Embed Size (px)

Citation preview

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 1/17

Recent developments in

India¶s Services Sector

Opportunities for Australia

Richard S Andrews

Executive Director

Economic Analytical Unit

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 2/17

Key points

Services sector is key to India¶sdevelopment prospects

This makes it a particularly prospectivesector for Australian companies.

While Australia is already capitalising tosome extent, there is scope to do more

But«need to be in it for the long haul

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 3/17

Services and India¶s development

Phenomenal growth in high-end serviceshas driven India¶s recent performance.

The question is ± can growth in one sector translate into an ³Indian developmentmodel´ based on services?

Services: 60 per cent of the Indianeconomy ± and growing.

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 4/17

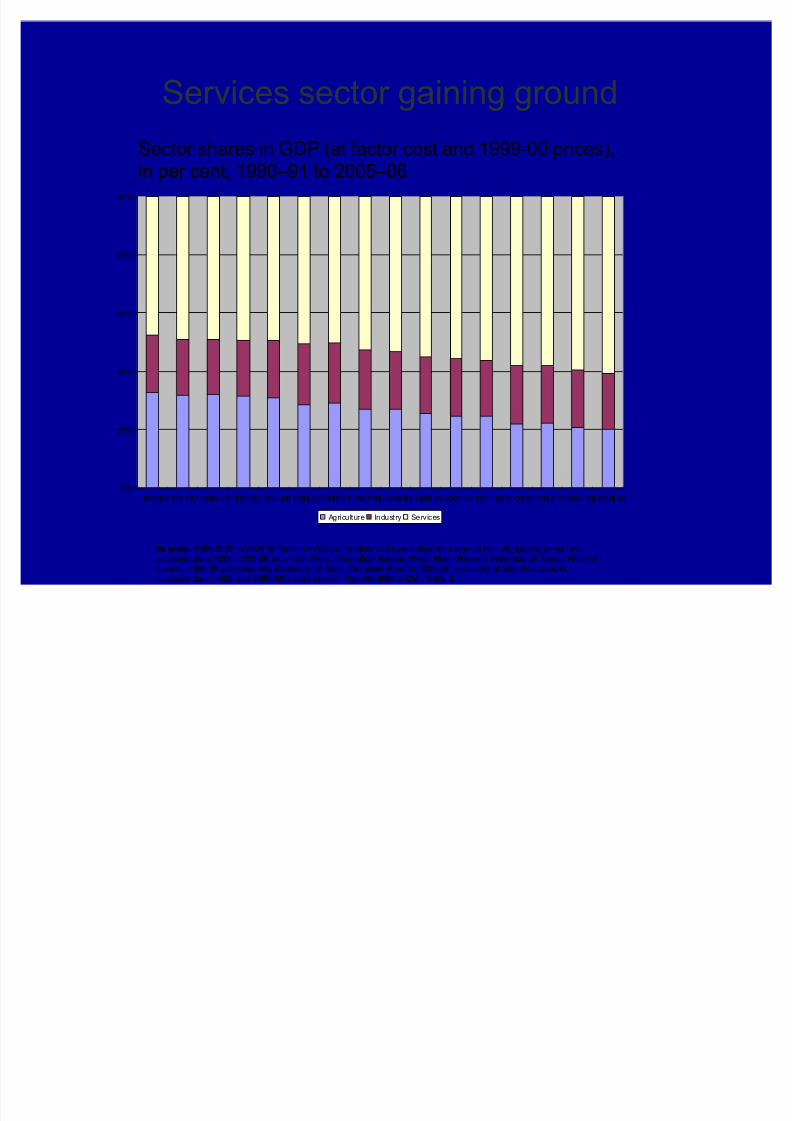

Services sector gaining ground

Sources:1999-2000 to 2004-05 data from Central Statistical Organisation, http://mospi.nic.in/5_gdpind_const.htm,accessed June 2006; 2005-06 data from Press Information Bureau, Press Note, 'Revised Estimates of Annual National

Income, 2005-06 and Quarterly Estimates of Gross Domestic Product, 2005-06', available at http://mospi.nic.in,accessed June 2006; pre-1999-2000 data from 31 May 2006RBI 2005b, Table 3.

Sector shares in GDP (at factor cost and 1999-00 prices),in per cent, 1990±91 to 2005±06

0%

20%

40%

60%

80%

100%

1990-91 1991-92 1992-93 1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Agriculture Industry Services

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 5/17

Services and India¶s development

Phenomenal growth in high-end serviceshas driven India¶s recent performance.

The question is ± can growth in one sector translate into an ³Indian developmentmodel´ based on services?

Services: 60 per cent of the Indianeconomy ± and growing.

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 6/17

What¶s happening.

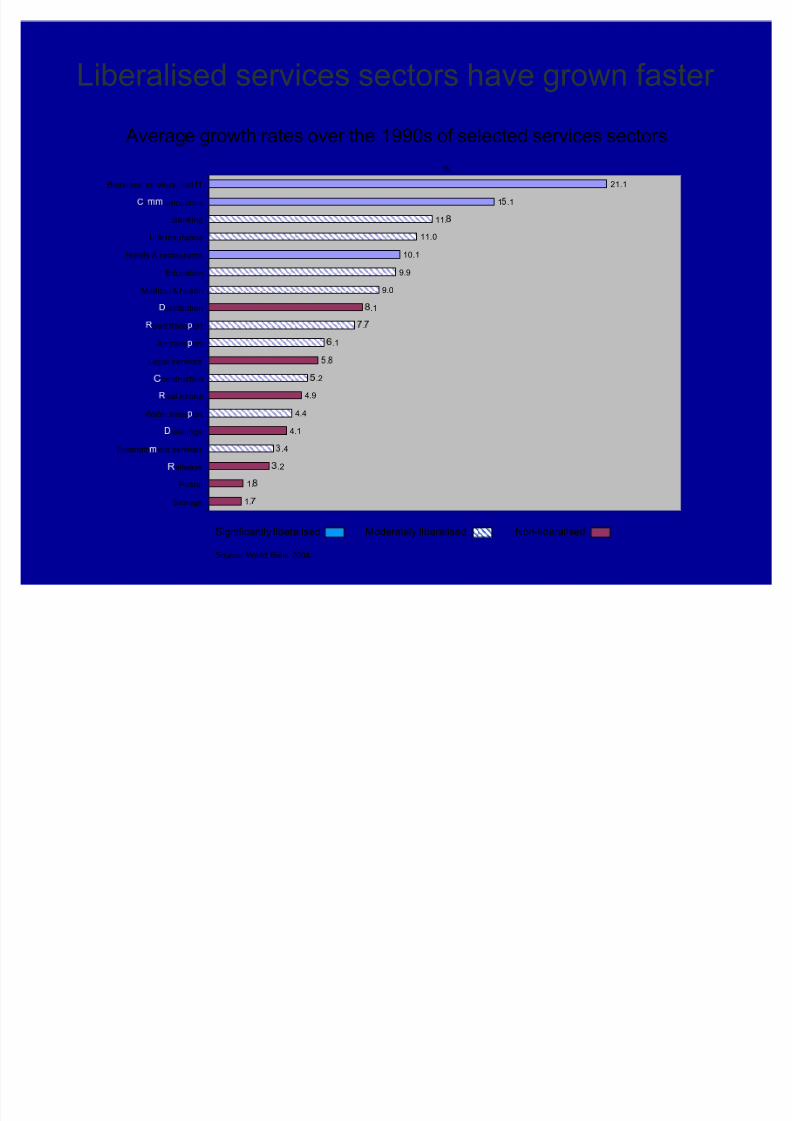

A critical element in the services sector¶s growthhas been government¶s change of mind onregulation

Deregulated or little-regulated sectors havegrown fastest

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 7/17

Liberalised services sectors have grown faster

Significantly liberalised Moderately liberalised Non-liberalised

Source: World Bank 2004.

Average growth rates over the 1990s of selected services sectors

21.1

1

.1

11.¡

11.0

10.1

9.99.0

¡

.1

¢

.¢

£ .1

.¡

.2

4.9

4.4

4.1

¤

.4

¤

.2

1.¡

1.¢

Business services, incl IT

¥ o ¦ ¦ unications

Banking

Life insurance

Hotels & restaurants

Education

Medical & health

§

istribution

̈

oad trans©

ort

Air trans©

ort

Legal services

¥ onstruction

̈

eal estate

Water trans©

ort§

wellings

Entertain¦

ent services

̈

ailways

Postal

Storage

%

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 8/17

What¶s happening.

A critical element in the services sector¶s growthhas been government¶s change of mind onregulation

Deregulated or little-regulated sectors havegrown fastest

The demonstration effect plus lobbying by thesuccess stories are driving further reformmomentum.

This means a dynamic environment ± which willcreate opportunities as nature of businesschanges.

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 9/17

Where the opportunities will be

While IT/ITES has been the headline-grabber, the services sector covers abroad spectrum

Important to look across whole servicessector for opportunities

These will differ depending on the role of the specific sector in the economy.

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 10/17

1. The IT/ITES boom

India¶s boom driving ³tradability revolution´ for services and emergence of multi-directionalinternational supply chains

± India¶s business services imports have boomed at thesame time as exports

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 11/17

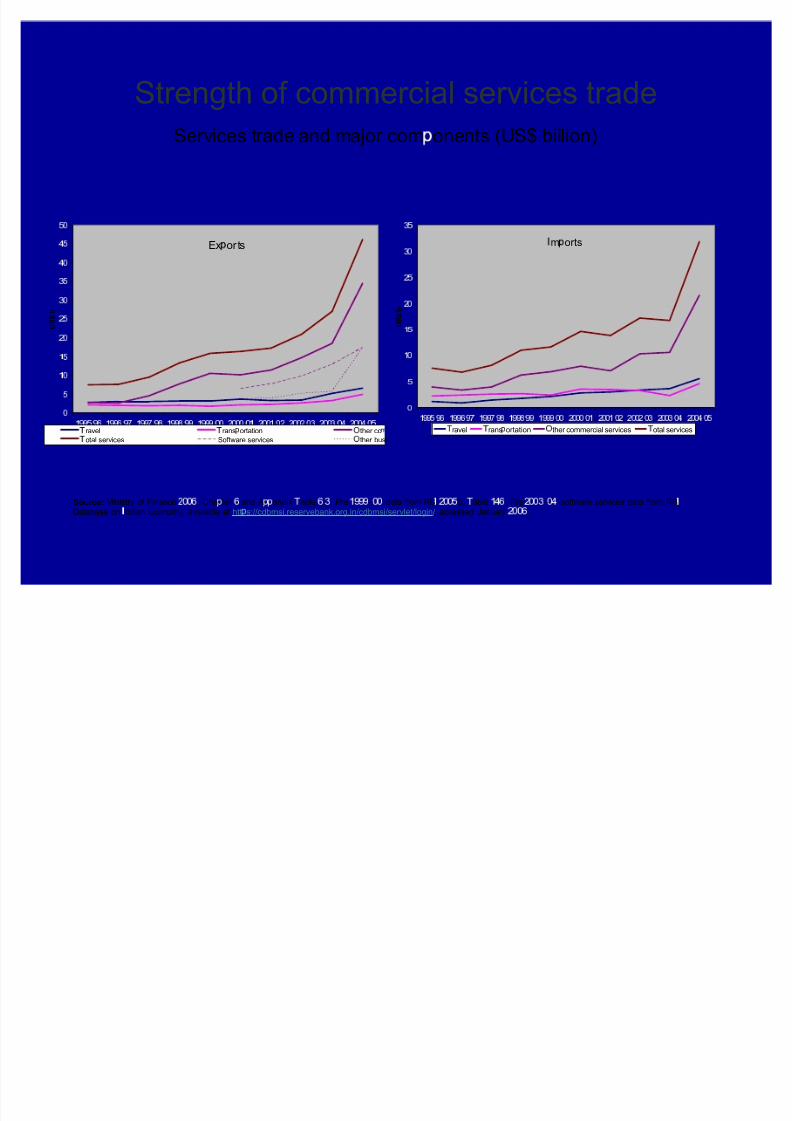

Strength of commercial services trade

-

-

-

-

-

-

-

-

-

-

U S $ b

ravel

rans ! ortation"

ther commercial services

otal services

m orts

Services trade and major com onents (US$ billion)

Source: Ministry of Finance# $ $ %

, Cha&

ter %

and A& &

endix'

able%

.(

. Pre)

0 0 0

±$ $

data from RB1

# $ $

2

b,'

able)

3 %

. Pre# $ $ (

±$ 3

software services data from RB1

Database on

1

ndian Economy, available at htt&

s://cdbmsi.reservebank.org.in/cdbmsi/servlet/login/, accessed January# $ $ %

.

4

5

6

4

6

5

7 4

7 5

8 4

8

5

9 4

9

5

5 4

6

@ @

5

-@ A

6

@ @ A

-@

B

6

@ @

B

-@ C

6

@ @ C

-@ @

6

@ @ @

-4 4 7 4 4 4

-4

6

7 4 4

6

-4 7 7 4 4 7

-4 8 7 4 4 8

-4 9 7 4 4 9

-4

5

U S $

b

D

ravelD

rans E ortationF

ther coD

otal services Software servicesF

ther busi

Ex orts

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 12/17

1. The IT/ITES boom

India¶s boom driving ³tradability revolution´ for services and emergence of multi-directionalinternational supply chains

± India¶s business services imports have boomed at thesame time as exports

± Opportunities for collaboration, participation in supplychains, and just staying up to date with internationaldevelopments.

± But highly competitive Also opportunities in other high-end services

such as biotechnology

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 13/17

2. Dynamic enablers

Telecommunications ± critical to ongoingIT/ITES boom ± uge growth (especially in mobile market) but huge

competition ± Mainly niche opportunities for Australia

Finance ± crucial to spreading growth ± Increasing affluence giving rise to demand for new

financial products

± Opportunities for project finance generated by needfor infrastructure development

± Ongoing reforms in banking and insurance

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 14/17

Dynamic enablers (cont)

Energy and transport infrastructure ± willdetermine sustainability of India¶s boom ± Recognition by government of need for external

involvement

± Improved public sector fiscal position andmechanisms for drawing in foreign capital andexpertise

± Australian companies (e.g. SMEC, Clough, Leighton)operating successfully already

± Specific areas of Australian expertise ± airports etc Education (key Australian export)

± Watch for changing profile

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 15/17

To be continued «

Retail ± burgeoning middle class drivesdemand for international standard retailing

± Structural and cultural shifts required withmajor implications for logistics and other industries

Tourism/hospitality

± Greater accessibility of travel (deregulatedairlines) will drive demand for expandedfacilities (e.g. middle-range hotels)

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 16/17

Australia¶s presence

Australia¶s second fastest growingservices market after China - but it¶smostly education

Increasing number of Australian successstories

Momentum from recent government ±

level visits and initiatives builds ongenerally favourable perceptions

Plenty of competition for limelight

8/8/2019 Dfat India

http://slidepdf.com/reader/full/dfat-india 17/17

To remember

India is a ³long haul´ investment destination ±reflected in differing assessments

± Rewards can be great and business environment is

becoming increasingly transparent ± Need to understand nature of business relationship &

± Pursue targeted marketing strategy: India is not ahomogeneous market.

± But difficulties should not be underestimated ± talk toothers who are doing it.