Embed Size (px)

Citation preview

Derek BurletonVice President and Deputy Chief Economist

June 2011

HOUSEHOLD DEBT IN CANADA: A REGIONAL

PERSPECTIVE

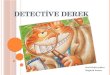

RISING PERSONAL INDEBTEDNESS IS A CONCERN

60

80

100

120

140

160

180

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Canada U.S.

Source: Statistics Canada, Federal reserve Board, Haver Analytics

Household debt to personal disposable income, %

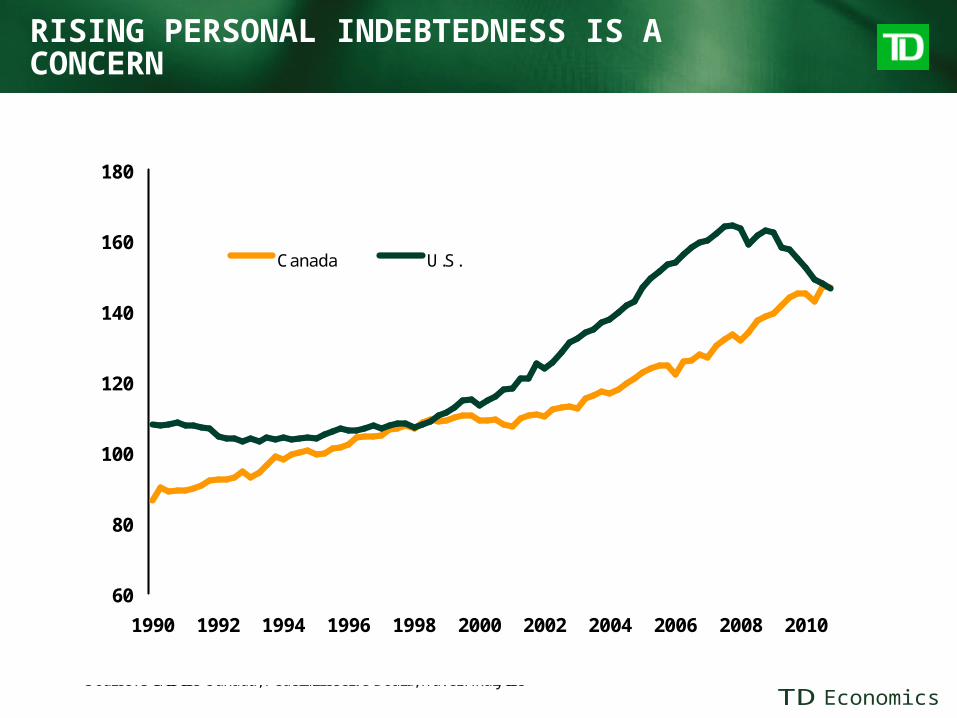

DEBT GROWTH HAS OUTPACED GROWTH IN ASSETS AND NET WORTH

10

12

14

16

18

20

22

24

26

1990 1993 1996 1999 2002 2005 2008

Debt-to-assets Debt-to-net worth

Source: Statistics Canada/Haver Analytics

Ratio

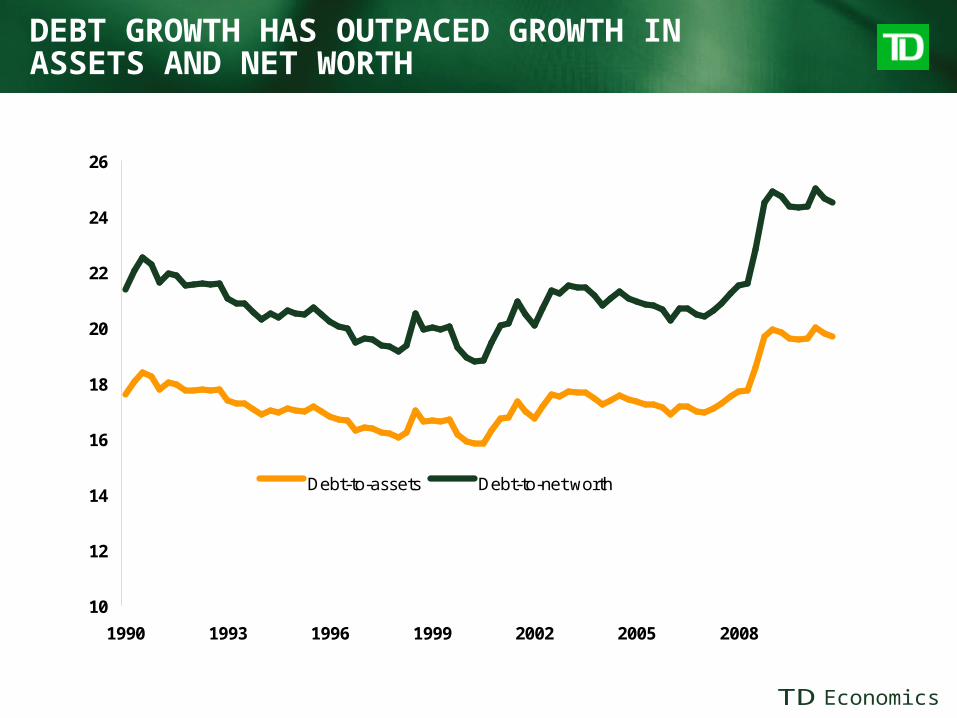

DEBT INTEREST PAYMENTS VULNERABLE TO FUTURE MONETARY POLICY TIGHTENING

-4.0

0.0

4.0

8.0

12.0

16.0

1990 1993 1996 1999 2002 2005 2008 2011 2014

6.0

7.0

8.0

9.0

10.0

11.0

12.0

3-month t-bill (lhs)Debt Service Ratio (rhs)

Yield, %%

forecast

Source: Statistics Canada, Bank of Canada, Haver Analytics, Forecast by TD Economics as of March 2011

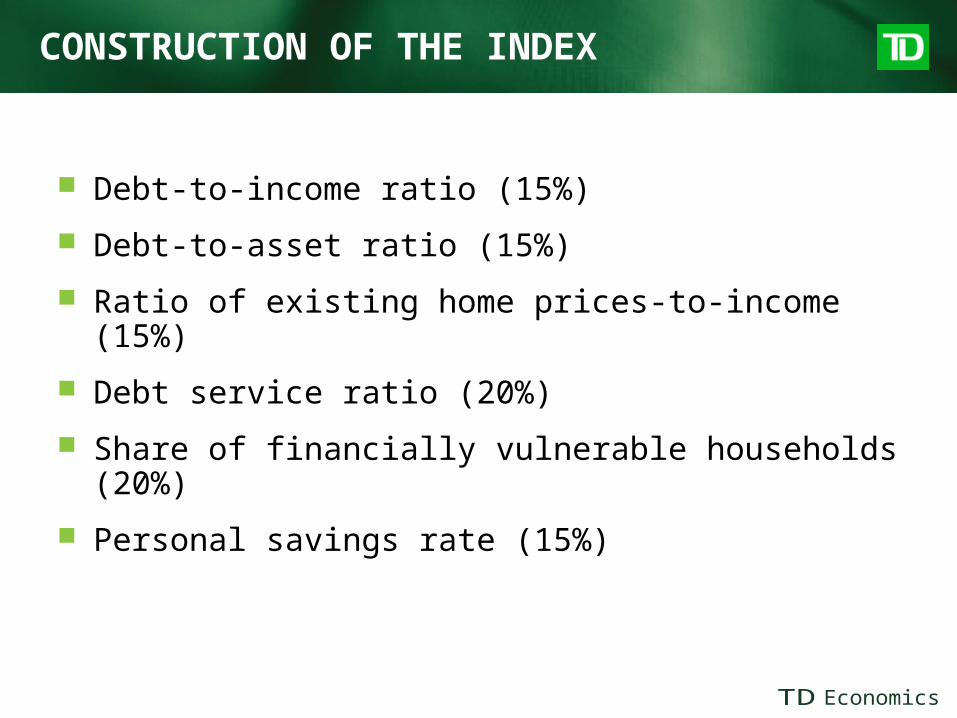

CONSTRUCTION OF THE INDEX

Debt-to-income ratio (15%)

Debt-to-asset ratio (15%)

Ratio of existing home prices-to-income (15%)

Debt service ratio (20%)

Share of financially vulnerable households (20%)

Personal savings rate (15%)

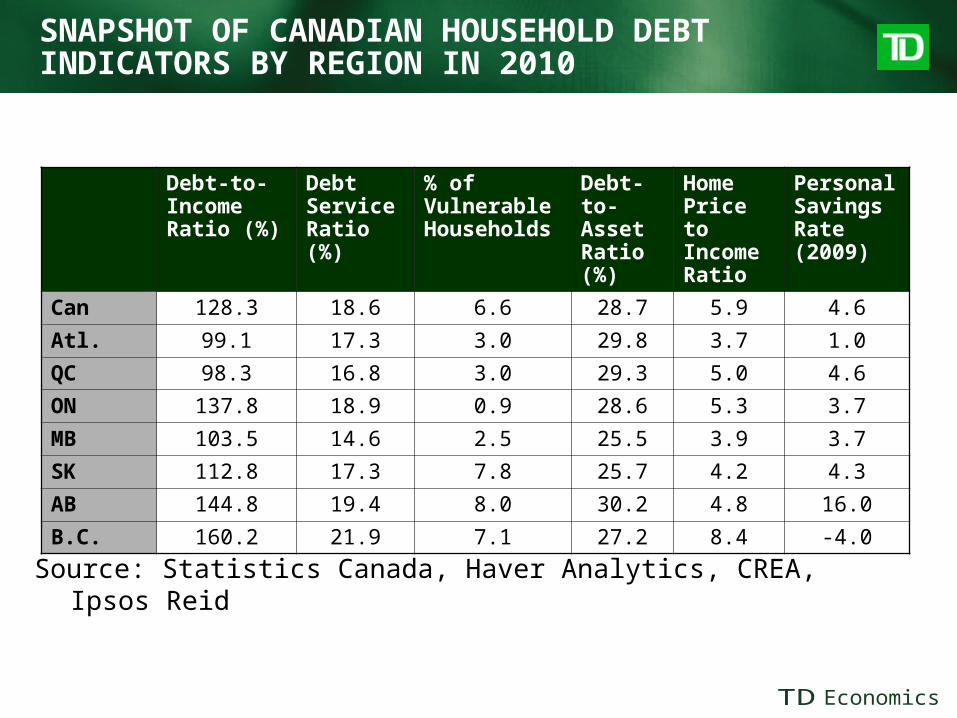

SNAPSHOT OF CANADIAN HOUSEHOLD DEBT INDICATORS BY REGION IN 2010

Debt-to-Income Ratio (%)

Debt Service Ratio (%)

% of Vulnerable Households

Debt-to-Asset Ratio (%)

Home Price to Income Ratio

Personal Savings Rate (2009)

Can 128.3 18.6 6.6 28.7 5.9 4.6

Atl. 99.1 17.3 3.0 29.8 3.7 1.0

QC 98.3 16.8 3.0 29.3 5.0 4.6

ON 137.8 18.9 0.9 28.6 5.3 3.7

MB 103.5 14.6 2.5 25.5 3.9 3.7

SK 112.8 17.3 7.8 25.7 4.2 4.3

AB 144.8 19.4 8.0 30.2 4.8 16.0

B.C. 160.2 21.9 7.1 27.2 8.4 -4.0

Source: Statistics Canada, Haver Analytics, CREA, Ipsos Reid

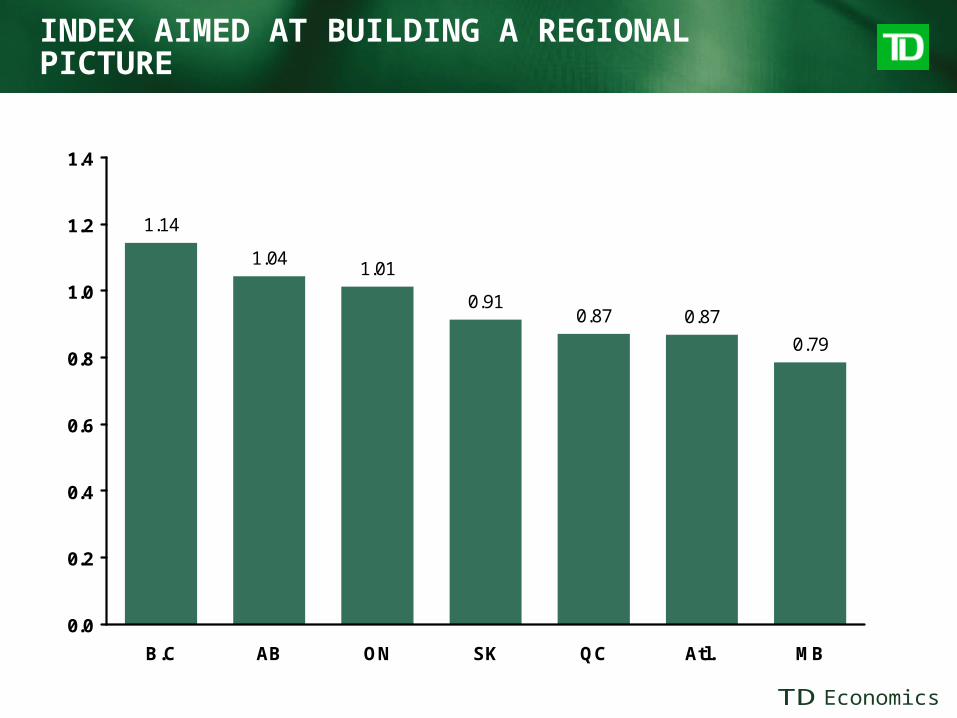

INDEX AIMED AT BUILDING A REGIONAL PICTURE

1.14

1.041.01

0.910.87 0.87

0.79

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

B.C AB ON SK QC Atl. MB

Source: Ipsos Reid, index generated by TD Economics

TD Economics Household Vulnerability Index 2010(Canada = 1.0)

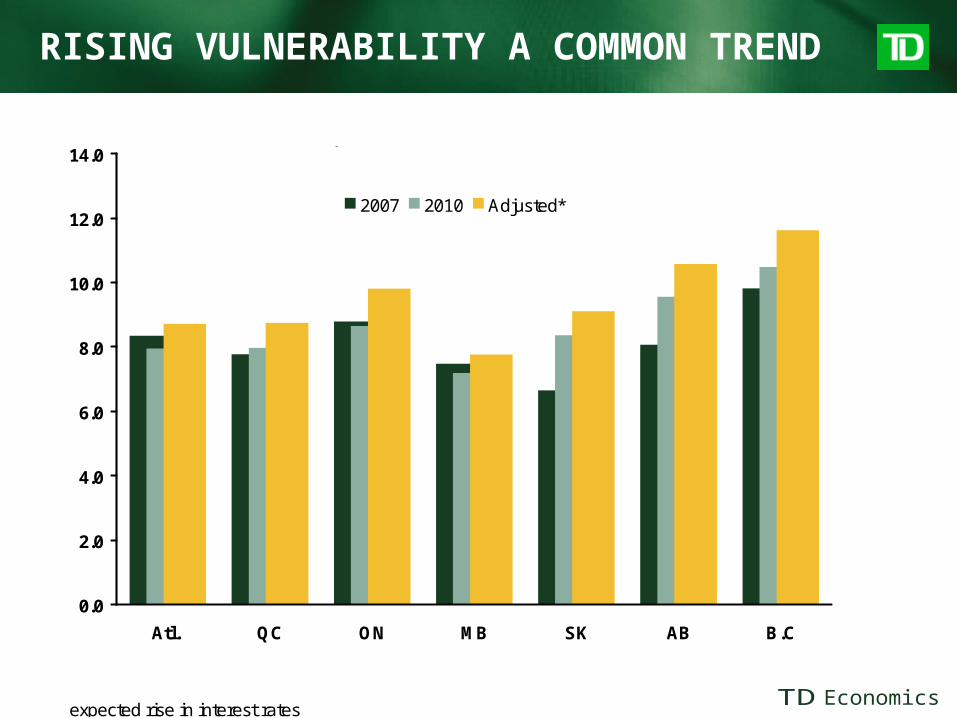

RISING VULNERABILITY A COMMON TREND

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Atl. QC ON MB SK AB B.C

2007 2010 Adjusted*

TD Economics' Vulnerability Index

Source: TD Economics, Ipsos Reid, Statistics Canada, * Adjusted for the expected rise in interest rates

SOME OTHER COMMON TRENDS

Rising household debt-to-income ratio and home price-to-income ratios have been the key drivers

Debt-service ratios have been falling and remain in a comfortable range

All regions will experience a substantial increase in vulnerability in coming years

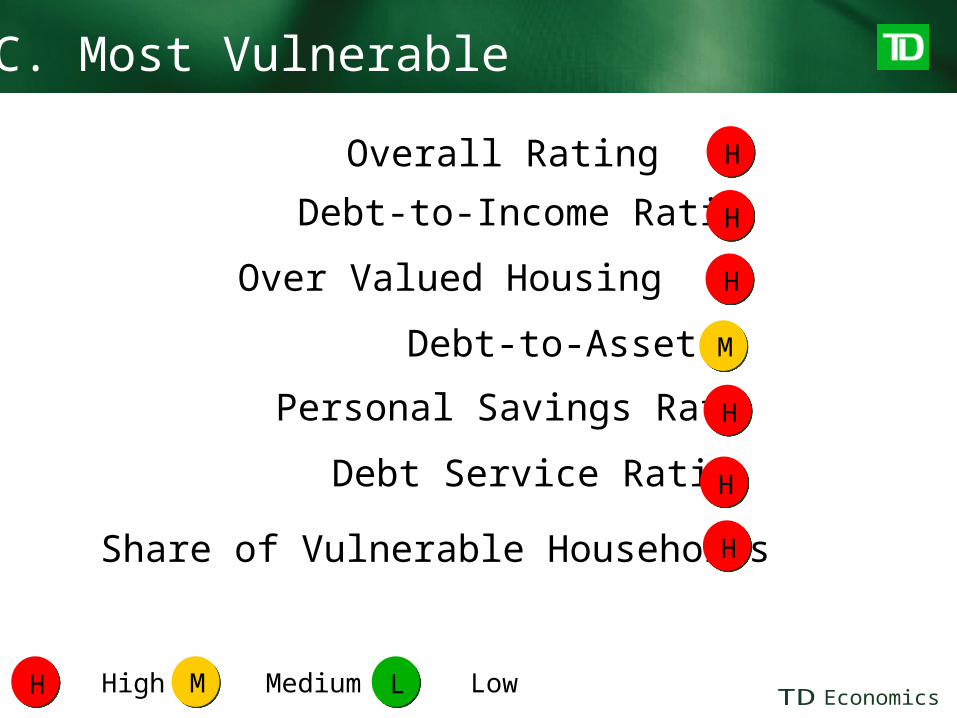

B.C. Most Vulnerable

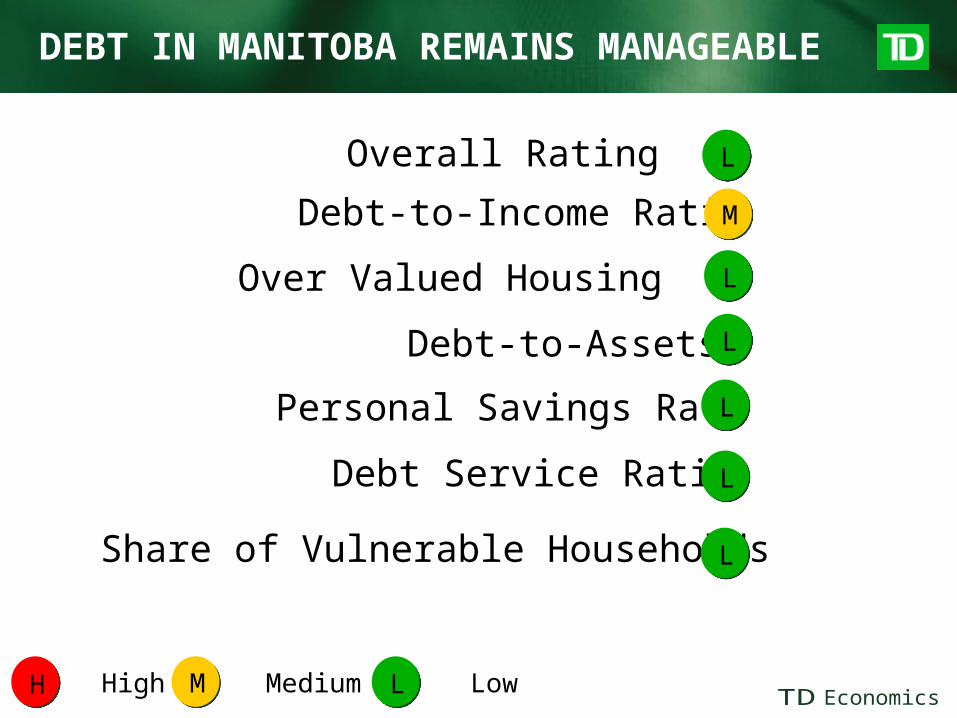

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

H

H

H

H

H

M

L LowM MediumH High

Share of Vulnerable Households H

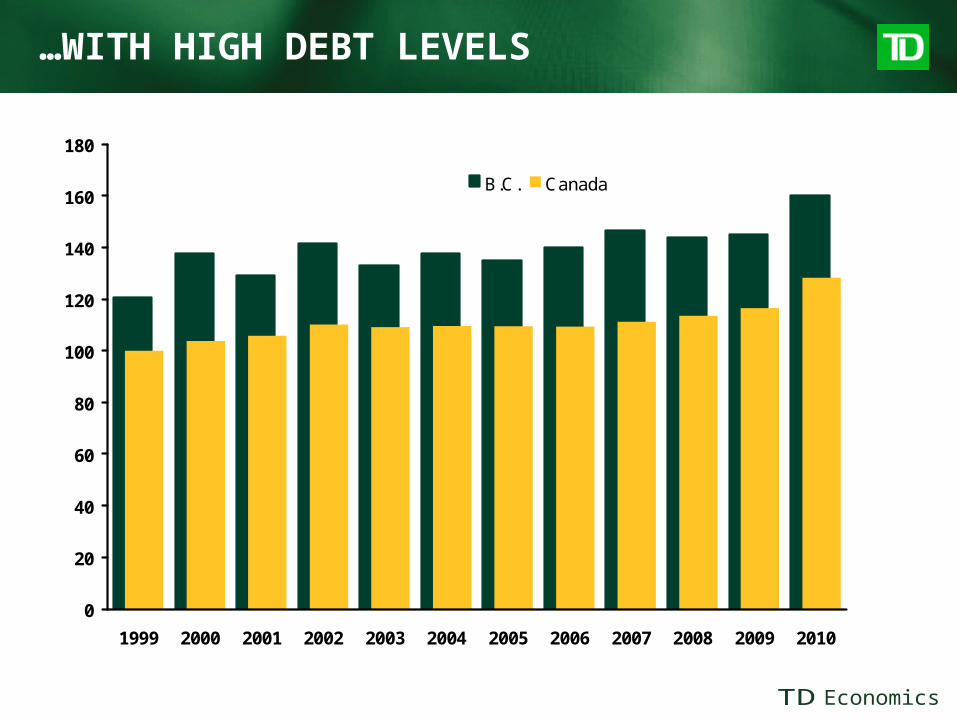

…WITH HIGH DEBT LEVELS

0

20

40

60

80

100

120

140

160

180

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

B.C. Canada

Household debt-to-income ratio

Source: Ipsos Reid

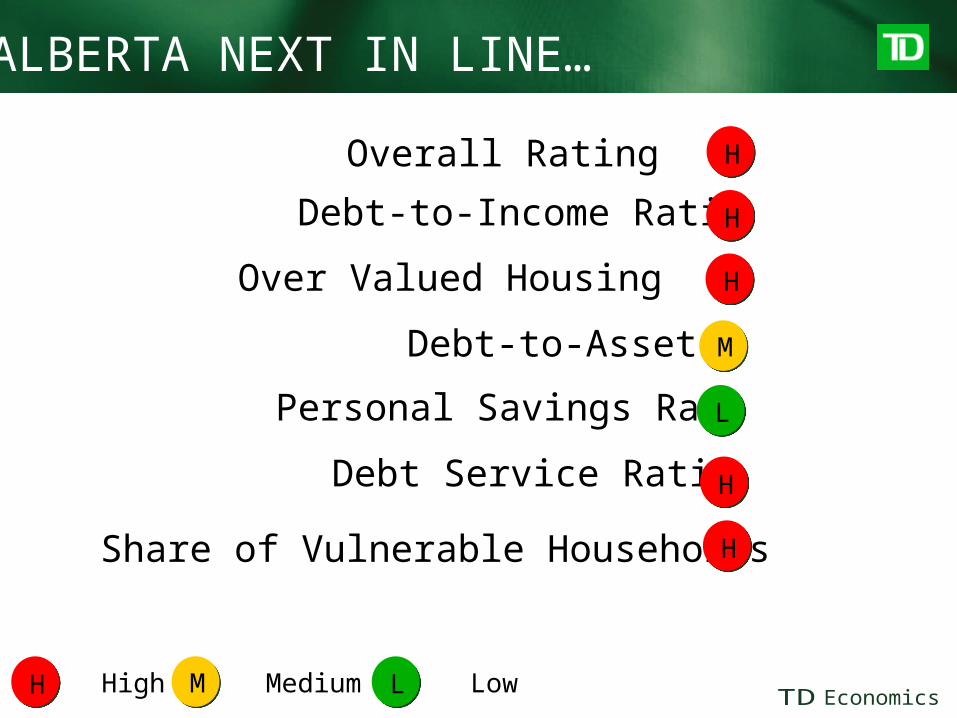

ALBERTA NEXT IN LINE…

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

H

H

H

H

M

L LowM MediumH High

Share of Vulnerable Households H

L

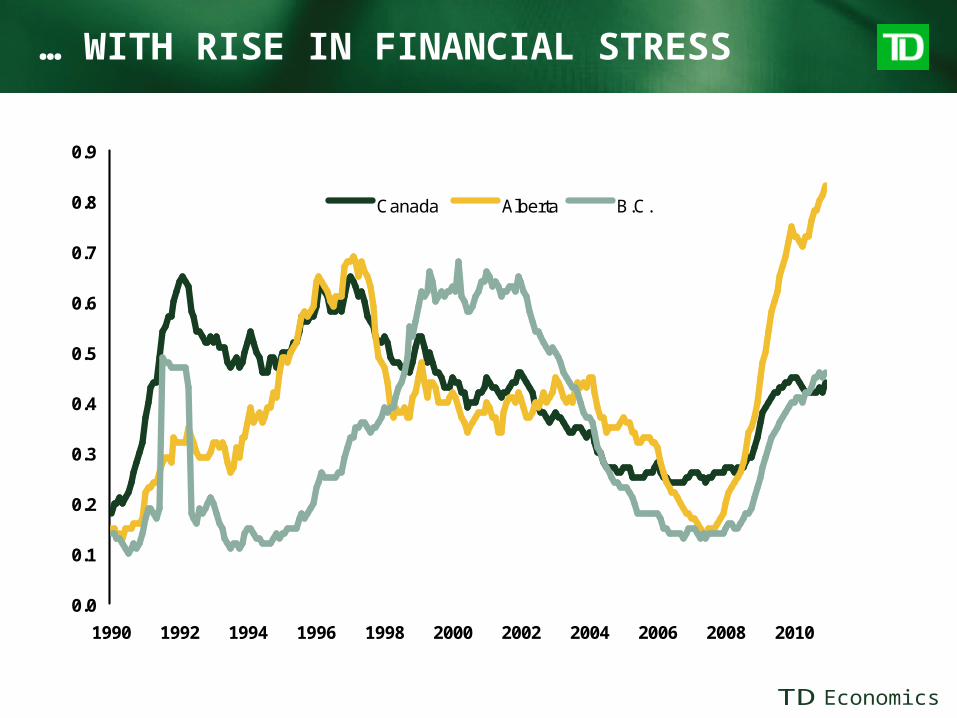

… WITH RISE IN FINANCIAL STRESS

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Canada Alberta B.C.

% of mortgages delinquent 90 days or more

Source: Canadian Banker's Association

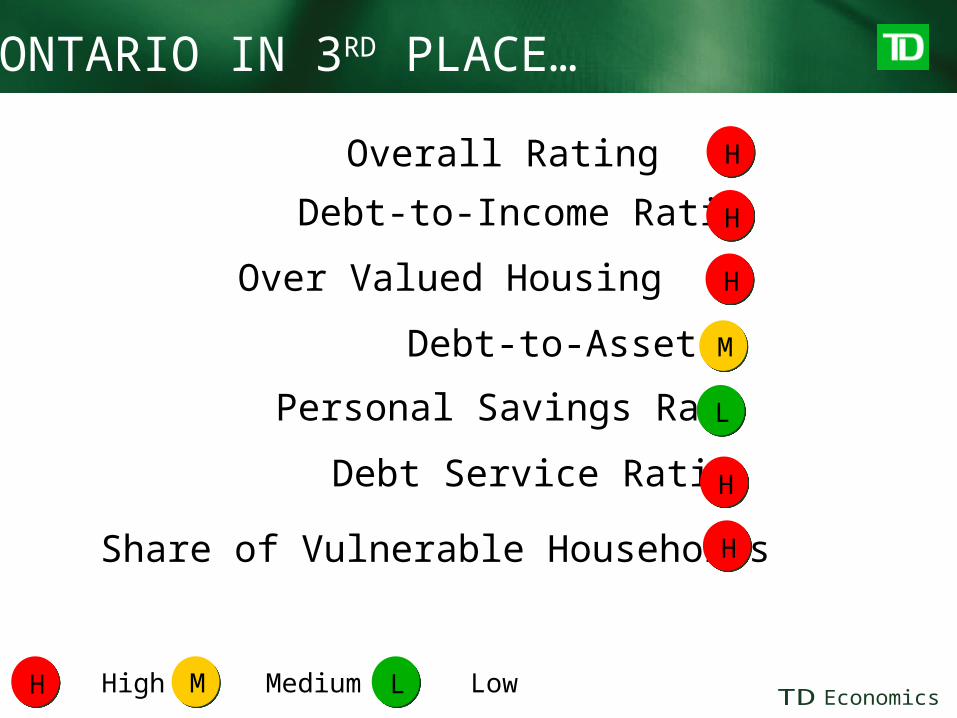

ONTARIO IN 3RD PLACE…

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

H

H

H

H

M

L LowM MediumH High

Share of Vulnerable Households H

L

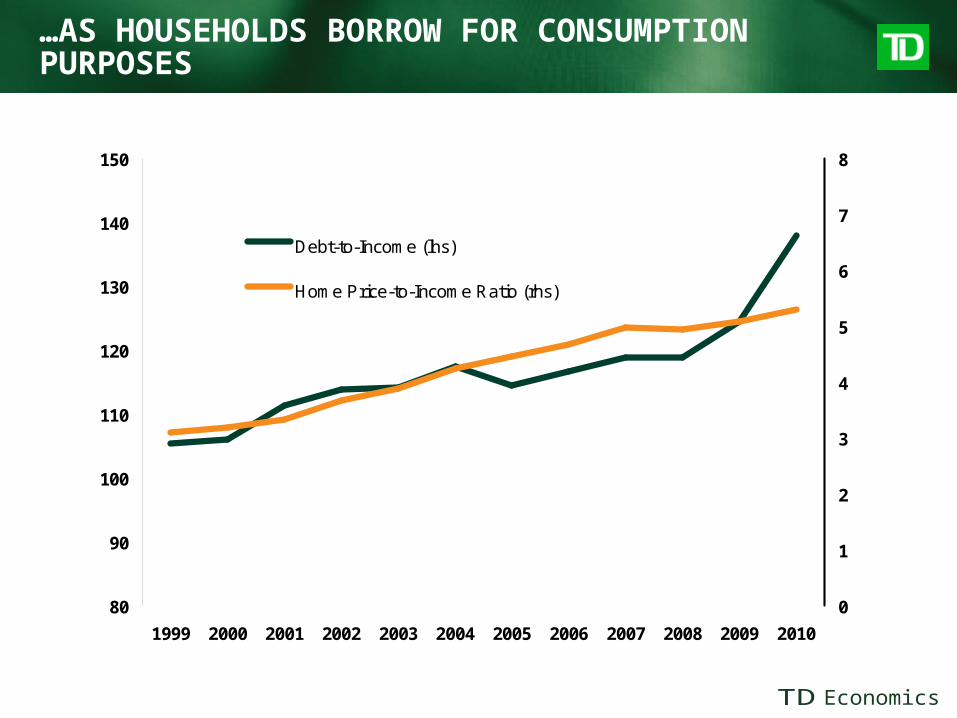

…AS HOUSEHOLDS BORROW FOR CONSUMPTION PURPOSES

80

90

100

110

120

130

140

150

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

0

1

2

3

4

5

6

7

8

Debt-to-Income (lhs)

Home Price-to-Income Ratio (rhs)

Source: Ipsos Reid, Statistics Canada, CREA, Haver Analytics

Ontario, % Ontario, Ratio

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

L LowM MediumH High

Share of Vulnerable Households H

L

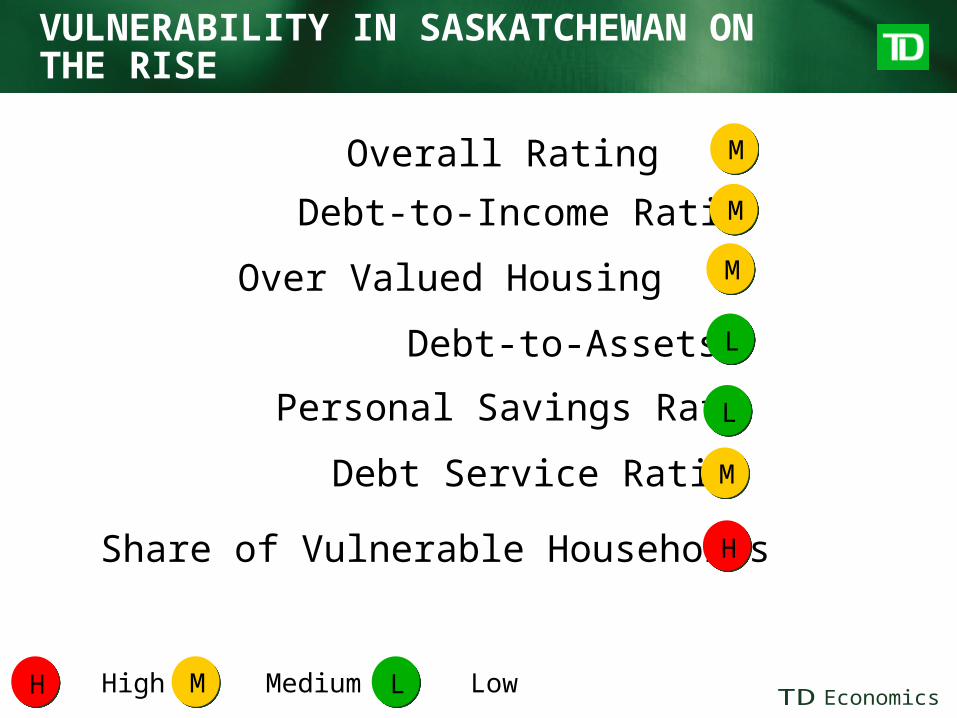

VULNERABILITY IN SASKATCHEWAN ON THE RISE

M

M

M

L

M

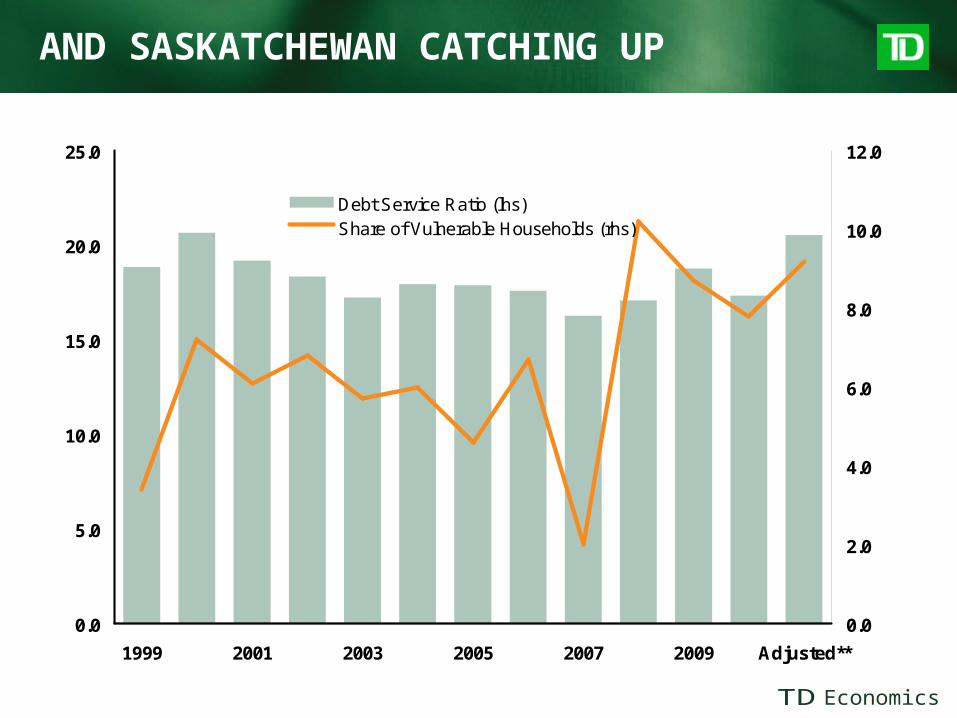

AND SASKATCHEWAN CATCHING UP

0.0

5.0

10.0

15.0

20.0

25.0

1999 2001 2003 2005 2007 2009 Adjusted**

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Debt Service Ratio (lhs)Share of Vulnerable Households (rhs)

Source: Ipsos Reid, calculated by TD Economics, ** adjusted for the expected future rise in interest rates

Saskatchewan, ratio interest and debt payments to income (%)

% of households with a debt service ratio above 40% in Saskatchewan

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

L LowM MediumH High

Share of Vulnerable Households

H

L

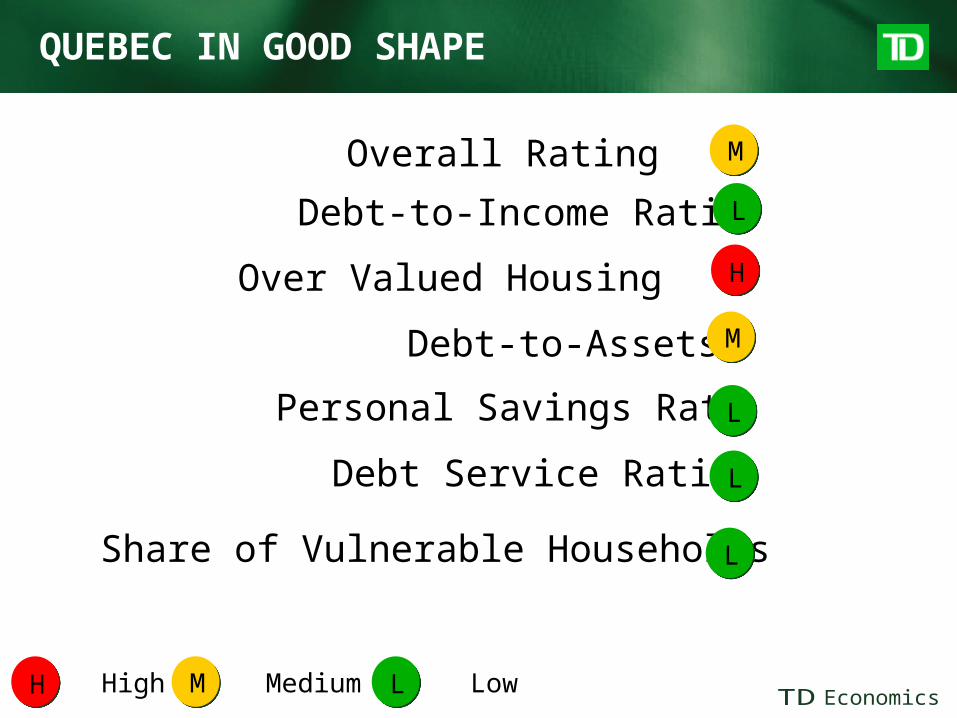

QUEBEC IN GOOD SHAPE

M

M

L

L

L

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

L LowM MediumH High

Share of Vulnerable Households

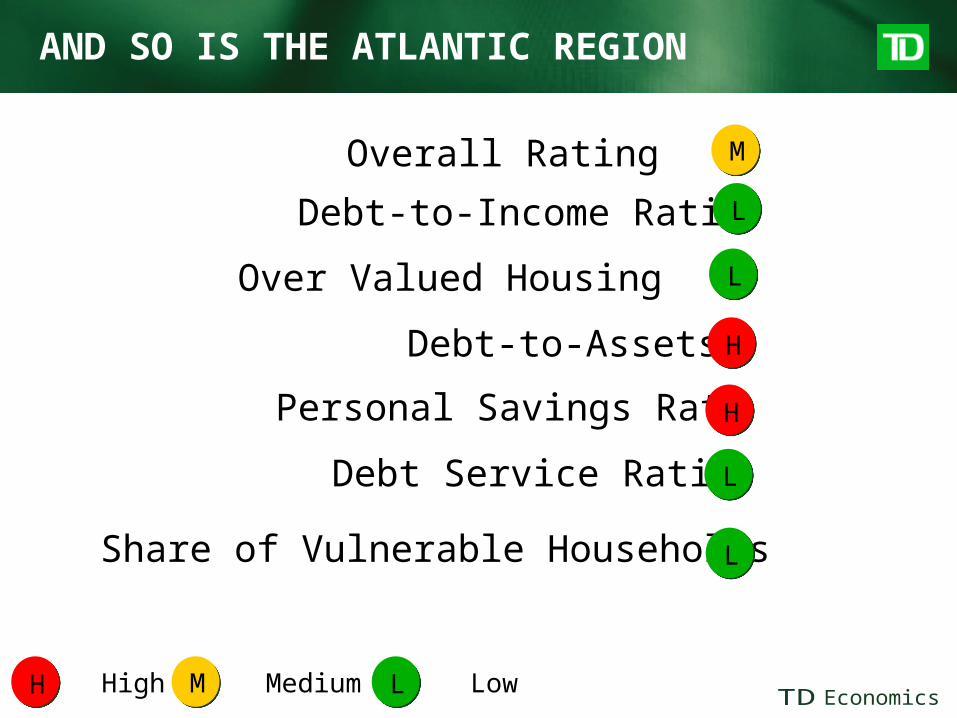

AND SO IS THE ATLANTIC REGION

M

L

L

L

L

H

H

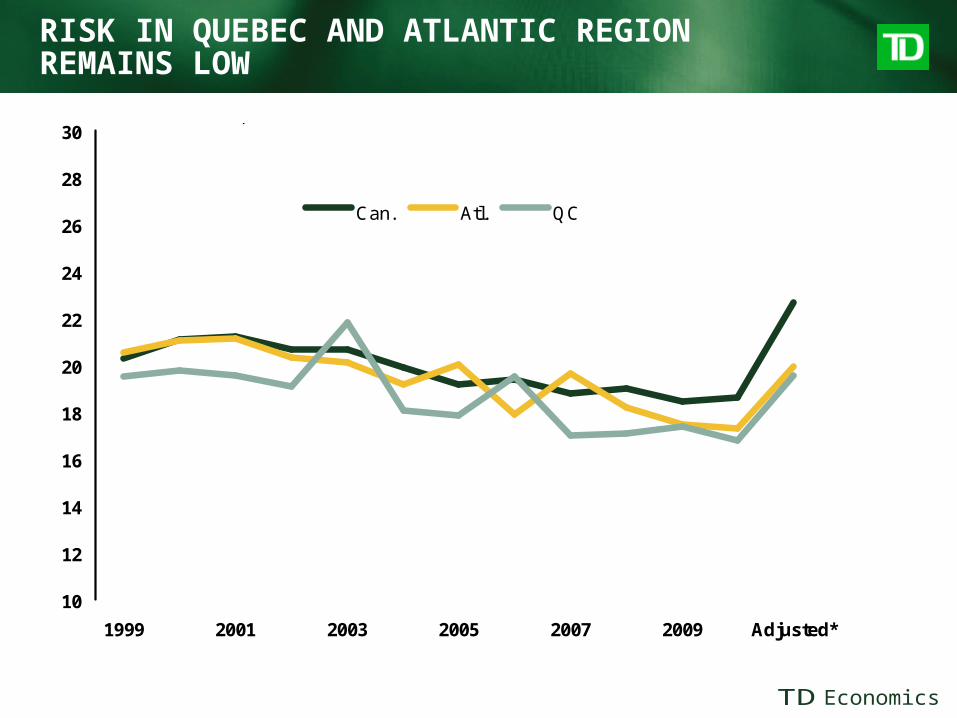

RISK IN QUEBEC AND ATLANTIC REGION REMAINS LOW

10

12

14

16

18

20

22

24

26

28

30

1999 2001 2003 2005 2007 2009 Adjusted*

Can. Atl. QC

Debt service ratio, %

Source: Ipsos Reid, * adjusted for expected future rise in interest rates by TD Economics

Overall Rating

Debt-to-Income Ratio

Over Valued Housing

Debt-to-Assets

Personal Savings Rate

Debt Service Ratio

L LowM MediumH High

Share of Vulnerable Households

DEBT IN MANITOBA REMAINS MANAGEABLE

L

L

L

L

M

L

L

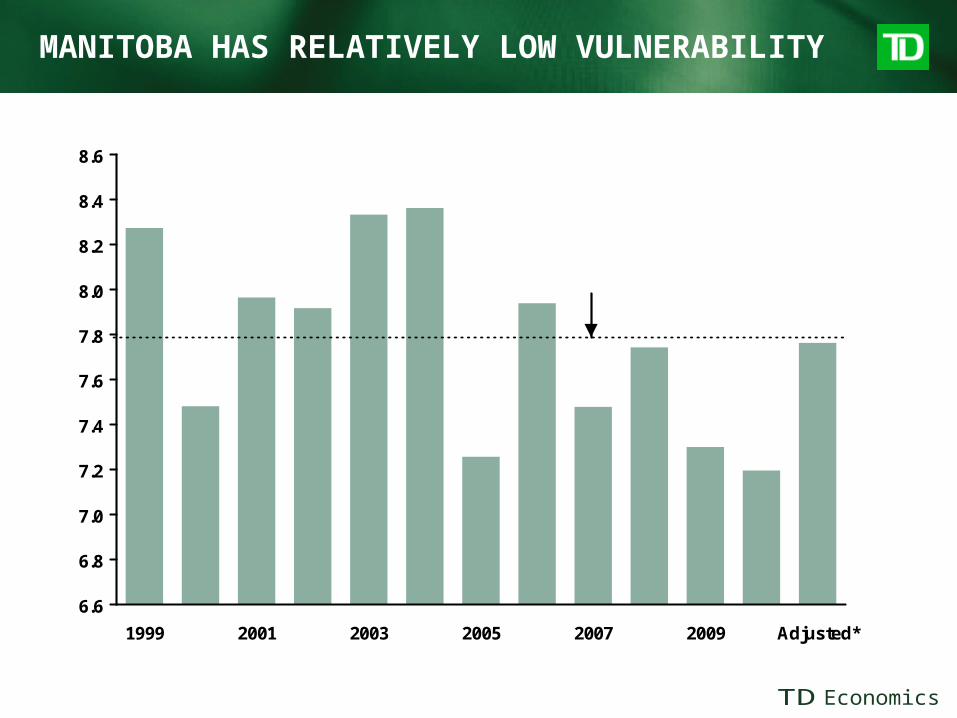

MANITOBA HAS RELATIVELY LOW VULNERABILITY

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

8.6

1999 2001 2003 2005 2007 2009 Adjusted*

Manitoba, Vulnerability Index

Source: Constructed by TD Economics, Ipsos Reid, * adjusted for expected future rise in interest rates

Historical Average

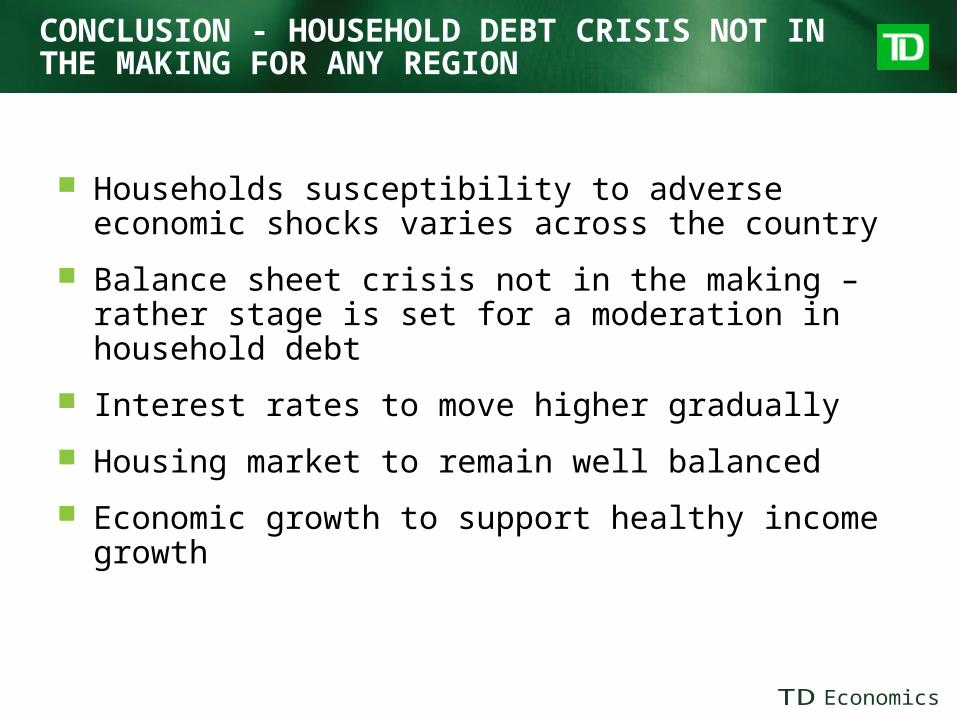

CONCLUSION - HOUSEHOLD DEBT CRISIS NOT IN THE MAKING FOR ANY REGION

Households susceptibility to adverse economic shocks varies across the country

Balance sheet crisis not in the making – rather stage is set for a moderation in household debt

Interest rates to move higher gradually

Housing market to remain well balanced

Economic growth to support healthy income growth

TD Economics

www.td.com/economics

This report is provided by TD Economics for customers of TD Bank Group. It is for information purposes only and may not be appropriate for other purposes. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. The report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.