Embed Size (px)

Citation preview

Development Impact of Remittances

Sanket Mohapatra (with Dilip Ratha and Ani Silwal)Migration and Remittances Unit

World Bank

UNITAR-IOM-UNFPA Seminar – Migration and the MDGs

New York

September 2, 2010

Outline

A. Stylized facts on international migration

B. Development impact of international

migration and remittances

C. Remittance trends during global financial

crisis and outlook for 2010-11

D. Policy implications

A. Stylized Facts on international

migration

1. Only 3% of world population are international

migrants; 97% are not.

2. Economic migrants account for 93% of global

migrant stock. Economic migration is set to

increase in future.

3. South-South migration is as high as South-North

migration.

South-South migration is almost as large as

South-North migration

South

43%

High-

income non-

OECD

14%

High-

income

OECD

43%

Source: Migration and Remittances Factbook 2011

Destination of migrants from the South

Outline

A. Stylized facts on international migration

B. Development impact of international

migration and remittances

B. Development impact of international migration

1. Migration benefits all parties – the migrants, the

destination country, and the origin country.

Migration benefits all parties

Global income gains of $356 billion from a 3% (14 million)

increase in labor force of industrial countries (GEP 2006)

Global income gains of $675 billion (Anderson and Winters,

2008)

“A conservative estimate of the welfare gain to a moderately

skilled worker… moving to the US is PPP$10,000 per worker,

per year…” (Clemens, Montenegro and Pritchett, 2008)

Dixon and Rimmer (2009) estimate that the difference between

the welfare effects for U.S. households of a tighter border policy

and a liberalized guest worker program with an visa charge is

about $260 billion a year

B. Development impact of international migration

1. Migration benefits all parties – the migrants, the

destination country, and the origin country.

2. Benefits to countries of origin are mostly through

remittances.

0

100

200

300

400

500

600

700

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

$ billions

Private debt &

port. equity

FDI

ODA

Recorded

Remittances

Remittance flows to developing countries remained

resilient during the crisis

49 48

2220

1511 10 10 10 10

India

Chi

na

Mex

ico

Phi

lippi

nes

Franc

e

Ban

glades

h

Spa

in

Ger

man

y

Nig

eria

Bel

gium

Smaller countries are top recipients of remittances

as share of GDP

50

3831

28 27 26 25 24 22 20

Taj

ikista

n

Tonga

Mol

dova

Kyr

gyz Rep

.

Lesot

ho

Sam

oa

Leban

on

Guy

ana

Nep

al

Hon

duras

$ billions, 2009 % of GDP, 2008

Remittances reduce poverty

Evidence from a few household surveys shows that

remittances reduce poverty

Remittances also finance education and health

expenditures, and ease credit constraints on small

businesses

Remittances reduce poverty: Nepal

23

42

32 31

15

20

25

30

35

40

45

% of household

receiving remittances

Poverty headcount rate

%

1995/6

2003/4

Source: World Bank, DFID, ADB Study 2006, Glinskaya and others 2006

Remittances help reduce poverty in Sri Lanka

0 0 1

1620

8

35

-1

-71 2 3 4 5 6 7 8 9 10

% of Sri Lankan households that moved up to a higher

income decile after receiving remittances, 1999-2000*

Income Decile

Remittances tend to rise following crisis,

natural disaster, or conflict

Remittances as % of private consumption

0.5

1.7

1.21.4

2.0 2.0

1.0

1.8

2.0

Indonesia Thailand Mexico

year before

year of crisis

year after

0

10

20

30

Mexico India Pakistan Bangladesh Philippines Nepal

Percent of GDP Remittances

Trade deficit

Remittances have partially or fully offset

trade deficits in some large recipients

0%

100%

200%

300%

Leba

non

Hai

ti

Nep

al

Jam

aica

Sud

an

Mol

dova

Pak

ista

n

El S

alva

dor

Rom

ania

Arm

enia

Including remittances

Excluding remittances

Remittances contribute to sovereign

creditworthiness

Debt as a percent of exports

Improving ratings

Remittances

(% of GDP,

2004)

Rating

excluding

remittances

Rating

including

remittances

Spread

reduction

(basis

pts)

Lebanon 14 B+ BB- 150

Haiti* 28 CCC B- 334

Nicaragua* 11 CCC+ B- 209

Uganda* 5 B- B 161

* Calculated using the benchmark model of Ratha, De and Mohapatra (2010)

Downside of remittances

Large remittance flows may lead to currency

appreciation and adverse effects on exports; but

sterilization of inflows may not be an appropriate

policy response

Remittances may create dependency

Remittance channels may be misused for money

laundering and financing of terror

Outline

A. Stylized facts on international migration

B. Development impact of international

migration and remittances

C. Remittance trends during global financial

crisis and outlook for 2010-11

Recent remittance trends

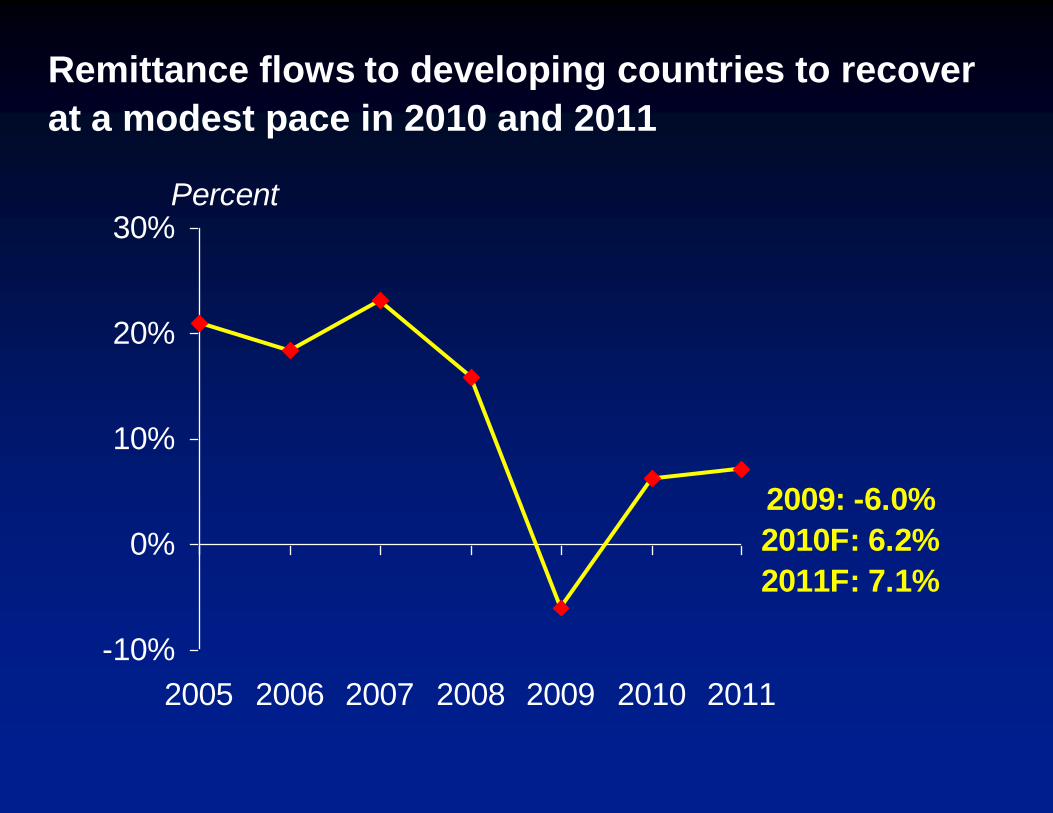

Remittances estimated to have declined by only 6%

in 2009, but expected to grow by 6.2% in 2010 and

7.1% in 2011

Risks to the outlook include jobless recovery,

currency movements, and rising protectionism

Outlook for remittance flows for 2009-11

$ billion 2008 2009 2010f 2011f

Developing countries 335.8 315.7 335.4 359.1East Asia and Pacific 86.1 85.7 94.1 102.7Europe and Central Asia 57.5 45.6 48.1 51.7Latin America and Caribbean 64.4 56.5 59.8 64.5Middle-East and North Africa 34.8 32.0 33.1 34.4South Asia 71.7 75.2 78.7 82.8Sub-Saharan Africa 21.3 20.7 21.6 22.9

Growth rate (%)

Developing countries 15.9% -6.0% 6.2% 7.1%East Asia and Pacific 20.7% -0.4% 9.8% 9.2%

Europe and Central Asia 13.3% -20.7% 5.4% 7.6%Latin America and Caribbean 2.1% -12.3% 5.7% 7.9%Middle-East and North Africa 9.8% -8.1% 3.6% 4.0%

South Asia 32.6% 4.9% 4.7% 5.2%Sub-Saharan Africa 14.1% -2.7% 4.4% 5.8%

-25

75

175

275

375

475

575

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

$ billion

Pvt debt &

port.

equity

FDI

ODA

Recorded

Remittances

Remittances proved to be resilient compared to other

flows

Remittance flows to developing countries to recover

at a modest pace in 2010 and 2011

-10%

0%

10%

20%

30%

2005 2006 2007 2008 2009 2010 2011

Percent

2009: -6.0%

2010F: 6.2%

2011F: 7.1%

Remittances remain resilient during

downturns in host countries

Remittances are sent by the stock (cumulated flows) of

migrants

Remittances are a small part of migrants’ incomes that can

be cushioned against income shocks by migrants

Duration of migration may increase in response to tighter

border controls

“Safe haven” factor or “home-bias” -- returnees will take

back accumulated savings

Sectoral shifts – and fiscal stimulus packages – may help

some migrants

Regional trends

Remittances to Latin America and Caribbean have

bottomed out since 4Q 2009

Flows to South Asia and East Asia have continued

to grow, but at a markedly lower pace

Flows to Europe & Central Asia and Middle-East

and North Africa fell more than expected

Flows to Sub-Saharan Africa remained flat, judging

from sparse data

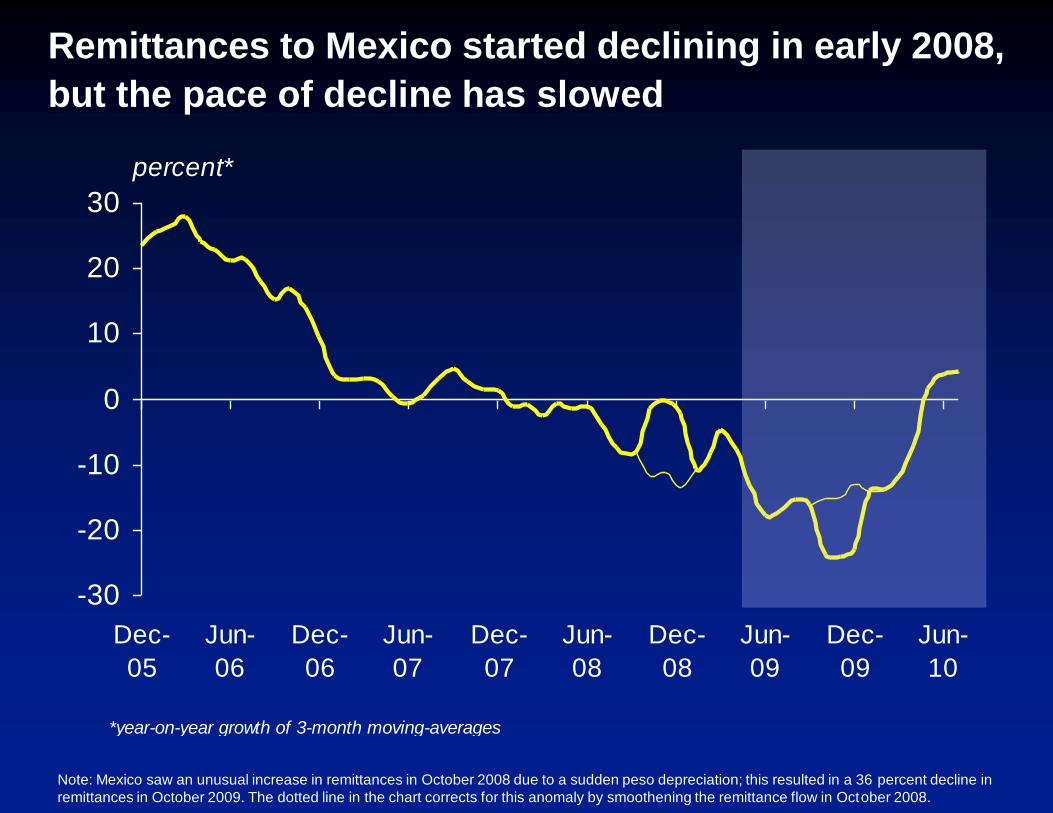

Remittances to Mexico started declining in early 2008,

but the pace of decline has slowed

-30

-20

-10

0

10

20

30

Dec-

05

Jun-

06

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

percent*

*year-on-year growth of 3-month moving-averages

Note: Mexico saw an unusual increase in remittances in October 2008 due to a sudden peso depreciation; this resulted in a 36 percent decline in

remittances in October 2009. The dotted line in the chart corrects for this anomaly by smoothening the remittance flow in October 2008.

Remittances to Latin America and Caribbean appear

to have bottomed out

-25

-15

-5

5

15

Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

El SalvadorHondurasGuatemalaDominican Rep.Jamaica

percent*

*year-on-year growth of 3-month moving-averages

-30

-20

-10

0

10

20

30

40

50

2007

-Q2

2007

-Q3

2007

-Q4

2008

-Q1

2008

-Q2

2008

-Q3

2008

-Q4

2009

-Q1

2009

-Q2

2009

-Q3

2009

-Q4

2010

-Q1

2010

-Q2

-600

-400

-200

0

200

400

600

800

1000

Percent, year-on-year growth Millions US$

Remittances to Ecuador have started falling

again

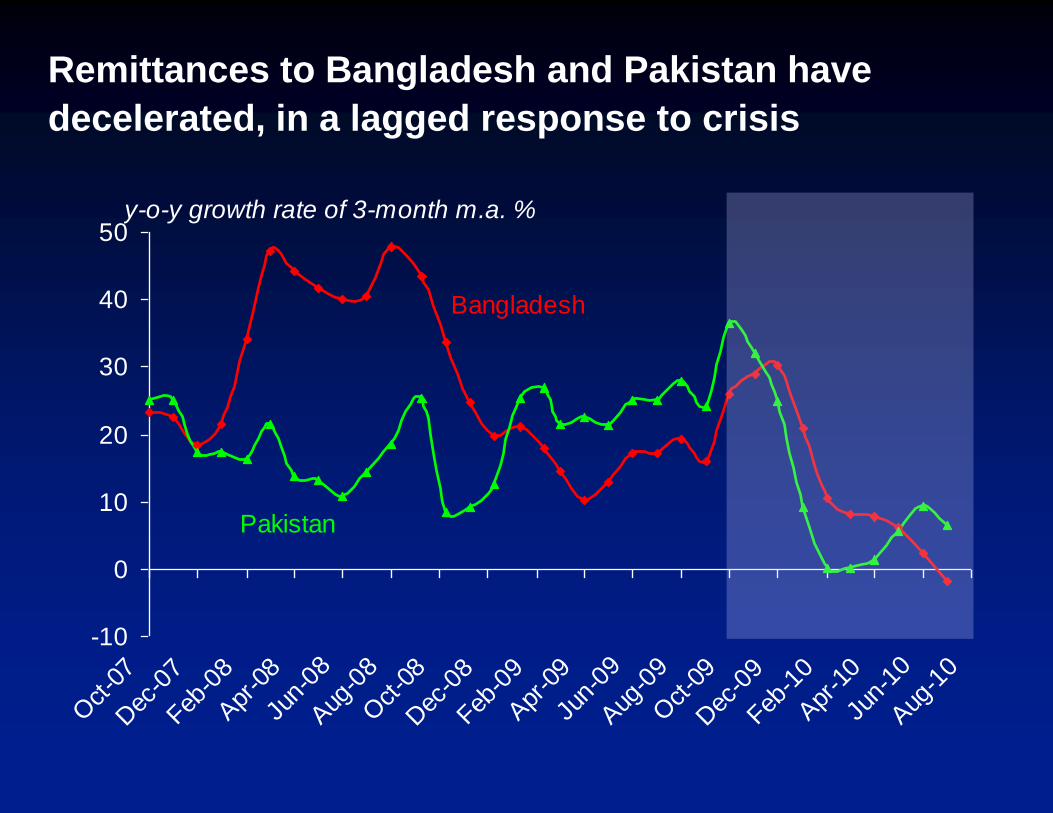

Remittances to Bangladesh and Pakistan have

decelerated, in a lagged response to crisis

-10

0

10

20

30

40

50

Oct

-07

Dec

-07

Feb-0

8

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-0

9

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb-1

0

Apr

-10

Jun-

10

Aug

-10

y-o-y growth rate of 3-month m.a. %

Bangladesh

Pakistan

Remittances to Philippines have been growing since

Q3 2009

0

5

10

15

20

25

Oct

-07

Dec

-07

Feb-0

8

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-0

9

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb-1

0

Apr

-10

Jun-

10

Aug

-10

y-o-y growth rate of 3-month m.a. %

Philippines

-40

-20

0

20

40

60

2007

-Q2

2007

-Q3

2007

-Q4

2008

-Q1

2008

-Q2

2008

-Q3

2008

-Q4

2009

-Q1

2009

-Q2

2009

-Q3

2009

-Q4

2010

-Q1

-10

-5

0

5

10

15

Percent, year-on-year growth US$ bn.

Remittances to India grew through the crisis

except in Q1 2009

Note: Private transfers comprise mostly remittances from Indian migrants, but also include other transfers.

Remittances outflows from Russia are correlated

with oil prices

0

2

4

6

8

2002

Q4

2003

Q4

2004

Q4

2005

Q4

2006

Q4

2007

Q4

2008

Q4

2009

Q4

0

20

40

60

80

100

120

140

$ billions

Remittance outflows

(left scale)

Crude oil price

(right scale)

$/barrel

Source: IMF Balance of Payments and Development Prospects Group, World Bank.

Remittance outflows from Saudi Arabia have been

uncorrelated with oil price since early 1990s

0

5

10

15

20

25

1973 1977 1981 1985 1989 1993 1997 2001 2005 2009

0

20

40

60

80

100$ billions

Remittance outflows

from Saudi Arabia

Crude oil price

(right scale)

$/barrel

Three observations

The more diverse the migration destinations, the

more resilient are remittances

The lower the barriers to labor mobility, the stronger

the link between remittances and economic cycles

in that corridor

Exchange rate movements produce valuation

effects, but they also influence the consumption-

investment motive for remittances

Outline

A. Stylized facts on international migration

B. Development impact of international

migration and remittances

C. Remittance trends during global financial

crisis and outlook for 2010-11

D. Policy implications

D. Policy implications

1. The international remittances agenda

International

Remittances

Agenda

1. Monitoring,

analysis, projection

2. Retail payment

systems

3. Financial

access for

households

4. Capital

market access

for institutions

International remittances Agenda

1. Improve monitoring, analysis, projection (MAPping)

2. Improve retail payment systems:

Reduce remittance costs

Improve competition in remittance industry

Share networks - avoid exclusivity contracts

Avoid overregulation of remittance industry

Introduce new technology

3. Leverage remittances for financial access for households

4. Leverage remittances for improving access to capital markets

for institutions/countries

D. Policy implications

1. The international remittances agenda

2. Know your migrants/diaspora

3. Help potential migrants acquire globally marketable

skills

4. Ethical recruitment policies may be ineffective, and

unethical –

5. Improve transparency in recruitment of migrants

6. Border control policies should be revisited

7. Migration is not a substitute for employment

creation at home

Summary

Migration generates substantial welfare gains and reduces poverty

Benefits to countries of origin are mostly through remittances (and also through trade, investments, and transfer of knowledge, skill and technology)

Remittances flows have been resilient during global financial crisis, but risks to outlook from jobless economic recovery and rising protectionism

Thank you!

![Silwal presentation [PDF 9.79MB]](https://img.pdfslide.net/doc/110x75/589edeb61a28abb24d8b6e2d/silwal-presentation-pdf-979mb.jpg)