Embed Size (px)

Citation preview

AUTHORAaron Fine, Partner at Oliver Wyman Frank Rohde, CEO of Nomis Solutions

EXECUTIVE BRIEF

Financial Services

DEPOSITS: A RETURN TO VALUE?

INTRODUCTION

In 2006 (ahead of the credit losses that would soon

decimate lending profits), one of the largest banks in

the United States publicly reported that 1/3rd of its

earnings and more than half of its shareholder value

added came from retail deposits and treasury services.

This bank has significant businesses in capital markets

and commercial banking, mortgage lending, credit

cards and wealth management. Yet the earnings power

of the deposit product set was so high that it quietly

dominated the economic value creation of the bank.

Since 2008 however, new regulation regarding debit

interchange and consumer overdraft, and even

more importantly the dramatic fall in base interest

rates, have greatly impacted the profitability of

US deposits. This has reduced retail deposit profit

margins on the order of 3/4ths at many banks.

In that light, it’s easy to understand the excitement

that even the slightest overtures of sustained rising

rates causes among deposit managers (and banking

executives more broadly). The recent rise in long-term

interest rates is more than enough to allow us to begin to

consider a return to more favorable times.

While it will obviously take several years for the

recovery to be complete, the current structure

of the yield curve indicates that by 2018 the rate

environment would closely resemble conditions in

2005 (coming out of the 2001 recession). Under the

deposit NIM that the aforementioned bank realized

in that year, and given its current balances, retail

deposit profitability would nearly regain pre-crisis

levels. And while that full recovery is still five years out,

the period between now and then would be one of

tailwinds rather than the headwinds of the past five.

Deposit businesses indeed have a lot to get

excited about.

However they also cannot afford to lose sight of five

critical challenges that will accompany the rise of rates.

Indeed, we believe that given the complexity of the

emerging deposit landscape, the rise of interest rates

could be a trigger that will create tremendous separation

between winners and losers. Banks that understand the

dramatic forces impacting the business, take steps to

respond to them, and successfully manage the transition

will emerge as market leaders well positioned to enjoy

the more favorable conditions we appear headed

towards. Those institutions that stumble, however, could

well find their strategic position so diminished that the

better environment will not be enough.

The five key factors impacting the deposit market as

rates rise:

1. The instability of balance growth since the crisis

2. New deposit competitors

3. Basel III and the Liquidity Coverage Ratio

4. Lagging and distorted FTP rates

5. The great unknown: the digital evolution

This is the first of a series of three publications that

Oliver Wyman will release over the next several

months detailing our views on the evolving deposit

landscape. In this publication we focus on the financial

implications and management challenges of the rising

rate environment. We also introduce our partnership

with Nomis Solutions to bring industry-leading deposit

product management tools to the market.

The second publication will focus more specifically on

the potential evolution of deposit product design. The

third will focus in detail on the potential for disruptive

threats to the industry. Given the time constraints of our

audience, we have opted to produce these publications

in an “executive brief” format that quickly illustrates

each of the key points. Those interested in a more

detailed discussion can reference the related webinar, or

contact us for a more in-depth conversation.

Copyright © 2013 Oliver Wyman 1

A RETURN TO DEPOSIT VALUE

Loss of fee income has received the bulk of attention

in deposits, but the deterioration of net interest

margin has had a similarly sized impact on deposit

profitability. While 2007 levels of fee income may

be a thing of the past, a return to a higher interest

rate environment could lead to a return to historical

levels of deposit NIM. As seen in a study of this

leading US retail bank, a return to the deposit NIM

experienced in 2005 – combined with balance

growth and improvements in operating efficiency

that have occurred since the crisis – would result in

deposit profit levels near those reached in 2007.

3.0% 6%

2.5% 5%

2.0% 4%

1.5% 3%

1.0% 2%

0.5% 1%

3.5% 7%

2007 2008 2009 2010 2011 2012 2013

DEPOSIT NIM 1 YEAR SWAP

1. BASE RATES FALL, LEADING TO A DECLINE IN NIM1,2

0%0%

Deposit NIM

1 year SWAP

H1 2007 Q3. 2013

2. RETAIL DEPOSIT PROFIT MARGIN SUFFERS1

InterestIncome

Fee Income

Operating expense

2.65%

0.69%

• The dramatic decline in base interest rates led to a 50% decline in NIM

• As a result of the declining NIM and regulatory pressure on fees, deposit profit margin fell 75%

Q3. 2005

5%

4%

1%

3%

2%

3 Months 12 Months 5 Years

0%

3. EXPECTATIONS OF RISING RATES3

DEC. 2016(implied)

SEP. 2013(actual)

DEC. 2018(implied)

H1. 2007 Q3. 2013 Q3. 2013@Q3. 2005 NIM

4. RAISE THE PROMISE OF A RETURN TO DEPOSIT VALUE1

Value of returnto Q3. 2005 NIM

• The current yield curve indicates a return to a 2005-like rate environment by the end of 2018

• If deposit NIM returned to Q3 2005 levels, deposit earnings would nearly regain their pre-crisis levels – despite the losses to fee income (all else being the same)

* CASE STUDY: LEADING US RETAIL BANK

Copyright © 2013 Oliver Wyman 2

FIVE FACTORS THAT WILL COMPLICATE THE RETURN TO VALUE

Unfortunately, at least five separate factors will

complicate banks’ efforts to recover historical levels

of deposit NIM. Any of these five on their own would

be difficult to navigate, but the five together represent

an unprecedented level of challenge. Of particular

importance will be the rise of digital technologies. The

period since the crisis has seen tremendous levels of

disruptive innovation in other industries. If a rise in

deposit value sparks similar change in retail deposits,

changes in customer access brought about by digital

could serve as a catalyst that links the other four factors

together, enhancing the possible effects.

2005 2006 2007

FTP

5-YearSWAP rate

4. LAGGING FUNDS TRANSFER PRICING

1. DISRUPTED BALANCES (CASE STUDY)1

FEDERAL RESERVE SYSTEM

12 CFR Part 249

Regulation WW; Docket No. R-[xxxx]

FEDERAL DEPOSIT INSURANCE CORPORATION

12 CFR Part 329

RIN 3064-AE04

Liquidity Coverage Ratio: Liquidity Risk Measurement, Standards, and Monitoring

AGENCIES: O�ce of the Comptroller of the Currency, Department of the Treasury; Board of Governors of the Federal Reserve System; and Federal Deposit Insurance Corporation.

ACTION: Notice of proposed rulemaking with request for public comment.

3. NEW RULES FOR LIQUIDITY5

2. COMPETITIVE PRESSURE4

5. DIGITAL

2007

TODAY

…………

……… …

VIDEO AUDIO COMMUNI-CATION

DEPOSITS

TOP 20 US BANK HOLDING COMPANIES (BY ASSETS)JPMorgan Chase & Co.

Bank of America Corp.

Citigroup Inc.

Wells Fargo & Co.

Goldman Sachs Group Inc.

Morgan Stanley

General Electric Capital Corp.

Bank of New York Mellon Corp.

U.S. Bancorp

HSBC North America Hldgs Inc.

Shading indicates new potential deposit competitor since financial crisis

11

12

13

14

15

16

17

18

19

20

1

2

3

4

5

6

7

8

9

10

Capital One Financial Corp.

PNC Financial Services Group

State Street Corp.

TD Bank US Holding Co.

BB&T Corp.

Ally Financial Inc.

SunTrust Banks Inc.

Principal Financial Group Inc.

American Express Co.

Charles Schwab Corp. Q12005

Q22007

Q32013

CHECKING DEPOSIT TOTAL

Q12005

Q22007

Q32013

90% growth 65% growth

Copyright © 2013 Oliver Wyman 3

1. DISRUPTED BALANCES

Many US institutions have seen significant growth in

deposit balances since the financial crisis. This growth

has – to a degree – helped to offset the decline in net

interest margin, and if the balances remain in place

as rates rise, deposit profits could soar. Most deposit

product managers and treasurers however are skeptical

of this growth, unsure how much will migrate to other

investments as the economy improves. As the yield curve

has steepened, many banks have found themselves with

a tempting dilemma: gamble and deploy the balances

against longer-term assets and elevate NIM now, or invest

the balances conservatively and reduce risk in the future.

Q12005

Q22007

Q32013

1. RECENT SURGE IN DEPOSIT GROWTH (CASE STUDY)1

CHECKING BALANCES DEPOSIT BALANCES

Q12005

Q22007

Q32013

90% growth65% growth

2. WHAT COULD HAVE CAUSED IT?

CAUSE

EXAMPLE

Changein business

• Acquisition

• New product structures

• Need for liquidity

Foreseeablemacro-economic

events

• Economic growth

• Shift of the yield curve

Crisis-specificevent

• Transaction Account Guarantee Program

A B C

• Deposit and checking growth was flat from 2005 through mid 2007, but has risen sharply since

• Targeted account level analysis can help organizations identify the likely causes of balance growth – and therefore what to expect as the environment shifts

20%

40%

60%

80%

-40%

-60%

-20%

Total growth Growth/online account

Growthin checking

Growthin CD

0%

3. WHAT DID CAUSE IT? (CASE STUDY)1

CHANGE IN BUSINESS PREDICTABLE VS.UNPREDICTABLE SHIFTS

4. IMPLICATIONS

1 Month 1 Year 3 Year 5 Year 10 Year

2.5% x 5% = 12.5 bps

LIBOR/Swap curve

• Growth per account that trails total growth indicates a potentially sustainable business shift. Offsetting declines in CD growth indicate a re-allocation of customer funds that likely will reverse (but stay with the bank)

• Each 5% of checking balances that could be invested “long-term” instead of “short-term” is worth 15 bps to total checking NIM – likely warranting an investment in deeper understanding

Copyright © 2013 Oliver Wyman 4

2. COMPETITIVE PRESSURE

In the wake of the financial crisis many of the largest

non-bank US financial institutions converted to bank

holding companies. At the time, there was speculation

that they could quickly become significant deposit

takers. Instead, they largely met their liquidity needs

directly through government-sponsored funding. As

the economy improves however, and rates rise, the

scenarios envisioned by that post-crisis speculation

could come to pass. If this pressure emerges, and

combines with pressure from traditional banks

accelerating their lending, the current liquidity rich

position that most institutions are enjoying will come

under substantial pressure.

1. THE “NEW” BANKS6

TOP 20 US BANK HOLDING COMPANIES (BY ASSETS)

JPMorgan Chase & Co.

Bank of America Corp.

Citigroup Inc.

Wells Fargo & Co.

Goldman Sachs Group Inc.

Morgan Stanley

General Electric Capital Corp.

Bank of New York Mellon Corp.

U.S. Bancorp

HSBC North America Hldgs Inc.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

Capital One Financial Corp.

PNC Financial Services Group

State Street Corp.

TD Bank US Holding Co.

BB&T Corp.

Ally Financial Inc.

SunTrust Banks Inc.

Principal Financial Group Inc.

American Express Co.

Charles Schwab Corp.

Shading indicates new potential deposit competitor since financial crisis

2. WHY THEIR DEPOSIT GROWTH HAS BEEN SLOW

Legal and regulatory complexity

Availability of goverment sponsored fundingat similar interest expense

$$ $

Low loan growth

• Five of the top twenty US bank holding companies today were not threats in the US deposit market before the crisis – but could be as rates begin to rise

• Deposit growth among these banks has been slow for three key reasons – all of which could erode as the economy improves, rates rise, and the cost advantage of deposits increases

3. LARGEST LOAN TO DEPOSIT GAPS OF US BANK HOLDING COMPANIES6

60

80

240

220

20

40

1 2 3 4 5 6 7 8 9 10

Represents the size of the US deposit base it would require to fill the gap

$BN

…

……

5

23

48

#

40

18

0

4. IMPLICATIONS7

% OF US TOTALCONSUMER DEPOSITS # OF ING DIRECTS

Conservativeestimate

Aggressiveestimate

6x

5.5%

10%

• Overall, BHCs with the ten largest loan to deposit gaps would require $450 BN of deposit funding to cover their current lending needs

• Closing that gap with retail deposits would represent 5-10% of the market – or 5.5 ING Directs. If institutions look to deposits to fund other earning assets (e.g., securities) that would increase pressure further

Copyright © 2013 Oliver Wyman 5

3. NEW RULES FOR LIQUIDITY

Complicating the potential fight for deposit liquidity:

the ‘liquidity value’ of many types of funding is about

to change. The Federal Reserve recently issued

preliminary liquidity regulations for the US market. Once

implemented, these regulations will alter the value of

certain types of funding vs. others. The good news for

retail deposit taking: retail balances will be viewed as

more stable (and therefore more valuable) than other

sources of funding. The bad news: if other sources of

funding are deemed less stable, there will likely be added

demand for liquidity overall, and pressure on retail

deposits as a result.

1. OVERVIEW OF FEDERAL RESERVE LIQUIDITY COVERAGE RATIO PROPOSAL5

A “Retail” deposits have run-o� rates of 3% or 10%

B To qualify as “stable” (and get 3%)

– Fully insured

– Either a transactional account or otherwise part of a broader relationship that makes them less likely to leave

C Most “Wholesale” deposits have run-o� rates of 20-100%

– Small business deposits that qualify as retail will have the 3-10% run-o� rate

2. THE VALUE OF STABLE VS. LESS STABLE DEPOSITS

% OF BALANCES THAT CAN FUND LONG-TERM ASSETS

VALUE OF LONG-TERM MONEY VS. SHORT-TERM

bps

97%

90%

7%

2.7%

0.1%

2.6%x = 18– –

• Retail deposits will be considered significantly more stable than commercial deposits and other forms of wholesale funding. As well, “stable” retail balances – likely defined largely based on the presence of a transaction account – will have lower run-off rates than less stable retail balances

• Given the current structure of the yield curve, stable retail balances (that can be used to fund long-term assets) could be worth as much as 15–20 bps more than unstable. They may be worth vastly more vs. wholesale deposits. Note that this calculation is indicative and actual value will vary

3. THE KEY UNKNOWNS

The final rules(these are “proposals”)

“Regulatory” vs. “Economic” liquidity

True value of “Stable” vs. “Unstable”

4. IMPLICATIONS

50k Saving account

IF YOU HAVETHIS

THE VALUE OFTHIS

ISTHIS

Checkingaccount

Increased valuecreated by movingsavings to “stable”

50k $100

• The ultimate value of stable vs. unstable balances will depend on how closely the final rules resemble this proposal – as well as how banks implement the framework and what their individual liquidity needs are

• The value generated by adding a checking account to existing savings balances could be used to pay for better rates, features, or ATM rebates on the checking product

Copyright © 2013 Oliver Wyman 6

4. LAGGING FUNDS TRANSFER PRICING

For banks that use it, FTP communicates the value

of deposits and plays a role in everything from

product pricing to incentives to network planning. As

traditionally employed, it is typically very good in stable

environments. However, it is also challenged in quickly

changing or unique situations. When rates rise rapidly,

the FTP for more stable products (e.g., checking and

low-rate savings) lags behind. There are good reasons

for this and some positive business impacts. But banks

that don’t account for it and make adjustments to how

they use it to manage their business could be at a severe

disadvantage vs. other institutions – particularly new

entrants that are looking to grow balances quickly.

4.5%

3.5%

5.0%

4.0%

5.5%

1. FTP RATES LAG (CASE STUDY)1

2005 2006 2007 2005 2006 20072004

3.0%

5-YEAR SWAP REPORTED CHECKING NIM 6.0%

5.5%

5.0%

4.5%

4.0%

3.5%

3.0%

2. DUE TO THE “TRACTOR” EFFECT

2001 2002 2003 2004 2005 2006 2007

2.5%

2001-2005 Average

2003-2007 Average

2002-2006 Average

• Between 2005 and 2007 – as long-term rates rose more than 100 bps – NIM on checking balances at the sample bank was essentially flat

• The FTP “lag” is due to the fact that long-term stable deposits are used to fund long-term assets. As a result, the value of the deposit book reflects not only current asset yields, but also the historical yields at which the balances were invested

3.5%

4.0%

4.5%

2.5%

3.0%

3. POTENTIAL IMPACT AS RATES RISE

EoY 2016 EoY 2018

2.0%

Trailingaverage of the 5-Year SWAP

5-YearSWAP rate

Marginal view

Book view

4. IMPLICATIONS

Pricing

“BOOK” LENS

“MARGINAL” LENS

Product design Infrastructure investment

VS.

• As rates rise in this recovery, the same phenomena will be exhibited. The trailing average of the 5-year Swap rate will lag up to 125–150 bps behind the spot rate. Institutions that take a marginal view of the value of a dollar of deposits will be heavily advantaged

• FTP systems do a good job representing the value of a book of deposits. However, to represent the value of a marginal dollar of deposits in a rising rate environment adjustments may need to be made. Without adjustments incumbents could find themselves at a significant economic disadvantage across business decisions

Copyright © 2013 Oliver Wyman 7

5. DIGITAL

Given how busy bankers have been, it is easy to

lose track of how significantly other industries have

changed as a result of advancements in digital and

data technology. In just the period from the crisis

to now, many of the current market leaders in other

industries rose from obscurity while their predecessors

disappeared from the landscape. Meanwhile the

market leaders in financial services have been largely

unaffected. This has resulted in arguments by some that

there are fundamental barriers to change in our industry.

This could be true – but it’s also possible that the delayed

impact was simply a matter of circumstance.

1. THE WORLD (OUTSIDE OF OURS) HAS CHANGED

2007

TODAY

VIDEO AUDIO COMMUNICATION DEPOSITS

…………

……… …

2. FUNDAMENTALLY DIFFERENT?

INERTIA

TRUST REGULATIONCONVENIENCE

TIPPINGPOINT

• As hard as it is to remember, market leaders like Netflix, the iPhone, Facebook and Amazon were just barely emerging in 2007. Six years later they’ve ridden the digital wave to the top of their respective categories. In deposits, we’ve seen little significant change

• This has caused some to discount the possibility of disruptive innovation in deposits – pointing to market barriers that may be present in retail financial services that didn’t exist in the categories that have shifted so quickly

3. OR DIFFERENT CIRCUMSTANCES?

THE CHANGING DIGITAL VALUE GAP FOR RETAIL DEPOSITS

Rate advantage

Conveniencedisadvantage(illustrative)

Rate advantage of online banking offers (MMDA)

4%

1%

%

2007 2013 2018

4. IMPLICATIONS

DEPOSITS MIGHT BE DIFFERENT

but

so

LACK OF CHANGE ISN’T PROOF

WE MUST BE PREPARED

• Another possibility: the rate advantage of disrupters declined dramatically just as they were solving for their convenience disadvantages. If the rate advantage returns and convenience continues to improve, the value exchange for clients could shift quickly – and market leadership among providers may follow

• There are no assurances that either the “fundamentally different” or “different circumstances” arguments are correct. More than likely, the answer lies somewhere in between. But both the threat and the severity are high enough that banks must be prepared

Copyright © 2013 Oliver Wyman 8

A COMPLEX PROBLEM

As interest rates rise, bringing renewed importance to

deposit funding, new (and old) banks will compete for

new deposit balances with new – and varied – rules for

determining value. While this situation is complex, in

the past the impact on deposit behavior might have

been mitigated by the importance of physical channels.

Competition to any pocket of customers would have

been limited and the inconvenience of switching

would have provided a measure of natural protection.

However, it is for this reason that the rise of digital

disruption – less and less hindered by the barriers of the

past – could create a catalyst that dramatically increases

the challenge of the situation. With the competitive

landscape, the value of deposits, and the access to

customers all fundamentally altered, deposit behavior

is likely to be very difficult to predict based on historical

practices and historical data.

1. NEW BALANCES

… may be a sign of trust

2. NEW COMPETITORS

… was created when regulatorsopened the gate

4. VARIED RULES FOR FTP

VS.

… may result in a value gap that overcomes inertia

TIPPINGPOINT

LCR

3. NEW RULES FOR LIQUIDITY

… may be the impetus for significant change

2007 H1. 2013

14%

–

E-BOOK SHARE OFUS CONSUMERBOOK SPENDING

… has overcome higher convenience hurdles

5. DIGITAL8

Copyright © 2013 Oliver Wyman 9

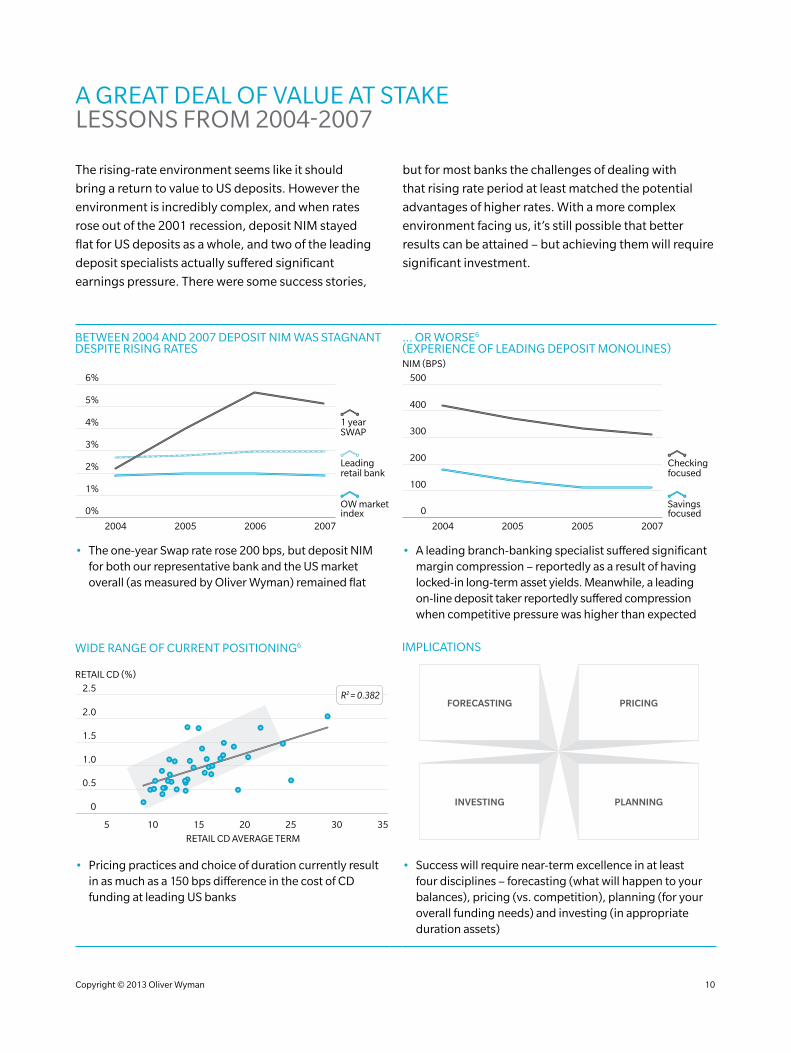

A GREAT DEAL OF VALUE AT STAKE LESSONS FROM 2004-2007

The rising-rate environment seems like it should

bring a return to value to US deposits. However the

environment is incredibly complex, and when rates

rose out of the 2001 recession, deposit NIM stayed

flat for US deposits as a whole, and two of the leading

deposit specialists actually suffered significant

earnings pressure. There were some success stories,

but for most banks the challenges of dealing with

that rising rate period at least matched the potential

advantages of higher rates. With a more complex

environment facing us, it’s still possible that better

results can be attained – but achieving them will require

significant investment.

BETWEEN 2004 AND 2007 DEPOSIT NIM WAS STAGNANT DESPITE RISING RATES

3%

4%

6%

5%

1%

2%

2004 2005 2006 2007

0%

Leading retail bank

OW marketindex

1 year SWAP

… OR WORSE6

(EXPERIENCE OF LEADING DEPOSIT MONOLINES)

300

400

500

100

200

2004 2005 2005 2007

0

Checkingfocused

Savingsfocused

NIM (BPS)

• The one-year Swap rate rose 200 bps, but deposit NIM for both our representative bank and the US market overall (as measured by Oliver Wyman) remained flat

• A leading branch-banking specialist suffered significant margin compression – reportedly as a result of having locked-in long-term asset yields. Meanwhile, a leading on-line deposit taker reportedly suffered compression when competitive pressure was higher than expected

0.5

WIDE RANGE OF CURRENT POSITIONING6

1.5

2.0

1.0

2.5

0

RETAIL CD AVERAGE TERM

5 10 15 20 25 30 35

R2 = 0.382

RETAIL CD (%)

Y-AXIS TITLE (LINE 1)Y-AXIS TITLE (LINE 2)

IMPLICATIONS

INVESTING

FORECASTING PRICING

PLANNING

• Pricing practices and choice of duration currently result in as much as a 150 bps difference in the cost of CD funding at leading US banks

• Success will require near-term excellence in at least four disciplines – forecasting (what will happen to your balances), pricing (vs. competition), planning (for your overall funding needs) and investing (in appropriate duration assets)

Copyright © 2013 Oliver Wyman 10

AN ADVANCED SOLUTION (SIMPLY)

Oliver Wyman and Nomis understands these

inplications, and realizes both the opportunities and the

challenges of the environment to come. As a result, we

have joined together to begin to deliver a suite of deposit

value management services that will efficiently and

flexibly position our clients to succeed. Our partnership

brings together Nomis’s capabilities in delivering

powerful software-based pricing solutions with

Oliver Wyman’s deep expertise across the deposit value

chain. The core of our offering is unique capabilities in

account and customer level data management. From

that starting point, we are able to deliver both tool-based

and custom solutions for each of four disciplines that

will be critical for success: deposit forecasting, pricing,

planning and investing.

CLOUD-BASED

• Account level data

• Customer levelflow of funds

“BIG DATA” COMPUTATIONAL POWER

PRICINGFORECASTING

INVESTING (FTP) PLANNING (LCR)

VS.

Stable Less Stable

$$$$$$

$$$ $

VS.

Copyright © 2013 Oliver Wyman 11

Our goal is to help bring both excellence and efficiency

to deposit value management at a critical time in the

evolution of the business. Stress testing and regulatory

guidance demand that all institutions must build a better

understanding of how their deposit balances are going to

behave as the economy changes. Similarly, all institutions

must understand the potential impact of new liquidity

regulations, and they must build the tools to be able to

assess that position on an ongoing basis.

By combining the work necessary to meet those

regulatory-driven demands with the implementation of

industry-leading deposit price optimization software, we

are able to help our clients use the same resources and

investment dollars to also set the foundation for better

investments of deposits in the near-term, better pricing

of deposits in the mid-term and better engagement

between treasury and deposit functions over the

long-term.

Our clients are able to choose which of our services meet

their needs, and to customize implementation for their

organizations. To learn more about how Oliver Wyman

and Nomis can help, or just to further discuss our views

on the evolving deposit landscape and the ways in which

each of these critical deposit disciplines can be efficiently

built together, please contact us.

Authors: Aaron Fine [email protected]

Frank Rohde [email protected]

Copyright © 2013 Oliver Wyman 12

FOOTNOTES AND SOURCES

1. Quarterly earnings releases (publicly disclosed)

2. Federal Reserve Interest Rates, Historical Data

3. Oliver Wyman Analysis

4. SNL Financial, Oliver Wyman analysis

5. Federal Reserve: Liquidity Coverage Ratio: Liquidity Risk Measurement, Standards, and Monitoring

6. SNL Financial, Oliver Wyman analysis

7. Federal Reserve Flow of Funds, Oliver Wyman Customer Insights Survey, Oliver Wyman Analysis

8. Publishers Weekly, Bowker Market Research

Note: LIBOR/Swap rate data

used throughout the report

is sourced from Thomson

Reuters Datastream and the

Federal Reserve

Copyright © 2013 Oliver Wyman 13

www.oliverwyman.com

Oliver Wyman is a global leader in management consulting that combines deep industry knowledge with specialized expertise in strategy, operations, risk management, and organization transformation.

For more information please contact the marketing department by email at [email protected] or by phone at one of the following locations:

AMERICAS

+1 212 541 8100

EMEA

+44 20 7333 8333

ASIA PACIFIC

+65 6510 9700

Copyright © 2013 Oliver Wyman

All rights reserved. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Oliver Wyman and Oliver Wyman accepts no liability whatsoever for the actions of third parties in this respect.

The information and opinions in this report were prepared by Oliver Wyman. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisors. Oliver Wyman has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Oliver Wyman disclaims any responsibility to update the information or conclusions in this report. Oliver Wyman accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages. The report is not an offer to buy or sell securities or a solicitation of an offer to buy or sell securities. This report may not be sold without the written consent of Oliver Wyman.