Embed Size (px)

Citation preview

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 1/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 2/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 3/56Mining or Growth: A review o outbound Mining M&A activity rom China 3

Executive summary 4

Methodology 5

China M&A survey ndings 6

M&A Review 28An interview with Deloitte China'sMining sector Partner 28

Macroeconomic drivers o outboundMining M&A 31

Chinese outbound Mininginvestment case study - Australia 39

The regulatory environment: a lookat regulatory rulings on Chineseoutbound Mining acquisitions 40

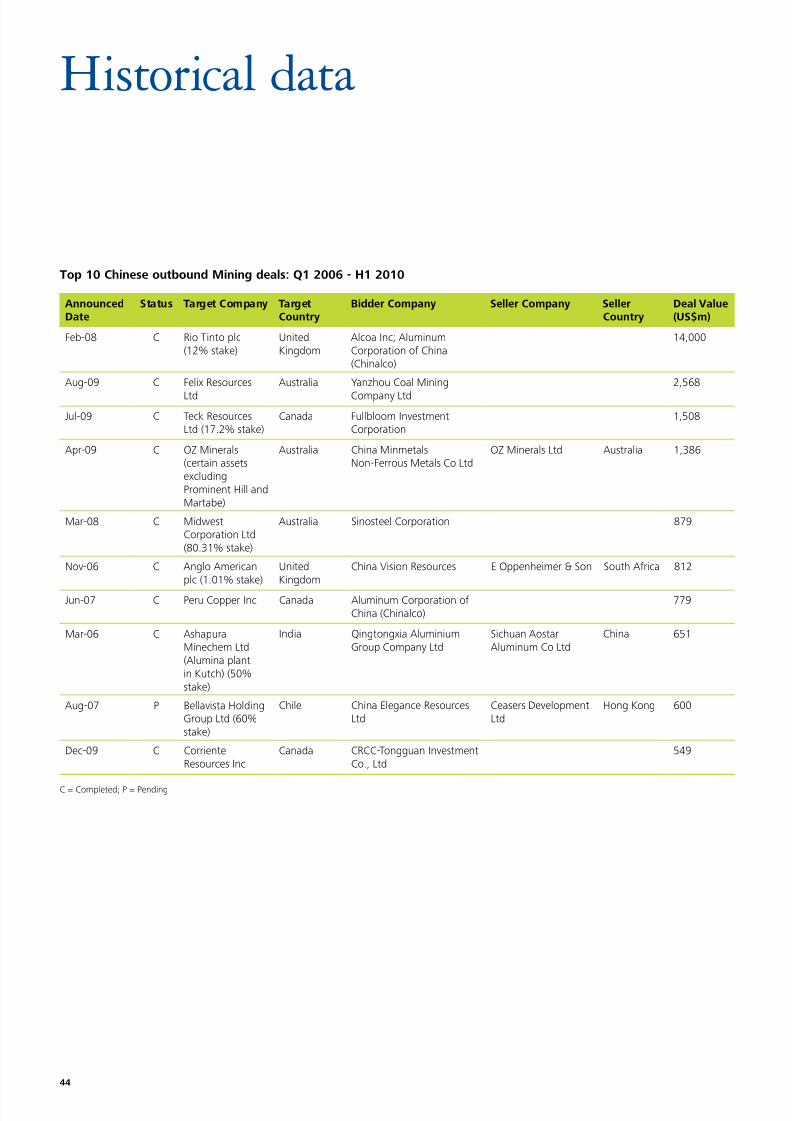

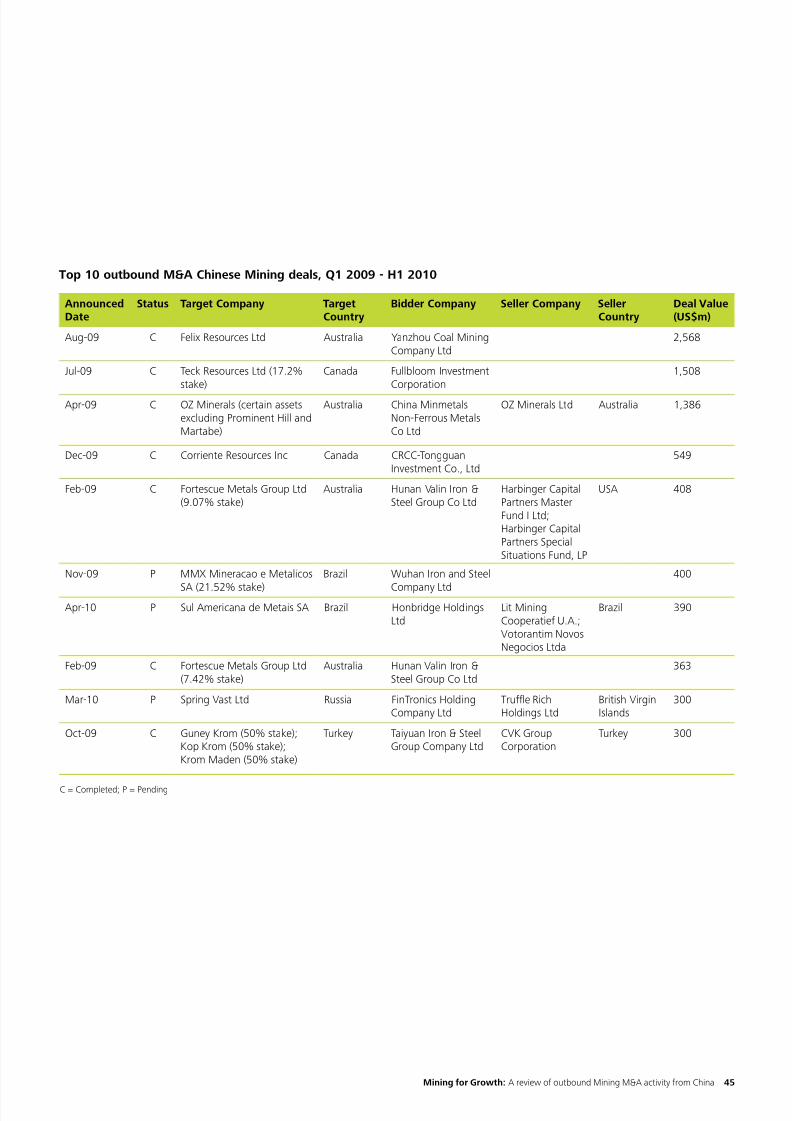

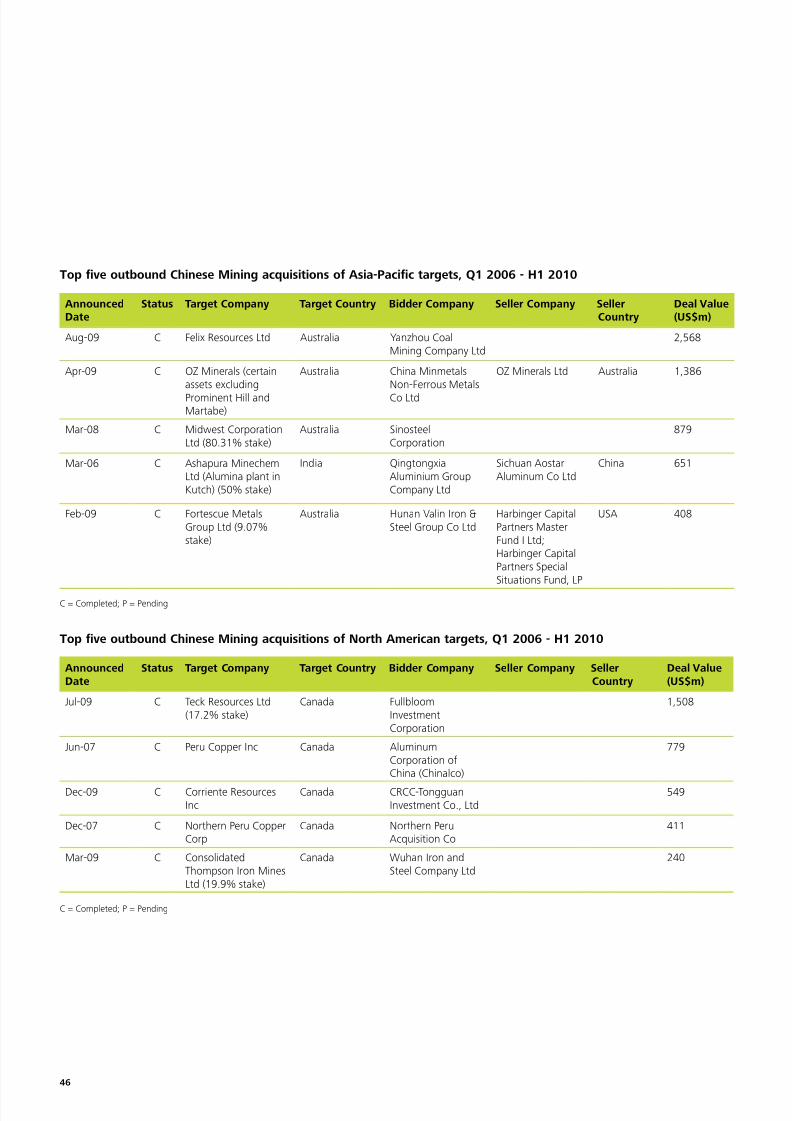

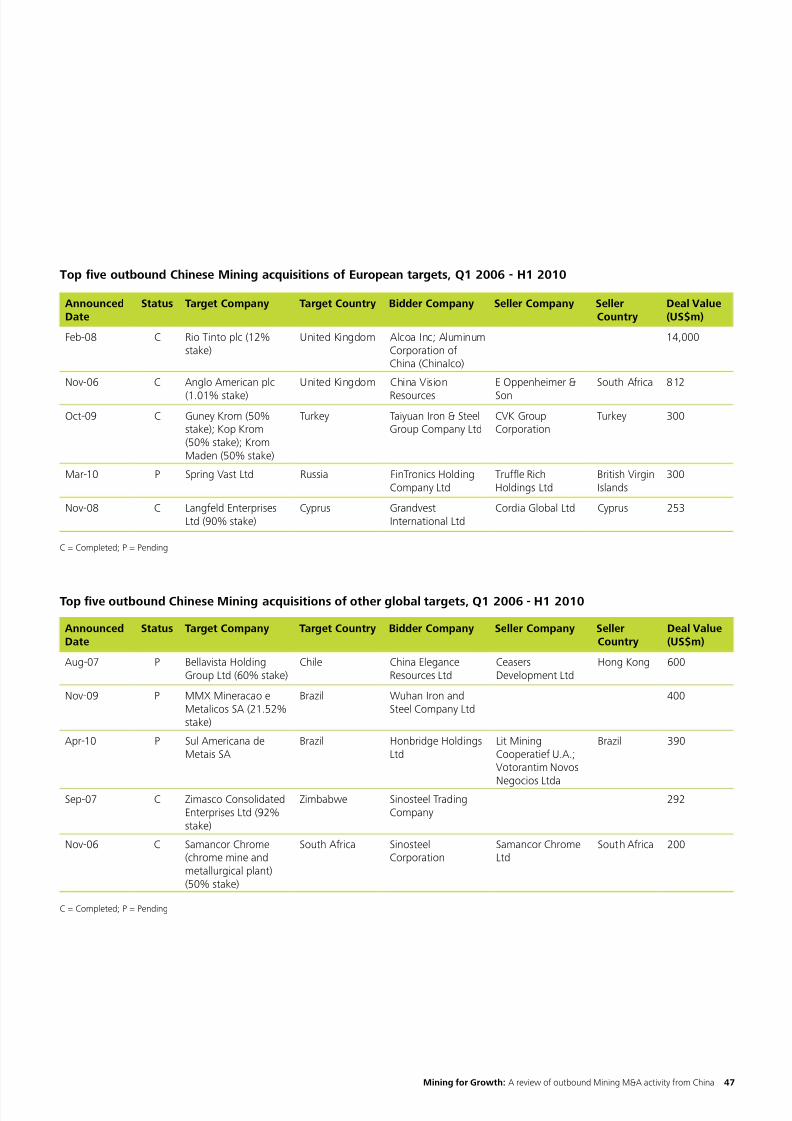

Historical data 44

Deloitte principal contacts 53

End notes 54

Mining or Growth

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 4/564

Executive summaryand methodology

Executive summary

Despite the global nancial crisis, Chineseacquirers have increasingly looked at oreign

Mining targets, with 2009 witnessing a record-

breaking number o transactions, with 33

announced deals worth US$9.2 billion, coming

to market, a marked increase on the 20 deals

seen in 2008. Looking ahead, this trend looksset to continue with a combined 73% o survey

respondents expecting dealmaking in the wider

Chinese Mining sector to increase over thecoming 12 months. More pertinently, 46% o

respondents expect outbound cross-border

activity to drive this increase.

While M&A is undertaken or a number odierent reasons, the need or Chinese companies

to secure supplies o commodities is undoubtedly

the principal driver o this recent wave o activity.

Indeed, 85% o respondents expect this to be

at least a signicant driver o outbound Miningsector deal fow over the next 12 months with

54% considering it the most important reason or

such transactions.

Furthermore, domestic demand or such resourcesis set to rise urther as China’s economic growth

story continues, reinorced by the act that 92%

o respondents consider the country’s economic

outlook to be either positive or very positive.One such respondent qualied this viewpoint by

saying: “There is huge internal demand within

China and this will drive economic growth going

orward.”

Looking at specic sub-sectors within the

Mining space, demand or iron ore is particularly

signicant with it rightly being considered as

one o the key building blocks o the Chinese

economy given the scale o the construction and

inrastructure projects currently being undertaken

there. Aside rom crude oil, iron ore is perhaps the

most important commodity in the world economy

and thereore, it is unsurprising that 69% o

respondents expect metal ore companies to see

the greatest levels o M&A investment in 2010.Although outbound M&A activity is predicted to

increase, the nature o these deals is set to alter

slightly in the coming months. Mining assets in

Australasia have traditionally been most actively

targeted by Chinese acquirers but this could

change with the largest proportion o respondents

(76%) naming Arica as the region expected

to witness the bulk o outbound activity going

orward. The proposed 'super tax' on Australian

Mining company prots, even in its recently

watered-down orm, is obviously a deterrent or

prospective investors, with 81% o respondents

believing that the legislation, slated to come into

law in 2012, will have a negative impact on the

level o Chinese investment in Australasia*.

It is o little surprise that 85% expect businesses

to look to target other regions, with Arica set to

be the main beneciary. Indeed, one respondent

points out that with Arican countries needing

help and inrastructure support, it is "easy to gain

access to their abundant resources by providing

them with help." Corporate valuations are also

playing a key role in this regard with valuationsproving to be robust in the traditional hotbeds

o activity, pushing investment to alternative

locations such as Arica and, to a lesser extent,

South America.

*Respondents answered survey beore revision to the proposed taxwere announced on 2 July 2010.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 5/56Mining or Growth: A review o outbound Mining M&A activity rom China 5

Certainly, the outlook or Chinese outboundinvestment in the Mining niche remains positive,largely underpinned by the continued growtho the domestic economy. However, obstaclesto dealmaking remain, primarily in the orm omacroeconomic uncertainties and exchange rateconcerns, although this will likely be outweighedby the desire to secure inputs at attractive prices.China remains as cash-rich and resource-hungryas ever and these actors will continue to driveMining sector outbound activity over the rest o2010 and into 2011.

Methodology

Over the course o April and June 2010, Remark,the research and publications d ivision o TheMergermarket Group, canvassed the opinionso 26 mainland China-based Mining corporates.All respondents had experience o an M&Atransaction at some stage over the last ve years.They were asked to give their opinions on anumber o issues, including the key opportunitiesand challenges that businesses in the sector acein the current trading environment. All answerswere condential and results have been reportedin aggregate.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 6/566

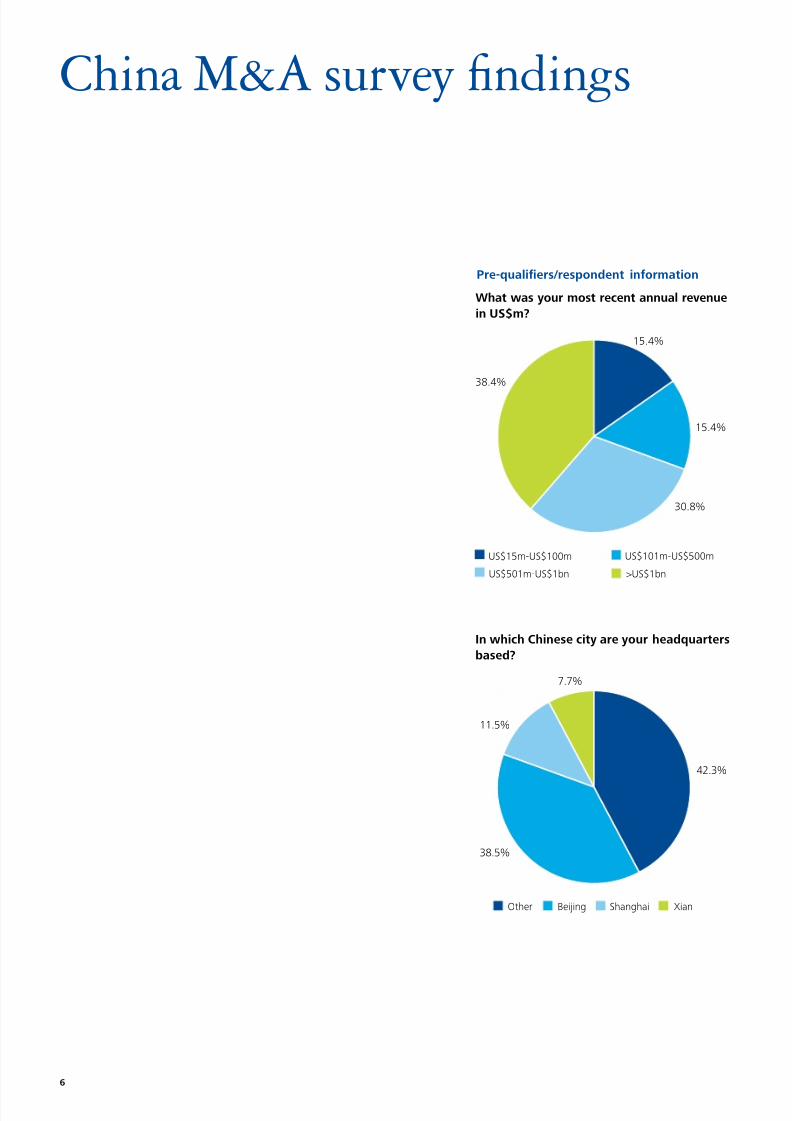

China M&A survey ndings

30.8%

38.4%

15.4%

15.4%

US$15m-US$100m US$101m-US$500m

US$501m-US$1bn >US$1bn

Other XianShanghaiBeijing

38.5%

42.3%

11.5%

7.7%

What was your most recent annual revenuein US$m?

In which Chinese city are your headquartersbased?

Pre-qualiers/respondent inormation

8/8/2019 Deloitte MINING English

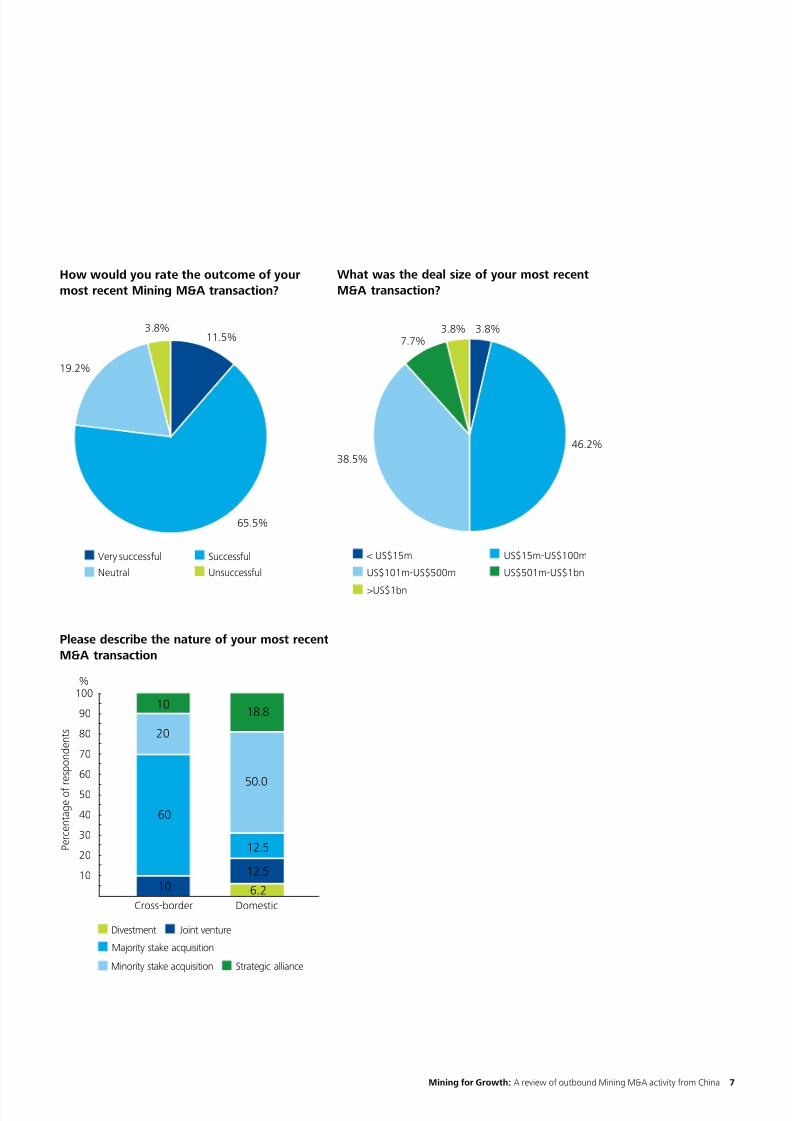

http://slidepdf.com/reader/full/deloitte-mining-english 7/56Mining or Growth: A review o outbound Mining M&A activity rom China 7

38.5%

46.2%

3.8%

< US$15m

US$101m-US$500m

US$15m-US$100m

US$501m-US$1bn

3.8%7.7%

>US$1bn

What was the deal size o your most recentM&A transaction?

6.210

12.5

60

12.5

20

50.0

1018.8

10

20

30

40

50

60

70

80

90

100

Cross-border

P e r c e n t a g e

o f r e s p o n d e n t s

Domestic

%

Divestment Joint venture

Majority stake acquisition

Strategic allianceMinority stake acquisition

Please describe the nature o your most recentM&A transaction

65.5%

3.8%

Very successful

Neutral

Successful

Unsuccessful

11.5%

19.2%

How would you rate the outcome o yourmost recent Mining M&A transaction?

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 8/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 9/56Mining or Growth: A review o outbound Mining M&A activity rom China 9

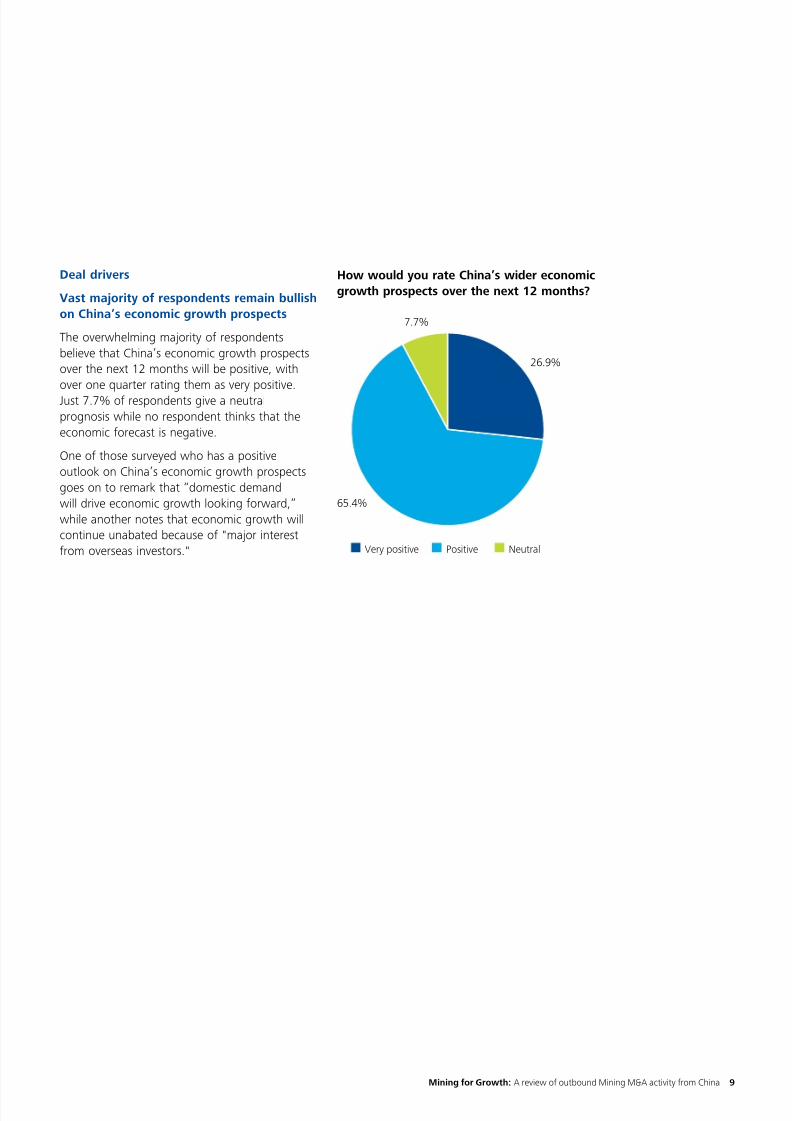

65.4%

Very positive Positive

7.7%

26.9%

Neutral

How would you rate China’s wider economicgrowth prospects over the next 12 months?

Deal drivers

Vast majority o respondents remain bullishon China’s economic growth prospects

The overwhelming majority o respondentsbelieve that China’s economic growth prospectsover the next 12 months will be positive, withover one quarter rating them as very positive.Just 7.7% o respondents give a neutralprognosis while no respondent thinks that theeconomic orecast is negative.

One o those surveyed who has a positiveoutlook on China’s economic growth prospectsgoes on to remark that “domestic demandwill drive economic growth looking orward,”while another notes that economic growth willcontinue unabated because o "major interestrom overseas investors."

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 10/5610

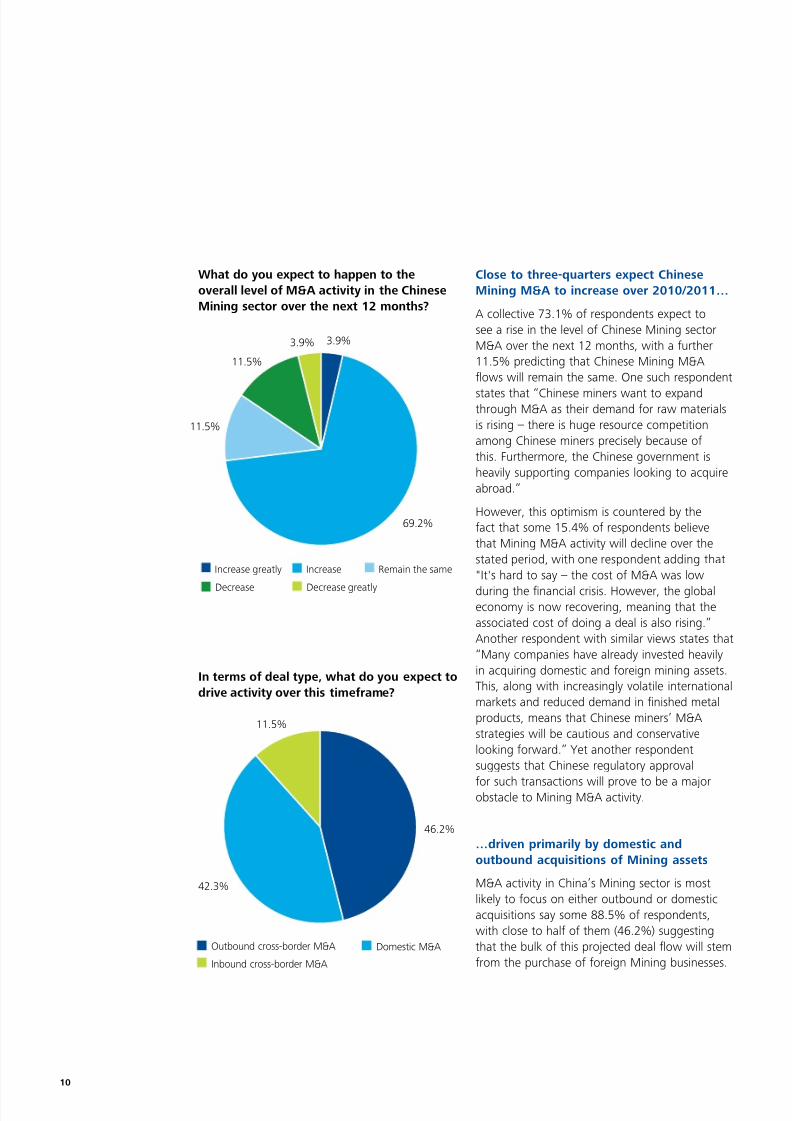

Close to three-quarters expect ChineseMining M&A to increase over 2010/2011…

A collective 73.1% o respondents expect tosee a rise in the level o Chinese Mining sectorM&A over the next 12 months, with a urther11.5% predicting that Chinese Mining M&Afows will remain the same. One such respondent

states that “Chinese miners want to expandthrough M&A as their demand or raw materialsis rising – there is huge resource competitionamong Chinese miners precisely because othis. Furthermore, the Chinese government isheavily supporting companies looking to acquireabroad.”

However, this optimism is countered by theact that some 15.4% o respondents believethat Mining M&A activity will decline over thestated period, with one respondent adding that"It's hard to say – the cost o M&A was low

during the nancial crisis. However, the globaleconomy is now recovering, meaning that theassociated cost o doing a deal is also rising.”Another respondent with similar views states that“Many companies have already invested heavilyin acquiring domestic and oreign mining assets.This, along with increasingly volatile internationalmarkets and reduced demand in nished metalproducts, means that Chinese miners’ M&Astrategies will be cautious and conservativelooking orward.” Yet another respondentsuggests that Chinese regulatory approval

or such transactions will prove to be a majorobstacle to Mining M&A activity.

…driven primarily by domestic andoutbound acquisitions o Mining assets

M&A activity in China’s Mining sector is mostlikely to ocus on either outbound or domesticacquisitions say some 88.5% o respondents,with close to hal o them (46.2%) suggestingthat the bulk o this projected deal fow will stemrom the purchase o oreign Mining businesses.

Increase greatly Increase

Decrease Decrease greatly

69.2%

11.5%

3.9% 3.9%

11.5%

Remain the same

What do you expect to happen to theoverall level o M&A activity in the ChineseMining sector over the next 12 months?

Inbound cross-border M&A

Outbound cross-border M&A Domestic M&A

46.2%

11.5%

42.3%

In terms o deal type, what do you expect todrive activity over this timerame?

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 11/56Mining or Growth: A review o outbound Mining M&A activity rom China 11

34.6

34.6

38.5

69.2

0 10 20 30 40 50 60 70

Coal-mining companies

Other miningsupport companies

Non-metallicore companies

Metallic ore companies

Percentage of respondents

%

(Respondents may have selected multiple answers)

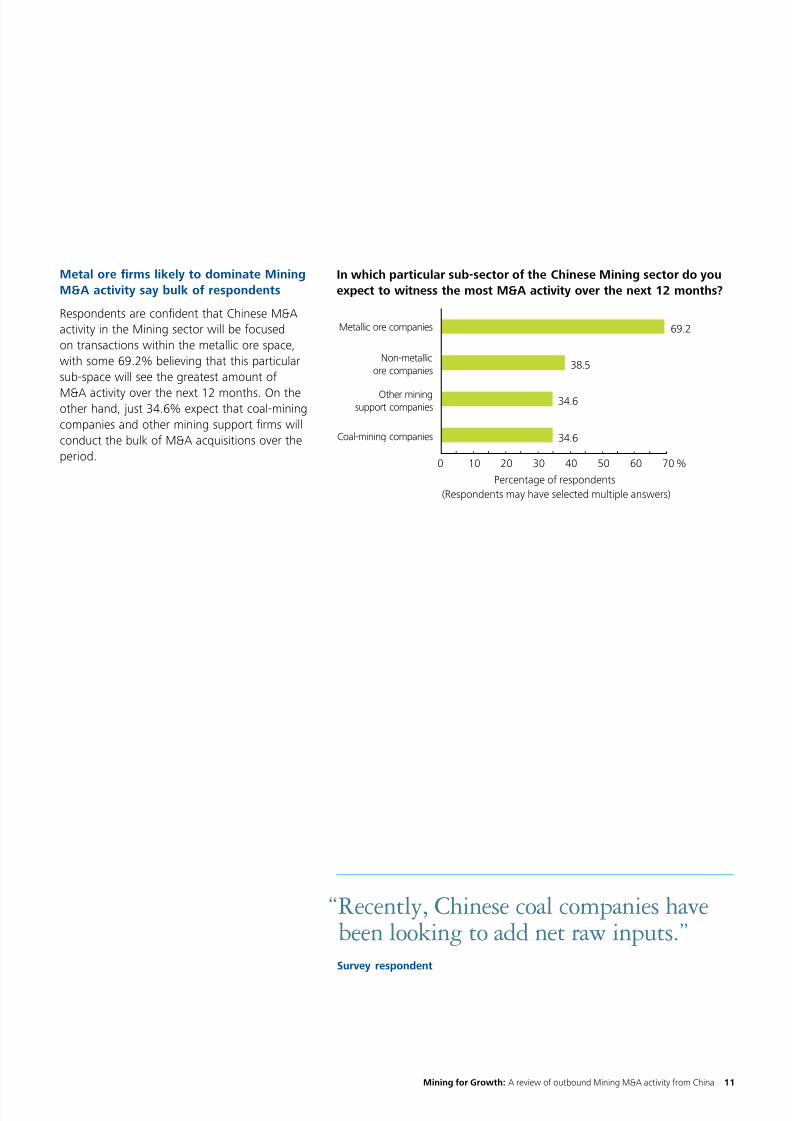

In which particular sub-sector o the Chinese Mining sector do youexpect to witness the most M&A activity over the next 12 months?

Metal ore rms likely to dominate MiningM&A activity say bulk o respondents

Respondents are condent that Chinese M&Aactivity in the Mining sector will be ocusedon transactions within the metallic ore space,with some 69.2% believing that this particularsub-space will see the greatest amount o

M&A activity over the next 12 months. On theother hand, just 34.6% expect that coal-miningcompanies and other mining support rms willconduct the bulk o M&A acquisitions over theperiod.

“Recently, Chinese coal companies havebeen looking to add net raw inputs.”Survey respondent

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 12/5612

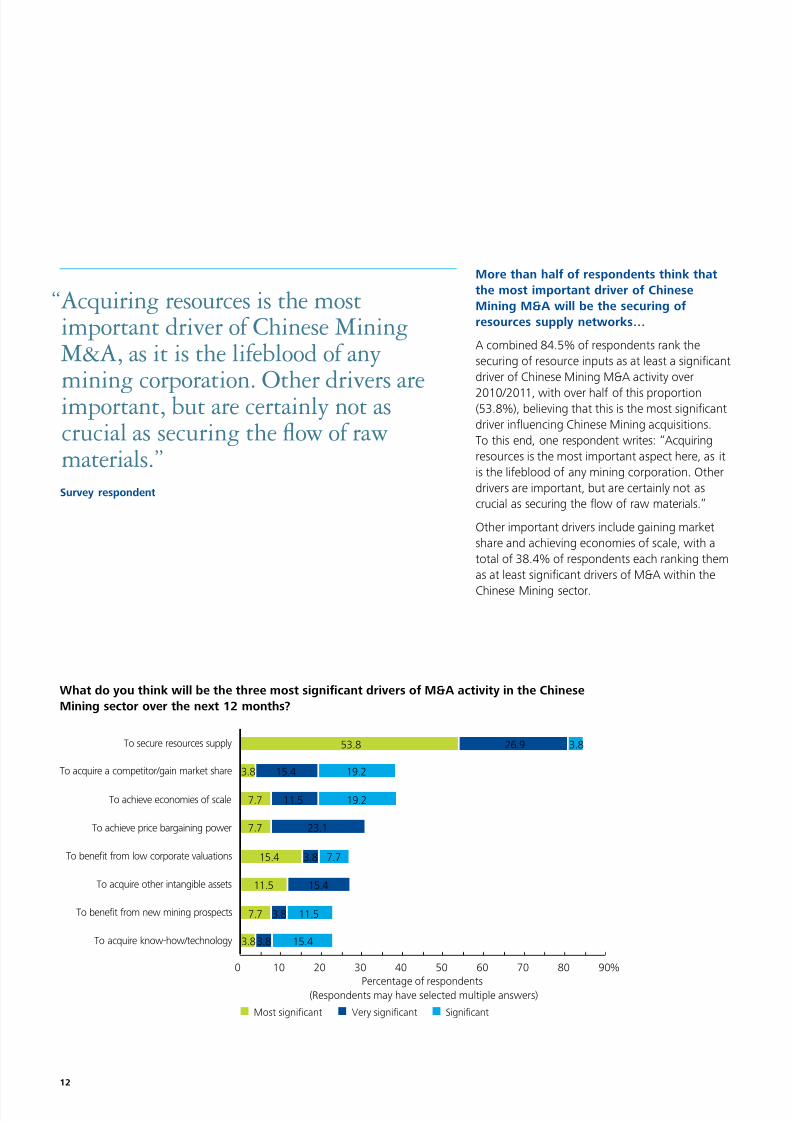

More than hal o respondents think thatthe most important driver o ChineseMining M&A will be the securing oresources supply networks…

A combined 84.5% o respondents rank thesecuring o resource inputs as at least a signicantdriver o Chinese Mining M&A activity over

2010/2011, with over hal o this proportion(53.8%), believing that this is the most signicantdriver infuencing Chinese Mining acquisitions.To this end, one respondent writes: “Acquiringresources is the most important aspect here, as itis the lieblood o any mining corporation. Otherdrivers are important, but are certainly not ascrucial as securing the fow o raw materials.”

Other important drivers include gaining marketshare and achieving economies o scale, with atotal o 38.4% o respondents each ranking themas at least signicant drivers o M&A within the

Chinese Mining sector.

What do you think will be the three most signicant drivers o M&A activity in the ChineseMining sector over the next 12 months?

0 10 20 30 40 50 60 70 80 90

To acquire know-how/technology

To benefit from new mining prospects

To acquire other intangible assets

To benefit from low corporate valuations

To achieve price bargaining power

To achieve economies of scale

To acquire a competitor/gain market share

To secure resources supply

%

53.8 26.9 3.8

Percentage of respondents

3.8 15.4 19.2

7.7 11.5 19.2

7.7 23.1

15.4 3.8 7.7

11.5 15.4

7.7 3.8 11.5

3.83.8 15.4

Most significant Very significant Significant

(Respondents may have selected multiple answers)

“Acquiring resources is the mostimportant driver o Chinese MiningM&A, as it is the lieblood o any

mining corporation. Other drivers areimportant, but are certainly not ascrucial as securing the fow o rawmaterials.”Survey respondent

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 13/56Mining or Growth: A review o outbound Mining M&A activity rom China 13

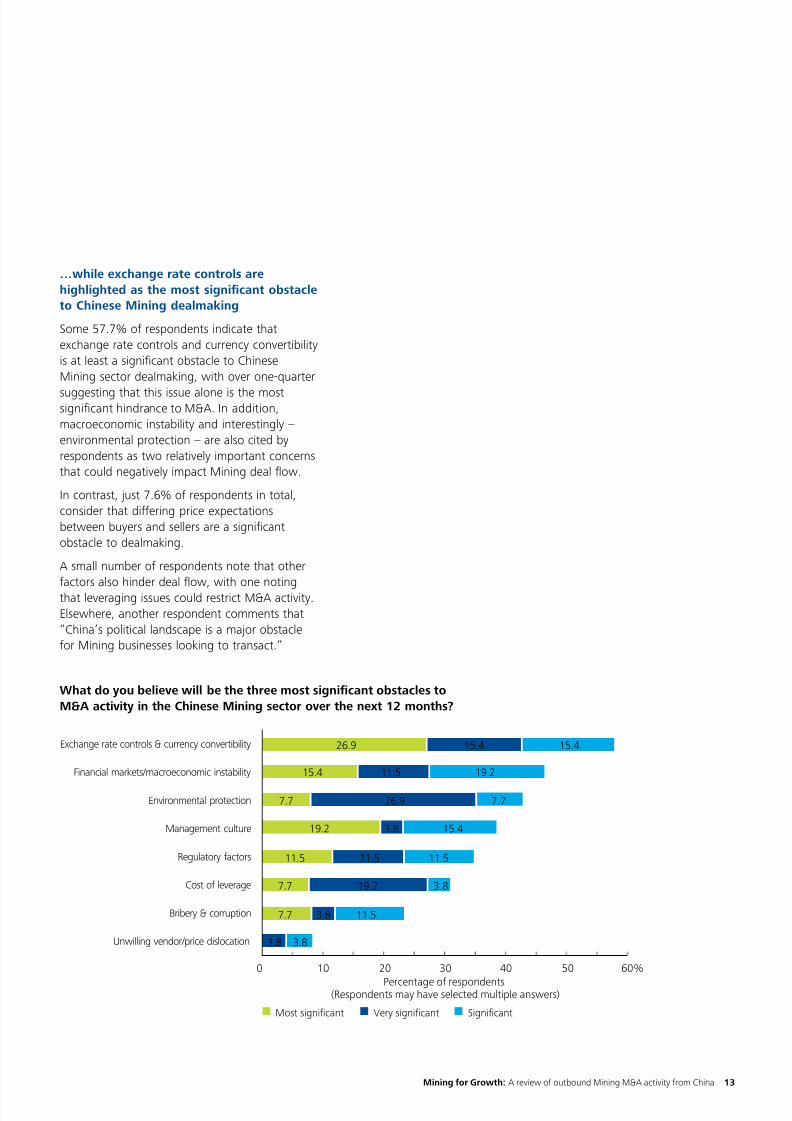

0 10 20 30 40 50 60%

26.9 15.4 15.4

Percentage of respondents

15.4 11.5 19.2

7.7 26.9 7.77.7

15.419.2 3.8

11.5 11.5 11.5

3.87.7 19.2

7.7 3.8 11.5

3.8 3.8Unwilling vendor/price dislocation

Bribery & corruption

Cost of leverage

Regulatory factors

Management culture

Environmental protection

Financial markets/macroeconomic instability

Exchange rate controls & currency convertibility

Most significant Very significant Significant

(Respondents may have selected multiple answers)

What do you believe will be the three most signicant obstacles toM&A activity in the Chinese Mining sector over the next 12 months?

…while exchange rate controls arehighlighted as the most signicant obstacleto Chinese Mining dealmaking

Some 57.7% o respondents indicate thatexchange rate controls and currency convertibilityis at least a signicant obstacle to ChineseMining sector dealmaking, with over one-quarter

suggesting that this issue alone is the mostsignicant hindrance to M&A. In addition,macroeconomic instability and interestingly –environmental protection – are also cited byrespondents as two relatively important concernsthat could negatively impact Mining deal fow.

In contrast, just 7.6% o respondents in total,consider that diering price expectationsbetween buyers and sellers are a signicantobstacle to dealmaking.

A small number o respondents note that otheractors also hinder deal fow, with one notingthat leveraging issues could restrict M&A activity.Elsewhere, another respondent comments that“China’s political landscape is a major obstacleor Mining businesses looking to transact.”

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 14/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 15/56Mining or Growth: A review o outbound Mining M&A activity rom China 15

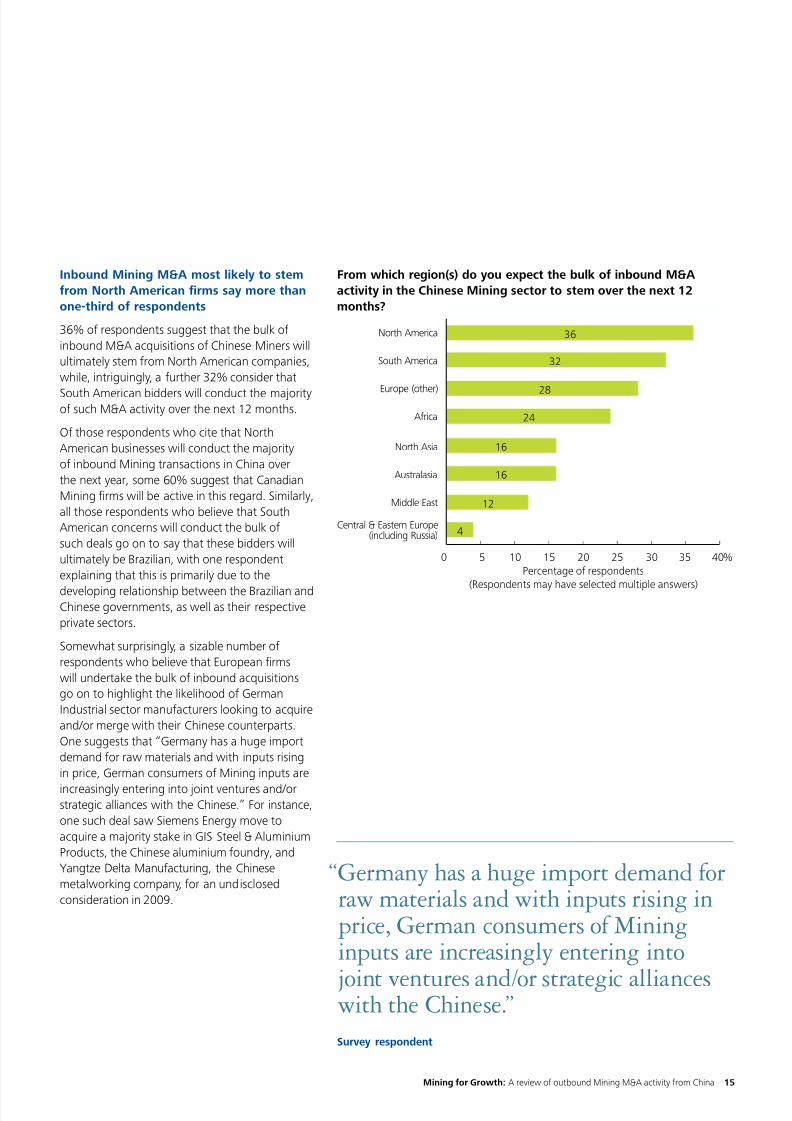

Inbound Mining M&A most likely to stemrom North American rms say more thanone-third o respondents

36% o respondents suggest that the bulk oinbound M&A acquisitions o Chinese Miners willultimately stem rom North American companies,while, intriguingly, a urther 32% consider that

South American bidders will conduct the majorityo such M&A activity over the next 12 months.

O those respondents who cite that NorthAmerican businesses will conduct the majorityo inbound Mining transactions in China overthe next year, some 60% suggest that CanadianMining rms will be active in this regard. Similarly,all those respondents who believe that SouthAmerican concerns will conduct the bulk osuch deals go on to say that these bidders willultimately be Brazilian, with one respondentexplaining that this is primarily due to the

developing relationship between the Brazilian andChinese governments, as well as their respectiveprivate sectors.

Somewhat surprisingly, a sizable number orespondents who believe that European rmswill undertake the bulk o inbound acquisitionsgo on to highlight the likelihood o GermanIndustrial sector manuacturers looking to acquireand/or merge with their Chinese counterparts.One suggests that “Germany has a huge importdemand or raw materials and with inputs risingin price, German consumers o Mining inputs are

increasingly entering into joint ventures and/orstrategic alliances with the Chinese.” For instance,one such deal saw Siemens Energy move toacquire a majority stake in GIS Steel & AluminiumProducts, the Chinese aluminium oundry, andYangtze Delta Manuacturing, the Chinesemetalworking company, or an undisclosedconsideration in 2009.

0 5 10 15 20 25 30 35 40%

36

Percentage of respondents

(Respondents may have selected multiple answers)

32

28

24

16

16

12

4Central & Eastern Europe

(including Russia)

Middle East

Australasia

North Asia

Africa

Europe (other)

South America

North America

From which region(s) do you expect the bulk o inbound M&Aactivity in the Chinese Mining sector to stem over the next 12months?

“Germany has a huge import demand orraw materials and with inputs rising inprice, German consumers o Mininginputs are increasingly entering into

joint ventures and/or strategic allianceswith the Chinese.”

Survey respondent

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 16/5616

0 10 20 30 40 50 60 70 80%

76

Percentage of respondents

(Respondents may have selected multiple answers)

44

24

20

8

8

4

4Central & Eastern Europe

(including Russia)

Middle East

Europe (other)

North Asia

South America

North America

Australasia

Africa

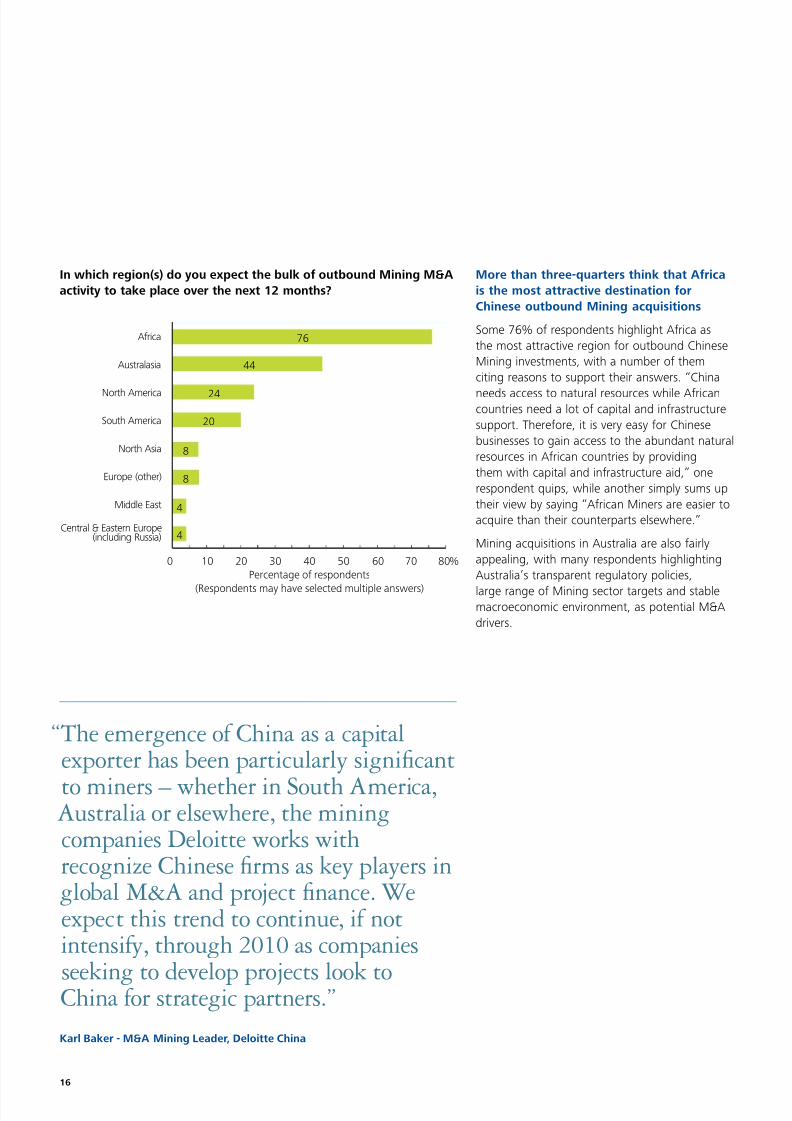

In which region(s) do you expect the bulk o outbound Mining M&Aactivity to take place over the next 12 months?

More than three-quarters think that Aricais the most attractive destination orChinese outbound Mining acquisitions

Some 76% o respondents highlight Arica asthe most attractive region or outbound ChineseMining investments, with a number o themciting reasons to support their answers. “China

needs access to natural resources while Aricancountries need a lot o capital and inrastructuresupport. Thereore, it is very easy or Chinesebusinesses to gain access to the abundant naturalresources in Arican countries by providingthem with capital and inrastructure aid,” onerespondent quips, while another simply sums uptheir view by saying “Arican Miners are easier toacquire than their counterparts elsewhere.”

Mining acquisitions in Australia are also airlyappealing, with many respondents highlightingAustralia’s transparent regulatory policies,

large range o Mining sector targets and stablemacroeconomic environment, as potential M&Adrivers.

“The emergence o China as a capitalexporter has been particularly signicant

to miners – whether in South America,Australia or elsewhere, the miningcompanies Deloitte works withrecognize Chinese rms as key players inglobal M&A and project nance. Weexpect this trend to continue, i notintensiy, through 2010 as companies

seeking to develop projects look toChina or strategic partners.”

Karl Baker - M&A Mining Leader, Deloitte China

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 17/56Mining or Growth: A review o outbound Mining M&A activity rom China 17

Nearly two-thirds o respondents expectprivate equity dealmaking in the ChineseMining space to increase

A combined 65.4% o respondents believe thatprivate equity dealmaking in the Mining sectorwill rise over the next 12 months, while just11.5% consider that private equity interest in

the sector will decrease. The remaining 23.1%o respondents think that deal fows will stay thesame.

One respondent who alls into the latter categoryexplains that “private equity investors are stillcautious o investing in the Mining sector due tomarket uncertainty. At the same time, they also donot want to lose out on the opportunity to investin the sector due to its buoyant undamentals.”

Local private equity players likely to lead

any upcoming increase, say respondents

Interestingly, nearly two-thirds (64%) orespondents believe that any increase in privateequity dealmaking within the Chinese Miningspace will predominantly stem rom localnancial investors, with one respondent goingon to explain that “local private equity rmsunderstand the Chinese Mining market very welland they want to be able to ully exploit anyuture opportunities."

Increase significantly Increase slightly

Remain the same Decrease slightly

50.0%

15.4%11.5%

23.1%

What do you expect to happen to the levelo private equity activity in the ChineseMining sector over the next 12 months?

Foreign private equity firmsLocal private equity firms

64%

36%

Do you think over the next 12 months, themajority o this interest will stem rom localprivate equity groups or oreign nancialinvestors?

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 18/5618

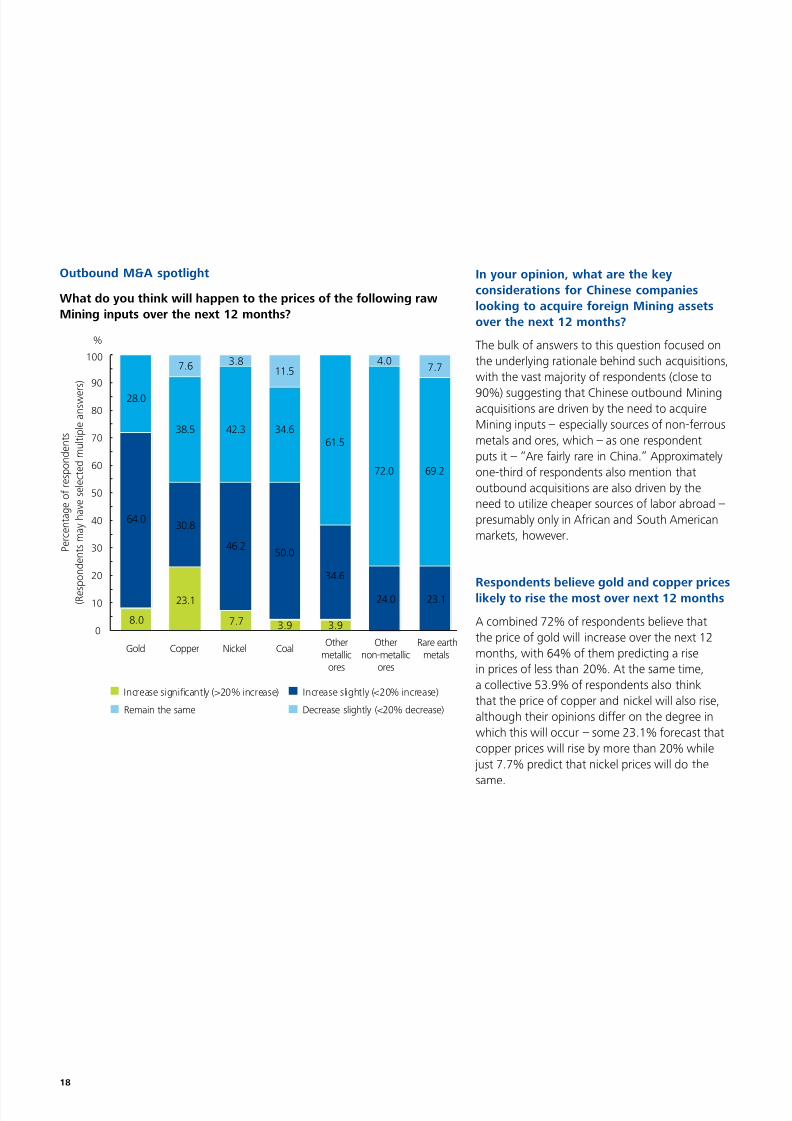

In your opinion, what are the keyconsiderations or Chinese companieslooking to acquire oreign Mining assetsover the next 12 months?

The bulk o answers to this question ocused onthe underlying rationale behind such acquisitions,with the vast majority o respondents (close to

90%) suggesting that Chinese outbound Miningacquisitions are driven by the need to acquireMining inputs – especially sources o non-errousmetals and ores, which – as one respondentputs it – “Are airly rare in China.” Approximatelyone-third o respondents also mention thatoutbound acquisitions are also driven by theneed to utilize cheaper sources o labor abroad –presumably only in Arican and South Americanmarkets, however.

Respondents believe gold and copper priceslikely to rise the most over next 12 months

A combined 72% o respondents believe thatthe price o gold will increase over the next 12months, with 64% o them predicting a risein prices o less than 20%. At the same time,a collective 53.9% o respondents also thinkthat the price o copper and nickel will also rise,although their opinions dier on the degree inwhich this will occur – some 23.1% orecast thatcopper prices will rise by more than 20% while just 7.7% predict that nickel prices will do the

same.

8.0

64.0

28.0

23.1

30.8

38.5

7.6

7.7

46.2

42.3

3.8

3.9

50.0

34.6

11.5

24.0

72.0

4.0

23.1

69.2

7.7

3.9

34.6

61.5

P e r c e n t a g e o f r e s p o n d e n t s

( R e s

p o n d e n t s m a y h a v e s e l e c t e d m u l t i p l e a n s w e r s )

0

10

20

30

40

50

60

70

80

90

100

%

Othernon-metallic

ores

Rare earthmetals

Othermetallic

ores

CoalNickelCopperGold

Increase significantly (>20% increase) Increase slightly (<20% increase)

Remain the same Decrease slightly (<20% decrease)

What do you think will happen to the prices o the ollowing rawMining inputs over the next 12 months?

Outbound M&A spotlight

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 19/56Mining or Growth: A review o outbound Mining M&A activity rom China 19

Very significantly

Not very significantly

Significantly

73.1%

11.5%15.4%

To what extent will the price o these inputsdetermine the level o outbound ChineseMining acquisitions over 2010?

Just less than 90% suggest thatinput prices play an important rolein determining the level o outboundacquisitions over 2010

A total o 88.5% o respondents consider thatMining input prices play a signicant role indetermining the level o outbound Mining

acquisitions over 2010, with 15.4% o thembelieving that price changes signicantlyimpact outbound Mining deal fow. One suchrespondent writes that “Rises in input pricescauses demand to all and lowers targetvaluations, which should positively impact thenumber o M&A transactions taking place.”

The bulk o respondents believe thatregulatory regimes impede outboundMining acquisitions

69.2% o respondents believe regulatory issuesare a signicant hindrance to acquisitive ChineseMiners looking to buy abroad, with respondentspointing the nger at a variety o regulators. Onerespondent believes that local regulators "Havedelayed previous transactions." Another suggeststhat North American and Australian regulatoryauthorities employ airly stringent antitrust policieswhile yet another goes on to state that this hasa knock-on impact on M&A regulatory situationsin other regions such as Arica. Finally onerespondent adopts a d ierent approach, stating

that more onerous environmental and qualitycontrol regulatory regimes abroad will increasinglyimpact on Chinese outbound Mining acquisitions.

Yes No

69.2%

30.8%

Do you believe regulatory issues are asignicant challenge to Chinese Miningcompanies looking to undertake dealsabroad?

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 20/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 21/56Mining or Growth: A review o outbound Mining M&A activity rom China 21

0 10 20 30 40 50 60 70 80 90%

Percentage of respondents

31.6 26.3

26.3 15.8

15.8 31.6

21.1 21.1

Most significant Very significant Significant

15.8

26.3

26.3

21.1Australian regulators

EU regulators

North American

regulators

Chinese regulators

(Respondents may have selected multiple answers)

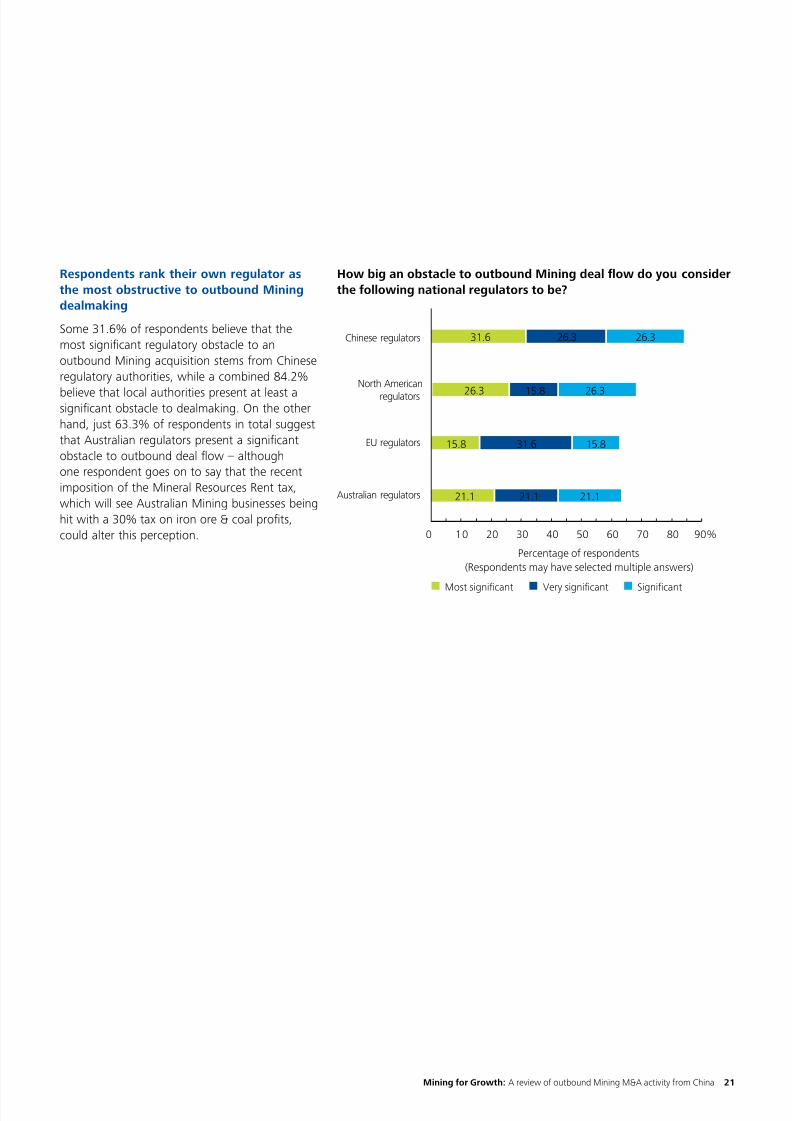

How big an obstacle to outbound Mining deal fow do you considerthe ollowing national regulators to be?

Respondents rank their own regulator asthe most obstructive to outbound Miningdealmaking

Some 31.6% o respondents believe that themost signicant regulatory obstacle to anoutbound Mining acquisition stems rom Chineseregulatory authorities, while a combined 84.2%

believe that local authorities present at least asignicant obstacle to dealmaking. On the otherhand, just 63.3% o respondents in total suggestthat Australian regulators present a signicantobstacle to outbound deal fow – althoughone respondent goes on to say that the recentimposition o the Mineral Resources Rent tax,which will see Australian Mining businesses beinghit with a 30% tax on iron ore & coal prots,could alter this perception.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 22/5622

0 10 20 30 40 50 60 %

Percentage of respondents(Respondents may have selected multiple answers)

57.7

26.9

19.2

11.5Commercial paper

IPO

Shares

Cash

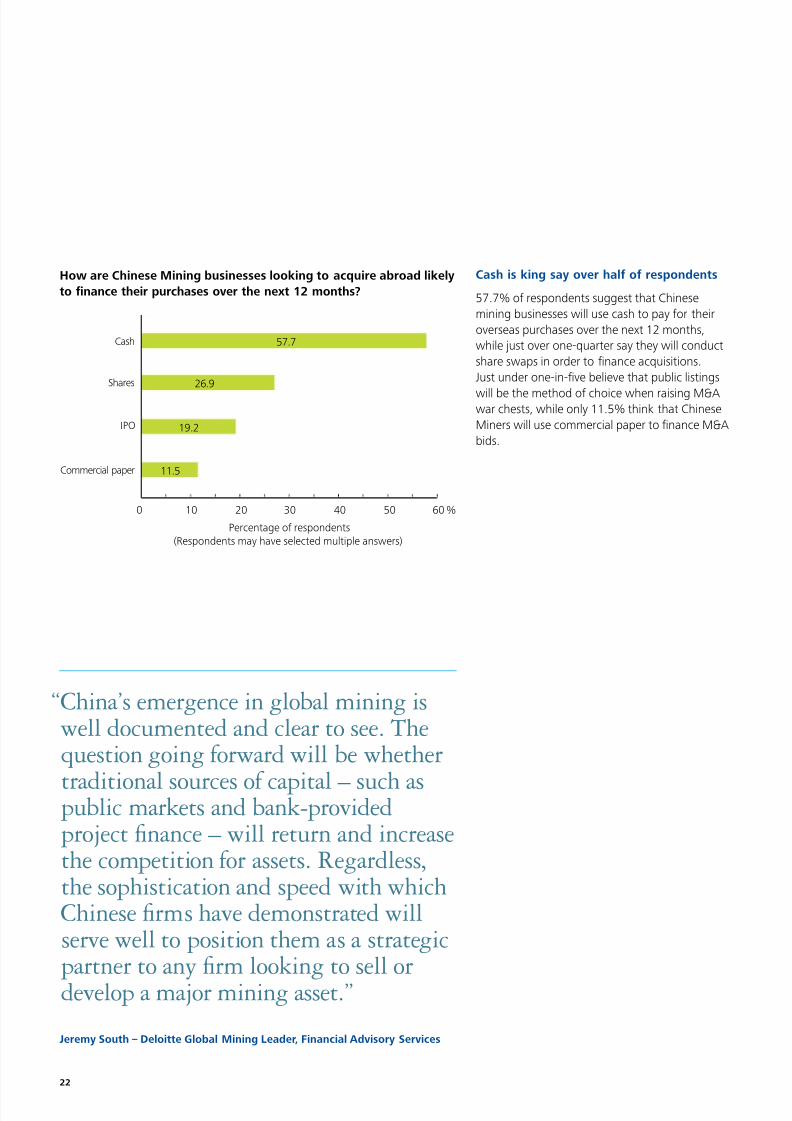

How are Chinese Mining businesses looking to acquire abroad likelyto nance their purchases over the next 12 months?

Cash is king say over hal o respondents

57.7% o respondents suggest that Chinesemining businesses will use cash to pay or theiroverseas purchases over the next 12 months,while just over one-quarter say they will conductshare swaps in order to nance acquisitions.Just under one-in-ve believe that public listings

will be the method o choice when raising M&Awar chests, while only 11.5% think that ChineseMiners will use commercial paper to nance M&Abids.

“China’s emergence in global mining iswell documented and clear to see. Thequestion going orward will be whether

traditional sources o capital – such aspublic markets and bank-providedproject nance – will return and increasethe competition or assets. Regardless,the sophistication and speed with whichChinese rms have demonstrated willserve well to position them as a strategicpartner to any rm looking to sell ordevelop a major mining asset.”

Jeremy South – Deloitte Global Mining Leader, Financial Advisory Services

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 23/56Mining or Growth: A review o outbound Mining M&A activity rom China 23

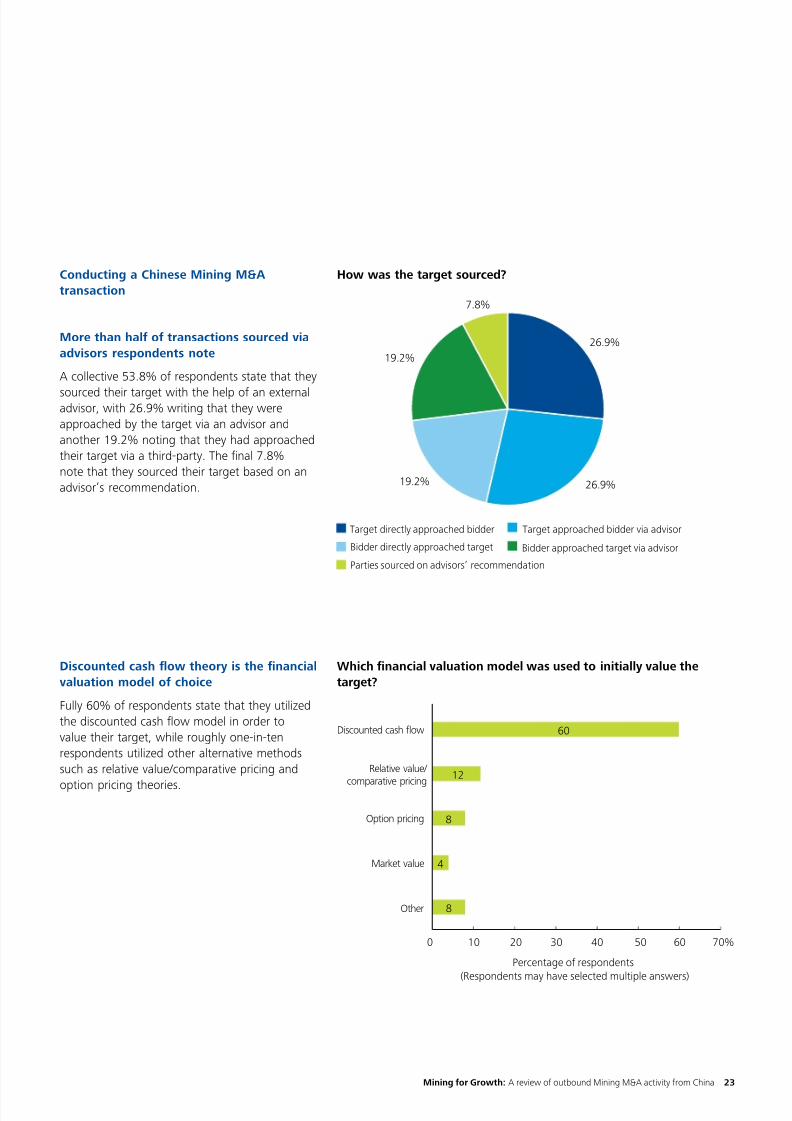

Discounted cash fow theory is the nancialvaluation model o choice

Fully 60% o respondents state that they utilizedthe discounted cash fow model in order tovalue their target, while roughly one-in-tenrespondents utilized other alternative methodssuch as relative value/comparative pricing and

option pricing theories.

Target directly approached bidder Target approached bidder via advisor

Bidder directly approached target

26.9%19.2%

7.8%

26.9%

19.2%

Bidder approached target via advisor

Parties sourced on advisors’ recommendation

How was the target sourced?

8

4

8

12

60

0 10 20 30 40 50 7060 %

Percentage of respondents

(Respondents may have selected multiple answers)

Other

Market value

Option pricing

Relative value/

comparative pricing

Discounted cash flow

Which nancial valuation model was used to initially value thetarget?

Conducting a Chinese Mining M&Atransaction

More than hal o transactions sourced viaadvisors respondents note

A collective 53.8% o respondents state that they

sourced their target with the help o an externaladvisor, with 26.9% writing that they wereapproached by the target via an advisor andanother 19.2% noting that they had approachedtheir target via a third-party. The nal 7.8%note that they sourced their target based on anadvisor’s recommendation.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 24/5624

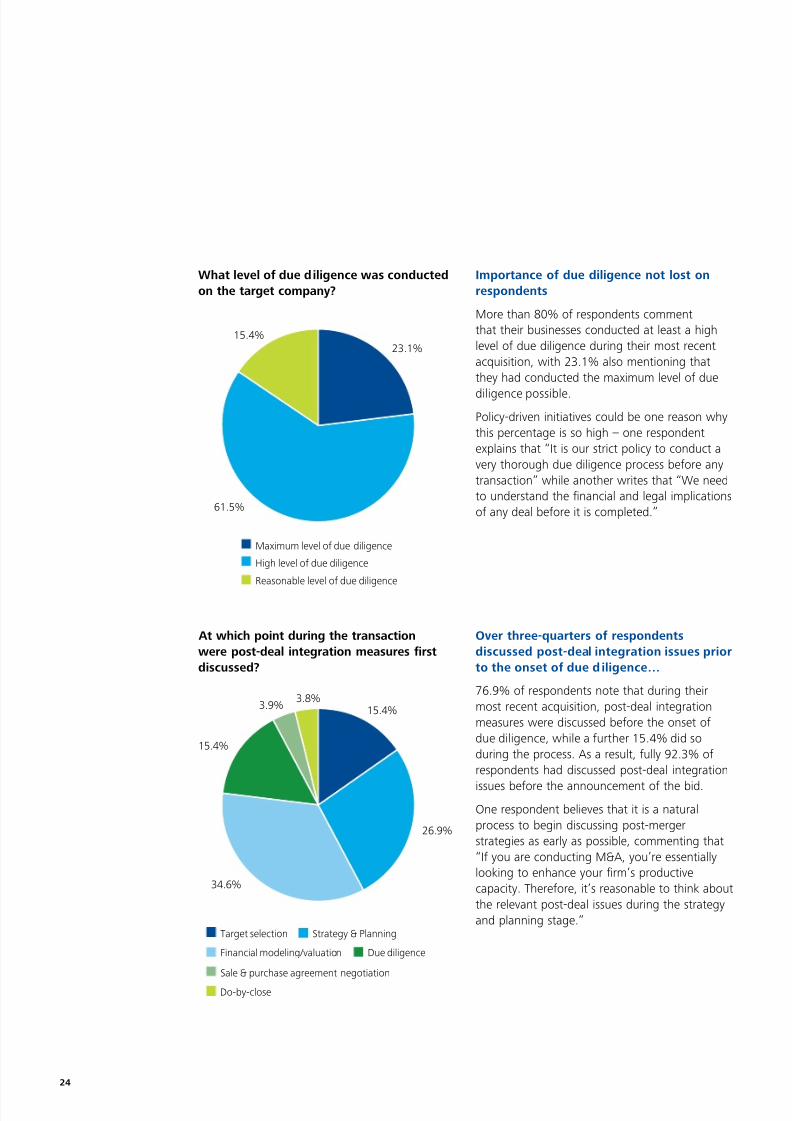

Maximum level of due diligence

High level of due diligence

Reasonable level of due diligence

61.5%

15.4%23.1%

What level o due diligence was conductedon the target company?

Importance o due diligence not lost onrespondents

More than 80% o respondents commentthat their businesses conducted at least a highlevel o due diligence during their most recentacquisition, with 23.1% also mentioning thatthey had conducted the maximum level o due

diligence possible.

Policy-driven initiatives could be one reason whythis percentage is so high – one respondentexplains that “It is our strict policy to conduct avery thorough due diligence process beore anytransaction” while another writes that “We needto understand the nancial and legal implicationso any deal beore it is completed.”

Do-by-close

Sale & purchase agreement negotiation

Due diligence

34.6%

15.4%3.9%3.8%

15.4%

26.9%

Target selection Strategy & Planning

Financial modeling/valuation

At which point during the transactionwere post-deal integration measures rstdiscussed?

Over three-quarters o respondentsdiscussed post-deal integration issues priorto the onset o due d iligence…

76.9% o respondents note that during theirmost recent acquisition, post-deal integrationmeasures were discussed beore the onset odue diligence, while a urther 15.4% did soduring the process. As a result, ully 92.3% orespondents had discussed post-deal integration

issues beore the announcement o the bid.

One respondent believes that it is a naturalprocess to begin discussing post-mergerstrategies as early as possible, commenting that“I you are conducting M&A, you’re essentiallylooking to enhance your rm’s productivecapacity. Thereore, it’s reasonable to think aboutthe relevant post-deal issues during the strategyand planning stage.”

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 25/56Mining or Growth: A review o outbound Mining M&A activity rom China 25

During the strategy/planning phase of the transaction

During the due diligence phase

40%

8%

12%

40%

Before the deal announcement

Never

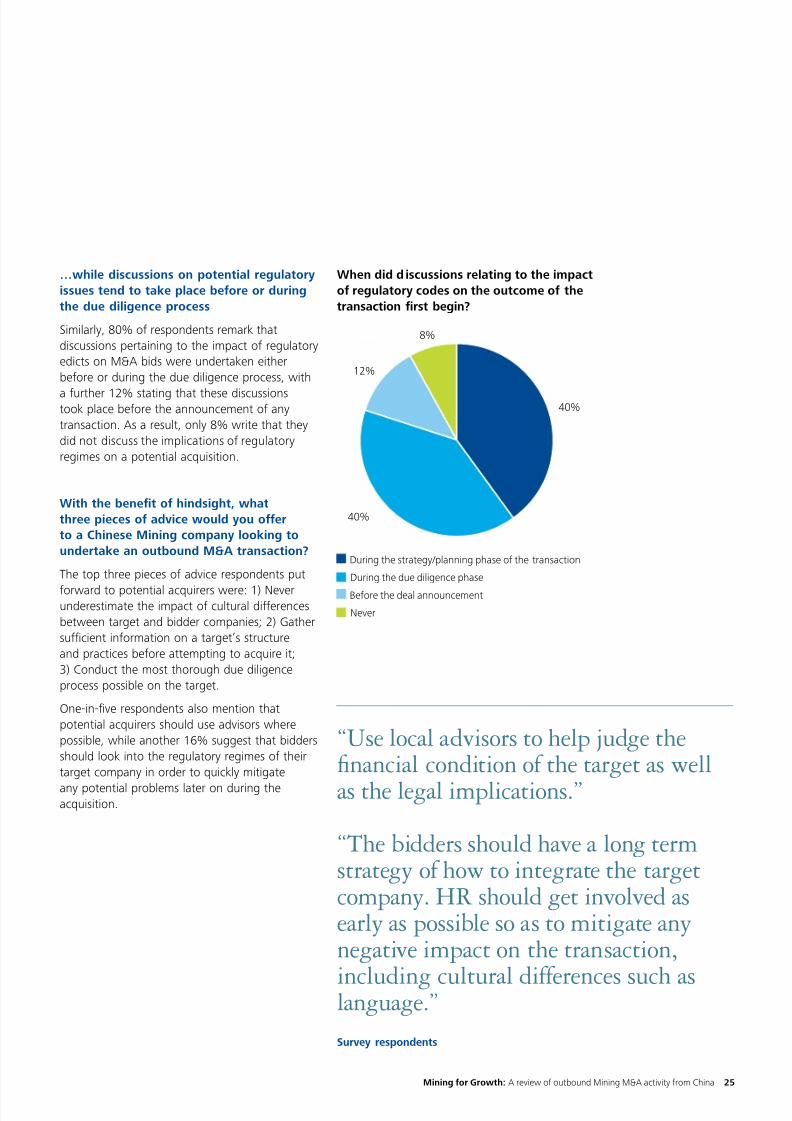

When did d iscussions relating to the impacto regulatory codes on the outcome o thetransaction rst begin?

…while discussions on potential regulatoryissues tend to take place beore or duringthe due diligence process

Similarly, 80% o respondents remark thatdiscussions pertaining to the impact o regulatoryedicts on M&A bids were undertaken eitherbeore or during the due diligence process, with

a urther 12% stating that these discussionstook place beore the announcement o anytransaction. As a result, only 8% write that theydid not discuss the implications o regulatoryregimes on a potential acquisition.

With the benet o hindsight, whatthree pieces o advice would you oerto a Chinese Mining company looking toundertake an outbound M&A transaction?

The top three pieces o advice respondents put

orward to potential acquirers were: 1) Neverunderestimate the impact o cultural dierencesbetween target and bidder companies; 2) Gathersucient inormation on a target’s structureand practices beore attempting to acquire it;3) Conduct the most thorough due diligenceprocess possible on the target.

One-in-ve respondents also mention thatpotential acquirers should use advisors wherepossible, while another 16% suggest that biddersshould look into the regulatory regimes o theirtarget company in order to quickly mitigate

any potential problems later on during theacquisition.

“Use local advisors to help judge thenancial condition o the target as well

as the legal implications.”

“The bidders should have a long termstrategy o how to integrate the targetcompany. HR should get involved asearly as possible so as to mitigate anynegative impact on the transaction,

including cultural dierences such aslanguage.”

Survey respondents

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 26/5626

A significant negative impactA slight negative impact

42.3%

15.4%19.2%

23.1%

A negative impactNo impact

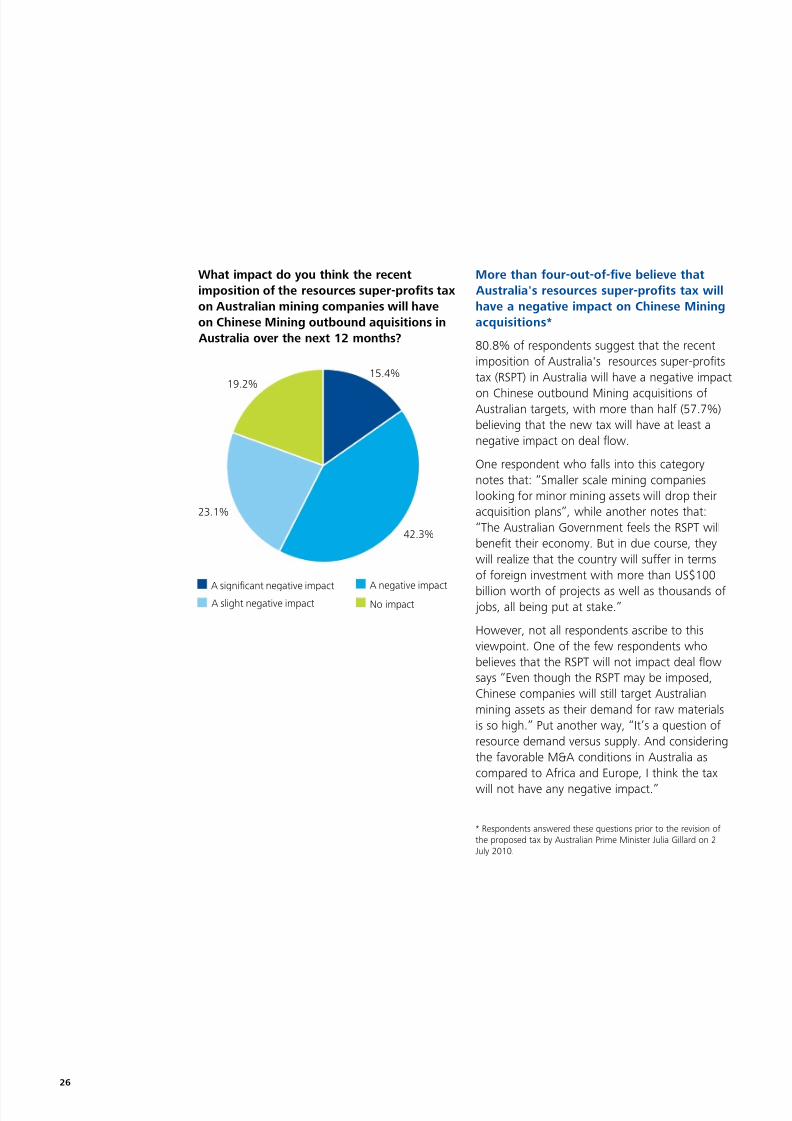

What impact do you think the recentimposition o the resources super-prots taxon Australian mining companies will haveon Chinese Mining outbound aquisitions in Australia over the next 12 months?

More than our-out-o-ve believe that Australia's resources super-prots tax willhave a negative impact on Chinese Miningacquisitions*

80.8% o respondents suggest that the recentimposition o Australia's resources super-protstax (RSPT) in Australia will have a negative impact

on Chinese outbound Mining acquisitions oAustralian targets, with more than hal (57.7%)believing that the new tax will have at least anegative impact on deal fow.

One respondent who alls into this categorynotes that: “Smaller scale mining companieslooking or minor mining assets will drop theiracquisition plans”, while another notes that:“The Australian Government eels the RSPT willbenet their economy. But in due course, theywill realize that the country will suer in termso oreign investment with more than US$100

billion worth o projects as well as thousands o jobs, all being put at stake.”

However, not all respondents ascribe to thisviewpoint. One o the ew respondents whobelieves that the RSPT will not impact deal fowsays “Even though the RSPT may be imposed,Chinese companies will still target Australianmining assets as their demand or raw materialsis so high.” Put another way, “It’s a question oresource demand versus supply. And consideringthe avorable M&A conditions in Australia ascompared to Arica and Europe, I think the tax

will not have any negative impact.”

* Respondents answered these questions prior to the revision othe proposed tax by Australian Prime Minister Julia Gillard on 2July 2010.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 27/56Mining or Growth: A review o outbound Mining M&A activity rom China 27

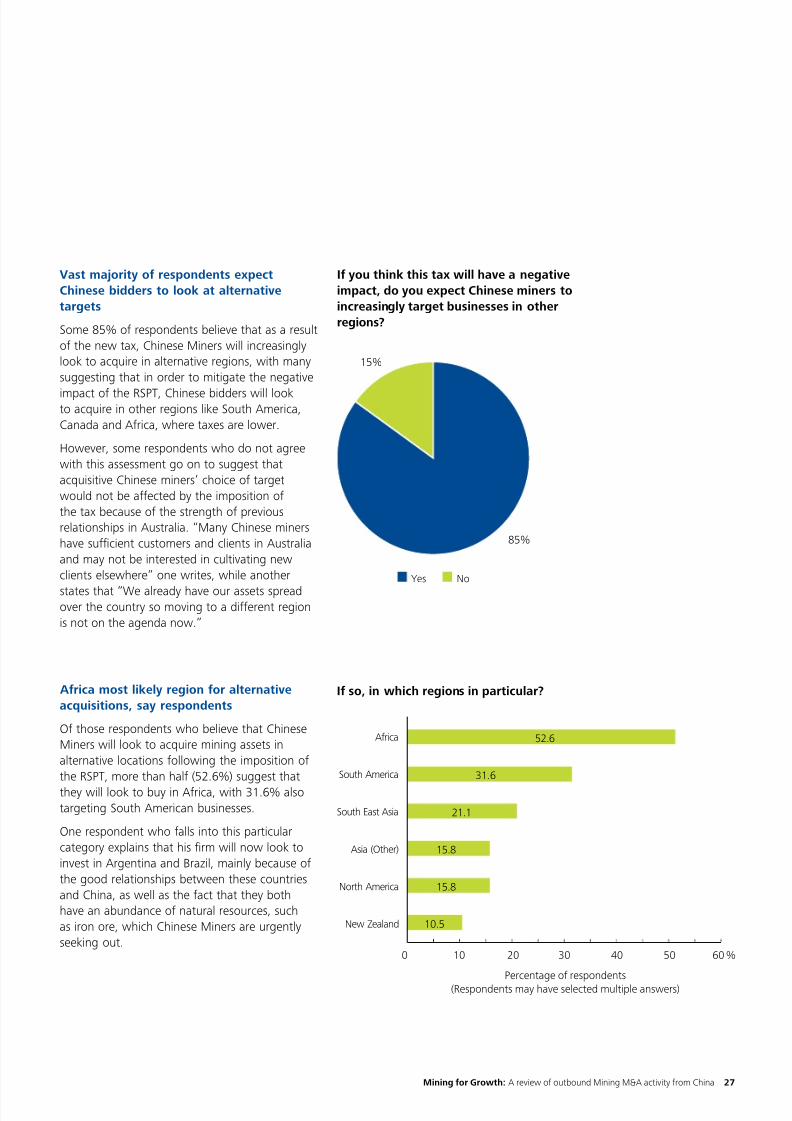

Vast majority o respondents expectChinese bidders to look at alternativetargets

Some 85% o respondents believe that as a resulto the new tax, Chinese Miners will increasinglylook to acquire in alternative regions, with manysuggesting that in order to mitigate the negative

impact o the RSPT, Chinese bidders will lookto acquire in other regions like South America,Canada and Arica, where taxes are lower.

However, some respondents who do not agreewith this assessment go on to suggest thatacquisitive Chinese miners’ choice o targetwould not be aected by the imposition othe tax because o the strength o previousrelationships in Australia. “Many Chinese minershave sucient customers and clients in Australiaand may not be interested in cultivating newclients elsewhere” one writes, while another

states that “We already have our assets spreadover the country so moving to a dierent regionis not on the agenda now.”

Yes No

85%

15%

I you think this tax will have a negativeimpact, do you expect Chinese miners toincreasingly target businesses in otherregions?

Arica most likely region or alternativeacquisitions, say respondents

O those respondents who believe that ChineseMiners will look to acquire mining assets inalternative locations ollowing the imposition othe RSPT, more than hal (52.6%) suggest thatthey will look to buy in Arica, with 31.6% alsotargeting South American businesses.

One respondent who alls into this particularcategory explains that his rm will now look toinvest in Argentina and Brazil, mainly because othe good relationships between these countriesand China, as well as the act that they bothhave an abundance o natural resources, suchas iron ore, which Chinese Miners are urgentlyseeking out.

New Zealand

North America

Asia (Other)

South East Asia

South America

Africa

10.5

15.8

15.8

31.6

21.1

0 10 20 30 40 50 60 %

Percentage of respondents

(Respondents may have selected multiple answers)

52.6

I so, in which regions in particular?

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 28/5628

An interview with Deloitte China's Mining

sector Partner

Karl Baker, Mining sector M&A Partner at

Deloitte China, expects to see a growing

trend o outbound M&A investments

stemming rom China over 2010. Going

orward, Chinese rms are likely to make

urther Arican and South AmericanMining plays as well as in historially-more

prominent Australia and Canada, primarily

driven by the need to secure supplies o

inputs at attractive prices.

Outbound M&A review

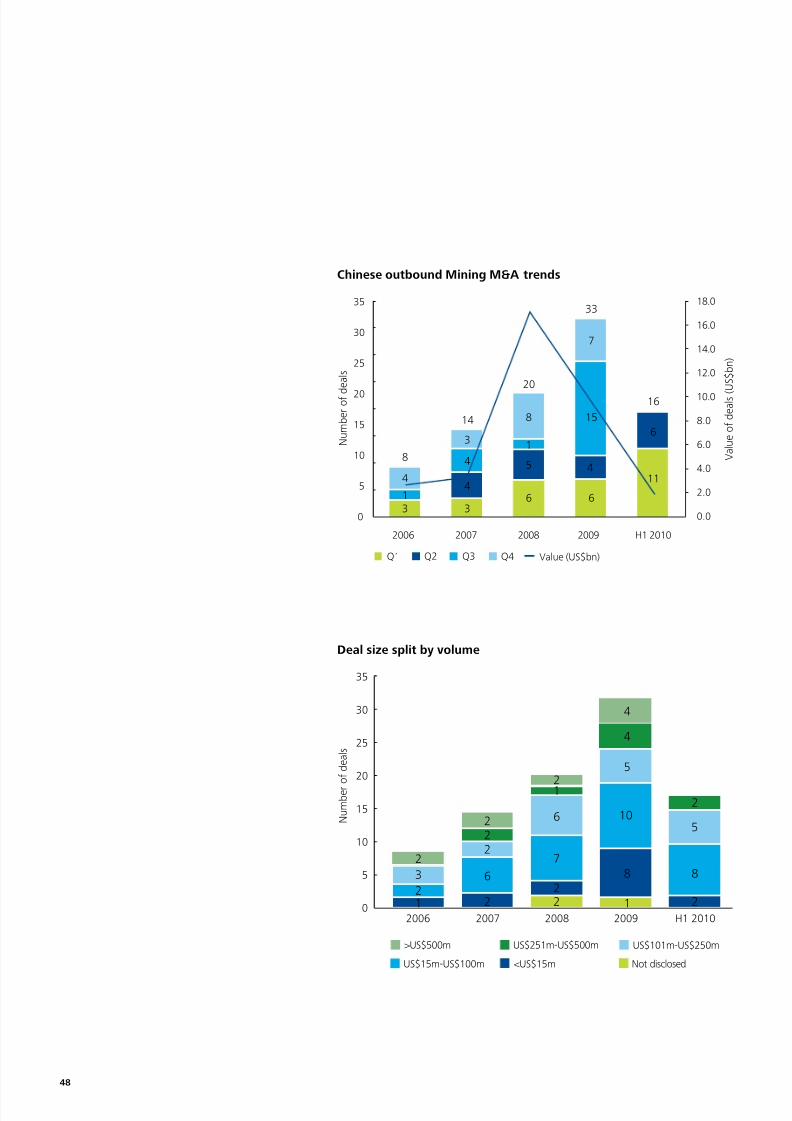

From the beginning o 2005 until the end o H1

2010, Chinese acquisitions o oreign Mining

assets have totalled some 91 deals, worth a total

o US$31.9 billion.17 such deals have come to the

market in the rst six months o 2010 alone withBaker suggesting that one o the drivers o this

recent surge in activity is simply due to the lawso supply and demand. “Chinese miners are being

driven to undertake acquisitions abroad primarily

to secure mining inputs at attractive prices,” he

said, continuing to explain that “While there is

currently talk about a residential property bubble

emerging in China, demand or raw materials is

not likely to all as there are continuing signicant

construction projects taking place across the

country.” Furthermore, as the wider economy

continues to grow, Chinese appetite or energyinputs will increase urther, leading to a rise in the

number o acquisitions o coal – and increasingly,

uranium – assets.

At the same time, Baker asserts that Chinese

Miners are using M&A as a method to urther

enhance strategic relationships with their global

Mining counterparts, one such example being

Chinalco’s US$14 billion acquisition, along

with the US rm Alcoa, o a 12% stake in Rio

Tinto, the Anglo-Australian Miner, back in early

2008. “Chinese Miners will continue to search

or attractive overseas opportunities, targetingmutually-benecial strategic relationships,

especially when they are able to prot rom

technological transers, the adoption o

managerial best practices, advantageous

pricing policies, and the increased likelihood o

subsequent joint ventures," he said.

However, Baker admits that making Mining

investments abroad isn’t always successul,

citing the ailed attempt by Chinalco to purchase

minority stakes in assets rom Rio Tinto or a

proposed US$11.8 billion back in 2009. The

Mining giant was close to tying up a stake sale

with Chinalco in order to reduce the level o

debt on its balance sheet to manageable levels

but backed out o the deal at the eleventh hour

ollowing a rapid bounce back in commodity

prices as the global economic recovery got

underway.

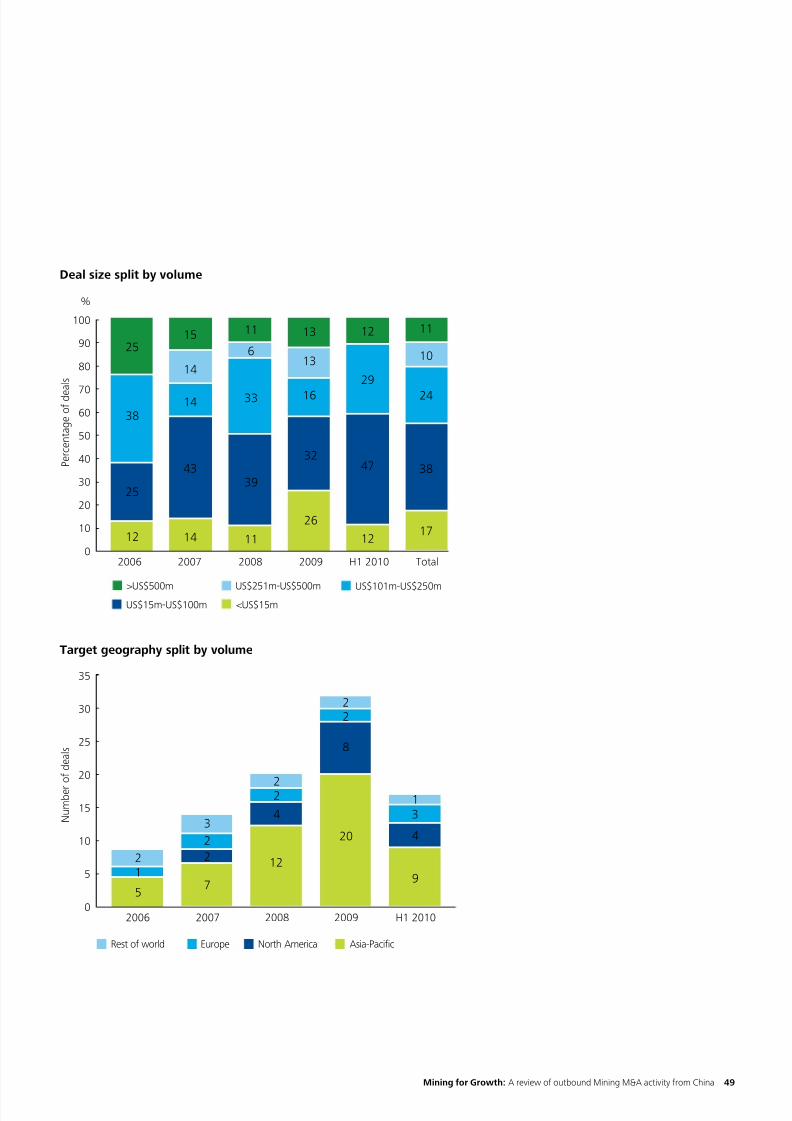

Mining M&A deal size

Transaction values o outbound Miningacquisitions rom China have allen in recent

times with no deals in the rst quarter o 2010

exceeding US$500 million, compared to our such

deals coming to market over 2009. Discussing

this trend, Baker says the decline has been

accompanied by a corresponding drop in the

size o equity stake acquisitions with alternative

deal structurings also being used. However, while

average deal sizes have certainly allen, oreign

Mining targets are not getting cheaper in absolute

terms.

In addition, Baker explains that “Chinese bidders

are starting to nd that political and regulatory

hurdles rom abroad are somewhat lessened i

they take a smaller equity stake in the target.”

Indeed, while local acquirers have lowered their

M&A expectations and are increasingly brokering

minority stake deals, they are still oten looking

to obtain operational interest in certain specic

Mining projects. In addition, Baker says that

local lending practices are becoming much more

thorough as the economy rebounds, meaning that

Chinese miners – whether they are state-ownedenterprises (SOEs) or private businesses – are now

acing tougher checks and balances as they look

to nance their acquisitions.

M&A Review

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 29/56Mining or Growth: A review o outbound Mining M&A activity rom China 29

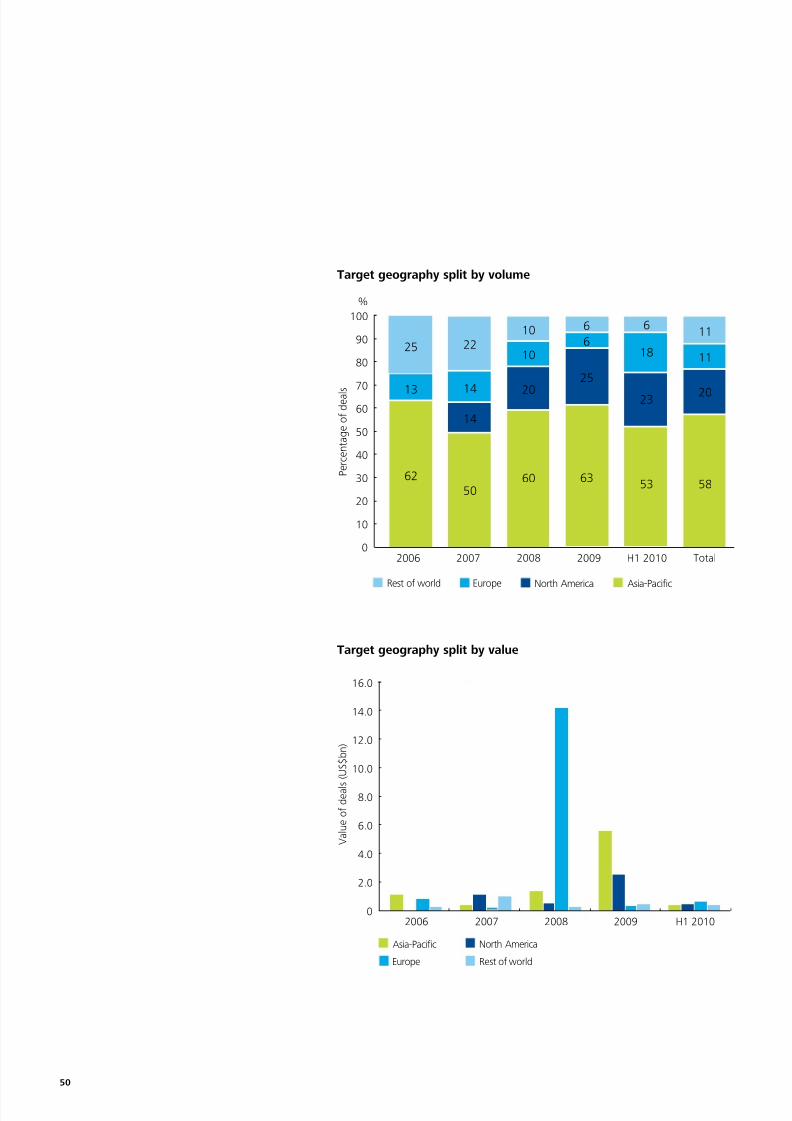

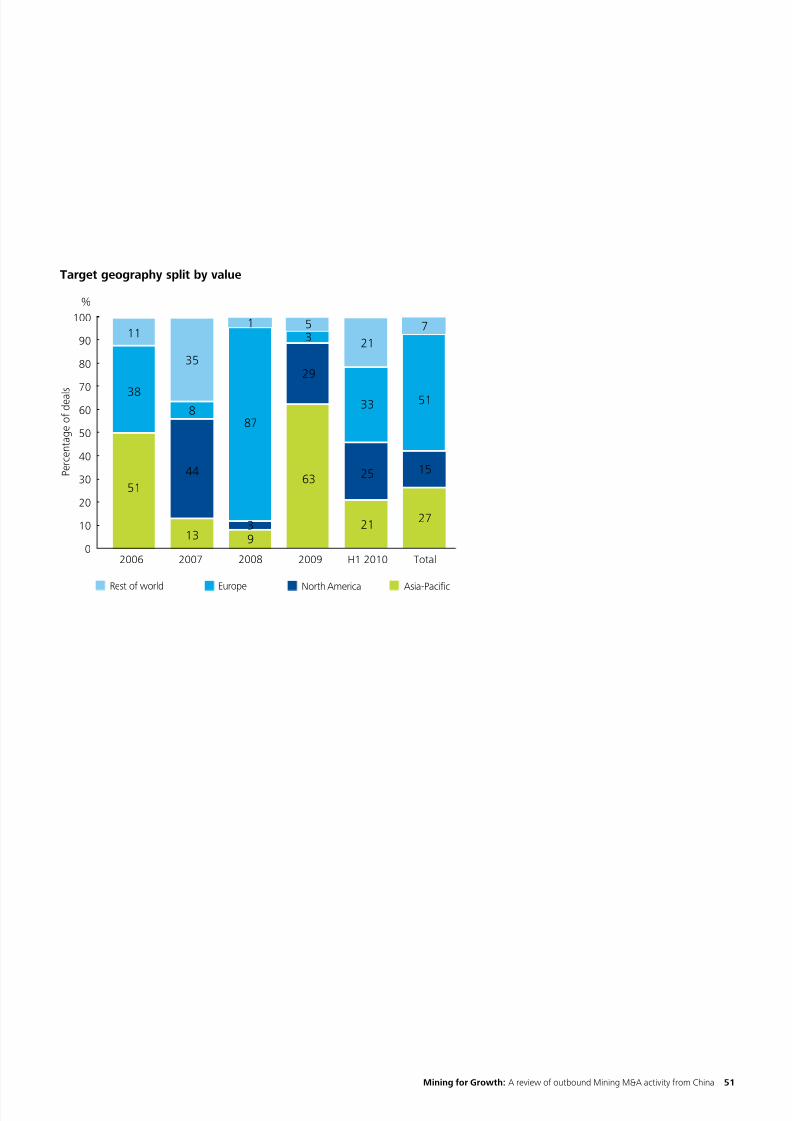

Country splits

Historically, Chinese Mining acquisitions havetended to ocus on making acquisitions across thewider Asia-Pacic region, with purchases o NorthAmerican and European assets accounting orthe minority o deal fow. However, Baker assertsthat these relationships have developed over time

and while the level o acquisitions undertaken inAsia has remained broadly constant, the numbero deals involving North American and EuropeanMining assets has increased.

Nevertheless, the global economic recovery hasseen Mining companies in Canada and Australia

return to health relatively quickly, along withvaluations. As a result, Chinese acquirers arebeginning to increasingly look at Mining assetsin alternative investment areas such as Arica andSouth America where corporate valuations arelower. Wuhan Iron and Steel’s bid or a 21.5%

stake in MMX Mineracao e Metalicos, the BrazilianMining company, or a total o US$400 million,announced back in November 2009, and theUS$244 million oer or a 12.5% stake in AricanMinerals, the UK-based mineral exploration anddevelopment company with an interest in Arica,by China Railway Materials, announced in January2010, are both good examples o this incipienttrend.

Looking orward

While Baker remains bullish on Mining M&Aprospects abroad over 2010 and beyond, hedoes admit that there are challenges that Chinesecompanies will have to overcome in order tosuccessully complete a transaction. Among theseremains the sometimes unpredictable nature o

regulatory bodies on both the buy- and sell-sideo a transaction.

“Chinese acquirers would do well to rememberthat domestic regulators are simply examining aproposed outbound transaction to ensure thatit supports the wider economic policies o the

Chinese government – as well as ensuring thatthe bidder can actually complete the transaction,”he said, going on to explain that “Despite a lot opublicity concerning rejected M&A bids, oreign

regulatory regimes are in act broadly supportive

o Chinese investments into their jurisdictions.”

He went on to cite the recent successul

acquisition o a 70% stake in Energy Metals,

the Australian rm engaged in the exploration

and development o uranium projects, by China

Uranium Development, or US$63 million, as

a good example o the transparency o theAustralian regulatory authorities. Signicantly,

the deal was approved in its original orm despite

obvious security concerns surrounding the export

o uranium to China.

Baker also remains airly optimistic on the

implications o the recently-revised resources

tax, explaining that "Under the new Minerals

Resource Rent Tax (MRRT), which replaces the

previously-announced Resource Super Prots

Tax (RSPT), the new tax regime will apply to the

mining o iron ore and coal in Australia but not

other commodities as would have been the caseunder the RSPT. The MRRT, which will be levied

at 30% and will be introduced on 1 July 2012,

will mean that Chinese companies interested

in buying Australian Mining assets will have to

re-evaluate the impact o the proposed tax on

uture protability as well as the overall viability

o existing and proposed investment projects.

However, with the tax now only applying to

iron ore and coal assets at a reduced rate, and

continuing strong demand rom Chinese rms

or iron ore and coal inputs over the oreseeable

uture, the potential impact o the MRRT onChinese outbound Mining acquisitions in

Australia has arguably been greatly reduced."

Baker ends on a positive note, highlighting

the growing maturity o Chinese bidders when

conducting M&A overseas, ranking it as a major

area in which Chinese miners have improved o

late. “Previously, some local Mining businesses

tended not to prioritize deal execution and post-

merger integration procedures. Now, they are

starting to see the value o preparation and to

this end, are beginning to hire external advisors

to help them through the process.“ Indeed, oneo the keys to M&A success remains thorough

planning and preparation. “Fail to prepare,

prepare to ail,” concludes Baker.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 30/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 31/56Mining or Growth: A review o outbound Mining M&A activity rom China 31

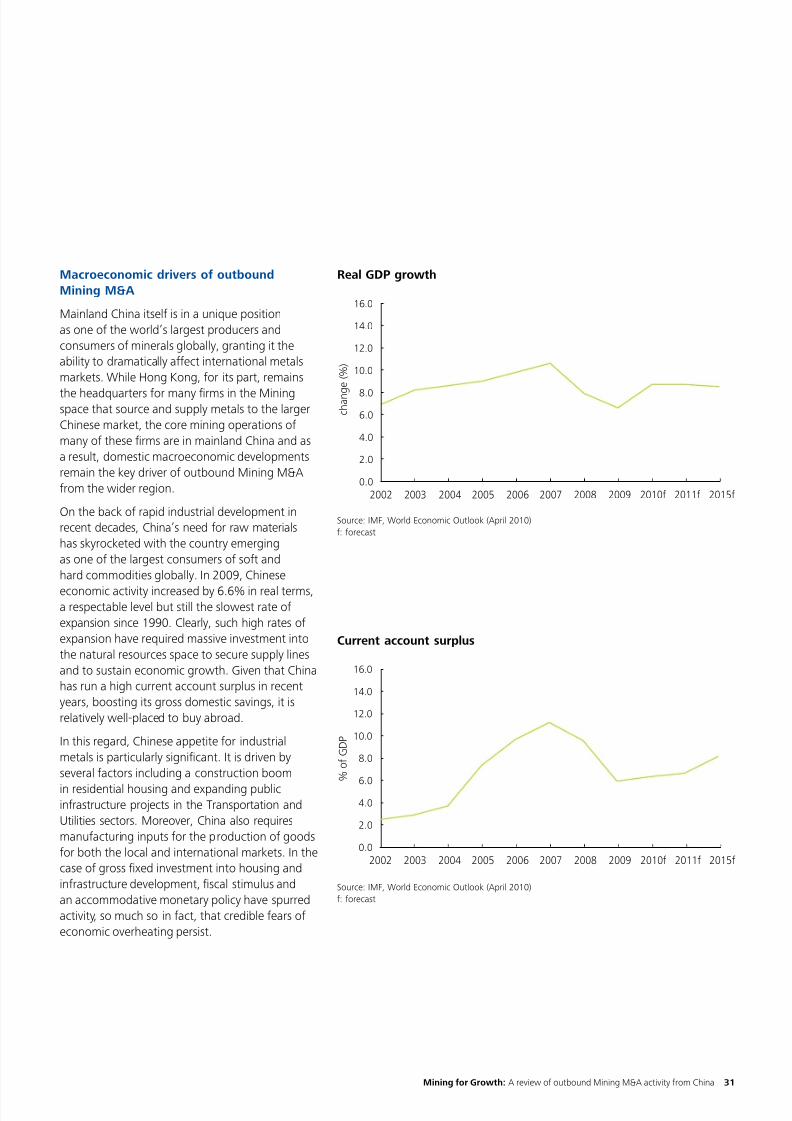

Macroeconomic drivers o outboundMining M&A

Mainland China itsel is in a unique positionas one o the world’s largest producers andconsumers o minerals globally, granting it theability to dramatically aect international metalsmarkets. While Hong Kong, or its part, remains

the headquarters or many rms in the Miningspace that source and supply metals to the largerChinese market, the core mining operations omany o these rms are in mainland China and asa result, domestic macroeconomic developmentsremain the key driver o outbound Mining M&Arom the wider region.

On the back o rapid industrial development inrecent decades, China’s need or raw materialshas skyrocketed with the country emergingas one o the largest consumers o sot andhard commodities globally. In 2009, Chinese

economic activity increased by 6.6% in real terms,a respectable level but still the slowest rate oexpansion since 1990. Clearly, such high rates oexpansion have required massive investment intothe natural resources space to secure supply linesand to sustain economic growth. Given that Chinahas run a high current account surplus in recentyears, boosting its gross domestic savings, it isrelatively well-placed to buy abroad.

In this regard, Chinese appetite or industrialmetals is particularly signicant. It is driven byseveral actors including a construction boom

in residential housing and expanding publicinrastructure projects in the Transportation andUtilities sectors. Moreover, China also requiresmanuacturing inputs or the production o goodsor both the local and international markets. In thecase o gross xed investment into housing andinrastructure development, scal stimulus andan accommodative monetary policy have spurredactivity, so much so in act, that credible ears oeconomic overheating persist.

0.0

2.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2015f2011f2010f20092008200720062005200420032002

c h a n g

e ( % )

Real GDP growth

0.0

2.0

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2015f2011f2010f20092008200720062005200420032002

% o

f G D P

Current account surplus

Source: IMF, World Economic Outlook (April 2010)

: orecast

Source: IMF, World Economic Outlook (April 2010)

: orecast

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 32/5632

Total value o China's Industrials sector

Total value o China's Construction sector

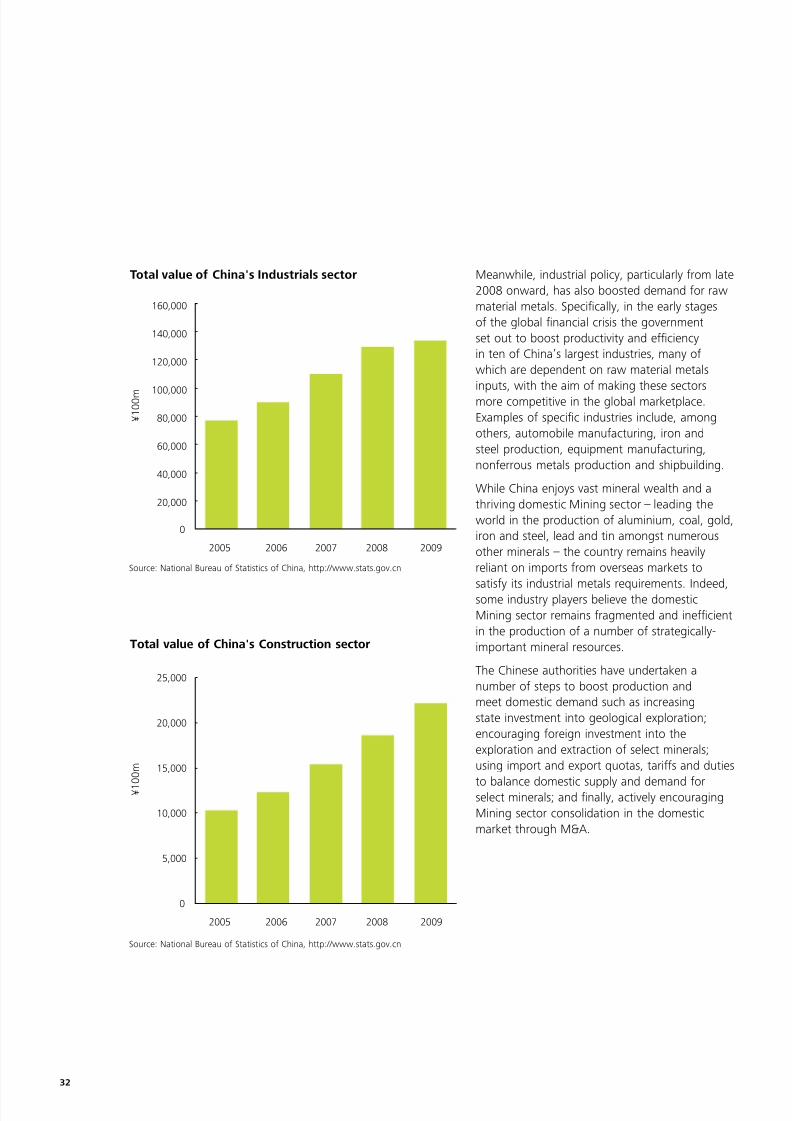

Meanwhile, industrial policy, particularly rom late2008 onward, has also boosted demand or rawmaterial metals. Specically, in the early stageso the global nancial crisis the governmentset out to boost productivity and eciencyin ten o China’s largest industries, many owhich are dependent on raw material metalsinputs, with the aim o making these sectorsmore competitive in the global marketplace.Examples o specic industries include, amongothers, automobile manuacturing, iron andsteel production, equipment manuacturing,nonerrous metals production and shipbuilding.

While China enjoys vast mineral wealth and athriving domestic Mining sector – leading theworld in the production o aluminium, coal, gold,iron and steel, lead and tin amongst numerousother minerals – the country remains heavilyreliant on imports rom overseas markets to

satisy its industrial metals requirements. Indeed,some industry players believe the domesticMining sector remains ragmented and inecientin the production o a number o strategically-important mineral resources.

The Chinese authorities have undertaken anumber o steps to boost production andmeet domestic demand such as increasingstate investment into geological exploration;encouraging oreign investment into theexploration and extraction o select minerals;using import and export quotas, taris and duties

to balance domestic supply and demand orselect minerals; and nally, actively encouragingMining sector consolidation in the domesticmarket through M&A.

¥ 1 0 0 m

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

20092008200720062005

Source: National Bureau o Statistics o China, http://www.stats.gov.cn

¥ 1

0 0 m

0

5,000

10,000

15,000

20,000

25,000

20092008200720062005

Source: National Bureau o Statistics o China, http://www.stats.gov.cn

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 33/56Mining or Growth: A review o outbound Mining M&A activity rom China 33

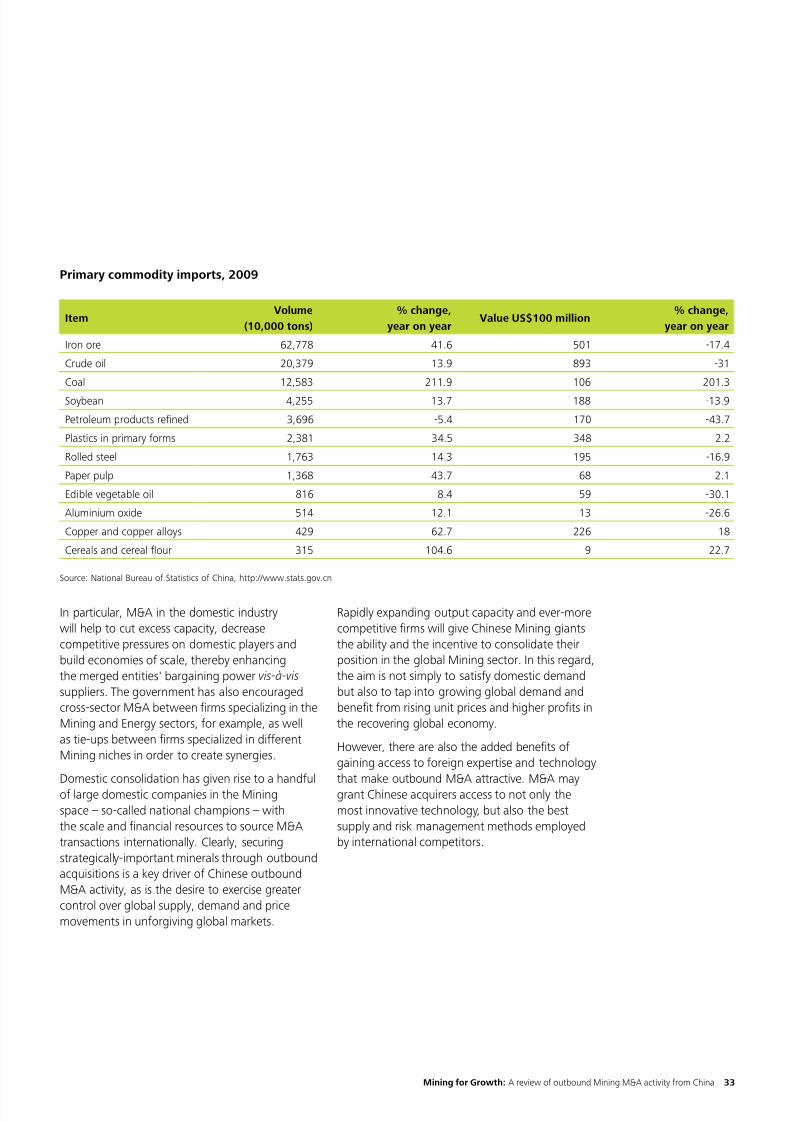

ItemVolume

(10,000 tons)

% change,

year on yearValue US$100 million

% change,

year on year

Iron ore 62,778 41.6 501 -17.4

Crude oil 20,379 13.9 893 -31

Coal 12,583 211.9 106 201.3

Soybean 4,255 13.7 188 -13.9

Petroleum products rened 3,696 -5.4 170 -43.7

Plastics in primary orms 2,381 34.5 348 2.2

Rolled steel 1,763 14.3 195 -16.9

Paper pulp 1,368 43.7 68 2.1

Edible vegetable oil 816 8.4 59 -30.1

Aluminium oxide 514 12.1 13 -26.6

Copper and copper alloys 429 62.7 226 18

Cereals and cereal four 315 104.6 9 22.7

Primary commodity imports, 2009

In particular, M&A in the domestic industrywill help to cut excess capacity, decreasecompetitive pressures on domestic players andbuild economies o scale, thereby enhancingthe merged entities' bargaining power vis-à-vis suppliers. The government has also encouragedcross-sector M&A between rms specializing in theMining and Energy sectors, or example, as wellas tie-ups between rms specialized in dierentMining niches in order to create synergies.

Domestic consolidation has given rise to a handulo large domestic companies in the Miningspace – so-called national champions – withthe scale and nancial resources to source M&Atransactions internationally. Clearly, securingstrategically-important minerals through outboundacquisitions is a key driver o Chinese outboundM&A activity, as is the desire to exercise greatercontrol over global supply, demand and pricemovements in unorgiving global markets.

Rapidly expanding output capacity and ever-morecompetitive rms will give Chinese Mining giantsthe ability and the incentive to consolidate theirposition in the global Mining sector. In this regard,the aim is not simply to satisy domestic demandbut also to tap into growing global demand andbenet rom rising unit prices and higher prots inthe recovering global economy.

However, there are also the added benets ogaining access to oreign expertise and technologythat make outbound M&A attractive. M&A maygrant Chinese acquirers access to not only themost innovative technology, but also the bestsupply and risk management methods employedby international competitors.

Source: National Bureau o Statistics o China, http://www.stats.gov.cn

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 34/5634

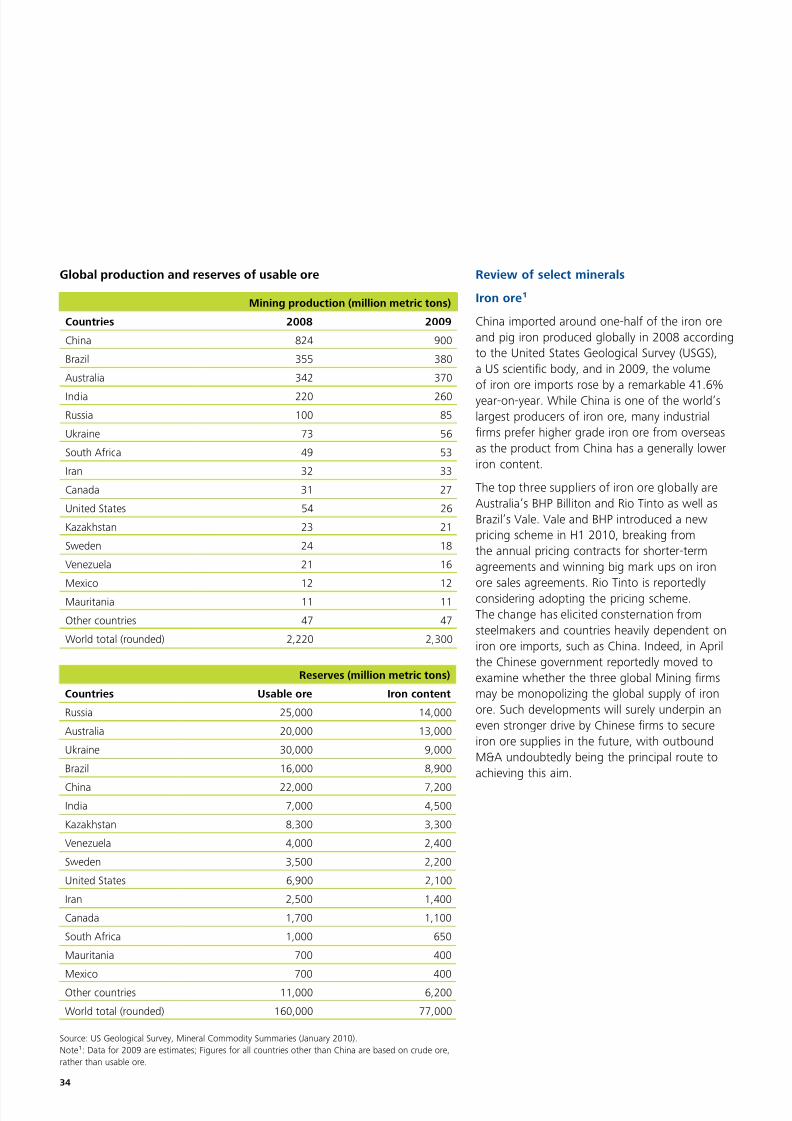

Review o select minerals

Iron ore¹

China imported around one-hal o the iron oreand pig iron produced globally in 2008 accordingto the United States Geological Survey (USGS),a US scientic body, and in 2009, the volumeo iron ore imports rose by a remarkable 41.6%year-on-year. While China is one o the world’slargest producers o iron ore, many industrialrms preer higher grade iron ore rom overseasas the product rom China has a generally loweriron content.

The top three suppliers o iron ore globally areAustralia’s BHP Billiton and Rio Tinto as well asBrazil’s Vale. Vale and BHP introduced a newpricing scheme in H1 2010, breaking romthe annual pricing contracts or shorter-termagreements and winning big mark ups on iron

ore sales agreements. Rio Tinto is reportedlyconsidering adopting the pricing scheme.The change has elicited consternation romsteelmakers and countries heavily dependent oniron ore imports, such as China. Indeed, in Aprilthe Chinese government reportedly moved toexamine whether the three global Mining rmsmay be monopolizing the global supply o ironore. Such developments will surely underpin aneven stronger drive by Chinese rms to secureiron ore supplies in the uture, with outboundM&A undoubtedly being the principal route toachieving this aim.

Mining production (million metric tons)

Countries 2008 2009

China 824 900

Brazil 355 380

Australia 342 370

India 220 260

Russia 100 85

Ukraine 73 56

South Arica 49 53

Iran 32 33

Canada 31 27

United States 54 26

Kazakhstan 23 21

Sweden 24 18

Venezuela 21 16

Mexico 12 12Mauritania 11 11

Other countries 47 47

World total (rounded) 2,220 2,300

Global production and reserves o usable ore

Reserves (million metric tons)

Countries Usable ore Iron content

Russia 25,000 14,000

Australia 20,000 13,000

Ukraine 30,000 9,000

Brazil 16,000 8,900

China 22,000 7,200

India 7,000 4,500

Kazakhstan 8,300 3,300

Venezuela 4,000 2,400

Sweden 3,500 2,200

United States 6,900 2,100

Iran 2,500 1,400

Canada 1,700 1,100

South Arica 1,000 650

Mauritania 700 400

Mexico 700 400

Other countries 11,000 6,200

World total (rounded) 160,000 77,000

Source: US Geological Survey, Mineral Commodity Summaries (January 2010).

Note¹: Data or 2009 are estimates; Figures or all countries other than China are based on crude ore,

rather than usable ore.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 35/56Mining or Growth: A review o outbound Mining M&A activity rom China 35

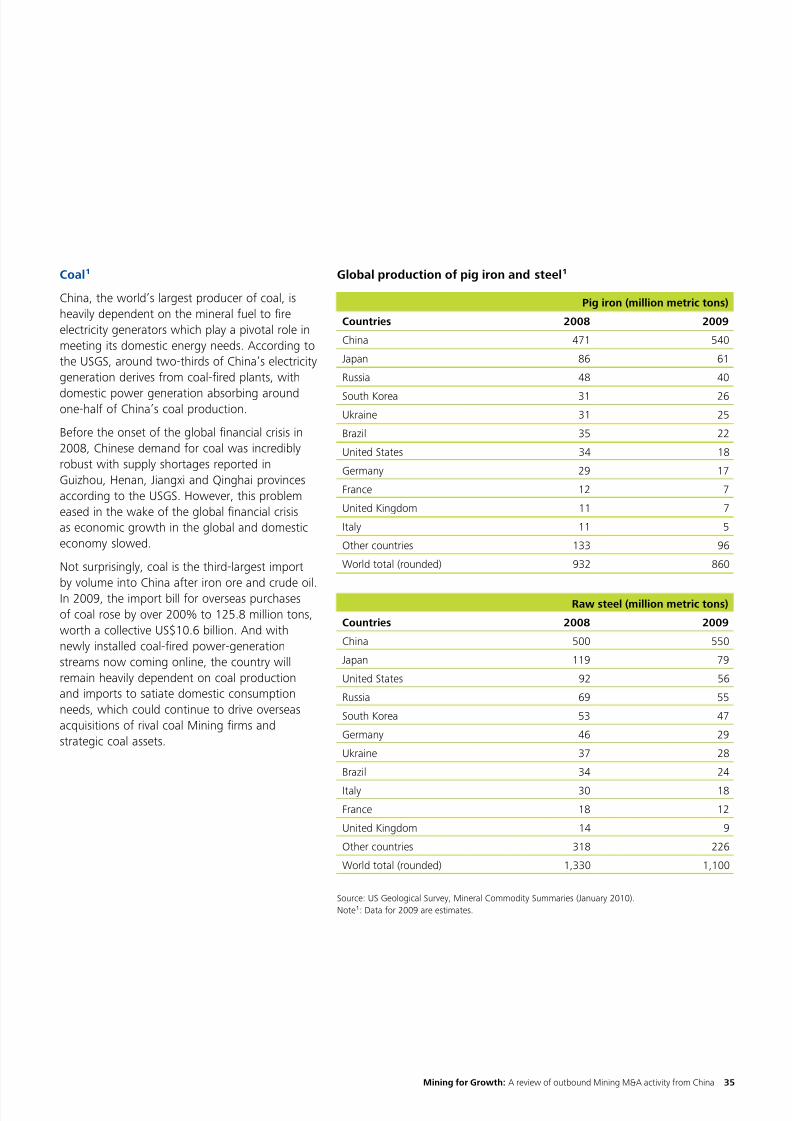

Coal¹

China, the world’s largest producer o coal, isheavily dependent on the mineral uel to reelectricity generators which play a pivotal role inmeeting its domestic energy needs. According tothe USGS, around two-thirds o China’s electricitygeneration derives rom coal-red plants, with

domestic power generation absorbing aroundone-hal o China’s coal production.

Beore the onset o the global nancial crisis in2008, Chinese demand or coal was incrediblyrobust with supply shortages reported inGuizhou, Henan, Jiangxi and Qinghai provincesaccording to the USGS. However, this problemeased in the wake o the global nancial crisisas economic growth in the global and domesticeconomy slowed.

Not surprisingly, coal is the third-largest import

by volume into China ater iron ore and crude oil.In 2009, the import bill or overseas purchaseso coal rose by over 200% to 125.8 million tons,worth a collective US$10.6 billion. And withnewly installed coal-red power-generationstreams now coming online, the country willremain heavily dependent on coal productionand imports to satiate domestic consumptionneeds, which could continue to drive overseasacquisitions o rival coal Mining rms andstrategic coal assets.

Global production o pig iron and steel¹

Pig iron (million metric tons)

Countries 2008 2009

China 471 540

Japan 86 61

Russia 48 40

South Korea 31 26

Ukraine 31 25

Brazil 35 22

United States 34 18

Germany 29 17

France 12 7

United Kingdom 11 7

Italy 11 5

Other countries 133 96

World total (rounded) 932 860

Raw steel (million metric tons)

Countries 2008 2009

China 500 550

Japan 119 79

United States 92 56

Russia 69 55

South Korea 53 47

Germany 46 29

Ukraine 37 28

Brazil 34 24

Italy 30 18

France 18 12

United Kingdom 14 9

Other countries 318 226

World total (rounded) 1,330 1,100

Source: US Geological Survey, Mineral Commodity Summaries (January 2010).

Note¹: Data or 2009 are estimates.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 36/5636

Aluminium¹

It is also notable that the Chinese Mining sectorhas witnessed an increase in the country’saluminium output capacity in recent years,largely thanks to rising investment in the space.Indeed, in 2009 alone, the year-on-year rise incapacity climbed 27% to 19 billion tons. The

country imported some 5.1 million tons o theraw ingredient or aluminium, known as aluminaor aluminium oxide, worth US$1.3 billion in 2009to support aluminium production, representing avolume increase o 12.1% year-on-year.

Production (million metric tons)

Countries 2008 2009

China 13,200 13,000

Russia 3,800 3,300

Canada 3,120 3,000

Australia 1,970 1,970

United States 2,658 1,710

India 1,310 1,600

Brazil 1,660 1,550

Norway 1,360 1,200

UAE, Dubai 910 950

Bahrain 865 870

South Arica 811 800

Iceland 787 790

Venezuela 610 550

Germany 550 520Mozambique 536 500

Other countries 4,850 4,600

World total (rounded) 39,000 36,900

Global production and capacity o aluminium

Capacity at year-end (million metric tons)

Countries 2008 2009

China 15,000 19,000

Russia 4,400 5,150

United States 3,620 3,500

Canada 3,120 3,090

India 1,800 2,000

Australia 1,970 1,970

Brazil 1,700 1,700

Norway 1,360 1,230

UAE, Dubai 950 950

South Arica 900 900

Bahrain 880 880

Iceland 790 790

Venezuela 625 625

Germany 620 620

Mozambique 570 570

Other countries 6,260 6,920

World total (rounded) 44,600 49,900

Source: US Geological Survey, Mineral Commodity Summaries (January 2010).

Note¹: Data or 2009 are estimates.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 37/56Mining or Growth: A review o outbound Mining M&A activity rom China 37

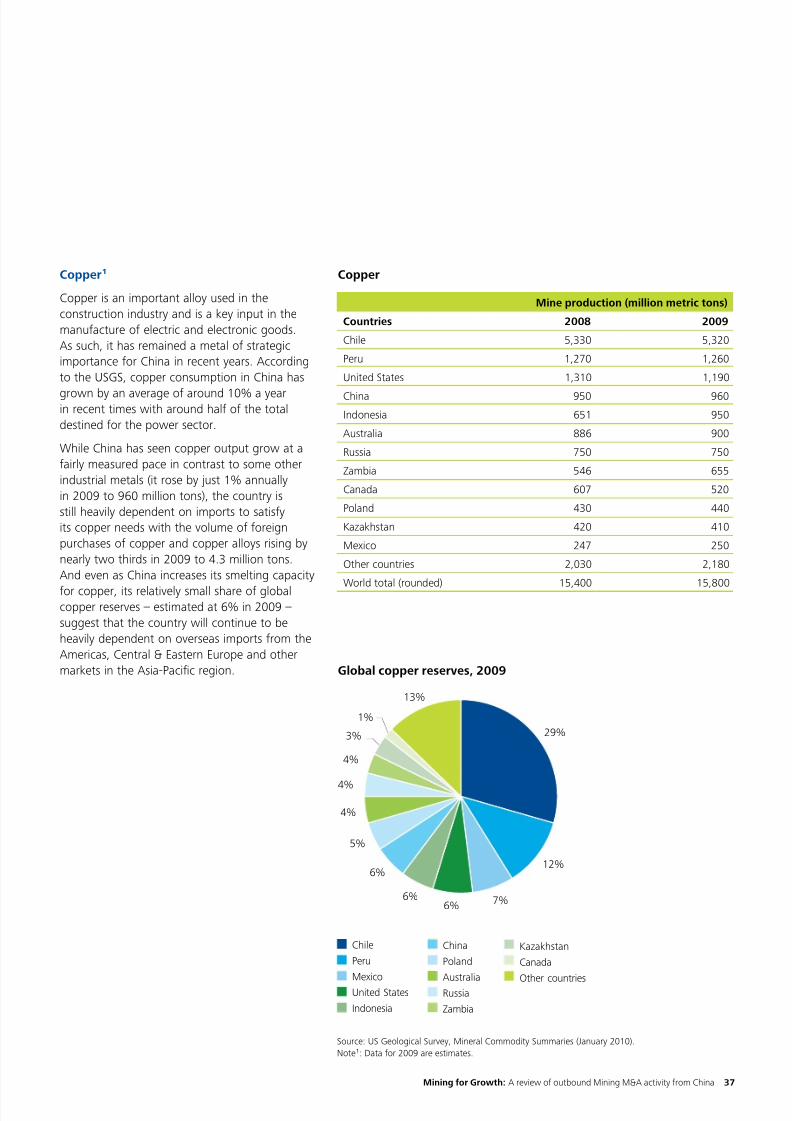

Copper¹

Copper is an important alloy used in theconstruction industry and is a key input in themanuacture o electric and electronic goods.As such, it has remained a metal o strategicimportance or China in recent years. Accordingto the USGS, copper consumption in China has

grown by an average o around 10% a yearin recent times with around hal o the totaldestined or the power sector.

While China has seen copper output grow at aairly measured pace in contrast to some otherindustrial metals (it rose by just 1% annuallyin 2009 to 960 million tons), the country isstill heavily dependent on imports to satisyits copper needs with the volume o oreignpurchases o copper and copper alloys rising bynearly two thirds in 2009 to 4.3 million tons.And even as China increases its smelting capacity

or copper, its relatively small share o globalcopper reserves – estimated at 6% in 2009 –suggest that the country will continue to beheavily dependent on overseas imports rom theAmericas, Central & Eastern Europe and othermarkets in the Asia-Pacic region.

Copper

Mine production (million metric tons)

Countries 2008 2009

Chile 5,330 5,320

Peru 1,270 1,260

United States 1,310 1,190

China 950 960

Indonesia 651 950

Australia 886 900

Russia 750 750

Zambia 546 655

Canada 607 520

Poland 430 440

Kazakhstan 420 410

Mexico 247 250

Other countries 2,030 2,180

World total (rounded) 15,400 15,800

12%

4%

4%

4%

3%

1%

Chile

Peru

Mexico

United States

Indonesia

13%

7%6%

6%

6%

5%

29%

China

Poland

Australia

Russia

Zambia

Kazakhstan

Canada

Other countries

Global copper reserves, 2009

Source: US Geological Survey, Mineral Commodity Summaries (January 2010).

Note¹: Data or 2009 are estimates.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 38/56

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 39/56Mining or Growth: A review o outbound Mining M&A activity rom China 39

Chinese outbound Mining investment case

study - Australia

China’s appetite or Australian Mining assets

is seemingly insatiable. Since the beginning o

2006, Chinese companies have undertaken 27

outbound M&A deals in this space, with an

aggregate disclosed value o US$6.6 billion. In

terms o overall outbound M&A, the Australianmarket leads the way with a signicant 46%

share o deal volume and 23% by value.

Given the cash-rich nature o many Chinese rms

operating in and around the Mining sector, it is

somewhat unsurprising that a number o notable

large-cap outbound transactions have been

announced in Australia in recent times. Indeed,

mergermarket data shows that three US$500

million+ deals have come to the market since the

rst quarter o 2006.

The largest and most high-prole transactionwas announced in August 2009 and saw

Yanzhou Coal Mining acquire Felix Resources,

the Australian coal producer, or US$2.6 billion.

Yanzhou were able to complete the transaction

at a 14% discount to Felix Resources' share

price one day prior to the deal announcement.

However, Yanzhou were unable to secure

control o Felix Resources' South Australian Coal

Corporation, which was ultimately spun o by

the target and listed on the ASX.

Elsewhere, deals that have so ar been brokered

in 2010 have generally allen rmly in and aroundthe mid-market space. The largest such deal was

valued at US$46 million and saw the Yunnan Tin

Group, the Chinese manuacturer and producer

o tin, acquire a 50% stake in Bluestone Mines

Tasmania, the Australian mining company rom

Metals X, the Australian company engaged in

exploration and mining, to orm a 50:50 joint

venture.

Despite the recent lack o large-cap activity, deal

volumes have held up remarkably well since the

onset o the global nancial crisis in the autumn

o 2008. The total number o transactionsannounced each year has steadily increased

in recent times, peaking with 33 announced

deals in 2009, a signicant 65% increase on

2008 numbers. Notably, the purchasing power

o Chinese rms has remained intact and many

would-be acquirers remain capable o conducting

a mega-deal i a situation makes strategic sense.

The above-mentioned statistics clearly show that

Chinese investment in Australian Mining assetsis signicant. In terms o the key drivers o this

activity, the underlying issue is the desire to

secure mining inputs at attractive and reasonable

prices. Such inputs are literally the building blocks

o China’s booming economy and are needed

due to the vast number o domestic construction

and inrastructure projects that continue to be

undertaken. Indeed, iron ore is a vital commodity

in this regard given that it is the main ingredient

in steel – vast amounts o which are used to

build, or example, skyscrapers and automobiles.

Despite this, it is still surprising and remarkable

that China’s imports o iron ore accounted or

around 75% o global iron ore trading in 2009,

according to Xin Guobin, an ocial with the

Ministry o Industry and Inormation Technology.

Looking ahead, the need or iron ore should

mean that China will continue to invest in the

Mining sector, particularly in Australia. The

primary driver o such activity will continue to be

the need to increase access to the commodity

although there are also several secondary

benets such as technology transers and theadoption o best practice operational techniques.

While Australia will no doubt remain a key

market, there are several obstacles to M&A.

Regulatory hurdles persist and while the Foreign

Investment Review Board (FIRB) welcomes

oreign investors, preerably in collaboration with

domestic rms, the regulator recently stated that

it has a clear preerence or oreign investment

in larger Australian companies to be capped at

15% with a 50% cap in early-stage companies.

Such regulatory attitudes to cross-border Chinese

Mining investments are discussed in detail in thenext chapter however.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 40/5640

Perhaps more signicantly, the Australiangovernment recently announced plans to levy atax on “super prots” rom resource companies,currently dened as prots above the 10-yearAustralian government bond rate. However,

the recent replacement o Kevin Rudd withJulia Gillard as Prime Minister has resulted in a

more conciliatory tone being adopted by thegovernment o late.

Industry gures have said that the tax, initiallyslated to come in to eect in 2012, will curtailinvestment in the sector and limit employmentopportunities. A reduction in the overallprotability o the Australian Mining sector is

obviously a concern or current and prospectiveChinese investors although M&A activity willlikely continue as long as the demand or mineralresources remains robust. This is set to be thecase with the current Mining surge likely to last

or an extended period given the huge potentialo economies such as China itsel and, to a lesserextent, India.

The regulatory environment: a look at

regulatory rulings on Chinese outboundMining acquisitions

Chinese Mining companies suddenly burstonto the global M&A scene in 2008 and 2009ollowing a series o high-prole acquisitions.A number o such deals have attracted the

attention o regional regulatory bodies and whilea large proportion o transactions have beenapproved, there have been several high-prole

examples o deals being blocked on regulatorygrounds. Remarkably, an Australian senatorwent so ar as to run television advertisementsopposing one such transaction, arguing thatanother sovereign nation should not be able toown a domestic sovereign asset.

Such widespread scaremongering must,however, be placed into the wider context. Sincethe beginning o 2005, Chinese miners have

undertaken 63 acquisitions o oreign assets,spending a cumulative US$31 billion in theprocess. O these, just three transactions worth

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 41/56Mining or Growth: A review o outbound Mining M&A activity rom China 41

US$2.6 billion ultimately lapsed due to regulatory

issues - surprisingly, all o them being bids or

Australian assets.

Moreover, the bulk o the overall valuation gure

is due to one deal – the Q1 2009 US$2.5 billion

bid or OZ Minerals by China Minmetals – which

was ultimately restructured and successully

completed. As a result, aborted cross-border

Mining acquisitions undertaken by Chinese

bidders comprised less than 5% o total activity

in volume terms, making the press coverage and

perceived tough stance o regulators somewhat

disproportionate to actual deal rejection gures.

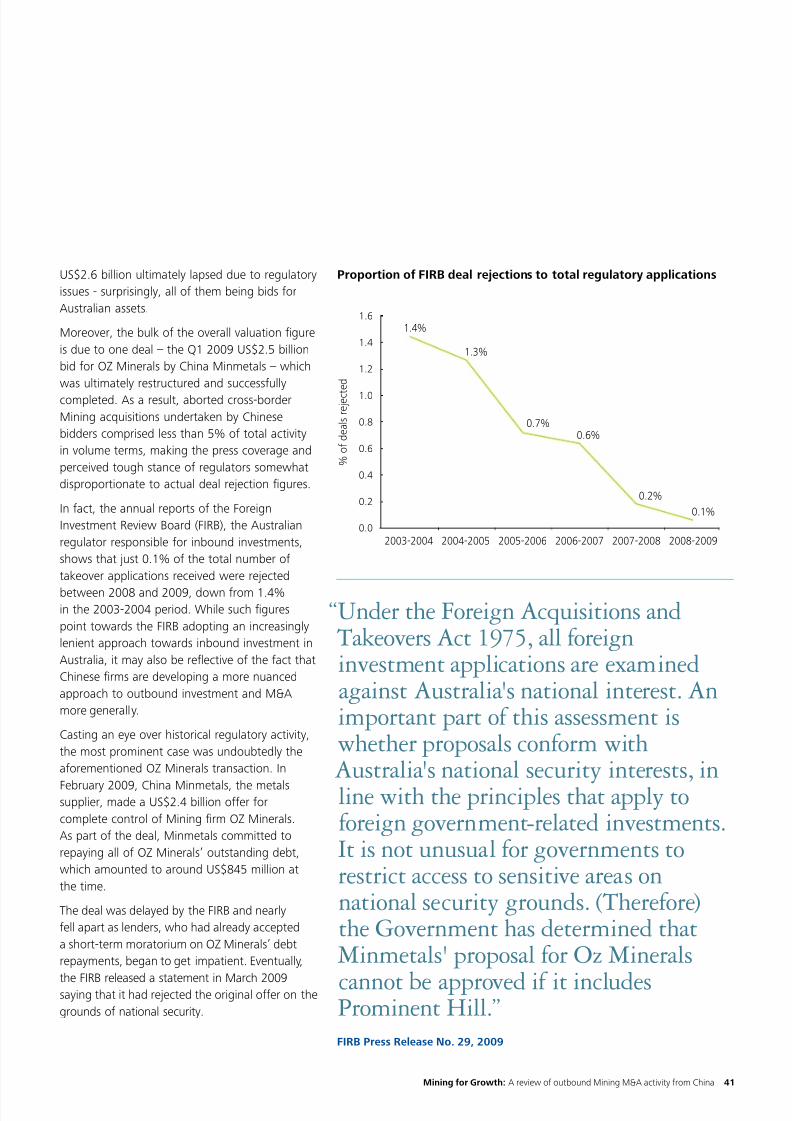

In act, the annual reports o the Foreign

Investment Review Board (FIRB), the Australian

regulator responsible or inbound investments,

shows that just 0.1% o the total number o

takeover applications received were rejected

between 2008 and 2009, down rom 1.4%in the 2003-2004 period. While such gures

point towards the FIRB adopting an increasingly

lenient approach towards inbound investment in

Australia, it may also be refective o the act that

Chinese rms are developing a more nuanced

approach to outbound investment and M&A

more generally.

Casting an eye over historical regulatory activity,

the most prominent case was undoubtedly the

aorementioned OZ Minerals transaction. In

February 2009, China Minmetals, the metalssupplier, made a US$2.4 billion oer or

complete control o Mining rm OZ Minerals.

As part o the deal, Minmetals committed to

repaying all o OZ Minerals’ outstanding debt,

which amounted to around US$845 million at

the time.

The deal was delayed by the FIRB and nearly

ell apart as lenders, who had already accepted

a short-term moratorium on OZ Minerals’ debt

repayments, began to get impatient. Eventually,

the FIRB released a statement in March 2009saying that it had rejected the original oer on the

grounds o national security.

“Under the Foreign Acquisitions andTakeovers Act 1975, all oreigninvestment applications are examinedagainst Australia's national interest. Animportant part o this assessment iswhether proposals conorm withAustralia's national security interests, inline with the principles that apply tooreign government-related investments.It is not unusual or governments torestrict access to sensitive areas onnational security grounds. (Thereore)the Government has determined thatMinmetals' proposal or Oz Minerals

cannot be approved i it includesProminent Hill.”FIRB Press Release No. 29, 2009

0.0

0.2

1.6

1.4

1.2

1.0

0.8

0.6

0.4

2008-20092007-20082006-20072005-20062004-20052003-2004

1.4%

1.3%

0.7%

0.6%

0.2%

0.1%

% o

f d e a l s r e j e c t

e d

Proportion o FIRB deal rejections to total regulatory applications

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 42/5642

In response to this development, China Minmetalssubmitted a revised US$1.4 billion oer whichexcluded the acquisition o the politically sensitiveProminent Hill Copper Mine, an asset close toWoomera Test Range, a strategic national assetgiven that it is described as the western world’slargest deence systems testing and evaluationrange. The revised oer also did not include otherAsian assets, including OZ Minerals’ MartabeMines in Indonesia as well as several otherexploration assets in Cambodia and Thailand. Therevised bid received FIRB approval just nine daysater it was rst announced, with the Treasurerstipulating some urther conditions, the main onesbeing that:

1) China Minmetals would continue to operatethe mines as a separate commercial businessto its core operations, and would retain OZMinerals’ headquarters in Australia.

2) Price OZ Minerals’ o-take on arms-lengthterms with reerence to internationalobservable benchmarks and global marketpractices.

3) China Minmetals maintain or increaseproduction and employment at OZ Minerals’other mines.

China Minmetals agreed to adhere to theserevised conditions and the deal was subsequentlyconsummated. More than one year on since thetransaction was completed, OZ Mineral’s share

price has consistently remained above the averagemonthly price o AU$0.88 per share at the time othe deal, suggesting that the transaction has so arbeen value-accretive to shareholders.

Elsewhere, China Nonerrous Metal Mining’s(CNMC) US$215 million bid to acquire a 51.66%stake in Australia’s Lynas Corporation, the rareearth metals miner, also suered the sameate as Minmetal’s initial oer. However, in thisinstance, it is thought that the FIRB rejected thedeal on antitrust grounds. According to the WallStreet Journal, Chinese rare earth miners account

or more than 95% o global rare earth metals

production and state-owned CNMC’s bid to take

control o Lynas was widely seen as an attempt

to reinorce the country’s monopoly over the

production o such metals. In this regard, it is

particularly notable that Lynas controls the world’s

richest rare earth metals deposit near Laverton,

Western Australia.

CNMC’s oer quickly aroused the suspiciono the FIRB, who had previously proved to

be accommodating towards the purchase o

Australian rare earth metals miners. Indeed, just

a ew months earlier, the board had approved

the US$15 million acquisition o a 25% stake

in Araura Resources, by the East China Mineral

Exploration & Development Bureau, without

conditions.

Ater an initial review, the FIRB announced

that it would approve the acquisition o Lynas

i CNMC reduced its proposed stake holding

to under 50%, ensuring that its directors did

not make up hal o more o Lynas’s board and

provided independent marketing o Lynas’ rare

earth products. The subsequent response rom

CNMC was unequivocal. Within one day o the

announcement, the rm had pulled its oer or

Lynas, presumably as it elt that the deal terms

were too onerous, and has subsequently not

made any urther inroads into Australia.

The third and nal instance o a regulator

ultimately shooting down an outbound Chinese

Mining acquisition was seen in May 2008 whenSinosteel attempted to acquire Murchison Metals

or US$1.2 billion. The company had previously

bought out Australia’s Midwest Corporation just

two months earlier, and used it as an acquisition

vehicle to bid or Murchison, an iron ore

miner. The deal was reerred to the FIRB, who

lengthened its review period o the transaction to

three months rom the customary 30 days. This

was enough to prompt Sinosteel to reduce its

oer to a 49.9% stake, a move which was viewed

avorably by the FIRB with the revised oer being

approved.

8/8/2019 Deloitte MINING English

http://slidepdf.com/reader/full/deloitte-mining-english 43/56Mining or Growth: A review o outbound Mining M&A activity rom China 43

Lessons learnt

Undoubtedly, a number o important lessons havebeen learnt in these deals. When Chinese rmsare looking to broker an overseas cross-borderacquisition, a number o actors must be keenlyconsidered. These include:

1) Engage regulators at the earliest possibleinstance. On many occasions, regulatorsare the last party to be consulted about apossible acquisition, invariably delaying thedeal timetable and increasing the likelihood oailure. This was especially prevalent during theCNMC/Lynas deal.