Embed Size (px)

Citation preview

W H AT ’ S I N S I D E

3 Covering the CapitalStructure: The Seller Note

5 GUEST COLUMN

Trends in Private Equity in Africa:Increased Commitmentsand Integration of (ESG)Factors in 2012

7 Brick by Brick: A Primer for DueDiligence in Each BRICCountry, Continuing withBrazil

9 What Are the Options?Bank Investment inUnaffiliated Private Equityand Hedge Funds Underthe Volcker Rule

11 Buyer Beware (Delaware Law Edition): Sometimes “SubstantiallyAll” Isn’t All That Much

13 Discount Shopping:Making the Most Out ofDistressed Asset Sales

15 Buyer Beware (Employee Edition): Employee BenefitCovenants Could HaveUnintended Consequenceson ERISA Plans

Fall 2011 Volume 12 Number 1

D e b e v o i s e & P l i m p t o nP r i v a t e E q u i t y Re p o r t

Del Monte:Staple Remover?

“Can't we just get along?"

The attention of the private equitycommunity was captured by both theDelaware Court of Chancery’s injunctiondelaying KKR’s acquisition of Del Monteover issues related in part to the sell-sidefinancial advisor’s participation in thebuyers’ financing, and the subsequentapproval of an $89.4 million settlement ofthe underlying litigation. While it isdifficult to come to a definitive view sincethe period following Del Monte coincidedwith a downturn in M&A activity, DelMonte appears to have led to a meaningfuldecrease in “stapled financings” (so calledbecause the financing offer is coupledwith—or “stapled” to—sales materialscirculated by the sell-side advisor) in sales ofpublic companies.While the potential conflicts require

careful monitoring, many sophisticatedsellers have concluded over the years thatthe advantages of stapledfinancings are substantial andthe risks manageable. Is DelMonte an asteroid that hasrendered the staple extinct?In the case of private targets,

certainly not, and, even in the case ofpublic targets, we think not. As ViceChancellor Laster noted in his Del Monteinjunction decision, the fundamentalproblem was not the Del Monte board’sdecision to permit the sell-side advisor toparticipate in the buyer’s financing but theabsence of “some justification reasonablyrelated to advancing stockholder interests...” Here are the key factors to consider as

you contemplate participation by sell-sideadvisors in buy-side financings, includinghow to structure a staple in ways thatshould mitigate litigation risk.

Why Offer a Staple?One key lesson from Del Monte is that aboard must be fully informed about thereasons for allowing a sell-side advisor to

participate in buy-side financing, includingby way of a staple. Whether the potential

advantages exist, and to whatdegree, will vary from deal todeal. A staple can be beneficialto a seller by providing aprice signaling device to

CONTINUED ON PAGE 17

© 2

011

Mar

c Ty

ler

Nob

lem

an /

ww

w.m

tnca

rtoo

ns.c

om

In tumultuous economic times, creativity is a key ingredient in the

deal recipe book. The articles in our current issue provide guidance

on how to manage the risks and rewards inherent in creative

structures and financings.

Stapled financings, once a “staple” in auctions of public companies,

are less common these days, not only because the public deals are rare

in the current market, but also as a result of reaction to the Delaware

Chancery Court’s injunction in connection with the acquisition of Del

Monte. Heightened judicial scrutiny of transactions with potential

conflicts of interest has made sellers wary not only of stapled financing,

but also of even permitting sell side advisors to participate in buy-side

financing. Especially in light of the decreasing number of financing

sources for larger transactions and their more limited appetites, sellers

who are at all open minded about permitting sell side advisors to

participate in buy side financing will be interested in the structuring

guidance we offer in our cover article on how to mitigate the potential

litigation risks of doing so.

Seller financing has always been a “staple” of mid market deals,

but never has it been more useful that when the financing markets

are difficult and valuations are uncertain. In this issue, we provide a

primer on the major issues to be considered in structuring seller

notes and their role in the capital structure.

The private equity world remains concerned about the

interpretation of the Volcker Rule during what seems like a never-

ending process of finalizing the implementing rules. In this issue we

continue our discussion of how and to what extent “banking

entities” will be allowed to invest in unaffiliated private equity and

hedge funds and provide an updated "cheat sheet" of the current

state of the Volcker Rule and its proposed implementing rules.

Elsewhere in this issue, we focus on a number of topics which

highlight the global nature of the private equity asset class. We

continue our around the world survey of the BRIC countries with an

examination of the due diligence climate in Brazil. While the Brazilian

deal community is familiar with the due diligence process and is ahead

of some other BRICs in its accounting standards, record keeping and

public search functions, it faces challenges similar to the others in some

areas, particularly with respect to corruption issues.

Private equity investors are beginning to look beyond the BRIC

countries. Over the last decade, over $10 billion of private equity

financing has been raised for investment in sub-Saharan Africa. In

our Guest Column, Graham Sinclair, a Principal of SinCo and

President of the Africa Sustainable Investment Forum, discusses the

requirement to integrate so-called ESG (environmental, social and

governance) factors into African investments, as well as recent

changes to local regulations allowing African pension funds to

increase allocations to private equity investment.

Given the economic climate, we also feature an article that

reviews the process that will permit private equity firms to participate

in auctions for assets being sold as part of a pre-packaged bankruptcy.

We hope you continue to find the Private Equity Report timely

and helpful reading. If there are specific questions or topics you

would like us to focus on in future issues, please feel free to let any

of us in the Private Equity Group know.

The Debevoise & PlimptonPrivate Equity Report is apublication of

Debevoise & Plimpton LLP919 Third AvenueNew York, New York 100221 212 909 6000

www.debevoise.com

Washington, D.C.1 202 383 8000

London44 20 7786 9000

Paris33 1 40 73 12 12

Frankfurt49 69 2097 5000

Moscow7 495 956 3858

Hong Kong852 2160 9800

Shanghai86 21 5047 1800

Private Equity Partner /Counsel Practice Group MembersFranci J. Blassberg Editor-in-Chief

Stephen R. Hertz Kevin A. RinkerAssociate Editors

Ann Heilman MurphyManaging Editor

David H. Schnabel Cartoon Editor

Please address inquiriesregarding topics covered in thispublication to the authors orany other member of thePractice Group.

All contents ©2011 Debevoise& Plimpton LLP. All rightsreserved.

The Private Equity Practice GroupAll lawyers based in New York, except where noted.

Private Equity FundsMarwan Al-Turki – LondonKenneth J. Berman– Washington,D.C.Erica BerthouJennifer J. BurleighWoodrow W. Campbell, Jr.Sherri G. CaplanJane EngelhardtMichael P. HarrellDavid Innes – LondonGeoffrey Kittredge – London Marcia L. MacHarg – FrankfurtAnthony McWhirter – LondonJordan C. Murray Andrew M. Ostrognai – Hong Kong Richard D. Robinson, Jr.David J. SchwartzRebecca F. Silberstein

Hedge FundsByungkwon LimGary E. Murphy

Mergers & AcquisitionsAndrew L. BabE. Raman Bet-Mansour – LondonPaul S. BirdFranci J. BlassbergColin Bogie – LondonRichard D. BohmThomas M. Britt III – Hong KongGeoffrey P. Burgess – LondonMargaret A. DavenportE. Drew Dutton – Hong Kong Michael J. GillespieGregory V. GoodingStephen R. HertzDavid Innes – LondonJames A. Kiernan III – LondonAntoine F. Kirry – ParisJonathan E. LevitskyGuy Lewin-Smith – London

Dmitri V. Nikiforov – MoscowRobert F. Quaintance, Jr.William D. RegnerKevin A. RinkerJeffrey J. RosenKevin M. SchmidtThomas Schürrle – FrankfurtWendy A. Semel – LondonAndrew L. SommerJames C. Swank – ParisJohn M. Vasily Peter Wand – FrankfurtNiping Wu – Shanghai

Leveraged FinanceKatherine Ashton – LondonWilliam B. BeekmanDavid A. BrittenhamPaul D. BrusiloffPierre Clermontel – Paris Alan J. Davies – LondonPeter Hockless – LondonAlan V. Kartashkin – Moscow

Letter from the Editor

Franci J. Blassberg

Editor-in-Chief

Classics are always in vogue. The “sellernote,” a payable issued by a buyer to a selleras part of the purchase price for anacquisition, is a classic accessory in the LBOensemble that tends to be most useful duringperiods of volatility in the capital markets andscarcity of debt capital. With the recent andongoing stormy weather in the capitalmarkets, and forecasts for more to come, dealprofessionals may wish to keep the seller notein mind for suitable occasions.

OverviewExtremely versatile, the seller note comes in avariety of sizes and can be tailored for avariety of purposes. For instance, a sellernote can patch a hole in a capital structure (aswhen a debt issue would be too small orotherwise unappealing for a third-partylender). It can even constitute a significantpiece in a capital structure (either as a bridgeto a better debt market or as a long-terminvestment). It can serve as acquisitioncurrency (as for a relatively small “tuck-in” bya leveraged company whose financingagreements permit acquisition debt). And,in many cases, it can enable a seller willing to

invest in an instrument supported by abusiness it knows well to attain a higherheadline valuation for its business.

Basic Patterns for a Seller NoteSeller notes follow many patterns, one of themost typical involving a transfer-restricted,subordinated note that is prepayable withoutpenalty, that requires only limited mandatorycash payments, and that imposes someaffirmative and negative covenants, often notextensive, on the buyer.Transfer restrictions exist in seller notes,

among other reasons, to keep the note withthe seller, which in turn facilitates purchaseprice adjustments and, in some cases, taxplanning (as discussed below), and supportsoff-sets of indemnification obligations. Sometransfers, to sellers’ families for example, maybe permitted without consent. When atransaction is designed to allow the seller torealize near-term liquidity, however, transferrestrictions may be more limited, confined tothose necessary to comply with securities lawsor to prevent acquisition by competitors.

Subordination is typically if notuniversally required by third-party lenders.

Subordination may be deep,requiring, for example, that there befew remedies, long “standstills”(periods during which the holder ofthe seller note cannot exercise anyremedies), and little or no cashpayments. In many cases, thesubordination will be “structural,”meaning that the holder of the sellernote has a claim for payment onlyagainst a holding company with noassets but stock of its operatingsubsidiaries, while the senior debthas a direct claim for paymentagainst the assets of such operatingsubsidiaries. (A structurallysubordinated note, without its owndirect claim on subsidiaries’ assets,

will not receive payment unless and until theholding company receives distributions (ifany) from those subsidiaries.)Prepayment is generally desirable to

holders of seller notes, and, therefore, theabsence of call protection is usually notcontroversial, unless a seller plans to marketthe notes to third-party investors who expectsuch protection.Reduced cash payments on a seller note

may not just be a result of subordinationprovisions imposed by senior lenders, butmay also be part of the economics of thetransaction, with the entire principal amountof the note due only at maturity and some orall of the interest payable by the accretion oforiginal issue discount (OID) or payablethrough the issuance of more notes (so called“pay-in-kind” or PIK interest).An absence of cash-pay requirements does

implicate a tax issue that perenniallyconfronts both the makers and holders of anyOID instrument. In general, the holder of aseller note must recognize interest incomecurrently, including interest that is notpayable in cash, resulting in “phantomincome” (i.e., income taxable to the holderprior to its receipt of cash). In addition,depending on the terms of a seller note, theremay be some risk that principal isrecharacterized as interest and treated asOID, to be taken into account as interestincome or expense annually, therebyaugmenting the amount of phantom income.These issues may be especially problematicfor individuals who might be selling a familybusiness.A buyer issuing a seller note will have its

own concerns about interest expense arisingfrom OID and PIK interest. (For taxpurposes, OID and PIK are treated as thesame.) The application of the “applicablehigh yield debt obligation” (AHYDO) rules

Covering the Capital Structure: The Seller Note

CONTINUED ON PAGE 4

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 3

Pierre Maugüé Margaret M. O’NeillNathan Parker – LondonA. David ReynoldsJeffrey E. RossPhilipp von Holst – Frankfurt

TaxJohn Forbes Anderson – LondonEric Bérengier – ParisAndrew N. BergPierre-Pascal Bruneau – ParisGary M. FriedmanPeter A. FurciFriedrich Hey – FrankfurtAdele M. KarigRafael KariyevVadim MahmoudovMatthew D. Saronson – LondonDavid H. SchnabelPeter F. G. SchuurRichard Ward – London

Trust & Estate PlanningJonathan J. RikoonCristine M. Sapers

Employee Compensation & BenefitsLawrence K. CagneyJonathan F. Lewis Alicia C. McCarthyElizabeth Pagel SerebranskyCharles E. Wachsstock

The articles appearing in thispublication provide summaryinformation only and are notintended as legal advice. Readersshould seek specific legal advicebefore taking any action withrespect to the matters discussed inthese articles. Any discussion ofU.S. Federal tax law contained inthese articles was not intended orwritten to be used, and it cannotbe used by any taxpayer, for thepurpose of avoiding penalties thatmay be imposed on the taxpayerunder U.S. Federal tax law.

page 4 l Debevoise & Plimpton Private Equity Report l Fall 2011

may prevent an issuer of the note (i.e., thebuyer) from deducting some of the non-cash interest accruals altogether and requiressuch a buyer to defer the deduction of therest of any interest not payable at leastannually in cash until actually paid in cash.It is often possible, however, to structure theterms of a note to avoid this loss anddeferral of valuable interest deductions, soany note that has significant OID and aterm of more than five years should bereviewed carefully for possible AHYDOconcerns and mitigants.Negotiation of the buyer’s obligations

under the seller note often focuses, amongother things, on the nature and extent ofrestrictions that the seller note may imposeon the buyer’s business. Seller notes ingeneral are typically less restrictive thanconcurrent third-party financings, as thethird-party financing both provides abenchmark and comes conditioned on theseller note having more flexibility than thethird-party debt.

VariationsBeyond these basic patterns, there arenumerous variations, including thefollowing.Adjustability. A seller note can be

structured to permit the principal to beincreased or decreased to implement anypurchase price adjustment, earn-out orindemnification obligation. Theseprovisions are typically found in private-to-private transactions, which, because of thelimited number of sellers involved, are thesort most susceptible to the use of a sellernote. An adjustability feature, while very

useful, can present a few additionalwrinkles. The adjustment is rarelyunilateral; therefore, an adjustable sellernote should provide a basis, such as mutualagreement or court judgment, fordefinitively establishing the increase ordecrease (similar to providing a basis for a

release from an escrow). An adjustable sellernote should also provide an end date,beyond which an adjustment can no longerbe made, such as the date the note matures,the date an equivalent escrow arrangementwould have terminated, or the date theindemnification obligations wouldterminate under the purchase agreement.The adjustability mechanisms will not workwell, if at all, if the note is held by a partyother than the seller, so this feature may bea key reason to defer cash payments (tokeep the note outstanding), impose transferrestrictions or even require the escrowing ofthe seller note. In addition, for thesemechanisms to work, any subordinationagreement, no matter how restrictiveotherwise, would have to permit any suchincrease or decrease; subordination thatwould in effect prohibit “all” changes to aseller note, for example, must at least havean exception to allow for these “non-cash”adjustments. Note that adjustments based on

earnings contingencies can raise questions asto whether the seller note should beclassified as equity for tax purposes, whichwould of course prevent interest deductionsentirely and could, if unanticipated, cause avariance to the buyer’s projections.Cash Payments.Mandatory cash interest

payments are not unusual, even thoughsome portion of the interest is often payablein kind. Amortization of principal in sellernotes is very rare. But sellers will sometimesseek mandatory prepayment triggered byspecific events. A refinancing of third-partydebt may be one such event, with the sellerarguing that a refinancing will mark the endof the need for the seller financing and thebuyer countering that capacity to refinancethird-party debt does not necessarily implya capacity to refinance the seller note. Achange of control may be another suchtrigger event, with the seller asserting that achange of control will mark the realizationof the buyer’s gains, the end of the buyer’s

investment, and, therefore, the end of theutility of the seller note as part of the capitalstructure or as a mechanism for adjustingamounts under the purchase agreement;while the buyer may counter that a changeof control may not represent an exit that iscomplete or even partial or that is otherwisesatisfactory. Belts & Suspenders for the Senior Debt.

The buyer proposing to issue a seller notemay be called upon to broker subordinationprovisions that will satisfy a senior lender,adding an extra layer of negotiation to thedeal. Lenders, in smaller deals, willoccasionally request subordination thatsellers and buyers may perceive to beunnecessary protection or extreme. Theseinclude, for example, that the seller notehave absolutely no cash interest orprepayment rights, no defaults, no remedyother than to sue for non-payment atmaturity, an extremely long remedy block,and/or extremely long-dated maturity.Indeed, even if a seller note is structurallysubordinated (i.e., having no recourse to thesenior lenders’ borrower), some lenders, insmaller transactions, may nonetheless stillask for the seller to submit to contractualsubordination.Disclosure. A seller will generally seek

information rights to monitor its ongoinginvestment in the buyer. How muchinformation is appropriate will benegotiated depending on the circumstances.A buyer may especially want to limit thatinformation for a seller with a short non-competition agreement. Seller notes willoften contain confidentiality provisions todeal with these issues, at least in part.Installment method. In some cases, a

seller may be permitted to elect to use the“installment method,” for U.S. federalincome tax purposes, to defer itsrecognition of gain (but not loss) on thesale, until it receives payments under the

Covering the Capital Structure: The Seller Note (cont. from page 3)

CONTINUED ON PAGE 19

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 5

Trends in Private Equity in Africa:Increased Commitments and Integration of (ESG) Factors in 2012

G U E S T C O L U M N

Led in part by private equity investment,sub-Saharan Africa is poised for significantgrowth in sustainable investment over thenext five years, according to a new studycommissioned by the InternationalFinance Corporation (IFC).1 That growthwill be led not just by private equity (PE)funds, but by demand from asset owners,and new regulations that, consistent withthe ethos of the continent, mandate theintegration of environmental, social andgovernance factors (colloquially known as“ESG”) in PE investments and also enablepension funds meaningfully to increaseallocations to PE investments.

Growth StoryAlthough Africa currently comprises onlya fraction of world investment markets, itis positioned for major growth. InDecember 2010, capitalization in Africaamounted to only one percent of globalmarket capitalization in the benchmarkMSCI Frontier Markets Index. However,the International Monetary Fund (IMF)projects the African economy will grow byfive percent in 2011 – up from 4.7percent in 2010. Private equity is growingrapidly in response to the region’simproving economic fundamentals. In thepast decade, PE funds have raised morethan $10 billion in the region and nowmanage an estimated $24 billion in Africa,with South Africa alone accounting for$14 billion.

According to the IFC study, 92 percentof PE investors interviewed expect anincrease in PE commitments in sub-Saharan Africa over the next five years andalmost two-thirds of those investors expectthe increase to be over 20 percent. Suchan increase is welcomed by thoseconcerned with sustainable investment inAfrica because PE funds have greaterexposure and experience in integratingESG factors in the region than theirgeneral asset management counterparts. Over the next three years, many PE

funds will be targeting health care,infrastructure, and housing in Africa. In2010, two agriculture-specific African PEfunds completed multimillion dollarfundraisings. In the next three toten years, PE investments are expected toflow into clean technology, alternativeenergy, and education. Infrastructure willalso remain a key investment focusthroughout the continent.

Asset Owners Demand ESG IntegrationBecause of the unique cultural sensibilitiesin a third-world region like Africa, successby investors on the continent will dependon their ability to demonstrate theircommitment to sustainable ESGinvestments. Historically, client mandates have

driven the integration of ESG factors inPE investment, especially wheredevelopment finance institutions (“DFIs”)are anchor investors in private equityfunds. Nearly half of all PE funds in sub-Saharan Africa have DFIs as investors. InSeptember 2011, 30 DFIs adopted theCorporate Governance DevelopmentFramework, a common set of guidelines

to support sustainable economicdevelopment in emerging markets.In addition, a large number of private

equity investors now consider ESG factorswhen selecting managers, which results inprivate equity managers focusing oncreating value in their portfolio companieswhile remaining sensitive to any ESGissues in their portfolios.The investment policies of South

Africa’s Government Employees PensionFund (“GEPF”), which is Africa’s largestinstitutional investor and among theworld’s 20 largest pension funds, is a largeinfluence on the market. GEPF recentlyadopted both a Responsible InvestmentPolicy, which calls for a portfolio-wideESG-integration approach, and aDevelopmental Investment Policy, whichallocates five percent of its assets (about$7 billion) to developmental investments.Because the GEPF has such a significantinfluence on the largest institutionalinvestment market in Africa, a policydecision by GEPF makes the rest of theindustry attentive to the sway of theUS$131 billion fund.

Regulation Increases FundsAvailable for PE andPromotes ESG IntegrationNew pension fund regulations acrossAfrica will both increase the possiblemarket for PE in Africa, making up toR100 billion ($14.5 billion) of newpension funds available for investmentinto private equity or hedge funds, andencourage the adoption of ESGintegration. In Namibia, new regulations will

increase the PE allocation limit from 2.5

CONTINUED ON PAGE 6

1 Sustainable Investment in Sub-Saharan AfricaI, (IFC-SinCo, July 2011). http://www.ifc.org/ifcext/sustainability.nsf/Content/Publications_Report_SI-SubSaharanAfrica. The IFC-commissioned study authored by SinCo,interviewed over 160 practitioners in privateequity and asset management in South Africa,Nigeria, and Kenya.

page 6 l Debevoise & Plimpton Private Equity Report l Fall 2011

to five percent in 2011. Similarly, in2011, Nigeria’s pension regulatorincreased the PE allocation ceiling to fivepercent, while Kenya’s Retirement BenefitAuthority increased the PE allocationlimit to ten percent. Historically, Kenyanand Nigerian pension funds have had littleappetite for PE, something that theregulators and PE industry are looking tochange with a series of workshops andeducation programs. As of 1 January 2012, all retirement

fund assets in South Africa will be subjectto a piece of enabling regulation thatspecifically promotes the importance ofESG considerations in sustainable long-term investment performance. Theregulation provides: “Prudent investingshould give appropriate consideration to anyfactor which may materially affect thesustainable long-term performance of theirinvestments, including those of anenvironmental, social, and governance

character.” 2

Voluntary codes also have a powerfulinfluence by nudging industryparticipants, especially those seeking to beleaders in their industry, and creatingreputation risks where institutionalinvestors fail to live up to theircommitments. Two ESG-related codesplay a role in industry self-regulation: forcompanies, the King Code for CorporateGovernance3 and for investors, the Codefor Responsible Investing by InstitutionalInvestors in South Africa (“CRISA”).4

Other soft rules like the Principles forResponsible Investment (“PRI”), and theExtractive Industries TransparencyInitiative are also raising the profile ofESG investment. Increasingly, the PRI,and CRISA, will be major drivers of ESGin investment as public commitments arecontrasted with practices in Africa, andthe clients of private equity managers, likepension funds, are subject to increasedscrutiny from their stakeholders.The particular importance of ESG

factors distinguish PE investment inAfrica from most other regions in theworld, and will continue to be a majorsource of attention and opportunity forprivate equity firms in Africa.

Graham SinclairPrincipal of SinCo and President of Africa SustainableInvestment Forum

Guest Column: Trends in Private Equity in Africa (cont. from page 5)

2 December 2, 2010 Government Notice (ForPublic Comment) Pension Funds Act, 24/1956:Publication of Amendment of Regulation 28 of theregulations made under Section 36.

3 See, http://www.iodsa.co.za/products_reports.asp?CatID=150. (First published in 1994 andupdated most recently in 2009, King III).

4 See, http://www.iodsa.co.za/downloads/documents/CRISACode31Augl2010_For_Public_Comment.pdf.

If you would like to take advantage ofthis service, indicate the delivery methodyou prefer and your email address. Pleasealso take this opportunity to update yourcontact information or to add additionalrecipients by copying and filling out thefollowing form and returning it to us.

I would like to receive my reports:

q via email

q via email and regular mail

q via regular mail

Name of Contact ________________________________________________________________________

Title __________________________________________________________________________________

Company Name ________________________________________________________________________

Address _______________________________________________________________________________

City ____________________________________ State or Province ___________ Postal Code __________

Country _________________________ E-mail Address _________________________________________

Telephone _________________________________ Direct Dial __________________________________

Fax ______________________________________ Direct Dial Fax _______________________________

Interested in receiving the Debevoise & Plimpton Private Equity Report by email?

To reply, please send information by fax to 1 212 521 8946 or by email [email protected]

By mail: Mikhail Angelovskiy, Marketing Dept.Debevoise & Plimpton LLP919 Third Avenue, New York, NY 10022

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 7

With its political stability, vibrant andentrepreneurial culture and impendingstatus as the center of the universe for theWorld Cup in 2014 and the Olympics in2016, Brazil appears positioned to continueto grow, albeit likely at a slower pace thanin recent years, due largely to the economicconditions prevailing elsewhere. As with its fellow BRICs, however,

Brazil is a challenging country in which toconduct due diligence on an investmentopportunity, in its case, particularly due tothe lack of a strong legal infrastructure,poor record keeping (historically), and thecultural sensitivities of Brazilian counter-parties to the kind of intrusiveness inherentin a normalized western due diligenceprocess. But unlike Russia, for instance,Brazil’s accounting standards areincreasingly conforming with IFRS, and itis well on the way to digitizing its recordkeeping and public search functions. It alsoseems poised to increase the sophisticationof its commercial and legal practices inorder to sustain its growth. Like its fellow BRICs, however, Brazil’s

rapid growth amid an evolving legal andenforcement system requires investors toevaluate carefully potential FCPA exposuresin connection with any investmentopportunity.Against that backdrop, the third

installment of our four-part series on doingdue diligence in BRICs countries continuesin this issue with Brazil.

Due Diligence Process

l Familiarity with due diligence process andrequirements: Unlike China, mostcompanies in Brazil are familiar with thedue diligence process and are aware of itscommercial importance. Still,management can be reluctant to share

information with outsiders out of acultural sense of invasiveness and likelysome concern for its impact on its ownfuture. In-house counsel, for example,may regard even ordinary requests andquestions in connection with duediligence as personal attacks against theirwork and may respond negatively. As inall of the BRICs (and elsewhere), buildingtrust with management is criticallyimportant to the success of the process.

l Internal organization: The strength ofthe internal organization of Braziliancompanies varies greatly. While manycompanies in Brazil, including all publiccompanies, are subject to mandatoryaudits, many others are not; companiessubject to independent audits of theirfinancial statements are generally betterorganized than those that are not subjectto audits. Most companies have legaldepartments and in-house counsel;however, decentralization of informationand knowledge is a common issue.There is a lack of standardizeddocumentation practices generally in thecountry and corporate records, such asminutes of the meetings of shareholdersor the board and the registry of shareownership and transfers, may not havebeen properly documented or registeredwith the competent authorities.

l Availability of public search resources: TheBrazilian government has madesubstantial investments in public searchresources, and a wide range of matterssuch as federal court litigation,trademarks, patents and domain, as wellas certain tax debts can be searchedthrough the internet. In some states, itis also possible to carry out publicinternet searches for labor and state

court litigation and corporate records. Asa general rule, if a public search cannotbe made through the internet, it can bemade at the public authority chargedwith keeping records of the particularinformation being sought.

Business Due Diligence

l FCPA: As reflected by the selectiveenforcement described in the next twobullets, Brazil is a “high-risk” country inthe anti-bribery area. The risk is higherstill in business sectors that operateunder governmental concessions orauthorizations and is also significantlyhigher in less developed regions of thecountry.

l Occupational safety and health: UnlikeChina, for instance, Brazil has extensiveoccupational safety/health laws andregulations, and employers that fail tocomply with such laws and regulationsare subject to fines and other sanctions.Like China, however, the enforcement ofoccupational safety/health laws and

CONTINUED ON PAGE 8

Brick by Brick: A Primer for Due Diligence in Each BRIC Country, Continuing with Brazil

...Unlike Russia, for

instance, Brazil’s

accounting standards

are increasingly

conforming with IFRS,

and it is well on the way

to digitizing its record

keeping and public

search functions.

regulations may vary depending on theregion and the business sector. Also,from time to time, the Braziliangovernment and NGOs havedenounced companies, especially thosein the agricultural sector, for subjectingworkers to inhumane conditions thatamounted to slave labor. Foreigninvestors may face reputational risk ifthe company in which it invests orwith which it does business has seriousoccupational safety/health issues.

l Environmental compliance andenforcement: In Brazil, federal, state,and municipal governments, have thepower to regulate environmentalmatters. Although these matters areusually regulated by federal laws, statesand municipalities have the power toimplement additional requirements and

proceedings for environmentalcompliance. As a result, compliancewith environmental laws can bechallenging, particularly for companiesoperating in multiple areas withinBrazil. The enforcement and levels ofcompliance with environmental lawsmay also vary depending on the regionand the size of a company’s operation.While large corporations are closelymonitored by environmentalauthorities, NGOs and smallerbusinesses, especially those operating incertain regions, are less likely to beclosely monitored and are, therefore,less likely to be in strict compliancewith environmental laws. Note thatBrazil has its own “Superfund”—likelaws providing that under certaincircumstances, a new owner of acontaminated area may be held jointlyand severally liable with the previousowners for the area’s recovery, regardlessof whether the new owner caused theenvironmental degradation.

l Foreign investment restrictions: On itsface, Brazilian law prohibits foreigninvestments in certain areas andactivities, such as nuclear energy,certain healthcare services, post officeand telegraph services, certainaerospace activities, domestic airlineservices, newspaper and magazinepublications and television and radionetworks. Foreign investments infinancial institutions, rural propertiesand in properties implicating nationalsecurity are also restricted. While mostof these restrictions can be waived bythe government, or otherwise avoidedby obtaining the prior authorization ofthe government or through othersimilar processes, this is not always thecase. Since 2010, for example, theBrazilian government has beenblocking foreign investment in rural

properties by looking through Brazilianinvestment vehicles controlled byforeigners that had been utilizedhistorically to attempt to comply withthese restrictions. In the past, theBrazilian congress has passedamendments to the constitution toremove or ease certain of theserestrictions, as was the case during theprivatization process of the late 1990’s,and it is currently discussing a bill thatwould address the issue of foreignownership of rural properties.

Legal Due DiligenceRegulatory environment: Brazil’s legalsystem is based on written statutes.Compared to common law jurisdictions,prior court decisions have limitedprecedential authority in Brazil. Manylaws and regulations are relatively new andcontain broad and sometimes ambiguousprovisions. As a result, as with all theBRICs, there is significant uncertainty asto one’s legal rights and obligations andgovernment authorities and courts havewide discretion in interpreting andenforcing Brazilian laws and regulations.Foreign exchange control: Foreign

investments in Brazil must be registeredwith the Central Bank. Non-compliancewith Brazilian registration requirementsmay jeopardize a foreign investor’s abilityto remit dividends or other distributionspayable to its investors outside of Braziland may require the repatriation of theinvestment. Registrations are madeelectronically by the company receivingthe investment through the electronicdeclaration registry of the Central Bankinformation system, but they are notsubject to prior examination orverification by the Central Bank.

l Regulated industries: Some industriesare regulated by the government, and

Brick by Brick: A Primer for Due Diligence in Each BRIC Country (cont. from page 7)

page 8 l Debevoise & Plimpton Private Equity Report l Fall 2011

Brazil’s legal system is

based on written statutes.

Compared to common law

jurisdictions, prior court

decisions have limited

precedential authority in

Brazil. Many laws and

regulations are relatively

new and contain broad

and sometimes ambiguous

provisions. As a result, as

with all the BRICs, there

is significant uncertainty

as to one’s legal rights and

obligations.... CONTINUED ON PAGE 20

What Are the Options? Bank Investment in Unaffiliated Private Equity and Hedge Funds Under the Volcker Rule A central question for sponsors of privateequity and hedge funds in the wake of thepassage of Section 619 of the Dodd-FrankWall Street Reform and Consumer ProtectionAct (the “Volcker Rule”) has been the extentto which “banking entities” (as defined underthe Volcker Rule) will be permitted to investin private equity and hedge funds that arenot otherwise affiliated with such bankingentities. We discussed this question in theSpring issue of the Debevoise & PlimptonPrivate Equity Report and now provide anupdate based on the detailed proposed rulesfor implementing the Volcker Rule (the“Proposed Rules”), which were published forpublic comment on October 11th and 12th.The precise answer to how the Volcker

Rule will be implemented won’t be knownuntil these implementing rules are finalized,after the public comment period ends onJanuary 13, 2012. The final implementingrules may contain substantial changes fromthe Proposed Rules. Indeed, there isconsiderable uncertainty as to the final formthat the implementing rules ultimately willtake, in part because there appears to be asubstantial difference of opinion among theregulators involved in the rulemaking process.Meanwhile, however, many sponsors of

private equity and hedge funds, particularlythose currently fund-raising or consideringfund-raising, face the difficulty ofdetermining which, if any, banks and bankaffiliates may invest in their funds. Below weset forth a simplified, updated summary ofthe current lay of the land under the VolckerRule and the Proposed Rules. This “cheatsheet” is based on our review of the VolckerRule statute and the Proposed Rules, as wellas our engagement in the rulemaking process.All guidance provided below is preliminary andsubject to revision pending the adoption of the

Proposed Rules; of course, specific facts andcircumstances should also be considered in anyanalysis.

Options for a U.S. Banking EntityIf the Proposed Rules are adopted aspublished, a U.S. bank (or other insureddepository institution) and its affiliates (a“banking entity”) generally would not bepermitted to invest directly from its ownbalance sheet in U.S. private equity or hedgefunds, unless the fund satisfies one of theexemptions noted below. In addition, itappears that a U.S. banking entity generallywould not be able to invest in non-U.S.private equity or hedge funds or, for thatmatter, even funds that are registered andpublicly offered in other jurisdictions (including,for example, European UCITS vehicles). Customer Funds. A U.S. banking entity

could set up one or more so-called“customer funds” to act as either a fund offunds, a parallel fund or a feeder fund thatinvests in or alongside an unaffiliatedprivate equity or hedge fund. The bankingentity’s investment in the “customer fund”would be limited to 3% of any suchcustomer fund’s capital and 3% of thebanking entity’s Tier 1 capital (aggregatedacross all of the banking entity’s investmentsin customer funds). These 3% limits wouldnot include rights to carried interest or, inmost circumstances, the individual investmentsof employees providing services to the“customer fund” (unless the investmentswere guaranteed or funded by the bankingentity). Investors in a customer fund wouldnot be required to have a pre-existingrelationship with the banking entitysponsoring the customer fund.General Account and Separate Account

Assets. Many commenters believe, based

on specific language in the Volcker Ruleand on policy grounds, that an insurancecompany affiliated with a U.S. bankshould be able to invest the insurancecompany’s general account and separateaccount assets in private funds, subject tocompliance with applicable state insurancelaws on permitted investments. We note,however, that the Proposed Rules do notaddress this point, even though theProposed Rules provide a clear exemptionfrom the proprietary trading prohibitionfor insurance company general accountand separate account assets.Hedging. A U.S. banking entity would

be able to make investments in privateequity and hedge funds designed to reducethe specific risks to the banking entity from

CONTINUED ON PAGE 10

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 9

...[U]nder...the

Proposed Rules, it is

possible that a U.S.

private equity or hedge

fund manager could

establish a Non-U.S.

Investor Fund to invest

side-by-side with

another fund sponsored

by the U.S. manager in

the same portfolio

companies and on the

same terms.

page 10 l Debevoise & Plimpton Private Equity Report l Fall 2011

either (1) acting as intermediary on behalfof a customer (that is not a banking entity)to facilitate the exposure by the customer tothe profits and losses of the private equityor hedge fund or (2) a compensationarrangement with an employee that directlyprovides investment advisory or otherservices to the private equity or hedge fund.

Options for a Non-U.S.Banking Entity with a U.S.Banking PresenceNon-U.S. Investor Funds. A non-U.S.banking entity with a U.S. bankingpresence (i.e., a branch, agency office orcommercial lending company or with asubsidiary U.S. bank) generally would beallowed under the Proposed Rules toinvest in an unaffiliated private equity orhedge fund that is marketed and soldsolely to non-U.S. residents so long as thenon-U.S. banking entity’s U.S. affiliatesand employees are not involved in theoffer or sale of the fund’s interests (a“Non-U.S. Investor Fund”). A non-U.S.banking entity with a U.S. bankingpresence would be able to invest in aNon-U.S. Investor Fund without beingsubject to the Volcker Rule’s limits, even ifthe Non-U.S. Investor Fund (1) wereorganized under U.S. law, (2) weremanaged by a U.S.-based manager and (3)invested principally in U.S. companies.We note that under this provision of theProposed Rules, it is possible that a U.S.private equity or hedge fund managercould establish a Non-U.S. Investor Fundto invest side-by-side with another fundsponsored by the U.S. manager in thesame portfolio companies and on thesame terms. However, any sucharrangement would need to be analyzed toensure that the Non-U.S. Investor Fund isnot deemed to be sold to U.S. residents.A Non-U.S. Investor Fund would notneed to meet the conditions applicable tocustomer funds.

Other Options. A non-U.S. bankingentity also would have the same options asa U.S. banking entity, described above, toinvest in unaffiliated private equity andhedge funds.

Options for a Non-U.S.Banking Entity with No U.S.Banking PresenceNo Restrictions. A non-U.S. bankingentity with no U.S. banking presence isnot subject to the Volcker Rule andshould be able to invest in all types offunds (including both U.S. and non-U.S.private equity and hedge funds).

Bank-Sponsored PensionPlans and Bank EmployeesPension Plans. A bank-sponsored pensionplan would be permitted to invest inunaffiliated private equity and hedgefunds if the plan is a “qualified plan”under the Internal Revenue Code. Employees and Employee Vehicles. The

Proposed Rules would allow bankemployees providing services to customerfunds generally to invest in those fundswithout such employee investmentscounting against either of the two separate3% limits described above that apply tobanking entity investments in customerfunds (unless such investments wereguaranteed or financed by the bankingentity). Banking entity employees shouldbe able to invest in unaffiliated privatefunds, although there is language in thepreamble to the Proposed Rules that castsdoubt on this point; clarification in thefinal regulations would be helpful.

Effect of Volcker RuleRestrictions on Fundraising byPrivate Funds That Are NotAffiliated with BankingEntitiesThe practical effect of the restrictionsunder the Volcker Rule and the ProposedRules on U.S. and non-U.S. private equity

and hedge fund managers that are notaffiliated with banking entities is to limitsignificantly their ability to access thecapital of U.S. banking organizations andnon-U.S. banking organizations that havea U.S. banking presence.Under the Proposed Rules, however,

such U.S. and non-U.S. private equityand hedge fund managers generally wouldbe permitted to raise capital for theirfunds from (1) banking entity-sponsoredcustomer funds (organized as feeder funds,funds of funds or parallel funds), subjectto the two separate 3% limits describedabove, (2) non-U.S. banks with nobanking presence in the United States, (3) non-U.S. banks that have a U.S.banking presence, so long as the funds inwhich those non-U.S. banks invest areoffered only to non-U.S. persons and (4)bank-sponsored pension plans. Suchmanagers also should be able to raisecapital from insurance company generalaccounts and separate accounts. Finally,such managers may be able to raise capitalfrom employees and pooled employeevehicles of banking entities; however,further guidance would be helpful.

What’s Next?As mentioned above, the actual reach

and operation of the Volcker Rule won’tbe known until the implementing rulessummarized above are finalized. The rulescould change substantially between nowand then. First, there appears to be asubstantial difference of opinion amongthe regulators involved in the rulemakingprocess as to the form that the final rulesshould take. Second, the release settingforth the Proposed Rules posed hundredsof questions for public comment. Third,advocates for greater or lesser regulation ofbanking entities have loudly and publiclyexpressed widely differing views on theform that the Proposed Rules should take,

Bank Investment Under the Volcker Rule (cont. from page 9)

CONTINUED ON PAGE 18

An unexpected stockholder approvalrequirement can throw a monkey wrenchinto the deal certainty calculus for divestituretransactions. In light of this year’s uptick insubsidiary divestitures (particularly via spin-off), private equity buyers (and sellers) shouldbe mindful of recent guidance from Delawarecourts on whether a shareholder vote orlender consent would be required to approvesuch divestitures. A shareholder vote cansignificantly lengthen the time and increasethe expense it takes to close the transaction,resulting in a private equity buyer’s loss ofappetite for a deal or their missingincreasingly ephemeral financing windows. Most people in the deal business know

that the sale of all or substantially all of theassets of a Delaware or New York corporationwould require shareholder approval, anddepending on the indenture, consent fromthe seller’s banks or bondholders.1

Unsurprisingly, there is no bright-line rule asto when a divestiture constitutes“substantially all” of a corporation’s assets.Practitioners will generally advise that a saleof 60% of the book value may be the tippingpoint, particularly when the corporation’sremaining assets are unprofitable.2 But, theyrecognize that there are multiple ways ofslicing and dicing—while shareholderapproval statutes and bond indentureprovisions often refer to “assets,” courts looknot only at book value, but also at otherindications of financial value includingEBITDA, net income, and cash flow.Less obvious is that a transaction for only

a small fraction of a corporation’s assets couldtrip those approval and consent requirementsin certain circumstances. The Delaware

Supreme Court recently reviewed abondholder’s challenge that a June, 2010split-off from Liberty Media Corporationrequired shareholder approval.3 Even thoughthe assets divested represented only 15% ofLiberty Media’s book value at the time thatthe alleged “disaggregation strategy”commenced, the indenture trustee contendedthat those assets, when combined with LibertyMedia’s other three divestitures under thealleged plan, constituted substantially all ofLiberty Media’s assets. The Court confirmedthat the “substantially all” analysis is not asnapshot, and that separate transactions,effected as part of an overall scheme, could beaggregated to determine if they constituted“substantially all” of the assets of thecorporation. In the case of Liberty Media,however, the Delaware Supreme Court upheldthe Chancery Court’s determination that thefour separate divestitures were not part ofsuch an overall plan, and thus did not needto be aggregated.4

A review of the Liberty Media case, as wellas other New York and Delaware precedent,identify some important questions a privateequity buyer should ask in the context of asubsidiary divestiture.5 The first step would

be to identify any past, pending or near-termfuture divestitures. The next step would beto review the divestitures’ materiality byassessing their size in terms of assets,EBITDA, and net income, as well as morequalitative factors including profit potentialand importance to the remaining business. Ifthe divestitures (taken together) couldconstitute “substantially all” of the seller’sassets, the buyer should conduct a detailedreview of the seller’s board minutes andpublic statements to ensure there was nooverarching plan or scheme of divestiture andthat each transaction had independentjustification, and review the other divestitureagreements to determine that each divestiturewas not linked contractually (e.g., as closingconditions) to one another. Although it maybe tempting for a buyer to rely upon furtherprotection in its own purchase agreement toensure that it has the right to terminate theagreement if its transaction is crediblychallenged or is determined to requireshareholder approval, both the buyer andseller need to be careful not to create a recordthat might attract such challenges for hold-upvalue. Otherwise, a termination right is ahairline trigger and may be too drastic. Ofcourse, a prudent seller would generallyanticipate this line of inquiry and providesupport for its conclusion that the varioussales should not be aggregated. Even if the parties have determined that

shareholder approval is not required, theyshould be prepared for challenges frombondholders, activist shareholders, or theplaintiff ’s bar. Although this area has notbeen fertile ground for strike suits by theplaintiff ’s bar, in the wrong circumstancessuch an attack could unravel a deal.

Franci J. [email protected]

Kamal Agrawal [email protected]

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 11

Buyer Beware (Delaware Law Edition): Sometimes “Substantially All” Isn’t All That Much

1 See Del. Gen. Corp. Law. Section 271; NY BCLSection 909.

2 At least one court has found that the sale of 51%of a corporation’s assets required shareholder approval.See Katz v. Bregman, 431 A.2d 1274 (Del. Ch.1981).

3 See Bank of New York Mellon Trust Co., N.A. v.Liberty Media Corp., 29 A.3d 225 (Del. 2011)(under the terms of an indenture, Liberty Mediaagreed not to transfer “substantially all of its assets”unless the successor entity assumed Liberty Media’sobligations under the indenture).

4 Because the Court found that there was no overallscheme or plan, it did not need to determine if thefour divestitures constituted “substantially all” ofLiberty Media’s assets, and the Court did not addressthe appropriate method for analyzing the“substantially all” calculation. Therefore, a thoughtfulbuyer would measure the divested businesses’ size atboth the time of sale as well as at the time of thealleged plan’s adoption.

5 Similarly, careful sellers, mindful of theshareholder and bondholder litigation risk, wouldaddress these issues in advance of any planneddivestiture.

page 12 l Debevoise & Plimpton Private Equity Report l Fall 2011

Recent Speaking Engagements October 7, 2011Erica BerthouGeoffrey Kittredge“The Shifting Landscape of Private EquityFund Terms”Danish Venture Capital AssociationSeminarCopenhagen

October 13, 2011Geoffrey P. Burgess (moderator)“The Opportunities—Looking at the BRICsand Beyond for the Growth Markets of theFuture”BVCA Summit 2011British Private Equity and Venture CapitalAssociationLondon

October 17, 2011Karolos Seeger“Responding to the New UK Bribery Act:How to Adjust your Compliance Program toMeet New “Adequate Procedures” in India”Second India Summit on Anti-CorruptionAmerican Conference Institute Mumbai

October 18, 2011Erica BerthouJennifer J. BurleighPeter A. FurciJordan C. Murray“Structuring Brazilian Private Equity Funds:Key Considerations” Debevoise & Plimpton LLP and MattosFilhoSão Paulo, Brazil

October 26, 2011Michael P. HarrellJonathan J. RikoonCristine M. Sapers “Estate Planning for Private EquityProfessionals and LGBT Families”Debevoise & Plimpton LLP and UBSNew York

October 27, 2011Andrew N. Berg“‘Topside’ Planning for Private Equity (andHedge) Fund Investments”Tax Strategies for Corporate Acquisitions,Dispositions, Spin-Offs, Joint Ventures,Financings, Reorganizations &Restructurings 2011Practising Law Institute New York, NY

October 27, 2011Michael P. HarrellSatish M. KiniGregory J. LyonsRebecca F. Silberstein“The New Volcker Rule Proposals: BankInvestments in Private Equity and HedgeFunds Seminar”Debevoise & Plimpton LLP and the PrivateEquity Growth Capital Council New York

October 27-28, 2011Franci J. Blassberg“Special Problems When Acquiring Divisionsand Subsidiaries; Negotiating the Acquisitionof the Private Company”ALI-ABA Corporate Mergers andAcquisitionsALI-ABABoston

November 1, 2011Rebecca F. Silberstein“One Size Fits All? Recent Case Studies ofBespoke Structuring of Funds for SpecificPurposes”International Bar Association AnnualConferenceDubai

November 30, 2011Satish M. Kini“The Volcker Rule – Cross Border IssuesAffecting Proprietary Trading, MarketMaking, and Relationships with Private-Equity and Hedge Funds” Implementation of the Dodd-Frank Act –Key Issues for International BanksInstitute of International BankersNew York, NY

December 1, 2011Franci J. Blassberg (moderator)“How Investors View the Asset Class Todayand their Plans for the Future”David Innes “Current Issues: A Mixed Bag of TopicalIssues”Private Equity Transaction Symposium2011International Bar AssociationLondon

December 1, 2011David H. Schnabel “‘Topside’ Planning for Private Equity (andHedge) Fund Investments”Tax Strategies for Corporate Acquisitions,Dispositions, Spin-Offs, Joint Ventures,Financings, Reorganizations &Restructurings 2011Practising Law InstituteLos Angeles

December 5, 2011Erica Berthou“Opening Remarks”Jennifer J. BurleighPeter A. Furci “Legal Developments/Fund Formation inBrazilGregory V. Gooding “Minority vs. Control Investments”Paul M. Rodel“Exit Strategies” Private Equity Brazil ForumSão Paulo

For more information about upcomingevents, visitwww.debevoise.com

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 13

Discount Shopping: Making the Most Out of Distressed Asset SalesPrivate equity lawyers may find someexceptional opportunities arising out ofother people’s problems. In the uncertaineconomic climate of the last few years, assetsales in bankruptcy—or “Section 363 sales”named after the section of the BankruptcyCode that authorizes them—have become acommon restructuring alternative fortroubled companies. The Section 363 saleprocess offers considerable advantages tosellers and buyers alike and, in a growingnumber of cases, is viewed as an efficientand fair way to maximize the value of adistressed business for the benefit of allconstituencies. Although default ratesremain somewhat surprisingly low, manybusinesses that kicked the proverbial candown the road through “amends &extends” or favorable refinancings will needto face the music eventually, and some ofthem may be attractive targets for privateequity buyers. To take full advantage ofthese opportunities, it is crucial tounderstand not only the basics of Section363 sales and their distinctive featurescompared to standard M&A transactions,but also emerging trends and issues indistressed asset sales.

Section 363 Sale BasicsSection 363 of the Bankruptcy Code allowsa debtor (i.e., a company in bankruptcy),with court approval, to sell assets outsidethe ordinary course of business.1 Thedebtor must establish that it obtained thehighest or best price for the assets. Thisrequirement is often satisfied by a “doubleauction.” The company first markets theassets, runs a sale process and ultimatelynegotiates and signs a purchase agreementwith the party that makes the best offer

(otherwise known as the “stalking horse”).To minimize the impact of the bankruptcyon the business, the stalking horseagreement is usually signed just before thecompany enters Chapter 11, providing amore certain outcome for the debtor. Thestalking horse agreement then serves as thefloor in an auction conducted in accordancewith bidding procedures negotiated withthe stalking horse and then approved by thebankruptcy court.2

A Section 363 sale can be approved bythe court only after notice to interestedparties and a hearing. Until the courtapproves the sale, the purchase agreement isbinding on the buyer, but not the debtor.For this reason, the bidding procedures aswell as any break-up fee and expensereimbursement granted to the stalkinghorse are typically approved by the courtbefore the auction so that they are bindingon the debtor.Section 363 sales offer many advantages

to buyers, including the ability to purchasethe assets free and clear of nearly all pre-closing liabilities and encumbrances,3 anopen auction process, and a relatively cleanand easy transfer of title. In turn, these

advantages can result in improvedrealization value for the debtor and itscreditors and, coupled with an efficientadministration of post-sale liabilities, mayresult in a confirmed Chapter 11 plan thatincludes releases of the debtor’s directorsand officers.

Who Are the Real Parties in Interest?Secured creditors are key players in Section363 sales. As a general matter, assets canonly be sold free and clear of a lien if thecreditor secured by the lien consents to thesale or is paid in full from the proceeds. Ifthe proceeds are not sufficient to pay thesecured debt in full, a potential buyer iseffectively negotiating not only with thedebtor and its management, but also withthe secured creditors. Understanding howone’s bid is valued by the secured creditorsis essential. For example, a buyer’sassumption of pre-bankruptcy unsecuredtrade obligations does not provide directvalue to the secured creditors, who arefocused on the actual proceeds of the sale.But leaving those obligations behind mayaffect the value of the debtor’s accountreceivables if trade creditors exercise setoffrights or stop doing business with thedebtor prior to the closing of the sale, whichsecured creditors may in fact care about.By contrast, a Section 363 sale can

usually be approved over the objection ofunsecured creditors if the court finds that,among other things, the marketing processwas robust and produced the highest orbest price for the assets in thecircumstances. Even if unsecured creditorscan establish that typical valuationprinciples would tend to suggest a highervaluation, the market test is generallycontrolling. In other words, if the auctionwas conducted fairly and without collusion,the winning bid is assumed to represent thebest price available in the market. Thus,unsecured creditors typically cannot preventthe sale under those circumstances, unlessthey are willing to put their money wheretheir mouth is and purchase the assetsthemselves for a higher price.

CONTINUED ON PAGE 14

1 For a detailed description of the Section 363 saleprocess, see “Section 363 Sales: How to Play theGame,” Debevoise & Plimpton Private EquityReport, Summer 2007, Volume 7, Number 4.

2 The process is in some ways similar to a public M&Atransaction in that the buyer is subject to being topped byother bidders even after it has signed a definitiveagreement.

3 Exceptions to keep in mind are environmentalliabilities and successor liability related to certain types oftort claims.

page 14 l Debevoise & Plimpton Private Equity Report l Fall 2011

How Fast is Too Fast?The historic $1.85 billion sale of Lehman’sNorth American business to Barclays in2008, which was approved andconsummated in a record seven days afterLehman’s bankruptcy filing, appears tohave opened the door to faster Section363 sales. It is now customary for debtorsto propose sale timelines of two monthsor less from the bankruptcy filing to thesale hearing, compared to what used to bea three-month rule of thumb.4

The actual length of the process willdepend on many factors, including thejudge’s availability, whether objections arefiled, the likelihood of other bidders, andwhether, like in the Lehman sale, thebusiness is truly a “melting ice cube” thatmust be sold without delay. Grumblingsabout the frequency and speed of Section363 sales appear to be increasing. Theseare often coupled with concerns thatSection 363 sales deprive unsecuredcreditors of certain protections that wouldotherwise be available if the business weresold pursuant to a Chapter 11 plan,including the requirement that the plan beapproved by affected classes of creditors.A purchase of assets (or stock in areorganized entity) pursuant to a Chapter11 plan provides many of the samebenefits as a Section 363 sale as well asadditional advantages, including theability to provide for appropriate releasesin the plan and exemptions from certaintransfer taxes and registrationrequirements under securities laws.Courts are generally sympathetic to

arguments that the Section 363 saleprocess should be slowed down to giveinterested parties a real opportunity toconduct diligence and submit bids.Ultimately, however, courts will bereluctant to meaningfully delay a sale if

the only debtor-in-possession financingavailable is tied to an expedited processand the alternative is a Chapter 7liquidation. This may be particularly truefor companies burdened by high levels ofsecured debt and therefore with limitedadditional assets to finance a fulloperational and financial restructuring,which typically takes longer and is moreexpensive than an asset sale.

Break-Up Fees: Are They at Risk?In exchange for its investment of time andmoney to conduct due diligence andnegotiate a purchase agreement, thestalking horse will usually insist on somedeal protection in the form of a break-upfee, expense reimbursement and certainprocedural advantages such as informationrights and minimum bid requirements.Resistance to a large break-up fee, whichcould have a chilling effect on bidding,can be expected from the debtor and anycreditors who will not be paid in full fromthe sale proceeds.The stalking horse should also consider

the possibility that another bidder mightattack the break-up fee by offering topurchase the assets on the same terms asthe stalking horse but without a break-upfee as evidence that a break-up fee is notnecessary to induce a party to act asstalking horse. Although disappointedbidders generally do not have standing toobject to a Section 363 sale, this tactic wassuccessfully employed in a handful ofcases in Delaware in recent years, wherethe court ultimately denied the break-upfee or approved a reduced break-up fee.5

The willingness of a party to buy theassets without a break-up fee makes itdifficult for the court to conclude that thefee is necessary to induce competitivebidding and therefore to preserve thevalue of the debtor’s estate.

Credit Bidding: Risk or Strategy?A secured creditor has the right topurchase its collateral in exchange for thesatisfaction of its claim (or “credit bid”) ina Section 363 sale. Because securedcreditors can bid the face amount of theirclaim regardless of the value of theunderlying collateral, secured debt tradingat a discount can be a valuable currencyfor potential buyers.Unless the secured creditors are willing toaccept less than full payment of theirclaims, a cash buyer risks being outbid bythe secured creditors. To minimize thisrisk, the stalking horse should request thatthe secured creditors consent to its bid.In addition, the stalking horse shouldmake sure that its break-up fee will bepaid in the event that a credit bid isselected as the winning bid. Because acredit bid by definition does not includecash, the debtor may not have sufficientfunds to pay the break-up fee. Therefore,the bidding procedures should require thatany credit bid include a cash componentsufficient to pay the break-up fee.Credit bidding is increasingly used by

sophisticated distressed investors as a wayto gain control over troubled businesses.The success of this “loan-to-own” strategydepends on a number of factors, includingwhether the liens securing the debt arevalid, perfected and non-avoidable. Inaddition, if an investor does not purchase100% of the debt, it is equally importantto ensure that the financingdocumentation allows the investor tocontrol the decision to credit bid. The

Making the Most Out of Distressed Asset Sales (cont. from page 13)

4 This is similar to a public M&A transactiontimeline, assuming no regulatory delays.

5 In re Reliant Energy Channelview LP, 594 F.3d200 (3d Cir. 2010); In re Magic Brands, LLC et al.,Case No. 10-11310 (BLS); In re SHC, Inc, et al., CaseNo. 03-12002 (MFW). Note a similar trend in recentpublic M&A auctions where topping bids have beenmade without a break-up fee in an attempt to pressurethe stalking horse into eliminating or reducing its break-up fee. CONTINUED ON PAGE 19

Fall 2011 l Debevoise & Plimpton Private Equity Report l page 15

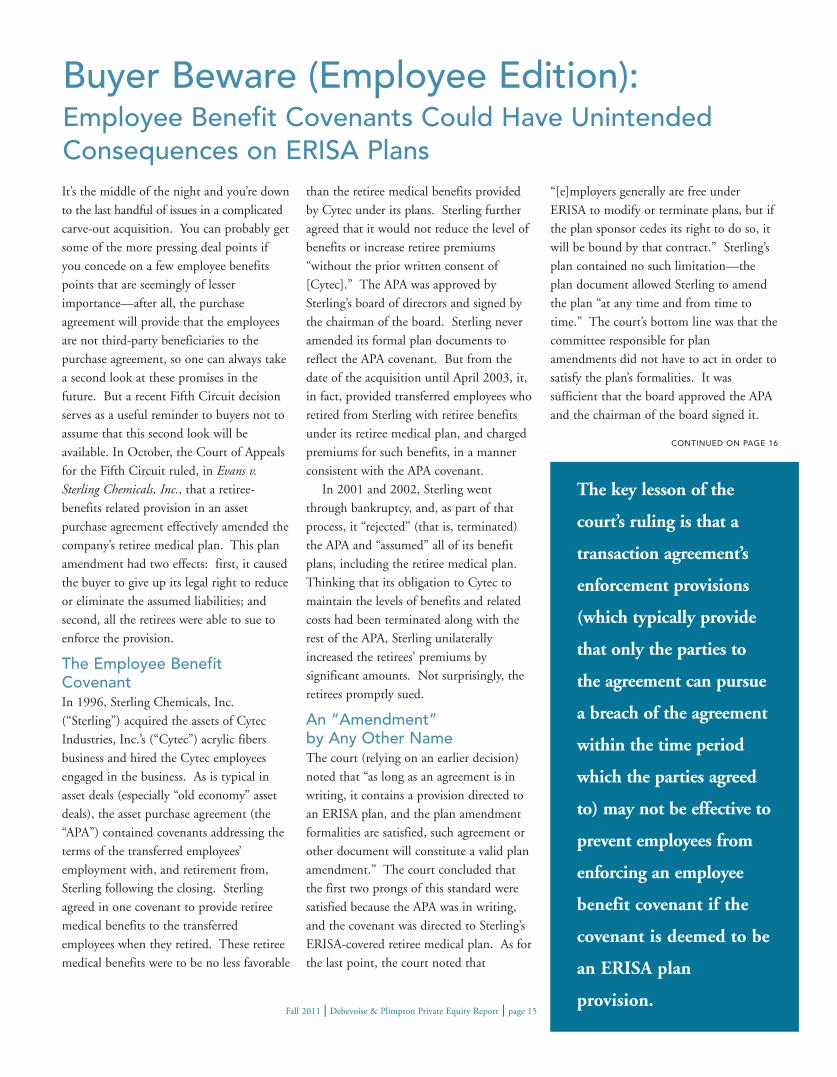

Buyer Beware (Employee Edition): Employee Benefit Covenants Could Have UnintendedConsequences on ERISA PlansIt’s the middle of the night and you’re downto the last handful of issues in a complicatedcarve-out acquisition. You can probably getsome of the more pressing deal points ifyou concede on a few employee benefitspoints that are seemingly of lesserimportance—after all, the purchaseagreement will provide that the employeesare not third-party beneficiaries to thepurchase agreement, so one can always takea second look at these promises in thefuture. But a recent Fifth Circuit decisionserves as a useful reminder to buyers not toassume that this second look will beavailable. In October, the Court of Appealsfor the Fifth Circuit ruled, in Evans v.Sterling Chemicals, Inc., that a retiree-benefits related provision in an assetpurchase agreement effectively amended thecompany’s retiree medical plan. This planamendment had two effects: first, it causedthe buyer to give up its legal right to reduceor eliminate the assumed liabilities; andsecond, all the retirees were able to sue toenforce the provision.

The Employee BenefitCovenantIn 1996, Sterling Chemicals, Inc.(“Sterling”) acquired the assets of CytecIndustries, Inc.’s (“Cytec”) acrylic fibersbusiness and hired the Cytec employeesengaged in the business. As is typical inasset deals (especially “old economy” assetdeals), the asset purchase agreement (the“APA”) contained covenants addressing theterms of the transferred employees’employment with, and retirement from,Sterling following the closing. Sterlingagreed in one covenant to provide retireemedical benefits to the transferredemployees when they retired. These retireemedical benefits were to be no less favorable

than the retiree medical benefits providedby Cytec under its plans. Sterling furtheragreed that it would not reduce the level ofbenefits or increase retiree premiums“without the prior written consent of[Cytec].” The APA was approved bySterling’s board of directors and signed bythe chairman of the board. Sterling neveramended its formal plan documents toreflect the APA covenant. But from thedate of the acquisition until April 2003, it,in fact, provided transferred employees whoretired from Sterling with retiree benefitsunder its retiree medical plan, and chargedpremiums for such benefits, in a mannerconsistent with the APA covenant. In 2001 and 2002, Sterling went

through bankruptcy, and, as part of thatprocess, it “rejected” (that is, terminated)the APA and “assumed” all of its benefitplans, including the retiree medical plan.Thinking that its obligation to Cytec tomaintain the levels of benefits and relatedcosts had been terminated along with therest of the APA, Sterling unilaterallyincreased the retirees’ premiums bysignificant amounts. Not surprisingly, theretirees promptly sued.

An “Amendment” by Any Other NameThe court (relying on an earlier decision)noted that “as long as an agreement is inwriting, it contains a provision directed toan ERISA plan, and the plan amendmentformalities are satisfied, such agreement orother document will constitute a valid planamendment.” The court concluded thatthe first two prongs of this standard weresatisfied because the APA was in writing,and the covenant was directed to Sterling’sERISA-covered retiree medical plan. As forthe last point, the court noted that

“[e]mployers generally are free underERISA to modify or terminate plans, but ifthe plan sponsor cedes its right to do so, itwill be bound by that contract.” Sterling’splan contained no such limitation—theplan document allowed Sterling to amendthe plan “at any time and from time totime.” The court’s bottom line was that thecommittee responsible for planamendments did not have to act in order tosatisfy the plan’s formalities. It wassufficient that the board approved the APAand the chairman of the board signed it.

CONTINUED ON PAGE 16

The key lesson of the

court’s ruling is that a

transaction agreement’s

enforcement provisions

(which typically provide

that only the parties to

the agreement can pursue

a breach of the agreement

within the time period

which the parties agreed

to) may not be effective to

prevent employees from

enforcing an employee

benefit covenant if the

covenant is deemed to be

an ERISA plan

provision.

Asset Purchase Agreement v. ERISA Plan (Advantage,ERISA Plan)The court also determined that the effectof the APA covenant survived bankruptcy,despite Sterling’s rejection of the APA.The court observed that the covenant wasboth “(i) a contractual obligation betweencorporate parties, and (ii) an ERISA planprovision enforceable by planparticipants.” According to the court, the“contractual obligation between” Sterlingand Cytec (that is, the APA) had beenterminated in the bankruptcy, but the“ERISA plan provision enforceable byplan participants” (that is, the retireemedical plan as amended by thecovenant) had been assumed by Sterling.This conclusion essentially punishedSterling for its failure to follow the“official” amendment process—if it haddone so, Sterling would have realized thatit also needed to reject the retiree medicalplan in the bankruptcy (which is acomplicated but not impossible process).However, because Sterling had neverincorporated the APA provisions into theplan document, it likely didn’t realize thatthe APA provision had replicated itselfwithin the plan. The key lesson of the court’s ruling is

that a transaction agreement’senforcement provisions (which typicallyprovide that only the parties to theagreement can pursue a breach of theagreement within the time period whichthe parties agreed to) may not be effectiveto prevent employees from enforcing anemployee benefit covenant if the covenantis deemed to be an ERISA plan provision.

Avoiding the UnintendedIn light of the Sterling line of cases, whennegotiating carve-out transactions, privateequity sponsors should try to avoid long-lived employee covenants. This isespecially (but not only) true with respectto retirees, who typically present theworst-case employee litigation scenario:(1) there are a lot of them and theyusually have a lot of time to enforce theirrights; (2) courts are sympathetic to them;and (3) unlike active employees, there areusually no other items of compensation(such as bonuses or equity, or sometimeseven continued employment) that makethem willing to compromise their claims.If these covenants are not avoidable, abuyer should be comfortable with theemployee benefit covenants to which itagrees and should expect that a court willfavor the employees in any close case,including by disregarding arguments

perceived as “technical” in nature (such asreliance on “no third-party beneficiary”language or the argument that theemployees are not able to enforce theprovision). Sterling also points out that process

and documentation matter. For example,it is an open question as to whether aprovision in the APA stating that no planamendment was intended by theemployee benefit covenants would havebeen effective. Transaction documentationshould also say (if consistent with the dealnegotiations) that the acquiror reservesthe right to amend or terminate itsemployee benefits plans at any time.Finally, it is important to follow theprocedures for amending plans forpurposes of reflecting employee benefitcovenants. Sterling would have had a morecompelling argument if (1) it had clearlydelineated that the agreement as to thepost-closing level of benefits and premiumswas solely an agreement between it andCytec, and (2) the plan documents hadreflected that distinction.

Jonathan F. [email protected]

Charles E. [email protected]

Buyer Beware (Employee Edition): Employee Benefit Covenants (cont. from page 15)

page 16 l Debevoise & Plimpton Private Equity Report l Fall 2011

Lookingfor a pastarticle?

A complete article index, along with

all past issues of the Debevoise & Plimpton

Private Equity Report, is available in the

“publications” section of the firm’s website,

www.debevoise.com.

buyers through proposed leverage ratios,which may have the effect of setting aprice floor in an auction. Offering stapledfinancing may attract more buyers to asale process by decreasing the costsassociated with sourcing financing,particularly in the early rounds of anauction, and by ensuring (even in difficultfinancing markets) that financing isavailable to all bidders that need it. Astaple may also provide a floor on non-price terms that will be available fromother lenders, creating a more robustauction and ultimately a better price forthe selling stockholders.A staple can also provide a seller with

access to market knowledge and visibilityinto leverage levels and pricing that itmight not otherwise have. This can helpa seller initially assess bids. Stapledfinancing may shorten the bidding processand the time to signing because the staplelender can complete its diligence and getcomfortable with the credit very early inthe auction process. Because the seller’sfinancial advisor will have a good chanceof earning buy-side financing fees, a sellermay even be able to negotiate a lower feefor the sell-side M&A advisory work.There may also be good reasons to

allow a sell-side advisor to offer buyerfinancing outside the context of a staple.For example, the participation of anadditional lender may, given the lender’sbalance sheet or market expertise,facilitate and expedite closing to theseller’s benefit, or facilitate execution in adifficult market by decreasing theindividual exposure of the othercommitting banks.

Understanding the RisksOf course, whenever a sell-side advisorparticipates in buy-side financing,including by way of a staple, there arepotential conflicts of interests – an issue

that was highlighted by the DelawareChancery Court in Del Monte and in the2005 Toys “R” Us decision. The key issueis that the sell-side advisor’s possibility ofearning fees from the buy-side financingcreates the risk that the advisor will seekto influence the process so that the dealgoes to a particular buyer (or particulartype of buyer, such as a private equitysponsor) that is most likely to utilize itsfinancing. This risk is heightened becausethe fees that can be earned on thefinancing are often larger than the sell-side M&A fees. A financing source’sinterests are also in some other respectspotentially adverse to sellers. Forexample, a financing source might want abuyer to pay less so that leverage levels arelower, and may even seek to scuttle thedeal or negotiate concessions (includingpurchase price reductions) if anyconditions to funding arguably have notbeen satisfied, such as in the case of amaterial adverse effect arising prior toclosing. There are risks for the buyer too. First