 5 years from now (2006–

4 Hahm and Kim (2003) provide an excellent exposition of the method that we employ in this paper. This section islargely based on Hahm and Kim (2003).

44444 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

2010) will depend upon realizations of term structures, fiscal requirements, refinancing policiesof maturing debts, and interim borrowing mixes to finance borrowing requirements over thenext 5 years. The control function f can be specified in various forms and necessarily involvesan attribute of the debt portfolio depending upon which risk is to be more actively managed.For instance, nominal values, market values, or debt service costs of the government debtcan serve as arguments of the control function depending upon the detailed objectives ofgovernment debt management. The control function usually involves a target risk measureand is often represented in the form of a penalty function. For more details, see Hahm and Kim(2003).

The objective and horizon of government debt management differ from those of privateinstitutions. For this reason, the types of risks actively managed at the sovereign level also differfrom those of the private sector. Since most governments tend to hold debts up to maturity and donot frequently liquidate and reconstruct debt portfolios, sovereign debt managers are more concernedabout debt service costs, which directly affect government budget expenses, rather than day-to-dayfluctuations in the market value of debt portfolios. Hence, in the present paper, we assume that thedebt service cost risk is a primary concern for the government in managing sovereign debts.

Also, as noted in Hahm and Kim (2003), the debt service cost of a debt portfolio in any givenyear depends upon the interest rates and debt issuance up to that year. Given the government borrowingrequirements over the debt management horizon and the description of stochastic processes of randomvariables during the horizon, we can solve the above problem to identify an optimal debt strategy.More specifically, once the government’s fiscal requirement over the debt management horizon isgiven, the first step in benchmarking is to identify the expected cost–risk trade-off over variousborrowing strategies satisfying the government financing requirements. This step corresponds toidentifying the decision choice sets D1, D2… into the future. An efficient portfolio set at theend of the debt management horizon is derived as a summary of the expected cost-risk trade-off based upon full-blown term structure simulations over the horizon. In the next step, weemploy a control function f, and based upon exogenously given control targets, an optimalbenchmark portfolio is identified from the efficient portfolio set.

III. EFFICIENT FRONTIER AND BENCHMARK PORTFOLIOFOR DOMESTIC GOVERNMENT DEBT

A. The Data: Basic Profiles of Government Debt Portfolios in Nepal

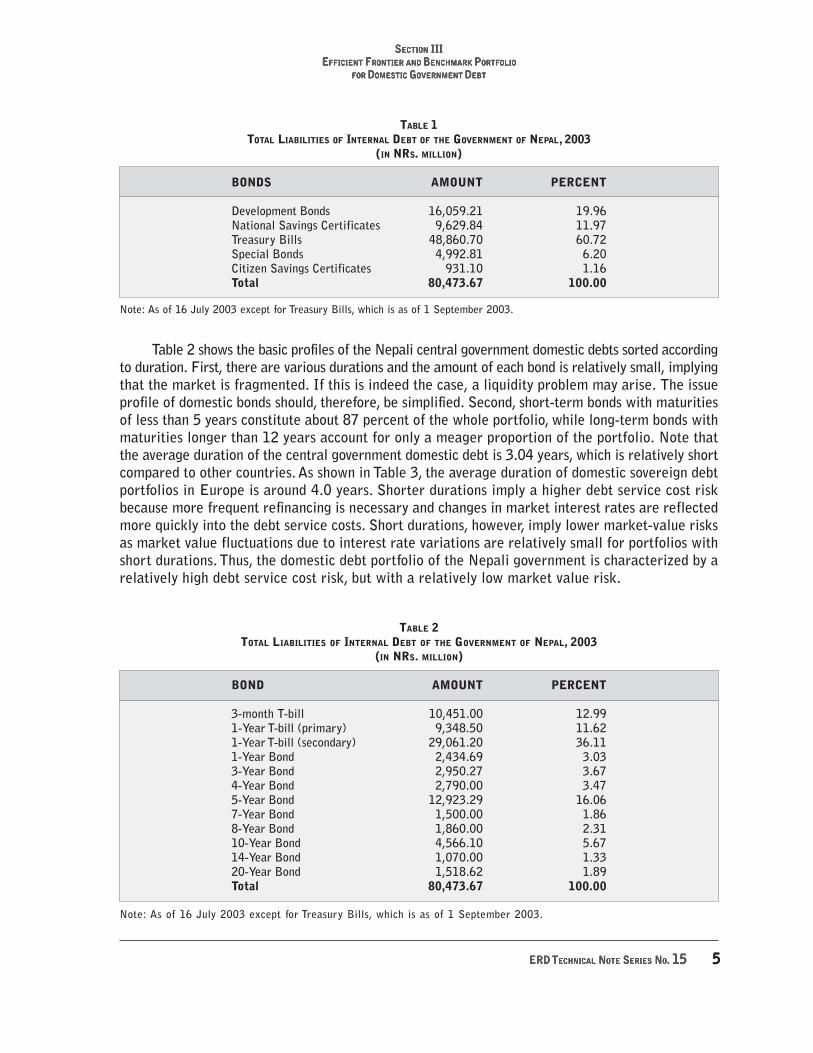

Table 1 summarizes the basic profiles of domestic debt of the central government in Nepalby category as of 16 July 2003. The domestic debt portfolio consists of treasury bills,development bonds, national saving certificates, special bonds, and citizen savings certificates.Treasury bills account for the largest share of the domestic debt portfolio, and developmentbonds and national savings certificates also represent relatively large shares.

55555ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

SSSSSECTIONECTIONECTIONECTIONECTION III III III III IIIEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR D D D D DOMESTICOMESTICOMESTICOMESTICOMESTIC G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

TABLE 1TOTAL LIABILITIES OF INTERNAL DEBT OF THE GOVERNMENT OF NEPAL, 2003

(IN NRS. MILLION)

BONDS AMOUNT PERCENT

Development Bonds 16,059.21 19.96National Savings Certificates 9,629.84 11.97Treasury Bills 48,860.70 60.72Special Bonds 4,992.81 6.20Citizen Savings Certificates 931.10 1.16Total 80,473.67 100.00

Note: As of 16 July 2003 except for Treasury Bills, which is as of 1 September 2003.

Table 2 shows the basic profiles of the Nepali central government domestic debts sorted accordingto duration. First, there are various durations and the amount of each bond is relatively small, implyingthat the market is fragmented. If this is indeed the case, a liquidity problem may arise. The issueprofile of domestic bonds should, therefore, be simplified. Second, short-term bonds with maturitiesof less than 5 years constitute about 87 percent of the whole portfolio, while long-term bonds withmaturities longer than 12 years account for only a meager proportion of the portfolio. Note thatthe average duration of the central government domestic debt is 3.04 years, which is relatively shortcompared to other countries. As shown in Table 3, the average duration of domestic sovereign debtportfolios in Europe is around 4.0 years. Shorter durations imply a higher debt service cost riskbecause more frequent refinancing is necessary and changes in market interest rates are reflectedmore quickly into the debt service costs. Short durations, however, imply lower market-value risksas market value fluctuations due to interest rate variations are relatively small for portfolios withshort durations. Thus, the domestic debt portfolio of the Nepali government is characterized by arelatively high debt service cost risk, but with a relatively low market value risk.

TABLE 2TOTAL LIABILITIES OF INTERNAL DEBT OF THE GOVERNMENT OF NEPAL, 2003

(IN NRS. MILLION)

BOND AMOUNT PERCENT

3-month T-bill 10,451.00 12.991-Year T-bill (primary) 9,348.50 11.621-Year T-bill (secondary) 29,061.20 36.111-Year Bond 2,434.69 3.033-Year Bond 2,950.27 3.674-Year Bond 2,790.00 3.475-Year Bond 12,923.29 16.067-Year Bond 1,500.00 1.868-Year Bond 1,860.00 2.3110-Year Bond 4,566.10 5.6714-Year Bond 1,070.00 1.3320-Year Bond 1,518.62 1.89Total 80,473.67 100.00

Note: As of 16 July 2003 except for Treasury Bills, which is as of 1 September 2003.

66666 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

5 This is just for convenience of indexation in the analysis. As the analysis is based on the accrual data up to 16 July2003, we are in the early part of 3Q2003. Therefore, for readers who are keen at counting dates, the actual periodsin the following analysis should be half a year back.

TABLE 3DURATION OF SOVEREIGN DEBT PORTFOLIOS, 1999–2000

DOMESTIC EXTERNALDEBT DEBT

COUNTRY PORTFOLIO PORTFOLIO

Austria 4.5 _Belgium 4.2 2.2Denmark 4.1 2Finland 3.9 _Italy 2.5 _Portugal 3 3.1Spain 3.2 _United Kingdom 6.8 _Average 4.0 2.4

Sources: World Bank (1999) and Hahm and Kim (2003).

Below, we conduct empirical analysis to obtain a set of efficient cost-risk trade-offs and toidentify the optimal benchmark portfolio. The analysis is based on actual Nepali government debtdata up to 16 July 2003. We suppose that we are at the end of period 4Q2003 (t=4Q2003),and the plan period or debt management horizon is assumed to be 9 years, 1Q2004–4Q2012(N=36).5 The decision interval or time unit of the analysis is assumed to be one quarter because3-month treasury bills are considered.

B. Obtaining the Efficient Portfolio Set Conditional upon Existing DomesticDebt Structure

The set of efficient portfolios for domestic government debt at the end of 4Q2012 isobtained from the set of expected cost–risk trade-offs. We obtain the efficient frontier in twodifferent cases. In Case 1, the instruments considered are the 3-month and 1-year treasurybills, and 3- and 5-year bonds. In Case 2, they are the 3-month and 1-year treasury bills; and3-, 5-, and 10-year bonds. There are bonds of 11 different maturities in our data set, but tosimplify our analysis, we assume that there are four and five different maturities, respectively,in Case 1 and in Case 2. To further simplify the analysis, we assume that both the principalamounts of maturing bonds and the interest payments on all existing bonds are refinancedby the same types of bonds.

We first need to get the values of the primary budget deficit in the period underconsideration. They are obtained based on a large macro model of the Nepali economy andare presented in Table 4.

77777ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

TABLE 4PRIMARY BUDGET DEFICIT UNDER BASIC SCENARIO

(IN NRS MILLION)

2004 2005 2006 2007 2008 2009 2010 2011 2012

23,181 26,195 30,079 34,757 40,314 46,810 54,764 64,548 76,646

We obtain values for the quarterly primary budget deficits over the debt management horizon(N=36) by dividing each annual value by four. We multiply a certain fraction θ =0.4218 to the amountof the budget deficit in a period to get the amount of domestic financing in the period. The fractionθ =0.4218 is the average ratio of the amount of domestic financing to the total budget deficit ineach year in the period 1975–2002. We denote the values of quarterly primary budget deficitsby {Pt+1, Pt+2, …, Pt+36}.

We consider Case 1 below. The same analysis applies to Case 2. In Case 1, the borrowing strategyof the government is a combination of borrowings of four maturities: 3-month and 1-year treasurybills, and 3- and 5-year bonds. We denote it by a vector of weights, w=(w1/4, w1, w3, w5), which sumto unity, where wj is the weight of the j-year bond. We assume that each borrowing strategy is time-invariant, implying that the same weights are maintained throughout the debt management horizon.

We denote the existing government debt portfolio at the end of period t by a vector

Zt t1/4

t1

t-11

t-21

t-31

t3

t-13

t-23

t-113= ( , , , , , , , , , ,z z z z z z z z z z tt

5t-15

t-25

t-195, z z z, , , ) ,

where a typical element zt-ij is the balance of the j-year bond issued in the period t-i. The elements

in Zt are determined by the Nepali central government’s domestic debt portfolio as of July 2003.

Now, for a given borrowing strategy w, the government’s total financing requirement for the next

year, Bt+1 , can be represented as the sum of primary budget deficit Pt+1 and the refinancing amount

αYt+1 , where α ∈[ , ]0 1 is the fraction of refinancing and Yt +1 is the sum of principals of maturingdebt and interest costs to be paid in period t+1. In the simulation, we assume that α =1, whichmeans 100% of maturing debt principals and interest expenses are refinanced.

SSSSSECTIONECTIONECTIONECTIONECTION III III III III IIIEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR D D D D DOMESTICOMESTICOMESTICOMESTICOMESTIC G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

88888 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

B P Y

Y z i z

z i z

t+1 t+1 t+1

t+1 t t t

t-31

t-31

t

where

= +

= +

+ +

α

( )

(

/ / /1 4 1 4 1 4

--3 t-21

t-21

t-11

t-11

t t

t t t t

1 1 1

113

113

113

+ + +

+ + +− − −

i z i z i z

z i z i

)

( −− − − −

− − − −

+ + +

+ + +10

310

31

31

3 3 3

195

195

195

1

z i z i z

z i z zt t t t t

t t t t

)

( 885

185

15

15 5 5z i z i zt t t t t− − −+ + + )

Note that i tj is the interest rate on the j-year bond issued in period t. Under the borrowing

strategy w, the actual issue amount for J respective maturity bonds in the year t+1 can becomputed as follows:

( , , , ) ( , , , )//z z z z B w w w wt t t t t+ + + + +=1

1 41

11

31

51 1 4 1 3 5

Now by the same logic, the total financing requirement for period t+2 and the actual issuanceamount for each bond in period t+2 under the time-invariant borrowing strategy w can be representedas follows.

B P Y

Y z i z

z i

t + + +

+ + + +

−

= +

= +

+ +

2 2 2

2 11 4

11 4

11 4

21

t t

t t t t

t

where

α

( )

(

/ / /

tt t t t t t t t

t t t

− − − − + +

− − −

+ + +

+ +2

12

11

11

1 1 11

11

1

103

103

z i z i z i z

z i z

)

( 1103

93

93 3 3

13

13

185

185

185

+ + + +

+ + +− − + +

− − −

i z i z i z

z i zt t t t t t

t t t

)

( zz z i z i z

z z z

t t t t t t

t t tand

− − + +

+ + +

+ + +175

175 5 5

15

15

21 4

21

23

)

( , , ,/ zz B w w w wt t+ +=25

2 1 4 1 3 5) ( , , , )/

Note that we are at the end of period t, and that Bt+2 is a random variable as interest

rates in the period t+1, ( , , , )/i i i it t t t+ + + +11 4

11

13

15 , are not observed at t. Note also that the actual

amount of bond issuance in period t+2 is determined by the amount borrowed in period t+1.Hence, the issuance amount of each bond in any given period is a function of the borrowingstrategy itself as well as the actual term structure of interest rates up to that period. The processcan be repeated until period t+N. A specific debt portfolio will emerge depending on the pathof term structures during the N periods.

For yield curve simulations, we assume that the yields of government bonds are random

variables that have a multivariate normal distribution.6 Thus, letting it+i t+i1/4

t+i1

t+i3

t+i5=(i , i , i , i ) , we

have it+i ~ ( , )N µ ∑ . We estimate µ µ µ µ µ by the average yield to maturities of Nepali governmentbonds. Due to the lack of data in Nepal, the variance–covariance matrix ∑ is estimated usingthe daily yield curve data on Korean bonds from 30 October 2000 to 28 November 2003.

6 We need much richer data in our analysis to allow possible non-normality, in which case we need to employ a moreor less sophisticated method such as bootstrapping.

(3)

(4)

99999ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

Given a stochastic process of the term structure of interest rates and given a borrowingstrategy w, we can obtain a conditional distribution of the debt service costs on the debt portfoliothat emerges at the end of the horizon by conducting simulations on the term structure ofinterest rates. Each borrowing strategy is characterized by the mean and standard deviationof debt service costs and/or by the cost at the 95th percentile associated with the resultingdebt portfolio. By conducting 1,000 iterations of the simulation for each of the borrowingstrategies, in Figure 1(a), we can obtain all period-end portfolios in the space of the meanand standard deviation, from which we can identify the efficient portfolio set conditional uponthe existing debt portfolio (Case 1). Figure 1(b) plots the mean and the standard deviationof period-end debt portfolios with the emphasis on those at the lower left corner of Figure1(a). The efficient frontier is then constructed in Figure 2 along with the choice of a benchmarkportfolio for domestic debt following the procedure in the next section. The same analysis appliesto Case 2, and the results are in Figures 3 and 4.

The figures show negative trade-offs between expected cost and risk. With the usualupward sloping yield curves, shorter-term financing implies lower expected debt service costbut higher volatility than longer-term financing. There are two reasons for this. First, short-term interest rates are more volatile than long-term interest rates, and short-term financingrequires more frequent refinancing in a debt management horizon. Second, under the liquiditypreference theory of term structures, longer-term financing tends to be associated with higherexpected average annual debt service cost but with lower conditional variance of the averageannual cost. We can obtain the efficient portfolio set by selecting portfolios that yield the lowestexpected cost at each level of standard deviation.

SSSSSECTIONECTIONECTIONECTIONECTION III III III III IIIEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR D D D D DOMESTICOMESTICOMESTICOMESTICOMESTIC G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

FIGURE 1

WHOLE PORTFOLIOS FOR DOMESTIC DEBT (IN RS. MILLION)CASE 1:

0.0 0.2 0.4 0.6 0.8 1.0 1.20

1

2

3

4

5

6

Expecte

dD

ebt

Serv

ice

Cost

x1

05

Risk

(a)X 10

7

1010101010 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

0 1 2 3 4 5 6 7 80.0

0.2

0.4

0.8

1.0

1.4

1.6

1.8

2.0

1.2

Risk

(b)X 10

5

Expecte

dD

ebt

Serv

ice

Cost

x10

5

0.6

4.4

4.0

3.6

3.2

2.8

2.4

2.07.0 7.4 7.8 8.2 8.6 9.0 9.4

X 104

9.8

Risk

Expecte

dD

ebt

Serv

ice

Cost

x1

04

FIGURE 2

EFFICIENT FRONTIER AND BENCHMARK PORTFOLIO

FOR DOMESTIC DEBT (IN RS. MILLION)

CASE 1:

Optimal Portfolio

1111111111ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

SSSSSECTIONECTIONECTIONECTIONECTION III III III III IIIEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR D D D D DOMESTICOMESTICOMESTICOMESTICOMESTIC G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

3

2

1

0

-1

-50.0 0.2 0.4 0.6 1.0 1.2 1.4

X 107

Risk

(a)

Expecte

dD

ebt

Serv

ice

Cost

x10

5

FIGURE 3

WHOLE PORTFOLIOS FOR DOMESTIC DEBT (IN RS. MILLION)CASE 2:

-2

-3

-4

0.8

0.5 1.0 1.5 2.0 3.0 3.5 4.0

X 105

Risk

(b)

2.5 4.5

1.4

1.2

1.0

0.8

0.0

Expecte

dD

ebt

Servic

eC

ost

x10

5

0.6

0.4

0.2

1212121212 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

1

0

-1

-2

-50.0 0.2 0.4 0.6 1.0 1.2 1.4

X 107Risk

(a)

Expecte

dD

ebt

Serv

ice

Cost

x10

5

FIGURE 4

EFFICIENT FRONTIER AND BENCHMARK PORTFOLIO

FOR DOMESTIC DEBT (IN RS. MILLION)

CASE 2:

-3

-4

0.8

Risk

(b)

Optimal Portfolio

2.4 2.82.01.61.20.80.40.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

3.6

Expecte

dD

ebt

Serv

ice

Cost

x10

4

X 105

3.2 3.6

1313131313ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

SSSSSECTIONECTIONECTIONECTIONECTION IV IV IV IV IVEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR E E E E EXTERNALXTERNALXTERNALXTERNALXTERNAL G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

C. Benchmark Portfolios and Optimal Borrowing Strategies

Given the efficient frontier, the next step is to identify a benchmark (or optimal) portfolio fromthe feasible choice set. Given the feasible efficient portfolio set and exogenous risk targets, a portfoliothat minimizes deviations from the exogenous targets can be selected as the benchmark portfolio.That is, the benchmark portfolio is identified by minimizing a penalty function defined as a weightedaverage of deviations from the respective risk targets. An example of exogenous targets is the costat risk (CaR) of a portfolio. A simple penalty function is one that only considers CaR for the target.Thus, letting CaR (95%) be the 95% CaR from a portfolio, we have a penalty function: f =CaR (95%).7 The value of 95% CaR for a borrowing strategy or portfolio is the 95th percentilein the distribution of debt service costs from the strategy. In our simulation study, we obtainthe distribution for each borrowing strategy from a set of 1,000 iterations. A portfolio thathas the minimum value of CaR (95%) is selected as the benchmark portfolio. The circled onein Figure 2 is the benchmark portfolio for domestic debt in Case 1. The same analysis appliesto Case 2, and the benchmark portfolio is circled in Figure 4.

Optimal borrowing strategies for Case 1 and Case 2 are summarized in Table 5. For Case1, the optimal debt issuance mix is 40% 3-month treasury bills, 0% 1-year treasury bills, 0%3-year bonds, and 60% five-year bonds. For Case 2, the optimal debt issuance mix is 30%3-month treasury bills, 10% 1-year treasury bills, 0% 3-year bonds, 0% 5-year bonds, and60% 10-year bonds. These results imply that it would be better for the Nepali economy tochoose a portfolio with longer-term debts to reduce the debt service cost risk and to simplifythe issue profile of domestic bonds.

TABLE 5OPTIMAL BORROWING STRATEGIES FOR DOMESTIC GOVERNMENT DEBT

BOND MATURITY (PERCENT)

3-MONTH 1-YEAR 3-YEAR 5-YEAR 10-YEAR

Case 1 40 0 0 60 –Case 2 30 10 0 0 60

IV. EFFICIENT FRONTIER AND BENCHMARK PORTFOLIOFOR EXTERNAL GOVERNMENT DEBT

What financial instruments are available to manage external risks? An important one for hedgingis the currency mix of foreign debt. This is particularly true for developing countries. Many developingcountries lack access to futures and options markets to hedge the enormous risks arising from thecurrency exposure of their foreign debt. Even if these markets are accessible, the maturities areoften too short compared to the maturities of long-term debts. In this section, we study the optimalcurrency mix of Nepali external debt based on the approach used in the previous section.

7 Alternatively, as in Hahm and Kim (2003), we can add duration targets in an attempt to control medium-term marketrisks as well as liquidity risks. In this case, the penalty function is a weighted average of deviations from an exogenousduration target and CaR.

1414141414 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

8 We do not consider multicurrency loans here due to insufficiency of data. Examples are loans in Euro and Japaneseyen.

A. The Data: Basic Profiles of External Debt Portfolios in Nepal

Table 6 shows the basic profiles of the government external debt by currency as of 30September 2002. The borrowing currencies are Nepali rupee, Saudi riyal, Kuwaiti dinar, USdollar, and Special Drawing Rights.8

TABLE 6TOTAL LIABILITIES OF EXTERNAL DEBT OF NEPAL, 2002

AMOUNT IN EACH AMOUNT INCURRENCY NATIONAL CURRENCY NEPALI RUPEES PERCENT

Nepal rupees (NRs) 19,073,535 19,073,535 0.01Saudi riyals (SAR) 184,399,830 3,857,867,974 2.58Kuwaiti dinars (KWD) 14,550,000 3,766,995,000 2.52US dollars (USD) 293,062,000 22,992,046,000 15.37Special Drawing Rights (SDR) 1,148,450,000 118,933,482,000 79.52

Total 149,569,464,509 100.00

Note: Amounts in NRs are calculated using the exchange rates of 30 September 2002.

In this section, we use the same methodology as in the previous section to identify theefficient cost–risk trade-offs and optimal benchmark portfolios for external debt. Note, however,that this time we use the currency composition (instead of the maturity structure of the debtportfolio) as the decision variable. The analysis is conducted based upon the actual Nepaligovernment external debt data as of 30 September 2002. Suppose that we are at the endof period 4Q2002 (t=4Q2002). The plan period or debt management horizon is 10 years 1Q2003to 4Q2012 (N=40). The decision interval or time unit of the analysis is a quarter.

B. Derivation of Efficient Portfolio Set Conditionalupon Existing External Debt Structure

The efficient frontier set for external government debt as of the end of 4Q2012 is derivedas a summary of the expected cost–risk trade-off. The currencies available for borrowingare the Saudi riyal, Kuwaiti dinar, US dollar, and Special Drawing Rights. We assume that thepayments of principal and interest on all outstanding bonds are refinanced by borrowing inany of these four currencies. We also assume that the maturities of loans are all 40 years andthat interest payments are made semiannually.

The primary budget deficit under the basic scenario is shown in Table 7.

1515151515ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

TABLE 7FOREIGN FINANCING OF PRIMARY BUDGET DEFICIT UNDER BASIC SCENARIO

(IN NRS. MILLION)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

11,594 13,403 15,146 17,392 20,097 23,310 27,066 31,664 37,322 44,317

From the annual budget deficit series above, the forecast of quarterly primary budgetdeficits over the debt management horizon from 1Q2003 to 4Q2012 (N=40) is obtained bydividing the annual data by four. These quarterly primary budget deficit series are exogenous

variables and are denoted by { , , , }P P Pt t t+ + +1 2 40 .

The government is considering a combination of SAR, KWD, USD, and SDR loans tofinance the primary budget deficits and to rollover maturing debts given the existing debtportfolio at the end of period 4Q2002. A borrowing strategy is denoted by a composition ofloans in these four currencies represented as a vector of weights, w = ( , , , )w w w wSAR KWD USD SDR ,which sum to unity. wj is the weight of the j-th currency. We assume that each borrowingstrategy is time-invariant, implying that under the borrowing strategy, the same weights ofrespective currencies are maintained throughout the debt management horizon.

In the case of external debts, it would be desirable to conduct a full-blown simulationwith respect to yield curves, exchange rates, and sovereign risk premia for Nepali governmentdebt. Such multivariate simulations covering all those factors, however, are not feasible andextremely costly. Our simulation study focuses on the exchange rate since our objective is tofind the currency composition of liabilities that minimizes risk stemming from the variabilityin values of foreign liability debt service. For this purpose, we assume that there is no sovereignrisk premium and that the semiannual interest rate for each currency loan is 3%. Then, theeffective interest rate on the loan from the j-th country can be written as follows:

( ) ( )( )*1 1 4+ = + +i i

E e

etj

ttj

tj (5)

where jti is the interest rate on the j-th currency issued in period t; i* and

E e

etj

tj

( )+4 are,

respectively, the foreign interest rate and rate of depreciation of the domestic currency relativeto currency j.

Note that the existing government external debt portfolio at the end of period t issummarized as a vector

Zt t t t t t t tz z z z z z z= − − − −( , , , , , , , ,SAR SAR SAR KWD KWD KWD1 159 1 159

UUSD USD KWD SDR SDR SDR, , , , , , , )z z z z zt t t t t− − − −1 159 1 159

where zt ij− is the balance of j-th currency loans borrowed in period t-i; the number 159 indicates

SSSSSECTIONECTIONECTIONECTIONECTION IV IV IV IV IVEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR E E E E EXTERNALXTERNALXTERNALXTERNALXTERNAL G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

1616161616 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

the last quarter at the end of 40 years. As in the case of domestic debt, the elements in Ztare determined by the Nepali central government’s external debt portfolio as of July 2003.Now, for a given borrowing strategy w, the government’s total financing requirement for thenext year, Bt+1, can be represented as the sum of the primary budget deficit Pt+1 and therefinancing amount αYt+1, where α∈[0,1] is the fraction of refinancing and Yt+1 is the sum ofprincipal and interest to be paid in period t+1. In simulation, we assume that 50% of principalpayments and interest expenses are refinanced every quarter (α = 0.5).

B P Y

Y i zkj

kj

t t t

t t twhere

+ + +

+ + −==

+

= +

= +⎛⎝⎜

⎞⎠⎟∑∑

1 1 1

1 1 21

80

1

4

1180

α

−−2kj

where k runs through 80, the number of half-year periods in 40 years.

We assume that a constant fraction of the principal of maturing bonds as well as interest paymentson all existing bonds is refinanced every quarter, and the remaining fraction is repaid from thegovernment budget. The actual issuance amount in year t+1 is a function of the borrowing strategyw:

( , , , ) ( , , ,z z z z B w w w wt t t t t+ + + + +=1 1 1 1 1SAR KWD USD SDR

SAR KWD USD SDR)) (7)

Now, by the same logic, the total financing requirement for period t+2 and the actualissuance amount for each bond in period t+2 under the time-invariant borrowing strategy wcan be represented as follows:

B P Y

Y i z

t t t

t t kj

kjt

+ + +

+ + −==

+

= +

= +⎛⎝⎜

⎞⎠⎟∑∑

2 2 2

2 2 21

80

1

4

2180

α

where −−

+ + + + +=

2

1 1 1 1 2

kj

t t t t tz z z z B w w wand SAR KWD USD SDRSAR KWD( , , , ) ( , , UUSD SDR, )w

Note that we are at the end of period t, so that Bt+2 is a random variable as exchange

rates and effective interest rates in period t+1, ( , , , )i i i it t t t+ + + +1 1 1 1SAR KWD USD SDR , are not observed at t.

Note also that the actual amount of bond issuance in period t+2 is determined by the borrowingamount in period t+1. Hence, the issuance amount of each bond in any given period is a functionof the borrowing strategy itself as well as the actual exchange rates up to that period. Theprocess can be repeated until period t+N. A specific debt portfolio will emerge depending onthe path of exchange rates during the N periods and the given specific borrowing strategy.

For simulating out of sample exchange rates, we employ the bootstrap method based on quarterlyexchange rate data from 1Q1957 to 2Q2003. The idea behind bootstrapping is to obtain anestimate of the small sample distribution of parameters without assuming that the innovationterms are Gaussian. We use a vector autoregression of order one in our bootstrap procedure.A VAR(1) is estimated for each series of exchange rates; NRs/SAR, NRs/KWD, NRs/USD, andNRS/SDR. We take a random draw from the fitted residuals for the exchange rates NRs/SAR,

(8)

(6)

1717171717ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

NRs/KWD, NRs/USD, and NRs/SDR and use it to construct the first year innovation in an artificialsample. The draw is continued with replacement to obtain a full sample exchange rate seriesfor the next 10 years, i.e., 40 quarters. Given a series of simulated exchange rates, actualportfolio evolution is traced for a given specific borrowing strategy. The debt service cost iscalculated for the resulting portfolio at the end of 40 quarters, i.e., 4Q2012. Next, we generatea second set of draws from the fitted residuals and calculate another debt service cost forthe resulting portfolio for the same borrowing strategy. As in the case of government domesticdebt, a set of 1,000 iterations of such a simulation was undertaken for each borrowing strategy.The mean, standard deviation, and 95% CaR value are obtained from the distribution of the1,000 debt service costs for each borrowing strategy.

By conducting 1,000 iterations of the simulation for each of the borrowing strategies,we can represent all period-end portfolios in the space of the mean and standard deviation.In turn, we can identify the efficient portfolio set conditional upon the existing debt portfolio.The simulation results are summarized in Figure 5, which shows a clear negative trade-offbetween expected cost and risk. In Figure 6, we have an efficient portfolio frontier obtainedby selecting portfolios that yield the lowest expected costs at each level of the standard deviationin Figure 5.

C. Benchmark Portfolios and Optimal Borrowing Strategies

The benchmark portfolio for external debt is identified from the set of efficient portfolios basedon the same penalty function as in Section III. Therefore, an optimal benchmark portfolio is identifiedfrom the efficient set by minimizing the 95% CaR. The circled one in Figure 6 is the benchmarkportfolio for external debt. The optimal borrowing strategy is summarized in Table 8. The optimalcurrency composition is 10% SAR, 10% KWD, 80% USD, and 0% SDR.

TABLE 8OPTIMAL BORROWING STRATEGIES FOR EXTERNAL GOVERNMENT DEBT

CURRENCY SAR KWD USD SDR

Percent 10 10 80 0

Why do we have the above results of optimal borrowing mixes for foreign debt portfolio? Theabove result has much to do with the statistical characteristics of each currency, in particularthe mean cost and risks contained in each currency. In Table 9 below we report mean and

variability of ∆eet

t. Notice that

∆eet

t is main determinant of the cost of borrowing in our study

as expresed in the interest rate parity equation (5). We can see that USD dominates in bothmean and variance of the cost; SAR is better than KWD in the mean cost, but KWD is betterthan SAR in variability; and SDR is inferior to all the other three currencies in both meanand variance. The statistics in Table 9, therefore, are consistent with the chosen benchmarkportfolio in Table 8.

SSSSSECTIONECTIONECTIONECTIONECTION IV IV IV IV IVEEEEEFFICIENTFFICIENTFFICIENTFFICIENTFFICIENT F F F F FRONTIERRONTIERRONTIERRONTIERRONTIER ANDANDANDANDAND B B B B BENCHMARKENCHMARKENCHMARKENCHMARKENCHMARK P P P P PORTFOLIOORTFOLIOORTFOLIOORTFOLIOORTFOLIO

FORFORFORFORFOR E E E E EXTERNALXTERNALXTERNALXTERNALXTERNAL G G G G GOVERNMENTOVERNMENTOVERNMENTOVERNMENTOVERNMENT D D D D DEBTEBTEBTEBTEBT

1818181818 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

TABLE 9MEAN AND VARIABILITY OF

∆ee

EXCHANGE RATE (e) NRs/SAR NRs/KWD NRs/USD NRs/SDR

Mean of ∆ee

0.0296 0.0316 0.0294 0.0336

Variance of ∆ee

0.0042 0.0041 0.0037 0.0048

Standard Deviation of ∆ee

0.0647 0.0641 0.0611 0.0695

By the results summarized in Tables 8 and 9 we can conclude that it is desirable to have alarger portion of the currency whose exchange rate relative to the Nepali rupee has lower average

rate of change, ∆eet

t , and smaller variability of rate of change than the other currencies.

In the above study we are confined to the situation where the mean and volatility of the borrowingcost are the only factors considered in portfolio selection. In such a case the optimal portfolio isthe one that has the lowest mean cost and the smallest variance of the cost. If we have other factorssuch as the interest rates on loans, term structure of loans, and the sovereign risk premium in oursimulation, we can perform richer analysis.

2.370

2.365

2.360

2.3451.0

X 108Risk

(a)

Expecte

dD

ebt

Serv

ice

Cost

x10

10

FIGURE 5

WHOLE PORTFOLIOS FOR EXTERNAL DEBT

2.355

2.350

2.375

1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6

1919191919ERD ERD ERD ERD ERD TTTTTECHNICALECHNICALECHNICALECHNICALECHNICAL N N N N NOTEOTEOTEOTEOTE S S S S SERIESERIESERIESERIESERIES N N N N NOOOOO..... 1515151515

SSSSSECTIONECTIONECTIONECTIONECTION VVVVVCCCCCONCLUDINGONCLUDINGONCLUDINGONCLUDINGONCLUDING R R R R REMARKSEMARKSEMARKSEMARKSEMARKS

V. CONCLUDING REMARKS

We have studied the problem of debt management for the Nepali economy by applyingthe framework studied in Hahm and Kim (2003). Some important conclusions from the analysisof the Nepali debt data are drawn. The analysis of domestic debt suggests that the Nepalieconomy needs to move to longer-term domestic borrowing, and that the issue profile ofdomestic bonds of Nepal should be simplified. From the analysis of foreign debt we have foundthat it is desirable to have a larger portion of the currency whose exchange rate relative tothe Nepali rupee has a lower average rate of change and smaller variability of rate of changethan the other currencies.

The analytical approach used in the study can be easily applied for other countries toidentify their benchmark government debt portfolios. The empirical exercise for the Nepalidata is only an example. As is noted in the previous sections, the empirical analysis for theNepali data is constrained due to limited availability of data. A richer and more informativedata set has to be accumulated to analyze more interesting issues and perform detailed analysisof debt management in Nepal in the future.

2.3515

2.3505

2.3495

2.34751.0

X 108Risk

Expecte

dD

ebt

Serv

ice

Cost

x10

10

FIGURE 6

EFFICIENT FRONTIER AND BENCHMARK PORTFOLIO FOR EXTERNAL DEBT

2.3485

2.3525

1.2 1.4 1.6 1.8 2.0 2.2

Optimal Portfolio

2020202020 DDDDDECEMBERECEMBERECEMBERECEMBERECEMBER 20052005200520052005

DDDDDEBTEBTEBTEBTEBT M M M M MANAGEMENTANAGEMENTANAGEMENTANAGEMENTANAGEMENT AAAAANALNALNALNALNALYSISYSISYSISYSISYSIS

OFOFOFOFOF NNNNNEPEPEPEPEPALALALALAL’’’’’SSSSS P P P P PUBLICUBLICUBLICUBLICUBLIC D D D D DEBTEBTEBTEBTEBT

SSSSSUUUUUNGSUPNGSUPNGSUPNGSUPNGSUP R R R R RAAAAA,,,,, C C C C CHANGHANGHANGHANGHANG YYYYYONGONGONGONGONG R R R R RHEEHEEHEEHEEHEE,,,,, ANDANDANDANDAND J J J J JOONOONOONOONOON-H-H-H-H-HOOOOO H H H H HAHMAHMAHMAHMAHM

REFERENCES

Carracedo, M., and P. Dattels. 1997. “Survey of Public Debt Management Frameworks in Selected Countries.”In V. Sundararajan et al. eds., Coordinating Public Debt and Monetary Management. InternationalMonetary Fund, Washington, DC.

Cassard, M., and D. Folkerts-Landau. 1997. Risk Management of Sovereign Asset and Liability. IMF WorkingPaper WP/97/166, International Monetary Fund, Washington, DC

Claessens, S. 1992. “The Optimal Currency Composition of External Debt: Theory and Applications to Mexicoand Brazil.” The World Bank Economic Review 6(3, September).

Cohen, D. 1991. Private Lending to Sovereign States. Cambridge, MA: MIT Press.Eaton, J. 1992. Sovereign Debt: A Primer. World Bank Working Paper No. WPS 855, Washington, DC.Hahm, J., and J. Kim. 2003. “Cost-at-Risk and Benchmark Government Debt Portfolio in Korea.” International

Economic Journal 17(2):79-103.Missale, A. 1999. Public Debt Management. Oxford (London): Oxford University Press.World Bank. 1999. Second Sovereign Debt Management Forum: Compilation of Presentations. World Bank,

Washington, DC.

21

PUBLICATIONS FROM THEECONOMICS AND RESEARCH DEPARTMENT

No. 9 Setting User Charges for Public Services: Policiesand Practice at the Asian Development Bank—David Dole, December 2003

No. 10 Beyond Cost Recovery: Setting User Charges forFinancial, Economic, and Social Goals—David Dole and Ian Bartlett, January 2004

No. 11 Shadow Exchange Rates for Project EconomicAnalysis: Toward Improving Practice at the AsianDevelopment Bank—Anneli Lagman-Martin, February 2004

No. 12 Improving the Relevance and Feasibility ofAgriculture and Rural Development OperationalDesigns: How Economic Analyses Can Help—Richard Bolt, September 2005

No. 13 Assessing the Use of Project Distribution andPoverty Impact Analyses at the Asian DevelopmentBank—Franklin D. De Guzman, October 2005

No. 14 Assessing Aid for a Sector Development Plan:Economic Analysis of a Sector Loan—David Dole, November 2005

No. 15 Debt Management Analysis of Nepal’s Public Debt—Sungsup Ra, Changyong Rhee, and Joon-HoHahm, December 2005

ERD TECHNICAL NOTE SERIES (TNS)(Published in-house; Available through ADB Office of External Relations; Free of Charge)

No. 1 Contingency Calculations for EnvironmentalImpacts with Unknown Monetary Values—David Dole, February 2002

No. 2 Integrating Risk into ADB’s Economic Analysisof Projects—Nigel Rayner, Anneli Lagman-Martin,

and Keith Ward, June 2002No. 3 Measuring Willingness to Pay for Electricity

—Peter Choynowski, July 2002No. 4 Economic Issues in the Design and Analysis of a

Wastewater Treatment Project—David Dole, July 2002

No. 5 An Analysis and Case Study of the Role ofEnvironmental Economics at the AsianDevelopment Bank—David Dole and Piya Abeygunawardena,September 2002

No. 6 Economic Analysis of Health Projects: A Case Studyin Cambodia—Erik Bloom and Peter Choynowski, May 2003

No. 7 Strengthening the Economic Analysis of NaturalResource Management Projects—Keith Ward, September 2003

No. 8 Testing Savings Product Innovations Using anExperimental Methodology—Nava Ashraf, Dean S. Karlan, and Wesley Yin,November 2003

ERD POLICY BRIEF SERIES (PBS)(Published in-house; Available through ADB Office of External Relations; Free of charge)

No. 1 Is Growth Good Enough for the Poor?—Ernesto M. Pernia, October 2001

No. 2 India’s Economic ReformsWhat Has Been Accomplished?What Remains to Be Done?—Arvind Panagariya, November 2001

No. 3 Unequal Benefits of Growth in Viet Nam—Indu Bhushan, Erik Bloom, and Nguyen MinhThang, January 2002

No. 4 Is Volatility Built into Today’s World Economy?—J. Malcolm Dowling and J.P. Verbiest,February 2002

No. 5 What Else Besides Growth Matters to PovertyReduction? Philippines—Arsenio M. Balisacan and Ernesto M. Pernia,February 2002

No. 6 Achieving the Twin Objectives of Efficiency andEquity: Contracting Health Services in Cambodia—Indu Bhushan, Sheryl Keller, and Brad Schwartz,March 2002

No. 7 Causes of the 1997 Asian Financial Crisis: WhatCan an Early Warning System Model Tell Us?—Juzhong Zhuang and Malcolm Dowling,June 2002

No. 8 The Role of Preferential Trading Arrangementsin Asia—Christopher Edmonds and Jean-Pierre Verbiest,July 2002

No. 9 The Doha Round: A Development Perspective—Jean-Pierre Verbiest, Jeffrey Liang, and LeaSumulong, July 2002

No. 10 Is Economic Openness Good for RegionalDevelopment and Poverty Reduction? ThePhilippines—E. M. Pernia and Pilipinas Quising, October2002

No. 11 Implications of a US Dollar Depreciation for AsianDeveloping Countries—Emma Fan, July 2002

No. 12 Dangers of Deflation—D. Brooks and Pilipinas Quising, December 2002

No. 13 Infrastructure and Poverty Reduction—What is the Connection?—Ifzal Ali and Ernesto Pernia, January 2003

No. 14 Infrastructure and Poverty Reduction—Making Markets Work for the Poor—Xianbin Yao, May 2003

No. 15 SARS: Economic Impacts and Implications—Emma Xiaoqin Fan, May 2003

No. 16 Emerging Tax Issues: Implications of Globalizationand Technology—Kanokpan Lao Araya, May 2003

No. 17 Pro-Poor Growth: What is It and Why is ItImportant?—Ernesto M. Pernia, May 2003

22

No. 1 Capitalizing on Globalization—Barry Eichengreen, January 2002

No. 2 Policy-based Lending and Poverty Reduction:An Overview of Processes, Assessmentand Options—Richard Bolt and Manabu Fujimura, January2002

No. 3 The Automotive Supply Chain: Global Trendsand Asian Perspectives—Francisco Veloso and Rajiv Kumar, January 2002

No. 4 International Competitiveness of Asian Firms:An Analytical Framework—Rajiv Kumar and Doren Chadee, February 2002

No. 5 The International Competitiveness of AsianEconomies in the Apparel Commodity Chain—Gary Gereffi, February 2002

No. 6 Monetary and Financial Cooperation in EastAsia—The Chiang Mai Initiative and Beyond—Pradumna B. Rana, February 2002

No. 7 Probing Beneath Cross-national Averages: Poverty,Inequality, and Growth in the Philippines—Arsenio M. Balisacan and Ernesto M. Pernia,March 2002

No. 8 Poverty, Growth, and Inequality in Thailand—Anil B. Deolalikar, April 2002

No. 9 Microfinance in Northeast Thailand: Who Benefitsand How Much?—Brett E. Coleman, April 2002

No. 10 Poverty Reduction and the Role of Institutions in

Developing Asia—Anil B. Deolalikar, Alex B. Brilliantes, Jr.,Raghav Gaiha, Ernesto M. Pernia, Mary Raceliswith the assistance of Marita Concepcion Castro-Guevara, Liza L. Lim, Pilipinas F. Quising, May2002

No. 11 The European Social Model: Lessons forDeveloping Countries—Assar Lindbeck, May 2002

No. 12 Costs and Benefits of a Common Currency forASEAN—Srinivasa Madhur, May 2002

No. 13 Monetary Cooperation in East Asia: A Survey—Raul Fabella, May 2002

No. 14 Toward A Political Economy Approachto Policy-based Lending—George Abonyi, May 2002

No. 15 A Framework for Establishing Priorities in aCountry Poverty Reduction Strategy—Ron Duncan and Steve Pollard, June 2002

No. 16 The Role of Infrastructure in Land-use Dynamicsand Rice Production in Viet Nam’s Mekong RiverDelta—Christopher Edmonds, July 2002

No. 17 Effect of Decentralization Strategy onMacroeconomic Stability in Thailand—Kanokpan Lao-Araya, August 2002

No. 18 Poverty and Patterns of Growth—Rana Hasan and M. G. Quibria, August 2002

ERD WORKING PAPER SERIES (WPS)(Published in-house; Available through ADB Office of External Relations; Free of Charge)

No. 18 Public–Private Partnership for Competitiveness—Jesus Felipe, June 2003

No. 19 Reviving Asian Economic Growth Requires FurtherReforms—Ifzal Ali, June 2003

No. 20 The Millennium Development Goals and Poverty:Are We Counting the World’s Poor Right?—M. G. Quibria, July 2003

No. 21 Trade and Poverty: What are the Connections?—Douglas H. Brooks, July 2003

No. 22 Adapting Education to the Global Economy—Olivier Dupriez, September 2003

No. 23 Avian Flu: An Economic Assessment for SelectedDeveloping Countries in Asia—Jean-Pierre Verbiest and Charissa Castillo,March 2004

No. 25 Purchasing Power Parities and the InternationalComparison Program in a Globalized World—Bishnu Pant, March 2004

No. 26 A Note on Dual/Multiple Exchange Rates—Emma Xiaoqin Fan, May 2004

No. 27 Inclusive Growth for Sustainable Poverty Reductionin Developing Asia: The Enabling Role ofInfrastructure Development—Ifzal Ali and Xianbin Yao, May 2004

No. 28 Higher Oil Prices: Asian Perspectives andImplications for 2004-2005—Cyn-Young Park, June 2004

No. 29 Accelerating Agriculture and Rural Development forInclusive Growth: Policy Implications forDeveloping Asia—Richard Bolt, July 2004

No. 30 Living with Higher Interest Rates: Is Asia Ready?—Cyn-Young Park, August 2004

No. 31 Reserve Accumulation, Sterilization, and PolicyDilemma—Akiko Terada-Hagiwara, October 2004

No. 32 The Primacy of Reforms in the Emergence ofPeople’s Republic of China and India

—Ifzal Ali and Emma Xiaoqin Fan, November2004

No. 33 Population Health and Foreign Direct Investment:Does Poor Health Signal Poor GovernmentEffectiveness?—Ajay Tandon, January 2005

No. 34 Financing Infrastructure Development: AsianDeveloping Countries Need to Tap Bond MarketsMore Rigorously—Yun-Hwan Kim, February 2005

No. 35 Attaining Millennium Development Goals inHealth: Isn’t Economic Growth Enough?—Ajay Tandon, March 2005

No. 36 Instilling Credit Culture in State-owned Banks—Experience from Lao PDR—Robert Boumphrey, Paul Dickie, and SamiuelaTukuafu, April 2005

No. 37 Coping with Global Imbalances and AsianCurrencies—Cyn-Young Park, May 2005

No. 38 Asia’s Long-term Growth and Integration:Reaching beyond Trade Policy Barriers—Douglas H. Brooks, David Roland-Holst, and FanZhai, September 2005

No. 39 Competition Policy and Development—Douglas H. Brooks, October 2005

No. 40 Highlighting Poverty as Vulnerability: The 2005Earthquake in Pakistan—Rana Hasan and Ajay Tandon, October 2005

No. 41 Conceptualizing and Measuring Poverty asVulnerability: Does It Make a Difference?—Ajay Tandon and Rana Hasan, October 2005

No. 42 Potential Economic Impact of an Avian FluPandemic on Asia—Erik Bloom, Vincent de Wit, and Mary JaneCarangal-San Jose, November 2005

No. 43 Creating Better and More Jobs in Indonesia: ABlueprint for Policy Action—Guntur Sugiyarto, December 2005

23

No. 19 Why are Some Countries Richer than Others?A Reassessment of Mankiw-Romer-Weil’s Test ofthe Neoclassical Growth Model—Jesus Felipe and John McCombie, August 2002

No. 20 Modernization and Son Preference in People’sRepublic of China—Robin Burgess and Juzhong Zhuang, September2002

No. 21 The Doha Agenda and Development: A View fromthe Uruguay Round—J. Michael Finger, September 2002

No. 22 Conceptual Issues in the Role of EducationDecentralization in Promoting Effective Schooling inAsian Developing Countries—Jere R. Behrman, Anil B. Deolalikar, and Lee-Ying Son, September 2002

No. 23 Promoting Effective Schooling through EducationDecentralization in Bangladesh, Indonesia, andPhilippines—Jere R. Behrman, Anil B. Deolalikar, and Lee-Ying Son, September 2002

No. 24 Financial Opening under the WTO Agreement inSelected Asian Countries: Progress and Issues—Yun-Hwan Kim, September 2002

No. 25 Revisiting Growth and Poverty Reduction inIndonesia: What Do Subnational Data Show?—Arsenio M. Balisacan, Ernesto M. Pernia, and Abuzar Asra, October 2002

No. 26 Causes of the 1997 Asian Financial Crisis: WhatCan an Early Warning System Model Tell Us?—Juzhong Zhuang and J. Malcolm Dowling,October 2002

No. 27 Digital Divide: Determinants and Policies withSpecial Reference to Asia—M. G. Quibria, Shamsun N. Ahmed, TedTschang, and Mari-Len Reyes-Macasaquit, October2002

No. 28 Regional Cooperation in Asia: Long-term Progress,Recent Retrogression, and the Way Forward—Ramgopal Agarwala and Brahm Prakash,October 2002

No. 29 How can Cambodia, Lao PDR, Myanmar, and VietNam Cope with Revenue Lost Due to AFTA TariffReductions?—Kanokpan Lao-Araya, November 2002

No. 30 Asian Regionalism and Its Effects on Trade in the1980s and 1990s—Ramon Clarete, Christopher Edmonds, andJessica Seddon Wallack, November 2002

No. 31 New Economy and the Effects of IndustrialStructures on International Equity MarketCorrelations—Cyn-Young Park and Jaejoon Woo, December2002

No. 32 Leading Indicators of Business Cycles in Malaysiaand the Philippines—Wenda Zhang and Juzhong Zhuang, December2002

No. 33 Technological Spillovers from Foreign DirectInvestment—A Survey—Emma Xiaoqin Fan, December 2002

No. 34 Economic Openness and Regional Development inthe Philippines—Ernesto M. Pernia and Pilipinas F. Quising,January 2003

No. 35 Bond Market Development in East Asia:Issues and Challenges—Raul Fabella and Srinivasa Madhur, January2003

No. 36 Environment Statistics in Central Asia: Progressand Prospects—Robert Ballance and Bishnu D. Pant, March2003

No. 37 Electricity Demand in the People’s Republic of

China: Investment Requirement andEnvironmental Impact—Bo Q. Lin, March 2003

No. 38 Foreign Direct Investment in Developing Asia:Trends, Effects, and Likely Issues for theForthcoming WTO Negotiations—Douglas H. Brooks, Emma Xiaoqin Fan,and Lea R. Sumulong, April 2003

No. 39 The Political Economy of Good Governance forPoverty Alleviation Policies—Narayan Lakshman, April 2003

No. 40 The Puzzle of Social CapitalA Critical Review—M. G. Quibria, May 2003

No. 41 Industrial Structure, Technical Change, and theRole of Government in Development of theElectronics and Information Industry inTaipei,China—Yeo Lin, May 2003

No. 42 Economic Growth and Poverty Reductionin Viet Nam—Arsenio M. Balisacan, Ernesto M. Pernia, andGemma Esther B. Estrada, June 2003

No. 43 Why Has Income Inequality in ThailandIncreased? An Analysis Using 1975-1998 Surveys—Taizo Motonishi, June 2003

No. 44 Welfare Impacts of Electricity Generation SectorReform in the Philippines—Natsuko Toba, June 2003

No. 45 A Review of Commitment Savings Products inDeveloping Countries—Nava Ashraf, Nathalie Gons, Dean S. Karlan,and Wesley Yin, July 2003

No. 46 Local Government Finance, Private Resources,and Local Credit Markets in Asia—Roberto de Vera and Yun-Hwan Kim, October2003

No. 47 Excess Investment and Efficiency Loss DuringReforms: The Case of Provincial-level Fixed-AssetInvestment in People’s Republic of China—Duo Qin and Haiyan Song, October 2003

No. 48 Is Export-led Growth Passe? Implications forDeveloping Asia—Jesus Felipe, December 2003

No. 49 Changing Bank Lending Behavior and CorporateFinancing in Asia—Some Research Issues—Emma Xiaoqin Fan and Akiko Terada-Hagiwara,December 2003

No. 50 Is People’s Republic of China’s Rising ServicesSector Leading to Cost Disease?—Duo Qin, March 2004

No. 51 Poverty Estimates in India: Some Key Issues—Savita Sharma, May 2004

No. 52 Restructuring and Regulatory Reform in the PowerSector: Review of Experience and Issues—Peter Choynowski, May 2004

No. 53 Competitiveness, Income Distribution, and Growthin the Philippines: What Does the Long-runEvidence Show?—Jesus Felipe and Grace C. Sipin, June 2004

No. 54 Practices of Poverty Measurement and PovertyProfile of Bangladesh—Faizuddin Ahmed, August 2004

No. 55 Experience of Asian Asset ManagementCompanies: Do They Increase Moral Hazard?—Evidence from Thailand—Akiko Terada-Hagiwara and Gloria Pasadilla,September 2004

No. 56 Viet Nam: Foreign Direct Investment andPostcrisis Regional Integration—Vittorio Leproux and Douglas H. Brooks,September 2004

No. 57 Practices of Poverty Measurement and PovertyProfile of Nepal

24

1. Improving Domestic Resource Mobilization ThroughFinancial Development: Overview September 1985

2. Improving Domestic Resource Mobilization ThroughFinancial Development: Bangladesh July 1986

3. Improving Domestic Resource Mobilization ThroughFinancial Development: Sri Lanka April 1987

4. Improving Domestic Resource Mobilization ThroughFinancial Development: India December 1987

5. Financing Public Sector Development Expenditurein Selected Countries: Overview January 1988

6. Study of Selected Industries: A Brief ReportApril 1988

7. Financing Public Sector Development Expenditurein Selected Countries: Bangladesh June 1988

8. Financing Public Sector Development Expenditurein Selected Countries: India June 1988

9. Financing Public Sector Development Expenditurein Selected Countries: Indonesia June 1988

10. Financing Public Sector Development Expenditurein Selected Countries: Nepal June 1988

11. Financing Public Sector Development Expenditurein Selected Countries: Pakistan June 1988

12. Financing Public Sector Development Expenditurein Selected Countries: Philippines June 1988

13. Financing Public Sector Development Expenditurein Selected Countries: Thailand June 1988

14. Towards Regional Cooperation in South Asia:ADB/EWC Symposium on Regional Cooperationin South Asia February 1988

15. Evaluating Rice Market Intervention Policies:Some Asian Examples April 1988

16. Improving Domestic Resource Mobilization ThroughFinancial Development: Nepal November 1988

17. Foreign Trade Barriers and Export Growth September1988

18. The Role of Small and Medium-Scale Industries in theIndustrial Development of the Philippines April 1989

19. The Role of Small and Medium-Scale ManufacturingIndustries in Industrial Development: The Experience ofSelected Asian Countries January 1990

20. National Accounts of Vanuatu, 1983-1987 January1990

21. National Accounts of Western Samoa, 1984-1986February 1990

22. Human Resource Policy and Economic Development:Selected Country Studies July 1990

23. Export Finance: Some Asian Examples September 199024. National Accounts of the Cook Islands, 1982-1986

September 199025. Framework for the Economic and Financial Appraisal of

Urban Development Sector Projects January 199426. Framework and Criteria for the Appraisal and

Socioeconomic Justification of Education ProjectsJanuary 1994

27. Investing in Asia 1997 (Co-published with OECD)28. The Future of Asia in the World Economy 1998 (Co-

published with OECD)29. Financial Liberalisation in Asia: Analysis and Prospects

1999 (Co-published with OECD)30. Sustainable Recovery in Asia: Mobilizing Resources for

Development 2000 (Co-published with OECD)31. Technology and Poverty Reduction in Asia and the Pacific

2001 (Co-published with OECD)32. Asia and Europe 2002 (Co-published with OECD)33. Economic Analysis: Retrospective 200334. Economic Analysis: Retrospective: 2003 Update 200435. Development Indicators Reference Manual: Concepts and

Definitions 2004

SPECIAL STUDIES, COMPLIMENTARY(Available through ADB Office of External Relations)

—Devendra Chhetry, September 2004No. 58 Monetary Poverty Estimates in Sri Lanka:

Selected Issues—Neranjana Gunetilleke and DinushkaSenanayake, October 2004

No. 59 Labor Market Distortions, Rural-Urban Inequality,and the Opening of People’s Republic of China’sEconomy—Thomas Hertel and Fan Zhai, November 2004

No. 60 Measuring Competitiveness in the World’s SmallestEconomies: Introducing the SSMECI—Ganeshan Wignaraja and David Joiner, November2004

No. 61 Foreign Exchange Reserves, Exchange RateRegimes, and Monetary Policy: Issues in Asia—Akiko Terada-Hagiwara, January 2005

No. 62 A Small Macroeconometric Model of the PhilippineEconomy—Geoffrey Ducanes, Marie Anne Cagas, Duo Qin,Pilipinas Quising, and Nedelyn Magtibay-Ramos,January 2005

No. 63 Developing the Market for Local Currency Bondsby Foreign Issuers: Lessons from Asia—Tobias Hoschka, February 2005

No. 64 Empirical Assessment of Sustainability andFeasibility of Government Debt: The PhilippinesCase—Duo Qin, Marie Anne Cagas, Geoffrey Ducanes,Nedelyn Magtibay-Ramos, and Pilipinas Quising,February 2005

No. 65 Poverty and Foreign AidEvidence from Cross-Country Data—Abuzar Asra, Gemma Estrada, Yangseom Kim,and M. G. Quibria, March 2005

No. 66 Measuring Efficiency of Macro Systems: AnApplication to Millennium Development GoalAttainment—Ajay Tandon, March 2005

No. 67 Banks and Corporate Debt Market Development—Paul Dickie and Emma Xiaoqin Fan, April 2005

No. 68 Local Currency Financing—The Next Frontier forMDBs?—Tobias C. Hoschka, April 2005

No. 69 Export or Domestic-Led Growth in Asia?—Jesus Felipe and Joseph Lim, May 2005

No. 70 Policy Reform in Viet Nam and the AsianDevelopment Bank’s State-owned EnterpriseReform and Corporate Governance Program Loan—George Abonyi, August 2005

No. 71 Policy Reform in Thailand and the Asian Develop-ment Bank’s Agricultural Sector Program Loan—George Abonyi, September 2005

No. 72 Can the Poor Benefit from the Doha Agenda? TheCase of Indonesia—Douglas H. Brooks and Guntur Sugiyarto,October 2005

No. 73 Impacts of the Doha Development Agenda onPeople’s Republic of China: The Role ofComplementary Education Reforms—Fan Zhai and Thomas Hertel, October 2005

No. 74 Growth and Trade Horizons for Asia: Long-termForecasts for Regional Integration—David Roland-Holst, Jean-Pierre Verbiest, andFan Zhai, November 2005

No. 75 Macroeconomic Impact of HIV/AIDS in the Asianand Pacific Region—Ajay Tandon, November 2005

25

OLD MONOGRAPH SERIES(Available through ADB Office of External Relations; Free of charge)

EDRC REPORT SERIES (ER)

No. 1 ASEAN and the Asian Development Bank—Seiji Naya, April 1982

No. 2 Development Issues for the Developing Eastand Southeast Asian Countriesand International Cooperation—Seiji Naya and Graham Abbott, April 1982

No. 3 Aid, Savings, and Growth in the Asian Region—J. Malcolm Dowling and Ulrich Hiemenz,

April 1982No. 4 Development-oriented Foreign Investment

and the Role of ADB—Kiyoshi Kojima, April 1982

No. 5 The Multilateral Development Banksand the International Economy’s MissingPublic Sector—John Lewis, June 1982

No. 6 Notes on External Debt of DMCs—Evelyn Go, July 1982

No. 7 Grant Element in Bank Loans—Dal Hyun Kim, July 1982

No. 8 Shadow Exchange Rates and StandardConversion Factors in Project Evaluation—Peter Warr, September 1982

No. 9 Small and Medium-Scale ManufacturingEstablishments in ASEAN Countries:Perspectives and Policy Issues—Mathias Bruch and Ulrich Hiemenz, January1983

No. 10 A Note on the Third Ministerial Meeting of GATT—Jungsoo Lee, January 1983

No. 11 Macroeconomic Forecasts for the Republicof China, Hong Kong, and Republic of Korea—J.M. Dowling, January 1983

No. 12 ASEAN: Economic Situation and Prospects—Seiji Naya, March 1983

No. 13 The Future Prospects for the DevelopingCountries of Asia—Seiji Naya, March 1983