Embed Size (px)

Citation preview

Derivatives Pricing a Forward / Futures Contract

Professor André Farber Solvay Brussels School of Economics and Management Université Libre de Bruxelles

Derivatives 02 Pricing forwards/futures |2 2/02/11

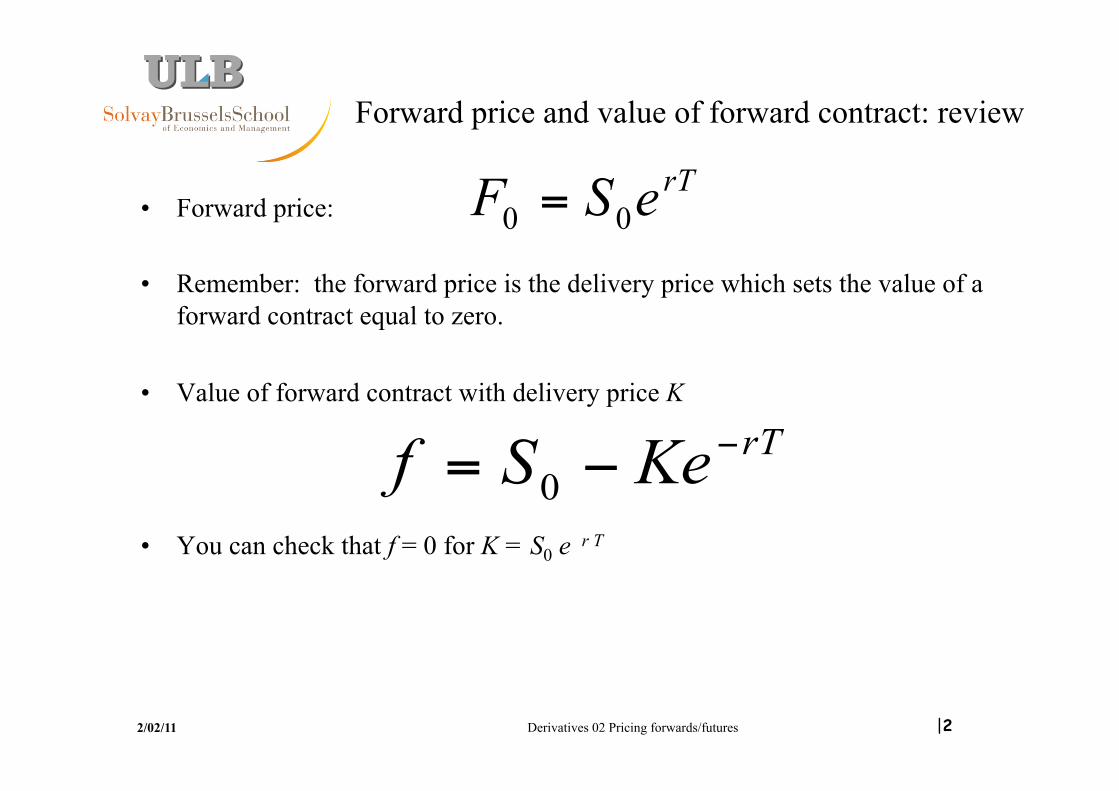

Forward price and value of forward contract: review

• Forward price:

• Remember: the forward price is the delivery price which sets the value of a forward contract equal to zero.

• Value of forward contract with delivery price K

• You can check that f = 0 for K = S0 e r T

rTeSF 00 =

rTKeSf −−= 0

Derivatives 02 Pricing forwards/futures |3 2/02/11

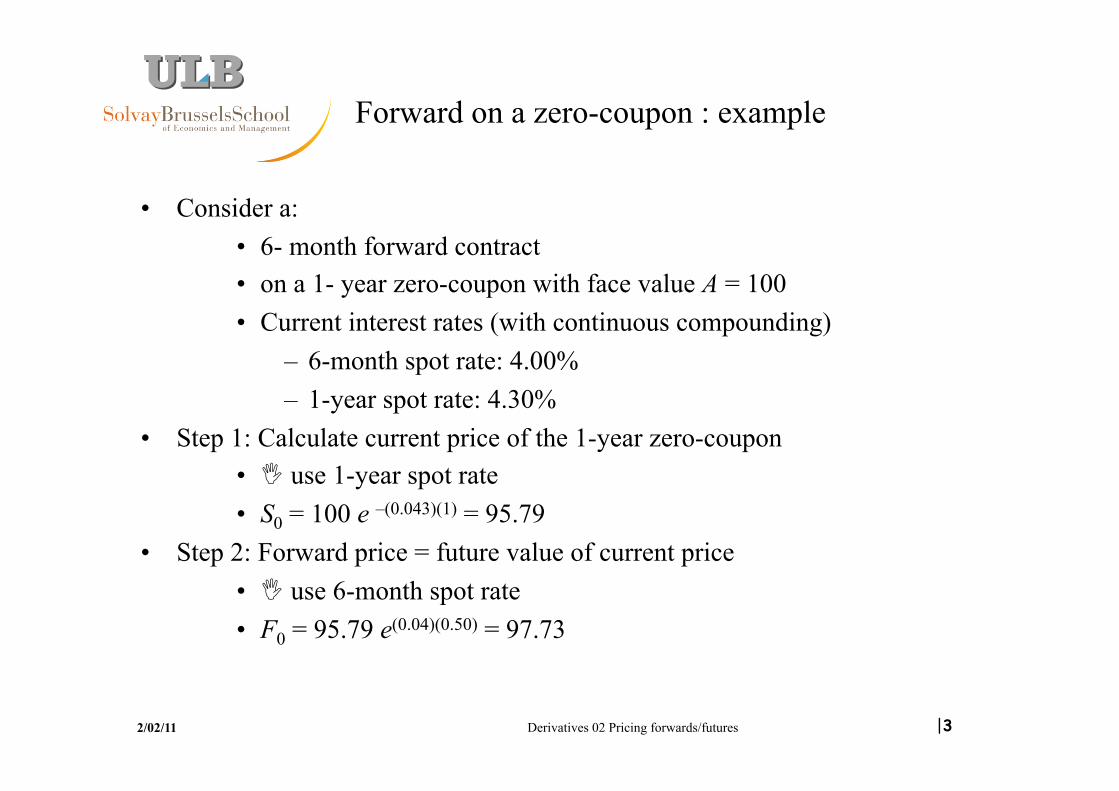

Forward on a zero-coupon : example

• Consider a: • 6- month forward contract • on a 1- year zero-coupon with face value A = 100 • Current interest rates (with continuous compounding)

– 6-month spot rate: 4.00% – 1-year spot rate: 4.30%

• Step 1: Calculate current price of the 1-year zero-coupon • I use 1-year spot rate • S0 = 100 e –(0.043)(1) = 95.79

• Step 2: Forward price = future value of current price • I use 6-month spot rate • F0 = 95.79 e(0.04)(0.50) = 97.73

Derivatives 02 Pricing forwards/futures |4 2/02/11

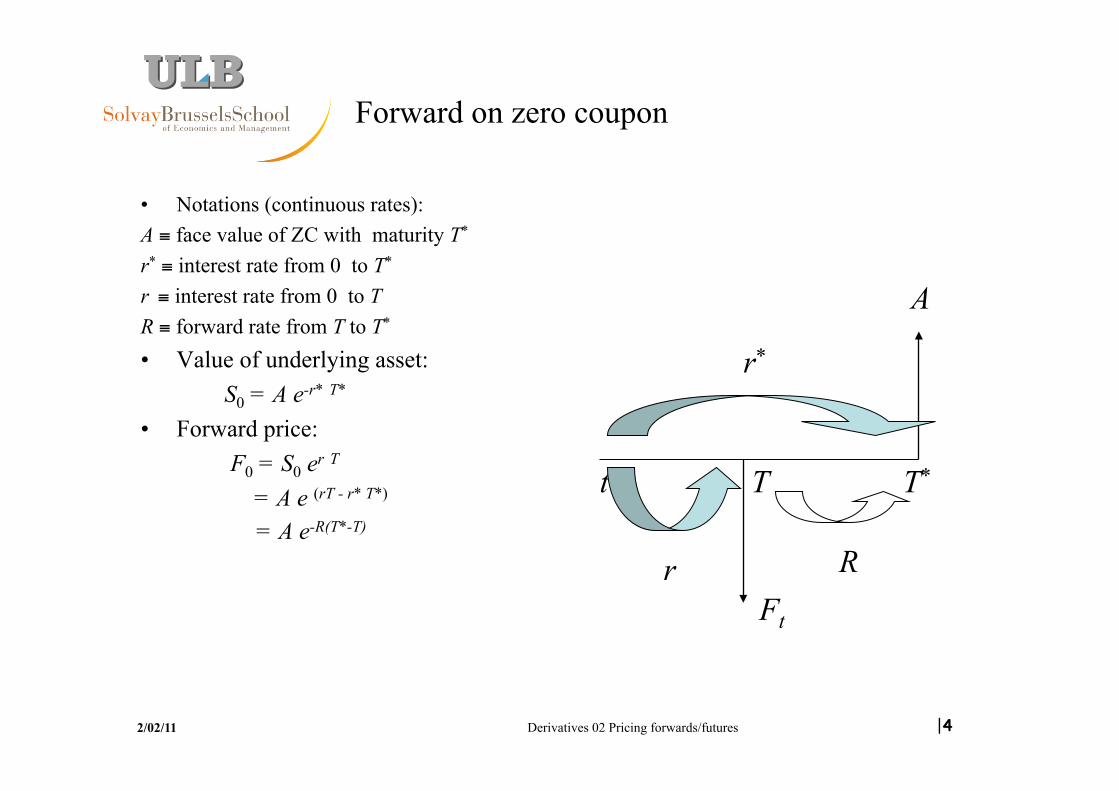

Forward on zero coupon

• Notations (continuous rates): A ≡ face value of ZC with maturity T* r* ≡ interest rate from 0 to T* r ≡ interest rate from 0 to T R ≡ forward rate from T to T* • Value of underlying asset: S0 = A e-r* T*

• Forward price: F0 = S0 er T = A e (rT - r* T*)

= A e-R(T*-T)

t T T*

Ft

A

r

r*

R

Derivatives 02 Pricing forwards/futures |5 2/02/11

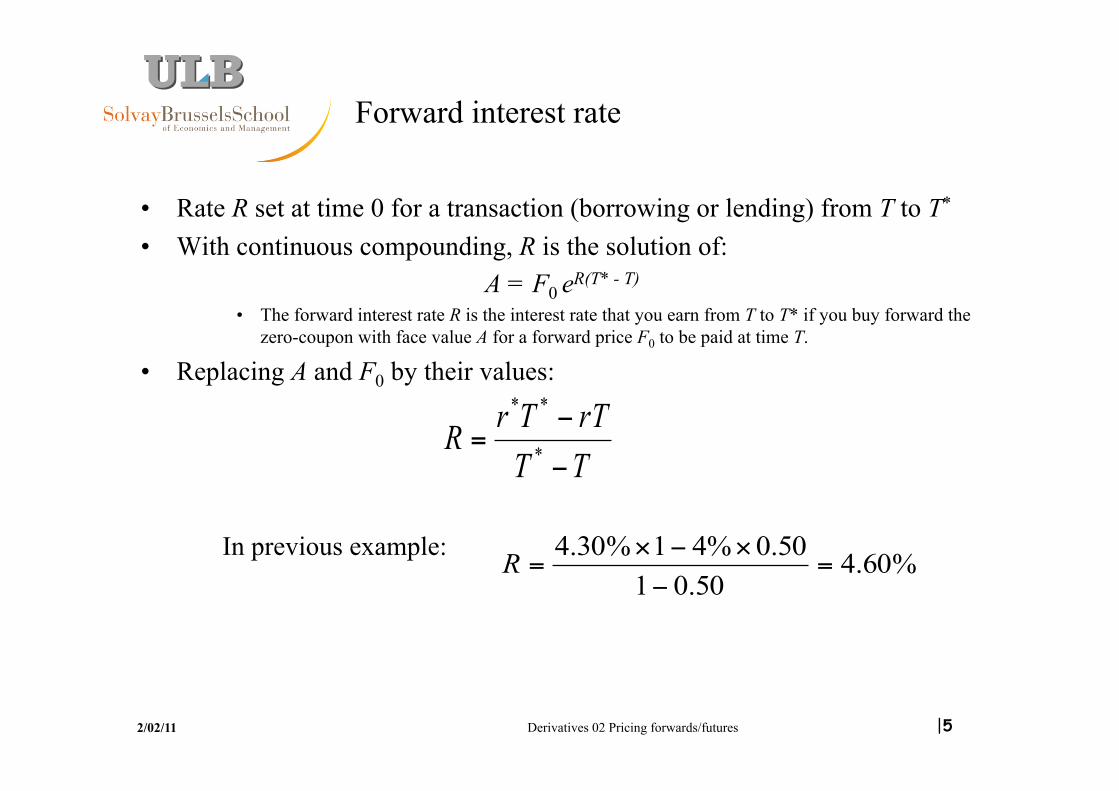

Forward interest rate

• Rate R set at time 0 for a transaction (borrowing or lending) from T to T*

• With continuous compounding, R is the solution of: A = F0 eR(T* - T)

• The forward interest rate R is the interest rate that you earn from T to T* if you buy forward the zero-coupon with face value A for a forward price F0 to be paid at time T.

• Replacing A and F0 by their values:

TTrTTrR

−

−= *

**

In previous example: %60.450.01

50.0%41%30.4=

−

×−×=R

Derivatives 02 Pricing forwards/futures |6 2/02/11

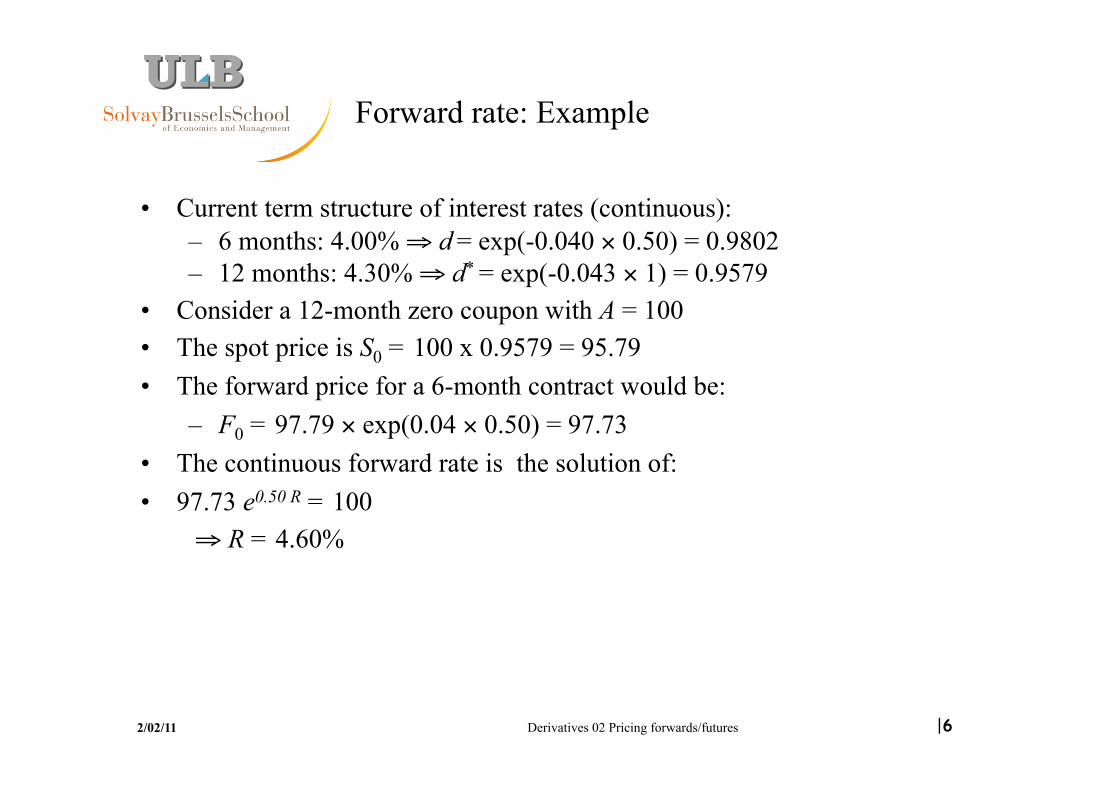

Forward rate: Example

• Current term structure of interest rates (continuous): – 6 months: 4.00% ⇒ d = exp(-0.040 × 0.50) = 0.9802 – 12 months: 4.30% ⇒ d*

= exp(-0.043 × 1) = 0.9579 • Consider a 12-month zero coupon with A = 100 • The spot price is S0 = 100 x 0.9579 = 95.79 • The forward price for a 6-month contract would be:

– F0 = 97.79 × exp(0.04 × 0.50) = 97.73 • The continuous forward rate is the solution of: • 97.73 e0.50 R = 100

⇒ R = 4.60%

Derivatives 02 Pricing forwards/futures |7 2/02/11

Forward borrowing

• View forward borrowing as a forward contract on a ZC You plan to borrow M for τ years from T to T*

The simple interest rate set today is RS

You will repay M(1+RS) at maturity • In fact, you sell forward a ZC

The face value is M(1+RS) The maturity is is T* The delivery price set today is M

• The interest will set the value of this contract to zero

Derivatives 02 Pricing forwards/futures |8 2/02/11

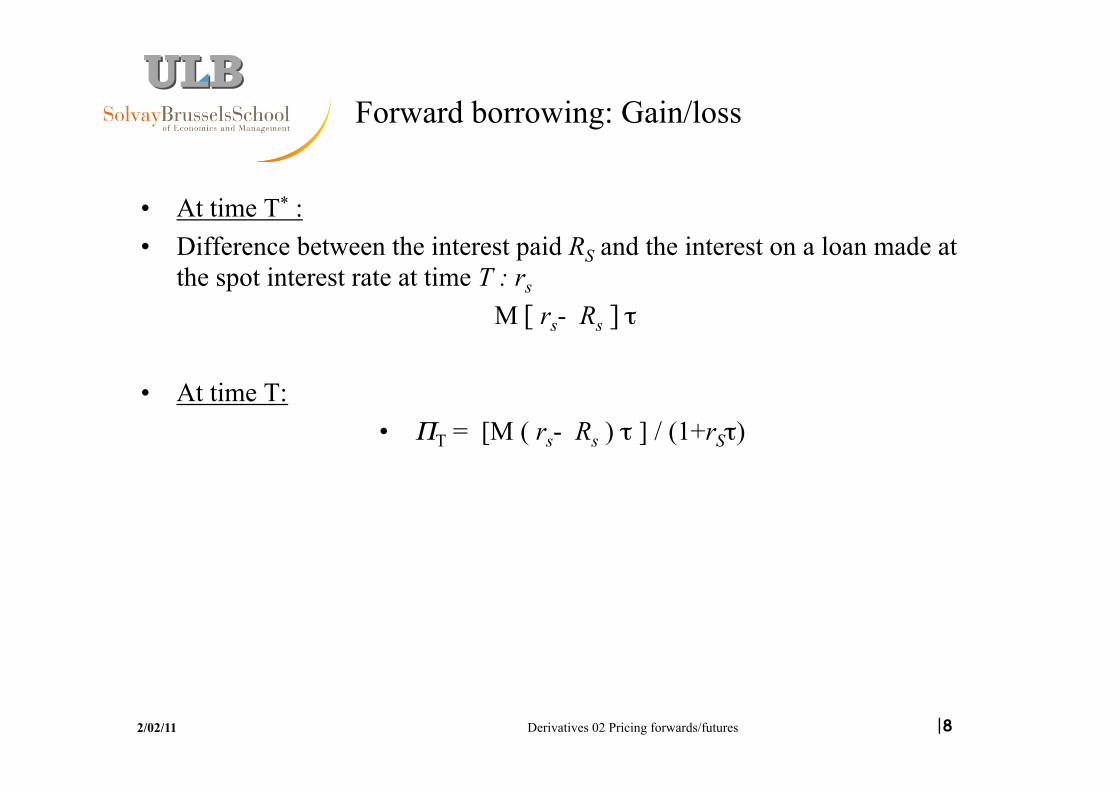

Forward borrowing: Gain/loss

• At time T* : • Difference between the interest paid RS and the interest on a loan made at

the spot interest rate at time T : rs M [ rs- Rs ] τ

• At time T: • ΠT = [M ( rs- Rs ) τ ] / (1+rSτ)

Derivatives 02 Pricing forwards/futures |9 2/02/11

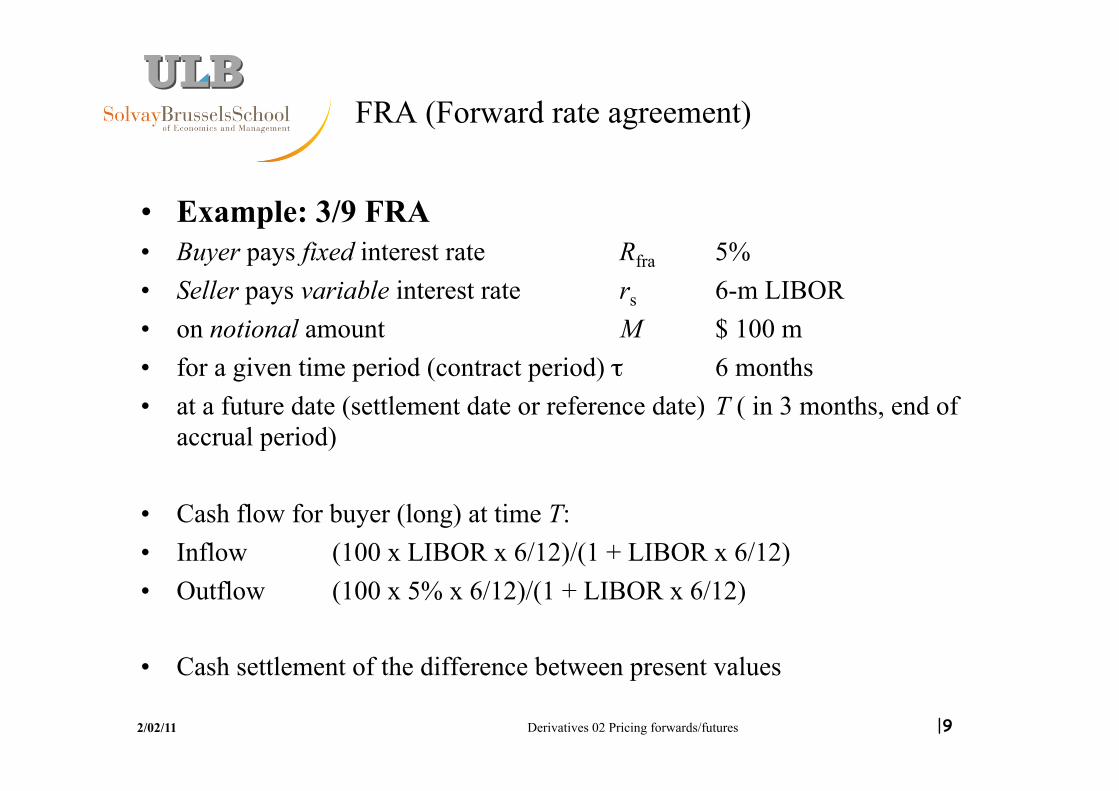

FRA (Forward rate agreement)

• Example: 3/9 FRA • Buyer pays fixed interest rate Rfra 5% • Seller pays variable interest rate rs 6-m LIBOR • on notional amount M $ 100 m • for a given time period (contract period) τ 6 months • at a future date (settlement date or reference date) T ( in 3 months, end of

accrual period)

• Cash flow for buyer (long) at time T: • Inflow (100 x LIBOR x 6/12)/(1 + LIBOR x 6/12) • Outflow (100 x 5% x 6/12)/(1 + LIBOR x 6/12)

• Cash settlement of the difference between present values

Derivatives 02 Pricing forwards/futures |10 2/02/11

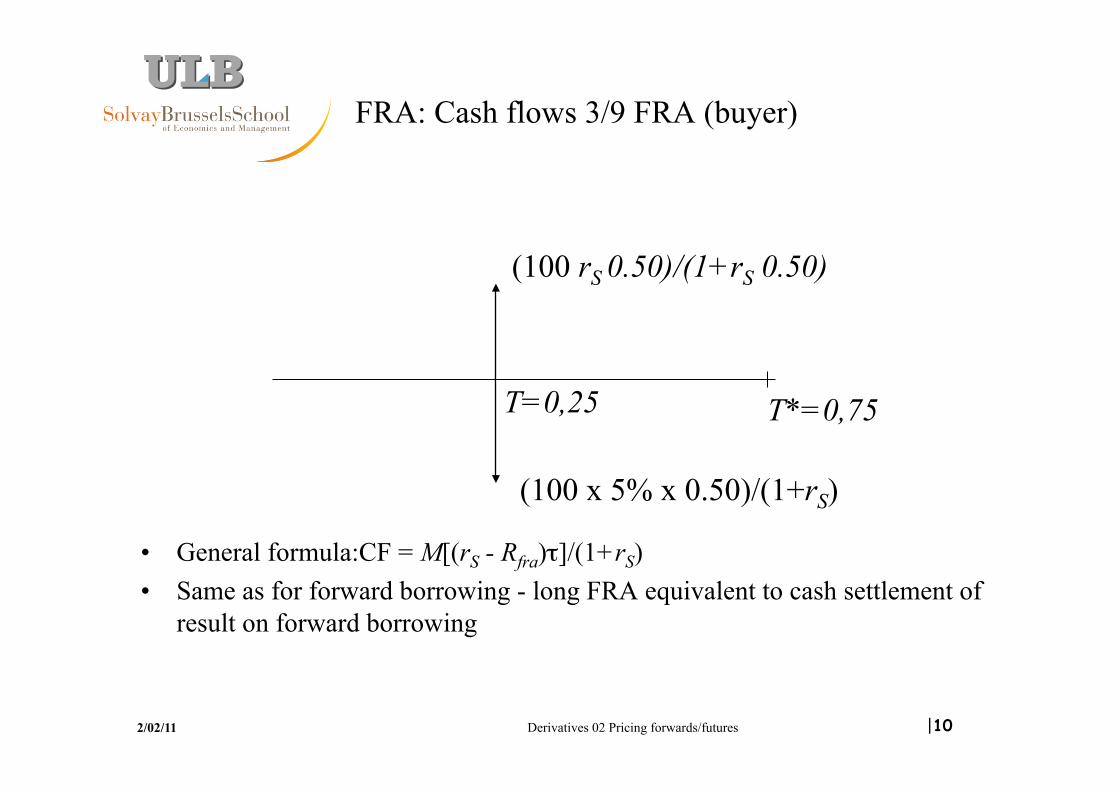

FRA: Cash flows 3/9 FRA (buyer)

• General formula:CF = M[(rS - Rfra)τ]/(1+rS) • Same as for forward borrowing - long FRA equivalent to cash settlement of

result on forward borrowing

(100 rS 0.50)/(1+rS 0.50)

T=0,25 T*=0,75

(100 x 5% x 0.50)/(1+rS)

Derivatives |11

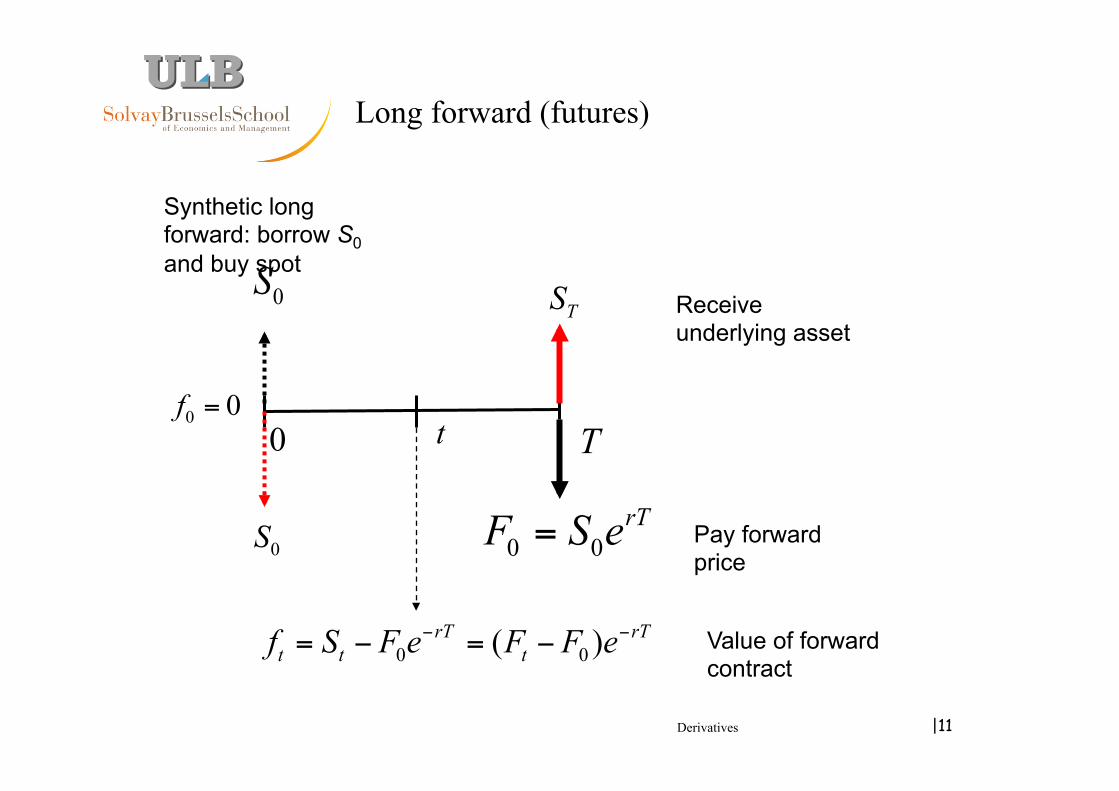

Long forward (futures)

0 0rTF S e=

TS

0 T

0S

0 0f =t

0 0( )rT rTt t tf S F e F F e− −= − = −

0S

Synthetic long forward: borrow S0 and buy spot

Pay forward price

Receive underlying asset

Value of forward contract

Derivatives |12

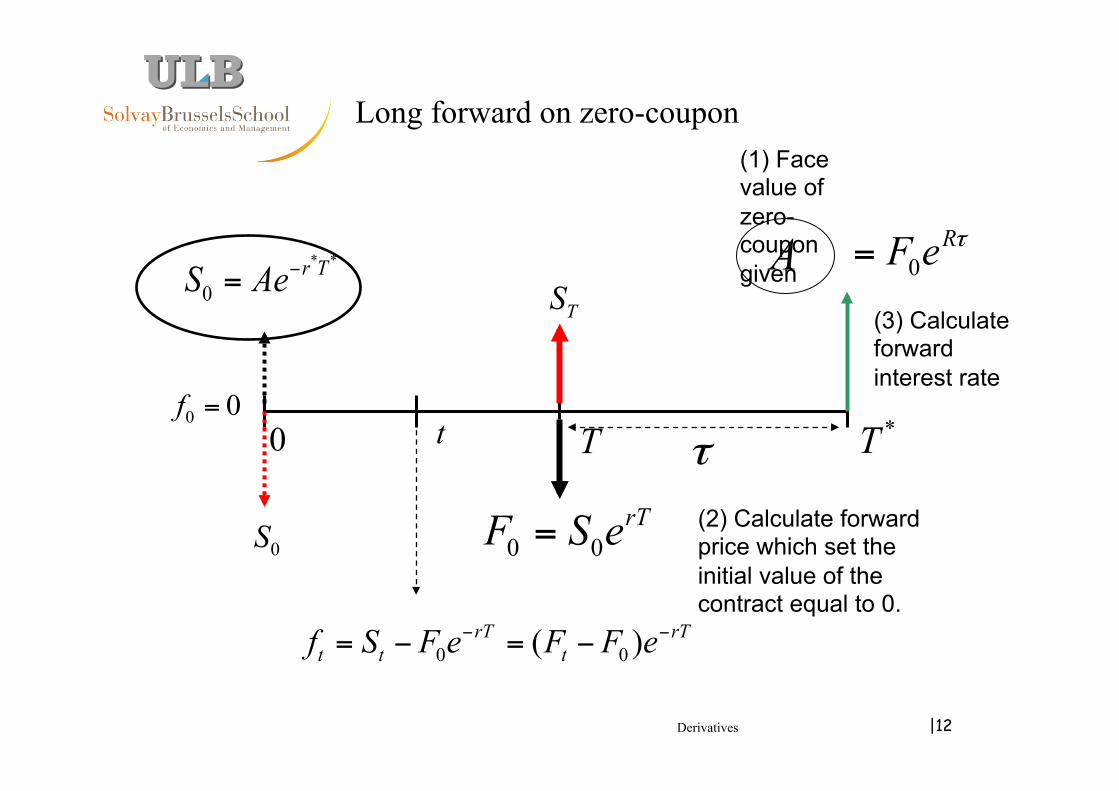

Long forward on zero-coupon

0 0rTF S e=

TS

0 T

0S

0 0f =t

0 0( )rT rTt t tf S F e F F e− −= − = −

* *

0r TS Ae−=

*T

A

τ

0RF e τ=

(1) Face value of zero-coupon given

(2) Calculate forward price which set the initial value of the contract equal to 0.

(3) Calculate forward interest rate

Derivatives |13

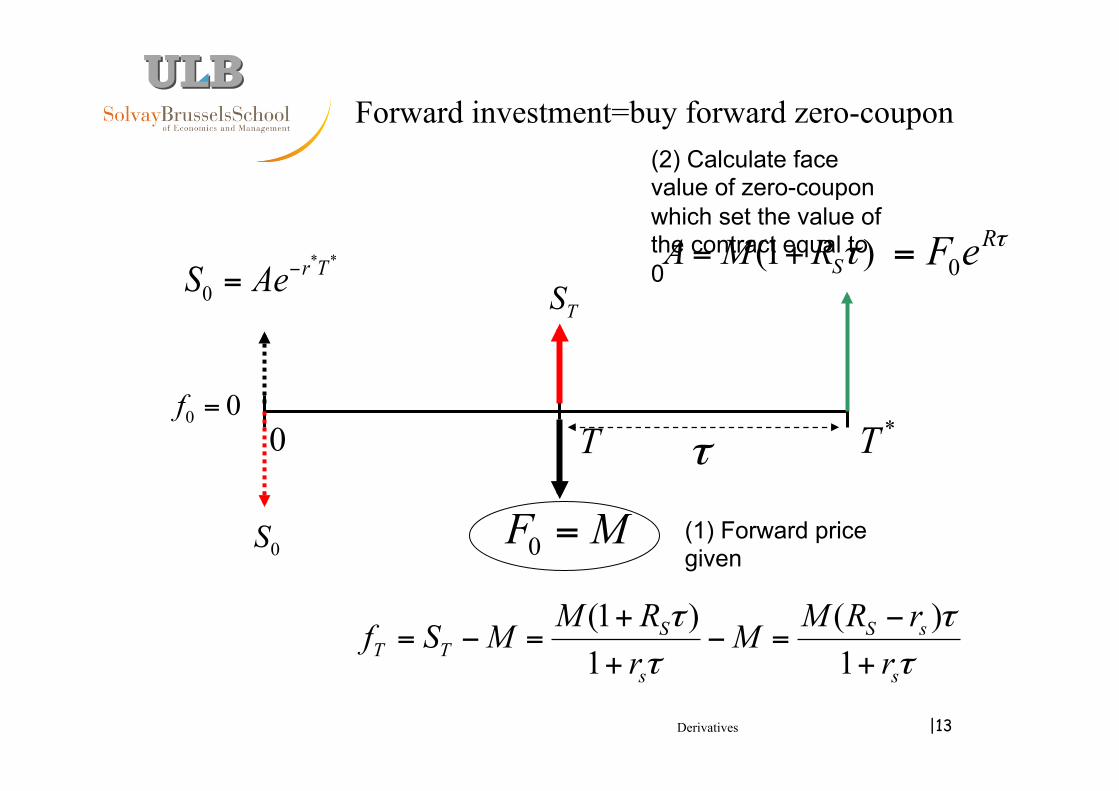

Forward investment=buy forward zero-coupon

0F M=

TS

0 T

0S

0 0f =

(1 ) ( )1 1

S S sT T

s s

M R M R rf S M Mr r

τ ττ τ

+ −= − = − =

+ +

* *

0r TS Ae−=

*T

(1 )SA M R τ= +

τ

0RF e τ=

(1) Forward price given

(2) Calculate face value of zero-coupon which set the value of the contract equal to 0

Derivatives |14

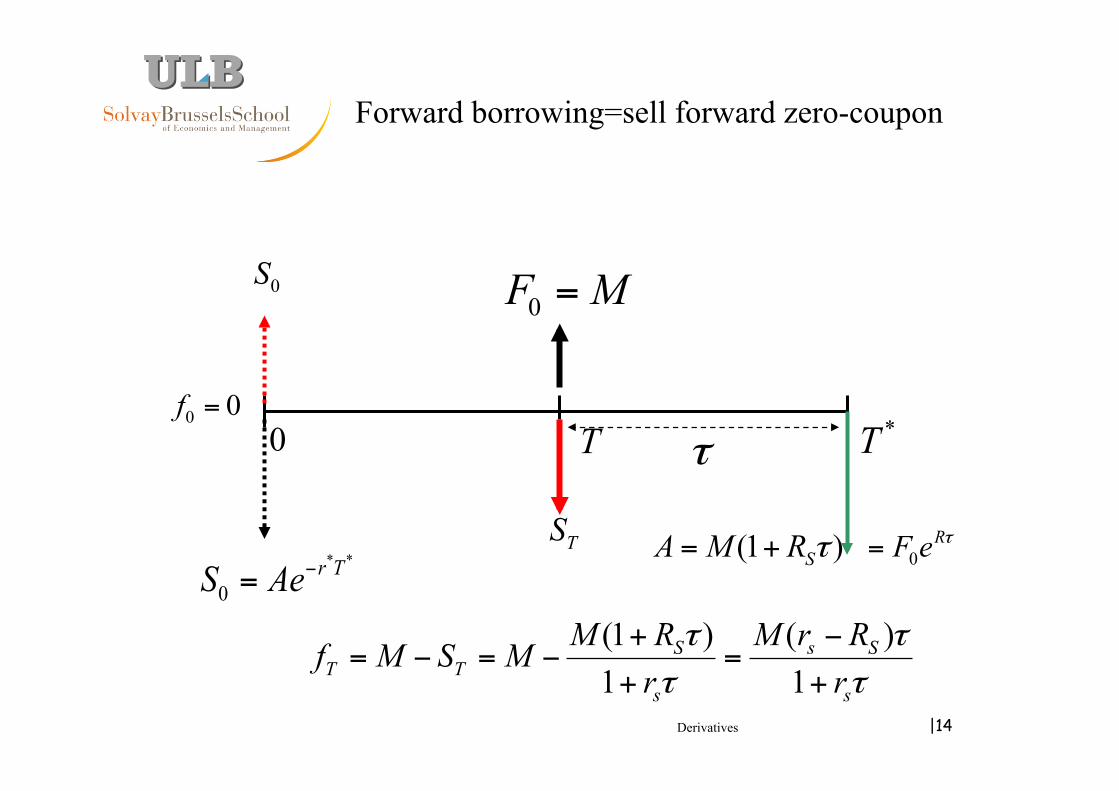

Forward borrowing=sell forward zero-coupon

0F M=

TS

0 T

0S

0 0f =

(1 ) ( )1 1

S s ST T

s s

M R M r Rf M S Mr r

τ ττ τ

+ −= − = − =

+ +

* *

0r TS Ae−=

*T

(1 )SA M R τ= +

τ

0RF e τ=

Derivatives |15

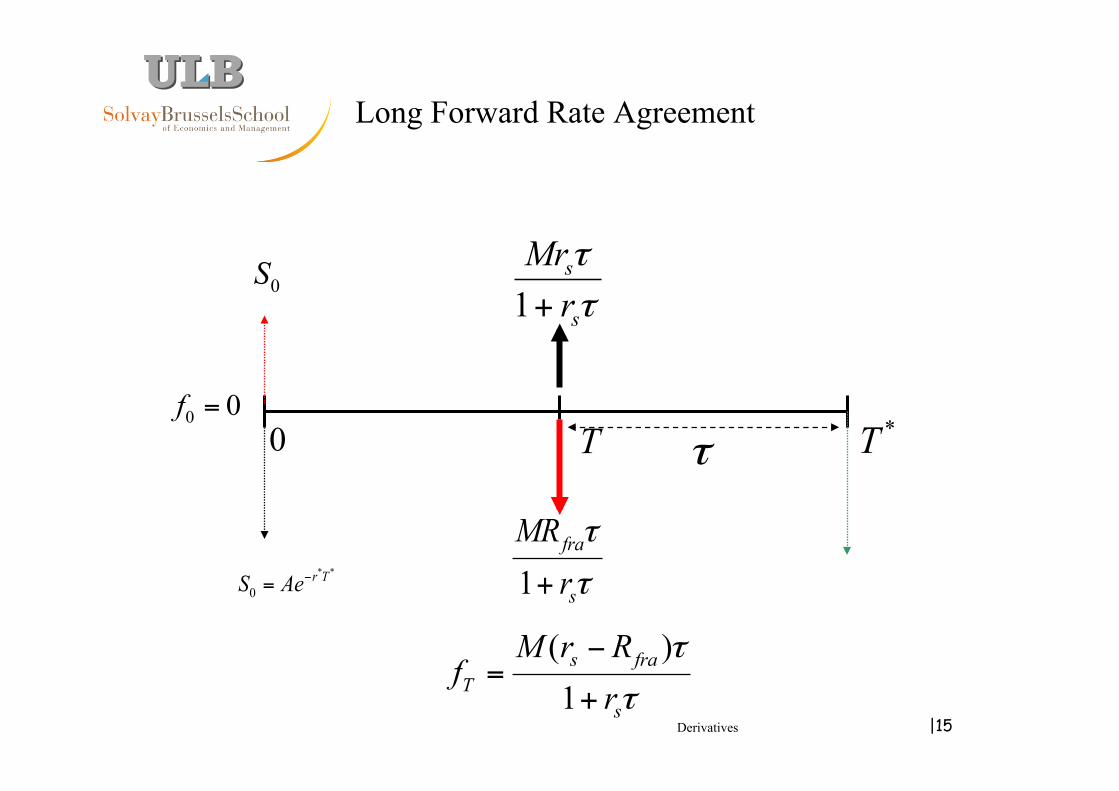

Long Forward Rate Agreement

* *

0r TS Ae−=

1s

s

Mrrττ+

0 T

0S

0 0f =

( )1s fra

Ts

M r Rf

rτ

τ

−=

+

*Tτ

1fra

s

MRrτ

τ+

Derivatives |16

To lock in future interest rate

Borrow short & invest long

Buy forward zero coupon

Invest forward at current forward interest rate

Sell FRA and invest at future (unknown) spot interest rate

Derivatives |17

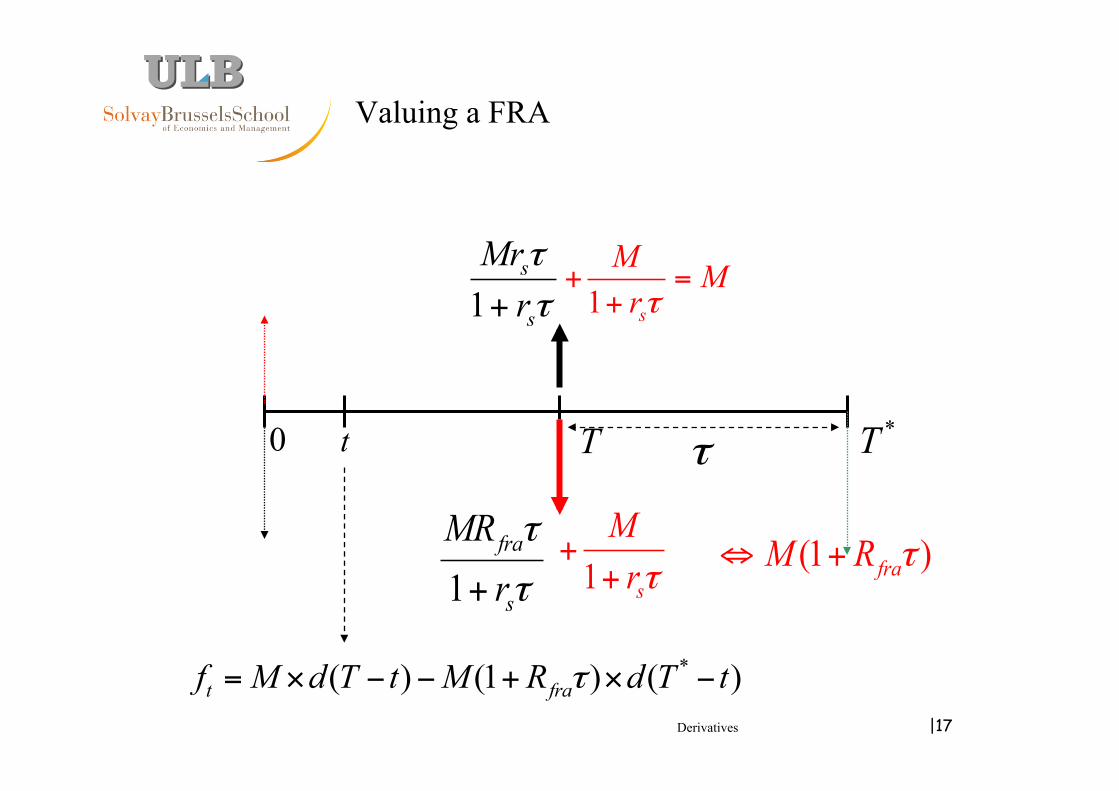

Valuing a FRA

1fra

s

MRrτ

τ+ 1 s

Mrτ

++

1s

s

Mrrττ+

0 T

*( ) (1 ) ( )t fraf M d T t M R d T tτ= × − − + × −

*Tτ

1 s

M Mrτ

+ =+

(1 )fraM R τ⇔ +

t

Derivatives 02 Pricing forwards/futures |18 2/02/11

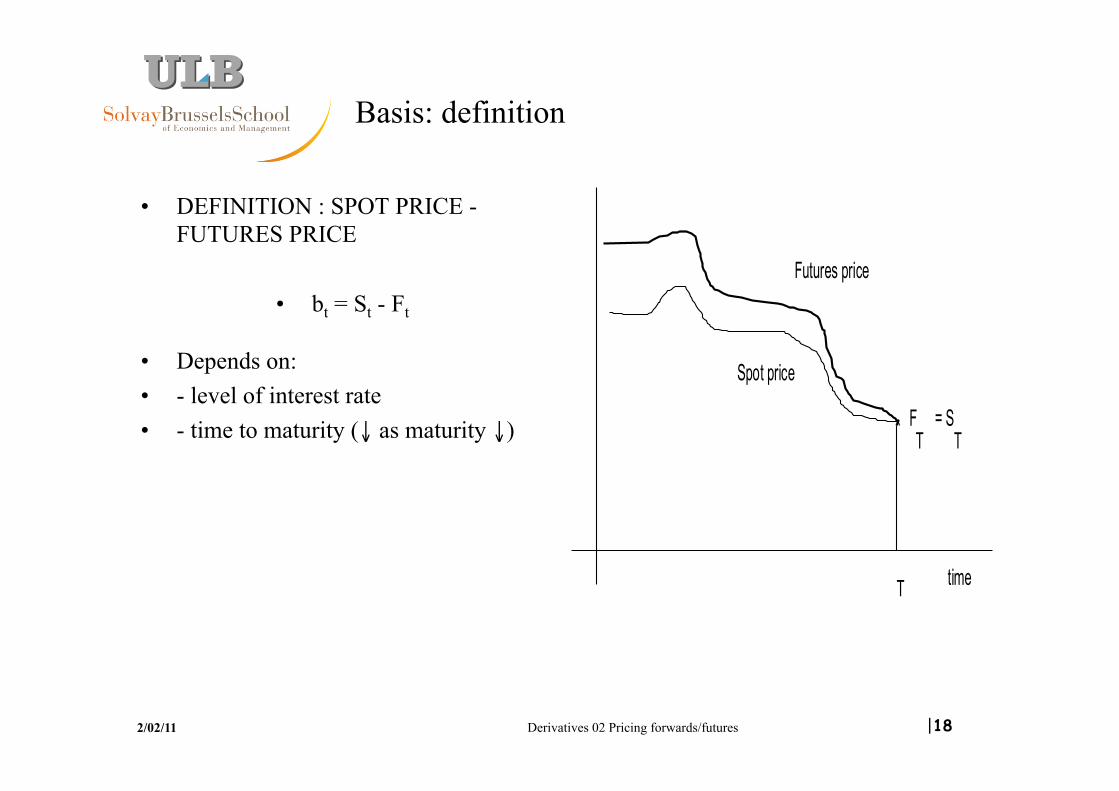

Basis: definition

• DEFINITION : SPOT PRICE - FUTURES PRICE

• bt = St - Ft

• Depends on: • - level of interest rate • - time to maturity (↓ as maturity ↓)

Spot price

Futures price

timeT

FT

= ST

Derivatives 02 Pricing forwards/futures |19 2/02/11

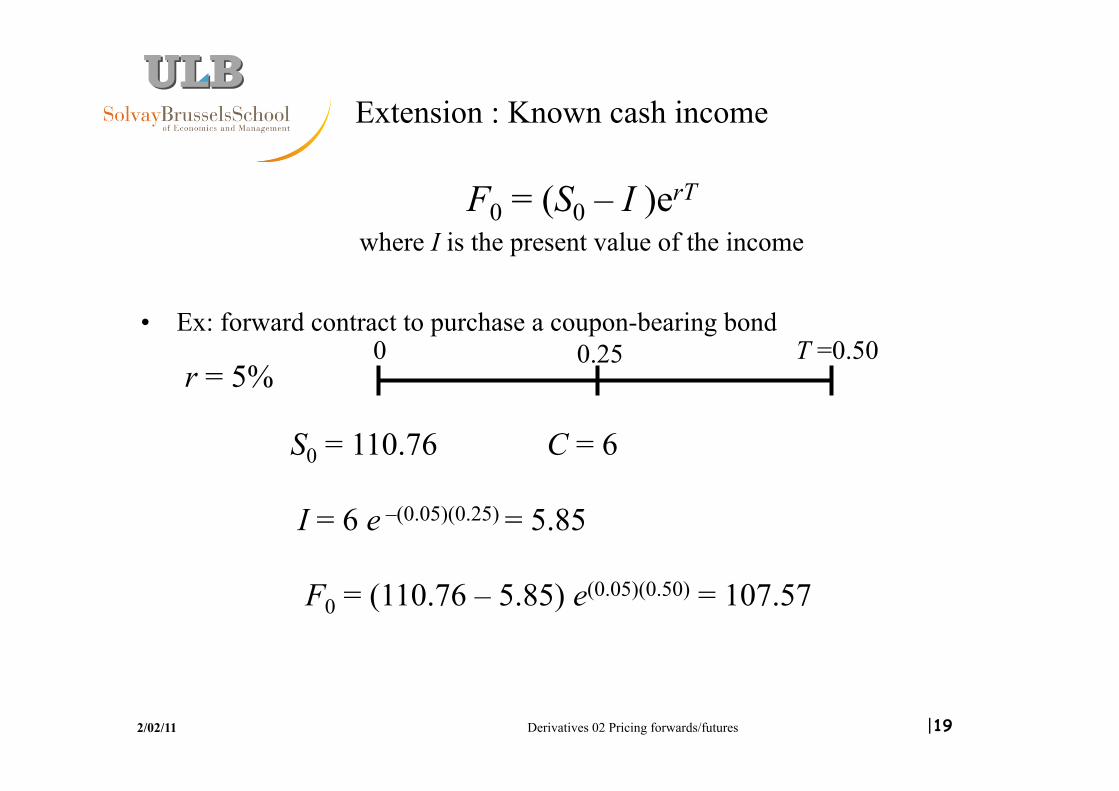

Extension : Known cash income

• Ex: forward contract to purchase a coupon-bearing bond

F0 = (S0 – I )erT where I is the present value of the income

0 0.25 T =0.50

S0 = 110.76

r = 5%

C = 6

I = 6 e –(0.05)(0.25) = 5.85

F0 = (110.76 – 5.85) e(0.05)(0.50) = 107.57

Derivatives 02 Pricing forwards/futures |20 2/02/11

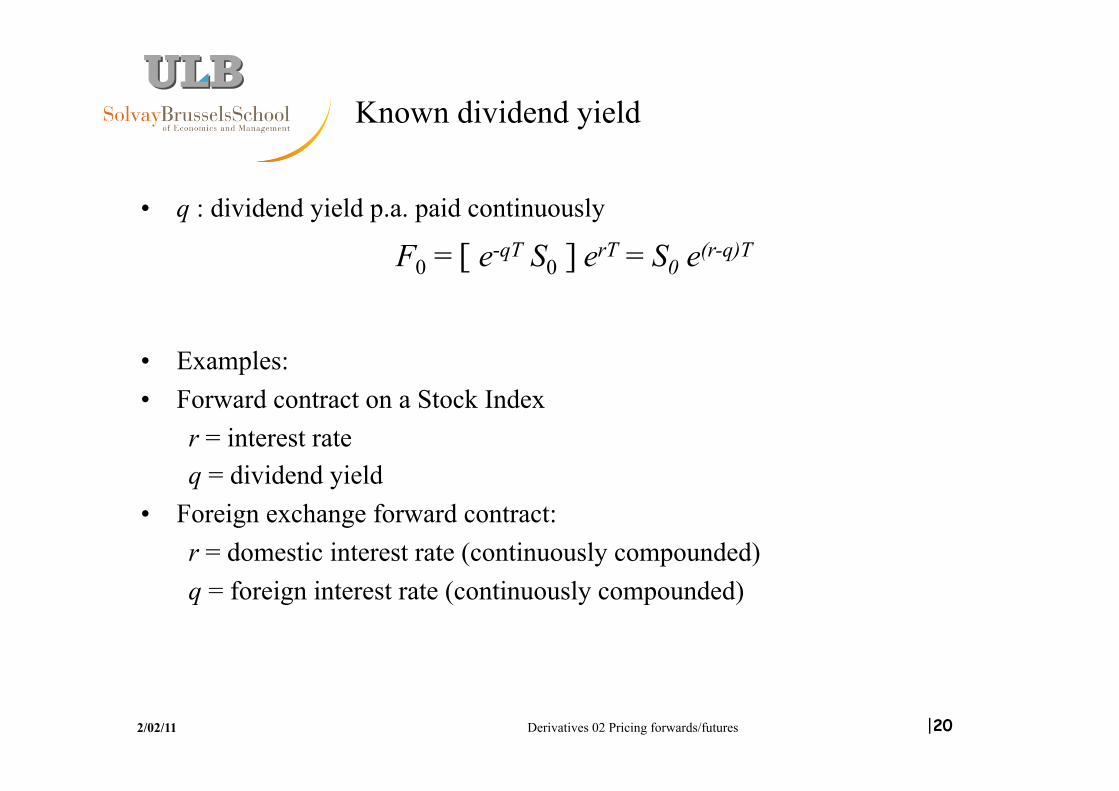

Known dividend yield

• q : dividend yield p.a. paid continuously

• Examples: • Forward contract on a Stock Index

r = interest rate q = dividend yield

• Foreign exchange forward contract: r = domestic interest rate (continuously compounded) q = foreign interest rate (continuously compounded)

F0 = [ e-qT S0 ] erT = S0 e(r-q)T

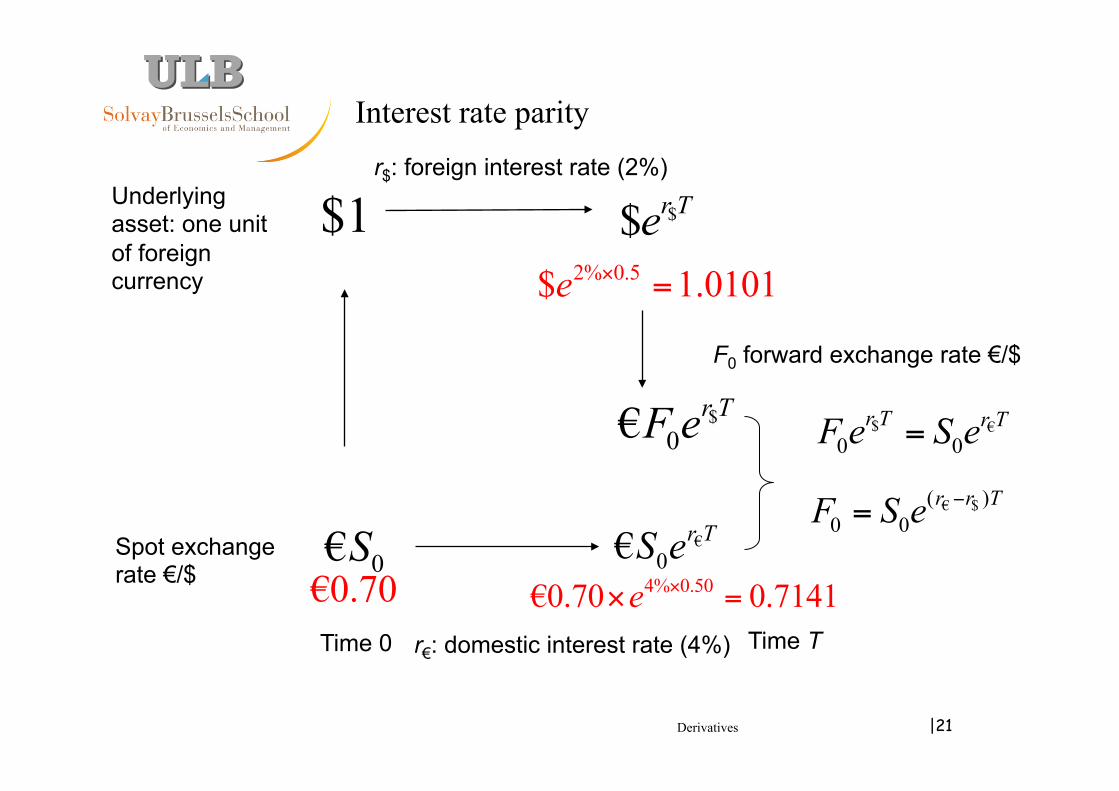

Derivatives |21

0€SSpot exchange rate €/$

$1

Time 0 Time T

$$ r Te

Interest rate parity

€0€r TS e

Underlying asset: one unit of foreign currency

€0.70

r$: foreign interest rate (2%)

2% 0.5$ 1.0101e × =

r€: domestic interest rate (4%)

4% 0.50€0.70 0.7141e ×× =

$0€r TF e

F0 forward exchange rate €/$

$ €0 0r T r TF e S e=

€ $( )0 0

r r TF S e −=

Derivatives 02 Pricing forwards/futures |22 2/02/11

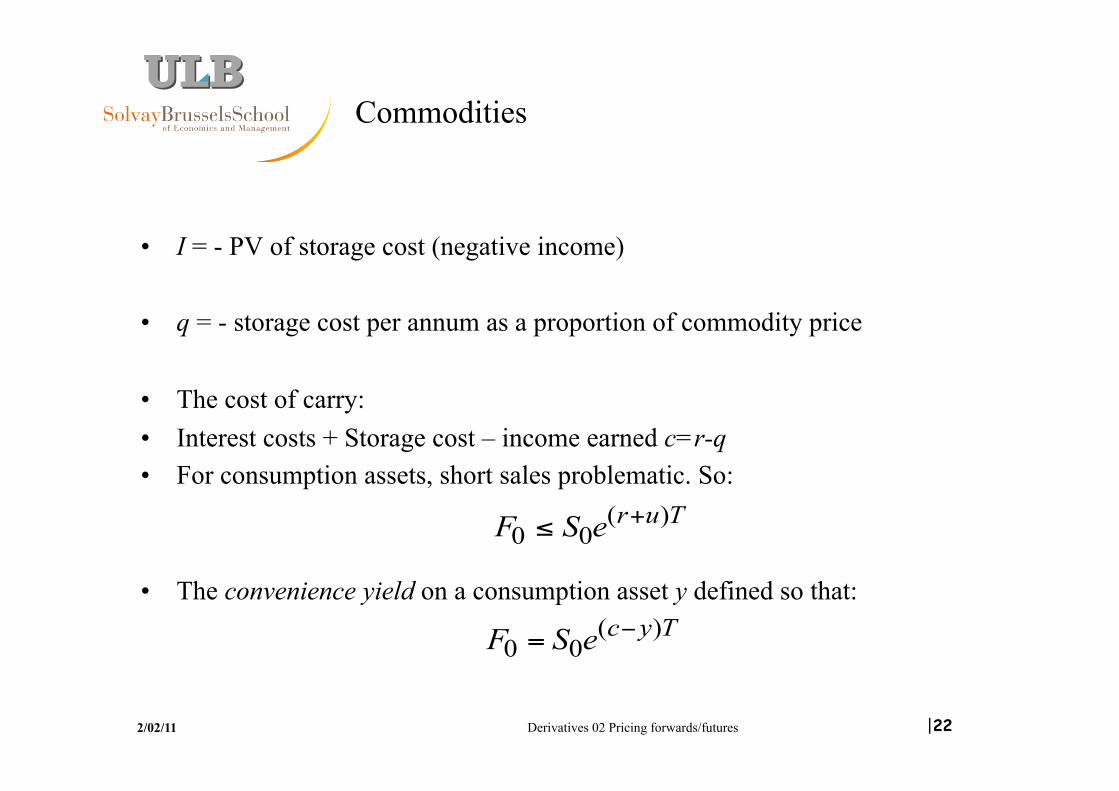

Commodities

• I = - PV of storage cost (negative income)

• q = - storage cost per annum as a proportion of commodity price

• The cost of carry: • Interest costs + Storage cost – income earned c=r-q • For consumption assets, short sales problematic. So:

• The convenience yield on a consumption asset y defined so that:

TureSF )(00

+≤

TyceSF )(00

−=

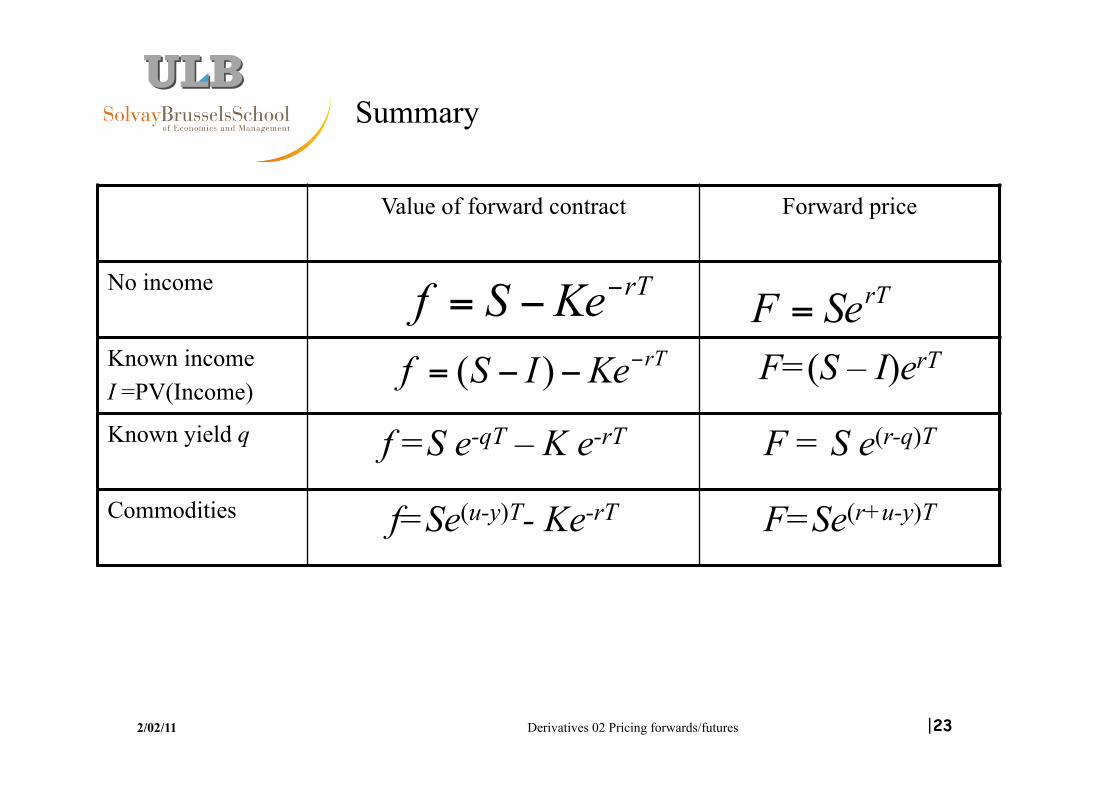

Derivatives 02 Pricing forwards/futures |23 2/02/11

Summary

rTSeF =

Value of forward contract Forward price

No income

Known income I =PV(Income)

F=(S – I)erT

Known yield q f =S e-qT – K e-rT F = S e(r-q)T

Commodities f=Se(u-y)T- Ke-rT F=Se(r+u-y)T

rTKeSf −−=rTKeISf −−−= )(

Derivatives 02 Pricing forwards/futures |24 2/02/11

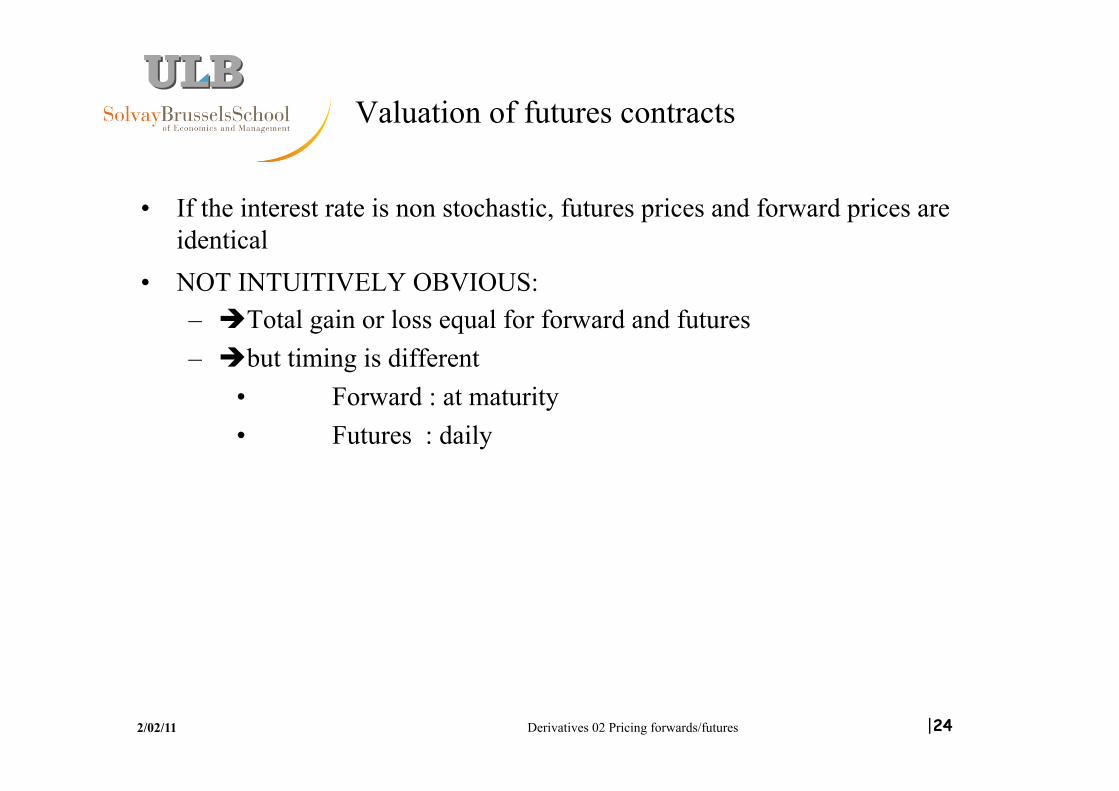

Valuation of futures contracts

• If the interest rate is non stochastic, futures prices and forward prices are identical

• NOT INTUITIVELY OBVIOUS: – èTotal gain or loss equal for forward and futures – èbut timing is different

• Forward : at maturity • Futures : daily

Derivatives 02 Pricing forwards/futures |25 2/02/11

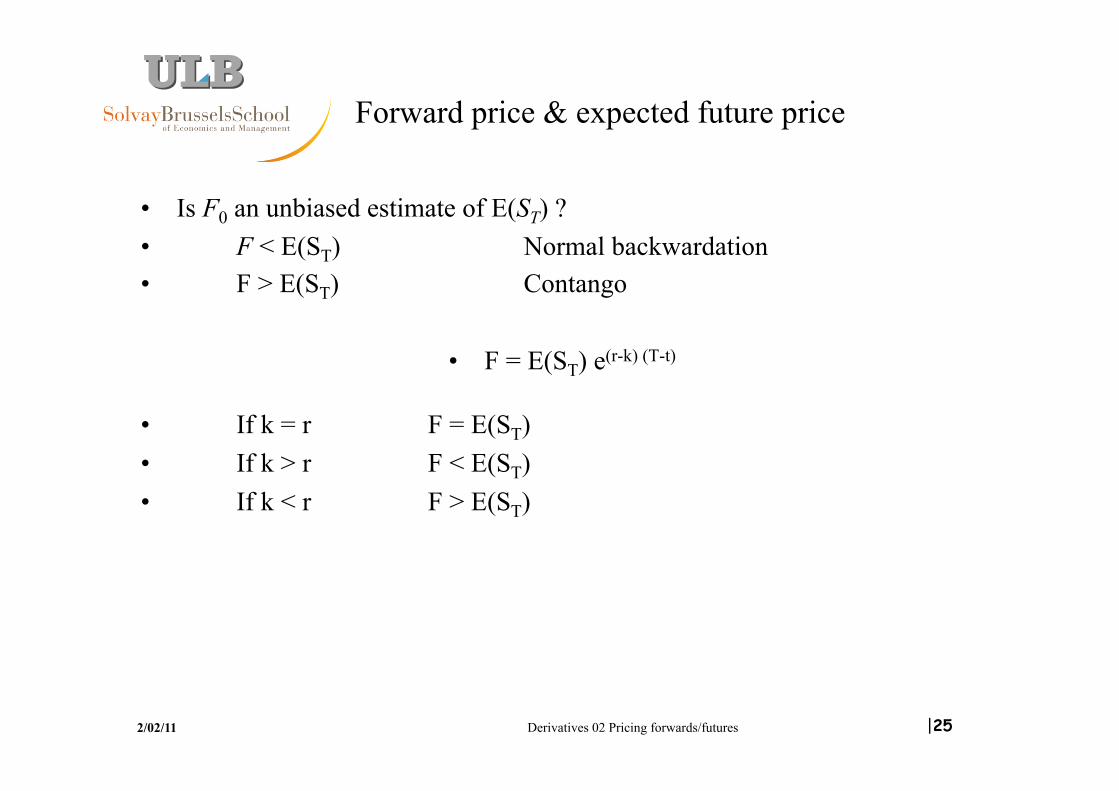

Forward price & expected future price

• Is F0 an unbiased estimate of E(ST) ? • F < E(ST) Normal backwardation • F > E(ST) Contango

• F = E(ST) e(r-k) (T-t)

• If k = r F = E(ST) • If k > r F < E(ST) • If k < r F > E(ST)