Embed Size (px)

Citation preview

1

Demystifying Budget Proposals and other regulatory changes and impact thereof on One’s Investments

Presenter: Prof. Satish Sawnani B.Com; FCA; ACS; CAIIB; CTM ; DISA & IFRS(ICAI)

CFO & Compliance Officer - ArthVeda Fund Management Pvt. Ltd.

Presentation Dated: 15th March 2013

2

A slide on Introduction of the Sponsor of Today’s Seminar

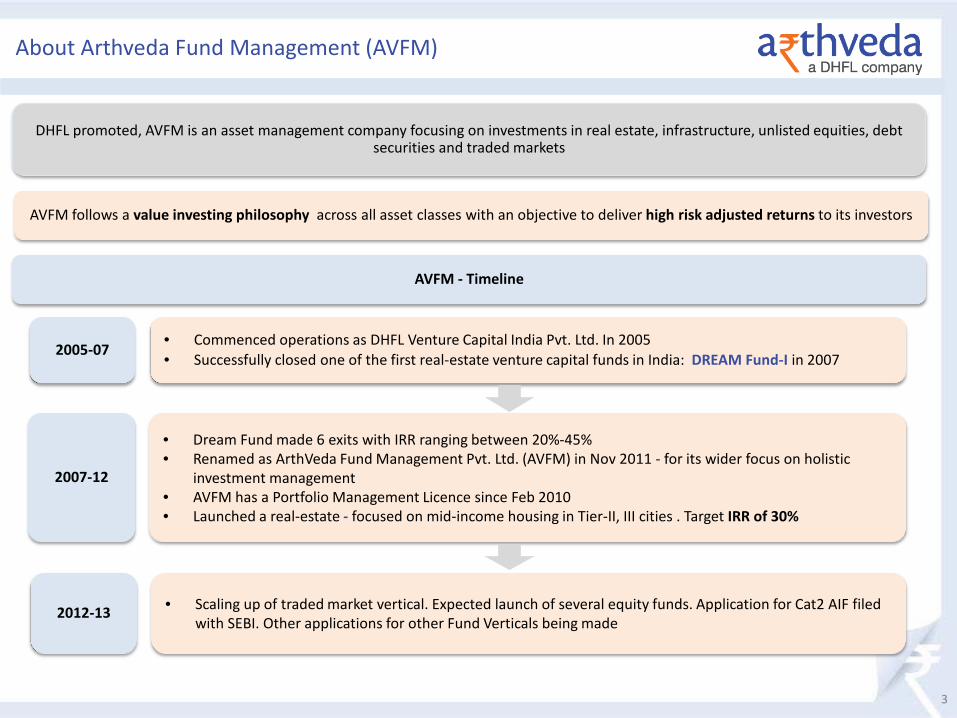

About Arthveda Fund Management (AVFM)

DHFL promoted, AVFM is an asset management company focusing on investments in real estate, infrastructure, unlisted equities, debt securities and traded markets

AVFM follows a value investing philosophy across all asset classes with an objective to deliver high risk adjusted returns to its investors

3

2005-07 • Commenced operations as DHFL Venture Capital India Pvt. Ltd. In 2005 • Successfully closed one of the first real-estate venture capital funds in India: DREAM Fund-I in 2007

2007-12

• Dream Fund made 6 exits with IRR ranging between 20%-45% • Renamed as ArthVeda Fund Management Pvt. Ltd. (AVFM) in Nov 2011 - for its wider focus on holistic

investment management • AVFM has a Portfolio Management Licence since Feb 2010 • Launched a real-estate - focused on mid-income housing in Tier-II, III cities . Target IRR of 30%

AVFM - Timeline

2012-13

• Scaling up of traded market vertical. Expected launch of several equity funds. Application for Cat2 AIF filed

with SEBI. Other applications for other Fund Verticals being made

Arthveda’s Philosophy

4

Risky asset classes need a rational approach to investing

Wealth (Arth)

Wisdom (Veda)

from

Investment Philosophy

• Unique value investing philosophy to address investment decision making in riskier asset classes

• Reduce risk and enhance return to generate superior risk adjusted returns and hence alpha

• Risk can be reduced by in-depth research on the opportunity and a good understanding of source of risk

• Returns can be enhanced by estimation of intrinsic value and buying at lower levels

5

Earlier Presentations by illustrious Speakers

• NEW Alternative Investment Fund (AIF) Regulations - Implications for Ultra HNI Investors and their Advisors Mr. Siddharth Shah (Partner at Nishith Desai Associates) June 08, 2012

• Does Value Investing generate Alpha? - Academic and Empirical Evidence Dr. Vikas V Gupta (Head- Research & Product Development) May 18, 2012

• Real Estate Fund – Cracking Intrinsic Value in Housing Mr. Rajeev Saraogi (Chartered Accountant and Certified Business Valuer) Mr. Harish Gagwani (Sr. Investment Officer) June 22, 2012

• How to Generate Alpha in the Indian Stock Markets Dr. Vikas V Gupta (Head- Research & Product Development) February 08, 2013

• Low-Income Housing - Next Wave Of Growth In The Indian Real Estate Harshil Mehta - CEO – Aadhar Housing Finance Pvt. Ltd. January 24, 2013

6

Budget Proposals & your current /Targeted Investments

7

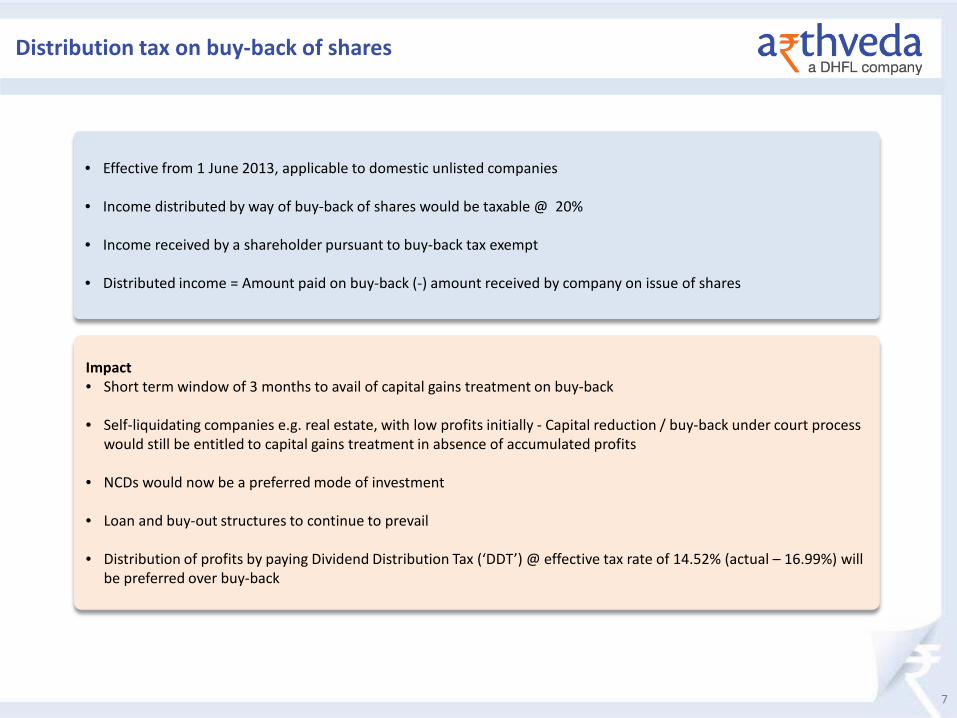

Distribution tax on buy-back of shares

• Effective from 1 June 2013, applicable to domestic unlisted companies

• Income distributed by way of buy-back of shares would be taxable @ 20%

• Income received by a shareholder pursuant to buy-back tax exempt

• Distributed income = Amount paid on buy-back (-) amount received by company on issue of shares

Impact • Short term window of 3 months to avail of capital gains treatment on buy-back

• Self-liquidating companies e.g. real estate, with low profits initially - Capital reduction / buy-back under court process

would still be entitled to capital gains treatment in absence of accumulated profits

• NCDs would now be a preferred mode of investment

• Loan and buy-out structures to continue to prevail

• Distribution of profits by paying Dividend Distribution Tax (‘DDT’) @ effective tax rate of 14.52% (actual – 16.99%) will be preferred over buy-back

8

DISTRIBUTION TAX ON BUY-BACK OF SHARES

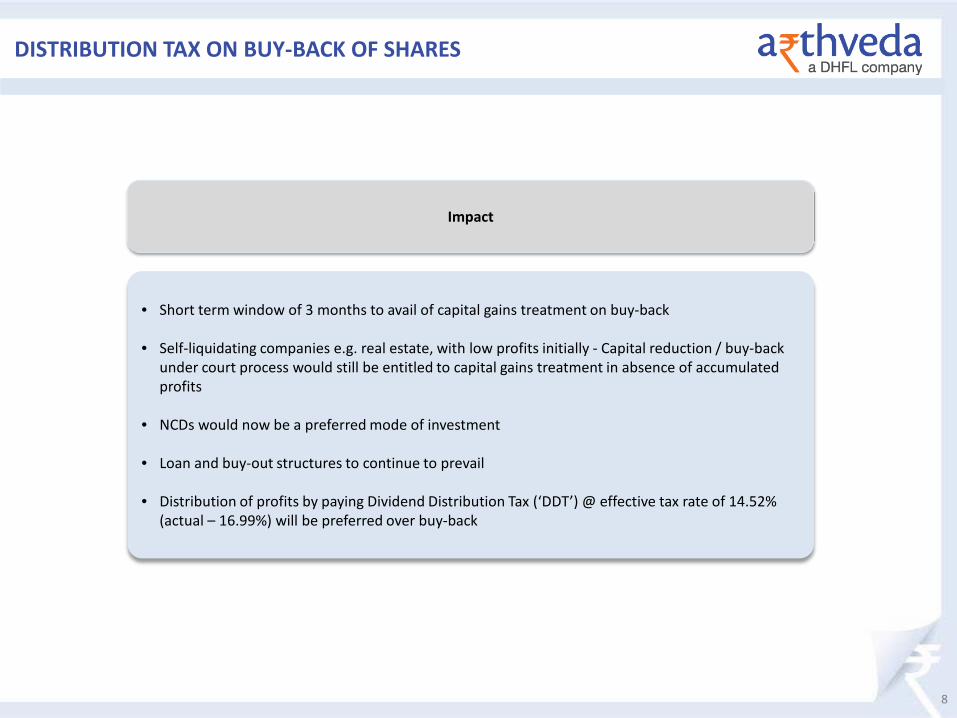

Impact

• Short term window of 3 months to avail of capital gains treatment on buy-back

• Self-liquidating companies e.g. real estate, with low profits initially - Capital reduction / buy-back under court process would still be entitled to capital gains treatment in absence of accumulated profits

• NCDs would now be a preferred mode of investment

• Loan and buy-out structures to continue to prevail

• Distribution of profits by paying Dividend Distribution Tax (‘DDT’) @ effective tax rate of 14.52% (actual – 16.99%) will be preferred over buy-back

9

Buy back Example

XYZ Pvt. Ltd. Issued 1,000 Equity shares of Rs. 10 each to Mr. S on 1st April,2003 at Rs. 20 per share

• S sold these shares to B at Rs. 40 per share on 1st April,2008

• XYZ Pvt. Ltd. Buys back these shares on payment of Rs. 100 per share on 1st May,2013

• Cost Inflation Index-2008-09-582 and for 2013-14 is likely to be say 900

• XYZ Pvt. Ltd. To pay distribution tax (Rs. 100-Rs.20) Rs.80 @ 20% Rs. 16 x 1,000= Rs. 16,000

• B would have paid capital gains tax on (Rs.100-Rs.62) Rs. 38 @20% Rs.7.60 x 1,000= Rs.7,600

10

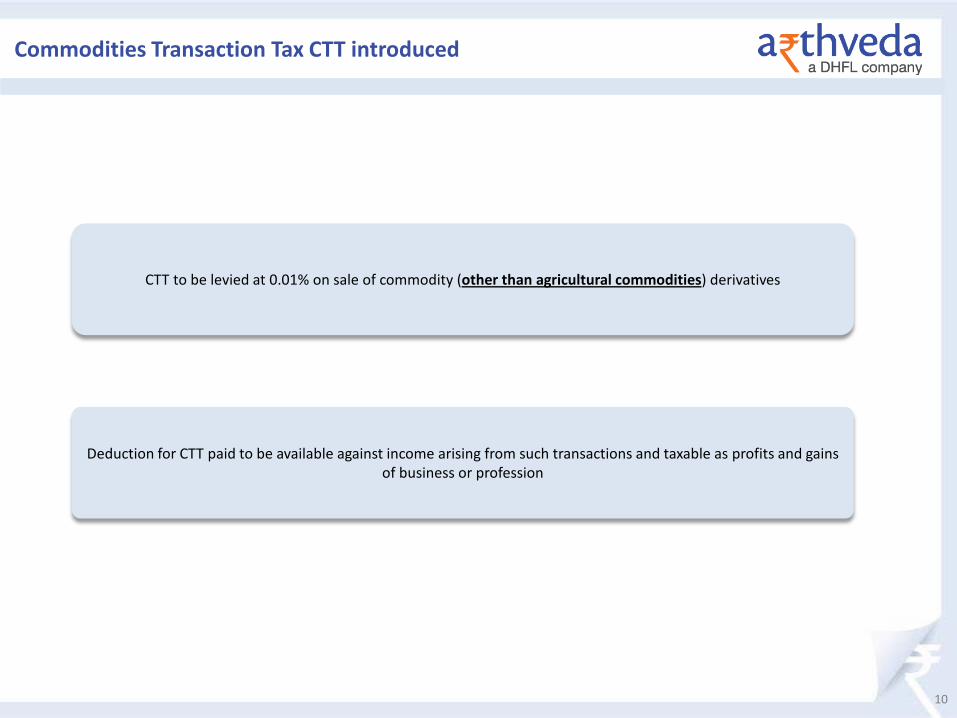

Commodities Transaction Tax CTT introduced

CTT to be levied at 0.01% on sale of commodity (other than agricultural commodities) derivatives

Deduction for CTT paid to be available against income arising from such transactions and taxable as profits and gains of business or profession

11

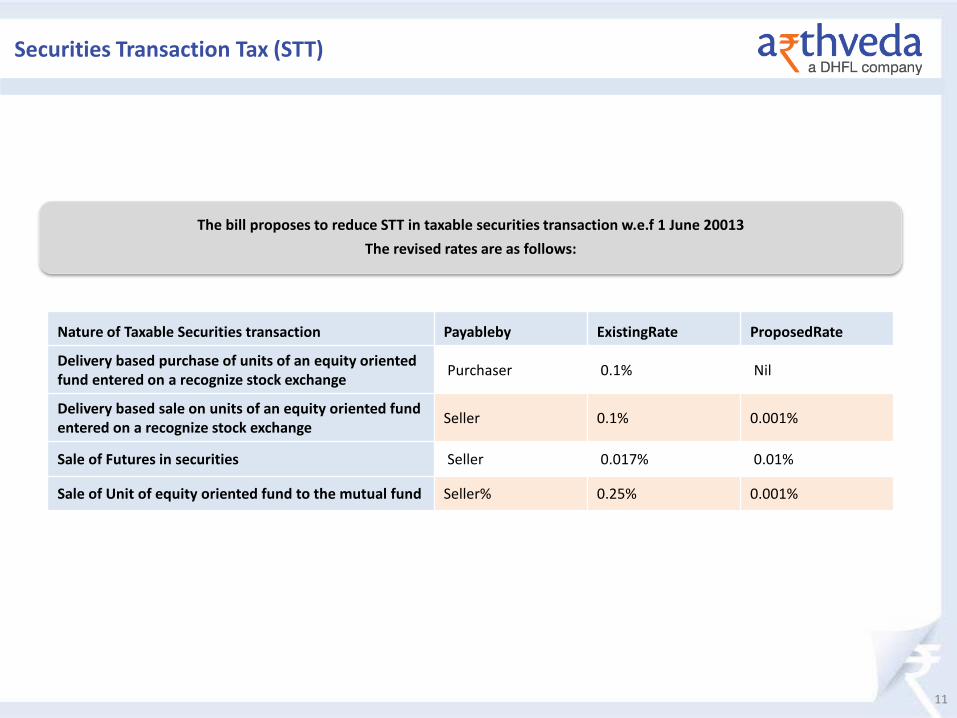

Securities Transaction Tax (STT)

The bill proposes to reduce STT in taxable securities transaction w.e.f 1 June 20013 The revised rates are as follows:

Nature of Taxable Securities transaction Payableby ExistingRate ProposedRate

Delivery based purchase of units of an equity oriented fund entered on a recognize stock exchange Purchaser 0.1% Nil

Delivery based sale on units of an equity oriented fund entered on a recognize stock exchange Seller 0.1% 0.001%

Sale of Futures in securities Seller 0.017% 0.01%

Sale of Unit of equity oriented fund to the mutual fund Seller% 0.25% 0.001%

12

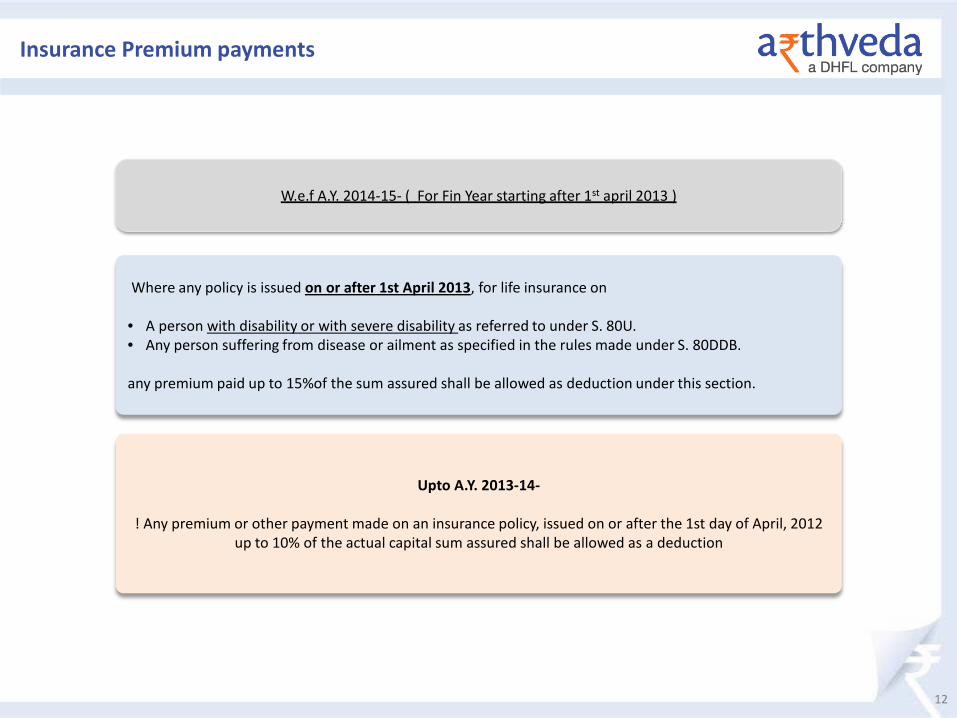

Insurance Premium payments

Where any policy is issued on or after 1st April 2013, for life insurance on • A person with disability or with severe disability as referred to under S. 80U. • Any person suffering from disease or ailment as specified in the rules made under S. 80DDB. any premium paid up to 15%of the sum assured shall be allowed as deduction under this section.

W.e.f A.Y. 2014-15- ( For Fin Year starting after 1st april 2013 )

Upto A.Y. 2013-14-

! Any premium or other payment made on an insurance policy, issued on or after the 1st day of April, 2012 up to 10% of the actual capital sum assured shall be allowed as a deduction

13

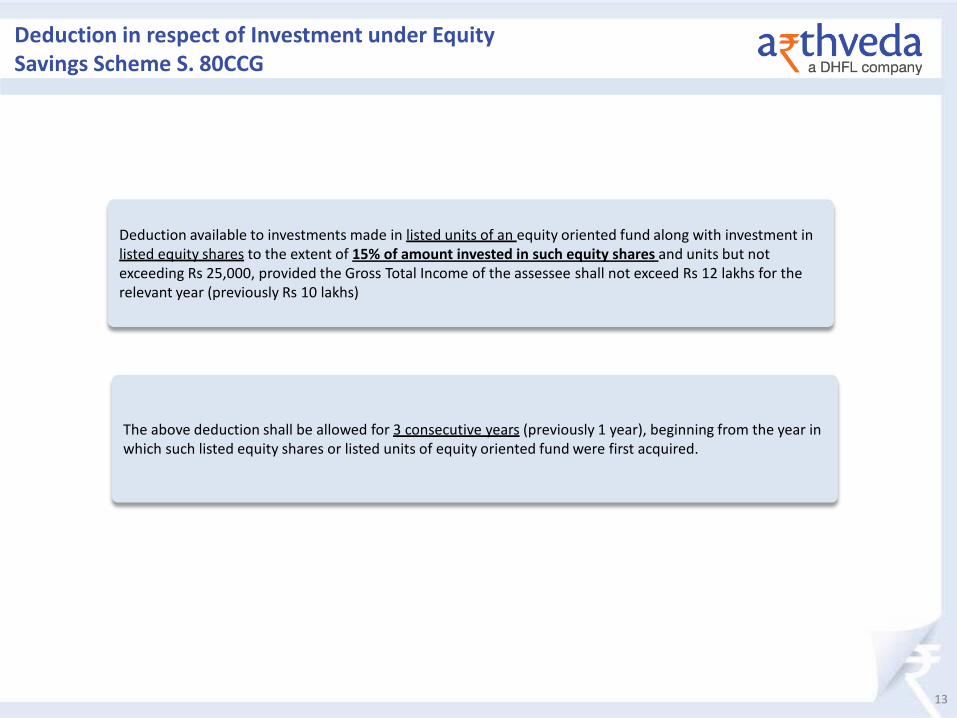

Deduction in respect of Investment under Equity Savings Scheme S. 80CCG

Deduction available to investments made in listed units of an equity oriented fund along with investment in listed equity shares to the extent of 15% of amount invested in such equity shares and units but not exceeding Rs 25,000, provided the Gross Total Income of the assessee shall not exceed Rs 12 lakhs for the relevant year (previously Rs 10 lakhs)

The above deduction shall be allowed for 3 consecutive years (previously 1 year), beginning from the year in which such listed equity shares or listed units of equity oriented fund were first acquired.

14

MEDICLAIM SCHEMES – Sec 80 D

Currently, any contribution made by an individual or a Hindu undivided family (HUF) under the Central Government Health Scheme is allowed as a deduction upto Rs 15,000.

Deduction of contributions towards Central Government Health Scheme extended to other schemes to be notified by the Government.

15

Deduction in respect of interest on loan taken for residential house property: Section 80EEE

Interest up to Rs 1 lakh allowed as a deduction on loan taken by an individual from any financial Institution during AY 2014-15 for the purpose of acquiring residential house property provided

The loan has been sanctioned during the FY 2013-14 • The loan < Rs 25 lakhs

• Value of the residential house property < =Rs 40 lakhs

• The assessee does not own any residential house property on the date of sanction of loan

• Deduction of balance amount of Rs 1 lakh can be claimed in AY 2015-16, if interest for A.Y. 2014BU-

1DG5ETis20l1e3s: Nsihtahr JaamnbuRsasri.a 1 lac.

16

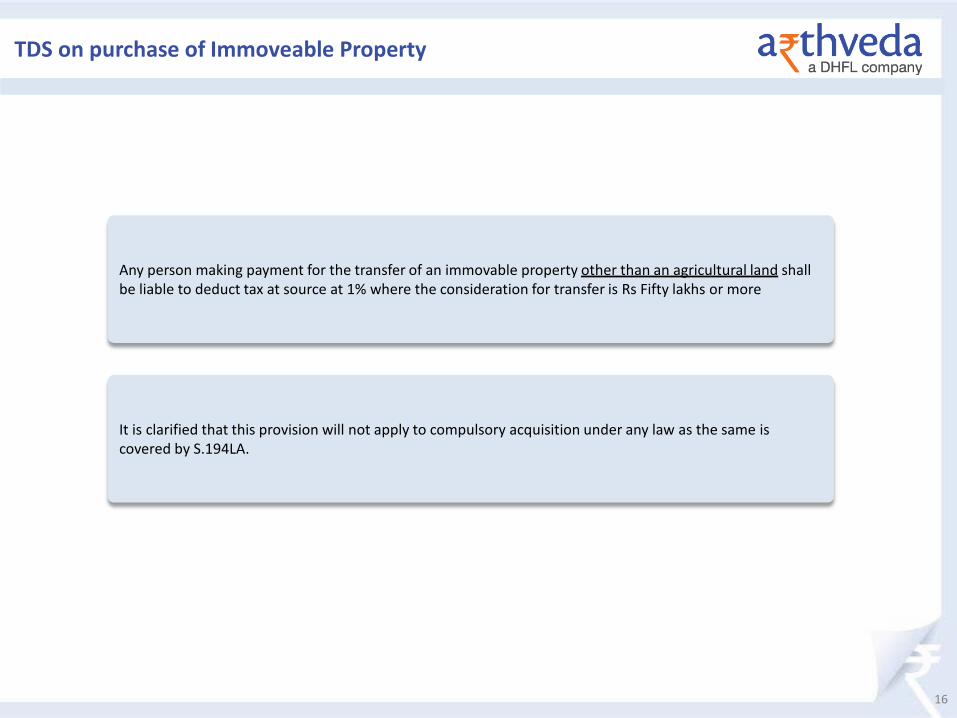

TDS on purchase of Immoveable Property

Any person making payment for the transfer of an immovable property other than an agricultural land shall be liable to deduct tax at source at 1% where the consideration for transfer is Rs Fifty lakhs or more

It is clarified that this provision will not apply to compulsory acquisition under any law as the same is covered by S.194LA.

17

Taxation of dividends received from ‘foreign companies’ at 15% - extended to 31 March 2014

No DDT on subsequent distribution of such dividends received from a ‘foreign subsidiary’ provided declared in the same FY (effective from 1 June 2013)

Indian companies holding between 26% and 50% in a Foreign company ineligible for the DDT relief

Particulars Before 1.6.2013 After 1.6.2013

Distributable profits (A) 100.00 100.00

Dividend from foreign subsidiary (B) 50.00 50.00

Tax on dividends @ 15% (C) 7.50 7.50

Net distributable profits (D) = (A)+(B)-(C) 142.50 142.50

Less: Credit for foreign dividends (E) = (B) - 50.00

Distributable profits on which DDT payable (F) = (D)-(E) 142.50 92.50

DDT @ 16.99% (G) 20.69 13.43

Dividends distributed in India (H) = (D) - (G) 121.81 129.07

OTHER AMENDMENTS – FOREIGN DIVIDENDS

18

Other Regulatory changes impacting investments

19

Recommendations provided in the report presented by the Financial Sector Legislative Reforms Commission will be examined.

WHAT DOES IT MEAN ???????????

20

Present Regulators in Financial Sector (7 agencies)

• RBI

• SEBI

• IRDA

• PFRDA(Pension Fund Regulatory & dev Authority)

• FMC(Forward Market Commission)

• SAT(Securities Appellate Tribunal)

• DICGC

• FSDC (Fin Sect Dev. Council)

21

Proposed Regulators in Financial Sector (8 agencies)

• RBI

• FSDC (Fin Sect Dev. Council)

• UFA (United Financial Agency) proposed merger of SEBI, IRDA, PFRDA &FMC)

• DMO (Debt Management Office)

• FRA( Financial Redressal Agency)

• FSAT

• Resolution Corporation

• (source TOI dt. 2/10/12-govt appointed panel)

22

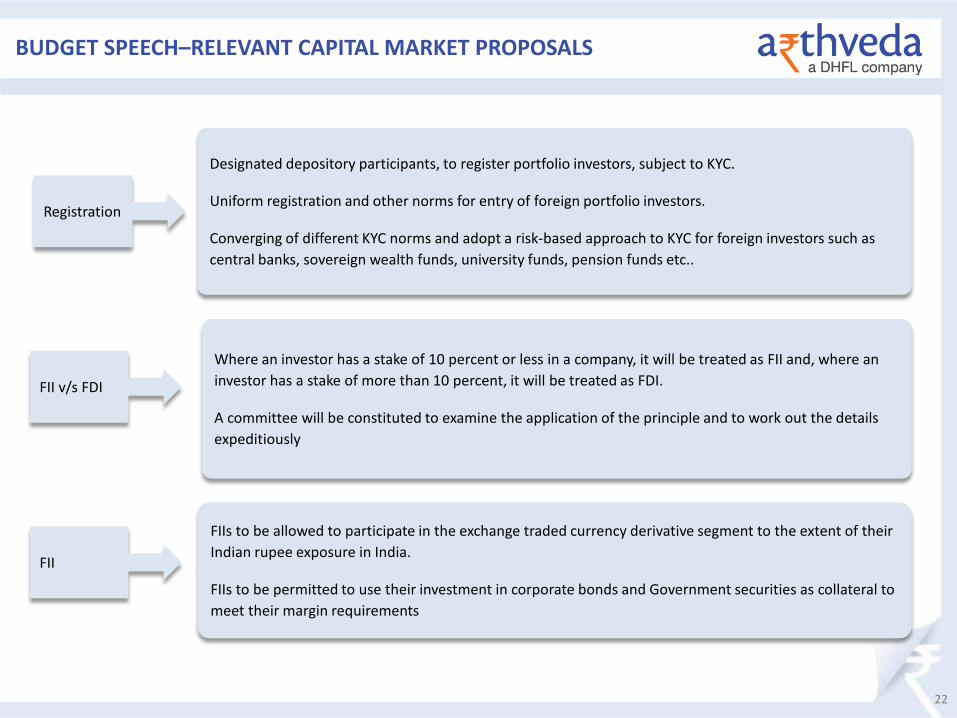

Registration

Designated depository participants, to register portfolio investors, subject to KYC.

Uniform registration and other norms for entry of foreign portfolio investors.

Converging of different KYC norms and adopt a risk-based approach to KYC for foreign investors such as central banks, sovereign wealth funds, university funds, pension funds etc..

FII v/s FDI

Where an investor has a stake of 10 percent or less in a company, it will be treated as FII and, where an investor has a stake of more than 10 percent, it will be treated as FDI.

A committee will be constituted to examine the application of the principle and to work out the details expeditiously

FII

FIIs to be allowed to participate in the exchange traded currency derivative segment to the extent of their Indian rupee exposure in India.

FIIs to be permitted to use their investment in corporate bonds and Government securities as collateral to meet their margin requirements

BUDGET SPEECH–RELEVANT CAPITAL MARKET PROPOSALS

23

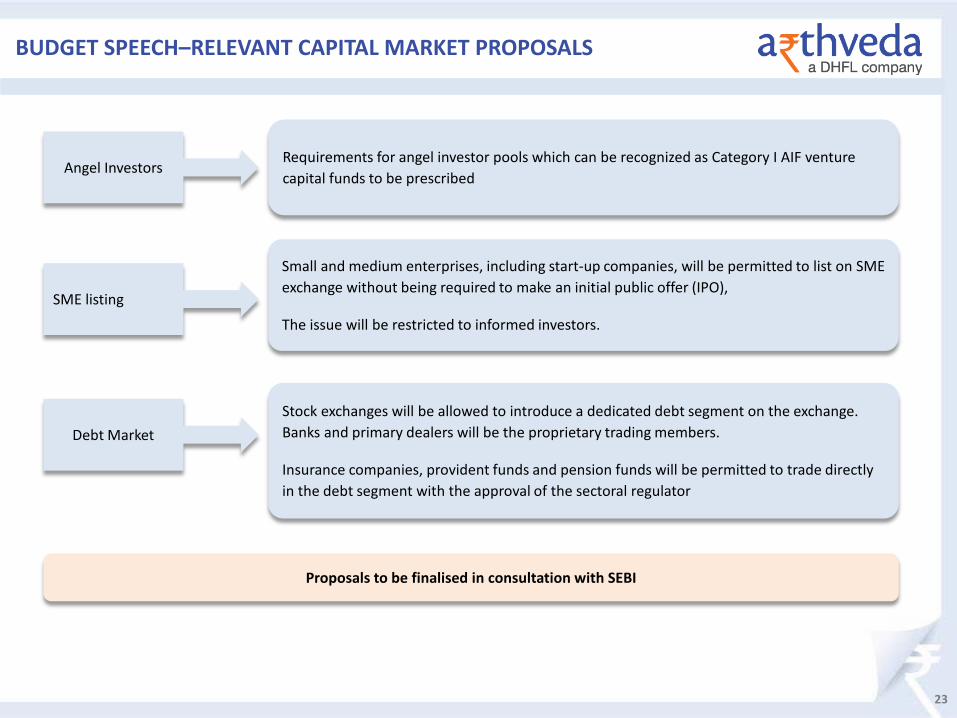

Angel Investors Requirements for angel investor pools which can be recognized as Category I AIF venture capital funds to be prescribed

SME listing

Small and medium enterprises, including start-up companies, will be permitted to list on SME exchange without being required to make an initial public offer (IPO),

The issue will be restricted to informed investors.

Debt Market Stock exchanges will be allowed to introduce a dedicated debt segment on the exchange. Banks and primary dealers will be the proprietary trading members.

Insurance companies, provident funds and pension funds will be permitted to trade directly in the debt segment with the approval of the sectoral regulator

Proposals to be finalised in consultation with SEBI

BUDGET SPEECH–RELEVANT CAPITAL MARKET PROPOSALS

24

Capital Market Reforms proposed

• Foreign portfolio investors uniform norms

• Converge different KYC norms to make it easier for Central banks, sovereign wealth funds, university funds, pension funds etc. to invest in India.

• FDI & FII route criteria distinguished (< , > 10%)

• FIIs will be permitted to participate in the exchange traded currency derivative segment upto their INR exposure .

• FIIs will be permitted to use their investment in corporate bonds and Government securities as collateral to meet their margin requirements.

• The list of eligible securities in which Pension Funds and Provident Funds may invest will be enlarged to include exchange traded funds, debt mutual funds and asset backed securities.

25

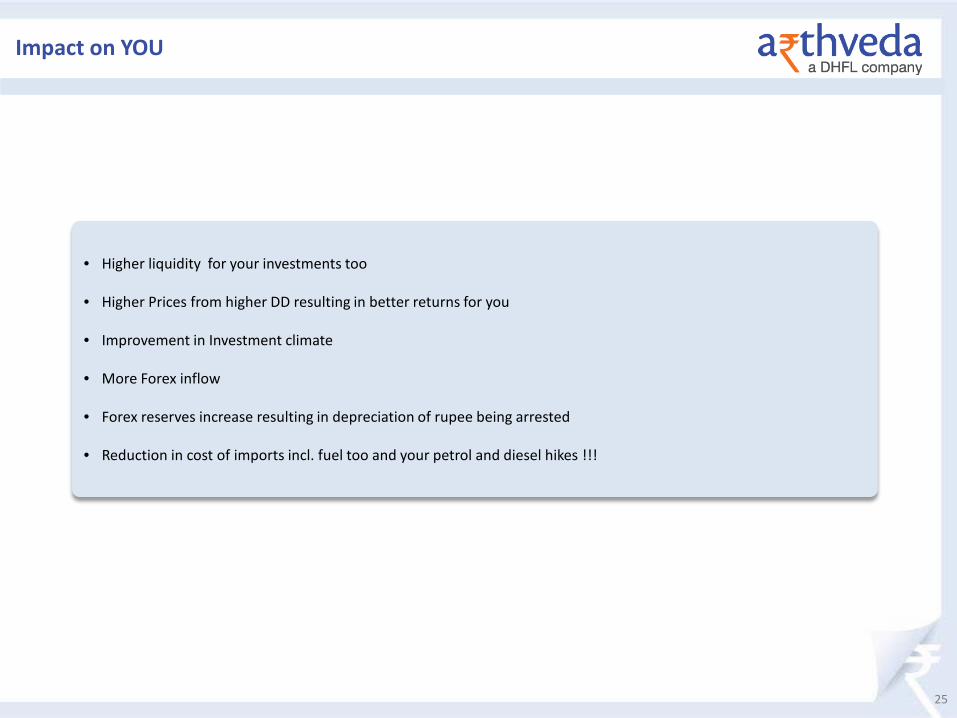

Impact on YOU

• Higher liquidity for your investments too

• Higher Prices from higher DD resulting in better returns for you

• Improvement in Investment climate

• More Forex inflow

• Forex reserves increase resulting in depreciation of rupee being arrested

• Reduction in cost of imports incl. fuel too and your petrol and diesel hikes !!!

26

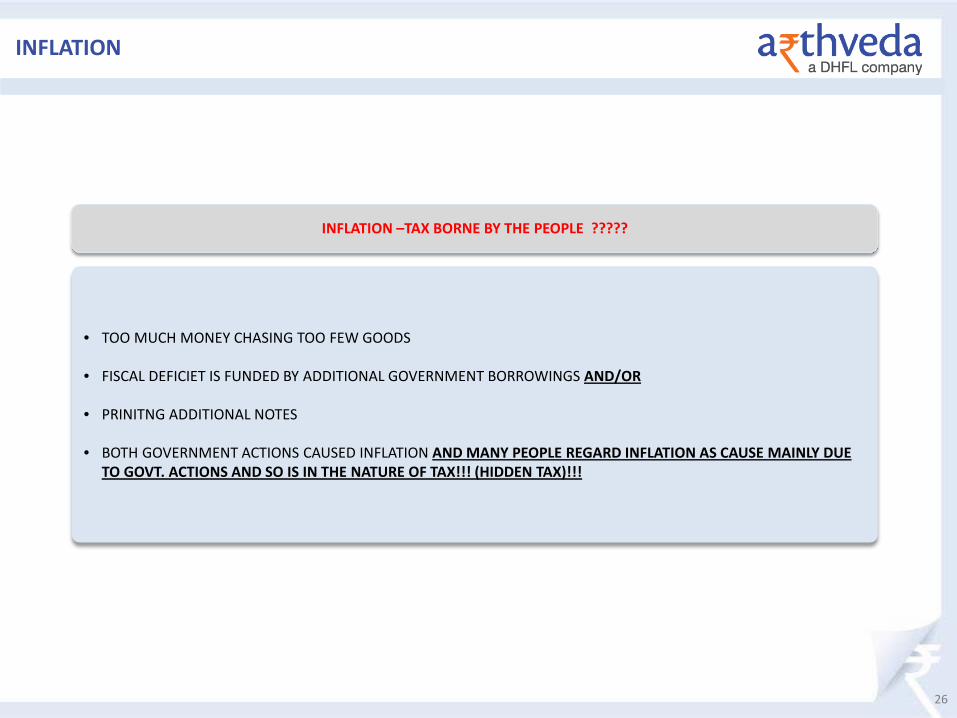

INFLATION

• TOO MUCH MONEY CHASING TOO FEW GOODS

• FISCAL DEFICIET IS FUNDED BY ADDITIONAL GOVERNMENT BORROWINGS AND/OR

• PRINITNG ADDITIONAL NOTES

• BOTH GOVERNMENT ACTIONS CAUSED INFLATION AND MANY PEOPLE REGARD INFLATION AS CAUSE MAINLY DUE TO GOVT. ACTIONS AND SO IS IN THE NATURE OF TAX!!! (HIDDEN TAX)!!!

INFLATION –TAX BORNE BY THE PEOPLE ?????

27

Pass through for domestic funds

28

Pass through for domestic funds

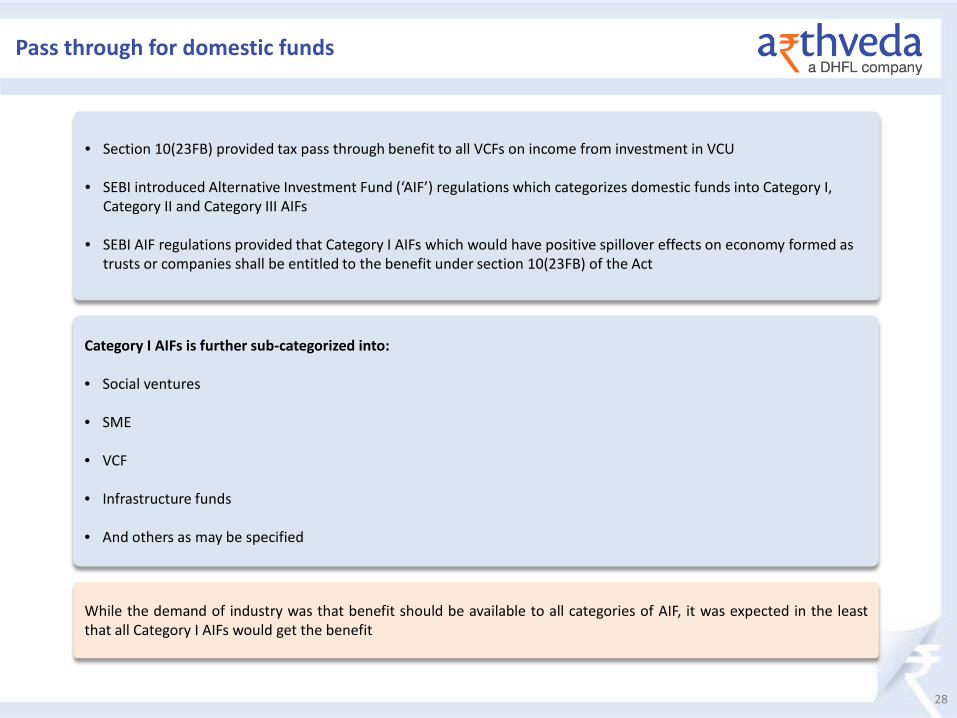

• Section 10(23FB) provided tax pass through benefit to all VCFs on income from investment in VCU

• SEBI introduced Alternative Investment Fund (‘AIF’) regulations which categorizes domestic funds into Category I, Category II and Category III AIFs

• SEBI AIF regulations provided that Category I AIFs which would have positive spillover effects on economy formed as trusts or companies shall be entitled to the benefit under section 10(23FB) of the Act

Category I AIFs is further sub-categorized into: • Social ventures

• SME

• VCF

• Infrastructure funds

• And others as may be specified

While the demand of industry was that benefit should be available to all categories of AIF, it was expected in the least that all Category I AIFs would get the benefit

29

Pass through for domestic funds

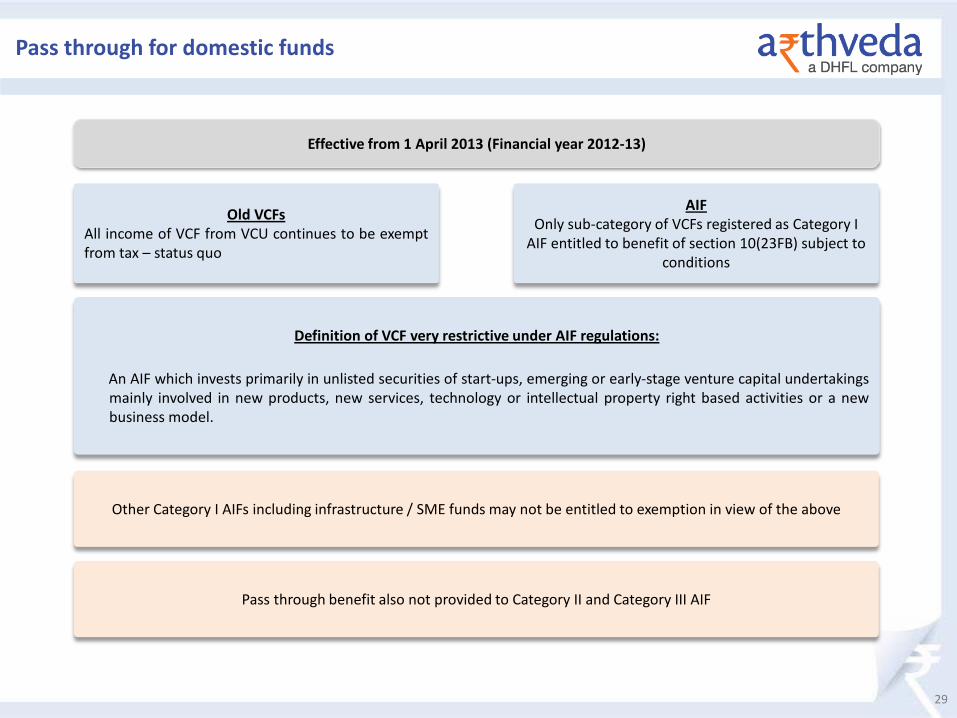

Old VCFs All income of VCF from VCU continues to be exempt from tax – status quo

Definition of VCF very restrictive under AIF regulations:

An AIF which invests primarily in unlisted securities of start-ups, emerging or early-stage venture capital undertakings mainly involved in new products, new services, technology or intellectual property right based activities or a new business model.

Other Category I AIFs including infrastructure / SME funds may not be entitled to exemption in view of the above

Effective from 1 April 2013 (Financial year 2012-13)

AIF Only sub-category of VCFs registered as Category I

AIF entitled to benefit of section 10(23FB) subject to conditions

Pass through benefit also not provided to Category II and Category III AIF

30

Private trusts and Pass Through Certificates

Matter of litigation for the mutual fund industry as such trusts charged to tax at MMR even though mutual funds are exempt from tax

• Private trusts created for the purposes of securitization of receivables / loans issued Pass Through Certificates (‘PTC’) to investors

• Trusts claimed that income should be taxed in hands of investors or in their hands in same and like manner as investors

• Tax authorities issued notices to several trusts levying tax in their hands treating it as business income taxable at MMR

31

REGULATORY CHANGES BY SEBI AFFECTING INVESTMENTS :

• MUTUAL FUNDS ( Direct subscription v/s via advisor different NAV’s) Total expense ratio limits and separate option for direct investments.

• ALTERNATIVE INVESTMENTS FUND ( Norms announced in May 2012 by SEBI ) Discussed earlier

• PORTFOLIO MANAGEMENT SERVICES ( New Norms announced in Feb 2012) Minimum limits raised from Rs. 5 Lac to Rs. 25 Lac.

32

SPECIAL THANKS :

Mr. Bikram Sen Ms. Shyamala Asangi Mr. Masban Pereira Mr. Soumen Dey

Ms. Shuchi Pandey Ms. Ruchi Chauhan

Employees of AVFM Employees of DHFL Group and associate companies

33

• The views expressed here in above are compiled by the author. The company or any of its associates does not necessarily endorse all the views expressed here in above.

• The author has also compiled data from various sources, considered to be reliable. However neither the author nor the company guarantees the accuracy of all the data or statements specified herein and absence of any inadvertent errors. However appropriate due diligence has been made to ensure that the data and statements are correct.

• The recipients and the attendees are requested to consult their personal tax consultants/advisors or help desk of the regulators etc. before acting on any suggestions.

• The above is not fully exhaustive but only some of the key issues have been taken up.

Disclaimer

Satyameva Jayate

Thank you

ArthVeda Fund Management Pvt. Ltd. Grd. Floor, HDIL Towers, Anant Kanekar Marg, Bandra (E),

Mumbai 400051, Maharashtra, India Contact no.: +91 22 67748500; Fax: +91 22 67748585

www.arthveda.co.in

34

Risks in Investments

35

Risk is just the flip side of opportunity. Investments even in G-SEC or Bank FD are not risk free

Business Risk

Fund manager Risk

Liquidity Risk

Sovereign Risk

Concentration Risk

Corporate governance Risk

Currency Risk

Economic Risk

Information Risk

Capital loss Risk

Tax Risk

Stock picking Risk Transaction cost Risk

Agency Risk

Trading Risk

Market Risk Allocation Risk

Composition Risk

Event Risk