Embed Size (px)

Citation preview

Florida & Metro Forecast2014-2017

I n s t i t u t e f o r E c o n o m i c C o m p e t i t i v e n e s s

C o l l e g e o f B u s i n e s s A d m i n i s t r a t i o n

U n i v e r s i t y o f C e n t r a l F l o r i d a

P u b l i s h e d D e c e m b e r 2 0 1 4

A B O U T U N I V E R S I T Y O F C E N T R A L F L O R I D A ( U C F )

A B O U T T H E C O L L E G E O F B U S I N E S S A D M I N I S T R AT I O N

2014 - 2017

D e c e m b e r 2 0 1 4 R e p o r t

I n s t i t u t e f o r E c o n o m i c C o m p e t i t i v e n e s s

C o l l e g e o f B u s i n e s s A d m i n i s t r a t i o n

U n i v e r s i t y o f C e n t r a l F l o r i d a

FLORIDA FORECAST

Published quarterly by the Institute for Economic Competitiveness, College of Business Administration, University of Central Florida

Copyright © 2014 Institute for Economic Competitiveness. All rights reserved.

This forecast was prepared based upon assumptions reflecting the Institute for Economic Competitiveness’ judgments as of the date it bears. Actual results could vary materially from the forecast. Neither the Institute for Economic Competitiveness nor the University of Central Florida shall be held responsible as a consequence of any such variance. Unless approved by the Institute for Economic Competitiveness, the publication or distribution of this forecast and the preparation, publication or distribution of any excerpts from this forecast are prohibited.

Publications of the Institute for Economic Competitiveness are made possible by the following staff:

Dr. Sean Snaith, DirectorAngela Ayala, Administrative AssistantJonathan Fagbohungbe, ResearcherAshley Miller, ResearcherTrevi Sellers, Researcher

TA

BL

E O

F C

ON

TE

NT

S

TABLE OF CONTENTS

Florida Highlights and Summary ....................... 5-12

Florida Forecast Tables ..................................... 13-18

Florida Forecast Charts ..................................... 19-27

Florida News Summaries ...................................... 28

Deltona-Daytona Beach-Ormond Beach ......... 30-34

Gainesville ........................................................ 35-39

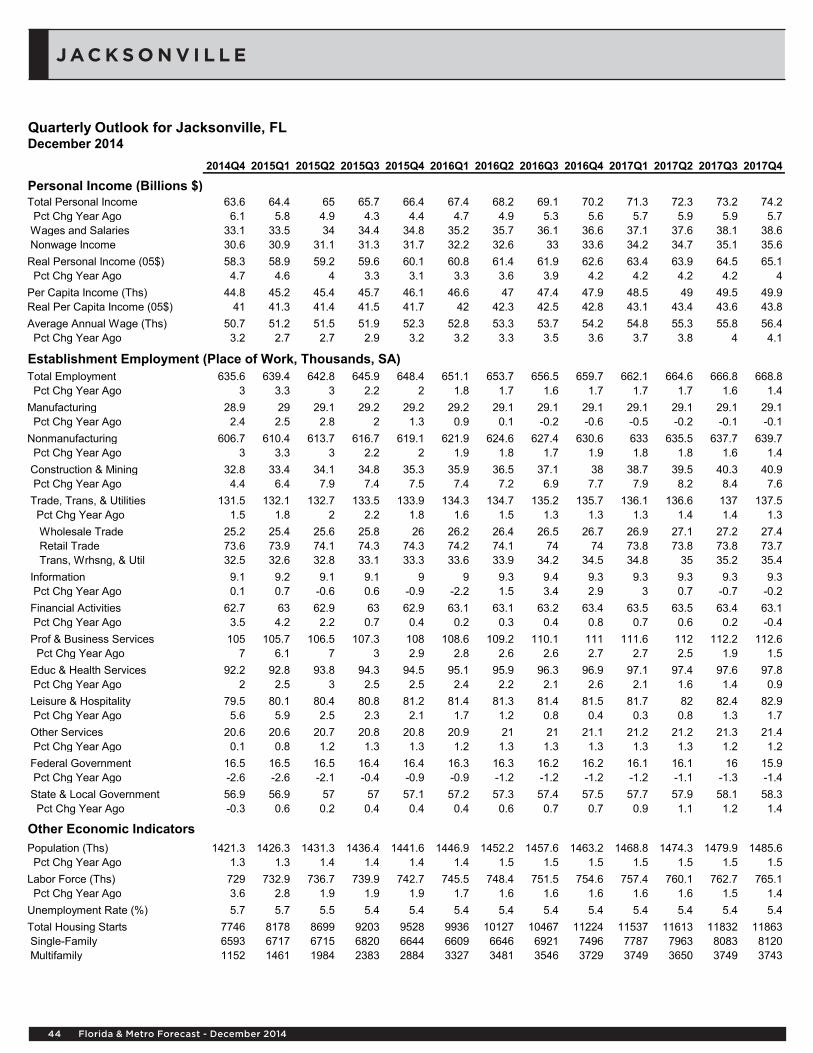

Jacksonville ...................................................... 40-44

Lakeland ........................................................... 45-49

Miami-Fort Lauderdale-Pompano Beach ......... 50-54

Naples-Marco Island ........................................ 55-59

Ocala ................................................................ 60-64

Orlando-Kissimmee ......................................... 65-69

Palm Bay-Melbourne-Titusville ........................ 70-74

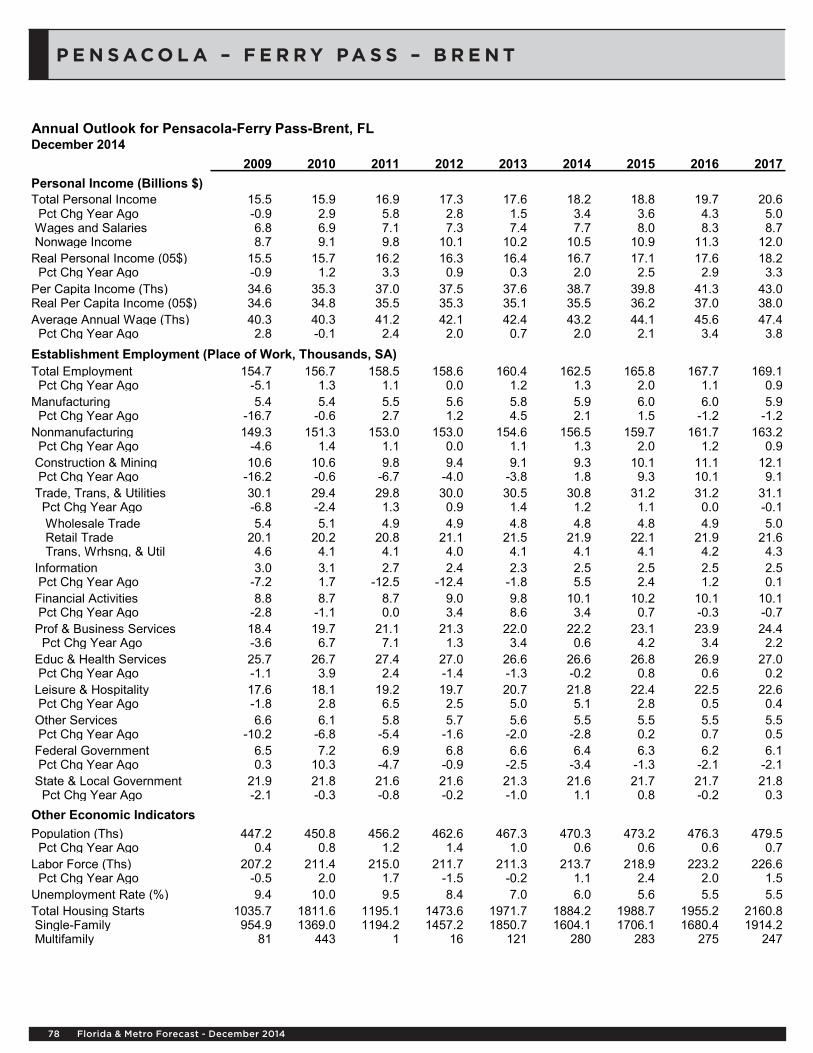

Pensacola-Ferry Pass-Brent ............................. 75-79

Tallahassee ....................................................... 80-84

Tampa-St. Petersburg-Clearwater ................... 85-89

Industry Location Quotient .................................... 90

F L O R I D A H I G H L I G H T S

Institute for Economic Competitiveness 5

• Kris Kringle has nothing on the Sunshine State. That 34th street miracle pales in comparison to the economic miracle in the 27th state.

• During 2014-2017 it is expected that Florida’s economy, as measured by real state GDP, will expand at an average annual rate of 2.8%, and that payroll job creation will average an annual pace of 2.2%. Both remain stronger than the pace expected for the national economy.

• As of October 2014, 39.9% of single-family home transactions in Florida were cash sales, down from 44.3% a year earlier. The share of cash purchases has declined year over year since June 2013. Investors may be reaching their fill of Florida residential real estate. Will traditional buyers pick up the slack?

• Payroll job growth year over year should average 2.8% in 2014, 2.3% in 2015, 1.9% in 2016, and 1.6% in 2017. It will be the 4th quarter of 2015 before payrolls recover to their pre-recession highs.

• Labor force growth in Florida will average 2.0% from 2014-2017. The faster pace of job creation has breathed new life into Florida’s labor market. The improved prospect of finding a job is putting more Floridians back on the job hunt.

• The growing labor force and rising labor force participation rate (60.6% in October 2014) will make lowering the unemployment rate more challenging. The pace of decline will slow dramatically (and could reverse direction in any given month) as labor force growth picks up. As a result of this headwind, the unemployment rate should still hover around 5.8% by the end of 2017.

• In Florida, Underemployment (U-6), a broader measure of labor market weakness than headline unemployment (U-3), remains at 13.4% through the 3rd quarter of 2014, down from 19.3% in 2010.

• The sectors expected to have the strongest average job growth during 2014-2017 are Construction (9.2%), Professional and Business Services (3.5%), Trade, Transportation & Utilities (3.3%), Leisure & Hospitality (2.0%), and Education & Health Services (1.9%).

• Housing starts continue to rise, but the pace of increase drops as interest rates rise. Total starts will be almost 83,400 in 2014, just over 111,500 in 2015, hit 133,700 in 2016, and level off at nearly 150,500 in 2017.

• Real Gross State Product (RGSP) will expand 2.6% in 2014; growth will be 2.7% in 2015 and 2.8% in 2016 before rising to 3.0% in 2017. Average growth will be 2.8% during 2014-2017, 0.4 percentage points faster than average U.S. GDP growth.

• Over 2014-2017 real personal income growth will accelerate and average 3.7%, with 3.5% growth in 2014 rising up to 4.2% growth in 2017.

• Retail sales will grow at an average pace of 4.5% during 2014-2017, with lower gasoline prices raising consumer confidence and disposable incomes.

H I G H L I G H T S O F T H E D E C E M B E R 2 0 1 4 F L O R I D A F O R E C A S T 2 0 1 4 - 2 0 1 7

F L O R I D A S U M M A R Y

6 Florida & Metro Forecast - December 2014

The October 2014 single-family home report released by Florida Realtors continues to depict a housing market that is improving at a slower pace. The median sales price for single-family homes increased $7,804 in October 2014 year over year and now stands at $177,000, a year-over-year price appreciation of 4.6%. Price appreciation in the townhome/condominium market slowed to 7.7% as the median sales price increased $10,000 year over year and registered $139,900 in October.

Inventories of single-family homes in October are up slightly from a year ago and are now 5.4 months, which according to the Florida Realtors report indicates a balance in the single-family market slightly favoring sellers1.

Inventories of condominiums rose from their level of 5.6 months’ supply back in October of 2013 and are now 5.9 months, which according to the Florida Realtors report indicates a balance in the condo market that is tipping in favor of buyers.

Distressed sales of single-family homes in the form of short sales are continuing to contract year over year (-48.0%), but foreclosure/REO sales are up versus October 2013 (38.8%), and traditional sales were up 18.6% year over year in October 2014.

Distressed sales of condos in the form of short sales are rapidly contracting year over year (-55.6%), but foreclosure/REO sales are up versus October 2014 (24.0%), while traditional sales were up 11.6% in October 2014 compared to October 2013.

The percentage of closed sales of single-family homes that were cash transactions stood at 39.9% in October 2014. For condos that figure was even higher as 65.3% of all closings were cash transactions. Both of these markets’ shares of cash transactions have fallen during the course of 2014, which may suggest a waning role of investors in Florida’s housing market.

The declining, though still high, levels of investor activity in residential real estate around the state continue to drive these high percentages of cash transactions.

1 According to the Florida Realtors, the benchmark for a balanced market (favoring neither buyer nor seller) is 5.5 months of inventory. Higher numbers indicate a buyers’ market, lower numbers a sellers’ market.

International buyers and individuals who are able to liquidate financial assets, whose values have soared in recent years, allowing them to make cash purchases are helping sustain these levels.

Will traditional buyers of homes in Florida be able to fill the vacuum as investors become less active in Florida’s residential real estate market? This transition will ultimately determine the path that the housing market follows in 2014 and beyond. Since traditional buyers are finance dependent, mortgage availability will be a primary determinant of how smoothly this transition from investors to traditional individual buyers transpires. Mortgage credit availability data raises the concern that this transition may be rocky.

The Mortgage Bankers Association’s Credit Availability Index has crept slightly higher since sliding at the start of 2014. It currently stands at 113.2, down from 116.1 in September 2014. The index is benchmarked to 100 in March 2012, and to get a sense of how far housing finance has contracted, the Mortgage Bankers Association recently released historical estimates of its Credit Availability Index stretching back ten years. The availability of mortgage credit has been dramatically curtailed relative to pre-recession levels. In 2006 the index was just under 869!

New regulations on qualified mortgages, part of the massive Dodd-Frank financial regulation law, are in effect. Higher capital standards for banks and stringent underwriting standards continue to impact lending.

Current levels of the mortgage credit availability index are only 13.0% of the 2006 peak levels. While the recklessly easy mortgage credit environment of 2006 should not have come to pass, the current tightness in the mortgage market with the availability of mortgages at a mere fraction of prerecession levels is not consistent with a housing market recovery maintaining momentum. Indeed in 2014 we watched price appreciation slow from solid double-digit levels to the sub 5.0% rate that has been the average over the last 3 months.

Figure 1 depicts the monthly realtor sales of existing single-family homes, as well as the 12-month moving average of these sales depicted as the less volatile of the two lines by smoothing out the seasonality in the housing market monthly data. Sales continue on an

FLORIDA’S HOUSING MARKET

F L O R I D A S U M M A R Y

Institute for Economic Competitiveness 7

upward trajectory after bottoming out in early 2008. The economic and demographic drivers of the housing market in Florida continue to strengthen. Job growth in Florida continues to outperform the labor market nationally, and the aging Baby Boomers bode well for continued population growth via the in-migration of

retirees to Florida. As the fundamentals of a healthy housing market in Florida continue to improve, we expect that the upward trend in sales will continue. This continued improvement in the housing market will be increasingly dependent on normalization of mortgage credit availability.

Figure 2 displays median sales prices for single-family existing homes. Median sales prices bottomed out until 2011, but since then have been on an upward climb. As stated in an earlier Florida & Metro forecast, the double-digit pace of price increases was not sustainable, and in 2014 the pace has slowed. Over the past year, the 12-month moving average of median sales prices has risen by nearly $11,700, up 7.1% from a year ago. This recovery in the housing market is a critical component of Florida’s continued economic recovery, and if price appreciation is sustained, it will help feed economic growth over the next several years.

Homeowners are still well below the levels of home equity wealth they had seen at the peak of the housing market (median prices are currently $80,800 below the 2006 peak of $257,800), but rising prices have allowed some homeowners to escape after being trapped in mortgages that were underwater for years. However, a high percentage of Floridians still remain underwater in their mortgages. RealtyTrac puts the percentage of mortgage holders in Florida that are severely underwater in their mortgage at 28%.

Florida’s housing market continues its recovery, but the upward progress is being met with an increasing headwind. There is

still a lot of damage that has yet to be repaired and it will be years before the housing market could be considered fully recovered.

If the availability of mortgage credit does not improve over the next couple years, and if the share of cash

Source: Florida Realtors

0

5,000

10,000

15,000

20,000

25,000

30,000

FloridaSingle-Family, Existing Homes

Realtor Sales Total

Moving Average

Figure 1.

Source: Florida Realtors

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

FloridaSingle-Family, Existing Homes

Median Sales Price Dollars

Moving Average

Figure 2.

F L O R I D A S U M M A R Y

8 Florida & Metro Forecast - December 2014

transactions declines as we are predicting they will, the demand for housing will be curtailed and this mortgage credit crunch will sap any remaining strength from the housing market’s recovery in Florida. In 2014 we have seen the signs of this weakening manifest itself in the form of slower rates of price appreciation, and in absence of an easing of the mortgage credit crunch; we expect to see this pattern continue throughout the forecast horizon.

OUTLOOK FOR FLORIDA 2014-2017GROSS STATE PRODUCTA Miracle in the 27th State?

Real Gross State Product (RGSP) growth in Florida is still expected to grow at a faster pace than we are forecasting for the U.S. economy over the next four years. Florida’s recession started before and ended well after the national recession. While no official dating of the business cycle is done at the state level, I would suggest that Florida spent an additional 32 months in recession compared to the U.S. as a whole.

Thirty-two months longer.That is just two months shy of the total number of

months the U.S. spent in recession over the past three recessions–combined.

This later end date for the recession in Florida indicates that Florida’s recession lasted 50 months in total, more than four full years. That is longer than the combined length of the past four recessions in the United States, which stretches back to 1981.

In 2012 Florida finally got back up off of the canvas after being knocked out cold by that Category 5 recession, and the economy grew at a modest rate of 2.2%. In 2013 the economy stayed at that pace of growth as rising consumer confidence, the housing market recovery, population growth, and the continuing progress in labor market helped set the stage for faster economic growth in the state.

These improvements in the fundamentals of the state’s economy will accelerate growth in 2014, 2015, 2016, and 2017 when Real GSP is expected to grow 2.6%, 2.7%, 2.8%, and 3.0% respectively.

This average growth of 2.8% through 2017 may be small in comparison to the 6.7% growth rate the state experienced in 2005, but it is based more on improvements in the fundamental drivers of the state’s economy and a more sustainable fiscal situation in state and local government. It is also higher than the average of our forecasted growth for the U.S. economy.

Housing prices have made a strong upward movement from the depths to which they plunged during the housing crisis. In the crisis, median home prices fell to a low of $122,200 but now are at a current level of $177,000. This price appreciation is repairing damage to Floridians’ household balance sheets, but it will take many more years to recover all the wealth that was lost when the housing market collapsed and housing prices plummeted from their median price high of $257,800.

Rising house prices are lifting more mortgage holders in the state above the surface of the water for the first time in several years, providing some financial breathing room, though thousands of Floridians remain deeply underwater in their mortgages. Despite this progress and as noted above, RealtyTrac estimates that 28% of mortgaged homes in Florida are deeply underwater.

Nominal Gross State Product continues to rise toward the $1 trillion mark, surpassing $963 billion in 2017, an increase of $163 billion from 2013 and $242 billion from 2009. In 2018 Florida will break that $1 trillion mark.

If the national economic policy and regulatory environment were more of a catalyst instead of becoming ever more restrictive as we discussed in the December 2014 U.S. Forecast, the outlook for Florida’s economy would be even brighter.

As we have gained some historical perspective and examined the revised data on the recession and subsequent recovery in Florida, the economic turnaround is looking more like a miracle that would surely put a twinkle in Kris Kringle’s eye.

PERSONAL INCOME, RETAIL SALES, AND AUTO SALES

Personal income growth in Florida lost momentum in 2013 as a number of factors conspired to bring about deceleration. One full year of sequester spending cuts took place, the payroll tax cut expired, dividend payments dropped off as many companies paid dividends at the end

F L O R I D A S U M M A R Y

Institute for Economic Competitiveness 9

of 2012 to avoid rising dividend tax rates in 2013, and a federal government shutdown took place. This led to a deceleration of personal income growth in Florida from 3.3% in 2012 to 2.4% in 2013.

This lost momentum in personal income growth has returned in 2014, and is expected to be preserved through the end of 2017. In 2014 Florida will experience personal income growth of 4.9%. That growth will ease slightly in 2015 as personal income growth comes in at 4.5%. From there it will accelerate to 5.1% in 2016, and then to 5.8% in 2017. After six years with personal income growth lower than the national rate, these positions reversed in 2013 as personal income growth in Florida grew 2.9% while U.S. growth was just 2.0%. Florida is expected to continue to outpace the nation with personal income growth that is an average of 0.7 of a percentage point higher than the national average growth for 2014 through 2017. Personal income growth during 2014-2017 will average 5.1% in Florida. Personal income will reach in excess of $989 trillion in 2017, with personal income growing nearly $55 billion that final year of our forecast.

In 2014 real disposable income growth will average 3.4%, up from the previous year’s 0.1%. Average growth during 2014-2017, however, will be a more robust 3.6% with growth peaking at 4.3% in 2017.

Financial markets have prospered since the low point of the financial crisis due in large part to the Federal Reserve Bank’s zero interest rate policy coupled with three subsequently larger rounds of quantitative easing. The Dow Jones Industrial Average fell to the 6,600 level in March of 2009, but has since surged back to exceed 17,000, though volatility has increased in recent days. The bond market also continues a strong bull run. Both of these runs will likely be over as the Fed implements interest rate hikes commencing in late 2015.

As a result of this bull run, financial assets held by U.S. households have values that are $27.2 trillion higher than the 2009 nadir of the financial crisis levels, and $15.4 trillion higher than prerecession peaks. Unfortunately, the same cannot be said for home equity wealth held by America’s households. That wealth is still over $2.3 trillion lower than 2005 highs, but home equity wealth has made sizable progress from the bottom of the housing crisis. U.S. households now hold $4.8 trillion more home equity wealth then they held at the low point of the housing market.

The housing market in Florida has not recovered as rapidly or as completely as financial markets have, but housing prices have been rising over the past couple years. The $2.3 trillion dollars in home equity still lost nationwide could take many years to recover with the housing recovery facing a stiffening headwind over the next several years. In Florida, this wealth effect will continue to weigh upon consumer spending through the end of 2017. As noted twice earlier, 28% of Florida’s mortgage holders are still severely underwater in their mortgages.

Years of persistently high unemployment and even higher underemployment compounded the effects of lost housing wealth on consumer spending in Florida. As the labor market in Florida continues to show an acceleration of job creation, there will be a boost in both consumer confidence and spending. Plummeting gasoline prices further buoy confidence and serve as a boost to retail sales outside of gasoline, with more money staying in consumers’ pockets that previously went into the tank.

Retail sales in Florida grew robustly in 2010 and 2011. Part of that growth was due to higher gasoline prices, but it also reflected an ongoing release of pent-up demand by Florida’s consumers as well as spending by domestic and international tourists. As the labor market recovery builds momentum and as more home equity wealth is recovered, retail spending will begin to recover across a broad array of sectors in the economy. The average year-over-year growth rate of retail sales will be over 4.5% during 2014-2017.

When the national recession came to an end, replacement needs and pent-up demand drove light vehicle sales significantly higher. Consumers began to purchase vehicles again after the recession’s end. This replacement demand has been reflected in national sales data despite the historically weak recovery, and earlier in the recovery reflected in consumer’s light vehicle demand. Vehicle registration growth in Florida exhibited that pent-up demand during 2010-2013 when registrations grew at a year-over-year average rate of near 12.0%. This burst followed three years during which registrations contracted at an average rate of near 20.0%.

The venting of pent-up demand being over means more modest growth in vehicle registration in Florida during 2014-2017 despite increased incentives and plentiful financing even to sub-prime borrowers. Over this period,

F L O R I D A S U M M A R Y

10 Florida & Metro Forecast - December 2014

vehicle registration in Florida is expected to average around 5.1%, with 2014 doing most of the heavy lifting in that average. Beyond 2014, growth will average a more modest 3.5% the following three years.

In 2017, Florida’s new passenger car and truck registrations will reach more than 1.34 million, representing an increase of over 634,000 registrations from the 2009 bottom. However, this much-improved level is still below the 2005 peak level of 1.45 million registrations during the height of the economic boom. EMPLOYMENT

Florida’s labor market recovery continues to outpace the recovery in the national job market. In 2013, payroll job growth was 2.5%. This is much stronger when compared to the national rate of job creation, which was 1.7% for the same year. In 2014, the labor market in Florida accelerated with job growth of 2.8%. Payroll job growth will ease to 2.3% in 2015 and 1.9% in 2016, before easing to 1.6% in 2017. Florida will outpace national job growth over the entire forecast horizon by an average of 0.8% over 2014-2017.

The Construction sector has broken free its terrible legacy. Devastated by the housing market’s collapse, it suffered job losses five straight years at an average annual rate of -12.9%. In 2009 alone, the sector had year-over-year job loss at a rate of -23.1%. Job growth finally returned in 2012 and continued to build momentum, exceeding 10% in 2014.

Construction job growth is expected to surge to 10.4% in 2014 before settling at 8.7% in 2015, 8.8% in 2016, and easing higher to 8.9% in 2017. Average annual job growth during 2014-2017 will be 9.2%. Construction will be the fastest growing sector in the state’s economy through 2017. This high-level employment growth may at first glance overstate the strength of the recovery in this sector since it is being calculated from a considerably lower base of employment.

The Professional and Business Services sector will be the state’s second fastest growing sector on average through 2017. Job growth in this sector is expected to be healthy, averaging 3.5% during 2014-2017. Job growth during the first four years of the sector’s recovery averaged 3.0%, but over the next four years it will see more robust growth. Job growth will hit 3.9% in 2014 before easing to 3.7% in 2015 and 2016. This sector, which includes

almost exclusively white collar businesses from law firms to notaries to advertising and PR firms, recovered jobs lost during the recession quickly and has already reached pre-recession peak levels of employment.

The Information sector in Florida experienced year-over-year job growth in 2013 for the first time since 2005. The industry is still roiled by changes as the gathering and delivery of information continues its rapid evolution. The traditional print and radio industry within the sector will be stagnant as the news industry continues to evolve under the unrelenting pressure from smaller digital channels of information dissemination. Sources of growth within this sector, such as software development, data processing and hosting, and wireless telecommunications, will help offset the loss of jobs in legacy media.

Mild annual job growth of 0.2% returned to the Information sector in 2013. After 1.3% growth in 2014 and 2015, growth will then rise to 1.7% in 2016. Average growth of 1.2% is expected during 2014-2017.

The Education and Health Services sector remained immune to the recession that wreaked havoc on most sectors of Florida’s economy. The Health Services sector actually continued to add jobs throughout the recession and continues to do so. This is the only sector of Florida’s economy that performed this recession-defying feat, and it is expected to continue to grow through the end of 2017. During 2014-2017 employment in this sector is expected to expand at an average rate of 1.9%.

Persistent uncertainty surrounding the Affordable Care Act’s impact on healthcare in the face of impending implementation of the law’s mandates and the growing concern about the fiscal feasibility of the law itself casts a pall over this sector. Healthcare providers continue to feel their way along, slowly navigating the multitude of uncertainties this law creates.

Regardless of the law’s ultimate fate in front of the Supreme Court, there will be expanded insurance coverage as a result of the passage of the law, and this expansion coupled with the aging of our already older-than-average population guarantees that the demand for health services in Florida should remain strong. This demand will continue to drive job growth in the Health and Education sector.

Manufacturing employment expanded in Florida at an average rate of 1.6% in 2012, but in 2013 growth eased as domestic and global economic environments weakened.

F L O R I D A S U M M A R Y

Institute for Economic Competitiveness 11

The weakening of economic expansions along with a series of minor crises in emerging economies, growing concern over a slowdown in China, a strengthening U.S. dollar, and persistent struggles in Europe will drive down job growth in the manufacturing sector beyond 2014.

After stumbling slightly in 2013, we are expecting to see job growth of 2.0% in manufacturing for the full year in 2014, followed by a year of milder job growth in 2015 when manufacturing employment will expand at a rate of 1.0%. Manufacturing is expected to revisit the job losses that have come to characterize the sector. In 2016 job growth is expected to be -0.9%, and the sector shrinks further in 2017 with employment growth at -0.6%.

The State & Local Government sector is seeing improved revenue streams, and budgets are recovering after being emaciated by the recession and housing crisis. The budgetary crisis impacted governments at all levels in Florida. Consequently, job losses in this sector persisted for five years extending through 2013. In 2014, job losses in the State and Local Government sector ended but growth was still non-existent. From this point, growth will remain positive and accelerate year over year, averaging 0.7% during 2015-2017. As Florida’s population and economy continue to grow, the demand for state and local government services will grow and employment growth will be a necessary part of the solution to meet the demands of our growing economy. State and local government will remain cautious in hiring. The housing bubble filled state and local government coffers to the point of overflow. The subsequent budget slashing that was necessitated as revenues plummeted forced local government to learn how to do more with less. This hard-learned lesson in austerity will keep the pace of job growth suppressed through the next several years while still being able to meet the growing demand for services.

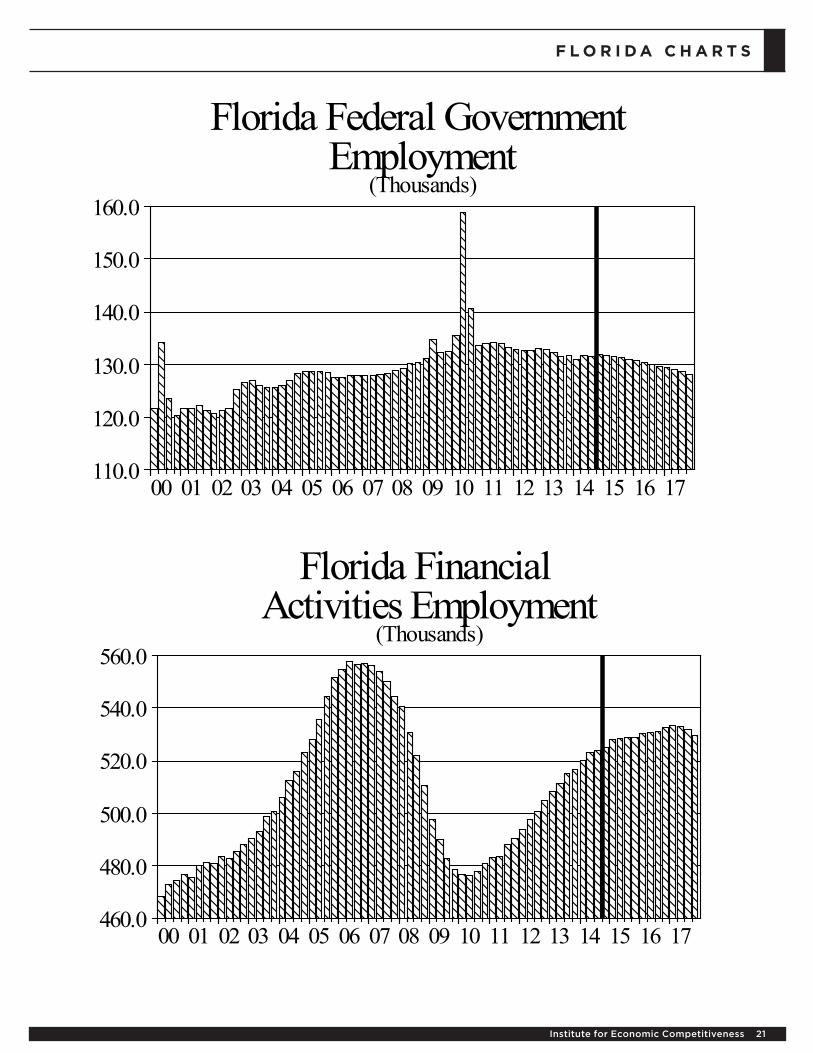

The outlook for Federal Government employment growth in Florida on the other hand, continues to be negative through the end of our 2017 forecast horizon. Any solution to our federal deficit and debt problems will require more revenue, but ultimately cuts in federal spending will be necessitated as well. As the Fed eventually embarks on a cycle of interest rate hikes in late 2015, the burden of servicing a national debt that is in excess of $18 trillion will consume a larger slice of federal tax revenue pie. This increasing share will have to come from somewhere, and the portion of federal tax revenue that goes toward discretionary spending will, by necessity,

get smaller. It is unlikely that there will be layoffs, but as federal employees retire or otherwise leave positions in the years ahead many of these posts will remain unfilled. It will likely be 2020 before the decennial census drives the first expansion in Federal Government employment in Florida since 2010. Employment in the sector will contract at an average rate of 0.6% during 2014-2017.

UNEMPLOYMENTThe unemployment rate in Florida continues to fall,

standing at 6.0% as of October 2014. Unemployment has substantially declined from its peak, and after spending many years above the national rate of unemployment, Florida’s unemployment rate is now 0.2 percentage points above that of the nation as a whole. These declines in the unemployment rate earlier in the recovery in Florida and the nation were in part driven by a shrinking labor force participation rate. Florida’s labor force participation in October stood at 60.6%, up from 59.9% a year earlier. The national labor force participation rate, however, stood at 62.8% in November 2014, the lowest since March 1978 and down 3.4 percentage points from the start of the recession.

Understanding these different trends in the labor force participation rate in Florida relative to the nation as a whole is critical to understanding comparative movements in the unemployment rate going forward. If Florida continues to see a rising labor force participation rate while the national rate languishes, it is likely we will see the unemployment rate in Florida continue to remain above that of the nation as a whole. As counterintuitive as it may seem, this will be evidence that Florida’s labor market is healing faster than the national labor market.

The unemployment rate in Florida, 6.0% in October 2014, represents a 5.4 percentage point decline from the peak unemployment rate in 2010.

We are forecasting stronger economic growth in Florida over the forecast horizon as well as continued strong payroll job growth. This faster economic growth, however, will be faced with a headwind of a rising labor force participation rate that will make progress in reducing the unemployment rate a more challenging task. We expect the labor force to grow more rapidly during 2014-2017 as job seekers become encouraged by job growth in the state and reenter the labor force. This will have a net result of seeing modest declines in

F L O R I D A S U M M A R Y

12 Florida & Metro Forecast - December 2014

unemployment rates and the occasional increase in the unemployment rate in Florida on a month-to-month basis.

The labor force in Florida is expected to grow an average of 2.0% during 2014-2017. That compares to an average growth rate of just 0.9% during the four years prior. As a result, the unemployment rate is expected to continue to hover around the 5.8% level during 2015- 2017. This will represent a decline in the average unemployment rate of just 0.2% during 2014-2017. Contrast that modest dip to the previous four years decline of 4.1 percentage points while the labor market did not face the stiff headwinds of a rapidly growing labor force.

Nationally and in Florida, the levels of underemployment—those who are working part-time but not by their choice, and workers marginally attached to the labor force (those who are neither working nor currently looking for work, but indicate that they want and are available for a job, and have looked for work sometime in the past twelve months)—are still elevated. When adding these workers to the headline unemployment figure we get the broadest measure of unemployment known as U-6. Looking at U-6 we see a labor market still deeply damaged, as U-6 in Florida averaged 13.4% for the four quarters ending in Q3 2014 according to the Bureau of Labor Statistics, while the national rate of U-6 stands at 12.5 over that same period.

While U-6 is down from its 2012 reading of 16.0%, the current rate still reflects more depth of the damage to the labor market in Florida than might be reflected in the current headline unemployment rate of 6.0%.

As the employer mandates of the Affordable Care Act are finally enforced in the next few years, the potential for increasing levels of underemployment in response to the full/part-time distinction in the law will require continued scrutiny of U-6 at the national and state level to fully gauge the impact of the healthcare law on the labor market.

F L O R I D A S U M M A R Y TA B L E S

Institute for Economic Competitiveness 13

Table 1. Annual Summary of the University of Central Florida Forecast for Florida

2009 2010 2011 2012 2013 2014 2015 2016 2017

Personal Income (Bil. $) 696.7 725.2 767.4 793.0 811.4 850.9 888.9 934.6 989.2Florida.(%Ch Year ago) -5.3 4.1 5.8 3.3 2.4 4.9 4.5 5.1 5.8U.S.(%Ch Year ago) -2.8 2.8 6.2 5.2 2.0 4.2 4.1 4.4 4.9Personal Income (Bil. 2005$) 696.7 713.3 736.9 747.6 755.9 782.0 808.3 838.7 873.7Florida.(%Ch Year ago) -5.2 2.4 3.3 1.5 1.1 3.5 3.4 3.8 4.2U.S.(%Ch Year ago) -2.7 1.2 3.7 3.3 0.8 2.8 3.0 3.1 3.3Disp. Income (Bil. 2005$) 643.2 658.8 673.1 679.3 680.1 703.2 725.4 751.8 784.1Florida.(%Ch Year ago) -3.4 2.5 2.2 0.9 0.1 3.4 3.2 3.6 4.3U.S.(%Ch Year ago) -0.4 1.0 2.5 3.0 -0.2 2.7 2.5 3.0 3.4GSP (Bil. $) 721.7 728.6 736.4 769.0 800.5 837.0 877.2 918.1 963.3(%Ch Year ago) -4.1 1.0 1.1 4.4 4.1 4.6 4.8 4.7 4.9GSP (Bil. 2005$) 721.7 721.0 718.2 734.3 750.5 770.3 791.5 813.7 837.7(%Ch Year ago) -6.1 -0.1 -0.4 2.2 2.2 2.6 2.7 2.8 3.0

Employment -5.7 -0.1 2.2 2.9 2.4 3.0 2.6 2.1 1.9Labor Force -1.4 0.9 1.1 1.1 0.7 1.9 2.2 2.1 1.9FL Unemployment Rate (%) 10.4 11.3 10.3 8.8 7.2 6.2 5.8 5.7 5.8U.S. Unemployment Rate (%) 9.3 9.6 8.9 8.1 7.4 6.2 5.8 5.8 5.8

Total Nonfarm U.S. -4.3 -0.7 1.2 1.7 1.7 1.8 1.7 1.2 1.0 Florida -6.3 -0.8 1.1 2.0 2.5 2.8 2.3 1.9 1.6Mining -11.5 -0.5 4.0 -0.3 0.3 3.4 0.8 -2.0 -0.2Construction -23.1 -11.2 -4.4 1.9 7.5 10.4 8.7 8.8 8.9Manufacturing -12.7 -4.5 1.1 1.6 1.4 2.0 1.0 -0.2 -0.5Nondurable Goods -10.0 -3.6 0.8 1.1 -0.5 -0.6 -0.1 -0.9 -0.6Durable Goods -14.0 -4.9 1.3 1.8 2.4 3.3 1.6 0.1 -0.4Trans. Warehs. & Utility -6.6 -2.0 3.7 2.2 2.7 3.6 2.6 3.7 3.4Wholesale Trade -7.9 -2.8 -0.3 1.8 1.0 2.2 2.0 2.5 2.5Retail Trade -6.6 0.2 2.3 2.4 2.8 3.1 1.8 -0.1 -0.5Financial Activities -7.3 -1.9 1.8 2.7 2.7 2.0 1.0 0.5 0.2Prof. and Business Services -8.2 1.2 3.0 3.7 4.0 3.9 3.7 3.7 2.8Edu & Health Services 1.2 1.9 1.9 1.7 1.7 2.0 2.4 2.1 1.4Leisure & Hospitality -4.5 0.5 2.8 4.2 3.9 3.6 2.3 1.1 1.1Information -8.5 -4.6 -1.0 -1.6 0.2 1.3 1.3 1.7 0.7Federal Gov't. 2.3 7.2 -5.4 -0.8 -0.5 -0.4 -0.1 -1.0 -1.0State & Local Gov't. -1.5 -1.2 -1.1 -1.4 -0.2 0.0 0.2 0.7 1.2

Population (thous) 18,682.3 18,879.7 19,113.0 19,349.2 19,581.9 19,817.7 20,085.0 20,379.1 20,694.0(%Ch Year ago) 0.8 1.1 1.2 1.2 1.2 1.2 1.3 1.5 1.5Net Migration (thous) 106.8 168.1 198.9 199.6 200.7 208.5 243.0 258.2 269.4(%Ch Year ago) 42.5 70.3 22.6 0.4 0.6 3.9 16.8 6.3 4.4

Housing Starts Tot. Private (thous) 33.7 38.1 41.6 59.7 81.2 83.4 111.6 133.7 150.5Housing Starts Single Family (thous) 26.8 31.8 32.0 42.8 55.0 57.8 74.3 87.2 103.2Housing Starts Multi-Family (thous) 6.9 6.3 9.6 16.9 26.1 25.6 37.3 46.5 47.3

(%Ch Year ago) -0.2 1.2 3.1 1.9 1.5 2.0 1.1 1.5 2.0Consumer Prices

Housing

Population and Migration

NonFarm Employment (Payroll Survey % Change Year Ago)

Employment and Labor Force (Household Survey % Change Year Ago)

Personal Income and GSP

F L O R I D A S U M M A R Y TA B L E S

14 Florida & Metro Forecast - December 2014

Table 2. Quarterly Summary of the University of Central Florida Forecast for Florida*

2014Q4 2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2 2017Q3 2017Q4

Personal Income (Bil. $) 865.8 876.0 884.0 892.6 902.9 916.3 927.6 940.3 954.1 969.3 982.7 995.7 1008.9Florida.(%Ch Year ago) 5.4 5.1 4.3 4.2 4.3 4.6 4.9 5.3 5.7 5.8 5.9 5.9 5.7U.S.(%Ch Year ago) 4.8 4.7 4.0 3.9 3.9 4.1 4.3 4.5 4.8 4.9 5.0 5.0 4.9Personal Income (Bil. 2005$) 793.2 801.1 805.4 809.9 816.9 826.7 834.2 842.3 851.6 861.9 869.5 877.6 885.8Florida.(%Ch Year ago) 4.0 4.0 3.4 3.1 3.0 3.2 3.6 4.0 4.3 4.3 4.2 4.2 4.0U.S.(%Ch Year ago) 3.5 3.5 3.1 2.8 2.6 2.7 3.0 3.2 3.4 3.3 3.3 3.3 3.2Disp. Income (Bil. 2005$) 714.4 719.9 722.7 726.6 732.4 740.5 747.4 755.3 764.1 772.1 779.7 788.1 796.5Florida.(%Ch Year ago) 4.2 4.1 3.4 2.6 2.5 2.9 3.4 3.9 4.3 4.3 4.3 4.3 4.2U.S.(%Ch Year ago) 3.4 3.2 2.5 2.3 2.1 2.4 2.8 3.2 3.5 3.4 3.4 3.4 3.4GSP (Bil. $) 853.3 862.8 872.2 882.5 891.3 900.9 912.0 923.8 935.7 946.5 957.8 968.6 980.2(%Ch Year ago) 4.5 5.6 4.6 4.6 4.5 4.4 4.6 4.7 5.0 5.1 5.0 4.9 4.8GSP (Bil. 2005$) 778.9 783.9 788.6 794.3 799.1 804.0 810.2 816.8 823.7 829.1 834.8 840.4 846.5(%Ch Year ago) 2.5 3.4 2.6 2.5 2.6 2.6 2.7 2.8 3.1 3.1 3.0 2.9 2.8

Employment 3.2 2.6 2.3 3.0 2.7 2.4 2.1 1.9 2.0 2.0 1.9 1.8 1.7Labor Force 2.6 2.3 1.8 2.4 2.4 2.2 2.1 2.0 2.0 2.0 1.9 1.9 1.8FL Unemployment Rate (%) 6.0 5.9 5.8 5.7 5.7 5.7 5.8 5.8 5.7 5.7 5.8 5.8 5.8U.S. Unemployment Rate (%) 5.8 5.8 5.7 5.7 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8

Total Nonfarm U.S. 1.9 2.0 1.8 1.7 1.4 1.3 1.2 1.1 1.2 1.1 1.1 0.9 0.8 Florida 2.5 2.5 2.2 2.3 2.2 2.0 1.9 1.8 1.9 1.8 1.7 1.6 1.4Mining 5.8 4.4 2.0 -1.2 -2.0 -2.4 -2.3 -1.8 -1.5 -0.9 -0.3 0.1 0.4Construction 8.7 8.5 9.0 8.5 8.8 8.7 8.7 8.6 9.3 9.3 9.2 9.0 8.2Manufacturing 1.5 0.7 1.2 1.3 0.7 0.4 -0.2 -0.5 -0.8 -0.7 -0.4 -0.3 -0.4Nondurable Goods -0.3 -0.2 0.5 -0.1 -0.7 -0.8 -0.9 -0.9 -1.0 -0.9 -0.6 -0.5 -0.3Durable Goods 2.3 1.2 1.6 2.0 1.4 1.0 0.2 -0.2 -0.6 -0.6 -0.3 -0.3 -0.4Trans. Warehs. & Utility 3.5 2.6 2.6 2.5 2.8 3.5 3.8 3.7 3.8 3.8 3.6 3.4 3.1Wholesale Trade 2.7 1.5 1.4 2.5 2.6 2.6 2.6 2.4 2.5 2.6 2.4 2.5 2.4Retail Trade 2.3 2.6 2.0 1.6 1.0 0.5 0.0 -0.4 -0.4 -0.6 -0.5 -0.5 -0.4Financial Activities 1.8 1.5 1.0 0.9 0.7 0.4 0.4 0.4 0.7 0.6 0.5 0.1 -0.5Prof. and Business Services 3.6 3.3 3.7 3.9 4.0 3.9 3.6 3.7 3.8 3.7 3.3 2.5 1.7Edu & Health Services 2.0 2.5 2.4 2.4 2.2 2.1 1.9 1.9 2.4 2.0 1.5 1.2 0.8Leisure & Hospitality 3.0 3.0 1.8 2.4 2.2 1.8 1.2 0.8 0.5 0.3 0.8 1.3 1.7Information 2.3 3.5 1.1 1.0 -0.5 -1.9 1.8 3.6 3.1 3.1 0.7 -0.8 -0.3Federal Gov't. 0.1 0.6 -0.1 -0.2 -0.7 -0.8 -1.0 -1.0 -1.0 -1.0 -0.9 -1.1 -1.2State & Local Gov't. -0.1 0.0 0.0 0.4 0.5 0.5 0.7 0.8 0.8 1.0 1.1 1.3 1.5

Population (thous) 19,911.1 19,979.4 20,048.8 20,119.7 20,191.9 20,265.5 20,340.3 20,416.5 20,494.2 20,573.6 20,653.6 20,734.0 20,814.8(%Ch Year ago) 1.2 1.3 1.3 1.4 1.4 1.4 1.5 1.5 1.5 1.5 1.5 1.6 1.6Net Migration (thous) 57.3 59.3 60.2 61.3 62.2 63.2 63.9 65.0 66.0 67.2 67.3 67.4 67.6(%Ch Year ago) 13.8 17.8 19.4 21.5 8.5 6.5 6.2 6.1 6.2 6.3 5.3 3.6 2.3

Housing Starts Tot. Private (thous) 90.9 99.5 108.9 116.3 121.6 127.3 129.7 134.1 143.9 147.9 149.0 152.2 152.8Housing Starts Single Family (thous) 62.6 68.5 72.7 77.5 78.6 80.8 83.3 88.2 96.5 100.6 102.8 104.4 104.8Housing Starts Multi-Family (thous) 28.3 31.0 36.2 38.8 43.0 46.5 46.5 45.9 47.3 47.3 46.2 47.7 48.0

(%Ch Year ago) 1.6 1.2 0.8 1.0 1.3 1.5 1.5 1.5 1.7 1.8 2.1 2.1 2.1

*Quarterly at an annual rate

Housing

Consumer Prices

Personal Income and GSP

Employment and Labor Force (Household Survey % Change Year Ago)

NonFarm Employment (Payroll Survey % Change Year Ago)

Population and Migration

F L O R I D A S U M M A R Y TA B L E S

Institute for Economic Competitiveness 15

Table 3. Employment Quarterly*

2014Q4 2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2 2017Q3 2017Q4

Total Nonfarm 7,856.9 7,906.7 7,952.1 7,995.1 8,029.3 8,065.3 8,101.1 8,139.3 8,181.0 8,210.4 8,241.6 8,269.3 8,295.8

Manufacturing 330.1 330.7 331.6 332.1 332.6 332.2 331.0 330.6 330.1 329.9 329.7 329.4 328.8

Durable Goods 223.4 224.2 225.2 226.0 226.7 226.4 225.6 225.5 225.2 225.1 225.0 224.8 224.3

Wood Products 10.8 10.9 11.0 11.1 11.2 11.2 11.1 11.2 11.2 11.3 11.3 11.3 11.2

Computer & Electronics 40.3 40.2 39.9 39.5 39.2 38.9 38.6 38.4 38.3 38.1 38.0 37.9 37.9

Transportation Equipment 39.0 39.2 39.3 39.2 39.1 38.8 38.5 38.2 38.0 37.9 37.7 37.4 37.2

Nondurables 106.7 106.6 106.4 106.1 105.9 105.7 105.4 105.1 104.8 104.8 104.7 104.6 104.5

Foods 28.5 28.5 28.5 28.5 28.5 28.4 28.4 28.3 28.2 28.3 28.3 28.4 28.4

Non-Manufacturing 7,526.8 7,576.0 7,620.5 7,663.0 7,696.7 7,733.2 7,770.1 7,808.7 7,851.0 7,880.5 7,911.9 7,939.8 7,967.0

Mining 5.9 5.9 5.9 5.9 5.8 5.8 5.8 5.8 5.7 5.8 5.8 5.8 5.8

Construction 418.3 426.9 436.3 446.6 455.1 464.1 474.4 485.1 497.4 507.5 518.2 528.6 538.0

Trans. Warehs. & Utility 259.2 259.6 261.3 263.7 266.3 268.6 271.2 273.6 276.3 278.8 280.9 282.8 284.8

Wholesale Trade 329.5 331.3 333.4 336.1 338.1 339.8 342.1 344.1 346.7 348.5 350.4 352.5 354.8

Retail Trade 1,047.5 1,051.7 1,054.4 1,057.6 1,057.6 1,056.6 1,054.7 1,053.8 1,053.2 1,050.3 1,049.8 1,049.1 1,048.6

Information 137.1 139.2 137.3 136.6 136.3 136.5 139.8 141.6 140.6 140.8 140.8 140.4 140.2

Prof. & Bus. Services 1,174.5 1,185.3 1,198.0 1,210.1 1,221.9 1,231.5 1,241.2 1,254.3 1,268.0 1,276.6 1,281.9 1,285.2 1,289.7

Admin. & Support 592.1 598.4 606.8 614.2 621.8 629.6 637.9 649.9 661.4 670.5 675.7 679.6 684.6

Prof. Sci & Tech 490.1 494.0 497.9 502.3 506.3 508.0 509.1 510.0 512.0 511.3 511.3 510.5 509.8

Mgmt. of Co. 92.4 93.0 93.3 93.6 93.8 94.0 94.2 94.3 94.6 94.8 94.9 95.1 95.3

Financial Activities 525.4 528.1 528.4 529.0 528.8 530.1 530.7 531.2 532.7 533.5 533.3 532.0 530.0

Real Estate & Rent 171.6 172.3 173.0 173.7 174.3 175.2 175.9 176.8 177.9 178.9 179.7 180.3 180.8

Fin. & Insurance 353.8 355.8 355.4 355.3 354.5 354.9 354.7 354.4 354.8 354.6 353.6 351.7 349.2

Edu. & Health Service 1,158.0 1,166.0 1,177.6 1,182.1 1,183.8 1,190.6 1,199.7 1,204.7 1,211.7 1,213.9 1,217.5 1,219.4 1,221.1

Education Services 148.7 149.3 149.1 149.1 149.0 149.0 148.8 148.5 148.3 147.8 147.3 146.8 146.0

Health Services 1,009.3 1,016.7 1,028.5 1,033.0 1,034.8 1,041.7 1,050.9 1,056.3 1,063.4 1,066.0 1,070.2 1,072.7 1,075.1

Leisure & Hospitality 1,082.3 1,090.8 1,095.4 1,100.9 1,106.1 1,110.3 1,108.9 1,109.9 1,111.2 1,113.7 1,118.3 1,124.5 1,130.6

Other Services 312.9 314.2 315.2 316.2 317.1 318.2 319.3 320.3 321.4 322.4 323.2 324.0 324.8

Government 1,076.2 1,076.8 1,077.4 1,078.1 1,079.7 1,080.9 1,082.3 1,084.3 1,086.1 1,089.0 1,092.0 1,095.4 1,098.7

Federal Gov't. 132.0 131.8 131.7 131.4 131.1 130.8 130.3 130.0 129.7 129.5 129.2 128.7 128.2

State & Local Gov't 944.1 945.0 945.7 946.8 948.6 950.1 952.0 954.3 956.4 959.6 962.8 966.7 970.5

*Quarterly at an annual rate

Florida Payroll Employment (Thousands)

F L O R I D A S U M M A R Y TA B L E S

16 Florida & Metro Forecast - December 2014

Table 4. Employment Annual

2009 2010 2011 2012 2013 2014 2015 2016 2017

Total Nonfarm 7,230.6 7,172.3 7,252.3 7,396.7 7,580.1 7,791.4 7,970.8 8,121.7 8254.3

Manufacturing 324.0 309.1 312.5 317.4 322.0 328.5 331.8 330.9 329.5

Durable Goods 214.5 203.6 206.2 209.9 215.0 222.1 225.5 225.7 224.8

Wood Products 9.1 8.4 8.6 8.8 10.4 10.8 11.0 11.2 11.3

Computer & Electronics 44.7 43.0 43.0 42.5 40.9 40.1 39.7 38.6 37.9

Transportation Equipment 34.9 33.8 34.2 35.4 36.6 38.4 39.2 38.4 37.6

Nondurables 109.5 105.5 106.3 107.5 107.0 106.4 106.2 105.3 104.7

Foods 27.9 27.5 28.7 29.2 29.2 28.4 28.5 28.3 28.3

Non-Manufacturing 6,906.6 6,863.3 6,939.7 7,079.3 7,258.2 7,463.0 7,639.0 7,790.7 7,924.8

Mining 5.5 5.4 5.7 5.6 5.7 5.8 5.9 5.8 5.8

Construction 396.7 351.1 335.4 341.9 367.7 405.9 441.2 480.2 523.1

Trans. Warehs. & Utility 231.8 227.1 235.4 240.6 247.2 256.0 262.7 272.5 281.8

Wholesale Trade 322.4 313.2 312.2 317.9 321.1 328.2 334.7 343.2 351.6

Retail Trade 932.3 934.0 955.3 978.3 1,005.4 1,036.9 1,055.3 1,054.6 1,049.4

Information 143.8 137.1 135.7 133.6 133.9 135.7 137.4 139.6 140.5

Prof. & Bus. Services 993.2 1,005.4 1,035.8 1,074.3 1,117.4 1,160.4 1,203.8 1,248.8 1,283.4

Admin. & Support 481.8 493.8 516.6 537.9 558.4 581.7 610.3 644.7 677.6

Prof. Sci & Tech 431.5 432.5 437.9 451.0 468.1 486.3 500.1 509.8 510.7

Mgmt. of Co. 80.0 79.1 81.4 85.4 90.9 92.4 93.4 94.3 95.0

Financial Activities 487.4 477.9 486.4 499.4 512.8 523.3 528.6 531.2 532.2

Real Estate & Rent 154.9 150.4 153.0 160.0 165.7 171.2 173.3 176.5 179.9

Fin. & Insurance 332.4 327.5 333.4 339.4 347.1 352.1 355.3 354.7 352.3

Edu. & Health Service 1,050.8 1,070.7 1,091.2 1,109.5 1,127.9 1,150.1 1,177.4 1,201.7 1,218.0

Education Services 127.6 134.6 136.8 139.6 142.7 147.5 149.1 148.6 147.0

Health Services 923.2 936.1 954.5 969.9 985.2 1,002.6 1,028.3 1,053.1 1,071.0

Leisure & Hospitality 926.9 931.2 957.2 997.5 1,036.4 1,073.2 1,098.3 1,110.1 1,121.8

Other Services 301.1 297.3 295.7 301.6 306.4 311.4 315.7 319.8 323.6

Government 1,114.8 1,112.8 1,093.5 1,079.1 1,076.4 1,076.1 1,078.0 1,083.4 1,093.8

Federal Gov't. 132.7 142.2 134.0 132.8 132.2 131.6 131.5 130.2 128.9

State & Local Gov't 982.2 970.6 959.6 946.3 944.3 944.5 946.5 953.2 964.9

Florida Payroll Employment (Thousands)

F L O R I D A S U M M A R Y TA B L E S

Institute for Economic Competitiveness 17

Table 5. Personal Income-Quarterly*

2014Q4 2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2 2017Q3 2017Q4

Personal Income 865.8 876.0 884.0 892.6 902.9 916.3 927.6 940.3 954.1 969.3 982.7 995.7 1008.9

Wages & Salaries 385.3 390.8 395.7 400.7 405.7 411.0 416.3 421.9 427.8 433.6 439.3 445.1 451.0

Other Labor Income 86.2 86.8 87.4 88.2 89.1 90.2 91.0 92.0 93.1 94.6 95.5 96.5 97.5

Nonfarm 51.7 52.5 53.4 54.0 54.5 55.3 56.2 56.7 57.3 57.9 58.7 58.9 59.3

Farm 1.2 1.1 1.1 1.2 1.3 1.3 1.4 1.4 1.4 1.4 1.3 1.4 1.4

Property Income 225.7 226.2 227.2 228.6 231.6 235.0 238.5 243.4 248.8 253.8 258.9 263.7 268.5

Transfer Payments 174.7 178.5 179.9 181.3 182.8 187.1 188.2 189.7 191.5 195.6 197.4 199.2 201.1

Social Insurance 61.2 62.4 63.1 63.8 64.6 66.0 66.6 67.4 68.3 70.1 71.0 71.8 72.6

Personal Income 793.2 801.1 805.4 809.9 816.9 826.7 834.2 842.3 851.6 861.9 869.5 877.6 885.8

Wages & Salaries 353.0 357.4 360.6 363.6 367.0 370.8 374.4 377.9 381.8 385.5 388.7 392.3 396.0

Other Labor Income 79.0 79.4 79.6 80.0 80.7 81.4 81.9 82.5 83.1 84.1 84.5 85.1 85.6

Nonfarm 47.4 48.0 48.7 49.0 49.3 49.9 50.6 50.8 51.2 51.5 51.9 51.9 52.1

Farm 1.1 1.1 1.0 1.1 1.2 1.2 1.2 1.3 1.2 1.2 1.2 1.2 1.2

Property Income 206.7 206.9 207.0 207.5 209.6 212.0 214.5 218.1 222.1 225.7 229.1 232.5 235.7

Transfer Payments 160.0 163.3 163.9 164.5 165.4 168.8 169.3 169.9 170.9 173.9 174.7 175.6 176.5

Social Insurance 56.1 57.0 57.5 57.9 58.4 59.5 59.9 60.4 61.0 62.3 62.8 63.3 63.8

New Passenger Car & Truck Registrations 1228.73 1224.71 1235.69 1251.72 1266.57 1281.17 1294.49 1301.58 1313.34 1325.74 1338.34 1351.82 1351.80

Retail Sales (Billions $) 297.4 299.8 303.0 306.7 309.6 312.7 316.2 320.5 324.1 327.5 331.9 335.4 338.9

Real Retail Sales (Billions 2005$) 272.5 274.1 276.0 278.3 280.1 282.1 284.4 287.1 289.3 291.2 293.7 295.6 297.5

*Quarterly at an annual rate

Billions Current Dollars

Billions 2005 $

F L O R I D A S U M M A R Y TA B L E S

18 Florida & Metro Forecast - December 2014

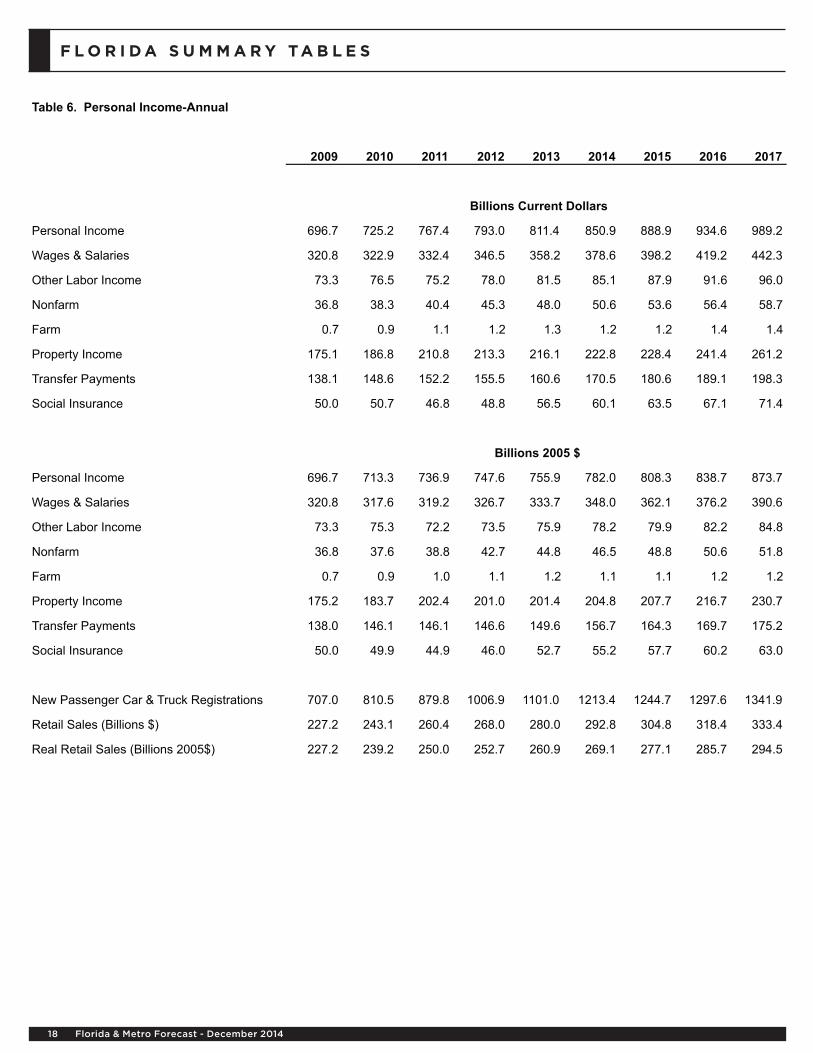

Table 6. Personal Income-Annual

2009 2010 2011 2012 2013 2014 2015 2016 2017

Personal Income 696.7 725.2 767.4 793.0 811.4 850.9 888.9 934.6 989.2

Wages & Salaries 320.8 322.9 332.4 346.5 358.2 378.6 398.2 419.2 442.3

Other Labor Income 73.3 76.5 75.2 78.0 81.5 85.1 87.9 91.6 96.0

Nonfarm 36.8 38.3 40.4 45.3 48.0 50.6 53.6 56.4 58.7

Farm 0.7 0.9 1.1 1.2 1.3 1.2 1.2 1.4 1.4

Property Income 175.1 186.8 210.8 213.3 216.1 222.8 228.4 241.4 261.2

Transfer Payments 138.1 148.6 152.2 155.5 160.6 170.5 180.6 189.1 198.3

Social Insurance 50.0 50.7 46.8 48.8 56.5 60.1 63.5 67.1 71.4

Personal Income 696.7 713.3 736.9 747.6 755.9 782.0 808.3 838.7 873.7

Wages & Salaries 320.8 317.6 319.2 326.7 333.7 348.0 362.1 376.2 390.6

Other Labor Income 73.3 75.3 72.2 73.5 75.9 78.2 79.9 82.2 84.8

Nonfarm 36.8 37.6 38.8 42.7 44.8 46.5 48.8 50.6 51.8

Farm 0.7 0.9 1.0 1.1 1.2 1.1 1.1 1.2 1.2

Property Income 175.2 183.7 202.4 201.0 201.4 204.8 207.7 216.7 230.7

Transfer Payments 138.0 146.1 146.1 146.6 149.6 156.7 164.3 169.7 175.2

Social Insurance 50.0 49.9 44.9 46.0 52.7 55.2 57.7 60.2 63.0

New Passenger Car & Truck Registrations 707.0 810.5 879.8 1006.9 1101.0 1213.4 1244.7 1297.6 1341.9

Retail Sales (Billions $) 227.2 243.1 260.4 268.0 280.0 292.8 304.8 318.4 333.4

Real Retail Sales (Billions 2005$) 227.2 239.2 250.0 252.7 260.9 269.1 277.1 285.7 294.5

Billions Current Dollars

Billions 2005 $

F L O R I D A C H A R T S

Institute for Economic Competitiveness 19

171615141312111009080706050403020100

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

Florida & U.S. Unemployment Rate(%)

FL Unemployment RateU.S. Unemployment Rate

171615141312111009080706050403020100

700.0

600.0

500.0

400.0

300.0

Florida Construction Employment(Thousands)

F L O R I D A C H A R T S

20 Florida & Metro Forecast - December 2014

171615141312111009080706050403020100

6%

4%

2%

0%

-2%

-4%

Florida Consumer Price Index(% change year ago)

FL CPI

171615141312111009080706050403020100

1250.01200.01150.01100.01050.01000.0950.0900.0850.0800.0

Florida Education & Health Services Employment

(Thousands)

F L O R I D A C H A R T S

Institute for Economic Competitiveness 21

171615141312111009080706050403020100

160.0

150.0

140.0

130.0

120.0

110.0

Florida Federal Government Employment

(Thousands)

171615141312111009080706050403020100

560.0

540.0

520.0

500.0

480.0

460.0

Florida Financial Activities Employment

(Thousands)

F L O R I D A C H A R T S

22 Florida & Metro Forecast - December 2014

171615141312111009080706050403020100

12%10%8%6%4%2%0%

-2%-4%-6%

Florida Gross State Product(% change year ago)

FL Gross State Product

171615141312111009080706050403020100

300.0

250.0

200.0

150.0

100.0

50.0

0.0

9%

8%

7%

6%

5%

4%

3%

Florida Housing Starts(thousands)

Total Private Housing Starts30 year Mortgage Rates

F L O R I D A C H A R T S

Institute for Economic Competitiveness 23

171615141312111009080706050403020100

190.0

180.0

170.0

160.0

150.0

140.0

130.0

120.0

Florida Information Employment(Thousands)

171615141312111009080706050403020100

1150.0

1100.01050.01000.0

950.0900.0

850.0800.0

Florida Leisure & Hospitality Employment

(Thousands)

F L O R I D A C H A R T S

24 Florida & Metro Forecast - December 2014

171615141312111009080706050403020100

500.0

450.0

400.0

350.0

300.0

250.0

Florida Manufacturing Employment(Thousands)

171615141312111009080706050403020100

30%20%10%0%

-10%-20%-30%-40%-50%

New Passenger Car & LightTruck Registrations

(% change year ago)

F L O R I D A C H A R T S

Institute for Economic Competitiveness 25

171615141312111009080706050403020100

8400.08200.08000.07800.07600.07400.07200.07000.06800.0

Florida Employment(Thousands)

Wage & Salary Employment

171615141312111009080706050403020100

12%

9%

6%

3%

0%

-3%

-6%

-9%

Florida Personal Income(% change year ago)

F L O R I D A C H A R T S

26 Florida & Metro Forecast - December 2014

171615141312111009080706050403020100

21000.0

20000.0

19000.0

18000.0

17000.0

16000.0

15000.0

Florida Population(Thousands)

171615141312111009080706050403020100

1300.0

1200.0

1100.0

1000.0

900.0

800.0

Florida Professional & Business Services Employment

(Thousands)

171615141312111009080706050403020100

10%

5%

0%

-5%

-10%

Florida Real Gross State Product(% change year ago)

F L O R I D A C H A R T S

Institute for Economic Competitiveness 27

171615141312111009080706050403020100

1050.0

1000.0

950.0

900.0

850.0

Florida State & Local Government Employment

(Thousands)

171615141312111009080706050403020100

1700.0

1650.0

1600.0

1550.0

1500.0

1450.0

Florida Trade, Transportation & Utilities Employment

(Thousands)

171615141312111009080706050403020100

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

Florida Unemployment Rate(percent)

Unemployment Rate

F L O R I D A N E W S S U M M A R I E S

28 Florida & Metro Forecast - December 2014

2014-15 forecast Citrus Season Shapes Up Favorably• Orange growers will see the farm price for oranges rise during

this season, however orange juice consumers may see prices fall and level out, according to Marisa Zansler, chief economist at the Florida Department of Citrus, who was present at a meeting with the Florida Citrus Commission.

• Zansler states that there may be an issue in the fact that the increases in revenue will be neutralized with higher costs. This may be made more apparent due to the high cost of combating this bacterial disease called Citrus Greening.

• For the current outlook of this season, a slowdown of the decline in U.S. retail orange juice sales may become more probable but still total sales will drop for the 13th time in the past 14 seasons.

• Polk County leads the state’s citrus producing counties with 81,810 grove acres and 10 million trees from the start of this current season, according to U.S. Department of Agriculture data. Orange growers should also see an increase of 10.5 percent in the farm price for their oranges harvested from October to March.

Source: The Ledger, October 23, 2014

Record number of tourists keep flocking to Florida• It was announced by Gov. Rick Scott that nearly 24 million

tourists visited the state of Florida during the third quarter of 2014. That is a 3.5 percent increase over the same time period a year ago.

• Visit Florida, reported that the record number of 23.7 million visitors includes 2.9 million foreigners and more than 500,000 Canadians.

• Gov. Rick Scott believes that an increase in spending by around $74 million on Visit Florida advertising will aid in boosting the state’s tourism industry.

• Almost 95 million people traveled to Florida for visits last year. Visit Florida estimated that nearly 74 million have passed the state through the end of September.

Source: Naples Daily News, November 20, 2014

Unemployment in Florida dips to lowest rate since June 2008• Data from the Florida Department of Economic Opportunity

shows that Florida’s unemployment rate reached around 6 percent for the first time since June 2008.

• Workforce data shows, 34,000 workers joined the workforce in Florida, in the last month.

• In regards to the Orlando metro area, unemployment dipped to 5.4 percent from 6.2 percent a year ago.

• The Orlando metro area’s four counties saw improvements of 0.7 percent to 0.9 percent year-over-year. Orange County’s unemployment rate improved to 5.4 percent from 6.2 percent, Osceola’s to 6.1 percent from 7 percent, Lake’s to 6 percent from 6.8 percent and Seminole’s to 5.0 percent from 5.7 percent. Each county has only made a slight progression—less than half a percentage point from the September’s figures.

Source: Orlando sentinel, November 21, 2014

Visit Florida offers $2.5M in grants for medical tourism• The marketing organization for the state of Florida, Visit

Florida, publicized the creation of a $2.5 million grant program to encourage medical tourism.

• Medical tourism is the trend by which individuals travel to a state for treatment, surgeries, and recovery. The program will be financed by the state legislature. In addition, some of the money will be used to promote Florida as a destination for medical conferences and training.

• Visit Florida President and CEO, Will Seccombe, hopes that the establishment of these grants is a tremendous first step in the process of highlighting Florida as a destination for top class doctors and facilities.

Source: Sun Sentinel, November 11, 2014

Florida PBS unveils free digital learning platform• Florida PBS was given $1 million out of the education budget,

for licensure and customization of digital learning content to meet Florida requirements.

• The features of platform include 87,000 learning objects that have been compiled and put together from PBS’s nonprofit association of public radio and television stations into relevant content that is searchable by grade level and topic. Florida PBS will look to increase that number from 87,000 to 100,000 this year.

• Florida PBS Learning Media will make sure that it is a safe and user-friendly place for students to enhance their learning online. For the parents who are worried about their students getting homework help in hazardous corners of the Internet, Florida PBS makes exceptional content available on this safe platform.

Source: Panama City News Herald, December 4, 2014

Florida’s sale of lux homes takes a twist in 2014• The sale of homes priced at $1 million or more has been on the

increase, however the increase in volume may be a cautionary sign that growth of sales are declining.

• A report from the Seattle-based Redfin, a real estate search and brokerage service, shows Florida’s third quarter sales of high-end homes measured 1,004, up 6 percent from 2013 and 115 percent from the same time in 2011.

• However this is a fall in growth from 2013, which saw a sharp 34 percent hike in million-dollar homes compared to to the previous year. Redfin’s study looked at 33 Florida regions, including some in Palm Beach County such as Palm Beach and Boca Raton.

• As a result, Redfin found that million-dollar-plus home sales were up a solid 9 percent in the third quarter compared to 2013, definitely outperforming the overall market, which saw a 1.2 percent decrease during the same time period.

Source: Palm Beach Post, December 5, 2014

F L O R I D A F O R E C A S T D e c e m b e r 2 0 14

ME

TR

OS

30 Florida & Metro Forecast - December 2014

D E LT O N A – D AY T O N A B E A C H – O R M O N D B E A C H

O U T L O O K S U M M A R I E SThe Deltona–Daytona–Ormond Beach Metropolitan

Statistical Area (MSA) is expected to show low levels of growth in most of the economic indicators measured in this forecast. Personal income is expected to average 4.6 percent growth, while the real per capita income level will average $34,000. Average annual wage will be the lowest level of the studied areas at $41,300. Average annual wage growth is expected to be moderate at 3.4 percent. Population growth will average 1.2 percent. Gross Metro Product will be at an average level of 13,020.19 million dollars.

The employment growth rate is expected to average 1.7 percent each year. Unemployment will average 6.2 percent.

The Deltona MSA will experience the most growth in the Construction and Mining sector, with an average growth rate of 8.1 percent annually. The Professional and Business Services sector will see the second highest average growth in the Deltona MSA at 4.8 percent annually. The Other Services sector follows with an average annual growth rate of 2.6 percent. The Information sector and Federal Government sector are the only sectors expected to experience declines, both at -0.5 percent.

M E T R O N E W S S U M M A R I E SDaytona airport eyes expansion; airline recruiting ongoing

• Daytona Beach International Airport has only had three of six boarding gates in use (by Delta and US Airways) since mid-2008 when two airlines pulled out during the Great Recession.

• Airport officials have continuously worked to recruit airlines and have proceeded with $65 million in capital improvement projects for the airport since 2006. Officials believe three hotels planned for the Daytona Beach area and larger events at the Ocean Center will drive new passenger growth.

• There is an additional $37 million in anticipated projects for the airport through 2018 including a commission to study the best use of 450 acres of

P R O F I L E SThe Deltona–Daytona–Ormond Beach MSA is

comprised only of Volusia County. It is located on the east coast of Florida and is notable for special events that occur throughout the year such as Bike Week. It is home to NASCAR headquarters and the Daytona International Speedway which hosts popular races such as the Daytona 500.

QUICK FACTS:• Population estimate of 600,756 as of July 1, 2013

census (U.S. Census Bureau).• Civilian labor force of 258,685 in October 2014

(Florida Research and Economic Database).• An unemployment rate of 5.7% as of October

2014, not seasonally adjusted. This amounts to 14,786 unemployed people (Florida Research and Economic Database).

TOP AREA EMPLOYERS:

• Volusia County Schools – 7,503• Halifax Health – 4,709• Florida Hospital Volusia-Flagler Market – 3,256• County of Volusia – 3,341• Daytona State College – 1,568• Embry-Riddle Aeronautical University – 1,423• Florida Health Care Plans, Inc. – 916• Frontier Communications – 800• Department of Transportation – 700• Bert Fish Medical Center – 700

Source: Volusia County Department of Economic Development and Enterprise Florida

Institute for Economic Competitiveness 31

D E LT O N A – D AY T O N A B E A C H – O R M O N D B E A C H

undeveloped property the airport could use for an expansion.

Source: Daytona Beach News-Journal, November 23, 2014

3,400-home project could create 1,900 jobs, developer’s study finds

• An economic impact report commissioned by project developer Minto Communities Florida suggests that their proposed 3,400-home gated Tomoka Community could generate $17 million in annual property taxes and create 1,900 permanent jobs.

• The community, which would be located just west of Interstate 95, would include a commercial center that could give the area a grocery store. The developer expects to spend $846 million to build the community in phases over a 15-year timeline.

• Minto Communities Florida is seeking a rezone and change of permissible land from the city for the 1600-acre development site.

Source: Daytona Beach News-Journal, November 22, 2014

Flagler tourism efforts ending year on high note• With renewed group business and many new athletic

events and conferences interest in coming to Flagler, Matt Dunn, Vice President of Tourism Development for the Flagler County Chamber of Commerce, said 2015 will be another busy year for the county.

• Dunn believes that 2015 will bring increases across the board for the county, including a significant increase in monthly bed-tax collections throughout the calendar year.

• The continued economic strength of Canada and the United Kingdom has brought a significant number of international visitors to the county.

Source: Daytona Beach News-Journal, November 23, 2014

US Foods Port Orange Division wins $312.6M contract with U.S. Navy

• The Navy awarded the national food services provider’s Port Orange division with a two-year contract to feed Navy personnel at Florida bases.

• Local business leaders say the contract is likely the largest ever awarded to a company in the Volusia-Flagler area. The contract will run through Oct 9, 2016 with options to be renewed for three more years.

• US Foods spokeswoman Lisa Lecas believes the contract will result in additional local jobs for the company, which currently employs 550 workers at its 409,000-square-foot Port Orange distribution center.

Source: Daytona Beach News-Journal, October 22, 2014

New York manufacturer Skyo Industries to open Ormond plant early next year

• City Commission unanimously approved the city’s $35,000 portion of an economic incentive package to offset New York-based hand tool manufacturer Skyo Industries’ relocation costs to Ormond Beach Aiport Business Park.

• Syko President Warren Anderson expects the plant to open in March, and is still waiting on official approval from the Florida Department of Economic Opportunity for the state’s portion of the $175,000 performance-based incentive package for creating new jobs.

• The job-creation incentive will only be received if the company meets its goal of creating 35 jobs within three years that pay an average of $42,600 a year.

Source: Daytona Beach News-Journal, December 3, 2014

32 Florida & Metro Forecast - December 2014

D E LT O N A – D AY T O N A B E A C H – O R M O N D B E A C H

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Total Nonagricultural Employment

Total Private

Goods Producing

Service Producing

Private Service Providing

Mining, Logging, and Construction

Manufacturing

Trade, Transportation, and Utilities

Wholesale Trade

Retail Trade

Transportation, Warehousing and Utilities

Information

Financial Activities

Professional and Business Services

Educational and Health Services

Leisure and Hospitality

Other Services

Government

Deltona - Daytona Beach - Ormond Beach MSA

Industry Location Quotients

171615141312111009080706050403020100

175.0170.0165.0160.0155.0150.0145.0140.0

Deltona-Daytona Beach Payroll Employment

(Thousands)

Deltona Payroll Employment

171615141312111009080706050403020100

14000.0

13500.0

13000.012500.0

12000.0

11500.0

11000.0

Deltona-Daytona BeachReal Gross Metro Product

(Millions 2000 $)

Real Gross Metro Product

171615141312111009080706050403020100

8.0%6.0%4.0%2.0%0.0%

-2.0%-4.0%-6.0%-8.0%

-10.0%

Deltona-Daytona BeachReal Personal Income

(percent change year ago)

Real Personal Income

171615141312111009080706050403020100

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

Florida & Deltona-Daytona BeachUnemployment Rate

(percent)

FL Unemployment RateDeltona Unemployment Rate

Institute for Economic Competitiveness 33

D E LT O N A – D AY T O N A B E A C H – O R M O N D B E A C H

Annual Outlook for Deltona-Daytona Beach-Ormond Beach, FL December 2014

2009 2010 2011 2012 2013 2014 2015 2016 2017Personal Income (Billions $)Total Personal Income 15.6 16.1 16.6 17.1 17.4 18.2 18.9 19.8 20.9 Pct Chg Year Ago -5.5 3.8 2.7 3.3 1.7 4.2 4.1 4.8 5.5 Wages and Salaries 5.6 5.7 5.7 5.9 6.0 6.3 6.7 7.0 7.4 Nonwage Income 10.0 10.5 10.9 11.2 11.4 11.8 12.2 12.8 13.5Real Personal Income (05$) 15.6 15.9 15.9 16.2 16.2 16.7 17.2 17.8 18.5 Pct Chg Year Ago -5.4 2.1 0.3 1.4 0.5 2.8 3.0 3.4 3.9Per Capita Income (Ths) 31.4 32.6 33.5 34.4 34.7 35.9 37.0 38.2 39.8Real Per Capita Income (05$) 31.4 32.1 32.2 32.5 32.4 33.0 33.6 34.3 35.1Average Annual Wage (Ths) 35.7 36.5 36.7 37.7 38.1 39.3 40.4 41.9 43.5 Pct Chg Year Ago -0.7 2.5 0.3 2.9 1.0 3.1 2.9 3.5 4.0Establishment Employment (Place of Work, Thousands, SA)Total Employment 156.3 153.6 154.2 155.3 157.2 160.2 163.5 166.1 168.3 Pct Chg Year Ago -5.8 -1.7 0.4 0.7 1.3 1.9 2.1 1.6 1.3Manufacturing 7.8 7.5 8.1 8.4 9.0 9.4 9.5 9.4 9.4 Pct Chg Year Ago -14.0 -3.9 8.5 3.4 6.9 4.4 0.7 -0.6 -0.5Nonmanufacturing 148.4 146.0 146.0 146.9 148.2 150.8 154.0 156.7 159.0 Pct Chg Year Ago -5.3 -1.6 0.0 0.6 0.9 1.7 2.1 1.7 1.4 Construction & Mining 8.9 7.9 7.4 7.6 8.2 8.5 9.3 10.2 11.1 Pct Chg Year Ago -22.0 -11.6 -6.3 2.6 7.6 4.7 8.5 10.2 8.9 Trade, Trans, & Utilities 30.1 30.0 30.0 30.2 30.0 30.0 30.4 30.5 30.6 Pct Chg Year Ago -7.3 -0.5 0.2 0.6 -0.5 0.1 1.0 0.5 0.3 Wholesale Trade 4.9 4.7 4.8 4.7 4.3 4.2 4.3 4.4 4.5 Retail Trade 23.2 23.3 23.4 23.6 23.7 23.9 24.0 24.0 23.7 Trans, Wrhsng, & Util 2.1 1.9 1.8 1.9 2.0 2.0 2.0 2.0 2.1 Information 2.3 2.0 2.0 2.0 1.8 1.7 1.7 1.8 1.8 Pct Chg Year Ago -11.9 -10.9 -1.6 -1.3 -7.6 -5.4 0.0 2.3 0.9 Financial Activities 7.1 7.2 7.3 7.6 7.7 7.7 7.7 7.7 7.7 Pct Chg Year Ago -7.8 0.7 2.2 3.9 1.2 -0.1 0.6 0.2 -0.2 Prof & Business Services 16.0 15.4 15.7 16.3 17.2 18.6 19.5 20.2 20.7 Pct Chg Year Ago 0.2 -3.3 1.6 4.0 5.3 8.4 4.7 3.6 2.4 Educ & Health Services 31.5 31.7 32.3 32.3 32.7 32.7 33.4 33.9 34.3 Pct Chg Year Ago -1.2 0.6 1.9 0.2 1.3 0.0 2.0 1.6 1.2 Leisure & Hospitality 21.6 21.5 22.1 22.7 23.1 23.7 24.1 24.3 24.4 Pct Chg Year Ago -5.7 -0.4 2.9 2.4 1.8 2.6 1.9 0.5 0.4 Other Services 8.2 7.9 7.4 7.4 7.4 7.7 7.9 8.0 8.1 Pct Chg Year Ago 2.6 -3.7 -6.3 -0.8 -0.1 4.7 3.0 1.3 1.1 Federal Government 1.4 1.5 1.3 1.1 1.1 1.1 1.1 1.1 1.1 Pct Chg Year Ago 2.3 5.8 -15.9 -11.1 -3.0 0.3 -0.3 -0.9 -0.9 State & Local Government 21.3 20.9 20.5 19.7 19.1 19.0 18.9 19.0 19.2 Pct Chg Year Ago -4.9 -1.7 -2.0 -3.9 -3.3 -0.6 -0.3 0.5 1.0Other Economic IndicatorsPopulation (Ths) 495.1 495.5 494.9 497.5 501.4 505.7 510.8 517.8 525.2 Pct Chg Year Ago -0.4 0.1 -0.1 0.5 0.8 0.9 1.0 1.4 1.4Labor Force (Ths) 252.4 252.0 252.1 252.1 251.8 256.0 263.0 269.8 275.9 Pct Chg Year Ago -0.8 -0.2 0.0 0.0 -0.1 1.7 2.7 2.6 2.2Unemployment Rate (%) 10.6 11.5 10.6 8.9 7.3 6.1 6.0 6.4 6.6Total Housing Starts 662.5 718.0 1021.9 766.1 1432.9 1596.7 2963.2 3533.8 3914.3 Single-Family 602.3 658.9 504.7 749.0 1220.2 1335.4 1898.5 2444.0 2930.3 Multifamily 60 59 517 17 213 261 1065 1090 984

34 Florida & Metro Forecast - December 2014

D E LT O N A – D AY T O N A B E A C H – O R M O N D B E A C H

Quarterly Outlook for Deltona-Daytona Beach-Ormond Beach, FL December 2014

2014Q4 2015Q1 2015Q2 2015Q3 2015Q4 2016Q1 2016Q2 2016Q3 2016Q4 2017Q1 2017Q2 2017Q3 2017Q4

Personal Income (Billions $)Total Personal Income 18.4 18.6 18.8 19 19.2 19.4 19.7 19.9 20.2 20.5 20.8 21 21.3 Pct Chg Year Ago 4.7 4.7 3.9 3.8 4 4.2 4.6 5 5.3 5.5 5.7 5.6 5.4 Wages and Salaries 6.4 6.5 6.6 6.7 6.8 6.9 6.9 7 7.1 7.2 7.3 7.4 7.5 Nonwage Income 12 12.1 12.2 12.3 12.4 12.6 12.7 12.9 13.1 13.3 13.4 13.6 13.8Real Personal Income (05$) 16.9 17 17.1 17.2 17.3 17.5 17.7 17.8 18 18.2 18.4 18.5 18.7 Pct Chg Year Ago 3.4 3.5 2.9 2.7 2.7 2.8 3.2 3.7 3.9 4 4 3.9 3.7Per Capita Income (Ths) 36.3 36.7 36.9 37.1 37.4 37.7 38 38.4 38.8 39.2 39.6 40 40.3Real Per Capita Income (05$) 33.3 33.5 33.6 33.6 33.8 34 34.2 34.4 34.6 34.9 35.1 35.2 35.4Average Annual Wage (Ths) 39.7 40 40.3 40.6 40.9 41.3 41.7 42.1 42.5 42.9 43.3 43.8 44.2 Pct Chg Year Ago 3.9 3 2.7 2.9 3.1 3.3 3.5 3.7 3.7 3.9 3.9 4 4.1

Establishment Employment (Place of Work, Thousands, SA)Total Employment 161.3 162.2 163.2 164 164.5 165.2 165.7 166.5 167.2 167.6 168.2 168.6 169 Pct Chg Year Ago 1.5 2 1.9 2.3 2 1.8 1.6 1.5 1.6 1.5 1.5 1.3 1.1Manufacturing 9.4 9.4 9.5 9.5 9.5 9.4 9.4 9.4 9.4 9.4 9.4 9.4 9.3 Pct Chg Year Ago 2.5 1 0.2 1 0.5 0.1 -0.5 -0.7 -1 -0.8 -0.4 -0.4 -0.4Nonmanufacturing 151.9 152.8 153.7 154.5 155.1 155.7 156.3 157 157.8 158.2 158.8 159.2 159.6 Pct Chg Year Ago 1.5 2.1 2 2.3 2.1 1.9 1.7 1.6 1.7 1.6 1.6 1.4 1.2 Construction & Mining 8.8 9 9.2 9.4 9.6 9.8 10.1 10.4 10.6 10.9 11 11.2 11.4 Pct Chg Year Ago 5 6.4 7.8 10.3 9.6 9.6 10 10.4 10.7 10.7 9.6 8.2 7.2 Trade, Trans, & Utilities 30.1 30.2 30.3 30.4 30.5 30.5 30.5 30.5 30.5 30.5 30.6 30.6 30.7 Pct Chg Year Ago -0.8 0.3 0.7 1.8 1.3 0.9 0.5 0.2 0.2 0.2 0.3 0.4 0.4 Wholesale Trade 4.2 4.2 4.3 4.3 4.3 4.3 4.4 4.4 4.4 4.5 4.5 4.5 4.6 Retail Trade 23.9 24 24 24.1 24.1 24 24 23.9 23.9 23.8 23.8 23.7 23.7 Trans, Wrhsng, & Util 1.9 1.9 1.9 2 2 2 2 2 2 2.1 2.1 2.1 2.1 Information 1.7 1.7 1.7 1.7 1.7 1.7 1.8 1.8 1.8 1.8 1.8 1.8 1.8 Pct Chg Year Ago -3.8 -1.1 -0.8 1.6 0.3 -1.2 2.5 4.2 3.7 3.6 1.1 -0.6 -0.2 Financial Activities 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 7.7 Pct Chg Year Ago -0.2 0.2 0.5 0.9 0.7 0.5 0.3 0 0.1 0.1 0 -0.2 -0.8 Prof & Business Services 18.9 19.1 19.4 19.6 19.8 20 20.1 20.3 20.5 20.6 20.7 20.7 20.8 Pct Chg Year Ago 6.3 5.1 4.7 4.3 4.6 4.3 3.6 3.3 3.2 3.1 3 2.2 1.5 Educ & Health Services 33 33.1 33.4 33.5 33.5 33.6 33.9 34 34.2 34.2 34.3 34.4 34.4 Pct Chg Year Ago 1.1 2.8 1.8 1.9 1.6 1.5 1.3 1.5 2 1.7 1.4 1.1 0.6 Leisure & Hospitality 23.9 24 24.1 24.2 24.2 24.3 24.2 24.2 24.2 24.3 24.3 24.4 24.5 Pct Chg Year Ago 1.3 1.7 2.5 1.8 1.5 1.1 0.6 0.2 0 -0.2 0.3 0.7 1 Other Services 7.9 7.9 7.9 7.9 8 8 8 8.1 8.1 8.1 8.1 8.1 8.2 Pct Chg Year Ago 5.6 5.1 4.2 1.5 1.5 1.2 1.3 1.3 1.5 1.4 1.2 1.1 0.9 Federal Government 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 Pct Chg Year Ago 0.7 0.3 -1 0 -0.6 -0.7 -0.9 -1 -1 -0.9 -0.8 -0.9 -1 State & Local Government 18.9 18.9 18.9 18.9 18.9 18.9 19 19 19 19.1 19.1 19.2 19.3 Pct Chg Year Ago -0.7 -0.7 -1.2 0.3 0.3 0.3 0.4 0.6 0.6 0.8 0.9 1 1.2

Other Economic IndicatorsPopulation (Ths) 507.3 508.5 509.9 511.5 513.2 515 516.8 518.7 520.7 522.5 524.3 526.1 527.9 Pct Chg Year Ago 0.8 0.9 0.9 1.1 1.2 1.3 1.4 1.4 1.5 1.5 1.4 1.4 1.4Labor Force (Ths) 257.7 260 262.2 264.1 265.8 267.4 269 270.6 272.2 273.7 275.2 276.6 277.9 Pct Chg Year Ago 2.3 2.3 2.3 3.1 3.1 2.8 2.6 2.5 2.4 2.4 2.3 2.2 2.1Unemployment Rate (%) 5.8 5.9 5.9 5.9 6.1 6.2 6.3 6.4 6.5 6.6 6.6 6.6 6.6Total Housing Starts 2010 2453 2861 3174 3365 3489 3461 3451 3734 3852 3885 3956 3964 Single-Family 1416 1649 1826 2017 2102 2212 2321 2499 2743 2858 2921 2967 2975 Multifamily 594 804 1035 1157 1263 1277 1140 952 990 994 964 989 990

Institute for Economic Competitiveness 35

G A I N E S V I L L E

O U T L O O K S U M M A R I E SThe Gainesville Metropolitan Statistical Area (MSA)

is expected to show low levels of growth in most of the economic indicators. Personal income growth will see an average of 4.3 percent growth, the second lowest of the studied MSAs. Real per capita income level is expected to average $37,400. Average annual wage growth is expected to be 3.6 percent, the second highest of the twelve studied MSAs, while the average annual wage level will be at $46,000. Population growth will average the lowest of the studied areas at 0.8 percent annually. Gross Metro Product will be the second lowest of the studied MSAs at an average level of 10,250.72 million dollars.

Gainesville will see an average employment growth rate of 1.1 percent annually, the lowest growth of the MSAs. The Gainesville MSA will, however, maintain the lowest average unemployment rate of the twelve studied, at 4.7 percent.

The fastest growing sector in the area will be the Construction and Mining sector, with an average growth rate of 5.5 percent annually. This is followed by the Professional and Business Services sector with an average annual growth rate of 2.7 percent. The Information, Financial Activities, and Federal Government sectors will experience declines, with average annual growth rates of -0.3, -0.3, and -1.7 percent, respectively.

M E T R O N E W S S U M M A R I E S Gainesville Dojo’s former location to be demolished to make way for office building

• Soon the location previously filled by the Gainesville Dojo will be demolished in order to accommodate the construction of a two-story, 15,000-square-foot office building being developed by Trimark Properties.

• The demolition and construction is planned for early 2015 and is expected to be completed in late 2015. The new Nimbus building will be geared towards office and research uses.

• The new plan involves converting Fifth Terrance to a one-way South-flowing street with angled on-street parking.

P R O F I L E SThe Gainesville MSA is comprised of Alachua and

Gilchrist Counties and is located in the central-north portion of the state. This Metro is home to the University of Florida and the Florida Museum of Natural History, Florida’s official natural history museum.

QUICK FACTS:• Metro population estimate of 270,382 as of July 1,

2013 (U.S. Census Bureau).• Alachua County population estimate of 253,451

as of July 1, 2013 (U.S. Census Bureau).• Gilchrist County population estimate of 16,931 as

of July 1, 2013 (U.S. Census Bureau).• Civilian labor force of 144,979 in October 2014

(Florida Research and Economic Database).• An unemployment rate of 4.7% as of October

2014, not seasonally adjusted. This amounts to 6,764 unemployed people (Florida Research and Economic Database).