Embed Size (px)

Citation preview

Singapore 2004

Developments in Risk AttributionInvestment Managers Association of SingaporeSeptember 23, 2004

Alex CarmichaelDirectorRisk Solutions & OperationsRiskMetrics Group Asia [email protected]

slide 2

Agenda

1. Introduction: VaR & TE2. Recent trends in risk measurement

and attribution3. Measuring the risk of alternative

investments4. Ideas for combined risk analysis of

traditional long-only portfolios with alternative investments

slide 3

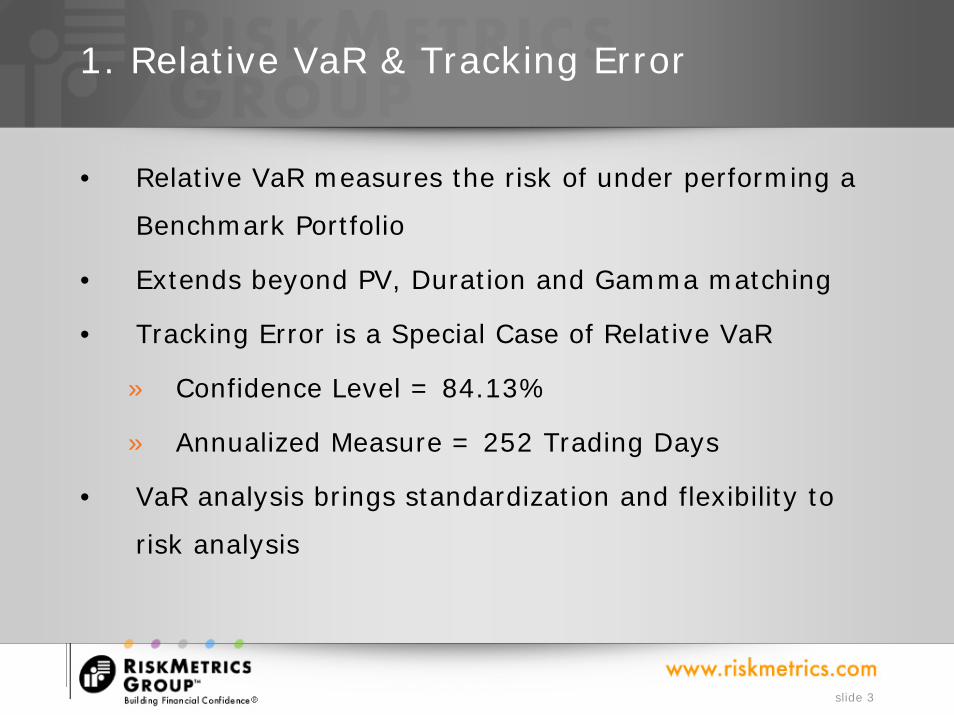

1. Relative VaR & Tracking Error

• Relative VaR measures the risk of under performing a

Benchmark Portfolio

• Extends beyond PV, Duration and Gamma matching

• Tracking Error is a Special Case of Relative VaR

» Confidence Level = 84.13%

» Annualized Measure = 252 Trading Days

• VaR analysis brings standardization and flexibility to

risk analysis

slide 4

2. Risk Management for Asset Managers –a spectrum of measures

Risk Measures Requirements

Market ExposureAbsolute and Relative Weights

Portfolio and Benchmark PositionsMultiple Classification Hierarchies

Exposure SensitivitiesDelta, Gamma, Duration

+ Security Modeling+ Cross-Asset Class Aggregation

Stress TestingHistorical, What if Scenarios

+ Market Data and Derived Data+ Volatility and Correlation Generation

Risk DecompositionTracking Error, Spread Risk

+ Full-Valuation Simulations+ Data Granularity

Risk AttributionAllocation and Security Selection

+ Investment Process Modeling+ Investment Process

slide 5

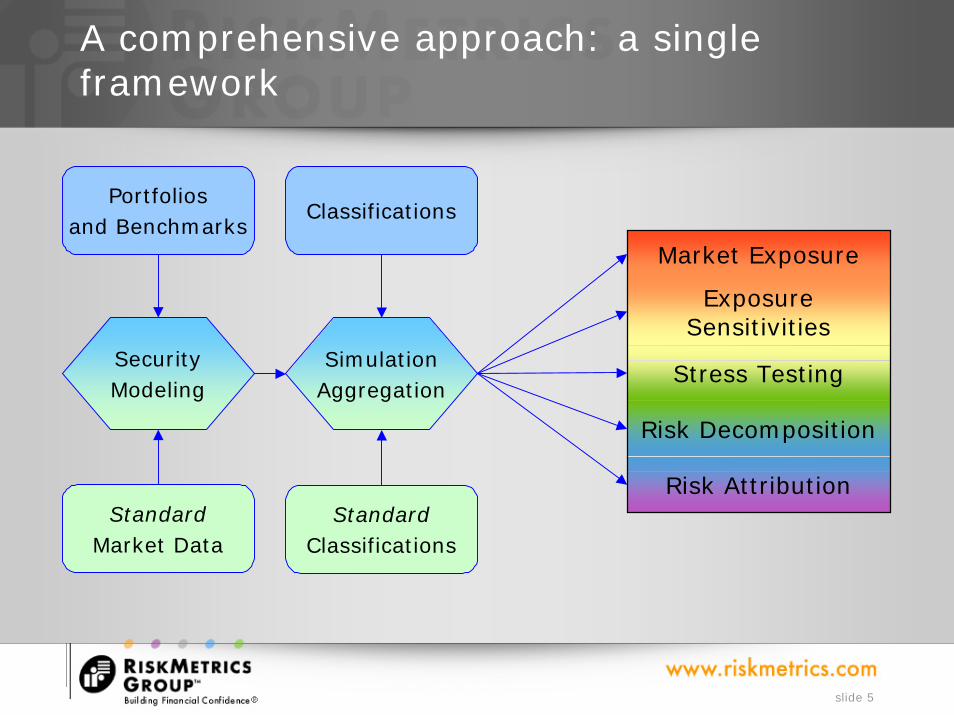

A comprehensive approach: a single framework

Portfoliosand Benchmarks

StandardMarket Data

StandardClassifications

Classifications

SecurityModeling

Market Exposure

Exposure Sensitivities

Stress Testing

Risk Decomposition

Risk Attribution

SimulationAggregation

slide 6

Risk Attribution

Equity Attribution:» Adjust by weights» Sector Allocation» Security Selection

Fixed Income Attribution:» Adjust by weights or duration» Duration» Segment Allocation» Security Selection» Currency Allocation» Spread

slide 7

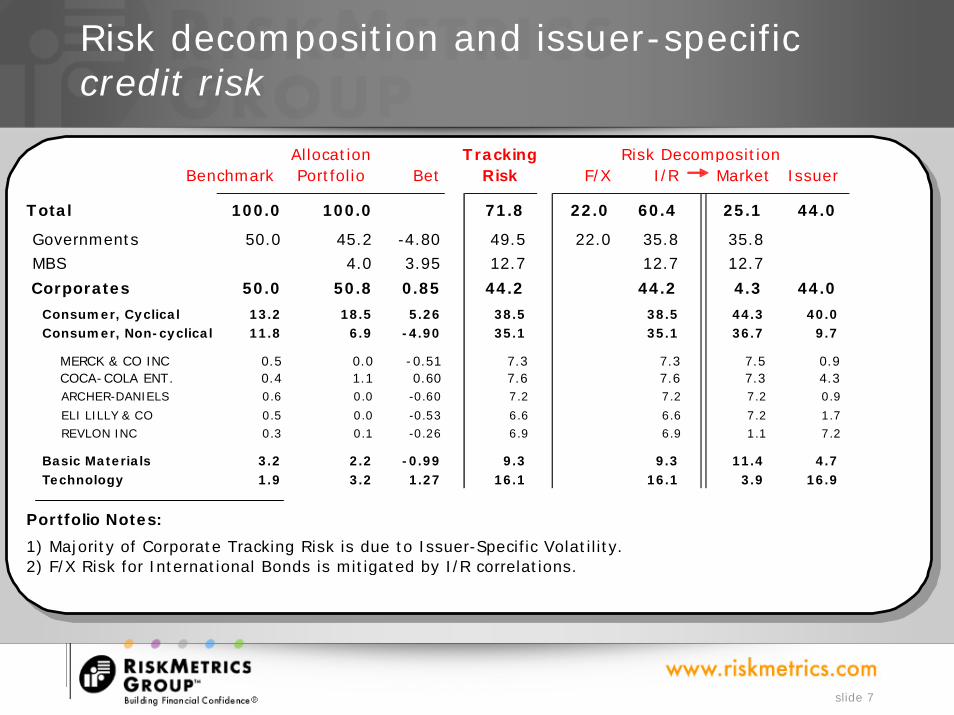

Risk decomposition and issuer-specific credit risk

TrackingBenchmark Portfolio Bet Risk F/X I/R Market Issuer

Total 100.0 100.0 71.8 22.0 60.4 25.1 44.0

Governments 50.0 45.2 -4.80 49.5 22.0 35.8 35.8 MBS 4.0 3.95 12.7 12.7 12.7

Corporates 50.0 50.8 0.85 44.2 44.2 4.3 44.0

Consumer, Cyclical 13.2 18.5 5.26 38.5 38.5 44.3 40.0 Consumer, Non-cyclical 11.8 6.9 -4.90 35.1 35.1 36.7 9.7

MERCK & CO INC 0.5 0.0 -0.51 7.3 7.3 7.5 0.9 COCA-COLA ENT. 0.4 1.1 0.60 7.6 7.6 7.3 4.3 ARCHER-DANIELS 0.6 0.0 -0.60 7.2 7.2 7.2 0.9

ELI LILLY & CO 0.5 0.0 -0.53 6.6 6.6 7.2 1.7 REVLON INC 0.3 0.1 -0.26 6.9 6.9 1.1 7.2

Basic Materials 3.2 2.2 -0.99 9.3 9.3 11.4 4.7 Technology 1.9 3.2 1.27 16.1 16.1 3.9 16.9

Portfolio Notes:

1) Majority of Corporate Tracking Risk is due to Issuer-Specific Volatility.2) F/X Risk for International Bonds is mitigated by I/R correlations.

Allocation Risk Decomposition

slide 8

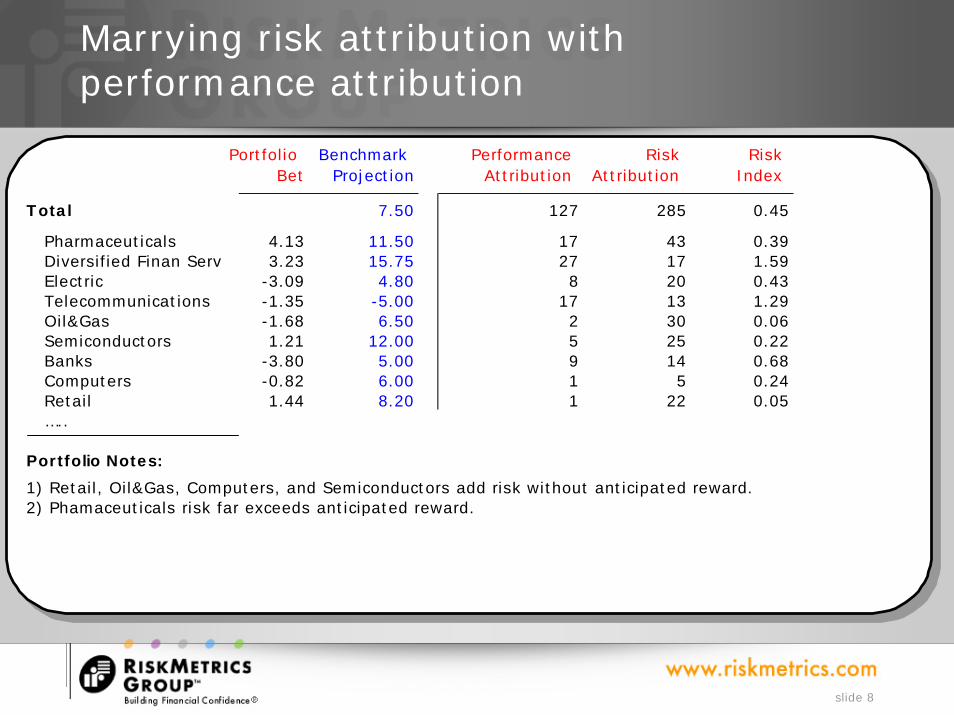

Marrying risk attribution with performance attribution

Portfolio Benchmark Performance Risk RiskBet Projection Attribution Attribution Index

Total 7.50 127 285 0.45

Pharmaceuticals 4.13 11.50 17 43 0.39 Diversified Finan Serv 3.23 15.75 27 17 1.59 Electric -3.09 4.80 8 20 0.43 Telecommunications -1.35 -5.00 17 13 1.29 Oil&Gas -1.68 6.50 2 30 0.06 Semiconductors 1.21 12.00 5 25 0.22 Banks -3.80 5.00 9 14 0.68 Computers -0.82 6.00 1 5 0.24 Retail 1.44 8.20 1 22 0.05 …..

Portfolio Notes:

1) Retail, Oil&Gas, Computers, and Semiconductors add risk without anticipated reward.2) Phamaceuticals risk far exceeds anticipated reward.

slide 9

3. Alternative Investments: Intelligence versus Information

• Position Transparency = Information» Managers providing investors with a list of positions

can be useless for today’s complex fund strategies.» Information ≠ Intelligence

• Analysis + Organization = Intelligence» Value is created when positions are independently

priced (standardized), linked to models and risk factors (data), analyzed, organized and aggregated

• Intelligence = Better Decisions» Better decisions are possible when well organized,

consistent reporting methods allow meaningful comparisons of valuations and risk results

slide 10

Risk Types

• Market Risk – potential loss due to market price volatility under normal and stressed conditions. Risk factors include equity time series, yield curves, volatilities, volatility surfaces, commodities, and currencies.

• Credit Risk – potential loss due to issuer specific risk. CreditGrades uses a structural Merton model to calculate issuer specific spread risk.

• Valuation Risk – potential loss due to hard to price, illiquid or mispriced securities.

slide 11

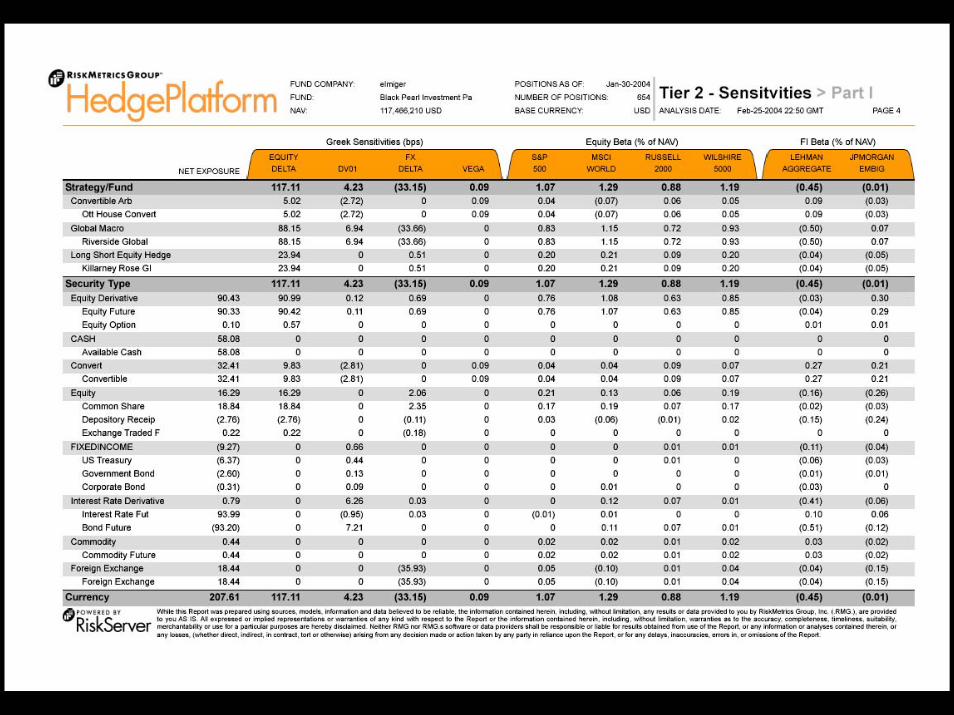

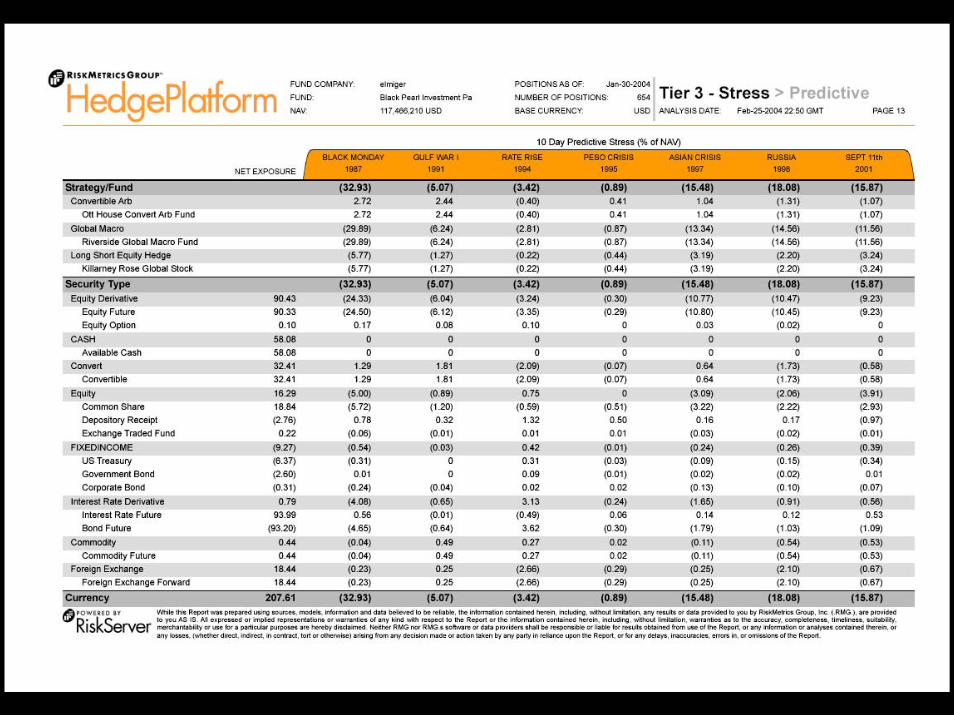

slide 12

slide 13

slide 14

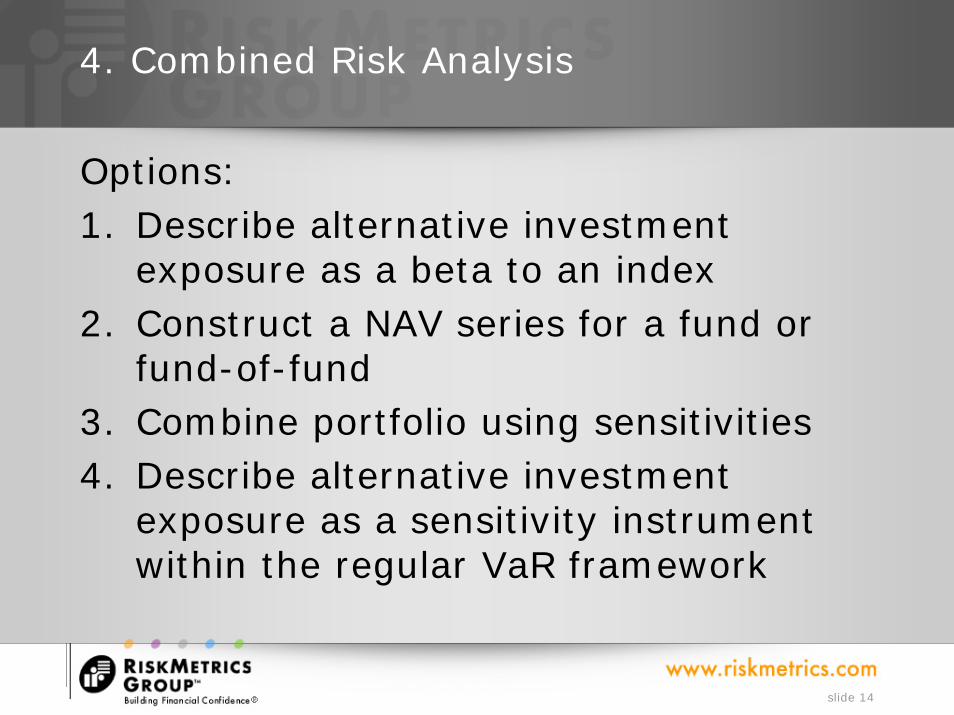

4. Combined Risk Analysis

Options:1. Describe alternative investment

exposure as a beta to an index2. Construct a NAV series for a fund or

fund-of-fund3. Combine portfolio using sensitivities4. Describe alternative investment

exposure as a sensitivity instrument within the regular VaR framework

slide 15

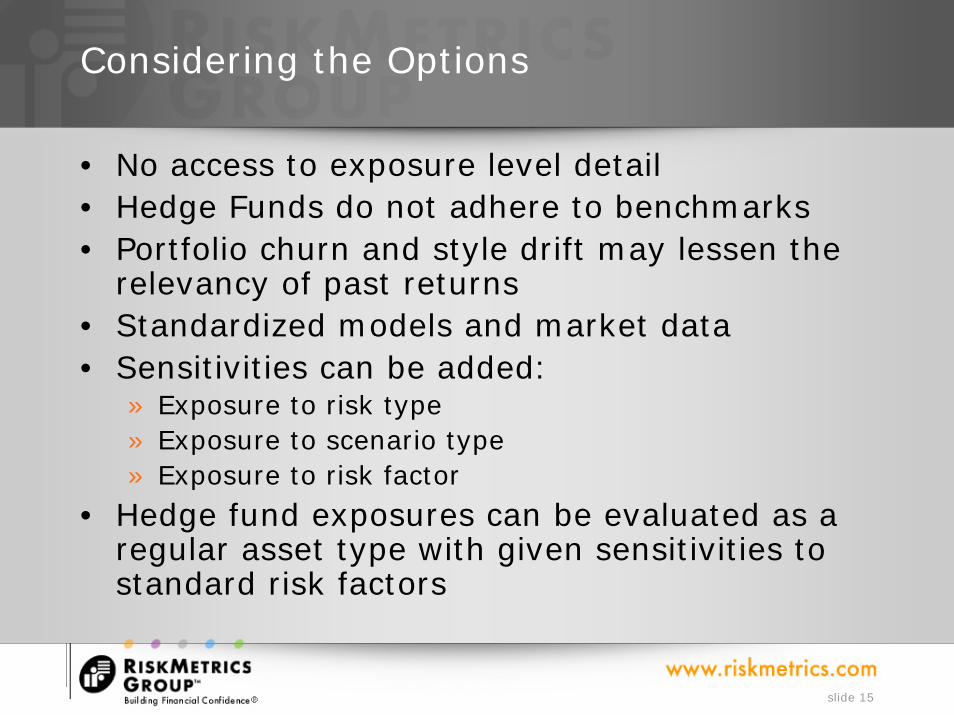

Considering the Options

• No access to exposure level detail• Hedge Funds do not adhere to benchmarks• Portfolio churn and style drift may lessen the

relevancy of past returns• Standardized models and market data• Sensitivities can be added:

» Exposure to risk type» Exposure to scenario type» Exposure to risk factor

• Hedge fund exposures can be evaluated as a regular asset type with given sensitivities to standard risk factors

slide 16

Adding Alternative Investments as an Asset Class in a VaR Framework

TrackingBenchmark Portfolio Bet Risk Total Asset Issuer Security

Total 100.0 100.0 71 71 28 46 -2

Corporates 50.0 50.8 0.85 46 42 2 40 Sun Microsystems Inc 0.4 1.7 1.29 18 11 9 Pep Boys 0.4 1.4 1.05 14 8 6 Ford Motor Co 0.3 1.2 0.90 12 8 6

Governments 50.0 45.2 -4.80 23 21 9 6 6 United States Govt 12.2 10.1 -2.15 13 8 1 3 Italy Govt 4.3 3.4 -0.99 8 5 2 2

Italy 6.50% BTP Nov 27 0.2 0.1 -0.19 2 1 1 Italy 4.25% BTP Nov 2009 0.3 0.0 -0.22 1 1 Italy 4.50% BTP May 2009 0.3 0.1 -0.21 1 1

Netherlands Govt 1.4 0.9 -0.46 3 2 1 1

Alternative Investments 0.0 4.0 3.95 15 9 17 -8 Oceanview Hedge Fund 0.0 3.1 3.06 12 6 -7

Portfolio Notes:

1) Corporate issuer selection is adding most risk.2) Only top 3 issuers and securities displayed.

Allocation Risk Contribution

slide 17

Summary

• Detailed analysis and attribution of risk is available for traditional long-only portfolios

• Alternative Investments pose challenging problems but can be solved with:» Transparency» Standardization

• Including Alternative Investments as an asset class can be done with sensitivities to:» Standard risk factors» Standard stress scenarios