Embed Size (px)

Citation preview

DEPRECIATION UNDER SCHEDULE II TO THE

COMPANIES ACT, 2013

CA Mohit Bhuteria

As per Accounting Standard, AS 6 -

Depreciation is measure of the wearing out, consumption or other loss of value of a depreciable asset

arising from use, efflux of time or obsolescence through technology and market changes.

Depreciation is allocated so as to charge a fair proportion of the depreciable amount in each accounting

period during the expected useful life of the asset.

Depreciation includes amortisation of assets whose useful life is predetermined.

As per Corporate Law -

The term “depreciation” was not defined in the Companies Act 1956.

For the first time, “Depreciation” and “Depreciable amount” has been defined in the Companies Act 2013

Para 1 of Part A to Schedule II of the Companies Act, 2013 defines:

“Depreciation” as a systematic allocation of the depreciable amount of an asset over its useful life;

“Depreciable amount” of an asset is the cost of an asset or other amount substituted for cost, less

its residual value.

As per Sec 123 of the Companies Act 2013, depreciation shall be calculated as per Schedule II and these

provisions have been bought into force from 1 April 2014

DEFINITION

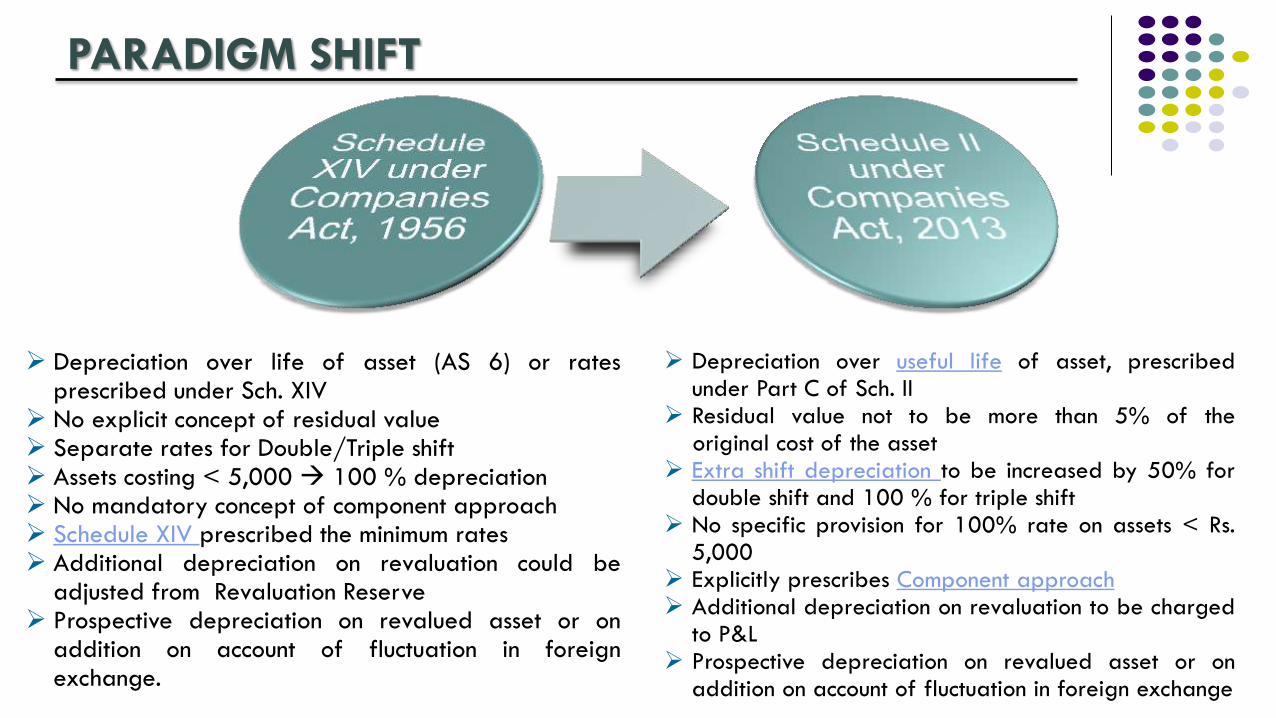

Depreciation over useful life of asset, prescribed under Part C of Sch. II

Residual value not to be more than 5% of the original cost of the asset

Extra shift depreciation to be increased by 50% for double shift and 100 % for triple shift

No specific provision for 100% rate on assets < Rs. 5,000

Explicitly prescribes Component approach Additional depreciation on revaluation to be charged

to P&L Prospective depreciation on revalued asset or on

addition on account of fluctuation in foreign exchange

PARADIGM SHIFT

Depreciation over life of asset (AS 6) or rates prescribed under Sch. XIV

No explicit concept of residual value Separate rates for Double/Triple shift Assets costing < 5,000 100 % depreciation No mandatory concept of component approach Schedule XIV prescribed the minimum rates Additional depreciation on revaluation could be

adjusted from Revaluation Reserve Prospective depreciation on revalued asset or on

addition on account of fluctuation in foreign exchange.

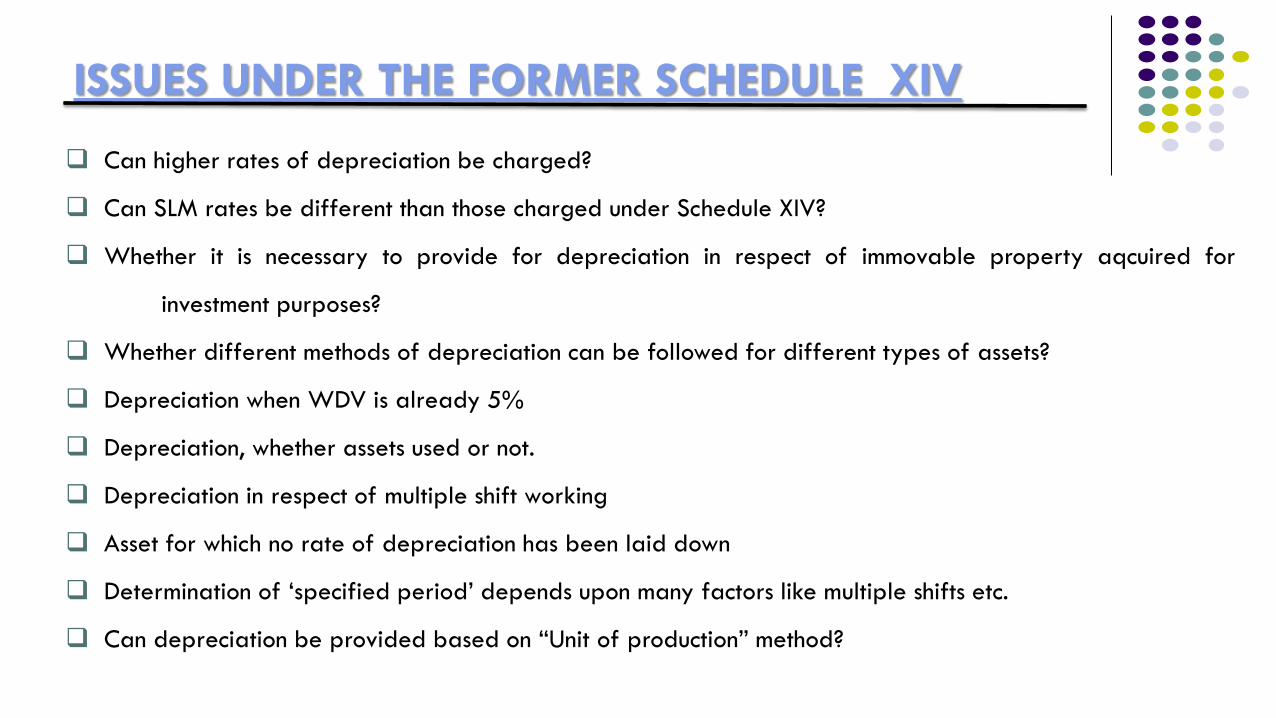

Can higher rates of depreciation be charged?

Can SLM rates be different than those charged under Schedule XIV?

Whether it is necessary to provide for depreciation in respect of immovable property aqcuired for

investment purposes?

Whether different methods of depreciation can be followed for different types of assets?

Depreciation when WDV is already 5%

Depreciation, whether assets used or not.

Depreciation in respect of multiple shift working

Asset for which no rate of depreciation has been laid down

Determination of ‘specified period’ depends upon many factors like multiple shifts etc.

Can depreciation be provided based on “Unit of production” method?

ISSUES UNDER THE FORMER SCHEDULE XIV

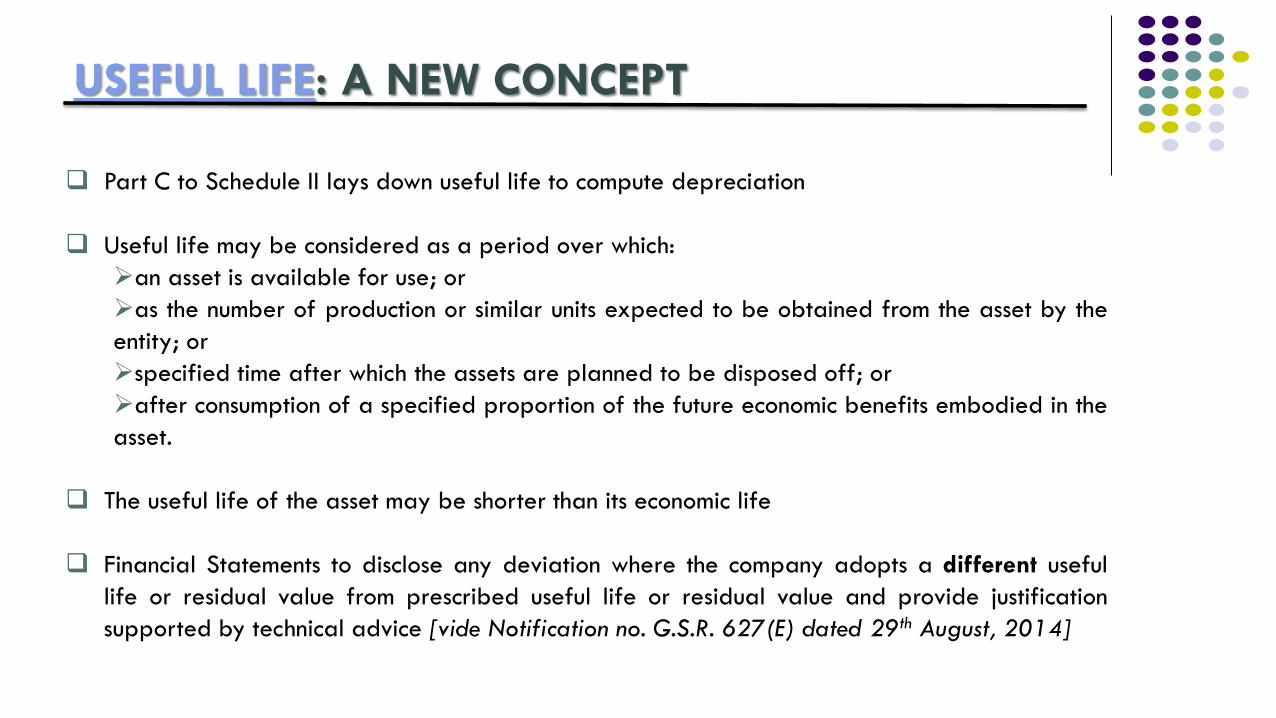

Part C to Schedule II lays down useful life to compute depreciation

Useful life may be considered as a period over which:

an asset is available for use; or

as the number of production or similar units expected to be obtained from the asset by the

entity; or

specified time after which the assets are planned to be disposed off; or

after consumption of a specified proportion of the future economic benefits embodied in the

asset.

The useful life of the asset may be shorter than its economic life

Financial Statements to disclose any deviation where the company adopts a different useful

life or residual value from prescribed useful life or residual value and provide justification

supported by technical advice [vide Notification no. G.S.R. 627(E) dated 29th August, 2014]

USEFUL LIFE: A NEW CONCEPT

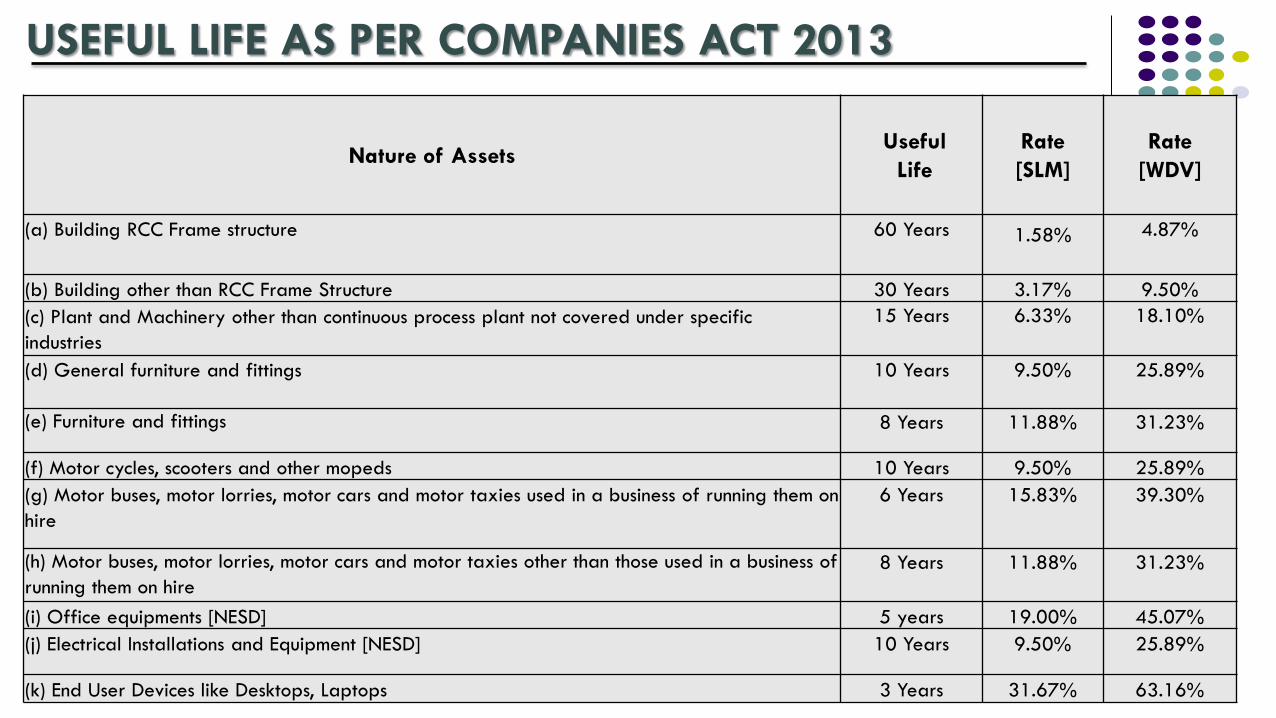

USEFUL LIFE AS PER COMPANIES ACT 2013

Nature of Assets

Useful

Life

Rate

[SLM]

Rate

[WDV]

(a) Building RCC Frame structure

60 Years 1.58%

4.87%

(b) Building other than RCC Frame Structure 30 Years 3.17% 9.50%

(c) Plant and Machinery other than continuous process plant not covered under specific

industries

15 Years 6.33% 18.10%

(d) General furniture and fittings

10 Years 9.50% 25.89%

(e) Furniture and fittings 8 Years 11.88% 31.23%

(f) Motor cycles, scooters and other mopeds 10 Years 9.50% 25.89%

(g) Motor buses, motor lorries, motor cars and motor taxies used in a business of running them on

hire

6 Years 15.83% 39.30%

(h) Motor buses, motor lorries, motor cars and motor taxies other than those used in a business of

running them on hire

8 Years 11.88% 31.23%

(i) Office equipments [NESD] 5 years 19.00% 45.07%

(j) Electrical Installations and Equipment [NESD] 10 Years 9.50% 25.89%

(k) End User Devices like Desktops, Laptops 3 Years 31.67% 63.16%

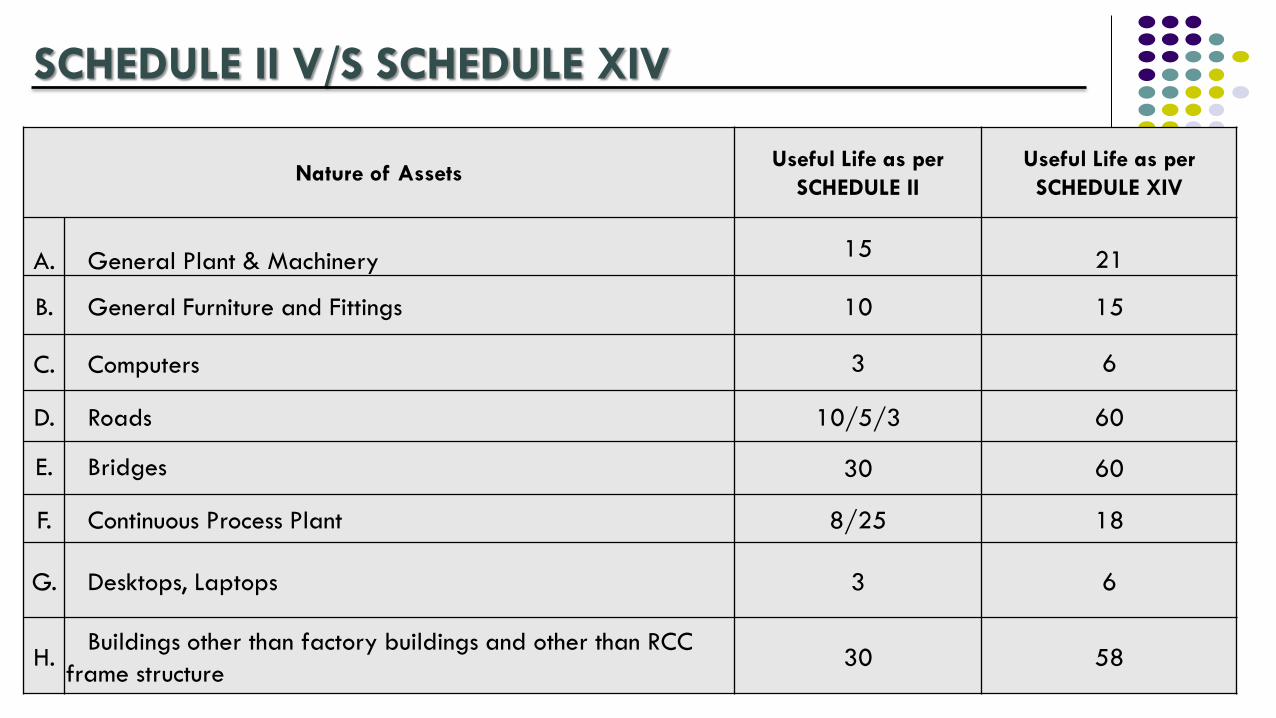

SCHEDULE II V/S SCHEDULE XIV

Nature of Assets Useful Life as per

SCHEDULE II

Useful Life as per

SCHEDULE XIV

A. General Plant & Machinery 15 21

B. General Furniture and Fittings 10 15

C. Computers 3 6

D. Roads 10/5/3 60

E. Bridges 30 60

F. Continuous Process Plant 8/25 18

G. Desktops, Laptops 3 6

H. Buildings other than factory buildings and other than RCC

frame structure 30 58

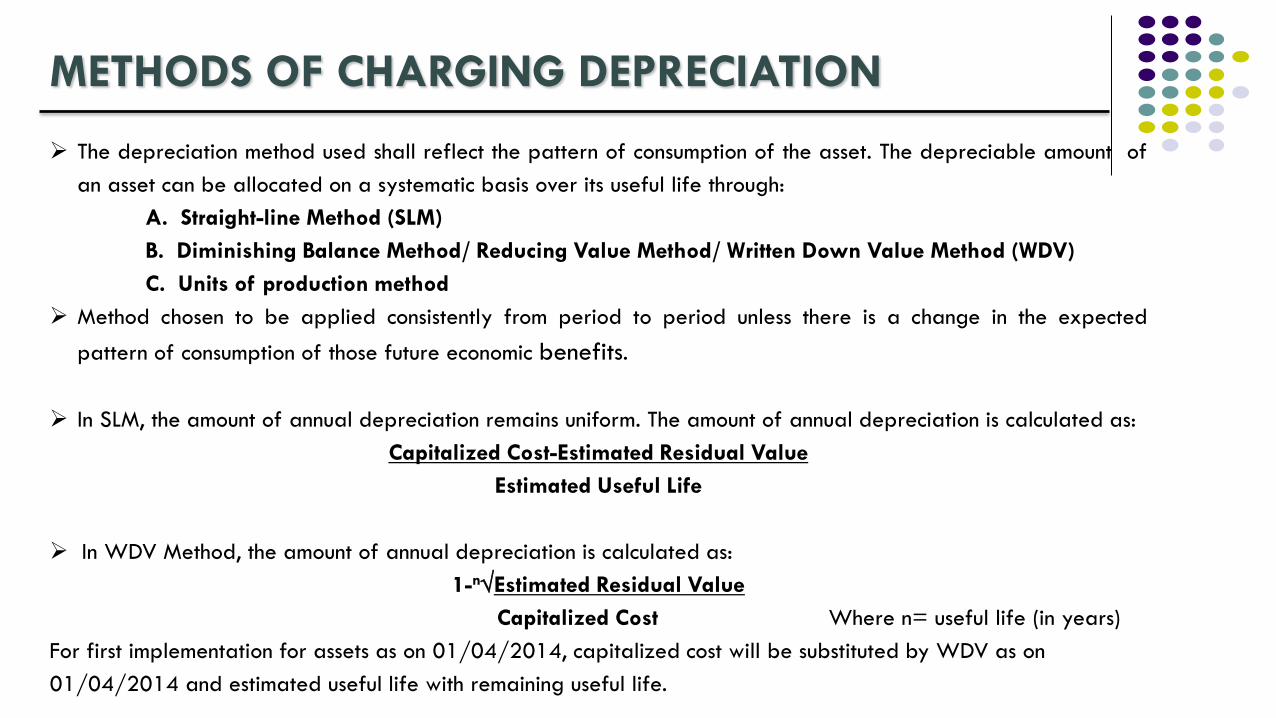

METHODS OF CHARGING DEPRECIATION

The depreciation method used shall reflect the pattern of consumption of the asset. The depreciable amount of

an asset can be allocated on a systematic basis over its useful life through:

A. Straight-line Method (SLM)

B. Diminishing Balance Method/ Reducing Value Method/ Written Down Value Method (WDV)

C. Units of production method

Method chosen to be applied consistently from period to period unless there is a change in the expected

pattern of consumption of those future economic benefits.

In SLM, the amount of annual depreciation remains uniform. The amount of annual depreciation is calculated as:

Capitalized Cost-Estimated Residual Value

Estimated Useful Life

In WDV Method, the amount of annual depreciation is calculated as:

1-nEstimated Residual Value

Capitalized Cost Where n= useful life (in years)

For first implementation for assets as on 01/04/2014, capitalized cost will be substituted by WDV as on

01/04/2014 and estimated useful life with remaining useful life.

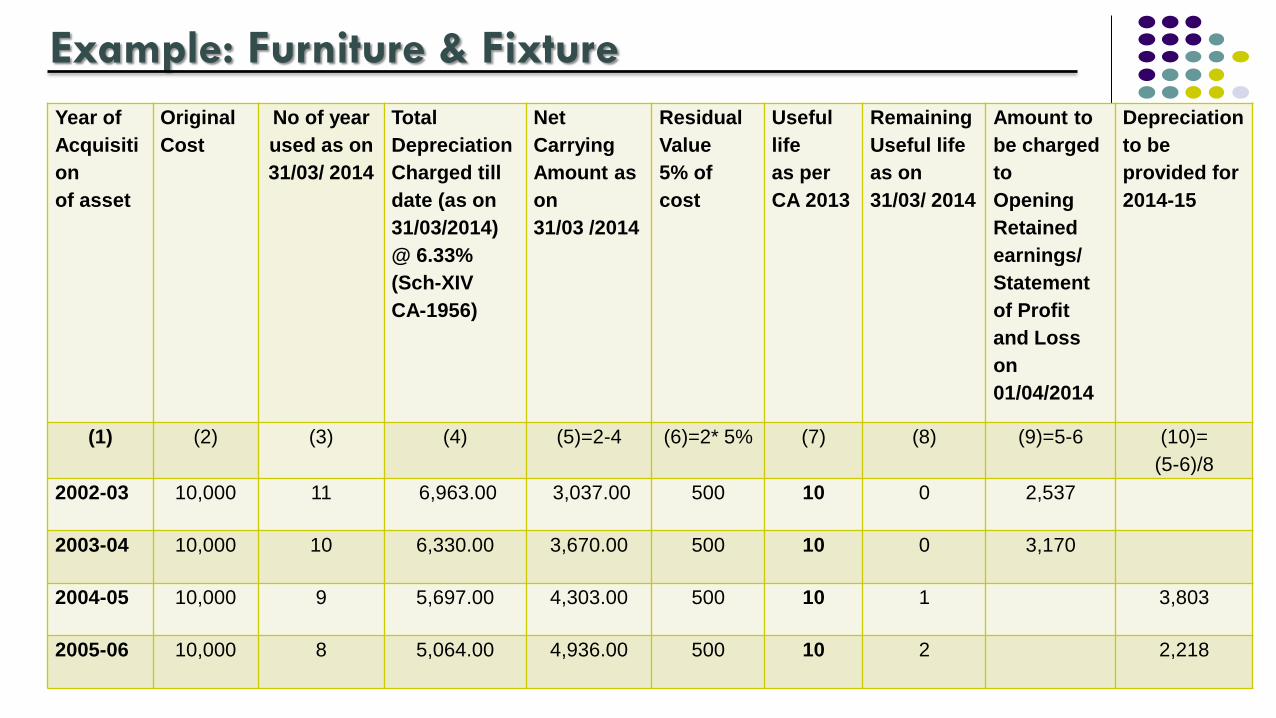

Year of

Acquisiti

on

of asset

Original

Cost

No of year

used as on

31/03/ 2014

Total

Depreciation

Charged till

date (as on

31/03/2014)

@ 6.33%

(Sch-XIV

CA-1956)

Net

Carrying

Amount as

on

31/03 /2014

Residual

Value

5% of

cost

Useful

life

as per

CA 2013

Remaining

Useful life

as on

31/03/ 2014

Amount to

be charged

to

Opening

Retained

earnings/

Statement

of Profit

and Loss

on

01/04/2014

Depreciation

to be

provided for

2014-15

(1) (2) (3) (4) (5)=2-4 (6)=2* 5% (7) (8) (9)=5-6 (10)=

(5-6)/8

2002-03 10,000 11 6,963.00 3,037.00 500 10 0 2,537

2003-04 10,000 10 6,330.00 3,670.00 500 10 0 3,170

2004-05 10,000 9 5,697.00 4,303.00 500 10 1 3,803

2005-06 10,000 8 5,064.00 4,936.00 500 10 2 2,218

Example: Furniture & Fixture

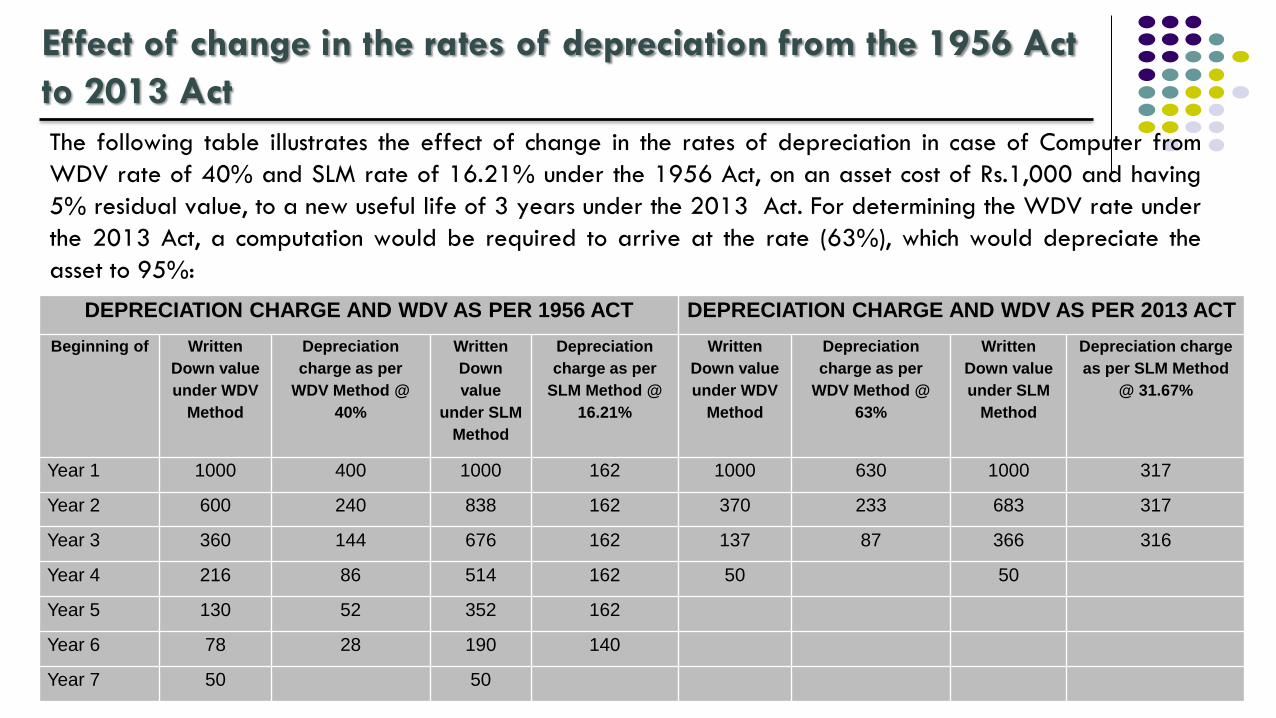

Effect of change in the rates of depreciation from the 1956 Act

to 2013 Act

The following table illustrates the effect of change in the rates of depreciation in case of Computer from

WDV rate of 40% and SLM rate of 16.21% under the 1956 Act, on an asset cost of Rs.1,000 and having

5% residual value, to a new useful life of 3 years under the 2013 Act. For determining the WDV rate under

the 2013 Act, a computation would be required to arrive at the rate (63%), which would depreciate the

asset to 95%:

DEPRECIATION CHARGE AND WDV AS PER 1956 ACT DEPRECIATION CHARGE AND WDV AS PER 2013 ACT

Beginning of Written

Down value

under WDV

Method

Depreciation

charge as per

WDV Method @

40%

Written

Down

value

under SLM

Method

Depreciation

charge as per

SLM Method @

16.21%

Written

Down value

under WDV

Method

Depreciation

charge as per

WDV Method @

63%

Written

Down value

under SLM

Method

Depreciation charge

as per SLM Method

@ 31.67%

Year 1 1000 400 1000 162 1000 630 1000 317

Year 2 600 240 838 162 370 233 683 317

Year 3 360 144 676 162 137 87 366 316

Year 4 216 86 514 162 50 50

Year 5 130 52 352 162

Year 6 78 28 190 140

Year 7 50 50

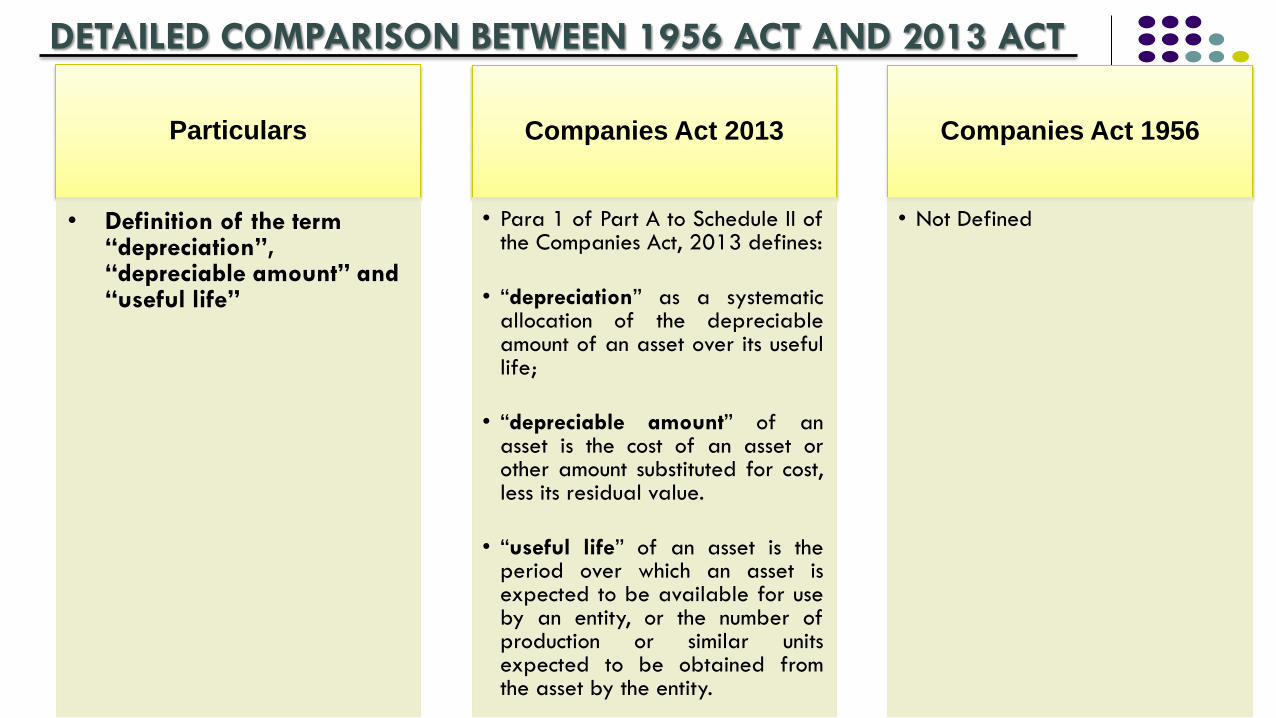

Particulars

• Definition of the term “depreciation”, “depreciable amount” and “useful life”

Companies Act 2013

• Para 1 of Part A to Schedule II of the Companies Act, 2013 defines:

• “depreciation” as a systematic allocation of the depreciable amount of an asset over its useful life;

• “depreciable amount” of an asset is the cost of an asset or other amount substituted for cost, less its residual value.

• “useful life” of an asset is the period over which an asset is expected to be available for use by an entity, or the number of production or similar units expected to be obtained from the asset by the entity.

Companies Act 1956

• Not Defined

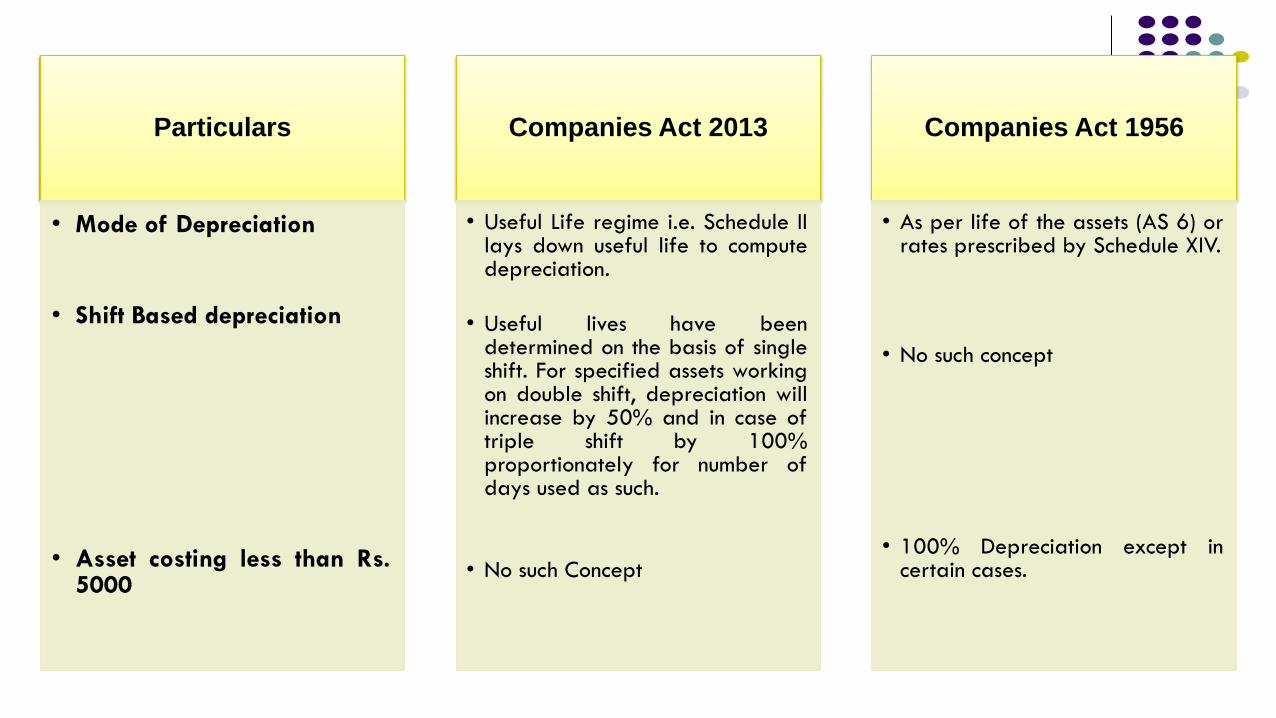

DETAILED COMPARISON BETWEEN 1956 ACT AND 2013 ACT

Particulars

• Mode of Depreciation

• Shift Based depreciation

• Asset costing less than Rs. 5000

Companies Act 2013

• Useful Life regime i.e. Schedule II lays down useful life to compute depreciation.

• Useful lives have been determined on the basis of single shift. For specified assets working on double shift, depreciation will increase by 50% and in case of triple shift by 100% proportionately for number of days used as such.

• No such Concept

Companies Act 1956

• As per life of the assets (AS 6) or rates prescribed by Schedule XIV.

• No such concept

• 100% Depreciation except in certain cases.

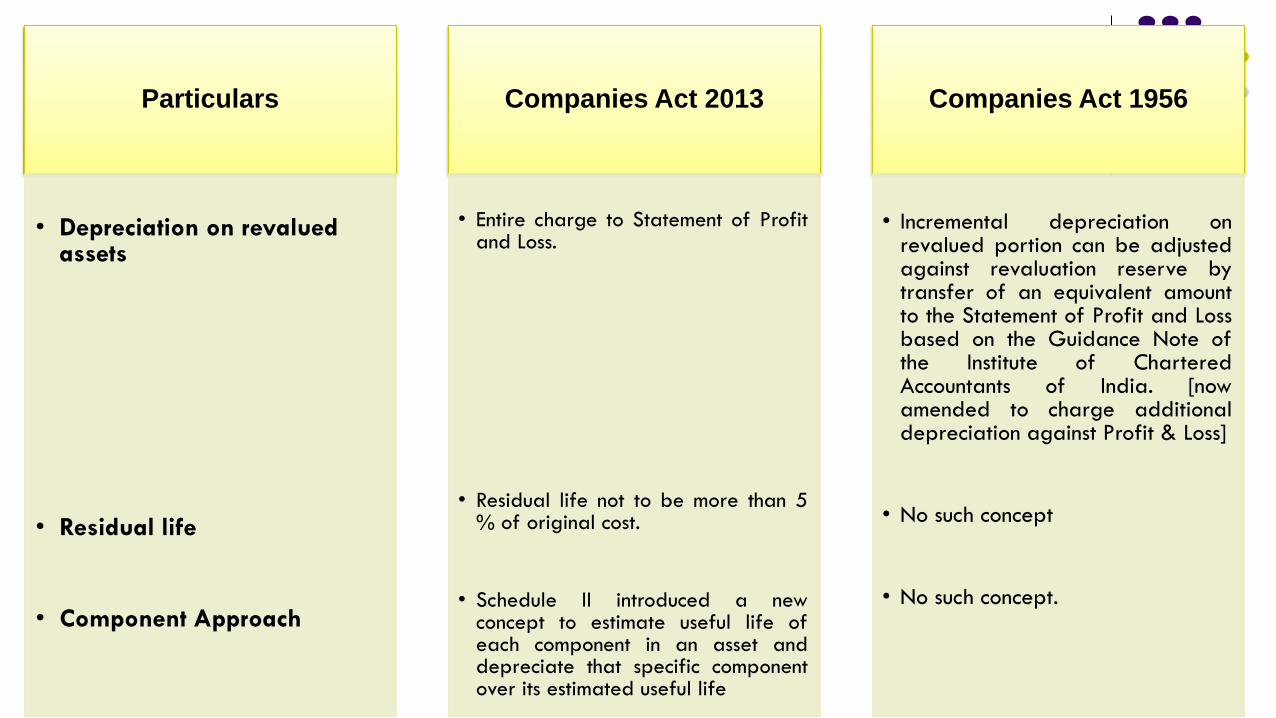

Particulars

• Depreciation on revalued assets

• Residual life

• Component Approach

Companies Act 2013

• Entire charge to Statement of Profit and Loss.

• Residual life not to be more than 5 % of original cost.

• Schedule II introduced a new concept to estimate useful life of each component in an asset and depreciate that specific component over its estimated useful life

Companies Act 1956

• Incremental depreciation on

revalued portion can be adjusted against revaluation reserve by transfer of an equivalent amount to the Statement of Profit and Loss based on the Guidance Note of the Institute of Chartered Accountants of India. [now amended to charge additional depreciation against Profit & Loss]

• No such concept

• No such concept.

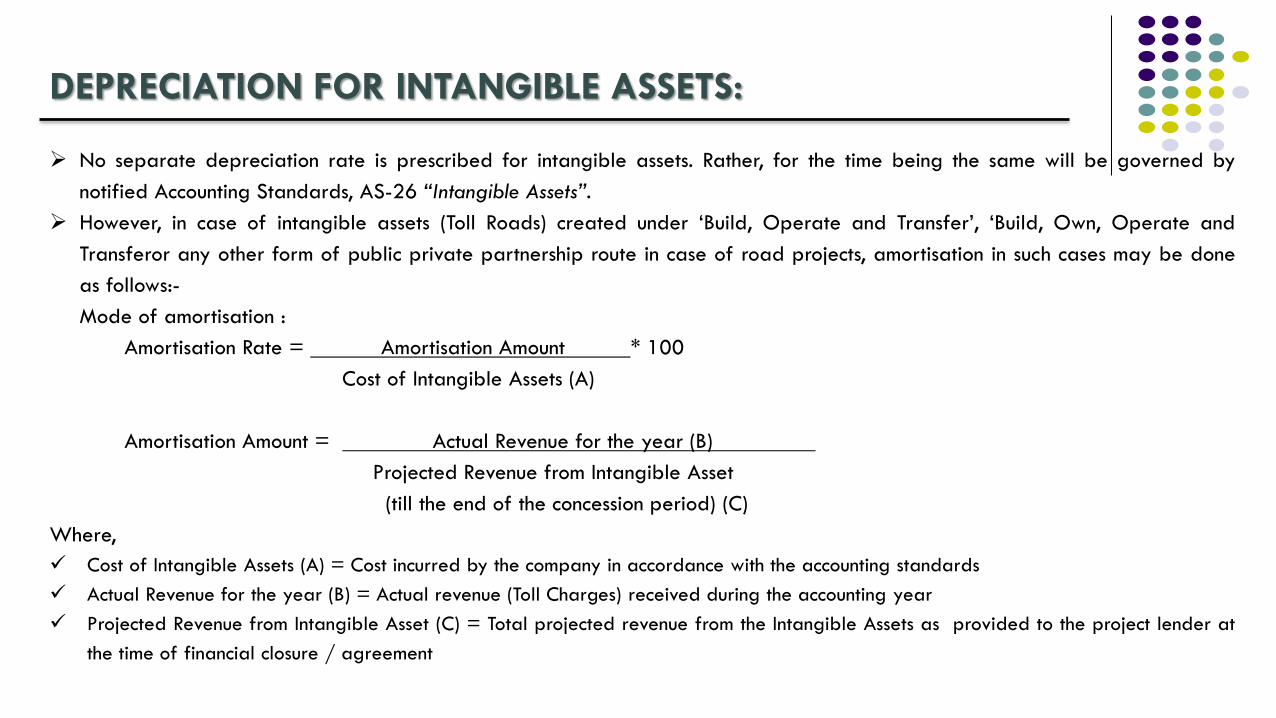

DEPRECIATION FOR INTANGIBLE ASSETS:

No separate depreciation rate is prescribed for intangible assets. Rather, for the time being the same will be governed by

notified Accounting Standards, AS-26 “Intangible Assets”.

However, in case of intangible assets (Toll Roads) created under ‘Build, Operate and Transfer’, ‘Build, Own, Operate and

Transferor any other form of public private partnership route in case of road projects, amortisation in such cases may be done

as follows:-

Mode of amortisation :

Amortisation Rate = Amortisation Amount * 100

Cost of Intangible Assets (A)

Amortisation Amount = Actual Revenue for the year (B)

Projected Revenue from Intangible Asset

(till the end of the concession period) (C)

Where,

Cost of Intangible Assets (A) = Cost incurred by the company in accordance with the accounting standards

Actual Revenue for the year (B) = Actual revenue (Toll Charges) received during the accounting year

Projected Revenue from Intangible Asset (C) = Total projected revenue from the Intangible Assets as provided to the project lender at

the time of financial closure / agreement

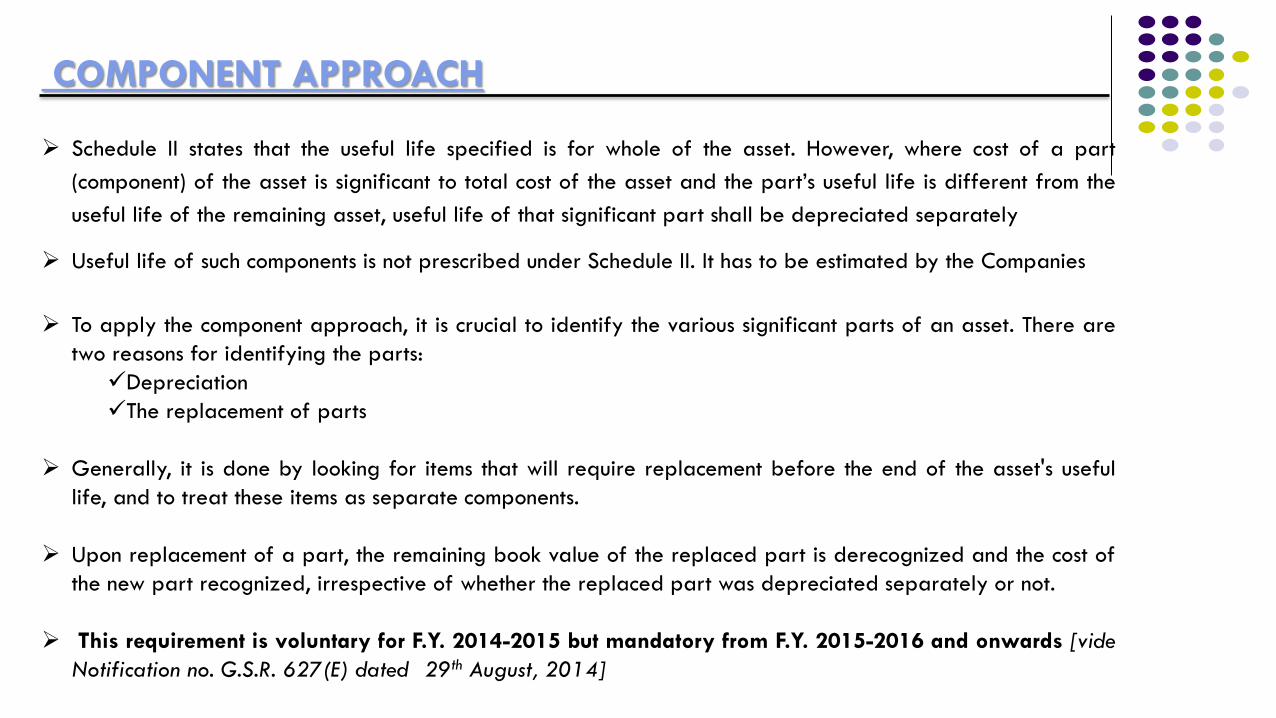

COMPONENT APPROACH

Schedule II states that the useful life specified is for whole of the asset. However, where cost of a part

(component) of the asset is significant to total cost of the asset and the part’s useful life is different from the

useful life of the remaining asset, useful life of that significant part shall be depreciated separately

Useful life of such components is not prescribed under Schedule II. It has to be estimated by the Companies

To apply the component approach, it is crucial to identify the various significant parts of an asset. There are

two reasons for identifying the parts:

Depreciation

The replacement of parts

Generally, it is done by looking for items that will require replacement before the end of the asset's useful

life, and to treat these items as separate components.

Upon replacement of a part, the remaining book value of the replaced part is derecognized and the cost of

the new part recognized, irrespective of whether the replaced part was depreciated separately or not.

This requirement is voluntary for F.Y. 2014-2015 but mandatory from F.Y. 2015-2016 and onwards [vide

Notification no. G.S.R. 627(E) dated 29th August, 2014]

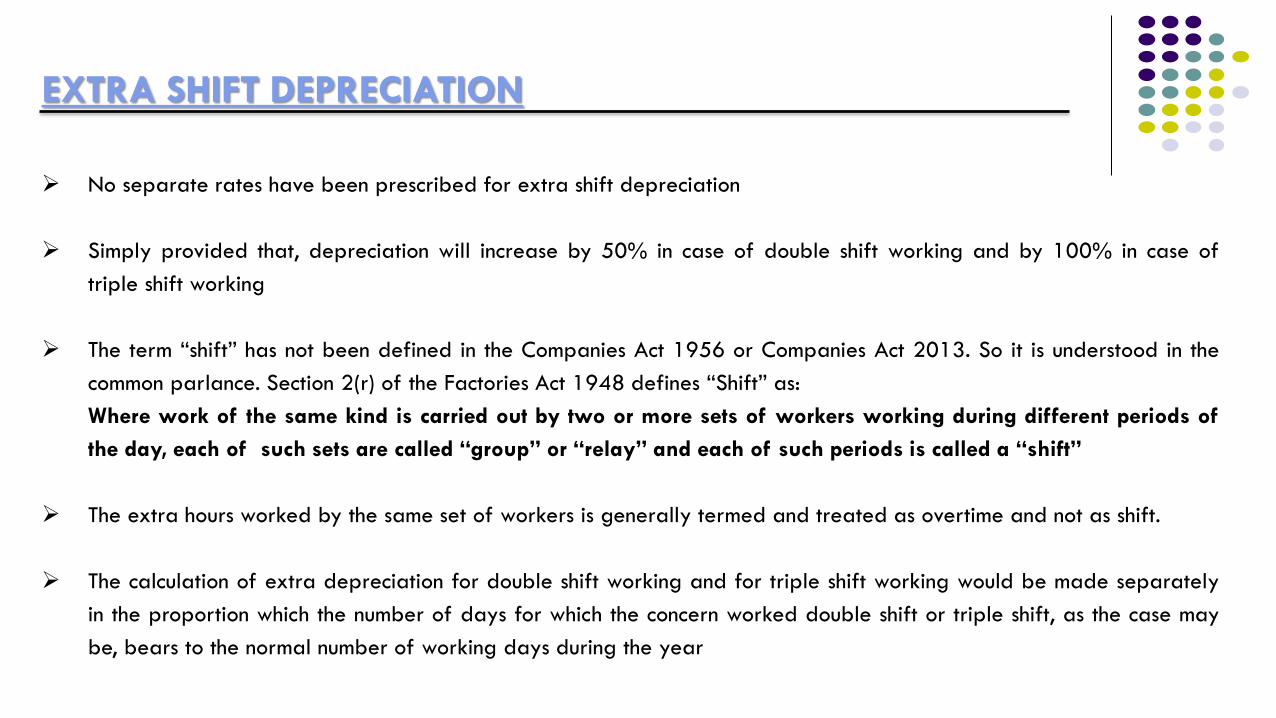

EXTRA SHIFT DEPRECIATION

No separate rates have been prescribed for extra shift depreciation

Simply provided that, depreciation will increase by 50% in case of double shift working and by 100% in case of

triple shift working

The term “shift” has not been defined in the Companies Act 1956 or Companies Act 2013. So it is understood in the

common parlance. Section 2(r) of the Factories Act 1948 defines “Shift” as:

Where work of the same kind is carried out by two or more sets of workers working during different periods of

the day, each of such sets are called “group” or “relay” and each of such periods is called a “shift”

The extra hours worked by the same set of workers is generally termed and treated as overtime and not as shift.

The calculation of extra depreciation for double shift working and for triple shift working would be made separately

in the proportion which the number of days for which the concern worked double shift or triple shift, as the case may

be, bears to the normal number of working days during the year

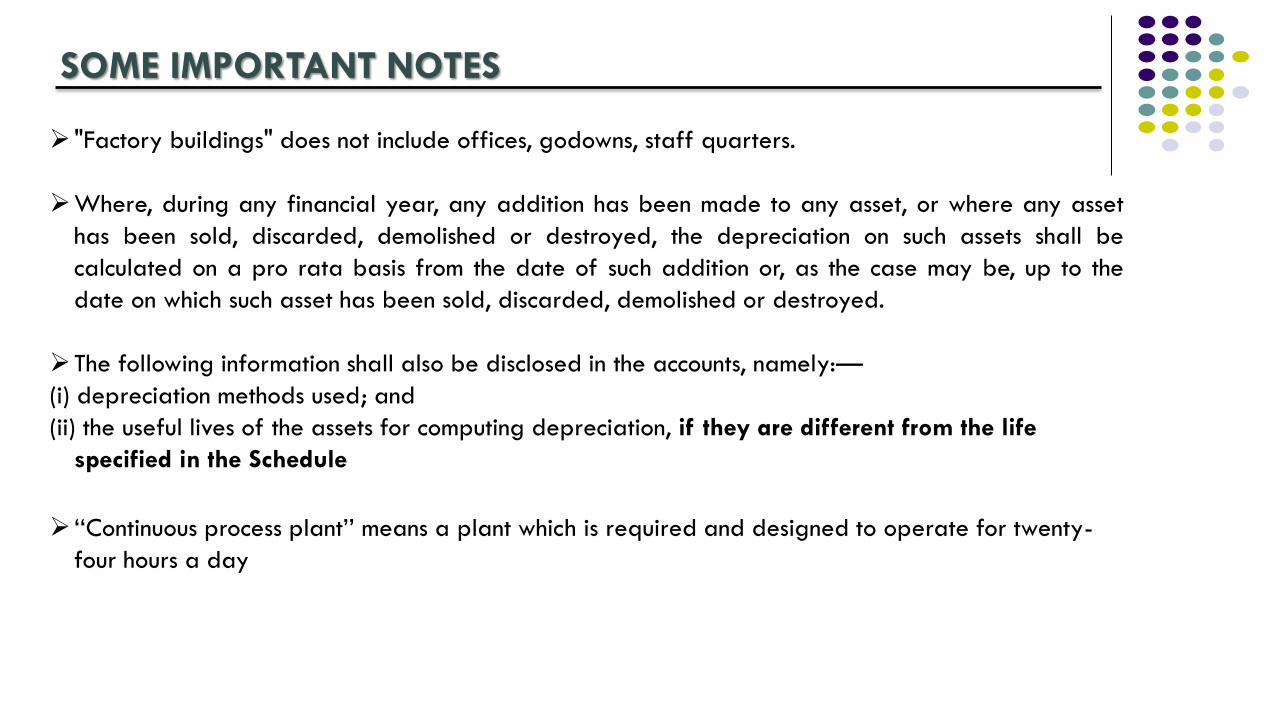

SOME IMPORTANT NOTES

"Factory buildings" does not include offices, godowns, staff quarters.

Where, during any financial year, any addition has been made to any asset, or where any asset

has been sold, discarded, demolished or destroyed, the depreciation on such assets shall be

calculated on a pro rata basis from the date of such addition or, as the case may be, up to the

date on which such asset has been sold, discarded, demolished or destroyed.

The following information shall also be disclosed in the accounts, namely:—

(i) depreciation methods used; and

(ii) the useful lives of the assets for computing depreciation, if they are different from the life

specified in the Schedule

‘‘Continuous process plant’’ means a plant which is required and designed to operate for twenty-

four hours a day

The Depreciation on fixed asset as per Schedule-II of Companies Act, 2013 became operational from

01/04/2014 vide MCA notification no S.O.902(E) dated 26/03/2014.

Transitional Provision

From the date this Schedule comes into effect, the carrying amount of the asset as on that date—

(a) shall be depreciated over the remaining useful life of the asset as per this Schedule;

(b) after retaining the residual value, may be recognized in the opening balance of retained earnings

where the remaining useful life of an asset is NIL

Where useful remaining life exists, however the residual WDV at the time of the first application of the

Schedule, falls below the residual value calculated @ 5% of the original cost of the asset, depreciation

charged during the year should be NIL. The remaining WDV shall be removed from the books when the

assets is sold, demolished or discarded.

THE TRANSITION

ISSUES

The useful life of an asset can be the number of production or similar units expected to be obtained from the asset.

This indicates that a company may be able to use Units of Production (UOP) method for depreciation,

which was previously prohibited for assets covered under Schedule XIV.

Significant components needs to be identified. The application of component accounting is likely to cause

significant change in accounting for replacement costs. Previously, companies needed to expense such costs in the year

of incurrence. Under the component accounting, companies will capitalize these costs, with consequent expensing of net

carrying value of the replaced part.

As per the amendment in ICAI guidance note on treatment of Revaluation Reserve, additional depreciation on

revaluation now cannot be charged against Revaluation Reserve but only charged against Statement

of Profit & Loss. This is expected to have significant impact on the statement of profit and loss. This is a major

change unnoticed at large. Dividend distribution and managerial remuneration may be significantly affected.

In case of assets with a nil remaining useful life on the date the Schedule II comes into effect, the transitional provisions

require that the carrying amount may be charged to retained earnings. The word 'shall' has been replaced by the

word 'may' by a beneficial notification which provides scope for charging the carrying amount in such case to

revenue as well. This will be a welcome relief to companies subject to Minimum Alternate Tax.

ISSUES (contd…)

Overall, many companies may need to charge higher depreciation in the P&L because of pruning

of useful lives as compared to the earlier specified rates. However, in some cases, the impact will be

lower depreciation, i.e. when the useful lives are much longer compared to the earlier specified rates.

The Companies will have to ascertain rates of depreciation for each individual item of fixed asset as on

01.04.2014 and the rate of depreciation may vary significantly depending on balance residual life as on the said

date. This will be a very cumbersome exercise and proper maintenance of fixed asset register will be a

pre requirement for the same.

Companies also need to assess the impact from implementation of Schedule II vis a vis depreciation as presently

charged and disclose the financial impact of the same in Financial Statements. Thus, for the first year

depreciation, both as per Companies Act, 2013 and Companies Act, 1956, needs to be calculated.

Companies may charge depreciation as per the Income Tax Act, however the same shall be

disclosed in Financial Statements and supported by technical advice.

THANK YOU