Embed Size (px)

Citation preview

Designed for Growth: Taxation and Productivity

CHAPTER 2 OF THE APRIL 2017 FISCAL MONITOR

PETERSON INSTITUTE FOR INTERNATIONAL ECONOMICS

APRIL 13, 2017

Outline

Motivation

Gains from reducing resource misallocation

How much can we expect from tax policy and revenue

administration?

Conclusion

Motivation

3

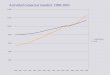

Raising productivity is a top challenge

-3

-2

-1

0

1

2

3

1990 1995 2000 2005 2010 2015 1990 1995 2000 2005 2010 2015 1990 1995 2000 2005 2010 2015

Growth in Total Factor Productivity, 1990―2016

(Five-year average growth rate, percent)

1. Advanced Economies 2. Emerging Market Economies 3. Low-Income Developing Countries

Source: Adler and others 2017.

Note: Group averages are weighted using GDP at purchasing power parity.

By pushing out the technology

frontier (April 2016 FM)

By narrowing the productivity

gap between firms (this FM).

How can fiscal policy help?

Source: Dabla-Norris and others (2015)

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

75

77

79

81

83

1983-93 1990-00 1997-07

TFP Frontier Growth Rate

(percent)

Average TFP Level

(percent of frontier)

Advanced economies: Stochastic Frontier Analysis,

by Country-Sector

Gains from reducing resource misallocation

6

Economy without Resource Misallocation

How does misallocation hurt productivity?

Sources: Dias, Marques, and Richmond 2014

wage wage

Share of workersA Share of workersB

Share of workersA + Share of workersB = Total workers

Marginal Product

of LaborA * PriceA

Marginal Product

of LaborB * PriceB

Economy with Resource Misallocation

How does misallocation hurt productivity?

Marginal Product

of LaborA * PriceA

Marginal Product

of LaborB * PriceB

(1+taxA) * wage

(1+taxB) * wage

Share of workersA + Share of workersB = Total workersSources: Dias, Marques, and Richmond 2014

Share of workersA Share of workersB

Deadweight Loss from Resource Misallocation

How does misallocation hurt productivity?

Lost production due to

misallocation

Sources: Dias, Marques, and Richmond 2014

Marginal Product

of LaborA * PriceA

Marginal Product

of LaborB * PriceB

(1+taxA) * wage

(1+taxB) * wage

Share of workersA + Share of workersB = Total workers

Share of workersA Share of workersB

What does misallocation look like?

0

4

8

12

16

20

24

28

32

0.0

3.0

6.0

9.0

12

.0

15

.0

18

.0

21

.0

24

.0

Pe

rce

nt o

f firm

s

Firm revenue productivity

More efficient country

Less efficient country

Distribution of Firm-Level Revenue Productivities

Sources: ORBIS; and IMF staff estimates.

Note: The figure shows the distribution for firms in the manufacturing sector for each country. More (less) efficient country is defined as a country at the 75th (25th) percentile of the distribution of

resource allocation efficiency, based on the ORBIS sample.

0

5

10

15

20

25

30

35

40

-2.6

-1.8

-1.0

-0.2

0.6

1.4

2.2

3.0

Perc

ent of firm

s

Log of firm revenue productivity scaled by corresponding country-industry average

What is at stake?

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

AEs EMEs LIDCs

Re

al G

DP

gro

wth

(p

erc

en

t)Estimated Annual Real GDP Growth Effects from Reducing Resource Misallocation

Sources: ORBIS; World Bank, Enterprise Surveys; and IMF staff estimates.

Note: The figure shows medians across country groups. Estimates are computed based on the assumption that the other sectors could achieve TFP gains similar to those estimated for

the manufacturing sector and that there are no adjustment costs. AEs = advanced economies; EMEs = emerging market economies; LIDCs = low-income developing countries.

Adds

1% to

real

GDP

growth

How much can we expect from tax policy and revenue administration?

12

Upgrading the tax system reduces misallocation

Selection of tax distortions that discriminate across:

1. Capital asset types

2. Sources of financing

3. Formal and informal firms

4. Small and large firms

13

Reducing these

distortions can add

¼ percent to annual

real GDP growth in

developing countries

1. Tax Distortions across Capital Asset Types

14

Developing Countries: Machinery as a Share of Total Assets,

by Industry (Percent of total assets)

Sources: Oxford University Center for Business Taxation; World Bank, Enterprise Surveys; and IMF staff estimates.

Note: Tax disparity is the effective marginal tax rate (EMTR) on machinery minus the EMTR on buildings. Countries with high (low)

EMTR disparity are those with EMTR differences above (below) the median across countries. Total assets are measured as the sum of

machinery and buildings.

40 45 50 55 60 65 70 75 80

Paper

Electronics

Nonmetallic and plastic materials

Textiles

Metals and machinery

Other manufacturing

Garments

Auto and auto components

Chemicals and pharmaceutics

Other transport equipment

Leather

Food and beverage

Wood and furniture

Countries with low tax disparity Countries with high tax disparity

Tax disparities across

capital asset types steer

investors toward lower-

return, tax-favored,

investments

2. Tax Distortions across Sources of Financing

15

Corporate debt bias

affects investment

decisions that depend

more on equity, such as

R&D

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Exte

rna

l e

qu

ity d

ep

en

den

ce

R&D Intensity

Sources: Brown and Martinsson (2016); and IMF staff estimates.

Note: R&D intensity is the average of industrial research and development expenditures normalized by vale

added across OECD countries). External equity dependence is the net external equity issues to total assets ratio

for the median U.S firm in each industry.

Advanced Economies: R&D Intensity and External Equity

Dependence, by Industry

3. Tax Distortions across Formal and Informal Firms

16

Source: WBES, and IMF staff estimates.

Note: Cheats are defined as registered firms associated with reporting less than 100 percent of their sales for

tax purposes. TFP was calculated at the firm-level, using the Levinsohn and Petrin (2004) method. EME =

Emerging market economies; LIDC = Low income developing countries.

4

4.2

4.4

4.6

4.8

5

Tax compliant Cheats

LIDCEME

Developing Countries: TFP across Tax Compliant Firms and Cheats

Tax evasion allows

“cheats” to stay in

business despite low

productivity

4. Tax Distortions across Small and Large Firms

17

Preferential tax treatment

based on size stunts firm

growth

1

2

3

4

5

<10

11

―2

0

21

―3

0

31

―4

0

40+

Ave

rag

e n

um

ber

of e

mp

loye

es (

resca

led

so

firm

s le

ss th

an

fiv

e y

ea

rs o

ld =

1)

Firm age (years)

Countries with lower tax rate for small firms

Countries without a lower tax rate for small firms

Sources: KPMG; World Bank, Enterprise Surveys; and IMF staff estimates.

Note: Lines represent the median for each group.

Developing Countries: Employment by Firm Age

What specific tax policies can help reduce misallocation?

Minimize differentiated tax treatment across assets and financing

Allowance for corporate equity (ACE); Cash Flow Tax

Level the playing field across firms

Lower tax compliance costs

Strengthen tax enforcement capacity

Target tax relief to new rather than small firms

18

Conclusion

19

To raise productivity:

Narrow the productivity gap between firms

Reducing distortions can lift annual real GDP growth rates by

1 percentage point

Developing countries can achieve ¼ of these gains by

improving the design of their tax system

Push out the technology frontier, through support to

R&D

Growth-friendly fiscal policies

Thank you!

21

22

Tax system affects long-term growth by affecting:

Allocative efficiency

Productive efficiency

State capacity

Resource misallocation arises from policies/practices that discriminate across firms:

Legislated provisions

Discretionary provisions

Market imperfections