Embed Size (px)

Citation preview

Debt Sustainability

in Japan

Jun Saito

Cabinet Office, Japan

December 9th, 2011

at

Asia Europe Economic Forum Conference

Seoul, Korea

How debt accumulated in Japan (1)

• Public Finance Law of 1947

– It only allows “construction bonds.” But not even construction bonds had been issued before 1965.

• “ Structural Recession ” in 1965• “ Structural Recession ” in 1965

– Since 1966, construction bonds became a essential source of revenue.

• First Oil Crisis in 1973

– Global recession required a locomotive. Since 1975, deficit-financing bonds began to be issued.

2

How debt accumulated in Japan (2)

• Burst of the “Bubble Economy” in early 1990s

– Series of economic stimulus packages was introduced, without much apparent impact.

– Decline in population and its aging started to exert pressure on social security expenditure.pressure on social security expenditure.

• Subprime Recession and Lehman Shock in late 2000s

– Another series of economic stimulus packages was introduced.

• Great East Japan Earthquake in 2011

– Spending is to be increase in the “concentrated reconstruction period” (5years).

3

Outstanding Stock of

Central Government Bonds

100.0

120.0

140.0

160.0

(percent of GDP)

Deficit-financing Bonds

0.0

20.0

40.0

60.0

80.0

100.0

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Fiscal Years

Construction Bonds

4

What is the appropriate

fiscal indicator?• Not general account of the central government

– There are special accounts, and local governments.

• Not general government

– Social security funds are managed as a modified pay-as-you go system.

– It was in surplus until 1997, when it shifted to deficit.

• Not net-government debt• Not net-government debt

– Assets accumulated by social security funds are for future benefit payments.

– Foreign reserves are accumulated by issuing short-term government debt.

– Non-financial assets may not be sellable or be hard to evaluate.

↓

• Our choice: central and local government long-term debt

5

Central and Local Government

Long-Term Debt

120.0

140.0

160.0

180.0

200.0

(percent of GDP)

Central government

0.0

20.0

40.0

60.0

80.0

100.0

120.0

1980 1985 1990 1995 2000 2005

Fiscal Years

Central government

Local governments

Source: Cabinet Office

6

Fiscal situation deteriorating

• Government debt to GDP ratio has risen

• Fiscal balance relative to GDP has widen again,

and may worsen further

– Since 1990s, both– Since 1990s, both

• (a)primary balance, and

• (b)interest rate-GDP growth rate difference

has contributed in the deterioration

7

Fiscal Balance of

Central and Local Governments

(Financial Balance)

0.0

2.0

4.0

(percent of

GDP)

Central government

(Primary Balance)

0.0

2.0

4.0

(percent of

GDP)

Local governments

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

1980 1985 1990 1995 2000 2005

Fiscal Year

Local governments

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

1980 1985 1990 1995 2000 2005Fiscal Year

Central

government

Source: Cabinet Office8

Changes in government debt to GDP ratio

0.0

4.0

8.0

12.0

16.0

(percent of GDP)

Primary balance

Nominal GDP growth rate

-20.0

-16.0

-12.0

-8.0

-4.0

0.0

1980 85 90 95 2000 05 09Fiscal Years

Nominal interest rate (effective)Other factors

Source: Cabinet Office 9

Tax revenues have been falling (in spite of introduction

and hike in consumption tax)- Long-term GDP elasticity is around unity

- Tax cuts had been popular

20.0

25.0

(percent of GDP)

Tax on consumption

Tax on capital

Breakdown of Government Tax Revenues

0.0

5.0

10.0

15.0

1980 1985 1990 1995 2000 2005

Fiscal years

Taxes on income, wealth, etc

Taxes on products and imports

10

Government Expenditures is on a rising trend- Public investment and other discretionary expenditures have been curtailed

- Strong upward pressure coming from social security expenditures,

particularly from “transfers to social security funds”

25.0

30.0

%, GDP

Transfers to Social Security Funds

Breakdown of government expenditures

0.0

5.0

10.0

15.0

20.0

1980 1985 1990 1995 2000 2005

Fiscal Year

Other expenditures

Public investment

Social assistance payments

11

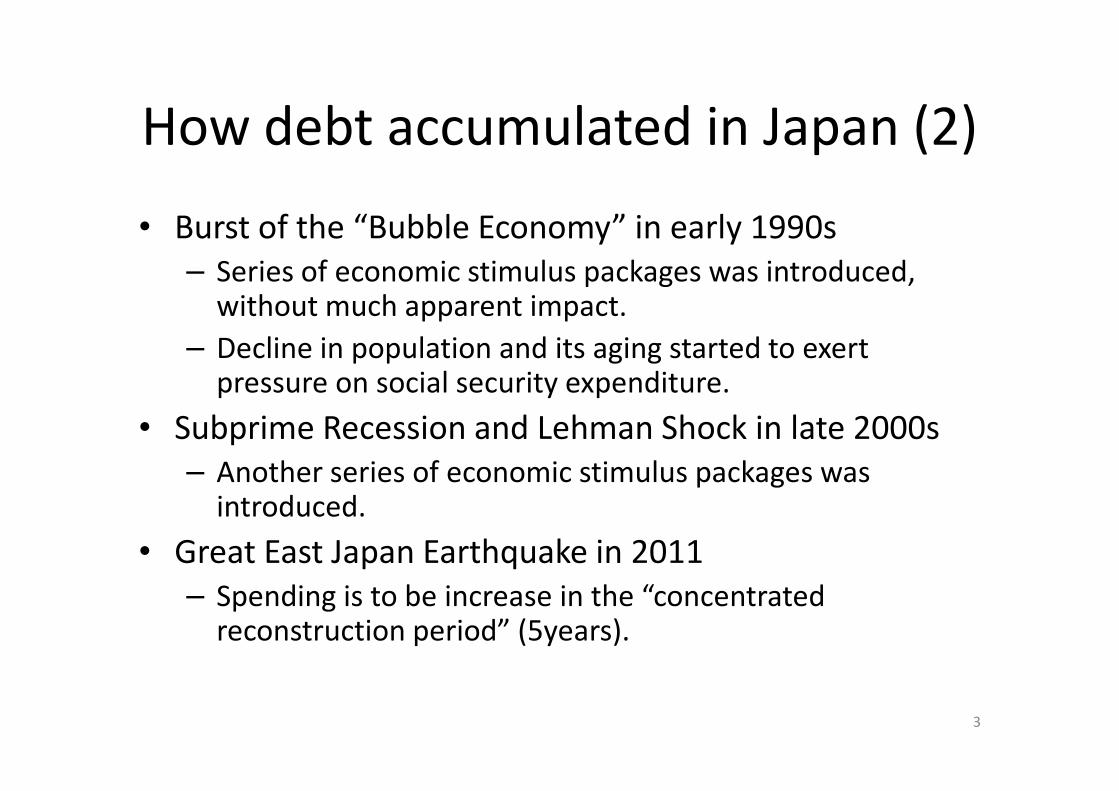

Aging of the population rapidly increased benefits paid

by the social security funds- premiums paid fall short of benefit payments

- transfers from the government is increasing, but is still not enough

- gap filled by running down assets

16.0

18.0

20.0

(Percent of GDP)

Social security benefits paid by

the social security funds

Balance of Social Security Funds

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1980 1985 1990 1995 2000 2005

Fiscal Years

Insurance premiums paid to the funds

Government transfers to the funds

the social security funds

12

Effective interest rate and GDP growth rate - Effective interest rates lag behind long-term interest rate.

- Effective rate also exceeds Nominal GDP Growth Rate.

4.0

6.0

8.0

10.0

(percent)

Long-term interest rate (10 year bonds)

Effective Interest Rate

(for local governments)

Interest Rates and Nominal GDP Growth Rate

-6.0

-4.0

-2.0

0.0

2.0

1981 1986 1991 1996 2001 2006

Fiscal Years

Effective Interest Rate

( for central government)

Nominal GDP Growth Rate

Source: Cabinet Office, and Bank of Japan.

13

Is Japanese fiscal situation

sustainable?

• Formal tests report that sustainability has been

lost since late 1990s.

• Medium-term simulations show that without

policy action debt to GDP ratio continues to rise.policy action debt to GDP ratio continues to rise.

• Generational accounting exercises show that

significant burden has been left for the future

generation to bear.

• Primary balance has not reacted positively to the

increase in government debt (Bohn’s condition).

14

PB GDP Ratio and Debt GDP ratio

(Bohn’s condition)

0.0

1.0

2.0

3.0

4.0

Primary Balance

(percent of GDP)

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

0.0 20.0 40.0 60.0 80.0 100.0 120.0 140.0 160.0 180.0 200.0

Government Debt

(percent of GDP)

1980

2009

15

Why is long-term interest rate so low?

• Is it that “dog didn’t bark” because they were irrational? Don’t think so.

• Japanese long-term interest rate is higher than what can be explained by (a) short-term interest rate, (b) real GDP growth rate, and (c) Inflation rate. real GDP growth rate, and (c) Inflation rate.

• Part of the gap can be explained by financial deficit. It means that fiscal risk premium is already incorporated.

• On the other hand, fiscal risk premium seems to be smaller in countries with current account surplus.

• For a high debt country, current account surplus helps.

16

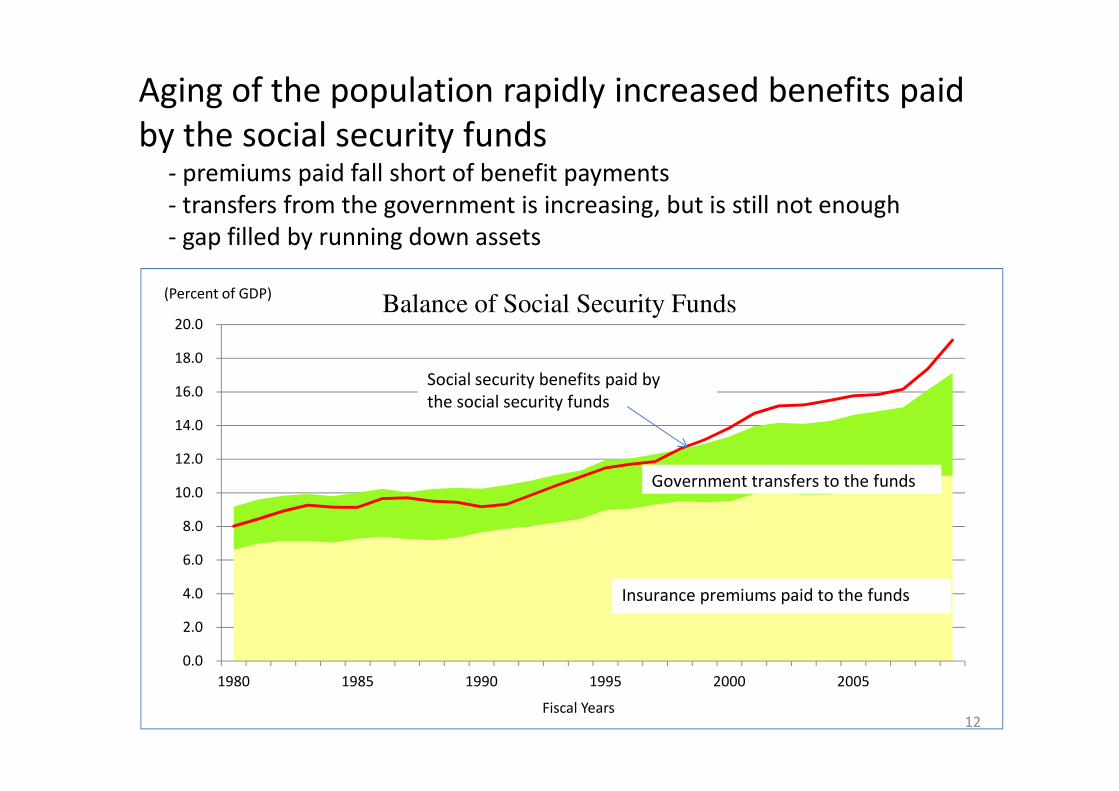

Measures for fiscal consolidation (1)

• Raising the growth rate

– Important, but tax revenue to GDP ratio do not

necessarily improve. GDP elasticity of tax revenue

in the long-term is about unity.in the long-term is about unity.

– Pension benefit and prices set for medical and

long-term care services partly reflects wage

increase and inflation. Thus, growth may also lead

to increase in government expenditure without a

reform on the social security system.

17

Measures for fiscal consolidation (2)

• Cutting expenditures– Cut in discretionary expenditures can be a source of

savings.

– Cut in mandatory expenditures more important, especially social security expenditures.especially social security expenditures.

• Pension system has already built-in adjustment mechanism; “price-slide” and “macroeconomic slide.” Problem is that deflation has prevented them from being activated.

• Medical and long-term care system still do not have such adjustment mechanisms.

– Social Security Reform is urgently needed.

18

Measures for fiscal consolidation (3)

• Raising tax– Income tax: since there is no social security number,

burden tend to fall on wage earners, rather than self-employed.

– Corporate Tax: already high by international standards. It will be reduced rather than raised.

– Corporate Tax: already high by international standards. It will be reduced rather than raised.

↓

– Raising consumption tax is the natural choice: • Current rate is low (at 5 percent).

• It raises stable revenue.

• It is also less distortional.

• Burden is shared by aged generation as well.

19

Current program in place (1)

• Central and local government is required;

– (a) to halve the primary deficit that existed in

FY2010 by FY2015, and achieve surplus by FY2020

– (b) to achieve decline in government debt to GDP – (b) to achieve decline in government debt to GDP

ratio after FY2020.

• Central government is also required to achieve

a target similar to that of (a).

20

Current program in place (2)

• Government is committed to raise the consumption tax rate in stages to 10 percent by mid-2010s. Tax revenue will be used for social security purposes.

• The schedule for the consumption tax rate • The schedule for the consumption tax rate increase will be made more concrete by the end of this year. The necessary legislation will be proposed to the Diet by the end of FY2011.

• The fiscal impact of the Great East Japan Earthquake will be designed so that it will not add to the burden of the future generation.

21

Current program in place (3)

• Raising consumption tax to 10 percent by mid-

2010s is expected to be enough to halve the

primary deficit that existed in FY2010.

• However, it is expected to be less than • However, it is expected to be less than

necessary to achieve surplus by FY2020.

• Debt to GDP ratio also will not decline.

• Further fiscal consolidation efforts are

necessary.

22

Further issues for consideration (1)

• First, timing and pace of fiscal consolidation

needs to be well designed.

– Must avoid tightening of fiscal stance when the

economic condition is too fragile.economic condition is too fragile.

– Conditions for implementation has to be well

defined and, in preparation for an emergency,

some kind of an escape clause needs to be fixed.

23

Further issues for consideration (2)

• Second, simultaneous fiscal consolidation by

major economies could bring about worsening

of the global economy.

– In turn, it would create a difficult environment for – In turn, it would create a difficult environment for

fiscal consolidation.

– Need for a well coordinated action by the

international community.

24

Issues for further consideration (3)

• Finally, the impatience of the market needs to

be taken into account.

– While current account surplus may be helpful,

quick shift in market sentiment could affect quick shift in market sentiment could affect

domestic investors.

– Forced action at an unfavorable economic

condition could be devastating.

– Confirm the need for a solid, credible, medium-

term fiscal consolidation program.

25

Thank you for listening

Jun Saito

Cabinet Office

Japan

26