Embed Size (px)

Citation preview

Development of ASEAN Power Grid –Implications for Northeast Asian Cooperation

SHI Xunpeng (Roc), PhDSenior Fellow, Deputy Head of Energy Economics

The 3rd Northeast Asia Energy Security ForumThe Plaza, Seoul, Republic of Korea, 17 December 2015

Issues

• ●Paradox in ASEAN: Green Vision vs Brown Outlook (mutual needs)

• ● What are the reality and challenges of the ASEAN Power Grid?

• ● The case of gas sector

• ● What could be suggested for NEA?

2

3

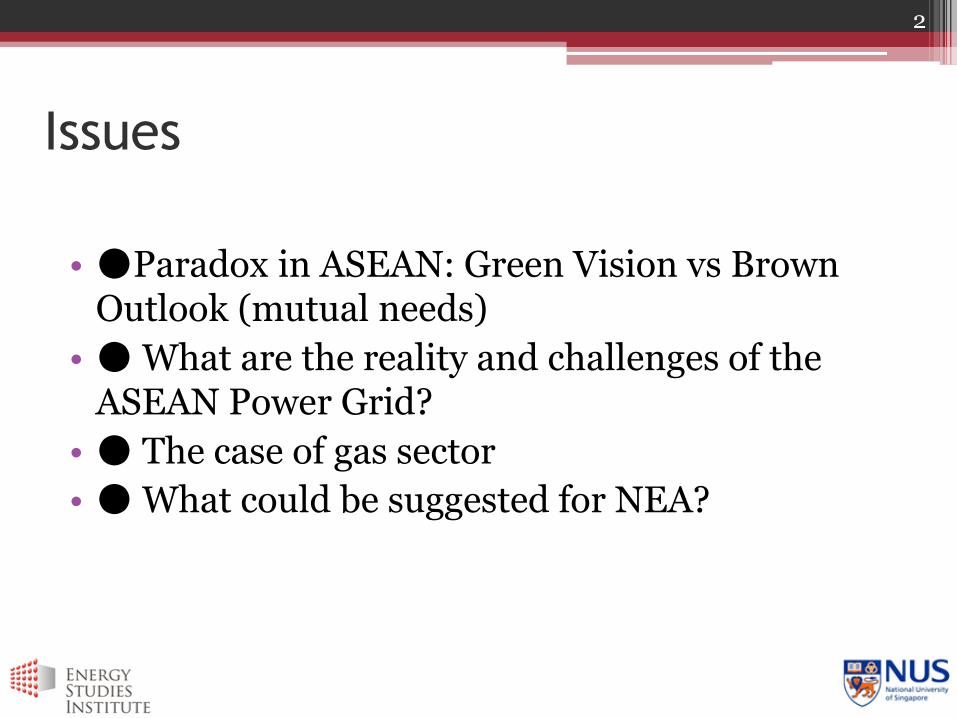

Paradox: Green Vision vs Brown Outlook

Source: IEA (2015), Southeast Asia Energy Outlook

Primary Energy Demand in Southeast Asia

4

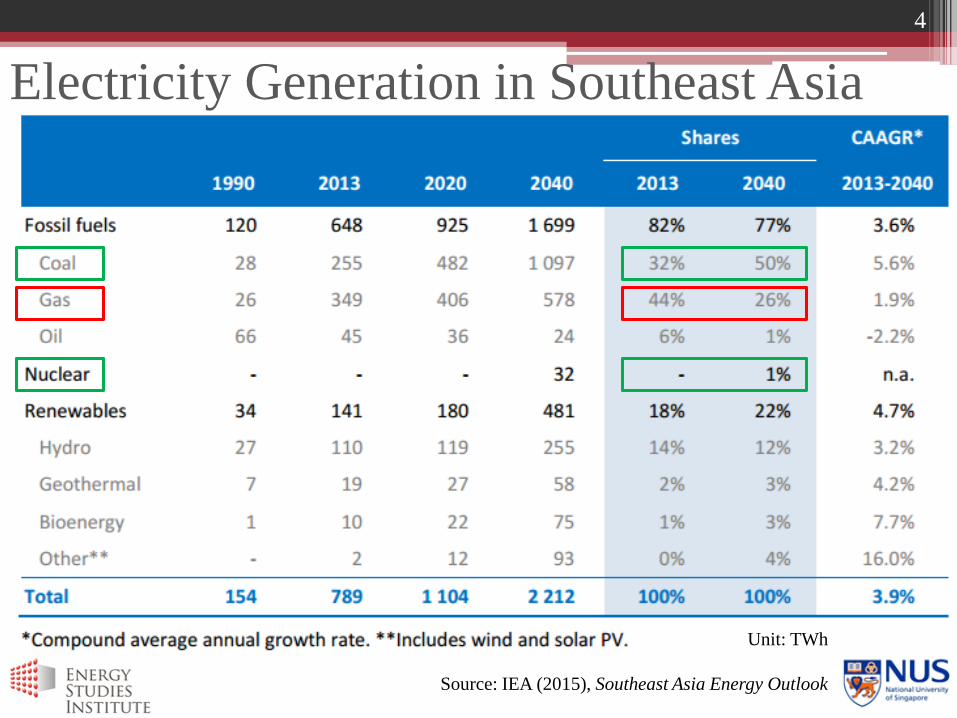

Electricity Generation in Southeast Asia

Unit: TWh

Source: IEA (2015), Southeast Asia Energy Outlook

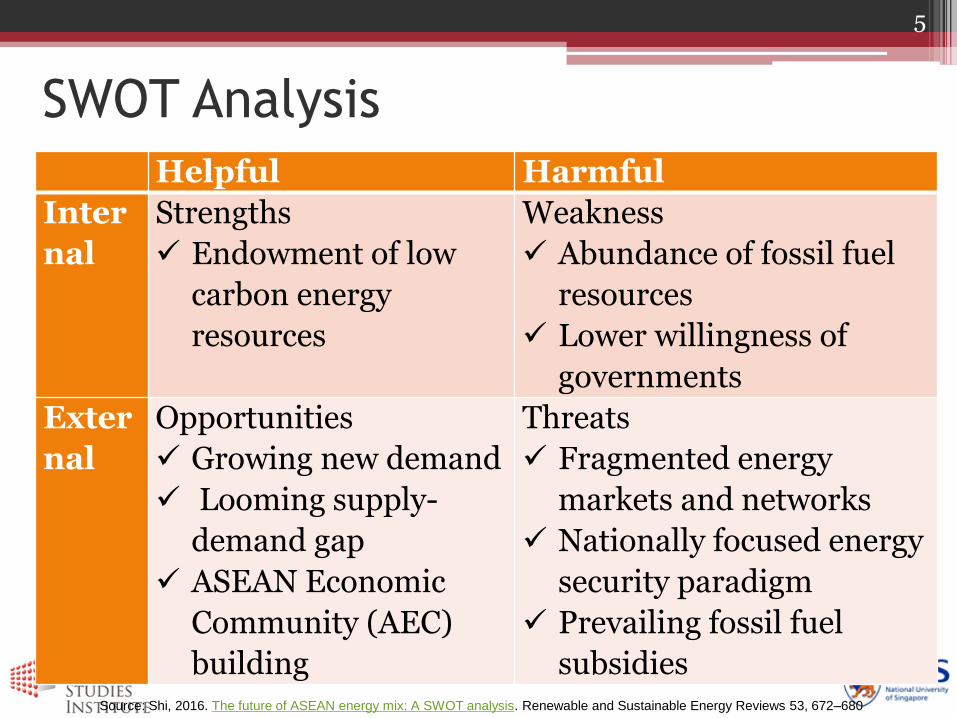

SWOT Analysis

Helpful Harmful

Inter

nal

Strengths

Endowment of low

carbon energy

resources

Weakness

Abundance of fossil fuel

resources

Lower willingness of

governments

Exter

nal

Opportunities

Growing new demand

Looming supply-

demand gap

ASEAN Economic

Community (AEC)

building

Threats

Fragmented energy

markets and networks

Nationally focused energy

security paradigm

Prevailing fossil fuel

subsidies

5

Source: Shi, 2016. The future of ASEAN energy mix: A SWOT analysis. Renewable and Sustainable Energy Reviews 53, 672–680

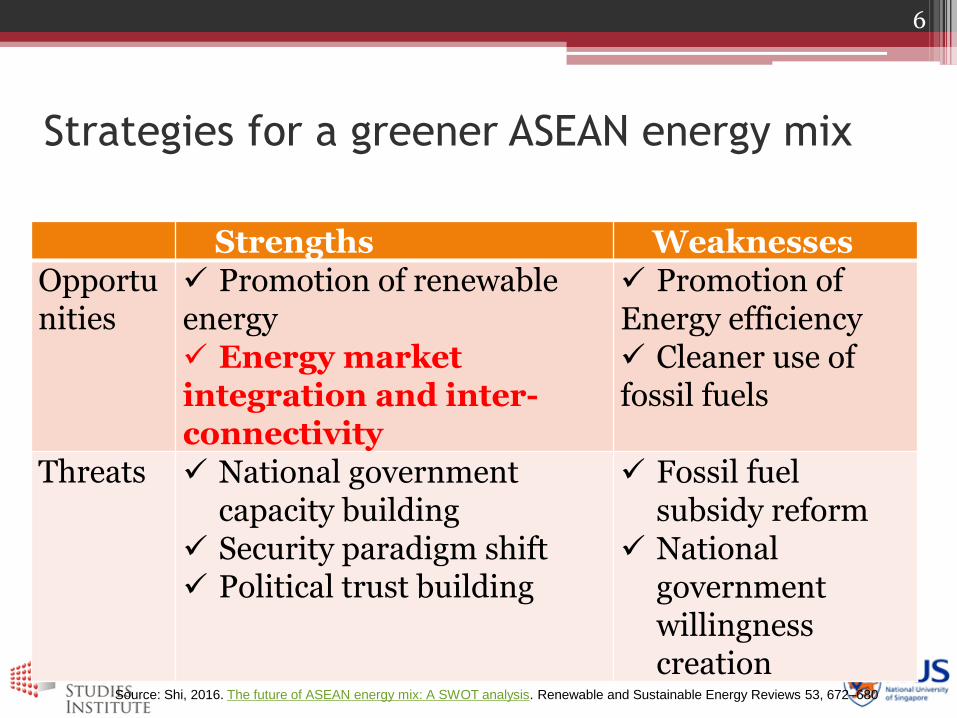

Strategies for a greener ASEAN energy mix

Strengths WeaknessesOpportunities

Promotion of renewable energy Energy market integration and inter-connectivity

Promotion of Energy efficiency Cleaner use of fossil fuels

Threats National government capacity building

Security paradigm shift Political trust building

Fossil fuel subsidy reform

National government willingness creation

6

Source: Shi, 2016. The future of ASEAN energy mix: A SWOT analysis. Renewable and Sustainable Energy Reviews 53, 672–680

Case Study: RE integration

• Intermittence of RE (Wind and solar)

Geographic difference; Resource complementary; System complementary

• Resource endowment difference

• Different load profile /consumption pattern

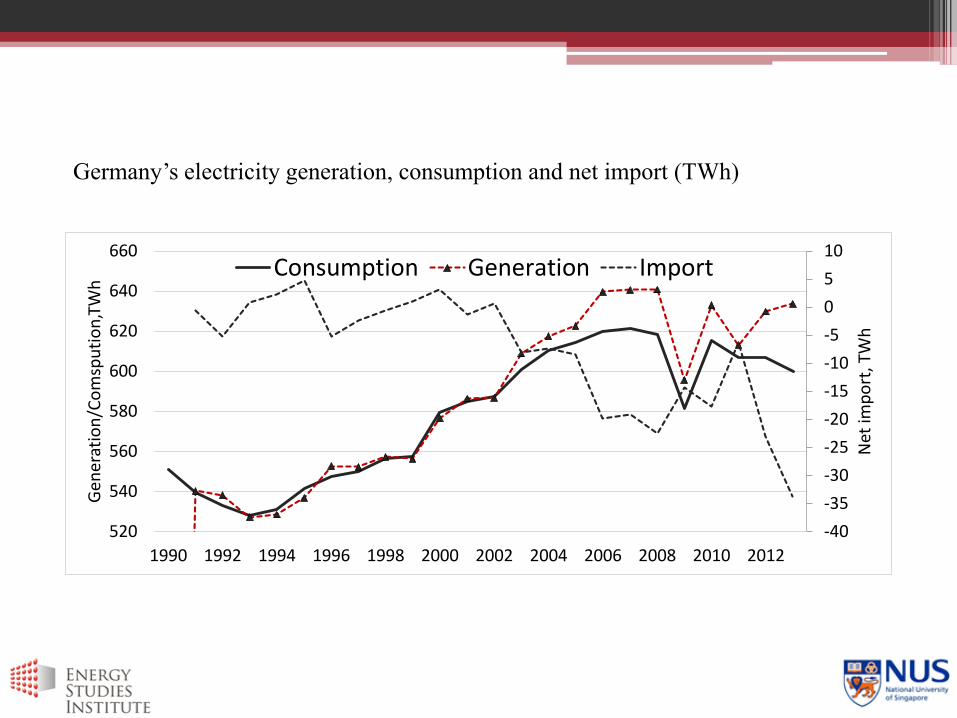

Germany’s electricity generation, consumption and net import (TWh)

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

520

540

560

580

600

620

640

660

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Net

imp

ort

, TW

h

Gen

erat

ion

/Co

msp

uti

on

,TW

h

Consumption Generation Import

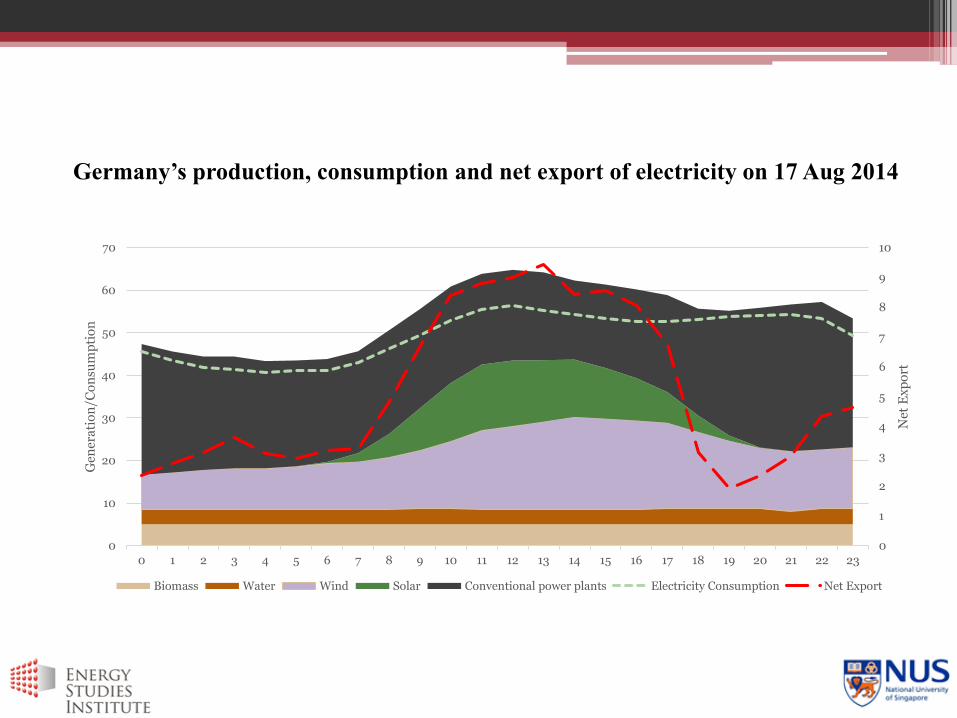

Germany’s production, consumption and net export of electricity on 17 Aug 2014

0

1

2

3

4

5

6

7

8

9

10

0

10

20

30

40

50

60

70

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Net

Ex

po

rt

Gen

era

tio

n/C

on

sum

pti

on

Biomass Water Wind Solar Conventional power plants Electricity Consumption Net Export

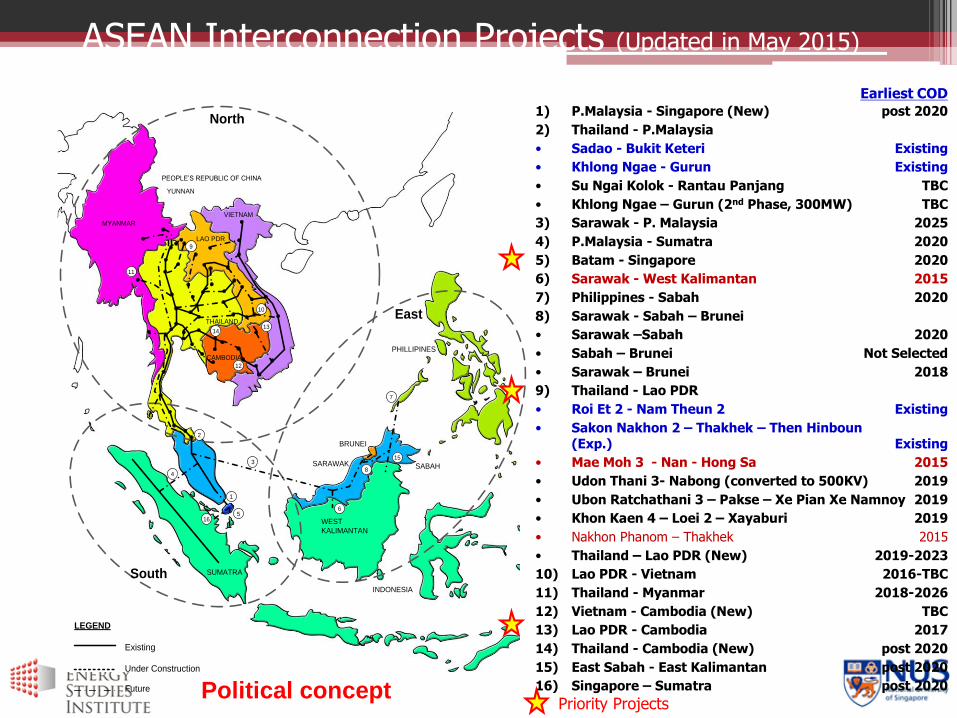

ASEAN Interconnection Projects (Updated in May 2015)

Earliest COD

1) P.Malaysia - Singapore (New) post 2020

2) Thailand - P.Malaysia

• Sadao - Bukit Keteri Existing

• Khlong Ngae - Gurun Existing

• Su Ngai Kolok - Rantau Panjang TBC

• Khlong Ngae – Gurun (2nd Phase, 300MW) TBC

3) Sarawak - P. Malaysia 2025

4) P.Malaysia - Sumatra 2020

5) Batam - Singapore 2020

6) Sarawak - West Kalimantan 2015

7) Philippines - Sabah 2020

8) Sarawak - Sabah – Brunei

• Sarawak –Sabah 2020

• Sabah – Brunei Not Selected

• Sarawak – Brunei 2018

9) Thailand - Lao PDR

• Roi Et 2 - Nam Theun 2 Existing

• Sakon Nakhon 2 – Thakhek – Then Hinboun(Exp.) Existing

• Mae Moh 3 - Nan - Hong Sa 2015

• Udon Thani 3- Nabong (converted to 500KV) 2019

• Ubon Ratchathani 3 – Pakse – Xe Pian Xe Namnoy 2019

• Khon Kaen 4 – Loei 2 – Xayaburi 2019

• Nakhon Phanom – Thakhek 2015

• Thailand – Lao PDR (New) 2019-2023

10) Lao PDR - Vietnam 2016-TBC

11) Thailand - Myanmar 2018-2026

12) Vietnam - Cambodia (New) TBC

13) Lao PDR - Cambodia 2017

14) Thailand - Cambodia (New) post 2020

15) East Sabah - East Kalimantan post 2020

16) Singapore – Sumatra post 2020

North

South

East

PHILLIPINES

BRUNEI

SARAWAK SABAH

WEST

KALIMANTAN

INDONESIA

SUMATRA

Existing

Under Construction

Future

LEGEND

11

9

14

10

13

12

2

4

1

3

165

6

8

7

15

CAMBODIA

THAILAND

LAO PDR

VIETNAM

MYANMAR

PEOPLE’S REPUBLIC OF CHINA

YUNNAN

Priority ProjectsPolitical concept

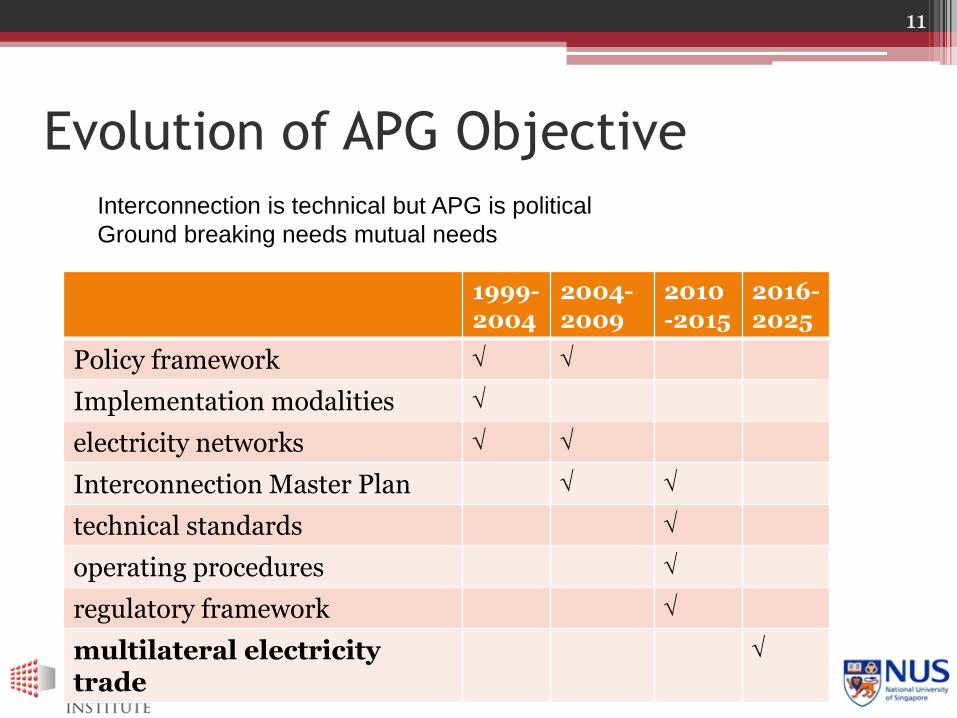

Evolution of APG Objective

1999-2004

2004-2009

2010-2015

2016-2025

Policy framework

Implementation modalities

electricity networks

Interconnection Master Plan

technical standards

operating procedures

regulatory framework

multilateral electricity trade

11

Interconnection is technical but APG is political

Ground breaking needs mutual needs

Lao PDR(L)

Thailand(T)

Malaysia(M)

Singapore(S)

TNL, PT-NK

PX-BKN

PB-MD2

TKH-NN

BY-SRD

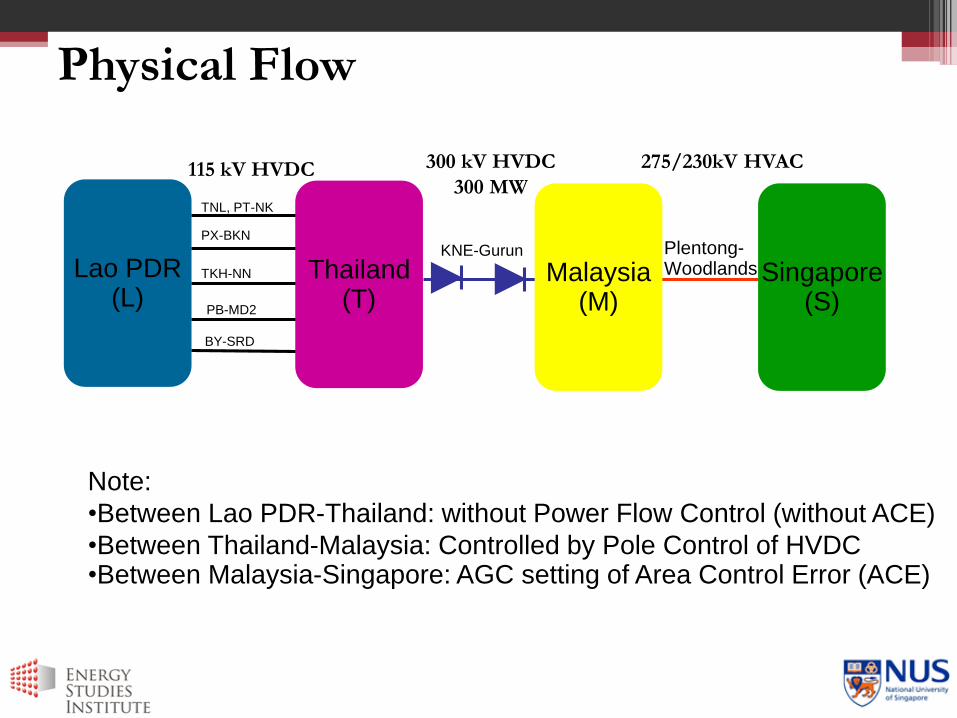

Physical Flow

KNE-Gurun Plentong-Woodlands

275/230kV HVAC300 kV HVDC

300 MW115 kV HVDC

Note:

•Between Lao PDR-Thailand: without Power Flow Control (without ACE)

•Between Thailand-Malaysia: Controlled by Pole Control of HVDC•Between Malaysia-Singapore: AGC setting of Area Control Error (ACE)

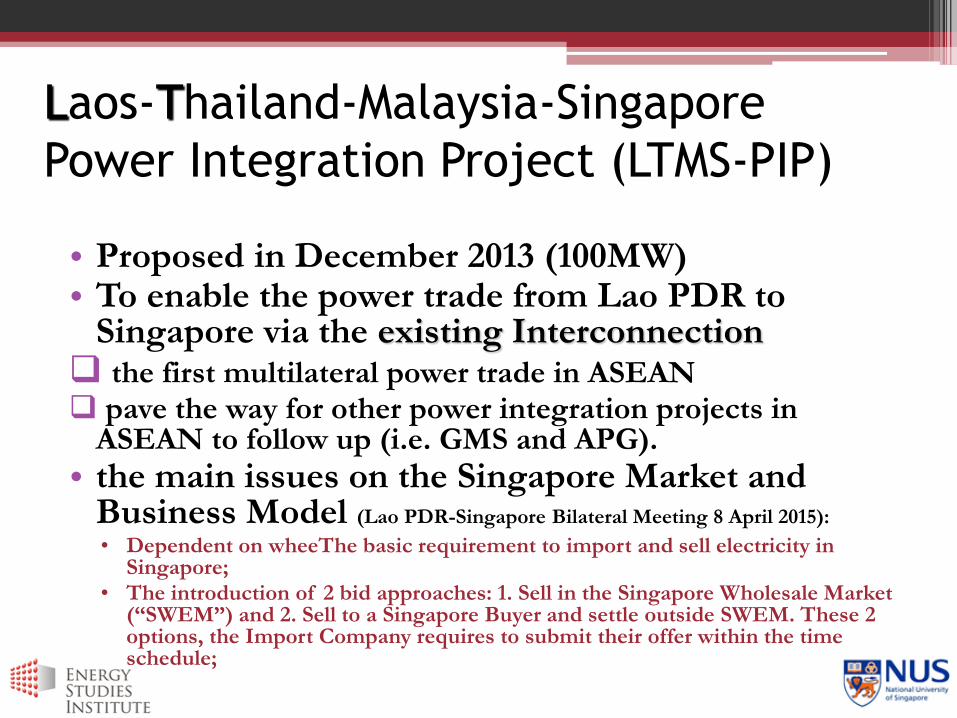

Laos-Thailand-Malaysia-Singapore

Power Integration Project (LTMS-PIP)

• Proposed in December 2013 (100MW)• To enable the power trade from Lao PDR to

Singapore via the existing Interconnection the first multilateral power trade in ASEAN pave the way for other power integration projects in

ASEAN to follow up (i.e. GMS and APG).

• the main issues on the Singapore Market and Business Model (Lao PDR-Singapore Bilateral Meeting 8 April 2015):

• Dependent on wheeThe basic requirement to import and sell electricity in Singapore;

• The introduction of 2 bid approaches: 1. Sell in the Singapore Wholesale Market (“SWEM”) and 2. Sell to a Singapore Buyer and settle outside SWEM. These 2 options, the Import Company requires to submit their offer within the time schedule;

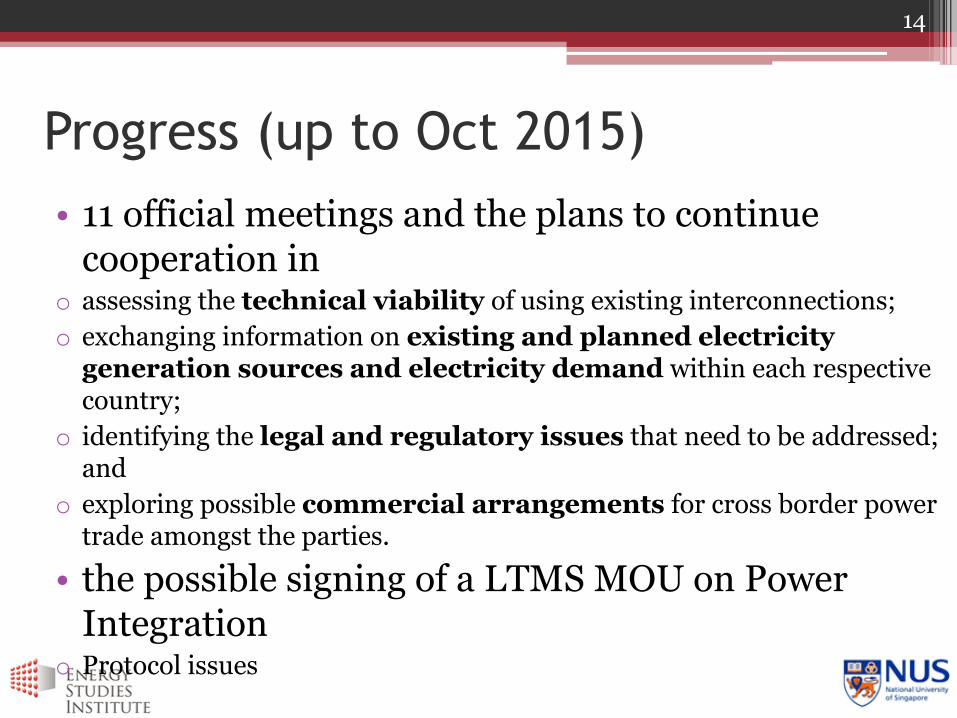

Progress (up to Oct 2015)

• 11 official meetings and the plans to continue cooperation in

o assessing the technical viability of using existing interconnections;

o exchanging information on existing and planned electricity generation sources and electricity demand within each respective country;

o identifying the legal and regulatory issues that need to be addressed; and

o exploring possible commercial arrangements for cross border power trade amongst the parties.

• the possible signing of a LTMS MOU on Power Integration

o Protocol issues

14

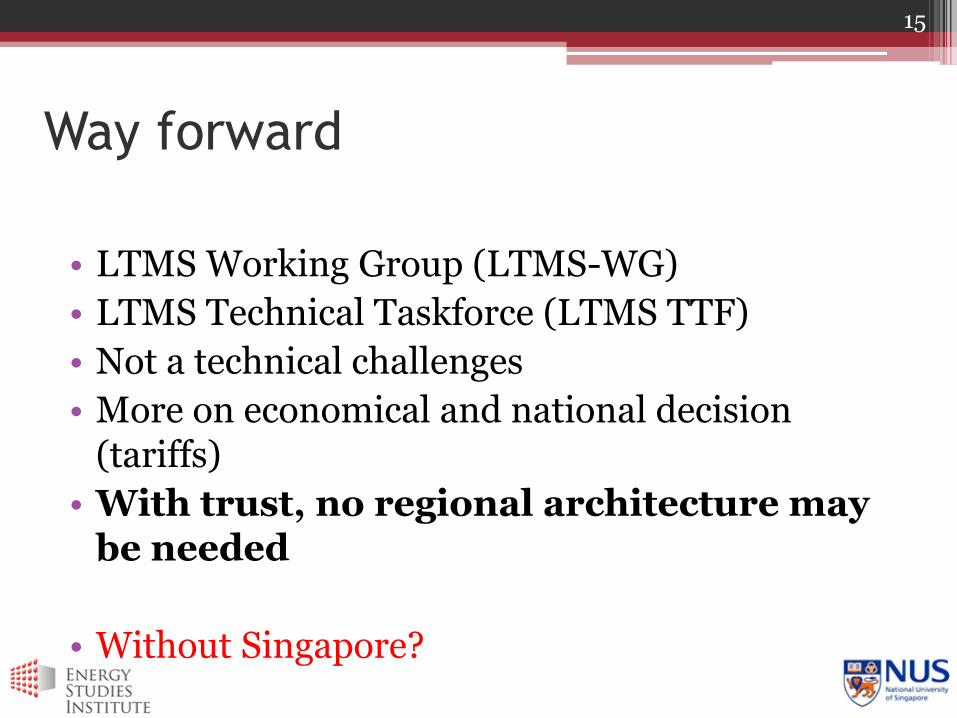

Way forward

• LTMS Working Group (LTMS-WG)

• LTMS Technical Taskforce (LTMS TTF)

• Not a technical challenges

• More on economical and national decision (tariffs)

• With trust, no regional architecture may be needed

• Without Singapore?

15

Future

• ASEAN Plan of Action for Energy Cooperation 2016-2025

• Green ASEAN (2020: energy intensity 20%;2025:23% renewables/TPES, 33EMM)

• Vs. brown outlook (2015: 8%; 15% Elec/9% TPES)

• Green Energy Network Initiative (interconnectivity, clean, and poverty reduction)

• Green interconnection

• Energy driver?

16

Bottom up vs. Top down

• Political willingness is the key

• It is not a prerequisite

• ASEAN electricity interconnection started before ASEAN was established

• “Grass-root” cooperation key to break ground

17

Natural gas cooperation

• Trans-ASEAN Gas Pipeline/Partnership (TAGP)

• Pricing mechanism: Oil Indexation vs. hub indexation

• Removal of destination clauses

• Take of Pay

18

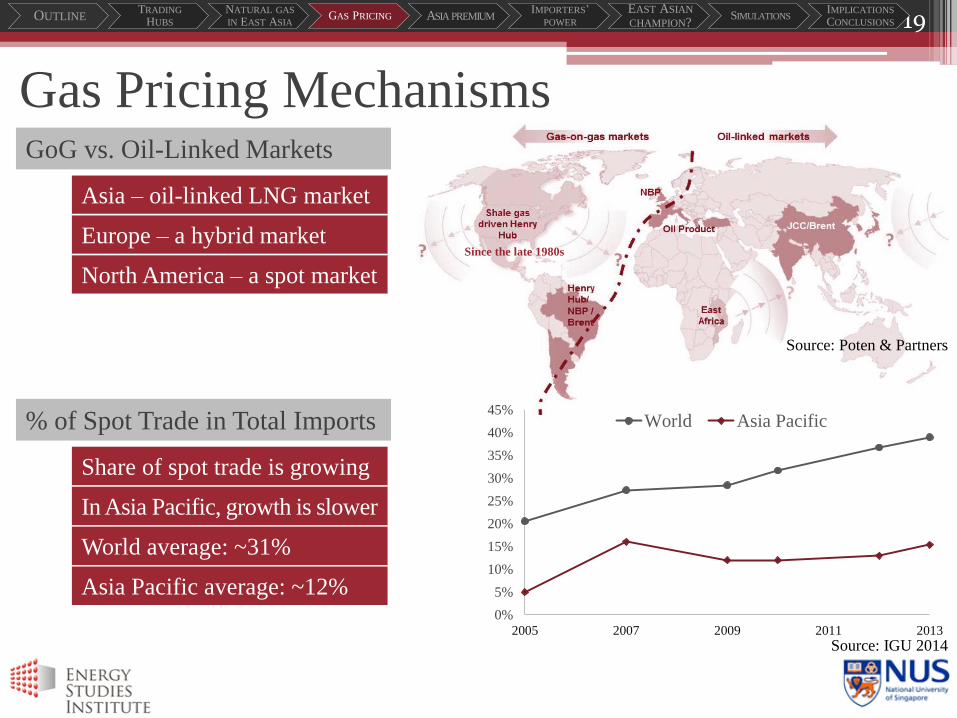

Since the late 1980s

19

Source: Poten & Partners

Source: IGU 2014

Gas Pricing Mechanisms

Asia – oil-linked LNG market

GoG vs. Oil-Linked Markets

Share of spot trade is growing

% of Spot Trade in Total Imports

Europe – a hybrid market

North America – a spot market

World average: ~31%

Asia Pacific average: ~12%

In Asia Pacific, growth is slower

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2005 2007 2009 2011 2013

World Asia Pacific

OUTLINETRADING

HUBS

NATURAL GAS

IN EAST ASIAGAS PRICING ASIA PREMIUM

IMPORTERS’ POWER

EAST ASIAN

CHAMPION?SIMULATIONS

IMPLICATIONS

CONCLUSIONS

20

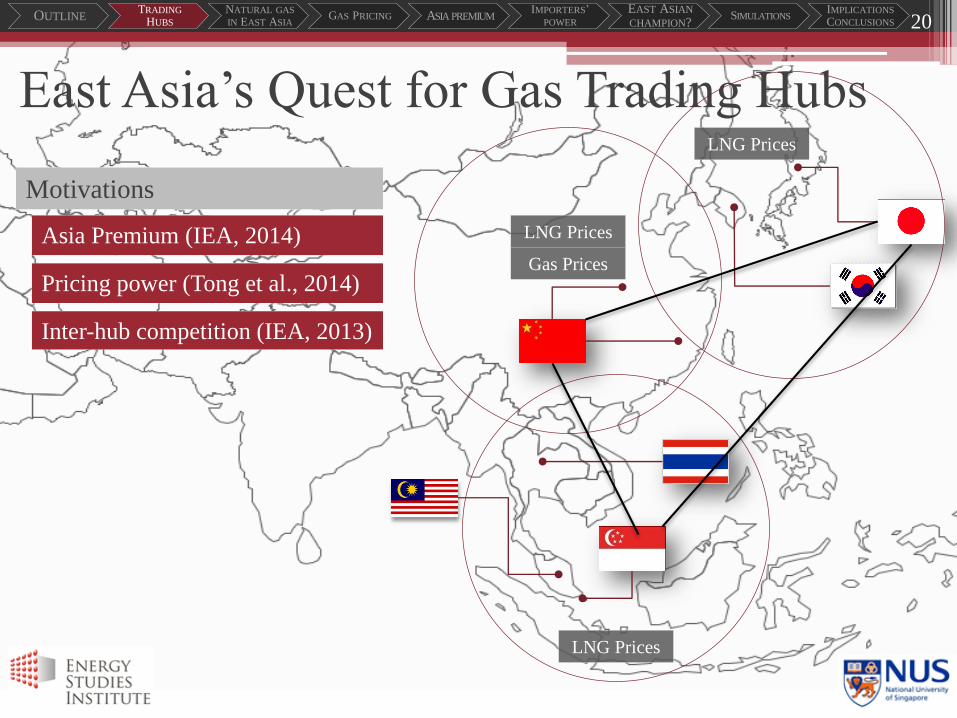

East Asia’s Quest for Gas Trading Hubs

Asia Premium (IEA, 2014)

Motivations

Pricing power (Tong et al., 2014)

Inter-hub competition (IEA, 2013)

LNG Prices

LNG Prices

LNG Prices

Gas Prices

OUTLINETRADING

HUBS

NATURAL GAS

IN EAST ASIAGAS PRICING ASIA PREMIUM

IMPORTERS’ POWER

EAST ASIAN

CHAMPION?SIMULATIONS

IMPLICATIONS

CONCLUSIONS

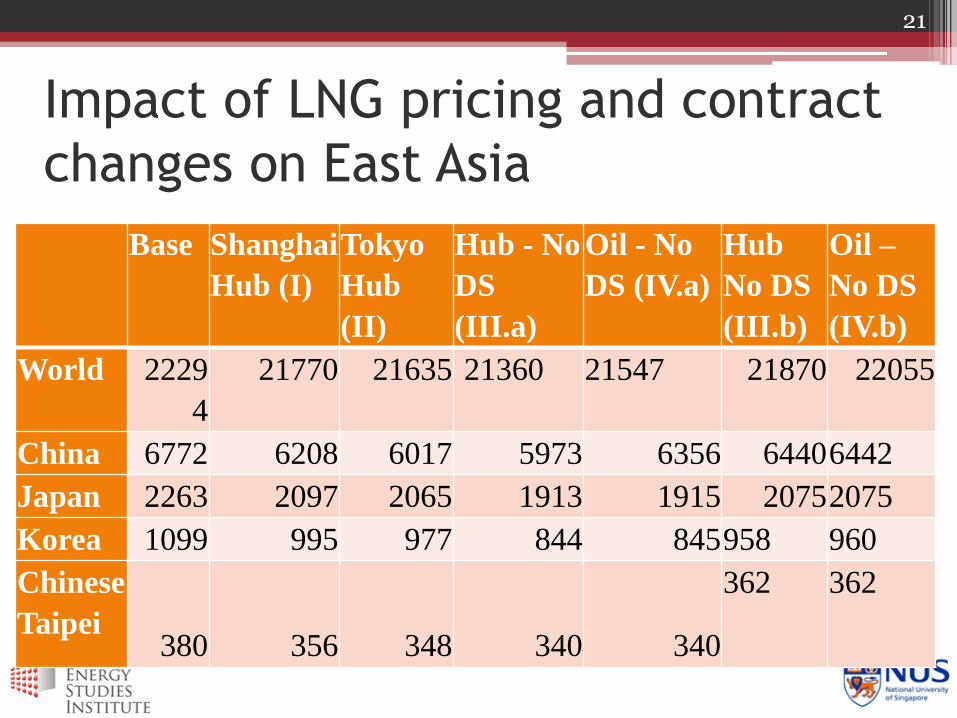

Impact of LNG pricing and contract

changes on East Asia

21

Base Shanghai

Hub (I)

Tokyo

Hub

(II)

Hub - No

DS

(III.a)

Oil - No

DS (IV.a)

Hub

No DS

(III.b)

Oil –

No DS

(IV.b)

World 2229

4

21770 21635 21360 21547 21870 22055

China 6772 6208 6017 5973 6356 64406442

Japan 2263 2097 2065 1913 1915 20752075

Korea 1099 995 977 844 845958 960

Chinese

Taipei380 356 348 340 340

362 362

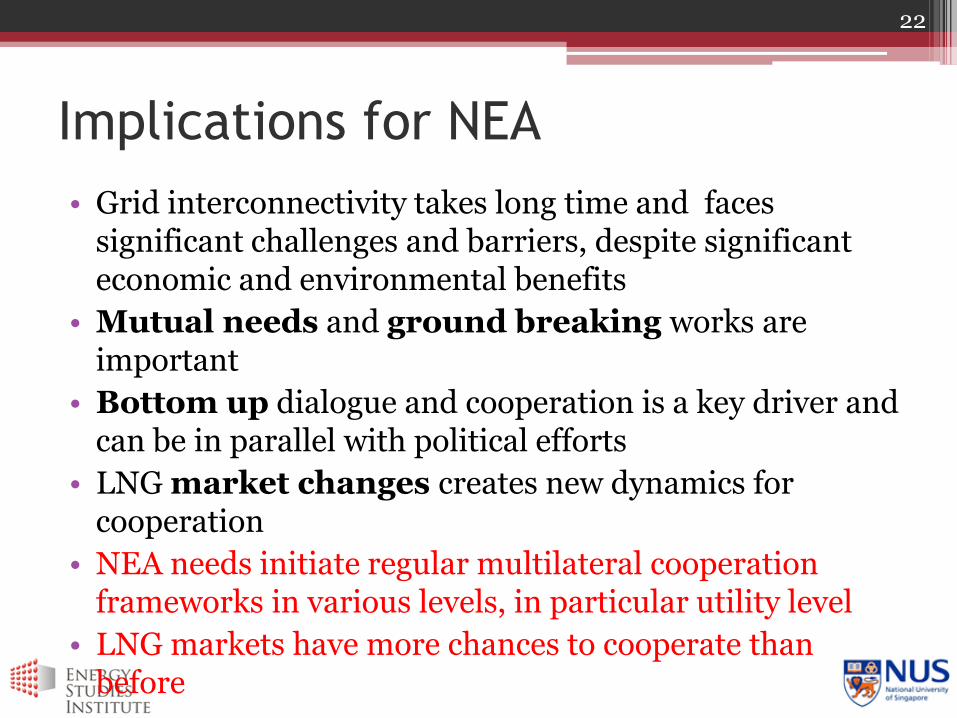

Implications for NEA

• Grid interconnectivity takes long time and faces significant challenges and barriers, despite significant economic and environmental benefits

• Mutual needs and ground breaking works are important

• Bottom up dialogue and cooperation is a key driver and can be in parallel with political efforts

• LNG market changes creates new dynamics for cooperation

• NEA needs initiate regular multilateral cooperation frameworks in various levels, in particular utility level

• LNG markets have more chances to cooperate than before

22

Thank you!

Energy Studies Institute29 Heng Mui Keng TerraceBlock A, #10-01Singapore 119620

For enquiries:

Dr. Xunpeng ShiTel: (65) 6516 5360Email: [email protected]

23

References

• Shi, X., 2016. The Future of ASEAN Energy Mix: A SWOT Analysis. Renewable & Sustainable Energy Reviews, 53:672-680.

• Shi, X., 2014. ASEAN Power Grid, Trans-ASEAN Gas Pipeline and ASEAN Economic Community: Vision, Plan and the Reality. Global Review, 2014 (Fall):115-131.

• Shi, X and Malik, C, 2013. Assessment of ASEAN Energy Cooperation within the ASEAN Economic Community. ERIA Discussion Paper Series 37. Link: http://www.eria.org/ERIA-DP-2013-37.pdf .

• Shi and Kimura, 2014, The Status and Prospects of Energy Market Integration in East Asia, Chapter 2 in Wu, Kimura and Shi (2014), Energy Market Integration in East Asia, Rutledge, pp9-24 (Political trust)

• Full papers available at: https://www.researchgate.net/profile/Xunpeng_Shi/contributions

24

![A bi-pole ± 285 kV HVDC line HVDC-VSC: transmission ...TG#08].pdf · for building multi-terminal HVDC schemes, as reversing power fl ow does not involve a change of DC polarity,](https://img.pdfslide.net/doc/110x75/5e64eaca2594e126f07d0fa9/a-bi-pole-285-kv-hvdc-line-hvdc-vsc-transmission-tg08pdf-for-building.jpg)