Embed Size (px)

Citation preview

DEVELOPMENT CREDIT AUTHORITY 2004 OPERATIONS MANUAL

DCA Operations Manual

Table of Contents

Section-Page

I. BACKGROUND .............................................................................................................................................I-4 A. INTRODUCTION TO THE OPERATIONS MANUAL............................................................................................. I-4 B. DCA OVERVIEW ........................................................................................................................................... I-4 C. DCA PRODUCTS ........................................................................................................................................... I-5 D. DCA GUIDING PRINCIPLES ........................................................................................................................... I-6

II. PROJECT DEVELOPMENT...................................................................................................................... II-7 A. OVERVIEW ...................................................................................................................................................II-7 B. CONCEPT PAPER...........................................................................................................................................II-8

1. Writing a Concept Paper .......................................................................................................................II-8 2. Reviewing a Concept Paper...................................................................................................................II-9

C. ACTION PACKAGE........................................................................................................................................II-9 1. Action Memorandum..............................................................................................................................II-9 2. Project Information Sheet ....................................................................................................................II-10 3. Activity Description .............................................................................................................................II-11 4. Economic Viability Analysis ................................................................................................................II-11 5. Financial Viability Analysis.................................................................................................................II-12 6. Fee Justification...................................................................................................................................II-22 7. Legal Terms and Conditions ................................................................................................................II-23 8. Risk Assessment ...................................................................................................................................II-24 9. Subsidy Cost Calculation.....................................................................................................................II-24 10. Monitoring Plan...................................................................................................................................II-25

D. ACTION PACKAGE FOR MULTIPLE GUARANTEES AND RE-APPROVALS......................................................II-33 E. CRB PRESENTATION & CFO APPROVAL ...................................................................................................II-33 F. GUARANTEE AGREEMENT (LEGAL) ...........................................................................................................II-34 G. FUNDS TRANSFER/OBLIGATION PROCESS..............................................................................................II-34

III. RISK ASSESSMENT............................................................................................................................III-36 IV. PROJECT MONITORING.................................................................................................................. IV-38

A. OVERVIEW ............................................................................................................................................... IV-38 B. FILING PROCEDURES ................................................................................................................................ IV-38 C. INITIAL MISSION/PARTNER CONTACT ...................................................................................................... IV-39 D. MONITORING DATABASE – CMS & REPORTS .......................................................................................... IV-39 E. UTILIZATION TARGETS -- LPGS............................................................................................................... IV-40 F. UTILIZATION FEES BILLINGS & COLLECTIONS......................................................................................... IV-41 G. CLAIMS .................................................................................................................................................... IV-41

1. Assessment and Payment of Claims ....................................................................................................IV-41 2. Trigger for Claim Audits.....................................................................................................................IV-43

H. RECOVERIES............................................................................................................................................. IV-43 I. PORTFOLIO REVIEW MEETINGS................................................................................................................ IV-43 J. RELATIONSHIP MANAGER CALLING PLANS ............................................................................................. IV-43 K. BIENNIAL REVIEWS / TRIP REPORTS ........................................................................................................ IV-44 L. SUBSIDY OUTLAYS .................................................................................................................................. IV-44 M. SUBSIDY RE-ESTIMATES .......................................................................................................................... IV-46

1. Overview .............................................................................................................................................IV-46 2. Process................................................................................................................................................IV-48

N. URBAN ENVIRONMENTAL (UE) & ISRAEL CREDIT PROGRAMS TRACKING................................................ IV-49 1. UE/HG Program.................................................................................................................................IV-49

DCA Operations Manual April 2004 I-2

2. Special Israel Guarantee Programs....................................................................................................IV-50 V. PROJECT CLOSE-OUT............................................................................................................................ V-52

A. FINAL REPORTS/FEES................................................................................................................................ V-52 B. CLAIM PAYMENTS..................................................................................................................................... V-52 C. SUBSIDY DE-OBLIGATION......................................................................................................................... V-52 D. PROJECT EVALUATION.............................................................................................................................. V-53

VI. PROJECT ADJUSTMENTS................................................................................................................VI-53 A. SUBSIDY MODIFICATIONS ........................................................................................................................ VI-53

1. Purpose ...............................................................................................................................................VI-53 2. Process................................................................................................................................................VI-54 3. Resources ............................................................................................................................................VI-55 4. Modification Responsibilities..............................................................................................................VI-56

B. SUBSIDY DEOBLIGATIONS........................................................................................................................ VI-57 VII. ACRONYMS ....................................................................................................................................... VII-59 VIII. GLOSSARY OF TERMS ..................................................................................................................VIII-60

DCA Operations Manual April 2004 I-3

I. Background

A. Introduction to the Operations Manual This manual provides the USAID Office of Development Credit (EGAT/DC) with guidance on standard operating procedures among its teams – Project Development (PD), Portfolio Management (PM), Risk Management (RM) – and other staff for Development Credit Authority (DCA) guarantees. The DCA Operations Manual is not a stand-alone document. The Automated Directive System (ADS) comprises USAID’s official, written guidance on policies, operating procedures, and delegations of authority for conducting USAID business. ADS No. 249 (http://www.usaid.gov/pubs/ads/200/249.doc) provides specific guidelines to the policies and procedures of DCA. Based on the policies outlined in the ADS No. 249, two manuals have been produced to further detail internal guidelines for DCA projects. The DCA Operations Manual provides EGAT/DC and USAID Missions and Bureaus with a set of standard operating procedures for DCA, while the USAID Development Credit Risk Assessment Handbook details how to assess DCA credit risk. Additional reference materials that guide the EGAT/DC activities will also be referenced in this manual, e.g., Office of Management and Budget (OMB) circulars, other ADS sections.

This manual focuses primarily on DCA guarantees. However, EGAT/DC also maintains certain responsibilities for the management of the Micro and Small Enterprise Development (MSED), Urban Environment (UE), and Israel credit portfolios. These responsibilities will also be described in this document.

B. DCA Overview

Authorized by Congress in FY1998 and certified by OMB in FY1999, the Development Credit Authority (DCA) provides overseas USAID Missions1 with a tool by which they may encourage the use of credit and expand financial services in underserved markets. This Authority, supported by the USAID Office of Development Credit, allows USAID Missions to partner with local lending institutions in making resources available for investments that support development objectives. Through DCA, Missions insure a portion of the risk with the lending institutions. As a result, a small amount of USAID development assistance funding facilitates the local banking sector and other sources of private capital to take on projects that otherwise would not be funded. DCA seeks to provide USAID with the flexibility to make more rational choices about appropriate financing tools - loans, guarantees, grants or a combination - used in project development. DCA is not a separate program, but rather a financing account similar to Development Assistance (DA), Economic Support Fund (ESF), or Support for East European Democracy (SEED). Credit projects offer several distinct and attractive advantages over other forms of assistance:

1 Throughout this manual, a “Mission” is identified as the USAID operating unit that can originate and develop a DCA project. Regional and technical USAID Bureaus can also develop DCA projects; Missions are solely identified to simplify this document.

DCA Operations Manual April 2004 I-4

• Access to local private capital – there is a large reserve of untapped capital in the private sector, which presently is not available to certain sectors and markets. The use of credit guarantees can provide the security to make that capital available for projects to develop key sectors and financial markets.

• Risk is shared to encourage lending - DCA guarantees cover up to 50% of a lender’s risk in providing financing and are often coupled with training and technical assistance designed to strengthen local financial institution’s long term interest in local credit markets, beyond DCA’s support.

• Mobilization of local private capital – credit guarantees encourage local market participants to utilize private capital to develop activities that may otherwise be cost-prohibitive or infeasible due to lack of access to financial markets or resistance in lending by financial institutions.

• Benefits of credit demonstrated (the “demonstration effect”) - as guaranteed loans demonstrate profitability, benefits of such lending are demonstrated to the guaranteed party and local financial institutions are more likely to expand financial services to traditionally underrepresented economic sectors and social groups that are the beneficiaries of guaranteed loans. Also, the partial credit guarantee leaves the guaranteed lender with real risk and an incentive to undertake thorough due diligence and careful monitoring of the loan. This process enables the guaranteed lender to develop its internal capacity for profitably making similar loans in the future.

• Agency resources are maximized - USAID can leverage up to 25 times the per-dollar-impact by using credit to finance development activities.

C. DCA Products

Private sector resources can be mobilized in many ways through a number of appropriate financial instruments available under DCA. The four DCA credit tools available to Missions are described below. The use of these instruments can be modified and tailored to address a particular project’s financing needs. Loan Guarantee The typical Loan Guarantee (LG), also referred to as a project-specific guarantee, allows USAID to use DCA for specific credit enhancement purposes in cases where the borrower, lender, and uses of loan proceeds are known. Loan Portfolio Guarantee A Loan Portfolio Guarantee (LPG) provides financial institutions with partial coverage on a portfolio of loans that they provide to their customers. In the case of the LPG, USAID agrees to share in the risk of a broadly defined category of bank loans with a view toward inducing local banks to extend credit toward an underserved sector. The individual borrowers under a LPG are not predetermined at the time the Guarantee Agreement is signed, but the borrowers must fall within a pre-agreed definition of “Eligible Borrowers,” such as borrowers that are small businesses operating in a specific geographic area. Bond Guarantee Bond Guarantees (BG) support the issuance of bonds by financial institutions, private sector corporations, or sub-national entities. The funds generated from the bond issuance can, for example,

DCA Operations Manual April 2004 I-5

assist in raising local funds to initiate municipal infrastructure or utility projects, which require substantial upfront capital investments. The Bond Guarantee or guarantees for other types of debt instruments2 are typically an option for DCA credit assistance if the capital and financial markets are fairly well advanced in a particular country to support a bond issuance. However, the DCA guarantee can also be used to encourage the development of bond issuances in less sophisticated markets. Portable Guarantee Slightly different than the Loan Guarantee, the Portable Guarantee (PG) provides an identified potential borrower with a letter of guarantee commitment through which the borrower may seek the most advantageous terms from the local financial market. Portable Guarantees are appropriate for specific credit enhancement purposes when the borrower is known, but the lender is not yet known. In these cases, a minimum credit rating (e.g., from rating agencies such as Standard & Poor’s and Moody’s) is established, and the risk calculation and subsidy cost are based on the assumption that the eventual lender will have a rating equal to or above this minimum rating.

D. DCA Guiding Principles Following is an abridged version of the DCA guiding principles as detailed in the ADS 249. Refer to this section of the ADS for more information.

• DCA is principally intended for credit enhancement purposes and may be used where (a) the Agency's sustainable development objectives may best be achieved effectively using credit, and (b) the risks of default may be reasonably estimated and managed.

• DCA is not a separate program, but rather a financing tool to be used in addition to or in lieu of grant funding where appropriate. Accordingly, the principles and policies applicable to the use of Development Assistance (DA) grant funding are presumed to be equally applicable to DCA funding, unless otherwise indicated.

• DCA loan guarantee agreements will be utilized only when the partner is a non-sovereign entity. For any sub-sovereign government entity involved in a DCA guarantee, e.g., municipalities, the entity must demonstrate strong financial discipline and management.

• DCA shall be a demand-driven initiative, with Operating Units having primary responsibility for designing, authorizing, and implementing activities in support of approved Strategic Objectives and within Administration and Congressional priorities for assistance.

• DCA operations require a clear separation of responsibility for assessing the developmental soundness and the financial soundness of each activity, with the latter responsibilities entrusted to the Credit Review Board (CRB) and the Chief Financial Officer (CFO).

• DCA requires true risk sharing. For loan guarantee transactions, USAID shall not cover more than 50% of a lender's risk unless the CRB otherwise approves.

• DCA financing shall not be used unless it is probable that the transaction would not go forward without it, taking into consideration whether such financing is available for the term needed and at a reasonable cost.

• DCA assistance shall be made at or near market rates. Direct loans shall be made at or above the U.S. Treasury cost of borrowing for comparable maturities.

2 “Other debt instruments” include (for example): securitizations, structured finance arrangements that involve several tiers or layers of various investment classes.

DCA Operations Manual April 2004 I-6

• DCA fees shall be based on risk with higher risk activities being charged higher fees to the extent feasible, taking into consideration the costs of the development conditionality imposed on the activity.

• Currency mismatches are discouraged. Currencies earned by DCA activities should match the borrowers' liabilities.

• DCA is intended to produce greater development impact and increase Agency performance as reported under the Government Performance and Results Act (GPRA). DCA is not intended for budget support or to increase the nominal assistance levels to specific borrowers.

• DCA is intended to be used in USAID presence countries in support of Agency Strategic Objectives and in support of Mission-financed policy and institutional reforms. DCA is also appropriate for use as part of an exit strategy in countries where USAID assistance is being phased out.

• DCA is intended to address market imperfections. Activities eligible for DCA financing shall have positive financial rates of return.

II. Project Development

A. Overview The EGAT/DC Project Development (PD) team is responsible for coordinating the development of new DCA guarantees with Missions or other USAID operating units. In many cases, the PD team will respond to Mission ideas on projects that could benefit from a DCA guarantee. In other situations, the PD team can also pursue a more proactive approach by contacting Missions to encourage the development of a DCA guarantee. EGAT/DC PD team support can also include: 1. Meeting with local financial institutions to explore possible links between lending activities and Missions Strategic Objectives (SOs), and 2. Brainstorming with Mission staff about potential ideas of how DCA can help the Mission achieve its SOs. The principal characteristics of this initial idea should be summarized in a “Concept Paper”. Following EGAT/DC review of this Concept Paper to ensure the proposed idea adheres to ADS 249 guidelines (http://inside.usaid.gov/EGAT/off-dc/ads-249_summary_checklist.pdf), the Mission and PD team will develop the Action Package to be presented to the Credit Review Board (CRB). At the same time, the Regional Legal Advisor drafts the basic terms and conditions of the legal agreement based on existing templates from the USAID Office of General Counsel. Upon completion of a significant portion of the Action Package, the EGAT/DC Risk Management (RM) team prepares the risk assessment, which is detailed in Section III of the Operations Manual and results in the calculation of the subsidy cost estimate. The risk assessment is the last section of the Action Package to be completed prior to CRB review. Following the CRB’s recommendation for CFO approval of the subsidy cost, funds are transferred to the DCA account according to federal government procedures to be obligated at the Mission level through the signing of a legal agreement. Further guidance on how a DCA project is developed can also be found in the 10-Step Guide to Preparing a DCA Project (http://inside.usaid.gov/EGAT/off-dc/index.html). The process, when all relevant parties, e.g, the Mission and the lending institution, are committed to the guarantee, should take no more than four to six months from the Concept Paper stage to the signing of guarantee agreement.

DCA Operations Manual April 2004 II-7

B. Concept Paper

1. Writing a Concept Paper A Mission identifies an opportunity to use credit to support one or more of its strategic objectives and/or ongoing activities. As the idea is developed, the Mission is encouraged to communicate with the EGAT/DC PD Team to obtain technical guidance related to credit tools/projects. Missions should take advantage of EGAT/DC institutional knowledge to consider lessons learned from previous DCA projects. To summarize this project idea, the Mission prepares a 2-3 page DCA Concept Paper using the following recommended outline. This step in the process, although not a requirement for ultimate project approval, can be extremely beneficial to the Mission prior to spending significant time and effort on the subsequent steps.

a) Description and Purpose of Project • Background and Rationale (briefly describe what the Mission proposes to do and why) • Developmental Importance • Relationship to Mission Strategy/SOs/Ongoing Activities • Collaboration with Other Parties, e.g., Donors, NGOs, Contractors, etc.

b) Structure of Project • Financial Intermediary (provide brief background, if available) • Borrower (provide brief background, if available) • Intended Beneficiaries (if different from borrower, if available) • Type of Credit Facility (loan guarantee, bond guarantee, portfolio guarantee, portable loan

guarantee) • Estimated Amount of Project Financing (maximum portfolio size - US$ amount) • Guarantee Ceiling (maximum USAID contingent liability -US$ amount) • Guarantee Percentage (%) (covering principal only [preferred] or principal and interest) • Term of Guarantee (number of years) • Currency of Guarantee (US$ or local currency)

c) Funding Source and Amount Available for DCA Credit Subsidy (Proposed funding transfers from existing budget resources)

d) Management Responsibility • Initial project monitoring plan • Clear identification of parties responsible for project development and implementation

e) Proposed Technical Assistance to support the DCA guarantee

f) Estimated Time Frame for Project Implementation

DCA Operations Manual April 2004 II-8

2. Reviewing a Concept Paper The Mission and EGAT/DC PD team should adhere to the following guidelines to ensure the proposed DCA guarantee adheres to ADS 249 guiding principles: http://inside.usaid.gov/EGAT/off-dc/ads-249_summary_checklist.pdf. If EGAT/DC considers the proposed project extremely risky, it will discuss the Concept Paper and provide technical feedback to the Mission. Consequently, the Mission may engage in efforts to restructure the proposed guarantee to reduce these perceived risks or it may abandon the project at this stage. The EGAT/DC PD team Relationship Manager may decide to convene a meeting to review the Concept Paper among EGAT/DC staff in order to provide feedback to the Mission as it further develops the idea and begins to prepare the Action Package. The Relationship Manager should summarize the feedback from this meeting in an email to the Mission contact person. Once internal Mission approvals for the Concept Paper are in place, work can begin on the Action Package.

C. Action Package Unless otherwise noted, the Action Package is the responsibility of the Mission in coordination with the EGAT/DC PD team. This document can also be developed in conjunction with Mission contract support.

1. Action Memorandum The template of this memorandum is presented in the following diagram and it is available on the USAID intranet – http://inside.usaid.gov/EGAT/off-dc/forms-tools.htm. The EGAT/DC PD team ensures that the memorandum is properly updated with the appropriate names of the USAID CFO and the CRB Chair. Prior to submitting the Action Package to the CFO, signatures of the Mission Director and the CRB Chair are necessary. The Mission should also ensure that its Regional Legal Advisor (RLA) and Controller are aware of the Action Package.

TO: [Name], Chief Financial Officer FROM: [Name], Chairman of the Credit Review Board SUBJECT: CRB Recommendation for [Approval] of Development Credit Authority Activity in

[Country] As described in the attached documents, USAID/[Mission] intends to sign a [bond/loan] guarantee agreement with [guaranteed party] in [country] in support of the Mission’s [Strategic Objective.] To successfully implement this agreement, USAID/[Mission] agrees to adhere to its Monitoring Plan responsibilities as outlined in this document. The Credit Review Board has reviewed this transaction and found that the risk has been appropriately assessed and that there is reasonable assurance of repayment of the obligations covered by these guarantees. Furthermore, the CRB has approved the subsidy cost to be associated with this activity and believes the Office of Development Credit has adequately provisioned for the risk entailed in this prospective agreement. RECOMMENDATION That the CFO sign below and thereby approve the findings of the Credit Review Board and the recommendation of the Chairman of the Credit Review Board with regard to this activity. (approvals by CFO and Mission Director)

DCA Operations Manual April 2004 II-9

2. Project Information Sheet The Mission with assistance from the EGAT/DC PD team will complete the following Project Information Sheet template, with the exception of risk assessment data, which is an EGAT/DC RM team responsibility.

Project Identifier: [Shorthand identifier for the activity, e.g., the name of the primary counter-party] Country Mission/Bureau Mission/Bureau Program Officer

Fin. Viability Analyst

ODC Relationship Officer Credit Analyst Concur: Chief Risk Officer Kathleen Wu Type Guarantee Number Lender(s) /Guaranteed Party

Borrower(s) Mission SO(s) Supported by Activity Sector Activity Description

Performance Indicators (Please provide a list of key measures of the benefits and performance of this activity)

Max. Cum. Disbursements ($) Guarantee currency Term (years) Type of Risk sharing Interest Rate (%) Guarantee

percentage

Revolving? Guarantee ceiling ($) Initial Disbursement (year) Payment guaranteed Notes on Transaction Terms

Commitment Fee ($) Utilization Fee (%) p.a. Util. fee payment Basis NPV ($)

For Loan Portfolio Guarantees (LPGs) For Bond Guarantees Est. number of sub loans Type Est. avg., sub-loan maturity (years) Coupon (%) Est. avg. size of sub-loans ($) Trustee Max. auth. Portfolio Amount ($) Investors Secondary

Investors

DCA Operations Manual April 2004 II-10

Subsidy

Cost $ % Net Defaults Fees Nom.

Defaults

Funding Source/FY

WARF Score Country (%) Borrower (%) Lender (%) Transaction (%) Key Risk Factors: Brief list of key factors (e.g., nature of the lending activity, specific management

concerns, sectoral concerns, etc.) Special conditions for approval:

3. Activity Description The Activity Description section outlines the structure of the proposed DCA guarantee. The Mission typically includes a description of the developmental objective of the activity – i.e., how the proposed activity and its expected outcomes will contribute to current or new Strategic Objectives (SOs). New intermediate results and indicators may be developed for the proposed DCA activity, as deemed appropriate and necessary by the Mission. The Mission writes the Activity Description, borrowing from the Concept Paper. The Activity Description is not submitted to the Credit Review Board for approval; however, it is included in the Action Package for reference purposes.

4. Economic Viability Analysis The Economic Viability Analysis (EVA) is the assessment of an activity in the context of the host country’s economy. In essence, this analysis justifies the utilization of the DCA guarantee in light of the economic and market factors relevant to the proposed activity. In other words, the EVA reviews USAID’s role in the DCA transaction and the value added by the guarantee. The analysis should discuss how USAID’s proposed guarantee is unique and necessary in this market, why USAID is not “crowding out” the private sector or duplicating the efforts of other donors in this initiative, and why the type of financing to be provided through the guarantee is not otherwise available in the market to the target group of borrowers. In short, the EVA should determine whether the proposed DCA activity is worthwhile for the country/region, and as appropriate, assess the activity’s impact in light of economic costs and benefits to the host country. In addition to a brief justification of the guarantee with respect to the economic conditions of the host country, two specific points should be addressed in the EVA:

DCA Operations Manual April 2004 II-11

• Market Imperfections: The activity will address in-country market imperfections. • Additionality: The DCA credit instrument will not supersede private sources of financing and

USAID is a guarantor/lender of last resort in such a way that the activity would not be possible without DCA. This is referred to as “additionality”, which implies that the guaranteed party would not extend the loan to the beneficiary without the DCA guarantee.

In-country Market Imperfections This component of the EVA addresses the overall conditions of the sector impacted by the potential DCA activity. The term “market imperfections” implies that the supply generated by market participants is insufficient to meet the demands of market customers. Market imperfections may also refer to specific barriers that discourage or prevent the entry of new approaches, e.g., renewable energy, microenterprises, and municipal infrastructure, into an existing market scheme. A common manifestation of these barriers is limited access to capital, represented by a banking sector’s unwillingness to lend to a new approach or a new sector. This unwillingness often stems from a lack of historical references for repayment abilities or unavailable or asymmetric information, as well as overly-cautious lending practices. In this regard, the EVA should address how the DCA credit instrument will help overcome some of these barriers, which currently limit market-based lending to the proposed project/sector. Additionality The DCA guarantee credit product should not displace the demand for capital and debt financing that could be fulfilled from private sector resources. This can be justified by confirming that the overall commercial banking sector is unwilling or extremely hesitant to lend funds to a particular sector and/or borrower on loan terms and conditions comparable to other borrowers, e.g., loan tenor. Furthermore, the EVA can indicate if the banking sector charges exorbitant interest rates or requests excessive collateral due to the perception of high risk towards this sector. The EVA highlights how the use of DCA extends credit to a project based on its actual risks, not its perceived risks. In this sense, DCA intends to be a catalyst, providing demonstration effects to more properly align the host country financial sector’s perception of risk with actual project risks in a certain sector. For example, the EVA could describe how the DCA guarantee intends to result in a decline in collateral requirements for a particular borrower. The borrower would then be in a position to demonstrate an ability to re-pay its debt and establish a favorable credit history; thereby eventually having the impact of lowering a bank’s perception of the borrower’s risk. Discussions with financial institution representatives related to a DCA proposal should confirm that the DCA guarantee provides an increased level of confidence from their perspective to facilitate the credit to the project. Without the DCA guarantee, financial institutions would be unwilling to lend to the borrower. In other words, the EVA must provide evidence that the involved or identified financial institution(s) would not extend credit to the activity if it were not for the DCA guarantee. In the case of a portable guarantee, the potential borrower should confirm that DCA will be the unique factor to enable the project/sector to benefit from fair, market-based debt financing.

5. Financial Viability Analysis The Financial Viability Analysis (FVA) is an assessment of the adequacy of a project’s or an activity’s financial return for the borrower(s) and/or the lender(s). Generally speaking, DCA assistance (and

DCA Operations Manual April 2004 II-12

USAID economic assistance) should be targeted toward sectors that are competitive or hold the promise of being competitive if the requisite reforms are undertaken. More specifically, as a reflection of the sustainability of economic activity in the sector, an activity should be funded under DCA only if the borrower is able to pay its operating and maintenance costs and financial obligations, including loan principal and interest payments. Likewise, the activity should be sustainable (i.e., capable of generating adequate rate of return) for lenders or investors as well. In the absence of these two conditions, the Mission or Bureau should reconsider the appropriateness of credit as a development tool for this specific project. The FVA is a quantitative determination of whether the proposed DCA project or activity is likely to yield a positive financial rate of return for borrowers and partner financial institutions (lenders) or investors. In other words, based on expected cash flows, the FVA:

• Assesses the ability of the borrower(s) to meet its financial obligations and service the debt related to the activity, and

• Ensures that the activity is unlikely to generate losses for the lender or investors. To do this, the FVA thoroughly examines the cash flows of the project or activity over the lifetime of DCA assistance and analyzes rates of return appropriate for the endeavor. Since the project or activity must be examined for both the borrower and the lender, there are in fact two analyses. The analyses are summarized at the end through calculation of the net present value (NPV) of the project or activity for both the borrower and the lender, along with calculations of its internal rate of return (IRR) for each. Although there are two types analyses (borrower or lender), it is necessary to complete only one, depending on the DCA project being considered. As a general rule, the financial viability analysis must be performed for the component of the activity where the developmental benefit of the activity is focused. For example, the developmental purpose behind most loan portfolio guarantees covering small or micro business loans is to increase access to credit for that sector. For the primary developmental effect (increased lending to small businesses) to be sustainable, such lending must be financially viable for the lender. Thus, for such a project, the FVA will cover the financial viability of the project from the lender’s perspective. While the Mission will need to gather some information related to the profitability of businesses within the targeted sector (this information will inform estimates of the risk--and thus the returns required by lenders), the primary focus of the FVA will be on the lender. For loan portfolio and lease portfolio guarantees to multiple borrowers, the lender viability analysis is generally more important than the borrower viability analysis. For loan guarantees and bond guarantees to single borrowers where the developmental purpose behind the activity is more closely related to the borrower’s activities (e.g., a loan guarantee for a borrower who is introducing new innovative technologies to a market), the borrower viability analysis is substantially more important than the lender viability analysis. The length and coverage of the financial viability analysis is left to the discretion of the analyst. FVAs can range from two to 20 pages depending on the quantity and quality of information available to the analyst and the complexity of the project and guarantee facility. The analyst should provide a brief discussion of the issues raised below based on the relevancy to the project in question. In many cases, a brief description of the key forecasting assumptions followed by presentation of simple cash flow projections will suffice. Missions should contact EGAT/DC with any questions regarding the scope and necessary level of detail of a FVA. Generally, Missions often find that after preparing an initial outline of the FVA, the EGAT/DC PD Relationship Manager can offer useful guidance that helps focus

DCA Operations Manual April 2004 II-13

the analysis and thus reduce the amount of work involved. As such, we encourage each Mission to contact its Relationship Manager as it begins to work on the FVA. Note that the focus of the FVA is on the project or activity, as opposed to the overall operations of the borrower(s) or lender(s). This narrow focus provides for a determination as to whether the direct sources of repayment for the loan are adequate to cover the borrower’s obligations and provide profits for the lender. In other words, the narrow focus assesses whether the project or activity is operationally sustainable on an incremental basis; in economic terms, the project or activity would thus be profitable “at the margin.” The credit risk assessment will separately consider other aspects of the overall operations of the borrower(s) and the lender(s), since there are also indirect sources of repayment for the loan (for example, from existing ongoing business activities). In most instances, however, the new activity is closely related to the existing activities of the borrower(s) and the lender(s). Cash flow projections and calculations of rates of return for the new project or activity would thus be appropriately based on historical cash flows and rates of return for the borrower(s) and lender(s), so careful attention to past years’ audited financial statements is required. In instances where the new activity is not similar to the existing activities of the borrower(s) or lender(s), attention must be focused on the assumptions underlying the new activity to generate the cash flows and rates of return. These issues are discussed in more detail in the next three sections on activity viability for the borrower, activity viability for the lender, and discount rates. Additional general guidance for the FVA is provided in the final part of this section or can be obtained from EGAT/DC relationship managers.

a) FVA Part I – Activity Viability for the Borrower Calculating borrower financial viability involves determining the estimated sources and uses of cash required by the activity. Simply put, viable activities are characterized by projected revenues that exceed projected operating costs and investment expenditures. Once the revenue and cost streams have been estimated for the length or term of the repayment of the borrowed funds, the cash inflows and outflows are compared to determine whether the proposed activity generates adequate income to support anticipated debt service and issuance. There are two main types of loan guarantee projects – those for single borrowers (e.g., loan guarantees, portable guarantees, and bond guarantees) and those for multiple borrowers (e.g., loan portfolio guarantees and lease portfolio guarantees). The data collection and analysis required will vary significantly between these two categories. Single Borrowers In the case of guarantees provided for a single project or company, i.e. loan guarantees, portable guarantees, and most bond guarantees, the financial viability assessment should focus primarily on the borrower’s ability to repay and service the debt. In most circumstances, the focus is on the new activity being financed, and borrower viability should analyze the cash flows associated with the new project. This is clearly the case for “project finance” which has no recourse to cash flows or assets outside the project. (Project finance is addressed in additional detail below.) It is also typically sufficient to examine the cash flows associated with the new activity even when the loan has recourse to cash flows and assets outside the projects, as long as the project cash flows analyzed:

DCA Operations Manual April 2004 II-14

• are based on the historical performance of the borrower’s existing projects, under the assumption that the borrower’s past performance best represents its future performance, and

• fully consider the impact on the other cash flows of the borrower (which is the issue of incremental cash flows developed below).

Recall that while the credit analysis of the project will take such alternative sources of repayment into account, the project or activity should be sustainable on a stand alone basis. One exception to this rule, for example, is for municipal borrowers, which are often forced to cross-subsidize activities due to market imperfections related to tax authority and customers’ willingness to pay for municipal services. Obtaining project/company information/projections. Prior to conducting the assessment itself, the analyst must obtain project or company information and projections regarding future performance. Most borrowers should be able to present financial statements (balance sheets and income statements) for the past three years as well as financial forecasts during the projected timeframe of the DCA guaranteed credit activity. Ideally, the financial statements will have been audited. At a minimum, most lenders and investors will have required borrowers to produce historical accounts of their performance as well as projections for future growth.3

OPERATING CASH FLOW COMPONENTS

Net revenue - Operating expenditures - Interest expense = Free cash flow + Increases in accounts payable - Increases in accounts receivable and

inventories - Capital expenditures required to offset depreciation = Net free cash flow - Short-term senior debt and current

maturities of senior long-term debt = Surplus or deficit

Assessment. With the appropriate financial statements and project information in hand, the analyst is ready to perform the financial viability analysis for the borrower. This assessment can be broken into four main steps.

• Step 1 – Prepare and Examine Assumptions. The most important step is to prepare and examine the assumptions which produce the numbers used in the quantitative analysis. After all, these assumptions are what give the numbers meaning. The analyst must consider how reasonable revenue growth and expense assumptions are for the project in terms of recent data and other considerations.

Generally speaking, the assessment should first examine the core assumptions that underpin growth or contraction of relevant variables (price, sales, cost, etc.) and compare these assumptions to audited historical figures. If revenues are projected to increase, for example, the analyst should examine factors such as market demand, price levels, competition, etc. The analyst should perform a brief review of each of the key variables (e.g., prices, input costs, scalability, competition, regulation). When questions arise, the analyst should provide additional information. For example, if revenues are projected to increase and

3 In some cases, however, particularly for micro- or small enterprises, such statements may not be available. In these instances, the analyst may use previous loan data and peer group analysis complemented by an assessment of the specific strengths and weaknesses of the borrower in question. In the absence of audited financial statements, however, it may not be possible to perform a risk assessment of the activity. Likewise, it is also less likely that the USAID intervention will produce a sustainable effect if it does not address questions related to information asymmetry between lender or investors and borrowers. While the DCA tool can improve problems of information asymmetry between creditors and debtor groups, and is in fact designed to do so, some instances will require upfront technical and/or grant assistance.

DCA Operations Manual April 2004 II-15

operating costs are predicted to remain fairly constant, the borrower will need to justify how it would achieve these efficiencies. Where possible, quantitative information should be used when assessing the assumptions underpinning the activity; however, it should be noted that qualitative assessments are often adequate. For example, if several reputable economic forecasters estimate strong growth in the sector in question, providing this information is sufficient. Other significant fluctuations in balance sheet and income statement line items should be identified. Again, the FVA should ensure that the projections are “reasonable” and internally consistent; e.g., a ten-fold increase of fixed assets on the balance sheet during a two-year period in the absence of a concurrent increase in depreciation-expenses on the income statement raises questions about the accuracy of the forecast.

• Step 2 – Project Free Cash Flows. Once the assumptions underpinning the projections have been vetted, cash flow projections for the project over the life of the DCA assistance can be prepared. These projections should focus on free cash flow (FCF) from operations, and should be denominated in the local currency unless the loan guarantee covers dollar debts. They should also be in nominal terms, or include the local inflation rate (or the dollar inflation rate if being denominated in dollars).

The cash flows of the project need to consider the full impact of the new project on the overall cash flows of the borrower. In other words, they need to represent all incremental cash flows to the borrower, for both revenues and costs, associated with undertaking the new activity. For example, if an expansion of an MFI is to be undertaken by opening a new office, some revenues at the new office might actually be siphoned off from established offices; the project cash flows must only consider the truly new revenues.

Denominate all cash flows in local currency unless the guarantee covers US dollar debts.

FCF is typically net revenues minus operating expenditures and interest expense. Operating expenses comprise cost of goods sold, selling and general administrative expenses, and taxes, but particularly exclude depreciation (since it is not a cash flow). Net FCF further adjusts for changes in working capital and capital expenditures required to maintain the firm’s projected productive capacity. Hence, the analyst must carefully consider the project’s working capital requirements. Working capital is essentially current assets (accounts receivable, inventory) less current liabilities (short-term debt, accounts payable). During periods of high growth, working capital cash flows are frequently negative – current assets increase significantly in comparison to current liabilities. Higher inventories and receivables represent cash outflows, while an additional short-term loan or account payable represents a cash inflow. In other words, as working capital increases, cash is used. A shortfall in cash may lead to a default regardless of the ultimate profitability of the activity. The capital expenditures required to maintain productive capacity essentially offset annual depreciation. This figure should not include cash flow from investing or financing activities (except for those expenditures necessary to maintain or meet the project’s projected productive capacity -- i.e., the loan or bond proceeds). The net FCF projections should then be compared to total debt repayment associated with short-term debt and current maturities of long-term debt on a period by period basis.

• Step 3 – Conduct Sensitivity Analysis. The sensitivity of the cash flows to changes in key

variables, such as price, sales, costs, interest rates, etc. should be tested and any significant

DCA Operations Manual April 2004 II-16

findings presented. This step is typically useful in uncovering a “worst-case scenario” and a “best-case scenario” to supplement the average or expected scenario.

• Step 4 – Discount Future Cash Flows and Calculate the Internal Rate of Return:

Lastly, the projected, future cash flows should be discounted to a present value using an appropriate “discount rate” or “cost of funds”. In addition, the projected cash flows should determine the internal rate of return for the project. The discount rate section below provides more information on determining the appropriate discount rate. This rate should be validated with the participating financial institution and/or other local banks.

Special Considerations for Project Finance: The term “project finance” refers to the raising of funds to finance a capital investment project that is separate and apart from an existing entity. Generally, project finance is limited to large-scale infrastructure projects because of the complexity and cost of structuring a project finance deal. The FVA of project finance is focused exclusively on the ability of the project activity to repay its debt obligations based solely on forecasted project cash flows, independent of whether it is a private or public sector entity. Conservative EBITDA (earnings before interest, taxes, depreciation, and amortization) cash flow projections must be sufficient to service all debt, provide for working capital, pay operating expenses, and still provide an adequate cushion for contingencies. Special Considerations for Municipalities: For municipal borrowers, the FVA will follow the steps described above with special consideration for credit repayment through “general obligation” funds (taxes and intra-government transfers) versus project-specific funds. First, the repayment history of the municipality should be examined to ensure that there is a positive track record by the municipality to repay its sovereign and non-sovereign debts. The projections collected from the municipality should be assessed with comparisons to its historical financial reports. Stability of central government transfers should also be evaluated in these forecasts. In addition, the ability of the municipality to generate and utilize its own tax and non-tax revenues as well as “unrestricted funds” that are not limited to specific programs will provide insights in the entity’s ability to re-pay liabilities. Lastly, administrative and operating budgets and expenditures should be reviewed to assess cost control measures. Much of this information will also be critical for the risk assessment of the project. Special Considerations for Grant Funding: Certain borrowers -- such as private voluntary organizations (PVOs), non-government organizations (NGOs), and microfinance institutions (MFIs) – receive part of their revenues as grant funds. Under these circumstances, the financial viability analysis must carefully consider the role of grant funding in the new project. Grants associated with the initial investments – such as purchase of real estate or equipment or for other start-up costs – may generally be included in the cash flows of the project insofar as such grants are already secured. These are often known as equity donations, as they contribute to shareholder equity in the balance sheet. However, the project must be subsequently operationally sustainable without ongoing grant funding in order to demonstrate enough financial viability to qualify for a DCA loan guarantee. Uncommitted grant funding associated with operating expenses – such as unrestricted annual donations – should therefore not be included in the cash flows of the project, as such donations are typically volatile and often distort the orientation of the project away from market and competitive analysis. Multiple Borrowers For a loan portfolio guarantee supporting many different projects, where the focus of the activity is on the general increase in access to credit for the sector, FVA should be focused on the lender. However, this analysis, as mentioned before, should briefly cover macroeconomic trends, growth estimates,

DCA Operations Manual April 2004 II-17

specific challenges, regulatory environment, management capacity (from a macro perspective), specific strengths or competitive advantages, general creditworthiness, etc. found in the borrower sector. The FVA should thus provide the CRB with an overview of the trends affecting potential borrowers and their prospects for growth. While it is not necessary to produce cash flow projections for specific borrowers in this case, Missions should provide the CRB with an example or two of these borrowers’ cash flows and/or debt repayments.

b) FVA Part II – Activity Viability for the Lender Activity viability for the lender is principally designed to ensure that a loan or lease portfolio guarantee will be applied to loan or lease activities that are profitable for the lender. The lender viability analysis follows the same principles as the borrower viability analysis. Begin by (1) analyzing the assumptions that underpin the activity, then (2) model the projected cash flows and changes in working capital, (3) evaluate the sensitivity of the project to changes in key variables, and finally (4) discount the cash flows to determine profitability. The Office of Development Credit has developed cash flow model templates for lenders. Please contact EGAT/DC can provide a template for an appropriate model. Here are some of the key inputs that should be evaluated and modeled for the purposes of determining the viability of the lending activity.

Definition of Inputs Notes Credit “Terms & Conditions” data Loan amount, Coverage percentage, Term of guarantee, Commitment fee percentage and Utilization fee percentage.

All of this information is presented in Attachment VI: Legal Terms and Conditions of the DCA Action Memorandum.

Sub-loan Maturity (Loan Portfolio Guarantees [LPGs] only)

The financial institution should verify the term of its typical loan or line-of-credit for the targeted borrower set in order to accurately estimate loan repayment schedules.

Cost of Funds Please see the following section on discount rates.

Average interest rates for deposits, loans and other liabilities should be collected during interviews with the senior management of the financial institution. Next, the weightings (percent of total value) of these debt components should be multiplied by the interest rates and then totaled to calculate a weighted average. This estimated cost of funds should be validated with senior management because data on the balance sheet may often not reflect the true current condition of a bank’s financial costs.

Client Loan Rate The estimated annual interest rate charged to the borrower(s) identified for this DCA activity.

Gather during interviews with senior management (preferably a chief loan officer) of the financial institution. This should be validated by discussions with a central bank entity and with the potential borrower(s).

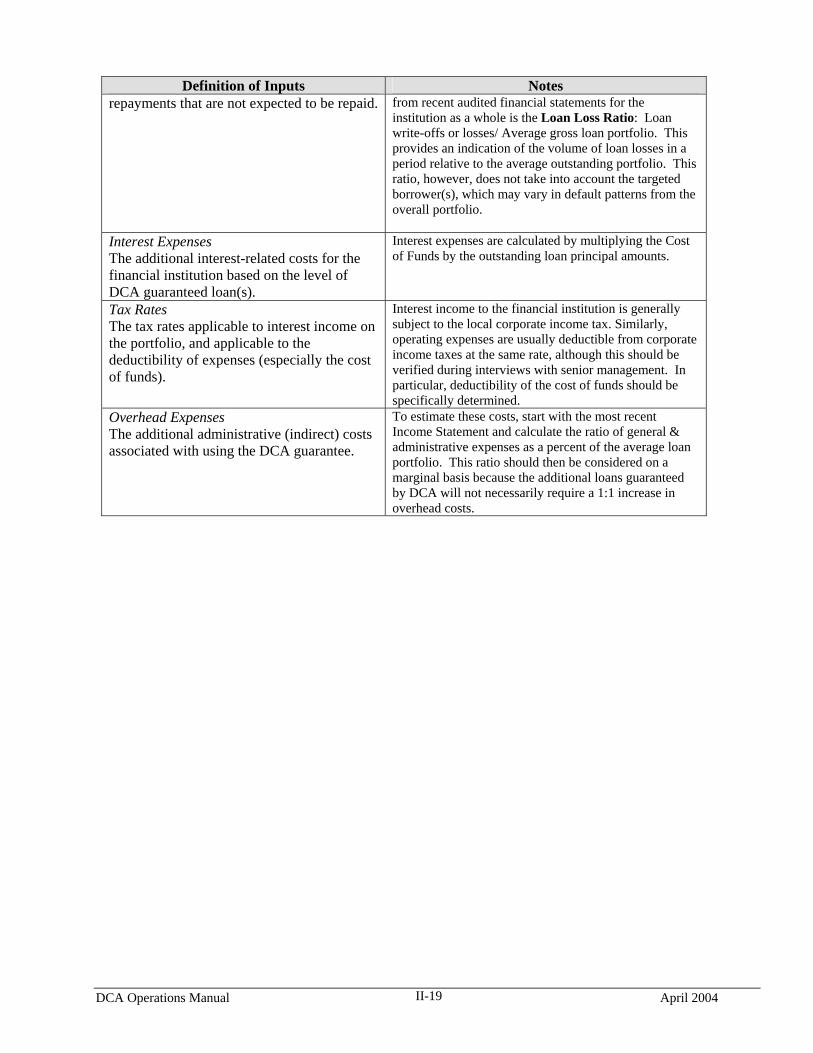

Anticipated Defaults The amount of loan principal and interest

Anticipated defaults should be based on a current default rate of loans in the targeted sector multiplied by the estimated principal repayments. An alternative measure

DCA Operations Manual April 2004 II-18

Definition of Inputs Notes repayments that are not expected to be repaid.

from recent audited financial statements for the institution as a whole is the Loan Loss Ratio: Loan write-offs or losses/ Average gross loan portfolio. This provides an indication of the volume of loan losses in a period relative to the average outstanding portfolio. This ratio, however, does not take into account the targeted borrower(s), which may vary in default patterns from the overall portfolio.

Interest Expenses The additional interest-related costs for the financial institution based on the level of DCA guaranteed loan(s).

Interest expenses are calculated by multiplying the Cost of Funds by the outstanding loan principal amounts.

Tax Rates The tax rates applicable to interest income on the portfolio, and applicable to the deductibility of expenses (especially the cost of funds).

Interest income to the financial institution is generally subject to the local corporate income tax. Similarly, operating expenses are usually deductible from corporate income taxes at the same rate, although this should be verified during interviews with senior management. In particular, deductibility of the cost of funds should be specifically determined.

Overhead Expenses The additional administrative (indirect) costs associated with using the DCA guarantee.

To estimate these costs, start with the most recent Income Statement and calculate the ratio of general & administrative expenses as a percent of the average loan portfolio. This ratio should then be considered on a marginal basis because the additional loans guaranteed by DCA will not necessarily require a 1:1 increase in overhead costs.

DCA Operations Manual April 2004 II-19

c) FVA Part III – Discount Rates With the forecasted cash flows as a basis, the Mission or Bureau should calculate two indicators to complete a Financial Viability Analysis: the Net Present Value (NPV) and the Internal Rate of Return (IRR).

Net Present Value (NPV): DCA projects must demonstrate a positive NPV, which is the present value of all cash outflows (investments) and inflows (returns) of a project at a given rate of return known as the discount rate. Since the streams of expenditures and receipts occur over a period of time, they are discounted to account for the “time value of money”,4 using the cost of funds to the borrowing or lending entity. When conducting a NPV analysis, the selection criterion is to accept DCA activities with a NPV greater than zero.

1

Internal Rate of Return (IRR): Another measure of financial viability is the IRR. IRR is the rate of return or discount rate at which the present value of an investment in a project is zero. When this IRR exceeds the cost of funds, the project is deemed to be an attractive investment. The IRR is somewhat less useful than the NPV calculation, as it is influenced by the profile of cash flows. In particular, IRR cannot be used for paths of cash flows that change sign (negative to positive or vice versa) more than once.

2

There are many issues to consider in determining the appropriate discount rate to use for calculating NPV. One is whether the discount rate is in local currency or dollars. When cash flows have been denominated in local currency, the discount rate must be a local currency rate. When cash flows have been denominated in dollars, which should be the case when the loan guarantee covers dollar debts, the discount rate must be a dollar rate. In both circumstances, data should be in nominal terms – which include inflation – since cash flows are also expressed in nominal terms. Whether analyzing the borrower or the lender, the preferred discount rate is the required rate of return on equity given the level of leverage provided by the debt. This is because the projected cash flows in the FVA use available information on the structure of the debt and include interest expenses and principal repayments as cash outflows. With the impact of debt already taken into account in the cash flows, the remaining cash flows (either positive or negative) represent the return to the equity holders. As a result, the remaining cash flows are to be discounted by the required rate of return on equity for the level of leverage provided by the debt. The required rate of return on equity is difficult to calculate. Using historical financial statements, however, the required rate of return may be approximated by the historical rate of return on equity (ROE). This is calculated by taking the earnings available to the shareholders (i.e., net of interest and taxes) and dividing by the value of equity. Furthermore, the value of equity should be the market value of equity rather than the historical value, which is easily available for publicly traded firms but not for privately held firms. The ROE should be averaged over several years in order to remove year-to-year volatility and move closer to a sustainable market equilibrium. Finally, the calculated ROE must be critically scrutinized to assure its credibility. For example, it must be higher than the interest rate on the firm’s debt, as returns to equity must be higher than returns to debt. (For financial institutions, it must be higher than the cost of funds.) It must also be sufficiently higher to compensate for the additional risks associated with equity, although the magnitude of such compensation is unknown.

4 The basic premise of the “time value of money” is that a dollar today is worth more than a dollar tomorrow due to the interest earned on today’s dollar.

DCA Operations Manual April 2004 II-20

It is also worth noting that using the historical ROE as the required return on equity presumes that the new project faces risks similar to those on already existing projects of the same firm. If the project presents wholly different risks than those presented by the borrower’s existing business, it is necessary to adjust for this risk by either adding a premium or subtracting a discount. If possible, use financial information for companies that are engaged in the projected type of business. Similarly, the required rate of return on equity will also depend on the firm’s leverage; the more highly leveraged a company, the higher the risk to equity holders and, thus, the higher the required return to equity. If the new project is roughly similar to existing projects with respect to leverage, then the calculated ROE might adequately capture the required rate of return to equity. However, if the new project significantly raises or lowers leverage of the firm, the required rate of return is somewhat higher or lower and the analyst should attempt to incorporate this change in this analysis. Since the required return on equity is difficult to calculate, some conceptual approaches are useful. The required rate of return on equity must be higher than the interest rate on debt. For financial institutions, it must be higher than the cost of funds. Hence, the simplest discount rate to use is the weighted average interest rate on debt, or, for financial institutions, the cost of funds calculated as the weighted average interest rate for deposits, loans, debt, and other liabilities. Using the weighted interest rate as the discount rate will produce a liberal estimate of the NPV, which must be positive in order for the debt to be fully serviced. This liberal estimate might be satisfactory, as it would indicate that the lenders would be compensated through their senior claims on the project even when shareholders are only minimally compensated. However, the project or activity is truly financially viable only when returns to equity can be sustained at market rates. More conservative estimates of the NPV are thus appropriate, and can be obtained by adding several percentage points to the interest rate on debt. This premium above the interest rate on debt may range from two or three points to nine or ten points, depending on the risk of the project vis-à-vis the existing business and its leverage. The analyst is urged to consider several different discount rates within this range as a way of performing sensitivity analysis on the calculated NPV.

d) FVA Part IV – Guidance for Financial Viability Analysis Analysts should recognize that this manual is not comprehensive, as FVAs depend on the exact characteristics of the project or activity being studied. If the Mission or Bureau needs assistance with the FVA, it should contact the EGAT/DC PD team. This will most likely be necessary in the case of municipal, project, or bond financing. Regardless of the level of EGAT/DC support, the Mission will lead efforts to gather information commonly required for DCA supported projects. In the case of a project-specific DCA structure, required inputs for the Financial Viability Analysis will include: • Project start-up costs • Future income generated by the project • Estimated operating and maintenance costs • Local interest rates (debt servicing costs), tax expenses, etc. As stated previously, for a portfolio guarantee, illustrative examples of a few borrowers or notional cash flows will be necessary to demonstrate a model for how the debt will be repaid. This model should contain data inputs as just listed for project-specific structures.

DCA Operations Manual April 2004 II-21

If the borrower is an existing organization, the Mission should collect audited financial statements from the last three years, as well as any forecasts the entity has prepared for the near term future. These documents should include: • Balance Sheet (assets, liabilities and equity components) • Income Statement (revenues, operating expenses, financing expenses, net income) • Cash Flow Statement (cash flows from operations, from investing, and from financing) • Sources and Uses of Funds. • Detailed estimates of variables such as costs, prices, sales volume, etc. Similar information about the lender needs to be collected in order to perform the lender viability analysis. These documents should include: • Balance Sheet (assets, liabilities and equity components) • Income Statement (revenues, operating expenses, financing expenses, net income) • Cash Flow Statement (cash flows from operations, from investing, and from financing) • The inputs detailed in the table under Lender Viability above. EGAT/DC has developed spreadsheet templates and samples for use in preparing financial viability analyses of loan/bond guarantees and loan/lease portfolio guarantees, which should substantially simplify the execution of the analysis. The EGAT/DC PD team will make these materials available to Missions or contractors as required. With the appropriate documents and data fully compiled for both the borrower and the lender, EGAT/DC can provide additional guidance.

6. Fee Justification The EGAT/DC PD team should use the following template for the Fees Justification section of the Action Package and adjust it accordingly to reflect the specific characteristics of the guarantee. Any deviations from this justification must comply with ADS 249. In addition, per OMB A-129 guidelines (Sec.II.3), EGAT/DC PM team will annually review the fee structure of DCA guarantees as part of the subsidy re-estimate process.5 This review will be discussed, documented and filed as part of the November or December Portfolio Review Meetings. 5 OMB A-129 Circular also states that fees “should be set at levels that minimize default and other subsidy costs while supporting the achievement of the program’s policy objectives. Unless inconsistent with program purposes, riskier borrowers should be charged more than those who pose less risk.” (Sec II.3)

DCA Operations Manual April 2004 II-22

Proposed Fees for this Activity: Origination Fee: X% of the guaranteed portion of the authorized amount

Utilization Fee: X% of the guaranteed portion of the outstanding principal balance per annum Justification The fees are consistent with program purposes and were set in consultation with the lendinginstitution so as to maximize utilization of the guarantee facility and not hinder financial viability of the projects. Since the USAID fees will contribute to the borrower’s overall cost of capital and thus thefinancial viability of the projects, special consideration was given when determining the fee structure. Every effort was made to consult with both the lending institution to ensure that thefee structure would not impede the financial viability of the projects or the utilization of theguarantee facility. The proposed fee structure is essential to accomplish several objectives:

• establish a high rate of utilization for the facility; • maximize the number of end-borrowers who may benefit from the guarantee; • ensure that the activity is profitable and capable of demonstrating viability to the market;

and; and • does not put undue stress on the partners USAID is trying to assist.

The proposed fee structure for this guarantee conforms to the guidance set forth in ADS 249.3.4

7. Legal Terms and Conditions The USAID Office of General Counsel (GC) from Washington or through one of its Regional Legal Advisors should draft, review and approve the guarantee agreement’s “term sheet”. The Mission or the EGAT/DC PD team will ensure adequate GC involvement in this process. The following is an example term sheet for a loan portfolio guarantee. THE GUARANTEE. To induce the Guaranteed Party to make “Qualifying Loans” to “Qualifying Borrowers” for “Qualifying Projects,” as defined below, the Parties agree to the following terms: 1. Maximum Authorized Portfolio Amount: The aggregate principal amount of all Qualifying Loans covered under

this Agreement at any one time shall not exceed the local currency equivalent of [numerical words] U.S. Dollars [US$x million].

2. Maximum Cumulative Disbursements: The maximum cumulative amount of all loan disbursements made under Qualifying Loans shall not exceed the local currency equivalent of [numerical words] U.S. Dollars [US$x million]. No loan disbursement shall be eligible for coverage under the Guarantee unless the amount of such disbursement, together with all previous disbursements made under Qualifying Loans, does not exceed the local currency equivalent of [numerical words] U.S. Dollars [US$x million].

3. USAID Guarantee Percentage: Fifty (50%) percent of the Guaranteed Party’s net losses of principal. (See Section 4.01 of the Standard Terms and Conditions for claim requirements).

4. Guarantee Ceiling (Maximum USAID Liability): [numerical words] U.S. Dollars [US$x million].

5. Final Date for Placing Qualifying Loans under Coverage: December 31, 2009.

6. Coverage Expiration Date: June 30, 2010.

7. Final Date for Submitting Claims: Six months after the Coverage Expiration Date, except as set forth in Article IV of the Standard Terms and Conditions attached hereto, provided further that no claims may be submitted in connection with any default on a loan that occurs after the Coverage Expiration Date.

8. Currency of Qualifying Loans Placed Under Guarantee Coverage: [insert local currency – include US Dollars if applicable as well].

9. Currency of Guarantee Payment: Local currency.

10. USAID Guarantee Fees:

10(a). Origination Fee: [numerical words] (x.x%) of the guaranteed portion of the authorized amount. [US$xx,xxx].

10(b). Utilization Fee: [numerical words] (x.xx%) per annum of the guaranteed portion of principal. This amount is to be calculated by taking the USAID guaranteed portion (50%) of the average of the total ending balances of all Qualified Loans at the end of the two most recent Guarantee Periods and then

DCA Operations Manual April 2004 II-23

multiplying such amount by one quarter of one percent (x.xx%) per annum. The fee is payable semi-annually, as billed.

11. Currency of Fee Payment: Local currency.

12. Guarantee Periods: The first Guarantee Period will commence upon the date of the Agreement and end on September 30, 2003. Subsequent Guarantee Periods will consist of each six-month period, beginning with the six-month period from October 1, 2003 to March 31, 2004, and the final Guarantee Period will commence April 1, 2010 and end on the Coverage Expiration Date.

CRITERIA FOR QUALIFYING LOANS. In addition to the criteria set forth in the Standard Terms and Conditions, Attachment 2, a "Qualifying Loan" is one made to a "Qualifying Borrower" for a “Qualifying Project,” each as defined below:

13. Qualifying Borrowers: Non-sovereign small and medium-sized hotels and manufacturing firms for productivity improvements that address environmental concerns, reduce environmental impacts and include environmental retrofitting; and small and medium-sized enterprises borrowing money for a variety of needs including business expansion, fixed asset improvement, working capital, and equipment purchase. A Qualifying Borrower includes any Affiliate of that borrower, including parent or subsidiary companies having the same or substantially similar ownership as such borrower. Any question regarding who is a Qualifying Borrower may be resolved in consultation with USAID, and USAID may waive in writing this restriction on loans to Affiliates.

14. Maximum Cumulative Principal Amount of Qualifying Loans Made To Any One Qualifying Borrower: The local currency equivalent of Five Hundred Thousand U.S. Dollars [US$500,000], unless otherwise agreed to by USAID in writing.

15. Qualifying Projects: Investments designed to encourage growth of Qualifying Borrowers through environmental retrofitting and/or by facilitating business expansion, fixed asset improvement, access to working capital, and equipment purchase.

16. True Risk Sharing by Guaranteed Party: To ensure that there will be true risk sharing between USAID and the Guaranteed Party, no Qualifying Loan shall be eligible for coverage under the Agreement if more than fifty percent (50%) of total payments of principal on such Loan is guaranteed by a government or international donor organization, including USAID.

8. Risk Assessment See Section III for more details. The Action Package includes the full text description of how the EGAT/DC Risk Management (RM) team analyzes the risk associated with the guarantee, summarized quantitatively by the Weighted Average Risk Factor (WARF). The RM team requires that the Action Package be drafted, with particular emphasis on the financial viability analysis and the term sheet, six weeks prior to the proposed CRB presentation. This allows for sufficient time to conduct the risk assessment, finalize other Action Package sections and distribute to CRB members.

9. Subsidy Cost Calculation Based on the WARF score and several of the basic terms and conditions of the guarantee (e.g., proposed fees, duration of the guarantee, maximum cumulative disbursements), the EGAT/DC RM team utilizes the Office of Management and Budget (OMB) subsidy risk calculator to calculate the subsidy cost estimate as a percent of the total facility amount, which in the legal agreement’s nomenclature is “Maximum Cumulative Disbursements” (MCD). Subsidy, as defined in OMB Circular A-11, is the estimated long-term cost to the government of a loan guarantee, calculated on a net present value basis, excluding administrative costs.

DCA Operations Manual April 2004 II-24

Following is a sample of the output of the OMB Credit Subsidy Calculator. The key fields in this output, which are also summarized in the Project Information Sheet (Attachment 1 of the Action Package), include:

• Total Subsidy: This number is expressed as a percent of the MCD. This is equal to the Default Subsidy plus the Subsidy Reduction for Fees.

• Default Subsidy: This figure accounts for the estimated cost of defaults (cash outflows) that USAID would pay to the guaranteed party in present value terms. This is also expressed as a percent of MCD. On the Project Information Sheet, Nominal Defaults are presented, which is MCD multiplied by the Default Subsidy rate.

• Subsidy Reduction for Fees: This statistic represents the estimate of fees received (cash inflows) from the guaranteed party.

d

d

d

d

d

d

d

d

10. Monitoring Plan Monitoring is a coordinated effort between the Mission and the Office of Development Credit (EGAT/DC). Monitoring responsibilities are divided into Development and Financial activities. The mission is solely responsible for Development Monitoring, while EGAT/DC and the Mission are both responsible for Financial Monitoring.

DEVELOPMENT MONITORING

The mission must insert a short description on how it plans to monitor the developmental aspects of this activity. This description should include the performance indicators related to Strategic Objective (SO) reporting that this DCA guarantee will support.

FINANCIAL MONITORING

DCA Operations Manual April 2004 II-25